a plan for agricultural business in the greater lansing region

TRANSCRIPT

A Plan for Agricultural Business in the Greater Lansing Region

October 2011

Page 2 of 24

ACKNOWLEDGEMENTS

Clinton, Eaton, and Ingham Counties, in cooperation with Tri-‐County Regional Planning Commission and with support from a Michigan State University Project GREEEN grant led the development of this plan to enhance agricultural economic development in the Greater Lansing region. Those directly involved in the project include:

Project Partners John Czarnecki, Clinton County Economic Alliance, Retired Claudine Hannold, Eaton County Community Development

Sandra Gower, Ingham County Economic Development Corporation Ed Reed, Delta Township Economic Development Corporation

Stacy Byers, Ingham County Farmland and Open Space Preservation Board and Clinton County Agricultural Preservation Board

Susan Pigg, Christine Hnatiw and Harmony Gmazel, Tri-‐County Regional Planning Commission

Steven Miller, Center for Economic Analysis, Michigan State University Mary Beth Graebert, Melissa Gibson, Tyler Borowy, Ryan Soucy and Mark Jones, Land

Policy Institute, Michigan State University

Advisory Committee John Forell, Eaton County Commissioner and farmer

David Roberts, Eaton County Farmland Preservation Board Chair Steve Thelen, Clinton County farmer

David Pohl, Clinton County Commissioner Jake Wambaugh, Ingham County Farmland and Open Space Preservation Board Laurie Koelling, Tanebaum Farms and Ingham County Farmland and Open Space

Preservation Board Dallas Henney, Leslie Township Supervisor, farmer, and Ingham County Farmland and

Open Space Preservation Board

Prepared by Kuntzsch Business Services, Inc. Rachel Kuntzsch, President

Meredith Johnson, Program and Policy Coordinator

Study Participants The research for this plan was made possible with the cooperation of farmers, agribusiness owners, elected officials, economic developers, planners, and landowners who attended forums, provided valuable input, and completed surveys.

Page 3 of 24

A. Table of Contents Introduction .............................................................................................................................. 4 Why Agriculture is Important to the Greater Lansing Region ................................. 5 The Economic Impact of Agriculture in the Greater Lansing Region ..................... 6 Our Planning Process ............................................................................................................. 8 Challenges to Agricultural Economic Development in Our Region ........................ 9 Opportunities for Agricultural Economic Development in Our Region ............. 14 Recommendations ............................................................................................................... 17 Conclusion ............................................................................................................................... 22 APPENDICES ........................................................................................................................... 24

Page 4 of 24

Introduction In the Greater Lansing counties of Clinton, Eaton, and Ingham, agriculture contributes approximately $450 million each year to our local economy and more than 5,000 jobs to our residents. Despite its importance to our region’s prosperity, local economic development planners often neglect to include the agricultural industry in their planning efforts. Economic development planning on a regional level that views the agricultural sector as an asset and supports agriculture industries will help our communities ensure their prosperity. This plan provides guidance for harnessing our local agriculture industry’s potential to drive future economic development for the region. The greater-‐metropolitan area of Lansing includes The City of East Lansing, Delta Charter Township, Delhi Charter Township and Meridian Charter Township. Other municipalities within the region include St. Johns, DeWitt, Charlotte, Eaton Rapids, Grand Ledge, Mason and Williamston. Our urban and suburban population provides substantial demand for fresh, local foods, while the significant amount of farmland can meet this demand. And while the total number of farms in the region has decreased over the last ten years, the total farm acreage has increased.1 The region continues to maintain and build upon its rich history in agriculture production. Despite the substantial job loss in the auto industry, the Lansing area has the unique opportunity to capitalize on its agricultural assets by planning for agricultural business. In order to grow as a viable industry, local farmers must adapt to changes by developing new markets, products, ways of doing business, and partnerships; and local economic developers should assist them in doing so. A hypothetical 5% increase in agricultural sales would create an additional $3.4 million in labor income, $5.7 million in property-‐type income, 259 new jobs and $22 million in economic output.2 This plan provides recommendations for improving the viability of agriculture and related industries, creating job opportunities, encouraging agricultural entrepreneurship, and driving economic prosperity. Specifically, these recommendations will help our agricultural community take innovative measures to 1 Michigan State University Land Policy Institute. (2011). Tri-County Agriculture: The Status, Conditions and Economic Impacts. East Lansing, MI. 2 Michigan State University Land Policy Institute. (2011). Tri-‐County Agriculture: The Status, Conditions and Economic Impacts. East Lansing, MI.

Page 5 of 24

increase the profitability of their farm businesses. They will also help local economic development professionals and land use planners recognize opportunities provided by agriculture-‐based businesses and link these businesses to critical incentives and opportunities.

Why Agriculture is Important to the Greater Lansing Region Agriculture in the Greater Lansing area provides significant economic support to the region while contributing to our unique cultural, environmental and social qualities. Farmers Produce and Market Locally Grown Foods Farmers in the Greater Lansing area have taken advantage of opportunities for marketing food to local consumers. Local farms provide a unique opportunity for residents to enjoy locally grown food, support the region’s farming heritage and economy and improve our quality of life. The Greater Lansing region hosts a multitude of farmers’ markets and roadside stands, providing fresh, healthy food to residents in rural, suburban, and urban areas. Our Region is an Agri-‐Tourism Destination Agri-‐tourism is a way of life for many in our area. In the fall, cider mills, pumpkin patches, and corn mazes draw thousands of visitors from the region’s population centers. Bed and Breakfasts located near farms attract visitors who are seeking to escape their busy lives to be nearer to open spaces. Increasingly, we look to agriculture as an entertainment source – visiting local farms to harvest Christmas trees or pick fruits and vegetables. Farms Contribute to our Unique Rural Character Many of us enjoy living in close proximity to open spaces and take advantage of the provisions and recreation that small towns supporting nearby farms provide. Charlotte, Grand Ledge, Williamston, DeWitt and St. Johns, which support the farming industry through infrastructure and marketing opportunities, each have unique, historic identities with which residents feel a special connection. These small towns and the surrounding rural areas also provide the opportunity for city dwellers in Lansing and surrounding suburbs to enjoy open lands without traveling great distances.

Page 6 of 24

Farms Limit Sprawl and Reduce Service Requirements for Local Governments Farmland provides another economic benefit to our region by lowering the level of services that local governments must provide. Agricultural lands do not demand sewer, utility, educational, and social services from local governments. Sustaining agriculture in the Greater Lansing region also helps to limit development pressure, while encouraging development in existing cities and villages where government services already exist. Our Farms Help Preserve the Natural Environment Agriculture allows for large expanses of land that help to preserve our region’s

natural environment. Farms help to minimize erosion, recharge groundwater, and sequester carbon, contributing to the health of the region’s residents while enhancing the quality of life that is attractive to new residents. Farms provide land suitable for many animal species, making hunting a sustainable economic activity in the region.

The Economic Impact of Agriculture in the Greater Lansing Region

Agriculture is a Significant Part of Our Economy Today In the Greater Lansing area, agriculture provides for 5,182 jobs3, which is more than the 4000 jobs that the local information technology sector provides,4 and $437 million in economic output, which is more than the $427 million that the local supply chain and logistics sector provides (see Figure 1).5 6 The region’s total agricultural sales are $320 million, but also add about $117 million in indirect and induced economic impact.7 However, the level of production in our region is not reflective of the amount of land engaged in farming practices, indicating a lower level of productivity compared to other regions of the state. The Greater Lansing region’s 3,409 farms and 679,982

3 Number includes direct, indirect and induced jobs (i.e. supply chain businesses and those contributing to the agriculture sector). 4 “Information Technology.” LeapInc. LeapInc. n.d. Web. 6 July 2011. 5 “Supply Chain Management and Logistics.” LeapInc. LeapInc. n.d. Web. 6 July 2011. 6 Michigan State University Land Policy Institute. (2011). Tri-County Agriculture: The Status, Conditions and Economic Impacts. East Lansing, MI. 7 United States Department of Agriculture. (2007). Census of Agriculture. Washington, DC: U.S. Government Printing Office.

