2015 michigan economic competitiveness benchmarking report

TRANSCRIPT

2015 Economic Competitiveness Benchmarking Report:

Data Supporting the Michigan Turnaround PlanNovember 2015

About Business Leaders for MichiganBusiness Leaders for Michigan, the state’s business roundtable, is dedicated to making Michigan a “Top Ten” state for jobs, personalincome and a healthy economy. The organization is composed exclusively of the chairpersons, chief executive officers, or most seniorexecutives of Michigan’s largest companies and universities. Our members drive over 32% of the state’s economy, provide nearly375,000 direct jobs in Michigan, generate over $1 trillion in annual revenue and serve nearly one half of all Michigan public universitystudents. Find out more at www.businessleadersformichigan.com

Copyright © 2015 Business Leaders for Michigan. All Rights Reserved.

1 Introduction

2 Methodology

4 Key Findings

7 Output Metrics

18 Input Metrics

66 Michigan’s Regional Performance

74 Business Leaders for Michigan Board of Directors

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

1

Introduction

This report provides a fact-based assessment of Michigan’s economic competitiveness

relative to other states. Michigan’s performance is compared on key output (e.g.,

employment, GDP) and input (e.g., labor cost) metrics. A set of “traditional,” “new economy,”

and “Top Ten” benchmark states were used to provide multiple reference points to evaluate

Michigan’s performance.

While the intent of this report is not to make recommendations, general conclusions are

outlined. These conclusions are used by Business Leaders for Michigan to help develop

strategies for making Michigan a “Top Ten” state for jobs, personal income, and a healthy

economy.

Why is it important for Michigan to be a “Top Ten” state? Simply put, it would

result in more jobs, better incomes and a stronger economy. If Michigan were performing

like a “Top Ten” state today, there would be:

120,000more Michigan people working

$11,000more income per person

$13,000more GDP per person

Research for the 2015 Economic Competitiveness Benchmarking Report was

conducted by Anderson Economic Group, a research and consulting firm with

expertise in economics, public policy, finance, and industry analysis.

Methodology

UNEMPLOYMENT RATE

RANK

Leve

l

467.3%

5.1%

th

Tren

dTo

p 1

0 A

vg.

How To Read This Report

Across the globe, analysts use a series of commonmeasures to determine the economic strength ofcountries, states, and regions. The measures aredivided into two categories: outputs and inputs.

•Output indicators like jobs, income,population and GDP show us the impact of policydecisions. They are the end result of ongoingeconomic development and policy changes.

• Input indicators measure the factorsbusinesses look at when deciding where tolocate. In this report, Michigan’s input metricsare divided into two categories: costindicators and value indicators. Whendeciding whether nor not to locate or expandin a region, job providers evaluate the costs(e.g., taxes, fees, utilities) of doing business ina region relative to the value (e.g., talent,infrastructure) it provides. Ultimately, areasthat offer more value for equal or lower costencourage business growth and attraction

which leads to more jobs, higher incomes and astronger economy. They include factors like thecost of doing business, the incentives available, thepool of talent, and available infrastructure tosupport company operations. When these indicatorsare positive, they greatly influence site selectiondecisions and, ultimately, lead to stronger outputs.

The correlation between the inputs and the outputsis important to keep in mind when reading thisreport. Ultimately, the inputs are the factors overwhich state leaders have the greatest amount ofcontrol. This year’s benchmarking results can offercontinuing direction as we collectively evaluate thenext crucial decisions for our economy.

With all this in mind, readers of this benchmarkingreport can see at a glance what progress has beenmade, where Michigan ranks relative to the rest ofthe U.S., and which direction we’re moving. Thekey below shows you how.

Michigan’srank amongthe 50 states, with #1 being topperformance and#50 being worstperformance inthe category.

Michigan’s level ofperformance for themost recent year

One-year trend

Average performanceof the “Top Ten” states

Positive Negative Holding

Business Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

2

3

STATE

North DakotaNew YorkTexasMassachusettsWyomingWashingtonAlaskaNebraskaPennsylvaniaIowa

OVERALRANK

123456789

10

EMPLOYMENTGROWTH2

1248

10145

16117

EMPLOYMENTLEVEL2

117312

2030374

116

POPULATIONGROWTH

11403

35101215273934

POPULATIONLEVEL

4742

14501348376

30

PER CAPITAINCOMEGROWTH

196172

244

151814

PER CAPITAINCOMELEVEL

64

2427

129

191725

PER CAPITAGDP

LEVEL

23

116591

152321

PER CAPITAGDP

GROWTH

143

1459

156

1812

Top Ten States

WA

OR

CA

NV

UT

AZNM

CO

ID

MT

KS

OK

MN

MO

AR

LA

ILIN

OH

KY

TN

MS AL GA

FL

SC

NC

VAWV

ME

NH

NJ

DE

MDDC

CTRI

MAWI

MI

HI

VT

Traditional Benchmarks

New Economy Benchmarks

Peer States

WA

OR

NV

UT

AZNM

WY

ID

MT ND

SD

NE

KS

OK

MN

IA

MO

AR

LA

KY

MS

FL

SC

WV

PA

NY

ME

NH

NJ

DE

MDDC

CTRI

MAWI

MI

AK

HI

VT

ND

SD

NEIA

TX

AK

NY

CA COIL

OH

TN

AL GA

NC

TX

IN

VA

WY

PA

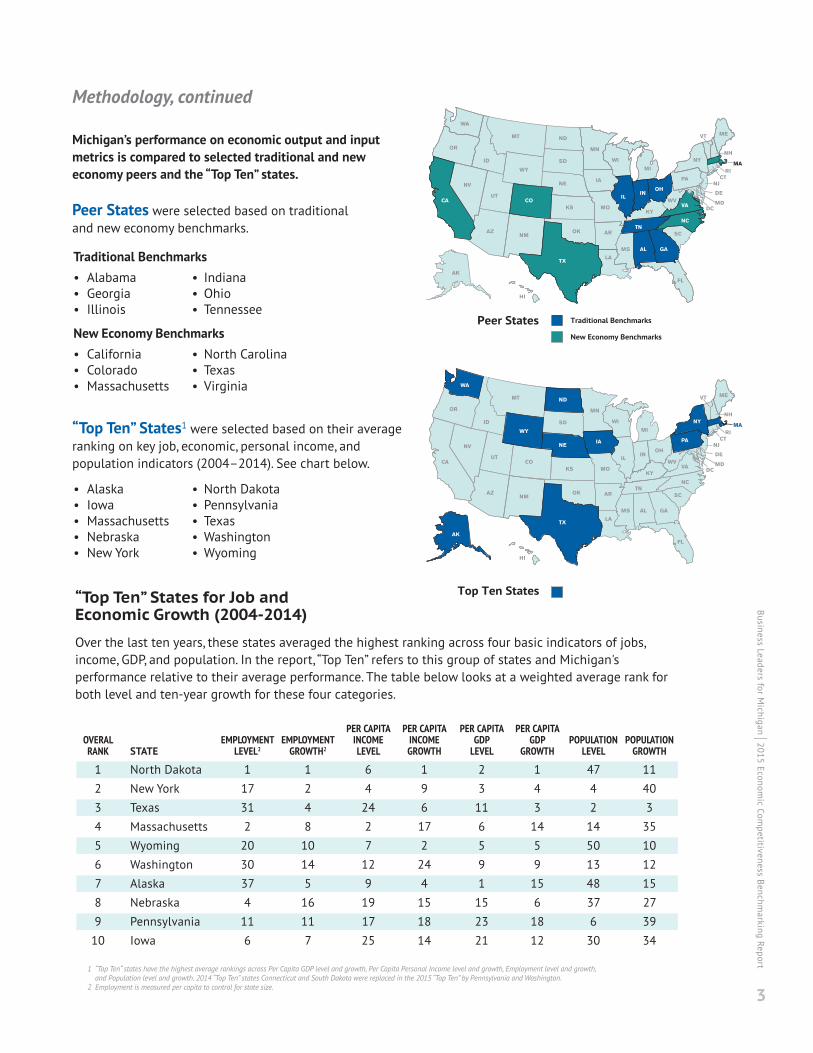

Methodology, continued

Michigan’s performance on economic output and inputmetrics is compared to selected traditional and neweconomy peers and the “Top Ten” states.

Peer States were selected based on traditionaland new economy benchmarks.

Traditional Benchmarks• Alabama • Indiana• Georgia • Ohio• Illinois • Tennessee

New Economy Benchmarks• California • North Carolina• Colorado • Texas• Massachusetts • Virginia

“Top Ten” States1 were selected based on their averageranking on key job, economic, personal income, andpopulation indicators (2004–2014). See chart below.

• Alaska • North Dakota• Iowa • Pennsylvania• Massachusetts • Texas• Nebraska • Washington• New York • Wyoming

“Top Ten” States for Job and Economic Growth (2004-2014)

Over the last ten years, these states averaged the highest ranking across four basic indicators of jobs,income, GDP, and population. In the report, “Top Ten” refers to this group of states and Michigan'sperformance relative to their average performance. The table below looks at a weighted average rank forboth level and ten-year growth for these four categories.

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

1 “Top Ten“ states have the highest average rankings across Per Capita GDP level and growth, Per Capita Personal Income level and growth, Employment level and growth,and Population level and growth. 2014 “Top Ten” states Connecticut and South Dakota were replaced in the 2015 “Top Ten” by Pennsylvania and Washington.

2 Employment is measured per capita to control for state size.

Business Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

4

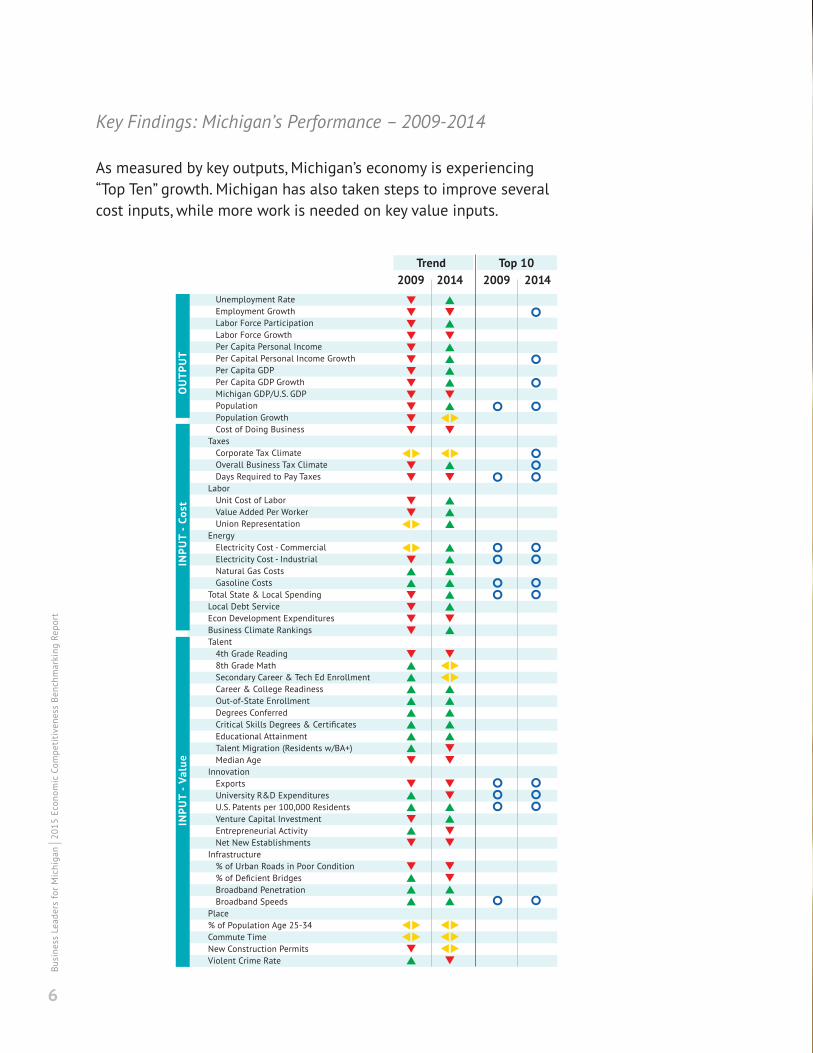

Key Findings

OutputIn 2009, Michigan was headed in the wrongdirection across 11 key output indicators ofeconomic performance.

In 2014, Michigan was headed in the rightdirection on most measures and ranked:

• 18th for employment growth• 10th for per capita personal income growth, and • 3rd for per capita gross domestic product growth.

Despite the fact that Michigan is growingfaster than most states, absolute levels foremployment, per capita income and per capitaGDP remain average or below.

While Michigan remains one of the 10 largeststates, population growth was slow, yielding aranking of only 41st nationwide.

2009

2014

0 2 4 6 8 10 12

Improving

Holding

11Declining

7Improving

1Holding

3 Declining

46thinUnemployment

Rate

36thinPer Capita

Personal Income

34thinGDP Per Capita

Michigan’s absolute levels:

5

Input - CostIn 2009, Michigan was headed in the wrongdirection on 10 of 15 indicators relative to thecost of being located in a given state.

In 2014, Michigan was headed in the rightdirection on 11 of 15 measures, and ranked:

• 10th for corporate tax climate, and• 13th for overall tax climate.

However this year, Michigan is trending in thewrong direction for both economicdevelopment expenditures and state unfundedpension liabilities, and ranks 28th for bothmeasures.

Input - ValueUnlike outputs and cost inputs, Michigan wasdoing better in 2009 on value inputs,improving in 15 of 24 areas.

In 2014, Michigan’s performance was flat orheaded in the wrong direction on 15measures, and ranked:

• 38th for 4th grade reading proficiency• 39th for urban road conditions, and • 41st for enrollment in high school careerand technical education.

While Michigan remains a Top Ten state forinnovation measures such as universityresearch and development and exports, recentperformance in those areas continues adownward trend.

Michigan ranked in the bottom five states forthe percent of population age 25–34.

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

2009

2014

0 2 4 6 8 10 12

2 Improving

3 Holding

10Declining

11Improving

1Holding

3 Declining

2009

2014

0 5 10 15

15 Improving

2 Holding

7Declining

9Improving

5Holding

10 Declining

Business Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

6

Unemployment Rate Employment Growth Labor Force Participation Labor Force Growth Per Capita Personal Income Per Capital Personal Income Growth Per Capita GDP Per Capita GDP Growth Michigan GDP/U.S. GDP Population Population Growth Cost of Doing Business

TaxesCorporate Tax ClimateOverall Business Tax ClimateDays Required to Pay Taxes

LaborUnit Cost of LaborValue Added Per WorkerUnion Representation

EnergyElectricity Cost - CommercialElectricity Cost - IndustrialNatural Gas CostsGasoline Costs

Total State & Local Spending Local Debt Service Econ Development Expenditures Business Climate Rankings Talent

4th Grade Reading8th Grade MathSecondary Career & Tech Ed EnrollmentCareer & College ReadinessOut-of-State Enrollment Degrees Conferred

Educational AttainmentTalent Migration (Residents w/BA+)Median Age

InnovationExportsUniversity R&D ExpendituresU.S. Patents per 100,000 ResidentsVenture Capital InvestmentEntrepreneurial ActivityNet New Establishments

Infrastructure% of Urban Roads in Poor Condition

Broadband PenetrationBroadband Speeds

Place% of Population Age 25-34Commute TimeNew Construction PermitsViolent Crime Rate

2009Trend Top 10

2014 2009 2014

OU

TPU

TIN

PUT

- Co

stIN

PUT

- Va

lue

Key Findings: Michigan’s Performance – 2009-2014

As measured by key outputs, Michigan’s economy is experiencing“Top Ten” growth. Michigan has also taken steps to improve severalcost inputs, while more work is needed on key value inputs.

