2018 final rating review report

TRANSCRIPT

Nigerian Breweries Plc.

2018 Final Rating Review Report

The copyright of this document is reserved by Agusto & Co. Limited. No matter contained herein may be reproduced, duplicated or copied by any means whatsoever without the prior written consent of Agusto & Co. Limited. Actio n will be taken against companies or individuals who ignore this warning. The information contained in this document has been obtained from published financial statements and other sources which we consi der to be reliable but do not guarantee as such. The opinions expressed in this document do not represent investment or other advice and should therefore not be construed as such . The circulation of this document is restricted to whom it has been addressed. Any unauthorized disclosure or use of the informat ion contained herein is prohibited.

2018 Corporate Rating Review Report

Nigerian Breweries Plc Rating Assigned:

Aa This is a company that possesses very strong financial condition and very strong

capacity to meet local currency obligations as and when they fall due.

Outlook: Stable

Issue Date: 25 June 2018

Expiry Date: 30 June 2019

Previous Rating: Aa

Industry: Brewery

Outline Page Rationale 1

Company Profile 4

Financial Condition 7

Ownership, Mgt & Staff 12

Outlook 14

Financial Summary 15

Rating Definition 18

Analysts:

Ikechukwu Iheagwam [email protected]

Isaac Babatunde [email protected]

Agusto & Co. Limited

UBA House (5th Floor)

57, Marina

Lagos

Nigeria

www.agusto.com

RATING RATIONALE Agusto & Co. hereby affirms the “Aa” rating assigned to Nigerian Breweries

Plc (“Nigerian Breweries”, “NB” or “the Company”). This rating is bolstered by

the Company’s very strong financial condition evidenced by good cash flow,

low leverage, adequate working capital and good profitability. However, the

weak macroeconomic environment continues to be a drag on the overall

performance of the Company.

Agusto & Co. recognizes Nigerian Breweries’ strong leadership position in

the Nigerian Brewery Industry with over 60% market share and a diversified

product portfolio. In addition, the Company enjoys strong parental support

from Heineken N.V Group of the Netherlands (the second largest brewing

company in the world with production in excess of 200 million hectoliters1)

as well as a stable, qualified and experienced management team.

Despite the challenging macroeconomic and business environment in the

financial year ended 31 December 2017 (FYE 2017), Nigerian Breweries

reported a 10% rise in revenue on account of volume growth supported by

innovative product offerings as well as slight price increases across different

brands to compensate for rising input costs. In the same period, increase in

the cost of raw materials and consumables as well as down trading, amongst

others pressured NB’s margins. Nonetheless, the Company posted a good

operating profit margin of 15.9%, return on assets of 13.3% and return on

equity of 26.1% in 2017.

In FYE 2017, Nigerian Breweries recorded an operating cash flow (OCF) of

₦74.4 billion, which was sufficient to cover returns to providers of finance

comprising dividend (89%) and interest (11%). In the same period, NB’s OCF

to sales ratio at 22% and the three year average (2015 - 2017) at 23%,

surpassed our benchmarks and supports our opinion on NB’s good cash

generating capacity.

As at 31 December 2017, Nigerian Breweries total liabilities stood at ₦204.5

billion, mainly comprising non-interest bearing liabilities (96%) and interest

1 Statista - https://www.statista.com/statistics/227197/leading-10-brewing-groups-worldwide-based-on-production-volume/

2 2018 Corporate Rating Review Report

Nigerian Breweries Plc

bearing liabilities (4%). In the same period under review, NB’s operating cash

flow was sufficient to cover interest expense 17 times, while interest

expenses to sales ratio remained low at 1.2%.

Synonymous with the Brewery Industry, Nigerian Breweries posted a short

term financing surplus of ₦130.2 billion and a long term financing need of

₦114.8 billion in FYE 2017. Over the last three years (2015 - 2017), Nigerian

Breweries has consistently posted yearly short term financing surpluses, as

well as recorded long term financing needs. Nevertheless, the Company’s

short-term financing surpluses have been adequate to cover the long term

financing needs on a continuing basis.

The unaudited accounts of Nigerian Breweries for the three months ended 31

March 2018 (Q1’2018), showed a 9% dip in topline performance from

comparable period in 2017. In the same period, cost of sales to revenue ratio

improved to 54.2%, but operating expenses worsened slightly to 24.8% of

revenue, thus resulting in a profit before tax margin of 18.4%. The Company

reported an OCF of ₦18.9 billion, which represented 23% of Q1’2018 sales,

depicting a good cash flow position, while interest expense to sales ratio at

3% and interest coverage ratio at 8 times, are in line with our expectations.

In our view, we expect NB’s cash flow to remain strong , precipitated by

favorable terms of trade from customers and suppliers. In addition, we expect

leverage to remain within acceptable limits, strongly supported by the

Company’s strong track record and good credit history, which it leverages to

access low cost funding in the market.

Based on the aforementioned, we have attached a stable outlook to Nigerian

Breweries Plc.

3 2018 Corporate Rating Review Report

Nigerian Breweries Plc

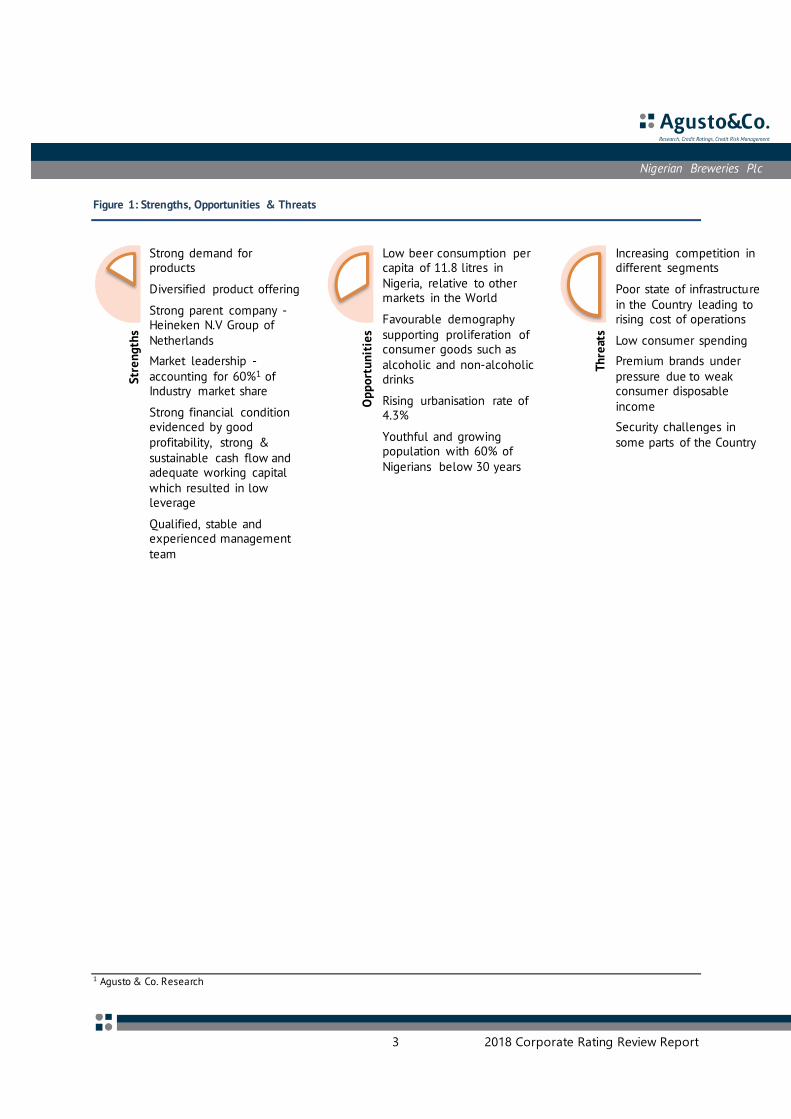

Figure 1: Strengths, Opportunities & Threats

1 Agusto & Co. Research

Str

en

gth

s

Strong demand for products

Diversified product offering

Strong parent company -Heineken N.V Group of Netherlands

Market leadership -accounting for 60%1 of Industry market share

Strong financial condition evidenced by good profitability, strong & sustainable cash flow and adequate working capital which resulted in low leverage

