20100927 for 20100927 econ 1

DESCRIPTION

We Don’t Need Another Hero... hFp://delong.typepad.com/econ_1_fall_2010/ J. Bradford DeLong, Michael Urbancic, and a cast of thousands... • What is the most likely outcome for the U.S. budget come 2060?TRANSCRIPT

We Don’t Need Another Hero...

Economics 1: Fall 2010

J. Bradford DeLong, Michael Urbancic, and a cast of thousands...

hFp://delong.typepad.com/econ_1_fall_2010/

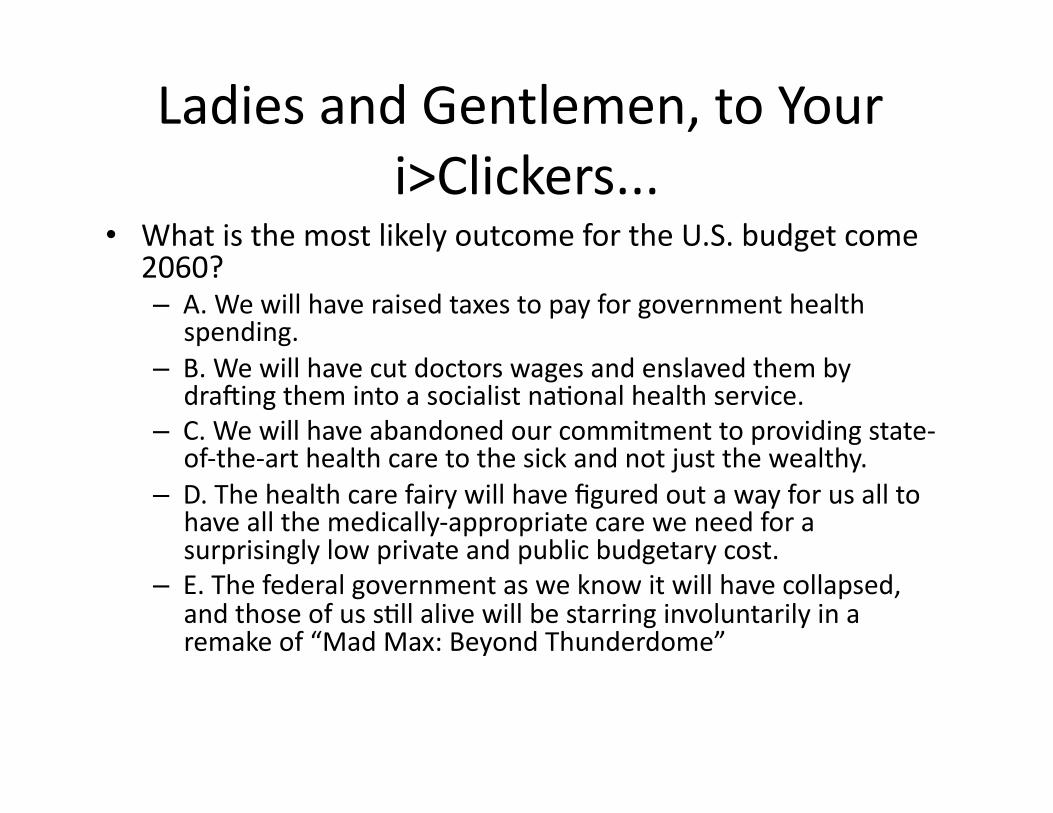

Ladies and Gentlemen, to Your i>Clickers...

• What is the most likely outcome for the U.S. budget come 2060? – A. We will have raised taxes to pay for government health

spending. – B. We will have cut doctors wages and enslaved them by

draVing them into a socialist naWonal health service. – C. We will have abandoned our commitment to providing state-‐

of-‐the-‐art health care to the sick and not just the wealthy. – D. The health care fairy will have figured out a way for us all to

have all the medically-‐appropriate care we need for a surprisingly low private and public budgetary cost.

– E. The federal government as we know it will have collapsed, and those of us sWll alive will be starring involuntarily in a remake of “Mad Max: Beyond Thunderdome”

Administrivia

• Complex dance for the midterm... – Want to get more space...

– Want to avoid the ten-‐minute caFle drive...

• Reviews for midterm... – Friday here, 12-‐1...

• Thank you for taking the midterm... – It’s about us, not about you—feedback device...

• Lilly Kuang...

We Don’t Need Another Hero...