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

7

Output Metrics

The end result of ongoing economic development and policy changes, outputmetrics help measure the impact of economic choices. Output metrics focus onareas indicative of strong economic performance: Employment, Per Capita GDP,Population and Per Capita Income.

Michigan continues to grow jobs, incomes and its economy faster than mostother states and, in fact, ranks in the top ten for personal income and GDPgrowth. But other states are not standing still. As impressive as Michigan’sgrowth has been, it must accelerate even faster for the state to reach the“Top Ten” in absolute terms.

output

18thinEmployment

Growth

46thin Unemployment

Rate

34thin Per Capita GDP

36thin Per Capita

Personal Income

in

10thin Per Capita

Personal IncomeGrowth

3rdPer Capita GDP Growth

Michigan continues to grow faster than average rate of “Top Ten” states

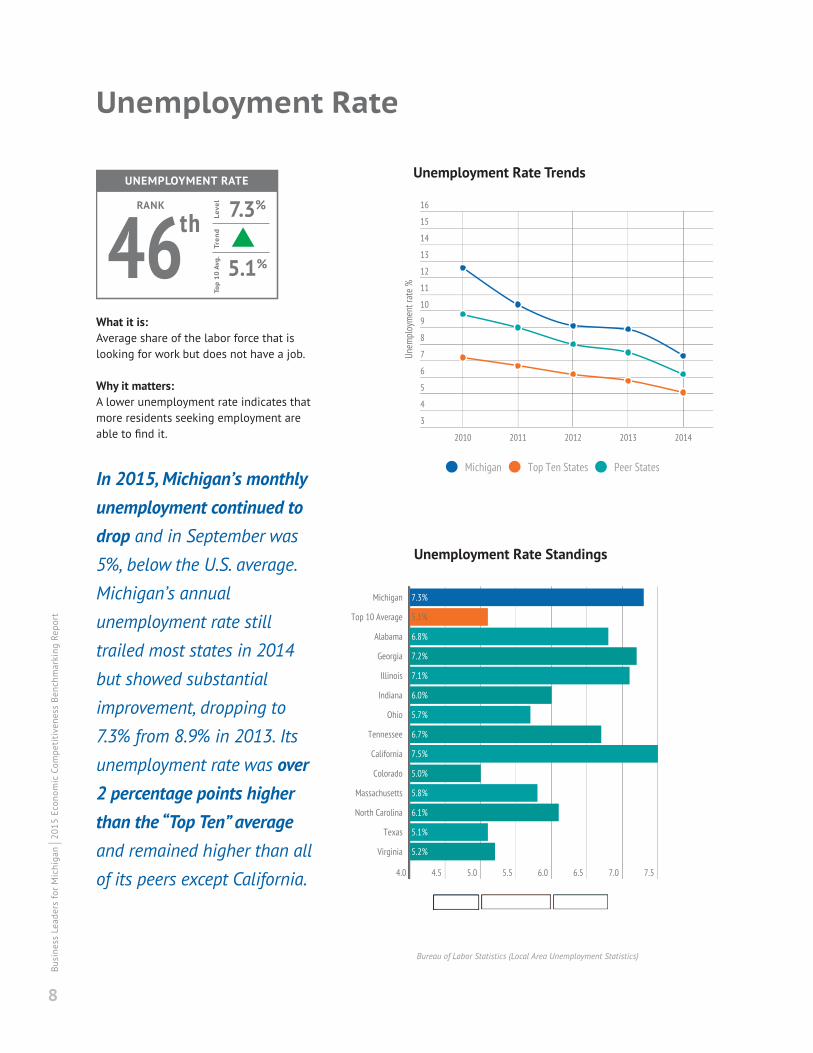

What it is:Average share of the labor force that islooking for work but does not have a job.

Why it matters:A lower unemployment rate indicates thatmore residents seeking employment areable to find it.

In 2015, Michigan’s monthlyunemployment continued todrop and in September was5%, below the U.S. average.Michigan’s annualunemployment rate stilltrailed most states in 2014but showed substantialimprovement, dropping to7.3% from 8.9% in 2013. Itsunemployment rate was over2 percentage points higherthan the “Top Ten” averageand remained higher than allof its peers except California.

Unemployment Rate Standings

Unemployment Rate

Bureau of Labor Statistics (Local Area Unemployment Statistics)

Business Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

8

UNEMPLOYMENT RATE

RANKLe

vel

467.3%

5.1%

thTr

end

Top

10

Avg

.

Unemployment Rate Trends

9

output

Employment Growth Trends

What it is:Average number of residents with aprivate sector job.

Why it matters:Higher levels of private employmentindicate both economic strength andprosperity among the state’s residents.

Michigan’s private sectoremployment growth wasslower, with the stateranking 18th from 2013 to2014. Michigan’s private

sector employment growth

rate was on par with the

“Top Ten” average, but came

behind six of its peers: Texas,

California, Colorado, North

Carolina, Tennessee and

Georgia.

Employment Standings

Bureau of Labor Statistics (Quarterly Census of Employment and Wages)

EMPLOYMENT GROWTH

RANKLe

vel

182.3%

2.3%

thTr

end

Top

10 A

vg.

Employment Growth

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

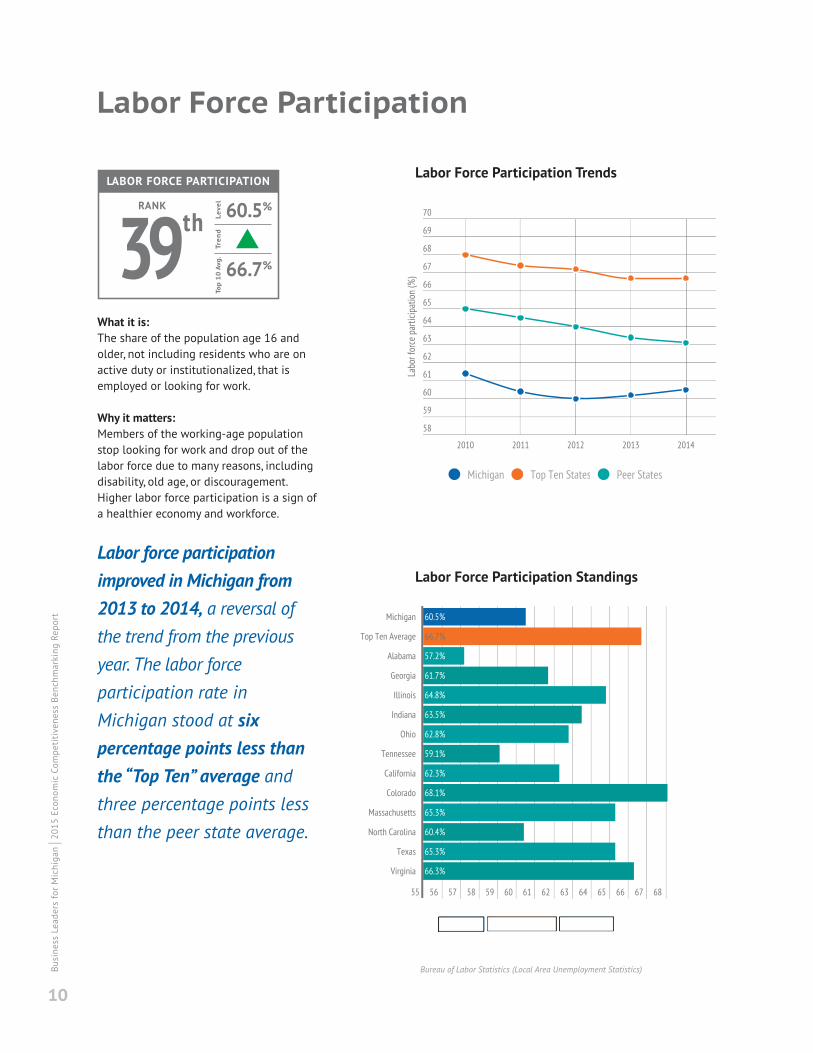

Labor Force Participation

Business Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

10

Labor Force Participation Trends

What it is:The share of the population age 16 andolder, not including residents who are onactive duty or institutionalized, that isemployed or looking for work.

Why it matters:Members of the working-age populationstop looking for work and drop out of thelabor force due to many reasons, includingdisability, old age, or discouragement.Higher labor force participation is a sign ofa healthier economy and workforce.

Labor force participationimproved in Michigan from2013 to 2014, a reversal ofthe trend from the previousyear. The labor forceparticipation rate inMichigan stood at sixpercentage points less thanthe “Top Ten” average andthree percentage points lessthan the peer state average.

Labor Force Participation Standings

Bureau of Labor Statistics (Local Area Unemployment Statistics)

LABOR FORCE PARTICIPATION

RANKLe

vel

3960.5%

66.7%

Tren

dTo

p 1

0 A

vg.

th

What it is:Change in the number of residentsemployed or looking for work.

Why it matters:Labor force includes the entire pool ofresidents that are interested in working,showing less volatility than employmentthroughout the business cycle. A growinglabor force shows a growing pool ofworkers for businesses.

The Michigan labor forcegrew more slowly from 2013to 2014 and now stands at

4.7 million. The increase in

Michigan’s labor force from

2013 to 2014 outpaced the

average increase for peer

states but was below the

average increase for the

“Top Ten” states.

Labor Force Standings

Labor Force Growth

Bureau of Labor Statistics (Local Area Unemployment Statistics)

11

output

LABOR FORCE GROWTH

RANKLe

vel

250.4%

0.7%

thTr

end

Top

10 A

vg.

Labor Force Growth Trends

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

Per Capita Personal Income

Business Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

12

PER CAPITA PERSONAL INCOME GROWTH

RANK

Level

102.2%

1.4%

th

Trend

Top

10 A

vg.

Per Capita Personal Income Trends

What it is:Personal income (2014 dollars) divided bypopulation. Personal income includessalaries, wages, and bonuses fromemployment; dividends and interest frominvestments; rental income; pensions, etc.

Why it matters:This is an indicator of prosperity andaverage standard of living in a state.

Michigan’s per capitaincome growth from 2013 to2014 was the 10th fastest inthe nation—nearly twice asfast as the “Top Ten” averageand faster than all of itspeers save Colorado.However, its per capitaincome level was belowmore than half of its peers.

Per Capita Personal Income Standings

Bureau of Economic Analysis (personal income summary), Bureau of Labor Statistics (CPI Inflation Calculator)

PER CAPITA PERSONAL INCOME

RANKLe

vel

36$40,556

$51,300

thTr

end

Top

10

Avg

.

What it is:Total amount of goods and servicesproduced by private industries in thestate, adjusted for inflation and changesin relative prices, divided by population.

Why it matters:Higher private sector GDP per capita isone of the primary measures of a region’seconomic strength.

Michigan’s per capita GDP in2013 was ranked in thebottom half of states.However, growth in Michigan’sper capita GDP between 2013and 2014 ranked 3rd in thenation and was over fourtimes faster than the “TopTen” average. Michigan’s percapita GDP remained belowmost of its peers but itsgrowth over the past yearwas faster than most.

Per Capita GDP Standings

Per Capita GDP

Bureau of Economic Analysis (personal income summary),Bureau of Labor Statistics (CPI Inflation Calculator)

13

output

Per Capita GDP TrendsPER CAPITA GDP

RANK

Leve

l

34$37,593

$51,029

th

Tren

dTo

p 10

Avg

.

PER CAPITA GDP GROWTH

RANK

Leve

l

33.20%

0.73%

rd

Tren

dTo

p 1

0 A

vg.

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

Business Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

14

What it is:Total amount of goods and servicesproduced in the state, as a share of allgoods and services produced in theUnited States.

Why it matters:A high share of United States GDP meansthat much of the country's production isoccurring in that state, and can result inhigher incomes for state workers.

Since 2009, Michigan’s

share of U.S. GDP has

remained relatively flat at

2.6% after falling from a

high of 3% in 2005.

Michigan GDP/U.S. GDP Standings

Michigan GDP/U.S. GDP

Bureau of Economic Analysis

Michigan GDP/U.S. GDP TrendsPER CAPITA GDP

RANKLe

vel

34$37,593

$51,029

thTr

end

Top

10 A

vg.

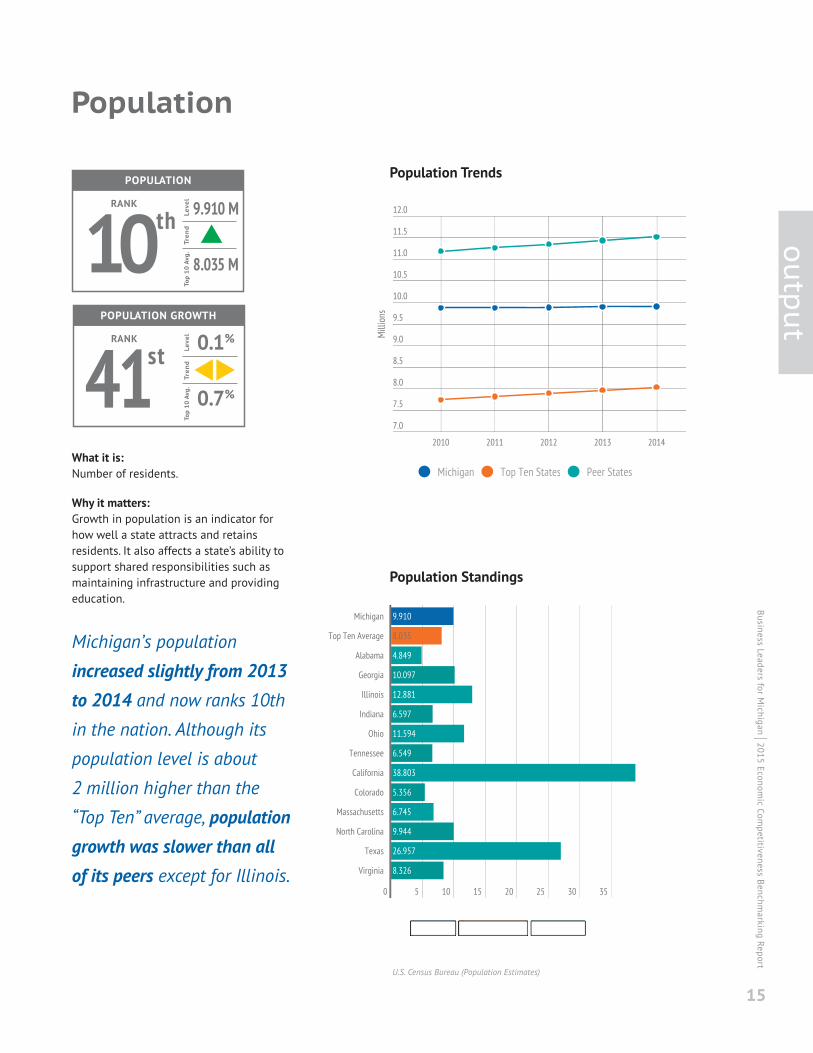

Population

POPULATION GROWTH

RANK

Leve

l

410.1%

0.7%

st

Tren

dTo

p 10

Avg

.

