a study on customer awareness on green banking in selected public and private sector banks in...

TRANSCRIPT

24

M. Narmadha, “A Study on Customer Awareness on Green Banking in Selected Public and Private

Sector Banks in Chennai” – (ICAM 2016)

A STUDY ON CUSTOMER AWARENESS ON GREEN BANKING IN

SELECTED PUBLIC AND PRIVATE SECTOR BANKS IN CHENNAI

M. Narmadha

Assistant Professor, SRM University - Ramapuram Campus, Chennai.

ABSTRACT

Green Banking means promoting environmental-friendly practices and reducing your

carbon footprint from our banking activities. Green banking will be mutually beneficial to the

Consumers, banks, industries and the economy. The study aims to identify the awareness on

Green banking among the customers of six different banks. Also it aims to find the customers

usage relating to Green Banking service. It is necessary to identify various initiatives taken by

bank on the concept of green banking in order to influence customer and make them user

friendly. Researcher will study the impact of different age group of customers with regard to

green initiatives taken by public and private sector banks.

Key words: Green Banking, Customer Awareness, Green Banking Initiatives, Online

Banking.

Cite this Article: M. Narmadha. A Study on Customer Awareness on Green Banking in

Selected Public and Private Sector Banks in Chennai. International Journal of Management,

7(2), 2016, pp. 24-35.

http://www.iaeme.com/ijm/index.asp

1. INTRODUCTION

Today every business organizations and corporations are adopting “GO GREEN” concept because of

the increasing friendly attitude of the society towards the environment. Banks play a critical role in the

economic development of the nations by providing various Socio-Economic activities like Job creation,

wealth generation, Poverty eradication, entrepreneurial activity etc. Besides these activities, banks are

introducing the practices of green banking in order to protect the environment and to reduce carbon

emission.

Green Banking means promoting environmental-friendly practices and reducing your carbon

footprint from our banking activities. Green banking will be mutually beneficial to the Consumers,

banks, industries and the economy. For consumers this shift towards green banking means that more

deposit and loan products will be available through online and mobile banking. It also means better

deposit rates on CDs, money market accounts and savings accounts. Green banks should also have

lower fees and give rate reductions on loans going towards energy-efficient projects. This is banking

beyond pure profit. Another important aspect of green banking is the involvement and outreach from

the individual banks to their local community.

INTERNATIONAL JOURNAL OF MANAGEMENT (IJM)

ISSN 0976-6502 (Print)

ISSN 0976-6510 (Online)

Volume 7, Issue 2, February (2016), pp. 24-35

http://www.iaeme.com/ijm/index.asp

Journal Impact Factor (2016): 8.1920 (Calculated by GISI)

www.jifactor.com

IJM

© I A E M E

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 -

6510(Online), Volume 7, Issue 2, February (2016), pp. 24-35 © IAEME Publication

25

M. Narmadha, “A Study on Customer Awareness on Green Banking in Selected Public and Private

Sector Banks in Chennai” – (ICAM 2016)

2. MEANING OF GREEN BANKING

Green Banking means promoting environmental – friendly practices and reducing your carbon

footprint from your banking activities. This comes in many forms:

Using online banking instead of branch banking.

Paying bills online instead of mailing them.

Opening up accounts at online banks, instead of large multi-branch banks.

Finding the local bank in your area that is taking the biggest steps to support local green

initiatives.

Green banks give more weight to environmental factors, their aim is to provide good

environmental and social business practice, they check all the factors before lending a loan, whether the

project is environmentally friendly and have any implications in the future, and loan will be awarded

only when all the environmental safety standards are followed.

3. CUSTOMER AWARENESS

Generally speaking awareness comprises a human's perception and cognitive reaction to a condition or

event. Awareness does not necessarily imply understanding, just an ability to be conscious of, feel or

perceive. To create more awareness for the customers, many banks can be involved in programmes that

support the environmentally friendly products and services.

4. GREEN BANKING FINANCIAL PRODUCTS

Green banking product coverage includes:

Green Loans: means giving loans to a project or business that is considered environmentally

sustainable.

Green Mortgages: Banks offer green mortgage with better rates or terms for energy efficient

houses. The savings in monthly energy bills can offset the higher monthly mortgage payments

and save money in the long run.

Green Credit Cards: These cards offer an excellent incentive for customers to use their green

card for their expensive purchases.

