2016 global stratecast csp billing mediation market ... global stratecast csp billing mediation...

TRANSCRIPT

2016 Global Stratecast CSP Billing Mediation

Market Leadership Award

2016

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 2 “We Accelerate Growth”

Contents Background and Company Performance ..................................................................... 2

Introduction .................................................................................................... 2

Stratecast End-to-End Billing Market Assessment .................................................. 4

Industry Challenges .......................................................................................... 8

Huawei ........................................................................................................... 9

Huawei Market Leadership ............................................................................... 11

Conclusion ..................................................................................................... 13

Understanding Market Leadership ........................................................................... 15

Key Performance Criteria ....................................................................................... 16

The Intersection between 360-Degree Research and Best Practices Awards .................. 17

About ODAM ........................................................................................................ 19

About Stratecast .................................................................................................. 19

About Frost & Sullivan .......................................................................................... 19

Background and Company Performance

Introduction

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 3 “We Accelerate Growth”

From a customer’s perspective, as shown by the figure below, everything is an app today. Everything is personalized. But, personalization means different things to different customer segments and personalization uses different amounts of data. For consumers, we expect 24 X 7 service availability, high throughput capacity, personal security, total reliability—voice, text or data messages from us to others and back again—and dependability of the apps we use to keep our digital lifestyles current.

Source: Stratecast

Personalization to a small business, and even large enterprise, means smartphones with apps designed to solve their particular business problems and, in many cases, enhance their customers’ experience. It means helping businesses engage with other industries to provide innovative and personalized service offers. Personalization, for many, also means that small and large businesses can utilize applications offered as cloud-based services, and meet their computing needs through an on-demand, cloud-based business strategy.

In support of personalized everything, data movement across a network can be substantial, according to app type—streaming movies, self-made video, or gaming entertainment. It can also be minimal—a simple information search or a weather check. But, new things are coming that will require very significant levels of data management functionality well beyond what is required to address the exabytes per month of data that now flows across today's global networks.

Shown in the figure below, over the next 3-5 years, evolving customer apps and services involving virtualized networks, the IoT, virtual or augmented reality, 3D and 4D printing, and 5G mobile networks, will require enhanced data management capabilities. Solutions involving these technologies are the basis for smart cities, smart cars, smart government

Internet Access (The Cloud)

2020+

2-Way Data Interaction

2015

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 4 “We Accelerate Growth”

services, and smart health/wellness care, to name a few. They hold great promise for businesses, enterprises, and the lifestyle improvements that will come to individuals.

Source: Stratecast

The amount of customer data (consumer or business) has been on an exponential climb for several years and the need for accountability of that data usage is now approaching a real-time level. Increasing data volumes places a heavy burden on all business and operations functions. With that heavy burden, the monetization processes, along with the partner management, order management, and network monitoring functions, must meet the needs of services defined by any combination of these technologies.

While it can easily be argued that the monetization processes are the most important business functions a CSP must pay attention to once a service is proven to work technically, billing mediation is the lynchpin that will keep the end-to-end billing and monetization processes functional. Most importantly, Stratecast believes that mediation must absorb the influx of massive data volumes from all sources, very close to real-time, in order to bridle the essential insights from this data into desired business outcomes and improvements to the customer experience.

Stratecast End-to-End Billing Market Assessment

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 5 “We Accelerate Growth”

The Stratecast ODAM1 team annually assesses the role of billing within the changing communications marketplace and within the CSP monetization practice. "Billing" is defined by Stratecast as shown in the figure below, to include the major business management functions of: billing mediation, rating & charging, other core billing, policy management, interconnect & settlement, and partner management. Along with associated analytics, these monetization functions enable the management approaches of today, as well as the hope for new revenue streams in the future.