$Z100,000,000,000,000

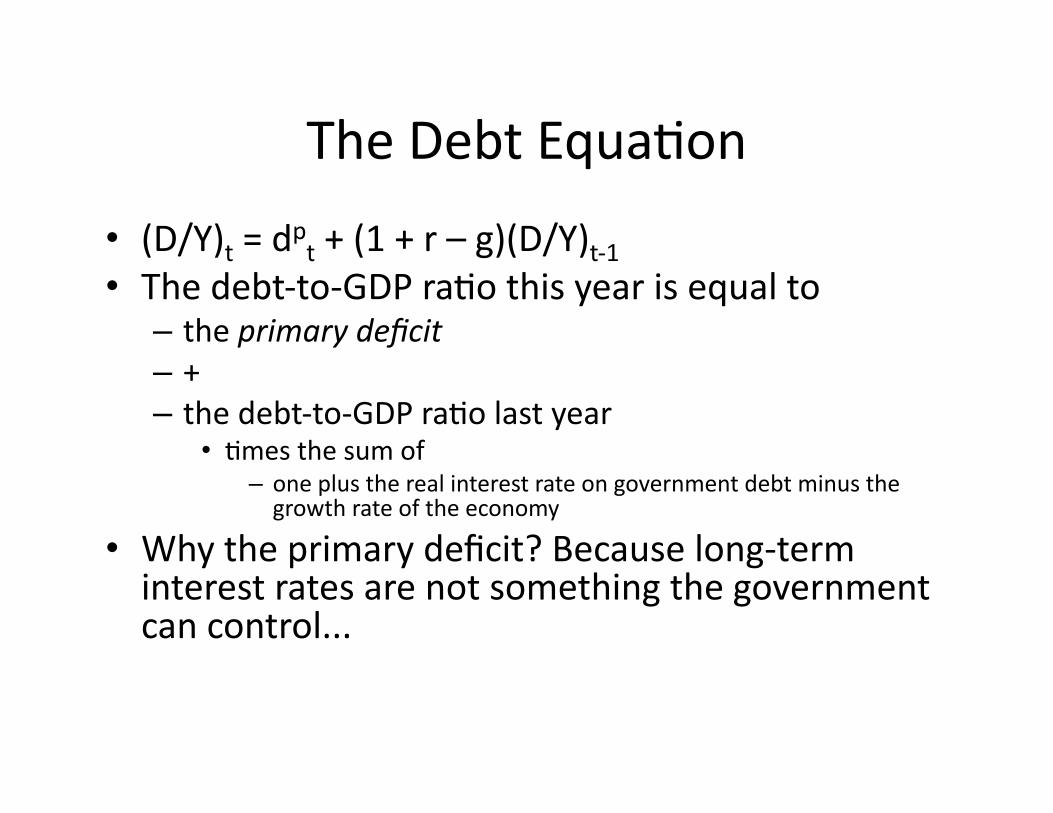

The Debt EquaWon

• (D/Y)t = dpt + (1 + r – g)(D/Y)t-‐1 • The debt-‐to-‐GDP raWo this year is equal to – the primary deficit – + – the debt-‐to-‐GDP raWo last year

• Wmes the sum of – one plus the real interest rate on government debt minus the growth rate of the economy

• Why the primary deficit? Because long-‐term interest rates are not something the government can control...

Solving for the Stable Debt-‐to-‐GDP RaWo

• (D/Y)t = dpt + (1 + r – g)(D/Y)t-‐1 • (D/Y)*= dpt + (1 + r – g)(D/Y)* • 0 = dpt + (r – g)(D/Y)* • -‐dpt = (r – g)(D/Y)* • Stability: (D/Y)* = -‐dpt /(r – g)

– If r > g, there had beFer be a primary surplus... • If not, then there is no stable debt-‐to-‐GDP raWo

– Either people believe that policy will change – Or you are headed for Zimbabwe

– If r < g, what is the problem? – But will r stay g?

– If people lose confidence in your government—if r goes up—then you can get into big trouble immediately

Economics 1: Fall 2010: The Government Budget in the

Medium Run

J. Bradford DeLong

September 27, 2010, 12-‐1 Wheeler Auditorium, U.C. Berkeley

Suppose That Public Finances Are Sound...

• No worries that the government won’t pay back its debts at all...

• Nevertheless, we want to consider what happens when the share of government spending G in the economy expands (or contracts)

Also Suppose That We Are Not in a “Depression Economics” SituaWon...