Green Deposits: Banks offer higher rates on commercial deposits, money market accounts,

checking accounts and savings account if customers opt to conduct their banking activities

online.

Green Reward Checking Accounts: Customers can earn higher checking account rates if

they meet monthly requirements that might include receiving electronic statements, paying

bills online or using a debit or check card.

Green Saving Accounts: In case of Green Saving Accounts, banks make donations on the

basis of savings done by customers’ .The more they save, the more the environment benefits

in form of contributions or donations done by banks.

Mobile banking and online banking: These new age banking forms include less paperwork,

less mail, and less travel to branch offices by bank customers, all of which has a positive

impact on the environment.

5. GREEN BANKING INITIATIVES BY INDIAN BANKS

Only six banks were taken for this study. They are as follows:

PUBLIC SECTOR BANKS

State Bank of India (SBI)

SBI had launched Green Channel Counter (GCC) facility at their branches in 2010. The bank had also

collaborated with Suzlon Energy Ltd for the generation of windmills. It has become a signatory to the

Carbon Disclosure Project in which they undertake various environmentally and socially sustainable

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 -

6510(Online), Volume 7, Issue 2, February (2016), pp. 24-35 © IAEME Publication

26

M. Narmadha, “A Study on Customer Awareness on Green Banking in Selected Public and Private

Sector Banks in Chennai” – (ICAM 2016)

initiatives. Export Import Bank of India (EXIM) and SBI entered into an agreement for building solar

plant in India.

Punjab National Bank (PNB)

According to Corporate Social Responsibility Report 2010-11 (PNB, 2011), they had taken various

steps for reducing emission and energy consumption. PNB is conducting Electricity Audit of offices as

an energy conversation initiative. The bank had organized more than 290 Tree Plantation Drives. It

started emphasizing on green building practices such as energy efficient lights, fans, etc. The

organization had signed a ‘Green Pledge’ under which they had set up the butterfly park at the

compound of Guruvayur temple which houses 18 types of medicinal plants. The organization had

sanctioned nine wind energy projects with an aggregation limit of 185.81 crore. They were also

awarded with a second prize for ‘Best Wind Energy Power Financer’ by wind power India 2011.

Canara Bank

According to Canara Bank (2013), the bank had taken many green initiatives such as: - As a part of

green banking initiative, the bank had adopted environmental friendly measures such as mobile

banking, internet banking, etc. Canara bank had set up e-lounges like internet banking, pass book

printing, ATM, online trading, etc. The bank is also not extending any finance to the units which are

producing ozone depletion substances. While appraising any project, they ensure the borrower to obtain

No Objection Certificate (NOC) from central or state pollution control board.

PRIVATE SECTOR BANKS

ICICI Bank Ltd

ICICI bank had adopted ‘Go Green’ initiative, which involves activities such as Green

products/offerings, Green engagement and green communication with customers as per ICICI Bank

(2014):-

Green Products and Services: The bank is offering green products and services like

Instabanking

It is a service which gives convenience to the customers to do banking anywhere and anytime through

internet banking, mobile banking, etc.

‘Vehicle Finance’

They are offering 50% waiver on processing fee of auto loans on the car models which uses alternate

sources of energy like the Civic Hybrid of Honda, Tata Indica CNG, Reva electric cars.

Home Finance

The bank had reduced the processing fee for the customers who are purchasing homes in LEED

certified buildings.

Green Engagements

During Diwali 2013, the organization had conducted an environmental awareness program for

employees and customers. It has also become partners with the Green theme CNBC – overdrive auto

awards. The bank is celebrating World Environment Day every year on June 5.

Green Partners: The organization is looking forward for partnerships with national and international

green organizations and NGO’s.

HDFC Bank Ltd – HDFC bank is taking up various measures in reducing their carbon footprints in

the area of waste management, paper use and energy efficiencies as per HDFC Bank (2013):-

The bank is encouraging their employees to prevent any wasteful use of natural resources and emission

of greenhouse gases. They are reducing the use of paper through issuing e-transaction. The

organization is exploring renewable energy by setting up of 20 solar ATMs. They are also managing

their waste by tying up with vendors for recycling of paper and plastic. The bank is procuring green

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 -

6510(Online), Volume 7, Issue 2, February (2016), pp. 24-35 © IAEME Publication

27

M. Narmadha, “A Study on Customer Awareness on Green Banking in Selected Public and Private

Sector Banks in Chennai” – (ICAM 2016)

products which are compliant with the norms of the Central Pollution Control Board and which are

rated by Energy Star.

