20131217 sevilla-regional policy-m gonzalez-sancho v3b

TRANSCRIPT

Regional Policy in EuropeSevilla 17.12.2013

“Regional Digital Agendas"

Miguel Gonzalez-SanchoEuropean CommissionDG Communications Networks, Content and Technology

Overview

• Digital Agenda and scoreboard

• Broadband

• Demand and service

• Cohesion policy and ICT

Digital Agenda for Europe

• Political context: Digital Agenda, one of the 7 EU 2020 flagships

• Rationale: ICT as sector and as enabler driving growth; must have > Convergence of faster networks with smarter devices and richer contents

• Holistic policy approach: networks > services > demand

• Structure: 7 pillars; 100 actions (+32 with 2012 review) for EC and countries; targets

• Monitoring (annual scoreboard): actions; key performance indicators

• Governance: assembly, national representatives group, Going Local (e.g. Sevilla 2011)

• Complement: DAE not 1st nor only digital strategy (Spain, Andalucía…); regional angle

Digital Agenda logic: networks, services, demand…

Interoperability & standards (+ cloud computing, after DAE review)

A vibrant digital single market

Trust & Security

Research & innovation

Using ICT to help society

Fast & ultra-fast Internet access

Digital literacy, skills & inclusion

101 actions (+ 32 after review), targets

5To find out more visit www.ec.europa.eu/digital-agenda/en/scoreboardhttps://ec.europa.eu/digital-agenda/en/scoreboard/portugal

Scoreboard 2013

Overview

• Digital Agenda and scoreboard

• Broadband

• Demand and services

• Cohesion policy and ICT

Broadband• Basic Broadband is now virtually everywhere in Europe – satellite performance has

improved, helping to cover the 4.5% of population not covered by fixed basic broadband. [target 1: 100% basic broadband coverage by 2013]

• Fast broadband now reaches half the population - 54% of EU citizens have broadband available at speeds greater than 30 Mbps. [target 2: 100% fast broadband (> 30 Mbps) coverage by 2020]

• Only 2% of homes have ultrafast broadband subscriptions (above 100 Mbps), far from the EU's 2020 target of 50%. [target 3: 50% households ultra-fast broadband (> 100 Mbps) subscriptions by 2020]

• Internet access is increasingly going mobile - 36% of EU citizens access the internet via a portable computer or other mobile device (access via mobile phone is up from 7% in 2008 to 27% in 2012). 4th generation mobile (LTE) coverage tripled to 26% in one year.

• Roaming prices in 2012 have fallen - by almost 5 euro-cents, mainly after the 1st July 2012 Roaming regulation.