• Y = Y* • If Y < Y*, we are in a “depression economics” situaWon – In which case the analysis of government spending and deficits is very different

– And we have already done that • So assume, also, that Y = Y*

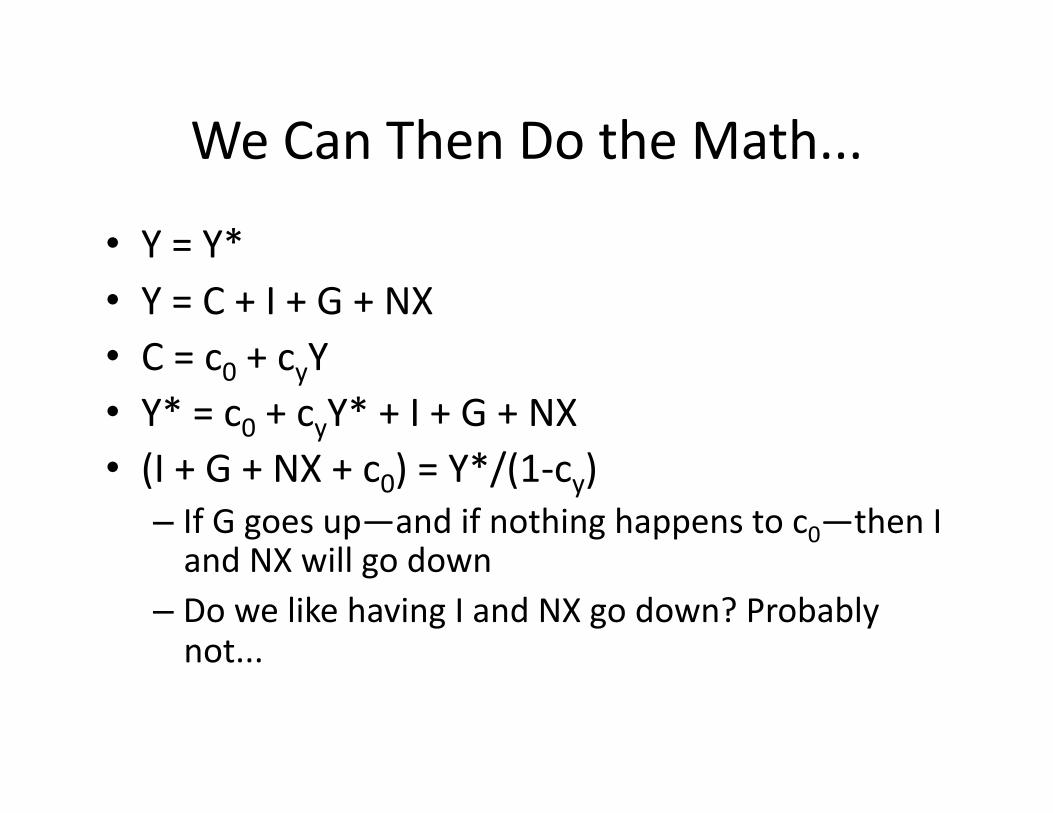

We Can Then Do the Math...

• Y = Y* • Y = C + I + G + NX • C = c0 + cyY • Y* = c0 + cyY* + I + G + NX • (I + G + NX + c0) = Y*/(1-‐cy) – If G goes up—and if nothing happens to c0—then I and NX will go down

– Do we like having I and NX go down? Probably not...

How Does NX Fall When G Rises?

• The math tells us what the answer is – It does not tell us how we get there – Here’s how:

• Government issues more bonds • Bond prices fall in dollars • Interest rates rise • More foreigners who have sold us imports decide not to by exports but instead to take advantage of the higher interest rates and buy bonds

