2019 economic & market outlook€¦ · monetary policy is now viewed as ti ght with real rates...

TRANSCRIPT

2019 Economic & Market OutlookJanuary 17, 2019

Presented by

Benjamin A. Pace, III

Chief Investment Officer

Confidential & Proprietary

Key Themes for 2019

2

Confidential & Proprietary

Equities are likely to resume the bull market.

The economic expansion continues.

Recession risk remains low for this year.

Capital spending is an important factor for 2019 GDP growth.

Fed ends tightening cycle in a benign inflationary environment.

China pulls policy levers to stabilize growth.

Resolution of U.S./China trade dispute is a risk to the outlook.

Favor credit over duration in fixed income.

Review of 2018No where to escape low returns

3

Confidential & Proprietary

1%

2% 2%

-5%

-1%

2%

-14%

-18%

-13%

-7%

-9%

-7%

0%

-3%

2% 2%

0%

-2%

-5%

3%

-4%

-10%

-14%-15%

-11%

-5%

-1%

-2%

-20%

-15%

-10%

-5%

0%

5%

Citi 3M T-bill

Barc 1-10 YrMuni Bond

Barc US AggBond

BAML HYMaster II

JPMorganEMBI

Citi WGBIHedged

S&P 500 Russell 2500 MSCI EAFE MSCI EM BbgCommodity

MSCI USREIT

Barc USTIPS

HFRI FoF

QTD YTDSource: Factset

Fixed Income

Equities

Global Growth Even with the slowdown in international markets, robust global growth is forecasted for 2019.

4

Confidential & Proprietary

3.9%4.0%

2.6%

3.6%

4.8%

2.5%

3.0%

4.3%

5.4%

4.9%

5.5%5.6%

3.0%

-0.1%

5.4%

4.3%

3.5% 3.5% 3.6%3.5%

3.3%

3.7% 3.7% 3.7% 3.7%

-1%

0%

1%

2%

3%

4%

5%

6%

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Global Real GDP Growth

Forecasted

Source: IMF

Nearing the End of the Economic CycleExpansion could extend further based on its inherently anemic nature, aging capital stock and corporate tax reform.

37

4539

24

106

36

58

12

92

120

73

114

0

20

40

60

80

100

120

140

October 1949to July 1953

May 1954 toAugust 1957

May 1954 toAugust 1957

April 1958 toApril 1960

February1961 to

December1969

November1970 to

November1973

March 1975 toJanuary 1980

July 1980 toJuly 1981

November1982 to July

1990

March 1991 toMarch 2001

November2001 to

December2008

June 2009 toCurrent

Nu

mb

er o

f Mon

ths

Time Period

Length of Economic Expansions Since World War II

Source: NBER

5

Confidential & Proprietary

Drivers of Growth – Capital Spending & ProductivityCapital spending and productivity increases will be vital to a continuation of the current expansion.

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

Mar-80 Mar-83 Mar-86 Mar-89 Mar-92 Mar-95 Mar-98 Mar-01 Mar-04 Mar-07 Mar-10 Mar-13 Mar-16

Private Nonresidential Fixed Investment

Private Nonresidential Fixed Investment (year over year %)Source: FRED

Confidential & Proprietary

6

The U.S. ConsumerA stalwart for both the U.S. and global economy – employment is strong with more job openings than those looking for jobs

Confidential & Proprietary

7

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

Mar-89 Mar-91 Mar-93 Mar-95 Mar-97 Mar-99 Mar-01 Mar-03 Mar-05 Mar-07 Mar-09 Mar-11 Mar-13 Mar-15 Mar-17

U.S. Consumption Growth

United States - Personal Consumption Expenditures, Bil Chained 2009, SAAR, Bil USDSource: Factset

There is a large difference between the slowdown in the growth rate and a directional change in sales, earnings and GDP. A recession does not seem to be an immediate risk.

-20%

-15%

-10%

-5%

0%

5%

10%

15%

Dec-00 Dec-02 Dec-04 Dec-06 Dec-08 Dec-10 Dec-12 Dec-14 Dec-16

S&P 500 Sales Growth

12 Month Sales per Share Growth (year over year %)Source: Factset

Rate of Change

8

Confidential & Proprietary

40%

42%

41%

40%

41%

42%

45%

46% 47%

46% 46%46%

45%

44%

44%

36%

38%

40%

42%

44%

46%

48%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Investment as a % of GDP

Gross Capital Formation as a % of Nominal GDP

China’s Rebalancing ActBeyond the headlines of the tariffs, China is attempting a delicate rebalancing of its economic growth drivers.