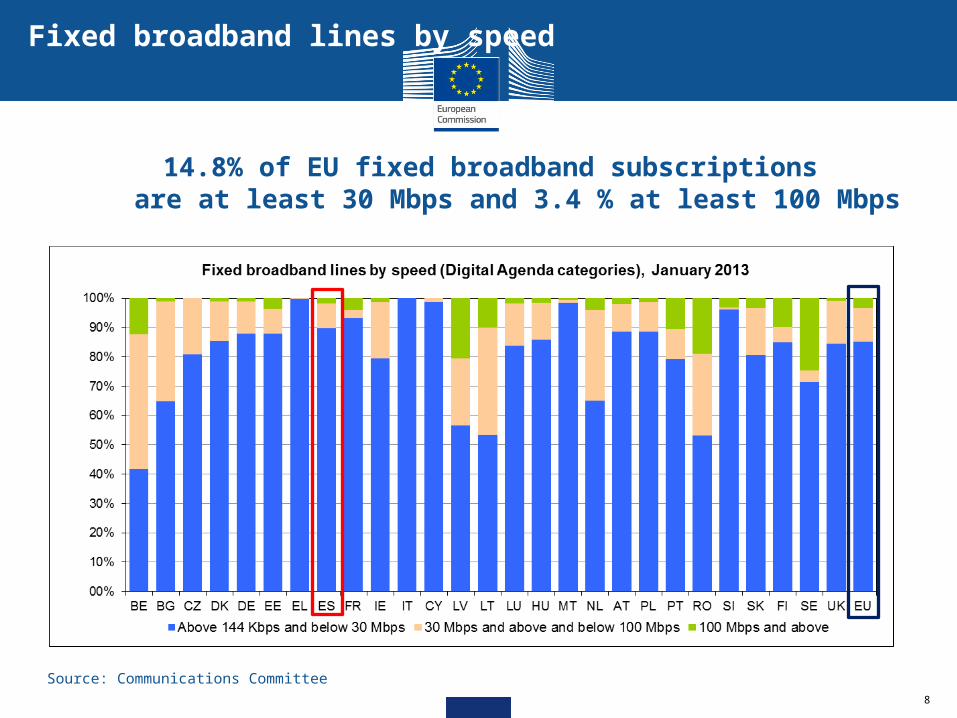

14.8% of EU fixed broadband subscriptions are at least 30 Mbps and 3.4 % at least 100 Mbps

Fixed broadband lines by speed

Source: Communications Committee8

Map of NGA broadband coverage (2012)

EU broadband policy – key areas

10

Financing and fundingFinancing

and fundingMarket

frameworkMarket

framework

• Cost reduction initiative

• eComms regulation, e. g. Recommendation on non-discrimination and costing methodologies

• Demand Stimulation

• Single EU authorisation

• European inputs: Spectrum and access products

• Single consumer space: Net neutrality, harmonised end user rights, roaming

• European Structural and Investment Funds (ESIF)

• Connecting Europe Facility (CEF)

• Broadband state aid guidelines

Single market for eComms

Single market for eComms

EU financing for broadband

• European Structural and Investment Funds (ERDF and EARDF): grants and financial instruments

• Connecting Europe Facility (CEF): Some complementary EU support by means of financial instruments

• Currently project bonds pilot – open for project proposals

• Possibly greater EIB lending activity in ICT/broadband following capital increase

EU financing

Overview

• Digital Agenda and scoreboard

• Broadband

• Demand and services

• Cohesion policy and ICT

Demand and services

• The proportion of EU citizens having never used the internet continues to decline (down 2 percentage points to 22%). However around 100 million EU citizens have still never used the internet, declaring too high costs, lack of interest, or lack of skills as the main barriers.

• 70% now use the internet regularly at least once a week, up from 67% last year; 54% of disadvantaged people use the internet regularly, up from 51% last year.

• 50% EU citizens have no or low computer skills – neither the amount nor the level of ICT user skills has improved over the last year. 40% of companies recruiting or trying to recruit IT specialists have difficulties in doing so and the current number of vacancies for ICT specialists has been projected to grow to 900 000 by 2015. The recently launched Grand Coalition for Digital Jobs will target actions toward closing this gap.

2% of Europeans have never used the Internet, 70% are regular Internet users (at least once a week) (2012)

