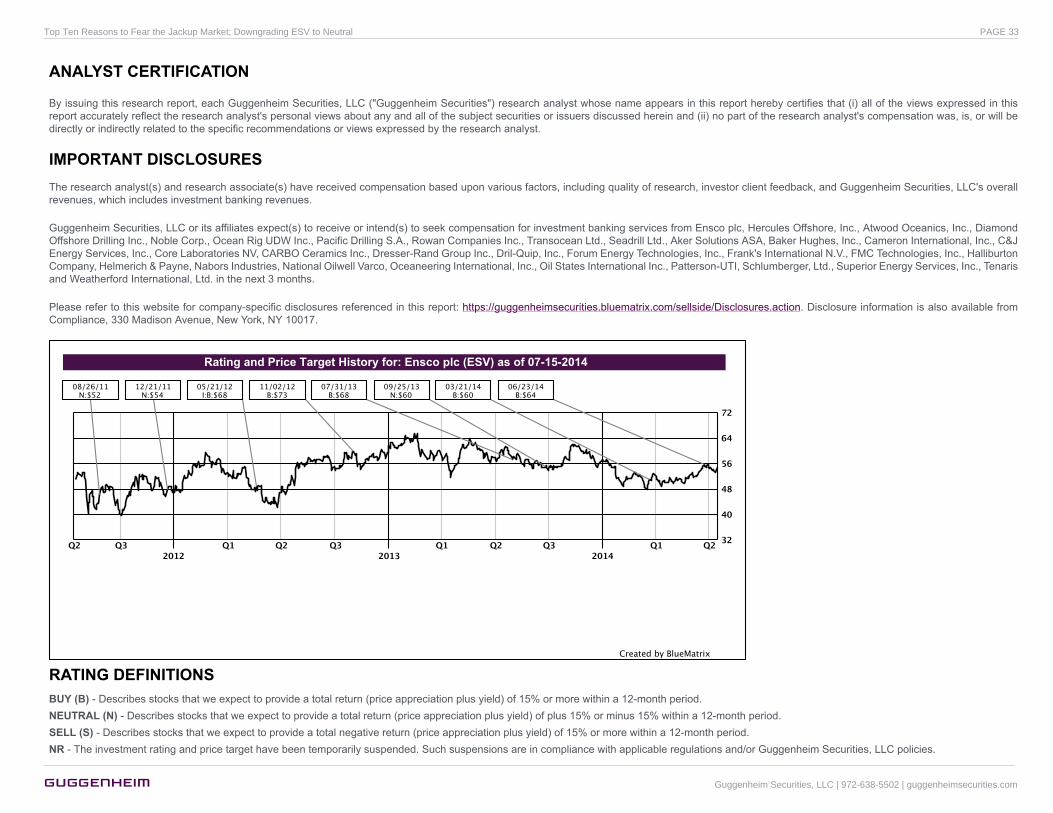

2014-07-16_esv downgrade - d. gacicia

TRANSCRIPT

People. Ideas. Success.

Guggenheim Securities, LLC Oilfield Services, Offshore Contract Drillers & Capital Equipment

July 16, 2014

Top Ten Reasons to Fear the Jackup Market; Downgrading ESV to Neutral

Darren Gacicia

(212) 293-3054

GUGGENHEIM SECURITIES, LLC See pages 33 - 34 for analyst certification and important disclosures.

This report is intended for Darren.G

acicia@guggenheim

partners.com at G

uggenheim. U

nauthorized distribution of this report is prohibited.

Concerns for the Jackup Market Leave Us Looking for Floater Leverage Rains in Floater Market Mask a Brewing Storm for Jackups. Investors’ focus on the near-term floater market woes distract them from bearish factors brewing in the

jackup market. In our view, the market has yet to discount jackup market risks, unlike floater market overhangs. We may prove early, but we see the potential risk to

jackup-levered shares to underperform, as negative scenarios play out. As a result, we would look to limit jackup exposure (especially older fleets) and increase exposure to

the floater market, where risks are better understood and “second derivatives” show signs of improvement. (See “Second Derivative” Leads Drivers, Despite Near-Term

Headwinds, 6/2/14). Based on our analysis (pgs. 5-6), ESV, RDC, HERO, and NE screen poorly for jackup exposure. Albeit, the Paragon transaction cleanses NE’s fleet.

Downgrading ESV to NEUTRAL from BUY; Lowering Our Price Target to $58. Given that ESV derives 30-35% of its estimated fleet value and 2015E EBITDA from a

jackup fleet that averages 25+ years old, we see a potential overhang for the shares under a negative scenario for shallow water assets (pgs. 5-6). In our view, rig-on-rig

competition presents the greatest threat to older, less capable assets. Since we feel forces are aligning against the jackup market (see below), we see potential EPS risk

outweighing a favorable payout strategy and solid execution track record. As a result, we look to group ESV with other jackup-weighted, Neutral-rated offshore drillers,

RDC (Neutral, $31.71) and HERO (Neutral, $4.04). We are lowering our price target for ESV to $58 from $64 to reflect our revised, risk-weighted NAV.

Lowering HERO PT to $4.50. To reflect our view toward increased risk to the near-term jackup market, we are lowering our HERO price target to $4.50 from $5.00.

Prefer Floater Exposure, Where Negatives Are Identified & Light at the End of the Tunnel Looks Clearer. Floater-levered stocks have generally stopped declining on

bad news, but negative floater contract optics may leave offshore driller shares range-bound in the near term. We would use volatility as an additional opportunity to buy

floater-levered names, where forecasts and shares already acknowledge bearish scenarios. For exposure to floater-centric names with minimal exposure to legacy

jackups, we prefer SDRL (BUY, $38.38) and RIG (BUY, $43.61) within large caps, and ATW (BUY, $50.66) and PACD (BUY, $9.99) among small/mid caps.

Negative Indicators Leave Concerns for the Jackup Market:

1) Overhang of Uncontracted Newbuilds Threatens Market Psychology (pg. 7). Even if rig additions enter the market in an orderly fashion, the market must adjust

for risks of negative scenarios. Thus, ESV, RDC, and HERO may prove laggards. With uncontracted newbuilds representing 20% of the 2016 jackup fleet and only

40% of newbuilds sponsored by established players, the market may be poised for a disruptive rig absorption period, in our view.

2) Shorter Contract Durations Mimic Floater Downturn (pg. 8). Jackup contract durations have been shortening, akin to the floater market before dayrates became

choppy. In our view, IOCs may be signaling a desire for more optionality in front of newbuild arrivals, a negative market indicator.

3) Future Jackup Demand Even Less Visible Than the Floater Market (pgs. 9-10). The lack of demand visibility for the jackup market leaves it more prone to

negative shifts in sentiment if the market gets “spooked” by the prospects of new rig arrivals, negative fixtures, or cautious guidance.

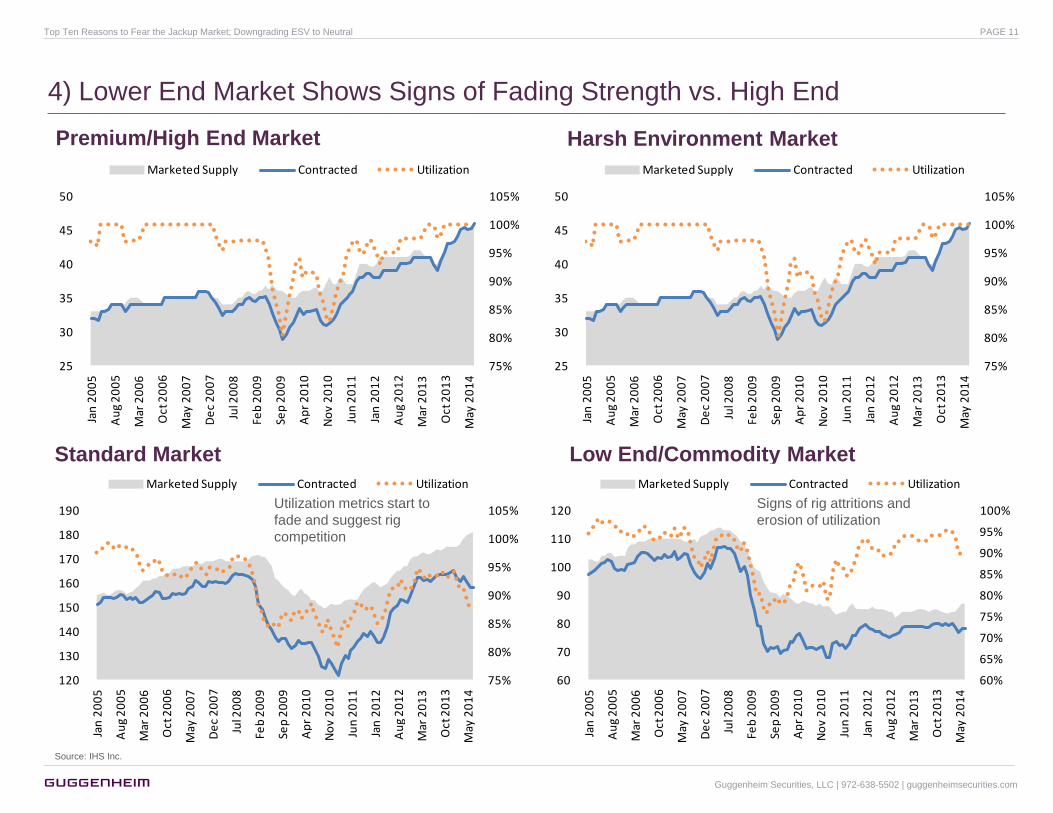

4) Lower End Jackups Shows Signs of Fading Strength (pg. 11). Standard and commodity jackups are starting to show some utilization weakness, despite

positive trends in dayrates. More idle rigs, without clarity on fleet retirements, may put pressure on market balances.

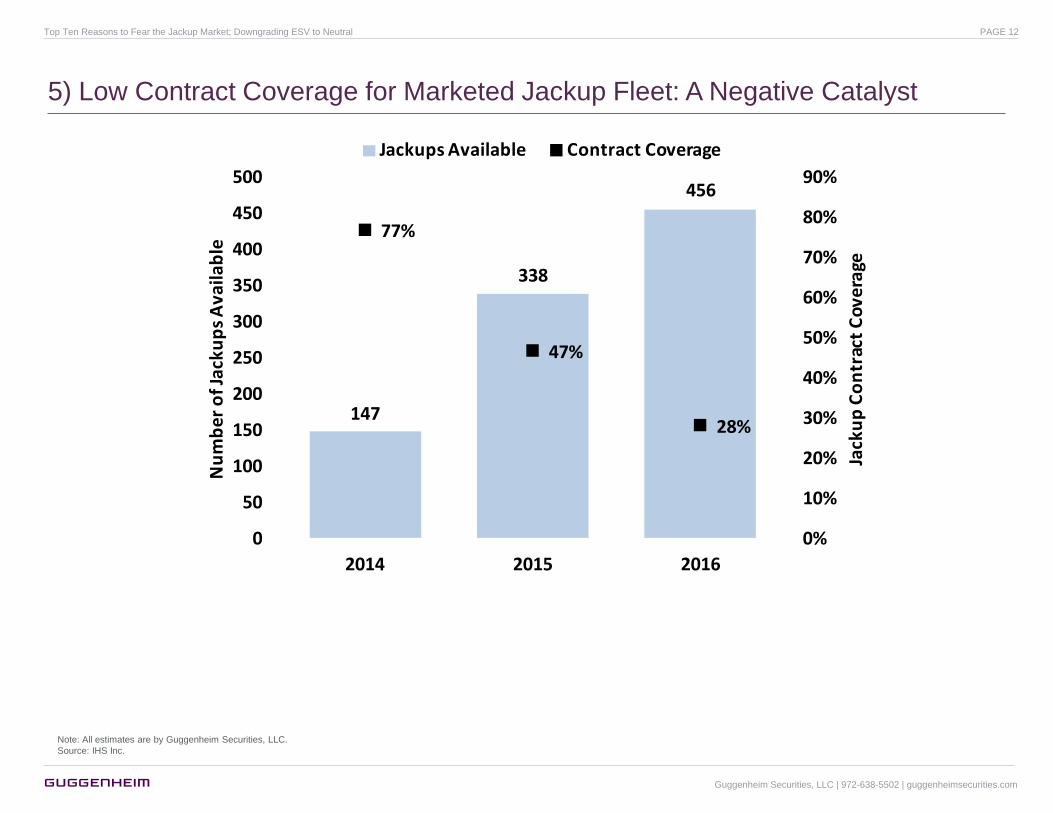

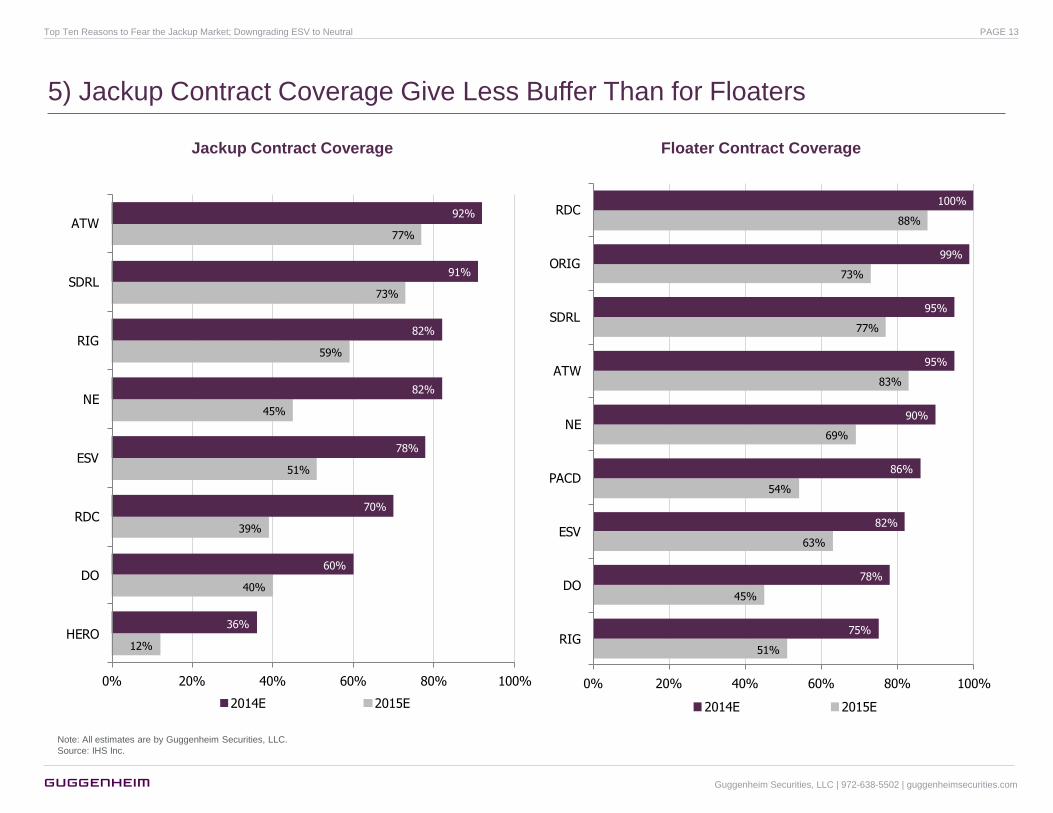

5) Market & Company Contract Coverage Remains a Concern (pgs. 12-13). Broader market and company jackup contract coverage remains traditionally lower

than the floater market, below 50% for 2015. Less coverage leaves EPS at greater risk to dayrate variance, especially for older units.

