2018 general rate case - southern california edison · 2018 general rate case transmission &...

TRANSCRIPT

Application No.: A.16-09- Exhibit No.: SCE-02, Vol. 9 Witnesses: C. Fanous

(U 338-E)

2018 General Rate Case

Transmission & Distribution (T&D) Volume 9 - Poles

Before the

Public Utilities Commission of the State of California

Rosemead, California

September 1, 2016

SUMMARY

This exhibit presents SCE’s requests for $44 million in O&M expenses for the 2018 Test Year

and $1,667 million in capital expenditures from 2016-2020.

Poles O&M Expenses 2018 Forecast

(Total Company – Constant 2015 $Millions)

This chapter describes SCE’s activities related to poles, which include:

1. Inspection and remediation of poles as part of the Pole Loading Program;

2. Inspection and remediation of poles as part of the Deteriorated Pole program; and

3. Other T&D activities such as Joint Pole credits and wood pole disposal.

Poles Capital Expenditures 2016-2020 Forecast

(CPUC-Jurisdictional Only – Nominal $Million)

SCE-02: Transmission & Distribution (T&D) Volume 9 - Poles

Table of Contents

Section Page Witness

-i-

SUMMARY OF POLE TESTIMONY ..............................................................1 C. Fanous

A. Overview ................................................................................................1

B. Comparison of Authorized 2015 to Recorded Costs .............................2

C. Summary of O&M Request ...................................................................5

D. Summary of Capital Request .................................................................6

E. Risk factors, Safety, Reliability .............................................................8

F. 2015 GRC Decision Requirements ........................................................8

POLE LOADING PROGRAM........................................................................10

A. Background ..........................................................................................10

B. Changes to Pole Loading Methodology ...............................................11

1. Overview of Changes and Expected Impact ............................11

2. SPIDACalc Selection Process ..................................................11

3. Identification of Areas for Improvement: Review of Software Performance After Deployment ...........................13

4. Technical Summary of Changes ..............................................14

5. Development and Implementation of Software Improvements ..........................................................................14

6. Recalculation Scope .................................................................15

7. Forecast Remediation rates ......................................................16

C. Pole Loading Program O&M Expenses ...............................................17

1. Pole Loading Program Assessment Variance Analysis....................................................................................17

2. Pole Loading Program Assessment Cost Forecast ...................19

3. Pole Loading Program Repair Variance Analysis ...................20

SCE-02: Transmission & Distribution (T&D) Volume 9 - Poles

Table of Contents (Cont.)

Section Page Witness

-ii-

4. Pole Loading Program Repair Cost Forecast ...........................21

5. Shareholder Costs ....................................................................22

D. Forecast Capital Expenditures .............................................................22

1. PLP-driven Pole Replacements ................................................22

2. Alternatives to Pole Replacement ............................................26

3. Coordination of Pole Replacements with Other Programmatic Work .................................................................27

4. Transformer Replacements, PLP Portion ................................27

5. Prefabrication, PLP Portion .....................................................28

DETERIORATED POLE PROGRAM ...........................................................30

A. Background ..........................................................................................30

B. Activity Description .............................................................................30

1. Replacements Driven by Program Inspections ........................30

2. Changes in the Intrusive Pole Inspection Program Standards ..................................................................................31

3. Restoration (steel stubbing) .....................................................34

4. Inspection-driven Replacements ..............................................35

5. Replacements Driven by Non-Programmatic Activities ..................................................................................37

6. Replacements Driven by Pole Loading Calculation Failures .....................................................................................39

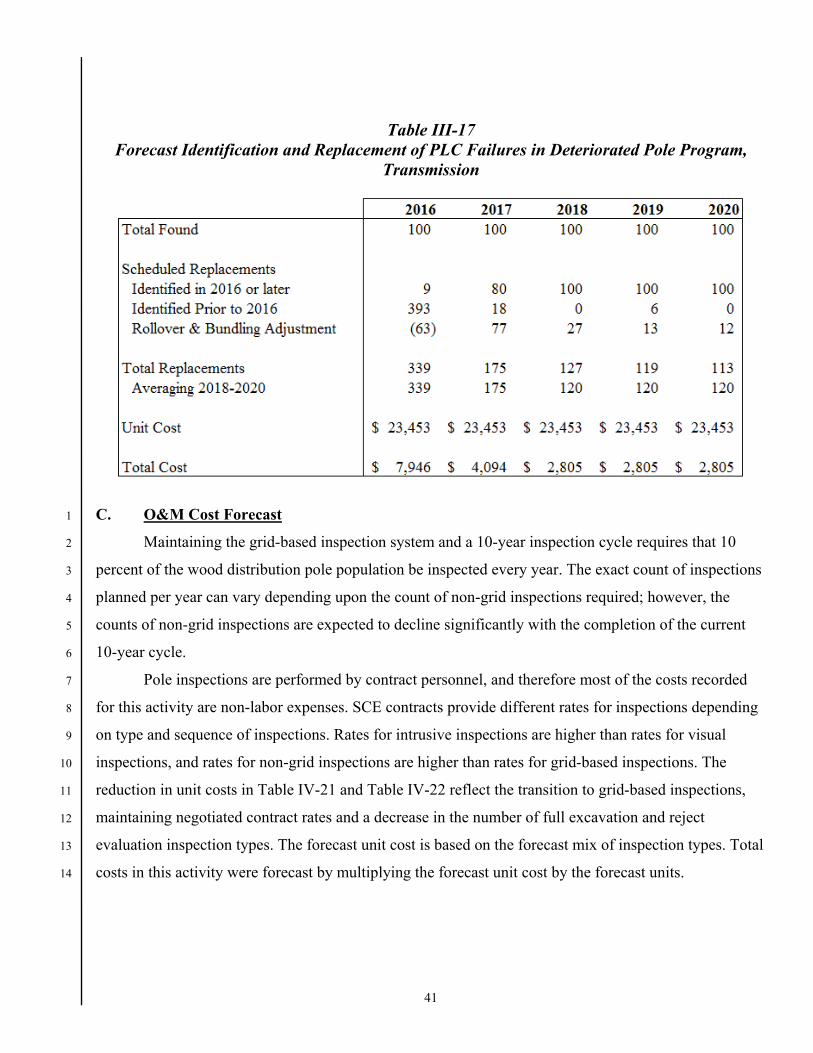

C. O&M Cost Forecast .............................................................................41

D. Deteriorated Pole Capital Replacements .............................................43

POLE CAPITAL REMEDIATION UNIT COSTS .........................................45

A. Pole Replacement Unit Cost Summary ................................................45

SCE-02: Transmission & Distribution (T&D) Volume 9 - Poles

Table of Contents (Cont.)

Section Page Witness

-iii-

B. Unit Cost Variance Analysis ................................................................46

1. Distribution Pole Unit Cost Analysis .......................................46

2. Transmission Pole Unit Cost Analysis ....................................49

C. Unit Cost Forecast Development .........................................................50

1. Distribution Pole Unit Cost Forecast .......................................50

2. Transmission Pole Unit Cost Forecast .....................................51

3. Steel Stubbing ..........................................................................52

4. Summary of Unit Cost Forecasts .............................................53

5. Ongoing Efforts to Reduce Unit Costs ....................................53

JOINT POLE ORGANIZATION AND ACTIVITY COST FORECASTS ...................................................................................................55

A. Overview of Joint Use .........................................................................55

B. General Discussion of Cost Sharing with Joint Owners and Renters .................................................................................................56

1. Cost Recovery from Joint Owners ...........................................59

2. Cost Recovery from Renters ....................................................64

3. Evaluation of Current Cost Recovery Practices .......................64

C. Joint Pole O&M Credits.......................................................................68

D. Joint Pole Organization (JPO) Expenses, Portion of FERC Account 583.125 ..................................................................................69

1. Joint Pole Organization Cost Forecast .....................................70

E. Joint Pole Capital Credits.....................................................................71

1. Credit Forecast .........................................................................71

OTHER POLE RELATED ACTIVITIES .......................................................75

SCE-02: Transmission & Distribution (T&D) Volume 9 - Poles

Table of Contents (Cont.)