14

Source: Eurostat

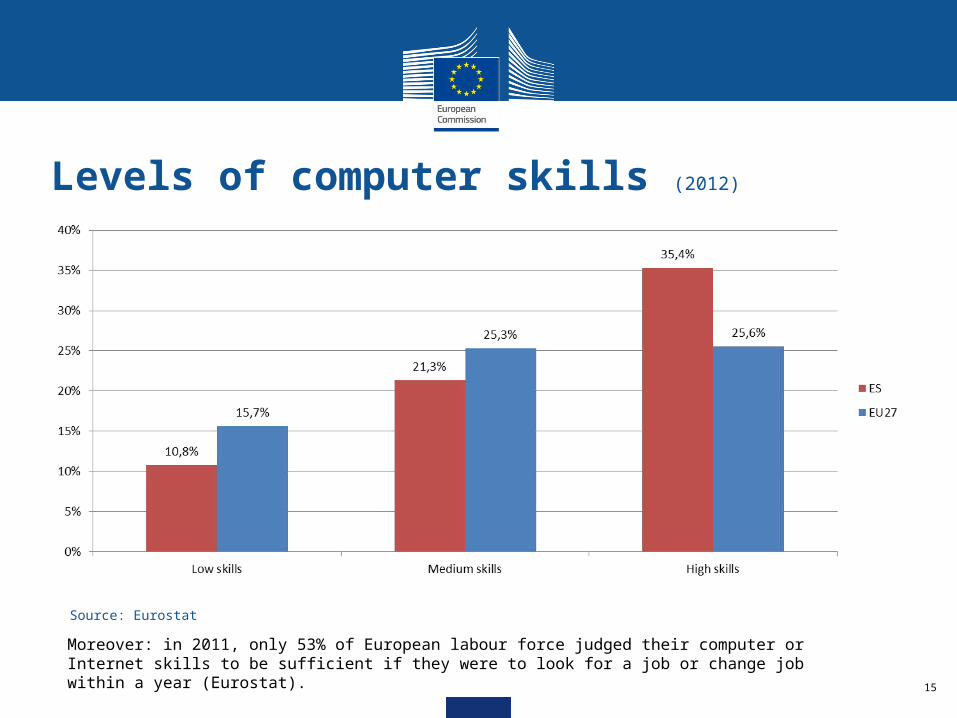

Levels of computer skills (2012)

15

Moreover: in 2011, only 53% of European labour force judged their computer or Internet skills to be sufficient if they were to look for a job or change job within a year (Eurostat).

Source: Eurostat

Demand and services

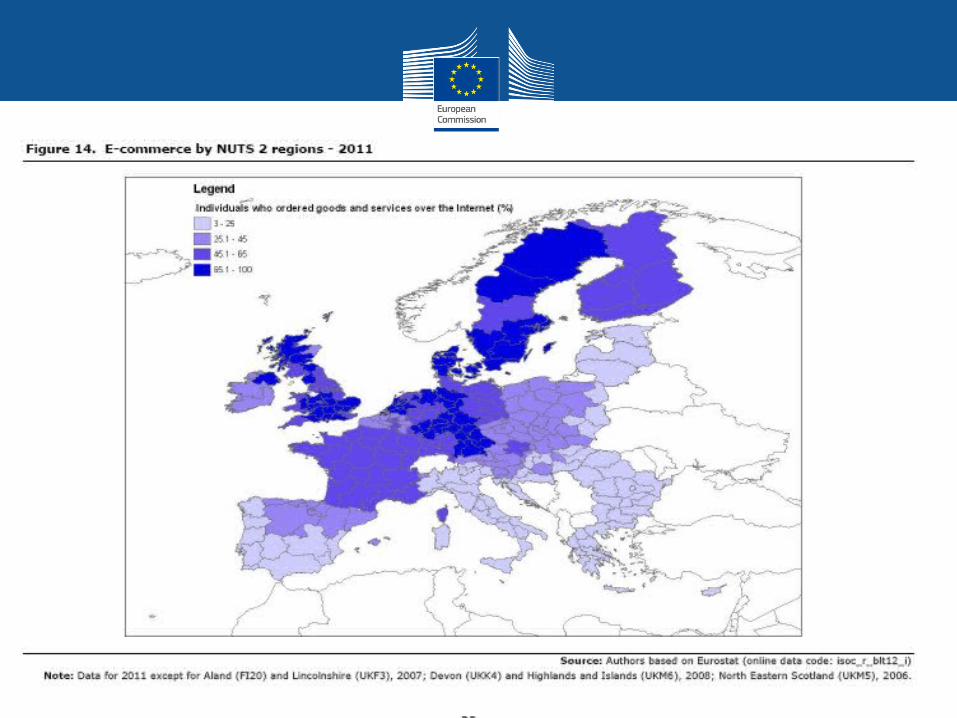

• eCommerce is growing steadily, but not cross-border - 45 % of individuals use the internet to buy goods and services, a moderate increase from 43% one year ago; very few buy across borders.

• eGovernment is now undertaken by most firms and citizens – 87% of enterprises use eGovernment and the proportion of citizens using eGovernment has also increased over the last year to 44% (both up by 3 percentage points).

Citizens engaging in eCommerce (domestic & cross border)(% of all citizens, 2012)