Axis Bank Ltd – AXIS bank implementing several initiatives in green banking such as per Axis Bank

(2013):-

In august 2011, the bank had initiated the process of collecting all the dry waste generated from the

corporate office and recycles it to notepads, notebooks and envelopes. The corporate office of the bank,

located in Mumbai, is designed and constructed a ‘Green Building’. Car-pooling has been initiated by

a bank to reduce carbon footprint. They are also encouraging their customers to use e-statements and

other electronic communications to reduce paper consumption. Annual reports are being sent through

emails. The organization had initiated Independent ATM Deployment (IAD) model in which ten solar

based ATM has been set up in Coimbatore circle.

6. REVIEW OF LITERATURE

Schmidheiny and Zorraquin (1996), “Green banking is generally defined as promoting environmentally

friendly practices that aid customers in reducing their carbon footprint through their banking operation

activities. These practices include such things as online banking, statements, bill payments, and account

opening. Banks also invest in internal initiatives to reduce their own carbon footprint”.

Sahoo, Pravakar and Nayak, Bibhu Prasad (2008), in their research article on “Green Banking in

India” highlighted that banking sector is one of the major stake holders in the industrial sector; it can

find itself faced with credit risk and liability risk. Thus the banks should go green and play a pro-active

role to take environmental and ecological aspects as part of their lending principle, which would force

customers to go for mandated investment for environmental management, use of appropriate

technologies and management systems.

Dharwal, Mridul and Agarwal, Ankur (2011), in research article on “Green Banking: An

Innovative initiative for Sustainable Development” concluded that Indian banks need to be made fully

aware of the environmental and social guidelines to which banks worldwide are agreeing to. As far as

green banking is concerned, Indian banks are far behind their counterparts from developed countries. If

Indian banks desire to enter global markets, it is important that they recognize their environmental and

social responsibilities.

Nigamananda Biswas (2011) interpreted Green Banking as combining operational improvements,

technology and changing client habits in market place. Adoption of greener banking practices will not

only be useful for environment, but also benefit in greater operational efficiencies, a lower

vulnerability to manual errors and fraud, and cost reductions in banking activities.

Khawaspatil, S.G. and More, R.P. (2013), in their research article concluded that in-spite of a lot

of opportunity in green banking and RBI notifications, Indian banks are far behind in implementation

of green banking. Only few banks have initiated in this regard. There is a lot of scope for all banks and

they can not only save our earth but also transform the whole world towards energy consciousness.

Banks must educate their customers about green banking and adopt all strategies to save earth and

build banks’ image.

Sharma, K& Gopal in their study “A study on Customer Awareness on Green Banking initiatives

in selected Public & Private sector banks with special reference to Mumbai” identified the opinion and

awareness of bank employees and customers as regards to green banking concept in Public and Private

sector banks. They found that green initiatives like Communication through press, Bank environmental

policy, Concession on energy savings, Solar ATMs, Green CDs is not familiar in green initiatives by

the bank as per the respondents.

7. STATEMENT OF THE PROBLEM

Indian Banks introduced Green Banking services since 1996. As the use of Green Banking services are

increasing day –by-day, it is important to study the customer awareness towards Green Banking

services in Chennai city. This study is one of such an attempt.

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 -

6510(Online), Volume 7, Issue 2, February (2016), pp. 24-35 © IAEME Publication

28

M. Narmadha, “A Study on Customer Awareness on Green Banking in Selected Public and Private

Sector Banks in Chennai” – (ICAM 2016)

AIM OF THE STUDY

The study aims to find out the awareness of the customers towards the use of Green Banking. During

the research, the researcher identifies the awareness on Green banking among the customers of six

different banks. Also it aims to find the customers usage relating to Green Banking service. One has to

approach the branch in person, to withdraw cash or deposit a cheque or request a statement of accounts.

In true Green banking, any inquiry or transaction is processed online without any reference to the

branch (anywhere banking) at any time. Providing Green banking is increasingly becoming a "need to

have" than a "nice to have" service. To enhance the level of awareness of customers, a detailed study

on the awareness of customers and their usage about various factors affecting Green Banking must be

studied.

