2017 hotels in india trends & opportunities of black money ... 1 department of industrial policy...

TRANSCRIPT

Achin Khanna, MRICS

Managing Director

Sanaya JijinaAssociate

HVS | 2nd Floor, Paras Downtown Centre, Golf Course Road, Sector 53, Gurugram 122 002, INDIAHVS.com

2017

HOTELS IN INDIATRENDS & OPPORTUNITIES

PAGE 2 | 2017 HOTELS IN INDIA TRENDS & OPPORTUNITIES

SleepisSilver,butMoneyisGold!-CityofDjinns,WilliamDalrymple

Introduction

As the 6AM alarm blares at dawn, who doesn't finddelight in pressing the snooze button ever so often?After all, sleep is silver.However, brushing aside theslumber,theactivemindsketchestasksaheadandoneleaps into the daily bustle. Crafting ideas, plottingschedulesandplanningconquests,thebusinessoflifeand livelihood comes into play.While catching fortywinks every now and then may be acceptable, oneusuallywouldn'ttradethejobofmakingmoneywiththelibertytoindulgeindailyafternoonsiestas.Afterall,moneyisgold!

The Indian hospitality sector has woken up after alongishnapand,itisnowtimetosetthecashregistersringing. While an assortment of influences hadrepressedthesector'sendeavourstogrowfrom2009to2015,lastyearprovidedsufficientevidencethatthenextup-cyclewas in theoffing.Resultantly,2016/17playedwitnesstoayear,thathasinnouncertaintermsbeenpositiveonallfronts.Nationwideoccupancywasthe highest since 2008, countrywide average roomrates clocked a clear and measurable increase overseveralprecedingyearsandtheoverallsupply-demandscale is now tilted squarely in favour of growth indemandoutpacingnewsupply.The time to reaphasarrived and industry stakeholders must not losecognizanceofthefactthattheinherentcyclicalnatureofthehotelbusinesswouldallowthisopportunityonlyforafiniteperiod.Lestwechoosetodozeoffagain,itistime for us hoteliers to truly elevate the sectoralperformancetothenextlevel.Indeed,SleepisSilver,butMoneyisGold!

Number of Rooms (00's) Number of Hotels Average Number of Rooms Per Hotel

FIGURE 1: SURVEY PARTICIPATION (1995/96 – 2016/17)

Source: HVS Research

Forover20years,HVShasgathereddatapertainingtothe hotel performance of the country through theannualTrends&OpportunitiesSurvey.Theresultantreportdepictsandanalyseskeyhospitalitytrends,andpresentsHVS'outlook,withanemphasison13majorIndianmarkets.Itfurtheroutlinesexistingandfutureopportunities of specific interest to investors,developersandhoteloperators.

The survey participant base has registered amomentous growth since 1995/96 from 120 hotelswith 18,160 rooms to record 941 hotels with1,19,219roomsin2016/17,anincreaseof54hotelsand5,597roomsovertheprevioussurvey.

ThegrowingnumberofsurveyparticipantseachyeardemonstratesariseinbothHVS'penetrationintothemarket,aswellasthemarket'ssize.Moreover,wehavemademinoralterationstothesamplesetforthetwomostrecentyearsinanattempttoremoveunorganisedsupply. This in turn has led to the 2015/16 figuresundergoingaminorchangeacrossallparameters.

Additionally, like last year, we have weighted thenumberofroomnightstoaccountforthenewsupplythatwasnot operational for the entire fiscal year tocomputetheoveralloccupancyandaveragerate.Theweighted room count of the survey base for2016/17 is 1,15,044, up from 1,08,682 for2015/16.Figure1illustratesthesurveyparticipationforthefiscalyears1995/96to2016/17.

The Indian Economy – An Overview

Indiaisoneofthefastestgrowingmajoreconomiesinthe world. The acceleration of investment friendlypolicies,structuralreformsandlowcommoditypriceshasprovidedastrongimpetusforgrowth.Thecentral

18

2

18

3

21

4

23

2

21

6

25

5

25

6

27

1

28

9

31

2

33

5

34

8

39

7

42

4

49

5

58

6

69

8

86

1

99

3

1,0

85

1,1

36

1,1

92

12

0

12

2

16

3

18

0

17

4

19

9

19

9

21

5

21

1

23

5

25

2

26

8

31

6

34

9

40

7

46

2

55

1

71

7

81

4

87

2

88

7

94

1

151 150

131 129124 128 129 126

137 133 133 130126 122 122

127 127120 122 124 128 127

-

20

40

60

80

100

120

140

160

-

200

400

600

800

1,000

1,200

1,400

government, despite some criticisms, has introducedseveralprogrammesoverthepastyear,includingonesto augment the ease of doing business, encouragedigitalisation, reduce skill insufficiencies, fosterentrepreneurshipandboosturbandevelopment.Thesederegulation measures, both current as well asforeseeable,haveboostedForeignDirectInvestments(FDI),whichregisteredagrowthof8.0%in2016/17¹overtheprecedingyear.

AccordingtotheEconomicSurveyofIndia2016/17,thebuoyancyinthecountry'sGDPremainsunchangedinrecentyears,with2015/16endingata7.6%growthand 2016/17 witnessing a GDP growth of 7.1%. Inparticular,thecountry'sservicessectorgrewat7.7%lastyear,withthetrade,hotels,transportandstoragesubsectorregisteringa7.8%growthestimate.

Figure 2 displays the GDP Growth, Inflation, andExchange Rate for the period from 2012/13 to2016/17.

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

2012/13 2013/14 2014/15 2015/16** 2016/17*

-

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Exchange Rate (`1/US$) GDP Growth Infla�on (CPI)***

FIGURE 2: GDP GROWTH, INFLATION AND EXCHANGE RATE– A FIVE-YEAR TREND

* Advance Estimates** First Revised Estimates*** RBI moved from Wholesale Price Index (WPI) to Consumer Price Index (CPI) in 2014, providing a more accurate indication of inflation

In 2016/17, the average exchange rate of the Indianrupee vis-a-vis the US dollar was `67.09:1US$,displaying a depreciation from the previous year.However,therupeeappreciatedinthelastquarterofthefiscalyearonaccountofbroad-basedweakeningofthe US dollar after the result of the US presidentialelections was greeted with skepticism by foreign-exchangemarkets.On thedomestic front, inflowsbyForeign Institutional Investors (FII), and a narrowerCurrent Account Deficit (CAD) in the first half of2016/17,gaveroomfortherupeetomoveupfurther.Atthetimeofgoingtoprint,theaverageexchangeratewas 64.02:1US$.

ThePrimeMinisterannouncedthe'demonetisation'of500and1,000-rupeenoteson8November2016,withtheintentionofcurbingcorruption,counterfeiting,theaccumulation of blackmoney, and the use of higherdenominationnotesforillegalandterroristactivities–an important development for the entire economy.While themove causeda short-termcashcrunch, itslarger political and economic impacts (both positiveandnegative)willonlybeseeninduetime.

Furthermore, other institutional reforms that are invarious stages of execution, such as the Goods andServices Tax (GST), the four Labour codes, theArbitration and ConciliationAct, and Insolvency andBankruptcy Act 2016, are likely to be significantcontributorstothecountry'seconomicgrowth,goingforward.

Notably,themuch-awaitedGSTwasrolledouton1July2017, under which the Indian hospitality industrystandstobenefitfromhomogeneousanduniformtaxes,inadditiontoeasyutilisationofInputTaxCredit(ITC).

FIGURE 3: GOODS AND SERVICES TAX SLABS

AverageRoomRate(`) GST

Below1,000 Notapplicable

1,001-2,500 12%

2,501-7,500 18%

Above7,500 28%

Inthepast,thetaxesthatwereappliedoninputs,suchas raw materials, food, cleaning supplies, andamenities, could not be adjusted against the outputwithoutmultiplecomplications.ThiswillnowbemucheasierundertheGSTregime.Otheradvantagesofthenewtaxationincludeadministrativeeaseandclarityforend consumers. Now, although, the GST at 28% forroomsaveragingarategreaterthan`7,500isstillthehighestintheregion,theoverallimpactofthisindirecttaxontheIndianhotelsectorislikelytobefavourable.Allinall,withtherobustgrowthindemandoutpacingthatofsupply,ouroutlookforthenation'shospitalityindustryremainsoptimistic,despitetheinitialhiccupsduringtheGSTimplementation.

Travel & Tourism – Facts and Figures

The Travel & Tourism industry has been a majorcontributor to the economic growth of India, and isfundamental in creatingemployment andgeneratingincomeforbothskilledandunskilledlabour.Tourismin India has witnessed steady growth over the past few years, aided by the rising purchasing power of the expanding middle classandtheshiftfromforeigntodomestic tourism. The industry contributed 9.3% of

India's Travel & Tourism sector was the fastest growing among the G20 countries in 2016.

1 Department of Industrial Policy and Promotion 2017 HOTELS IN INDIA TRENDS & OPPORTUNITIES | PAGE 3

5.6%

7.8%

9.8%

8.5%

-

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

-

2,00,000

4,00,000

6,00,000

8,00,000

10,00,000

12,00,000

14,00,000

16,00,000

2012 2013 2014 2015 2016

Direct Contribu�on Total Contribu�on Percentage Change (Direct)

FIGURE 4: TRAVEL & TOURISM CONTRIBUTION TO INDIA'S GDP (2012 – 2016, ` CRORE)

Source: World Travel & Tourism Council's Economic Impact 2017 – India Report

88.0%

12.0%

Domes�c Spending Foreign Visitor Spending

² World Travel & Tourism Council's Economic Impact 2017 – India Report ³ World Travel & Tourism Council

FIGURE 5: SPENDING PATTERNS – CONTRIBUTION TO INDIA'S DIRECT TRAVEL & TOURISM GDP (2016)

5.4%

94.6%

Business SpendingLeisure Spending

FIGURE 7: FOREIGN TOURIST ARRIVALS AND DOMESTIC VISITATION TRENDS (2007 − 2016, IN LAKH)

Source: Ministry of Tourism, Government of India

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Foreign Tourist Arrivals 50.8 52.8 51.7 57.8 63.1 65.8 69.7 76.8 80.3 88.0

% change 4.0% -2.2% 11.8% 9.2% 4.3% 5.9% 10.2% 4.5% 9.7%

Domestic Tourist Visits 5,267.0 5,630.3 6,688.0 7,477.0 8,645.3 10,450.5 11,425.3 12,828.0 14,319.7 16,135.5

% change 6.9% 18.8% 11.8% 15.6% 20.9% 9.3% 12.3% 11.6% 12.7%

FIGURE 8: FOREIGN TOURIST ARRIVALS BY SOURCE COUNTRIES (2016)

Bangladesh

15.7%

U.S.A.