Page 7 of 24

farmland acres comprise 6.8% of Michigan’s land base and 6.1% of Michigan’s total number of farms but contribute only 5.6% of Michigan’s total agricultural sales.

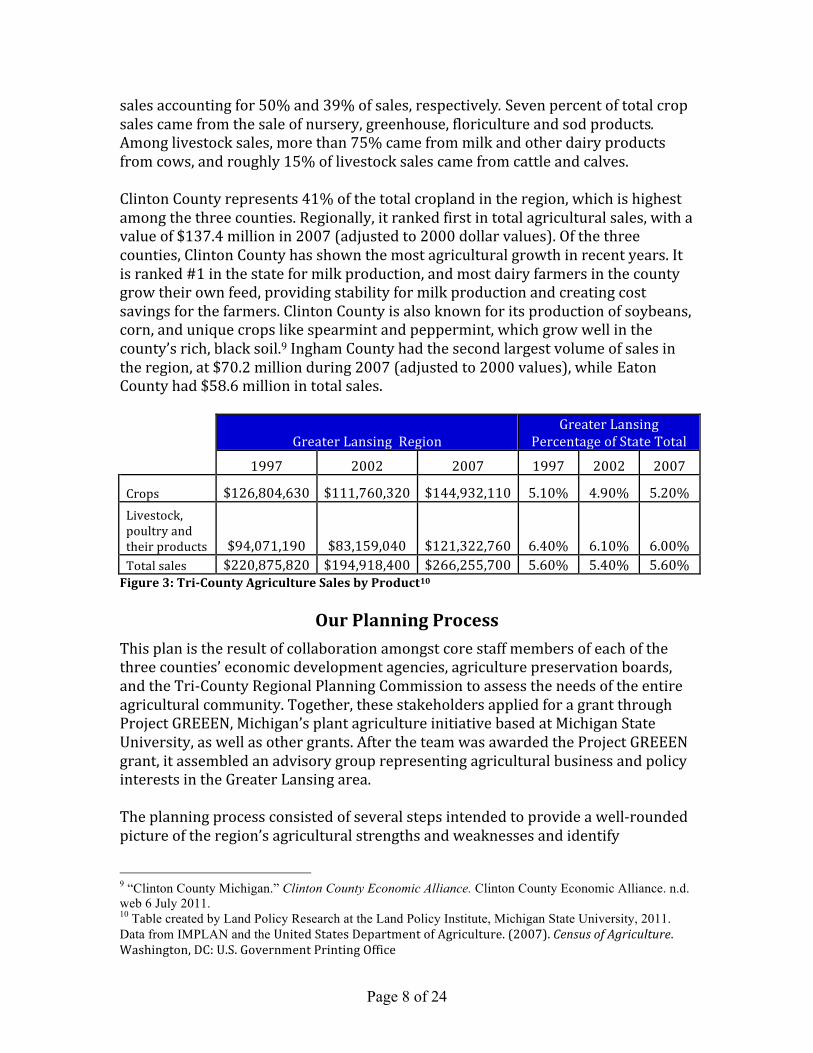

Figure 1: Current Contribution of Agriculture to the Greater Lansing Region’s Economy8 Regardless, agriculture has an economic impact that extends beyond crop production. Many non-‐agricultural businesses in our region supply the needs of farmers with farming equipment, electricity, petroleum, hired farm labor, and feed. After foods are harvested, they are stored, packed, shipped, and sold – creating a demand for jobs and putting more money into the economy. In order to sustain their businesses, agricultural producers must invest in real estate, capital and livestock, requiring loans and interest paid on those loans. Acreage and Production have not Changed in Recent Years Between 1997 and 2007, the number of farms in the region decreased but acreage and production remained relatively the same. Our region’s portion of the state’s farms, acreage and total sales of agricultural products (see Figure 2) have remained virtually unchanged from 1997 to 2007. The majority of regional sales are from crops, which were reported to be nearly $145 million in 2007 (adjusted to year 2000 dollars). Apart from regional sales figures, Clinton County’s greatest sales were from milk and other dairy products, and Ingham and Eaton County’s highest sales were from grains, oilseeds, dry beans, and dry peas. During the 10-‐year period between 1997 and 2007, agricultural sales were fairly evenly distributed between crops and livestock, with sales from crops exceeding those of livestock products by $23.6 million in 2007. More than 83% of crop sales came from grains, oilseeds, dry beans and dry peas in 2007 with corn and soybean 8 Table created by Land Policy Research at the Land Policy Institute, Michigan State University, 2011. Data from IMPLAN and the United States Department of Agriculture. (2007). Census of Agriculture. Washington, DC: U.S. Government Printing Office

Impact Category Direct Indirect Induced TotalLabor Income $35,649,535 $20,197,015 $12,461,951 $68,308,501Property-Type Income $82,409,608 $24,078,052 $7,900,661 $114,388,320Employment (People) 4,281 527 373 5,182Value of Output $320,788,996 $77,966,081 $38,283,211 $437,038,288

Figure 2: Tri-‐County Sales Compared to State Sales

Page 8 of 24

sales accounting for 50% and 39% of sales, respectively. Seven percent of total crop sales came from the sale of nursery, greenhouse, floriculture and sod products. Among livestock sales, more than 75% came from milk and other dairy products from cows, and roughly 15% of livestock sales came from cattle and calves. Clinton County represents 41% of the total cropland in the region, which is highest among the three counties. Regionally, it ranked first in total agricultural sales, with a value of $137.4 million in 2007 (adjusted to 2000 dollar values). Of the three counties, Clinton County has shown the most agricultural growth in recent years. It is ranked #1 in the state for milk production, and most dairy farmers in the county grow their own feed, providing stability for milk production and creating cost savings for the farmers. Clinton County is also known for its production of soybeans, corn, and unique crops like spearmint and peppermint, which grow well in the county’s rich, black soil.9 Ingham County had the second largest volume of sales in the region, at $70.2 million during 2007 (adjusted to 2000 values), while Eaton County had $58.6 million in total sales.

Greater Lansing Region Greater Lansing

Percentage of State Total

1997 2002 2007 1997 2002 2007

Crops $126,804,630 $111,760,320 $144,932,110 5.10% 4.90% 5.20% Livestock, poultry and their products $94,071,190 $83,159,040 $121,322,760 6.40% 6.10% 6.00% Total sales $220,875,820 $194,918,400 $266,255,700 5.60% 5.40% 5.60% Figure 3: Tri-‐County Agriculture Sales by Product10

Our Planning Process This plan is the result of collaboration amongst core staff members of each of the three counties’ economic development agencies, agriculture preservation boards, and the Tri-‐County Regional Planning Commission to assess the needs of the entire agricultural community. Together, these stakeholders applied for a grant through Project GREEEN, Michigan’s plant agriculture initiative based at Michigan State University, as well as other grants. After the team was awarded the Project GREEEN grant, it assembled an advisory group representing agricultural business and policy interests in the Greater Lansing area. The planning process consisted of several steps intended to provide a well-‐rounded picture of the region’s agricultural strengths and weaknesses and identify

9 “Clinton County Michigan.” Clinton County Economic Alliance. Clinton County Economic Alliance. n.d. web 6 July 2011. 10 Table created by Land Policy Research at the Land Policy Institute, Michigan State University, 2011. Data from IMPLAN and the United States Department of Agriculture. (2007). Census of Agriculture. Washington, DC: U.S. Government Printing Office

Page 9 of 24

opportunities for change. Early on, the project partners commissioned the Land Policy Institute at Michigan State University (MSU-‐LPI) to develop a methodology to gather and analyze data on agricultural production, which they shared at stakeholder meetings. To develop a plan for growing the viability of agriculture in the Greater Lansing region, it was critical to examine the region’s current agricultural profile and benchmark the sector’s economic impact. To that end, the project partners engaged MSU-‐LPI to develop a report, previously referenced – Tri-‐County Agriculture: The Status, Conditions, and Economic Impacts, which examines the Greater Lansing region’s agriculture makeup. The Report, contained in the appendices, highlights county-‐level statistics on agricultural production and sales, examines changes that occurred between 1997 and 2007, and estimates the agricultural sector’s impact on the economy. In order to get an “on the ground” assessment of the relationship between agriculture and economic development and establish goals for improving agricultural economic development in the region, a survey was distributed to farmers throughout the region with the assistance of Clinton, Eaton and Ingham County Farm Bureaus. The responses were used to develop the challenges and opportunities section of this plan and to identify recommendations for improving the region’s agricultural economy. The survey results, included in the appendices, can continue to be used to shape future agricultural economic development decisions. Farmers were asked to join local and regional planning officials, economic developers, agribusiness owners, and policy makers at the discussion forums. At these forums, participants, through small groups, responded to questions about challenges and opportunities impacting the region and determined. These discussions also helped inform this plan’s recommendations.