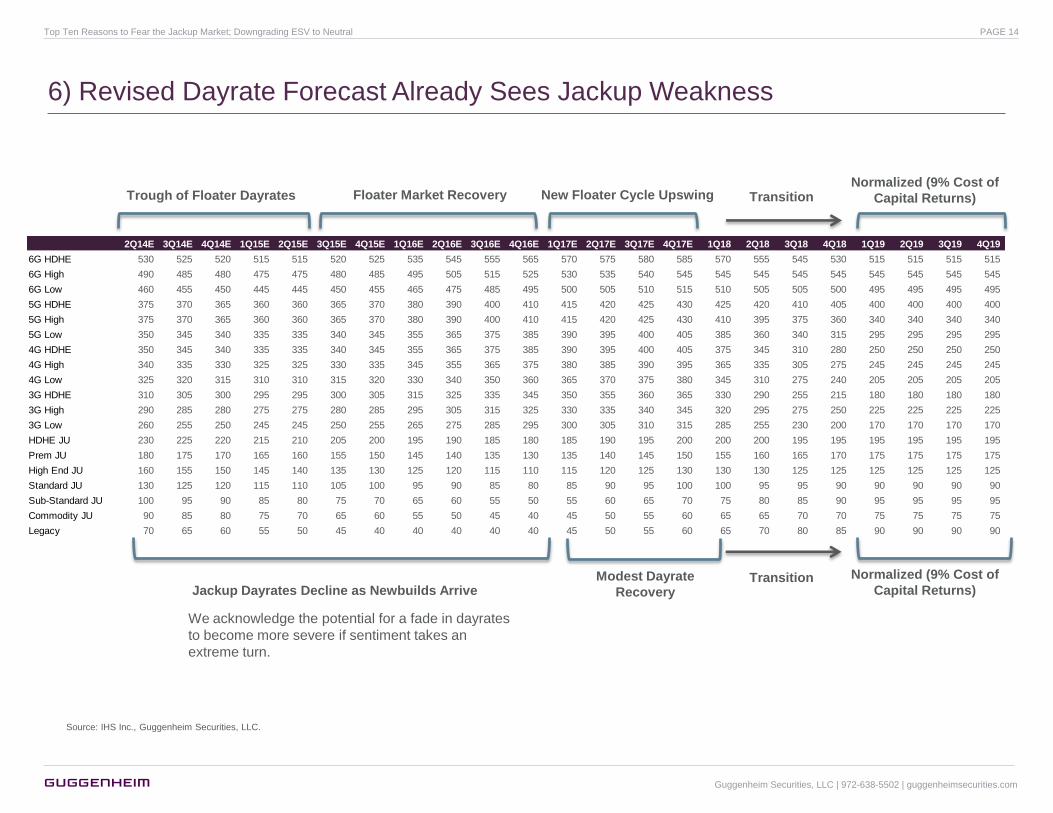

6) Lower Dayrates Baked Into Forecast, but Market Shift May Prove More Extreme Than Our Forecast (pg. 14). We are expecting a gradual fade in jackup

dayrates, down 30-40% through 2016. More extreme or accelerated dayrate volatility may put our EPS estimates at risk.

7) Continued Dayrate Strength Leaves Market Poised for Negative Surprises (pgs. 15-16). Concerns about the floater market continue to dominate the spotlight

and jackup dayrate trends and guidance remains relatively benign. Current complacency toward changes in the jackup market, which catches investors off guard in

the event of a downturn, may amplify moves to the downside.

8) Fleet Replacement Cycle May Prove Sloppy (pgs. 17-19). Upcoming surveys may foreshadow retirements for older jackups, but the potential number of

retirements to match incoming uncontracted supply may prove too daunting to maintain an orderly marker, as rig-on-rig competition from drillers looking to

maximize cash flows likely leads jackup dayrates lower.

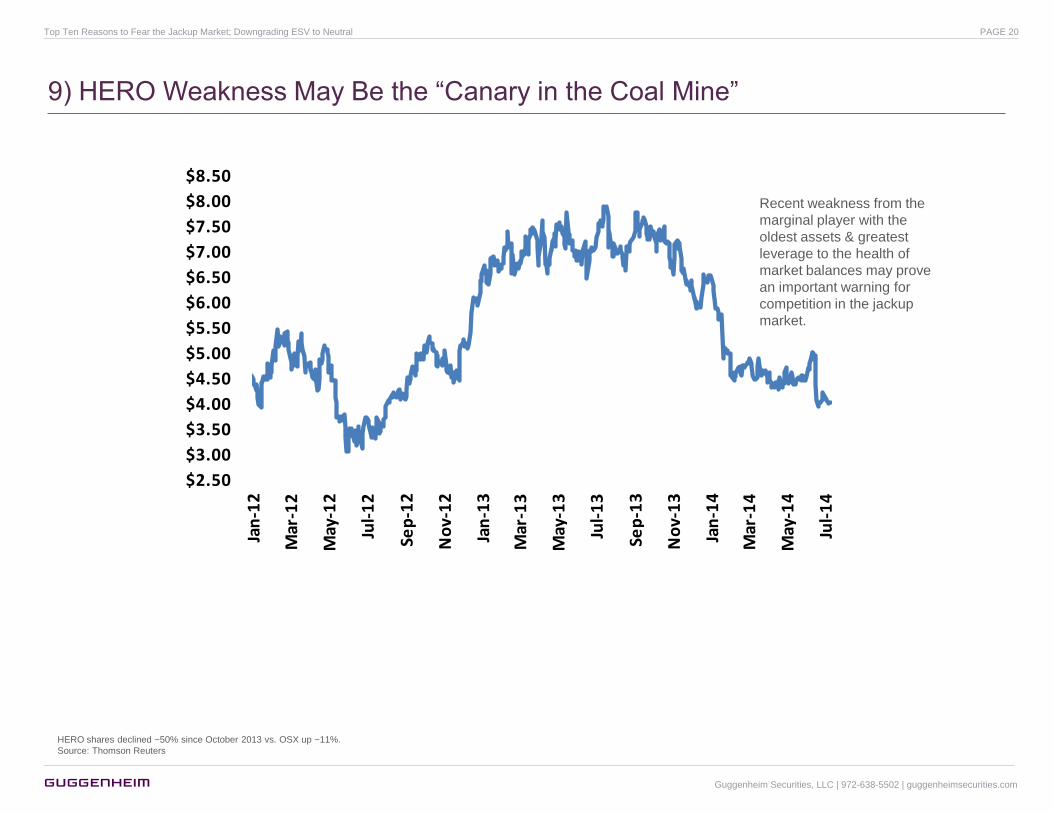

9) HERO: “Canary in the Coal Mine”? (pg. 20). HERO is the marginal player with the oldest jackup assets. The shares have been cut in half since the fall of 2013

(OSX up ~12%). In our view, the shares may be sending an early warning sign for the jackup market that greater rig-on-rig competition looms.

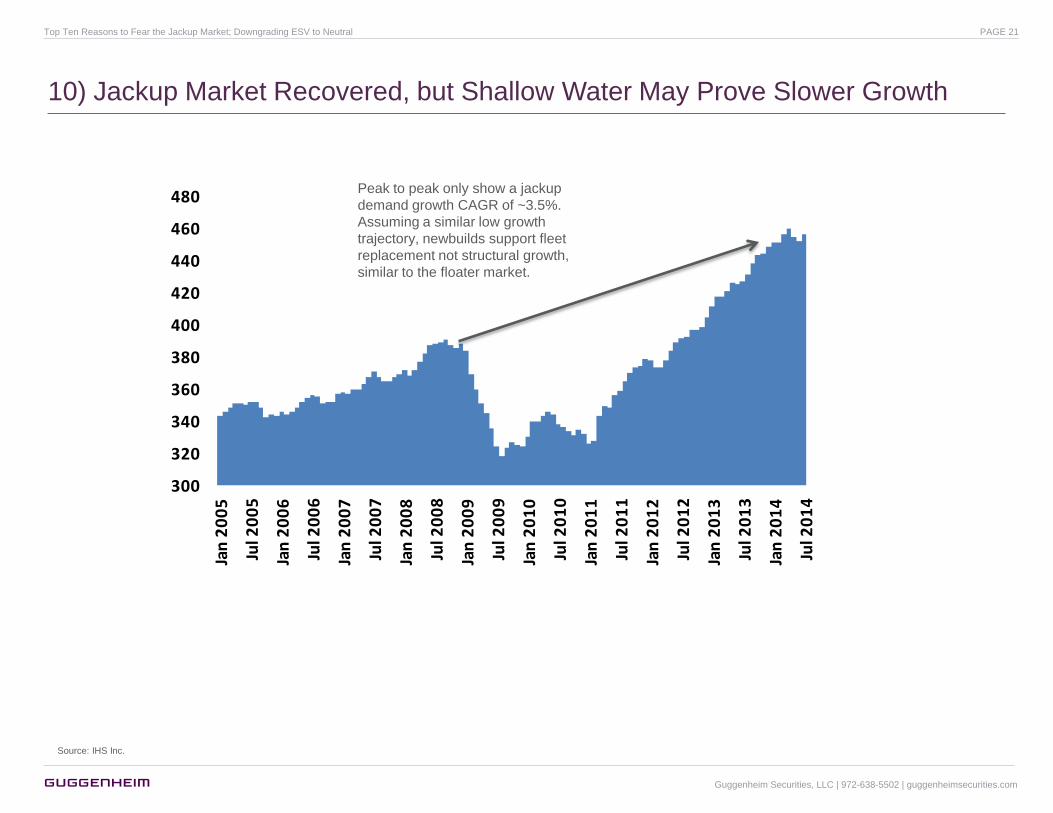

10) Shallow Water May Show Slower Activity Growth (pg. 21). A trend toward more complex plays and greater rig spec. requirements has fueled the rig replacement

cycle, not growth in the jackup market. Therefore, rig attrition, with all of the frictional factors discussed above, not market growth, must allow for new rig absorption.

Guggenheim Securities, LLC | 972-638-5502 | guggenheimsecurities.com

Top Ten Reasons to Fear the Jackup Market; Downgrading ESV to Neutral PAGE 2

Positive Leverage for Shares: Asset Concentration, Quality & Capital Strategies

Leveraged to a Turn in Fundamentals

SDRL – BUY – PT $50: Delivery of newbuilds &

accretive financing from SDLP (NC, $32.22) offers

upside leverage to distributions and yield-based

valuations. The recent SDLP unit issuance near 6-7%

yields & NADL/Rosneft deal remain positive indicators.

RIG – BUY – PT $55: Meaningful discount to NAV

leaves hope that activist involvement and reformulated

Board of Directors, with renewed dividend policy and

MLP plans, may lead to a transformation of the

company

ATW – BUY – PT $62: Attractive growth profile, solid

execution, and potential for future payout-friendly bias.

PACD – BUY – PT $14: Good management, pure-play

ultra-deepwater assets, recent favorable refinancing,

and longer-term dividend bias offer meaningful upside

potential.

DO – BUY – PT $65: Overly slighted for its older fleet,

we like DO’s high payout strategy. We see a more

positive outlook for the rig markets removing the

overhang created by risks to DO’s older fleet.

NE – BUY – PT $42: Potential for further upside on

spin-off of older asset, as investors give the company a

“fresh look” as the transaction provides a positive

catalyst.

Trapped in Multiple Compression

ESV – NEUTRAL – PT $58: We are concerned that

jackup exposure may overhang shares. There

remains an opportunity for upside with an emerging

track record for its distribution policy, which may

include dividends and share repurchases.

RDC – NEUTRAL – PT $36: Trading closer to NAV,

we see potential for continued multiple compression

as investors infer higher capital budgeting risk , with

the need for scale in its floater fleet or a payout

strategy to give better leverage to its cash flow

profile. Meanwhile, leverage to the jackup market

may create downside for the shares.

HERO – NEUTRAL – PT $4.50: Peak-cycle

economics and stretched balance sheet create a

challenging risk/reward, despite solid execution on

recent newbuilds and a good management team.

ATW & PACD: Attractive fleets and

cash flow profiles may see offsets in

slowed growth plans and more distant

term payout strategies.

NE: As we size the opportunities for

NE, post-spin, we will need to assess

jackup risk to the premium asset

company that remains.

ORIG: Concerns about unconventional

ownership and corporate structure may

challenge the story for the shares.

SDRL: Investors remain concerned about the

dividend amidst the downturn in dayrates.

Special Situations – Transaction/Catalyst-Driven

ORIG – BUY – PT $28: The need for cash and ORIG

shares as a source of funding at DRYS should prompt

a dividend strategy from ORIG and efforts to re-rate the

shares on yield-based metrics.

Guggenheim Securities, LLC | 972-638-5502 | guggenheimsecurities.com

Top Ten Reasons to Fear the Jackup Market; Downgrading ESV to Neutral PAGE 3

Large Cap Services 8.9 x

Large Cap Equipment 9.9 x

Small/Mid Cap Svcs &

Equipment 10.5 x

Offshore Drilling 7.3 xOnshore Drilling

6.7 x

Engineering & Construction 8.1x

5.0 x

6.0 x

7.0 x

8.0 x

9.0 x

10.0 x

11.0 x

0% 5% 10% 15% 20% 25%

EV

/EB

ITD

A '14E

EBITDA Growth, '14E vs. '13E

Large Cap Services 8.9 x

Large Cap Equipment 9.9 x

Small/Mid Cap Svcs &

Equipment 10.5 x

Offshore Drilling 7.3 x

Onshore Drilling 6.7 x

Engineering & Construction 8.7

x

5.5 x

6.5 x

7.5 x

8.5 x

9.5 x

10.5 x

11.5 x

10.0 x 12.0 x 14.0 x 16.0 x 18.0 x 20.0 x 22.0 x

EV

/EB

ITD

A '14E

Price/Earnings '14E

NAVs & Relative Valuation Leave Offshore Driller Shares Screening Attractively

Source: IHS Inc. Thomson Reuters, Guggenheim

Securities, LLC

Implied Growth for Equipment and E&C names

not translating for Offshore Drillers, despite

common drivers.

Offshore Drillers Least Expensive Sub-Sector Drillers Screen Cheap vs. Growth

PX NAV-B/U NAV-R P/NAV-B/U P/NAV-R

Company Rating 7/15 Target PX

Rtn to

Target

2014

PE

2015

PE

2014

EV/EBITDA

2015

EV/EBITDA

EV/EBITDA

'14

EV/EBITDA

'15 2014E 2014E 2014E 2014E

ATW Buy 50.66$ $62 22% 12.9x 8.9x 10.6x 7.3x 7.8x 5.6x 61 69 83% 73%

DO Buy 49.34$ $65 32% 16.3x 11.6x 12.3x 8.8x 5.4x 4.0x 59 60 84% 82%

ESV Neutral 54.56$ $58 6% 10.6x 9.7x 10.0x 9.1x 7.1x 6.3x 58 64 94% 85%

HERO Neutral 4.04$ $4.50 11% 9.8x 90.0x 8.8x 80.8x 5.0x 6.3x 4.5 5 90% 81%

NE Buy 32.28$ $42 30% 11.4x 10.8x 8.7x 8.3x 5.4x 5.0x 42 42 77% 77%

ORIG Buy 18.39$ $28 52% 14.0x 10.0x 9.2x 6.6x 7.0x 6.1x 27 28 68% 66%

PACD Buy 10.42$ $14 34% 14.7x 11.2x 11.0x 8.3x 8.1x 5.9x 14 14 74% 74%

RDC Neutral 31.71$ $36 14% 13.8x 7.6x 12.2x 6.7x 7.1x 4.8x 35 42 91% 75%

RIG Buy 43.61$ $55 26% 11.7x 13.6x 9.3x 10.8x 6.2x 6.7x 55 55 79% 79%

SDRL Buy 38.38$ $50 30% 15.9x 16.1x 12.2x 12.4x 9.5x 9.1x 28 33 137% 116%

Averages 10.4x 15.9x 6.9x 6.0x 88% 81%

Target Current

Guggenheim Securities, LLC | 972-638-5502 | guggenheimsecurities.com

Top Ten Reasons to Fear the Jackup Market; Downgrading ESV to Neutral PAGE 4

Wary of Fleet Value & Cash Flow at Risk From Jackup Exposure

Source: IHS Inc. Thomson Reuters, Guggenheim

Securities, LLC

Offshore drillers trade at a significant discount to NAV, suggesting a favorable

risk/reward

Gross Fleet Value Breakdown Estimated EBITDA Breakdown, 2015

We are gravitating away from offshore drillers that

derive too much cash flow and marked-to-market fleet

value from jackups in an effort to avoid potential

volatility.

Ticker Jackups 2G 3G 4G 5G 6G Other

ATW 15% 0% 1% 9% 0% 75% 0%

DO 4% 5% 6% 16% 17% 53% 0%

ESV 34% 0% 1% 10% 20% 35% 1%

HERO 75% 0% 0% 0% 0% 0% 25%

NE 10% 0% 17% 19% 16% 37% 0%

ORIG 0% 0% 0% 0% 11% 89% 0%

PACD 0% 0% 0% 0% 0% 100% 0%

RDC 60% 0% 0% 0% 0% 40% 0%

RIG 11% 2% 6% 5% 23% 53% 0%

SDRL 24% 0% 0% 1% 3% 72% 0%

TOTAL 17% 1% 7% 9% 13% 52% 0%

Ticker Jackups 2G 3G 4G 5G 6G Other

ATW 15% 0% 3% 19% 0% 63% 0%

DO 5% 15% 18% 19% 21% 22% 0%

ESV 28% 0% 2% 14% 19% 35% 2%

HERO 69% 0% 0% 0% 0% 0% 31%

NE 38% 0% 13% 9% 11% 29% 0%

ORIG 0% 0% 0% 0% 21% 79% 0%

PACD 0% 0% 0% 0% 0% 100% 0%

RDC 64% 0% 0% 0% 0% 36% 0%

RIG 8% 3% 11% 11% 31% 36% 0%

SDRL 24% 0% 0% 3% 3% 70% 0%

TOTAL 22% 2% 6% 9% 15% 46% 1%

Guggenheim Securities, LLC | 972-638-5502 | guggenheimsecurities.com

Top Ten Reasons to Fear the Jackup Market; Downgrading ESV to Neutral PAGE 5

DOHERO

NE - Legacy

ESV

RDC

RIG

ATW

SDRL

PRGN

NE -New Co.