Qualified, stable and experienced management team

Op

po

rtu

nit

ies

Low beer consumption per capita of 11.8 litres in Nigeria, relative to other markets in the World

Favourable demography supporting proliferation of consumer goods such as alcoholic and non-alcoholic drinks

Rising urbanisation rate of 4.3%

Youthful and growing population with 60% of Nigerians below 30 years

Th

reat

s

Increasing competition in different segments

Poor state of infrastructure in the Country leading to rising cost of operations

Low consumer spending

Premium brands under pressure due to weak consumer disposable income

Security challenges in some parts of the Country

4 2018 Corporate Rating Review Report

Nigerian Breweries Plc

PROFILE OF NIGERIAN BREWERIES PLC Overview & Background

Nigerian Breweries Plc, a subsidiary of The Heineken N.V. Group (the second largest brewing company in the

world by volume with operations spanning over 70 countries), is the pioneer and largest brewing Company in

Nigeria. Nigerian Breweries Limited was incorporated in 1946 as a limited liability company and produced

the first bottle of Star lager beer at the Lagos Brewery in June 1949. The Company later became a public

limited liability company and was listed on the Nigerian Stock Exchange (NSE) in 1973.

Since inception in 1946, the Company has grown both organically and through acquisitions to become the

leading Brewing company in Nigeria, controlling more than two-thirds of the lager market share in the

Country. Other major players in the Brewing Industry are Guinness Nigeria Plc and AB InBev2. Following the

conclusion of the merger between the NB and Consolidated Breweries Plc in 2014, Nigerian Breweries now

holds an 89.3% equity interest in Benue Bottling Company Limited3 (BBCL). As at 31 May 2018, NB stood as

one of the most capitalised stock on the NSE with a market capitalisation of ₦847.6 billion.

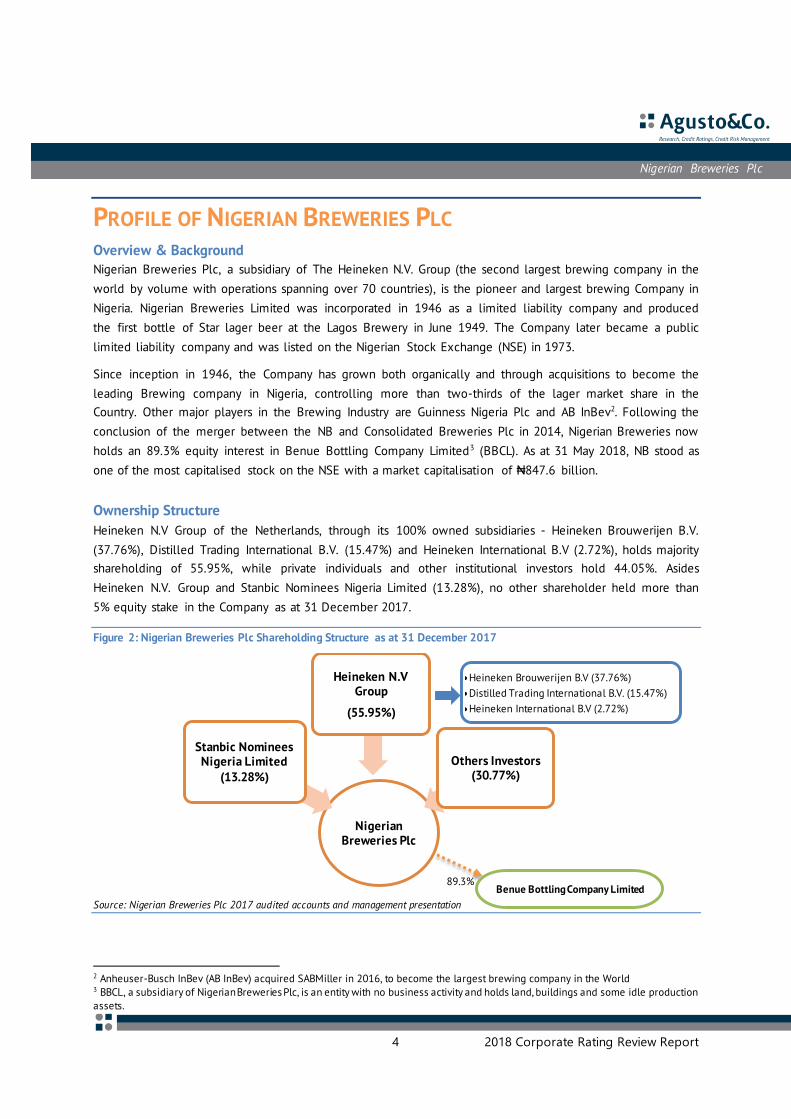

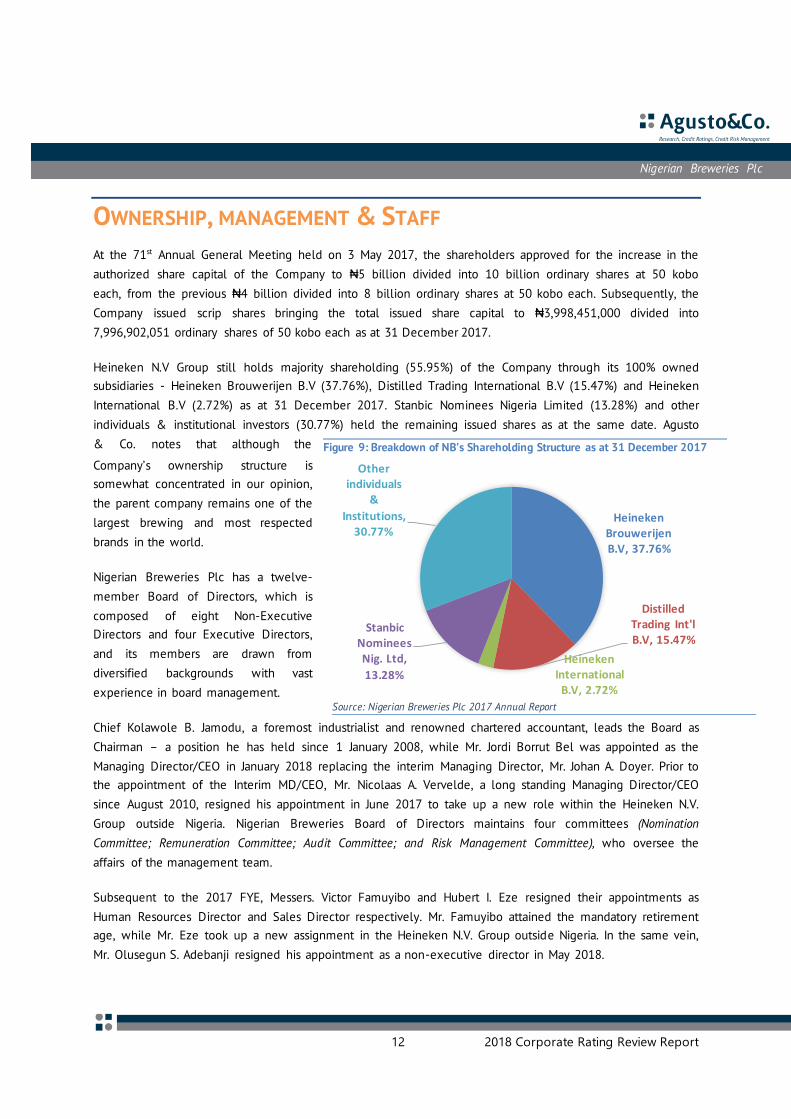

Ownership Structure

Heineken N.V Group of the Netherlands, through its 100% owned subsidiaries - Heineken Brouwerijen B.V.