• NX fall

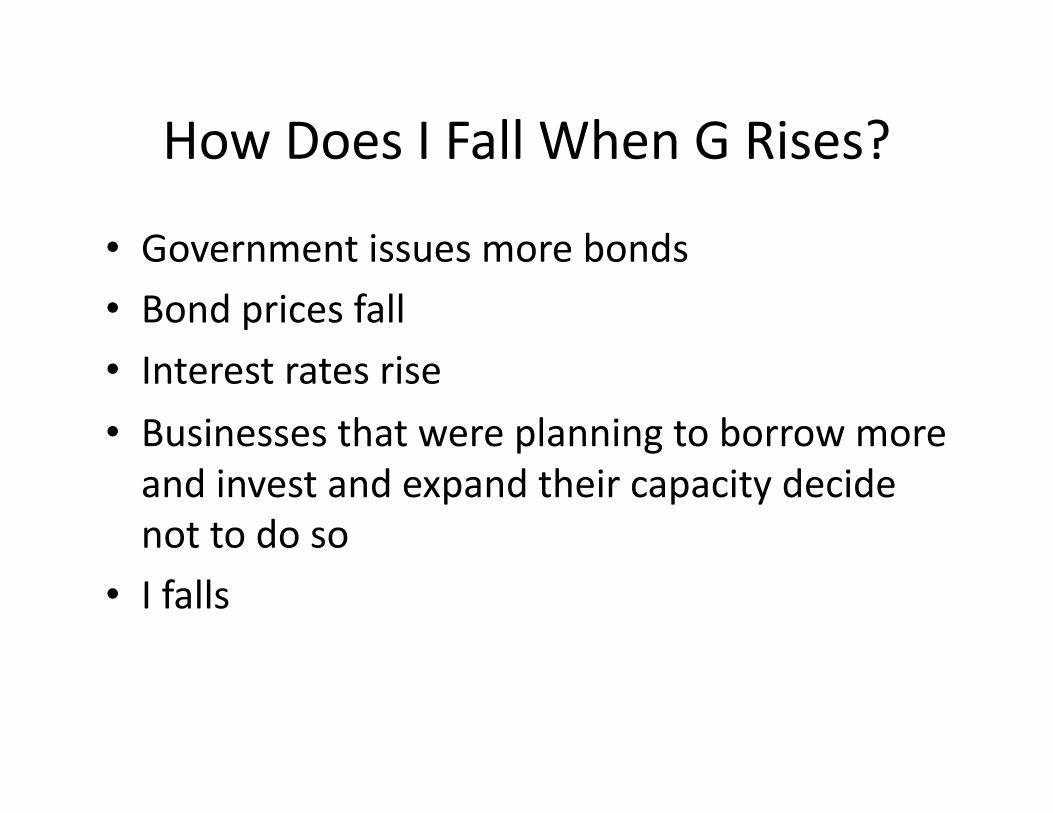

How Does I Fall When G Rises?

• Government issues more bonds • Bond prices fall • Interest rates rise • Businesses that were planning to borrow more and invest and expand their capacity decide not to do so