14.7%

U.K.

10.7%

Canada

3.6%Malaysia

3.4%

Sri Lanka

3.4%

Germany

3.0%

France

2.7%

China (including

Taiwan)

3.4%

Australia

3.3%

Others

36.1%

Source: Ministry of Tourism, Government of India

FIGURE 9: TOP 15 BUSIEST AIRPORTS IN INDIA BY PASSENGER TRAFFIC(2015/16 – 2016/17, IN LAKH)

Delhi (DIAL)

Mumbai (MIAL)

Bengaluru (BIAL)

Chennai

Kolkata

Hyderabad (GHIAL)

Cochin (CIAL)

Ahmedabad

Goa

Pune

Source: Airports Authority of India

the total employment (both direct and indirect) in2016². India's Travel & Tourism sectorwas also thefastestgrowingamongtheG20countries,growingby8.5% in 2016³. The followingmatrices highlight theperformanceoftheTravel&TourismindustryinIndia.

FIGURE 6: INDIAN TRAVEL & TOURISM SECTOR – FOREIGN EXCHANGEEARNINGS (2012 – 2016, ` CRORE)

Foreign Exchange Earnings % Change

Source: India Tourism Statistics 2015 – Ministry of Tourism, Government of IndiaState/UT - Wise Domestic and Foreign Tourist Visits, 2015-2016, Ministry of TourismGovernment of India

14.0%

14.5%

9.6%

14.0%

-

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

-

20,000

40,000

60,000

80,000

1,00,000

1,20,000

1,40,000

1,60,000

2012 2013 2014 2015 2016

Lucknow

Thiruvananthapuram

Guwahati

Jaipur

Kozhikode

2015/16

484.2

416.7

189.7

152.2

127.6

123.9

77.5

64.8

53.8

54.2

32.4

34.7

27.8

28.9

23.1

2016/17

577.0

451.5

228.8

183.6

158.2

151.0

89.6

74.1

68.6

67.7

39.7

38.8

37.9

37.8

26.5

% Change

19.2%

8.4%

20.6%

20.7%

24.0%

21.9%

15.6%

14.3%

27.5%

25.0%

22.4%

11.8%

36.1%

31.0%

15.0%

PAGE 4 | 2017 HOTELS IN INDIA TRENDS & OPPORTUNITIES

Up, Up and A-Wait for it?On a nationwide basis, new branded and organisedsupply (when weighted for days open in 2016/17)grewbymerely5.9%overtheprecedingyear.Overalldemand increased by 9.6% in the same period.Marketwide occupancy of 65.6% was consequently3.5%higherthanthe2015/16performanceof63.3%.ItispertinenttonotethatthelasttimeIndiaregisteredanationwideoccupancythatwasnorthof65%wasin2007/08.

When viewed by positioning, Five-Star Deluxe andThree-Star hotels clocked66.5% occupancy each in2016/17, while Four-Starh o t e l s a c h i e ve d 6 5 . 6%occupancy. Five-Star hotelswerejustshyofthe65%markand closed at a nationwide

occupancy of 64.6%, whereas Two-Star hotelsmanaged62.7%.Therefore, it isapparentthathotelsacross all positioning benefited from the supply-demandgapthispastyear.Figure10,below,offersthe

nationwidesupplyanddemandperformancefora15-yearperiod.

AverageRoomRates(ARRs)toohaveshownpromiseasthe nationwide numbers appreciated by 2.4% in2016/17overlastfiscalandwerethehighestinfouryears.Thoughthisincreasewasexpectedtooccur,thedegree to which rates have grown continues to bemarginal. We have been analysing the average ratemovementcloselyforthepastseveraleditionsofthispublicationandhavecommentedat lengthaboutthesector'sinabilitytomovetheneedleontheARRfront.Wereiteratetheneedforrecognisingthefactthatthedemand-supplyequationtodayaswellas inthenext48-60 months is more than likely to present anopportunityforsubstantialaveragerateenhancementand,hoteloperatorsthatdraftstrategiestoseizethisoccasion will have a clear advantage. Indeed, theplanningforrateimprovementsmusthappennowandwhilesomemaychoosetoseekcomfortinthefactthattheirratesarenolongerdeclining,otherswillrealisethat a 2.4% nationwide increase in ARR is still sub-inflationarygrowth.Giventhealmostcertainelevationofoccupancyoverthenextfewyears,enhancingARRssignificantly only makes business sense. We hadmentionedlastyearthatonly2.5%ofIndia'sbrandedsupply averaged a year-round rate of more thanUS$200.Thatnumberwasat3.1%in2016/17.So,eventhoughtheneedleismovingintherightdirection,itspacecoulddowithsomeimprovement.Indiahassomeofthefinesthotelsinthispartoftheworld–bothinurbanaswellasleisuredestinations;theirinabilitytoearn a net room rate that is commensurate to theirproductandserviceofferingisunfortunate.

Available Room Nights Per Day Room Night Demand Per Day Occupancy

* 2015/16 data has been modified to remove the performance of irrelevant supplySource: HVS Research

Marketwide occupancy was r e c o r d e d a t 6 5 . 6 % i n 2016/17. It is pertinent to note that the last time India witnessed a nationwide occupancy that was north of 65% was in 2007/08!

FIGURE 10: ROOM NIGHT DEMAND VS AVAILABLE ROOM NIGHTS (2002/03 – 2016/17)

The Government of India has launched severalbrandingandmarketinginitiativessuchas'IncredibleIndia'and'AthitiDevoBhava',whichhaveprovidedafocuseddrivetogrowth.Ithasalsomadeseriouseffortstoboostinvestmentsinthetourismsectorbyallowing100% FDI through the automatic route. Moreover,'IncredibleIndia2.0'aimsatshowcasingthecountryasa spiritual and wellness destination; with this, thecountryispoisedtoemergeasanimportantwellnessdestinationinSouthAsia.

57.2%

64.8%

69.0%71.5% 71.4%

68.8%

59.5% 59.5% 60.6%

59.3% 57.8% 58.4%59.8%

63.3%65.6%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

1,00,000

1,10,000

2017 HOTELS IN INDIA TRENDS & OPPORTUNITIES | PAGE 5

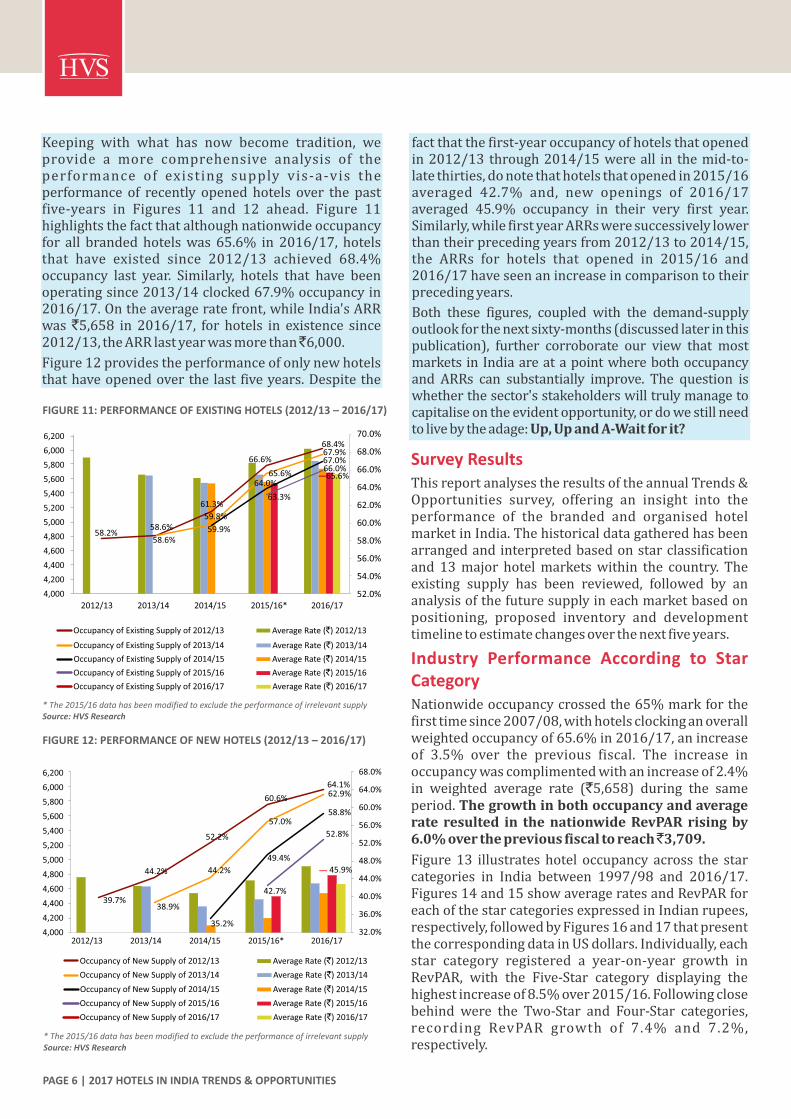

Keeping with what has now become tradition, weprovide a more comprehensive analysis of theperformance of existing supply vis-a-vis theperformance of recently openedhotels over the pastfive-years in Figures 11 and 12 ahead. Figure 11highlightsthefactthatalthoughnationwideoccupancyfor all brandedhotelswas 65.6% in 2016/17, hotelsthat have existed since 2012/13 achieved 68.4%occupancy last year. Similarly, hotels that have beenoperatingsince2013/14clocked67.9%occupancyin2016/17.Ontheaverageratefront,whileIndia'sARRwas`5,658 in 2016/17, for hotels in existence since2012/13,theARRlastyearwasmorethan 6,000.

Figure12providestheperformanceofonlynewhotelsthathaveopenedoverthelast fiveyears.Despitethe

FIGURE 11: PERFORMANCE OF EXISTING HOTELS (2012/13 – 2016/17)

* The 2015/16 data has been modified to exclude the performance of irrelevant supplySource: HVS Research

Survey ResultsThisreportanalysestheresultsoftheannualTrends&Opportunities survey, offering an insight into theperformance of the branded and organised hotelmarketinIndia.Thehistoricaldatagatheredhasbeenarrangedandinterpretedbasedonstarclassificationand 13major hotelmarketswithin the country. Theexisting supply has been reviewed, followed by ananalysisofthefuturesupplyineachmarketbasedonpositioning, proposed inventory and developmenttimelinetoestimatechangesoverthenextfiveyears.