(37.76%), Distilled Trading International B.V. (15.47%) and Heineken International B.V (2.72%), holds majority

shareholding of 55.95%, while private individuals and other institutional investors hold 44.05%. Asides

Heineken N.V. Group and Stanbic Nominees Nigeria Limited (13.28%), no other shareholder held more than

5% equity stake in the Company as at 31 December 2017.

Figure 2: Nigerian Breweries Plc Shareholding Structure as at 31 December 2017

Source: Nigerian Breweries Plc 2017 audited accounts and management presentation

2 Anheuser-Busch InBev (AB InBev) acquired SABMiller in 2016, to become the largest brewing company in the World 3 BBCL, a subsidiary of Nigerian Breweries Plc, is an entity with no business activity and holds land, buildings and some idle production

assets.

Nigerian Breweries Plc

Stanbic Nominees Nigeria Limited

(13.28%)

Heineken N.V Group

(55.95%)

Others Investors (30.77%)

Benue Bottling Company Limited 89.3%

Heineken Brouwerijen B.V (37.76%)

Distilled Trading International B.V. (15.47%)

Heineken International B.V (2.72%)

5 2018 Corporate Rating Review Report

Nigerian Breweries Plc

Board Composition and Structure

Nigerian Breweries Plc has a twelve-member Board of Directors comprising eight Non-Executive Directors

and four Executive Directors. The Board is led by Chief Kolawole B. Jamodu (CFR) as Chairman, while Mr.

Jordi Borrut Bel was appointed Managing Director/CEO in January 2018, following the resignation of Mr.

Johan A. Doyer as interim MD/CEO.

Subsequent to FYE 2017, Messers. Victor Famuyibo and Hubert I. Eze resigned their appointments as Human

Resources Director and Sales Director respectively. Mr. Famuyibo attained the mandatory retirement age,

while Mr. Eze took up a new assignment in the Heineken N.V. Group outside Nigeria. In the same vein, Mr.

Olusegun S. Adebanji resigned his appointment as a non-executive director in May 2018.

Nigerian Breweries Plc’s Board of Directors operates through four board committees, namely Nomination

Committee; Remuneration Committee; Audit Committee; and Risk Management Committee.

Table 1: Current Directors

Chief Kolawole B. Jamodu Chairman

Mr. Jordi Borrut Bel Managing Director/CEO

Mr. Mark P. Rutten Finance Director

Mr. Hendrik A. Wymenga Supply Chain Director

Mr. Franco Maggi Marketing Director

Mr. Roland Pirmez Non-Executive Director

Chief Samuel O. Bolarinde Non-Executive Director

Dr. Obadiah Mailafia Non-Executive Director

Mrs. Ndidi O. Nwuneli Non-Executive Director

Mr. Atedo N. Peterside Non-Executive Director

Mr. Sijbe Hiemstra Non-Executive Director

Mrs. Ifueko M Omoigui-Okauru Non-Executive Director Source: Nigerian Breweries Plc 2017 Annual Report and management presentation

The Nomination Committee is chaired by Mr. Sijbe Hiemstra, a non-executive director, and supported by two

other members. Mr. Atedo N. Peterside, is the Remuneration Committee Chairman with two other non-

executive directors providing support, while Mr. Roland Pirmez leads the Risk Management Committee

alongside two non-executive members. The Audit Committee comprises six members – three Shareholders’

representatives and three Directors’ representatives. Chief. Timothy A. Adesiyan (Shareholders representative)

chairs the Board Audit Committee.

Operating Structure

Nigerian Breweries has nine breweries, two malting plants and two distribution centres spread across the

country. The Company product portfolio consist of over 20 high quality alcoholic and non-alcoholic products,

which cut across the premium, mainstream and value brands. NB has a range of household brands which

cater for the needs of different segments of the market including Heineken, Star, Gulder, “33” Export lager

beer, Goldberg, Legend Extra Stout, Maltina, Amstel Malta, Hi-malt, Strong Bow, Star Radler and Star Lite

among others.

6 2018 Corporate Rating Review Report

Nigerian Breweries Plc

During the financial year ended 31 December 2017, NB launched two new products into the market – Stella

Premium lager beer and Ace Desire Zobo Flavour Drink. Subsequent to FYE 2017, the Company introduced

the Tiger lager brand to further compete in the premium segment. Although, Nigeria remains the dominant

market for the Company’s brands, some of the products are exported mainly to the United Kingdom, the

Netherlands and United States of America.

Nigerian Breweries Plc operates two distribution centres and several depots, which it leverages to deliver its

products nationwide. The Company’s route to market consist of an extensive network of key distributors,

wholesalers, bulk breakers and retail stores covering over 525,000 retail touch points across the six geo-

political zones in the Country.

Other Information

As at 31 December 2017, Nigerian Breweries’ total assets grew by 4% to ₦382.7 billion (2016: ₦367.6

billion), while total shareholders’ fund stood at ₦178.2 billion. In the financial year ended 31 December

2017, the Company generated turnover of ₦344.5 billion and recorded profit after tax of ₦33 billion. In the

review period, NB had a total of 3,328 persons on its payroll as at 31 December 2017 (2016: 3,646).

As at 31 December 2017, Nigerian Breweries Plc’s contingent liabilities in respect of pending litigation and

claims amounted to ₦9 billion (2016: ₦1,558 billion). In the opinion of the Directors and based on

independent legal advice, the Company's liabilities are not likely to be material, but the amount cannot be

determined with sufficient reliability thus no provision was made in the 2017 financial statements.

Table 2: Background Information Authorized Share Capital: ₦5 billion

Paid-up Capital: ₦3.99 billion Shareholders’ Funds: ₦178.2 billion

Registered Office: Iganmu House, 1 Abebe Village Road, Iganmu, Lagos Principal Business: Brewing Auditors: Deloitte & Touche

Source: Nigerian Breweries Plc 2017 Annual Report

7 2018 Corporate Rating Review Report

Nigerian Breweries Plc

FINANCIAL CONDITION ANALYSTS’ COMMENTS

Nigerian Breweries Plc (“Nigerian Breweries”, “NB” or “the Company”) and its subsidiary Benue Bottling Company Limited (“BBCL”) are

jointly referred to as the Nigerian Breweries Group (“NB Group” or “the Group”). We have analysed the audited financial statements of

Nigerian Breweries Plc, the Company, for the three-year period ended 31 December 2017.

PROFITABILITY Nigerian Breweries Plc’s principal activities involve the brewing, marketing and sale of lager, stout, non-

alcoholic malt drinks and soft drinks, from which the Company derives its revenue. Nigerian Breweries’

primary geographical market is Nigeria, accounting for 99.9% of its sales in 2017.

During the financial year ended 31 December 2017 (FYE 2017), NB recorded turnover of ₦344.5 billion,

which represented a 10% growth from prior year. This was mainly driven by volume growth supported by

innovative product offerings as well as slight price increases across different brands. Agusto & Co. notes

positively, that Nigerian Breweries’ revenue has continued to grow year-on-year, evidenced by a five-year

(2013 - 2017) compound annual growth rate (CAGR) of 5.1%, amidst increasing competition in the Industry

and challenging macroeconomic environment.

In 2017, the Company’s cost of sales to revenue ratio rose marginally to 58.3% (2016: 56.8%), principally due

to the increase in the cost of imported raw materials and consumables purchased in the period. Although,

cost of sales has been trending upwards (both in absolute and as a percentage of sales) over the last three

years, Agusto & Co. recognizes that the Company’s cost leadership strategy has helped to manage input costs

at relatively competitive level despite the impact of recession, devaluation of the domestic currency and

inflationary pressures, amongst others. As a result, the Company recorded a gross profit margin of 41.7% in

2017 (2016: 43.2%).