Confidential & Proprietary

9

Source: Factset

China & TariffsSo far, the U.S. has “won” the trade war in market terms.

Confidential & Proprietary

10

6.20

6.30

6.40

6.50

6.60

6.70

6.80

6.90

7.00

7.10

90

95

100

105

110

115

120

125

130

135

140

Jan-18 Feb-18 Mar-18 Apr-18 May-18 Jun-18 Jul-18 Aug-18 Sep-18 Oct-18 Nov-18 Dec-18 Jan-19

Relative Performance of the U.S./Chinese Stock Market & U.S. Dollar/Yuan Exchange Rate

iShares Core S&P 500 ETF Relative to iShares MSCI China ETF (Total Return), lhs U.S. Dollar/ Chinese Yuan, rhsSource: Factset

Europe FallingGrowth rates in the Eurozone have been falling since the end of 2017 with Italy at the epicenter.

Confidential & Proprietary

11

40

45

50

55

60

65

Sep-15 Mar-16 Sep-16 Mar-17 Sep-17 Mar-18 Sep-18

European Manufacturing Surveys

Germany Manufacturing PMI Italy Manufacturing PMI

Expanding

Contracting

Source: Factset

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Jan-89 Jan-91 Jan-93 Jan-95 Jan-97 Jan-99 Jan-01 Jan-03 Jan-05 Jan-07 Jan-09 Jan-11 Jan-13 Jan-15 Jan-17 Jan-19 Jan-21

Fed Funds Rate

Fed Funds Rate FOMC year-end estimates

The Biggest Risk: The FedMonetary policy is now viewed as tight with real rates above zero. Watch the yield curve, but also watch inflation indicators. Without real price pressures, the Fed should be able to pause and then end rate increases.

