2015 · sigma members are motor fuel marketers, but they market in a wide variety of ways and in...

TRANSCRIPT

2015STATISTICAL REPORT

AN IN-DEPTH

SURVEY OF SIGMA

MEMBERS

OPERATIONS, SALES,

AND SERVICE

DURING 2014

B

SIGMA STATISTICAL REPORT 2015

EXECUTIVE COMMITTEE

PresidentThomas G. GreshamDouble Quick, Inc.Indianola, MS

First Vice PresidentDavid BakerWarrenton Oil CompanyWarrenton, MO

Second Vice PresidentWilliam Bradford PuryearMansfield Energy Corp.Gainesville, GA

Secretary TreasurerDavid CollinsWilson Fuel Co. LtdHalifax, NS, Canada

Immediate Past PresidentThomas A. SchmidtU.S. Venture, Inc.Appleton, WI

BOARD OF DIRECTORSBob ColemanColeman Oil CompanyLewiston, ID

Erin GraziosiRobinson Oil CorporationSanta Clara, CA

Richard GuttmanGuttman Energy Inc.Belle Vernon, PA

Doug HartleyThe Hartley CompanyCambridge, OH

David HutchinsonHutchinson Oil Co.Elk City, OK

Jeff LeBeouf2825 Railroad AveCeres, CA

Jeff LykinsLykins Energy SolutionsMilford, OH

Max E. McBrayer, Jr.RaceTrac Petroleum, Inc.Atlanta, GA

Kerry OliverCarterEnergy, a division of World Fuel Services, Inc.Overland Park, KS

Jack C. PesterPester Marketing CompanyHouston, TX

Brian S. YoungYoung Oil, Inc.Piedmont, AL

Joseph ZietlowKwik Trip, Inc.La Crosse, WI

CounselR. Timothy ColumbusSteptoe & Johnson, LLPWashington, DC

Staff LiaisonRyan McNuttSIGMAFairfax, VA 22030

SIGMA PRESIDENTS

Phil L. Siteman1958 1960, Missouri

A.M. Blakely1960 1961, Arizona

Calvin Houghland1961 1962, Tennessee

R.J. Peterson1962 1963, Missouri

George H. Panuska1963 1965, Ohio

Mary Hudson1965 1967, Kansas

James Thornton1967 1968, Indiana

Randy Deer1968 1969, Ohio

R.J. Peterson1969 1972, Illinois

Frederick Lichtman1972 1974, Michigan

Newell Baker1974 1976, Missouri

Herbert A. Sostek1976 1978, Massachusetts

Thomas N. Allen1978 1980, Virginia

Richard L. Singletary1980 1981, Georgia

Roy R. Mason1981 1983, Alabama

Michael S. Kirschner1983 1985, Pennsylvania

John A. Wickland III1985 1987, California

Carl Bolch, Jr.1987 1989, Georgia

F.C. Tally Roberts, Jr.1989-1991, North Carolina

R. H. Tod Butler, Jr.1991-1993, Michigan

Douglas L. True1993-1995, Washington

Leo Liebowitz1995-1997, New York

Bob Phillips, Jr.1997-1999, Oklahoma

Thomas L. Robinson1999-2001, California

Michael Ports2001-2004, Ohio

William S. Shipley, III2004-2006, Pennsylvania

Paul Reid2006-2008, New York

Carl Boyett2008-2010, California

Frank Greinke2010-2012, California

Thomas Schmidt2012-2014, Wisconsin

Thomas Gresham2014-Present, Mississippi

SIGMA STAFF AND COUNSEL

Chief Executive OfficerRyan McNutt [email protected]

Director of EducationDennis [email protected]

Director of Marketing Services and Database ManagerBrian [email protected]

Director of Meetings and Manager of AdministrationMary Alice [email protected]

Staff Support ManagerMaria [email protected]

Director of MarketingNancy [email protected]

Director of Communications and Political EngagementAmy [email protected]

Director of Business DevelopmentMarilyn [email protected]

Assitant Director of MarketingGinny [email protected]

SIGMA EXECUTIVE OFFICES3930 Pender Drive, Suite 340Fairfax, VA 22030PHONE: (703) 709-7000FAX: (703) 709-7007E-MAIL: [email protected]: www.sigma.org

COUNSELR. Timothy [email protected](202)429-6222

Steptoe & Johnson1330 Connecticut Ave. NWWashington, D.C. 20036-1795PHONE: (202) 429 3000FAX: (202) 429-3902

2015 STATISTICAL REPORT

C

SIGMA STATISTICAL REPORT 2015

NUMBER OF GALLONS SOLD (BILLIONS)

EACH YEAR, SIGMA conducts a survey of its members. This survey enables SIGMA to develop a better understanding of what is happening in the fuels market, which, in turn, allows SIGMA to better serve its members. The report also provides timely information on how SIGMA members are responding to current industry challenges– whether they are legislative–regulatory, or market-related as well as how they are approaching new opportunities.