-

5

10

15

20

25

30

35

40

0%

5%

10

%

15

%

20

%

25

%

30

%

35

%

40

%

45

%

50

%

55

%

60

%

65

%

70

%

75

%

80

%

Ave

rage

Jac

kup

Age

Jackups - % Fleet Value

DOHERO

NE - Legacy

ESV

RDC

RIG

ATW SDRL

PRGN

NE -New Co.

-

5

10

15

20

25

30

35

40

0%

5%

10

%

15

%

20

%

25

%

30

%

35

%

40

%

45

%

50

%

55

%

60

%

65

%

70

%

75

%

80

%

85

%

Ave

rage

Jac

kup

Age

2015 EBITDA Contribution

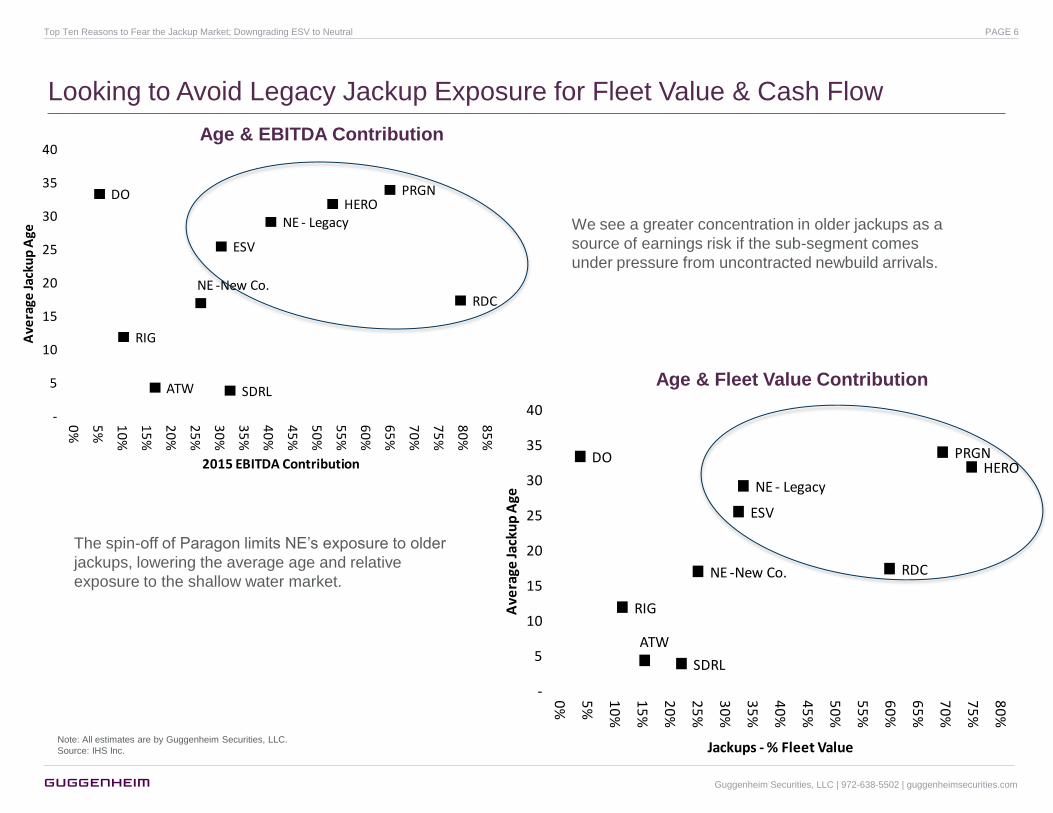

Looking to Avoid Legacy Jackup Exposure for Fleet Value & Cash Flow

Age & EBITDA Contribution

Age & Fleet Value Contribution

We see a greater concentration in older jackups as a

source of earnings risk if the sub-segment comes

under pressure from uncontracted newbuild arrivals.

The spin-off of Paragon limits NE’s exposure to older

jackups, lowering the average age and relative

exposure to the shallow water market.

Note: All estimates are by Guggenheim Securities, LLC.

Source: IHS Inc.

Guggenheim Securities, LLC | 972-638-5502 | guggenheimsecurities.com

Top Ten Reasons to Fear the Jackup Market; Downgrading ESV to Neutral PAGE 6

1) Uncontracted Jackup Deliveries Threatens Sentiment & Orderly Markets

Note: All estimates are by Guggenheim Securities, LLC.

Source: IHS Inc.

Jackup Newbuild Projections

Jackup Fleet Growth Projections

By our estimation, ~20% of the jackup

fleet that will exist (without retirements) at

the end of 2016 is represented by

uncontracted supply coming to market.

4 3 2 1 4 - - - - 2 1 1 1 - - - - - - -1

11 6 7

13

6 19 19 15

5 6 5

4 - 1 - - - - -

1

12

18

25

38

44

63

82

97 102

108 113

117 117 118 118 118 118 118 118

-

20

40

60

80

100

120

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

Nu

mb

er

of

Rig

s

Contracted Uncontracted Cumulative Uncontracted

95 96 96 96 96

180 181 181 181 181

173 198

243 255 257

48 53

70 82 82

496 527

590 614 616

-

100

200

300

400

500

600

700

2014E 2015E 2016E 2017E 2018E

Pro

jecte

d T

ota

l R

ig S

up

ply

Commodity Standard Premium Harsh Environment

Less than 40% of newbuid jackups

coming to market have been ordered by

traditional jackup market participants.

The presence of speculators, some from

financial players and others from

shipyards themselves, only increase the

possibility for disorderly market

absorption to fleet additions. The added

scramble for financing may only

exacerbate strains on smaller, new

market participants.

Guggenheim Securities, LLC | 972-638-5502 | guggenheimsecurities.com

Top Ten Reasons to Fear the Jackup Market; Downgrading ESV to Neutral PAGE 7

-

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

Jan

-03

Ju

n-0

3

No

v-0

3

Ap

r-04

Sep

-04

Feb

-05

Ju

l-05

Dec-0

5

May-0

6

Oct-

06

Mar-

07

Au

g-0

7

Jan

-08

Ju

n-0

8

No

v-0

8

Ap

r-09

Sep

-09

Feb

-10

Ju

l-10

Dec-1

0

May-1

1

Oct-

11

Mar-

12

Au

g-1

2

Jan

-13

Ju

n-1

3

No

v-1

3

Co

ntr

act

Du

raq

tio

n (

years

)

Jackup - Rolling 6-Month Avg.

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Mar-

03

Au

g-0

3

Jan

-04

Ju

n-0

4

No

v-0

4

Ap

r-05

Sep

-05

Feb

-06

Ju

l-06

Dec-0

6

May-0

7

Oct-

07

Mar-

08

Au

g-0

8

Jan

-09

Ju

n-0

9

No

v-0

9

Ap

r-10

Sep

-10

Feb

-11

Ju

l-11

Dec-1

1

May-1

2

Oct-

12

Mar-

13

Au

g-1

3

Jan

-14

Co

ntr

act

Du

rati

on

(years

)

Drillship - Rolling 6-Month Avg.

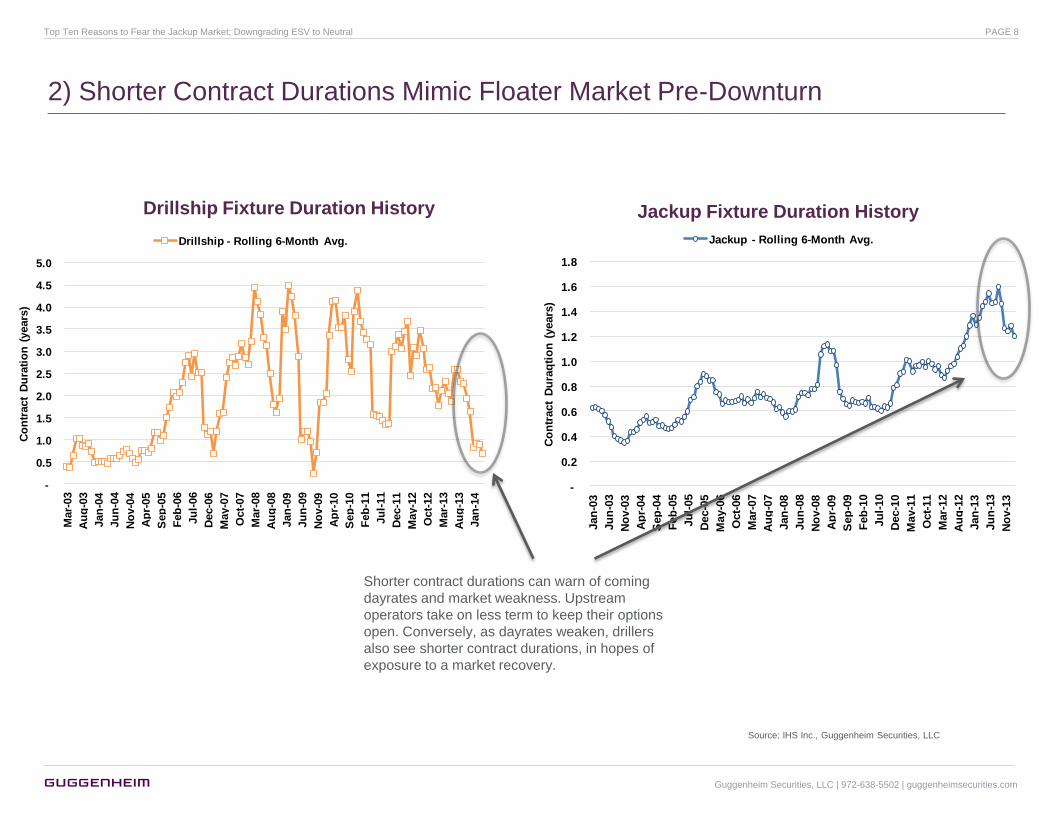

2) Shorter Contract Durations Mimic Floater Market Pre-Downturn

Drillship Fixture Duration History Jackup Fixture Duration History

Shorter contract durations can warn of coming

dayrates and market weakness. Upstream

operators take on less term to keep their options

open. Conversely, as dayrates weaken, drillers

also see shorter contract durations, in hopes of

exposure to a market recovery.

Source: IHS Inc., Guggenheim Securities, LLC

Guggenheim Securities, LLC | 972-638-5502 | guggenheimsecurities.com

Top Ten Reasons to Fear the Jackup Market; Downgrading ESV to Neutral PAGE 8

3) Jackup Tenders Provide Limited Demand Visibility Through 2015

10

34 40 45 45 45 42 38 39 36 7

18 21

26 21 22 21

18 16 13

13

23

28 24 29 33

27 27 28

24

11

31

38 35 37 33

36 35 31

28

-

20

40

60

80

100

120

140

3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16

Nu

mb

er

of

Rig

s

Tender Pre-tender Probable PossibleTender activity does not account for the

300+ jackups that will come available by the

end of 2015.

Source: IHS Inc., Guggenheim Securities, LLC

Guggenheim Securities, LLC | 972-638-5502 | guggenheimsecurities.com

Top Ten Reasons to Fear the Jackup Market; Downgrading ESV to Neutral PAGE 9

3) “Risked” Tenders Do Not Reflect a Tight High End of the Market

Tender Demand Segmented for High End of Jackup Market

Given that tenders target higher-end jackups, we

segmented market availability only looking at rigs

rated above 300ft water depth, 2,000 ton+ variable

deck loads, 18k+ drilling depths, 15k+ BOP psi ratings,

and hook load capacities above 1.5m lbs.

Historically, the jackup market has

operated as a “spot” market, with

tendering activity only prevalent for the

high end of the rig market.

Probability-weighted

demand looks to better

gauge actual demand from

an extensive project

inventory.

Note: All estimates are by Guggenheim Securities, LLC.

Source: IHS Inc., Guggenheim Securities, LLC

Jackups

2014E 2015E

Exploration 16 19

Appraisal 1 -

Development 16 27

Other 1 1

Tender 34 47

Exploration 7 10

Appraisal 1 -

Development 9 14

Other 1 2

Pre-Tender 18 26

Firm Demand 52 73

Exploration (25-50% Probability) 3 7

Appraisal (25-50% Probability) 1 2

Development (25-50% Probability) 3 13

Other - 1

Probable 7 23

Exploration (25% Probability) - 7

Appraisal (25% Probability) - 1

Development (25% Probability) - 5

Other 2 3

Possible 2 16

Potential Demand 9 39

Total Availability 70 131

Total Availability 70 131

Less: Firm Demand 52 73

Less: Carried Demand - -

Surplus/(Deficit), Firm & Adjusted 18 58

Adjusted Potential Demand 9 39

Surplus/(Deficit), Firm & Adjusted 9 19

Tender analysis shows a rig

surplus.

Guggenheim Securities, LLC | 972-638-5502 | guggenheimsecurities.com

Top Ten Reasons to Fear the Jackup Market; Downgrading ESV to Neutral PAGE 10

4) Lower End Market Shows Signs of Fading Strength vs. High End

75%

80%

85%

90%

95%

100%

105%

25

30

35

40

45

50

Jan

20

05

Au

g 2

00

5

Mar

20

06

Oct

20

06

May

20

07

De

c 2

00

7

Jul 2

00

8

Feb

20

09

Sep

20

09

Ap

r 2

01

0

No

v 2

01

0

Jun

20

11

Jan

20

12

Au

g 2

01

2

Mar

20

13

Oct

20

13

May

20

14

Marketed Supply Contracted Utilization

75%

80%

85%

90%

95%

100%

105%

25

30

35

40

45

50

Jan

20

05

Au

g 2

00

5

Mar

20

06

Oct

20

06

May

20

07

De

c 2

00

7

Jul 2

00

8

Feb

20

09

Sep

20

09

Ap

r 2

01

0

No

v 2

01

0

Jun

20

11

Jan

20

12

Au

g 2

01

2

Mar

20

13

Oct

20

13

May

20

14

Marketed Supply Contracted Utilization

Premium/High End Market Harsh Environment Market

Standard Market Low End/Commodity Market

60%

65%

70%

75%

80%

85%

90%

95%

100%

60

70

80

90

100

110

120

Jan

20

05

Au

g 2

00

5

Mar

20

06

Oct

20

06

May

20

07

De

c 2

00

7

Jul 2

00

8

Feb

20

09

Sep

20

09

Ap

r 2

01

0

No

v 2

01

0

Jun

20

11

Jan

20

12

Au

g 2

01

2

Mar

20

13

Oct

20

13

May

20

14

Marketed Supply Contracted Utilization

75%

80%

85%

90%

95%

100%

105%

120

130

140

150

160

170

180

190

Jan

20

05

Au

g 2

00

5

Mar

20

06

Oct

20

06

May

20

07

De

c 2

00

7

Jul 2

00

8

Feb

20

09

Sep

20

09

Ap

r 2

01

0

No

v 2

01

0

Jun

20

11

Jan

20

12

Au

g 2

01

2

Mar

20

13

Oct

20

13

May

20

14

Marketed Supply Contracted Utilization

Source: IHS Inc.

Signs of rig attritions and

erosion of utilization

Utilization metrics start to

fade and suggest rig

competition

Guggenheim Securities, LLC | 972-638-5502 | guggenheimsecurities.com

Top Ten Reasons to Fear the Jackup Market; Downgrading ESV to Neutral PAGE 11

5) Low Contract Coverage for Marketed Jackup Fleet: A Negative Catalyst

147

338

456

77%

47%

28%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0

50

100

150

200

250

300

350

400

450

500

2014 2015 2016

Jack

up

Co

ntr

act

Cov

erag

e

Nu

mb

er o

f Jac

kup

s A

vaila

ble

Jackups Available Contract Coverage

Note: All estimates are by Guggenheim Securities, LLC.

Source: IHS Inc.

Guggenheim Securities, LLC | 972-638-5502 | guggenheimsecurities.com

Top Ten Reasons to Fear the Jackup Market; Downgrading ESV to Neutral PAGE 12

5) Jackup Contract Coverage Give Less Buffer Than for Floaters

Jackup Contract Coverage Floater Contract Coverage

12%

40%

39%

51%

45%

59%

73%

77%

36%

60%

70%

78%

82%

82%

91%

92%

0% 20% 40% 60% 80% 100%

HERO

DO

RDC

ESV

NE

RIG

SDRL

ATW

2014E 2015E

51%

45%

63%

54%

69%

83%

77%

73%

88%

75%

78%

82%

86%

90%

95%

95%

99%

100%

0% 20% 40% 60% 80% 100%

RIG

DO

ESV

PACD

NE

ATW

SDRL

ORIG

RDC

2014E 2015E

Note: All estimates are by Guggenheim Securities, LLC.

Source: IHS Inc.