OBJECTIVE OF THE STUDY

1. To study the awareness on Green Banking among the customers.

2. To know which age group of customers is using different Green Banking facilities.

3. To find out the factors influence the adoption of Green Banking services.

4. To suggest ways to promote Green Banking in India.

LIMITATIONS OF THE STUDY

1. The geographical scope of the study is limited to Chennai city.

2. The sample size is confined to 200.

3. Only six banks were taken for the study.

4. The respondents were unable to spend much time for filing up the questionnaire.

5. Time was a limiting factor in conducting the study.

8. RESEARCH METHODOLOGY

The research methodology used in this study is based on primary as well as secondary data. The

primary data was collected from the study conducted through questionnaire. The information is

collected by issuing questionnaire to some of the respondents’ directly in person and to the remaining

respondents through E – Mail. Secondary data for the study has been collected from Websites of

various banks and Journals related to Banking.

SAMPLING METHOD

General public of the city and Sampling Units are chosen on the basis of Convenience Sampling.

SAMPLE SIZE

200 Respondents

TOOLS USED:

The following statistical tools have been used for the purpose of analyzing data collected.

Percentage Analysis,

Chi – square Test,

Kolmogorov – Simornov test,

One – way ANOVA Test.

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 -

6510(Online), Volume 7, Issue 2, February (2016), pp. 24-35 © IAEME Publication

29

M. Narmadha, “A Study on Customer Awareness on Green Banking in Selected Public and Private

Sector Banks in Chennai” – (ICAM 2016)

9. DATA ANALYSIS AND INTERPRETATION:

PERCENTAGE ANALYSIS:

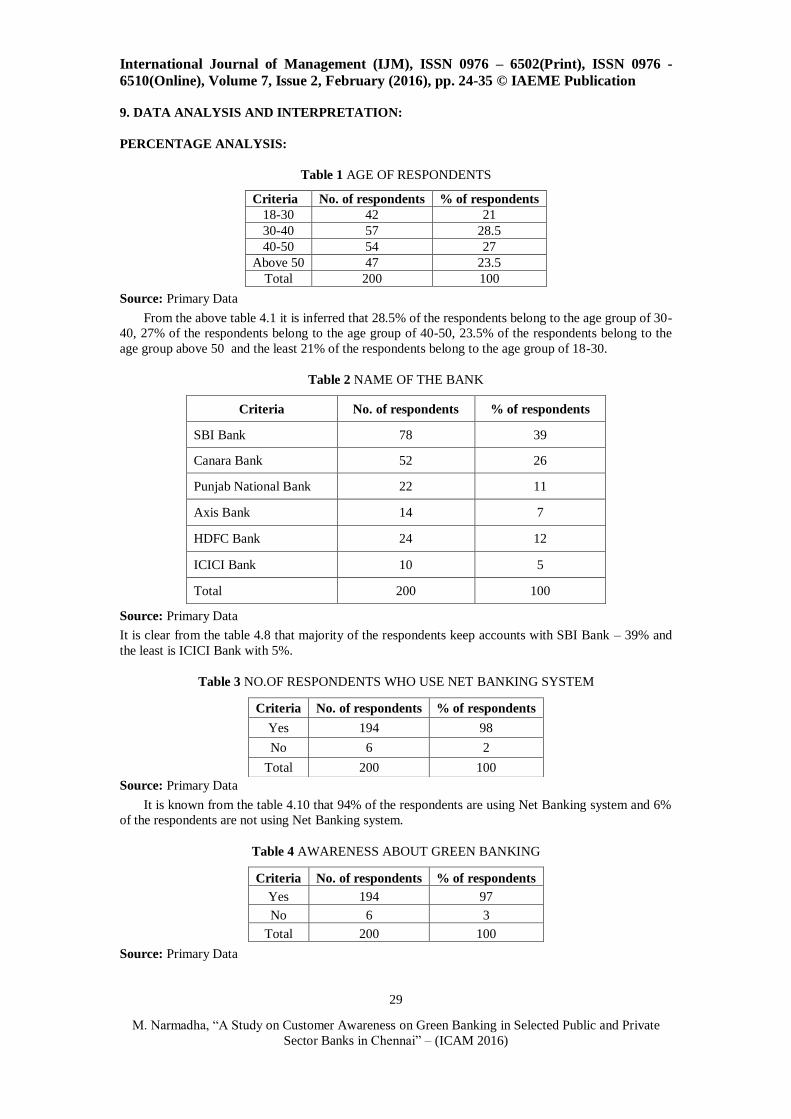

Table 1 AGE OF RESPONDENTS

Criteria No. of respondents % of respondents

18-30 42 21

30-40 57 28.5

40-50 54 27

Above 50 47 23.5

Total 200 100

Source: Primary Data

From the above table 4.1 it is inferred that 28.5% of the respondents belong to the age group of 30-

40, 27% of the respondents belong to the age group of 40-50, 23.5% of the respondents belong to the

age group above 50 and the least 21% of the respondents belong to the age group of 18-30.