2014 marked a period of significant change in the fuel marketing industry. As SIGMA members evolved to remain on the cutting edge as the most innovative marketers, so too did our survey evolve to better capture the activities in which SIGMA members are currently involved. In this regard, outdated questions were eliminated from the survey and new questions added, with the intention of providing a more precise and thorough snapshot of SIGMA members and what they do.

As in previous years, it was clear from the responses received that SIGMA members continue to maintain a unique balance between fuel supply and operations management in their business strategies. This leads to lower consumer prices for both gasoline and diesel fuel and benefits the overall U.S. economy tremendously.

In 2014, SIGMA members continued to adapt to the changing nature of the fuel marketing industry. Declining demand has created a new market landscape. As new fuels continue to enter the market, SIGMA members’ decisions regarding what fuels to sell remain driven by their availability, as well as federal and state requirements related to their sale. For this reason, the Renewable Fuel Standard still tops the list as one of SIGMA’s most significant issues.

Of particular note in 2015, issues related to payment systems, including data breach and security

legislation and swipe fees, are also of significant interest to SIGMA members. Employment matters, such as proposals to revise the rules related to overtime pay and the franchisee-franchisor relationship are also a priority for SIGMA. And, of course, funding for the Highway Trust Fund remains of paramount importance as Congress considers long-term funding mechanisms for federal surface transportation programs.

SIGMA is responsive to its members’ needs, and has therefore added internet gaming (banning online lottery sales) and menu labeling requirements to the list of priority issues under consideration in the 114th Congress.

As the market, both domestic and global, in which SIGMA members operate continues to change, so do SIGMA members’ interests and operations. This ongoing evolution, and SIGMA members’ longstanding commitment to meeting demand, is reflected in the 2015 Annual Statistical Report.

EMPLOYEES (GASOLINE OR C-STORE ONLY)

353,549

382,000

367,023

325,500

225,406

2014

2013

2012

2011

2010

NUMBER OF RETAIL FUEL OUTLETS SUPPLIED

50,980

55,800

56,015

55,000

2014

2013

2012

2011

79.5

76.3

67.4

70.4

2014

2013

2012

2011

D

SIGMA STATISTICAL REPORT 2015

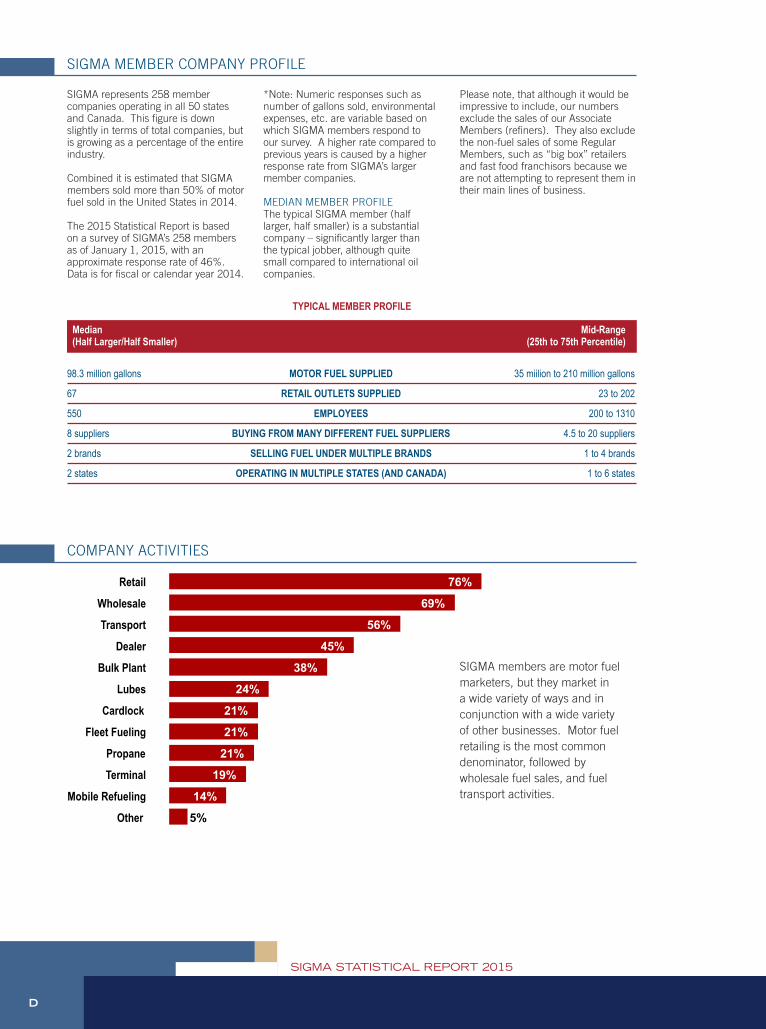

SIGMA represents 258 member companies operating in all 50 states and Canada. This figure is down slightly in terms of total companies, but is growing as a percentage of the entire industry.