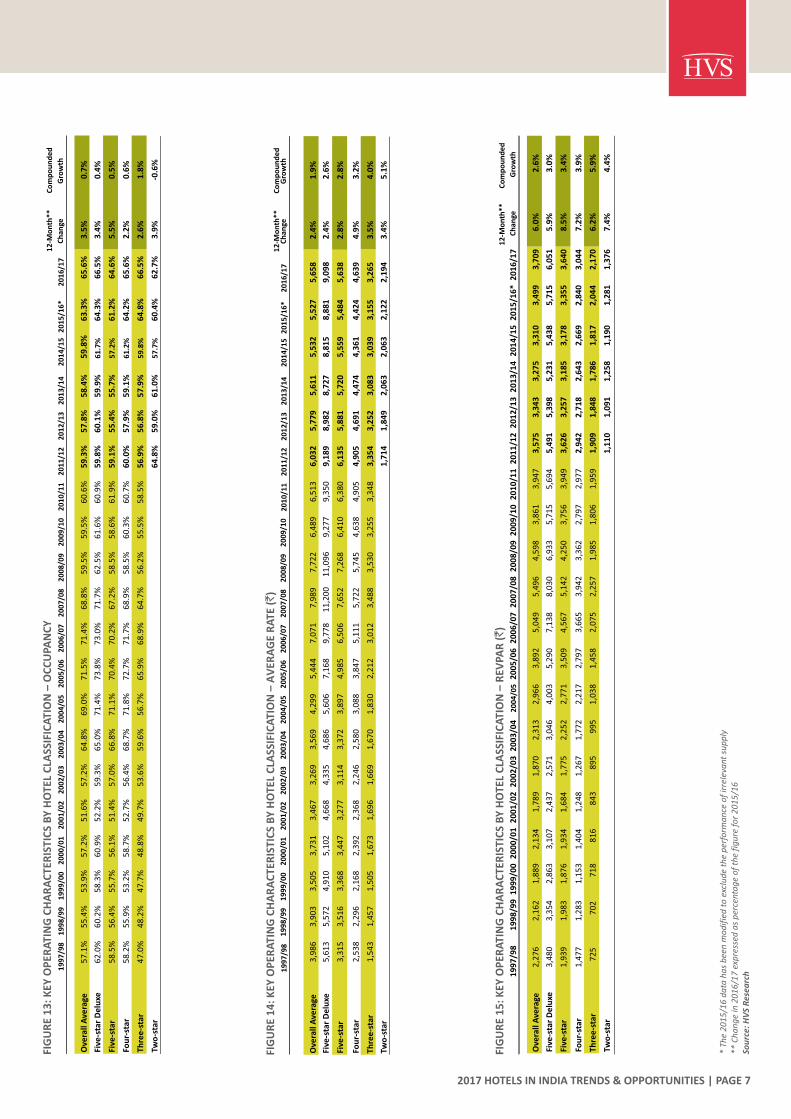

Industry Performance According to Star CategoryNationwideoccupancycrossedthe65%markforthefirsttimesince2007/08,withhotelsclockinganoverallweightedoccupancyof65.6%in2016/17,anincreaseof 3.5% over the previous fiscal. The increase inoccupancywascomplimentedwithanincreaseof2.4%in weighted average rate (`5,658) during the sameperiod.Thegrowthinbothoccupancyandaveragerate resulted in thenationwideRevPARrisingby6.0%overthepreviousfiscaltoreach 3,709.

Figure13 illustrateshotel occupancy across the starcategories in India between 1997/98 and 2016/17.Figures14and15showaverageratesandRevPARforeachofthestarcategoriesexpressedinIndianrupees,respectively,followedbyFigures16and17thatpresentthecorrespondingdatainUSdollars.Individually,eachstar category registered a year-on-year growth inRevPAR, with the Five-Star category displaying thehighestincreaseof8.5%over2015/16.Followingclosebehind were the Two-Star and Four-Star categories,recording RevPAR growth of 7.4% and 7.2%,respectively.

FIGURE 12: PERFORMANCE OF NEW HOTELS (2012/13 – 2016/17)

39.7%

44.2%

52.2%

60.6%

64.1%

38.9%

44.2%

57.0%

62.9%

35.2%

49.4%

58.8%

42.7%

52.8%

45.9%

32.0%

36.0%

40.0%

44.0%

48.0%

52.0%

56.0%

60.0%

64.0%

68.0%

4,000

4,200

4,400

4,600

4,800

5,000

5,200

5,400

5,600

5,800

6,000

6,200

2012/13 2013/14 2014/15 2015/16* 2016/17

* The 2015/16 data has been modified to exclude the performance of irrelevant supplySource: HVS Research

Average Rate (`) 2012/13

Average Rate (`) 2015/16

Average Rate (`) 2013/14

Average Rate (`) 2016/17

Average Rate (`) 2014/15

Occupancy of New Supply of 2013/14

Occupancy of New Supply of 2016/17

Occupancy of New Supply of 2014/15

Occupancy of New Supply of 2012/13

Occupancy of New Supply of 2015/16

Average Rate (`) 2012/13

Average Rate (`) 2015/16

Average Rate (`) 2013/14

Average Rate (`) 2016/17

Average Rate (`) 2014/15

Occupancy of Exis�ng Supply of 2013/14

Occupancy of Exis�ng Supply of 2016/17

Occupancy of Exis�ng Supply of 2014/15

Occupancy of Exis�ng Supply of 2012/13

Occupancy of Exis�ng Supply of 2015/16

factthatthefirst-yearoccupancyofhotelsthatopenedin2012/13through2014/15wereall inthemid-to-latethirties,donotethathotelsthatopenedin2015/16averaged 42.7% and, new openings of 2016/17averaged 45.9% occupancy in their very first year.Similarly,whilefirstyearARRsweresuccessivelylowerthantheirprecedingyearsfrom2012/13to2014/15,the ARRs for hotels that opened in 2015/16 and2016/17haveseenanincreaseincomparisontotheirprecedingyears.

Both these figures, coupled with the demand-supplyoutlookforthenextsixty-months(discussedlaterinthispublication), further corroborate our view that mostmarketsinIndiaareatapointwherebothoccupancyand ARRs can substantially improve. The question iswhetherthesector'sstakeholderswilltrulymanagetocapitaliseontheevidentopportunity,ordowestillneedtolivebytheadage:Up,UpandA-Waitforit?

PAGE 6 | 2017 HOTELS IN INDIA TRENDS & OPPORTUNITIES

52.0%

54.0%

56.0%

58.0%

60.0%

62.0%

64.0%

66.0%

68.0%

70.0%

4,000

4,200

4,400

4,600

4,800

5,000

5,200

5,400

5,600

5,800

6,000

6,200

2012/13 2013/14 2014/15 2015/16* 2016/17

58.2%58.6%

58.6%

61.3%

59.8%

59.9%

66.6%

65.6%64.0%

63.3%

68.4%67.9%67.0%66.0%65.6%

FIG

UR

E 1

4:

KEY

OP

ERA

TIN

G C

HA

RA

CTE

RIS

TIC

S B

Y H

OTE

L C

LASS

IFIC

ATI

ON

– A

VER

AG

E R

ATE

(`)

1

99

7/9

81

99

8/9

91

99

9/0

02

00

0/0

12

00

1/0

22

00

2/0

32

00

3/0

42

00

4/0

52

00

5/0

62

00

6/0

72

00

7/0

82

00

8/0

92

00

9/1

02

01

0/1

12

01

1/1

22

01

2/1

32

01

3/1

42

01

4/1

52

01

5/1

6*

20

16

/17

12

-Mo

nth

**

Ch

ange

Co

mp

ou

nd

ed

G

row

th

Ove

rall

Ave

rage

3,9

86

3,9

03

3,5

05

3,7

31

3,4

67

3,2

69

3,5

69

4,2

99

5,4

44

7,0

71

7,9

89

7,7

22

6,4

89

6,5

13

6,0

32

5,7

79

5,6

11

5,5

32

5,5

27

5,6

58

2.4

%1

.9%

Five

-sta

r D

elu

xe5

,61

35

,57

24

,91

05

,10

24

,66

84

,33

54

,68

65

,60

67

,16

89

,77

81

1,2

00

11

,09

69

,27

79

,35

09

,18

98

,98

28

,72

78

,81

58

,88

19

,09

82

.4%

2.6

%

Five

-sta

r 3

,31

53

,51

63

,36

83

,44

73

,27

73

,11

43

,37

23

,89

74

,98

56

,50

67

,65

27

,26

86

,41

06

,38

06

,13

55

,88

15

,72

05

,55

95

,48

45

,63

82

.8%

2.8

%

Fou

r-st

ar2

,53

82

,29

62

,16

82

,39

22

,36

82

,24

62

,58

03

,08

83

,84

75

,11

15

,72

25

,74

54

,63

84

,90

54

,90

54

,69

14

,47

44

,36

14

,42

44

,63

94

.9%

3.2

%

Thre

e-s

tar

1,5

43

1,4

57

1,5

05

1,6

73

1,6

96

1,6

69

1,6

70

1,8

30

2,2

12

3,0

12

3,4

88

3,5

30

3,2

55

3,3

48

3,3

54

3,2

52

3,0

83

3,0

39

3,1

55

3,2

65

3.5

%4

.0%

Two

-sta

r1

,71

41

,84

92

,06

32

,06

32

,12

22

,19

43

.4%

5.1

%

2017 HOTELS IN INDIA TRENDS & OPPORTUNITIES | PAGE 7

FIG

UR

E 1

5:

KEY

OP

ERA

TIN

G C

HA

RA

CTE

RIS

TIC

S B

Y H

OTE

L C

LASS

IFIC

ATI

ON

– R

EVPA

R (`)