Confidential & Proprietary

12

Source: FRED

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

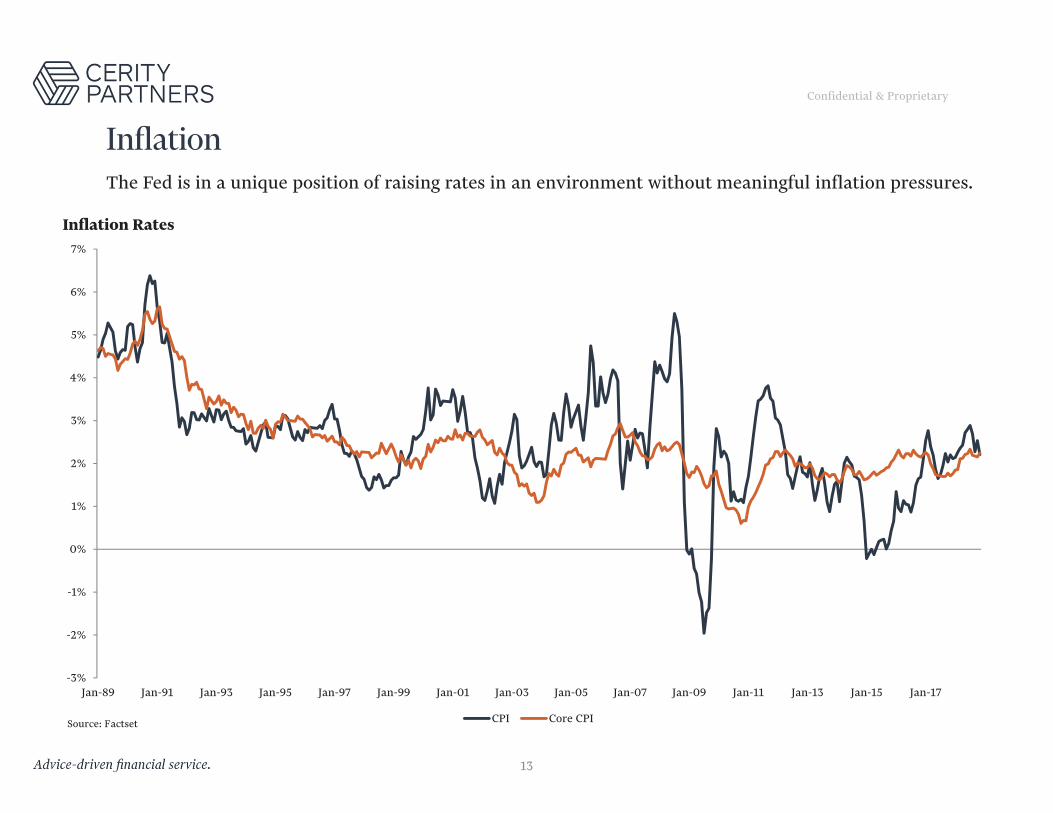

Jan-89 Jan-91 Jan-93 Jan-95 Jan-97 Jan-99 Jan-01 Jan-03 Jan-05 Jan-07 Jan-09 Jan-11 Jan-13 Jan-15 Jan-17

Inflation Rates

CPI Core CPISource: Factset

InflationThe Fed is in a unique position of raising rates in an environment without meaningful inflation pressures.

Confidential & Proprietary

13

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Federal Budget Surplus/Deficit as a % of GDP

Fiscal PolicyThe effectiveness of tax cuts and spending increases may be called into question given the impact on the deficit. Watch for the crowding out effect of higher deficits on real interest rates.

Confidential & Proprietary

14

Source: FRED

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

Jan-09 Oct-09 Jul-10 Apr-11 Jan-12 Oct-12 Jul-13 Apr-14 Jan-15 Oct-15 Jul-16 Apr-17 Jan-18 Oct-18

10-Year Treasury Yield

Fixed IncomeInterest rate “normalcy” close to being achieved – maybe the Fed can achieve a soft landing, but rising deficits may awaken the bond vigilantes.

Confidential & Proprietary

15

Source: Factset

Credit Over DurationSpreads continue to reflect the low default environment.

Confidential & Proprietary

16

0%

5%

10%

15%

20%

25%

Dec-97 Dec-99 Dec-01 Dec-03 Dec-05 Dec-07 Dec-09 Dec-11 Dec-13 Dec-15 Dec-17

U.S. High Yield Spread

ICE BofAML US High Yield - Spread - Option Adj Spread AverageSource: Factset

0

10

20

30

40

50

60

VIX (CBOE Volatility Index)

Volatility RisingHeightened volatility should be the norm in a Fed tightening cycle.

Confidential & Proprietary

17

Source: Factset

8x

10x

12x

14x

16x

18x

20x

Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17 Jan-18

Forward P/E Ratio of the S&P 500

S&P 500 - PE - NTM Average

Multiple ContractionEarnings will be key. They will be slower than 2018, but still positive. How positive? Mid to high single digits vs. mid to low could make a big difference in equity returns.

Confidential & Proprietary

18

Source: Factset

International EquitiesThe current U.S. / International equity cycle has lasted longer than previous cycles.

Confidential & Proprietary

19

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

Dec‐74 Dec‐77 Dec‐80 Dec‐83 Dec‐86 Dec‐89 Dec‐92 Dec‐95 Dec‐98 Dec‐01 Dec‐04 Dec‐07 Dec‐10 Dec‐13 Dec‐16

5-Y

ear

An

nu

aliz

ed R

etu

rns

U.S. Equities vs. Developed International Equities

Difference

U.S. Outperforming

Developed International Outperforming

Source: Morningstar Direct Notes: U.S. index is the S&P 500, Developed International index is the MSCI World ex USA

Emerging Market (EM) EquitiesThe dollar’s rise has been a headwind for emerging markets. The effect, however, is not uniform across EM countries.