Combined it is estimated that SIGMA members sold more than 50% of motor fuel sold in the United States in 2014.

The 2015 Statistical Report is based on a survey of SIGMA’s 258 members as of January 1, 2015, with an approximate response rate of 46%. Data is for fiscal or calendar year 2014.

*Note: Numeric responses such as number of gallons sold, environmental expenses, etc. are variable based on which SIGMA members respond to our survey. A higher rate compared to previous years is caused by a higher response rate from SIGMA’s larger member companies.

MEDIAN MEMBER PROFILEThe typical SIGMA member (half larger, half smaller) is a substantial company – significantly larger than the typical jobber, although quite small compared to international oil companies.

Please note, that although it would be impressive to include, our numbers exclude the sales of our Associate Members (refiners). They also exclude the non-fuel sales of some Regular Members, such as “big box” retailers and fast food franchisors because we are not attempting to represent them in their main lines of business.

SIGMA MEMBER COMPANY PROFILE

TYPICAL MEMBER PROFILE

Median Mid-Range(Half Larger/Half Smaller) (25th to 75th Percentile)

98.3 million gallons MOTOR FUEL SUPPLIED 35 miilion to 210 million gallons

67 RETAIL OUTLETS SUPPLIED 23 to 202

550 EMPLOYEES 200 to 1310

8 suppliers BUYING FROM MANY DIFFERENT FUEL SUPPLIERS 4.5 to 20 suppliers

2 brands SELLING FUEL UNDER MULTIPLE BRANDS 1 to 4 brands

2 states OPERATING IN MULTIPLE STATES (AND CANADA) 1 to 6 states

SIGMA members are motor fuel marketers, but they market in a wide variety of ways and in conjunction with a wide variety of other businesses. Motor fuel retailing is the most common denominator, followed by wholesale fuel sales, and fuel transport activities.

5%

14%

19%

21%

21%

21%

24%

38%

45%

56%

69%

76%

Other

Mobile Refueling

Terminal

Propane

Fleet Fueling

Cardlock

Lubes

Bulk Plant

Dealer

Transport

Wholesale

Retail

COMPANY ACTIVITIES

E

SIGMA STATISTICAL REPORT 2015

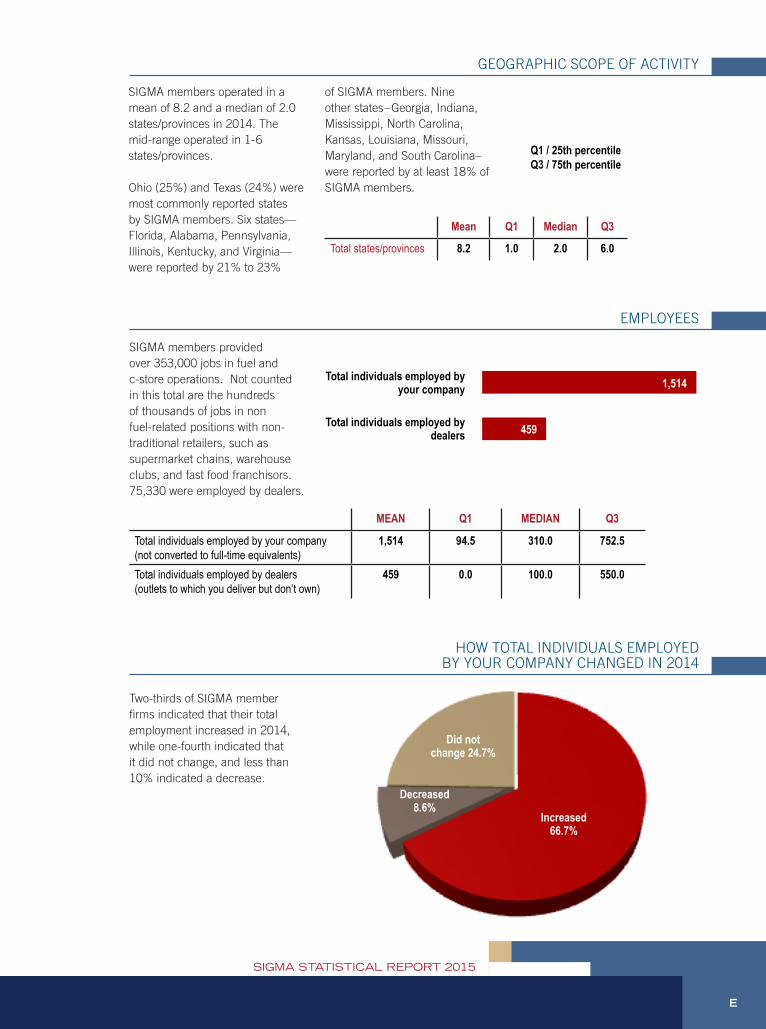

EMPLOYEES

SIGMA members provided over 353,000 jobs in fuel and c-store operations. Not counted in this total are the hundreds of thousands of jobs in non fuel-related positions with non-traditional retailers, such as supermarket chains, warehouse clubs, and fast food franchisors. 75,330 were employed by dealers.