Section Page Witness

-iv-

A. Wood Pole Disposal .............................................................................75

1. Cost Forecast ............................................................................75

B. Pole Related Expense ...........................................................................78

CONTINUATION OF THE POLE LOADING AND DETERIORATED POLE PROGRAMS BALANCING ACCOUNT ......................................................................................................79

SUMMARY OF GRC ACCOUNTS ...............................................................80

A. GRC Account 566.125 .........................................................................80

B. GRC Account 571.125 .........................................................................81

C. GRC Account 583.125 .........................................................................82

D. GRC Account 593.125 .........................................................................83

1

1

SUMMARY OF POLE TESTIMONY 2

A. Overview 3

This volume will cover SCE’s proposals for Pole related activities. This includes the 4

Deteriorated Pole Program, which inspects and remediates poles in compliance with General Order 165 5

(GO 165). It also includes the Pole Loading Program (PLP). The Pole Loading Program is an inspection 6

and remediation program that identifies poles for repair or replacement that do not meet safety factor 7

requirements of General Order 95 and SCE’s internal design and construction standards, including wind 8

loading in high wind areas of our service territory. This volume also covers other pole expenditures 9

primarily related to the overall activities within T&D such as Joint Pole credits and wood pole disposal 10

costs. 11

The pole programs at SCE address major safety and reliability risks, and compliance 12

requirements. While the Deteriorated Pole program has been active since 1997, the Pole Loading 13

Program was only initiated in 2014, and adopted in SCE’s 2015 GRC. There have been notable 14

enhancements in our pole programs since the 2015 GRC. In 2013, SCE engaged an experienced 15

meteorological engineering firm to perform a system-wide wind study based on a scientific evaluation of 16

historical wind events. The result of this wind study is that SCE added a new 24 pounds per square foot 17

wind loading specification in certain areas and the wind loading criteria in many other areas was 18

increased. The revised wind loadings were implemented in March 2014. Furthermore, we have updated 19

the remediation criteria for deteriorated poles, and leveraged the risk evaluation framework described in 20

SCE-02, Volume 1, in evaluating those criteria. SCE also enhanced the pole loading assessment 21

methodology, and evaluated alternatives to pole replacement to strengthen poles. 22

This testimony describes the impact of these changes on the scope and cost of the programs as 23

follows: 24

Section II outlines changes to the Pole Loading Program methodology, and forecasts 25

expenses and capital expenditures based on those changes 26

Section III describes updated remediation criteria for the Deteriorated Pole Program, and 27

forecasts expenses and capital expenditures based on those new criteria 28

Section IV provides a detailed analysis of historical and forecast trends in unit costs 29

utilized in Pole Loading Program and Deteriorated Pole Program forecasts, including 30

improvements driven by alternative remediations and other efficiencies 31

2

Sections V and VI describe forecasts associated with the Joint Pole Organization and 1

other activities 2

Sections VII and VIII discuss SCE’s proposal to continue balancing account treatment for 3

the Pole Loading Program and Deteriorated Pole Program, and summarizes O&M 4

expenses presented in this volume 5

B. Comparison of Authorized 2015 to Recorded Costs 6

This section compares the amounts authorized by the Commission in the 2015 GRC to 2015 7

recorded O&M and Capital spend. 8

Figure I-1 Poles1

2015 GRC Authorized Variance Summary 2015 O&M (Total Company - Constant 2015 $Millions)

1 Refer to WP SCE-02, Vol. 9, pp. 82-83 (O&M Authorized vs. Recorded).

($11)

($7)($2)

$3

$50

$46

$28

0

10

20

30

40

50

60

2015 Request 2015 Authorized Assessments Repairs & RelatedExpense

InstrusiveInspections

Joint Pole 2015 Recorded

Joint Pole Intrusive Inspections Repairs & Related Expense Assessments

3

SCE performed approximately 63,0002 fewer assessments than originally forecasted for the Pole 1

Loading Program in 2015, which led to significantly fewer repairs. Furthermore, the repair rate was less 2

than the 3% forecast in the 2015 GRC. Also, there was a delay in completing repairs as discussed in 3

Section III.B.6. Lastly, $1.8 million associated with planning the PLP remediation work that was 4

forecast as O&M expense in the 2015 GRC was later determined to be a planning activity and therefore 5

not recorded to expense in 2015. The combined impact of fewer assessments and fewer repairs drove the 6

majority of the variance between authorized and recorded expense. 7

2 205,754 forecast for 2015 (SCE-03, Vol. 06, Part 2 – 2015 GRC testimony), compared to 142,382 performed,

a difference of 63,372. Furthermore, a portion of the spending was funded by shareholders as discussed in Section II.C.5. Therefore, those costs are not shown in the recorded costs.

4

Figure I-2 Pole Replacement3

2015 GRC Authorized Variance Summary4 2015 Capital (CPUC-Jurisdictional – Nominal $Millions)

SCE’s 2015 recorded programmatic pole replacement volumes closely matched the forecast. 1

However, transmission pole replacements represented a larger percentage of the total replacements than 2

anticipated.5 This increased the recorded costs. In addition, both transmission and distribution pole 3

replacement unit costs increased relative to forecasts, which also led to an increase in recorded costs. 4

The mix of replacements under the Deteriorated Pole Program and Pole Loading Program also 5

differed from the forecast for each program (Table I-1). Pole loading replacements were less than the 6

forecast due to fewer assessments being completed. Deteriorated pole replacements increased relative to 7

3 Refer to WP SCE-02, Vol. 9, pp. 84-85 (Capital Authorized vs. Recorded). 4 Includes expenditures associated with the Aged Pole program. 5 This was primarily due to an increase in intrusive inspection failure rates as discussed in Section III.B.2.

($82) ($3)

$320

$1

$465

$337

$573

-100

0

100

200

300

400

500

600

700

2015 Request 2015Authorized

DeterioratedPole

Replacements

PLP PoleReplacements

Joint PoleCredits

Other 2015Recorded

Other Joint Pole Credits PLP Pole Replacements Deteriorated Pole Replacements

5

forecasts. The majority of the variance was driven by pole replacements originally scheduled for 2016 1

that were shifted into 2015 scope due to operational circumstances. These drivers are discussed in more 2

detail in the related sections of testimony that follow. 3

Table I-16 Total Programmatic Pole Replacements, Forecast vs. Recorded

C. Summary of O&M Request 4

Table I-2 Pole O&M Activities

(Total Company – Constant 2015 $000)

6 These unit counts exclude replacements associated with the Aged Pole program.

2013 2014 2015Total, 2013-

152015 GRC Forecast Replacements

PLP 3,000 25,000 28,000 Det Pole 7,500 7,600 8,102 23,202 Total, All Programs 7,500 10,600 33,102 51,202

Recorded ReplacementsPLP - 299 10,690 10,989 Det Pole 12,251 14,065 23,198 49,514 Total, All Programs 12,251 14,364 33,888 60,503

Forecast vs. Recorded VariancePLP - (2,701) (14,310) (17,011) Det Pole 4,751 6,465 15,096 26,312 Total Variance 4,751 3,764 786 9,301

Activity 2018 ForecastPole Loading Program Assessments $24,407Pole Loading Program Related Expense $2,601Pole Loading Program Repairs $5,474Intrusive Pole Inspections $5,668Joint Pole Credits -$3,140Joint Pole Organization $8,548

Total $43,559

6

D. Summary of Capital Request 1

Table I-3 Pole Capital Activities

(Total Company – Nominal $000)

Description WBS/Activity Group 2016 2017 2018 2019 2020Pole Loading Distribution Pole Replacements

CET-PD-IR-PD 106,353 112,368 119,731 123,488 127,414

Pole Loading Transmission Pole Replacements

CET-PD-IR-PT 8,808 16,116 24,628 25,277 25,940

Transformer Capital Expenditures, PLP Portion

CET-PD-OT-TR 4,804 5,360 6,024 6,213 6,411

Prefabrication Capital Expenditures, PLP Portion

CET-PD-OT-PF-PL 3,260 3,638 4,088 4,217 4,351

Distribution Deteriorated Pole Replacement and Restoration

CET-PD-IR-DP 219,123 193,402 177,355 184,746 190,804

Transmission Deteriorated Pole Replacement and Restoration

CET-PD-IR-TR 82,748 76,451 64,362 66,482 68,224

Pole Capital Savings CET-OT-OT-OX (4,002) (19,837) (21,133) (21,663) (22,527)

Joint Pole Capital Credit, Distribution

CET-PD-CR-JD (54,417) (51,615) (50,766) (52,799) (47,469)

Joint Pole Capital Credit, Transmission

CET-PD-CR-JT (9,900) (10,133) (9,846) (10,179) (9,087)

Wood Pole Disposal CET-PD-OT-WP 3,743 3,612 3,548 3,660 3,776

$360,521 $329,362 $317,992 $329,441 $347,837Total

7

Table I-4 Pole Capital Activities

(CPUC-Jurisdictional – Nominal $000)

Table I-5 Summary of Forecast and Recorded Pole Replacement Counts7

7 These counts exclude replacements associated with the Aged Pole program and steel stubbing.

Description WBS/Activity Group 2016 2017 2018 2019 2020Pole Loading Distribution Pole Replacements