Ove

rall

Ave

rage

Five

-sta

r D

elu

xe

Five

-sta

r

Fou

r-st

ar

Thre

e-s

tar

Two

-sta

r

12

-Mo

nth

**

Ch

ange

6.0

%

5.9

%

8.5

%

7.2

%

6.2

%

7.4

%

Co

mp

ou

nd

ed

Gro

wth

2.6

%

3.0

%

3.4

%

3.9

%

5.9

%

4.4

%

19

97

/98

2,2

76

3,4

80

1,9

39

1,4

77

72

5

19

98

/99

2,1

62

3,3

54

1,9

83

1,2

83

70

2

19

99

/00

1,8

89

2,8

63

1,8

76

1,1

53

71

8

20

00

/01

2,1

34

3,1

07

1,9

34

1,4

04

81

6

20

01

/02

1,7

89

2,4

37

1,6

84

1,2

48

84

3

20

02

/03

1,8

70

2,5

71

1,7

75

1,2

67

89

5

20

03

/04

2,3

13

3,0

46

2,2

52

1,7

72

99

5

20

04

/05

2,9

66

4,0

03

2,7

71

2,2

17

1,0

38

20

05

/06

3,8

92

5,2

90

3,5

09

2,7

97

1,4

58

20

06

/07

5,0

49

7,1

38

4,5

67

3,6

65

2,0

75

20

07

/08

5,4

96

8,0

30

5,1

42

3,9

42

2,2

57

20

08

/09

4,5

98

6,9

33

4,2

50

3,3

62

1,9

85

20

09

/10

3,8

61

5,7

15

3,7

56

2,7

97

1,8

06

20

10

/11

3,9

47

5,6

94

3,9

49

2,9

77

1,9

59

20

11

/12

3,5

75

5,4

91

3,6

26

2,9

42

1,9

09

1,1

10

20

12

/13

3,3

43

5,3

98

3,2

57

2,7

18

1,8

48

1,0

91

20

13

/14

3,2

75

5,2

31

3,1

85

2,6

43

1,7

86

1,2

58

20

14

/15

3,3

10

5,4

38

3,1

78

2,6

69

1,8

17

1,1

90

20

15

/16

*

3,4

99

5,7

15

3,3

55

2,8

40

2,0

44

1,2

81

20

16

/17

3,7

09

6,0

51

3,6

40

3,0

44

2,1

70

1,3

76

FIG

UR

E 1

3:

KEY

OP

ERA

TIN

G C

HA

RA

CTE

RIS

TIC

S B

Y H

OTE

L C

LASS

IFIC

ATI

ON

– O

CC

UPA

NC

Y

19

97

/98

19

98

/99

19

99

/00

20

00

/01

20

01

/02

20

02

/03

20

03

/04

20

04

/05

20

05

/06

20

06

/07

20

07

/08

20

08

/09

20

09

/10

20

10

/11

20

11

/12

20

12

/13

20

13

/14

20

14

/15

20

15

/16

*2

01

6/1

7

12

-Mo

nth

**

Ch

ange

Co

mp

ou

nd

ed

Gro

wth

Ove

rall

Ave

rage

57

.1%

55

.4%

53

.9%

57

.2%

51

.6%

57

.2%

64

.8%

69

.0%

71

.5%

71

.4%

68

.8%

59

.5%

59

.5%

60

.6%

59

.3%

57

.8%

58

.4%

59

.8%

63

.3%

65

.6%

3.5

%0

.7%

Five

-sta

r D

elu

xe6

2.0

%6

0.2

%5

8.3

%6

0.9

%5

2.2

%5

9.3

%6

5.0

%7

1.4

%7

3.8

%7

3.0

%7

1.7

%6

2.5

%6

1.6

%6

0.9

%5

9.8

%6

0.1

%5

9.9

%6

1.7

%6

4.3

%6

6.5

%3

.4%

0.4

%

Five

-sta

r 5

8.5

%5

6.4

%5

5.7

%5

6.1

%5

1.4

%5

7.0

%6

6.8

%7

1.1

%7

0.4

%7

0.2

%6

7.2

%5

8.5

%5

8.6

%6

1.9

%5

9.1

%5

5.4

%5

5.7

%5

7.2

%6

1.2

%6

4.6

%5

.5%

0.5

%

Fou

r-st

ar5

8.2

%5

5.9

%5

3.2

%5

8.7

%5

2.7

%5

6.4

%6

8.7

%7

1.8

%7

2.7

%7

1.7

%6

8.9

%5

8.5

%6

0.3

%6

0.7

%6

0.0

%5

7.9

%5

9.1

%6

1.2

%6

4.2

%6

5.6

%2

.2%

0.6

%

Thre

e-s

tar

47

.0%

48

.2%

47

.7%

48

.8%

49

.7%

53

.6%

59

.6%

56

.7%

65

.9%

68

.9%

64

.7%

56

.2%

55

.5%

58

.5%

56

.9%

56

.8%

57

.9%

59

.8%

64

.8%

66

.5%

2.6

%1

.8%

Two

-sta

r6

4.8

%5

9.0

%6

1.0

%5

7.7

%6

0.4

%6

2.7

%3

.9%

-0.6

%

* Th

e 2

01

5/1

6 d

ata

ha

s b

een

mo

dif

ied

to

exc

lud

e th

e p

erfo

rma

nce

of

irre

leva

nt s

up

ply

** C

ha

ng

e in

20

16

/17

exp

ress

ed a

s p

erce

nta

ge

of

the

fig

ure

fo

r 2

01

5/1

6So

urc

e: H

VS

Res

earc

h

FIG

UR

E 1

7:

KEY

OP

ERA

TIN

G C

HA

RA

CTE

RIS

TIC

S B

Y H

OTE

L C

LASS

IFIC

ATI

ON

– R

EVPA

R (

US$

)

* Th

e 2

01

5/1

6 d

ata

ha

s b

een

mo

dif

ied

to

exc

lud

e th

e p

erfo

rma

nce

of

irre

leva

nt s

up

ply

** C

ha

ng

e in

20

16

/17

exp

ress

ed a

s p

erce

nta

ge

of

the

fig

ure

fo

r 2

01

5/1

6So

urc

e: H

VS

Res

earc

h

Ove

rall

Ave

rage

Five

-sta

r D

elu

xe

Five

-sta

r

Fou

r-st

ar

Thre

e-s

tar

Two

-sta

r

12

-Mo

nth

**

Ch

ange

2.7

%

2.6

%

5.2

%

3.9

%

2.9

%

4.1

%

Co

mp

ou

nd

ed

G

row

th

-0.7

%

-0.3

%

0.1

%

0.6

%

2.6

%

-2.4

%

Exch

ange

Rat

e

19

97

/98 63

96 53

41

20

36

.3

19

98

/99

50 77

44

34 18

42

.2

19

99

/00 43

66 43

27

16

43

.5

20

00

/01

48 69 43

31

18

44

.9

20

01

/02

38 52

36

26

18

47

.2

20

02

/03

39 53

37

26 19

48

.2

20

03

/04 50

66 49

39

22

46

.0

20

04

/05

66 89

62

49 23

44

.9

20

05

/06 87

11

9

79 63

33

44

.5

20

06

/07

11

6

16

4

10

5

84 48

43

.6

20

07

/08

13

7

20

0

12

8

98

56

40

.2

20

08

/09

10

0

15

1

93

73

43

45

.9

20

09

/10 81

12

0 79

59

38

47

.7

20

10

/11

87

12

5

87 65

43

45

.6

20

11

/12

75

11

4 76 61

40 23

48

.0

20

12

/13

61

99

60

50

34 20

54

.5

20

13

/14

54

87

53

43

29

21

60

.7

20

14

/15

54 89

52

44 30 19

61

.2

20

15

/16

*

54

88

52

44

31

20

65

.0

20

16

/17

55

90

54 45

32

21

67

.1

PAGE 8 | 2017 HOTELS IN INDIA TRENDS & OPPORTUNITIES

Existing Supply – 2016/17

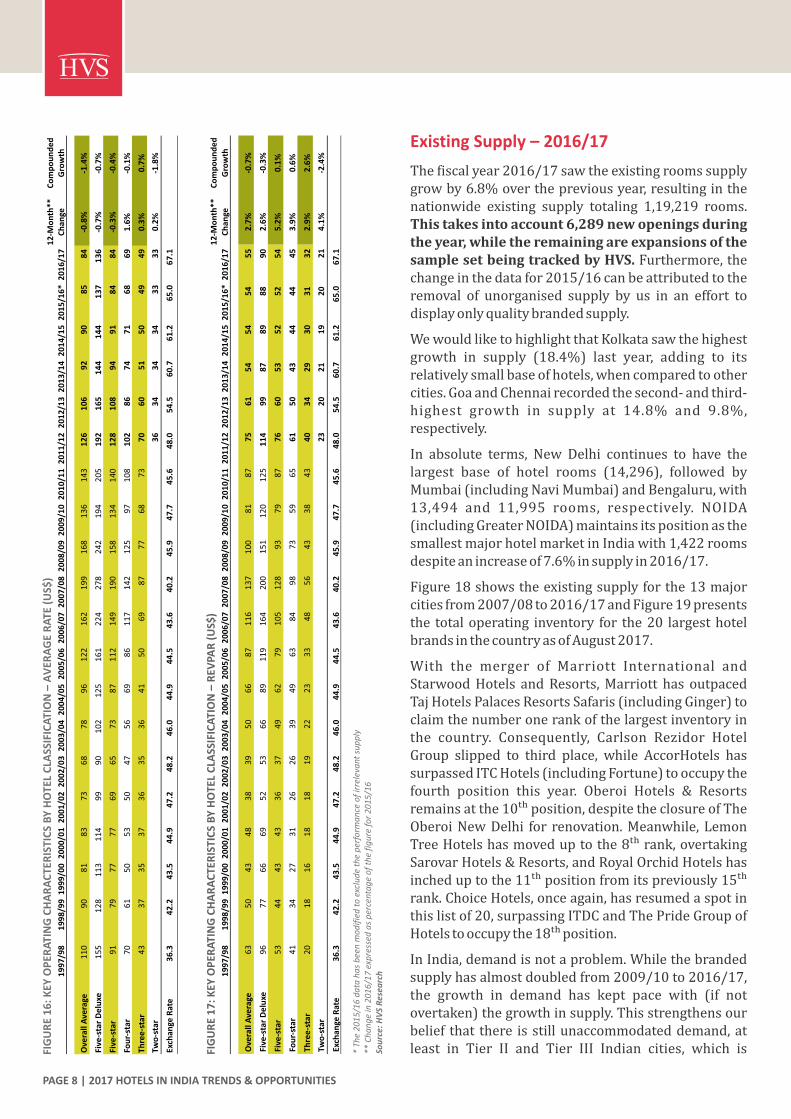

Thefiscalyear2016/17sawtheexistingroomssupplygrowby6.8%overthepreviousyear,resultinginthenationwide existing supply totaling 1,19,219 rooms.Thistakesintoaccount6,289newopeningsduringtheyear,whiletheremainingareexpansionsofthesamplesetbeingtrackedbyHVS.Furthermore,thechangeinthedatafor2015/16canbeattributedtotheremoval of unorganised supply by us in an effort todisplayonlyqualitybrandedsupply.