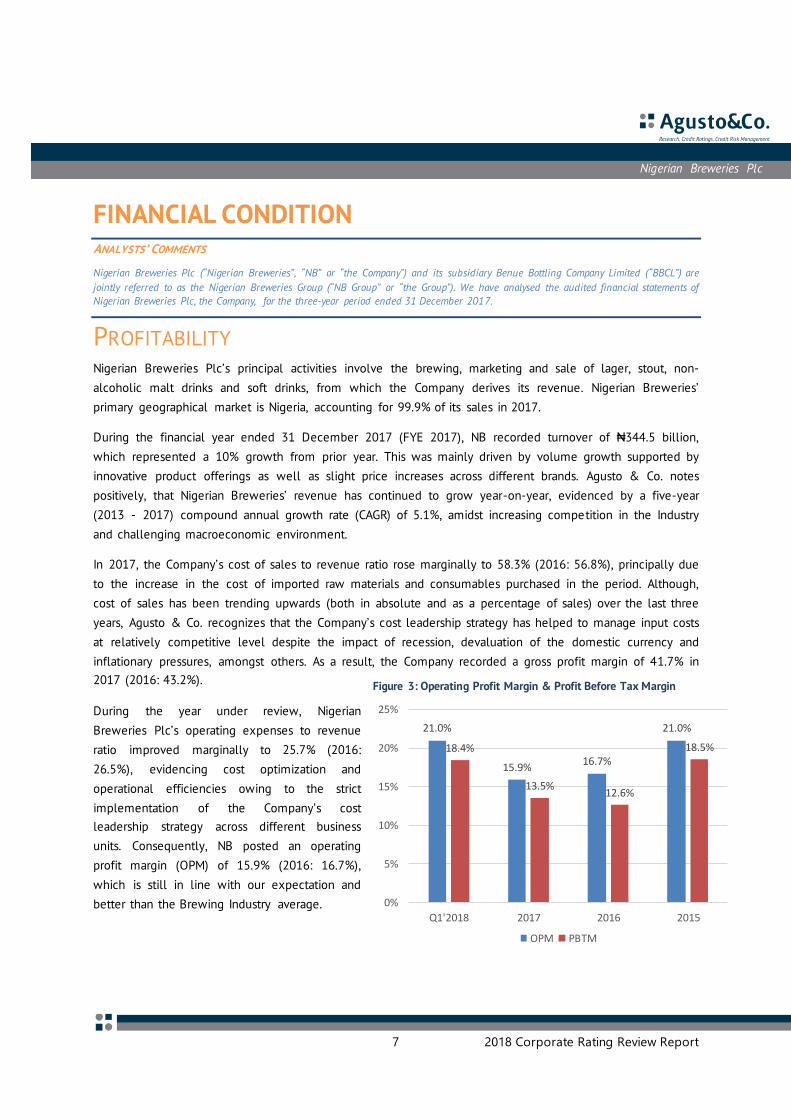

During the year under review, Nigerian

Breweries Plc’s operating expenses to revenue

ratio improved marginally to 25.7% (2016:

26.5%), evidencing cost optimization and

operational efficiencies owing to the strict

implementation of the Company’s cost

leadership strategy across different business

units. Consequently, NB posted an operating

profit margin (OPM) of 15.9% (2016: 16.7%),

which is still in line with our expectation and

better than the Brewing Industry average.

21.0%

15.9%16.7%

21.0%

18.4%

13.5%12.6%

18.5%

0%

5%

10%

15%

20%

25%

Q1'2018 2017 2016 2015

OPM PBTM

Figure 3: Operating Profit Margin & Profit Before Tax Margin

8 2018 Corporate Rating Review Report

Nigerian Breweries Plc

In 2017, the Company’s other income arising mainly from insurance claim, sale of scrap as well as interest

income on bank deposits, amounted to ₦2.3 billion. Whereas, other expenses comprising foreign exchange

losses amounted to ₦6.5 billion, thus resulting in a net other expenses to turnover ratio of 1.2%. In the same

period under review, NB posted a finance cost of ₦4.2 billion, which represented just 1.2% of revenue. This in

our opinion is the lowest in the Industry and gives credence to NB’s strong credit profile, which it leverages

to attract favourable interest rate pricing. As a result, Nigerian Breweries Plc reported a profit before tax to

sales ratio of 13.5% in 2017 and a three-year (2015 - 2017) weighted average of 14.1%, both of which we

consider to be satisfactory.

In FYE 2017, Nigerian Breweries posted a return on assets (ROA) and a return on equity (ROE) of 13.3% and

26.1% respectively, both of which are in line with our expectations. Furthermore, Agusto & Co. notes

positively, that Nigerian Breweries Plc has consistently delivered value to its shareholders, evidenced by

return on equity, well above the average yield on government securities, over the last five years.

The unaudited accounts of Nigerian Breweries

Plc for the three months ended 31 March 2018

(Q1’2018), showed a 9% dip in topline

performance from comparable period in 2017.

In the same period, cost of sales to revenue

ratio improved to 54.2%, while operating

expenses worsened slightly to 24.8% of

revenue, thus resulting in a profit before tax

margin of 18.4% (Q1’2017: 19.1%).

NB recorded an improvement in ROA and ROE

of 17.8% and 32.3% respectively for the period

ended 31 March 2018. Overall, we believe that

consolidating the gains from the ongoing cost

leadership strategy will help reduce operating

cost going forward.

In our opinion, Nigerian Breweries’ profitability level is good and sustainable.

Figure 4: Return on Assets & Return on Equity – (2015 – Q1’2018)

17.8%

13.3%11.9%

17.0%

32.3%

26.1%23.9%

31.6%

0%

5%

10%

15%

20%

25%

30%

35%

Q1'2018 2017 2016 2015

ROA ROE 364-Day Treasury Bill yield

9 2018 Corporate Rating Review Report

Nigerian Breweries Plc

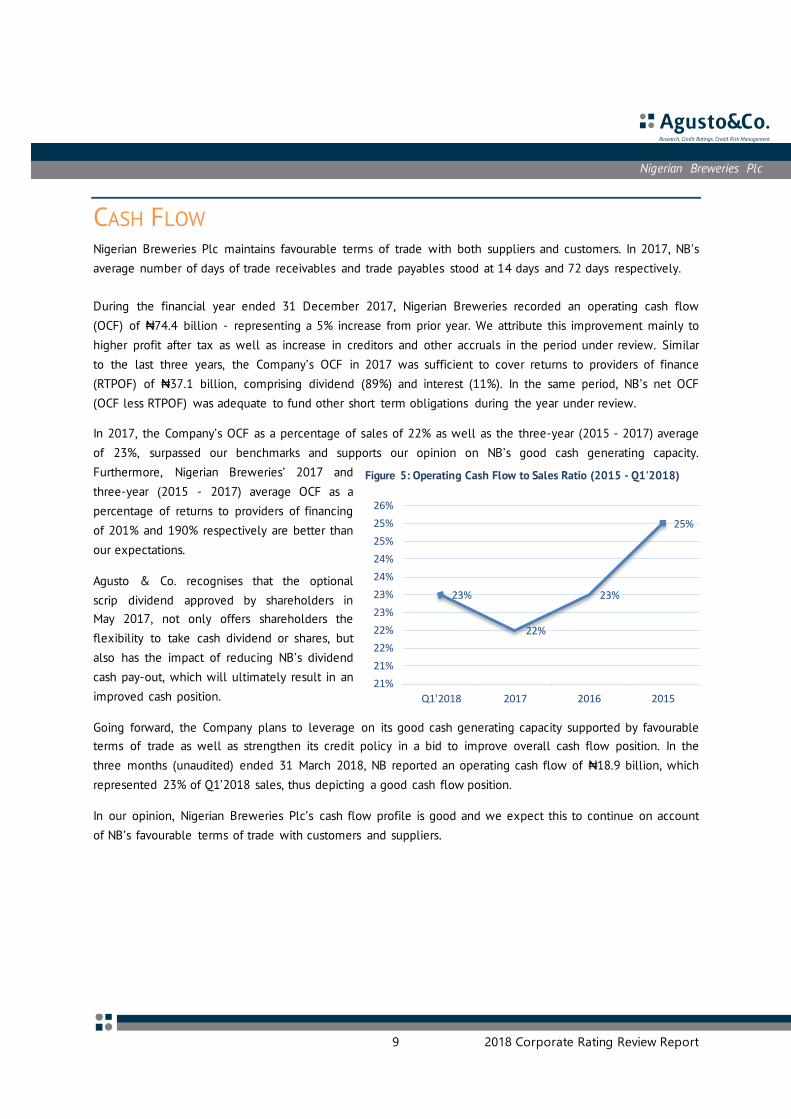

CASH FLOW Nigerian Breweries Plc maintains favourable terms of trade with both suppliers and customers. In 2017, NB’s

average number of days of trade receivables and trade payables stood at 14 days and 72 days respectively.