CET-PD-IR-PD 106,353 112,368 119,731 123,488 127,414

Pole Loading Transmission Pole Replacements

CET-PD-IR-PT 8,104 14,828 24,351 24,992 25,647

Transformer Capital Expenditures, PLP Portion

CET-PD-OT-TR 4,804 5,360 6,024 6,213 6,411

Prefabrication Capital Expenditures, PLP Portion

CET-PD-OT-PF-PL 3,260 3,638 4,088 4,217 4,351

Distribution Deteriorated Pole Replacement and Restoration

CET-PD-IR-DP 219,123 193,402 177,355 184,746 190,804

Transmission Deteriorated Pole Replacement and Restoration

CET-PD-IR-TR 76,135 70,341 63,636 65,732 67,455

Pole Capital Savings CET-OT-OT-OX (4,002) (19,837) (21,133) (21,663) (22,527)

Joint Pole Capital Credit, Distribution

CET-PD-CR-JD (54,417) (51,615) (50,766) (52,799) (47,469)

Joint Pole Capital Credit, Transmission

CET-PD-CR-JT (9,900) (10,133) (9,846) (10,179) (9,087)

Wood Pole Disposal CET-PD-OT-WP 3,743 3,612 3,548 3,660 3,776

$353,204 $321,964 $316,988 $328,406 $346,774Total

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020Deteriorated Poles

Distribution Replacements 7,715 7,972 11,092 11,050 19,395 14,206 12,177 10,791 10,791 10,791 Transmission Replacements 684 822 1,159 3,015 3,803 3,481 3,133 2,558 2,558 2,558 Deteriorated Pole Total 8,399 8,794 12,251 14,065 23,198 17,686 16,030 14,957 15,821 15,896

Pole LoadingDistribution Replacements 295 10,317 6,853 7,060 7,342 7,342 7,342 Transmission Replacements 4 373 370 663 989 989 989 Pole Loading Total 299 10,690 7,224 7,723 8,331 8,331 8,331

Total Poles Mitigated 8,399 8,794 12,251 14,364 33,888 24,910 23,033 21,680 21,680 21,680 Total Distribution Poles 7,715 7,972 11,092 11,345 29,712 21,059 19,237 18,133 18,133 18,133 Total Transmission Poles 684 822 1,159 3,019 4,176 3,851 3,796 3,547 3,547 3,547

Recorded Forecast

8

E. Risk factors, Safety, Reliability 1

As discussed in SCE-01, SCE continues to improve and use risk-informed planning to identify, 2

assess, and prioritize risks; identify and evaluate ways to mitigate risk; and help develop spending plans 3

to support risk mitigation. As part of this effort, and consistent with the Commission’s direction in the 4

Safety Model Assessment Proceeding (S-MAP),8 SCE has conducted detailed analyses to incorporate a 5

risk-informed approach in evaluating pole program activities. 6

The risk modeling framework developed for pole programs and the degree to which this analysis 7

influenced operational decisions related to pole programs is discussed in SCE-02 Volume 1 on 8

Operational Overview and Risk-Informed Decision Making. 9

F. 2015 GRC Decision Requirements 10

The Commission adopted SCE’s proposed pole related programs and costs with some 11

modifications in D.15-11-021. The Commission expressed some concerns that SCE had not fully 12

evaluated all of the options available on remediating poles, and needed to do more work on the recovery 13

of costs from the other owners of jointly-owned poles and companies that rent space on poles. The 14

Commission set some requirements that SCE must meet in the 2018 GRC. 15

1. SCE will provide a review of its efforts on recovery of costs from other companies that 16

either jointly own or rent space on poles that must be replaced or repaired. (See V.B 17

below.) 18

2. SCE will provide information on the number of jointly owned poles, the number of pole 19

renters (See V.A below), and describe the arrangements for cost sharing with other 20

parties. (See V.B below) 21

3. SCE will provide additional analysis on options to remediate overloaded poles in ways 22

other than repair or replace, and will specifically address the issues of removing 23

attachments, strengthening poles, and increasing the recovery of costs from pole users 24

(See II.D.2, III.B.2, IV.C.5 and V.B below). 25

4. SCE will address unauthorized attachments by providing quantitative information and 26

describing their efforts to minimize their impact. (See V.C below.) 27

8 D.14-12-025. Decision Incorporating a Risk-Based Decision-Making Framework into the Rate Case Plan and

Modifying Appendix A of Decision 07-07-004.

9

5. If SCE believes a Commission proceeding is needed to address issues raised by joint 1

ownership and renters, SCE need not wait for its next GRC.9 (See V.B.3 below.) 2

On April 28, 2016, the Commission held an En Banc to discuss a variety of issues related to 3

poles, including those raised in (5) above. 4

Included in the 2015 GRC was an SCE proposal to systematically replace older poles. This 5

program, called the Aged Pole program, was designed to transition and prepare the company to the 6

greater level of annual pole replacements we were forecasting. The Commission partially accepted our 7

proposal, but determined that the Company had not fully evaluated other alternatives, and disallowed 8

part of our spending for the years 2014 and 2015.10 SCE’s proposal on this previous disallowance for the 9

2018 GRC is addressed in SCE-09, Volume 2 by Mr. Gunn. 10

As part of its implementing advice letter for the 2015 GRC decision, SCE included a section 11

providing a definition of the Pole Loading and Deteriorated Pole Balancing account, Part J of the 12

Preliminary Statement. This included a reporting requirement for SCE’s 2018 GRC filing, to provide 13

recorded information on spending for the Deteriorated Pole and Pole Loading programs, and information 14

on the number of repairs made and poles replaced. This information is provided in various sections of 15

this testimony.16

9 D.15-11-021, p. 104, 137; Ordering Paragraph 9. 10 D.15-11-021, p. 113, Conclusion of Law 57.

10

1

POLE LOADING PROGRAM 2

A. Background 3

The Pole Loading Program (PLP) was adopted in the 2015 General Rate Case as a 4

comprehensive way to address pole overloading issues.11 The program assesses T&D’s poles12 to 5

identify and repair or replace those poles that do not meet G.O. 95 minimum safety factors or, to the 6

extent higher, SCE’s internal safety standards. PLP assessments began in January 2014, with the initial 7

focus on highest-risk areas including high fire regions.13 SCE expects to complete assessments in high 8

fire areas in 2017. The pole remediation phase is expected to continue for 12 years until 2025. Under 9

PLP, a pole will be replaced between 72 hours and 59 months depending on the safety factor and its 10

location relative to high fire areas. On a small percentage of poles, the pole can be made compliant by 11

installing or redesigning a “down guy.”14 12

The main risk associated with poles that do not meet minimum safety factor requirements is that 13

they may break or fail at wind loads below the minimum design wind loads for that geographic location, 14

resulting in an increased risk to public safety and system reliability. 15

SCE’s design and construction standards require that newly constructed poles meet the safety 16

factors specified in G.O. 95 at the time of installation, in addition to any SCE internal design standards 17

that may exceed minimum regulatory requirements. SCE’s internal standards also require that a pole 18

loading calculation be performed whenever equipment is attached or modified that will materially 19

increase the loading on the pole.15 SCE’s facilities are designed and constructed to meet the standards 20

applicable at the time of installation. 21

11 G.O. 95 requires that utility poles maintain a certain safety factor. This safety factor calculation is called “pole

loading.” 12 PLP will include all wood, light duty steel, and other non-engineered structures. Engineered steel poles and

transmission towers are excluded. 13 SCE has defined the high fire regions to exceed the areas defined by the Commission in D.09-08-029 and

D.12-01-032, which adopted, on an interim basis, the CalFire FRAP map “extreme” and “very high” fire threat zones for Southern California.

14 A down guy is a guy wire anchored to the ground. 15 CPUC General Order 95, Rule 44.2 defines a material increase as follows: “a material increase in load is an

addition which increases the load on a structure by more than five percent per installation, or ten percent over a 12-month span, of the electric utility’s or Communication Infrastructure Provider’s current load.”