18

Source: Eurostat

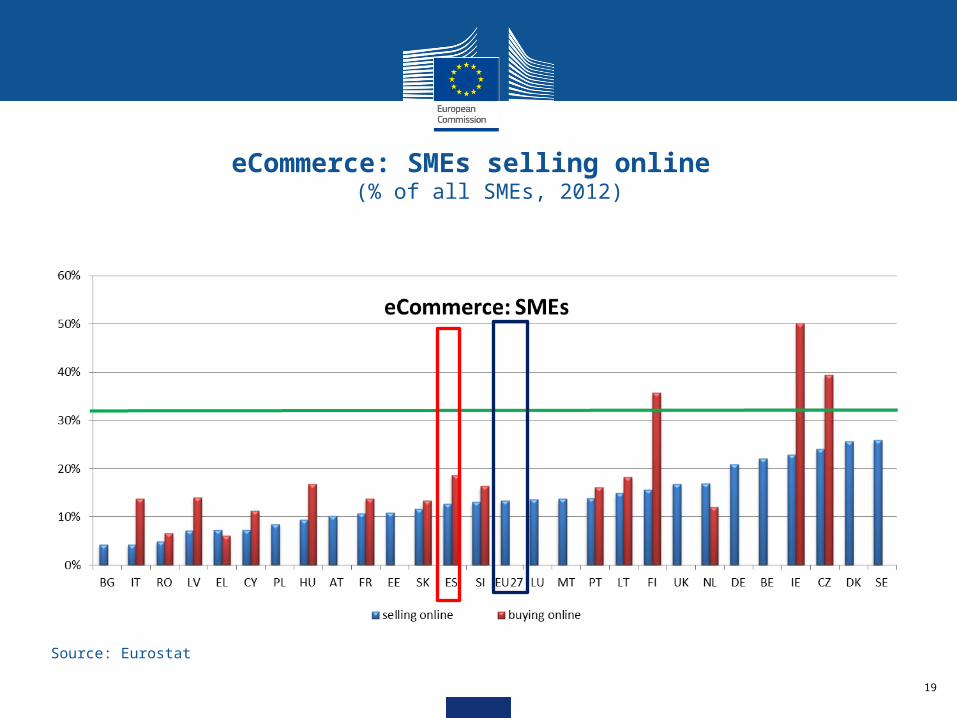

eCommerce: SMEs selling online(% of all SMEs, 2012)

19

Source: Eurostat

•Electronic interaction by citizens* with public authorities (2012)

Source: Eurostat

*Citizens aged between 25 and 54

21

eGovernment

Source: Eurostat

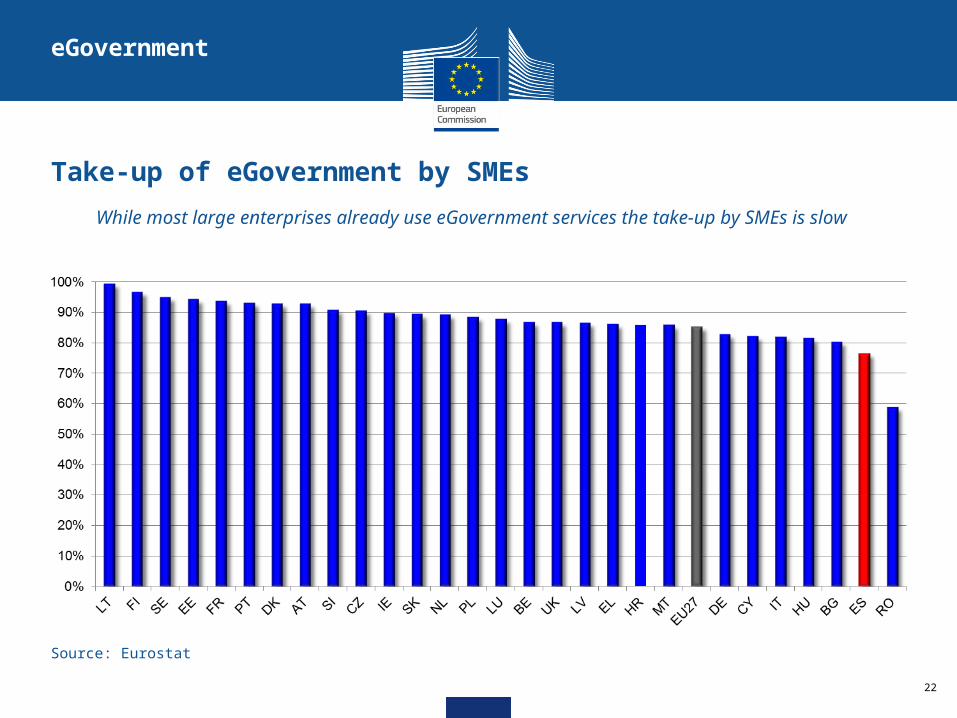

Take-up of eGovernment by SMEs

22

eGovernment

While most large enterprises already use eGovernment services the take-up by SMEs is slow

Source: Eurostat

Overview

• Digital Agenda and scoreboard

• Broadband

• Demand and services

• Cohesion policy and ICT

Cohesion policy• For many years EU structural funds support ICT: infrastructure, services, skills…

> 2007-13: over EUR 15 billion or 4.4% of the total cohesion policy budget> Absorption challenge: administrative capacity; reprogramming.