Challenges to Agricultural Economic Development in Our Region While agriculture has a significant impact on our region, there are challenges that hinder its growth. Part of our planning process was to seek out and identify these challenges. The following highlights primary challenges identified by regional stakeholders including farmers, economic developers, planners, agribusiness owners, and other community leaders who responded to a survey or attended a discussion forum. The survey and discussion forums, along with the Report

Page 10 of 24

referenced above, provided evidence that agriculture in the Greater Lansing region is fairly strong but faces some challenges, including conflict between agriculture and non-‐agriculture communities, and balancing environmental and quality of life values with the need to retain agriculture. A Lack of Processing Facilities Hinders Our Farmers Currently, there are no meat processing plants in the Greater Lansing area. ADM, Cargill and Tyson are the only three plants in the state, and they are located outside of the region. Because farmers are required to ship their raw goods to these locations, transportation costs are high and it becomes less likely that farmers will sell their products locally. According to the survey and the discussion forums, the Greater Lansing region lacks critical infrastructure for effective marketing of agricultural products. In addition to heightened transportation costs for getting products to processing facilities, there are few inexpensive options for farmers to transport their goods to market both within the region and to consumers outside the region. Zoning Regulations May Not Recognize Innovative Practices Participants in the discussion forums noted that zoning may limit agricultural use, particularly that which goes beyond traditional farming. Zoning regulations may not support new, innovative business opportunities (e.g. roadside farm stands, u-‐pick farms, biofuel production). Local ordinances may inadvertently stifle entrepreneurship through property maintenance codes or signage limitations. At the same time, as more residential development occurs in rural farming areas, incompatible uses between residents and the agricultural community become apparent, which could further limit innovative practices. Agriculture Lacks Support from Policymakers Some survey respondents and forum participants contend that policymakers do not provide adequate leadership for developing pro-‐farming policies and resist supporting the region’s agricultural economy as compared to its manufacturing economy. Studies support these observations -‐ government investment in food and agriculture in Michigan falls behind most other states.11 11 Cocciarelli, S., Smalley, S. and Hamm, M. (2011). Farm Viability and Development: Michigan Good Food Work Group Report No. 4 of 5. K. Colasanti (ed.) East Lansing, MI.

Page 11 of 24

Inactive Farmers Networks or Cooperatives Farmers Networks and Cooperatives can reduce costs by helping farmers market goods while reducing the amount of time farmers must spend away from their farms. Without the support of networks and cooperatives, farmers spend precious time attempting to market their own goods or have little choice over who buys their goods. This reduces the capacity for farmers to explore other revenue-‐building activities, like producing new varieties of specialty crops or starting an agribusiness enterprise on their farm. Lack of Access to Capital Many individuals who have the interest and knowledge to farm, including young farmers, have difficulty acquiring the necessary capital for starting a new agricultural business. According to the Chicago Federal Reserve Bank, Michigan farmland value has increased by better than ten percent, in contrast to a continuing decline in residential property value.12 This makes costs related to purchasing agricultural land relatively high in comparison to other opportunities. Farmers in our region may have difficulty accessing capital because they lack personal equity, are unable to convey farm production knowledge or establish a personal credit plan, and/or they lack a business plan or the ability to project a realistic cash flow.13 In addition there are few institutions in the region other than Greenstone Farm Credit Services that support agriculture, leaving farmers few options for lending sources. Farmers who wish to start new farm-‐based business start-‐ups, such as u-‐picks and cheese processing operations, face challenges in acquiring loans for these new projects. The lack of capital for expanded operation caps agricultural growth and prevents the production of local products. High Costs and Land Unavailability Limit Farmers’ Profitability Forum participants contend that there is not enough land available for purchase in our region, and even those who have access to land are faced with high fuel, fertilizer, processing and transportation costs. These factors create a barrier for

12 Wittenberg, E. and Hanson, S. (2009). Farmland Values Climb, Farm Earnings Soften. Michigan Farm News, February 15, 2009. 13 Cocciarelli, S., Smalley, S. and Hamm, M. (2011). Farm Viability and Development: Michigan Good Food Work Group Report No. 4 of 5. K. Colasanti (ed.) East Lansing, MI.

Page 12 of 24

younger generations of farming families who wish to continue farming operations as well as those who wish to start new businesses. Even for those who have an operating farm, it is not a given that the farm will generate sufficient revenue to cover farming expenses. More than half of the farmers surveyed either cannot cover expenses or cannot receive a meaningful income from farming (See Figure 4). This encourages some current farmers to sell their land and discontinue farming, and may act as a deterrent to young, qualified entrepreneurs who have the potential to enter the agriculture business.

According to the survey, larger farms tend to be more profitable. Two-‐thirds of farmers whose farm is their primary source of income operated more than 501 acres. Approximately 43% of farmers who indicated their farm is their secondary source of income, operated between 161 and 500 acres. As farm size decreases, more and more respondents answered that revenues do not contribute to total income nor do they cover expenses. In other words, respondents operating larger farms tended to be more financially viable. The average size of farms in the region is 200 acres and 40% of the region’s farms are 10 to 49 acres, which means most farms in our region are probably not profitable or covering costs.14 14 United States Department of Agriculture. (2007). Census of Agriculture. Washington, DC: U.S. Government Printing Office.

Figure 4: Farmer Revenue Generation

Page 13 of 24

Farmers Encounter Development Pressure Even though pressure on local farms to convert to non-‐agricultural uses has slowed somewhat in recent years due to the sluggish economy, 78% of farmers surveyed still feel development pressure is high. The promise of large buy-‐outs and comfortable retirements can be enticing to farmers who face volatile agricultural prices and inconsistent incomes.15 Furthermore, land that is suitable for agricultural production also tends to be desirable land for residential development. 16 If agricultural land is not profitable, it could transition out of agricultural use to residential use. Consumers Lack Knowledge about Farming According to the individuals that participated in the discussion forums, consumers in the Greater Lansing region lack knowledge of the benefits of supporting local agriculture (and the impact of not doing so). Many consumers believe that locally grown specialty items are too expensive for everyday consumption, but know little about the economic and nutritional benefits to consuming locally grown products, or how production of these local foods helps boost local job growth – not just directly on farms, but also at related businesses, such as farm implement dealers. Producers Need Greater Access to Information Based on comments from the discussion forums, producers may lack information about new crop types that can be successful in the region, partly due to limited access to the latest research or market trends. Most farmers surveyed indicated they were sticking to the production they know well rather than diversifying. Skilled Farm Labor is Difficult to Find and Retain Historically, farmers have relied on big families to provide labor for their farming operations. With smaller families becoming the norm and more children going on to college and professional careers outside of farming, the number of capable laborers has dropped significantly. The aging population of the farming sector may create a labor problem, as well. Among farmers responding to the survey, 76% are 50 years old or older, while only 18% are 40 years old or younger (See Figure 5). As farmers age and are no longer able to continue farming operations, there will be fewer young farmers to carry on where they left off.

15 Michigan State University Land Policy Institute. (2011). Tri-County Agriculture: The Status, Conditions and Economic Impacts. East Lansing, MI. 16 Cocciarelli, S., Smalley, S. and Hamm, M. (2011). Farm Viability and Development: Michigan Good Food Work Group Report No. 4 of 5. K. Colasanti (ed.) East Lansing, MI.