Source: Stratecast

1 The processes and tools that communications service providers (CSPs) have utilized to run their businesses have changed over time. More than a half-century ago, CSP network and business management processes were manual (OAM&P). As CSPs evolved over the years, so did the operations support systems (OSS) and business support systems (BSS) that address CSP business and network management needs. In recent years, the lines between OSS and BSS have become less clear, with much overlap. In addition, the roles in which OSS and BSS operate have expanded beyond traditional boundaries. As such, Stratecast now uses the term Operations, Orchestration, Data Analytics & Monetization (ODAM) to encompass both the traditional OSS and BSS functions and the new areas in which business and operations management must now work together, including virtualized networks and telecom data analysis.

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 6 “We Accelerate Growth”

Stratecast Billing Report Series The recently completed Stratecast assessment of the global billing marketplace involves over 100 suppliers each doing business in most regions of the world today. The findings from our analysis are delivered as a multi-part report series consisting of:

• Global CSP Billing 2016 Edition Part 1: End-to-End CSP Billing Market Forecast and Market Share Analysis provides a market share analysis and five-year market forecast for the overall, end-to-end global CSP billing market. Recently released,2 this report identifies the overall billing industry leaders, and highlights billing solution leaders by revenue within the various global regions.

• Global CSP Billing 2016 Edition Part 2: Billing Mediation Market Forecast and Market Share Analysis assesses the billing mediation sector, provides a global market share analysis, and establishes a five-year forecast for this market. This soon to be published report3 is the source for this award. It provides a market share analysis of approximately 50 suppliers that deliver mediation solutions to the global CSP market, along with a five-year revenue forecast.

• Global CSP Billing 2016 Edition Part 3: Rating & Charging and Other Core Billing Market Forecast and Market Share Analysis assesses the rating & charging sector and the other core billing sector, both individually and in combination. For each, the report delivers a five-year market forecast, and a global market share analysis of approximately 90 suppliers that operate within one or both of these billing domains. The report is scheduled for publication in July 2016.4

• Global CSP Billing 2016 Edition Part 4: Policy Management Market Forecast and Market Share Analysis. Global CSP Billing Part 4 assesses the policy management sector—in particular, what is known as the rules function. It provides a market share analysis of approximately 55 suppliers that deliver policy management rules function solutions, along with a five-year global forecast. The report will be published during third quarter 2016.

• Global CSP Billing 2016 Edition Part 5: Interconnect & Settlement and Partner Management Market Forecast and Market Share Analysis. Global CSP Billing Part 5 assesses the interconnect & settlement sector and the partner management sector, both individually and in combination. The report establishes a five-year market forecast for these two markets, and a market share analysis of the more than 60 suppliers that operate within them. This report will be published during third quarter 2016.

2 See OSSCS 17-05, Global CSP Billing 2016 Edition Part 1: End-to-End CSP Billing Market Forecast and Market Share Analysis, June, 2016. 3 See OSSCS 17-06, Global CSP Billing 2016 Edition Part 2: Billing Mediation Market Forecast and Market Share Analysis, July, 2016. 4 See OSSCS 17-07, Global CSP Billing 2016 Edition Part 3: Rating & Charging and Other Core Billing Market Forecast and Market Share Analysis, July, 2016.

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 7 “We Accelerate Growth”

These five reports constitute what Stratecast refers to as our “numbers” reports, providing market forecast and market share data for the CSP end-to-end billing market and the six billing sub-sectors. These five reports are delivered annually.

Additional Billing Functions

The monetization needs of today’s complex services require an increasingly real-time business support process that involves interaction with various network technologies, computing capabilities, external partners, and suppliers. The end-to-end billing process consists of the six primary functions previously noted in addition to others including:

• Customer Relationship Management (CRM) software has long been adjacent to CSP billing, which is used by CSPs to communicate with their end-customers. Self-care is a function that has risen in importance in recent years, to allow customers to address business issues interactively with automated systems rather than with a customer care agent. Stratecast delineates self-care as part of Other Core Billing.

• Analytics, in particular what Stratecast refers to as purpose-built analytics, is now part of each of the major billing segments.

• Product and service catalogs are an integral part of a CSP billing system, acting as business logic "glue" to define what customers pay for and what they are provided by the technology that renders a service offering. As a whole, the product catalog does not fit neatly into any of the billing segments. However, because product and service catalogs describe what defines a service, what the role is for each sub-system delivering a service, and lays out the business rules for how customers are charged when they use a service, the product and service catalog function is counted as part of Other Core Billing.