Population Trends

What it is:Number of residents.

Why it matters:Growth in population is an indicator forhow well a state attracts and retainsresidents. It also affects a state’s ability tosupport shared responsibilities such asmaintaining infrastructure and providingeducation.

Michigan’s population

increased slightly from 2013to 2014 and now ranks 10thin the nation. Although its

population level is about

2 million higher than the

“Top Ten” average, populationgrowth was slower than allof its peers except for Illinois.

Population Standings

U.S. Census Bureau (Population Estimates)

POPULATION

RANK

Level

10 9.910 M

8.035 M

th

Trend

Top

10 A

vg.

15

output

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

Output Conclusions

Despite Michigan’s outstanding post-recession growth,significant gaps remain between Michigan and “Top Ten” statesin job, income, and GDP levels.

Why is it important to be “Top Ten?”

Simply put, it would result in more jobs, betterincomes and a stronger economy. If Michigan wasperforming like a “Top Ten” state today, there would be:

More Jobs: 120,000 more Michigan people working

Higher incomes: $11,000 more income per person

Stronger economy: $13,000 more GDP per person

Business Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

16

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

17

output

Business Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

18

Input Metrics

In this report, Michigan’s input metrics are divided into two categories: cost indicatorsand value indicators. When deciding whether nor not to locate or expand in a region,job providers evaluate the costs (e.g., taxes, fees, utilities) of doing business in aregion relative to the value (e.g., talent, infrastructure) it provides. Ultimately, areasthat offer more value for equal or lower cost encourage business growth andattraction which leads to more jobs, higher incomes, and a stronger economy.

Cost indicators represent a region’s basic level of competitiveness. States that are notcompetitive on most cost factors don’t often get a second glance from job providerslooking to locate or expand their business.

Value indicators are what separate regions from one another when other factors areequal. When comparing two or more regions with similar cost structures, the regionwith better infrastructure, available talent, and innovation capabilities will often win.

When the relationship between cost and value indicators is positive, it can greatlyinfluence site selection decisions and, ultimately, lead to stronger outputs.

input

Cost Value

Moody's North American Business Cost Review (2012 data)

Cost of Doing Business

19

input

cost

Cost of Doing Business Trends

What it is:Index that compares the state’s averagebusiness costs (labor, energy, and state &local tax burden) with the nationalaverage (U.S. = 100).

Why it matters:Lower business costs make it easier forexisting businesses to succeed and makethe state more attractive to newbusinesses.

On average, businesses paid

more to operate in Michigan

than in “Top Ten” states and

peer states in 2012.

Michigan had the 12thhighest cost of doingbusiness in the nation. Theonly peer states whose costs

of doing business exceeded

Michigan’s were California

and Massachusetts.

Index: Cost of Doing Business Standings

COST OF DOING BUSINESS

RANKLe

vel 105

98

Tren

dTo

p 10

Avg

.39th

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

Corporate Tax Climate

Business Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

20

Corporate Tax Climate Trends

What it is:Index that compares corporate tax burdenbased on corporate income tax and grossreceipts tax (10 = most favorable, 0 = leastfavorable).

Why it matters:A lower corporate tax burden can improvea state’s attractiveness to both new andexisting businesses.

Michigan was among the“Top Ten” states in terms ofcorporate tax climate in2014. Michigan’s corporate

tax climate rank exceeded all

of the “Top Ten” states except

Wyoming and tied for best

among peer states with

Virginia and Georgia.

Index: Corporate Tax Climate Standings

Tax Foundation (2014 State Business Tax Climate Index)

CORPORATE TAX CLIMATE

RANKLe

vel

105.8

5.3

thTr

end

Top

10

Avg

.

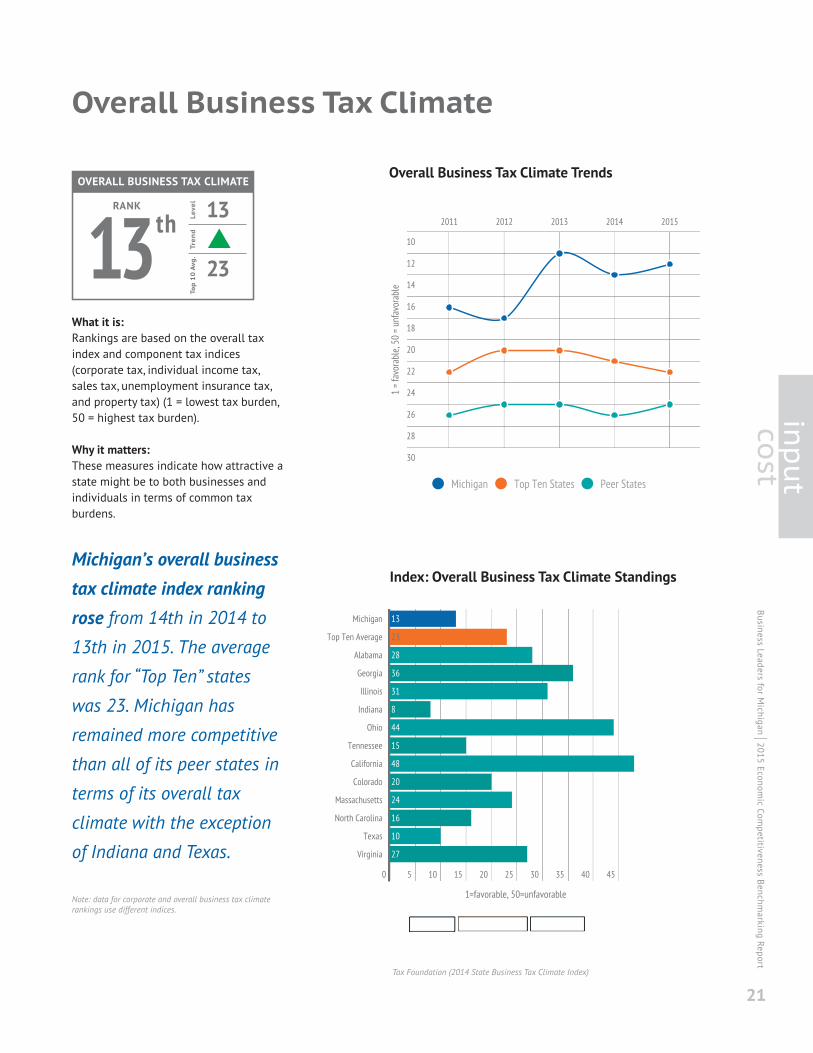

What it is:Rankings are based on the overall taxindex and component tax indices(corporate tax, individual income tax,sales tax, unemployment insurance tax,and property tax) (1 = lowest tax burden,50 = highest tax burden).

Why it matters:These measures indicate how attractive astate might be to both businesses andindividuals in terms of common taxburdens.

Michigan’s overall businesstax climate index rankingrose from 14th in 2014 to13th in 2015. The average

rank for “Top Ten” states

was 23. Michigan has

remained more competitive

than all of its peer states in

terms of its overall tax

climate with the exception

of Indiana and Texas.

Note: data for corporate and overall business tax climaterankings use different indices.

Index: Overall Business Tax Climate Standings

Overall Business Tax Climate

Tax Foundation (2014 State Business Tax Climate Index)

21

input

cost

OVERALL BUSINESS TAX CLIMATE

RANKLe

vel

1313

23

thTr

end

Top

10

Avg

.

Overall Business Tax Climate Trends

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

Business Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

22

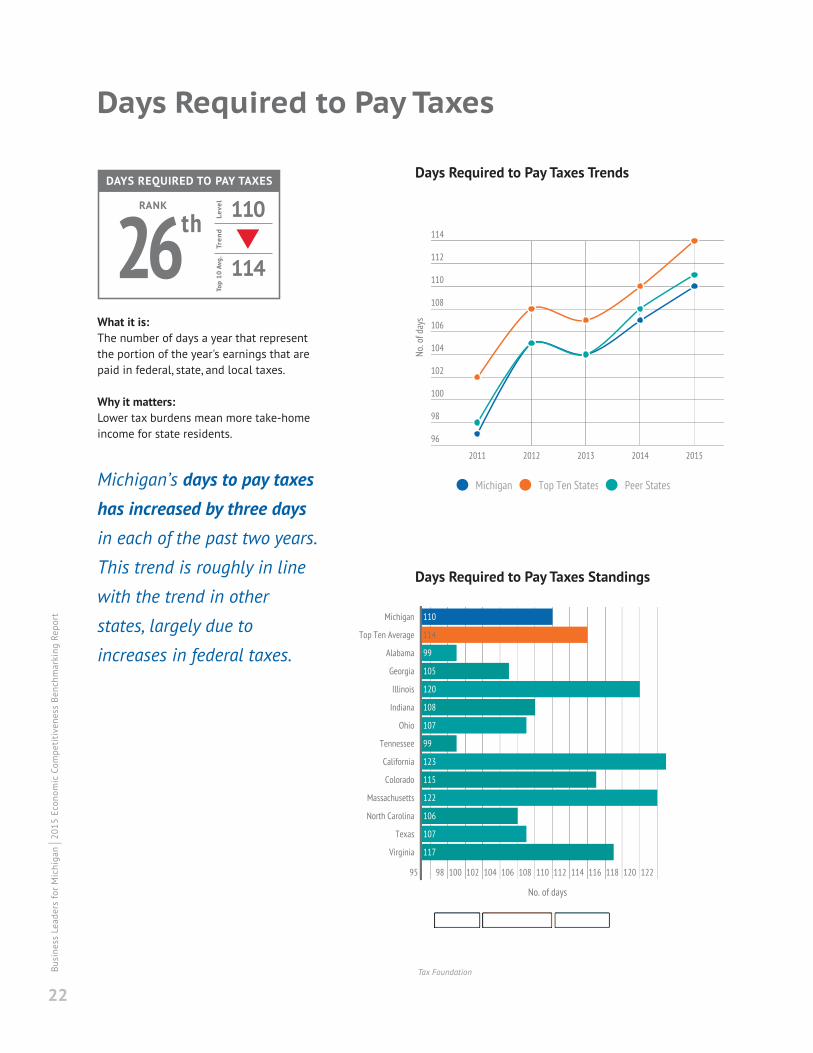

Days Required to Pay Taxes

Days Required to Pay Taxes Trends

What it is:The number of days a year that representthe portion of the year's earnings that arepaid in federal, state, and local taxes.

Why it matters:Lower tax burdens mean more take-homeincome for state residents.

Michigan’s days to pay taxeshas increased by three daysin each of the past two years.

This trend is roughly in line

with the trend in other

states, largely due to

increases in federal taxes.

Days Required to Pay Taxes Standings

Tax Foundation

DAYS REQUIRED TO PAY TAXES

RANKLe

vel 110

114

Tren

dTo

p 10

Avg

.26th

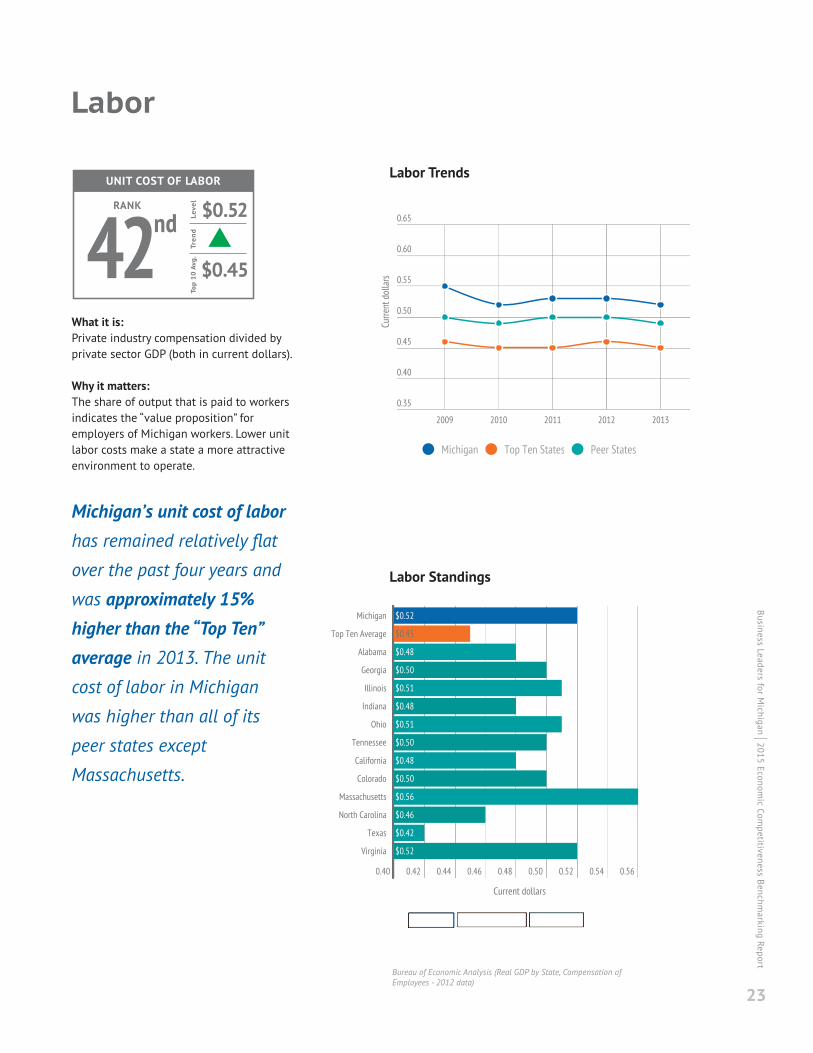

Labor

Labor Trends

What it is:Private industry compensation divided byprivate sector GDP (both in current dollars).

Why it matters:The share of output that is paid to workersindicates the “value proposition” foremployers of Michigan workers. Lower unitlabor costs make a state a more attractiveenvironment to operate.

Michigan’s unit cost of laborhas remained relatively flat

over the past four years and

was approximately 15%higher than the “Top Ten”average in 2013. The unitcost of labor in Michigan

was higher than all of its

peer states except

Massachusetts.

Labor Standings

Bureau of Economic Analysis (Real GDP by State, Compensation ofEmployees - 2012 data)

UNIT COST OF LABOR

RANKLe

vel

42$0.52

$0.45

ndTr

end

Top

10

Avg

.

23

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

What it is:Real Private Industry GDP divided byaverage annual non-farm employment.

Why it matters:This is a measure of the amount ofproduction per worker, which is animportant way to increase income andeconomic activity.

Value added per workerin Michigan was 15% lowerthan the “Top Ten” averagein 2014 and ranked below

all but four of its peer

states. However, the growthin worker productivity inMichigan from 2013 to

2014 exceeded that of overhalf of its peer states.

Value Added Per Worker Standings

Value Added Per Worker

Bureau of Economic Analysis (Real GDP by State), Bureau of Labor Statistics(State and Metro Area Employment, Hours, and Earnings)

VALUE ADDED PER WORKER

RANKLe

vel

24$89,130

$105,000

thTr

end

Top

10 A

vg.

Value Added Per Worker Trends

Business Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

24

25

input

cost

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

Union Representation

Union Representation Trends

What it is:Employees represented by a union (as apercent of those employed) (1 = best, 50 =worst).