Table 2 NAME OF THE BANK

Criteria No. of respondents % of respondents

SBI Bank 78 39

Canara Bank 52 26

Punjab National Bank 22 11

Axis Bank 14 7

HDFC Bank 24 12

ICICI Bank 10 5

Total 200 100

Source: Primary Data

It is clear from the table 4.8 that majority of the respondents keep accounts with SBI Bank – 39% and

the least is ICICI Bank with 5%.

Table 3 NO.OF RESPONDENTS WHO USE NET BANKING SYSTEM

Source: Primary Data

It is known from the table 4.10 that 94% of the respondents are using Net Banking system and 6%

of the respondents are not using Net Banking system.

Table 4 AWARENESS ABOUT GREEN BANKING

Criteria No. of respondents % of respondents

Yes 194 97

No 6 3

Total 200 100

Source: Primary Data

Criteria No. of respondents % of respondents

Yes 194 98

No 6 2

Total 200 100

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 -

6510(Online), Volume 7, Issue 2, February (2016), pp. 24-35 © IAEME Publication

30

M. Narmadha, “A Study on Customer Awareness on Green Banking in Selected Public and Private

Sector Banks in Chennai” – (ICAM 2016)

It is inferred from the table 4.14 that 97% of the respondents are aware of the Green Banking

services provided by their bank and 3% of the respondents are not aware of the Green Banking services

provided by their bank.

Table 5 VARIOUS GREEN BANKING INITIATIVES PROVIDED BY THE BANK

Source: Primary Data

It is more than 200 respondents because respondents have aware more than one initiative.

It is evident from the table 4.15 among all Green Banking initiatives, customers are aware of

Green Checking with 88%, Online Bill Payment with 78%, Facility of e – statement registration with

75% and they are not aware of Green Mortgages(68%), E – Investment services(61%), Conducting

Workshops and Seminars(60%), etc.

CHI-SQUARE ANALYSIS

HYPOTHESIS:

H0: There is no relationship between age of customers and awareness of Green Banking.

H1: There is a relationship between age of customers and awareness of Green Banking.

Awareness of Green Banking * Age of customers

Green Banking Initiatives

Aware Not Aware

No. of

respondents

% of

respondents

No. of

respondents

% of

respondents

Green Checking 176 88 24 12

Online Bill Payment 156 78 44 22

Facility of e-statement registration 150 75 50 25

Cash Deposit System 146 73 54 27

Reduced wastage of papers and

energy through Net Banking

approach

130 65 70 35

Use of Solar Powered ATMs 114 57 86 43

Using recycle paper or recycle waste 106 53 94 47

Green Mortgages 64 32 136 68

E – Investment services 78 39 122 61

Conducting Workshops and Seminars

for Green Banking 80 40 120 60

Green Loans 86 43 114 57

Providing recyclable debit cards and

credit cards 96 48 104 52

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 -

6510(Online), Volume 7, Issue 2, February (2016), pp. 24-35 © IAEME Publication

31

M. Narmadha, “A Study on Customer Awareness on Green Banking in Selected Public and Private

Sector Banks in Chennai” – (ICAM 2016)

Table 6 (Crosstabs)

Awareness of

Green Banking

AGE OF CUSTOMERS TOTAL

18-30 30-40 40-50 50 & above

N % N % N % N % N %

Yes 40 95.2% 57 100% 51 94.4% 46 97.9% 194 97%

No 2 4.8% 0 0% 3 5.6% 1 2.1% 6 3.0%

Total 42 100.0% 57 100.0% 54 100.0% 47 100.0% 200 100.0%

Source: Primary Data

Table 7 Chi-Square Tests

Value df Asymp. Sig. (2-sided)

Pearson Chi-Square

Likelihood Ratio

Linear-by-Linear Association

N of Valid Cases

3.546(a)

4.964

.005

200

3

3

1

.315

.174

.944

Source: Primary Data

4 cells (50.0%) have expected N less than 5. The minimum expected N is 1.26.

