9 months 2004 results announcement

DESCRIPTION

9 Months 2004 Results Announcement. 26 October, 2004. Scope of Briefing. Address by Executive Chairman Group Financial Highlights Business Review & Outlook. Group Financial Highlights. 9M 2004 Performance. PATMI of S$352m, up 21% from 9M 2003 EPS of 45.4 cents, up 21% from 9M 2003 - PowerPoint PPT PresentationTRANSCRIPT

1

9 Months 2004 Results Announcement26 October, 2004

2

Scope of Briefing

Address by Executive Chairman

Group Financial Highlights

Business Review & Outlook

Group Financial Highlights

4

9M 2004 Performance

PATMI of S$352m, up 21% from 9M 2003

EPS of 45.4 cents, up 21% from 9M 2003

Annualised ROE increased to 15.6%

EVA improved by S$148m over 9M 2003

Free cash flow of S$320m

Divestments of S$160m

0.74x gearing

5

Earnings & EPS GrowthS$m 9M 20039M 2004 % Change

Turnover 4,7312,795 (41)EBITDA 536465 (13)Operating Profit 368346 (6)Profit Before Tax 399478 20PATMI 290352 21

EPS (cents) 37.545.4 21

Solid PATMI and EPS growth

PATMI (excl. deferred tax adjustment)

290338 17

6

S$m9M 2003 %9M 2004 % % Change

Offshore & Marine 1,035 221,632 58 58

Property 611 13550 20 (10)

Infrastructure 618 13556 20 (10)

Sub Total 2,264 482,738 98 21

Investments* 2,467 5257 2 (98)

Total 4,731 1002,795 100 (41)

Turnover by Segments

* Deconsolidation of SPC reduced Investments’ turnover

7

S$m9M 2003 %9M 2004 % % Change

Offshore & Marine 112 39143 41 28

Property 69 2489 25 29

Infrastructure 45 1533 9 (27)

Sub Total 226 78265 75 17

Investments 64 2287 25 36

Total* 290 100352 100 21

PATMI by Segments

* 9M 2004 PATMI includes deferred tax adjustments of S$10m in Offshore & Marine, S$3m in Property and S$1m in Investments

8

Consistent Growth

1H 2H

PATMI (S$m) EPS (Cents)

108

129

112

56132

9482

83

108

98100

39

988189

10593

'00 '01 '02 '03 '04

237267

356

13.9

16.8

14.5

7.317.0

10.7 12.2

10.9

13.9

13.1 12.75.1

10.5 12.611.5

1213.6

'00 '01 '02 '03 '04

30.734.8

46.3

1Q:

2Q:

3Q:

4Q:4Q:

3Q:

2Q:

1Q: 1Q:

2Q:

3Q:

4Q:

1Q:

2Q:

3Q:

4Q:

395 51.1

4Q:

3Q:

2Q:

1Q:

4Q:

3Q:

2Q:

1Q:

1Q: 1Q:

2Q: 2Q:

352 45.4

3Q:3Q:

9

Positive EVA

(800)

(600)

(400)

(200)

0

200

+ S$370m

+ S$170m

+ S$148m

‘01 ‘02 ‘03 9M ‘04

(665)

(295)

(125)

23

S$m

10

ROE above 15%

15.6%14.1%13.4%

10.1%8.6%

2000 2001 2002 2003 9M 2004*

* Annualised ROE

11

Healthy Free Cash Flow9M 2004

S$mCash flow from operating activities Operating profit 346 Depreciation & amortisation 116

Working capital changes (233)

Net cash from operating activities 187

Net cash from investing activities 133

Free Cash Flow 320

Operational capex (75) Proceeds from divestments 153

Interest & tax paid (42)

Dividend income 55

Dividends paid (264)

462

Business Review & Outlook

13

3Q Business Trends

Higher price benchmark by oil majors

Sustained momentum in E & P spending

Overall improvement in rig utilisation

Strong shipping and shipbuilding market

Higher refining margins

Stronger demand for regional residential properties

Improving domestic property market

14

Offshore & Marine

15

Positive Market Fundamentals

Favourable factors supporting E&P activities

• Additional secured supply needed to meet growing global demand for oil and gas

• Sustained high oil and gas prices

• Deeper and more challenging drilling requirements needing new rigs

Outlook for FPSO conversions and offshore support vessels is strong

16

Sustainable Offshore Cycle

Ageing rig fleet with current average age of 23 years versus 4.5 years in 1980

Improving rig utilisation and charter rates

Number of rigs built still modest

0

20

40

60

80

100

120

140

1979 1984 1989 1994 1999 2004

No.

of

dri

llin

g r

igs

bu

ilt

50

55

60

65

70

75

80

85

90

95

100

Avera

ge u

tili

sati

on

rate

s

All rigs Average utilisation of Jack ups + Semis

* Source: Rigzone, ODS-Petrodata (Utilisation rates as at Aug ’04)

17

2,5202,190

670

1,4301,210

2000 2001 2002 2003 9M '04

S$m

Record contracts secured

18

Strong Job Prospects

Products/Services Estimated Value

Semi-submersibles (Newbuildings/Repairs/Upgrading)

0.8

Jackups (Newbuildings/Repairs/Upgrading)

2.2

FPSOs (Conversions/Upgrades)

0.5

Shipbuilding (AHTS/Tugs/Supply Vessels etc.)