Why it matters:An indicator of labor market bargainingpower, labor flexibility, and pro-businesssentiments in the state. For someemployers, lower union membership makesa state a more attractive place to operate.

Michigan had the 11th-highest share of workers thatare represented by a unionin 2014. Michigan’s

unionization rate was two

percentage points higher

than the “Top Ten” average.

Michigan’s union

membership and

representation rate remained

higher than all peer states

except California and Illinois.

Union Representation Standings

Bureau of Labor Statistics (Current Population Survey)

UNION REPRESENTATION

RANKLe

vel

3915.7%

13.9%

thTr

end

Top

10 A

vg.

Business Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

26

What it is:Price per kilowatt-hour (kwh) ofelectricity for commercial users (1 = best,50 = worst).

Why it matters:Maintaining competitive energy costscontributes to a state’s attractiveness tobusinesses.

Michigan’s electricity costsfor commercial customerswere even with the “TopTen” average in 2014. Thisrepresented a decline of0.2¢ relative to 2013 forMichigan. Electricity costsfor commercial customers inMichigan are higher thanthose in all peer statesexcept Massachusetts andCalifornia but only 2%above the national average.

Note: 2015 rates are based on monthly reported datathrough August.

Electricity Costs - Commercial Standings

Electricity Costs - Commercial

Energy Information Administration

ELECTRICITY COSTS: COMMERCIAL

RANKLe

vel

3310.3¢

11.0¢

rdTr

end

Top

10 A

vg.

Electricity Costs - Commercial Trends

27

input

cost

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

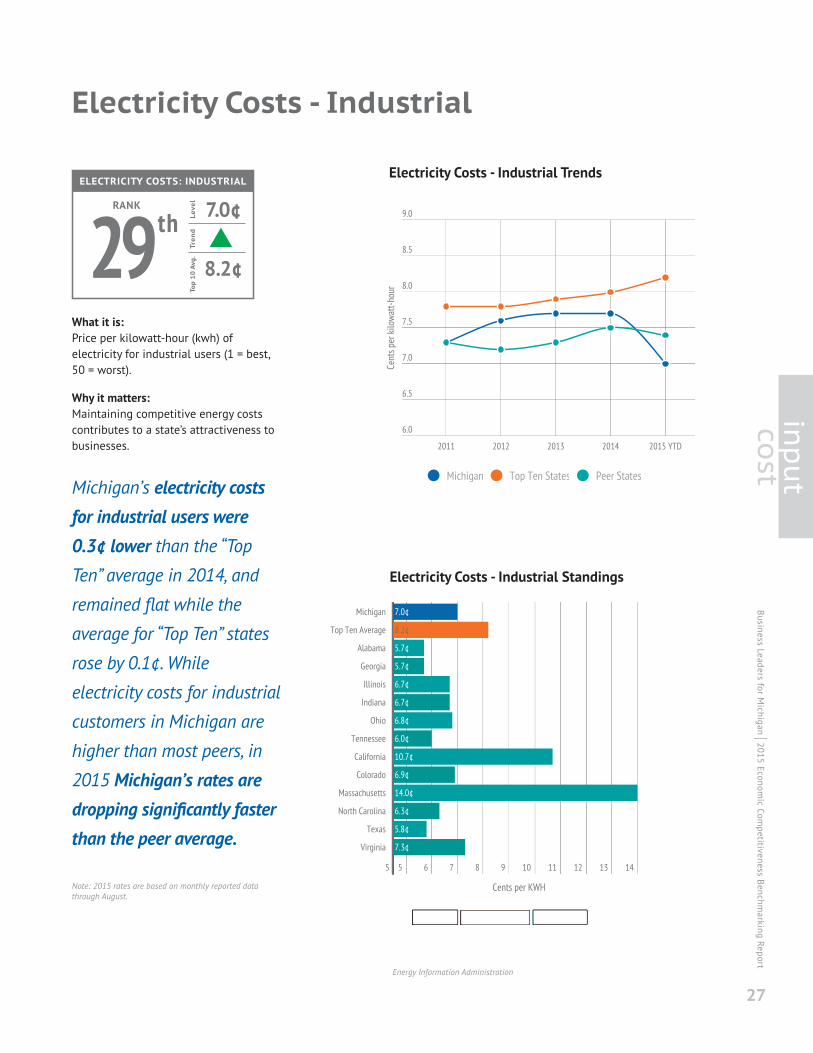

What it is:Price per kilowatt-hour (kwh) ofelectricity for industrial users (1 = best,50 = worst).

Why it matters:Maintaining competitive energy costscontributes to a state’s attractiveness tobusinesses.

Michigan’s electricity costsfor industrial users were0.3¢ lower than the “TopTen” average in 2014, and

remained flat while the

average for “Top Ten” states

rose by 0.1¢. While

electricity costs for industrial

customers in Michigan are

higher than most peers, in

2015 Michigan’s rates aredropping significantly fasterthan the peer average.

Note: 2015 rates are based on monthly reported datathrough August.

Electricity Costs - Industrial Standings

Electricity Costs - Industrial

Energy Information Administration

ELECTRICITY COSTS: INDUSTRIAL

RANKLe

vel

297.0¢

8.2¢

thTr

end

Top

10 A

vg.

Electricity Costs - Industrial Trends

Business Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

28

What it is:A weighted average of the price perthousand cubic feet of natural gas forIndustrial and Commercial users,weighted by the proportion ofconsumption from each sector.

Why it matters:Maintaining competitive energy costscontributes to a state’s attractiveness tobusinesses.

Michigan’s natural gasprices have been fallingevery year since 2008, but

are still higher than theaverage of the “Top Ten”

states and all of its peer

states, except for

Massachusetts and North

Carolina.

.

Natural Gas Costs Standings

Natural Gas Costs

U.S. Energy Information Administration

NATURAL GAS COSTS

RANKLe

vel

257.52¢

7.17¢

thTr

end

Top

10 A

vg.

Natural Gas Costs Trends

29

input

cost

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

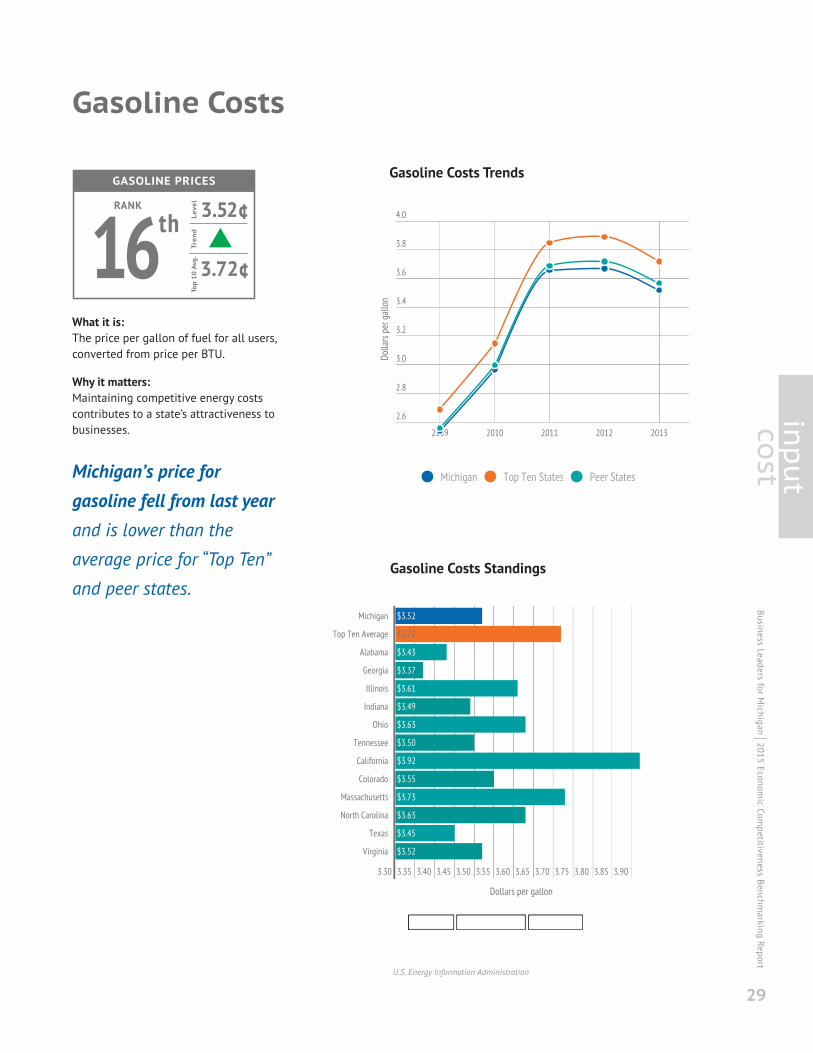

What it is:The price per gallon of fuel for all users,converted from price per BTU.

Why it matters:Maintaining competitive energy costscontributes to a state’s attractiveness tobusinesses.

Michigan’s price forgasoline fell from last yearand is lower than the

average price for “Top Ten”

and peer states.Gasoline Costs Standings

Gasoline Costs

U.S. Energy Information Administration

GASOLINE PRICES

RANKLe

vel

163.52¢

3.72¢

thTr

end

Top

10 A

vg.

Gasoline Costs Trends

Business Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

30

State Unfunded Pension Liabilities

Unfunded Pension Liability Trends

What it is:State government unfunded pension andother postemployment benefit liability(UAAL) divided by population.

Why it matters:This measure indicates the burden ofunfunded retiree benefits on taxpayers.Payments for high unfunded liabilities maycrowd out spending for competing needs,such as infrastructure and education.

Michigan’s unfunded pensionliability per capita was lessthan the “Top Ten” average

in 2013.

Unfunded Pension Liability Standings

Census of Governments, Pew Center on the States

STATE UNFUNDED PENSION LIABILITIES

RANKLevel

$3,311

$3,372

Trend

Top

10 A

vg.28th

31

input

cost

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

OPEB Liability Trends

What it is:State government unfunded otherpostemployment benefit liability (OPEB)divided by population.

Why it matters:This measure indicates the burden ofunfunded retiree benefits on taxpayers.Payments for high unfunded liabilitiesmay crowd out spending for competingneeds, such as infrastructure andeducation.

Michigan’s OPEB unfunded

liability per capita was less

than the “Top Ten” average

in 2012, but over $700 perperson higher than theaverage of peer states.

Note: “Top Ten” average for OPEB excludes Nebraska due todata availability. Cannot make inter-year comparisons forOPEB due to use of a different data source for 2012.

OPEB Liability Standings

State Unfunded Non-Pension (OPEB) Liabilities

Census of Governments, Pew Center on the States

STATE UNFUNDED OPEB LIABILITIES

RANKLevel

41$2,384

$2,473

stTrend

Top

10 A

vg.

Business Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

32

Local Debt Service

Local Debt Service Trends

What it is:Local government interest payments ondebt, divided by local government directexpenditures (both in current dollars).

Why it matters:Maintaining debt service at low levels is anindicator of fiscal sustainability.

Local government interest ondebt in Michigan exceededthe “Top Ten” average andranked in the bottom half ofthe nation. However, it wasrelatively constant from 2009

to 2012. Michigan is on par

with its peer average, and

only Illinois, Colorado, North

Carolina, and Texas had

higher local government

interest spending than

Michigan.

Note: This measure does not include debt service on principalsince the Census of Governments does not report a direct debtservice measure.

Local Debt Service Standings

Census of Governments (Annual Survey of State and Local Government Finances)

LOCAL DEBT SERVICE

RANKLe

vel

324.4%

3.9%

ndTr

end

Top

10 A

vg.

33

input

cost

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

Total State & Local Spending

Total State & Local Spending Trends

What it is:Total state and local governmentexpenditures (2014 dollars) divided bypopulation (1 = best, 50 = worst).

Why it matters:State and local government expendituresare used for important investments ineducation, infrastructure, and public safety.On the other hand, high expenditures cancrowd out private sector economic activityby redirecting tax revenue and stateworkers away from private use.

Michigan’s state and localspending was 28% lowerthan the “Top Ten” averagein 2012. Michigan was also4% below average among itspeer states. The growth inper capita governmentspending in Michigan was4th lowest in the nation overthe preceding decade andsecond behind only Georgiaamong its peer states.

Total State & Local Spending Standings

Census of Governments (Annual Survey of State and Local Government Finances)

TOTAL STATE & LOCAL SPENDING

RANKLe

vel

$9.30

$12.93

Tren

dTo

p 10

Avg

.19th

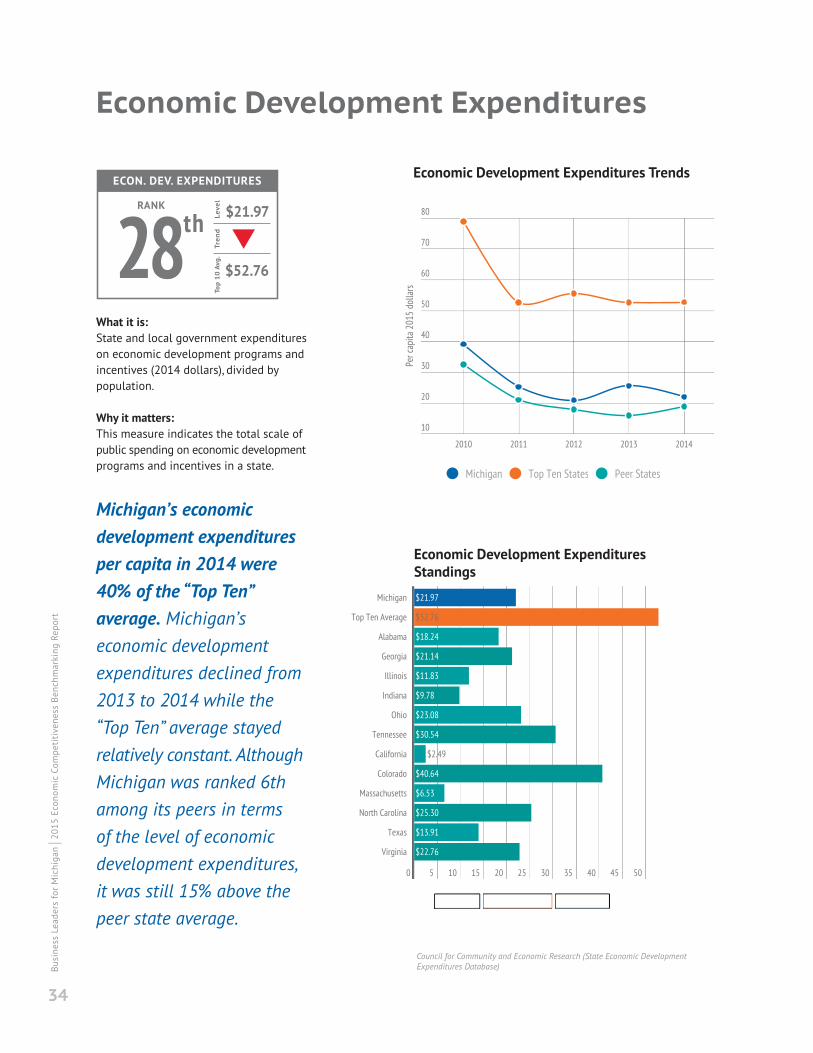

What it is:State and local government expenditureson economic development programs andincentives (2014 dollars), divided bypopulation.