MEAN Q1 MEDIAN Q3

Total individuals employed by your company (not converted to full-time equivalents)

1,514 94.5 310.0 752.5

Total individuals employed by dealers (outlets to which you deliver but don’t own)

459 0.0 100.0 550.0

459

1,514

Total individuals employed by dealers

Total individuals employed by your company

SIGMA members operated in a mean of 8.2 and a median of 2.0 states/provinces in 2014. The mid-range operated in 1-6 states/provinces.

Ohio (25%) and Texas (24%) were most commonly reported states by SIGMA members. Six states—Florida, Alabama, Pennsylvania, Illinois, Kentucky, and Virginia—were reported by 21% to 23%

of SIGMA members. Nine other states–Georgia, Indiana, Mississippi, North Carolina, Kansas, Louisiana, Missouri, Maryland, and South Carolina–were reported by at least 18% of SIGMA members.

Mean Q1 Median Q3

Total states/provinces 8.2 1.0 2.0 6.0

GEOGRAPHIC SCOPE OF ACTIVITY

Q1 / 25th percentileQ3 / 75th percentile

HOW TOTAL INDIVIDUALS EMPLOYED BY YOUR COMPANY CHANGED IN 2014

Two-thirds of SIGMA member firms indicated that their total employment increased in 2014, while one-fourth indicated that it did not change, and less than 10% indicated a decrease.

Increased 66.7%

Decreased 8.6%

Did not change 24.7%

F

SIGMA STATISTICAL REPORT 2015

SIGMA members report a mean of 194 total motor fuel outlets, including 114 direct operated retail (COCO), 54 open or “contract” direct retail outlets (DODO), 19.1 lessee dealer retail outlets (CODO), and 7.3 other types of outlets. As with many of our other indicators, the median is frequently 0 because not all SIGMA members operate them and the statistics below are based on the member responses received. A total of 78% of SIGMA members operate COCO, 52% CODO, 50% DODO, and 38% some other types of outlets, including cardlocks, bulk, or plant.

194

7.3

19.1

53.9

113.9

Total Outlets

Other types of outlets (cardlocks, bulk, plant)

Lessee Dealer Retail Outlet (CODO)

Open ("contract") Dealer Retail Outlet (DODO)

Direct Operated Retail Outlet (COCO)

MEAN Q1 MEDIAN Q3

Direct Operated Retail Outlet (COCO) 113.9 3 20 57

Lessee Dealer Retail Outlet (CODO) 19.1 0 1 12

Open (“contract”) Dealer Retail Outlet (DODO) 53.9 0 0 42

Other types of outlets (cardlocks, bulk, plant) 7.3 0 0 4

Total Outlets 194 23 67 202

MOTOR FUEL OUTLETS: TOTAL SUPPLIED BY CATEGORY

INDUSTRY LOCATIONS ENTERED OR EXITED, PAST 12 MONTHS

SIGMA members reported a mean of 5.1 COCO, 3.7 DODO, and 0.8 CODO new to industry in 2014; while they exited a mean of 2.8 COCO, 8.0 DODO, and 0.4 CODO locations. Aggregating all responses shows SIGMA members exited a net of 200 more locations than they entered in 2014. As indicated in the table below, the actual proportion of members who entered or exited is a minority of responding members, and some did not answer the question because was not applicable. PROPORTION CHANGING NEW EXITED

