9/6/2015 1 litigating claims under the unfair trade practice’s act and common law claims saving...

TRANSCRIPT

04/19/231

Litigating Claims Under the Unfair Litigating Claims Under the Unfair Trade Practice’s Act and Common Trade Practice’s Act and Common Law Claims Law Claims

Saving People’s Homes

Andrea Bopp Stark of Molleur Law Office

04/19/232

Introduction Introduction

Predatory Lending: the practice of a lender deceptively convincing borrowers to agree to unfair and abusive loan terms, or systematically violating those terms in ways that make it difficult for the borrower to defend against.

Subprime Lending: lending at a higher rate than the prime rate. “Subprime loans” refers to loans that do not meet Fannie Mae or Freddie Mac guidelines. It may or may not reflect credit status of the borrower as being less than ideal and may not even reflect the interest rate on the loan itself.

Car loans, payday loans, credit cards, mortgage loans

04/19/233

Warning Signs of a Predatory Loan Warning Signs of a Predatory Loan

Steering to subprime high rate lenders Door-to-door solicitation of home improvement or financing arranged by

contractor Large fees or kickbacks promised to the mortgage broker Making loans to non-English speaking homeowners Paying off low-rate mortgages Shifting unsecured debt into mortgages Loans in excess of 100% loan-to-value (LTV) Foreclosure Rescue Scams Inflated income reported on loan application Adjustable rate mortgage that adjusts to over 12% Balloon notes 80/20 loans Home Equity Line of Credit (HELOC) loan Inflated Appraisal Terms at closing different from what borrower promised

04/19/234

Maine Law Claims and Defenses to Maine Law Claims and Defenses to Predatory Mortgage Loans Predatory Mortgage Loans Maine Unfair Trade Practices Act: 5 M.R.S.A. §§ 206-

216

– Prohibits unfair methods of competition and unfair or deceptive acts or practices in the conduct of any trade or commerce

– Consumer remedy against Unfair and Deceptive trade practices by a business

– Consumer has private right of action

– Attorney General Can also bring action to enforce UTPA

WHENWHEN

Statue of Limitations: – Private (not state) action must be commenced

within 6 years of the UTPA violation

– Can argue that period begins when reasonable person would have been put on notice concerning the unfair or deceptive act

What Consumers Must Prove and Doo Consumer must show:

o Loss of money or propertyo Transaction involved primarily personal, family, or

household purposeo Business benefited from violation when seeking

restitution Must send demand letter for relief 30 days prior

to filing an action for damages. (See Kilroy v. Northeast Sunspaces Inc., et al., 2007 ME 119, 930 A.2d 1060.)

04/19/236

What Consumers can Receive – Damages or– Equitable Relief (Rescission, Void Contract) – Injunction– Restitution

Must show loss of money or property and benefit on violator

– Attorneys fees (!) (But see Kilroy, 2007 ME 119, ¶15, 930 A.2d at 1064.(denial of fees possible remedy for failure to send demand notice.))

04/19/237

What constitutes an unfair trade practice– Act or practice is a violation of established

policy– Act or practice substantially injured the

consumer– Act or practice is immoral, unethical,

oppressive, or unscrupulous

(FTC v. Sperry & Hutchinson Co., 405 U.S. 233 (1972))

State of Maine v. Weinschenk, 868 A.2d 200 (2005):

“[t]o justify a finding of unfairness, the act or practice:

(1)must cause, or be likely to cause, substantial injury to consumers;

(2)that is not reasonably avoidable by consumers; and

(3)that is not outweighed by any countervailing benefits to consumers or competition.”

04/19/239

Commonwealth v. Fremont Investment and Loan, 897 N.E. 2d 548 (MA Dec. 2008)

Lender’s combination of four loan characteristics into single loan package was considered presumptively unfair

(1) the loans were ARM loans with an introductory rate period of three years or less; (2) they featured an introductory rate for the initial period that was at least three per cent below the fully indexed rate; (3) they were made to borrowers for whom the debt-to-income ratio would have exceeded fifty per cent had Fremont measured the borrower's debt by the monthly payments that would be due at the fully indexed rate rather than under the introductory rate; and (4) the loan-to-value ratio was one hundred per cent, or the loan featured a substantial prepayment penalty (defined by the judge as greater than the “conventional prepayment penalty” defined in G.L. c. 183C, § 2) or a prepayment penalty that extended beyond the introductory rate period.