Why it matters:This measure indicates the total scale ofpublic spending on economic developmentprograms and incentives in a state.

Michigan’s economicdevelopment expendituresper capita in 2014 were40% of the “Top Ten”average. Michigan’seconomic developmentexpenditures declined from2013 to 2014 while the“Top Ten” average stayedrelatively constant. AlthoughMichigan was ranked 6thamong its peers in termsof the level of economicdevelopment expenditures,it was still 15% above thepeer state average.

Economic Development ExpendituresStandings

Economic Development Expenditures

Council for Community and Economic Research (State Economic DevelopmentExpenditures Database)Bu

siness Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

34

ECON. DEV. EXPENDITURES

RANKLe

vel

28$21.97

$52.76

thTr

end

Top

10

Avg

.

Economic Development Expenditures Trends

35

input

cost

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

What it is:Average of three major business climateindices that account for several factorssuch as business costs, business leaders’perceptions, regulatory climate, quality oflife, etc. (1 = best, 50 = worst).

Why it matters:This measure is an indicator for howattractive a state might be for businesses.

Michigan’s average rankingacross three major businessclimate indices improved bythree spots from 2013 to

2014, but still remained inthe bottom 15 states.Michigan’s average ranking

was below all peer states

except Illinois and

California.

Index: Business Climate Ranking Standings

Business Climate Rankings

CEO Magazine (Best and Worst States for Business), CNBC (Top States for Business), Forbes (Best States for Business)

BUSINESS CLIMATE RANKINGS

RANKLe

vel

3837.7

21.5

thTr

end

Top

10

Avg

.

Business Climate Rankings Trends

4th Grade Reading

Business Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

36

4th Grade Reading Trends

What it is:Average score for reading proficiencyamong 4th graders, relative to the basescore (41.6% = basic, 47.6% = proficient).

Why it matters:This provides an indicator of how wellschools are meeting competitive academicstandards.

Michigan 4th graders areperforming below both the“Top Ten” average and thepeer state average in readingby about one percentagepoint. Both the Michiganaverage and the “Top Ten”average exceeded the “basic”level, but fall short of the“proficient” level. Michiganscores have declined since2007 and were among thebottom half among all states.Michigan’s 4th grade readingscores were outranked by allpeer states except Californiaand Texas.

4th Grade Reading Standings

National Center for Education Statistics (National Assessment of Educational Progress)

4TH GRADE READING

RANKLe

vel

3843.4%

44.6%

thTr

end

Top

10

Avg

.

What it is:Average score for mathematicsproficiency among 8th graders, relative tothe base score (52.4% = basic, 59.8% =proficient).

Why it matters:This provides an indicator of how wellschools are meeting competitiveacademic standards.

Michigan 8th gradersperformed below the “TopTen” average in mathematicsby 1.6 percentage points,and below the peer stateaverage by 0.9 percentagepoints. Both the Michiganaverage and the “Top Ten”average exceeded the “basic”level, but fall short of the“proficient” level. Michiganscores have improved overthe past decade, but werestill in the bottom half of thenation and were outrankedby over half of peer states.

8th Grade Math Standings

8th Grade Math

National Center for Education Statistics (National Assessment of Educational Progress)

37

input

value

8TH GRADE MATH

RANKLe

vel

3756.0%

57.6%

thTr

end

Top

10

Avg

.

8th Grade Math Trends

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

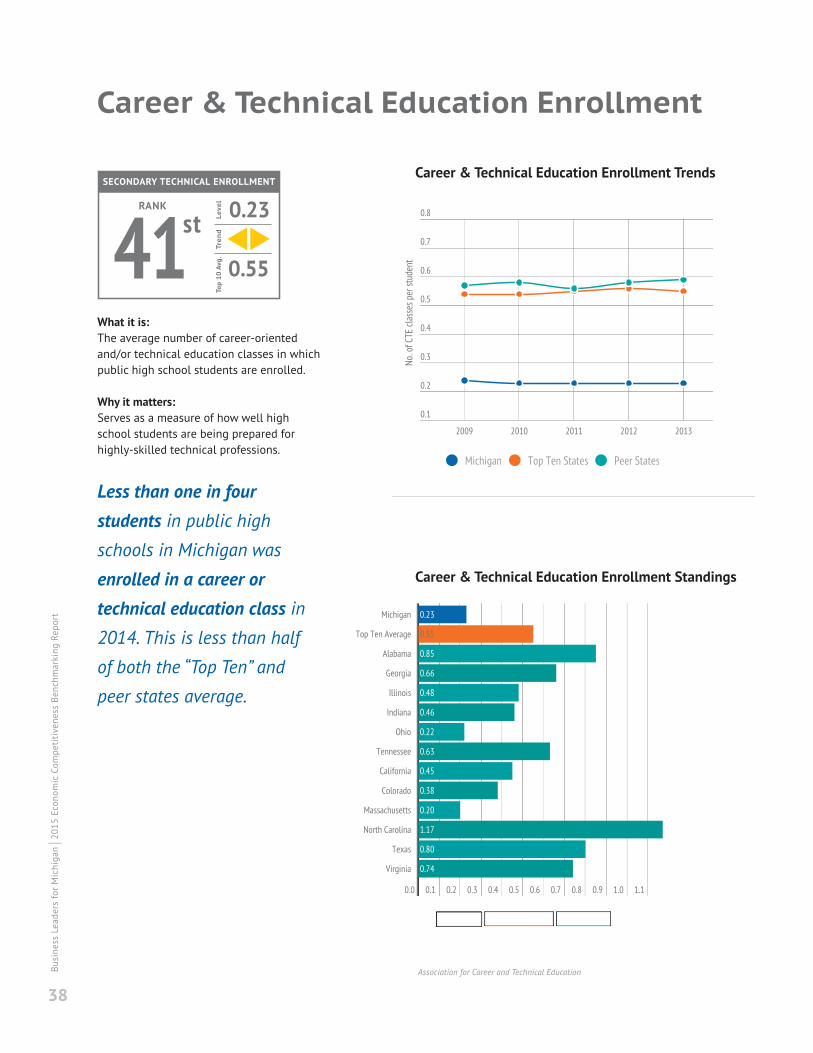

Career & Technical Education Enrollment

Business Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

38

Career & Technical Education Enrollment Trends

What it is:The average number of career-orientedand/or technical education classes in whichpublic high school students are enrolled.

Why it matters:Serves as a measure of how well highschool students are being prepared forhighly-skilled technical professions.

Less than one in fourstudents in public highschools in Michigan was

enrolled in a career ortechnical education class in2014. This is less than half

of both the “Top Ten” and

peer states average.

Career & Technical Education Enrollment Standings

Association for Career and Technical Education

SECONDARY TECHNICAL ENROLLMENT

RANKLe

vel

410.23

0.55

stTr

end

Top

10 A

vg.

39

input

value

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

What it is:Percent of students tested that met orexceeded the ACT College ReadinessBenchmarks in all four subjects (English,reading, mathematics, science).

Why it matters:This is an indicator of how well-preparedhigh school graduates are for enteringcollege and future careers.

The percentage of college-and career-ready graduatesin Michigan improved by onepercentage point from 2013to 2014, but is about 11percentage points lower thanthe “Top Ten” average.Michigan was among thebottom half of states in termsof college-ready graduatesand was outranked by allbut three of its peer states:Alabama, Tennessee, andNorth Carolina.

Career & College Readiness Standings

Career & College Readiness

ACT College and Career Readiness Benchmarks

CAREER & COLLEGE READINESS

RANKLe

vel

3522.0%

32.6%

thTr

end

Top

10

Avg

.

Career & College Readiness Trends

Business Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

40

Out-of-State Enrollment

Out-of-State Enrollment Trends

What it is:Percent of entering first-yearundergraduates from out of state.

Why it matters:This indicates how well higher educationinstitutions are attracting students fromout of state to provide an infusion of talentand capital. This should be compared within-state enrollment to ensure that statesare maintaining in-state enrollment.

The rate of out-of-stateenrollment at highereducation institutions inMichigan was less than half ofthe “Top Ten” average in 2012and trailed all but four states inthe nation. However, Michigan’sout-of-state enrollment rategrew by 1.2 percentage-pointsfrom 2010 to 2012 comparedto the “Top Ten” average.Among peer states, onlyinstitutions in California andTexas have lower out-of-stateenrollment rates thanMichigan.

Out-of-State Enrollment Standings

National Center for Education Statistics Integrated Postsecondary EducationData System, U.S. Census Bureau Population Estimates (2012 data)

OUT-OF-STATE ENROLLMENT

RANKLe

vel

4611.7%

28.1%

thTr

end

Top

10 A

vg.

41

input

value

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

What it is:Total associate, bachelor’s, master’s, anddoctorate degrees conferred per 10,000residents by public and private institutions.

Why it matters:Number of students earning a degreeeach year. Educational attainment is afactor in accessing the quality of a state’stalent pool.

The number of degreesconferred by highereducation institutions in

Michigan has been

increasing, but remainedbelow the “Top Ten” averageby about 10% in 2014.

Michigan was near the

middle of its peers but above

average in terms of the

number of degrees conferred

per 10,000 of population.

Note: Degrees include associate, bachelor’s, andgraduate/professional degrees. Higher education institutionsinclude all public and private degree-granting institutions.

Degrees Conferred Standings

Degrees ConferredAssociate’s+ Per 10,000

National Center for Education Statistics (Integrated PostsecondaryEducation Data System), U.S. Census Bureau (Population Estimates)

DEGREES CONFERRED

RANKLe

vel

23201

224

rdTr

end

Top

10 A

vg.

Degrees Conferred Trends

Business Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

42

Technical EducationCritical Skills Degrees & Certificates

Technical Education Trends

What it is:Total critical skills degrees and certificatesconferred divided by the working agepopulation (ages 20 through 64, inclusive).

Why it matters:These degrees especially prepare studentsfor high-skilled occupations, particularly inthe STEM fields, which are the types ofjobs Michigan expects to increase in thefuture.

The number of critical skillsdegrees and certificatesawarded in Michigan percapita has increased by over50% since 2005. However,the level of degrees awardedis still 12% lower than the“Top Ten” average in 2014.Michigan also came in 6thamong its peers in terms ofthe level of critical skillsdegrees and certificatesawarded.

Note: Higher education institutions include all public andprivate degree-granting institutions.

Technical Education Standings

National Center for Education Statistics (Integrated PostsecondaryEducation Data System), U.S. Census Bureau (Population Estimates)

CRITICAL SKILLS DEG. & CERT.

RANKLevel

2795.8

109.4

thTrend

Top

10 A

vg.

43

input

value

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

What it is:Share of residents aged 25 to 64 with anassociate degree or higher.

Why it matters:The availability of highly educated talentcan promote future growth of theeconomy, particularly in highly skilledprofessions.

The level of highly educatedtalent available in Michiganhas increased by about 14

percentage points in the

last decade, but was fourpercentage points lowerthan the “Top Ten” averagein 2013. Michigan was

among the bottom half

of states in terms of

educational attainment

and was outranked by

half of its peer states.

Educational Attainment Standings

Educational Attainment Population age 25-64 with Associates+

U.S. Census Bureau (American Community Survey)

EDUCATIONAL ATTAINMENT

RANKLe

vel

3138.4%

42.4%

stTr

end

Top

10

Avg

.

Educational Attainment Trends

Business Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

44

Talent Migration Educated Adults with BA+

Talent Migration Trends

What it is:Immigrants with a bachelor’s degree orhigher minus emigrants with a bachelor’sdegree or higher.

Why it matters:This measure indicates how well a stateattracts and retains highly educatedindividuals to live in the state.

2013 marked the secondconsecutive year in whichMichigan had a net positivemigration of talentedindividuals after five prioryears of net losses. However,

the net migration of educated

residents in Michigan was

lower than the “Top Ten”

average. Michigan gained

highly educated residents at

a slower pace in 2013 than

it had the year before, and

ranked third from the bottom

among peer states.

Talent Migration Standings

U.S. Census Bureau (American Community Survey)

TALENT MIGRATION

RANKLe

vel

2,838

10,562

Tren

dTo

p 10

Avg

.28th

45

input

value

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

Median Age

Median Age Trends

What it is:Median age of state residents.

Why it matters:Increase in the median age is an indicatorof an aging population, where thepopulation growth rate of middle age andsenior citizens outpaces that for childrenand young adults. States with a highmedian age among residents may be goodat attracting retirees, but it also can be asign that younger people are seeking outother places to work and raise a family.

Michigan was among the top10 oldest states in 2013,with the ninth-highestmedian age. Michigan’smedian age increasedslightly from 2012 to 2013,rising by 0.1 years. Thiscontinues a trend that hasseen the Michigan medianage increase by 2.7 yearssince 2005. Michigan’smedian age was higher thanall of its peers and all of the“Top Ten” states except forPennsylvania.

Median Age Standings

U.S. Census Bureau (Population Estimates)

MEDIAN AGE

RANKLe

vel

4139.6

36.9

stTr

end

Top

10 A

vg.

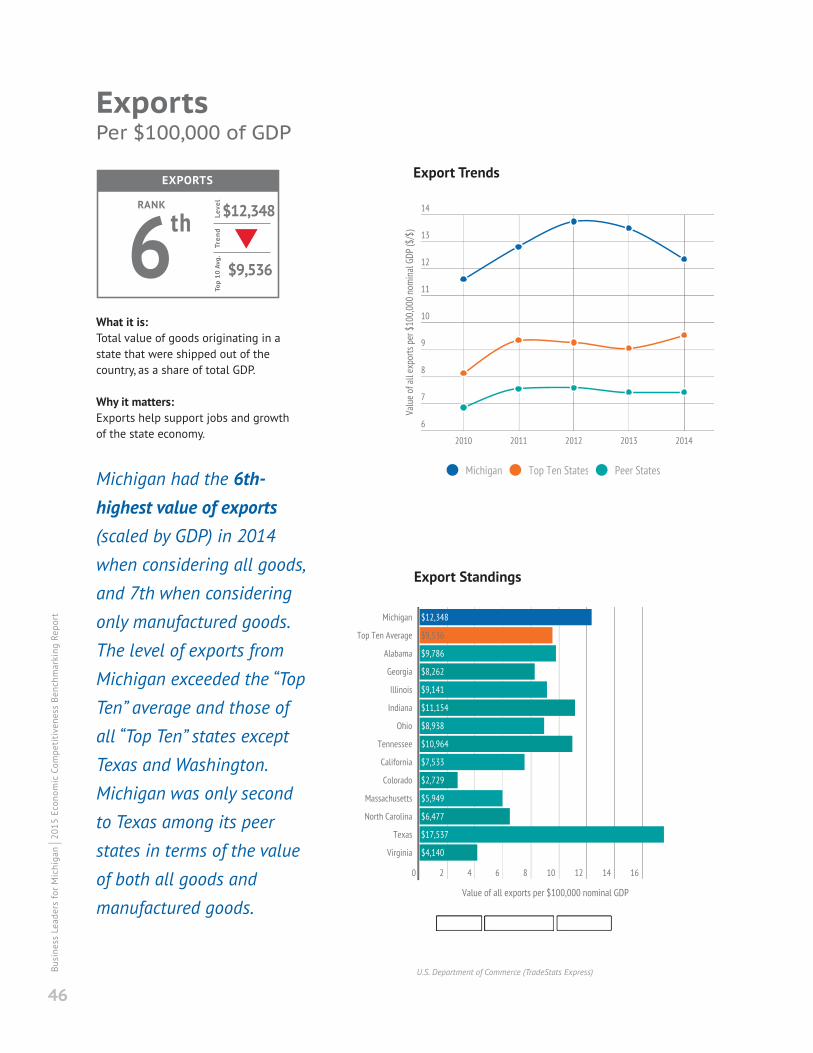

What it is:Total value of goods originating in astate that were shipped out of thecountry, as a share of total GDP.