• 2014-20020: ICT 1 of 11 thematic objectives (in line with EU2020)> enhancing access to, and use and quality of, ICT > but ICT is tranversal, so can be present in the other objectives

• ERDF: ICT investment priority > broadband; ICT products and services; ICT applications > 1 in 4 concentration priorities > infrastructure can be supported in more developed regions

• Ex-ante conditionalities (to justify in partnership agreements): e-growth strategies, NGAs

• EARDF can support ICT rural projects

• Alignment with European semester: broadband in Country Specific Recommendations

Funds allocated to ICTs in 2007-13: •over EUR 15 billion or 4.4% of the total cohesion policy budget. •Shift in the investment priorities from infrastructure to support for content development, both in the public sector (eHealth, eGovernment, etc.) and for SMEs (eLearning, eBusiness, etc.)

Basics on current Cohesion Policy

Cohesion Policy

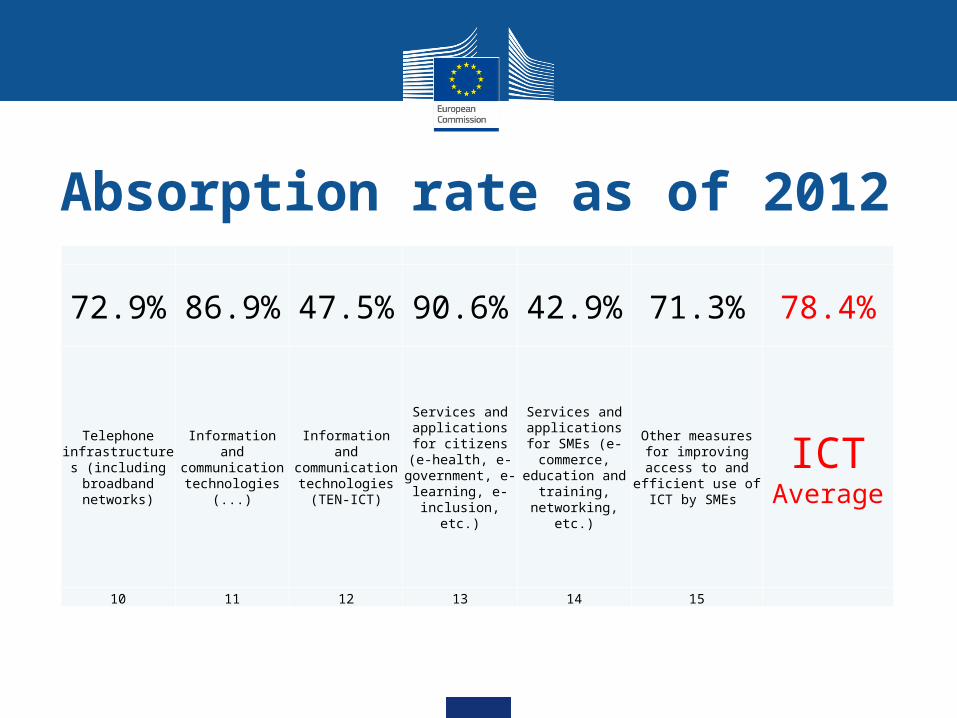

Absorption rate as of 2012

72.9% 86.9% 47.5% 90.6% 42.9% 71.3% 78.4%

Telephone infrastructures

(including broadband networks)

Information and communication

technologies (...)

Information and communication

technologies (TEN-ICT)

Services and applications for

citizens (e-health, e-

government, e-learning, e-

inclusion, etc.)

Services and applications for

SMEs (e-commerce,

education and training,

networking, etc.)