11

B. Changes to Pole Loading Methodology 1

1. Overview of Changes and Expected Impact 2

SCE began using SPIDACalc as the enterprise-wide tool to calculate pole loading safety 3

factors for its poles in April of 2013. In December of 2014, SCE engineering identified some potential 4

improvement areas in SPIDACalc’s safety factor calculation methodology to increase its accuracy while 5

maintaining compliance with safety factors.16 SCE worked with the software provider to develop the 6

scope of the improvements, which were first incorporated into the SPIDACalc software in May of 2015 7

and fully deployed in the production version of the improved software in November of 2015. The 8

changes enabled SPIDACalc to more accurately model poles in the field, and as a result significantly 9

reduced the rate at which poles fail pole loading calculations. SCE’s initial estimates suggested that 10

remediation rates will be approximately 9%17 compared to the overall remediation rate of approximately 11

22% (3% requiring repair and 19% requiring replacement) forecast in 2015 GRC testimony.18 SCE met 12

with the Commission staff to discuss this impact on April 19, 2016, and also discussed the impact of the 13

change at the Pole En Banc held on April 28, 2016. 14

When SCE understood the impact of this software release in late August of 2015, SCE 15

instructed its pole loading contractor to hold all work not already provided to SCE starting on September 16

1, 2015, so it could be reassessed using the new version of the software. In addition, SCE reassessed all 17

poles at “Gate 1” of the planning and execution process: poles identified for replacement that had not yet 18

been released to design. The reassessment was later expanded to poles in various stages of planning and 19

design. As of March of 2016, the recalculation effort included approximately 40,000 poles, as discussed 20

at the April 19, 2016 meeting with Safety and Enforcement Division.19 21

The technical details of the changes and timeline of the development and deployment 22

process are summarized below. 23

2. SPIDACalc Selection Process 24

The changes described above are SCE’s latest improvements to pole loading methods and 25

processes driven by evolving GO 95 requirements. In August of 2009, D.09-08-029 ordered that pole 26

loading be performed whenever adding facilities could materially increase load, and added a 27

16 Throughout this volume, when the term compliance is used with respect to pole loading safety factors,

compliance refers to compliance with General Order 95 and SCE internal pole loading standards. 17 Refer to WP SCE-02, Vol. 9, pp. 86-87 (August_2015_SCE_SPIDACalc_Impact_Assessment). 18 Refer to WP SCE-02, Vol. 9, pp. 88-104 (2013 SCE Pole Loading Study). 19 Refer to WP SCE-02, Vol. 9, pp. 105-119 (2016-04-19 SED Briefing).

12

requirement that pole load calculations be retained for ten years. In January of 2012, D.12-01-032 1

further increased the record retention requirement for pole load calculations to the life of the structure. 2

SCE initiated the Pole Loading Application Replacement (PoLAR) initiative in 2012 to identify a pole 3

loading software solution that could meet these requirements in a production environment, in which 4

planners would perform a large volume of pole loading calculations. 5

As described in SCE’s 2015 GRC testimony, Wind Load Estimator was deployed in 2001 6

to automate the hand calculation of bending moment at the ground line as described in Appendix F of 7

GO95, and to enable the calculation of safety factors for guy wires.20 While this improved upon the 8

engineering tables previously used, there were scenarios where such methods could not accurately 9

calculate safety factors. SCE sought a replacement for the Wind Load Estimator tool which employed 10

modern calculation techniques, considered safety factors not only at the ground line but also along the 11

entire length of the pole, and came pre-configured with SCE poles, arms, wires, and equipment to enable 12

planners to quickly and accurately perform pole loading analyses. 13

The volume and nature of SCE’s work requires a software package and platform simple 14

enough to be used by non-engineers, capable of hundreds of concurrent users, and robust enough to 15

identify noncompliant poles with high confidence. These requirements necessitated trade-offs that are 16

incorporated into these software packages. To reduce the risk of not identifying noncompliant poles, 17

these software packages use conservative assumptions while requiring less technical sophistication from 18

the operator. 19

Several software packages were evaluated in a Request for Proposal (RFP) process, 20

which detailed technical, business, and integration requirements to continue to meet GO requirements. 21

These packages included SPIDACalc, O-Calc, and PLS-CADD/LITE. The technical requirements of the 22

RFP included the performance of pole loading calculations in various scenarios, including bending, 23

buckling, incorporating pole damage, guying, and varying pole types. In its initial evaluation of software 24

packages identified in its RFP process, SCE determined that SPIDACalc provided the best balance 25

among accuracy, simplicity, and conservatism. SCE selected the SPIDACalc software package and 26

began its utilization in April of 2013. SCE requested cost recovery for purchasing and deploying 27

SPIDACalc in its 2015 GRC testimony,21 and the request was authorized in D.15-11-021. 28

20 SCE-03, Vol. 06, Part 2, p. 5 (2015 GRC). 21 SCE-05, Vol. 02, Part 2 (2015 GRC).

13

3. Identification of Areas for Improvement: Review of Software Performance After 1

Deployment 2

In 2014, SCE planners noted that sometimes SPIDACalc called for larger pole sizes than 3

planners were anticipating to meet minimum safety factor requirements. However, the wind study 4

implemented in March 2014 updated and expanded the boundaries of high-wind areas throughout SCE’s 5

service territory, and introduced new, higher wind loading specifications, which also affected safety 6

factors and pole sizes. This made it difficult to isolate the impact due to the use of SPIDA. In July 2014, 7

SCE engineers began to evaluate how SPIDACalc handled the design situations in which these results 8

were obtained. The review included a detailed re-assessment of pole types representing a variety of 9

configurations, including those associated with the unexpected SPIDACalc results. SCE engineers 10

developed models of these poles using the full engineering version of PLS-CADD, rather than PLS-11

CADD/LITE tested in the original RFP. PLS-CADD required additional field measurements and a much 12

longer model development process, which could take an engineer 1 to 2 days per pole compared to less 13

than an hour for a planner using SPIDACalc. 14

The engineering version of PLS-CADD was not considered in the RFP because it was not 15

suitable for performing large volumes of assessments by planners. In addition, all the software packages 16

considered used broadly similar assumptions, which are described in the following section. These 17

assumptions were considered appropriate by the industry for performing pole loading assessments. Since 18

SCE sought to evaluate the impact of these common assumptions, a standard engineering tool such as 19

PLS-CADD had to provide a basis for comparison. 20

When summarized in December of 2014, the evaluation determined that SPIDACalc 21

calculated a lower safety factor in some of the analyzed poles examined when benchmarked against the 22

full engineering version of PLS-CADD. These results reflected conservative assumptions of the 23

software, as discussed below. As a result of these findings, SCE encouraged SPIDA to incorporate 24

enhancements recommended by SCE into the SPIDACalc upgrade and release cycle. While these 25

changes were expected to impact reject rates and pole classes22 required in certain situations, the general 26

prevalence of these configurations in SCE’s system was not well understood, and the overall impact of 27

the changes on the program was not yet clear. 28

22 Pole sizes are categorized by the pole “class,” which is determined by a pole’s circumference at the base and

top.

14

4. Technical Summary of Changes 1

From its initial deployment in April 2013 through November 2015, SPIDACalc used a 2

pole loading methodology similar to that implemented in comparable software packages. These options 3

surpass the hand-calculation methods shown in GO 95 Appendix F in terms of accuracy, ease of use, 4

and speed. However, in certain circumstances each incorporated conservative assumptions regarding the 5

role of wire tension in balancing the forces exerted on poles. 6

Improvements to SPIDACalc include the integration of geometric nonlinear modeling, 7

displacement-based loading, dynamic wire tensions, and the supporting data needed to enable these 8

capabilities. Together these improvements represent a significant increase in sophistication relative to 9

the software packages considered during the original RFP process. A more technical description of the 10

effect of wire tension on the pole and the changes that were made to more accurately model the pole is 11

in included in workpapers.23 12

5. Development and Implementation of Software Improvements 13

Every software change requires a development and testing process to confirm accuracy, 14

adequate performance, and integration with back-end systems of record. This process is described in this 15

section. Based on the findings of the engineering study, SCE worked with the SPIDA company from 16

December 2014 through the end of March 2015 to develop improvements that would increase the 17

accuracy of the model in these design situations. In April 2015, a test version of SPIDACalc was 18

provided for re-evaluation of the poles used in the initial engineering study. SCE Engineering 19

determined that the software still required additional development to correctly model what are called 20

dynamic wire tensions. Additionally, the database of equipment characteristics used to build models, 21

called a “client file,” was updated to improve the accuracy of equipment characteristics represented in 22

the models.24 In May of 2015, the initial delivery of dynamic wire tensions for the most common SCE 23

conductors were provided to the SPIDA company, and work began on compiling dynamic tension 24

values for telecom and cable TV spans. 25

Two improvements were incorporated in SPIDACalc Version 6.0, which was released on 26

May 21, 2015, to more accurately model the effect of wire tension on the pole. The new capabilities 27

became available not only to SCE but to other utilities that employed SPIDACalc software for pole 28

23 Refer to WP SCE-02, Vol. 9, pp. 120-122 (Technical Summary of SPIDACalc Changes). 24 In order to fully update the tensions in the client file, Engineering had to set up and run a tension calculation

program approximately 6,000 times.

