4.1.1 change in real gross domestic product · 2014. source: sloos, haver analytics net percentage...

TRANSCRIPT

-4

-2

0

2

4

-4

-2

0

2

4

2006 2007 2008 2009 2010 2011 2012 2013 2014

Source: BEA, Haver Analytics

As Of: 2014 Q4 Percent 4.1.1 Change in Real Gross Domestic Product

Note: Annual changes are Q4/Q4.

Percent

-4

-2

0

2

4

-4

-2

0

2

4

2006 2007 2008 2009 2010 2011 2012 2013 2014

Source: BEA, Haver Analytics

As Of: 2014 Q4 Percent 4.1.2 Change in Real Personal Consumption Expenditures

Note: Annual changes are Q4/Q4.

Percent

0.0

0.1

0.2

0.3

0.4

0.5

0.0

0.5

1.0

1.5

2.0

2002 2004 2006 2008 2010 2012 2014

Source: Census Bureau, Haver Analytics

As Of: Mar-2015 Millions of Units 4.1.3 Private Housing Starts

Note: Seasonally adjusted at an annualized rate. Multifamily housing starts are calculated on a 3-month moving average. Gray bar signifies NBER recession.

Millions of Units

Single-family (left axis)

Multifamily (right axis)

0

2

4

6

8

10

12

0

2

4

6

8

10

12

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

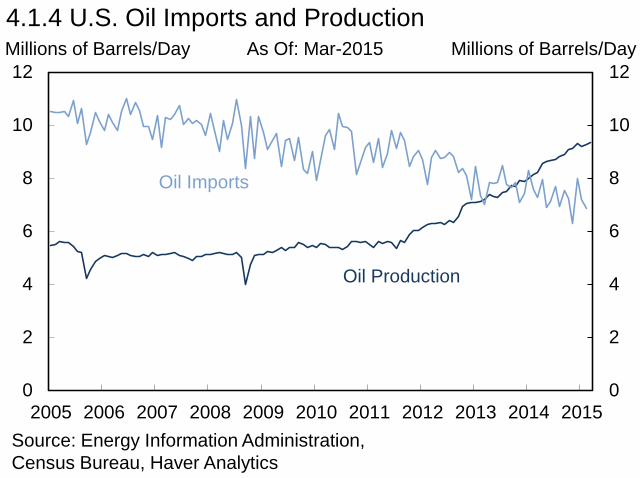

4.1.4 U.S. Oil Imports and Production Millions of Barrels/Day Millions of Barrels/Day

Source: Energy Information Administration, Census Bureau, Haver Analytics

As Of: Mar-2015

Oil Imports

Oil Production

-1000

-800

-600

-400

-200

0

200

400

600

-1000

-800

-600

-400

-200

0

200

400

600

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Source: BLS, Haver Analytics

As Of: Apr-2015 Thousands of Jobs 4.1.5 Net Change in Nonfarm Payroll Employment

Note: Gray bar signifies NBER recession.

Thousands of Jobs

Monthly Change

3-Month Moving Average

3

6

9

12

3

6

9

12

1982 1987 1992 1997 2002 2007 2012

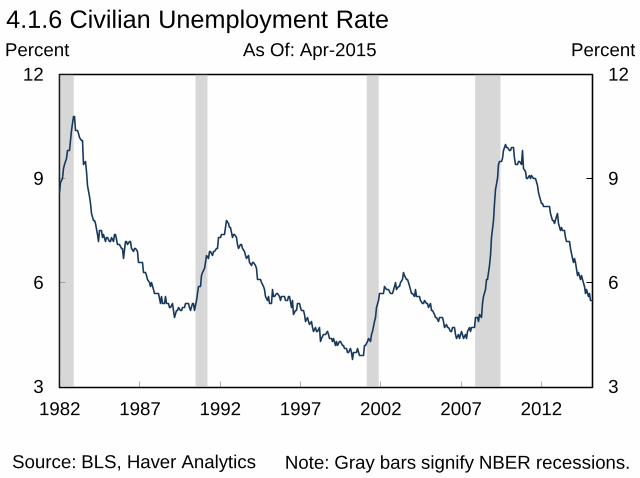

Source: BLS, Haver Analytics

As Of: Apr-2015 Percent 4.1.6 Civilian Unemployment Rate

Note: Gray bars signify NBER recessions.

Percent

62

63

64

65

66

67

68

62

63

64

65

66

67

68

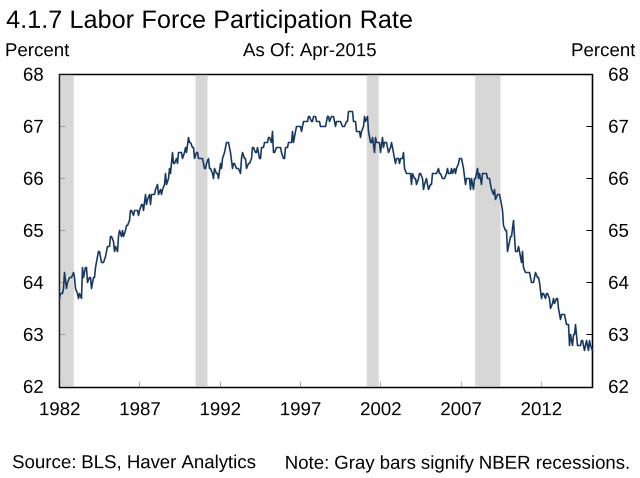

1982 1987 1992 1997 2002 2007 2012

Source: BLS, Haver Analytics

As Of: Apr-2015 Percent 4.1.7 Labor Force Participation Rate

Note: Gray bars signify NBER recessions.

Percent

0

10

20

30

40

50

0

10

20

30

40

50

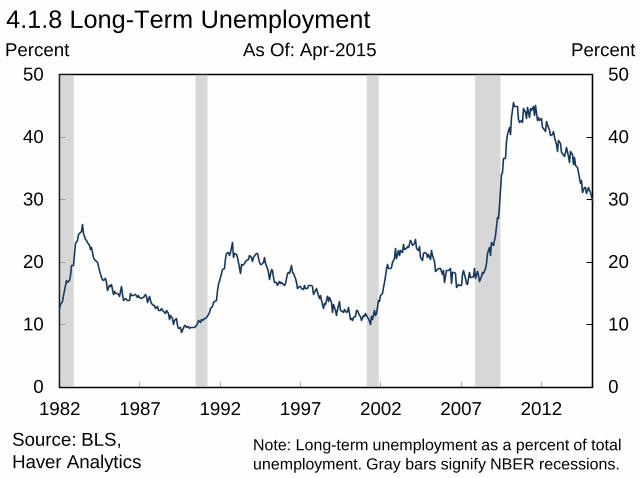

1982 1987 1992 1997 2002 2007 2012Source: BLS, Haver Analytics

As Of: Apr-2015 Percent 4.1.8 Long-Term Unemployment

Note: Long-term unemployment as a percent of total unemployment. Gray bars signify NBER recessions.

Percent

0

50

100

150

200

0

50

100

150

200

1992 1996 2000 2004 2008 2012

Source: BEA, Financial Accounts of the United States, Haver Analytics

As Of: 2014 Q4 Percent of Nominal GDP 4.2.1 Private Nonfinancial Debt

Percent of Nominal GDP

Consumer and Other Household Debt

Nonfinancial Noncorporate Debt Nonfinancial Corporate Debt

Mortgages

Note: Other Household Debt includes debts of both households and nonprofits.

16

18

20

22

24

26

28

16

18

20

22

24

26

28

1980 1985 1990 1995 2000 2005 2010Source: Financial Accounts of the United States, Haver Analytics

As Of: 2014 Q4 Percent 4.2.2 Debt to Assets for Nonfinancial Corporations

Note: Gray bars signify NBER recessions.

Percent

-100

-50

0

50

100

-100

-50

0

50

100

2000 2002 2004 2006 2008 2010 2012 2014Source: SLOOS, Haver Analytics

As Of: Feb-2015 Net Percentage 4.2.3 Bank Business Lending Standards and Demand

Note: Data includes firms with annual sales of $50 million or more over the last 3 months. Net percentage balance of responses. Gray bars signify NBER recessions.

Net Percentage

Reporting Stronger Demand from Large and

Medium-Sized Firms

Reporting Tighter Standards for Large and

Medium-Sized Firms

0

1

2

3

4

0

1

2

3

4

2000 2002 2004 2006 2008 2010 2012 2014

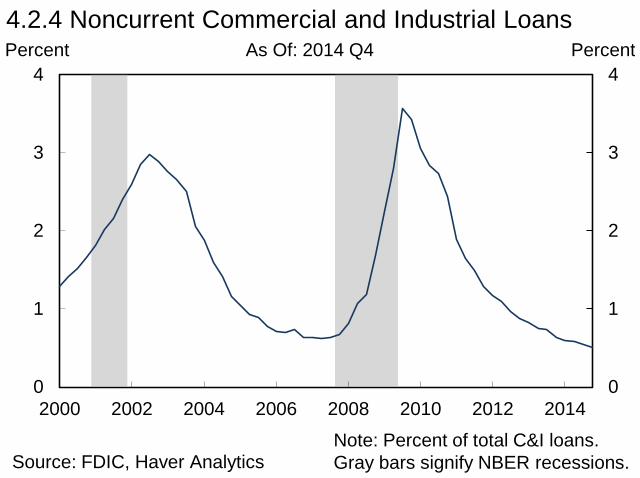

Source: FDIC, Haver Analytics

As Of: 2014 Q4 Percent 4.2.4 Noncurrent Commercial and Industrial Loans

Note: Percent of total C&I loans. Gray bars signify NBER recessions.

Percent

0

2

4

6

8

10

0

2

4

6

8

10

1981 1986 1991 1996 2001 2006 2011

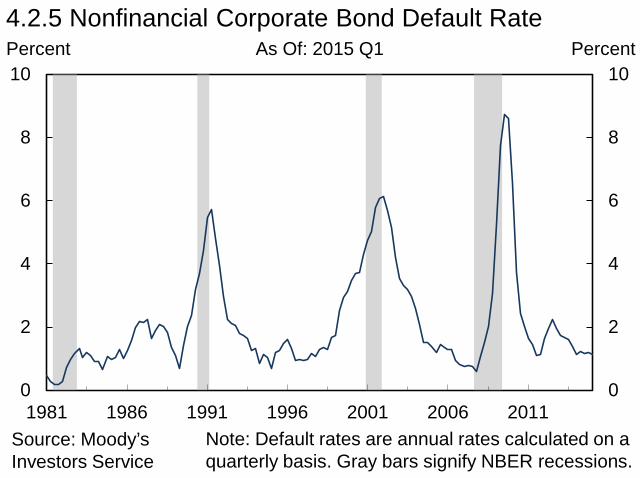

4.2.5 Nonfinancial Corporate Bond Default Rate Percent Percent

Source: Moody’s Investors Service

Note: Default rates are annual rates calculated on a quarterly basis. Gray bars signify NBER recessions.

As Of: 2015 Q1

0

20

40

60

80

100

0

20

40

60

80

100

1990 1994 1998 2002 2006 2010 2014Source: Financial Accounts of the United States, Haver Analytics

As Of: 2014 Q4 Percent of Total Assets 4.2.6 Nonfinancial Noncorporate Assets

Percent of Total Assets

Other Assets

Cash and Securities

Nonresidential Real Estate

Accounts Receivable

Residential Real Estate

-400

-200

0

200

400

600

-400

-200

0

200

400

600

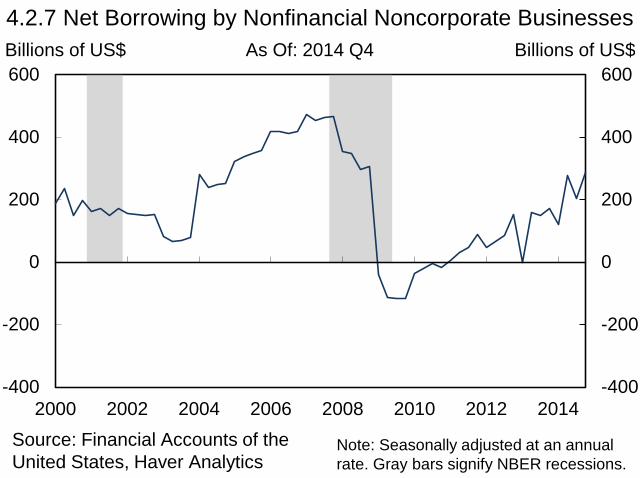

2000 2002 2004 2006 2008 2010 2012 2014Source: Financial Accounts of the United States, Haver Analytics

As Of: 2014 Q4 Billions of US$ 4.2.7 Net Borrowing by Nonfinancial Noncorporate Businesses

Note: Seasonally adjusted at an annual rate. Gray bars signify NBER recessions.

Billions of US$

-100

-50

0

50

100

-100

-50

0

50

100

2000 2002 2004 2006 2008 2010 2012 2014Source: SLOOS, Haver Analytics

As Of: Feb-2015 Net Percentage 4.2.8 Bank Business Lending Standards and Demand

Note: Data includes firms with annual sales of less than $50 million over the last 3 months. Net percentage balance of responses. Gray bars signify NBER recessions.

Net Percentage

Reporting Stronger Demand from Small

Firms

Reporting Tighter Standards for Small

Firms

0

4

8

12

16

0

4

8

12

16

2000 2002 2004 2006 2008 2010 2012 2014

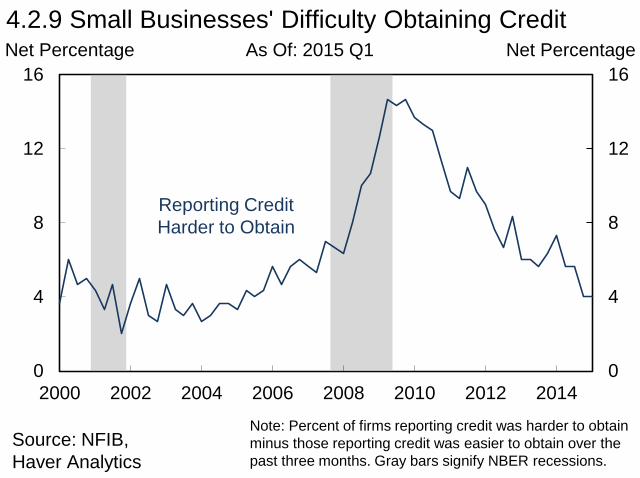

Source: NFIB, Haver Analytics

As Of: 2015 Q1 Net Percentage 4.2.9 Small Businesses' Difficulty Obtaining Credit

Note: Percent of firms reporting credit was harder to obtain minus those reporting credit was easier to obtain over the past three months. Gray bars signify NBER recessions.