Other measures for improving access

to and efficient use of ICT by SMEs

ICTAverage

10 11 12 13 14 15

27

General regulation adopted

Partnership Agreement Submitted (MS)

Max 4 months

All OPs incl. Ex-ante eval. (except ETC) (MS)

Partnership Agreement Adoption

Max 1 month

OP Adoption (EC)

ETC OPs (MS)Observations by EC

ETC OP Adoption (EC)

Observations by EC

Partnership Agreement Country / region specific

Operational programmes

European Territorial Cooperation ("INTERREG") programmes

Observations by EC

Max 3 monthsMax 3 months

Max 3 months

Max 3 months

Max 9 months

Max 3 months

Max 3 months

Calendar for partnership agreements & OPs

RISRIS33

2nd half

of 2013

Is already on-going

on an informal basis …

Eu

rop

e 2

020

Eu

rop

e 2

020

inclu

siv

esu

sta

inab

lesm

art

Thematic objectivesThematic objectives1. Research and innovation2. Information and Communication Technologies3. Competitiveness of Small and Medium-Sized

Enterprises (SME)4. Shift to a low-carbon economy5. Climate change adaptation and risk management and

prevention6. Environmental protection and resource efficiency7. Sustainable transport and disposal of congestion on major

network infrastructure8. Employment and support for labour mobility9. Social inclusion and poverty reduction10. Education, skills and lifelong learning11. Increased institutional capacity and effectiveness of public

administration

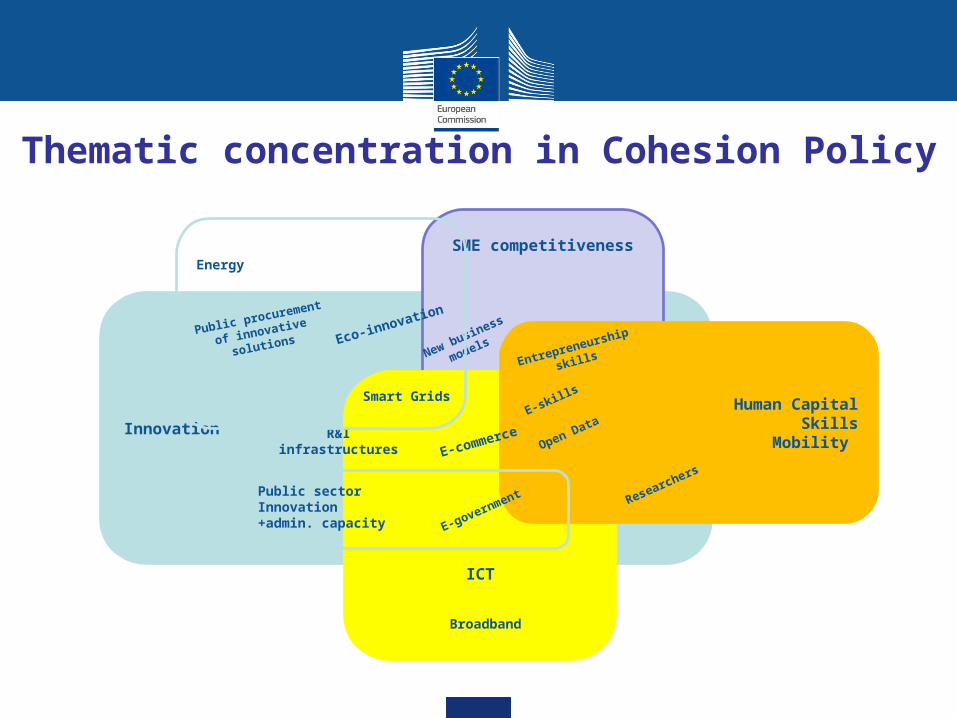

Thematic concentration in Cohesion Policy

Innovation

SME competitiveness

ICT

Human CapitalSkills

Mobility

Public sectorInnovation+admin. capacity

Eco-innovation

Broadband

E-commerce

E-government

R&I infrastructures

E-skills

Entrepreneurship

skills

Researchers

New business

models

Energy

Public

procurement of

innovative

solutions

Smart Grids

Open Data

Less developed regionsDeveloped regions and

transition regions

60% 20%

6%

44%

Flexibility (different regions present different needs)Special arrangements for the previously convergence regions

Research and Innovation Energy efficiency and renewable energy

SMEs competitiveness + ICT access, quality and use

Transition regions: 60 % concentration (incl. 15% for energy/renewables)