Page 14 of 24

Figure 5: Age Range of Survey Respondents

Opportunities for Agricultural Economic Development in Our Region

While there are challenges that hinder the growth of the community, there are countless opportunities to build our agricultural economy. The following highlights opportunities identified by those who responded to a survey or attended a discussion forum. Farmer Commitment to Keeping Farms in the Family Based on the survey responses, farmers in the region are committed to keeping their land in the family. Responding to the survey, 64% of farmers indicated they would not sell their land if offered a fair market value (See Figure 6) and 82% said they would give, sell, or will their land to a family member after they retire. This may indicate a

18-‐29 10%

30-‐39 8% 40-‐49 6%

50-‐59 28%

60+ 48%

Age range of Farmer Survey respondents

Figure 6: Farmer Motivation to Sell Land

Page 15 of 24

desire for farmers to continue to use their land for farming and to pass on agriculture skills to family members. Consumer Interest in Locally Grown Food The region has seen growth in interest for locally grown food and the benefits they provide. Currently, there are many farmers’ markets, food co-‐ops, community gardens and community-‐supported agriculture groups operating in the three counties, with distribution occurring in rural and suburban areas as well as the urban neighborhoods of Lansing. It is estimated farmers’ market sales result in an additional 50 cents in indirect or induced sales for every $1 of personal income earned.17 The Greater Lansing region boasts large production of specialty crops, which are conducive to supplying the demand for local foods. In fact, 44% of farmers responding to the survey grow specialty crops. Furthermore, farmers themselves believe that the public interest in locally grown food can benefit their businesses. Of farmers surveyed, 60% agreed or strongly agreed local efforts that support the “local food” movement will enhance their businesses. Government Programs Supporting Agriculture There are several state and federal government programs, which support our region’s agricultural base. Michigan’s Farmland and Open Space Preservation Program enables farmers to enter into development rights agreements with the state, promising to keep the land in agricultural use for a term of years in exchange for income tax benefits and exemptions from special assessments. Also, in recent years, the Michigan Department of Licensing and Regulatory Affairs and the Michigan Economic Development Corporation (MEDC) have provided increased support to agricultural businesses, including grants for farmers’ markets and

hoophouses (greenhouses with plastic roofs that can be used year-‐round for growing produce), and the formation of agricultural alliances in Southeast and Northwest Michigan.18 The Michigan Department of Agriculture and Rural Development (MDARD) provides support to agricultural businesses, including grant opportunities, a website of resources for agricultural business development, and training for food

17 Cocciarelli, S., Smalley, S. and Hamm, M. (2011). Farm Viability and Development: Michigan Good Food Work Group Report No. 4 of 5. K. Colasanti (ed.) East Lansing, MI. 18 Cocciarelli, S., Smalley, S. and Hamm, M. (2011). Farm Viability and Development: Michigan Good Food Work Group Report No. 4 of 5. K. Colasanti (ed.) East Lansing, MI.

Page 16 of 24

safety and pest management, among others. Our three counties also collaborate with MDARD to provide purchase of development rights opportunities for local farmers. The Michigan Agriculture Environmental Assurance Program (MAEAP) helps farms minimize agricultural pollution risks in a cost-‐effective way.19 Sixty-‐six percent of farmers surveyed indicated that the Michigan Right to Farm Act, which protects farmers from nuisance lawsuits, is important to the success of their businesses. The Michigan Right to Farm Act authorizes the Michigan Commission of Agriculture to develop and adopt Generally Accepted Agricultural and Management Practices (GAAMPs), which promote environmental stewardship and help maintain a farmer’s right to farm.20 Federal government subsidies and assistance are also available for area farmers. The Conservation Reserve Enhancement Program (CREP) is a voluntary land retirement program that helps agricultural producers protect environmentally sensitive land, restore wildlife habitat, and safeguard ground and surface water while receiving financial incentives.21 The federal Farm and Ranch Lands Protection Program (FRPP) provides matching funds to help purchase development rights to keep productive farms in active agricultural use.22 Entrepreneurial Farmers Some area farmers make added income by using farmlands for business opportunities other than crop production and livestock. These farmers engage in agri-‐tourism practices such as wineries, u-‐pick orchards, and restaurants that sell prepared food sourced from the farm. More farms are providing opportunities for sport hunting, which brings in revenue. In some places, agricultural zoning provides a community with balance by designating land for farming and other agricultural activities including farmstands and agri-‐tourism. The ability to provide services and products directly to consumers brings opportunity for business growth and continued farming while meeting needs of local citizens.23

19 http://www.maeap.org/maeap 20 http://www.michigan.gov/mdard/0,1607,7-125-1567_1599_47930---,00.html 21 http://www.apfo.usda.gov/FSA/webapp?area=home&subject=copr&topic=cep 22 http://www.nrcs.usda.gov/programs/frpp/ 23 Agricultural Tourism Local Zoning Guidebook and Zoning Ordinance Provisions, Michigan Agricultural Tourism Advisory Commission, 2007, p. 4.

Page 17 of 24

Access to Research and Other Resources Michigan State University (MSU), the nation’s first land grant institution and a leader in agricultural research and education, is located at the heart of the Greater Lansing region. The proximity of farms and local agricultural businesses to MSU provides unique access to research on agricultural best practices, technology advances, and a newly educated farm labor source. MSU Extension works with farmers to increase the success of their business and reach new markets through research and training.

Recommendations The following recommendations address the region’s challenges while capitalizing upon our agricultural opportunities. When implemented, these recommendations will help to drive economic prosperity by improving the viability of our region’s agriculture and related industries, creating job opportunities, and encouraging entrepreneurship. Economic development professionals can implement these proposed recommendations by including them as part of their local government’s economic development plans. Local government boards and officials may pass resolutions adopting the recommendations. Farmers may also advocate for the adoption of these recommendations. Include Agriculture in Economic Development Planning Economic development professionals should connect agriculture-‐based businesses with resources that can support agricultural economic development in the region. For example, economic development professionals should be aware of various state and federal funding opportunities for agriculture, as well as financing options, which can assist in the expansion of their businesses. In addition, strategies to support agriculture-‐based businesses should be included in economic development plans throughout the region. Currently, 10 out of 24 master plans in our region include language pertaining to the improvement or maintenance of the viability of the local agricultural economy. Fifty-‐seven percent of local zoning jurisdictions have single agricultural districts for general agricultural activities (farming, raising livestock, etc.); ten out of forty-‐two have additional agricultural districts specifically for preservation of prime farmland, and thirty-‐one jurisdictions allow for agricultural activity in districts not zoned for agriculture. Develop Zoning that Supports Innovative Farming Activities Local agencies can be of great assistance to farmers trying to engage in new agribusiness activities by working with farmers to develop zoning regulations that

Page 18 of 24

recognize new and innovative farming and agribusiness practices. By working collaboratively, farmers and local agencies can proactively develop zoning that is supportive of business growth. This may be accomplished through inclusion of farmers and agribusiness owners on local zoning boards, whereby stakeholders can develop a shared understanding of how current and future zoning practices help or hinder agriculture. Regional stakeholders could develop a model zoning ordinance conducive to agriculture and agribusinesses to be adopted by local governments, for example. Additionally, local agencies should provide local farmers’ groups and farmer networks with information about the beneficial services available to farmers that are attempting to engage in new agricultural practices. Agencies should also provide farmers with information on how to best work with current zoning regulations and acquire the right permits to engage in on-‐farm activities that will boost production. Encourage Development in Non-‐Agricultural areas In order to preserve productive agricultural land and allow farming operations to occur without pressure from development, commercial and residential growth should be concentrated in non-‐agricultural areas. Local planners and developers should focus new building near existing centers where infrastructure exists. Local planning boards, with the input of farming board members or stakeholders, should focus on this type of “smart growth” and develop zoning laws and practices that support the growth of our region’s agricultural economy.