Net Percentage

Reporting Credit Harder to Obtain

0

25

50

75

100

125

150

0

25

50

75

100

125

150

1992 1996 2000 2004 2008 2012

Source: BEA, Financial Accounts of the United States, Haver Analytics

As Of: 2014 Q4 Percent

4.2.10 Household Debt as a Percent of Disposable Personal Income

Note: Other Household Credit includes debts of both households and nonprofits.

Percent

Other Household Credit Consumer Credit Mortgages

9

10

11

12

13

14

15

9

10

11

12

13

14

15

1980 1985 1990 1995 2000 2005 2010

Source: Federal Reserve, Haver Analytics

As Of: 2014 Q4 Percent 4.2.11 Household Debt Service Ratio

Note: Ratio of debt service payments to disposable personal income. Seasonally adjusted. Gray bars signify NBER recessions.

Percent

0

3

6

9

12

15

0

3

6

9

12

15

2003 2005 2007 2009 2011 2013

Source: FRBNY Consumer Credit Panel/Equifax, Haver Analytics

As Of: 2014 Q4 Percent 4.2.12 Share of Household Debt by Delinquency Status

Note: Severely derogatory loans are loans for which there are reports of a repossession, charge off to bad debt, or foreclosure.

Percent

Severely Derogatory 120+ Days Late 90 Days Late 60 Days Late 30 Days Late

-40

-20

0

20

40

60

80

100

120

-40

-20

0

20

40

60

80

100

120

2000 2002 2004 2006 2008 2010 2012 2014Source: Financial Accounts of the United States, Haver Analytics

As Of: 2014 Q4 Trillions of US$ 4.2.13 Household and Nonprofit Balance Sheets

Note: Other Assets primarily include life insurance reserves, pension entitlements, and noncorporate equities. Other Debt primarily includes security credit, trade payables, and unpaid life insurance premiums.

Trillions of US$

Other Assets Equities Credit Market Instruments Cash Instruments Real Estate

Mortgages Consumer Credit Other Debt

Net Worth

30

40

50

60

70

30

40

50

60

70

1990 1994 1998 2002 2006 2010 2014

1990-2005 Average

4.2.14 Owners’ Equity as Share of Household Real Estate Percent Percent

Source: Financial Accounts of the United States, Haver Analytics

Note: Gray bars signify NBER recessions.

As Of: 2014 Q4

0

200

400

600

800

1000

1200

0

200

400

600

800

1000

1200

2003 2006 2009 2012Source: FRBNY Consumer Credit Panel/Equifax, Haver Analytics

As Of: 2014 Q4 Billions of US$ 4.2.15 Components of Consumer Credit

Note: Gray bar signifies NBER recession.

Billions of US$

Credit Card Debt

Auto Loans

Student Loans

Other Household Debt

0

3

6

9

12

15

0

3

6

9

12

15

2003 2006 2009 2012Source: FRBNY Consumer Credit Panel/Equifax, Haver Analytics

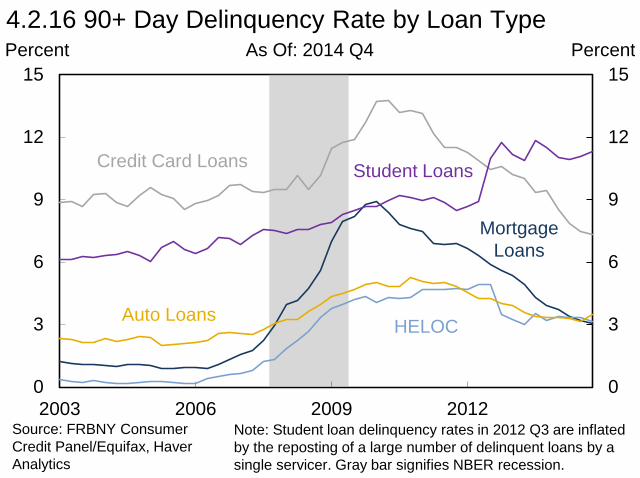

As Of: 2014 Q4 Percent 4.2.16 90+ Day Delinquency Rate by Loan Type

Note: Student loan delinquency rates in 2012 Q3 are inflated by the reposting of a large number of delinquent loans by a single servicer. Gray bar signifies NBER recession.

Percent

Mortgage Loans

HELOC Auto Loans

Credit Card Loans Student Loans

13

16

19

22

25

13

16

19

22

25

1965 1975 1985 1995 2005 2015 2025

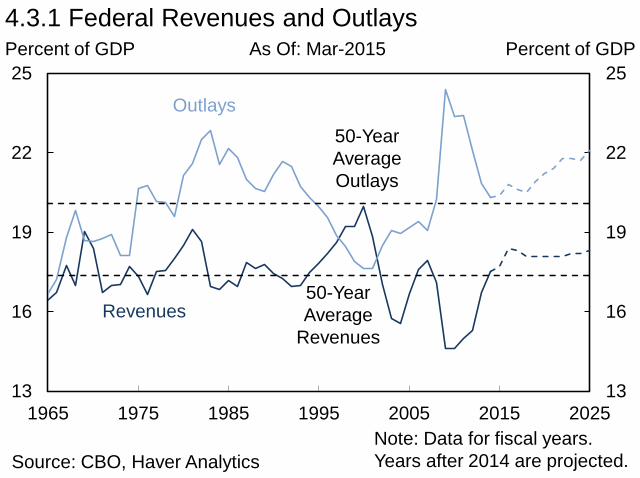

Percent of GDP As Of: Mar-2015 4.3.1 Federal Revenues and Outlays

Source: CBO, Haver Analytics

Percent of GDP

Revenues

Outlays

Note: Data for fiscal years. Years after 2014 are projected.

50-Year Average Outlays

50-Year Average

Revenues

0

2

4

6

8

10

0

2

4

6

8

10

1965 1975 1985 1995 2005 2015 2025

Percent of GDP As Of: Mar-2015 4.3.2 Outlays in Major Budget Categories

Source: CBO, Haver Analytics

Percent of GDP

Medicare and Medicaid Social Security Other Mandatory Defense Discretionary Nondefense Discretionary Net Interest

Note: Other Mandatory comprises all mandatory spending other than that for Medicare, Medicaid, and Social Security. Data for fiscal years. Years after 2014 are projected.

0

30

60

90

120

150

0

30

60

90

120

150

1948 1958 1968 1978 1988 1998 2008 2018

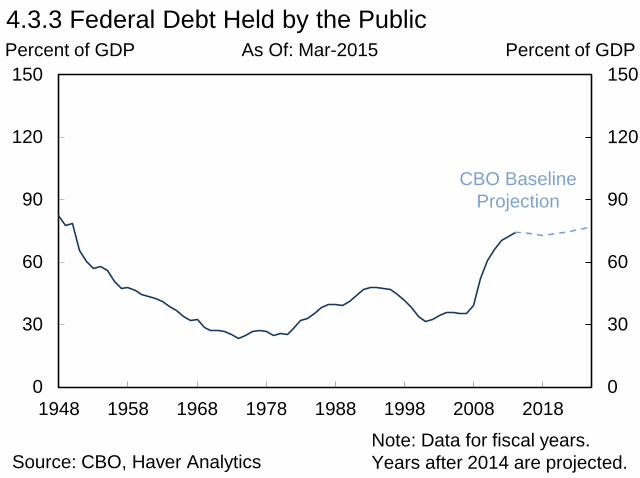

Source: CBO, Haver Analytics

As Of: Mar-2015 Percent of GDP 4.3.3 Federal Debt Held by the Public

Note: Data for fiscal years. Years after 2014 are projected.

Percent of GDP

CBO Baseline Projection

40

44

48

52

56

60

64

68

72

1.0

1.4

1.8

2.2

2.6

3.0

3.4

1981 1986 1991 1996 2001 2006 2011Source: BEA, OMB, Haver Analytics

As Of: 2014 Q4 Percent of GDP

4.3.4 Interest Outlays and Average Maturity of U.S. Public Debt

Note: Gray bars signify NBER recessions.

Months

Interest Outlays (left axis)

Average Maturity of Outstanding Debt

(right axis)

-6-4-202468101214

-6-4-202468

101214

1998 2000 2002 2004 2006 2008 2010 2012 2014

4.3.5 Change in State and Local Government Tax Revenues Percent Percent

Source: Census Bureau

Note: Data represents year-over-year change. Revenue measures includes revenues from property, individual income, corporate income, and sales taxes. Gray bars signify NBER recessions.

As Of: 2014 Q4

17.5

18.0

18.5

19.0

19.5

20.0

17.5

18.0

18.5

19.0

19.5

20.0

2000 2002 2004 2006 2008 2010 2012 2014

Source: BLS, Haver Analytics

As Of: Apr-2015 Millions of Employees 4.3.6 State and Local Government Employment

Note: Gray bars signify NBER recessions.

Millions of Employees

-20

-15

-10

-5

0

5

10

15

-20

-15

-10

-5

0

5

10

15

2007 2008 2009 2010 2011 2012 2013 2014 2015

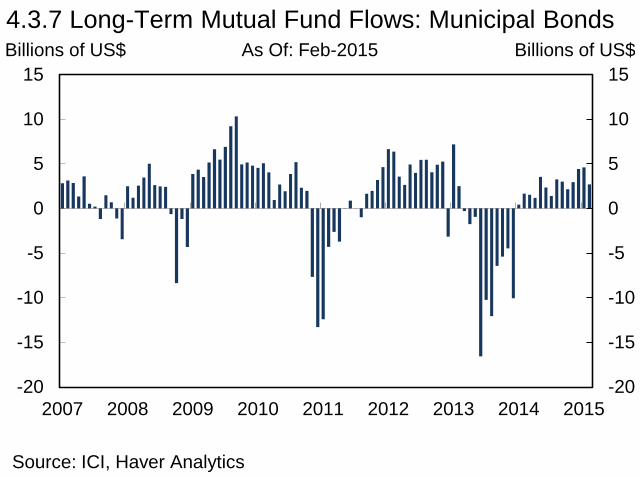

Source: ICI, Haver Analytics

As Of: Feb-2015 Billions of US$ 4.3.7 Long-Term Mutual Fund Flows: Municipal Bonds

Billions of US$

Billions of US$

0

100

200

300

400

500

600

0

100

200

300

400

500

600

2004 2006 2008 2010 2012 2014

New Capital Refunding

4.3.8 Municipal Bond Issuance Billions of US$

Source: Thomson Reuters, SIFMA

As Of: 2014

Note: Excludes maturities of 13 months or less and private placements.

4.3.9 Municipal Bond Spreads

Source: Thomson Reuters MMD

-200

0

200

400

600

800

-200

0

200

400

600

800

2008 2009 2010 2011 2012 2013 2014 2015

Basis Points Basis Points As Of: 31-Mar-2015

Note: Spreads between 10-year municipal and 10-year Treasury securities.

AAA GO

Michigan California

A GO

Illinois Puerto Rico

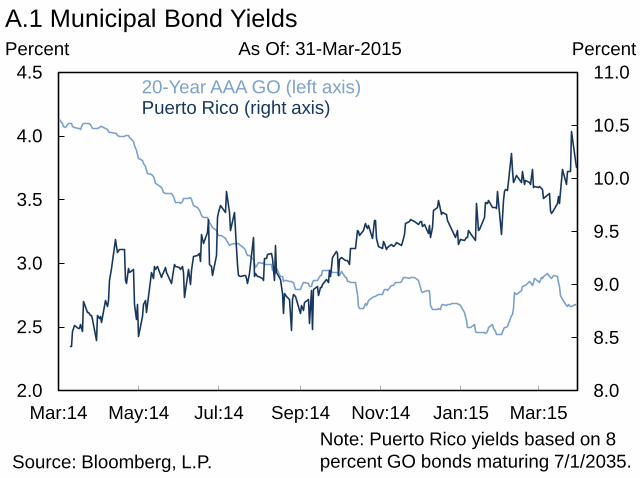

A.1 Municipal Bond Yields

Source: Bloomberg, L.P.

8.0

8.5

9.0

9.5

10.0

10.5

11.0

2.0

2.5

3.0

3.5

4.0

4.5

Mar:14 May:14 Jul:14 Sep:14 Nov:14 Jan:15 Mar:15

Percent Percent As Of: 31-Mar-2015

20-Year AAA GO (left axis) Puerto Rico (right axis)

Note: Puerto Rico yields based on 8 percent GO bonds maturing 7/1/2035.

-8

-6

-4

-2

0

2

4

6

8

-8

-6

-4

-2

0

2

4

6

8

2014 Q1 2014 Q2 2014 Q3 2014 Q4

4.4.1 Advanced Economies Real GDP Growth Percent Percent As Of: 2014 Q4

Source: Eurostat, CAO, BEA, Haver Analytics

Note: Data represents seasonally adjusted quarter-over-quarter annualized real GDP growth rates.

United Kingdom Japan

Euro Area

United States

-6

-4

-2

0

2

4

6

8

10

-6

-4

-2

0

2

4

6

8

10

2000 2004 2008 2012 2016 2020

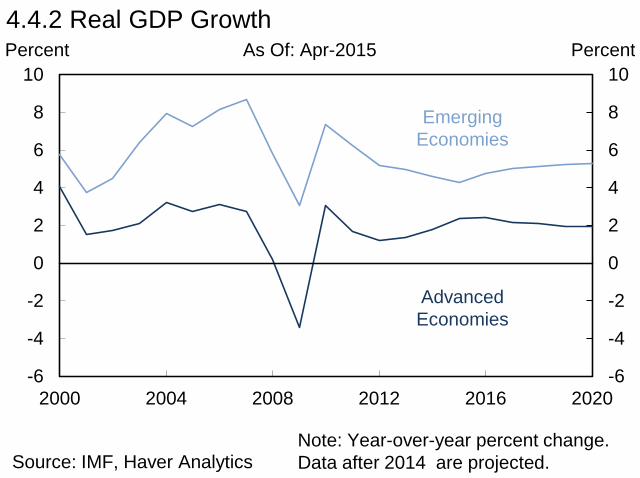

Source: IMF, Haver Analytics

As Of: Apr-2015 Percent 4.4.2 Real GDP Growth

Note: Year-over-year percent change. Data after 2014 are projected.

Percent

Advanced Economies

Emerging Economies

-6

-4

-2

0

2

4

6

-6

-4

-2

0

2

4

6

2002 2005 2008 2011 2014 2017 2020

Source: IMF, Haver Analytics

As Of: Apr-2015 Percent 4.4.3 Euro Area Real GDP Growth

Note: Year-over-year percent change. Data after 2014 are projected.

Percent

Spain France Euro Area Italy Germany

-1

0

1

2

3

4

5

-1

0

1

2

3

4

5

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

4.4.4 Euro Area Consumer Price Inflation Percent Percent

Source: Statistical Office of the European Communities, Haver Analytics

As Of: Mar-2015

Headline Current Target

Note: Year-over-year percent change.