• Policy management, as depicted in the figure above, consists of a rules function, which Stratecast includes as part of billing, and an enforcement function, which Stratecast views as network capabilities mostly beyond the scope of billing.

The Role of Billing Mediation

Billing mediation was initially established as an off-line function to collect and validate network usage records for the postpaid billing process. It is designed to gather usage data from all network elements and service nodes, normalize the data, and pass this normalized data to the rating & charging engine for payment calculation. Off-line mediation can address all postpaid service functions; however, it is not equipped to handle the real-time table stakes requirements for support of prepaid services, broadband connectivity bundles, data aggregation for OSS, or the rising number of use cases tied to customer insight analysis.

To meet today’s network and service needs, to align user control functions with business and network processes, and to support customer notification requirements, mediation systems are now engineered to engage in policy-defined, bi-directional communication with any network device or business system. The concept of what Stratecast refers to as Mediation 2.0—off-line and bi-directional online mediation through a single platform,

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 8 “We Accelerate Growth”

working in collaboration with other billing functions—is critical for the success of most real-time services that involve tiered pricing plans, usage thresholds, decision analysis, and partner interactions. Mediation 2.0 solutions are essential to both business-to-business (B2B) and business-to-consumer (B2C) strategies. Mediation 2.0 is also necessary to address the evolving business needs associated with new network technologies and virtual networks.

Industry Challenges The first report in this billing series, OSSCS 17-05, Global CSP Billing 2016 Edition Part 1: End-to-End CSP Billing Market Forecast and Market Share Analysis, June 2016, provides a market share analysis for the end-to-end billing market, utilizing a base year of 2015. As in previous Stratecast forecasts, this analysis is based on the sum of revenue generated by supplier offerings in six related global billing segments including:

• Billing Mediation

• Rating & Charging

• Other Core Billing functions

• Policy Management (Rules Function)

• Interconnect & Settlement

• Partner Management

The source report for this award, Global CSP Billing 2016 Edition Part 2: Billing Mediation Market Forecast and Market Share Analysis, provides a market share analysis for the Billing Mediation market.

The findings, as published in this report, show that Huawei leads in market share for the Billing Mediation market. Stratecast believes that Huawei addresses approximately 22% of the Billing Mediation market based on revenue collected from the sale of Billing Mediation solutions. The next four competitors address approximately 18%, 12%, 12%, and 7% of the market respectively by revenue.

For this report series, Stratecast contacted more than 100 billing suppliers that address one or more of the above mentioned market segments, including approximately 48 suppliers that offer billing mediation solutions. Stratecast revenue estimates include vendors with software solution offerings that obtain revenue from license fees, maintenance fees, services associated with the initial installation and configuration of a solution, service bureau fees, cloud services fees, and installed solutions managed by a supplier. Internal CSP spending attributed to internal work teams or assistance from professional services consulting resources is not included. In addition, hardware-related revenue and revenue generated by systems integrators or companies without their own billing solutions are not included. The professional services fees for integration of new solutions with existing systems, and updates to CSP business processes are also not included in the market share analysis.

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 9 “We Accelerate Growth”

The market share analysis is developed by analyzing multiple sources including information supplied to Stratecast through a market questionnaire, information from public sources, direct interviews, and raw market data. The analysis is developed from 2015 company-level revenues, projections of future earnings, global financial market insights, as available, and our strategic acumen concerning billing functions.

To obtain estimated revenues and associated market share, Stratecast used a modified Delphi method for revenue analysis. Factors such as known deployments, publicly and privately reported revenue, customers served, press releases, financial reports, and related information were analyzed by a multi-person analyst team, each working independently, to estimate each vendor’s 2015 revenues, where such was not specifically provided. Final estimates were iterated to reach a consensus using a 90% confidence interval.