15

loading. However, the dynamic tension data for communication company wires and some SCE wires 1

was not yet complete, so these improvements could not yet be used in the production version of the 2

software. This majority of the data was compiled and provided to SPIDA in June 2015. The data was 3

also provided to SCE’s assessment vendor so that they could determine the level of effort required to 4

adopt the new client file. The final data was delivered to SPIDA early August 2015. SPIDA then 5

configured the data so that it could be used in SPIDACalc, and then provided the configured data to the 6

assessment vendor so that the assessment vendor could make necessary updates in its systems. 7

In July 2015, testing of the software determined that reject rates would drop when the 8

new version was deployed. Accordingly, in August 2015, SCE performed an assessment of 9

approximately 1,400 poles, which suggested that reject rates with the new software and client file may 10

be approximately 9%.25 Testing of the new capabilities and the required client file also revealed 11

significant performance impacts: sometimes, a calculation that previously could have been completed in 12

less than four minutes would take more than an hour to complete. 13

SCE sought to balance the benefit of lower remediation rates against the risk of delaying 14

the identification and remediation of poles with noncompliant safety factors, and impeding the design 15

process and delaying other maintenance and infrastructure replacement work that required a pole 16

loading assessment. SPIDACalc assessments were necessary not only for the PLP program, but for any 17

maintenance or infrastructure replacement activity in any program that would materially impact the load 18

on a pole. For these reasons, SCE decided on August 8, 2015 to delay implementation of the client file 19

until performance issues could be addressed. An improved version of SPIDACalc which addressed these 20

issues was approved on October 27, 2015, and became effective on November 19, 2015. 21

6. Recalculation Scope 22

While performance issues were being addressed, SCE determined that the benefit of 23

reduced remediation rates would justify reassessing certain in-progress poles when the updated 24

SPIDACalc version was ready for deployment. SCE began by instructing the PLP assessment vendor to 25

hold all poles assessed, and placed poles identified as rejects not yet released to design (Gate 1 – see 26

Table II-6 for gate definitions) as of September 1, 2015, in the queue for reassessment when the new 27

SPIDACalc became available. On December 31, 2015, SCE added poles released to design (Gate 2) to 28

the queue, and on March 7, 2016, poles in various stages of design and review prior to being released to 29

25 Refer to WP SCE-02, Vol. 9, pp. 86-87 (August 2015 SCE SPIDACalc Impact Assessment).

16

construction (Gates 3 and 4) were added. As of March 2016, approximately 40,000 pole replacements 1

were included in the recalculation effort.26 2

Table II-6 Summary of Pole Gate Movement

7. Forecast Remediation rates 3

Initial reassessments on approximately 1,400 poles compiled in August 2015 suggested 4

that assessment reject rates could fall to approximately 9%.27 This assessment is the basis for SCE 5

forecasts in this GRC. 6

26 In addition, approximately 2,600 down guys with noncompliant safety factors were included in the

recalculation effort. 27 Refer to WP SCE-02, Vol. 9, pp. 86-87 (August 2015 SCE SPIDACalc Impact Assessment).

• Poles identified for repair or replacement, poles are grouped and work order number is assigned

Gate 1

Identified for Remediation

• Poles assigned to design resourceGate 2

Released for Design

• Work orders in approval process, design completed, Joint Pole Agreements initiated, environmental, rights checks/railroad request submitted

Gate 3

Design Approval

• Work orders approved and pending release to construction based on all constraints being cleared

Gate 4

Pole Program Clearance

• Work scope is assigned to construction resources and in scheduling process for final execution

Gate 5

Released to Construction

• Pole is installed in field and considered “used and useful”

Gate 6

Installation

17

C. Pole Loading Program O&M Expenses 1

PLP operating expenses are composed of pole assessment cost and pole repair costs. Pole 2

loading assessments are performed to determine a pole’s safety factor. Pole loading assessments require 3

a field assessment and a desktop analysis to calculate each pole’s safety factor. Inputs include the 4

physical attributes of the pole, its attachments, and local weather conditions. The field assessment 5

measures or validates the pole’s attributes (such as species and type) and the size and equipment it 6

supports. Collecting the data to perform a pole loading calculation requires an experienced field 7

assessor. The field assessor must be able to access poles throughout SCE’s service territory, including 8

those in remote terrain and other difficult to access locations, such as customer backyards, in order to 9

take accurate measurements. Assessors must be close enough to the pole to measure the ground line 10

circumference and have sufficient room around the pole to measure attachment heights and span lengths. 11

Photographs are also taken of each pole. The desktop analysis uses SPIDACalc to calculate the pole’s 12

safety factor. 13

1. Pole Loading Program Assessment Variance Analysis 14

Table II-7 shows the historical cost and number of assessments completed in 2014 and 15

2015. These volumes are somewhat lower than SCE’s forecast in its 2015 GRC (A.12-11-003). When 16

the forecast was made in early 2013, SCE was in the early stages of planning the program. The forecast 17

had called for 205,000 assessments per year for 7 years beginning in 2014. SCE began the Pole Loading 18

Program in January 2014 and continued ramping up the volume throughout the year. Due to the time to 19

ramp up resources, SCE completed 184,461 assessments in 2014.28 20

In 2015, SCE considered extending the seven-year assessment plan and temporarily 21

adjusted its target assessment rate. SCE considered the challenges of the rapid ramp-up and the 22

regulatory uncertainty associated with SED’s29 and ORA’s30 support for a 10-year assessment plan. In 23

addition, SCE weighed the relative risk impact of extending the assessment timeframe for lower-risk 24

poles while maintaining a shorter timeframe for higher-risk poles.31 In 2015, SCE completed 142,519 25

28 7,252 of the 184,461 assessments were completed under SCE’s Settlement of the Malibu Fire OII as

shareholder-funded work. Therefore, those costs are not shown in the recorded costs of this volume. 29 Refer to WP SCE-02, Vol. 9, pp. 123-126 (SED Letter RE: D.12-11-051, OP 17 and 18). 30 See A.13-11-003 Exhibit ORA-08, page 31. 31 SCE-19, Vol. 06, Pt. 2, page 4 (2015 GRC, Rebuttal Testimony).

18

assessments – an assessment level consistent with a 10-year timeframe.32 When the 2015 GRC decision 1

was issued in November 2015 authorizing a seven year timeframe, SCE revised its assessment forecast. 2

As detailed in Table II-7, SCE intends to complete 200,000 assessments in 2016, 220,000 in 2017 and 3

230,000 in 2018. 4

Pole assessments are performed by contract personnel. Therefore, most of the costs 5

recorded for this activity are non-labor expenses. The cost per assessment has stayed relatively constant 6

throughout the recorded period and is expected to stay constant throughout the forecast period. 7

32 1,338 and 34,758 of the 142,519 were completed under the Malibu and San Gabriel Windstorm Settlements,

respectively as shareholder-funded work. Therefore, those costs are not shown in the recorded costs of this volume.

19

Table II-7 Pole Loading Program Assessments33,34

Portions of GRC Account 566.125 and 583.125 Recorded and Adjusted 2011-2015/Forecast 2016-201835

(Constant 2015 $000)

2. Pole Loading Program Assessment Cost Forecast 1

Pole loading assessments under PLP are primarily driven by contract costs of vendors 2

conducting the assessments; a smaller amount of SCE labor cost is included for the assessment staff. 3

The assessment staff works with the vendor, manages the data exchange between the vendor and SCE, 4

updates SCE’s systems with the assessment results and performs field checks on certain poles. SCE’s 5

assessment contract calls for contract rates to decline by approximately 1.5% per year from 2016 6

through 2018 when the contract expires. 7

33 Refer to WP SCE-02, Vol. 9, pp. 1-63. 34 Total assessments were forecast as Distribution. In reality, there will be a mix of Distribution and

Transmission. Since the price per assessment is the same for both distribution and transmission this has no impact on the expected spend.

35 Refer to Confidential Workpaper: SCE-02, Vol. 9, p. 1-2 (PLP Assessment Forecast).

2011 2012 2013 2014 2015 2016 2017 2018566.125

Labor $ $ $7 $330 $256 $ $ $Non-Labor $ $ $4 $2,457 $1,205 $ $ $ Subtotal 566.125 $ $ $11 $2,787 $1,461 $ $ $

583.125Labor $ $1,022 $828 $3,251 $2,493 $1,692 $1,692 $1,692Non-Labor $ $377 $1,401 $15,113 $9,763 $20,806 $22,053 $22,715 Subtotal 583.125 $ $1,399 $2,229 $18,365 $12,255 $22,499 $23,746 $24,407

Total $ $1,399 $2,239 $21,152 $13,716 $22,499 $23,746 $24,407

Labor $ $1,022 $835 $3,582 $2,749 $1,692 $1,692 $1,692Non-Labor $ $377 $1,405 $17,570 $10,968 $20,806 $22,053 $22,715

Assessments 0 0 0 184,461 142,382 200,000 220,000 230,000Cost Per Assessment 0 0 0 112 106 112 108 106

Ratio of Labor to Total 73% 37% 17% 20% 8% 7% 7%

Basis of Forecast: Itemized ForecastBasis of Labor/Non-Labor Split: Itemized Forecast

Recorded Forecast

20

3. Pole Loading Program Repair Variance Analysis 1

Repair involves the design and installation or modification of guy wires.36 Design 2

involves determining the appropriate size and placement of a guy wire(s) such that the design conforms 3

to SCE design standards and produces a compliant safety factor. Then a drawing is developed that 4

shows the location of the pole that must be repaired, the placement of the guy on the pole and the guy 5

specifications. This drawing is be used by construction to perform the work in the field. Environmental 6

review and land rights checks, when needed, are conducted as part of the design process. Once the 7

design work is completed, the repair notification is sent to construction. The construction of the guy may 8

be completed by either an SCE crew or a contractor. 9

SCE completed 222 repair designs and constructed 20 repairs under the pole loading 10

program in 2014.37 In 2015, SCE completed 2,711 repair designs and constructed 569 repairs under the 11

pole loading program.38 The number of repairs required is directly related to the number of assessments 12

completed. Just as the number of assessments ramped up over 2014, the number of repairs ramped up as 13

well. Repairs may be completed one or two years after the assessment, depending on whether the pole is 14

in a high fire or non-high fire area. 15

36 SCE is responsible for guy repair at electrical levels only. If guy repairs are required at communication levels,

SCE will notify the communication company. The communication company is responsible to make the repair and is solely responsible for its cost of repairs.