Core

-8

-6

-4

-2

0

2

4

6

8

-8

-6

-4

-2

0

2

4

6

8

2014Q1

2014Q2

2014Q3

2014Q4

2015 2016 2017

4.4.5 Japanese Real GDP Growth Percent Percent As Of: 2014 Q4

Source: Cabinet Office of Japan, IMF, Haver Analytics

Note: Data from 2014 represents seasonally adjusted annualized quarter-over-quarter real GDP growth rates. Data from 2015 and beyond represents seasonally adjusted year-over-year real GDP growth rates. Data after 2014 is projected.

-3

-2

-1

0

1

2

3

-3

-2

-1

0

1

2

3

1997 2000 2003 2006 2009 2012 2015

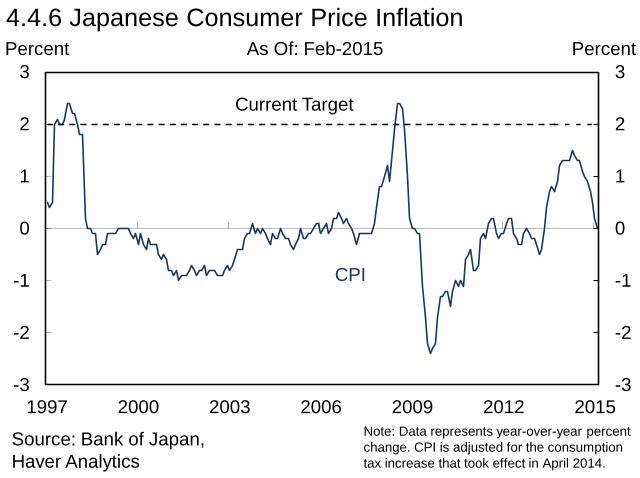

4.4.6 Japanese Consumer Price Inflation Percent Percent

Source: Bank of Japan, Haver Analytics

As Of: Feb-2015

CPI

Current Target

Note: Data represents year-over-year percent change. CPI is adjusted for the consumption tax increase that took effect in April 2014.

0

2

4

6

8

10

12

14

16

0

2

4

6

8

10

12

14

16

2000 2002 2004 2006 2008 2010 2012 2014

4.4.7 Chinese Real GDP Growth Percent Percent

Source: China National Bureau of Statistics, Haver Analytics

As Of: 2014

Note: Year-over-year percent change from the fourth quarter of the previous year.

100

104

108

112

116

120

-15

-10

-5

0

5

10

15

2011 2012 2013 2014 2015

4.4.8 Chinese Property Prices Percent Index

Source: China National Bureau of Statistics, Haver Analytics

As Of: Mar-2015

Note: 2010 = 100 in property price index. Monthly changes expressed at an annualized rate. Data represents the arithmetic mean of a 70-city sample.

Monthly Change (left axis)

Property Price Index (right axis)

Percent As Of: Mar-2015 4.4.9 Chinese Credit Growth

Source: The People’s Bank of China, Haver Analytics

0

10

20

30

40

50

60

70

0

10

20

30

40

50

60

70

2008 2009 2010 2011 2012 2013 2014 2015

Percent

Bank Credit

Nonbank Credit

Total Credit

Note: 12-month percentage change of 3-month rolling average.

Percent As Of: Mar-2015 4.4.10 Components of Chinese Nonbank Credit Growth

Source: The People’s Bank of China, Haver Analytics

-50

0

50

100

150

200

250

300

-50

0

50

100

150

200

250

300

2008 2009 2010 2011 2012 2013 2014 2015

Percent

Other Nonfinancial Equity Financing Bankers’ Acceptance Bills Trust Loans Entrusted Loans

Note: 12-month percentage change of 3-month rolling average.

100

120

140

160

180

200

100

120

140

160

180

200

2008 2009 2010 2011 2012 2013 2014

4.4.11 Credit to the Chinese Nonfinancial Private Sector Percent of GDP Percent of GDP As Of: 2014 Q3

Source: China National Bureau of Statistics, BIS, Haver Analytics Note: Rolling 4-quarter sum of GDP.

Percent As Of: 31-Mar-2015 5.1.1 10-Year Treasury Yields

Source: U.S. Department of the Treasury

-2

-1

0

1

2

3

4

5

-2

-1

0

1

2

3

4

5

2009 2010 2011 2012 2013 2014 2015

Percent

Treasury Notes

Treasury Inflation-Protected Securities

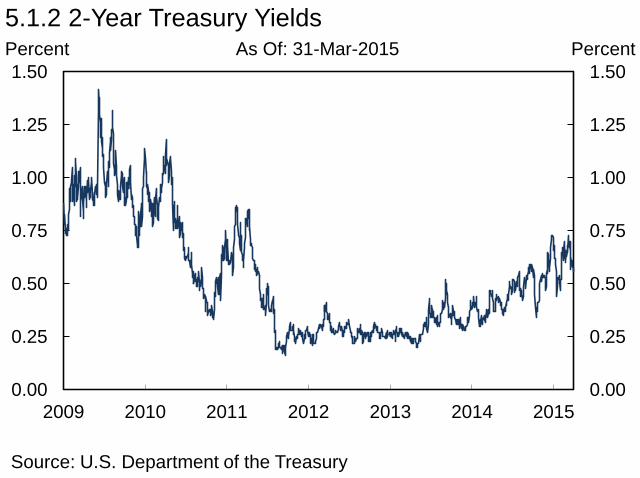

Percent As Of: 31-Mar-2015 5.1.2 2-Year Treasury Yields

Source: U.S. Department of the Treasury

0.00

0.25

0.50

0.75

1.00

1.25

1.50

0.00

0.25

0.50

0.75

1.00

1.25

1.50

2009 2010 2011 2012 2013 2014 2015

Percent

0

3

6

9

12

15

0

3

6

9

12

15

2001 2003 2005 2007 2009 2011 2013 2015Source: U.S. Department of the Treasury, Haver Analytics

As Of: Mar-2015 Trillions of US$ 5.1.3 Publicly Held Federal Debt Outstanding

Trillions of US$

0

20

40

60

80

100

0

20

40

60

80

100

2000 2002 2004 2006 2008 2010 2012 2014

5.1.4 Foreign Holders of U.S. Federal Debt Percent Percent

Source: U.S. Department of the Treasury, Haver Analytics

As Of: Feb-2015

China

Japan

Euro Area

Other

0

50

100

150

200

250

300

0

50

100

150

200

250

300

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Merrill Lynch Option Volatility Estimate

(MOVE) Index

1994-Present MOVE Average

5.1.5 Fixed Income Implied Volatility Basis Points Basis Points

Source: Bloomberg, L.P.

As Of: 31-Mar-2015

Note: Implied volatility is calculated using a yield curve-weighted index of the normalized implied volatility on 1-month Treasury options.

0

8

16

24

32

40

0

4

8

12

16

20

2010 2011 2012 2013 2014 2015

Source: Bloomberg, L.P.

As Of: 31-Mar-2015 Percent 5.1.6 European 10-Year Yields

Percent

Greece (right axis) Portugal (left axis) Spain (left axis) Italy (left axis) United Kingdom (left axis) Germany (left axis)

-300

-100

100

300

500

-300

-100

100

300

500

2006 2007 2008 2009 2010 2011 2012 2013 2014

Net Inflows

Portfolio Flows Bank Flows

Foreign Direct Investment

5.1.7 Gross Capital Flows to EMEs Billions of US$ Billions of US$

Source: IMF, Haver Analytics

As Of: 2014 Q3

0

100

200

300

400

500

600

700

0

100

200

300

400

500

600

700

2004 2006 2008 2010 2012 2014

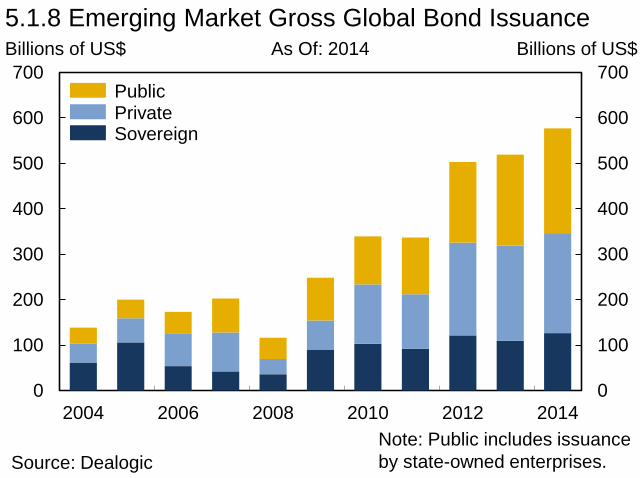

5.1.8 Emerging Market Gross Global Bond Issuance Billions of US$ Billions of US$

Source: Dealogic

As Of: 2014

Note: Public includes issuance by state-owned enterprises.

Private Public

Sovereign

0

200

400

600

800

1000

0

200

400

600

800

1000

2008 2009 2010 2011 2012 2013 2014 2015Source: JP Morgan, Haver Analytics

As Of: 31-Mar-2015 Basis Points 5.1.9 Emerging Market Bond Spreads

Note: JP Morgan EMBI+ Sovereign Spreads indices for each region.

Basis Points

Latin America Europe Asia

0.0

0.5

1.0

1.5

2.0

2.5

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2005 2007 2009 2011 2013 2015

Source: Bloomberg, L.P.

As Of: 31-Mar-2015 Percent 5.1.10 Agency MBS Yield and Spread

Percent

Fannie Mae 30-Year MBS (left axis)

Agency MBS Spread Over 10-Year Treasury

(right axis)

0

50

100

150

200

250

0

50

100

150

200

250

2001 2003 2005 2007 2009 2011 2013

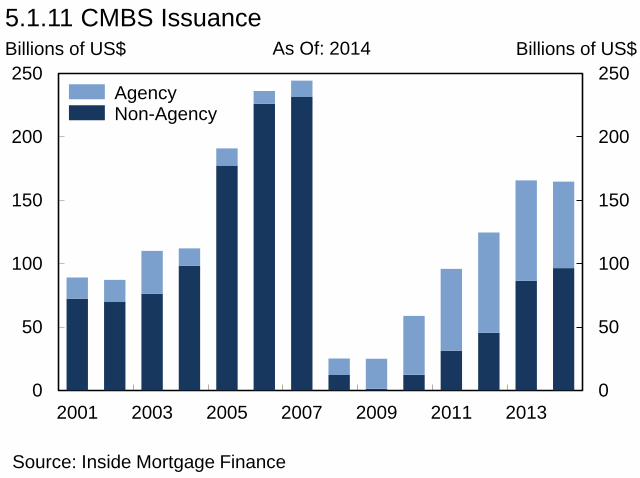

5.1.11 CMBS Issuance Billions of US$ Billions of US$

Source: Inside Mortgage Finance

As Of: 2014

Agency Non-Agency

0

50

100

150

200

250

0

50

100

150

200

250

Mar:11 Mar:12 Mar:13 Mar:14 Mar:15

New Issue LCF

5.1.12 CMBS Senior Debt Spreads Basis Points Basis Points

Source: Barclays

As Of: 26-Mar-2015

Note: Cash spread of new issue non-agency 3.0 duper 10-year LCF CMBS.

0

200

400

600

800

1000

0

50

100

150

200

250

300

350

400

2010 2011 2012 2013 2014 2015

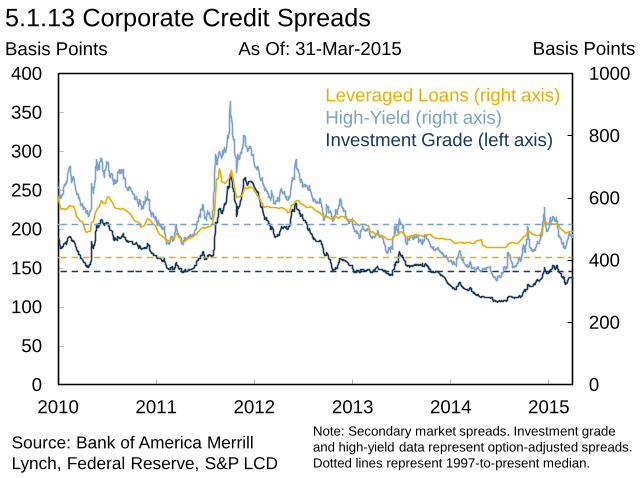

5.1.13 Corporate Credit Spreads

Source: Bank of America Merrill Lynch, Federal Reserve, S&P LCD

As Of: 31-Mar-2015

Leveraged Loans (right axis) High-Yield (right axis) Investment Grade (left axis)

Basis Points Basis Points

Note: Secondary market spreads. Investment grade and high-yield data represent option-adjusted spreads. Dotted lines represent 1997-to-present median.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2004 2006 2008 2010 2012 2014

5.1.14 Total High-Yield Debt Outstanding Trillions of US$ Trillions of US$

Source: BAML High-Yield Strategy, S&P LCD

As Of: 2014

High-Yield Bonds Leveraged Loans

0

1

2

3

4

0

1

2

3

4

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

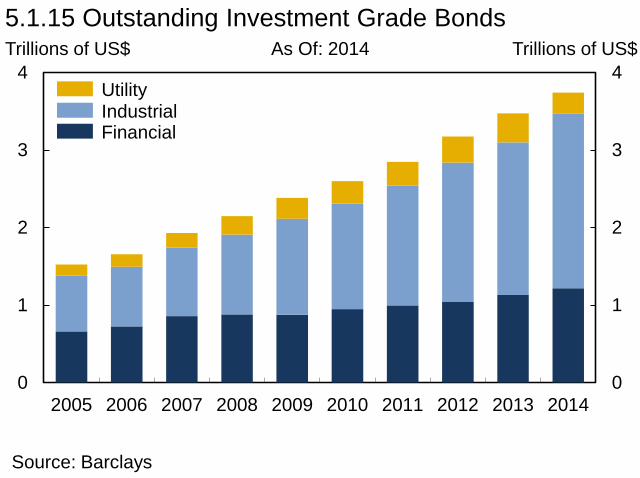

5.1.15 Outstanding Investment Grade Bonds Trillions of US$ Trillions of US$ As Of: 2014

Industrial Utility

Financial

Source: Barclays

0

1

2

3

4

5

6

7

8

0

1

2

3

4

5

6

7

8

2001 2003 2005 2007 2009 2011 2013

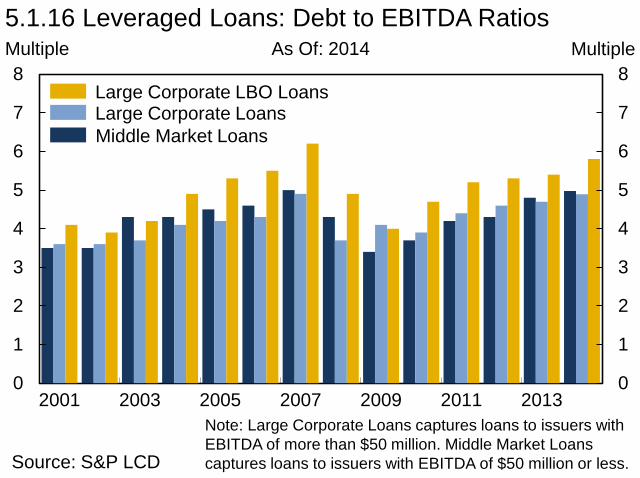

5.1.16 Leveraged Loans: Debt to EBITDA Ratios Multiple Multiple

Source: S&P LCD

As Of: 2014

Large Corporate LBO Loans Large Corporate Loans

Note: Large Corporate Loans captures loans to issuers with EBITDA of more than $50 million. Middle Market Loans captures loans to issuers with EBITDA of $50 million or less.