Why it matters:Exports help support jobs and growthof the state economy.

Michigan had the 6th-highest value of exports(scaled by GDP) in 2014when considering all goods,and 7th when consideringonly manufactured goods.The level of exports fromMichigan exceeded the “TopTen” average and those ofall “Top Ten” states exceptTexas and Washington.Michigan was only secondto Texas among its peerstates in terms of the valueof both all goods andmanufactured goods.

Export Standings

ExportsPer $100,000 of GDP

U.S. Department of Commerce (TradeStats Express)Business Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

46

EXPORTS

RANKLevel

6$12,348

$9,536

thTrend

Top

10 A

vg.

Export Trends

47

input

value

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

University R&D ExpendituresPer $1M of GDP

University R&D Expenditure Trends

What it is:Research and development expendituresby higher education institutions, as ashare of total GDP.

Why it matters:Research and development expenditures byuniversities improve the state’s attractivenessto out-of-state students and talent, andprovide an important source of innovationand entrepreneurship in the state.

Research and developmentexpenditures at universitiesin Michigan were 6th in thenation in 2013 and werehigher than all of the “Top Ten”states except Massachusetts.Michigan universities’

research and development

expenditures were greater

than those of all of its peers

except Massachusetts and

North Carolina.

University R&D Expenditure Standings

National Science Foundation Higher Education R&D Expenditures by State,Bureau of Economic Analysis Real GDP by State

UNIVERSITY R&D EXPEND

RANKLe

vel

6 $5,879

$4,740

thTr

end

Top

10

Avg

.

What it is:Number of U.S. patents awarded per100,000 residents.

Why it matters:Patents provide an incentive forinnovators and entrepreneurs to improvetechnology. The states whose residentsare the source of this innovation have anadvantage in reaping the economicbenefits derived from them.

Michigan ranked 12th inthe nation in terms ofpatents per capita andexceeded the “Top Ten”

average. Michigan inventors

were more prolific than

those for all of its peers

except Massachusetts,

Colorado, and California on

a per capita basis.

U.S. Patent Standings

U.S. PatentsPer 100,000 Residents

U.S. Patent and Trademark Office (Patents By Country, State, and Year -Utility Patents), U.S. Census Bureau (Population Estimates)

Business Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

48

US PATENTS

RANKLe

vel

1253.5

39.8

thTr

end

Top

10 A

vg.

U.S. Patent Trends

49

input

value

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

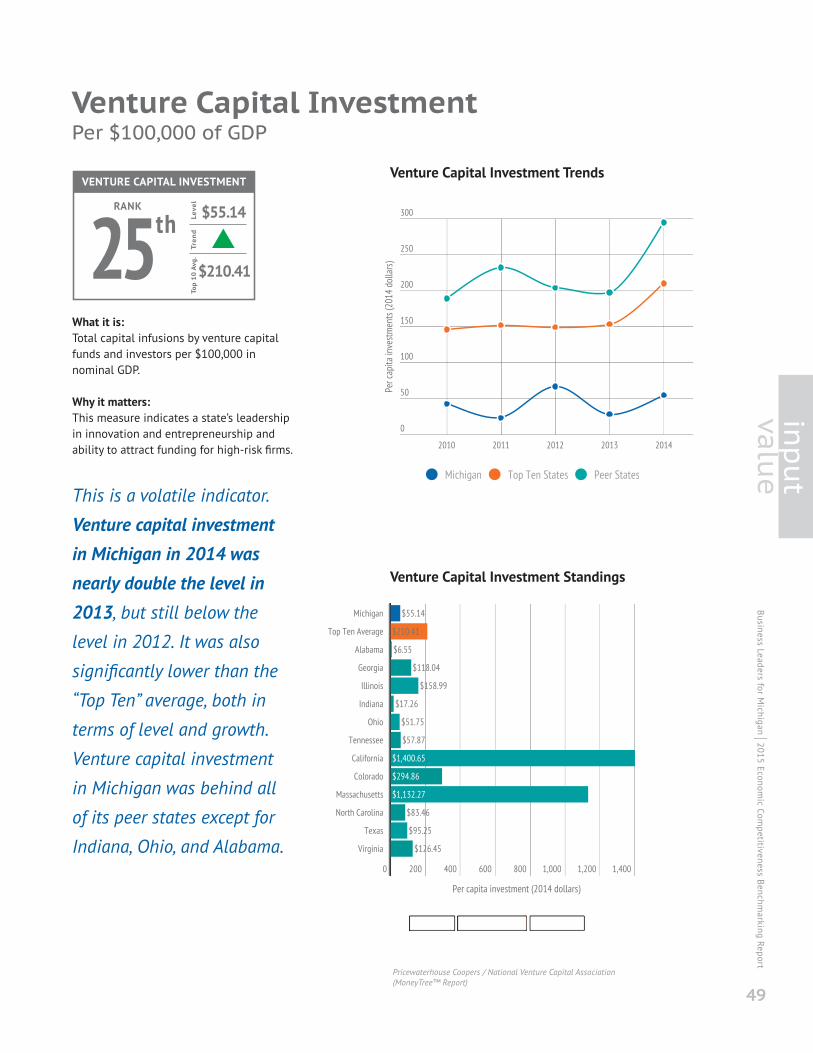

Venture Capital InvestmentPer $100,000 of GDP

Venture Capital Investment Trends

What it is:Total capital infusions by venture capitalfunds and investors per $100,000 innominal GDP.

Why it matters:This measure indicates a state’s leadershipin innovation and entrepreneurship andability to attract funding for high-risk firms.

This is a volatile indicator.

Venture capital investmentin Michigan in 2014 wasnearly double the level in2013, but still below thelevel in 2012. It was also

significantly lower than the

“Top Ten” average, both in

terms of level and growth.

Venture capital investment

in Michigan was behind all

of its peer states except for

Indiana, Ohio, and Alabama.

Venture Capital Investment Standings

Pricewaterhouse Coopers / National Venture Capital Association(MoneyTree™ Report)

VENTURE CAPITAL INVESTMENT

RANKLe

vel

25 $55.14

$210.41

thTr

end

Top

10 A

vg.

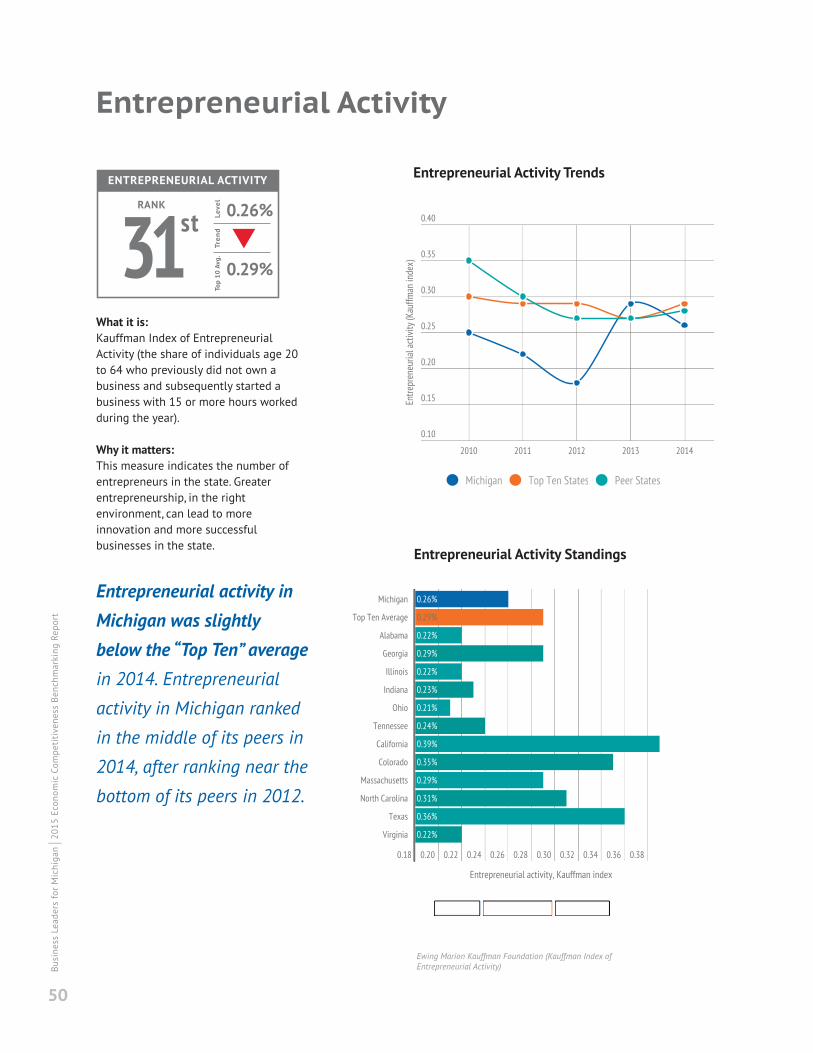

What it is:Kauffman Index of EntrepreneurialActivity (the share of individuals age 20to 64 who previously did not own abusiness and subsequently started abusiness with 15 or more hours workedduring the year).

Why it matters:This measure indicates the number ofentrepreneurs in the state. Greaterentrepreneurship, in the rightenvironment, can lead to moreinnovation and more successfulbusinesses in the state.

Entrepreneurial activity inMichigan was slightlybelow the “Top Ten” averagein 2014. Entrepreneurial

activity in Michigan ranked

in the middle of its peers in

2014, after ranking near the

bottom of its peers in 2012.

Entrepreneurial Activity Standings

Entrepreneurial Activity

Ewing Marion Kauffman Foundation (Kauffman Index ofEntrepreneurial Activity)Bu

siness Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

50

ENTREPRENEURIAL ACTIVITY

RANKLe

vel

0.26%

0.29%

Tren

dTo

p 10

Avg

.31st

Entrepreneurial Activity Trends

51

input

value

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

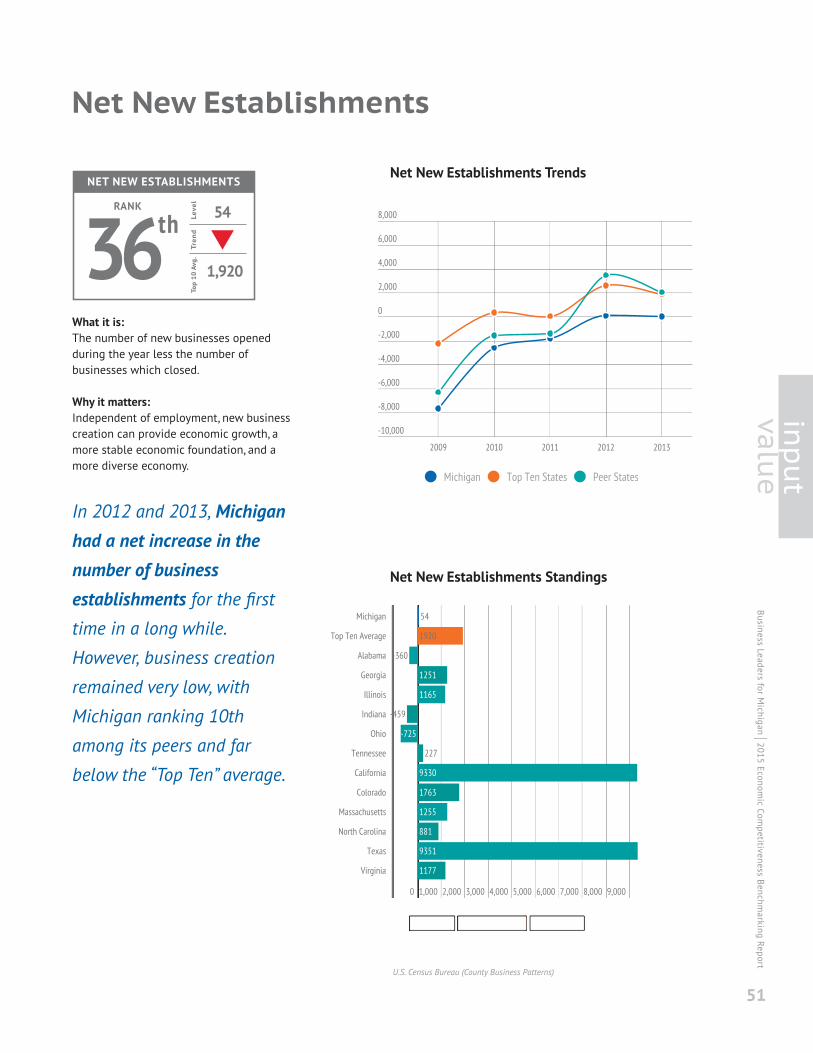

Net New Establishments

Net New Establishments Trends

What it is:The number of new businesses openedduring the year less the number ofbusinesses which closed.

Why it matters:Independent of employment, new businesscreation can provide economic growth, amore stable economic foundation, and amore diverse economy.

In 2012 and 2013, Michiganhad a net increase in thenumber of businessestablishments for the firsttime in a long while.

However, business creation

remained very low, with

Michigan ranking 10th

among its peers and far

below the “Top Ten” average.

Net New Establishments Standings

U.S. Census Bureau (County Business Patterns)

NET NEW ESTABLISHMENTS

RANKLe

vel

3654

1,920

thTr

end

Top

10 A

vg.

What it is:The number of new, privately owned,housing units authorized for constructionper 1,000 residents.

Why it matters:This measure indicates how quickly newhousing stock is being created in thestate—a proxy for growing populationand household formation, and a source ofeconomic growth.

Permits for new constructionin Michigan have improvedin recent years but remainfar below pre-recession

levels. There were fewer new

construction permits issued

per capita in Michigan than

in all “Top Ten” states and all

peer states except for Illinois.

New Construction Permit Standings

New Construction Permits

U.S. Census Bureau

Business Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

52

NEW CONSTRUCTION PERMITS

RANKLe

vel

461.6

4.6

thTr

end

Top

10 A

vg.

New Construction Permit Trends

53

input

value

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

Average Earnings ineconomy sectors

Average Earnings Trends - New Michigan sectors

What it is:Average annual earnings (in 2014 dollars), realGDP, and employment as a share of working-age population in the engineering, geographictrade, higher education, life sciences,automotive, and natural resources sectors.

Why it matters:These six sectors represent majoropportunities crucial for growing Michigan’seconomy, and moving it forward in the newglobal economy. These three major indicators(GDP, employment, and earnings) show howthese sectors are contributing to a state’sproduction and to residents' well-being.

While earnings in theindustries that have beenidentified as New Michiganopportunities remain wellabove the average earningsin Michigan, they have beenstagnant from 2011 to 2013.In earnings, employment, andGDP for these sectors,Michigan ranks in the middleof the pack among its peersand below the “Top Ten”average.