37 1 repair design was completed under the Malibu Settlement as shareholder-funded work. Therefore, the costs of that repair are not shown in the recorded costs of this volume.

38 404 repair designs and 89 constructed repairs were completed under the Malibu Settlement as shareholder-funded work. Therefore, those costs are not shown in the recorded costs of this volume.

21

Table II-8 Pole Loading Program Repairs39,40

Portion of GRC Account 571.125 and 593.125 Recorded and Adjusted 2011-2015 / Forecast 2016-2018

(Constant 2015 $000)41

4. Pole Loading Program Repair Cost Forecast 1

Total repair costs are expected to increase relative to 2015 levels as the initial ramp-up in 2

assessments is reflected in repair activity. The current repair rates for poles in high fire areas and non-3

high fire areas are 1.53% and 1.19%, respectively, which are rates based on the new version of 4

SPIDACalc. The repair rates were applied to the assessment forecast to develop a forecast number of 5

repairs.42 The costs to complete the drawing and repair are forecast using historical values as they are 6

39 Refer to WP SCE-02, Vol. 9, pp.1-63. 40 Repairs were forecast as contract non-labor. In reality, there will be a mix of contract and SCE labor. This not

expected to have an impact on the total cost because the cost per repair used in the forecast was based on the historical cost per repair which is a mix of contract and SCE labor.

41 Refer to WP SCE-02, Vol. 9, pp. 129-132 (PLP Distribution Repair Forecast and PLP Transmission Repair Forecast).

42 Refer to WP SCE-02, Vol. 9, pp. 133-134 (PLP Repair Unit Forecast).

2011 2012 2013 2014 2015 2016 2017 2018571.125

Labor $ $ $ $1 $5 $ $ $Non-Labor $ $ $ $ $17 $298 $620 $547 Subtotal 571.125 $ $ $ $1 $22 $298 $620 $547

593.125Labor $ $ $ $19 $261 $ $ $Non-Labor $ $ $ $33 $549 $2,678 $5,579 $4,927 Subtotal 593.125 $ $ $ $52 $810 $2,678 $5,579 $4,927

Total $ $ $ $53 $832 $2,976 $6,199 $5,474Labor $ $ $ $20 $266 $ $ $Non-Labor $ $ $ $33 $566 $2,976 $6,199 $5,474

Ratio of Labor to Total 38% 32% 0% 0% 0%

Basis of Forecast: Itemized ForecastBasis of Labor/Non-Labor Split: Itemized Forecast

Recorded Forecast

22

expected to remain constant over the forecast period. Unit costs are based on the recorded costs to 1

design and construct repairs; the total unit cost for design and repair is $1,913 per pole.43 2

5. Shareholder Costs 3

In D.13-09-028, the Commission approved a settlement agreement (Malibu Settlement) 4

between the SED and SCE resolving issues raised in the Malibu Canyon Fire OII, I.09-01-018. The 5

Malibu Settlement required SCE to spend $17 million of shareholder funds to perform pole loading 6

inspections and remediation in the Malibu area. The Commission further required SCE to perform work 7

along Malibu Canyon Road in conjunction with AT&T Mobility, LLC, Verizon Wireless, and Sprint 8

Communications Company under their settlement with the SED.44 9

In D.14-08-009, the Commission approved a settlement agreement (San Gabriel 10

Windstorm Settlement) between the SED and SCE resolving issues raised in I.14-03-004. The San 11

Gabriel Windstorm Settlement required SCE to spend $3 million of shareholder funds to reduce the 12

probability of overloaded poles. 13

The costs associated with the Settlement Agreement work are not included in the 14

recorded amounts shown here. The unit counts associated with shareholder-funded work are noted 15

separately in the appropriate sections. 16

D. Forecast Capital Expenditures 17

1. PLP-driven Pole Replacements 18

The annual volume of PLP-driven pole replacements is determined by the pace of 19

assessments, assessment remediation rates, and the rate at which these replacements are completed. The 20

expected remediation rates for assessments going forward are described in Section II.B.7 above. 21

After assessments, the poles identified as needing replacement are assigned due dates 22

based on severity. The due dates range from poles which must be made safe within 72 hours to poles 23

that can be scheduled for replacement within 59 months. 24

Sometimes, poles scheduled for replacement may not be remediated due to execution 25

constraints, such as environmental or permitting requirements or limited physical access to the pole due 26

to adjacent structures or remote locations. While SCE goes to great lengths to work with agencies and 27

43 Refer to WP SCE-02, Vol. 9, pp. 129-132 (PLP Distribution Repair Forecast and PLP Transmission Repair

Forecast). 44 D.13-09-028, issued 9/24/2013, OP 1.

23

property owners to get access to poles, a percentage of poles may roll over from the scheduled year for 1

remediation into the following year until these issues are resolved. 2

In other cases, performance of work in one location may offer the opportunity to replace 3

poles in the same location scheduled for replacement in future years. Those poles may be moved 4

forward from their scheduled year and bundled with other work in the current year to achieve 5

efficiencies.45 6

The table below summarizes the forecast rate of pole assessments, expected remediation 7

rates, the volume of poles in the replacement queue, and replacements performed each year. The volume 8

of poles replaced each year depends upon the priority levels of poles in the replacement queue, rollover 9

of poles due to execution challenges, and bundling of poles as described above. The attached 10

workpapers quantify these factors in detail.46 11

Forecast unit costs for replacement shown in Table II-9 are explained in Section IV 12

below and summarized in workpapers.47 13

45 The benefits of bundling work and portfolio management are described in Exhibit SCE-04, Vol. 2. 46 Refer to WP SCE-02, Vol. 9, pp. 135-136 (PLP Detailed Replacement Forecast Volume). 47 Refer to WP SCE-02, Vol. 9, pp. 137-138 ( Pole Replacement Unit Cost Forecast Details).

24

Table II-9 Forecast Assessments, Identified Replacements, and Scheduled Replacement Volumes:

Transmission and Distribution

Forecast capital expenditures in the PLP program are based on the forecast volume of 1

replacements in Table II-9 and on the forecast unit costs discussed in Section IV.C below. The resulting 2

forecast capital expenditures for PLP-driven distribution and transmission pole replacements are shown 3

in Figure II-3 and Figure II-4, respectively. 4

2016 2017 2018 2019 2020Assessments 200,000 220,000 230,000 230,000 230,000Reject Rate

Total 9% 9% 9% 9% 9% 9%

Reject CountTotal 18,000 19,800 20,700 20,700 20,700 Identified Prior to 2016 7,765 0 5 6,053 10,210

Poles in Queue 25,765 38,341 51,318 66,560 79,657

Total Replacements 7,224 7,723 5,458 7,602 11,932 7,224 7,723 8,331 8,331 8,331 6,853 7,060 7,342 7,342 7,342

370 663 989 989 989

Unit Cost, 2015 $Distribution 15,231$ 15,302$ 15,294$ 15,294$ 15,294$ Transmission 23,453$ 23,453$ 23,453$ 23,453$ 23,453$

Total Cost, 2015 $000Distribution 104,382$ 108,039$ 112,290$ 112,290$ 112,290$ Transmission 8,689$ 15,553$ 23,195$ 23,195$ 23,195$

Averaging 2018-2020DistributionTransmission

25

Figure II-3 Pole Loading Distribution Pole Replacements48

CET-PD-IR-PD Recorded 2011-2015/Forecast 2016-2020

(CPUC-Jurisdictional – Constant 2015 and Nominal $000)49

48 Refer to WP SCE-02, Vol. 9, pp. 64-81. 49 Refer to WP SCE-02, Vol. 9, pp. 139-140 (CET-PD-IR-PD Distribution PLP Pole Replacement) and Table

IV-23 for forecast unit costs, and Table II-9 for forecast unit volumes.