Middle Market Loans

0

10

20

30

40

50

60

0

10

20

30

40

50

60

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

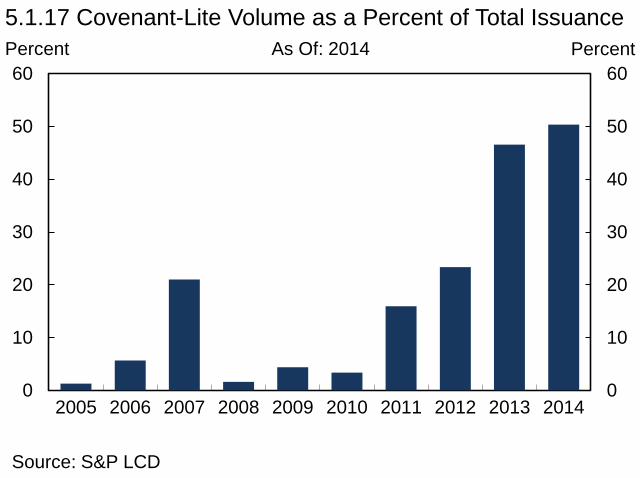

5.1.17 Covenant-Lite Volume as a Percent of Total Issuance Percent Percent

Source: S&P LCD

As Of: 2014

0

20

40

60

80

100

120

140

0

20

40

60

80

100

120

140

2004 2006 2008 2010 2012 2014

5.1.18 CLO Issuance Billions of US$ Billions of US$

Source: S&P LCD

As Of: 2014

5.1.19 Share of Leveraged Loan Primary Market by Investor Type

Source: S&P LCD

0

10

20

30

40

50

60

70

0

10

20

30

40

50

60

70

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Percent Percent

Finance & Security Companies

As Of: 2014

CLOs

Insurance Companies Loan Mutual Funds Hedge Funds

Banks

0

20

40

60

80

100

120

140

160

0

100

200

300

400

500

600

1995 1999 2003 2007 2011 2015

C.1 Commodity Prices: Metals vs. Oil Index US$/Barrel

Source: Bloomberg, L.P.

As Of: 31-Mar-2015

Brent Oil (right axis)

GSCI Metals Index (left axis)

0

200

400

600

800

1000

0

200

400

600

800

1000

2010 2011 2012 2013 2014 2015

C.2 High-Yield Bond Spreads Basis Points Basis Points

Source: Bloomberg, L.P.

As Of: 31-Mar-2015

High-Yield Energy Sector

High-Yield

Note: Spreads to worst.

90

100

110

120

130

140

90

100

110

120

130

140

1998 2000 2002 2004 2006 2008 2010 2012 2014

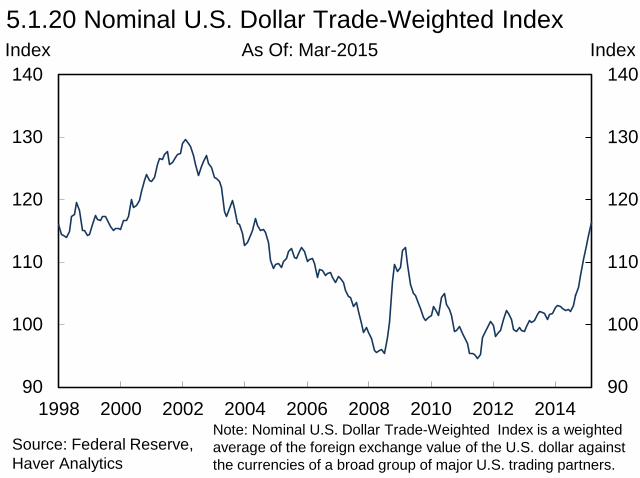

Source: Federal Reserve, Haver Analytics

As Of: Mar-2015 Index 5.1.20 Nominal U.S. Dollar Trade-Weighted Index

Note: Nominal U.S. Dollar Trade-Weighted Index is a weighted average of the foreign exchange value of the U.S. dollar against the currencies of a broad group of major U.S. trading partners.

Index

0

5

10

15

20

25

30

35

40

0

5

10

15

20

25

30

35

40

2008 2009 2010 2011 2012 2013 2014 2015

Currency VIX Average,

2002-Present

5.1.21 Currency Implied Volatility Percent Percent As Of: 31-Mar-2015

Source: Bloomberg, L.P.

3-Month Euro-Dollar 3-Month Dollar-Yen Currency VIX

60

70

80

90

100

110

120

130

140

150

60

70

80

90

100

110

120

130

140

150

2008 2009 2010 2011 2012 2013 2014 2015

Source: Federal Reserve, Haver Analytics

As Of: 31-Mar-2015 Index 5.1.22 U.S. Dollar Exchange Rates

Note: 1-Jan-2008 = 100. EM is a weighted average of the FX values of the dollar against a subset of currencies in the broad index that do not circulate widely outside the country of issue.

Index

Euro-Dollar Major Dollar Index EM Yen-Dollar

-40

-30

-20

-10

0

10

20

-40

-30

-20

-10

0

10

20

5.1.23 Change in Exchange Rates (Mar 2014 - Mar 2015) Percent Percent

Source: JP Morgan, Haver Analytics

As Of: Mar-2015

Note: Change in exchange rate is the change in a country's JP Morgan Broad Nominal Effective Exchange Rate Index.

Change from 31-Mar-2014 to 31-Mar-2015

Annual growth rate from 31-Mar-2010 to

31-Mar-2015 Major Economies U.S. (S&P) 10% 12% Euro (Euro Stoxx) 17% 6% Japan (Nikkei) 30% 12% U.K. (FTSE) 3% 4% Selected Europe Germany (DAX) 25% 14% France (CAC) 15% 5% Italy (FTSE MIB) 7% 0% Spain (IBEX) 11% 1% Emerging Markets MSCI Emerging Market Index -2% -1% Brazil (Bovespa) 1% -6% Russia (RTS) -28% -11% India (Sensex) 25% 10% China (Shanghai SE) 84% 4% Hong Kong (Hang Seng) 12% 3%

5.1.24 Returns in Selected Equities Indices

Source: Capital IQ

1.0

1.5

2.0

2.5

3.0

3.5

10

15

20

25

30

2008 2009 2010 2011 2012 2013 2014 2015

5.1.25 S&P 500 Key Ratios Ratio Ratio

Source: Bloomberg, L.P.

P/B Ratio (right axis)

Trailing P/E Ratio (left axis)

As Of: 31-Mar-2015

Note: Dotted lines represent 1995-to-present median.

0

20

40

60

80

100

0

20

40

60

80

100

2008 2009 2010 2011 2012 2013 2014 2015

VIX

1995-2014 Average

5.1.26 Market Volatility Percent Percent

Source: Capital IQ

As Of: 31-Mar-2015

0

25

50

75

100

125

150

175

200

0

25

50

75

100

125

150

175

200

2008 2009 2010 2011 2012 2013 2014 2015Source: Energy Information Administration, S&P, Haver Analytics

As Of: 31-Mar-2015 Index 5.1.27 Commodities

Note: 02-Jan-2008 = 100.

Index

Agriculture (S&P GSCI Agricultural Spot Index) Industrial Metals (S&P GSCI Industrial Metals Spot Index) Crude Oil (WTI) Natural Gas

80

100

120

140

160

180

200

220

80

100

120

140

160

180

200

220

2000 2002 2004 2006 2008 2010 2012 2014Source: CoreLogic, FHFA, Haver Analytics

As Of: Feb-2015 Index 5.1.28 National Repeat Sales Home Price Indices

Note: Jan-2000 = 100. Gray bars signify NBER recessions.

Index

CoreLogic (including

distressed sales) CoreLogic (excluding

distressed sales)

FHFA

0

2

4

6

8

10

12

0

200

400

600

800

1000

1200

1992 1996 2000 2004 2008 2012

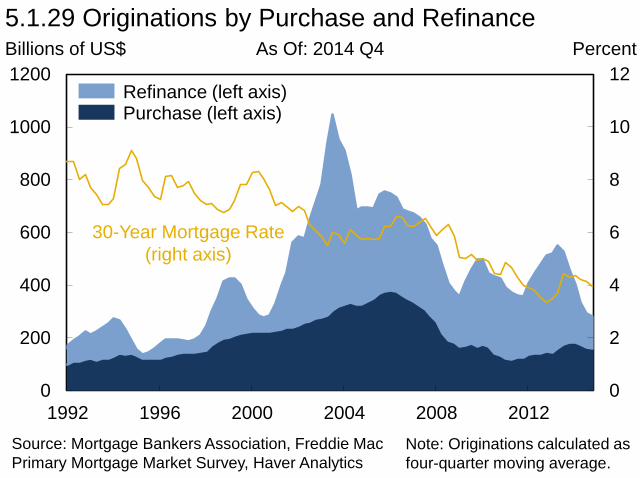

30-Year Mortgage Rate (right axis)

5.1.29 Originations by Purchase and Refinance Billions of US$ Percent

Source: Mortgage Bankers Association, Freddie Mac Primary Mortgage Market Survey, Haver Analytics

As Of: 2014 Q4

Refinance (left axis) Purchase (left axis)

Note: Originations calculated as four-quarter moving average.

0

5

10

15

20

25

30

300

400

500

600

700

800

900

2010 2011 2012 2013 2014

Value of Negative Equity in Residential Mortgages

(left axis)

Percent of Residential

Mortgages with Negative Equity

(right axis)

5.1.30 Mortgages with Negative Equity Billions of US$ Percent

Source: CoreLogic

As Of: 2014 Q4

0

1

2

3

4

5

6

0

1

2

3

4

5

6

2000 2002 2004 2006 2008 2010 2012 2014Source: Mortgage Bankers Association, Haver Analytics

As Of: 2014 Q4 Percent 5.1.31 Mortgage Delinquency and Foreclosure

Note: Percent of all mortgages.

Percent

Mortgage Foreclosure Inventory

Mortgage Payments Past-Due 90+ Days

0

20

40

60

80

100

0

20

40

60

80

100

2002 2004 2006 2008 2010 2012 2014

5.1.32 Purchase Origination Volume by Credit Score Percent of Originations Percent of Originations

Source: CoreLogic, Inside Mortgage Finance, OFR calculations

As Of: 2014

Note: Includes first lien purchases only.

<600

600-660

660-700

700-720

720-760

>760

0

20

40

60

80

100

0

20

40

60

80

100

2000 2002 2004 2006 2008 2010 2012 2014

5.1.33 Mortgage Originations by Product Percent of Originations Percent of Originations

Source: Inside Mortgage Finance

As Of: 2014

FHA / VA

GSE

Private Portfolio and Securitized

0.0

0.5

1.0

1.5

2.0

2.5

3.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2000 2002 2004 2006 2008 2010 2012 2014

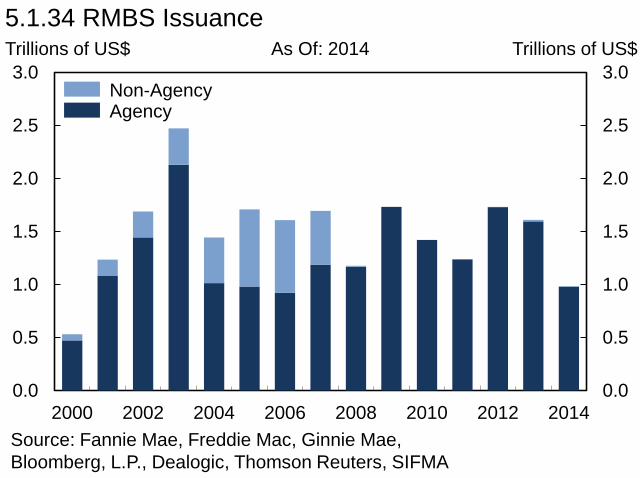

5.1.34 RMBS Issuance Trillions of US$ Trillions of US$

Source: Fannie Mae, Freddie Mac, Ginnie Mae, Bloomberg, L.P., Dealogic, Thomson Reuters, SIFMA

As Of: 2014

Non-Agency Agency

0

2

4

6

8

10

0

2

4

6

8

10

2011 2012 2013 2014

5.1.35 Mortgage Servicing Market Trillions of US$ Trillions of US$

Source: Inside Mortgage Finance

As Of: 2014 Q4

Nonbank Bank

Note: Data covers top 25 servicers in each quarter.

40

60

80

100

120

140

40

60

80

100

120

140

2008 2009 2010 2011 2012 2013 2014 2015

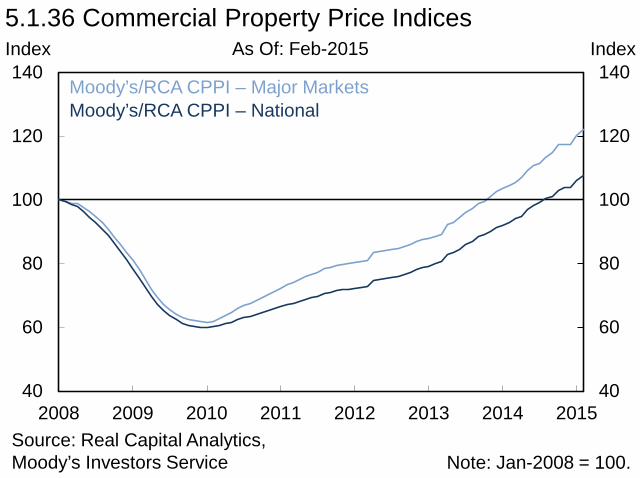

5.1.36 Commercial Property Price Indices Index Index

Source: Real Capital Analytics, Moody’s Investors Service

Moody’s/RCA CPPI – National

Note: Jan-2008 = 100.