Huawei Based in Shenzhen, China, Huawei Technologies is a private information and communications technology (ICT) provider. Founded in 1987, Huawei has grown from a small local company to a global organization, with publicly-reported 2015 revenues of approximately US $60.8 billion. In addition to network equipment and network-based solutions, Huawei offers a range of ODAM products, as well as solutions aimed at the consumer and enterprise markets. The company reports that its monetization solutions are addressing the communications needs of approximately 1.5 billion customers at over 140 CSPs, in more than 95 countries.

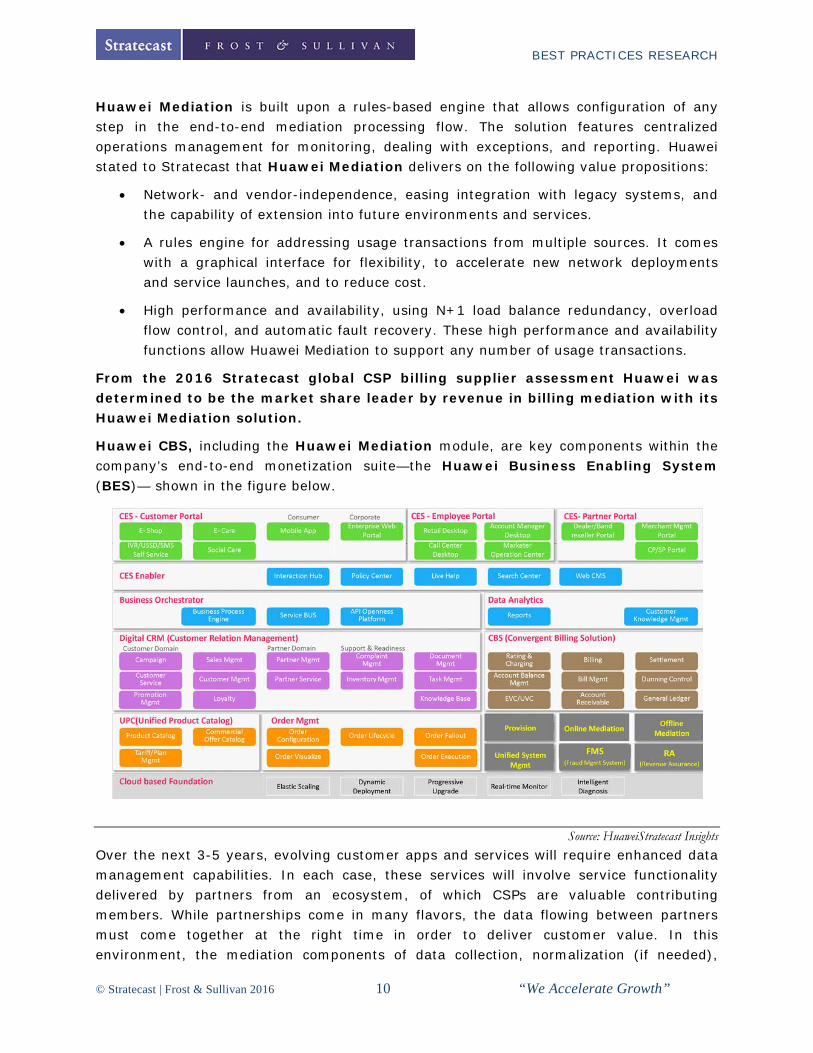

Huawei offers a full complement of billing, policy, customer, and partner management solutions that span all six segments of CSP billing. Most of the functionality modules that define Huawei's billing solution, are contained within the Huawei Convergent Billing Solution (CBS). The Huawei Mediation module is a part of CBS as noted in the figure below.

Source: Huawei Huawei Mediation delivers convergent mediation capabilities that support any service, on any network. Designed for ease of configuration and management, the solution includes pre-built interfaces, templates, and a Web-based configuration platform to simplify integration with new network elements, services, and downstream systems. The company reports to Stratecast that the solution improves time to market for new services from “months to days.”

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 10 “We Accelerate Growth”

Huawei Mediation is built upon a rules-based engine that allows configuration of any step in the end-to-end mediation processing flow. The solution features centralized operations management for monitoring, dealing with exceptions, and reporting. Huawei stated to Stratecast that Huawei Mediation delivers on the following value propositions:

• Network- and vendor-independence, easing integration with legacy systems, and the capability of extension into future environments and services.