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020Nominal $ - - - 5,263 147,324 106,353 112,368 119,731 123,488 127,414Constant 2015$ - - - 5,406 147,324 104,382 108,039 112,290 112,290 112,290

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

$160,000

Nominal $ Constant 2015$

26

Figure II-4 Pole Loading Transmission Pole Replacements50

CET-PD-IR-PT Recorded 2011-2015/Forecast 2016-2020

(Total Company – Constant 2015 and Nominal $000)51

2. Alternatives to Pole Replacement 1

SCE is evaluating the use of an Extended Truss (ET) to remediate poles that have a 2

noncompliant safety factor. SCE is assessing whether the installation of the ET is a viable restoration 3

method for poles with noncompliant safety factors. Since the ET will reach much farther up the length of 4

the pole than a standard steel stub which may be used to restore poles that have internal degradation, 5

new ET design and construction standards compatible with existing construction standards and required 6

clearances must be developed. Furthermore, if SCE decides to move forward with the ET, additional 7

time would be required to set up the ET in SCE’s IT systems, coordinate with joint owners, train 8

employees who will encounter the truss in the field, select and onboard vendors to install the truss and 9

develop work management processes. Because SCE has not made a decision on the feasibility of the ET, 10

and much work remains before that decision can be implemented, the forecast does not include ET 11

remediation. 12

50 Refer to WP SCE-02, Vol. 9, pp. 64-81. 51 Refer to WP SCE-02, Vol. 9, pp.141-142-y (CET-PD-IR-TR CET-PD-IR-PT Transmission PLP Pole

Replacement) and Table IV-24 for forecast unit costs, and Table II-9 for forecast unit volumes.

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020Nominal $ - - - 68 9,574 8,808 16,116 24,628 25,277 25,940Constant 2015$ - - - 69 9,574 8,689 15,552 23,195 23,195 23,195

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

Nominal $ Constant 2015$

27

3. Coordination of Pole Replacements with Other Programmatic Work 1

PLP program design and operations practices allow coordination with other 2

programmatic work when possible.52 First, SCE has a replacement timeframe for certain PLP failures of 3

up to 59 months. This timeframe enables lower-risk PLP failures to be addressed with other planned 4

work, which may occur prior to the replacement due date. Changes to the intrusive pole inspection 5

remediation timeframes (see Section III.B.2) will also permit bundling pole replacements with other 6

planned pole replacements, or other programmatic work. For example, an overhead conductor 7

replacement project may be combined with nearby deteriorated pole replacements. By grouping work, 8

SCE will minimize customer outages and customer disruption. SCE expects the work to be completed 9

more efficiently when grouped with other work in the same geographic area. 10

4. Transformer Replacements, PLP Portion 11

Distribution transformer replacements are described in SCE-02, Volume 2; a portion of 12

these replacements are associated with pole replacements under the PLP program. We determined the 13

PLP portion of distribution transformer replacements based on the ratio of PLP-driven transformer 14

capital expenditures and PLP-driven pole replacements authorized in the 2015 GRC decision (4.17%).53 15

The resulting forecast for PLP-related transformer replacements is shown below. (Figure II-5) 16

52 As stated in 2015 GRC testimony (SCE-03, Vol. 06, Part 2, p. 14) and D.15-11-021, p. 117. 53 Refer to WP SCE-02, Vol 9, pp. 143-144 (PLP Driven Prefab and Transformer Replacements).

28

Figure II-5 Transformer Capital Expenditures, PLP Portion54

WBS Element CET-PD-OT-TR-PL Recorded 2011-2015/Forecast 2016-2020

(CPUC-Jurisdictional – Constant 2015 and Nominal $000)

5. Prefabrication, PLP Portion 1

Capital expenditures for prefabrication are described in SCE-02, Volume 5; a portion of 2

these capital expenditures are associated with the PLP program. The PLP portion of prefabrication 3

capital expenditures was forecast based on the ratio of PLP-driven prefabrication expenditures and PLP-4

driven pole replacements authorized in the 2015 GRC decision (2.83%).55 The resulting forecast for 5

PLP-related prefabrication expenditures is shown below. (Figure II-6) 6

54 Refer to WP SCE-02, Vol. 9, pp. 64-81 and WP SCE-02, Vol 9, pp. 143-144 (PLP Driven Prefab and

Transformer Replacements). These expenditures are not included in the pole balancing account. 55 WP SCE-02, Vol 9, pp. 143-144 (PLP Driven Prefab and Transformer Replacements).

29

Figure II-6 Prefabrication Capital Expenditures, PLP Portion56

WBS Element CET-PD-OT-PF-PL Recorded 2011-2015/Forecast 2016-2020

(CPUC-Jurisdictional – Constant 2015 and Nominal $000)

56 Refer to WP SCE-02, Vol. 9, pp. 64-81, and WP SCE-02, Vol. 9, pp. 143-144 (PLP Driven Prefab and

Transformer Replacements). These expenditures are not included in the pole balancing account.

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020Nominal $ - - - 148 3,976 3,260 3,638 4,088 4,217 4,351Constant 2015$ - - - 152 3,976 3,200 3,498 3,834 3,834 3,834

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

$5,000

Nominal $ Constant 2015$

30

1

DETERIORATED POLE PROGRAM 2

A. Background 3

Several factors drive inspection and replacement of SCE’s over 1.4 million poles, primarily 4

maintaining pole strength, which might be compromised due to pole deterioration or pole loading. The 5

programs to assess and remediate pole deterioration are included in this section. The Pole Loading 6

Program is discussed in Section II. SCE also performs pole replacements after storms, when vehicles or 7

other external factors damage poles, or when poles must be relocated, to name just a few scenarios. The 8

costs associated with these activities are included in the relevant accounts for those activities, and are 9

not included here. This chapter discusses pole inspections, maintenance, and replacement for 10

Distribution and Transmission poles due to deterioration. 11

B. Activity Description 12

1. Replacements Driven by Program Inspections 13

SCE established the distribution pole inspection program to comply with G.O. 165, 14

which became effective in 1997. G.O. 165 requires intrusive inspections for all poles at least 15 years 15

old to be completed within 10 years of program inception. Thereafter, it requires all poles to be 16

intrusively inspected by the time they are 25-years old and then re-inspected at least once every 20 17

years. SCE completed its first cycle of intrusive inspections in 2007. 18

G.O. 165 defines intrusive inspections as “involving movement of soil, taking samples 19

for analysis, and/or using more sophisticated diagnostic tools beyond visual inspections or instrument 20

reading.” “Intrusive” inspections involve drilling into the pole’s interior to identify and measure the 21

extent of internal decay which is typically undetectable with external observation alone. SCE’s 22

inspection standards describe six types of inspections satisfying this definition which apply different 23

combinations of digging, boring, and sounding depending on the type of pole and its setting. Intrusive 24

inspectors may also perform a visual inspection on poles that are in the inspection grid but that are 25

younger than 15 years old, or that have already had an intrusive inspection within the last 10 years, to 26

look for signs of obvious external damage such as damage from vehicles or woodpeckers. 27

Poles due for inspection under G.O. 165 guidelines in any year are spread over SCE’s 28

50,000 square-mile service territory, often requiring significant drive time between poles. Moreover, the 29

number of inspections due any year can vary significantly from year-to-year, depending on the ages of 30

the poles and when the last inspections were performed. This can lead to significant variation in the 31

31

number of pole replacements required from one year to the next. Both are inefficient for resource 1

allocation. 2

These inspections require inspectors with proper training and experience. Maintaining a 3

stable inspection workforce is key to a successful intrusive inspection program. In 2009, SCE performed 4

inspections on a “grid” basis to reduce travel time per inspection and to levelize the number of 5

inspections (and therefore replacements) required per year. Besides inspecting every pole due under the 6

minimum G.O. 165 requirements, SCE inspected all poles within a defined area or “grid” during the 7

same year. All poles receiving intrusive inspections within the grid will be due for their next inspection 8

in the same future year. 9

In 2009, SCE also began transitioning to a 10-year inspection cycle that meets and 10

exceeds G.O. 165 requirements and matches industry best practices. The other two California IOUs, 11

SDG&E and PG&E, have also transitioned to 10-year pole inspection cycles. SCE performs both a 12

visual and an intrusive inspection on every pole due for an intrusive inspection under G.O. 165. For 13

poles not due for an intrusive inspection until the next inspection cycle, SCE only performs a visual 14

inspection. A new pole might be installed within a grid three years after that grid underwent intrusive 15

inspections; seven years later, all poles in that grid will be inspected again. To meet G.O. 165 16

requirements, this pole must be intrusively inspected at least once before the end of its 25th year. 17

However, under the grid-based system it will be inspected twice, once at age 7 and again at age 17. 18