Concentration on "two or

more of the thematic

objectives 1, 2, 3 and 4"

Thematic concentration of the ERDF

Thematic Objective 2Thematic Objective 2:: Enhancing access to + use and quality of, information and communication technologies

ERDF nvestment priorities under TO 2:

a) diffusion of broadband and high speed networks, supporting adoption of emerging technologies and networks for the digital economy

b) development of ICT products and services, electronic commerce and increased demand for ICT

c) strengthening the application of ICT for eGovernment, eLearning, eInclusion and eHealth

Ex ante conditionalities:

Next Generation Access

Plan

Strategic policy framework for digital growth (also in RIS3)

Ex-ante conditionalities

Ex ante conditionality Criteria for fulfilment

2.2. Next Generation Network (NGN) Infrastructure:

The existence of national and/or regional NGN Plans which take account of regional actions in order to reach the Union high-speed Internet access targets and promote territorial cohesion, focusing on areas where the market fails to provide an open infrastructure at an affordable cost and of a quality in line with the EU competition and State aid rules, and to provide accessible services to vulnerable groups.

A national or regional NGN Plan is in place that contains:

– a plan of infrastructure investments based on an economic analysis taking account of existing private and public infrastructures and planned investments;

– sustainable investment models that enhance competition and provide access to open, affordable, quality and future proof infrastructure and services;

– measures to stimulate private investment.

Ex-ante conditionality N°2(2) for ICT infrastructure

Modifications by:

Council + EP

ESF; Horizon2020• Importance of ESF to support digital capacity:

>employment and mobility; better education; social inclusion; better public administration

• October 2013 European Council dedicate to digital economy and innovation “part of the European Structural and Investment Funds (2014-2020) should be used for ICT education, support for retraining, and vocational education and training in ICT, including through digital tools and content, in the context of the Youth Employment Initiative”

• Horizon 2020 for research and innovation; much on ICT

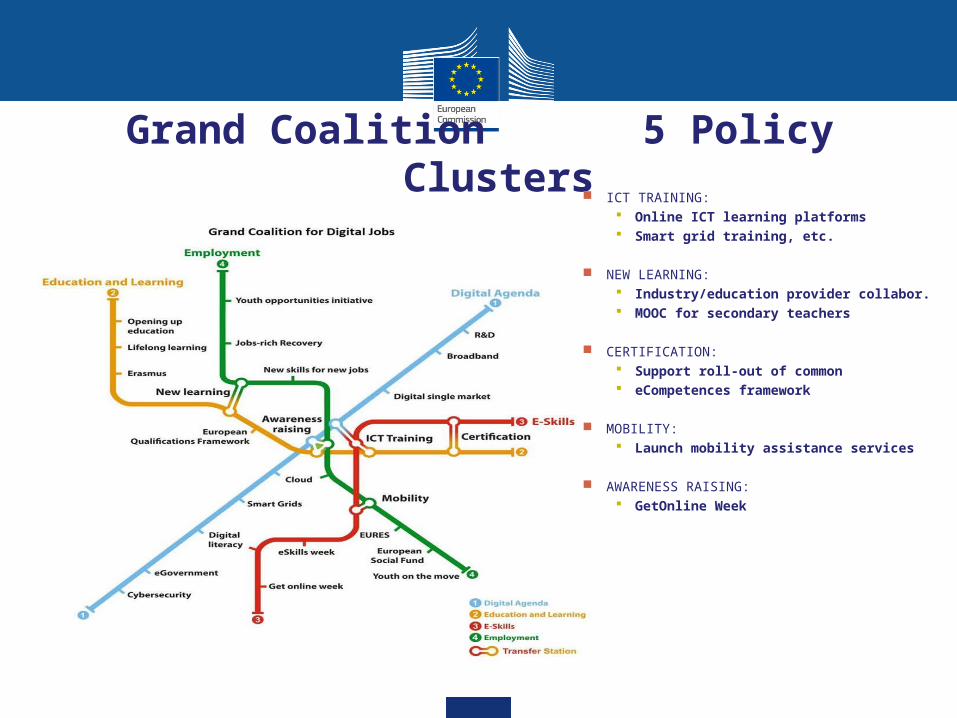

Grand Coalition 5 Policy Clusters ICT TRAINING:

Online ICT learning platforms Smart grid training, etc.