• A rules engine for addressing usage transactions from multiple sources. It comes with a graphical interface for flexibility, to accelerate new network deployments and service launches, and to reduce cost.

• High performance and availability, using N+1 load balance redundancy, overload flow control, and automatic fault recovery. These high performance and availability functions allow Huawei Mediation to support any number of usage transactions.

From the 2016 Stratecast global CSP billing supplier assessment Huawei was determined to be the market share leader by revenue in billing mediation with its Huawei Mediation solution.

Huawei CBS, including the Huawei Mediation module, are key components within the company’s end-to-end monetization suite—the Huawei Business Enabling System (BES)— shown in the figure below.

Source: HuaweiStratecast Insights Over the next 3-5 years, evolving customer apps and services will require enhanced data management capabilities. In each case, these services will involve service functionality delivered by partners from an ecosystem, of which CSPs are valuable contributing members. While partnerships come in many flavors, the data flowing between partners must come together at the right time in order to deliver customer value. In this environment, the mediation components of data collection, normalization (if needed),

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 11 “We Accelerate Growth”

aggregation by customer, and correlation with each customer service, are essential for effective service operability.

As a service delivers customer value, usage information should be collected and analyzed to help partners understand customer behavior. Data analysis, through usage data mediation, is essential for comparing service usage with B2B partner contract terms, and in identifying accountability of each partner-provided piece of service functionality.

Huawei continues to gain momentum within the global business and operations management sectors of the communications industry. Huawei has shown market growth with its billing solutions, particularly over the past seven years, equal to or exceeding the growth rate of the global end-to-end billing market. Most importantly, in 2016 Huawei leads the billing mediation market segment by revenue. It has accomplished this feat through the support it provides to CSP customers across the world.

Huawei has achieved success in the global CSP mediation market by winning new CSP customers each year, and by expanding its billing solution capabilities with existing customers—a formula that works in any industry. Stratecast expects Huawei’s success to continue, and for the company to challenge the market leaders in every segment of billing in the months to come.

Huawei Market Leadership The 2016 Stratecast Global Market Leadership Award in CSP Billing for the Billing Mediation Market is judged based on ten criteria detailed later in this document. Huawei was compared against two other leading suppliers in the CSP billing mediation space.

The following details a selection of the comparisons from the ten criteria. The data supporting these comparisons comes from Stratecast report: OSSCS 17-06, Global CSP Billing 2016 Edition Part 2: Billing Mediation Market Forecast and Market Share Analysis, July 2016.

Growth Strategy Excellence

Stratecast assesses the end-to-end CSP billing market every year, which involves a reach out to over 100 suppliers of billing solution functionality. This market, and most of its components, have each grown over the last six years with some segments growing faster than others. One of these growth segments is billing mediation. Stratecast forecasts the five-year compound annual growth rate (CAGR) for the billing mediation market to continue to climb at a high single-digit rate from 2016-2020, one of the highest growth rates of all billing sectors. This growth comes from a number of sources, each relating to changing business needs and customer expectations.

In a market that has been expanding such as CSP billing mediation, growth is essential to the supplier community for even maintaining one’s market position. Comparing the Stratecast 2016 billing mediation market assessment with the previous assessment, some of the top seven suppliers grew their annual revenue attained in billing mediation and still lost market share. Huawei increased its annual mediation-based revenues substantially

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 12 “We Accelerate Growth”

and in so doing, increased market share in this sector. Huawei now addresses approximately 22% of the billing mediation market, up from 20% as noted in our 2015 global billing assessment. This increase is a direct result of the need by service providers to address the growing volume of user generated data, the accountability of that data, and now the mediation of data for multiple internal business functions that go beyond just billing.