WewouldliketohighlightthatKolkatasawthehighestgrowth in supply (18.4%) last year, adding to itsrelativelysmallbaseofhotels,whencomparedtoothercities.GoaandChennairecordedthesecond-andthird-highest growth in supply at 14.8% and 9.8%,respectively.

In absolute terms, New Delhi continues to have thelargest base of hotel rooms (14,296), followed byMumbai(includingNaviMumbai)andBengaluru,with13,494 and 11,995 rooms, respectively. NOIDA(includingGreaterNOIDA)maintainsitspositionasthesmallestmajorhotelmarketinIndiawith1,422roomsdespiteanincreaseof7.6%insupplyin2016/17.

Figure18showstheexistingsupplyforthe13majorcitiesfrom2007/08to2016/17andFigure19presentsthe totaloperating inventory for the20 largesthotelbrandsinthecountryasofAugust2017.

With the merger of Marriott International andStarwoodHotels andResorts,Marriott has outpacedTajHotelsPalacesResortsSafaris(includingGinger)toclaimthenumberonerankofthelargestinventoryinthe country. Consequently, Carlson Rezidor HotelGroup slipped to third place, while AccorHotels hassurpassedITCHotels(includingFortune)tooccupythefourth position this year. Oberoi Hotels & Resortsremainsatthe10��position,despitetheclosureofTheOberoiNewDelhi for renovation.Meanwhile,LemonTreeHotelshasmoveduptothe8��rank,overtakingSarovarHotels&Resorts,andRoyalOrchidHotelshasincheduptothe11��positionfromitspreviously15��rank.ChoiceHotels,onceagain,hasresumedaspotinthislistof20,surpassingITDCandThePrideGroupofHotelstooccupythe18��position.

InIndia,demandisnotaproblem.Whilethebrandedsupplyhasalmostdoubledfrom2009/10to2016/17,the growth in demand has kept pace with (if notovertaken)thegrowthinsupply.Thisstrengthensourbelief that there isstillunaccommodateddemand,atleast in Tier II and Tier III Indian cities, which isFI

GU

RE

16

: K

EY O

PER

ATI

NG

CH

AR

AC

TER

ISTI

CS

BY

HO

TEL

CLA

SSIF

ICA

TIO

N –

AV

ERA

GE

RA

TE (

US$

)

Ove

rall

Ave

rage

Five

-sta

r D

elu

xe

Five

-sta

r

Fou

r-st

ar

Thre

e-s

tar

Two

-sta

r

12

-Mo

nth

**

Ch

ange

-0.8

%

-0.7

%

-0.3

%

1.6

%

0.3

%

0.2

%

Co

mp

ou

nd

ed

G

row

th

-1.4

%

-0.7

%

-0.4

%

-0.1

%

0.7

%

-1.8

%

Exch

ange

Rat

e

19

97

/98

11

0

15

5

91

70 43

36

.3

19

98

/99

90

12

8 79

61

37

42

.2

19

99

/00 81

11

3

77

50 35

43

.5

20

00

/01 83

11

4 77 53

37

44

.9

20

01

/02 73

99

69

50

36

47

.2

20

02

/03

68

90 65

47 35

48

.2

20

03

/04 78

10

2

73

56

36

46

.0

20

04

/05

96

12

5

87

69

41

44

.9

20

05

/06

12

2

16

1

11

2

86

50

44

.5

20

06

/07

16

2

22

4

14

9

11

7

69

43

.6

20

07

/08

19

9

27

8

19

0

14

2

87

40

.2

20

08

/09

16

8

24

2

15

8

12

5

77

45

.9

20

09

/10

13

6

19

4

13

4 97

68

47

.7

20

10

/11

14

3

20

5

14

0

10

8 73

45

.6

20

11

/12

12

6

19

2

12

8

10

2

70

36

48

.0

20

12

/13

10

6

16

5

10

8

86

60

34

54

.5

20

13

/14 92

14

4

94

74 51

34

60

.7

20

14

/15

90

14

4 91

71

50

34

61

.2

20

15

/16

*

85

13

7

84 68 49

33

65

.0

20

16

/17

84

13

6

84 69

49

33

67

.1

currentlybeingtappedbytheunbranded/unorganisedinventory.

Going forward, brands must be cognizant of themarkets they are entering. Over the past few years,duetothesurgeindomestictourism,hotelcompanieshaveshiftedtheirfocustowardbudgetandmidmarketpositionedhotelsinTierIIandTierIIIcitiestocatertothe lower paying domestic traveler and to capturethe previously untapped demand that exists inthesecities.

Future Supply

Given thedynamicnatureof thehospitality industryandtheever-changingproposedsupplylandscape,itisimpossible to determinewith absolute certainty theexacttimelineforhotelopenings.Thereareanumberofexternalforceswhichcandelayprojectsforvariousreasons.Overtheyears,HVShas followedacautiousand comprehensive approach for tracking newhoteldevelopmentsthatarelikelytoentermarketsoverthenextfiveyears.Theinformation,thatissystematically

12-Month* Compounded

2007/08 2008/09 2009/10 2010/11 2011/12 2012/13 2013/14 2014/15 2015/16** 2016/17 Change Growth

Agra 1,336 1,419 1,439 1,439 1,739 1,299 1,293 1,755 2,036 2,092 2.8% 5.1%

Ahmedabad 675 800 1,521 1,785 1,975 2,477 2,777 2,944 3,054 3,117 2.1% 18.5%

Bengaluru 3,456 3,889 5,597 5,947 7,713 8,536 10,162 11,117 11,539 11,995 4.0% 14.8%

Chennai 2,826 3,307 3,806 4,066 4,904 6,330 7,105 7,444 7,585 8,332 9.8% 12.8%

New Delhi*** 9,019 8,625 8,129 9,111 10,697 11,338 12,370 13,193 14,142 14,296 1.1% 5.3%

Gurugram 1,980 3,246 3,782 4,559 5,190 5,323 5,117 5,263 2.9% 15.0%

NOIDA 300 351 527 841 1,239 1,322 1,322 1,422 7.6% 24.9%

Goa 2,768 2,795 3,288 3,375 3,885 4,406 4,703 5,298 5,574 6,400 14.8% 9.8%

Hyderabad 2,554 2,761 3,782 4,036 4,797 5,411 5,734 5,954 5,992 6,254 4.4% 10.5%

Jaipur 1,556 1,683 2,472 2,554 3,054 4,129 4,523 4,822 4,931 5,058 2.6% 14.0%

Kolkata 1,396 1,373 1,520 1,588 1,787 2,163 2,243 2,701 2,701 3,199 18.4% 9.7%

Mumbai 8,454 7,948 9,877 11,303 12,052 12,807 13,022 12,865 13,054 13,494 3.4% 5.3%

Pune 1,346 1,518 2,672 4,691 5,672 5,317 6,159 6,137 6,108 6,445 5.5% 19.0%

Other Ci�es**** 11,596 12,357 15,412 18,039 21,729 24,642 24,657 26,820 28,445 31,852 12.0% 11.9%

FIGURE 18: EXISTING SUPPLY ACROSS MAJOR CITIES (2007/08 – 2016/17)

* Change in 2016/17 expressed as percentage of the figure for 2015/16** Supply tracked in 2015/16 has been modified due to the removal of irrelevant supply*** Delhi NCR data (Shaded Portion), rest New Delhi (excluding Gurugram, NOIDA and Greater NOIDA) data**** Other Cities includes all other hotel markets across India

, , , , , , , , , , , , , ,

FIGURE 19: TOP 20 HOTEL BRANDS BY EXISTING INVENTORY (AUGUST 2017)

Source: HVS Research

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

Number of Rooms

2017 HOTELS IN INDIA TRENDS & OPPORTUNITIES | PAGE 9

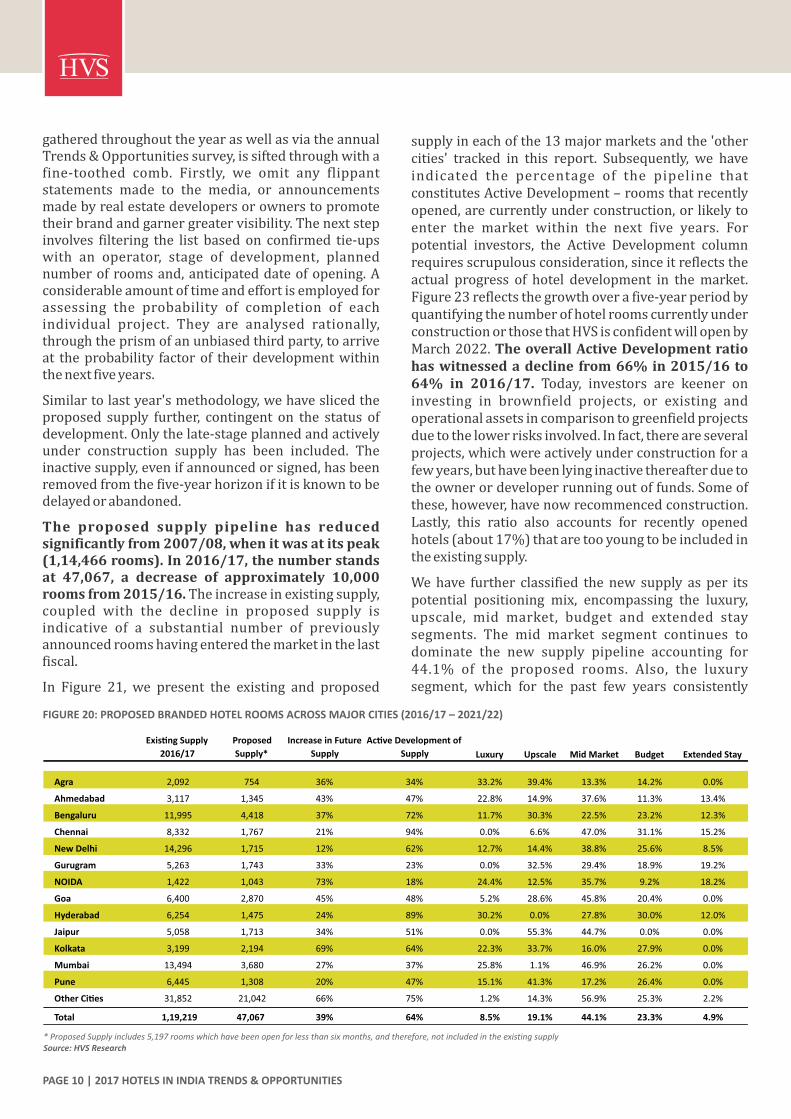

FIGURE 20: PROPOSED BRANDED HOTEL ROOMS ACROSS MAJOR CITIES (2016/17 – 2021/22)