During the financial year ended 31 December 2017, Nigerian Breweries recorded an operating cash flow

(OCF) of ₦74.4 billion - representing a 5% increase from prior year. We attribute this improvement mainly to

higher profit after tax as well as increase in creditors and other accruals in the period under review. Similar

to the last three years, the Company’s OCF in 2017 was sufficient to cover returns to providers of finance

(RTPOF) of ₦37.1 billion, comprising dividend (89%) and interest (11%). In the same period, NB’s net OCF

(OCF less RTPOF) was adequate to fund other short term obligations during the year under review.

In 2017, the Company’s OCF as a percentage of sales of 22% as well as the three-year (2015 - 2017) average

of 23%, surpassed our benchmarks and supports our opinion on NB’s good cash generating capacity.

Furthermore, Nigerian Breweries’ 2017 and

three-year (2015 - 2017) average OCF as a

percentage of returns to providers of financing

of 201% and 190% respectively are better than

our expectations.

Agusto & Co. recognises that the optional

scrip dividend approved by shareholders in

May 2017, not only offers shareholders the

flexibility to take cash dividend or shares, but

also has the impact of reducing NB’s dividend

cash pay-out, which will ultimately result in an

improved cash position.

Going forward, the Company plans to leverage on its good cash generating capacity supported by favourable

terms of trade as well as strengthen its credit policy in a bid to improve overall cash flow position. In the

three months (unaudited) ended 31 March 2018, NB reported an operating cash flow of ₦18.9 billion, which

represented 23% of Q1’2018 sales, thus depicting a good cash flow position.

In our opinion, Nigerian Breweries Plc’s cash flow profile is good and we expect this to continue on account

of NB’s favourable terms of trade with customers and suppliers.

23%

22%

23%

25%

21%

21%

22%

22%

23%

23%

24%

24%

25%

25%

26%

Q1'2018 2017 2016 2015

Figure 5: Operating Cash Flow to Sales Ratio (2015 - Q1'2018)

10 2018 Corporate Rating Review Report

Nigerian Breweries Plc

FINANCING STRUCTURE AND ADEQUACY OF WORKING CAPITAL

As at 31 December 2017, Nigerian Breweries’ working assets stood at ₦65.8 billion, representing a 23%

increase from prior year. The major components of the working assets as at same date were stocks (56%),

trade debtors (20%) and deposits for imports (11%). Over the last three years (2015 – 2017), the Company’s

working asset position has increased with inventory accounting for the largest portion, owing to a deliberate

management policy of holding optimum stock levels as well as attendant impact of exchange rate

differential on cost of imported raw materials.

As at the end of 2017, the Company’s spontaneous financing (non-interest bearing liabilities) increased by

7% to ₦196.1 billion (2016: ₦183.9 billion), on the back of an increase in trade creditors, other creditors and

accruals as well as rise in amounts due to related parties. The main composition of NB’s spontaneous

financing are trade creditors (20%), amounts due to related parties (18%), advance deposits for returnable

packaging materials (15%) and other creditors & accrual (12%). Similar to the last three years, Nigerian

Breweries’ spontaneous financing was sufficient to cover working assets, leaving a short-term financing

surplus (STFS) of ₦130.2 billion as at FYE 2017. This trend is consistent with industry practice as payments

are generally received in advance from customers, while suppliers offer substantial trade credits.

As at 31 December 2017, Nigerian Breweries Plc’s long term assets stood at ₦300.9 billion, representing a

marginal decline from prior year. As at the same date, NB’s long term funds of ₦186.1 billion, comprising

equity (96%) and long term borrowing (4%), was insufficient to cover the long term assets, thus leaving a

long term financing need (LTFN) of ₦114.8 billion. Agusto & Co. notes that this long term financing need

was adequately covered by the Company’s short term financing surplus, leaving an overall working capital

surplus of ₦15.3 billion.

Over the last three years (2015 - 2017), NB has

consistently posted short term financing surpluses

as well as potential long term financing needs

(LTFN). Nevertheless, the Company’s short-term

financing surpluses have been adequate to cover

the long term financing needs, except for 2015.

In our opinion, the Company has adequate working

capital but the financing structure requires

improvement.

130.2 130.4120.2

114.8 119.1

137.3

0

20

40

60

80

100

120

140

2017 2016 2015

STFS LTFN

Figure 6: STFS vs LTFN

11 2018 Corporate Rating Review Report

Nigerian Breweries Plc

LEVERAGE Nigerian Breweries Plc total liabilities stood at ₦204.5 billion as at FYE 2017, mainly comprising non-interest

bearing liabilities (96%) and interest bearing liabilities (4%). As at the same date, non-interest bearing

liabilities (NIBL) of ₦196.1 billion mostly consisted of trade creditors (20%), amounts due to related parties

(18%), advance deposits for returnable packaging materials (15%) and other creditors & accrual (12%).

Whereas, interest bearing liabilities (IBL) of ₦8.4 billion, comprised principally the outstanding portion of

NB’s long term unsecured revolving credit facilities4.

As at FYE 2017, the Company’s interest expenses to sales ratio remained within our expectation at 1.2%,

while the interest coverage ratio of 17 times surpassed our benchmark. Agusto & Co. notes positively that

Nigerian Breweries has a strong track record and good credit history, which it leverages to access funds at

lower rates in the market.

As at 31 December 2017, Nigerian Breweries’ total assets were funded by total liabilities (54%) and

shareholders’ fund (46%), thus depicting a satisfactory equity cushion. Nonetheless, we note positively that

over 96% of the Company’s total liabilities are non-interest bearing. As at the same date, NB’s IBL to equity

ratio at 5% as well as net liabilities (total liabilities less cash) as a percentage of average total assets at 52%

are in line with our expectations.

As at the three months ended 31 March 2018 (Q1’2018), some of the Company’s key leverage indices such as

interest expense to sales ratio at 3% and interest coverage ratio at 8 times, were in line with our

expectations. In addition, IBL to equity ratio at 5% and net liabilities (total liabilities less cash) as a

percentage of average total assets of 50% are better than our benchmarks.

In our opinion, Nigerian Breweries has low leverage.

4 This refers to the outstanding portion of unsecured revolving credit facilities with five Nigerian banks to finance NB’s working capital.

The total cumulative approved limit amounts to ₦66 billion, with each bank’s loan having a tenor of five years.