Guggenheim Securities, LLC | 972-638-5502 | guggenheimsecurities.com

Top Ten Reasons to Fear the Jackup Market; Downgrading ESV to Neutral PAGE 13

6) Revised Dayrate Forecast Already Sees Jackup Weakness

Source: IHS Inc., Guggenheim Securities, LLC.

2Q14E 3Q14E 4Q14E 1Q15E 2Q15E 3Q15E 4Q15E 1Q16E 2Q16E 3Q16E 4Q16E 1Q17E 2Q17E 3Q17E 4Q17E 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19

6G HDHE 530 525 520 515 515 520 525 535 545 555 565 570 575 580 585 570 555 545 530 515 515 515 515

6G High 490 485 480 475 475 480 485 495 505 515 525 530 535 540 545 545 545 545 545 545 545 545 545

6G Low 460 455 450 445 445 450 455 465 475 485 495 500 505 510 515 510 505 505 500 495 495 495 495

5G HDHE 375 370 365 360 360 365 370 380 390 400 410 415 420 425 430 425 420 410 405 400 400 400 400

5G High 375 370 365 360 360 365 370 380 390 400 410 415 420 425 430 410 395 375 360 340 340 340 340

5G Low 350 345 340 335 335 340 345 355 365 375 385 390 395 400 405 385 360 340 315 295 295 295 295

4G HDHE 350 345 340 335 335 340 345 355 365 375 385 390 395 400 405 375 345 310 280 250 250 250 250

4G High 340 335 330 325 325 330 335 345 355 365 375 380 385 390 395 365 335 305 275 245 245 245 245

4G Low 325 320 315 310 310 315 320 330 340 350 360 365 370 375 380 345 310 275 240 205 205 205 205

3G HDHE 310 305 300 295 295 300 305 315 325 335 345 350 355 360 365 330 290 255 215 180 180 180 180

3G High 290 285 280 275 275 280 285 295 305 315 325 330 335 340 345 320 295 275 250 225 225 225 225

3G Low 260 255 250 245 245 250 255 265 275 285 295 300 305 310 315 285 255 230 200 170 170 170 170

HDHE JU 230 225 220 215 210 205 200 195 190 185 180 185 190 195 200 200 200 195 195 195 195 195 195

Prem JU 180 175 170 165 160 155 150 145 140 135 130 135 140 145 150 155 160 165 170 175 175 175 175

High End JU 160 155 150 145 140 135 130 125 120 115 110 115 120 125 130 130 130 125 125 125 125 125 125

Standard JU 130 125 120 115 110 105 100 95 90 85 80 85 90 95 100 100 95 95 90 90 90 90 90

Sub-Standard JU 100 95 90 85 80 75 70 65 60 55 50 55 60 65 70 75 80 85 90 95 95 95 95

Commodity JU 90 85 80 75 70 65 60 55 50 45 40 45 50 55 60 65 65 70 70 75 75 75 75

Legacy 70 65 60 55 50 45 40 40 40 40 40 45 50 55 60 65 70 80 85 90 90 90 90

Trough of Floater Dayrates Floater Market Recovery New Floater Cycle Upswing Normalized (9% Cost of

Capital Returns) Transition

Jackup Dayrates Decline as Newbuilds Arrive

Normalized (9% Cost of

Capital Returns) Transition Modest Dayrate

Recovery

We acknowledge the potential for a fade in dayrates

to become more severe if sentiment takes an

extreme turn.

Guggenheim Securities, LLC | 972-638-5502 | guggenheimsecurities.com

Top Ten Reasons to Fear the Jackup Market; Downgrading ESV to Neutral PAGE 14

20

30

40

50

60

70

80

90

100

110

120

130

140

150

160

170

180

190

200

210

20

30

40

50

60

70

80

90

100

110

120

130

140

150

160

170

180

190

200

210

Jan

-03

Ju

n-0

3

No

v-0

3

Ap

r-04

Sep

-04

Feb

-05

Ju

l-05

Dec-0

5

May-0

6

Oct-

06

Mar-

07

Au

g-0

7

Jan

-08

Ju

n-0

8

No

v-0

8

Ap

r-09

Sep

-09

Feb

-10

Ju

l-10

Dec-1

0

May-1

1

Oct-

11

Mar-

12

Au

g-1

2

Jan

-13

Ju

n-1

3

No

v-1

3

Ap

r-14

JU >300ft Avg. Dayrate JU Premium Avg. Fixture JU High End Avg. Fixture

7) Premium & Standard Jackup Fixtures May Offer False Security

Source: IHS Inc., Guggenheim Securities, LLC.

Jackup: Premium/High End Dayrate History

Jackup: Standard Dayrate History

25

50

75

100

125

150

175

200

225

25

50

75

100

125

150

175

200

225

Jan

-03

Ju

n-0

3

No

v-0

3

Ap

r-04

Sep

-04

Feb

-05

Ju

l-05

Dec-0

5

May-0

6

Oct-

06

Mar-

07

Au

g-0

7

Jan

-08

Ju

n-0

8

No

v-0

8

Ap

r-09

Sep

-09

Feb

-10

Ju

l-10

Dec-1

0

May-1

1

Oct-

11

Mar-

12

Au

g-1

2

Jan

-13

Ju

n-1

3

No

v-1

3

Ap

r-14

JU 300-IC Avg Dayrate JU Standard Avg. Fixture

Jackup fixtures continue to trend

above current dayrate averages.

Although there are few signs of

weakness, we see the optics of the

arrival of several uncontracted

newbuilds as an overhang on

dayrates in the near term. As a result,

we forecast a fade in average

dayrates over the near term.

Guggenheim Securities, LLC | 972-638-5502 | guggenheimsecurities.com

Top Ten Reasons to Fear the Jackup Market; Downgrading ESV to Neutral PAGE 15

7) Harsh Environment Jackups Also Present a Favorable Trend

Source: IHS Inc., Guggenheim Securities, LLC.

Jackup: Harsh-Standard Dayrate History

25

50

75

100

125

150

175

200

225

250

25

50

75

100

125

150

175

200

225

250 Jan

-03

Ju

n-0

3

No

v-0

3

Ap

r-04

Sep

-04

Feb

-05

Ju

l-05

Dec-0

5

May-0

6

Oct-

06

Mar-

07

Au

g-0

7

Jan

-08

Ju

n-0

8

No

v-0

8

Ap

r-09

Sep

-09

Feb

-10

Ju

l-10

Dec-1

0

May-1

1

Oct-

11

Mar-

12

Au

g-1

2

Jan

-13

Ju

n-1

3

No

v-1

3

Ap

r-14

JU Harsh Standard Avg Dayrate JU Harsh Standard Avg Fixture

Guggenheim Securities, LLC | 972-638-5502 | guggenheimsecurities.com

Top Ten Reasons to Fear the Jackup Market; Downgrading ESV to Neutral PAGE 16

0

2

4

6

8

10

12

14

16

19

53

19

54

19

55

19

56

19

57

19

58

19

59

19

60

19

61

19

62

19

63

19

64

19

65

19

66

19

67

19

68

19

69

19

70

19

71

19

72

19

73

19

74

19

75

19

76

19

77

19

78

19

79

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

# o

f R

igs

-

10

20

30

40

50

60

70

80

90

19

58

19

59

19

60

19

61

19

62

19

63

19

64

19

65

19

66

19

67

19

68

19

69

19

70

19

71

19

72

19

73

19

74

19

75

19

76

19

77

19

78

19

79

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

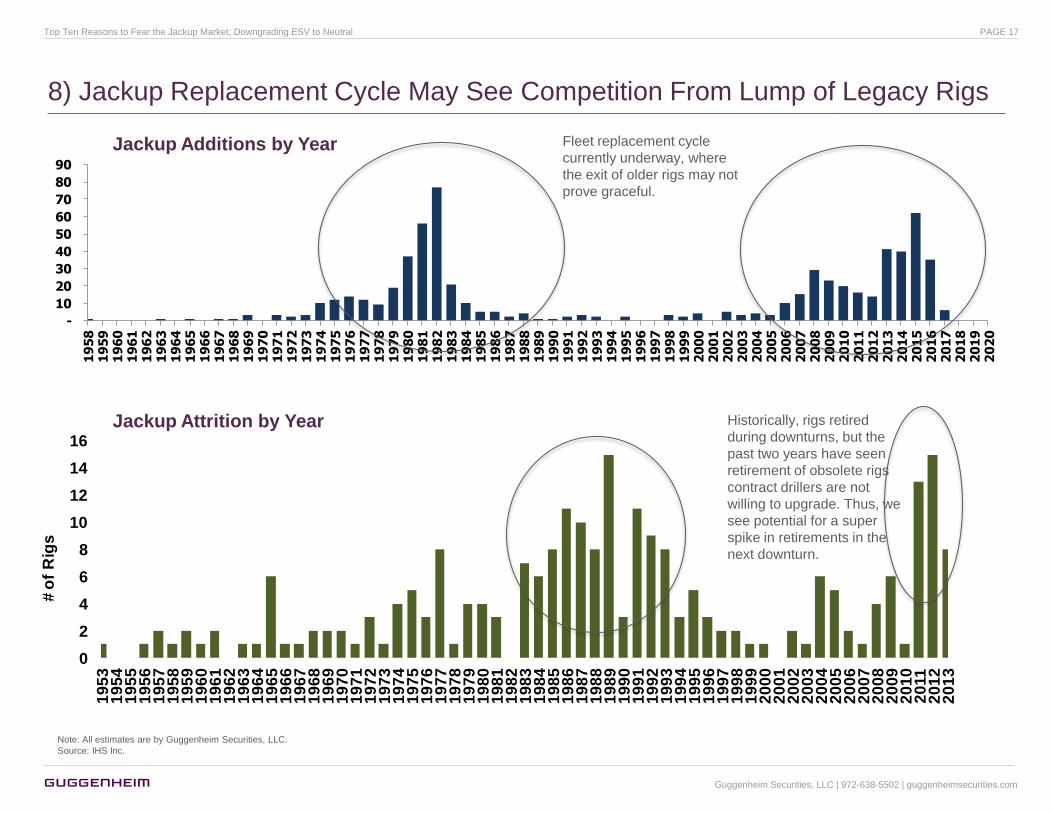

8) Jackup Replacement Cycle May See Competition From Lump of Legacy Rigs

Jackup Additions by Year

Jackup Attrition by Year

Fleet replacement cycle

currently underway, where

the exit of older rigs may not

prove graceful.

Historically, rigs retired

during downturns, but the

past two years have seen

retirement of obsolete rigs

contract drillers are not

willing to upgrade. Thus, we

see potential for a super

spike in retirements in the

next downturn.

Note: All estimates are by Guggenheim Securities, LLC.

Source: IHS Inc.

Guggenheim Securities, LLC | 972-638-5502 | guggenheimsecurities.com

Top Ten Reasons to Fear the Jackup Market; Downgrading ESV to Neutral PAGE 17

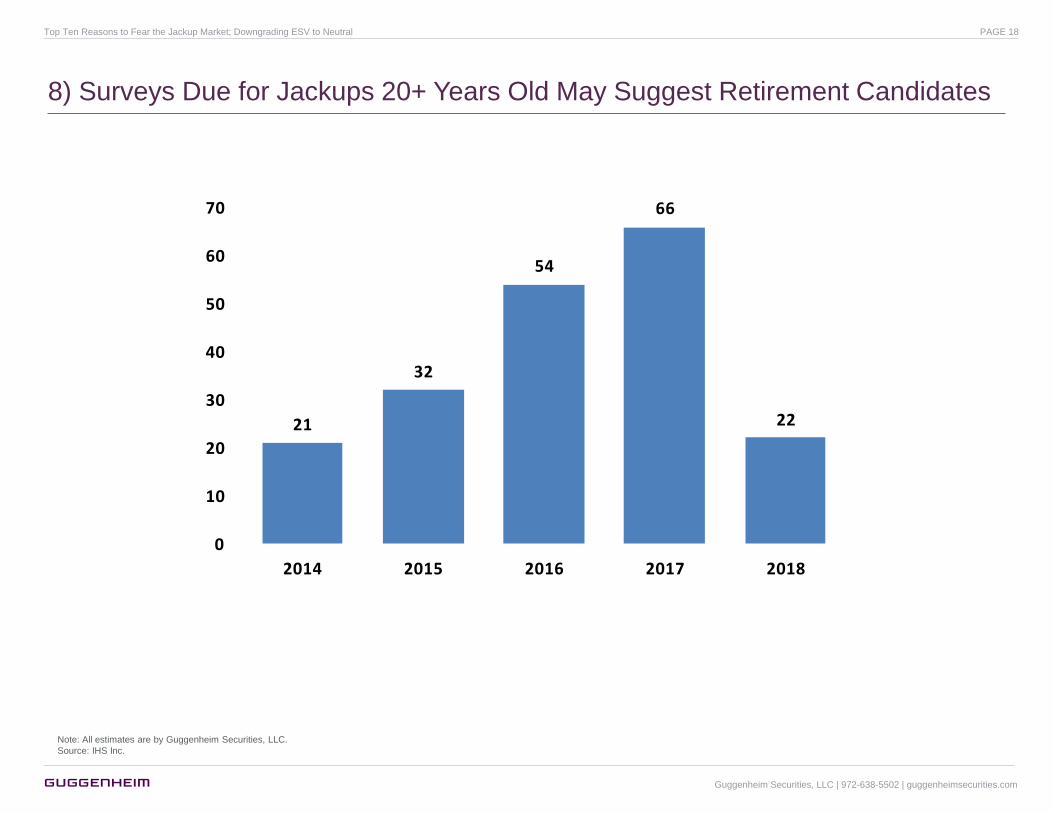

8) Surveys Due for Jackups 20+ Years Old May Suggest Retirement Candidates

21

32

54

66

22

0

10

20

30

40

50

60

70

2014 2015 2016 2017 2018

Note: All estimates are by Guggenheim Securities, LLC.

Source: IHS Inc.

Guggenheim Securities, LLC | 972-638-5502 | guggenheimsecurities.com

Top Ten Reasons to Fear the Jackup Market; Downgrading ESV to Neutral PAGE 18

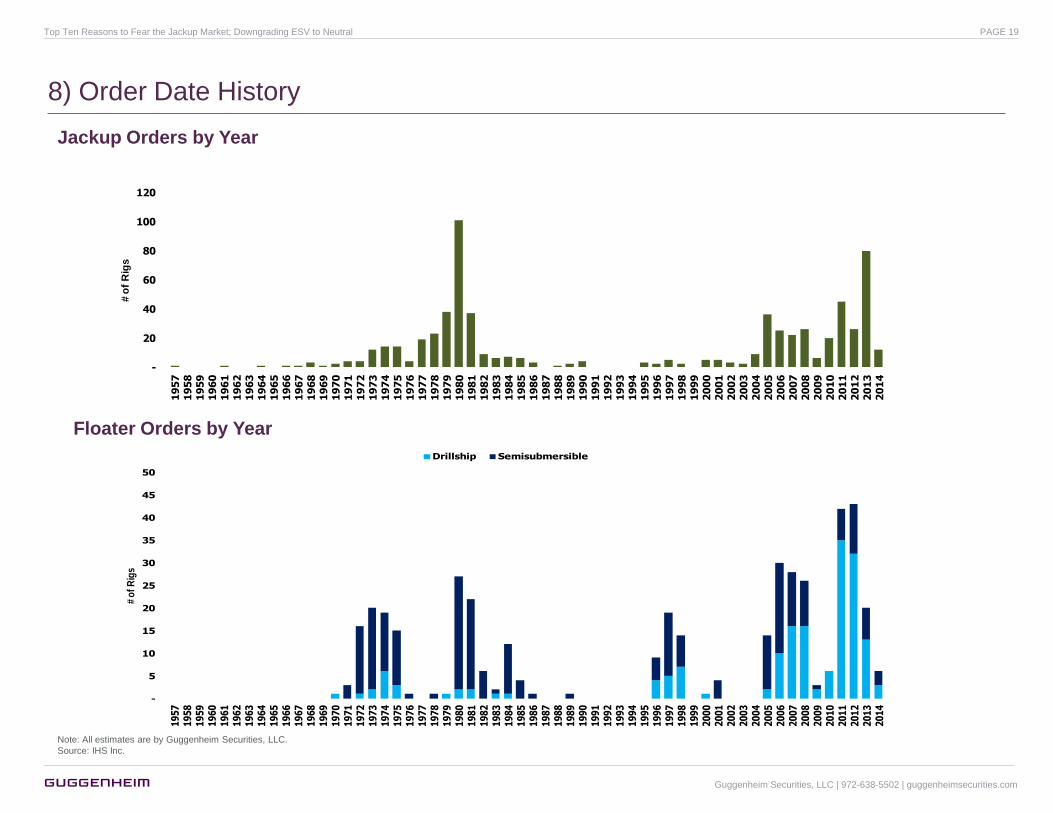

8) Order Date History

Jackup Orders by Year

Floater Orders by Year

-

20

40

60

80

100

120

19

57

19

58

19

59

19

60

19

61

19

62

19

63

19

64

19

65

19

66

19

67

19

68

19

69

19

70

19

71

19

72

19

73

19

74

19

75

19

76

19

77

19

78

19

79

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

# o

f R

igs

-

5

10

15

20

25

30

35

40

45

50

19

57

19

58

19

59

19

60

19

61

19

62

19

63

19

64

19

65

19

66

19

67

19

68

19

69

19

70

19

71

19

72

19

73

19

74

19

75

19

76

19

77

19

78

19

79

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

# o

f R

igs

Drillship Semisubmersible

Note: All estimates are by Guggenheim Securities, LLC.