Moody’s/RCA CPPI – Major Markets

As Of: Feb-2015

60

80

100

120

140

160

180

4

5

6

7

8

9

10

2003 2005 2007 2009 2011 2013

Source: FDIC, Financial Accounts of the United States, Haver Analytics

As Of: 2014 Q4 Trillions of US$ 5.2.1 Composition of Bank Short-Term Funding

Note: Retail deposits are from all FDIC-insured institutions. Wholesale funding includes a system-wide measure of repurchase agreements.

Percent

Short-Term Wholesale Funding (left axis)

Wholesale Funding as a Percent of Retail Deposits

(right axis)

Retail Deposits (left axis)

0.0

0.5

1.0

1.5

2.0

2.5

0.0

0.5

1.0

1.5

2.0

2.5

2001 2003 2005 2007 2009 2011 2013 2015

5.2.2 Commercial Paper Outstanding Trillions of US$ Trillions of US$ As Of: 25-Mar-2015

Domestic Financial Domestic Nonfinancial Foreign Financial

Asset-Backed

Other Foreign Nonfinancial

Source: Federal Reserve Note: Domestic includes CP issued in the U.S. by entities with foreign parents.

0

1

2

3

4

5

0

1

2

3

4

5

2002 2004 2006 2008 2010 2012 2014

5.2.3 Value of the Repo Market Trillions of US$ Trillions of US$

Source: FRBNY

As Of: 31-Mar-2015

Note: Limited data were provided by the clearing banks prior to April 2008. These figures are estimates based on the data provided. Daily Federal Reserve RRP operations beginning in September 2013 are depicted; small-scale RRP test operations undertaken periodically at earlier dates are not depicted. Gray bar signifies NBER recession.

FR 2004 Primary Dealer Repo

Tri-Party Repo Market (excluding Federal

Reserve RRPs)

Tri-Party Repo Market (including Federal Reserve RRPs)

0

1

2

3

4

5

0

1

2

3

4

5

2000 2002 2004 2006 2008 2010 2012 2014

5.2.4 Primary Dealer Repo Agreements Trillions of US$ Trillions of US$ As Of: 25-Mar-2015

Source: FRBNY

Overnight/Continuing Term

0.0

0.5

1.0

1.5

2.0

2.5

3.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Jan:13 Jul:13 Jan:14 Jul:14 Jan:15

5.2.5 Collateral in Tri-Party Repo Trillions of US$ Trillions of US$

Source: FRBNY, Haver Analytics

As Of: 10-Mar-2015

Note: Other includes CDOs, international, money market, municipal debt, and whole loans.

Agency MBS Agency Debentures and Strips Agency CMOs

U.S. Treasuries excluding Strips ABS Equities U.S. Treasury Strips

Corporates

Other Private Label CMOs

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2008 2009 2010 2011 2012 2013 2014 2015

5.2.6 Value of Securities on Loan Trillions of US$ Trillions of US$

Source: Markit Group Limited

Global Market (including U.S.)

U.S. Market

As Of: 31-Mar-2015

Note: Data is based on a survey of agent-based lenders.

0

20

40

60

80

100

0

20

40

60

80

100

2008 2009 2010 2011 2012 2013 2014 2015

5.2.7 Composition of Securities Lending by Security Type Percent of Lending Percent of Lending

Source: Markit Group Limited

Government Bonds

As Of: 31-Mar-2015

Equities

Note: Data is based on a survey of agent-based lenders. Other includes ETFs, emerging market bonds, and depository receipts.

Corporate Bonds

Other

0

50

100

150

200

250

0.0

0.3

0.6

0.9

1.2

1.5

1.8

2000 2002 2004 2006 2008 2010 2012 2014

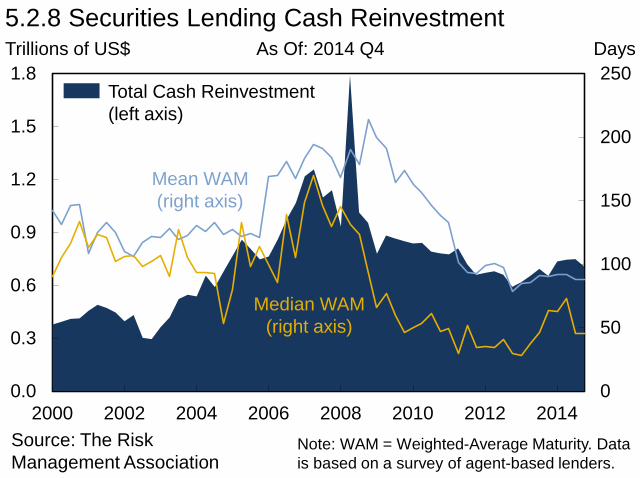

5.2.8 Securities Lending Cash Reinvestment Trillions of US$ Days

Source: The Risk Management Association

Mean WAM (right axis)

Median WAM (right axis)

As Of: 2014 Q4

Note: WAM = Weighted-Average Maturity. Data is based on a survey of agent-based lenders.

Total Cash Reinvestment (left axis)

-1200

-900

-600

-300

0

300

600

900

1200

-1200

-900

-600

-300

0

300

600

900

1200

2006 2007 2008 2009 2010 2011 2012 2013 2014

5.3.1 Domestic BHC Pre-Tax Income Billions of US$ Billions of US$

Source: FR Y-9C

As Of: 2014

Noninterest Income Net Interest Income

Total Pre-Tax Income

Provisions Noninterest Expense Realized Gains/Losses on Investments

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Percent Percent As Of: 2014 Q4

Source: FR Y-9C

5.3.2 Return on Average Assets for Domestic BHCs

1996-2005 Average

-100

0

100

200

300

400

2.0

2.4

2.8

3.2

3.6

4.0

2000 2002 2004 2006 2008 2010 2012 2014

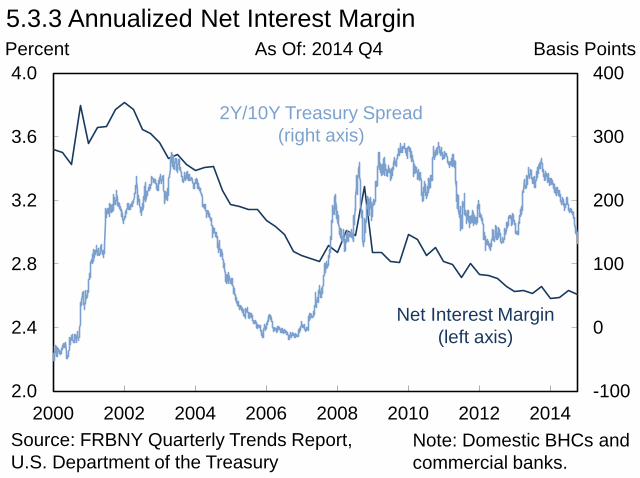

2Y/10Y Treasury Spread (right axis)

5.3.3 Annualized Net Interest Margin Percent Basis Points

Source: FRBNY Quarterly Trends Report, U.S. Department of the Treasury

As Of: 2014 Q4

Note: Domestic BHCs and commercial banks.

Net Interest Margin (left axis)

0

100

200

300

400

500

600

700

0

100

200

300

400

500

600

700

2012 2013 2014

5.3.4 Total Residential Mortgage Originations Billions of US$ Billions of US$

Source: Mortgage Bankers Association, Haver Analytics

As Of: 2014 Q4

Purchases Refinancings

0.0

0.4

0.8

1.2

1.6

2.0

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

2010 2011 2012 2013 2014 2015

Source: Bloomberg, L.P.

As Of: 31-Mar-2015 Percent 5.3.5 U.S. Mortgage Spread

Percent

30-Year Agency MBS Yield (left axis)

30-Year Mortgage Rate (left axis)

Spread (right axis)

0

10

20

30

40

50

0

10

20

30

40

50

2010 2011 2012 2013 2014

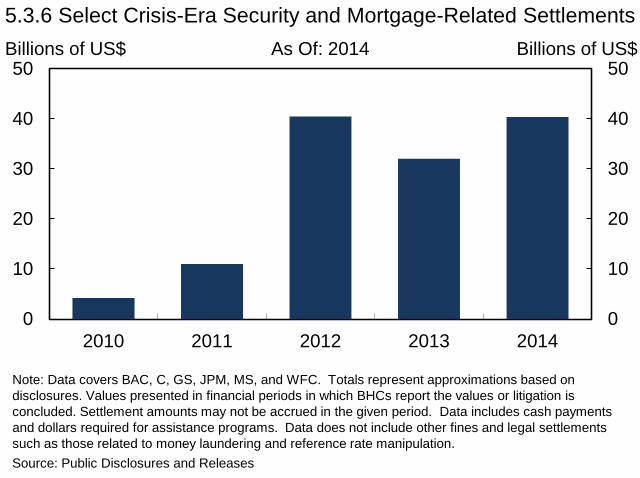

5.3.6 Select Crisis-Era Security and Mortgage-Related Settlements Billions of US$ Billions of US$

Source: Public Disclosures and Releases

As Of: 2014

Note: Data covers BAC, C, GS, JPM, MS, and WFC. Totals represent approximations based on disclosures. Values presented in financial periods in which BHCs report the values or litigation is concluded. Settlement amounts may not be accrued in the given period. Data includes cash payments and dollars required for assistance programs. Data does not include other fines and legal settlements such as those related to money laundering and reference rate manipulation.

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.00

0.05

0.10

0.15

0.20

0.25

0.30

-5 0 5 10 15

5.3.7 Maturity Gap at Large Banks Density Density

Source: Call Reports; Federal Reserve staff estimates

2003 Q3 2012 Q4 2013 Q4 2014 Q4

As Of: 2014 Q4

Note: Banks with assets over $50 billion. Approximations based on midpoint of Call Report ranges. Liquid deposits assumed to have 1-year maturity.

Increasing Interest Rate Sensitivity

Years

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.00

0.05

0.10

0.15

0.20

0.25

0.30

-5 0 5 10 15 20

5.3.8 Maturity Gap at Small Banks Density Density

Source: Call Reports; Federal Reserve staff estimates

2003 Q3 2012 Q4 2013 Q4 2014 Q4

As Of: 2014 Q4

Note: Banks with assets less than or equal to $50 billion. Approximations based on midpoint of Call Report ranges. Liquid deposits assumed to have 1-year maturity.

Increasing Interest Rate Sensitivity

Years

0

20

40

60

80

100

120

140

160

0

20

40

60

80

100

120

140

160

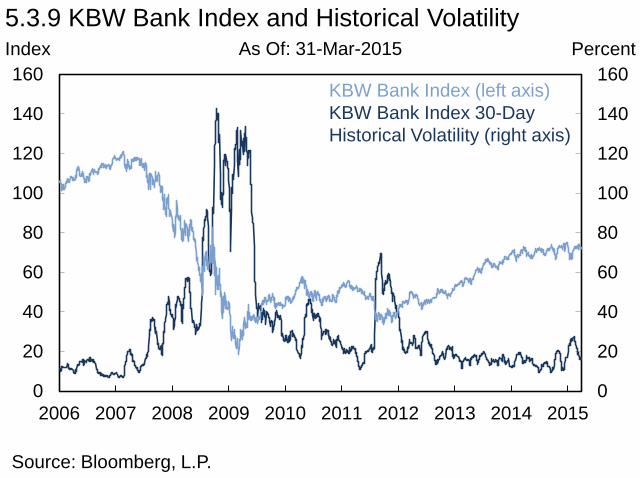

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

5.3.9 KBW Bank Index and Historical Volatility Index Percent

Source: Bloomberg, L.P.

As Of: 31-Mar-2015

KBW Bank Index (left axis) KBW Bank Index 30-Day Historical Volatility (right axis)

5.3.10 P/B and P/E Ratios of Six Large Complex BHCs

Source: Bloomberg, L.P.

0

10

20

30

40

50

60

0

1

2

3

4

5

2000 2002 2004 2006 2008 2010 2012 2014

Ratio Ratio As Of: 31-Mar-2015

P/B Ratio (left axis)

2000-2014 Average P/E (right axis)

2000-2014 Average P/B

(left axis)

P/E Ratio (right axis)

Note: Market cap-weighted average of BAC, C, GS, JPM, MS, and WFC.

Basis Points

0

100

200

300

400

500

600

700

0

100

200

300

400

500

600

700

2009 2010 2011 2012 2013 2014 2015

5.3.11 CDS Spreads of Six Large Complex BHCs Basis Points As Of: 31-Mar-2015

Source: Markit Group Limited Note: CDS spreads of BAC, C, GS, JPM, MS, and WFC.

Maximum Value Equal-Weighted Average Minimum Value

11.65 11.76

9

10

11

12

13

9

10

11

12

13

CommonEquity Capital

Ratio(4Q13)

RWAChangeImpact

NetIssuanceof Stock

RetainedEarnings

OtherAdjustments

CommonEquity Capital

Ratio(4Q14)

(1.10) .77

.52

(.10)

5.3.12 Change in Aggregate Common Equity Capital Ratios for Domestic BHCs

Percent of RWA Percent of RWA

Source: FR Y-9C

As Of: 2014 Q4

Note: In 2013 Q4, the tier 1 common capital ratio is used to measure common equity capital for all BHCs. In 2014 Q4, the tier 1 common capital ratio is used for non-advanced approaches BHCs and the common equity tier 1 capital ratio is used for advanced approaches BHCs.

0

5

10

15

20

25

30

0

5

10

15

20

25

30

2007 2008 2009 2010 2011 2012 2013 2014

5.3.13 Consolidated BHC Liquid Assets Ratio by Firm Size Percent Percent

Source: FR Y-9C

BHCs > $700B All BHCs BHCs $50-700B BHCs < $50B

As Of: 2014 Q4

Note: Liquid assets ratio is the sum of interest-bearing bank balances, FFS, repos, U.S. Treasury securities, U.S. government agencies, and U.S. government-sponsored agencies less pledged securities divided by total assets.

5.3.14 Non-Performing Loans (90+ Days and Non-Accrual)

Source: SNL Financial

0

2

4

6

8

10

0

2

4

6

8

10

2009 2010 2011 2012 2013 2014

Percent Percent

Residential

As Of: 2014 Q4

Other Consumer

C&I

Credit Card

Total NPLs CRE

0

1

2

3

4

5

6

0

1

2

3

4

5

6

2000 2002 2004 2006 2008 2010 2012 2014

5.3.15 Credit Quality Percent of Total Loans Percent of Total Loans As Of: 2014 Q4

Annualized Net Charge-Offs

Total Non-Performing

Loans

Source: FRBNY Quarterly Trends Report

Note: Domestic BHCs and commercial banks. Non-performing loans include loans that are 90+ days past due and still accruing and loans that are non-accrual.