3.0%

1.2% 1.3%

2.1%

8

1817

12

0

2

4

6

8

10

12

14

16

18

20

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

Q1'2018 2017 2016 2015

Inte

rest

cov

erag

e ra

tio

(tim

es)

Inte

rest

exp

ense

s to

sal

es (

%)

Figure 7: Interest expense to Sales & Interest Coverage Figure 8: Net Liabilities to Total Assets

50%52%

54%52%

0%

10%

20%

30%

40%

50%

60%

Q1'2018 2017 2016 2015

12 2018 Corporate Rating Review Report

Nigerian Breweries Plc

OWNERSHIP, MANAGEMENT & STAFF

At the 71st Annual General Meeting held on 3 May 2017, the shareholders approved for the increase in the

authorized share capital of the Company to ₦5 billion divided into 10 billion ordinary shares at 50 kobo

each, from the previous ₦4 billion divided into 8 billion ordinary shares at 50 kobo each. Subsequently, the

Company issued scrip shares bringing the total issued share capital to ₦3,998,451,000 divided into

7,996,902,051 ordinary shares of 50 kobo each as at 31 December 2017.

Heineken N.V Group still holds majority shareholding (55.95%) of the Company through its 100% owned

subsidiaries - Heineken Brouwerijen B.V (37.76%), Distilled Trading International B.V (15.47%) and Heineken

International B.V (2.72%) as at 31 December 2017. Stanbic Nominees Nigeria Limited (13.28%) and other

individuals & institutional investors (30.77%) held the remaining issued shares as at the same date. Agusto

& Co. notes that although the

Company’s ownership structure is

somewhat concentrated in our opinion,

the parent company remains one of the

largest brewing and most respected

brands in the world.

Nigerian Breweries Plc has a twelve-

member Board of Directors, which is

composed of eight Non-Executive

Directors and four Executive Directors,

and its members are drawn from

diversified backgrounds with vast

experience in board management.

Chief Kolawole B. Jamodu, a foremost industrialist and renowned chartered accountant, leads the Board as

Chairman – a position he has held since 1 January 2008, while Mr. Jordi Borrut Bel was appointed as the

Managing Director/CEO in January 2018 replacing the interim Managing Director, Mr. Johan A. Doyer. Prior to

the appointment of the Interim MD/CEO, Mr. Nicolaas A. Vervelde, a long standing Managing Director/CEO

since August 2010, resigned his appointment in June 2017 to take up a new role within the Heineken N.V.

Group outside Nigeria. Nigerian Breweries Board of Directors maintains four committees (Nomination

Committee; Remuneration Committee; Audit Committee; and Risk Management Committee), who oversee the

affairs of the management team.

Subsequent to the 2017 FYE, Messers. Victor Famuyibo and Hubert I. Eze resigned their appointments as

Human Resources Director and Sales Director respectively. Mr. Famuyibo attained the mandatory retirement

age, while Mr. Eze took up a new assignment in the Heineken N.V. Group outside Nigeria. In the same vein,

Mr. Olusegun S. Adebanji resigned his appointment as a non-executive director in May 2018.

Source: Nigerian Breweries Plc 2017 Annual Report

Figure 9: Breakdown of NB’s Shareholding Structure as at 31 December 2017

Heineken Brouwerijen B.V, 37.76%

Distilled Trading Int'l B.V, 15.47%

Heineken International

B.V, 2.72%

Stanbic Nominees Nig. Ltd,

13.28%

Other individuals

&

Institutions, 30.77%

13 2018 Corporate Rating Review Report

Nigerian Breweries Plc

The Company’s management team is composed of executive directors and senior management personnel

covering various segments of the business. Members of the management team report directly to the MD/CEO.

In the year under review, Mrs. Grace Omo-Lamai and Mr. Uche Unigwe, were appointed as Human Resources

Director and Sales Director respectively. We note that the majority of the members of the management team

have been with the Company for more than a decade, having also worked within the Heineken N.V Group in

various capacities both locally and internationally. Agusto & Co. notes positively that the Company’s

management team is stable, qualified and experienced.

Nigerian Breweries Plc has a robust coaching programme within Heineken N.V Group, which affords staff

opportunities for cross-border experience. In the year under review, 17 Nigerian employees were deployed to

different Heineken operating companies across the world. The Company has a very robust training

programme, which cuts across all functions and different cadres of staff. In the financial year under review,

about 2,794 employees participated in various training programmes, both locally and internationally.

As at 31 December 2017, Nigerian Breweries had 3,328 staff on its payroll, compared to 3,646 personnel in

2016. The reduction in staff number was largely due to the shut down and subsequent conversion of Makurdi

Brewery into a distribution centre. In the same period under review, the Company’s average cost per

employee amounted to ₦12.5 million, representing a growth of 17% over prior year. NB’s operating profit per

staff of ₦29 million was able to cover the average cost per employee 2.3 times during the same period.

Overall, we consider the Company’s staff productivity level to be satisfactory.

Management Team

Mr. Jordi Borrut Bel

Mr. Borrut Bel was appointed Managing Director/CEO of the Company on 22 January 2018. He joined the

Heineken N.V. Group in 1997 as a Sales Representative at Heineken Spain. He has held various commercial

positions, first as Distribution Project Manager in Slovakia and thereafter as Brand Manager at Heineken

France followed by a Trade Marketing role at Group Commerce in Amsterdam. He returned to Heineken Spain

first as Regional Sales Director, then On-Premise National Sales Director and subsequently On-Premise Sales

and Distribution Director. Mr. Borrut Bel was, until his appointment to his current position in Nigerian

Breweries Plc, the Managing Director of Brarudi SA, the Heineken Operating Company in Burundi.

Table 3: Other members of Nigerian Breweries Plc’s senior management team

Mr. Mark P. Rutten Finance Director

Mr. Hendrik Wymenga Supply Chain Director

Mr. Franco Maggi Marketing Director

Mrs. Grace Omo-Lamai Human Resources Director

Mr. Uche Unigwe Sales Director

Mr. Kufre Ekanem Corporate Affairs Adviser

Mr. Uaboi G. Agbebaku Company Secretary/Legal Adviser Source: Nigerian Breweries Plc 2017 annual report and management presentation

14 2018 Corporate Rating Review Report

Nigerian Breweries Plc

OUTLOOK In the financial year ended 31 December 2017, Nigerian Breweries Plc’s financial condition was characterised

by good cash flow, low leverage and good profitability. However, the Company’s long term financing

structure requires improvement in our opinion. Agusto & Co. notes positively that the Company’s strong

leadership position in the Brewery Industry is supported by a wide product breadth, strong brand across

different segments and good route to market covering over 525,000 retail touch points. In addition, the

Company enjoys strong parental support from Heineken N.V Group of the Netherlands – the second largest

brewing company in the world.

Agusto & Co. notes that though NB’s topline performance grew in 2017, there were pressures on margins, as

down trading was a prominent feature with consumers moving to lower priced brands due to economic

downturn. In spite of these macroeconomic challenges amongst others, Nigerian Breweries was able to

improve its overall profitability performance in 2017 by moderating operating and interest costs as well as

increase its prices, which resulted in a satisfactory return on assets of 13.3% and return on equity of 26.1%.

In the short term, we expect NB’s cash flow to remain strong precipitated by optimal operating cycle. In

addition, we expect leverage to remain within acceptable limits, strongly supported by the Company’s strong

track record and good credit history, which it leverages to access low cost funding in the market.

Agusto & Co. believes that the Nigerian Brewery Industry has huge potential for growth despite the huge

infrastructure deficits, increasing competition as well as weak consumer disposable income - which has put

premium brands under pressure. In our view, the Industry’s outlook remains positive on account of the good

industry fundamentals such as youthful & growing population, low beer consumption per capital of 11.8

litres, improving urbanisation rate of 4.3%5 and opportunities for export to West African countries.

Agusto & Co. is of the view, that Nigerian Breweries’ twin strategic objective of Cost Leadership (hinged on a

strong central backbone with efficient processes and economies of scale) and Market Leadership (buttressed

by strong brands, affordable prices and increased market share) bolstered by continuous innovation, will

enable the Company retain leadership position in the market and take advantage of the Industry’s inherent

potentials in the short to medium term.

Based on the aforementioned, we attach a stable outlook to Nigerian Breweries Plc.