Source: IHS Inc.

Guggenheim Securities, LLC | 972-638-5502 | guggenheimsecurities.com

Top Ten Reasons to Fear the Jackup Market; Downgrading ESV to Neutral PAGE 19

9) HERO Weakness May Be the “Canary in the Coal Mine”

$2.50

$3.00

$3.50

$4.00

$4.50

$5.00

$5.50

$6.00

$6.50

$7.00

$7.50

$8.00

$8.50

Jan

-12

Mar

-12

May

-12

Jul-

12

Sep

-12

No

v-1

2

Jan

-13

Mar

-13

May

-13

Jul-

13

Sep

-13

No

v-1

3

Jan

-14

Mar

-14

May

-14

Jul-

14

HERO shares declined ~50% since October 2013 vs. OSX up ~11%.

Source: Thomson Reuters

Recent weakness from the

marginal player with the

oldest assets & greatest

leverage to the health of

market balances may prove

an important warning for

competition in the jackup

market.

Guggenheim Securities, LLC | 972-638-5502 | guggenheimsecurities.com

Top Ten Reasons to Fear the Jackup Market; Downgrading ESV to Neutral PAGE 20

10) Jackup Market Recovered, but Shallow Water May Prove Slower Growth

300

320

340

360

380

400

420

440

460

480

Jan

20

05

Jul 2

00

5

Jan

20

06

Jul 2

00

6

Jan

20

07

Jul 2

00

7

Jan

20

08

Jul 2

00

8

Jan

20

09

Jul 2

00

9

Jan

20

10

Jul 2

01

0

Jan

20

11

Jul 2

01

1

Jan

20

12

Jul 2

01

2

Jan

20

13

Jul 2

01

3

Jan

20

14

Jul 2

01

4

Source: IHS Inc.

Peak to peak only show a jackup

demand growth CAGR of ~3.5%.

Assuming a similar low growth

trajectory, newbuilds support fleet

replacement not structural growth,

similar to the floater market.

Guggenheim Securities, LLC | 972-638-5502 | guggenheimsecurities.com

Top Ten Reasons to Fear the Jackup Market; Downgrading ESV to Neutral PAGE 21

Valuation & EPS Comp Sheets

Guggenheim Securities, LLC | 972-638-5502 | guggenheimsecurities.com

Top Ten Reasons to Fear the Jackup Market; Downgrading ESV to Neutral PAGE 22

NADL 9.2%

OII 2.5%

SDLP, 6.8%

DO, 7.1%

ESV, 5.5%

NE, 4.7%

ORIG, 4.1%

RDC, 1.3%

RIG, 6.9%

SDRL, 10.4%

CRR, 0.8%

SPN, 6.8%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

12.0%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Div

iden

d Y

ield

(L

ate

st

Qu

art

er

An

nu

ali

zed

)

DPS/CEPS 2Q14E (annulaized)

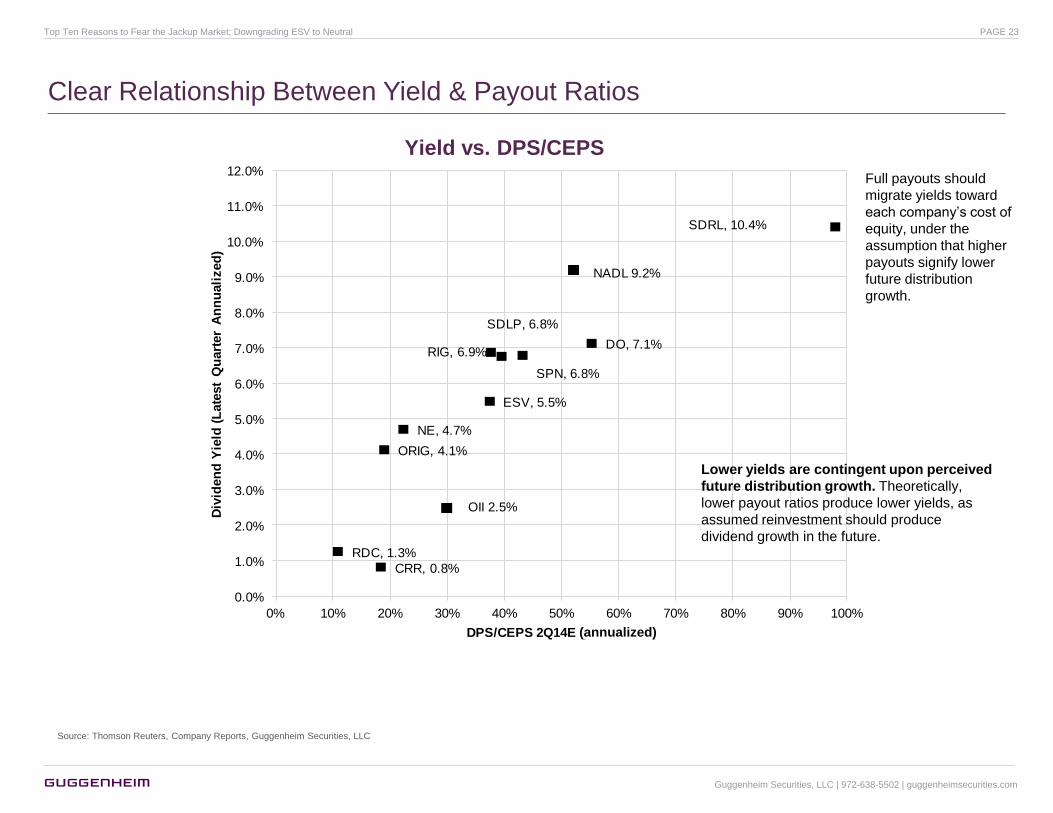

Clear Relationship Between Yield & Payout Ratios

Yield vs. DPS/CEPS

Source: Thomson Reuters, Company Reports, Guggenheim Securities, LLC

Full payouts should

migrate yields toward

each company’s cost of

equity, under the

assumption that higher

payouts signify lower

future distribution

growth.

Lower yields are contingent upon perceived

future distribution growth. Theoretically,

lower payout ratios produce lower yields, as

assumed reinvestment should produce

dividend growth in the future.

(annualized)

Guggenheim Securities, LLC | 972-638-5502 | guggenheimsecurities.com

Top Ten Reasons to Fear the Jackup Market; Downgrading ESV to Neutral PAGE 23

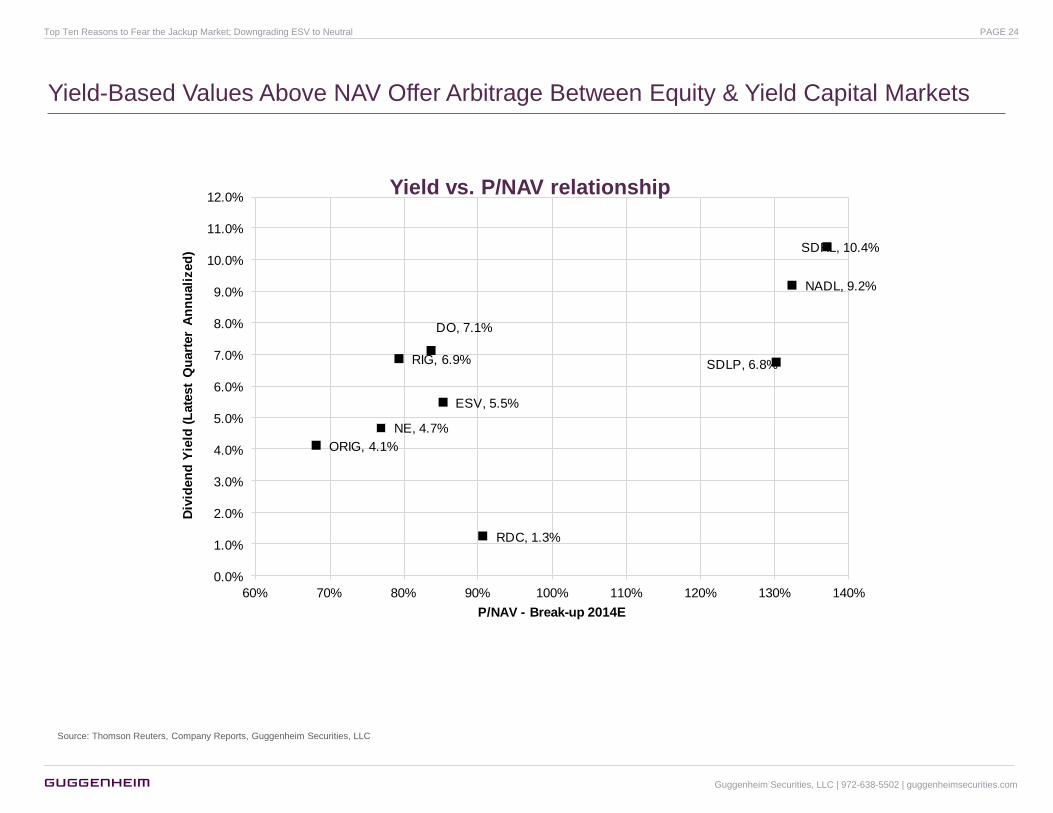

DO, 7.1%

ESV, 5.5%

NE, 4.7%

ORIG, 4.1%

RDC, 1.3%

RIG, 6.9%

SDRL, 10.4%

NADL, 9.2%

SDLP, 6.8%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

12.0%

60% 70% 80% 90% 100% 110% 120% 130% 140%

Div

iden

d Y

ield

(L

ate

st

Qu

art

er

An

nu

ali

zed

)

P/NAV - Break-up 2013E

Yield-Based Values Above NAV Offer Arbitrage Between Equity & Yield Capital Markets

Yield vs. P/NAV relationship

Source: Thomson Reuters, Company Reports, Guggenheim Securities, LLC

2014E

Guggenheim Securities, LLC | 972-638-5502 | guggenheimsecurities.com

Top Ten Reasons to Fear the Jackup Market; Downgrading ESV to Neutral PAGE 24

OFS Earnings Metrics

Source: Thomson Reuters, Guggenheim Securities, LLC

Price Gugg EPS PE Consensus EPS EPS Variance

Company Ticker Rating 7/15 Target Upside P/NAV* 2Q14E 13 14E 15E 13 14E 15E 2Q14E 14E 15E 2Q14E 14E 15E

S&P 500 SPX 1,973 13.5 16.8 15.5 117.32 127.11

Large Cap Services

Baker Hughes BHI Neutral 72.82 75 3% NA 0.89 2.69 4.05 5.15 27.1 18.0 14.1 0.90 4.17 5.40 -1% -3% -5%

Halliburton HAL Neutral 70.26 75 7% NA 0.90 3.15 3.95 5.05 22.3 17.8 13.9 0.91 3.99 5.16 -2% -1% -2%

Schlumberger SLB Buy 114.46 130 14% NA 1.35 4.79 5.65 6.75 23.9 20.3 17.0 1.36 5.70 6.81 0% -1% -1%

Weatherford WFT Neutral 22.17 18 -19% NA 0.21 0.60 1.10 1.50 37.0 20.2 14.8 0.21 1.08 1.68 0% 2% -11%8.54

Mean 27.6 19.0 14.9

Large Cap Equipment

Cameron CAM Buy 68.08 75 10% NA 0.85 3.28 3.90 5.00 20.8 17.5 13.6 0.87 3.92 4.89 -3% -1% 2%

FMC Tech FTI Buy 60.28 75 24% NA 0.63 2.11 2.70 3.40 28.6 22.3 17.7 0.63 2.70 3.34 0% 0% 2%

Nat Oil Varco NOV Buy 83.88 100 19% NA 1.47 5.52 6.05 6.60 15.2 13.9 12.7 1.44 6.00 6.71 2% 1% -2%

Tenaris TS Buy 45.10 65 44% NA 0.70 2.62 2.80 4.05 17.2 16.1 11.1 0.70 2.80 3.10 -1% 0% 31%

Mean 20.4 17.4 13.8

SMid Cap Svcs & Equipment

Aker Solutions AKSO Buy kr 94.35 kr 125 32% NA kr 1.41 kr 5.25 kr 5.80 kr 7.45 18.0 16.3 12.7 1.41 kr 6.09 kr 8.09 0% -5% -8%

C&J Energy Svcs CJES Neutral 32.43 32 -1% NA 0.24 1.21 1.20 2.15 26.8 27.0 15.1 0.26 1.20 2.21 -7% 0% -3%

Core Laboratories CLB Neutral 164.82 170 3% NA 1.34 5.32 5.85 6.30 31.0 28.2 26.2 1.34 5.88 6.62 0% 0% -5%

Carbo Ceramics CRR Neutral 146.09 165 13% NA 1.06 3.70 4.40 5.65 39.5 33.2 25.9 0.97 4.36 5.82 9% 1% -3%

Dresser-Rand DRC Neutral 60.30 67 11% NA 0.39 3.00 2.70 3.35 20.1 22.3 18.0 0.39 2.64 3.17 -1% 2% 6%

Dril-Quip DRQ Neutral 104.84 110 5% NA 1.15 4.23 4.85 5.90 24.8 21.6 17.8 1.15 4.95 6.06 0% -2% -3%

Forum Energy Tech FET Neutral 35.17 32 -9% NA 0.41 1.46 0.74 0.95 24.1 19.3 37.0 0.43 1.83 2.30 -4% -59% -59%

Frank's International FI Buy 23.11 30 30% NA 0.31 1.98 1.30 1.45 11.7 17.8 15.9 0.31 1.28 1.45 0% 2% 0%

Oceaneering OII Neutral 73.17 80 9% NA 1.01 3.40 4.00 4.55 21.5 18.3 16.1 1.01 4.04 4.69 0% -1% -3%

Oil States Int'l OIS Neutral 62.41 62 -1% NA 0.95 6.18 4.15 4.05 10.1 15.0 15.4 0.86 3.69 4.14 10% 13% -2%

Superior Energy Svcs SPN Neutral 35.89 34 -5% NA 0.39 1.56 1.50 2.25 23.0 21.1 16.0 0.41 1.70 2.44 -5% -12% -8%

U.S. Silica Holdings SLCA NC 55.97 NC - NA - - - - 38.1 28.6 20.0 0.46 1.96 2.80 - - -132% 39.91

Mean 24.0 22.4 19.7

Offshore Drilling

Atwood Oceanics* ATW Buy 50.66 62 22% 82% 1.13 5.32 4.80 6.95 9.5 10.6 7.3 1.07 4.99 7.20 6% -4% -4%

Diamond DO Buy 49.34 65 32% 84% 0.75 4.77 4.00 5.60 10.3 12.3 8.8 0.57 3.46 4.34 31% 16% 29%

Ensco plc ESV Neutral 54.56 58 6% 85% 1.30 6.16 5.46 6.00 8.9 10.0 9.1 1.33 5.58 5.77 -3% -2% 4%

Hercules Offshore HERO Neutral 4.04 4.50 11% 81% 0.08 0.24 0.46 0.05 16.8 8.8 80.8 0.02 0.38 0.49 433% 21% -90%

Noble Corp NE Buy 32.28 42 30% 77% 0.70 2.89 3.70 3.90 11.2 8.7 8.3 0.67 3.48 3.68 5% 6% 6%

Ocean Rig UDW ORIG Buy 18.39 28 52% 66% 0.47 0.84 2.00 2.80 21.9 9.2 6.6 0.39 1.66 2.21 21% 20% 27%

Pacific Drilling PACD Buy 9.99 14 40% 71% 0.21 0.42 0.95 1.25 23.8 10.5 8.0 0.18 0.78 1.26 14% 22% -1%

Rowan RDC Neutral 31.71 36 14% 88% 0.29 1.96 2.60 4.75 16.2 12.2 6.7 0.26 2.27 4.20 11% 15% 13%

Transocean RIG Buy 43.61 55 26% 79% 1.21 4.12 4.70 4.05 10.6 9.3 10.8 1.13 4.33 3.52 7% 9% 15%

Seadrill SDRL Buy 38.38 50 30% 132% 0.60 3.02 3.15 3.10 12.7 12.2 12.4 0.77 3.10 3.64 -22% 1% -15%

Mean 84% 12.0 10.5 18.0

Onshore Drilling

Helm & Payne* HP Neutral 112.93 110 -3% NA 1.61 5.67 6.25 6.80 19.9 18.1 16.6 1.63 6.33 7.25 -1% -1% -6%

Nabors NBR Neutral 28.44 28 -2% NA 0.22 1.02 1.15 1.80 27.9 24.7 15.8 0.35 1.16 1.98 -36% -1% -9%

Precision Drilling PDS NC 13.40 NC - NA - - - - 21.9 16.6 12.4 (0.00) 0.81 1.08 - - -

Patterson UTI PTEN Neutral 34.54 35 1% NA 0.32 1.16 1.40 1.80 29.8 24.7 19.2 0.32 1.42 2.02 2% -2% -11%

Mean 24.9 21.0 16.0

*Quarterly EPS figures for ATW and HP reflect calendar year reporting basis. NAV figures for Offshore Drilling companies are Break-Up NAVs. PDS estimates in CAD. All units in $m except per share data.