Attract Agriculture Processing Facilities to the Region Of farmers surveyed, 78% felt that food processing business should be increased in the region. By increasing the number of food processing businesses in the region, farmers would benefit from cheaper, more efficient shipping. Instead of having to send their products 100 miles away or more, shipping distances will be reduced to 10-‐50 miles. Economic developers in the region should work with local farmers to develop innovative strategies for attracting processing facilities to the area. Encourage Agricultural Entrepreneurship Although dairy and row crop production are the strongest agriculture sectors in our region, potential growth opportunities in other areas are significant. The farmers surveyed ranked advanced agricultural technology, commodity crops, and alternative energy as having the most potential for economic growth. Other areas for growth include biomass electrical generation, value-‐added land-‐based products and timber management, local food processing, horticulture and nurseries, farm supply services and organic products.

Page 19 of 24

Some farmers have begun making their farms available to visitors for recreation. Farms make excellent locations for festivals, family reunions, and weddings, and more events of this type could be encouraged through providing farmers with access to marketing resources. Farmers should also be encouraged to find new uses for their products. For example, a Michigan State University researcher found that the cancer-‐fighting drug Taxol can be produced using enzymes from yew trees, a much cheaper method than current semi-‐synthetic organic chemistry approaches24. Local farmers can capitalize upon the discovery of new markets like this to make their businesses more profitable and sustainable. Our region needs to focus resources towards the opportunity for agricultural growth in order to foster agricultural entrepreneurship. Local financial institutions should be encouraged to lend to agricultural producers with new ideas, and processing facilities, suppliers, and agricultural services industries need to be incentivized to locate in our region.

Link Agricultural Activities to Community Development Efforts Local and downtown development activities do not need to occur separately from agricultural economic development opportunities. Downtown development organizations should be encouraged to cooperate with local agricultural vendors. Some localities have embraced opportunities to leverage agricultural and non-‐agricultural local economic growth. Many communities in the region host a farmers’ market in their downtown areas. This provides multiple benefits by drawing people that are primarily there to pick up fruits and vegetables at the farmers market into nearby stores for gifts or lunch, while those who are visiting downtowns to shop at the stores may purchase items from one of the farmers’ market vendors. This scenario allows for increased marketing for both shops and market vendors. The benefits and success of farmers’ markets in the region should be shared with other communities to encourage the expansion of additional markets. Food vendors can also be clustered into food business districts to attract buyers and encourage vendors to work together. The Lansing City Market is an example of a food district that provides exposure for local agricultural producers with value-‐added businesses. Shoppers can purchase fresh fruit and vegetables, stop at a café for lunch, and pick up some gelato or homemade cookies, all purchased from local 24 http://www.in-pharmatechnologist.com/Processing-QC/Effective-biosynthetic-alternative-to-Taxol-production-discovered

Page 20 of 24

producers. Other communities in the region could work with area growers to develop and promote food districts. Advocate for Government Support Our agriculture community should reach out to state and local policy leaders, emphasizing that agriculture and agricultural products should be given equal weight to the re-‐tooling of the auto-‐industry. State government should help support exports from the region and financial capital for agricultural practices. Agriculture-‐related organizations should work to ensure agriculture is incorporated into local economic development planning efforts. According to the farmer survey, 78% of farmers whose farms provide their primary source of income have more than three-‐quarters of their land enrolled in the State of Michigan’s Farmland and Open Space Preservation Program (commonly referred to as PA 116). The majority of respondents whose farms do not provide a primary source of income have no land enrolled in the program. This data may indicate that farmers tend to thrive when they can receive the tax benefits associated with farmland preservation. Regional planners, economic development officials, and policymakers should work with local groups to ensure area farmers are fully aware and take advantage of financial incentive programs such as PA 116, FRPP, CREP and the state farmland preservation program. These groups may consider providing services to area farmers to assist them with the application process to such programs. Market Our Agricultural Products Our region should work to promote the importance and prevalence of agricultural products in our communities, as well as the variety of different types of farming practices, like organic and local. Promotion and education is necessary to achieve a positive public perception of farming in the region, and to help farmers get to know the needs of consumers. Agriculture should be included in local economic development promotion. An inventory of agricultural assets would be a helpful guidance tool for farmers and a source of information for the community as a whole. Regional branding and the location of value-‐added practices, like marketing, processing and distribution, within the region would create a community connection to agriculture and encourage farmers and processors to locate their business and invest here. Consumers and farmers should buy agricultural products and supplies from local suppliers. By focusing demand inward, more dollars will be put into the local

Page 21 of 24

economy, and farmers and suppliers will be encouraged to expand or create new businesses. Our region is home to hundreds of schools, hospitals, colleges, universities and large businesses that have the power to influence the local food supply chain. These entities should be encouraged to source products, such as milk, fruits and vegetables from local producers. To encourage marketing of locally grown food, relationships between local restaurants and local producers should also be encouraged. Improve Access to Financial Resources Revenue sharing, property tax alternatives, cost-‐sharing, tax rebates and grants are all financial incentives that help to attract new farming operations to the community and retain current ones. Tax incentives for farming operations should be encouraged. State agencies can establish loan programs for first-‐time farmers, or provide banks with loan guarantees. MDARD can set aside grants for farm financial planning. Local financial institutions should be educated about the benefits of lending to agricultural businesses and encouraged to do so. Economic development professionals can connect agricultural businesses with the resources needed to apply for SBA loans. Finally, angel investors and venture capitalists should be encouraged to look at entrepreneurial agricultural businesses as a smart way to invest their resources and contribute to the local economy. Improve and Expand Farmers’ Networks Farmers’ networks and co-‐operatives (co-‐ops) are examples of organizations through which farmers share resources that help save costs or encourage innovation and help to expand the capacity of these groups. Economic development coordinators and non-‐governmental organizations should initiate support for these types of networks. Some successful examples of current networks include the Michigan Farmers Market Association, which provides services such as insurance, education, policy support and peer-‐to-‐peer networking to members.25 The Starting Block Incubator in Hart, Michigan provides licensed commercial facilities, entrepreneurial education, and peer-‐to-‐peer networking to food and natural resource related businesses26. Networks should have access to production, market and other data that can show trends in the local food supply chain.

25 http://www.mifma.org/home/ 26 http://www.startingblock.biz/about.htm

Page 22 of 24

Make Information About Local Agriculture Accessible It is critical to educate planners, economic developers, policymakers, retailers, consumers, and youth about what is grown in our region and how supporting local agriculture benefits the economy in the Greater Lansing region. Regional leaders could develop a promotional campaign to educate and collaborate with these audiences to promote local agriculture. Farmers themselves need access to education, including assistance with business plans, production, and management.27 This can be achieved with the development of start-‐up assistance apprenticeships. Access to information on marketing materials, including information on supply, demand, and markets is also crucial. Farmers also need information on best practices and new technologies that could improve or make their operations more innovative, perhaps meeting a certain market need. Groups that provide services to farmers, like the MSU Agricultural Product Center and MSU Extension, and other non-‐governmental organizations, should hold conferences and disseminate newsletters and brochures with information about new agricultural technologies.

Conclusion Agriculture and agriculture-‐based businesses are key drivers to Greater Lansing’s regional economy. This plan was developed to further encourage agriculture economic development in the region. Recommendations include:

• Include Agriculture in Local Economic Development Planning • Develop Zoning that Supports Innovative Farming Activities • Encourage Development in Non-‐Agricultural Areas • Attract Agriculture Processing Facilities to the Region • Encourage Agricultural Entrepreneurship • Link Agricultural Activities to Community Development Efforts • Advocate for Government Support • Market Our Agricultural Products • Improve Access to Financial Resources • Improve and Expand Farmers’ Networks • Make Information About Local Agriculture Accessible

It is the aim of this plan’s authors that local economic developers, planners, agriculture-‐based business owners, farmers, local officials, and other stakeholders will work together to implement these recommendations. Many of these strategies will require additional funding to complete. For example, follow-‐on projects could include: convening stakeholders to draft a model zoning ordinance that is favorable to agribusinesses; identifying and cataloguing resources for farmers, economic 27 Cocciarelli, S., Smalley, S. and Hamm, M. (2011). Farm Viability and Development: Michigan Good Food Work Group Report No. 4 of 5. K. Colasanti (ed.) East Lansing, MI.