Implementation Excellence

Stratecast recognizes that to be a leader in CSP billing, in an individual segment of CSP billing, or in any of the areas of CSP ODAM, a supplier must be able to implement the solutions they have sold; each and every time. An implementation that goes less smoothly than planned, can cause a CSP to lose trust in a supplier; an implementation that fails can have reverberations far beyond the individual CSP customer. The CSP community (and analyst community) is relatively small and less than expected results are noted throughout the industry, sometimes for an extended time.

Stratecast's knowledge of the excellence in implementation with regard to Huawei is well founded based on several customer testimonials, continued press from the company that identifies CSPs by name, and the ongoing discussions Stratecast has with both Huawei and its competitors. Together, these factors indicate that Huawei is keeping its existing customers happy as it continues to gain new ones.

Brand Strength

Brand is often of great importance to a customer when choosing a product for purchase. This is true of consumer goods and it holds for CSPs when they choose their ODAM systems with price tags that usually reach into the millions of dollars. In the area of CSP end-to-end billing, CSPs are trusting their ability to generate revenue, and even in their ability to stay in business, on a vendor—trust in a company and a brand is of utmost importance.

Stratecast is certain that increasing revenues correlate strongly with CSP brand trust. Huawei increased its revenues significantly and therefore its brand strength since Stratecast’s previous assessment of the CSP billing market one year ago. This occurred at both the overall billing market level and within various billing segments, including billing mediation.

Product Quality

Similar to the previous two criteria, product quality is very important to CSPs, who expect any solution they purchase to not only work as promised, but to meet their specific business needs within the timeframe of delivery that is agreed to with the software supplier. Poor quality solutions immediately cause issues with the CSP customer and, as mentioned under the implementation section of this report, bad news travels fast, which is hard to overcome within the communications marketplace. Stratecast is certain revenue growth indicates that CSP customers continue to put trust in a supplier, the quality of their

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 13 “We Accelerate Growth”

products, and in the supplier's ability to satisfy all needed business change needs in order for the new solution to operate effectively.

Huawei’s continued growth over the last few years, one of the highest rates amongst the revenue leaders, is a strong indicator that its CSP customers find the company's products and solution delivery capabilities to either meet or exceed expectations.

Price/Performance Value

Huawei entered the ODAM marketplace as a lower cost supplier, initially offset by its network equipment sales, to gain a foothold in the market. As the company has grown to be a revenue leader in the CSP billing market, its billing solution offerings, including mediation, have increased in functionality, in quality, and in performance. Additionally, the company's business support software group now stands on its own and "deals" involving network equipment bundles are no longer the major means for project delivery success. The Huawei business management software group carries a profit/loss quota.

To impress its customers on pricing, Huawei provides a price/performance advantage that is attractive to many of its customers, especially those in emerging markets. In fact, Huawei explained to Stratecast that many of its newest CSP customers have purchased its mediation and billing solution offerings due not only to Huawei's solution pricing offers, but also from the company's long-term strategy and vision tied to its latest release of its end-to-end billing, customer and partner management solution, known as the Huawei Business Enablement System (BES).

Customer Service Experience

Customer service is very important to CSPs, who expect any solution they purchase to work as promised and their suppliers to always put their experience as the top of the list. Poor quality solutions immediately cause issues with the CSP customer and degrade their service experience. As mentioned under the implementation section of this report, bad news travels fast, which is hard to overcome. Customer service experience is not something that Stratecast measures directly, but revenue growth indicates that CSP customers continue to put trust in a supplier and the quality of their products.

Huawei’s continued growth over the last few years, one of the highest rates amongst the global CSP billing solution leaders by revenue, is a strong indicator that its CSP customers find their customer service experience with Huawei’s products and solution capabilities to meet or exceed expectations.

Huawei has had a solid "can do" attitude for several years, in delivering solutions that meet customer expectations. With this approach to business, combined with Huawei's long-term strategy for the communications marketplace, CSP customers are finding that Huawei solutions can and do meet their expectations.