• I falls

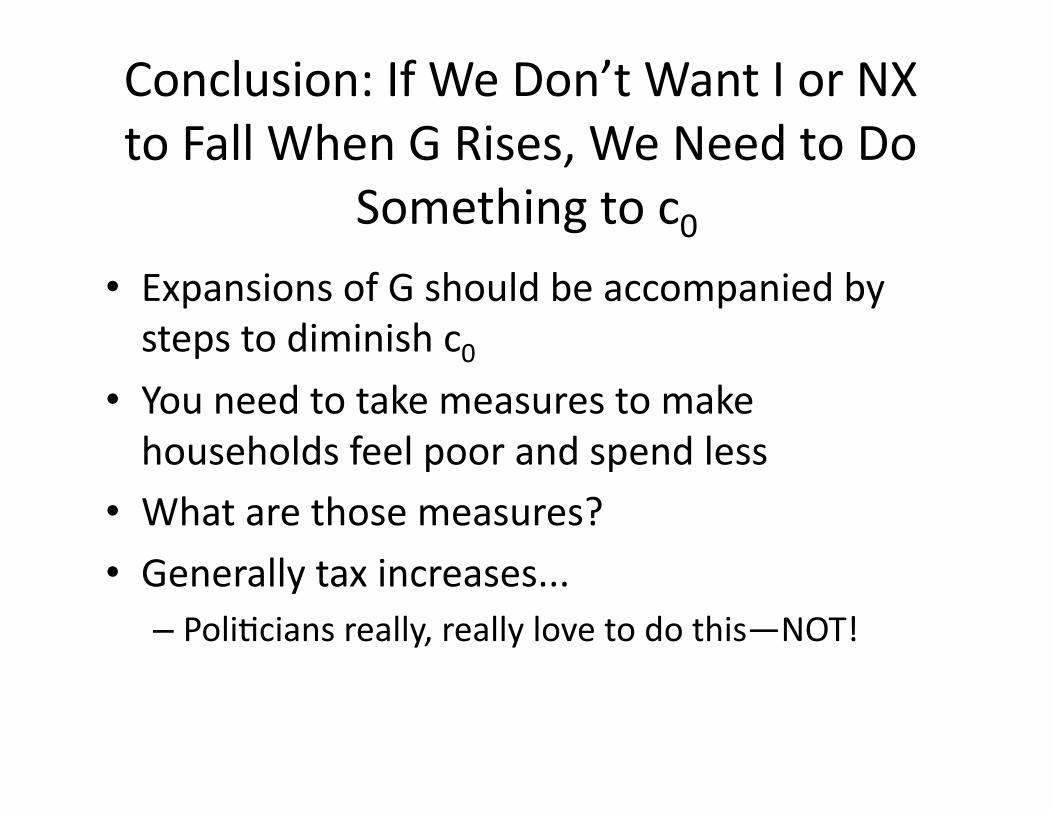

Conclusion: If We Don’t Want I or NX to Fall When G Rises, We Need to Do

Something to c0 • Expansions of G should be accompanied by steps to diminish c0

• You need to take measures to make households feel poor and spend less

• What are those measures?

• Generally tax increases... – PoliWcians really, really love to do this—NOT!

Nobody Likes Tax Increases...

• But we have to do them eventually – Or else debt crises and hyperinflaWon...

• What if we postpone them unWl later? – A good reason to postpone them: depression economics—a cyclical deficit is a good thing

– But if we are not in depression economics, postponing the tax increases is a bad idea

– The deficits you run lower NX and lower I, and make everybody worse off

Four Rules for Public Finance

• Budget balance over the business cycle – Repay your cyclical deficits when the economy is in a boom

• Milton Friedman’s PAYGO

• Keep plenty of headroom in your debt capacity—in your D/Y raWo

• Balance present and future in your D/Y raWo – OK to borrow

Are These Rules Sustainable?

• James Buchanan’s criWque: – “cyclical deficit in downturns good, permanent structural deficit bad” is just too complicated for the poliWcal system to process

– Hence if you tolerate and approve of cyclical deficits to fight downturns

– Then you are sesng the poliWcal stage for permanent structural deficits

– Those will slow growth – And possibly lead to financial crises and hyperinflaWon

Is Buchanan Right? • The possibility seems distressingly likely... • The number of excuses to avoid tax increases is infinite...

• The number of ways since 1980 that people—usually Republicans—have found to try to permanently unbalance the government budget in the long run is truly astonishing... – The “Laffer Curve”: cut taxes and actually raise tax revenues: • Works in some “depression economics” situaWons • Works with tariffs • Works when the taxes are just the levers for corrupt extorWon • In the North AtlanWc? Not so much...