0

50

100

150

200

250

300

350

0

50

100

150

200

2000 2002 2004 2006 2008 2010 2012 2014

As a Percent of Non-Performing Loans

(left axis) As a Percent of Annualized Net

Charge-Offs (right axis)

5.3.16 Loan Loss Reserves Percent Percent As Of: 2014 Q4

Source: FRBNY Quarterly Trends Report, FSOC calculations

Note: Domestic BHCs and commercial banks. Non-performing loans include loans that are 90+ days past due and still accruing and loans that are non-accrual.

0

2

4

6

8

10

12

14

0

2

4

6

8

10

12

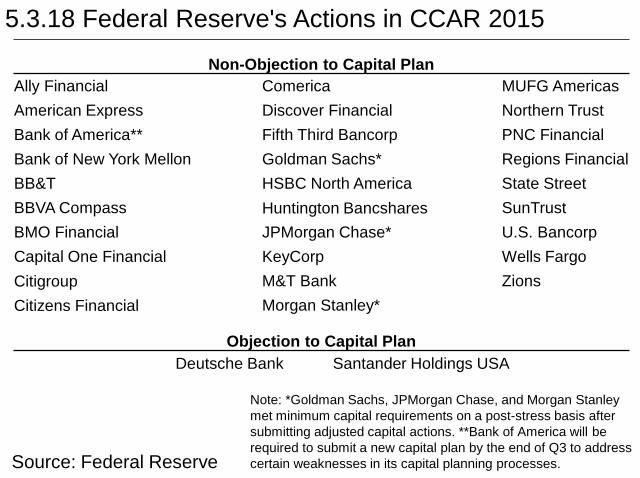

14Pre-Stress Post-Stress Minimum

5.3.17 Initial and Stressed Tier 1 Common Capital Ratios Percent Percent

Source: Federal Reserve

As Of: Mar-2015

Note: Aggregate ratios shown for all participants in each year. Post-stress ratios reflect the minimum ratio observed at any point under the severely adverse supervisory scenario.

DFAST 2013 DFAST 2014 DFAST 2015

5.3.18 Federal Reserve's Actions in CCAR 2015

Note: *Goldman Sachs, JPMorgan Chase, and Morgan Stanley met minimum capital requirements on a post-stress basis after submitting adjusted capital actions. **Bank of America will be required to submit a new capital plan by the end of Q3 to address certain weaknesses in its capital planning processes. Source: Federal Reserve

Non-Objection to Capital Plan Ally Financial Comerica MUFG Americas American Express Discover Financial Northern Trust Bank of America** Fifth Third Bancorp PNC Financial Bank of New York Mellon Goldman Sachs* Regions Financial BB&T HSBC North America State Street BBVA Compass Huntington Bancshares SunTrust BMO Financial JPMorgan Chase* U.S. Bancorp Capital One Financial KeyCorp Wells Fargo Citigroup M&T Bank Zions Citizens Financial Morgan Stanley*

Objection to Capital Plan Deutsche Bank Santander Holdings USA

0

1

2

3

4

5

0

100

200

300

400

500

600

1980 1985 1990 1995 2000 2005 2010Source: BEA, FDIC, Haver Analytics

As Of: 2014 Number of Institutions 5.3.19 FDIC-Insured Failed Institutions

Note: No FDIC-insured institutions failed during 2005 and 2006.

Percent

Number of Institutions (left axis)

Assets of Failed Institutions as a Percent

of Nominal GDP (right axis)

-1000

-750

-500

-250

0

250

500

750

1000

-1000

-750

-500

-250

0

250

500

750

1000

2006 2007 2008 2009 2010 2011 2012 2013 2014

Noninterest Income Net Interest Income

Noninterest Expense Provisions

Realized Gains/Losses on Investments

5.3.20 Commercial Bank and Thrift Pre-Tax Income Billions of US$ Billions of US$

Source: FDIC Note: Includes all FDIC-insured commercial banks and thrifts.

As Of: 2014

Total Pre-Tax Income

63

66

69

72

75

78

-1.5

-1

-0.5

0

0.5

1

1.5

2

2006 2008 2010 2012 2014

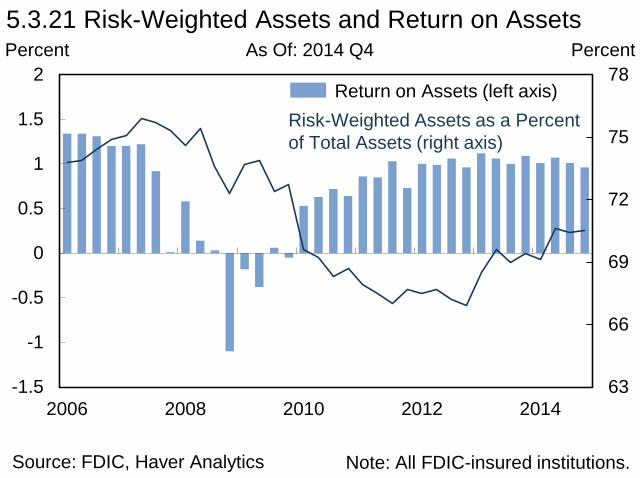

Source: FDIC, Haver Analytics

As Of: 2014 Q4 Percent 5.3.21 Risk-Weighted Assets and Return on Assets

Note: All FDIC-insured institutions.

Percent

Return on Assets (left axis) Risk-Weighted Assets as a Percent of Total Assets (right axis)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2004 2006 2008 2010 2012 2014Source: Federal Reserve, Haver Analytics

As Of: 2014 Q4 Trillions of US$ 5.3.22 U.S. Branches and Agencies of Foreign Banks: Assets

Note: Other assets includes government securities, asset-backed securities, and other trading assets.

Trillions of US$

Cash and Balances Due from Depository Institutions (excluding Reserve Balances)

Non-C&I Loans C&I Loans Net Due From Related Depository Institutions

Reserve Balances

Other Assets

Securities Purchased with Repos & Fed Funds Sold

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2004 2006 2008 2010 2012 2014Source: Federal Reserve, Haver Analytics

As Of: 2014 Q4 Trillions of US$

5.3.23 U.S. Branches and Agencies of Foreign Banks: Liabilities

Note: Other liabilities includes transaction accounts, non-transaction accounts, and other borrowed money.

Trillions of US$

Deposits & Credit Balances Net Due to Related Depository Institutions

Other Liabilities Securities Sold with Repos & Fed Funds Purchased

0.6

0.8

1.0

1.2

1.4

1.6

0.6

0.8

1.0

1.2

1.4

1.6

Jan:13 Jul:13 Jan:14 Jul:14 Jan:15

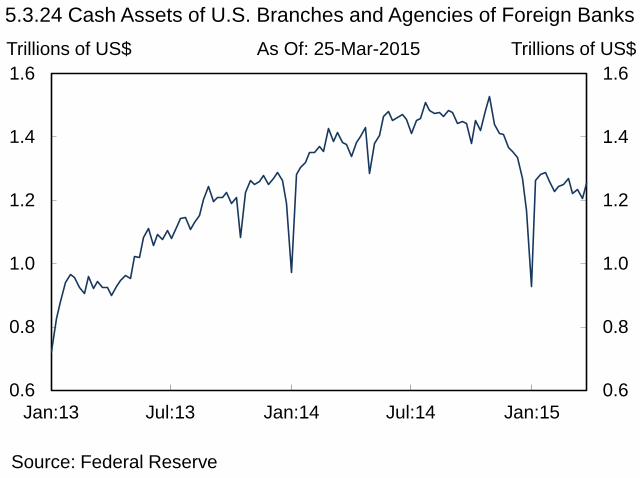

5.3.24 Cash Assets of U.S. Branches and Agencies of Foreign Banks Trillions of US$ Trillions of US$

Source: Federal Reserve

As Of: 25-Mar-2015

-60

-45

-30

-15

0

15

30

45

60

-60

-45

-30

-15

0

15

30

45

60

2006 2007 2008 2009 2010 2011 2012 2013 2014

Net Income

5.3.25 Federally Insured Credit Union Income Billions of US$ Billions of US$

Source: NCUA

As Of: 2014

Noninterest Income Net Interest Income

Noninterest Expense Provisions

Realized Gains/Losses on Investments

45

50

55

60

65

20

25

30

35

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

5.3.26 Credit Union Deposits Percent Percent

Source: NCUA

As Of: 2014 Q4

Money Market and IRA Deposit Share

(left axis)

Interest-Sensitive Deposit Share

(right axis)

0

10

20

30

40

50

0

10

20

30

40

50

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

5.3.27 Credit Union Net Long-Term Assets Percent of Total Assets Percent of Total Assets

Source: NCUA

As Of: 2014 Q4

Mortgage Loans Maturing in 5+ Years

Long-Term Investments Business Loans Fixed Assets

0

5

10

15

20

25

30

35

0

5

10

15

20

25

30

35

2006 Q4 2012 Q4 2013 Q4 2014 Q4

5.3.28 Credit Union Investments by Maturity Percent of Total Assets Percent of Total Assets

Source: NCUA

As Of: 2014 Q4

1-3 Years 3-5 Years

5-10 Years <1 Year

>10 Years

Note: Investments <1 Year excludes securities with maturities <3 months.

0

100

200

300

400

0

100

200

300

400

2009 2010 2011 2012 2013 2014

Sale of Investment Company Shares

Margin Interest Other

Underwriting

Fees – Supervision, Advisory, Administration

Commissions

5.4.1 Broker-Dealer Revenues Billions of US$ Billions of US$

Source: FINRA

As Of: 2014

0

1

2

3

4

5

6

7

2005 2006 2007 2008 2009 2010 2011 2012 2013 20140

8

16

24

32

40

5.4.2 Broker-Dealer Assets and Leverage Trillions of US$ Ratio

Source: FINRA

As Of: 2014

Note: Leverage is the ratio of total assets to total ownership equity.

Total Assets (left axis)

Leverage (right axis)

24

28

32

36

40

0

1

2

3

4

5

2010 2011 2012 2013 2014

BHC-Affiliated Assets (left axis) FBO-Affiliated Assets (left axis) Other Affiliation Assets (left axis)

BHC-Affiliated Leverage (right axis) FBO-Affiliated Leverage (right axis) Other Affiliation Leverage (right axis)

5.4.3 Large Broker-Dealer Assets and Leverage by Affiliation Trillions of US$ Ratio

Source: FINRA

As Of: 2014

Note: Leverage is the ratio of total assets to total ownership equity. Data covers the 20 largest broker-dealers.

-300

-200

-100

0

100

200

300

400

500

2002 2004 2006 2008 2010 2012 2014-300

-200

-100

0

100

200

300

400

500

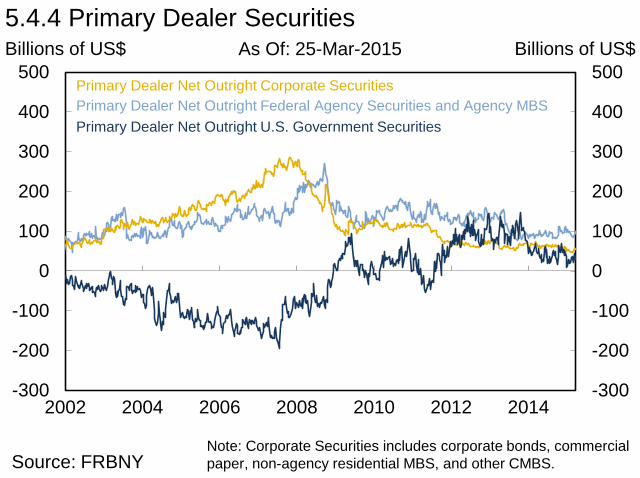

5.4.4 Primary Dealer Securities Billions of US$ Billions of US$

Source: FRBNY

Primary Dealer Net Outright Corporate Securities

Primary Dealer Net Outright U.S. Government Securities Primary Dealer Net Outright Federal Agency Securities and Agency MBS

As Of: 25-Mar-2015

Note: Corporate Securities includes corporate bonds, commercial paper, non-agency residential MBS, and other CMBS.

Name Total Assets Name Total Assets JPMorgan Chase 2,572,773,000 PNC 345,243,081 Bank of America 2,106,796,000 Capital One 309,083,481 Citigroup Inc. 1,842,181,000 HSBC North America 290,100,702 Wells Fargo 1,687,155,000 State Street 274,119,072 MetLife 902,337,000 TIAA-CREF 272,073,395 Goldman Sachs 856,301,000 New York Life 265,555,200 Morgan Stanley 801,510,000 Lincoln 253,377,000 Prudential Financial 766,655,000 TD Bank 248,144,842 Berkshire Hathaway 526,186,000 Hartford 245,013,000 AIG 515,581,000 Northwestern Mutual 230,089,502 GE Capital 508,255,287 Voya 226,951,400 U.S. Bancorp 402,529,000 Principal 219,087,000 Bank of New York Mellon 385,303,000 MassMutual 209,136,072

5.4.5 Select U.S. Financial Holding Companies and Insurers

Note: Thousands of U.S. dollars. Data as of 2014 Q4. GAAP and SAP accounting. Insurers listed in blue. Entity classifications correspond to those used by the National Information Center and SNL Financial. Asset levels correspond to consolidated financial reporting.

Source: National Information Center, SNL Financial

0

15

30

45

60

75

0

15

30

45

60

75

2009 2010 2011 2012 2013 2014

5.4.6 Insurance Industry Net Income Billions of US$ Billions of US$

Source: SNL Financial

As Of: 2014

Life P&C

Note: Life includes accident and health.

2

3

4

5

6

7

2009 2010 2011 2012 2013 20142

3

4

5

6

7

5.4.7 Net Yield on Invested Assets Percent Percent

Source: SNL Financial, Bank of America Merrill Lynch

Life

P&C

Yield on A-Rated Corporate Debt

As Of: 2014

Note: Life includes accident and health.