COCO 39% 31%

CODO 12% 8%

DODO 29% 20%

8.0

0.4

2.8

3.7

0.8

5.1

DODO

CODO

COCO

New locations Exited locations

G

SIGMA STATISTICAL REPORT 2015

BRANDS

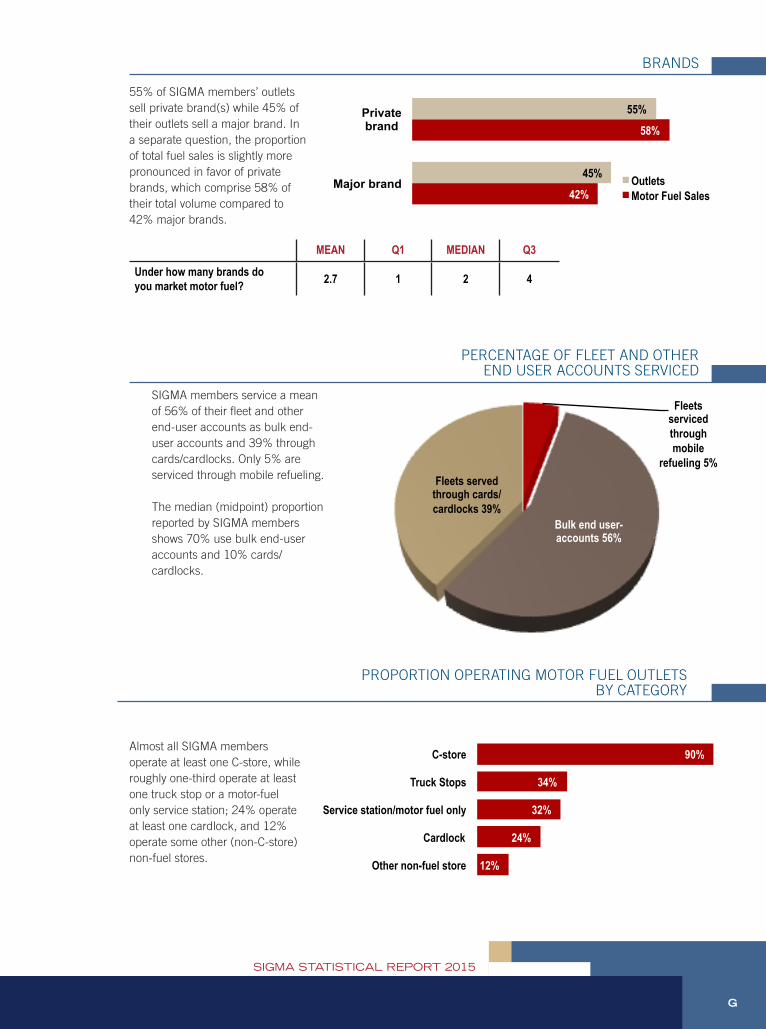

55% of SIGMA members’ outlets sell private brand(s) while 45% of their outlets sell a major brand. In a separate question, the proportion of total fuel sales is slightly more pronounced in favor of private brands, which comprise 58% of their total volume compared to 42% major brands.

MEAN Q1 MEDIAN Q3

Under how many brands do you market motor fuel? 2.7 1 2 4

PERCENTAGE OF FLEET AND OTHER END USER ACCOUNTS SERVICED

SIGMA members service a mean of 56% of their fleet and other end-user accounts as bulk end-user accounts and 39% through cards/cardlocks. Only 5% are serviced through mobile refueling.

The median (midpoint) proportion reported by SIGMA members shows 70% use bulk end-user accounts and 10% cards/cardlocks.

Fleets serviced through mobile

refueling 5%

Bulk end user-accounts 56%

Fleets served through cards/ cardlocks 39%

42%

58%

45%

55%

Major brand

Private brand

Outlets Motor Fuel Sales

PROPORTION OPERATING MOTOR FUEL OUTLETS BY CATEGORY

Almost all SIGMA members operate at least one C-store, while roughly one-third operate at least one truck stop or a motor-fuel only service station; 24% operate at least one cardlock, and 12% operate some other (non-C-store) non-fuel stores. 12%

24%

32%

34%

90%

Other non-fuel store

Cardlock

Service station/motor fuel only

Truck Stops

C-store

H

SIGMA STATISTICAL REPORT 2015

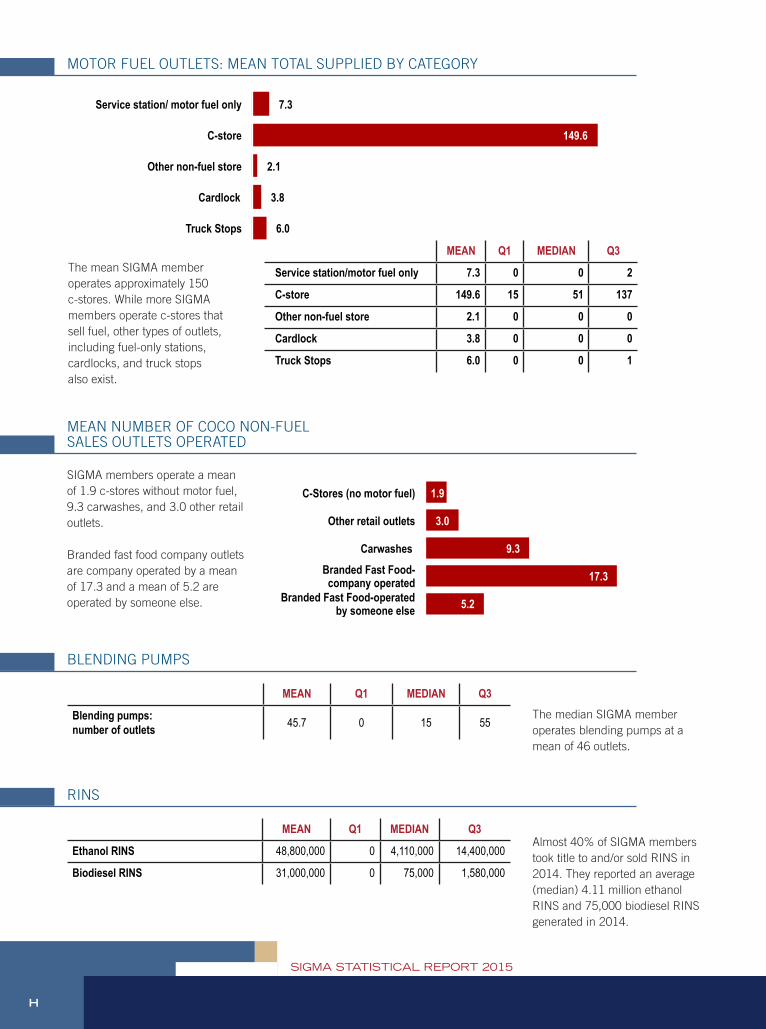

The mean SIGMA member operates approximately 150 c-stores. While more SIGMA members operate c-stores that sell fuel, other types of outlets, including fuel-only stations, cardlocks, and truck stops also exist.