NEW LEARNING: Industry/education provider collabor. MOOC for secondary teachers

CERTIFICATION: Support roll-out of common eCompetences framework

MOBILITY: Launch mobility assistance services

AWARENESS RAISING: GetOnline Week

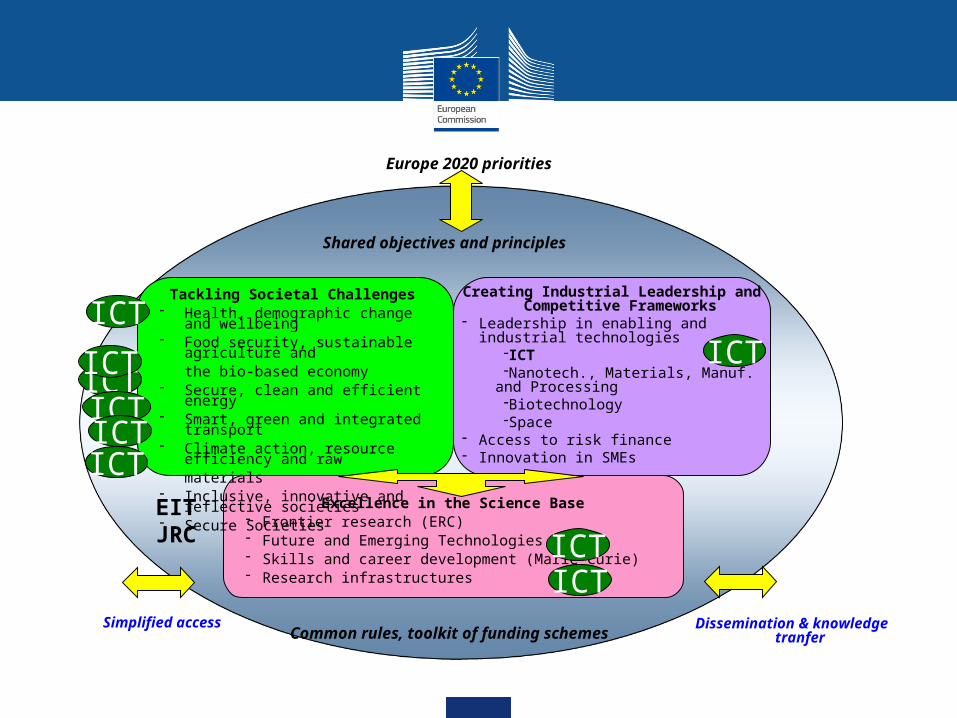

Creating Industrial Leadership and Competitive Frameworks

Leadership in enabling and industrial technologies

ICTNanotech., Materials, Manuf. and

Processing BiotechnologySpace

Access to risk finance Innovation in SMEs

Excellence in the Science Base Frontier research (ERC) Future and Emerging Technologies (FET) Skills and career development (Marie Curie) Research infrastructures

Shared objectives and principles

Common rules, toolkit of funding schemes

Europe 2020 priorities

Simplified access Dissemination & knowledge tranfer

Tackling Societal Challenges Health, demographic change and wellbeing Food security, sustainable agriculture and

the bio-based economy Secure, clean and efficient energy Smart, green and integrated transport Climate action, resource efficiency and raw

materials Inclusive, innovative and reflective

societies Secure Societies

EITJRC

ICT

ICTICTICTICT

ICT

ICTICT

ICT

Conclusions

• Digital revolution; Europe cannot stay behind > Remove barriers in the European space; towards a Digital Single Market>Build European capacity: networks, data/ cloud, skills, R&D&I, industrial base…

• Role for public sector ; European/ national/ local digital agendas > Strategic guidance; mobilise stakeholders; combine tools (regulation, funding….) > European orientations and targets (EU200 > DAE > EU semester; CSR); tools > Regional action key (best adapted to local context needs and strengths)

• Digital sector important per se but even more as enabler > ICT supply > demand > impact

• Increasing digital angle in all policies: regional, R&D, employment, education, industry…

• Digital will remain priority in new EU legislature starting 2014; the future is digital…

blogs.ec.europa.eu/digital-agenda

@DigitalAgendaEU

DigitalAgenda

ec.europa.eu/digital-agenda

Gracias