Guggenheim Securities, LLC | 972-638-5502 | guggenheimsecurities.com

Top Ten Reasons to Fear the Jackup Market; Downgrading ESV to Neutral PAGE 25

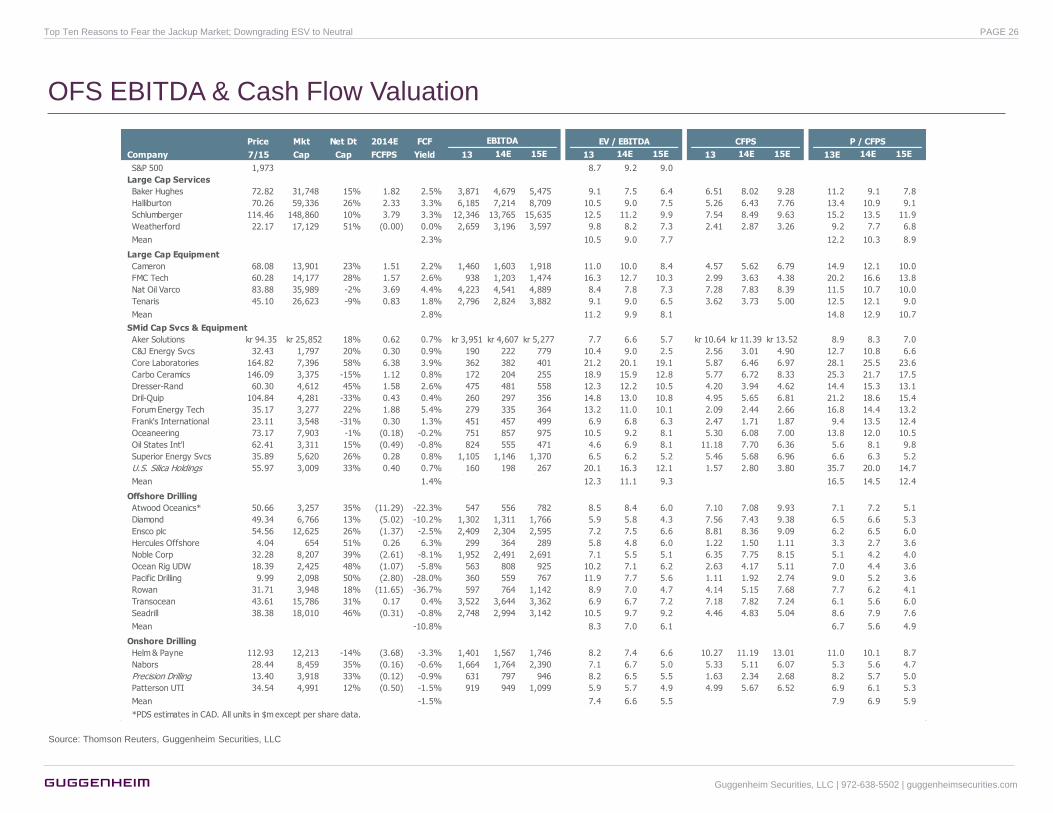

OFS EBITDA & Cash Flow Valuation

Source: Thomson Reuters, Guggenheim Securities, LLC

Price Mkt Net Dt 2014E FCF EBITDA EV / EBITDA CFPS P / CFPS

Company 7/15 Cap Cap FCFPS Yield 13 14E 15E 13 14E 15E 13 14E 15E 13E 14E 15E

S&P 500 1,973 8.7 9.2 9.0

Large Cap Services

Baker Hughes 72.82 31,748 15% 1.82 2.5% 3,871 4,679 5,475 9.1 7.5 6.4 6.51 8.02 9.28 11.2 9.1 7.8

Halliburton 70.26 59,336 26% 2.33 3.3% 6,185 7,214 8,709 10.5 9.0 7.5 5.26 6.43 7.76 13.4 10.9 9.1

Schlumberger 114.46 148,860 10% 3.79 3.3% 12,346 13,765 15,635 12.5 11.2 9.9 7.54 8.49 9.63 15.2 13.5 11.9

Weatherford 22.17 17,129 51% (0.00) 0.0% 2,659 3,196 3,597 9.8 8.2 7.3 2.41 2.87 3.26 9.2 7.7 6.8

Mean 2.3% 10.5 9.0 7.7 12.2 10.3 8.9

Large Cap Equipment

Cameron 68.08 13,901 23% 1.51 2.2% 1,460 1,603 1,918 11.0 10.0 8.4 4.57 5.62 6.79 14.9 12.1 10.0

FMC Tech 60.28 14,177 28% 1.57 2.6% 938 1,203 1,474 16.3 12.7 10.3 2.99 3.63 4.38 20.2 16.6 13.8

Nat Oil Varco 83.88 35,989 -2% 3.69 4.4% 4,223 4,541 4,889 8.4 7.8 7.3 7.28 7.83 8.39 11.5 10.7 10.0

Tenaris 45.10 26,623 -9% 0.83 1.8% 2,796 2,824 3,882 9.1 9.0 6.5 3.62 3.73 5.00 12.5 12.1 9.0

Mean 2.8% 11.2 9.9 8.1 14.8 12.9 10.7

SMid Cap Svcs & Equipment

Aker Solutions kr 94.35 kr 25,852 18% 0.62 0.7% kr 3,951 kr 4,607 kr 5,277 7.7 6.6 5.7 kr 10.64 kr 11.39 kr 13.52 8.9 8.3 7.0

C&J Energy Svcs 32.43 1,797 20% 0.30 0.9% 190 222 779 10.4 9.0 2.5 2.56 3.01 4.90 12.7 10.8 6.6

Core Laboratories 164.82 7,396 58% 6.38 3.9% 362 382 401 21.2 20.1 19.1 5.87 6.46 6.97 28.1 25.5 23.6

Carbo Ceramics 146.09 3,375 -15% 1.12 0.8% 172 204 255 18.9 15.9 12.8 5.77 6.72 8.33 25.3 21.7 17.5

Dresser-Rand 60.30 4,612 45% 1.58 2.6% 475 481 558 12.3 12.2 10.5 4.20 3.94 4.62 14.4 15.3 13.1

Dril-Quip 104.84 4,281 -33% 0.43 0.4% 260 297 356 14.8 13.0 10.8 4.95 5.65 6.81 21.2 18.6 15.4

Forum Energy Tech 35.17 3,277 22% 1.88 5.4% 279 335 364 13.2 11.0 10.1 2.09 2.44 2.66 16.8 14.4 13.2

Frank's International 23.11 3,548 -31% 0.30 1.3% 451 457 499 6.9 6.8 6.3 2.47 1.71 1.87 9.4 13.5 12.4

Oceaneering 73.17 7,903 -1% (0.18) -0.2% 751 857 975 10.5 9.2 8.1 5.30 6.08 7.00 13.8 12.0 10.5

Oil States Int'l 62.41 3,311 15% (0.49) -0.8% 824 555 471 4.6 6.9 8.1 11.18 7.70 6.36 5.6 8.1 9.8

Superior Energy Svcs 35.89 5,620 26% 0.28 0.8% 1,105 1,146 1,370 6.5 6.2 5.2 5.46 5.68 6.96 6.6 6.3 5.2

U.S. Silica Holdings 55.97 3,009 33% 0.40 0.7% 160 198 267 20.1 16.3 12.1 1.57 2.80 3.80 35.7 20.0 14.716,938 18,309 21,815 76 79 92

Mean 1.4% 12.3 11.1 9.3 16.5 14.5 12.4

Offshore Drilling

Atwood Oceanics* 50.66 3,257 35% (11.29) -22.3% 547 556 782 8.5 8.4 6.0 7.10 7.08 9.93 7.1 7.2 5.1

Diamond 49.34 6,766 13% (5.02) -10.2% 1,302 1,311 1,766 5.9 5.8 4.3 7.56 7.43 9.38 6.5 6.6 5.3

Ensco plc 54.56 12,625 26% (1.37) -2.5% 2,409 2,304 2,595 7.2 7.5 6.6 8.81 8.36 9.09 6.2 6.5 6.0

Hercules Offshore 4.04 654 51% 0.26 6.3% 299 364 289 5.8 4.8 6.0 1.22 1.50 1.11 3.3 2.7 3.6

Noble Corp 32.28 8,207 39% (2.61) -8.1% 1,952 2,491 2,691 7.1 5.5 5.1 6.35 7.75 8.15 5.1 4.2 4.0

Ocean Rig UDW 18.39 2,425 48% (1.07) -5.8% 563 808 925 10.2 7.1 6.2 2.63 4.17 5.11 7.0 4.4 3.6

Pacific Drilling 9.99 2,098 50% (2.80) -28.0% 360 559 767 11.9 7.7 5.6 1.11 1.92 2.74 9.0 5.2 3.6

Rowan 31.71 3,948 18% (11.65) -36.7% 597 764 1,142 8.9 7.0 4.7 4.14 5.15 7.68 7.7 6.2 4.1

Transocean 43.61 15,786 31% 0.17 0.4% 3,522 3,644 3,362 6.9 6.7 7.2 7.18 7.82 7.24 6.1 5.6 6.0

Seadrill 38.38 18,010 46% (0.31) -0.8% 2,748 2,994 3,142 10.5 9.7 9.2 4.46 4.83 5.04 8.6 7.9 7.6

Mean -10.8% 8.3 7.0 6.1 6.7 5.6 4.9

Onshore Drilling

Helm & Payne 112.93 12,213 -14% (3.68) -3.3% 1,401 1,567 1,746 8.2 7.4 6.6 10.27 11.19 13.01 11.0 10.1 8.7

Nabors 28.44 8,459 35% (0.16) -0.6% 1,664 1,764 2,390 7.1 6.7 5.0 5.33 5.11 6.07 5.3 5.6 4.7

Precision Drilling 13.40 3,918 33% (0.12) -0.9% 631 797 946 8.2 6.5 5.5 1.63 2.34 2.68 8.2 5.7 5.0

Patterson UTI 34.54 4,991 12% (0.50) -1.5% 919 949 1,099 5.9 5.7 4.9 4.99 5.67 6.52 6.9 6.1 5.3

Mean -1.5% 7.4 6.6 5.5 7.9 6.9 5.9

*PDS estimates in CAD. All units in $m except per share data.

Guggenheim Securities, LLC | 972-638-5502 | guggenheimsecurities.com

Top Ten Reasons to Fear the Jackup Market; Downgrading ESV to Neutral PAGE 26

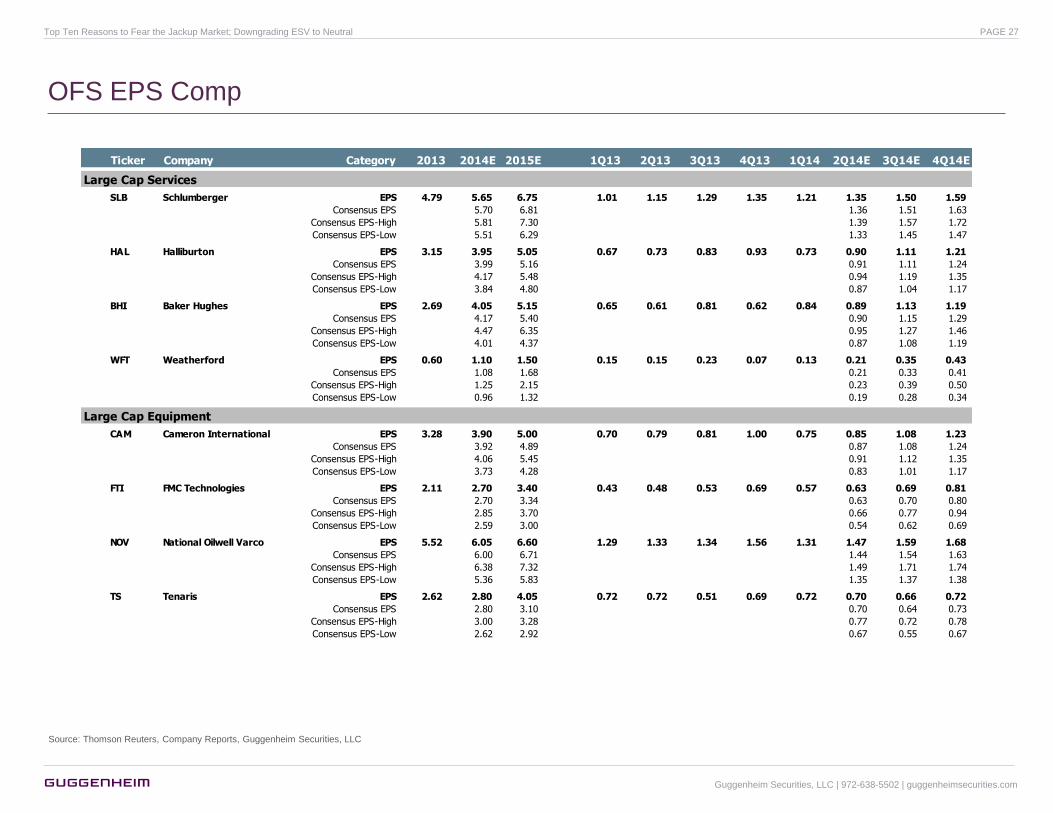

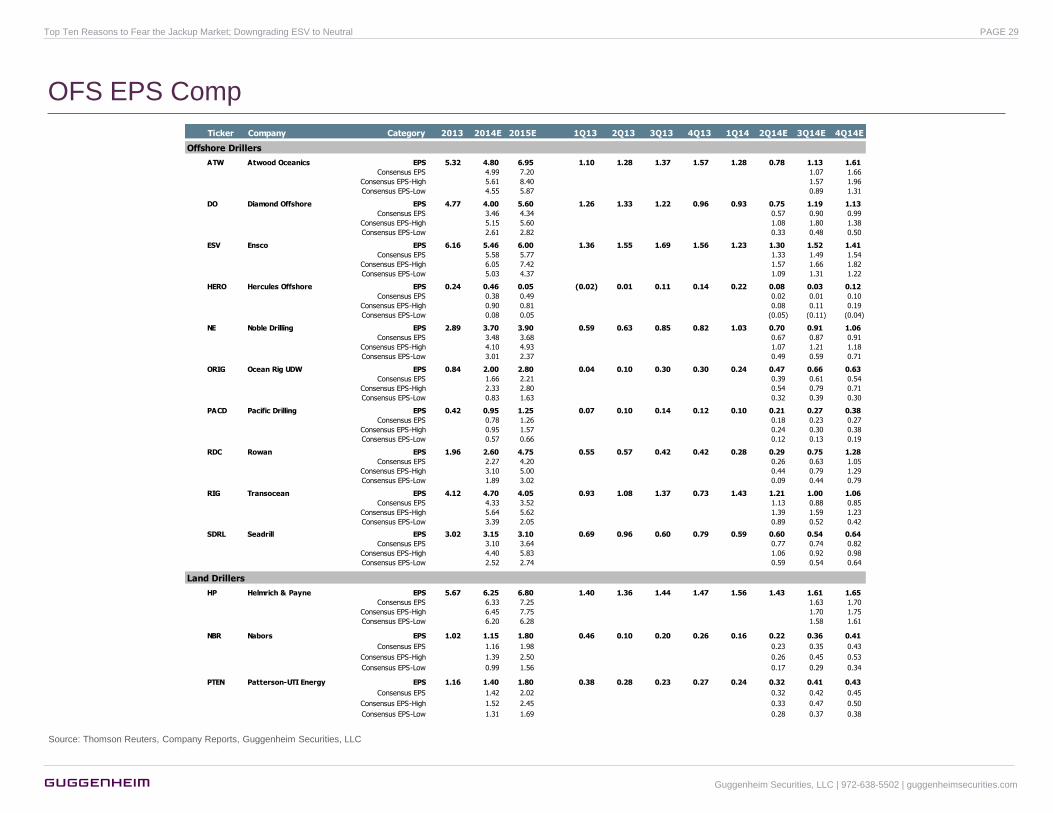

OFS EPS Comp

Source: Thomson Reuters, Company Reports, Guggenheim Securities, LLC

Ticker Company Category 2013 2014E 2015E 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14E 3Q14E 4Q14E