04/19/2310

– Examples:– Not providing material information (failing to

state material fact)– Making false advertising claims– Use of high pressure sales tactics – Deprivation of various post-purchase remedies(American Financial Services v. FTC, 767 F.2d 957, 979 (1985))

– Violation must be substantial– Must not outweigh any countervailing benefits

to consumers or competition that the practice produces

– Must be an injury that consumers themselves could not have avoided

(Suminski v. Maine Appliance Warehouse Inc., 602 A.2d 1173 (Me. 1992);

State of Maine v. Weinschenk et al., 2005 ME 28, 868 A.2d 200)

What is a deceptive trade practice? – Misrepresentation, omission, or other practice

the misleads consumer to consumer’s detriment Lack of necessary qualifications of representations

– Inconspicuous representations or qualifications (ie: too small print, confusing terms not explained)

(FTC)

An act or practice is deceptive if it is a material representation, omission, act or practice that is likely to mislead consumers acting reasonably under the circumstances.State of Maine v. Weinschenk, 868 A.2d 200

(2005)

04/19/2314

Darling, v. Western Thrift & Loan, 600 F.Supp.2d 189 (Feb. 2009): a genuine issue of fact exists with regard to whether the Darlings were misinformed about the existence or nature of the YSP and that such misinformation would be material.

04/19/2315

MacCormack v. Brower, 2008 ME 86: “[t]he definitions of ‘unfair’ and ‘deceptive’ are questions of fact, and whether a particular act or practice is ‘unfair’ or ‘deceptive’ is determined on a case-by-case basis.”

04/19/2316

Potential UTPA claims for predatory lending cases:– Failure to disclose disadvantageous terms, costs, fees,

and the nature of the loan – Failure to disclose to consumer any fact relating to the

loan transaction, disclosure of which may have influenced consumer not to enter into the transaction

– Inflating income to qualify buyer– Inflating appraisal value to qualify for loan– Failure to disclosure changes in terms of loan: Bait and

switch– Failure to consider consumer’s ability to repay the loan – Intentionally and knowingly placing consumer in a loan

product that consumer could not afford – Misrepresentations and non-disclosures of material facts.

§208(1) provides: Nothing in this chapter shall apply to transactions or actions otherwise permitted under laws as administered by any regulatory board or officer acting under statutory authority of the State or of the United States.

04/19/2318

Previous Line of Cases: Maine Commodities v. Dube, 534 A.2d 1298 (1987): exclusive

listing agreements between licensed brokers and vendors of real estate are controlled by state Real Estate Commission and thus, activities fell outside scope of Unfair Trade Practices Act and Solicitation Sales Act.

Keatinge v. Biddle , 2000 WL 761015 (D.Me.) : Lawyers are not subject to the Act because they are already extensively regulated under Maine law

Wyman v. Prime Discount Sec. , 819 F.Supp. 79 (1993) :securities transactions exempt from coverage under Act because, in Maine, the sale of securities must be licensed and is permitted only under the authority of the Revised Maine Securities Act and under the rules and regulations promulgated pursuant to the Securities Exchange Act of 1934.

04/19/2319

But see:

Good v. Altria Group, Inc. 502 F.3d 29 (1st Cir.2007) : regarding cigarette manufacturer's liability under UTPA: “conduct is exempt from the [Maine] Unfair Trade Practices Act where it is subject to specific standards left to the enforcement of an administrative agency, not merely those circumstances in which the agency's regulatory scheme is generally extensive' or detailed.”

04/19/2320

Provencher v. T&M Mortgage Solutions 2008 WL 2447472 (DCt. Me. June 18, 2008) : discussed Good v. Altria Group, Inc. and indicated that Good required the District Court to construe First of Maine Commodities differently than it had in Keatinge v. Biddle and Wyman v. Prime Discount Sec. (“Good has interpreted the Maine [UTPA] statute [contrary to the way the District Court did in Keatinge and Wyman so it is no longer appropriate to apply section 208(1) of the UTPA to entire industries or professions]”)

Where consumer did not seek to hold the defendants liable under the Unfair Trade Practices Act for complying with a specific regulatory standard, the defendants would not be exempt from the Act

04/19/2321

WHEREWHERE

– Consumers can bring action in:

Small Claims Court ($4500 or less)

District Court

Superior Court

Combined with Federal Claims, in Federal District Court or Bankruptcy Court

Effective Jan. 1, 2008: Maine Public Law, Chapter 273, “An Act to Protect Maine Homeowners from Predatory Lending.”