– A Laffer coefficient of 1/10 is what you should keep in the back of your mind

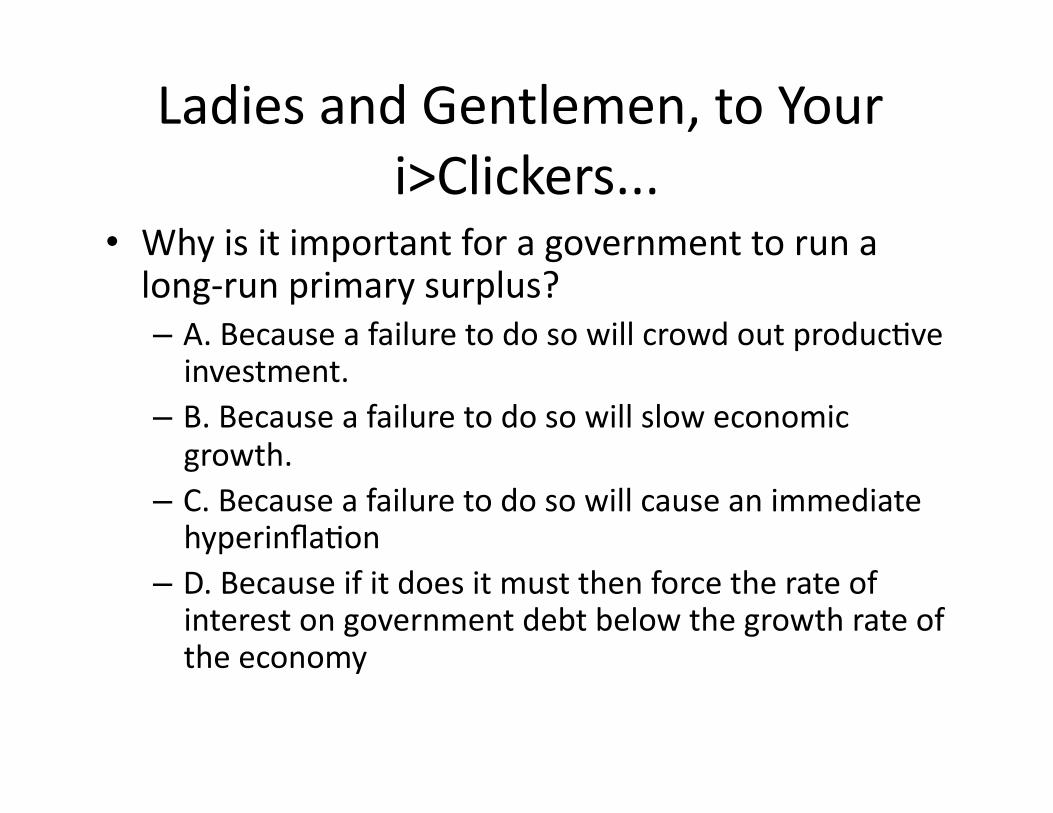

Ladies and Gentlemen, to Your i>Clickers...

• Why is it important for a government to run a long-‐run primary surplus? – A. Because a failure to do so will crowd out producWve investment.

– B. Because a failure to do so will slow economic growth.

– C. Because a failure to do so will cause an immediate hyperinflaWon

– D. Because if it does it must then force the rate of interest on government debt below the growth rate of the economy