Average Earnings Standings - New Michigan sectors

New Michigan: The 2015 Report on Michigan's Progress inLeveraging Six Opportunities

AVERAGE EARNINGS

RANK

Leve

l

14$63,234

$64,593

th

Tren

dTo

p 10

Avg

.

newmichigan

What it is:Average annual earnings (in 2014dollars), real GDP, and employment as ashare of working-age population in theengineering, geographic trade, highereducation, life sciences, automotive, andnatural resources sectors.

Why it matters:These six sectors represent majoropportunities crucial for growingMichigan’s economy, and moving itforward in the new global economy.These three major indicators (GDP,employment, and earnings) show howthese sectors are contributing to a state’sproduction and to residents' well-being.

In real GDP among theindustries that have beenidentified as New Michiganopportunity industries,Michigan has improvedconsiderably over the pastfew years. In earnings,employment, and GDP,Michigan ranks in themiddle of the pack amongits peers and below the“Top Ten” average.

GDP Per Capita - New Michigan Standings

GDP Per Capita ineconomy sectors

New Michigan: The 2015 Report on Michigan's Progress inLeveraging Six OpportunitiesBu

siness Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

54

GDP PER CAPITAL – NEW MI

RANKLe

vel

22 $7,973

$14,187

ndTr

end

Top

10 A

vg.

GDP Per Capita - New Michigan Trends

newmichigan

55

input

value

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

Employment/Working Age Population ineconomy sectors

Employment/Working Age Population Trends

What it is:Average annual earnings (in 2014 dollars),real GDP, and employment as a share ofworking-age population in theengineering, geographic trade, highereducation, life sciences, automotive, andnatural resources sectors.

Why it matters:These six sectors represent majoropportunities crucial for growingMichigan's economy, and moving it forwardin the new global economy. These threemajor indicators (GDP, employment, andearnings) show how these sectors arecontributing to a state's production and toresidents' well-being.

Michigan has improvedconsiderably over the pastfew years. In employmentamong the industries that

have been identified as New

Michigan opportunity

industries. Michigan ranks in

the middle of the pack

among its peers and below

the “Top Ten” average.

Employment/Working Age Population Standings

New Michigan: The 2015 Report on Michigan's Progress inLeveraging Six Opportunities

EMPLOYMENT PERCENTAGE

RANK

Leve

l

2313.2%

16.1%

rd

Tren

dTo

p 10

Avg

.

newmichigan

Business Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

56

Urban Roads in Poor Condition

Urban Roads in Poor Condition Trends

What it is:Share of urban roads in poor condition, bylength.

Why it matters:A strong, reliable transportation systembenefits both businesses and individuals.Poor road quality imposes many tangiblecosts and reduces productivity.

The percentage of poor-quality urban roads inMichigan increased from2012 to 2013. Urban roadquality was worse in

Michigan than the “Top Ten”

average, and Michigan

ranked 39th among all

states. Among peers,only Massachusetts andCalifornia have a greaterpercentage of urban roadsin poor condition.

Note: Includes interstate highways, freeways, expressways, andmajor arterial roads in urban areas.

Urban Roads in Poor Condition Standings

U.S. Department of Transportation Federal Highway Administration(Length by measured pavement roughness, all systems)

URBAN ROADS IN POOR CONDITION

RANKLevel

3913.3%

11.8%

thTrend

Top

10

Avg

.

57

input

value

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

U.S. Department of Transportation Federal Highway Administration(Area of bridges by Functional Classification)

What it is:Percent of bridges in deficient condition,by area.

Why it matters:A strong, reliable transportation systembenefits both businesses and individuals.Poor bridge quality imposes manytangible costs and reduces productivity.

The share of bridgescategorized as deficient inMichigan has declinedconsiderably over the past10 years, declining at aconsiderably higher ratethan that for the “Top Ten”average and for peer states.However, the share ofbridges that are deficient inMichigan remains abovethose two averages.Michigan has a higher shareof deficient bridges than allpeer states except Californiaand Massachusetts.

Deficient Bridge Standings

Deficient Bridges

DEFICIENT BRIDGES

RANKLe

vel

4233.5%

32.0%

ndTr

end

Top

10 A

vg.

Deficient Bridge Trends

Akami

Business Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

58

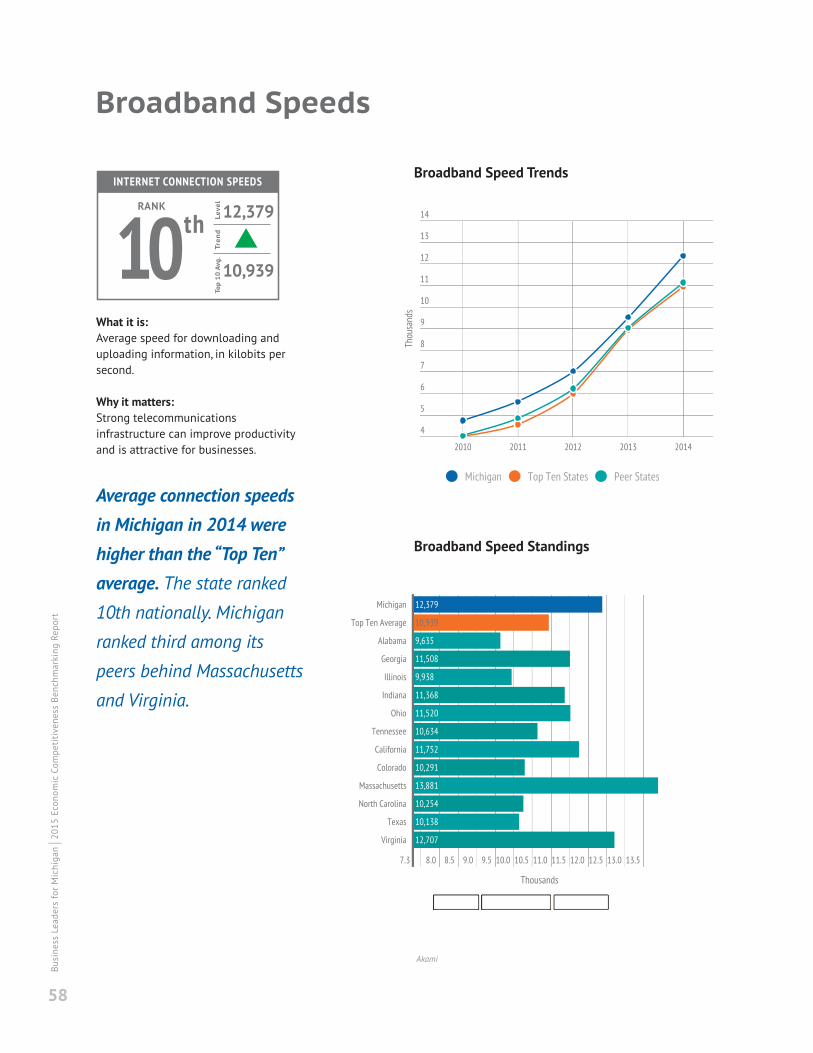

Broadband Speeds

Broadband Speed Trends

What it is:Average speed for downloading anduploading information, in kilobits persecond.

Why it matters:Strong telecommunicationsinfrastructure can improve productivityand is attractive for businesses.

Average connection speedsin Michigan in 2014 werehigher than the “Top Ten”average. The state ranked10th nationally. Michigan

ranked third among its

peers behind Massachusetts

and Virginia.

Broadband Speed Standings

INTERNET CONNECTION SPEEDS

RANKLevel

10 12,379

10,939

thTrend

Top

10 A

vg.

59

input

value

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

What it is:The percent of households with high-speed Internet connections, based onhousehold survey data.

Why it matters:Access to Internet at home makes iteasier for students, workers, andentrepreneurs to stay connected.

The number of households

with access to quality

internet service increased

by 25 percentage points

between 2007 and 2013.

However, Michigan still ranksbelow the averages of both“Top Ten” and peer states.

Broadband Penetration Standings

Broadband Penetration

U.S. Census Bureau

BROADBAND PENETRATION

RANKLe

vel

3870.7%

75.0%

thTr

end

Top

10 A

vg.

Broadband Penetration Trends

Business Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

60

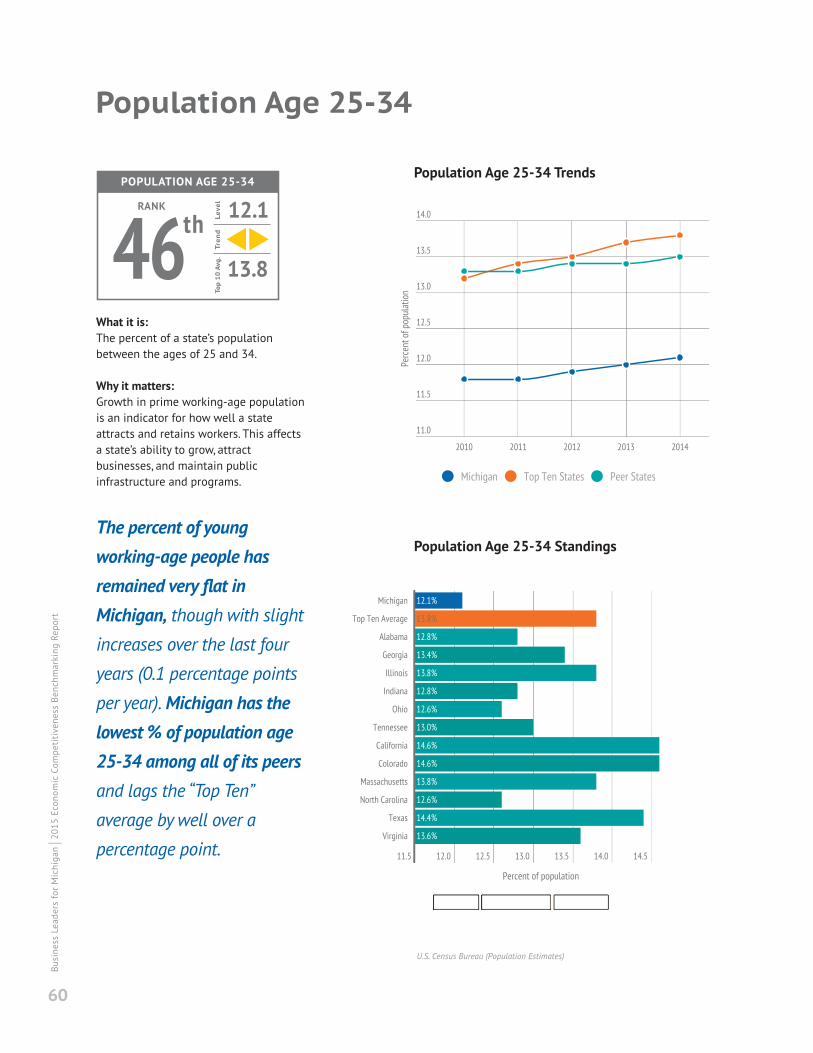

Population Age 25-34

Population Age 25-34 Trends

What it is:The percent of a state’s populationbetween the ages of 25 and 34.

Why it matters:Growth in prime working-age populationis an indicator for how well a stateattracts and retains workers. This affectsa state’s ability to grow, attractbusinesses, and maintain publicinfrastructure and programs.

The percent of youngworking-age people hasremained very flat inMichigan, though with slightincreases over the last four

years (0.1 percentage points

per year). Michigan has thelowest % of population age25-34 among all of its peersand lags the “Top Ten”

average by well over a

percentage point.

Population Age 25-34 Standings

U.S. Census Bureau (Population Estimates)

POPULATION AGE 25-34

RANKLe

vel

4612.1

13.8

thTr

end

Top

10 A

vg.

61

input

value

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

What it is:The average number of minutes it takesfor a worker to travel to and from work.

Why it matters:A shorter commute time means easieraccess to jobs for workers and lessproductive time wasted duringcommutes.

Michigan ranks in themiddle of all states forcommute time, with slightlylonger commutes than the

“Top Ten” average, but

shorter commutes than nine

of its peer states.

Commute Time Standings

Commute Time

US Census Bureau

COMMUTE TIME

RANKLe

vel

2824.0

22.7

thTr

end

Top

10 A

vg.

Commute Time Trends

Business Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

62

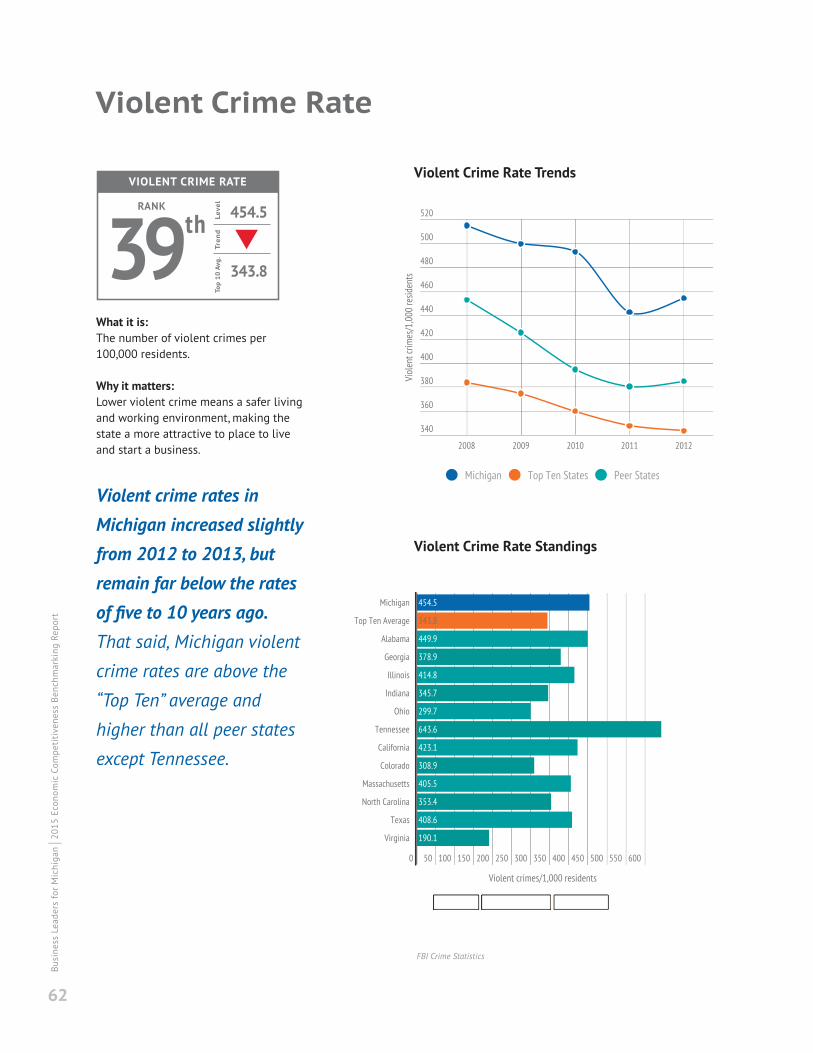

Violent Crime Rate

Violent Crime Rate Trends

What it is:The number of violent crimes per100,000 residents.

Why it matters:Lower violent crime means a safer livingand working environment, making thestate a more attractive to place to liveand start a business.

Violent crime rates inMichigan increased slightlyfrom 2012 to 2013, butremain far below the ratesof five to 10 years ago.That said, Michigan violent

crime rates are above the

“Top Ten” average and

higher than all peer states

except Tennessee.