0.6

Total 4.9

Platforms/Topsides/Turrets etc. 0.8

S$b

19

Property

20

Growth Strategy:Regional Thrust

Regional economies in industrialization phase

Rising affluence and middle income earners

Supportive government policies

0%

2%

4%

6%

8%

10%

GD

P g

row

th

2003 2004 2005

* Source: Asian Development Bank, Apr ‘04

Growing pool of potential home owners

21

The Waterfront(Chengdu)

The Seasons(Beijing)

8 Park Ave(Shanghai)

Villa Riviera(HCMC)

Indicative sales from regional launches

73%

97%92%

52%

Units Launched in 2004

337 321 230 25

% Sold YTD

22

Overseas pipeline next two years

Shanghai Beijing Chengdu Bangkok HCMC Bangalore

Units to be launched

1,4231,538

2,778

587 588

2,002

23

Domestic market turns the corner

Outlook for private residential properties expected to improve

• Caribbean at Keppel Bay: 87% of 135 units launched in Aug ‘04 sold. Total % of Caribbean sold: 44%

• Urbana: 78% of 65 units launched in Jul ’04 sold. Total % of project sold: 40%

Expected recovery in prime office properties, supported by limited new supply in next two years

• Tenant took up 30% of South Tower at One Raffles Quay, largest office leasing transaction since 1998

24

Infrastructure

25

Finalising Keppel Cogen power project

Alternatives for power barges under consideration

Continue to build up core competencies in Environmental Engineering

• Enhancing technology capabilities

• Strengthening marketing network

• Developing strategic partnerships

Pursuing S$800m new contracts

Infrastructure Outlook

26

2004 Financial Targets

Sustained growth

EPS CAGR of 8-12% through 2005

Maintain ROE of 15%

Continued EVA improvement

Maintain dividend payout ratio of 30-35%

27

Keppel Corporation 9M 2004 Results

Thank YouQ&A

28

Additional Info

29

Keppel Corporation

30

Financial Highlights – Keppel Corp

S$m 1Q 20031Q 2004 % Change

Turnover 1,744896 (49)EBITDA 175147 (16)Operating Profit 121109 (10)Profit Before Tax 132148 12PATMI 94132 40

PATMI (excl. deferred tax adjustments)

94118 26

31

Financial Highlights – Keppel Corp

S$m 2Q 20032Q 2004 % Change

Turnover 1,476922 (38)EBITDA 172163 (5)Operating Profit 120121 1Profit Before Tax 122158 30PATMI 98108 10

32

Financial Highlights – Keppel Corp

S$m 3Q 20033Q 2004 % Change

Turnover 1,511977 (35)EBITDA 189155 (18)Operating Profit 127116 (9)Profit Before Tax 145172 19PATMI 98112 14

33

Total SingaporeOverseasS$m %%

Offshore & Marine 1,632 1288

Infrastructure 556 3961

Property 550 6832

Sub total 2,738 2971

Investments 57 3961Total 2,795 2971

9M 2004

71% of total turnover came from overseas customers

Turnover by Customers

34

S$m9M 2003 %9M 2004 % % Change

Offshore & Marine 197 37217 47 10

Property 137 25160 34 17

Infrastructure 90 1772 16 (20)

Sub Total 424 79449 97 6

Investments 112 2116 3 (86)

Total 536 100465 100 (13)

EBITDA by Segments

35

PATMI By Segments

69

6486

3345

86

133112

14

0

100

200

300

400

9M 2003 9M 2004

S$m

S$290m

21% growth

Offshore & Marine

InfrastructureProperty

Investments

S$352m

Deferred Tax Adjustments

17% growth

Note: 9M 2004 PATMI includes deferred tax adjustments of S$10m in Offshore & Marine, S$3m in Property and S$1m in Investments

36

Capital/Gearing/ROE

S$m

Shareholders' Funds

Capital Employed

Net Debt

Net Gearing

ROE

* Annualised ROE

30 Sep 2004 31 Dec 2003

2,969 2,890

4,067 3,959

2,994 3,040

0.74x 0.77x

15.6%* 14.1%

37

Offshore & Marine

38

S$m9M 20039M 2004 % Change

Turnover 1,0351,632 58EBITDA 197217 10Operating Profit 144174 21Profit Before Tax 143175 22PATMI 112143 28