MEAN Q1 MEDIAN Q3

Service station/motor fuel only 7.3 0 0 2

C-store 149.6 15 51 137

Other non-fuel store 2.1 0 0 0

Cardlock 3.8 0 0 0

Truck Stops 6.0 0 0 1

6.0

3.8

2.1

149.6

7.3

Truck Stops

Cardlock

Other non-fuel store

C-store

Service station/ motor fuel only

MOTOR FUEL OUTLETS: MEAN TOTAL SUPPLIED BY CATEGORY

MEAN NUMBER OF COCO NON-FUEL SALES OUTLETS OPERATED

SIGMA members operate a mean of 1.9 c-stores without motor fuel, 9.3 carwashes, and 3.0 other retail outlets.

Branded fast food company outlets are company operated by a mean of 17.3 and a mean of 5.2 are operated by someone else.

The median SIGMA member operates blending pumps at a mean of 46 outlets.

Almost 40% of SIGMA members took title to and/or sold RINS in 2014. They reported an average (median) 4.11 million ethanol RINS and 75,000 biodiesel RINS generated in 2014.

BLENDING PUMPS

RINS

MEAN Q1 MEDIAN Q3

Blending pumps: number of outlets 45.7 0 15 55

MEAN Q1 MEDIAN Q3

Ethanol RINS 48,800,000 0 4,110,000 14,400,000

Biodiesel RINS 31,000,000 0 75,000 1,580,000

5.2

17.3

9.3

3.0

1.9

Branded Fast Food-operated by someone else

Branded Fast Food-company operated

Carwashes

Other retail outlets

C-Stores (no motor fuel)

I

SIGMA STATISTICAL REPORT 2015

MEAN Q1 MEDIAN Q3

From how many different suppliers did you purchase fuel

17.0 4.5 8.0 20.0

Refined in the U.S. 95%

Directly imported by or for you

1%

Imported as refined

product, but by someone

else 4%

SUPPLIERS: ESTIMATED PORTION OF TOTAL PRODUCT PURCHASES

AVERAGE ANNUAL SALES OF MOTOR FUEL

0.9

6.1

27.7

125.0

132.0

142.0

E85

All blends above E10 &below E85

Biodiesel (B5, B11, B20-99, B100)

Gasoline, blended

Conventional diesel

Gasoline, conventional

Millions of

MEAN Q1 MEDIAN Q3 % REPORTING

Conventional diesel 132,000,000 3,750,000 11,900,000 48,000,000 86%Biodiesel (B5, B11, B20-99, B100) 27,700,000 0 0 3,000,000 47%Gasoline, conventional 142,000,000 0 889,000 18,200,000 63%Gasoline, blended 125,000,000 0 26,000,000 109,000,000 70%E85 865,000 0 0 151,000 32%All blends above E10 &below E85 6,080,000 0 0 0 9%Total gallons (all types) 434,000,000 35,000,000 98,300,000 210,000,000

Estimated 2014 fuel sales by SIGMA members totaled 79.5 billion gallons, which is higher than in 2013. SIGMA members account for more than 50 percent of the U.S. motor fuels business.

An average SIGMA member sold about 434 million gallons of fuel in 2014. That number is influenced by the nearly 10 percent of member companies that sell in excess of one billion gallons each. The more meaningful number is the median of 98.3 million gallons.