Since the p value (0.315) is greater than the table value (0.05).Therefore, this test shows that there

is no relationship between the age of customers and their awareness of Green Banking. (Chi – square =

3.546, p = 0.315).

This correlation is flagged as not significant, with the same p – value that was given for the Chi –

square test.

HYPOTHESIS

H0: There is no relationship between age of customers and usage of Green Banking.

H1: There is a relationship between age of customers and usage of Green Banking.

Usage of Green Banking * Age of customers

Table No. 8(Crosstabs)

AGE Total

18-30 30-40 40-50 50&

above

Using GB service YES N 37 55 51 45 188

% 88.1% 96.5% 94.4% 95.7% 94.0%

NO N 5 2 3 2 12

% 11.9% 3.5% 5.6% 4.3% 6.0%

Total N 42 57 54 47 200

% 100.0% 100.0% 100.0% 100.0% 100.0%

Source: Primary Data

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 -

6510(Online), Volume 7, Issue 2, February (2016), pp. 24-35 © IAEME Publication

32

M. Narmadha, “A Study on Customer Awareness on Green Banking in Selected Public and Private

Sector Banks in Chennai” – (ICAM 2016)

Table 9 Chi-Square Tests

Value df Asymp. Sig. (2-sided)

Pearson Chi-Square

Likelihood Ratio

Linear-by-Linear Association

N of Valid Cases

3.496(a)

3.082

1.472

200

3

3

1

.321

.379

.225

Source: Primary Data

4 cells (50.0%) have expected N less than 5. The minimum expected N is 2.52.

This test shows that there is no relationship between age of customers and usage of Green

Banking. (Chi – square = 3.496, p = 0.321). Therefore, H0 is accepted.

KOLMOGOROV – SMIRNOV TEST FOR A SINGLE SAMPLE

RANKING THE DIFFERENT MODES OF GREEN BANKING

Table 10

MODES LIKERT SCALE

TOTAL RANK 1 2 3

Solar Powered ATMs 126 110 57 293 I

Net Banking 110 100 120 330 II

Mobile Banking 70 80 270 420 III

Source: Primary Data

It is revealed from the table 5.15 that the respondents ranked ‘1’ for Solar Powered ATMs, Second

place is for Net Banking and 3rd

place is for Mobile Banking.