Large Cap Services

SLB Schlumberger EPS 4.79 5.65 6.75 1.01 1.15 1.29 1.35 1.21 1.35 1.50 1.59

Consensus EPS 5.70 6.81 1.36 1.51 1.63

Consensus EPS-High 5.81 7.30 1.39 1.57 1.72

Consensus EPS-Low 5.51 6.29 1.33 1.45 1.47

HAL Halliburton EPS 3.15 3.95 5.05 0.67 0.73 0.83 0.93 0.73 0.90 1.11 1.21

Consensus EPS 3.99 5.16 0.91 1.11 1.24

Consensus EPS-High 4.17 5.48 0.94 1.19 1.35

Consensus EPS-Low 3.84 4.80 0.87 1.04 1.17

BHI Baker Hughes EPS 2.69 4.05 5.15 0.65 0.61 0.81 0.62 0.84 0.89 1.13 1.19

Consensus EPS 4.17 5.40 0.90 1.15 1.29

Consensus EPS-High 4.47 6.35 0.95 1.27 1.46

Consensus EPS-Low 4.01 4.37 0.87 1.08 1.19

WFT Weatherford EPS 0.60 1.10 1.50 0.15 0.15 0.23 0.07 0.13 0.21 0.35 0.43

Consensus EPS 1.08 1.68 0.21 0.33 0.41

Consensus EPS-High 1.25 2.15 0.23 0.39 0.50

Consensus EPS-Low 0.96 1.32 0.19 0.28 0.34

Large Cap Equipment

CAM Cameron International EPS 3.28 3.90 5.00 0.70 0.79 0.81 1.00 0.75 0.85 1.08 1.23

Consensus EPS 3.92 4.89 0.87 1.08 1.24

Consensus EPS-High 4.06 5.45 0.91 1.12 1.35

Consensus EPS-Low 3.73 4.28 0.83 1.01 1.17

FTI FMC Technologies EPS 2.11 2.70 3.40 0.43 0.48 0.53 0.69 0.57 0.63 0.69 0.81

Consensus EPS 2.70 3.34 0.63 0.70 0.80

Consensus EPS-High 2.85 3.70 0.66 0.77 0.94

Consensus EPS-Low 2.59 3.00 0.54 0.62 0.69

NOV National Oilwell Varco EPS 5.52 6.05 6.60 1.29 1.33 1.34 1.56 1.31 1.47 1.59 1.68

Consensus EPS 6.00 6.71 1.44 1.54 1.63

Consensus EPS-High 6.38 7.32 1.49 1.71 1.74

Consensus EPS-Low 5.36 5.83 1.35 1.37 1.38

TS Tenaris EPS 2.62 2.80 4.05 0.72 0.72 0.51 0.69 0.72 0.70 0.66 0.72

Consensus EPS 2.80 3.10 0.70 0.64 0.73

Consensus EPS-High 3.00 3.28 0.77 0.72 0.78

Consensus EPS-Low 2.62 2.92 0.67 0.55 0.67

Guggenheim Securities, LLC | 972-638-5502 | guggenheimsecurities.com

Top Ten Reasons to Fear the Jackup Market; Downgrading ESV to Neutral PAGE 27

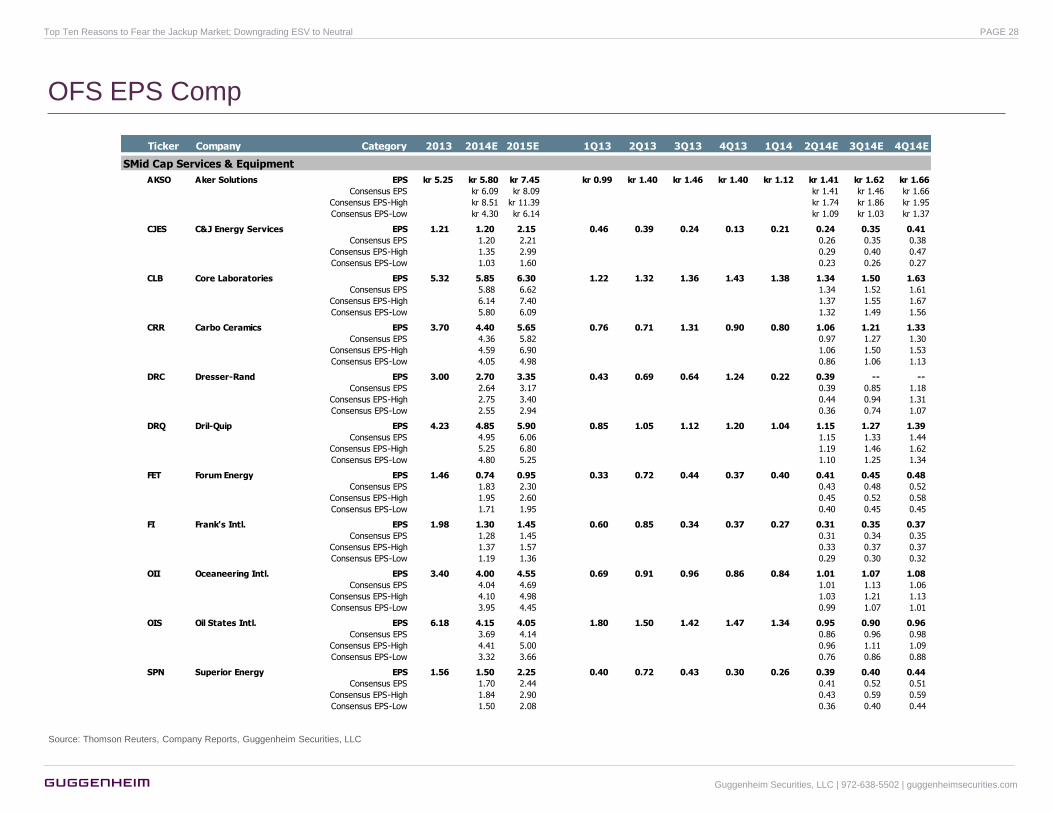

OFS EPS Comp

Source: Thomson Reuters, Company Reports, Guggenheim Securities, LLC

Ticker Company Category 2013 2014E 2015E 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14E 3Q14E 4Q14E

SMid Cap Services & Equipment

AKSO-NOAKSO Aker Solutions EPS kr 5.25 kr 5.80 kr 7.45 kr 0.99 kr 1.40 kr 1.46 kr 1.40 kr 1.12 kr 1.41 kr 1.62 kr 1.66

Consensus EPS kr 6.09 kr 8.09 kr 1.41 kr 1.46 kr 1.66

Consensus EPS-High kr 8.51 kr 11.39 kr 1.74 kr 1.86 kr 1.95

Consensus EPS-Low kr 4.30 kr 6.14 kr 1.09 kr 1.03 kr 1.37

CJES C&J Energy Services EPS 1.21 1.20 2.15 0.46 0.39 0.24 0.13 0.21 0.24 0.35 0.41

Consensus EPS 1.20 2.21 0.26 0.35 0.38

Consensus EPS-High 1.35 2.99 0.29 0.40 0.47

Consensus EPS-Low 1.03 1.60 0.23 0.26 0.27

CLB Core Laboratories EPS 5.32 5.85 6.30 1.22 1.32 1.36 1.43 1.38 1.34 1.50 1.63

Consensus EPS 5.88 6.62 1.34 1.52 1.61

Consensus EPS-High 6.14 7.40 1.37 1.55 1.67

Consensus EPS-Low 5.80 6.09 1.32 1.49 1.56

CRR Carbo Ceramics EPS 3.70 4.40 5.65 0.76 0.71 1.31 0.90 0.80 1.06 1.21 1.33

Consensus EPS 4.36 5.82 0.97 1.27 1.30

Consensus EPS-High 4.59 6.90 1.06 1.50 1.53

Consensus EPS-Low 4.05 4.98 0.86 1.06 1.13

DRC Dresser-Rand EPS 3.00 2.70 3.35 0.43 0.69 0.64 1.24 0.22 0.39 -- --

Consensus EPS 2.64 3.17 0.39 0.85 1.18

Consensus EPS-High 2.75 3.40 0.44 0.94 1.31

Consensus EPS-Low 2.55 2.94 0.36 0.74 1.07

DRQ Dril-Quip EPS 4.23 4.85 5.90 0.85 1.05 1.12 1.20 1.04 1.15 1.27 1.39

Consensus EPS 4.95 6.06 1.15 1.33 1.44

Consensus EPS-High 5.25 6.80 1.19 1.46 1.62

Consensus EPS-Low 4.80 5.25 1.10 1.25 1.34

FET Forum Energy EPS 1.46 0.74 0.95 0.33 0.72 0.44 0.37 0.40 0.41 0.45 0.48

Consensus EPS 1.83 2.30 0.43 0.48 0.52

Consensus EPS-High 1.95 2.60 0.45 0.52 0.58

Consensus EPS-Low 1.71 1.95 0.40 0.45 0.45

FI Frank's Intl. EPS 1.98 1.30 1.45 0.60 0.85 0.34 0.37 0.27 0.31 0.35 0.37

Consensus EPS 1.28 1.45 0.31 0.34 0.35

Consensus EPS-High 1.37 1.57 0.33 0.37 0.37

Consensus EPS-Low 1.19 1.36 0.29 0.30 0.32

OII Oceaneering Intl. EPS 3.40 4.00 4.55 0.69 0.91 0.96 0.86 0.84 1.01 1.07 1.08

Consensus EPS 4.04 4.69 1.01 1.13 1.06

Consensus EPS-High 4.10 4.98 1.03 1.21 1.13

Consensus EPS-Low 3.95 4.45 0.99 1.07 1.01

OIS Oil States Intl. EPS 6.18 4.15 4.05 1.80 1.50 1.42 1.47 1.34 0.95 0.90 0.96

Consensus EPS 3.69 4.14 0.86 0.96 0.98

Consensus EPS-High 4.41 5.00 0.96 1.11 1.09

Consensus EPS-Low 3.32 3.66 0.76 0.86 0.88

SPN Superior Energy EPS 1.56 1.50 2.25 0.40 0.72 0.43 0.30 0.26 0.39 0.40 0.44

Consensus EPS 1.70 2.44 0.41 0.52 0.51

Consensus EPS-High 1.84 2.90 0.43 0.59 0.59

Consensus EPS-Low 1.50 2.08 0.36 0.40 0.44

Guggenheim Securities, LLC | 972-638-5502 | guggenheimsecurities.com

Top Ten Reasons to Fear the Jackup Market; Downgrading ESV to Neutral PAGE 28

OFS EPS Comp

Source: Thomson Reuters, Company Reports, Guggenheim Securities, LLC

Ticker Company Category 2013 2014E 2015E 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14E 3Q14E 4Q14E

Offshore Drillers

ATW Atwood Oceanics EPS 5.32 4.80 6.95 1.10 1.28 1.37 1.57 1.28 0.78 1.13 1.61

Consensus EPS 4.99 7.20 1.07 1.66

Consensus EPS-High 5.61 8.40 1.57 1.96

Consensus EPS-Low 4.55 5.87 0.89 1.31

DO Diamond Offshore EPS 4.77 4.00 5.60 1.26 1.33 1.22 0.96 0.93 0.75 1.19 1.13

Consensus EPS 3.46 4.34 0.57 0.90 0.99

Consensus EPS-High 5.15 5.60 1.08 1.80 1.38

Consensus EPS-Low 2.61 2.82 0.33 0.48 0.50

ESV Ensco EPS 6.16 5.46 6.00 1.36 1.55 1.69 1.56 1.23 1.30 1.52 1.41

Consensus EPS 5.58 5.77 1.33 1.49 1.54

Consensus EPS-High 6.05 7.42 1.57 1.66 1.82

Consensus EPS-Low 5.03 4.37 1.09 1.31 1.22

HERO Hercules Offshore EPS 0.24 0.46 0.05 (0.02) 0.01 0.11 0.14 0.22 0.08 0.03 0.12

Consensus EPS 0.38 0.49 0.02 0.01 0.10

Consensus EPS-High 0.90 0.81 0.08 0.11 0.19

Consensus EPS-Low 0.08 0.05 (0.05) (0.11) (0.04)

NE Noble Drilling EPS 2.89 3.70 3.90 0.59 0.63 0.85 0.82 1.03 0.70 0.91 1.06

Consensus EPS 3.48 3.68 0.67 0.87 0.91

Consensus EPS-High 4.10 4.93 1.07 1.21 1.18

Consensus EPS-Low 3.01 2.37 0.49 0.59 0.71

ORIG Ocean Rig UDW EPS 0.84 2.00 2.80 0.04 0.10 0.30 0.30 0.24 0.47 0.66 0.63

Consensus EPS 1.66 2.21 0.39 0.61 0.54

Consensus EPS-High 2.33 2.80 0.54 0.79 0.71

Consensus EPS-Low 0.83 1.63 0.32 0.39 0.30

PACD Pacific Drilling EPS 0.42 0.95 1.25 0.07 0.10 0.14 0.12 0.10 0.21 0.27 0.38

Consensus EPS 0.78 1.26 0.18 0.23 0.27

Consensus EPS-High 0.95 1.57 0.24 0.30 0.38

Consensus EPS-Low 0.57 0.66 0.12 0.13 0.19

RDC Rowan EPS 1.96 2.60 4.75 0.55 0.57 0.42 0.42 0.28 0.29 0.75 1.28

Consensus EPS 2.27 4.20 0.26 0.63 1.05

Consensus EPS-High 3.10 5.00 0.44 0.79 1.29

Consensus EPS-Low 1.89 3.02 0.09 0.44 0.79

RIG Transocean EPS 4.12 4.70 4.05 0.93 1.08 1.37 0.73 1.43 1.21 1.00 1.06

Consensus EPS 4.33 3.52 1.13 0.88 0.85

Consensus EPS-High 5.64 5.62 1.39 1.59 1.23

Consensus EPS-Low 3.39 2.05 0.89 0.52 0.42

SDRL Seadrill EPS 3.02 3.15 3.10 0.69 0.96 0.60 0.79 0.59 0.60 0.54 0.64

Consensus EPS 3.10 3.64 0.77 0.74 0.82

Consensus EPS-High 4.40 5.83 1.06 0.92 0.98

Consensus EPS-Low 2.52 2.74 0.59 0.54 0.64

Land Drillers

HP Helmrich & Payne EPS 5.67 6.25 6.80 1.40 1.36 1.44 1.47 1.56 1.43 1.61 1.65

Consensus EPS 6.33 7.25 1.63 1.70

Consensus EPS-High 6.45 7.75 1.70 1.75

Consensus EPS-Low 6.20 6.28 1.58 1.61

NBR Nabors EPS 1.02 1.15 1.80 0.46 0.10 0.20 0.26 0.16 0.22 0.36 0.41

Consensus EPS 1.16 1.98 0.23 0.35 0.43

Consensus EPS-High 1.39 2.50 0.26 0.45 0.53

Consensus EPS-Low 0.99 1.56 0.17 0.29 0.34

PTEN Patterson-UTI Energy EPS 1.16 1.40 1.80 0.38 0.28 0.23 0.27 0.24 0.32 0.41 0.43

Consensus EPS 1.42 2.02 0.32 0.42 0.45

Consensus EPS-High 1.52 2.45 0.33 0.47 0.50

Consensus EPS-Low 1.31 1.69 0.28 0.37 0.38

Guggenheim Securities, LLC | 972-638-5502 | guggenheimsecurities.com

Top Ten Reasons to Fear the Jackup Market; Downgrading ESV to Neutral PAGE 29

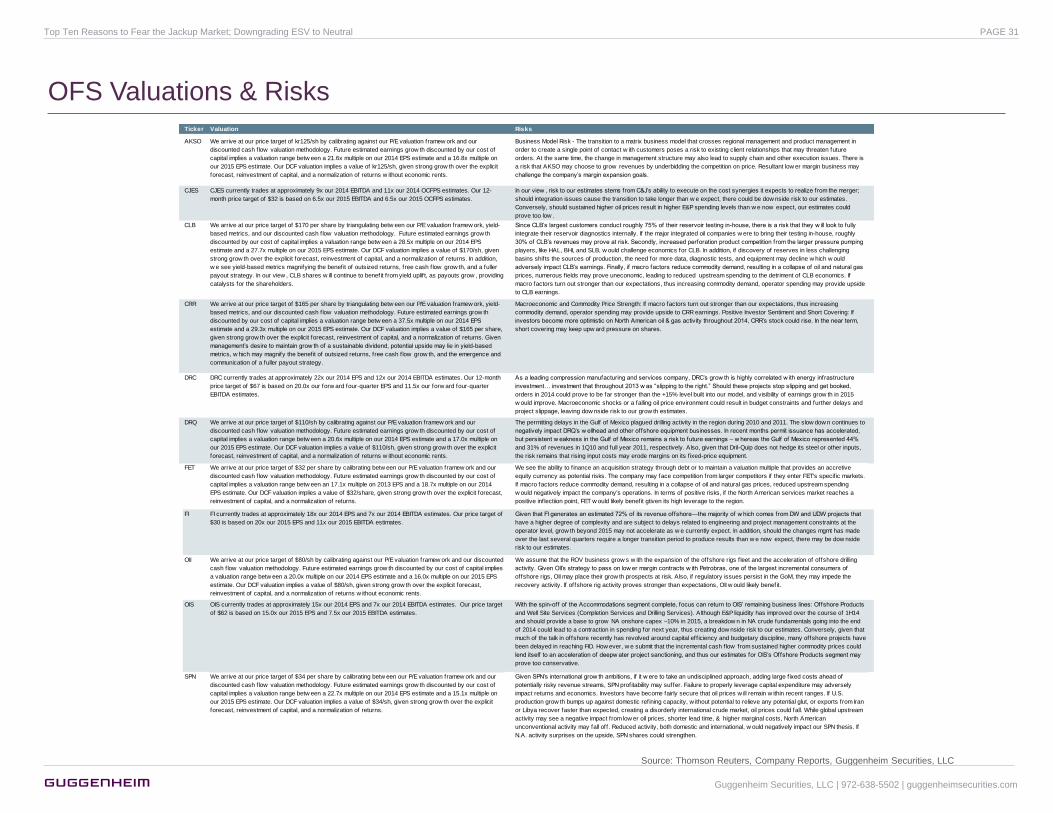

OFS Valuations & Risks

Source: Thomson Reuters, Company Reports, Guggenheim Securities, LLC

Ticker Valuation Risks

BHI BHI currently trades at approximately 18x our 2014 EPS and 8x our 2014 EBITDA estimates. Our 12-month

price target of $75 is based on 15.0x our 2015 EPS and 6.5x our 2015 EBITDA estimates.