5 CIA World Fact Book on Nigeria

15 2018 Corporate Rating Review Report

Nigerian Breweries Plc

FINANCIAL SUMMARY STATEMENT OF FINANCIAL POSITION FOR THE YEAR

ENDED

31-Dec-17 31-Dec-16 31-Dec-15

₦'000 ₦'000 ₦'000

ASSETS

IDLE CASH 15,865,776 4.1% 12,155,254 3.3% 5,105,713 1.4%

MARKETABLE SECURITIES & TIME DEPOSITS

CASH & EQUIVALENTS 15,865,776 4.1% 12,155,254 3.3% 5,105,713 1.4%

FX PURCHASED FOR IMPORTS 7,474,027 2.0% 8,429,048 2.3% 2,233,797 0.6%

ADVANCE PAYMENTS AND DEPOSITS TO SUPPLIERS

STOCKS 36,988,387 9.7% 24,785,242 6.7% 22,257,253 6.2%

TRADE DEBTORS 13,137,794 3.4% 12,753,803 3.5% 11,719,662 3.3%

DUE FROM RELATED PARTIES 1,499,014 0.4% 1,042,728 0.3% 742,304 0.2%

OTHER DEBTORS & PREPAYMENTS 6,786,189 1.8% 6,478,662 1.8% 5,091,462 1.4%

TOTAL TRADING ASSETS 65,885,411 17.2% 53,489,483 14.5% 42,044,478 11.8%

INVESTMENT PROPERTIES - 2,453,836 0.7% 4,177,379 1.2%

OTHER NON-CURRENT INVESTMENTS 829,625 0.2% 829,625 0.2% 829,625 0.2%

PROPERTY, PLANT & EQUIPMENT 195,050,394 51.0% 190,996,700 52.0% 197,108,847 55.3%

SPARE PARTS, RETURNABLE CONTAINERS, ETC 5,740,475 1.5% 6,459,461 1.8% 6,152,450 1.7%

GOODWILL, INTANGIBLES & OTHER L T ASSETS 99,354,859 26.0% 101,255,556 27.5% 101,288,631 28.4%

TOTAL LONG TERM ASSETS 300,975,353 78.6% 301,995,178 82.1% 309,556,932 86.8%

TOTAL ASSETS 382,726,540 100.0% 367,639,915 100.0% 356,707,123 100.0%

Growth 4.1% 3.1% 2.0%

LIABILITIES & EQUITY

SHORT TERM BORROWINGS 470,930 0.1% 870,611 0.2% 22,214,988 6.2%

CURRENT PORTION OF LONG TERM BORROWINGS

LONG-TERM BORROWINGS 8,000,000 2.1% 17,000,000 4.6% -

TOTAL INTEREST BEARING LIABILITIES (TIBL) 8,470,930 2.2% 17,870,611 4.9% 22,214,988 6.2%

TRADE CREDITORS 39,597,344 10.3% 28,649,372 7.8% 26,313,230 7.4%

DUE TO RELATED PARTIES 35,883,080 9.4% 32,624,891 8.9% 14,736,561 4.1%

ADVANCE PAYMENTS AND DEPOSITS FROM CUSTOMERS 29,930,949 7.8% 31,450,256 8.6% 30,668,755 8.6%

OTHER CREDITORS AND ACCRUALS 23,234,670 6.1% 19,596,065 5.3% 14,107,127 4.0%

TAXATION PAYABLE 19,553,190 5.1% 18,989,567 5.2% 20,215,330 5.7%

DIVIDEND PAYABLE 8,028,742 2.1% 12,676,038 3.4% 12,399,599 3.5%

DEFERRED TAXATION 26,666,864 1.0% 29,876,508 1.0% 31,914,564 1.0%

OBLIGATIONS UNDER UNFUNDED PENSION SCHEMES 13,209,837 3.5% 10,101,065 2.7% 11,903,504 3.3%

MINORITY INTEREST

REDEEMABLE PREFERENCE SHARES

TOTAL NON-INTEREST BEARING LIABILITIES 196,104,676 45.3% 183,963,762 42.9% 162,258,670 37.5%

TOTAL LIABILITIES 204,575,606 53.5% 201,834,373 54.9% 184,473,658 51.7%

SHARE CAPITAL 3,998,451 1.0% 3,964,551 1.1% 3,964,551 1.1%

SHARE PREMIUM 73,770,356 19.3% 64,950,103 17.7% 64,950,103 18.2%

IRREDEEMABLE DEBENTURES

REVALUATION SURPLUS 748,450 0.2% 571,106 0.2% 365,702 0.1%

OTHER NON-DISTRIBUTABLE RESERVES -

REVENUE RESERVE 99,633,677 26.0% 96,319,782 26.2% 102,953,109 28.9%

SHAREHOLDERS' EQUITY 178,150,934 46.5% 165,805,542 45.1% 172,233,465 48.3%

TOTAL LIABILITIES & EQUITY 382,726,540 100.0% 367,639,915 100.0% 356,707,123 100.0%

16 2018 Corporate Rating Review Report

Nigerian Breweries Plc

STATEMENT OF COMPREHENSIVE INCOME FOR THE

YEAR ENDED

31-Dec-17 31-Dec-16 31-Dec-15

₦'000 ₦'000 ₦'000

TURNOVER 344,562,517 100.0% 313,743,147 100.0% 293,905,792 100.0%

COST OF SALES (201,013,357) -58.3% (178,218,528) -56.8% (151,443,890) -51.5%

GROSS PROFIT 143,549,160 41.7% 135,524,619 43.2% 142,461,902 48.5%

OTHER OPERATING EXPENSES (88,641,438) -25.7% (83,231,870) -26.5% (80,676,444) -27.4%

OPERATING PROFIT 54,907,722 15.9% 52,292,749 16.7% 61,785,458 21.0%

OTHER INCOME/(EXPENSES) (4,109,586) -1.2% (8,631,850) -2.8% (1,124,848) -0.4%

PROFIT BEFORE INTEREST & TAXATION 50,798,136 14.7% 43,660,899 13.9% 60,660,610 20.6%

INTEREST EXPENSE (4,225,823) -1.2% (4,037,985) -1.3% (6,152,242) -2.1%

PROFIT BEFORE TAXATION 46,572,313 13.5% 39,622,914 12.6% 54,508,368 18.5%

TAX (EXPENSE) BENEFIT (13,563,021) -3.9% (11,226,137) -3.6% (16,458,850) -5.6%

PROFIT AFTER TAXATION 33,009,292 9.6% 28,396,777 9.1% 38,049,518 12.9%

NON-RECURRING ITEMS (NET OF TAX) (1,449,678) -0.4% 1,304,129 0.4% (837,623) -0.3%

MINORITY INTERESTS IN GROUP PAT

PROFIT AFTER TAX & MINORITY INTERESTS 31,559,614 9.2% 29,700,906 9.5% 37,211,895 12.7%

DIVIDEND (28,453,982) -8.3% (36,473,864) -11.6% (37,266,774) -12.7%

PROFIT RETAINED FOR THE YEAR 3,105,632 0.9% (6,772,958) -2.2% (54,879) 0.0%

SCRIP ISSUES

OTHER APPROPRIATIONS/ ADJUSTMENTS 208,263 139,631 281,488

PROFIT RETAINED B/FWD 96,319,782 102,953,109 102,726,500

PROFIT RETAINED C/FWD 99,633,677 96,319,782 102,953,109

Proof - - -

ADDITIONAL INFORMATION 31-Dec-17 31-Dec-16 31-Dec-15

Staff costs (₦'000) 41,640,292 39,031,407 38,047,404

Average number of staff 3,328 3,646 3,777

Staff costs per employee (₦'000) 12,512 10,705 10,073

Staff costs/Turnover 12% 12% 13%

Capital expenditure (₦'000) 37,352,323 22,312,880 30,554,005

Depreciation expense - current year (₦'000) 32,686,134 28,268,009 26,854,735

(Profit)/Loss on sale of assets (₦'000) - - -

Number of 50 kobo shares in issue at year end ('000) 7,996,902 7,929,101 7,929,101