Public Law, Chapter 471, “An Act Relating to Mortgage Lending and Credit Availability.” Applies retroactively to January 1, 2008 and clarifies questions regarding the intent of PL 2007, Chapter 273

Maine's homestead exemption, effective July 18, 2008. For a single homeowner: $47,500 (up from $35,000) and for joint owners: $95,000. Individuals over the age of 60, or who are disabled, or who have disabled or elderly dependents can also claim an exemption of $95,000 per person for a maximum exemption of $190,000 per couple.

04/19/2323

COMMON LAW CLAIMSCOMMON LAW CLAIMS

Unconscionability – Court is empowered to void contracts that are

procedurally and substantively unconscionable, i.e., that could lead to unfair surprise and that are oppressive to the disadvantaged parties.(See Barrett v. McDonald Investment Inc., et al. 2005 ME 43, ¶¶ 32-36, 870 A.2d 146 (J. Alexander concurring))

See also Maine Consumer Credit Code Title 9-A §9-402

– Facts/Claims: Disparity in bargaining power: borrowers unsophisticated

with regard to financial matters, creditor sophisticated and experienced entities, which sought to profit directly from the evident disparity in bargaining power.

Borrower had no reasonable opportunity to understand terms of contract: limited English, education, etc.

Terms of the loans so oppressive and unreasonably favorable to creditor.

Terms of loan changed at last minute. Creditor induced borrower into loan knew, or reasonably

should have known, that the borrowers were incapable of repaying, with total disregard of their ability to pay and without regard for the consequences to them of entering into the loan.

Absence of meaningful choice for borrower.

Fraudulent Inducement to Contract– Defendant provided a false statement of material fact

– That defendant knew or should have known was false or acted in reckless disregard of whether it was true or false

– That induced the plaintiff to enter into the contract

– That proximately caused injury to the plaintiff when acting in reliance of that statement

(Letellier v.Small, 400 A.2d 371, 376 (Me. 1979); Veilleux v. National

Broadcasting Co., et al. 206 F.3d 92 (1st Cir. 2000))

See also MCCC §9-401

Tort LiabilityTort Liability

Negligence– A duty of care owed by the defendant to

plaintiff– Breach of that duty of care by defendant– Injury to the plaintiff and– Defendant’s breach caused the plaintiff’s

injury

First hurdle: duty of care owed by lender/ servicer to homeowner – ie: failure of servicer to respond to QWR

– Duty to maintain proper and accurate loan records

Second hurdle: conduct was proximate cause of injury

Negligent Misrepresentation– Defendant makes false statement of material

fact– Defendant fails to exercise reasonable care in

obtaining or communicating the false information and

– Plaintiff is injured by misrepresentation (Binette v. Dyer Library Assoc., 688 A.2d 898, 903 (Me. 1996))

See also MCCC §9-401

Intentional Infliction of Emotional Distress– The defendant’s conduct was extreme and

outrageous (goes beyond all possible bounds of decency)

– The conduct was intentional and reckless and– The conduct actually caused severe emotional

distress(Curtis v. Porter, 2001 ME 158, ¶10, 784 A.2d 18)

Intentional Interference with Contractual Relations– Contractual relationship– Defendant’s knowledge of the contract– Intent to interfere– Existence of damages suffered by the plaintiff– Eg: Lenders failure to provide accurate payoff

figure for refinancing out of predatory loan (Rutland v. Mullen, 2002 ME 98, ¶13, 798 A.2d 1104)

Civil Conspiracy to Commit a Civil Conspiracy to Commit a Tort Tort Not recognized as independent tort An agreement between two or more parties to deprive a

third party of legal rights or deceive a third party to obtain an illegal objective

Must share a general conspiratorial objective– Eg: All defendants (real estate agent, mortgage

broker, lender) acted in concert to inflict a wrong against and injure plaintiff by providing a mortgage that was unconscionable and that they knew the plaintiff could never repay, to obtain a substantial, excessive profit which caused the plaintiffs to suffer substantial damages. (See Cohen v. Bowdoin, 288 A.2d 106 (Me. 1972)

04/19/2333

Other ClaimsOther Claims Equal Credit Opportunity Act: 15 USC 1691-

1691f (ECOA) Fair Housing Act 42 USC 3601 to 3631 Racketeering and Corrupt Organizations Act

(RICO) Breach of Fiduciary Duty Licensing Violations Contract Claims Civil Liability

But See MCCC §§5-201(5) and 9-405(5): Except as otherwise provided, no violation of this Act impairs rights on a debt.