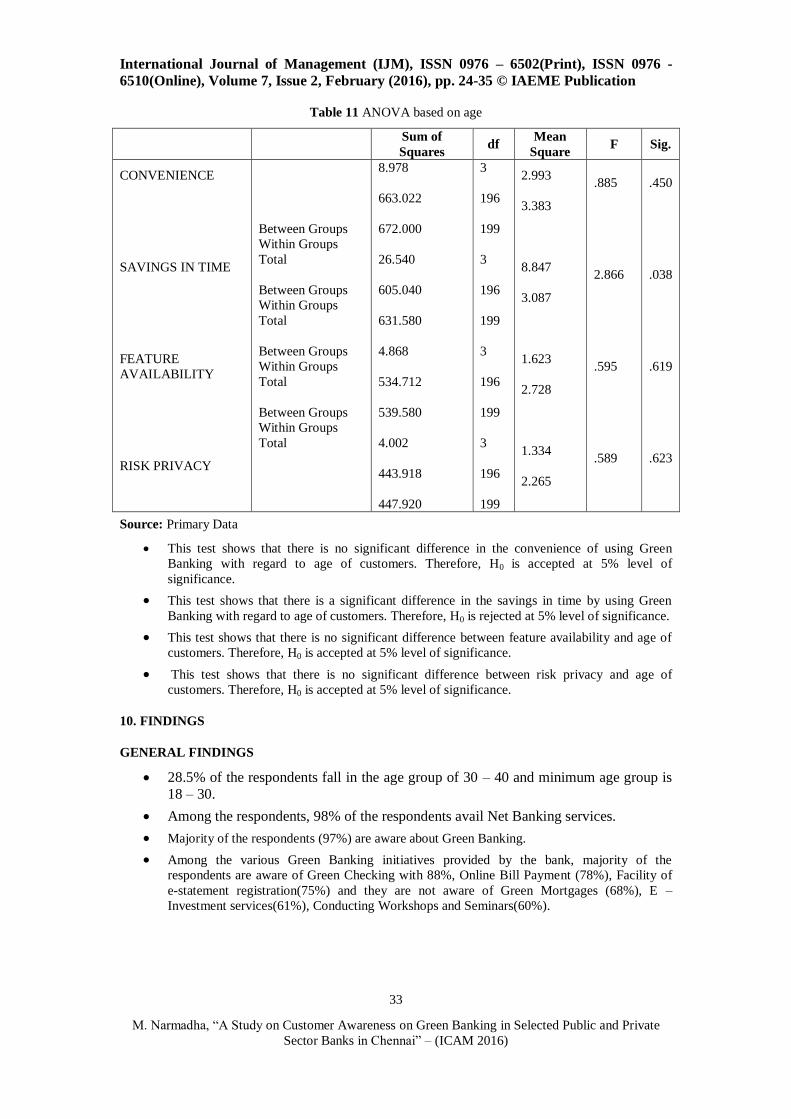

ONE – WAY ANOVA

HYPOTHESIS

H0: There is no significant difference in the convenience of using Green Banking with regard to age of

customers.

H1: There is a significant difference in the convenience of using Green Banking with regard to age of

customers.

H0: There is no significant difference in the savings in time by using Green Banking with regard to age

of customers.

H1: There is a significant difference in the savings in time by using Green Banking with regard to age

of customers.

H0: There is no significant difference in the feature availability with regard to age of customers.

H1: There is a significant difference in the feature availability with regard to age of customers.

H0: There is no significant difference between risk privacy and age of customers.

H1: There is a significant difference between risk privacy and age of customers.

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 -

6510(Online), Volume 7, Issue 2, February (2016), pp. 24-35 © IAEME Publication

33

M. Narmadha, “A Study on Customer Awareness on Green Banking in Selected Public and Private

Sector Banks in Chennai” – (ICAM 2016)

Table 11 ANOVA based on age

Sum of

Squares df

Mean

Square F Sig.

CONVENIENCE

SAVINGS IN TIME

FEATURE

AVAILABILITY

RISK PRIVACY

Between Groups

Within Groups

Total

Between Groups

Within Groups

Total

Between Groups

Within Groups

Total

Between Groups

Within Groups

Total

8.978

663.022

672.000

26.540

605.040

631.580

4.868

534.712

539.580

4.002

443.918

447.920

3

196

199

3

196

199

3

196

199

3

196

199

2.993

3.383

8.847

3.087

1.623

2.728

1.334

2.265

.885

2.866

.595

.589

.450

.038

.619

.623

Source: Primary Data

This test shows that there is no significant difference in the convenience of using Green

Banking with regard to age of customers. Therefore, H0 is accepted at 5% level of

significance.

This test shows that there is a significant difference in the savings in time by using Green

Banking with regard to age of customers. Therefore, H0 is rejected at 5% level of significance.

This test shows that there is no significant difference between feature availability and age of

customers. Therefore, H0 is accepted at 5% level of significance.

This test shows that there is no significant difference between risk privacy and age of

customers. Therefore, H0 is accepted at 5% level of significance.

10. FINDINGS

GENERAL FINDINGS

28.5% of the respondents fall in the age group of 30 – 40 and minimum age group is

18 – 30.

Among the respondents, 98% of the respondents avail Net Banking services.

Majority of the respondents (97%) are aware about Green Banking.

Among the various Green Banking initiatives provided by the bank, majority of the

respondents are aware of Green Checking with 88%, Online Bill Payment (78%), Facility of

e-statement registration(75%) and they are not aware of Green Mortgages (68%), E –

Investment services(61%), Conducting Workshops and Seminars(60%).

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 -

6510(Online), Volume 7, Issue 2, February (2016), pp. 24-35 © IAEME Publication

34

M. Narmadha, “A Study on Customer Awareness on Green Banking in Selected Public and Private

Sector Banks in Chennai” – (ICAM 2016)

SPECIFIC FINDINGS

There is no relationship between age of customers and awareness of Green Banking.

There is no relationship between age of customers and usage of Green Banking.

Solar Powered ATM is the preferred mode of Green Banking and the least mode is Mobile

Banking.

There is no significant difference in the convenience of using Green Banking with regard to

age of customers.

There is a significant difference in the cost saved by using Green Banking with regard to age

of customers.

There is no significant difference between feature availability and age of customers.

There is no significant difference between risk privacy and age of customers.

SUGGESTIONS

For Bankers

Bankers may educate the customers with Green Banking initiatives such as Green loans,

Green Mortgages, E – Investment services, etc.