Page 23 of 24

development professionals, and zoning officials; or developing a public outreach campaign on agriculture’s impact to the regional economy. Project partners are committed to exploring funding sources to implement this plan, which will support our rich agricultural heritage, create job growth, and enhance our quality of life.

Page 24 of 24

APPENDICES

Tri-‐County Agriculture: The Status, Conditions, and Economic Impacts Report

Farmer Survey Results

Tri-‐County Agricultural Zoning Assessment

A REPORT ON CLINTON, EATON AND INGHAM COUNTIES

MICHIGAN TRI-COUNTY AGRICULTURE

status, conditions andeconomic impactsTH

E

August 31, 2011

BY THE LAND POLICY INSTITUTE AT MICHIGAN STATE UNIVERSITY

08.31.11

Support for this project was provided by Project

GREEEN at Michigan State University and the

W.K. Kellogg Foundation through the People

and Land Initiative, administered by the MSU

Land Policy Institute (LPI) and Public Sector

Consultants. The Land Policy Institute would

like to thank our partners on this project:

� The Tri-County Regional Planning

Commission;

� The Ingham County Agricultural

Preservation Board;

� The Clinton County Economic

Development Alliance;

� The Eaton County Community

Development Department;

� The MSU Department of Agriculture,

Food and Resource Economics; and

� Kuntzsch Business Services.

About Land Policy Research

Research and analysis is supported by the Land

Policy Research (LPR) team at the Land Policy

Institute at Michigan State University.

Tyler BorowyResearch Analyst

Ben CalninData and Informatics Coordinator

Melissa GibsonResearch Manager

Mary Beth GraebertAssociate Director for Programs and Operations

Acknowledgements

repo

rt

TRI-COUNTY AGRICULTURE

In order to ensure that agriculture remains

a sustainable and viable resource for

the Tri-County Region of the Greater

Lansing Area (Clinton, Eaton and Ingham

counties in Mid-Michigan) and a vital part of

the state’s economy, an agricultural economic

development plan is needed to focus regional

efforts and bring greater awareness to the

critical role agriculture and agricultural

businesses can play as part of a comprehensive

economic development strategy. To achieve

this, the Land Policy Institute (LPI) at

Michigan State University (MSU); the Ingham

County Agricultural Preservation Board; the

Tri-County Regional Planning Commission;

the MSU Department of Agriculture, Food

and Resource Economics; the Clinton County

Economic Development Alliance; and the

Eaton County Community Development

Department Alliance partnered to develop

the Tri-County Regional Agricultural Economic

Development Plan. The planning process

consists of five steps, that once complete, will

comprise the Agricultural Economic Development

Plan, including:

� A regional agricultural sector baseline

assessment (this report).

� A series of listening sessions involving

farmers, citizens, local planning

officials, local and regional leaders, and

other policy makers (completed in the

spring of 2011).

� A survey of farmers to assess the

relationship between agriculture and

economic development in the region

(May–June, 2011).

� An assessment of zoning ordinances

and master plans pertaining to

agricultural land uses (June 2011).

� The development of A Plan for

Agricultural Business in the Greater Lansing

Region (August 2011).

This report presents the regional agricultural

baseline assessment of the Tri-County

Region. It highlights county-level statistics on

agricultural production and sales, examines

the changes that have occurred over the

10-year period from 1997 to 2007, in five-

TRI-COUNTY AGRICULTURE: Status, Conditions and Economic Impacts

THIS REPORT PRESENTS THE REGIONAL AGRICULTURAL BASELINE ASSESSMENT OF THE TRI-COUNTY REGION (CLINTON, EATON AND INGHAM COUNTIES) OF THE GREATER LANSING AREA. IT HIGHLIGHTS COUNTY-LEVEL STATISTICS ON AGRICULTURAL PRODUCTION AND SALES, EXAMINES THE CHANGES THAT HAVE OCCURRED OVER THE 10-YEAR PERIOD FROM 1997 TO 2007, IN FIVE-YEAR INCREMENTS, AND ESTIMATES THE REGIONAL ECONOMIC IMPACT OF THE AGRICULTURAL SECTOR.

Executive Summary

i

the status, conditions and economic impacts

land

pol

icy

inst

itut

e

year increments (U.S. Census of Agriculture

information is released every five years),

and estimates the regional economic impact

of the agricultural sector. Having a firm

understanding of the status and conditions of

the agricultural industry and the contribution

it makes to the local economy, and the

promotion of such information and the sector’s

needs, can bring greater awareness to this

sector of the economy—which is often ignored

in economic development planning. This

report is one step in promoting awareness

and understanding of the status of tri-county

agriculture in Mid-Michigan.

When examining agricultural statistics

for the Tri-County Region, Table 1 suggests

that agriculture in the Tri-County Region is

diverse and relatively strong, but that it also

may face some challenges. In 2007, its sales

contributions to Michigan’s agricultural

economy (5.6%) are slightly less than its

percentage of land in farms (6.8%) and its total

number of farms (6.1%). A minor decline in

sales between 1997 and 2002 was overcome by

a sizeable gain between 2002 and 2007. From

1997–2007, tri-county agriculture kept pace

with the state in terms of sales, but did not

exceed the state trend.

As a robust sector of our regional and state

economies, understanding the economic

impacts of agriculture to the regional economy

is necessary for increasing agricultural

awareness and encouraging its incorporation

into economic development plans. Table

2 presents the total economic impact of

agriculture in the Tri-County Region (in 2007

dollar values), which includes:

� $68 million in labor income;

� $114 million in property-type income;

Table 1: Tri-County Region Agricultural Statistics for 1997, 2002, and 2007

Michigan Tri-County RegionTri-County % of

State Total1997 2002 2007 1997 2002 2007 1997 2002 2007

Crops ($1,000) $2,476,501 $2,268,123 $2,763,840 $126,805 $111,760 $144,932 5.1% 4.9% 5.2%

Livestock, Poultry, and Their Products ($1,000) $1,476,796 $1,353,415 $2,011,332 $94,071 $83,159 $121, 323 6.4% 6.1% 6%

Total Sales ($1,000) $3,953,297 $3,621,538 $4,775,172 $220,876 $194,918 $266,256 5.6% 5.4% 5.6%

Number of Farms 53,519 53,315 56,014 3,507 3,418 3,409 6.6% 6.4% 6.1%

Land in Farms (Acres) 10,443,935 10,142,958 10,031,807 702,348 679,152 679,982 6.7% 6.7% 6.8%

Harvested Cropland (Acres) 6,989,300 6,827,903 6,859,081 514,972 515,271 523,490 7.4% 7.6% 7.6%

Sources: Table created by the Land Policy Institute, Michigan State University, 2011. Data from the 2002 and 2007 USDA National Agricultural Statistics Service, Census of Agriculture. Note: See Appendix B for Global Commodity Price Index.

the status, conditions and economic impacts

land

pol

icy

inst

itut

e

ii

repo

rt

TRI-COUNTY AGRICULTUREiii

� More than 5,182 jobs; and

� Approximately $437 million in

economic output.

A hypothetical 5% increase in agricultural

sales would create an additional:

� $3.4 million in labor income;

� $5.7 million in property-type income;

� 259 new jobs; and

� $22 million in economic output.

The Tri-County Region is endowed with

a variety of land cover types. The greater-

metropolitan area of Lansing includes East

Lansing, Delta Township, Delhi Township

and Meridian Township. Several nearby cities

include St. Johns, Dewitt, Charlotte, Eaton

Rapids, Mason and Williamston. Outside of

the region’s urbanized area, predominant land

cover includes agricultural types, primarily

those devoted to row crops and grains, hay,

and seeds. Natural land types compose the

majority of the remainder of land cover in the

region (see Figures 1 and 2).

Based on Cropland Data Layer (CDL) and

U.S. Census of Agriculture information, the

following briefly highlight agricultural figures

of the three counties included in the Tri-

County Region:

Clinton County

� Contains 41% of the total cropland in

the region, which is highest among the

three counties.