Maine TILA Maine TILA Maine is one of 5 states where creditors have to

comply only with the state TILA statute: 9-A M.R.S.A. §1-102 et .seq.

Granted exemption by the Federal Reserve Board in1982 because state law is substantially similar to the requirements imposed by TILA

But: Exemptions do not extend to civil liability provisions of TILA. Regulation Z §226.29(b)(1) Belini v. Washington Mutual Bank, FA, 412 F.3d 17, 19,20 (1st Cir. 2005)

Also- preemption if state law is inconsistent with the federal law

04/19/2334

04/19/2335

Remedies under TILARemedies under TILA

15 USC 1640(a)Statutory Damages $200-$2000Actual DamagesCostsAttorney FeesRescission for lack of material disclosures

04/19/2336

Home Ownership and Equity Home Ownership and Equity Protection Act of 1994 (HOEPA)Protection Act of 1994 (HOEPA)TILA Amendment That Limits Cost-

related Terms In Covered High-cost Home Equity Loans

– 15 USC § 1602(aa); 1639 (Federal)– 9-A M.R.S.A. § 8-103 (F-1); 206-A

(Maine-refers to Fed. statute)– Refinance loans only

04/19/2337

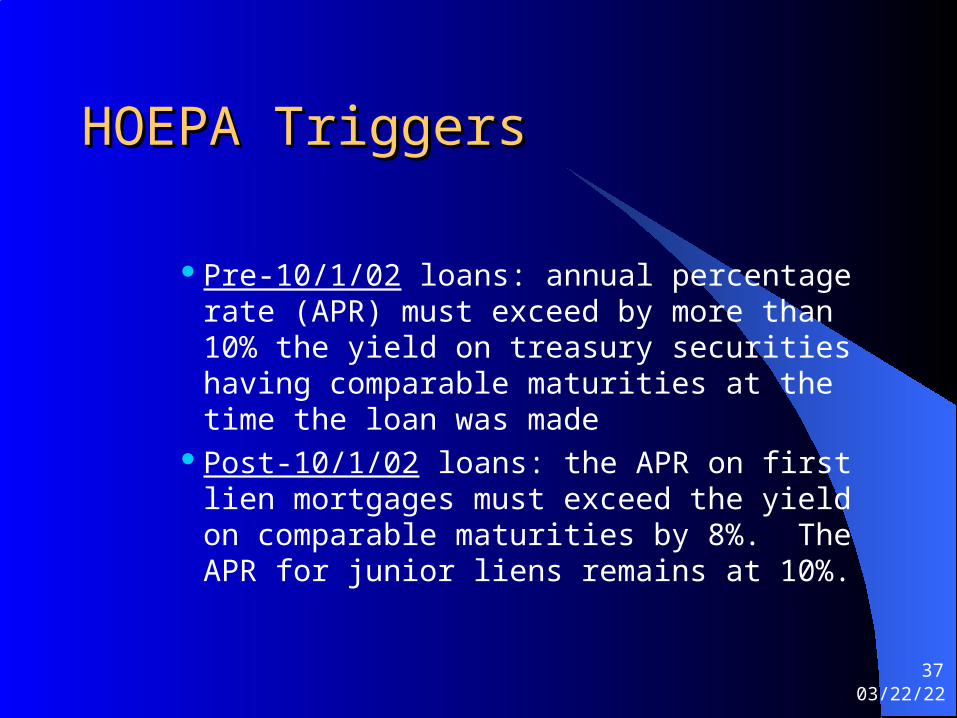

HOEPA TriggersHOEPA Triggers

Pre-10/1/02 loans: annual percentage rate (APR) must exceed by more than 10% the yield on treasury securities having comparable maturities at the time the loan was made

Post-10/1/02 loans: the APR on first lien mortgages must exceed the yield on comparable maturities by 8%. The APR for junior liens remains at 10%.

