9 november 2015 sustainable oceans summit marina...

TRANSCRIPT

Outlook for the Global Offshore Oil and Gas Sector

9 November 2015

Sustainable Oceans Summit

Marina Mandarin, Singapore

Prepared by Douglas- Westwood Singapore

Jason Waldie, Director

www.dw-1.com

LNG

offshore

onshore

downstream

power

LNG

renewables

• Established 1990

• 50 professional staff

• Aberdeen, London, Houston,

Singapore

Activity & Service Lines

• Business strategy & advisory

• Commercial due-diligence

• Market research & analysis

• Published market studies

Large, Diversified Client Base

>1,020 projects, >450 clients

>72 countries, >230 sectors

• Clients include the top-10:

• Oil & Gas Companies

• Oilfield Services

• Investment Banks

• Private Equity firms

• Government Agencies

Our business: research and consulting

11/03/2015

Global Energy Demand Outlook Growing Importance of Gas

Global Energy Demand by Sector

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1990 2035

Power Transport Industry

-

1,000

2,000

3,000

4,000

5,000

6,000

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035

Global Energy Demand by Fuel

Gas 2020-2035

Oil 2020-2035

• The combination of increased energy efficiency throughout OECD states and growing

economies in Asia is driving demand for power generation at the expense of transportation.

• Natural gas is becoming an increasingly popular fuel for power generation offering a relatively

safe (compared to nuclear); cheap (compared to oil); and clean (compared to coal) energy

source.

• Demand for natural gas to increase by 55% over the next 20 years...

42%51%

mtoe

Primary Energy Demand – Bullish Outlook

• +30% growth by 2035. From 86% to 81% use of fossil fuels. Liquids at 110 Mboe/d.

• Driven by Asian economies, power generation and industry.

• China + India = 60% of GDP growth, 50% of primary energy growth

• Natgas +40%, Oil +20%, Coal +20%, Nuclear +40%, Hydro +40%, Ren +240%

OECD / Non-OECD (Btoe)

0

2

4

6

8

10

12

14

16

18

20

2015 2020 2025 2030 2035

Non-OECD

OECD

China

0

1

2

3

4

5

6

7

8

9

2015 2020 2025 2030 2035

Transport Power

Industry Others

0

2

4

6

8

10

12

14

16

18

20

2015 2020 2025 2030 2035

Renewables HydroNuclear CoalNatural Gas Liquids

Demand by fuel (Btoe) Demand by sector (Btoe)

Source: BP Energy Outlook 2035, Feb 2015 issue

A more gaseous world

Natural Gas production (Btoe) New energy supply (Btoe)

• Unconventionals (shale gas, tight oil) and renewables account for 50% of energy growth.

• Global gas production boosted by US shale revolution, unlikely to be exported.

• 2035, USA: 60% tight oil and 30% shale gas exploited.

• 2035, elsewhere: 5% tight oil and 5% shale gas exploited.

• More diverse gas supply. LNG supply is set to overtake gas pipes in 2035

0

1

2

3

4

5

2015 2020 2025 2030 2035

Asia Pacific Africa

Middle East Europe & FSU

Latin America North America

Source: BP Energy Outlook 2035, Feb 2015 issue

• The whole American continent is expected to reach energy independence in 2020.

North America emerge as an established net energy exporter, +560 Mtoe in 2035.

• By 2035, the only net energy importers will be Europe and Asia.

While Europe remains flat (~900 Mtoe), Asia would have almost double its imbalance in 20 years (-

2,200 Mtoe in 2035).

• Asian economies are highly dependent on oil and gas imports.

China’s oil imbalance is currently estimated at -60%.