Conclusion Stratecast recently concluded its annual assessment of the end-to-end global CSP billing market. We specifically evaluated the role of billing and policy management within the CSP

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 14 “We Accelerate Growth”

business support system and monetization operations. In so doing, Stratecast reached out to and analyzed over 100 suppliers, covering various aspects of the end-to-end CSP billing marketplace. Stratecast defines CSP billing to include six related segments: Billing Mediation; Rating & Charging; Other Core Billing functionality; Policy Management (Rules Function); Interconnect & Settlement; and Partner Management capabilities.

Stratecast analysis of the Mediation segment of the global end-to-end CSP billing market revealed that Huawei leads in market share based on 2015 supplier revenue. Stratecast analysis identified Huawei as addressing approximately 22% of this market.

In recognition of Huawei's superior ability to lead in market share and address communications service provider’s key challenges, Stratecast awards the 2016 Stratecast Global Market Leadership Award in CSP Billing for the Billing Mediation Market to Huawei.

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 15 “We Accelerate Growth”

Significance of Market Leadership Ultimately, growth in any organization depends upon customers purchasing from your company, and then making the decision to return time and again. Loyal customers become brand advocates; brand advocates recruit new customers; the company grows; and then it attains market leadership. To achieve and maintain market leadership, an organization must strive to be best-in-class in three key areas: understanding demand, nurturing the brand, and differentiating from the competition.

Understanding Market Leadership As discussed on the previous page, driving demand, strengthening the brand, and competitive differentiation all play a critical role in a company’s path to market leadership. This three-fold focus, however, is only the beginning of the journey and must be complemented by an equally rigorous focus on the customer experience. Best-practice organizations therefore commit to the customer at each stage of the buying cycle and continue to nurture the relationship once the customer has made a purchase. In this manner, such companies build a loyal, ever-growing customer base and methodically add to their market share over time.

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 16 “We Accelerate Growth”

Key Performance Criteria For the Market Leadership Award, Stratecast | Frost & Sullivan analysts focused on specific criteria to determine the areas of performance excellence that led to the company’s leadership position. The criteria that were considered include (although not limited to) the following:

Criterion Requirement

Growth Strategy Excellence Demonstrated ability to consistently identify, prioritize, and pursue emerging growth opportunities

Implementation Excellence Processes support the efficient and consistent implementation of tactics designed to support the strategy

Brand Strength The possession of a brand that is respected, recognized, and remembered

Product Quality The product or service receives high marks for performance, functionality and reliability at every stage of the life cycle

Product Differentiation The product or service has carved out a market niche, whether based on price, quality, uniqueness of offering (or some combination of the three) that another company cannot easily duplicate

Technology Leverage Demonstrated commitment to incorporating leading edge technologies into product offerings, for greater product performance and value

Price/Performance Value Products or services offer the best value for the price, compared to similar offerings in the market

Customer Purchase Experience Customers feel like they are buying the most optimal solution that addresses both their unique needs and their unique constraints

Customer Ownership Experience Customers are proud to own the company’s product or service, and have a positive experience throughout the life of the product or service

Customer Service Experience Customer service is accessible, fast, stress-free, and of high quality

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 17 “We Accelerate Growth”

The Intersection between 360-Degree Research and Best Practices Awards Stratecast | Frost & Sullivan’s 360-degree research methodology represents the analytical rigor of our research process. It offers a 360-degree-view of industry challenges, trends, and issues by integrating all 7 of Stratecast | Frost & Sullivan's research methodologies. Too often, companies make important growth decisions based on a narrow understanding of their environment, leading to errors of both omission and commission. Successful growth strategies are founded on a thorough understanding of market, technical, economic, financial, customer, best practices, and demographic analyses. The integration of these research disciplines into the 360-degree research methodology provides an evaluation platform for benchmarking industry players and for identifying those performing at best-in-class levels.

360-DEGREE RESEARCH: SEEING ORDER IN THE CHAOS

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 18 “We Accelerate Growth”

Best Practices Recognition: 10 Steps to Researching, Identifying, and Recognizing Best Practices Stratecast | Frost & Sullivan Awards follow a 10-step process to evaluate award candidates and assess their fit with select best practice criteria. The reputation and integrity of the Awards are based on close adherence to this process.