04/19/2338

HOEPA Triggers con’tHOEPA Triggers con’t

The total amount of points and fees charged exceeds both 8% of the total loan amount and $400

04/19/2339

RemediesRemedies

– Statutory damages under TILA– Material violations – enhanced damages of the

sum of all finance charges and fees paid by the consumer

– Rescission– Attorney Fees

04/19/2340

Real Estate Settlement Real Estate Settlement Procedures Act (RESPA)Procedures Act (RESPA)

– 12 USC §§ 2601 – 2617– Protect from unnecessarily high settlement

charges and abusive practices

04/19/2341

Remedies under RESPARemedies under RESPA

– Statutory remedies for servicer obligations, kickbacks, and title company violations

– Look to UDAP/ Maine UTPA: 5 M.R.S.A. §§ 206-216

– SOLs 1 year; servicer obligations 3 years

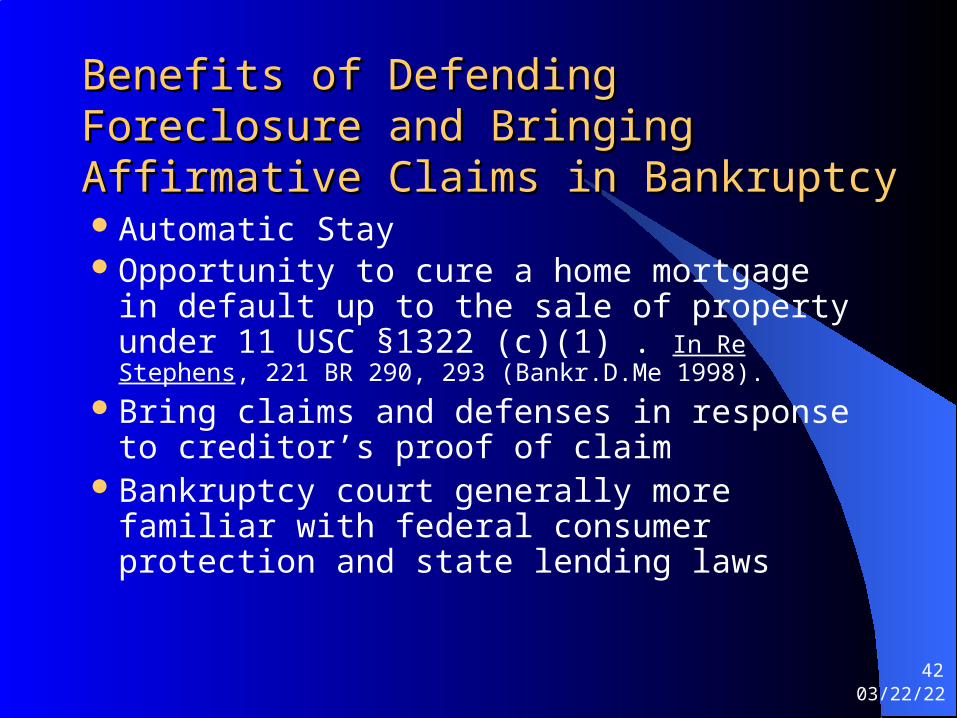

Benefits of Defending Foreclosure and Benefits of Defending Foreclosure and Bringing Affirmative Claims in Bankruptcy Bringing Affirmative Claims in Bankruptcy

Automatic StayOpportunity to cure a home mortgage in

default up to the sale of property under 11 USC §1322 (c)(1) . In Re Stephens, 221 BR 290, 293 (Bankr.D.Me 1998).

Bring claims and defenses in response to creditor’s proof of claim

Bankruptcy court generally more familiar with federal consumer protection and state lending laws

04/19/2342

Tender with Rescission in Bankruptcy CourtTender with Rescission in Bankruptcy Court

– Before, where TILA rescission enforced in bankruptcy proceeding, consumer’s tender obligation may be treated as unsecured claim

– In a bankruptcy setting, rescission by an obligor is not conditioned by tender or payment. See Jaaskelainen v. Wells Fargo Bank, N.A., 2008 WL 2705522 (Bankr. D. Mass 2008)

04/19/2343

But: Overruled in United States District Court, District Of Massachusetts, Civil Action No. 08-11299-rwz, Memorandum And Order (May 28, 2009) (Zobel, D.J.): the bankruptcy court was in error when it concluded that Appellants’

security interest became void upon Debtor’s notice of rescission and that requiring

tender was inappropriate in the bankruptcy context

04/19/2344