BHI could outperform should its asset turnover improve, w hich in turn w ould push operating margins higher. In 2013, BHI’s PPE

turnover w as 2.5x, vs. 2.7x for HAL and 3.0x for SLB. How ever, given BHI’s higher mix of product sales (i.e., manufacturing vs.

services), w e believe it should have higher PPE turnover than its peers. Should BHI execute on its current “self-help” initiatives

and deliver peer-leading turnover, our estimates w ould likely prove too conservative. Conversely, should the macro environment

encounter any disruptions due to saturation risk late in 2014, our estimates may prove too high.

HAL HAL currently trades at approximately 18x our 2014 EPS and 9x our 2014 EBITDA estimates. Our 12-month

price target of $75 is based on 15.0x our 2015 EPS and 8.0x our 2015 EBITDA estimates.

HAL’s U.S. onshore execution has been excellent, and should the company be able to demonstrate higher EPS grow th into 2015,

our estimates w ould prove to be too low . How ever, should crude saturation risk begin to w eigh on North American fundamentals

in late 2014 due to delays in condensate export approval or w eakness in Brent, our estimates may prove too high.

SLB SLB currently trades at approximately 20x our 2014 EPS and 11x our 2014 EBITDA estimates. Our 12-month

price target of $130 is based on 19.0x our 2015 EPS and 11.5x our 2015 EBITDA estimates.

Much of the investment thesis for SLB rests w ith its ability to grow market share by delivering superior services quality and tool

reliability, and reduce the cost of services delivery. To the extent that execution of this strategy takes longer than w e currently

expect, our estimates—especially margins—could prove too aggressive. Similarly, SLB’s human resources program has long been

a competitive advantage, and to the extent that the company loses key people (particularly to IOCs), its competitive positioning in

the industry could w eaken.

WFT WFT currently trades at approximately 20x our 2014 EPS and 8x our 2014 EBITDA estimates. Our 12-month

price target of $18 is based on 12.5x our forw ard 4 quarter EPS and 6.5x our forw ard 4 quarter EBITDA

estimates.

This year, WFT needs to 1) execute on both its strategic divestitures, 2) high-grade its core portfolio of businesses to focus on

higher margin projects, and 3) deliver +/-$1bn in free cash f low from higher earnings, improved w orking capital turns, and low er

capex. It’s a tall order, but should the company deliver—particularly on the free cash f low generation—its relative valuation should

begin to improve. How ever, w ith its early production facilities contracts in Iraq not likely to be completed until 3Q14, the company

remains susceptible to further cash losses associated w ith this w ork, and potential disappointments w ith respect to cash f low

generation.

CAM CAM currently trades at approximately 18x our 2014 EPS estimate and 10x our 2014 EBITDA estimate. Our

12-month price target of $75 reflects a multiple of 17.0x our forw ard 4 quarter EPS and 10.5x our forw ard 4

quarter EBITDA estimates.

Although the stock has started to act better recently, investor confidence in management’s ability to execute remains low .

Although w e believe the low level of confidence should be view ed as a low bar—and therefore easy to deliver upon—w e

acknow ledge that failure to execute could leave CAM in a value trap zip code.

FTI FTI currently trades at approximately 22x our 2014 EPS and 13x our 2014 EBITDA estimates. Our 12-month

price target of $75 reflects a multiple of 22.0x our 2015 EPS and 13.0x our 2015 EBITDA estimates.

Execution continues to be the biggest risk for FTI. In our view , management needs to deliver on its stated goal of mid-teens

margins, and overruns and delays on the current backlog to get full credit for the 30% y/y increase in revenue/tree in backlog.

NOV NOV currently trades at approximately 14x our 2014 EPS estimate and 8x our 2014 EBITDA estimate. Our 12-

month price target of $100 reflects a multiple of 15.0x our forw ard 4 quarter EPS and 8.5x our forw ard 4

quarter EBITDA estimates.

Many investors still believe that NOV only w orks as a stock w hen backlog is grow ing (i.e., book-to-bill is greater than 1x) and

margins are expanding. Whereas last year, orders w ere strong and margins w eak, the concern for 2014 is the exact opposite:

that orders w ill be w eak even as margins improve modestly q/q. In our view , this conventional approach to the stock is more

consistent w ith a philosophy of momentum investing in oil services—a philosophy that does not apply in the current slow /no

grow th environment. How ever, w ithin a more relevant framew ork of sustainable competitive advantage, low capital intensity, and

high cash return, w e believe NOV screens w ell.

TS TS currently trades at approximately 16x our 2014 EPS and 9x our 2014 EBITDA estimates. Our 12-month

price target of $65 is based on 16.0x our 2015 EPS and 9.5x our 2015 EBITDA estimates.

The deferral of line pipe projects in Brazil has been a large contributor to the decline in w elded pipe margins and volumes for

Tenaris—volumes w hich have dropped to as low as 55% of the previous peak. How ever, our thesis draw s support from our

expectation for line pipe grow th to reaccelerate over the 2015-17 time frame as PBR ramps up gas production nearly 60% over

the next 4 years. How ever, should delays or budgetary limitations slow this production grow th, orders for Brazil may not

accelerate as fast as w e now expect and there may be dow nside risk to our estimates.

Guggenheim Securities, LLC | 972-638-5502 | guggenheimsecurities.com

Top Ten Reasons to Fear the Jackup Market; Downgrading ESV to Neutral PAGE 30

OFS Valuations & Risks

Source: Thomson Reuters, Company Reports, Guggenheim Securities, LLC

Ticker Valuation Risks

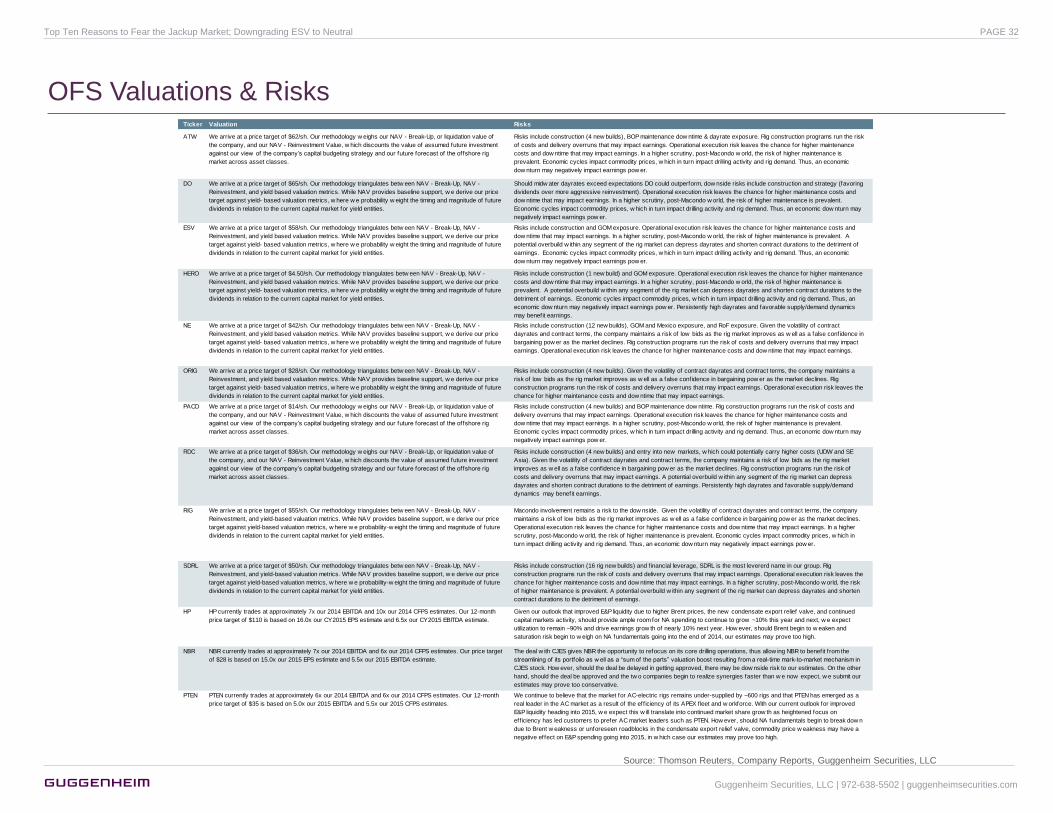

AKSO We arrive at our price target of kr125/sh by calibrating against our P/E valuation framew ork and our

discounted cash f low valuation methodology. Future estimated earnings grow th discounted by our cost of

capital implies a valuation range betw een a 21.6x multiple on our 2014 EPS estimate and a 16.8x multiple on

our 2015 EPS estimate. Our DCF valuation implies a value of kr125/sh, given strong grow th over the explicit

forecast, reinvestment of capital, and a normalization of returns w ithout economic rents.

Business Model Risk - The transition to a matrix business model that crosses regional management and product management in

order to create a single point of contact w ith customers poses a risk to existing client relationships that may threaten future

orders. At the same time, the change in management structure may also lead to supply chain and other execution issues. There is

a risk that AKSO may choose to grow revenues by underbidding the competition on price. Resultant low er margin business may

challenge the company’s margin expansion goals.

CJES CJES currently trades at approximately 9x our 2014 EBITDA and 11x our 2014 OCFPS estimates. Our 12-

month price target of $32 is based on 6.5x our 2015 EBITDA and 6.5x our 2015 OCFPS estimates.

In our view , risk to our estimates stems from C&J’s ability to execute on the cost synergies it expects to realize from the merger;

should integration issues cause the transition to take longer than w e expect, there could be dow nside risk to our estimates.

Conversely, should sustained higher oil prices result in higher E&P spending levels than w e now expect, our estimates could

prove too low .

CLB We arrive at our price target of $170 per share by triangulating betw een our P/E valuation framew ork, yield-

based metrics, and our discounted cash f low valuation methodology. Future estimated earnings grow th

discounted by our cost of capital implies a valuation range betw een a 28.5x multiple on our 2014 EPS

estimate and a 27.7x multiple on our 2015 EPS estimate. Our DCF valuation implies a value of $170/sh, given

strong grow th over the explicit forecast, reinvestment of capital, and a normalization of returns. In addition,

w e see yield-based metrics magnifying the benefit of outsized returns, free cash f low grow th, and a fuller

payout strategy. In our view , CLB shares w ill continue to benefit from yield uplif t, as payouts grow , providing

catalysts for the shareholders.

Since CLB’s largest customers conduct roughly 75% of their reservoir testing in-house, there is a risk that they w ill look to fully

integrate their reservoir diagnostics internally. If the major integrated oil companies w ere to bring their testing in-house, roughly

30% of CLB’s revenues may prove at risk. Secondly, increased perforation product competition from the larger pressure pumping

players, like HAL, BHI, and SLB, w ould challenge economics for CLB. In addition, if discovery of reserves in less challenging

basins shifts the sources of production, the need for more data, diagnostic tests, and equipment may decline w hich w ould

adversely impact CLB’s earnings. Finally, if macro factors reduce commodity demand, resulting in a collapse of oil and natural gas

prices, numerous f ields may prove uneconomic, leading to reduced upstream spending to the detriment of CLB economics. If

macro factors turn out stronger than our expectations, thus increasing commodity demand, operator spending may provide upside

to CLB earnings.

CRR We arrive at our price target of $165 per share by triangulating betw een our P/E valuation framew ork, yield-

based metrics, and our discounted cash f low valuation methodology. Future estimated earnings grow th

discounted by our cost of capital implies a valuation range betw een a 37.5x multiple on our 2014 EPS

estimate and a 29.3x multiple on our 2015 EPS estimate. Our DCF valuation implies a value of $165 per share,

given strong grow th over the explicit forecast, reinvestment of capital, and a normalization of returns. Given

management’s desire to maintain grow th of a sustainable dividend, potential upside may lie in yield-based

metrics, w hich may magnify the benefit of outsized returns, free cash f low grow th, and the emergence and

communication of a fuller payout strategy.

Macroeconomic and Commodity Price Strength: If macro factors turn out stronger than our expectations, thus increasing

commodity demand, operator spending may provide upside to CRR earnings. Positive Investor Sentiment and Short Covering: If

investors become more optimistic on North American oil & gas activity throughout 2014, CRR’s stock could rise. In the near term,

short covering may keep upw ard pressure on shares.

DRC DRC currently trades at approximately 22x our 2014 EPS and 12x our 2014 EBITDA estimates. Our 12-month

price target of $67 is based on 20.0x our forw ard four-quarter EPS and 11.5x our forw ard four-quarter

EBITDA estimates.

As a leading compression manufacturing and services company, DRC’s grow th is highly correlated w ith energy infrastructure

investment… investment that throughout 2013 w as “slipping to the right.” Should these projects stop slipping and get booked,

orders in 2014 could prove to be far stronger than the +15% level built into our model, and visibility of earnings grow th in 2015

w ould improve. Macroeconomic shocks or a falling oil price environment could result in budget constraints and further delays and

project slippage, leaving dow nside risk to our grow th estimates.

DRQ We arrive at our price target of $110/sh by calibrating against our P/E valuation framew ork and our

discounted cash f low valuation methodology. Future estimated earnings grow th discounted by our cost of

capital implies a valuation range betw een a 20.6x multiple on our 2014 EPS estimate and a 17.0x multiple on

our 2015 EPS estimate. Our DCF valuation implies a value of $110/sh, given strong grow th over the explicit

forecast, reinvestment of capital, and a normalization of returns w ithout economic rents.

The permitting delays in the Gulf of Mexico plagued drilling activity in the region during 2010 and 2011. The slow dow n continues to

negatively impact DRQ’s w ellhead and other offshore equipment businesses. In recent months permit issuance has accelerated,

but persistent w eakness in the Gulf of Mexico remains a risk to future earnings – w hereas the Gulf of Mexico represented 44%

and 31% of revenues in 1Q10 and full year 2011, respectively. Also, given that Dril-Quip does not hedge its steel or other inputs,

the risk remains that rising input costs may erode margins on its f ixed-price equipment.

FET We arrive at our price target of $32 per share by calibrating betw een our P/E valuation framew ork and our

discounted cash f low valuation methodology. Future estimated earnings grow th discounted by our cost of

capital implies a valuation range betw een an 17.1x multiple on 2013 EPS and a 18.7x multiple on our 2014

EPS estimate. Our DCF valuation implies a value of $32/share, given strong grow th over the explicit forecast,

reinvestment of capital, and a normalization of returns.

We see the ability to f inance an acquisition strategy through debt or to maintain a valuation multiple that provides an accretive

equity currency as potential risks. The company may face competition from larger competitors if they enter FET's specif ic markets.

If macro factors reduce commodity demand, resulting in a collapse of oil and natural gas prices, reduced upstream spending

w ould negatively impact the company's operations. In terms of positive risks, if the North American services market reaches a

positive inflectiion point, FET w ould likely benefit gtiven its high leverage to the region.

FI FI currently trades at approximately 18x our 2014 EPS and 7x our 2014 EBITDA estimates. Our price target of

$30 is based on 20x our 2015 EPS and 11x our 2015 EBITDA estimates.

Given that FI generates an estimated 72% of its revenue offshore—the majority of w hich comes from DW and UDW projects that

have a higher degree of complexity and are subject to delays related to engineering and project management constraints at the