0

150

300

450

600

750

900

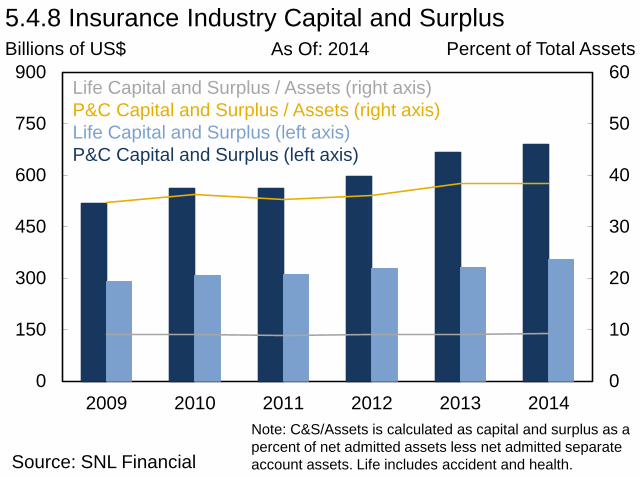

2009 2010 2011 2012 2013 20140

10

20

30

40

50

60

5.4.8 Insurance Industry Capital and Surplus Billions of US$ Percent of Total Assets

Life Capital and Surplus / Assets (right axis) P&C Capital and Surplus / Assets (right axis) Life Capital and Surplus (left axis) P&C Capital and Surplus (left axis)

As Of: 2014

Note: C&S/Assets is calculated as capital and surplus as a percent of net admitted assets less net admitted separate account assets. Life includes accident and health. Source: SNL Financial

20

25

30

35

40

45

0

200

400

600

800

1000

2008 2009 2010 2011 2012 2013 2014

5.4.9 Variable Annuities with Guaranteed Living Benefits Billions of US$ Percent

Source: LIMRA

As Of: 2014

Variable Annuity Assets with GLBs (left axis)

Share of Variable Annuity Assets with GLBs

(right axis)

Note: Data is based on a survey of domestic insurance companies.

0.0

0.4

0.8

1.2

1.6

2.0

0.0

0.4

0.8

1.2

1.6

2.0

2001 2003 2005 2007 2009 2011 2013 2015

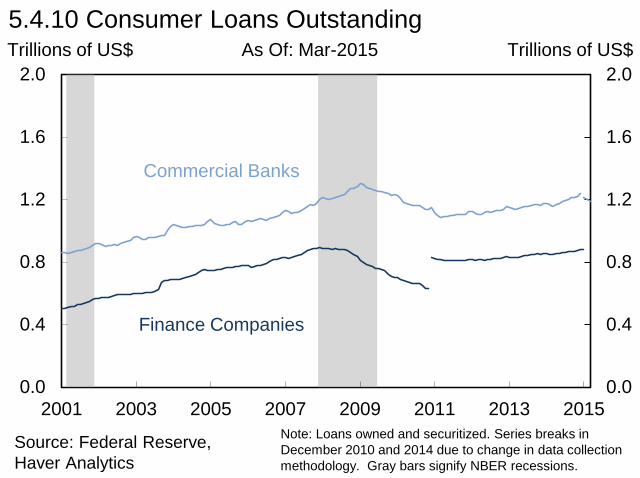

Source: Federal Reserve, Haver Analytics

As Of: Mar-2015 Trillions of US$ 5.4.10 Consumer Loans Outstanding

Note: Loans owned and securitized. Series breaks in December 2010 and 2014 due to change in data collection methodology. Gray bars signify NBER recessions.

Trillions of US$

Commercial Banks

Finance Companies

0.0

0.4

0.8

1.2

1.6

2.0

0.0

0.4

0.8

1.2

1.6

2.0

2001 2003 2005 2007 2009 2011 2013 2015

Source: Federal Reserve, Haver Analytics

As Of: Mar-2015 Trillions of US$ 5.4.11 Business Loans Outstanding

Trillions of US$

Commercial Banks

Finance Companies

Note: Loans owned and securitized. Series break in December 2010 due to change in data collection methodology. Gray bars signify NBER recessions.

0

15

30

45

60

75

0

200

400

600

800

1000

1200

2000 2002 2004 2006 2008 2010 2012 2014

5.4.12 Auto Loans Outstanding and Originations by Type Billions of US$ Billions of US$

Source: FRBNY Consumer Credit Panel/Equifax, Haver Analytics

Bank Originations (right axis)

Finance Company Originations (right axis)

As Of: 2014 Q4

Aggregate Balance Outstanding (left axis)

Note: Originations calculated as four-quarter moving average.

0

50

100

150

200

250

300

0

50

100

150

200

250

300

2008 2009 2010 2011 2012 2013 2014

Credit Card Student Loans

Auto Housing Related Other

Equipment

5.4.13 ABS Issuance Billions of US$ Billions of US$

Source: Thomson Reuters, SIFMA

As Of: 2014

0

50

100

150

200

250

0

50

100

150

200

250

2010 2011 2012 2013 2014 2015

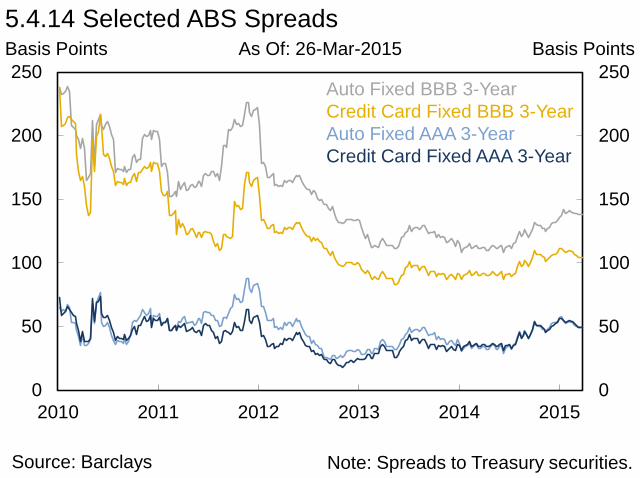

5.4.14 Selected ABS Spreads Basis Points Basis Points

Source: Barclays

Auto Fixed BBB 3-Year Credit Card Fixed BBB 3-Year Auto Fixed AAA 3-Year Credit Card Fixed AAA 3-Year

As Of: 26-Mar-2015

Note: Spreads to Treasury securities.

As Of: 2014 Q4

0

100

200

300

400

500

0

3

6

9

12

15

18

2000 2002 2004 2006 2008 2010 2012 2014

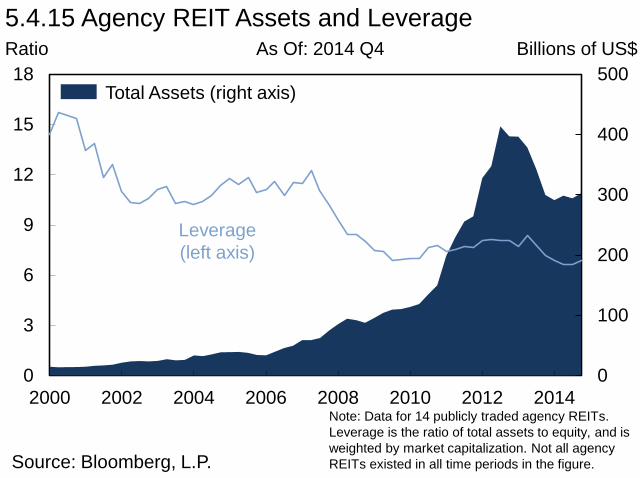

5.4.15 Agency REIT Assets and Leverage Ratio Billions of US$

Source: Bloomberg, L.P.

Leverage (left axis)

Total Assets (right axis)

Note: Data for 14 publicly traded agency REITs. Leverage is the ratio of total assets to equity, and is weighted by market capitalization. Not all agency REITs existed in all time periods in the figure.

0.0

0.5

1.0

1.5

2.0

0.0

0.5

1.0

1.5

2.0

2000 2002 2004 2006 2008 2010 2012 2014

5.4.16 Agency REIT Price-to-Book Ratio Ratio Ratio

Source: Bloomberg, L.P.

As Of: 2014 Q4

Note: Data for 14 publicly traded agency REITs. Price-to-book ratio is weighted by market capitalization. Not all agency REITs existed in all time periods in the figure.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2011 2012 2013 2014 2015

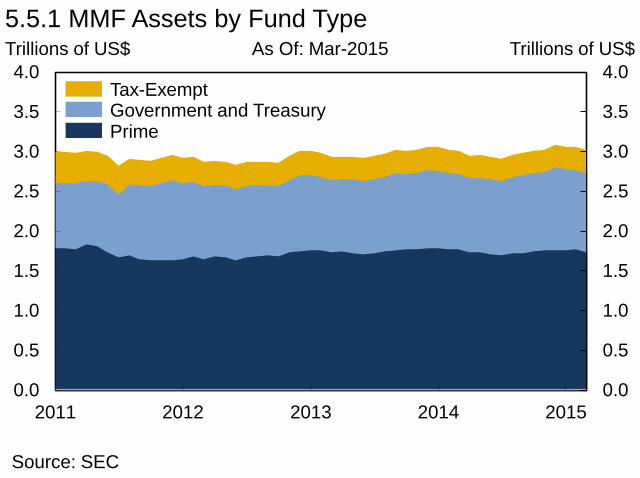

5.5.1 MMF Assets by Fund Type Trillions of US$ Trillions of US$

Source: SEC

As Of: Mar-2015

Prime Government and Treasury Tax-Exempt

0

100

200

300

400

500

600

700

0

100

200

300

400

500

600

700

2011 2012 2013 2014 2015

Repo with European Counterparties

ABCP issued by European Entities

5.5.2 U.S. MMF Holdings of European Entities’ CP, CD, and Repos Billions of US$ Billions of US$ As Of: Feb-2015

Source: SEC Form N-MFP filings, OFR calculations

Unsecured CDs and CP issued by

European Entities

Note: Assets valued at amortized cost.

20

25

30

35

40

45

50

20

25

30

35

40

45

50

2011 2012 2013 2014 2015

5.5.3 Liquidity of Prime MMFs Percent of Total Assets Percent of Total Assets

Source: SEC

As Of: Mar-2015

Daily Liquidity

Weekly Liquidity

Note: Weighted by fund size.

Note: Weighted by fund size.

5.5.4 Weighted-Average Life of MMFs

Source: SEC

60

65

70

75

80

85

60

65

70

75

80

85

2011 2012 2013 2014 2015

Days Days

Prime Funds

All Funds

As Of: Mar-2015

0

4

8

12

16

20

0

4

8

12

16

20

1990 1994 1998 2002 2006 2010 2014

5.5.5 Net Assets of the Investment Company Industry Trillions of US$ Trillions of US$ As Of: 2014

ETFs Other

Equity Bond/Hybrid MMFs

Note: Other is composed of unit investment trusts and closed-end funds. Source: ICI, Haver Analytics

-70-60-50-40-30-20-10010203040

-70-60-50-40-30-20-10

010203040

Jan:13 May:13 Sep:13 Jan:14 May:14 Sep:14 Jan:15

Source: ICI, Haver Analytics

As Of: Feb-2015 Billions of US$ 5.5.6 Monthly Bond Mutual Fund Flows

Billions of US$

Tax-Exempt Taxable

-30

-20

-10

0

10

20

30

40

-30

-20

-10

0

10

20

30

40

Jan:13 May:13 Sep:13 Jan:14 May:14 Sep:14 Jan:15

Source: ICI, Haver Analytics

As Of: Feb-2015 Billions of US$ 5.5.7 Monthly Equity Mutual Fund Flows

Billions of US$

-30

-20

-10

0

10

20

30

40

50

60

70

-30

-20

-10

0

10

20

30

40

50

60

70

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

5.5.8 Bank Loan Mutual Funds: Annual Flows Billions of US$ Billions of US$

Source: Morningstar, Inc.

As Of: 2014

-5

0

5

10

15

20

25

30

35

40

45

-5

0

5

10

15

20

25

30

35

40

45

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

5.5.9 Alternative Mutual Funds: Annual Flows Billions of US$ Billions of US$

Source: Morningstar, Inc.

As Of: 2014

-600

-400

-200

0

200

400

600

-600

-400

-200

0

200

400

600

2009 2010 2011 2012 2013 2014 2015

5.5.10 Cumulative Equity Fund Flows Billions of US$ Billions of US$

Source: Morningstar, Inc.

As Of: Mar-2015

Note: Includes ETFs and mutual funds.

International Passively Managed U.S. Passively Managed International Actively Managed U.S. Actively Managed

0

4

8

12

16

20

24

28

0

4

8

12

16

20

24

28

2007 2008 2009 2010 2011 2012 2013 2014Source: Financial Accounts of the United States, Haver Analytics

As Of: 2014 Q3 Trillions of US$ 5.5.11 Retirement Fund Assets by Plan Type

Trillions of US$

Private Defined Benefit Plans

Individual Accounts Private Defined Contribution Plans

State and Local Federal

60

70

80

90

100

110

120

60

70

80

90

100

110

120

2002 2004 2006 2008 2010 2012 2014

5.5.12 Public and Private Pension Funding Levels

Source: Public Fund Survey, Milliman 2015 Pension Funding Study

Percent Percent

Public Defined Benefit Plans

Private Defined Benefit Plans

As Of: 2014

0.0

0.6

1.2

1.8

2.4

0.0

0.6

1.2

1.8

2.4

2002 2004 2006 2008 2010 2012 2014

5.5.13 U.S. Private Equity AUM Trillions of US$ Trillions of US$

Source: Preqin

As Of: 2014 Q3

YTD

Undeployed Capital Existing Investments

5.0

5.5

6.0

6.5

7.0

7.5

8.0

240

260

280

300

320

2010 2011 2012 2013 2014 2015

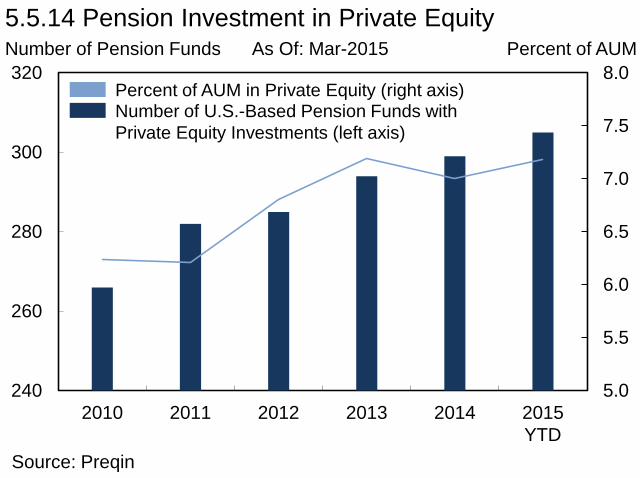

5.5.14 Pension Investment in Private Equity Number of Pension Funds Percent of AUM

Source: Preqin

As Of: Mar-2015

YTD

Percent of AUM in Private Equity (right axis) Number of U.S.-Based Pension Funds with Private Equity Investments (left axis)

0

10

20

30

40

50

60

0.0

1.5

3.0

4.5

6.0

7.5

9.0

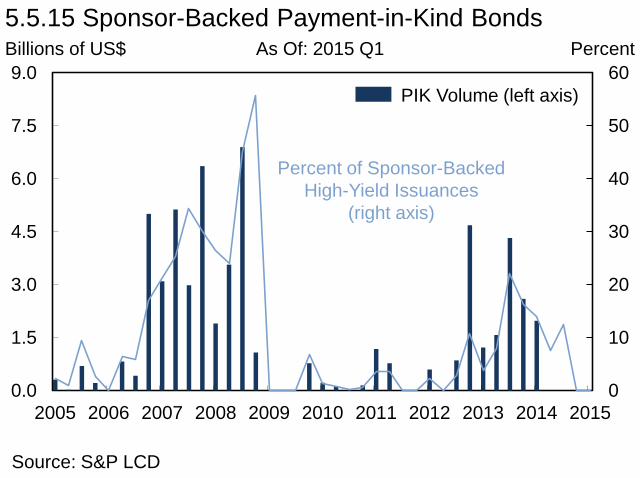

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

5.5.15 Sponsor-Backed Payment-in-Kind Bonds Billions of US$

Source: S&P LCD

As Of: 2015 Q1

PIK Volume (left axis)

Percent of Sponsor-Backed High-Yield Issuances

(right axis)

Percent

0

300

600

900

1200

1500

1800

0.0

0.5

1.0

1.5

2.0

2.5

2007 2008 2009 2010 2011 2012 2013 2014

5.5.16 U.S.-Listed ETP AUM and Count Trillions of US$ Number of Funds

Source: Morningstar, Inc.