-100%

-90%

-80%

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

Gas Balance Oil Balance

Asia China India Japan S. Korea40% 22% 5% 4% 2%

% of global energy demand

Shifting Energy Trades

Net Primary Energy Balances (Btoe) Asian Oil and Gas Import Dependency

-4

-3

-2

-1

0

1

2

3

4

2015 2020 2025 2030 2035

Asia Pacific EuropeAfrica Latin AmericaNorth America FSUMiddle East

Source: BP Energy Outlook 2035, Feb 2015 issue

Douglas-Westwood Limited

Exploration Drilling and Production Wildcards

Supply Side Demand Side

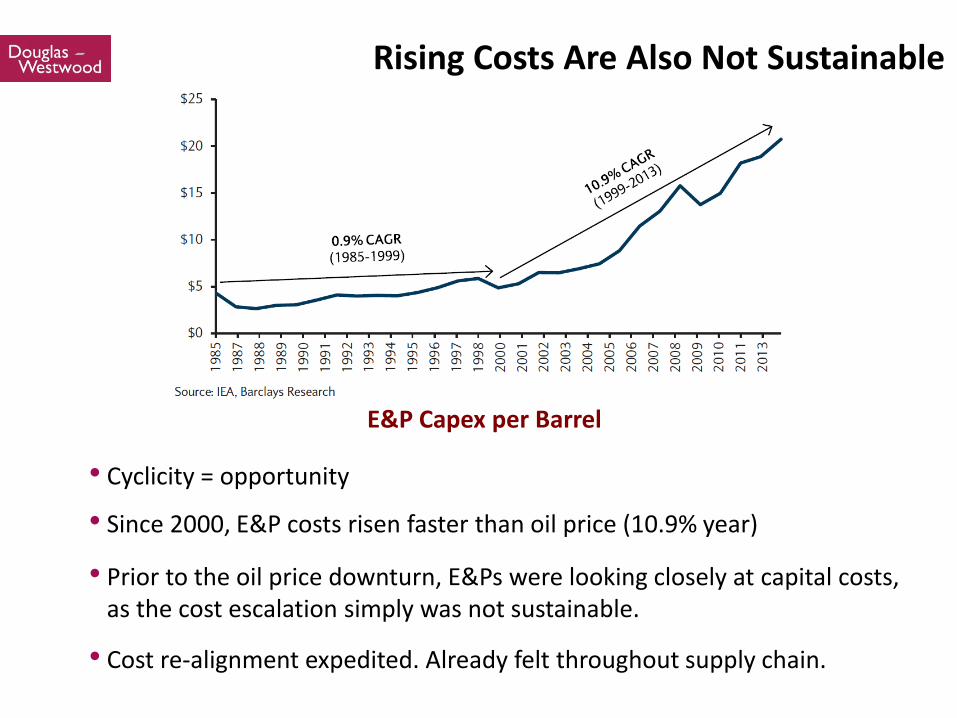

Rising Costs Are Also Not Sustainable

E&P Capex per Barrel

• Cyclicity = opportunity

• Since 2000, E&P costs risen faster than oil price (10.9% year)

• Prior to the oil price downturn, E&Ps were looking closely at capital costs, as the cost escalation simply was not sustainable.

• Cost re-alignment expedited. Already felt throughout supply chain.

Oil Majors in Trouble a Year Ago at $100/bbl!

Cash Return On Cash Invested (CROCI) of The Global Supermajors vs. Real Oil Price

CEO Shamsul Azhar Abbas"We have suffered from lower oil prices.

But if you look at the costs, they have increased further. If there is a need to

defer some of projects, we will do that."

Source: Goldman Sachs

Oil Majors – End of Business as Usual?

Majors’ Oil Production

Source: Douglas-Westwood & Company Reports

Production (000

b/d) 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Royal Dutch Shell 2,359 2,379 2,253 2,093 2,030 1,899 1,771 1,680 1,709 1,666 1,633 1,541

Statoil 1,112 1,132 1,135 1,102 1,058 1,070 1,055 1,067 967 945 966 964

Total 1,589 1,661 1,695 1,621 1,506 1,509 1,456 1,381 1,340 1,226 1,220 1,167

Eni 921 981 1,034 1,111 1,079 1,020 1,026 1,007 997 845 882 833

BP 2,018 2,121 2,531 2,562 2,475 2,414 2,401 2,535 2,374 2,157 2,056 2,013

ConocoPhillips 701 953 924 926 1,489 1,433 1,371 1,429 1,268 866 871 867

Exxon Mobil 2,496 2,516 2,571 2,523 2,681 2,616 2,405 2,387 2,422 2,312 2,185 2,202

Chevron 1,897 1,823 1,737 1,701 1,759 1,783 1,676 1,872 1,923 1,849 1,764 1,731

Petrobras 1,533 1,701 1,661 1,847 1,920 1,918 1,975 2,112 2,150 2,167 2,119 2,040

Petrochina 2,109 2,119 2,265 2,270 2,276 2,299 2,380 2,311 2,350 2,428 2,504 2,556

Control of Oil Reserves

Source: ENI Review 2014 Oil Discoveries & Production

Source: BP Energy Outlook 2035

NOCs79%

IOCs3%

Others18%

0

10

20

30

40

50

60

70

80

90

100

0

50

100

150

200

250

300

350

400

450

500

19

00

19

10

19

20

19

30

19

40

19

50

19

60

19

70

19

80

19

90

20

00

20

10

20

20

20

30

Oil

Pro

duction (

mboed/d

)

Dis

coveries (

bn b

/d)

Discovery

• IOCs face major challenges

• NOCs control 80% of reserves

• IOCs forced to focus on high cost projects

• Too big for unconventionals?