� Regionally, it ranked first in total

agricultural sales, with a value of

$137.4 million in 2007 (adjusted to

2000 dollar values), with more than

$83.2 million in livestock, poultry and

their products.

Ingham County

� In 2007, had the second largest value

of sales in the region, at $70.2 million

(adjusted to 2000 values).

� Had high sales in grains, oilseeds, dry

beans, and dry peas along, with milk

and other dairy products from cows

accounting for most of these sales.

Table 2: Contribution of Agriculture to the Tri-County Region’sEconomy for 2007

Impact Category Direct Indirect Induced TotalLabor Income $35,649,535 $20,197,015 $12,461,951 $68,308,501

Property-Type Income $82,409,608 $24,078,052 $7,900,661 $114,388,320

Employment (People) 4,281 527 373 5,182

Value of Output $320,788,996 $77,966,081 $38,283,211 $437,038,288

Sources: Table created by the Land Policy Institute, Michigan State University, 2011. Data from IMPLAN and the 2007 USDA National Agricultural Statistics Service, Census of Agriculture.Note: See Appendix C for definitions of Direct, Indirect, Induced and Total Effects.

the status, conditions and economic impacts

land

pol

icy

inst

itut

e

Figure 2: Proportional Land Cover for theTri-County Region for 2007

Source: Figure created by the Land Policy Institute, Michigan State University, 2011. Data from the USDA National Agricultural Statistics Service, 2009 Michigan Cropland Data Layer.

iv

Figure 1: Land Cover Types for the Tri-County Region of Mid-Michigan

Source: Figure created by the Land Policy Institute, Michigan State University, 2011. Data from the USDA National Agricultural Statistics Service, 2009 Michigan Cropland Data Layer.

repo

rt

TRI-COUNTY AGRICULTURE

Eaton County

� With $58.6 million in

total sales (adjusted

to 2000 dollar

values), Eaton County

saw most of its sales

come from grains,

oilseeds, dry beans

and dry peas.

The Tri-County Region has an

established agricultural base

that, based on this report and

listening session responses,

could be expanded and

enhanced to help the region

achieve increased agricultural

economic activity, and could

increase its sales and bolster

its markets.

This report identifies the

region’s agricultural status and conditions

alongside economic impacts. It will be

integrated into the Agricultural Economic

Development Plan, which will assist in linking

agriculture and economic development. The

plan will also help guide the region along

a mutually beneficial path toward regional

and statewide prosperity through expanding

agricultural business opportunities.

v

the status, conditions and economic impacts

land

pol

icy

inst

itut

e

1

Executive Summary................................................................................................................................................................i

Tri-County Agriculture Assessment..............................................................................................................................3

Background.......................................................................................................................................................................3

Agricultural Base of the Tri-County Region.......................................................................................................5

Agriculture-Related Industries, Region-Wide................................................................................................10

Economic Impact of Agriculture in the Tri-County Region......................................................................13

County-Based Assessments of Agriculture in the Tri-County Region of Mid-Michigan.....................16

Clinton County Agriculture Assessment...........................................................................................................18

Eaton County Agriculture Assessment..............................................................................................................22

Ingham County Agriculture Assessment..........................................................................................................26

Conclusion...............................................................................................................................................................................30

Appendices...............................................................................................................................................................................31

References................................................................................................................................................................................38

Table of Contents

Figure 1: Land Cover Types for the Tri-County Region of Mid-Michigan...................................................iv

Figure 2: Proportional Land Cover for the Tri-County Region for 2007......................................................iv

Figure 3: Number of Farm Proprietors and Their Net Income for the Tri-County Region

for 1969–2007........................................................................................................................................................15

Figure 4: Clinton County Land Cover Types............................................................................................................19

Figure 5: Clinton County Proportional Land Cover for 2009...........................................................................21

Figure 6: Number of Clinton County Farm Proprietors and Their Net Income for 1969–2007.........21

Figure 7: Eaton County Land Cover Types................................................................................................................23

Figure 8: Eaton County Proportional Land Cover for 2009..............................................................................23

Figure 9: Number of Eaton County Farm Proprietors and Their Net Income for 1969–2007.............25

Figure 10: Ingham County Land Cover Types..........................................................................................................27

Figure 11: Ingham County Proportional Land Cover for 2009.........................................................................27

Figure 12: Number of Ingham County Farm Proprietors and Their Net Income for 1969–2007.......29

Figure 13: Global Corn, Soybean and Wheat Prices for 1996–2011.................................................................34

Figure 14: Global Beef and Poultry Prices for 1996–2011......................................................................................35

Figures

repo

rt

TRI-COUNTY AGRICULTURE2

Table 1: Tri-County Region Agricultural Statistics for 1997, 2002 and 2007................................................ii

Table 2: Contribution of Agriculture to the Tri-County Region’s Economy for 2007.............................iii

Table 3: Percentage of Total Land Cover Acreages for 2007 for Michigan and the

Tri-County Region................................................................................................................................................7

Table 4: Agricultural Sales by Type for 1997, 2002 and 2007 for Michigan and the

Tri-County Region................................................................................................................................................8

Table 5: Farms and Acreage for 1997, 2002 and 2007 for Michigan and the Tri-County Region.........8

Table 6: Agricultural Sales by Type for 1997, 2002 and 2007 for the Tri-County Region........................9

Table 7: Number of Businesses, Employment and Sales for the Tri-County Region for 2009........11-12

Table 8: Current Contribution of Agriculture to the Tri-County Region’s Economy.............................14

Table 9: Potential Increased Contribution to the Tri-County Region’s Economy from a 5%

Increase in Agricultural Sales.........................................................................................................................14

Table 10: Each County’s Percentage of Agricultural Acreage in the Tri-County Region for 2007.....17

Table 11: Clinton County Land Cover Acreages for 2009....................................................................................18

Table 12: Clinton County Farms and Farm Acreage for 1997, 2002 and 2007.............................................19

Table 13: Clinton County Agricultural Sales by Type for 1997, 2002 and 2007.........................................20

Table 14: Eaton County Land Cover Acreages for 2009.......................................................................................22

Table 15: Eaton County Farms and Farm Acreage for 1997, 2002 and 2007................................................24

Table 16: Eaton County Agricultural Sales by Type for 1997, 2002 and 2007.............................................24

Table 17: Ingham County Land Cover Acreages for 2009...................................................................................26

Table 18: Ingham County Farms and Farm Acreage for 1997, 2002 and 2007............................................28

Table 19: Ingham County Agricultural Sales by Type for 1997, 2002 and 2007........................................28

Tables

Appendix A: Data Sources and Issues..........................................................................................................................31

Appendix B: Global Commodity Sales for Major Crops and Livestock.......................................................34

Appendix C: Glossary of Terms......................................................................................................................................36

Appendices

the status, conditions and economic impacts

land

pol

icy

inst

itut

e

tri-county region agriculture assessment

MICHIGAN IS ENDOWED WITH THE COMBINATION OF SOIL, CLIMATE AND WEATHER PATTERNS TO CREATE ONE OF THE MOST DIVERSE AGRICULTURE SECTORS IN THE NATION. IT RANKS SECOND ONLY TO CALIFORNIA IN THE DIVERSITY OF AGRICULTURAL PRODUCTS. MICHIGAN HAS A SIGNIFICANT EDGE, WITH ITS UNIQUE ENDOWMENT AND ABUNDANCE OF AVAILABLE WATER TO SUPPORT A WIDE-RANGE OF FARMING OPERATIONS ACROSS THE STATE. THE TRI-COUNTY REGION IS WELL-POSITIONED, BOTH GEOGRAPHICALLY AND ECONOMICALLY, TO CAPITALIZE ON ITS AGRICULTURAL ASSETS.

Tri-County Region

3

Background

Land is the primary resource upon which

American prosperity was built. Until

the mid to late 1850s, the utilization

of land to optimize the performance of land-

based industries (e.g., agriculture or industry)

was the primary focus of land planning and

policy. Thomas Jefferson and Alexander

Hamilton vigorously debated the future of the

U.S. development of land. Jefferson believed

that the republic’s strength lay in its agrarian

roots and a decentralized government.