Here, SCE performs a visual inspection in the pole’s 7th year and an intrusive inspection in its 17th year 19

meeting G.O. 165’s requirement. 20

SCE expects to complete its first grid-based cycle in 2018. Completing this transition will 21

cause lower cost per inspection, as shown in Table III-18. Maintaining a steady rate of inspections is 22

necessary to maintain this cost advantage, as non-grid inspections are more expensive than grid-based 23

inspections.57 The grid-based approach yields reduced inspection intervals with a less than proportional 24

increase in average annual inspection costs. Shorter inspection intervals reduce prevalence and severity 25

of pole decay. 26

2. Changes in the Intrusive Pole Inspection Program Standards 27

Three changes were made to inspections standards since 2012 that impact the recorded 28

and forecast rates of pole replacement under the Deteriorated Pole Program. The first change, which 29

57 See A.13-11-003, Exhibit SCE-03, Vol. 07 Part 1 p. 39.

32

took effect in 2013, included clarification of visual reject criteria and reclassified replacement 1

timeframes for certain poles from longer to shorter timeframes. Clarification of visual reject criteria, 2

along with a relatively large proportion of inspections being performed in regions prone to wildlife-3

driven pole damage, resulted in higher than anticipated overall failure rates. In addition, SCE 4

reclassified certain pole structure types58 with decay as one-year rather than two or three-year 5

replacements due to concerns about the potential risk posed by these structures if decay is present. This 6

drove up the required minimum volumes of replacements in the short term. This change contributed to 7

the increase in deteriorated pole replacements relative to the 2015 GRC forecast, which relied on 2011 8

and 2012 inspection failure rates. 9

Table III-10 Historical Reject Rates for Intrusive Pole Inspections

The second and third changes, which took effect in 2016, will reduce replacement rates 10

by changing the criteria for when a pole must be replaced and by reinforcing poles with a steel stub as an 11

alternative to replacement.59 In SCE’s 2015 GRC, the Commission challenged SCE to consider 12

reinforcing poles to avoid a replacement and to reduce the number of poles being replaced.60 To evaluate 13

potential changes to the standards, a team was formed to consider the estimated cost savings, the change 14

in risk and benchmarking of other utilities. 15

Intrusive pole inspection standards are described in SCE’s material standard MS-454. 16

MS-454 provides detailed instructions to inspectors on performing inspections and evaluating inspection 17

results, including a definition of key metrics that determine pole inspection failure. Among these metrics 18

58 Poles with equipment and poles with pole-top extensions. 59 Steel stubbing is described in IV.B.2. 60 D15-11-021, Page 135. While the comment was made in the pole loading discussion section, SCE believes

the commission’s intent is equally applicable to other pole replacements. Therefore, SCE considered alternative methods to remediate noncompliant poles through alternative methods.

Inspection YearAggregate Failure Rate

(Distribution and Transmission)

2013-2015 8%

2008-2012 7%

2001-2007 17%

33

is Remaining Section Modulus (RSM), a numerical assessment of pole degradation. The team evaluated 1

various levels of RSM to determine at what level of degradation the pole should fail the intrusive 2

inspection and at what level of degradation a steel stub installation would be appropriate if the pole 3

failed. The team analyzed the customer savings versus the risk increase for various pole failure 4

thresholds. SCE selected the failure threshold based on the point where the incremental increase in 5

savings did not justify the increased risk. Relative to the benchmarked utilities, SCE appears more 6

conservative in its RSM failure threshold. However, since pole populations, construction practices, 7

environmental conditions etc. vary significantly between utilities, SCE relied on its risk modeling and 8

determined that accepting the risk from additional degradation was not justified. 9

The new standard, introduced in April 2016, includes the second and third change 10

referenced above. The second change will reduce the pole failure threshold to 95% RSM. The change in 11

failure threshold will reduce forecast distribution pole replacement rates from 7.6% to 5.8% and 12

transmission pole replacement rates from 12.5% to 6.2% (Table III-11). With forecast distribution and 13

transmission inspection volumes of 135,000 and 13,000, respectively, in 2017 (Table III-18), this change 14

will cause approximately 2,400 fewer three-year distribution pole replacements and approximately 800 15

fewer three-year transmission pole starting in 2020. The third change will set the allowed RSM 16

threshold for installation of a steel stub to a minimum RSM of 67%.61 This will further reduce the count 17

of pole replacements by an average of approximately 1,700 distribution poles and 180 transmission 18

poles per year from 2017 through 2020. 19

61 Additional criteria described in MS-454 also apply. Refer to WP SCE-02, Vol. 9, pp. 145-207.

34

Table III-11 Impact of Inspection Standard Changes on Forecast Restoration and Replacement

Rates

3. Restoration (steel stubbing) 1

Steel stubbing is expected to extend the life of a deteriorated pole over 15 years and 2

likely much more than that. 3

Steel stubbing offers a significant cost advantage over pole replacement without 4

compromising safety: the forecast unit cost for stubbing is $4,190 for transmission poles and $2,155 for 5

distribution poles,62 compared to a unit cost of $23,453 (Table IV-24) for transmission pole replacement 6

and a weighted average of $15,169 (Table IV-23) for distribution pole replacements. 7

SCE anticipates that approximately 2% of its inspected poles will be steel stub candidates 8

based on their RSM and other criteria established in the inspection standards (Table III-11). Of these, 9

SCE estimates that 10% will be reclassified as replacements after a more detailed evaluation of field 10

circumstances. The expected count of pole restorations is shown in Table III-12 and Table III-13. 11

62 Refer to WP SCE-02, Vol. 9, pp. 208-209, (CET-PD-IR-DP CET-PD-IR-TR Steel Stub Unit Cost Estimate).

2015 Reject Rate (Before SPEC

Change)

Estimated 2015 Reject Rate (After SPEC

Change)

1 Year 5.30% 0.94%

2 Years 1.06% 1.70%

3 Years 1.19% 1.11%

Steel Stub Repairs 0.08% 2.00%

7.63% 5.75%

Distribution Reject Rates

Reject Rate By Priority - Recommended Action (RAC)

Total

2015 Reject Rate (Before SPEC Change)

Estimated 2015 Reject Rate (After SPEC

Change)

1 Year 7.15% 0.74%

2 Years 1.53% 2.38%

3 Years 3.62% 1.11%

Steel Stub Repairs 0.20% 2.00%

12.50% 6.23%

Transmission Reject Rates

Reject Rate By Priority - Recommended Action (RAC)

Total

35

4. Inspection-driven Replacements 1

The annual volume of inspection-driven deteriorated pole remediations determines the 2

rates at which poles flow into the remediation queue, and the rate at which these remediations are 3

completed. The expected remediation rates for intrusive inspections are described in the previous 4

section. 5

After inspection, the poles identified as needing replacement are prioritized based on the 6

extent of deterioration. The priority ratings are: 7

1. Priority 1, the pole must be made safe within 72 hours and replaced within 45 days of 8

inspection 9

2. Priority 2A, the pole must be replaced within one year of inspection 10

3. Priority 2B, the pole needs to be replaced within two years of inspection 11

4. Priority 2C, the pole needs to be replaced within three years of inspection63 12

Sometimes, poles scheduled for replacement may not be remediated due to factors such 13

as unique permitting requirements or limited physical access to the pole due to adjacent structures or 14

remote locations. A percentage of poles may rollover from the scheduled year for remediation into the 15

following year until these issues are resolved. 16

In other cases, performance of work in one location may offer the opportunity to replace 17

poles in the same location scheduled for replacement in future years. Those poles may be moved 18

forward from their scheduled year and bundled with poles in the current year to achieve efficiencies. 19

The table below summarizes the forecast rate of pole inspections, the expected 20

remediation rates by priority level, forecast replacements by scheduled year of replacement, and rollover 21

and bundling for inspection-driven deteriorated pole replacements.64 Unit rates applied to these forecast 22

volumes are described in Section IV below and summarized in workpapers.65 23

63 The visual and RSM criteria for each timeframe are described in MS-454. Refer to WP SCE-02, Vol. 9, pp.

145-207. 64 Refer to WP SCE-02, Vol. 9, pp. 210-211 (IPI Driven Deteriorated Pole Replacement Detailed Forecast

Distribution), WP SCE-02, Vol. 9, pp. 212-213 (IPI Driven Deteriorated Pole Replacement Detailed Forecast Transmission) for details.

65 Refer to WP SCE-02, Vol. 9, pp. 137-138 (Pole Replacement Unit Cost Forecast Details).

36

Table III-12 Forecast Inspection Volumes, Remediation rates, and Inspection-Driven Pole

Remediation: Distribution

2017 2018 2019 2020Q1 Q2-4

Intrusive Inspections 36,739 108,000 135,000 128,500 120,500 120,500Failure Rate

Total 7.63% 5.75% 5.75% 5.75% 5.75% 5.75%

Failure CountTotal 2,803 6,210 7,763 7,389 6,929 6,929

Scheduled ReplacementsIdentified in 2016 or later 381 3,034 3,686 5,375 4,991Identified Prior to 2016 9,809 1,892 1,323 6 0Rollover & Bundling Adjustment (1,632) 1878 1071 635 630