Confidential & Proprietary

20

60

65

70

75

80

85

90

95

100

105

110100

105

110

115

120

125

130

135

Jan-14 May-14 Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17 May-17 Sep-17 Jan-18 May-18 Sep-18 Jan-19

Relative Performance of the MSCI EM/S&P 500 & The Dollar Index

Trade Weighted U.S. Dollar Index: Broad(reversed), rhs iShares MSCI Emerging Markets ETF Relative to iShares Core S&P 500 ETF (total return), lhs

Source: Factset, FRED

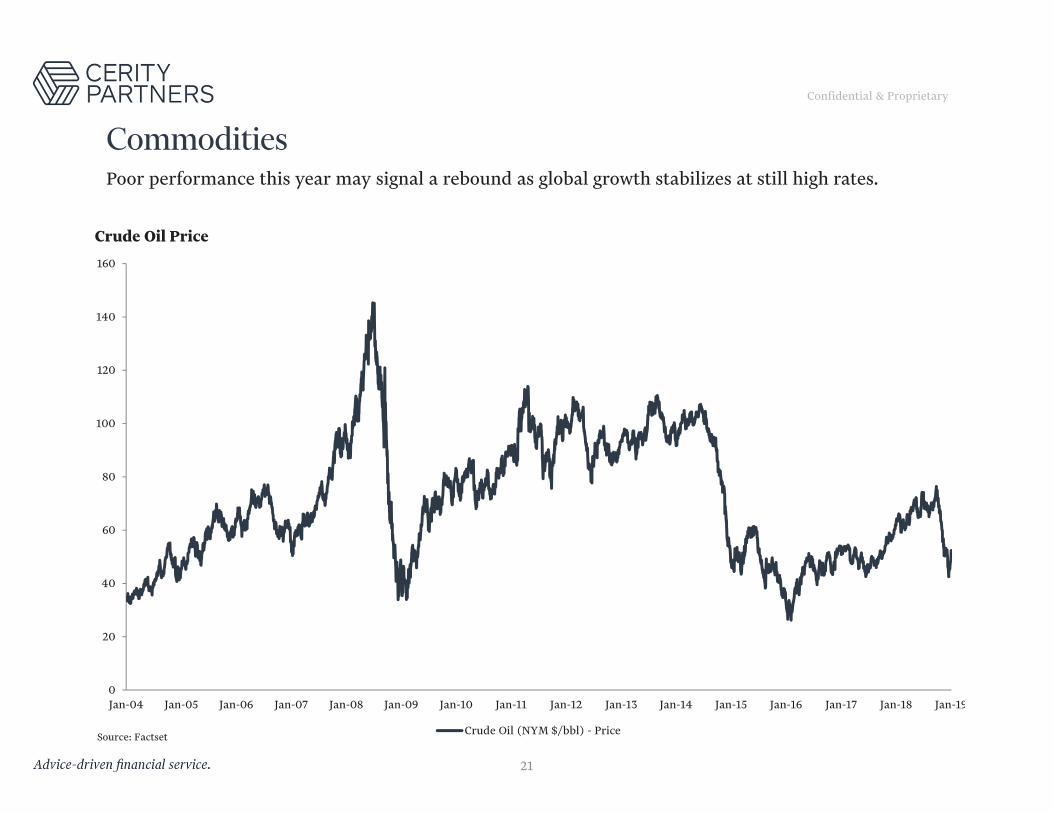

CommoditiesPoor performance this year may signal a rebound as global growth stabilizes at still high rates.

Confidential & Proprietary

21

0

20

40

60

80

100

120

140

160

Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17 Jan-18 Jan-19

Crude Oil Price

Crude Oil (NYM $/bbl) - PriceSource: Factset

Confidential & Proprietary

Important NotesCerity Partners LLC (“Cerity Partners”) is an SEC-registered investment adviser with offices in New York, Illinois, Ohio, Michigan and California. This commentaryis limited to general information about Cerity Partners’ services and its financial market outlook, which may not be suitable for everyone. The informationcontained herein should not be construed as personalized investment advice. Past performance is no guarantee of future results. There is no guarantee that theviews and opinions expressed in this brochure will come to pass. Investing in the financial markets involves risk, including the risk of loss of the principal amountinvested; and may not be appropriate for everyone. The information presented is subject to change without notice and should not be considered as an offer to sellor a solicitation of an offer to buy any security. All information is deemed reliable but is not guaranteed. For information pertaining to the registration status ofCerity Partners, please contact us or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov). For additional information about CerityPartners, including fees and services, send for our disclosure statement as set forth on Form ADV Part 2A using the contact information herein. Please read thedisclosure statement carefully before you invest or send money.

©2019 Cerity Partners LLC, an SEC-registered investment adviser. All Rights Reserved. (01/19)

22