* Proposed Supply includes 5,197 rooms which have been open for less than six months, and therefore, not included in the existing supplySource: HVS Research

Exis�ng Supply

2016/17

Proposed

Supply*

Increase in Future

Supply

Ac�ve Development of

Supply Luxury Upscale Mid Market Budget Extended Stay

Agra 2,092 754 36% 34% 33.2% 39.4% 13.3% 14.2% 0.0%

Ahmedabad 3,117 1,345 43% 47% 22.8% 14.9% 37.6% 11.3% 13.4%

Bengaluru 11,995 4,418 37% 72% 11.7% 30.3% 22.5% 23.2% 12.3%

Chennai 8,332 1,767 21% 94% 0.0% 6.6% 47.0% 31.1% 15.2%

New Delhi 14,296 1,715 12% 62% 12.7% 14.4% 38.8% 25.6% 8.5%

Gurugram 5,263 1,743 33% 23% 0.0% 32.5% 29.4% 18.9% 19.2%

NOIDA 1,422 1,043 73% 18% 24.4% 12.5% 35.7% 9.2% 18.2%

Goa 6,400 2,870 45% 48% 5.2% 28.6% 45.8% 20.4% 0.0%

Hyderabad 6,254 1,475 24% 89% 30.2% 0.0% 27.8% 30.0% 12.0%

Jaipur 5,058 1,713 34% 51% 0.0% 55.3% 44.7% 0.0% 0.0%

Kolkata 3,199 2,194 69% 64% 22.3% 33.7% 16.0% 27.9% 0.0%

Mumbai 13,494 3,680 27% 37% 25.8% 1.1% 46.9% 26.2% 0.0%

Pune 6,445 1,308 20% 47% 15.1% 41.3% 17.2% 26.4% 0.0%

Other Ci�es 31,852 21,042 66% 75% 1.2% 14.3% 56.9% 25.3% 2.2%

Total 1,19,219 47,067 39% 64% 8.5% 19.1% 44.1% 23.3% 4.9%

gatheredthroughouttheyearaswellasviatheannualTrends&Opportunitiessurvey,issiftedthroughwithafine-toothed comb. Firstly, we omit any flippantstatements made to the media, or announcementsmadebyrealestatedevelopersorownerstopromotetheirbrandandgarnergreatervisibility.Thenextstepinvolves filtering the list based on confirmed tie-upswith an operator, stage of development, plannednumberofroomsand,anticipateddateofopening.Aconsiderableamountoftimeandeffortisemployedforassessing the probability of completion of eachindividual project. They are analysed rationally,throughtheprismofanunbiasedthirdparty,toarriveat theprobability factorof theirdevelopmentwithinthenextfiveyears.

Similartolastyear'smethodology,wehaveslicedtheproposed supply further, contingent on the status ofdevelopment.Onlythelate-stageplannedandactivelyunder construction supply has been included. Theinactivesupply,evenifannouncedorsigned,hasbeenremovedfromthefive-yearhorizonifitisknowntobedelayedorabandoned.

The proposed supply pipeline has reducedsignificantlyfrom2007/08,whenitwasatitspeak(1,14,466rooms).In2016/17,thenumberstandsat 47,067, a decrease of approximately 10,000roomsfrom2015/16.Theincreaseinexistingsupply,coupled with the decline in proposed supply isindicative of a substantial number of previouslyannouncedroomshavingenteredthemarketinthelastfiscal.

In Figure 21, we present the existing and proposed

supplyineachofthe13majormarketsandthe'othercities' tracked in this report. Subsequently, we haveindicated the percentage of the pipeline thatconstitutesActiveDevelopment–roomsthatrecentlyopened,arecurrentlyunderconstruction,orlikelytoenter the market within the next five years. Forpotential investors, the Active Development columnrequiresscrupulousconsideration,sinceitreflectstheactual progress of hotel development in themarket.Figure23reflectsthegrowthoverafive-yearperiodbyquantifyingthenumberofhotelroomscurrentlyunderconstructionorthosethatHVSisconfidentwillopenbyMarch2022.TheoverallActiveDevelopmentratiohaswitnessedadecline from66%in2015/16to64% in 2016/17. Today, investors are keener oninvesting in brownfield projects, or existing andoperationalassetsincomparisontogreenfieldprojectsduetothelowerrisksinvolved.Infact,thereareseveralprojects,whichwereactivelyunderconstructionforafewyears,buthavebeenlyinginactivethereafterduetotheownerordeveloperrunningoutoffunds.Someofthese,however,havenowrecommencedconstruction.Lastly, this ratio also accounts for recently openedhotels(about17%)thataretooyoungtobeincludedintheexistingsupply.

Wehave further classified the new supply as per itspotential positioning mix, encompassing the luxury,upscale, mid market, budget and extended staysegments. The mid market segment continues todominate the new supply pipeline accounting for44.1% of the proposed rooms. Also, the luxurysegment, which for the past few years consistently

PAGE 10 | 2017 HOTELS IN INDIA TRENDS & OPPORTUNITIES

FIG

UR

E 2

1:

DIS

TRIB

UTI

ON

OF

EXIS

TIN

G A

ND

PR

OP

OSE

D B

RA

ND

ED H

OTE

L R

OO

MS

AC

RO

SS M

AJO

R C

ITIE

S (2

00

7/0

8 –

20

16

/17

)

* D

elh

i NC

R (

Sha

ded

Po

rtio

n),

res

t N

ew D

elh

i (ex

clu

din

g G

uru

gra

m, N

OID

A a

nd

Gre

ate

r N

OID

A)

da

taSo

urc

e: H

VS

Res

earc

h

Exis

�n

g Su

pp

lyP

rop

ose

d S

up

ply

Ac�

ve D

eve

lop

me

nt

of

Sup

ply

FIGURE 22: GROWTH OF ROOM SUPPLY – INDIA (2000/01 – 2021/22)