STEP OBJECTIVE KEY ACTIVITIES OUTPUT

1 Monitor, target, and screen

Identify award recipient candidates from around the globe

• Conduct in-depth industry research

• Identify emerging sectors • Scan multiple geographies

Pipeline of candidates who potentially meet all best-practice criteria

2 Perform 360-degree research

Perform comprehensive, 360-degree research on all candidates in the pipeline

• Interview thought leaders and industry practitioners

• Assess candidates’ fit with best-practice criteria

• Rank all candidates

Matrix positioning all candidates’ performance relative to one another

3

Invite thought leadership in best practices

Perform in-depth examination of all candidates

• Confirm best-practice criteria

• Examine eligibility of all candidates

• Identify any information gaps

Detailed profiles of all ranked candidates

4 Initiate research director review

Conduct an unbiased evaluation of all candidate profiles

• Brainstorm ranking options • Invite multiple perspectives

on candidates’ performance • Update candidate profiles

Final prioritization of all eligible candidates and companion best-practice positioning paper

5 Assemble panel of industry experts

Present findings to an expert panel of industry thought leaders

• Share findings • Strengthen cases for

candidate eligibility • Prioritize candidates

Refined list of prioritized award candidates

6 Conduct global industry review

Build consensus on award candidates’ eligibility

• Hold global team meeting to review all candidates

• Pressure-test fit with criteria • Confirm inclusion of all

eligible candidates

Final list of eligible award candidates, representing success stories worldwide

7 Perform quality check

Develop official award consideration materials

• Perform final performance benchmarking activities

• Write nominations • Perform quality review

High-quality, accurate, and creative presentation of nominees’ successes

8 Reconnect with panel of industry experts

Finalize the selection of the best-practice award recipient

• Review analysis with panel • Build consensus • Select winner

Decision on which company performs best against all best-practice criteria

9 Communicate recognition

Inform award recipient of award recognition

• Present award to the CEO • Inspire the organization for

continued success • Celebrate the recipient’s

performance

Announcement of award and plan for how recipient can use the award to enhance the brand

10 Take strategic action

Share award news with stakeholders and customers

• Coordinate media outreach • Design a marketing plan • Assess award’s role in future

strategic planning

Widespread awareness of recipient’s award status among investors, media personnel, and employees

BEST PRACTICES RESEARCH

© Stratecast | Frost & Sullivan 2016 19 “We Accelerate Growth”

About ODAM The processes and tools that communications service providers (CSPs) have utilized to run their businesses have changed over time. More than a half-century ago, CSP network and business management processes were manual (OAM&P). As CSPs evolved over the years, so did the operations support systems (OSS) and business support systems (BSS) that address CSP business and network management needs. In recent years, the lines between OSS and BSS have become less clear, with much overlap. In addition, the roles in which OSS and BSS operate have expanded beyond traditional boundaries. As such, Stratecast now uses the term Operations, Orchestration, Data Analytics & Monetization (ODAM) to encompass both the traditional OSS and BSS functions and the new areas in which business and operations management must now work together, including virtualized networks and telecom data analysis.

About Stratecast Stratecast collaborates with our clients to reach smart business decisions in the rapidly evolving and hyper-competitive Information and Communications Technology markets. Leveraging a mix of action-oriented subscription research and customized consulting engagements, Stratecast delivers knowledge and perspective that is only attainable through years of real-world experience in an industry where customers are collaborators; today’s partners are tomorrow’s competitors; and agility and innovation are essential elements for success. Contact your Stratecast Account Executive to engage our experience to assist you in attaining your growth objectives.

About Frost & Sullivan Frost & Sullivan, the Growth Partnership Company, enables clients to accelerate growth and achieve best in class positions in growth, innovation and leadership. The company's Growth Partnership Service provides the CEO and the CEO's Growth Team with disciplined research and best practice models to drive the generation, evaluation and implementation of powerful growth strategies. Frost & Sullivan leverages almost 50 years of experience in partnering with Global 1000 companies, emerging businesses and the investment community from 31 offices on six continents. To join our Growth Partnership, please visit http://www.frost.com.