As Of: 2014

AUM (left axis)

Number of Funds (right axis)

0

100

200

300

400

500

600

700

800

0

100

200

300

400

500

600

700

800

2000 2002 2004 2006 2008 2010 2012 2014

Source: BIS, Haver Analytics

As Of: 2014 Q4 Trillions of US$ 5.6.1 Global OTC Derivatives Market

Note: Notional values.

Trillions of US$

Unallocated

Interest Rate Contracts

Commodity Contracts Credit Default Swaps

Equity-linked Contracts

FX Contracts

0

10

20

30

40

50

60

70

0

10

20

30

40

50

60

70

2005 2007 2009 2011 2013

Source: BIS, Haver Analytics

As Of: 2014 Q4 Trillions of US$ 5.6.2 Credit Derivatives Outstanding

Note: Notional values.

Trillions of US$

Single Name Multi-Name

0

1

2

3

4

5

6

0

1

2

3

4

5

6

2000 2002 2004 2006 2008 2010 2012 2014

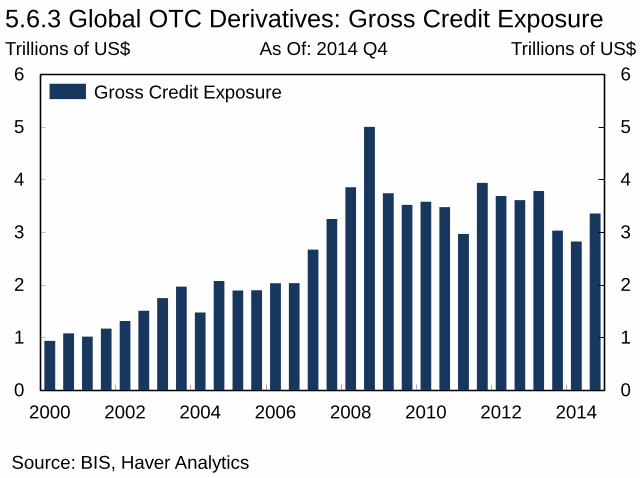

5.6.3 Global OTC Derivatives: Gross Credit Exposure Trillions of US$ Trillions of US$

Source: BIS, Haver Analytics

As Of: 2014 Q4

Gross Credit Exposure

0

50

100

150

200

250

0

50

100

150

200

250

Futures andForwards

Options CreditDerivatives

Total Swaps Total DerivativeNotionals

5.6.4 Concentration of U.S. Derivative Exposures Trillions of US$ Trillions of US$ As Of: 2014 Q4

Source: OCC Quarterly Report on Bank Trading and Derivatives Activities

Note: Notional values. Data covers insured U.S. commercial banks and savings associations.

All Other Banks Top 4 Banks

0

1

2

3

4

Jan:14 Mar:14 May:14 Jul:14 Sep:14 Nov:14 Jan:150

1

2

3

4

5.6.5 Swap Execution Facility Weekly Volume Trillions of US$ Trillions of US$

Source: Futures Industry Association

As Of: 30-Jan-2015

Note: Notional values.

FX Interest Rate

Credit

D.1 Bilateral Derivatives Market

Uncleared

Large Financial Institution

Large Financial Institution

Large Financial Institution

Large Financial Institution

Large Financial Institution

Small Financial Institution

Small Financial Institution

Small Financial Institution

Small Financial Institution

Client

Client

Clients

Client

Client

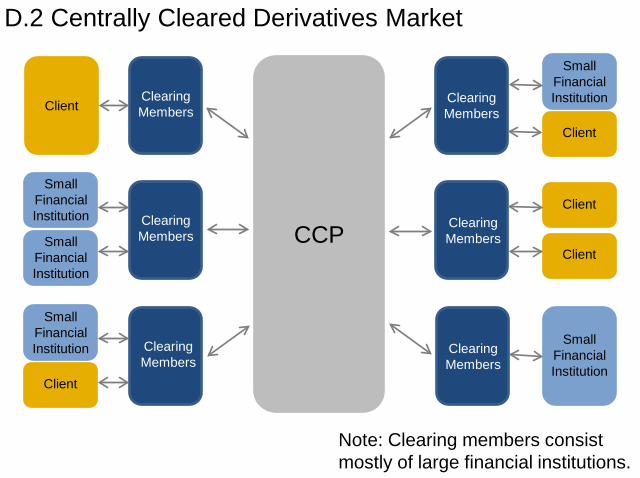

D.2 Centrally Cleared Derivatives Market

Note: Clearing members consist mostly of large financial institutions.

CCP

Client

Small Financial Institution

Client

Clearing Members

Clearing Members

Clearing Members

Clearing Members

Clearing Members

Clearing Members

Small Financial Institution

Small Financial Institution

Small Financial Institution

Client

Client

Client

Small Financial Institution

0

20

40

60

80

100

0

20

40

60

80

100

Oct:12 Apr:13 Oct:13 Apr:14 Oct:14

D.3 Centrally Cleared Swap Market

Source: CFTC

Percent Percent

Percentage of Interest Rate

Swaps Cleared

Percentage of Credit Swaps

Cleared

As Of: 27-Mar-2015

Note: Notional values. Data are adjusted for double-counting of cleared trades to show a single exposure for each trade. Methodology for collecting and reporting data changed in October 2013.

0

20

40

60

80

100

0

20

40

60

80

100

Futures CashEquities

FX (Spot) U.S.Treasuries

Agencies Std. InterestRate Swaps

IG (Cash)

7.3.1 Use of Electronic Trading by Asset Class Percent Percent As Of: 2012

Source: McKinsey

Note: Projected 2015 Level displays McKinsey projections. U.S. Treasuries measures on-the-run securities in the dealer-to-client market.

Projected 2015 Level Estimated 2012 Level

1.8

1.9

2.0

2.1

2.2

1.8

1.9

2.0

2.1

2.2

8:00 9:00 10:00 11:00 12:00 1:00 2:00 3:00

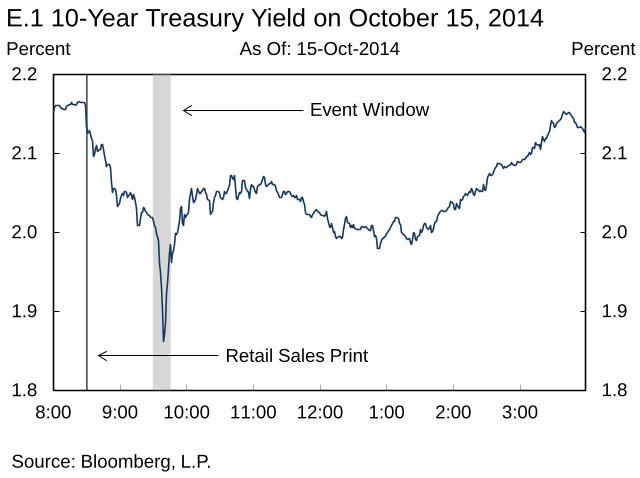

E.1 10-Year Treasury Yield on October 15, 2014 Percent Percent

Source: Bloomberg, L.P.

As Of: 15-Oct-2014

Retail Sales Print

Event Window

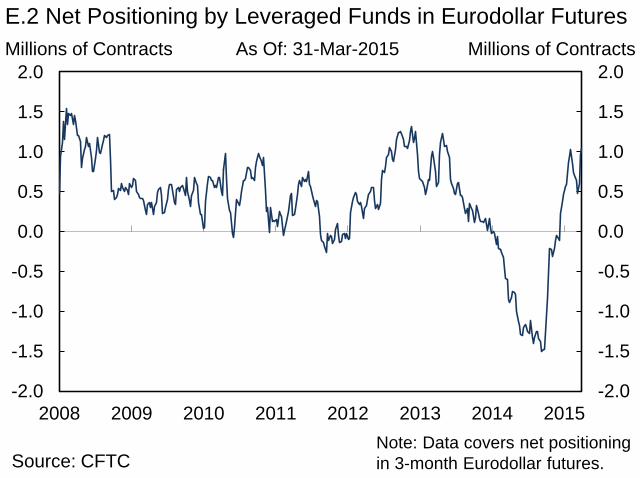

Millions of Contracts As Of: 31-Mar-2015

E.2 Net Positioning by Leveraged Funds in Eurodollar Futures

Source: CFTC

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2008 2009 2010 2011 2012 2013 2014 2015

Millions of Contracts

Note: Data covers net positioning in 3-month Eurodollar futures.

0

1

2

3

4

5

0

1

2

3

4

5

JPMorganChase

Citigroup Bank ofAmerica

Wells Fargo GoldmanSachs

MorganStanley

7.8.1 Total Exposure of Six Large Complex BHCs Trillions of US$ Trillions of US$

Source: Company Y-15 Reports

As Of: 2014

2012 2013

Note: Total exposure is calculated using total assets plus the net value of certain securities financing transactions, credit derivatives and commitments, and counterparty risk exposures.

2014

0.0

0.5

1.0

1.5

2.0

2.5

0.0

0.5

1.0

1.5

2.0

2.5

JPMorganChase

Citigroup Bank ofAmerica

Wells Fargo GoldmanSachs

MorganStanley

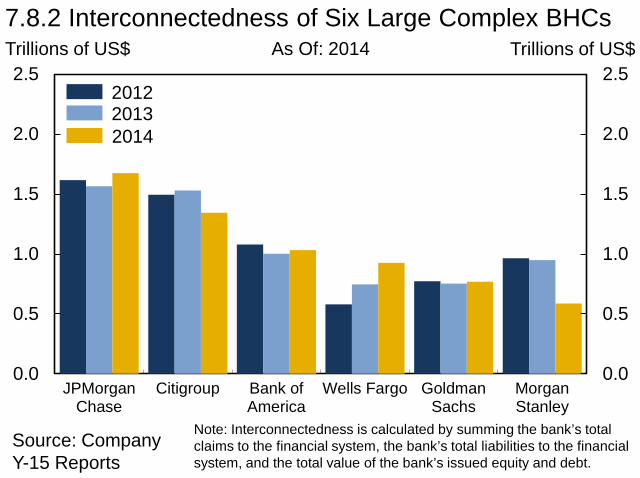

7.8.2 Interconnectedness of Six Large Complex BHCs Trillions of US$ Trillions of US$

Source: Company Y-15 Reports

As Of: 2014

2012 2013

Note: Interconnectedness is calculated by summing the bank’s total claims to the financial system, the bank’s total liabilities to the financial system, and the total value of the bank’s issued equity and debt.

2014

0

20

40

60

80

100

0

20

40

60

80

100

JPMorganChase

Citigroup Bank ofAmerica

Wells Fargo GoldmanSachs

MorganStanley

7.8.3 OTC Derivatives Held by Six Large Complex BHCs Trillions of US$ Trillions of US$

Source: Company Y-15 Reports

As Of: 2014

2012 2013 2014

Note: Notional values.

0

30

60

90

120

150

0

30

60

90

120

150

JPMorganChase

Citigroup Bank ofAmerica

Wells Fargo GoldmanSachs

MorganStanley

7.8.4 Level 3 Assets Held by Six Large Complex BHCs Billions of US$ Billions of US$

Source: Company Y-15 Reports

As Of: 2014

2012 2013

Note: Level 3 assets are assets whose fair value cannot be determined by using observable inputs.

2014

0

1

2

3

4

5

6

0

1

2

3

4

5

6

2005 2007 2009 2011 2013 2015

7.8.5 Systemic Risk Measures

Source: Bloomberg, L.P., OFR calculations

As Of: Mar-2015

CoVaR SES DIP

Index Index

Note: Sample consists of BAC, C, GS, JPM, MS, and WFC. Measures are standardized by their historical volatility.

0

2

4

6

8

0

2

4

6

8

2007 2008 2009 2010 2011 2012 2013 2014 2015

7.8.6 Moody’s Systemic Support Uplift Notches Notches

Citibank

Bank of America

JPMorgan Chase Bank Bank of

New York Mellon

Wells Fargo Bank

U.S. Bank

As Of: Mar-2015

Source: Moody’s Analytics, FRBNY calculations

Note: Uplift is defined as the difference between Moody’s long-term issuer rating and Moody’s bank financial strength rating, which provides an estimate of the effect of implicit guarantees and external support.

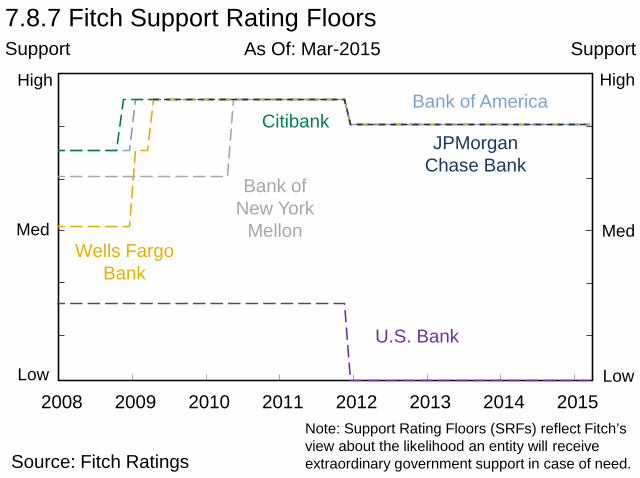

2008 2009 2010 2011 2012 2013 2014 2015

Support High

Med

Low

Source: Fitch Ratings

7.8.7 Fitch Support Rating Floors Support

Citibank Bank of America

JPMorgan Chase Bank

Bank of New York

Mellon Wells Fargo

Bank

U.S. Bank

As Of: Mar-2015

Note: Support Rating Floors (SRFs) reflect Fitch’s view about the likelihood an entity will receive extraordinary government support in case of need.

High

Med

Low