Source: HVS Research

Number of Rooms Trendline

Agr

a1

,29

91

,29

31

,75

52

,03

62

,09

26

70

40

05

10

66

76

50

1,3

36

1,4

19

86

69

90

1,4

39

50

31

,43

96

22

75

41

,73

95

5%

75

%4

1%

22

%8

0%

76

%8

2%

43

%2

8%

34

%

Ah

me

dab

ad2

,47

72

,77

72

,94

43

,05

43

,11

73

,66

43

,05

82

,33

92

,31

92

,55

06

75

80

01

,85

71

,37

21

,52

11

,02

61

,78

51

,23

81

,34

51

,97

54

7%

71

%6

9%

73

%6

9%

66

%8

6%

64

%7

1%

47

%

Be

nga

luru

8,5

36

10

,16

21

1,1

17

11

,53

91

1,9

95

15

,54

21

0,7

84

9,8

19

12

,50

99

,71

63

,45

63

,88

91

0,7

31

6,9

11

5,5

97

5,3

17

5,9

47

5,2

09

4,4

18

7,7

13

60

%5

8%

65

%6

7%

71

%7

5%

66

%5

2%

67

%7

2%

Ch

en

nai

6,3

30

7,1

05

7,4

44

7,5

85

8,3

32

7,1

47

4,9

45

5,9

95

7,8

19

7,5

47

2,8

26

3,3

07

5,3

31

3,8

85

3,8

06

3,3

11

4,0

66

2,3

12

1,7

67

4,9

04

71

%6

7%

72

%5

7%

58

%6

5%

80

%8

3%

10

0%

94

%

Ne

w D

elh

i1

1,3

38

12

,37

01

3,1

93

14

,14

21

4,2

96

22

,36

01

6,5

60

20

,02

11

8,6

08

5,6

26

9,0

19

8,6

25

6,1

44

5,3

55

8,1

29

2,5

02

9,1

11

2,7

92

1,7

15

10

,69

75

1%

53

%7

5%

75

%8

7%

84

%7

1%

87

%9

2%

62

%

Gu

rugr

am4

,55

95

,19

05

,32

35

,11

75

,26

35

,81

85

,03

33

,26

81

,98

02

,08

43

,24

61

,95

91

,74

33

,78

25

5%

53

%5

4%

10

%7

0%

23

%

NO

IDA

84

11

,23

91

,32

21

,32

21

,42

25

,52

25

,61

52

,40

63

00

1,8

73

35

12

,56

11

,04

35

27

37

%2

8%

70

%1

3%

9%

18

%

Go

a4

,40

64

,70

35

,29

85

,57

46

,40

03

,35

32

,17

81

,73

62

,15

42

,42

22

,76

82

,79

52

,62

22

,29

13

,28

81

,74

33

,37

52

,06

22

,87

03

,88

54

2%

31

%4

1%

53

%5

3%

62

%6

8%

50

%9

0%

48

%

Hyd

era

bad

5,4

11

5,7

34

5,9

54

5,9

92

6,2

54

8,2

50

5,8

84

5,3

02

5,7

13

5,2

65

2,5

54

2,7

61

3,4

33

2,8

93

3,7

82

2,4

74

4,0

36

2,4

64

1,4

75

4,7

97

64

%7

3%

63

%7

7%

74

%8

7%

78

%6

1%

32

%8

9%

Jaip

ur

4,1

29

4,5

23

4,8

22

4,9

31

5,0

58

2,9

37

3,3

57

2,6

64

4,8

67

3,3

56

1,5

56

1,6

83

2,8

59

1,7

06

2,4

72

1,1

19

2,5

54

96

01

,71

33

,05

45

3%

53

%7

7%

45

%5

2%

56

%8

2%

92

%8

9%

51

%

Ko

lkat

a2

,16

32

,24

32

,70

12

,70

13

,19

95

,96

54

,02

53

,48

13

,61

23

,11

81

,39

61

,37

33

,51

12

,58

41

,52

02

,87

01

,58

83

,20

92

,19

41

,78

74

9%

62

%5

1%

58

%7

4%

64

%7

2%

70

%6

4%

64

%

Mu

mb

ai1

2,8

07

13

,02

21

2,8

65

13

,05

41

3,4

94

10

,61

31

3,3

86

7,4

77

12

,12

11

0,8

96

8,4

54

7,9

48

9,8

02

7,8

96

9,8

77

5,5

61

11

,30

34

,16

63

,68

01

2,0

52

62

%7

3%

60

%3

5%

47

%4

2%

49

%3

3%

39

%3

7%

Pu

ne

5,3

17

6,1

59

6,1

37

6,1

08

6,4

45

8,2

43

8,0

54

5,1

96

5,5

45

4,6

45

1,3

46

1,5

18

3,7

05

2,6

20

2,6

72

2,0

05

4,6

91

1,9

65

1,3

08

5,6

72

66

%5

2%

67

%5

6%

69

%6

7%

72

%6

4%

73

%4

7%

Oth

er

Ci�

es

24

,64

22

4,6

57

26

,82

02

8,4

45

31

,85

22

5,7

22

21

,48

42

4,9

09

26

,50

42

6,2

24

11

,59

61

2,3

57

23

,14

12

3,8

73

15

,41

22

3,8

82

18

,03

92

5,3

93

21

,04

22

1,7

29

60

%6

0%

65

%5

6%

48

%5

5%

71

%7

0%

71

%7

5%

20

08

/09

20

12

/13

20

13

/14

20

14

/15

20

15

/16

20

16

/17

20

07

/08

20

08

/09

20

09

/10

20

10

/11

20

11

/12

20

07

/08

20

12

/13

20

13

/14

20

09

/10

20

14

/15

20

10

/11

20

15

/16

20

16

/17

20

11

/12

20

07

/08

20

08

/09

20

09

/10

20

10

/11

20

11

/12

20

12

/13

20

13

/14

20

14

/15

20

15

/16

20

16

/17

Tota

l9

4,2

55

1,0

1,1

77

1,0

7,6

95

1,1

1,6

00

1,1

9,2

19

1,1

4,4

66

94

,11

58

9,4

49

1,0

2,4

38

93

,35

54

6,9

82

48

,47

58

4,6

50

68

,05

06

1,7

95

56

,27

07

1,5

31

56

,91

24

7,0

67

84

,31

35

8%

60

%6

7%

60

%5

8%

60

%6

9%

61

%6

6%

64

%

24,905

1,19,219

1,49,276

40,000

60,000

80,000

1,00,000

1,20,000

1,40,000

1,60,000

1,80,000

2,00,000

20,000

2000/01 2016/17 2021/22

-

represented about 6.5%of theproposed supply, hasnow shown an increase for the first time since2013/14.

Analysingtheyear-on-yeargrowthinpotentialsupplyacross the 13 markets, we observe that NOIDA(including Greater NOIDA) and Kolkata continue toshowcase the highest anticipated increase in supply,largelydue to their smallbaseof rooms. Inabsoluteterms,Bengaluru,followedbyMumbai,areanticipatedtohave thehighestnumberof roomsadded to theirexistinginventoriesinthefive-yearhorizon.

Figure 22 depicts the growth of room supply acrossIndiaovera20-yearperiod.

Ashighlightedearlier,theactivedevelopmentofsupplyin India saw a slight decline in 2016/17 whencompared to 2015/16. We anticipate a little over30,000brandedhotelroomstobedevelopedoverthefollowing five years, taking thetotalanticipatedbrandedsupplyto 1,49,276 rooms by 2021/22.Figure22 illustrates thegrowthin hotel room supply from2000/01 to 2016/17 , andanticipated existing supply in2021/22.

The highest percentages of supply actively under development are in Chennai (94%), followed by Hyderabad (89%) and Bengaluru (72%).

2017 HOTELS IN INDIA TRENDS & OPPORTUNITIES | PAGE 11

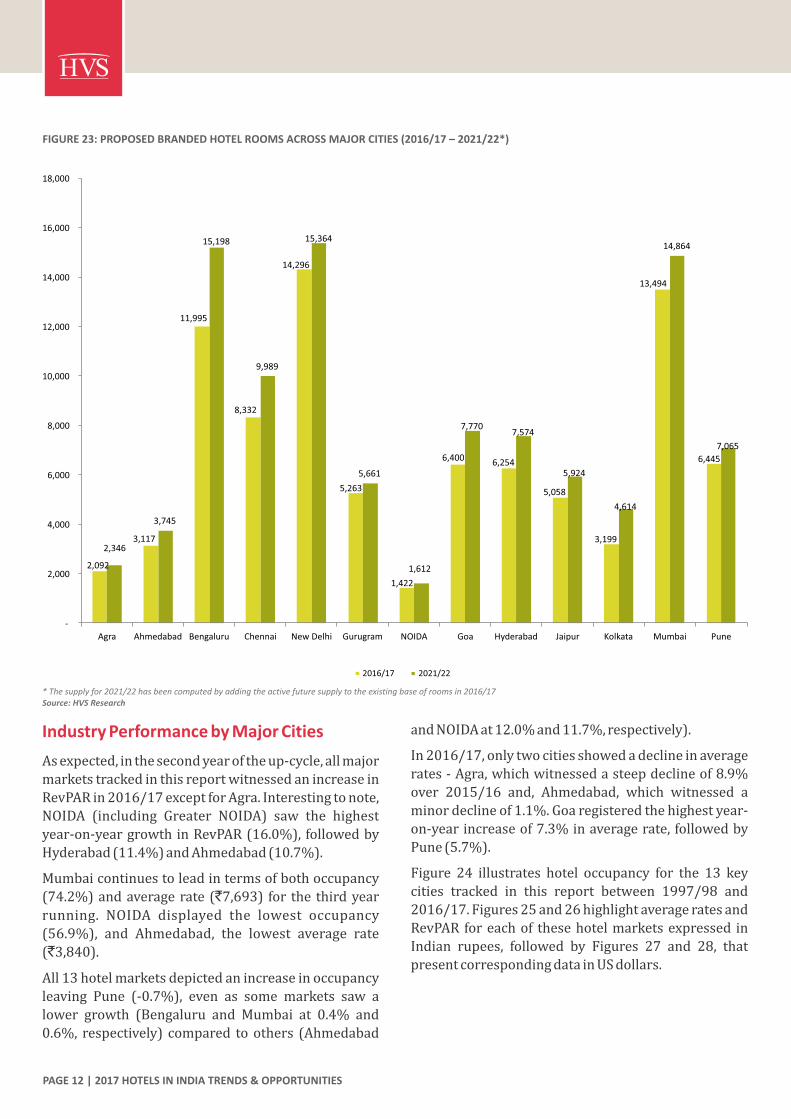

FIGURE 23: PROPOSED BRANDED HOTEL ROOMS ACROSS MAJOR CITIES (2016/17 – 2021/22*)

* The supply for 2021/22 has been computed by adding the active future supply to the existing base of rooms in 2016/17Source: HVS Research

2016/17 2021/22

2,092

3,117

11,995

8,332

14,296

5,263

1,422

6,400 6,254

5,058

3,199

13,494

6,445

2,346

3,745

15,198

9,989

15,364

5,661

1,612

7,770 7,574

5,924

4,614

14,864

7,065

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

Agra Ahmedabad Bengaluru Chennai New Delhi Gurugram NOIDA Goa Hyderabad Jaipur Kolkata Mumbai Pune

Industry Performance by Major Cities

Asexpected,inthesecondyearoftheup-cycle,allmajor

marketstrackedinthisreportwitnessedanincreasein

RevPARin2016/17exceptforAgra.Interestingtonote,

NOIDA (including Greater NOIDA) saw the highest

year-on-yeargrowthinRevPAR(16.0%),followedby

Hyderabad(11.4%)andAhmedabad(10.7%).

Mumbaicontinuestoleadintermsofbothoccupancy

(74.2%)andaveragerate (`7,693) for the thirdyear

running. NOIDA displayed the lowest occupancy

(56.9%), and Ahmedabad, the lowest average rate

(`3,840).

All13hotelmarketsdepictedanincreaseinoccupancy

leaving Pune (-0.7%), even as some markets saw a

lower growth (Bengaluru and Mumbai at 0.4% and

0.6%, respectively) compared toothers (Ahmedabad

andNOIDAat12.0%and11.7%,respectively).

In2016/17,onlytwocitiesshowedadeclineinaverage

rates-Agra,whichwitnessedasteepdeclineof8.9%

over 2015/16 and, Ahmedabad, which witnessed a

minordeclineof1.1%.Goaregisteredthehighestyear-

on-yearincreaseof7.3%inaveragerate,followedby

Pune(5.7%).

Figure 24 illustrates hotel occupancy for the 13 key

cities tracked in this report between 1997/98 and

2016/17.Figures25and26highlightaverageratesand

RevPARforeachof thesehotelmarketsexpressed in

Indian rupees, followed by Figures 27 and 28, that

presentcorrespondingdatainUSdollars.