J

SIGMA STATISTICAL REPORT 2015

LUBRICANTS

Under major brands 76.8%

Private brands 23.3%

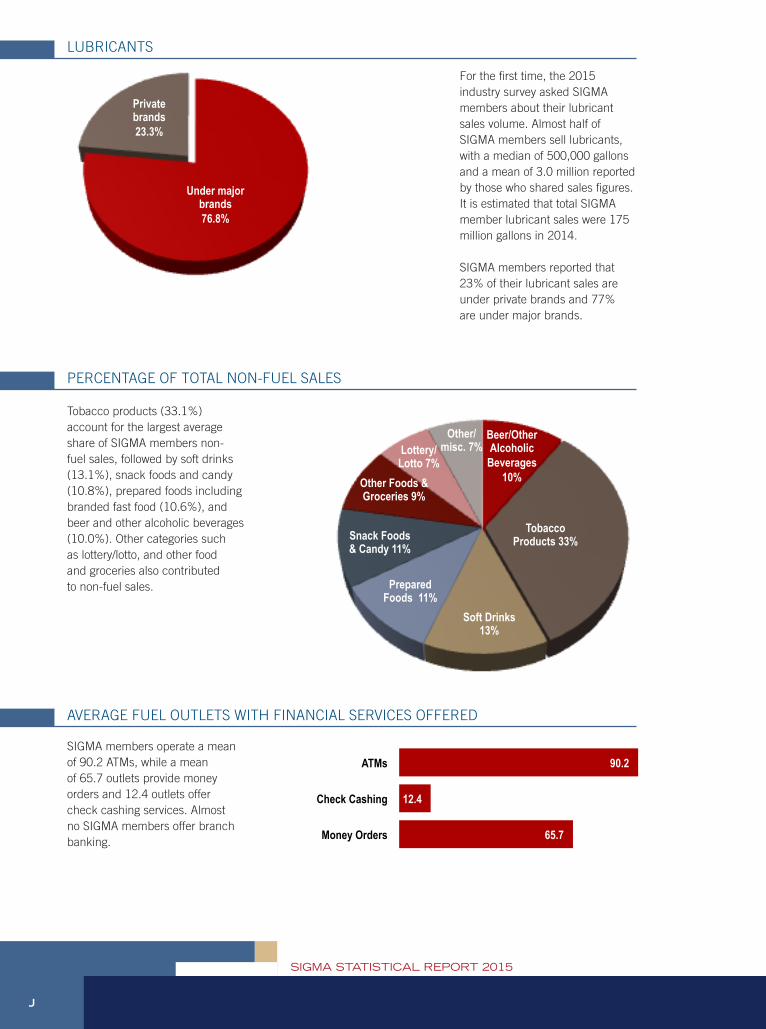

For the first time, the 2015 industry survey asked SIGMA members about their lubricant sales volume. Almost half of SIGMA members sell lubricants, with a median of 500,000 gallons and a mean of 3.0 million reported by those who shared sales figures. It is estimated that total SIGMA member lubricant sales were 175 million gallons in 2014.

SIGMA members reported that 23% of their lubricant sales are under private brands and 77% are under major brands.

PERCENTAGE OF TOTAL NON-FUEL SALES

Tobacco products (33.1%) account for the largest average share of SIGMA members non-fuel sales, followed by soft drinks (13.1%), snack foods and candy (10.8%), prepared foods including branded fast food (10.6%), and beer and other alcoholic beverages (10.0%). Other categories such as lottery/lotto, and other food and groceries also contributed to non-fuel sales.

AVERAGE FUEL OUTLETS WITH FINANCIAL SERVICES OFFERED

SIGMA members operate a mean of 90.2 ATMs, while a mean of 65.7 outlets provide money orders and 12.4 outlets offer check cashing services. Almost no SIGMA members offer branch banking.

65.7

12.4

90.2

Money Orders

Check Cashing

ATMs

Beer/Other Alcoholic

Beverages 10%

Tobacco Products 33%

Soft Drinks 13%

Prepared Foods 11%

Snack Foods & Candy 11%

Other Foods & Groceries 9%

Lottery/ Lotto 7%

Other/ misc. 7%

K

SIGMA STATISTICAL REPORT 2015

TOTAL ENVIRONMENTAL COSTS

TOTAL ENVIRONMENTAL COSTS

MEAN Q1 MEDIAN Q3

Company’s total capital expenditure for environmentally-related equipment:

$214,000 $0 $23,000 $250,000

Total spent on tank testing, soil analysis, remediation, and other non-capital environmental compliance:

$1,110,000 $2,000 $50,000 $200,000

Net cost of environmental insurance and state tank trust fund:

$179,000 $5,000 $45,000 $160,000

Estimated internal costs of complying with environmental regulations:

$2,000,000 $5,000 $50,000 $120,000

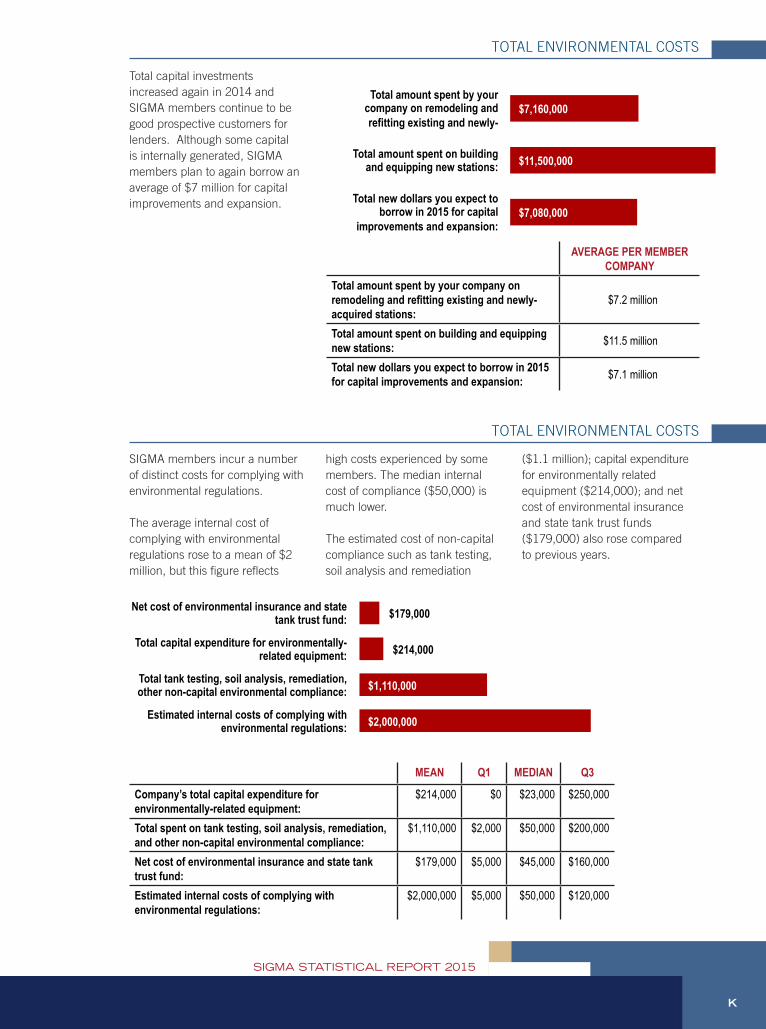

SIGMA members incur a number of distinct costs for complying with environmental regulations.

The average internal cost of complying with environmental regulations rose to a mean of $2 million, but this figure reflects

high costs experienced by some members. The median internal cost of compliance ($50,000) is much lower.

The estimated cost of non-capital compliance such as tank testing, soil analysis and remediation

($1.1 million); capital expenditure for environmentally related equipment ($214,000); and net cost of environmental insurance and state tank trust funds ($179,000) also rose compared to previous years.

AVERAGE PER MEMBER COMPANY

Total amount spent by your company on remodeling and refitting existing and newly-acquired stations:

$7.2 million

Total amount spent on building and equipping new stations: $11.5 million

Total new dollars you expect to borrow in 2015 for capital improvements and expansion: $7.1 million

Total capital investments increased again in 2014 and SIGMA members continue to be good prospective customers for lenders. Although some capital is internally generated, SIGMA members plan to again borrow an average of $7 million for capital improvements and expansion.

$7,080,000

$11,500,000

$7,160,000

Total new dollars you expect to borrow in 2015 for capital

improvements and expansion:

Total amount spent on building and equipping new stations:

Total amount spent by your company on remodeling and refitting existing and newly-

$2,000,000

$1,110,000

$214,000

$179,000

Estimated internal costs of complying with environmental regulations:

Total tank testing, soil analysis, remediation, other non-capital environmental compliance:

Total capital expenditure for environmentally-related equipment:

Net cost of environmental insurance and state tank trust fund:

L

SIGMA STATISTICAL REPORT 2015

SIGMA is the leading national trade association representing independent chain retailers and marketers of motor fuel, both branded and unbranded.

Founded in 1958 as the Society of Independent Gasoline Marketers of America (SIGMA), SIGMA has become a fixture in the motor fuel marketing industry. After over fifty years of leadership, SIGMA is the national trade association representing the most successful, progressive, and innovative independent fuel marketers and chain retailers in the United States and Canada. From the outset, the association has served to further the interests of this independent segment of the industry while providing information and services to members.

SIGMA’s benefits to member companies include a wide variety of publications and timely mailings, as well as legal advice. The association holds meetings

throughout the year to allow marketers and fuel suppliers to meet one-on-one and to give members a chance to participate in informative educational sessions. Leadership of the organization is provided by volunteers from SIGMA’s member companies, giving the association the advantage of advice from some of the most well-respected entrepreneurs in the nation.

SIGMA’s policies and operating procedures are determined by its members through the Board of Directors and volunteer committees. Regular membership in SIGMA is available to companies involved in motor fuel retailing or wholesaling that are not owned by a refiner. Associate membership is open to other companies directly related to the manufacture or sale of motor fuels.

In addition, Associate Membership is available to companies that offer financial services, fuel transport

services, and fleet card services. SIGMA member companies have long been recognized, both within and outside the industry, as the most aggressive, innovative, and price-competitive segment of petroleum marketers.

From its headquarters in suburban Washington, D.C., the association engages in the legislative process in Congress and the regulatory process in the executive branch, including independent agencies of the federal government. Throughout the year, SIGMA plays an important role in informing, explaining, and interpreting laws and rules to its members. The association also offers comments and input on regulations that affect independent marketers. This serves the dual purpose of ensuring that lawmakers and regulators have valid data on which to base their decisions, while guaranteeing that the perspectives and opinions of independent marketers are heard.

3930 Pender Drive, Suite 340Fairfax, VA 22030Phone: 703-709-7000Fax: 703-709-7007www.sigma.org

CONCLUSION