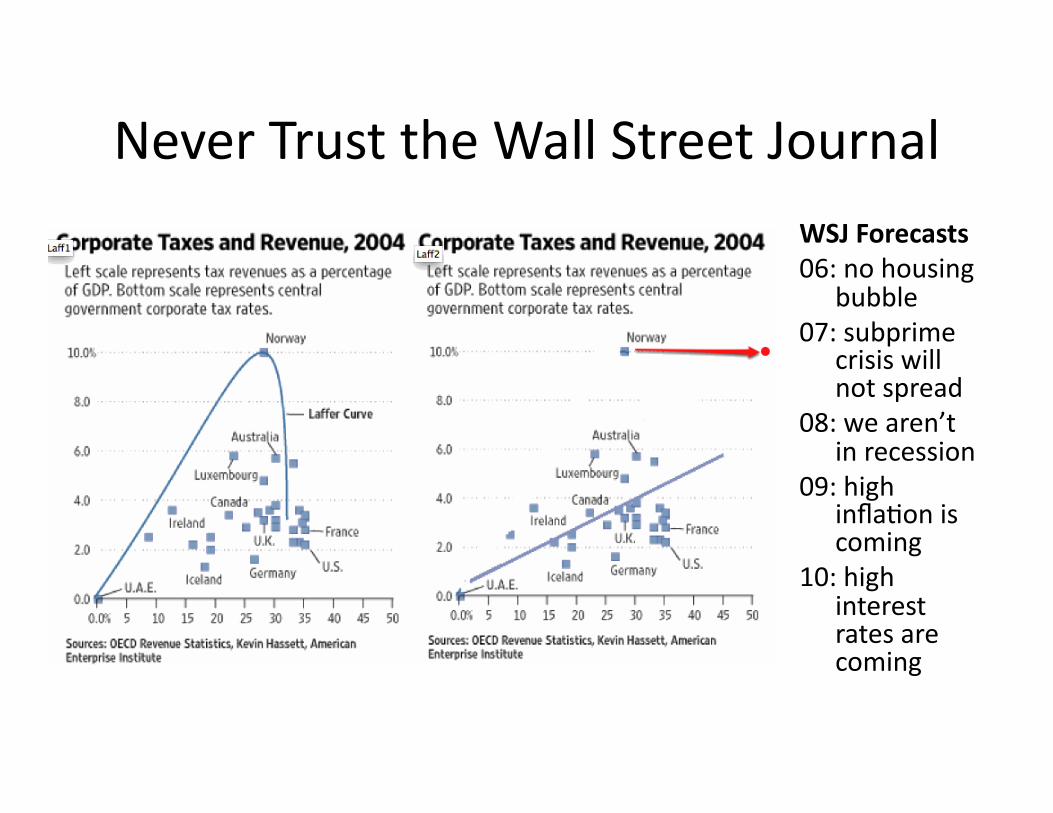

Never Trust the Wall Street Journal WSJ Forecasts 06: no housing

bubble 07: subprime

crisis will not spread

08: we aren’t in recession

09: high inflaWon is coming

10: high interest rates are coming

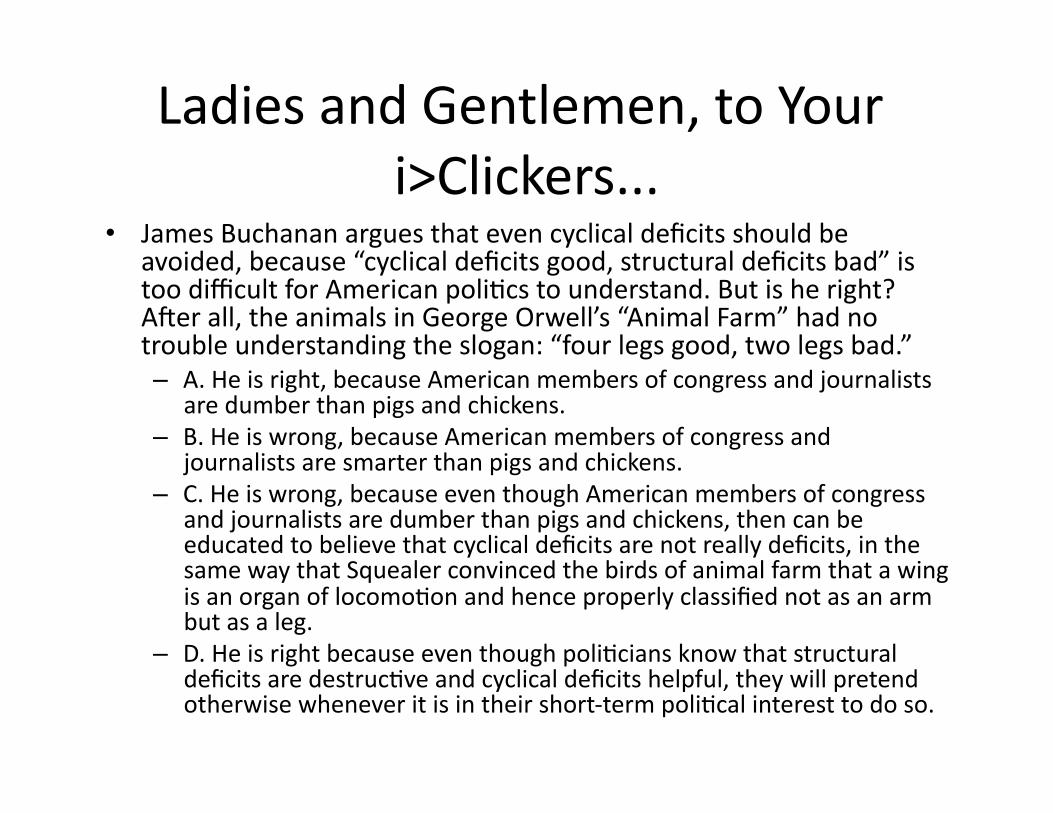

Ladies and Gentlemen, to Your i>Clickers...

• James Buchanan argues that even cyclical deficits should be avoided, because “cyclical deficits good, structural deficits bad” is too difficult for American poliWcs to understand. But is he right? AVer all, the animals in George Orwell’s “Animal Farm” had no trouble understanding the slogan: “four legs good, two legs bad.” – A. He is right, because American members of congress and journalists

are dumber than pigs and chickens. – B. He is wrong, because American members of congress and

journalists are smarter than pigs and chickens. – C. He is wrong, because even though American members of congress

and journalists are dumber than pigs and chickens, then can be educated to believe that cyclical deficits are not really deficits, in the same way that Squealer convinced the birds of animal farm that a wing is an organ of locomoWon and hence properly classified not as an arm but as a leg.

– D. He is right because even though poliWcians know that structural deficits are destrucWve and cyclical deficits helpful, they will pretend otherwise whenever it is in their short-‐term poliWcal interest to do so.

Test Your Knowledge • Since the interest rate on Treasury debt r is less than the

economy’s growth rate g, our budgetary situaWon is fine, except that we want short-‐term deficits in order to reduce cyclical unemployment—right?

• How do you calculate what the long-‐run debt-‐to-‐GDP raWo will be?

• Why is it important that a government run a primary surplus?

• Even if the naWonal debt is sustainable, why is it good to run a balanced budget—or even a surplus—over the business cycle?

• Why don’t governments run balanced budgets over the cycle?

• What is James Buchanan’s criWque of cyclical deficit spending?

• What is the Laffer curve? • Should you ever trust the Wall Street Journal?