Reward or Incentive can be given to the users of Green Banking.

Conducting Workshops, Seminars frequently to the bank employees as well as to the

customers and advertisement regarding Green Banking initiatives may be widely publicized.

Security aspects of the Green Banking may be enhanced through proper legislation.

Banking policies may be addressed on who hesitate to using Green Banking initiatives.

For Customers

To follow the restriction provided by the banks while using the Green Banking initiatives.

Personal Identification Number (PIN)/ Password to be kept secret.

Policies to bring illiterate people under the scope.

11. CONCLUSION

Banks are responsible corporate citizens. Banks believe that every small ‘GREEN’ step taken today

would go a long way in building a greener future and that each one of them can work towards to better

global environment. ‘Go Green’ is an organization wide initiative that moving banks, their processes

and their customers to cost efficient automated channels to build awareness and consciousness of

environment, nation and society. From the above research we can see that green initiatives like Green

Mortgages, E – Investment services, Conducting workshops and seminars for green banking, Green

Loans, Providing recyclable debit and credit cards is not familiar in Green initiatives by the bank as per

the respondents.

This concept of “Green Banking” will be mutually beneficial to the banks, industries and the

economy. Not only “Green Banking” will ensure the greening of the industries but it will also facilitate

in improving the asset quality of the banks in future.

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 -

6510(Online), Volume 7, Issue 2, February (2016), pp. 24-35 © IAEME Publication

35

M. Narmadha, “A Study on Customer Awareness on Green Banking in Selected Public and Private

Sector Banks in Chennai” – (ICAM 2016)

REFERENCES

[1] Axis Bank. (2013). Annual Report 2012-13.Mumbai-Axis Bank.

[2] Biswas N (2011), “Sustainable Green Banking Approach: The Need of the Hour”,

Business Spectrum, I (1), 32-38.

[3] Canara Bank (2013). 2012-13 Annual Report. Bangalore: Canara Bank.

[4] Green, C.F. “Business Ethics in Banking”. Journal of Business Ethics 8.8 (1989):631-

634

[5] HDFC Bank (2013). 2012-13. Annual Report. Bangalore: Canara Bank.

[6] ICICI Bank. (2014, 03 10). Go Green: ICICI Bank. Retrieved from ICICI Bank.

[7] Jasdeep Kaur (2014). “Green Banking in India”. Indian Journal of Applied Research.

Volume 4/Issue 1/January 2014/ ISSN 2249-555X

[8] JOMASS Volume 1/ Issue 1 /February 2014. ISSN 2348-6317

[9] Lalit M. Johri and Kanokthip S. (1998). “Green marketing of cosmetics and toiletries in

Thailand”. Journal of Consumer Marketing, 15(3), 265 – 281.

[10] Laxmi Mehar (2014). “Green Banking in India”. International Journal of Applied

Research and Studies. Volume 3, Issue 7, July 2014, ISSN: 2278-9480.

[11] Mamta Jain, Shailja Singh, T.N. Mathur (2014). “Green Banking- A Practical Approach

for Future Sustainability”. TRANS Asian Research Journals, Volume No.3, Issue-

1,January 2014, ISSN:2279-0667

[12] Neetu Sharma, Sarika. K. and R. Gopal. “A Study on Customers’ Awareness on Green

Banking in selected public and private sector banks with special reference to Mumbai”.

IOSR Journal of Economic and Finance. e –ISSN: 2231-5933; p-ISSN: 2348-6317, pp

28-35.

[13] PNB. (2011). 2010-11 Corporate Social Responsibility Report .New Delhi: PNB.

Retrieved from PNB – India.

[14] Sahoo, Pravakar and Nayak, Bibhu Prasad, (2008), Working Paper submitted to Institute

of Economic Growth, New Delhi.

[15] Sarita Bahl (2012). “The Role of Green Banking in Sustainable Growth”. International

Journal of Marketing, Financial Services and Management Research, Vol.1 No. 2,

February 2012, ISSN 2277 3622

[16] Sharma, K& Gopal. “A study on Customer Awareness on Green Banking initiatives in

selected Public & Private sector banks with special reference to Mumbai”

[17] State Bank of India (2014, 03 07). Web files: State Bank of India. Retrieved from SBI.

WEBSITE_GREEN_CHANNEL_COUNTER_NEW.pdf

[18] TRANS Asian Research Journals, Volume 3, Issue 1, January 2014, ISSN: 2279-0667.