Market value per share of 50 kobo (year end) 13,490 14,200 13,600

Market capitalisation (₦'000) 1,078,782,080 1,125,932,484 1,078,357,872

Market/Book value multiple 6 7 6

Non-operating assets at balance sheet date (₦'000) 829,625 3,283,461 5,007,004

Market value of tradeable assets (₦'000)

Revaluation date - Investment properties

Revaluation date - Other properties

Average age of depreciable assets (years) 6 7 4

Sales at constant prices - base year 1985 (₦'000) 1,193,914 1,236,758 1,373,680

Auditors DELOITTE &

TOUCHE

DELOITTE &

TOUCHE

DELOITTE &

TOUCHE

Opinion CLEAN CLEAN CLEAN

17 2018 Corporate Rating Review Report

Nigerian Breweries Plc

CASH FLOW STATEMENT FOR YEAR ENDED 31-Dec-17 31-Dec-16 31-Dec-15

=N='000 =N='000 =N='000

OPERATING ACTIVITIES

Profit after tax 33,009,292 28,396,777 38,049,518

ADJUSTMENTS

Interest expense 4,225,823 4,037,985 6,152,242

Minority interests in Group PAT - - -

Depreciation 32,686,134 28,268,009 26,854,735

(Profit)/Loss on sale of assets - - -

Other non-cash items 385,607 345,035 405,514

Potential operating cash flow 70,306,856 61,047,806 71,462,009

INCREASE/(DECREASE) IN SPONTANEOUS FINANCING:

Trade creditors 10,947,972 2,336,142 (25,382,476)

Due to related parties 3,258,189 17,888,330 6,185,719

Advance payments and deposits from customers (1,519,307) 781,501 30,668,755

Other creditors & accruals 3,638,605 5,488,938 (9,462,651)

Taxation payable 563,623 (1,225,763) (2,729,299)

Deferred taxation (3,209,644) (2,038,056) 4,080,832

Obligations under unfunded pension schemes 3,108,772 (1,802,439) 1,167,908

Minority interest - - -

Cash from (used by) spontaneous financing 16,788,210 21,428,653 4,528,788

(INCREASE)/DECREASE IN WORKING ASSETS:

FX purchased for imports 955,021 (6,195,251) (1,869,123)

Advance payments and deposits to suppliers - - -

Stocks (12,203,145) (2,527,989) 84,340

Trade debtors (383,991) (1,034,141) (425,734)

Due from related parties (456,286) (300,424) (307,795)

Other debtors & prepayments (307,527) (1,387,200) 1,359,756

Cash from (used by) working assets (12,395,928) (11,445,005) (1,158,556)

CASH FROM (USED IN) OPERATING ACTIVITIES 74,699,138 71,031,454 74,832,241

RETURNS TO PROVIDERS OF FINANCING

Interest paid (4,225,823) (4,037,985) (6,152,242)

Dividend paid (33,101,278) (36,197,425) (32,430,466)

CASH USED IN PROVIDING RETURNS ON FINANCING (37,327,101) (40,235,410) (38,582,708)

OPERATING CASH FLOW AFTER PAYMENTS TO

PROVIDERS OF FINANCING 37,372,037 30,796,044 36,249,533

NON-RECURRING ACTIVITIES

Non-recurring items (net of tax) (1,449,678) 1,304,129 (837,623)

CASH FROM (USED IN) NON-RECURRING ACTIVITIES (1,449,678) 1,304,129 (837,623)

INVESTING ACTIVITIES

Capital expenditure (37,352,323) (22,312,880) (30,554,005)

Sale of assets 612,495 157,018 160,047

Purchase of other long term assets (net) (2,925,926)

Sale of other long term assets (net) 5,073,519 1,449,607 -

CASH FROM (USED IN) INVESTING ACTIVITIES (31,666,309) (20,706,255) (33,319,884)

FINANCING ACTIVITIES

Increase/(Decrease) in short term borrowings (399,681) (21,344,377) 21,984,608

Increase/(Decrease) in long term borrowings (9,000,000) 17,000,000 (24,670,000)

Proceeds of shares issued 8,854,153 - -

CASH FROM (USED IN) FINANCING ACTIVITIES (545,528) (4,344,377) (2,685,392)

CHANGE IN CASH INC/(DEC) 3,710,522 7,049,541 (593,366)

OPENING CASH & MARKETABLE SECURITIES 12,155,254 5,105,713 5,699,079

CLOSING CASH & MARKETABLE SECURITIES 15,865,776 12,155,254 5,105,713

18 2018 Corporate Rating Review Report

Nigerian Breweries Plc

STATEMENT OF CASHFLOW SUMMARY 31-Dec-17 31-Dec-16 31-Dec-15

₦'000 ₦'000 ₦'000

Operating cash flow (OCF) 74,699,138 71,031,454 74,832,241

Less: Returns to providers of finance (37,327,101) (40,235,410) (38,582,708)

OCF after returns to providers of finance 37,372,037 30,796,044 36,249,533

Non-recurring items (1,449,678) 1,304,129 (837,623)

Free cash flow 35,922,359 32,100,173 35,411,910

Investing activities (31,666,309) (20,706,255) (33,319,884)

Financing activities (545,528) (4,344,377) (2,685,392)

Change in cash 3,710,522 7,049,541 (593,366)

PROFITABILITY 2017 2016 2015

PBT as % of turnover 14% 13% 19%

Return on equity 27% 23% 32%

Real sales growth -3.5% -10.0% 0.7%

Sales growth 9.8% 6.7% 10.3%

ROA (pre-tax) 12.41% 10.94% 15.43%

CASH FLOW

Interest cover (times) 17.7 17.6 12.2

Principal payback (years) - - -

WORKING CAPITAL

Working capital need (days) - - -

Working capital deficiency (days) - - 21

LEVERAGE

Interest bearing debt to Equity 5% 11% 13%

Total debt to Equity 115% 122% 107%

IBD net of cash and Equiv. as a % of Equity without rev. 0% 3% 10%

Net Debt/Avg Total Assets Exc. Cash and Rev. Surplus 52% 54% 52%

19 2018 Corporate Rating Review Report

Nigerian Breweries Plc

RATING DEFINITIONS Aaa This is the highest rating category. It indicates a company with impeccable financial

condition and overwhelming ability to meet obligations as and when they fall due.

Aa This is a company that possesses very strong financial condition and very strong

capacity to meet obligations as and when they fall due. However, the risk factors are

somewhat higher than for Aaa obligors.

A This is a company with good financial condition and strong capacity to repay

obligations on a timely basis.

Bbb This refers to companies with satisfactory financial condition and adequate capacity to

meet obligations as and when they fall due.

Bb This refers to companies with satisfactory financial condition but capacity to meet

obligations as and when they fall due may be contingent upon refinancing. The

company may have one or more major weakness (es).

B This refers to a company that has weak financial condition and capacity to meet

obligations in a timely manner is contingent on refinancing.

C This refers to an obligor with very weak financial condition and weak capacity to meet

obligations in a timely manner.

D In default.

Rating Category Modifiers

A "+" (plus) or "-" (minus) sign may be assigned to ratings from ‘Aa’ to ‘C’ to reflect comparative position within the rating category. Therefore, a

rating with + (plus) attached to it is a notch higher than a rating without the + (plus) sign and two notches higher than a rating with the -

(minus) sign.

20 2018 Corporate Rating Review Report

THIS PAGE HAS BEEN LEFT BLANK INTENTIONALLY

www.agusto.com

© Agusto&Co.

UBA House (5th Floor)

57 Marina Lagos

Nigeria.

P.O Box 56136 Ikoyi

+234 (1) 2707222-4

+234 (1) 2713808

Fax: 234 (1) 2643576

Email: [email protected]