Economics 1: Fall 2010: Economic Growth

J. Bradford DeLong

September 27, 2010, 12-‐1 Wheeler Auditorium, U.C. Berkeley

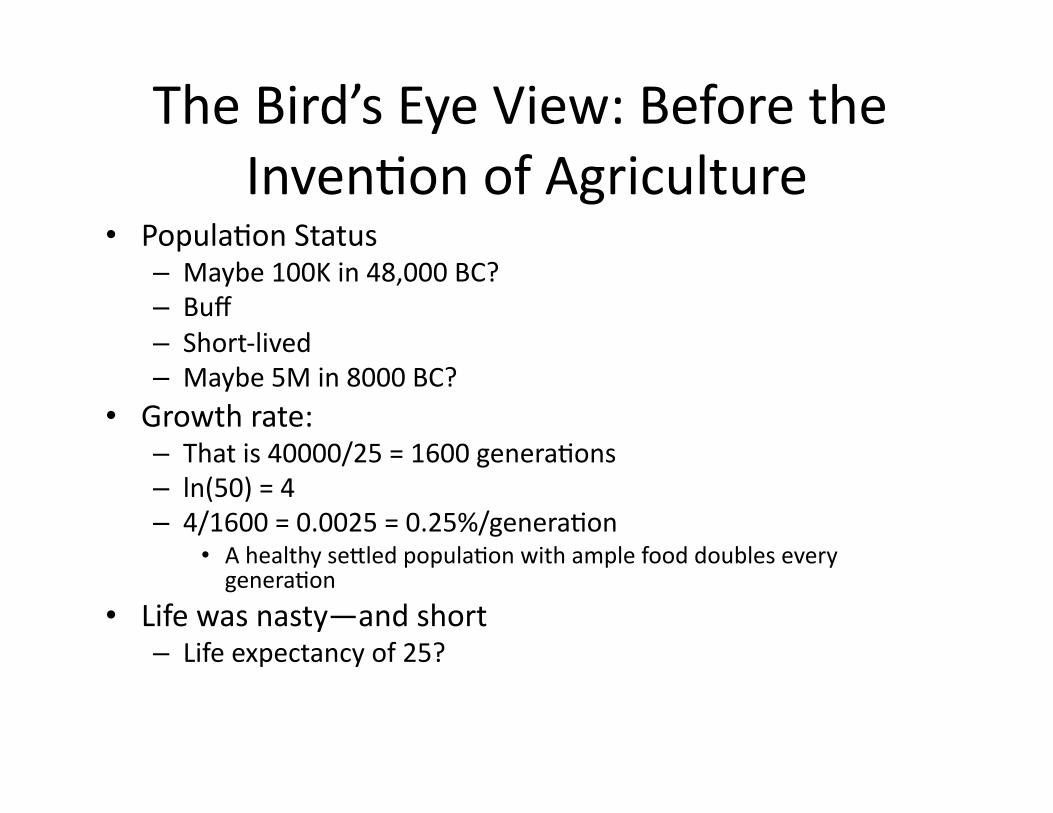

The Bird’s Eye View: Before the InvenWon of Agriculture

• PopulaWon Status – Maybe 100K in 48,000 BC? – Buff – Short-‐lived – Maybe 5M in 8000 BC?

• Growth rate: – That is 40000/25 = 1600 generaWons – ln(50) = 4 – 4/1600 = 0.0025 = 0.25%/generaWon

• A healthy seFled populaWon with ample food doubles every generaWon

• Life was nasty—and short – Life expectancy of 25?

The Bird’s Eye View: Agrarian SocieWes

• PopulaWon Status – Maybe 5M in 8200 BC? – Short: from 5’9” to 5’1”

• Upper classes different – Lose your teeth – Petri dishes for bacteria – Maybe 750M by 1800

• Growth rate: – That is 10000/25 = 400 generaWons – ln(150) = 5 – 5/400 = 0.0125 = 1.25%/generaWon

• A healthy seFled populaWon with ample food doubles every generaWon

• Life was bruWsh—and short – Life expectancy of 25? – And you are really bored – Your back doesn’t do too well either

Guessing at Some Numbers • Growth rates of populaWon

– HG: 0.01%/year – AS: 0.05%/year – >1800: 1.0%/year

• Growth rates of technological and organizaWonal knowledge – HG: ???? – AS: 0.01%/year – EM: 0.09%/year – IS: 2%/year

• Growth rates of global GDP – AS: 0.05%/year – EM: 0.2%/year – EIS: 1.4%/year – IS: 3.4%/year