Financial Highlights – Offshore & Marine

PATMI (excl. deferred tax adjustments)

112133 19

39

Financial Highlights – Offshore & Marine

S$m 1Q 20031Q 2004 % Change

Turnover 393547 39EBITDA 6582 26Operating Profit 4968 39Profit Before Tax 4870 46PATMI 3672 100PATMI (excl. deferred tax adjustments)

3662 72

40

S$m 2Q 20032Q 2004 % Change

Turnover 332498 50EBITDA 6463 (2)Operating Profit 4749 4Profit Before Tax 4748 2PATMI 3834 (11)

Financial Highlights – Offshore & Marine

41

S$m 3Q 20033Q 2004 % Change

Turnover 310587 89EBITDA 6872 6Operating Profit 4857 19Profit Before Tax 4857 19PATMI 3837 (3)

Financial Highlights – Offshore & Marine

42

Offshore & Marine Review

S$324m contracts secured in 3Q 2004:

1 JU newbuild, 2 JU repairs, 1 semi repair, TPG 500 suction cans, 1 derrick barge upgrade, 2 AHTS, 1 FSO conversion, 1 cruise vessel refurbishment

Major contract completions in 3Q 2004:

1 floating dock upgrade, 1 derrick barge upgrade, 1 semi upgrade, 2 AHTS, 1 tender barge upgrade, 2 JU upgrades, 2 shuttle tanker conversions, 2 tugs

43

Offshore & Marine OrderbookClients

For delivery in 20044 Jack Up Upgrades / Repairs / 1 Processing Platform

31 Ensco / GSF / JDC / Sedco / Petrovietnam

TOTAL as at 30 Sep 2004 S$3.6b

2 Semi Conversions / Upgrades / 2 FPSOConversions

23 JCE Group / Diamond / Halliburton / Perenco

For delivery in 20052 Jack Ups / 2 Jack Up Upgrades / Repairs / 1 Semi Modification

1 Cruise Vessel Lengthening / 1 Cruise Vessel Refurbishment / 1 Derrick Barge Upgrade / Suction Cans / 2 PSVs / 10 AHTS / 2 Tugs

240 BP / NDC / Ensco / Atwood / Boeing

Kvaener / easyCruise / Saipem / Technip/ Maersk / Gulfmark Offshore / Pacific Richfield / Bourbon / Smit / Hadi Hammam / PSA Marine

Contract Value

Balance Order

157

154

3 AHTS / 4 Tugs / 1 Support Vessel Refit / 1 Cement Carrier Conversion

29 Delba Maritima /CH Offshore / Hadi Hammam / Keppel Smit / PSA Marine / RFA / Windstor

122

659

For delivery in 20071 Semi (P52) 1,073 Petrobras1,073

S$4.5b

S$m

For delivery in 20064 Jack Ups / 3 AHTS 819 Skeie / Ensco / Odfjell / Bourbon / Smit / Hadi

Hammam871

For delivery in 20081 Semi (P51) 1,093 Petrobras1,093

363 272

44

Property

45

Financial Highlights - Property

NB: Property segment includes all property related businesses of KCL

S$m9M 20039M 2004 % Change

Turnover 611550 (10)EBITDA 137160 17Operating Profit 125150 20Profit Before Tax 120154 28PATMI 6989 29PATMI (excl. deferred tax

adjustments)6986 25

46

Financial Highlights – Property

S$m 1Q 20031Q 2004 % Change

Turnover 170139 (18)EBITDA 4437 (16)Operating Profit 4034 (15)Profit Before Tax 3839 3PATMI 2025 25

PATMI (excl. deferred tax adjustments)

2022 10

NB: Property segment includes all property related businesses of KCL

47

Financial Highlights – Property

S$m 2Q 20032Q 2004 % Change

Turnover 206209 1EBITDA 4057 43Operating Profit 3853 39Profit Before Tax 3552 49PATMI 2329 26

NB: Property segment includes all property related businesses of KCL

48

Financial Highlights – Property

S$m 3Q 20033Q 2004 % Change

Turnover 235202 (14)EBITDA 5366 25Operating Profit 4763 34Profit Before Tax 4763 34PATMI 2635 35

NB: Property segment includes all property related businesses of KCL

49

Infrastructure

50

S$m 9M 20039M 2004 % Change

Turnover 618556 (10)EBITDA 9072 (20)Operating Profit 3420 (41)Profit Before Tax 4536 (20)PATMI 4533 (27)