• The days of ‘easy oil’ are over.

-35%

-15%

-30%-18%-5%-10%-12%-5%+20%+21%

0

50

100

150

200

250

Mid

dle

East

Oth

er

Co

nven

tio

na

l O

il

Bra

zil

Pre

-Salt

De

ep

wate

r

Ve

ne

zu

ela

Ori

noco

Be

lt

Ca

na

dia

n O

il S

an

ds

Oil

Sh

ale

Coa

l to

Liq

uid

Arc

tic O

il

Conventional Unconventional

Viability of oil developments ($/bbl)

Unviable

Viable

Sources: Douglas-Westwood

WTI $60

“To grow oil production, the North American E&P industry needs $85-90 WTI” Simmons & Co,

WTI $110

Source: Douglas-Westwood D&P, Jan 2015

• Low oil price, spiralling E&P costs, softening demand activity slowdown

• Natural production decline rates (with well maintenance) average around 5% p.a.

• Unconventional wells decline much faster: 40-50% p.a. (Haynesville, Bakken)

• Important in the context of declining US activity with low oil prices – recent additions

to production capacity will be eroded very quickly as activity slows – quick correction

Production Decline Will Erode Excess Capacity

Production Outlook – Existing Wells and Required Additions

0

20

40

60

80

100

120

140

160

180

2014 2015 2016 2017 2018 2019 2020

Pro

du

ctio

n (

mb

oe

/d)

Legacy Production Required Additions

0

20

40

60

80

100

120

140

160

180

2014 2015 2016 2017 2018 2019 2020

Pro

duction (

mboe/d

)

Legacy Production Required Additions

Where is the industry heading?

• Many offshore projects are long term and rarely cancelled post-FID.

• Momentum following several years of high oil prices 2011-mid 2014 will carry the industry through a flat period of spend to 2017.

• Recovery 2018 onwards.

-

100

200

300

400

500

600

2008 2010 2012 2014 2016 2018 2020

$b

illio

ns Stagnation

Sustained Investment

Offshore Capex – Actual and Forecast

Source: Douglas-Westwood, Jan 2015

Africa13%

Asia25%

Australasia5%

Eastern Europe & FSU

2%

Latin America

16%

Middle East7%

North America

17%

Western Europe

15%

2015-20 Spend by Region

• Evercore view - revised downward:

• “Sharp recession in the oilfield”

• “Middle East the only Bright Spot”

• “Disappearance of new offshore rig orders”

• “Rapid fall in US activity and bottoming of rig count in Q3 or Q4”

• “Recovery in 2016”

+7.9%

-15%

$200

$250

$300

$350

$400

$450

$500

$550

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

International: -15%

4863

89 96119

8298

128 140 146174

-30%

25

30

36 33

38

25

38

4944 43

51

$0

$25

$50

$75

$100

$125

$150

$175

$200

$225

'04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14E '15E

North America: -30%

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Rest of the World

Canada

United States

Actual Estimates

Recovery: Circa 7% p.a. 2016 & 2017

Exploration & Production Spending – Actual and Forecast

Where is the industry heading?

Source: Evercore, Jan 2015

15

16

Offshore & Deepwater Supply Growth

Shallow:

• Shallow water production is set to grow 13% over the forecast period due to success in the gas drilling side of the market. This is despite a mature oil market that requires significant investment to stop production rapidly declining, particularly in the North Sea and US Gulf of Mexico

Deepwater:

• Four countries dominate the deepwater drilling sector – Angola, Brazil, Nigeria and the USA.

• Despite the downturn in oil price, projects already sanctioned will see deepwater output increase in all of these countries over the forecast period.

Shallow water production (Mboe/d)

Source: DW World Drilling & Production Forecast 2015-2021

Deepwater production (Mboe/d)

North Sea Decommissioning Market Outlook- Projects