Violent Crime Rate Standings

FBI Crime Statistics

VIOLENT CRIME RATE

RANKLe

vel

39454.5

343.8

thTr

end

Top

10 A

vg.

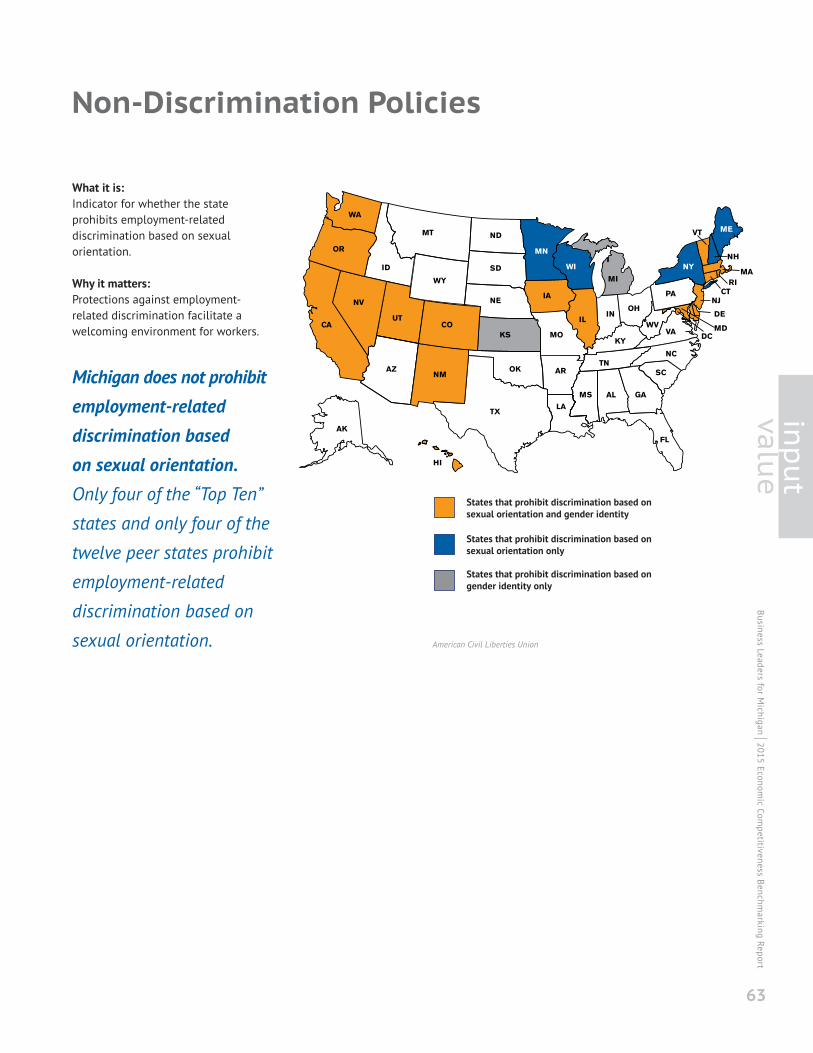

States that prohibit discrimination based on sexual orientation and gender identity

WA

OR

CA

NV

UT

AZNM

CO

WY

ID

MT ND

SD

NE

KS

OK

MN

IA

MO

AR

TXLA

ILIN

OH

KY

TN

MS AL GA

FL

SC

NC

VAWV

PA

NY

ME

NH

NJ

DE

MDDC

CTRI

MAWI

MI

AK

HI

VT

States that prohibit discrimination based on sexual orientation only

States that prohibit discrimination based on gender identity only

63

input

value

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

Non-Discrimination Policies

What it is:Indicator for whether the stateprohibits employment-relateddiscrimination based on sexualorientation.

Why it matters:Protections against employment-related discrimination facilitate awelcoming environment for workers.

Michigan does not prohibitemployment-relateddiscrimination basedon sexual orientation.Only four of the “Top Ten”

states and only four of the

twelve peer states prohibit

employment-related

discrimination based on

sexual orientation. American Civil Liberties Union

Business Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

64

Input Conclusions

Michigan has achieved Top Ten performance on cost inputssuch as Business and Overall Tax Climates and is trendingpositive on Labor and Energy cost inputs.

Michigan’s performance on key value inputs is mixed withstrengths in innovation areas such as University Researchand Development, Exports and Patents. Michigan’sperformance is in the bottom third of states on severaltalent measures, including 4th grade reading, career- andcollege-ready graduates, out-of-state enrollment, andeducational attainment.

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

65

input

Bottom10

RoadQuality

4th GradeReading

Career &CollegeReadiness

Patents

Top 10

UniversityR&D

Exports

Educational Attainment

TaxClimate

Business Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

66

KEWEENAWW

ONTONAGON

GOGEBIC

IRON

BARAGA

MARQUETTE

DICKINSON

MENOMINEE

DELTA

ALGERSCHOOLCRAFT

LUCE

MACKINAC

CHIPPEWA

EMMET

CHEBOYGANPRESQUE ISLE

CHARLEVOIX

ALPENA

MONTMORENCYOTSEGANTRIM

LEELANAU

BENZIEGRAND

TRAVERS

KALKASKACODA ALCONA

IOSCOOGEMAWROSCOMMONUKEEWEXFORMANISTEE

MASON LAKE OSCEOLA CLARE GLADWINARENAC

HURON

MIDLAND

TUSCOLA SANILAC

LAPSHIAWASSEE

GRATIOAGINAW

GENESEE

MECOSTANEWAYGO

OCEANA

OTTAWA

MONTCALM

IONIA CLINTON

EATOLIVINGSTON

ALLEGAN

VAN BURENJACKSON

BERRIEN CAS JOSEPH BRANCH HILLSDALE WEE MONROE

HOUGHTON

ISABELLA

MUSKEGON

KENT

GHAM

KALAMAZOO CALHOUN WASHTENAW WAYNE

OAKLAND

MACOMB

ST. CLAIR

BAY

CRAWF

BARRY

1

SE

KALKA

MIMISSMISSAURD2

MGO

OSCORD3

KENT

4MIDLAND

OTSA

5 A SAN

PEER S

6CLINTON

ON ING7

ON

LENAW

W

9WAYNE

10SS ST. J

KALA

8

1

5

9

3

7

2

6

10

4

8

Upper Peninsula region

Lake Superior Community

Partnership

Northwest region NWMCOG

Northeast region NEMCOG

West Michigan region The Right Place

East Central Michigan region

Saginaw Future

East Michigan region Flint and Genesee Chamber of Commerce

South Central region LEAP

Southwest region Southwest Michigan First

Southeast Michigan region

Ann Arbor SPARK

Detroit Metro region Detroit Economic Growth Corp

Oakland County PCD

Macomb County PED

Wayne County EDGE

REGIONS

Michigan’s Regional PerformanceMichigan is not one economy; rather it is multiple economies identified by commonregional assets. This section illustrates the economic performance of Michigan'sregions over the last five years.

OutputEmployment GrowthUnemployment RateLabor ForcePer Capita IncomePopulation

InputDegrees ConferredTechnical EducationEducational AttainmentPatents Per 100,000 Residents

What it is:Seasonally-adjusted average number of residents

with a private-sector job.

Why it matters:Higher levels of private employment indicate both

economic strength and prosperity among the

region’s residents.

Employment Growth

What it is:Average share of labor force that is looking for

work but does not have a job (not seasonally-

adjusted).

Why it matters:A lower unemployment rate indicates that more

residents seeking employment are able to find it.

Unemployment Rate

67

regional

Bureau of Labor Statistics (Quarterly Census of Employment and Wages)

Bureau of Labor Statistics (Local Area Unemployment Statistics)

2014 Unemployment Rate

2009-14 Employment CAGR

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

Business Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

68

What it is:The share of the population age 16 and older, not

including residents who are on active duty or

institutionalized, that is employed or looking for work.

Why it matters:Members of the working-age population can stop

looking for work and drop out of the labor force due

to many reasons, including disability, old age, or

discouragement. Higher labor force participation is

a sign of a healthier economy and workforce.

Labor Force

Bureau of Labor Statistics (Local Area Unemployment Statistics)

What it is:Share of residents aged 25 to 64 with an

associates degree or higher.

Why it matters:The availability of highly educated talent can

promote future growth of the economy.

Educational Attainment

U.S. Census Bureau (American Community Survey)

2009–14 Labor Force CAGR

Educational Attainment (2009–13 Estimates)

69

regional

What it is:Personal income (2014 dollars) divided by

population. Personal income includes salaries,

wages, and bonuses from employment; dividends

and interest from investments; rental income;

pensions, etc.

Why it matters:Personal income is an indicator of prosperity and

average standard of living in a region.

Per Capita Income 2013 Per Capita Personal Income

Bureau of Economic Analysis (Personal income summary), Bureau of Labor Statistics (CPI Inflation Calculator)

2008-13 Per Capita Personal Income CAGR

Business Leaders for Michigan I 2015 Econom

ic Competitiveness Benchm

arking Report

Business Leaders for Michigan I20

15 Economic Com

petitiveness Benchmarking Report

70

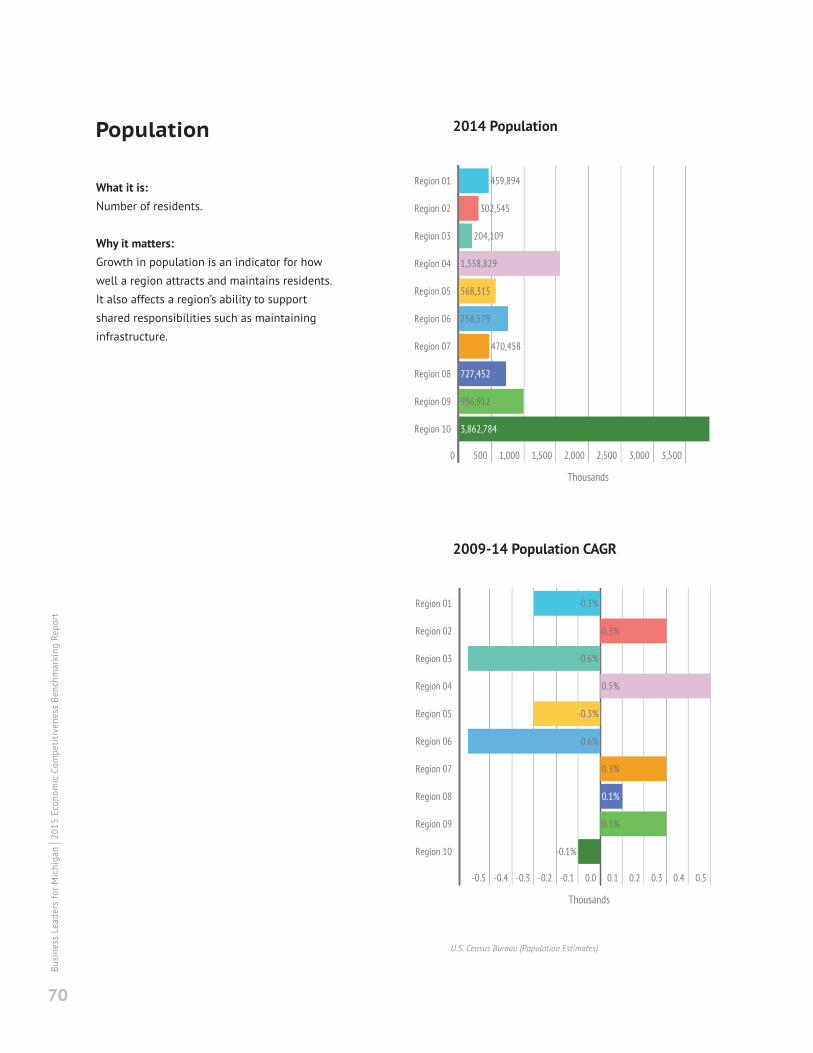

What it is:Number of residents.

Why it matters:Growth in population is an indicator for how

well a region attracts and maintains residents.

It also affects a region’s ability to support

shared responsibilities such as maintaining

infrastructure.

Population

U.S. Census Bureau (Population Estimates)

2014 Population

2009-14 Population CAGR

71

regional

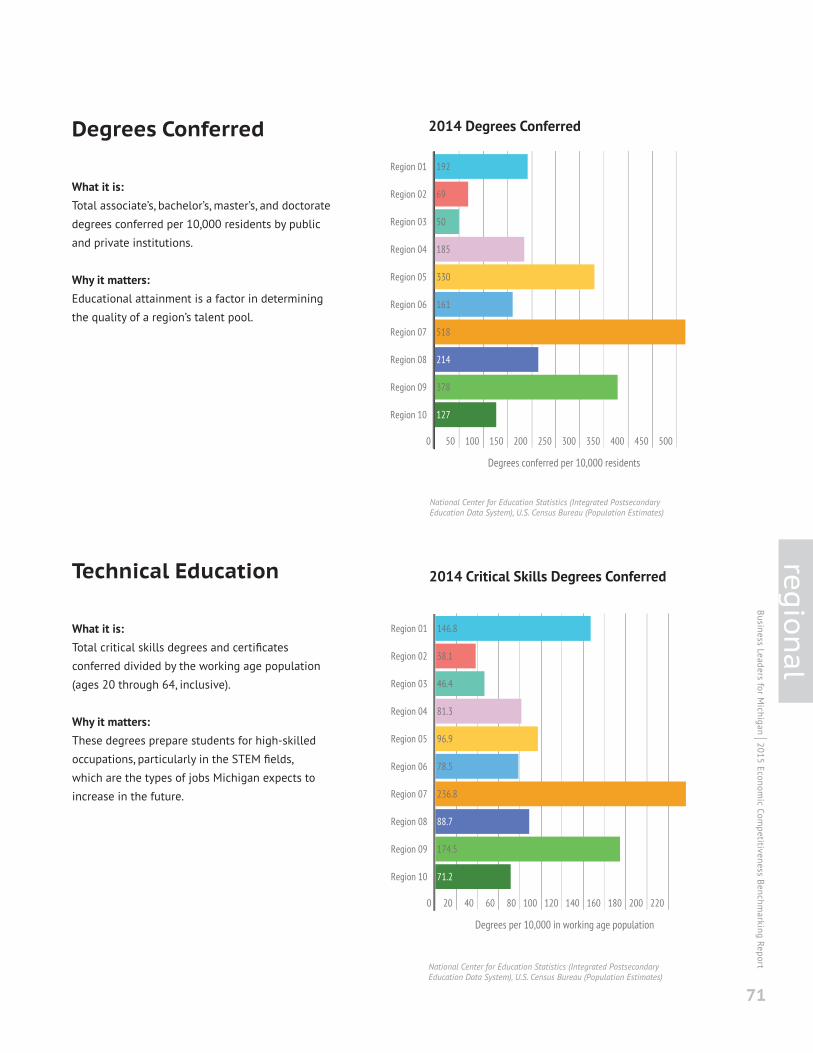

What it is:Total associate’s, bachelor’s, master’s, and doctorate

degrees conferred per 10,000 residents by public

and private institutions.

Why it matters:Educational attainment is a factor in determining

the quality of a region’s talent pool.

Degrees Conferred

National Center for Education Statistics (Integrated PostsecondaryEducation Data System), U.S. Census Bureau (Population Estimates)

2014 Degrees Conferred

What it is:Total critical skills degrees and certificates