Financial Highlights – Infrastructure

51

Financial Highlights – Infrastructure

S$m 1Q 20031Q 2004 % Change

Turnover 183187 2EBITDA 3327 (18)Operating Profit 1411 (21)Profit Before Tax 1515 -PATMI 1915 (21)

52

Financial Highlights – Infrastructure

S$m 2Q 20032Q 2004 % Change

Turnover 218195 (11)EBITDA 2828 -Operating Profit 109 (10)Profit Before Tax 1315 15PATMI 1313 -

53

Financial Highlights – Infrastructure

S$m 3Q 20033Q 2004 % Change

Turnover 217174 (20)EBITDA 2917 (41)Operating Profit 100 (100)Profit Before Tax 176 (65)PATMI 135 (62)

54

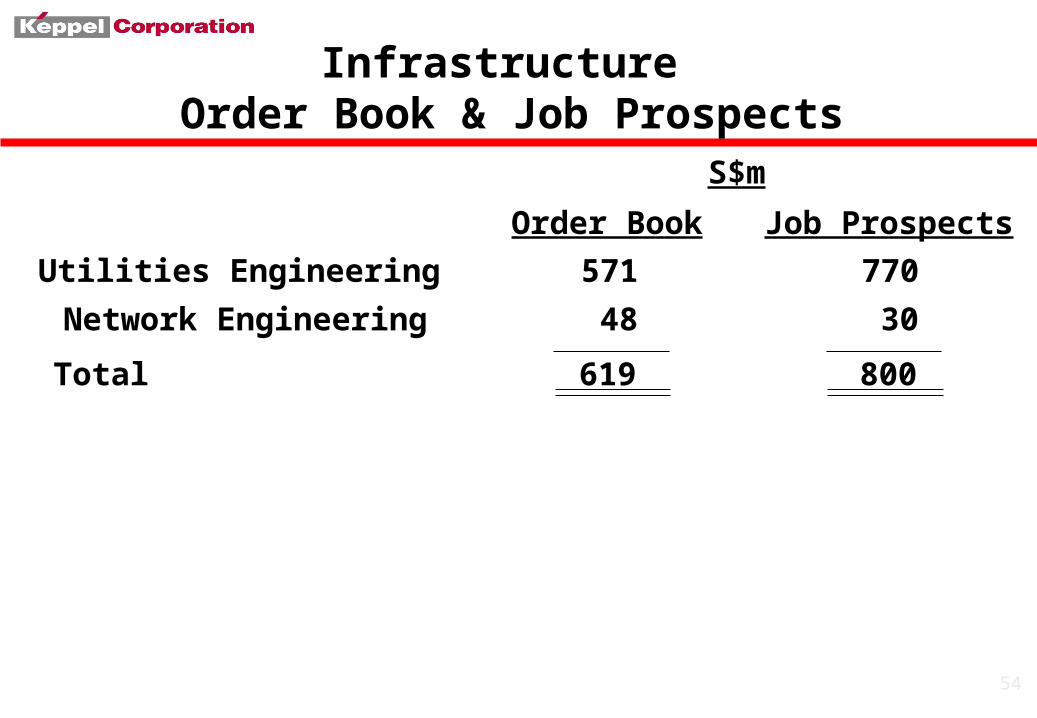

Infrastructure Order Book & Job Prospects

S$m

Utilities Engineering 571

Network Engineering 48

Total 619

770

30

800

Job ProspectsOrder Book

55

Investments

56

Financial Highlights - Investments

S$m9M 20039M 2004 % Change

Turnover 2,46757 (98)EBITDA 11216 (86)Operating Profit 652 (97)Profit Before Tax 91113 24PATMI 6487 36PATMI (excl. deferred tax

adjustments)6486 34

57

Financial Highlights – Investments

S$m 1Q 20031Q 2004 % Change

Turnover 99823 (98)EBITDA 331 (97)Operating Profit 18(4) NMProfit Before Tax 3124 (23)PATMI 1920 5

PATMI (excl. deferred tax adjustments)

1919 -

58

Financial Highlights – Investments

S$m 2Q 20032Q 2004 % Change

Turnover 72020 (97)EBITDA 4015 (63)Operating Profit 2510 (60)Profit Before Tax 2743 59PATMI 2432 33

59

Financial Highlights – Investments

S$m 3Q 20033Q 2004 % Change

Turnover 74914 (98)EBITDA 39- (100)Operating Profit 22(4) NMProfit Before Tax 3346 39PATMI 2135 67

60

This release may contain forward-looking statements which are subject to risks and uncertainties that could cause actual results to differ materially from such statements. Such risks and uncertainties include industry and economic conditions, competition, and legal,

governmental and regulatory changes. The forward-looking statements reflect the current views of Management on future

trends and developments.