Hamilton advocated for industry in urban

centers and a strong and efficient central

federal government. Clearly, parts of both

philosophies prevailed and, as a result, both

agriculture and industry have flourished since

the founding of the United States.

Following the Civil War, a key goal of U.S.

agricultural policy was the enhancement

of agricultural yield and productivity,

while guaranteeing national food security.

Commodity price support programs helped

to mask various inefficiencies inherent

in commodity-focused agriculture, while

obscuring unique market and ecological

opportunities for agriculture at the state and

local levels (Keeney and Kemp, 2003).

Since the Industrial Revolution, however, the

focus on land in the United States has been

more on its potential for development into

non-agricultural uses (such as for locating

manufacturing industries or housing) than on

the maintenance of an agricultural base. The

post-World War II phenomenon of sprawling

cities changed how people perceived land.

Where once it was valued for the quality of its

soil and potential for agricultural production,

it came to be judged by its locational proximity

and building potential. The development

pressure facing farm families, with the promise

of large buy-outs and comfortable retirements,

was and remains enticing, particularly with

the volatile agricultural prices farmers face.

Since the 1983 Dairy and Tobacco Adjustment

Act and the subsequent diminished emphasis

on national government intervention,

repo

rt

TRI-COUNTY AGRICULTURE4

agricultural policy development has

increasingly become the responsibility of state

and local governments (Offutt et al., 2004).

For example, in the area of marketing, such

issues as eco-tourism, agro-entertainment,

value-added farm diversification, right-to-farm,

specialty markets, farmland preservation,

direct marketing, new use agriculture

and the management skills of farmers are

increasingly being pursued at the state level as

opportunities to enhance the competitiveness

and retention potential for agriculture (Babb

and Long, 1987). Simultaneously, the aesthetic

and ecological dimensions of the industry are

also becoming more clearly illuminated (Offutt

et al., 2004).

The enhancement of farm viability has, thus,

become an agricultural policy goal at state

and local levels (Adelaja and Sullivan, 1998).

Rapid consolidation of farms and the apparent

limited viability of many mid-size farms,

in the 1960s and 1970s, led many states to

explore mechanisms for direct intervention

in the economic plight of state agriculture.

In such states as Iowa, Michigan, Maryland,

Massachusetts, Minnesota, New Jersey and

Ohio, policies are being implemented to

address viability issues.

The debate about the future survival of

agriculture has gone well beyond the discourse

in the 1980s about farm viability (Adelaja

and Rose-Tank, 1988; Adelaja et al., 1989).

Farmers must coexist with their neighbors

and take advantage of the unique local features

in order to survive well into the future.

Water management practices, chemical

usage strategies, good neighbor relations,

participation in federal conservation programs

(e.g., Conservation Reserve Programs), generally

accepted agricultural management practices

(GAAMPs) and other factors that contribute to

sustainability could potentially impact viability.

The chemistry between agriculture and

economic development can certainly be

traced back to Jefferson and Hamilton. Yet

its modern roots took shape in the 1960s.

Johnston and Mellor (1961) discuss the false

dichotomy between agricultural and industrial

development, arguing that agriculture’s role in

economic development is primarily dependent

on the amount of people living in rural areas

and at what stage of economic development

a particular community may be facing. In

other words, agricultural and industrial

developments are not mutually exclusive.

tri-county region agriculture assessment

the status, conditions and economic impacts

land

pol

icy

inst

itut

e

5

Yet even today, the economic development

literature has favored the development of the

modern industrial sector over agriculture (Self

and Grabowski, 2007). However, the authors

highlight the importance and potentially high

economic impacts of agricultural technology

in re-establishing agriculture as having a vital

role in economic development. They also state

that more recent economic models have found

significant contributions to economic growth

from agriculture and agricultural technologies.

Regardless of the literature, experience

has shown that over the past few decades,

rural and small town poverty—resulting

from slowdowns in agriculture and

manufacturing—has taken its toll on many

communities. Michigan was not immune

to this slowdown. The economic declines

in rural communities have been a result of

high interest rates, farmland speculation

and over-production (Blakely and Bradshaw,

2002). As industries and farms collapsed, so

too did employment levels, which had a harsh

ripple-effect throughout rural communities

(Blakely and Bradshaw, 2002). Furthermore,

the fluctuation of global commodity prices,

and the decisions of manufacturing firms and

other raw-material-extracting businesses

to close plants or relocate, has exacerbated

the negative economic and social effects on

communities (Blakely and Bradshaw, 2002).

Surely, such challenges, when combined with

speculative real estate development pressure,

necessitate the need to closer examine the

potential positive interactions of agriculture

and economic development.

Recognizing the importance of this

interaction, this report summarizes the

agricultural base of the Tri-County Region

(Clinton, Eaton and Ingham counties) of

Mid-Michigan to underscore the current

agricultural assets and the changes that have

occurred in recent years. The report does not

delve into rural challenges and poverty, and

how past economic development efforts have

targeted them, but merely presents the current

trends and conditions of agriculture and

agriculture-related businesses.

Agricultural Base of the Tri-County Region

Despite projected statewide losses of farmland,

Michigan’s agricultural production is expected

to increase, due to technological advances

and farm specialization (Leholm et al., 2003).

However, the question remains: As farms

become more productive will they also become

more profitable and economically viable, and

how will agri-business opportunities play a

role? The effects of climate change may also

affect Michigan agriculture, as other regions

become too arid for diverse crop production,

or as cooler climates—such as Michigan’s—

experience changes in their production

potential. This may also provide interesting

opportunities for agricultural diversification

and alternative energy production.

The issues mentioned above are important

to consider for farms and farmers in the Tri-

County Region too. The agricultural landscape

of Mid-Michigan is varied and diverse, with few

elevation changes providing prime landscape for

row crops. The three counties of Clinton, Eaton

repo

rt

TRI-COUNTY AGRICULTURE

tri-county region agriculture assessment

and Ingham are located in this region of the

state, and their central location and proximity

to the State Capitol and Michigan State

University offer unique market opportunities

and partnerships. All three counties have

harvested cropland acreage and total sales

greater than the state’s county average of 82,640

acres and $69.3 million, respectively.

By examining the agricultural base and sales

between 1997 and 2007, it is possible to see

how agriculture has changed in the Tri-County

Region. It is important to understand the path

agriculture has been on before suggesting

modifications to that path. It is also important

to understand the agri-business opportunities

that may be present. A breakdown of the acres

of farmland harvested by crop for the year 2009

(based on Cropland Data Layer (CDL) data),

as well as acreage devoted to other uses for the

state of Michigan and the Tri-County Region’s

percentage of the state’s total is presented in

Table 3. This snapshot in time reveals that in

2009, nearly three times as much land was

devoted to agricultural production, and nearly

two-and-a-half times as much devoted to

natural land types than to urban/developed

land. This exemplifies the highly rural/

agricultural nature of the region and the need

for targeted economic development planning

for agriculture and agri-businesses.

As of the 2007 Census of Agriculture, the Tri-

County Region accounted for 7.6% of the state’s

harvested cropland, and 6.1% of the state’s

farms, and contributed 5.6% of the state’s total

sales (see Tables 4 and 5). However, the region’s

share of the state’s total farms decreased from

6.6% in 1997 to 6.1% in 2007, its share of land

(acres) in farms increased from 6.7% in 1997 to

6.8% in 2007, its acreage of harvested cropland

increased to 7.6% from 7.4%, and its share of

the state’s total sales remained steady at 5.6%

from 1997 to 2007. It would appear that the

tri-county’s portion of the state’s farms, acreage

and total sales of agricultural products has

remained virtually unchanged from 1997 to

2007. During the same period, the region lost

98 farms and retained land in farms at a rate

similar to the state—the state lost 3.9% and the

region 3.1%. Michigan’s total harvested cropland

decreased by 1.9% from 1997 to 2007, while

the same measure for the Tri-County Region

increased by 1.7%. Thus, while the statewide