PAGE 12 | 2017 HOTELS IN INDIA TRENDS & OPPORTUNITIES

FIG

UR

E 2

4:

KEY

OP

ERA

TIN

G C

HA

RA

CTE

RIS

TIC

S B

Y M

AJO

R C

ITIE

S −

OC

CU

PAN

CY

* Th

e 2

01

5/1

6 d

ata

ha

s b

een

mo

dif

ied

to

exc

lud

e th

e p

erfo

rma

nce

of

irre

leva

nt s

up

ply

** C

ha

ng

e in

20

16

/17

exp

ress

ed a

s p

erce

nta

ge

of

the

fig

ure

fo

r 2

01

5/1

6�

Del

hi N

CR

da

ta (

Sha

ded

Po

rtio

n),

res

t N

ew D

elh

i (ex

clu

din

g G

uru

gra

m, N

OID

A a

nd

Gre

ate

r N

OID

A)

da

ta�

NO

IDA

da

ta in

clu

des

Gre

ate

r N

OID

A�

Mu

mb

ai d

ata

incl

ud

es N

avi

Mu

mb

ai

Sou

rce:

HV

S R

esea

rch

12

-Mo

nth

**

Ch

ange

Agr

a6

.1%

1.5

%

Ah

me

dab

ad1

2.0

%-0

.7%

Be

nga

luru

0.4

%0

.4%

Ch

en

nai

4.3

%-0

.2%

Ne

w D

elh

ia5

.5%

0.8

%

Gu

rugr

am4

.5%

0.1

%

NO

IDAb

11

.7%

-3.7

%

Go

a3

.0%

1.1

%

Hyd

era

bad

7.2

%0

.9%

Jaip

ur

6.9

%1

.2%

Ko

lkat

a1

.4%

0.7

%

Mu

mb

aic

20

01

/02

33

.7%

53

.2%

64

.3%

56

.5%

53

.3%

53

.6%

68

.0%

48

.3%

66

.4%

52

.0%

0.6

%0

.7%

Pu

ne

19

97

/98

46

.1%

71

.8%

61

.2%

68

.4%

60

.2%

59

.2%

53

.4%

51

.7%

61

.8%

65

.3%

19

98

/99

46

.4%

58

.0%

59

.0%

64

.7%

54

.1%

58

.6%

66

.0%

45

.6%

57

.8%

67

.6%

19

99

/00

40

.1%

50

.8%

64

.4%

65

.3%

52

.9%

53

.3%

61

.3%

47

.0%

54

.8%

64

.5%

20

00

/01

42

.5%

55

.8%

69

.8%

64

.6%

58

.9%

60

.6%

69

.1%

55

.0%

62

.9%

64

.6%

20

02

/03

30

.7%

53

.8%

72

.0%

58

.3%

60

.4%

60

.5%

68

.9%

44

.9%

65

.4%

63

.4%

71

.0%

20

03

/04

50

.0%

63

.2%

78

.5%

66

.6%

73

.1%

59

.3%

75

.9%

58

.8%

62

.8%

69

.7%

68

.9%

20

04

/05

57

.1%

68

.3%

81

.4%

72

.9%

79

.1%

62

.5%

78

.7%

67

.2%

69

.0%

72

.0%

86

.4%

20

05

/06

56

.0%

69

.1%

76

.7%

78

.2%

80

.8%

67

.8%

82

.0%

65

.7%

76

.4%

76

.2%

83

.1%

20

06

/07

58

.9%

67

.9%

72

.5%

74

.7%

76

.9%

72

.8%

72

.1%

65

.5%

75

.5%

77

.9%

83

.4%

20

07

/08

58

.3%

73

.3%

65

.3%

72

.8%

73

.9%

72

.2%

65

.7%

64

.7%

73

.9%

74

.6%

69

.5%

20

08

/09

52

.4%

61

.2%

54

.6%

63

.1%

67

.3%

61

.1%

55

.8%

54

.1%

69

.5%

60

.6%

62

.2%

20

09

/10

55

.9%

58

.2%

53

.2%

62

.1%

68

.3%

66

.0%

74

.0%

65

.1%

53

.3%

57

.3%

67

.5%

62

.5%

50

.9%

20

10

/11

60

.2%

54

.3%

58

.4%

67

.2%

68

.7%

66

.5%

80

.7%

67

.7%

57

.1%

57

.7%

68

.3%

62

.4%

46

.7%

20

11

/12

57

.1%

59

.9%

56

.6%

65

.7%

63

.8%

62

.0%

56

.2%

68

.5%

54

.0%

55

.2%

70

.0%

63

.7%

51

.3%

20

12

/13

58

.9%

53

.7%

55

.6%

60

.0%

61

.7%

58

.0%

44

.4%

68

.9%

49

.3%

54

.7%

71

.5%

64

.3%

58

.2%

20

13

/14

60

.4%

52

.7%

57

.7%

55

.4%

60

.9%

58

.8%

53

.5%

68

.7%

51

.7%

54

.3%

70

.2%

67

.0%

57

.4%

20

14

/15

61

.5%

53

.9%

58

.1%

58

.9%

61

.7%

61

.1%

48

.0%

69

.7%

57

.1%

54

.5%

67

.8%

71

.8%

61

.3%

20

15

/16

*

57

.7%

55

.6%

65

.7%

62

.7%

66

.7%

63

.7%

51

.0%

70

.2%

59

.3%

60

.8%

69

.3%

73

.7%

65

.6%

20

16

/17

61

.2%

62

.3%

65

.9%

65

.4%

70

.3%

66

.6%

56

.9%

72

.3%

63

.6%

65

.0%

70

.2%

74

.2%

65

.2%

-0.7

%-0

.6%

Co

mp

ou

nd

ed

Gro

wth

FIG

UR

E 2

5:

KEY

OP

ERA

TIN

G C

HA

RA

CTE

RIS

TIC

S B

Y M

AJO

R C

ITIE

S –

AV

ERA

GE

RA

TE (`)

12

-Mo

nth

**C

om

po

un

de

d

Ch

ange

Gro

wth

Agr

a-8

.9%

5.4

%A

hm

ed

abad

-1.1

%4

.0%

Be

nga

luru

3.8

%2

.6%

Ch

en

nai

0.4

%1

.0%

Ne

w D

elh

ia1

.9%

1.3

%

Gu

rugr

am2

.4%

-3.5

%

NO

IDA

b3

.9%

-4.4

%

Go

a7

.3%

6.4

%

Hyd

era

bad

3.9

%5

.9%

Jaip

ur

2.4

%3

.6%

Ko

lkat

a3

.8%

2.1

%

Mu

mb

aic

19

97

/98

2,0

27

1,8

33

3,4

51

3,9

77

4,9

13

2,3

03

1,6

46

2,4

73

3,9

51

6,1

69

20

01

/02

1,8

40

2,3

54

3,7

35

3,5

35

4,3

38

2,6

76

2,4

14

2,9

49

3,4

09

4,9

32

4.6

%1

.2%

Pu

ne

19

98

/99

1,9

06

2,2

20

3,2

54

3,6

00

4,6

26

2,8

63

1,5

79

2,5

33

3,8

88

6,2

97 1

99

9/0

0

1,6

38

2,7

05

3,0

25

3,4

24

4,1

15

2,7

27

1,8

67

2,5

14

3,5

57

5,6

61

20

00

/01

1,5

86

2,7

36

3,6

02

3,7

96

4,5

26

2,9

14

2,3

16

2,9

02

3,6

98

5,5

55

20

02

/03

1,9

54

2,1

64

3,7

52

3,2

24

4,0

89

2,7

54

2,5

41

2,7

28

2,9

17

4,1

84

2,6

03

20

03

/04

2,4

31

2,4

10

4,8

32

3,3

23

4,2

69

3,0

86

2,7

74

2,9

80

3,0

21

4,3

56

2,8

05

20

04

/05

3,0

12

2,7

87

7,4

70

3,7

14

5,1

03

3,9

85

3,7

72

3,4

61

3,2

40

4,8

22

3,5

21

20

05

/06

3,6

22

3,1

11

8,7

62

4,3

57

6,9

09

4,8

04

4,8

70

4,4

07

3,8

87

6,0

41

4,9

15

20

06

/07

4,7

15

3,5

26

10

,40

6

5,3

78

9,1

92

5,8

01

5,9

62

5,2

85

5,2

88

8,7

38

6,5

23

20

07

/08

5,2

62

4,3

51

9,8

27

6,3

40

10

,42

9

6,2

55

6,2

71

5,6

64

6,5

75

10

,93

2

7,9

46

20

08

/09

5,3

22

4,7

54

9,4

95

6,6

77

9,8

11

6,2

71

6,2

97

5,9

82

6,6

86

10

,67

9

7,4

93

20

09

/10

5,7

73

4,5

40

6,5

97

5,7

10

8,8

34

8,2

47

7,4

96

5,6

13

5,1

46

4,5

39

6,0

87

8,4

28

5,8

10

20

10

/11

6,2

43

4,2

85

6,7

76

5,6

32

8,6

34

7,5

54

7,7

52

6,0

56

5,1

73

4,7

18

6,4

08

8,1

94

4,9

49

20

11

/12

5,9

58

3,9

17

6,2

93

5,5

24

8,1

74

7,6

39

7,4

16

6,1

62

5,0

26

4,7

27

6,0

49

7,9

23

4,1

63

20

12

/13

6,1

26

3,9

04

5,9

60

5,4

40

7,3

87

6,8

31

6,7

24

6,5

13

4,8

54

4,8

43

6,0

93

7,5

50

3,8

61

20

13

/14

6,3

38

3,7

34

5,3

79

5,0

50

6,9

41

6,5

69

5,9

64

6,6

92

4,5

56

4,7

43

5,7

39

7,1

58

3,9

08

20

14

/15

6,4

88

3,7

53

5,3

68

4,8

25

6,5

68

6,2

41

5,4

29

6,8

19

4,5

35

4,7

43

5,7

34

7,2

30

3,8

46

20

15

/16

*

6,0

83

3,8

84

5,3

92

4,7

67

6,2

11

6,2

53

5,2

81

7,0

20

4,7

41

4,7

21

5,6

07

7,3

53

3,9

22

20

16

/17

5,5

41

3,8

40

5,5

96

4,7

85

6,3

32

6,4

04

5,4

84

7,5

34

4,9

27

4,8

35

5,8

18

7,6

93

4,1

47

5.7

%3

.4%

FIG

UR

E 2

6:

KEY

OP

ERA

TIN

G C

HA

RA

CTE

RIS

TIC

S B

Y M

AJO

R C

ITIE

S –

REV

PAR

(`)

12

-Mo

nth

**

20

02

/03

20

03

/04

20

04

/05

20

05

/06

20

06

/07

20

07

/08

20

08

/09

20

09

/10

20

10

/11

20

11

/12

20

12

/13

20

13

/14

20

14

/15

20

15

/16

*C

han

geG

row

th

Agr

a6

00

1,2

16

1,7

20

2,0

28

2,7

77

3,0

68

2,7

90

3,2

27

3,7

58

3,4

00

3,6

05

3,8

27

3,9

88

3,5

10

-3.3

%7

.0%

Ah

me

dab

ad1

,16

41

,52

31

,90

42

,15

02

,39

43

,18

92

,90

82

,64

22

,32

72

,34

72

,09

81

,96

72

,02

42

,15

91

0.7

%3

.2%

Be

nga

luru

2,7

01

3,7