2006 - grupocatalanaoccidente.com/media/files/g/grupo-cat... · - investment returns m. € 165 194...

TRANSCRIPT

1

2006 ANNUAL REPORT Grupo Catalana Occidente, S.A. and Subsidiaries

THE CATALANA OCCIDENTE CONSOLIDATED GROUP 3 YEAR’S SUMMARY AND KEY DATA 4 CONSOLIDATED DIRECTORS’ REPORT 6 BOARD OF DIRECTORS OF THE PARENT COMPANY 7 COMMERCIAL PERFORMANCE 8

Income 8 Portfolio Composition 8 Geographical Distribution 9 Sales Network – Agents 9

PROFIT FOR THE YEAR AND PROPOSED DISTRIBUTION 11

Profit for the year 11 Changes in Consolidated and Attributable Profit 11 Proposed Distribution of Profit 12 Shareholder Remuneration 12

PERFORMANCE OF THE BUSINESS BY AREAS OF ACTIVITY 13

Non-life insurance 13 Multirisk insurance 14 Auto insurance 15 Other 16 Reinsurance 18 Life, Pension Plans and Mutual Funds 19 General Expenses and Commissions 20 Agents’ Balances and Outstanding Premiums 20 Financial Result 21

BALANCE SHEET PERFORMANCE 22

Balance Sheet 22 Change in Equity 23 Technical Provisions and Coverage 23 Solvency Margin 24 Investments and Funds under Management 24 Investees 25

CORPORATE SOCIAL RESPONSABILITY 27

The group’s contribution to society 27 Customers 27 Group employees 28 Cultural and environmental policy 29 Technological development and investment in new technologies 29

INTERNAL CONTROL. Risk Control Systems 30 OUTLOOK FOR 2007: Strategy and Objectives. 31 STANDARDS AND LEGISLATION 32 STOCK MARKET DATA 34 AUDIT 35 CONSOLIDATED FINANCIAL STATEMENTS PREPARED IN ACCORDANCE WITH INTERNATIONAL FINANCIAL REPORTING STANDARDS

Consolidated Balance Sheets 36 Consolidated Income Statement 39 Segmental Consolidated Balance Sheets At 31 December 2006 40 Segmental Consolidated Income Statement 42 Statement of Recognised Income and Expense - Changes In Consolidated Equity 43 Consolidated Cash Flow Statement 44

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS PREPARED IN ACCORDANCE WITH INTERNATIONAL FINANCIAL REPORTING STANDARDS AUDITOR’S REPORT ON CONSOLIDATED FINANCIAL STATEMENTS

3

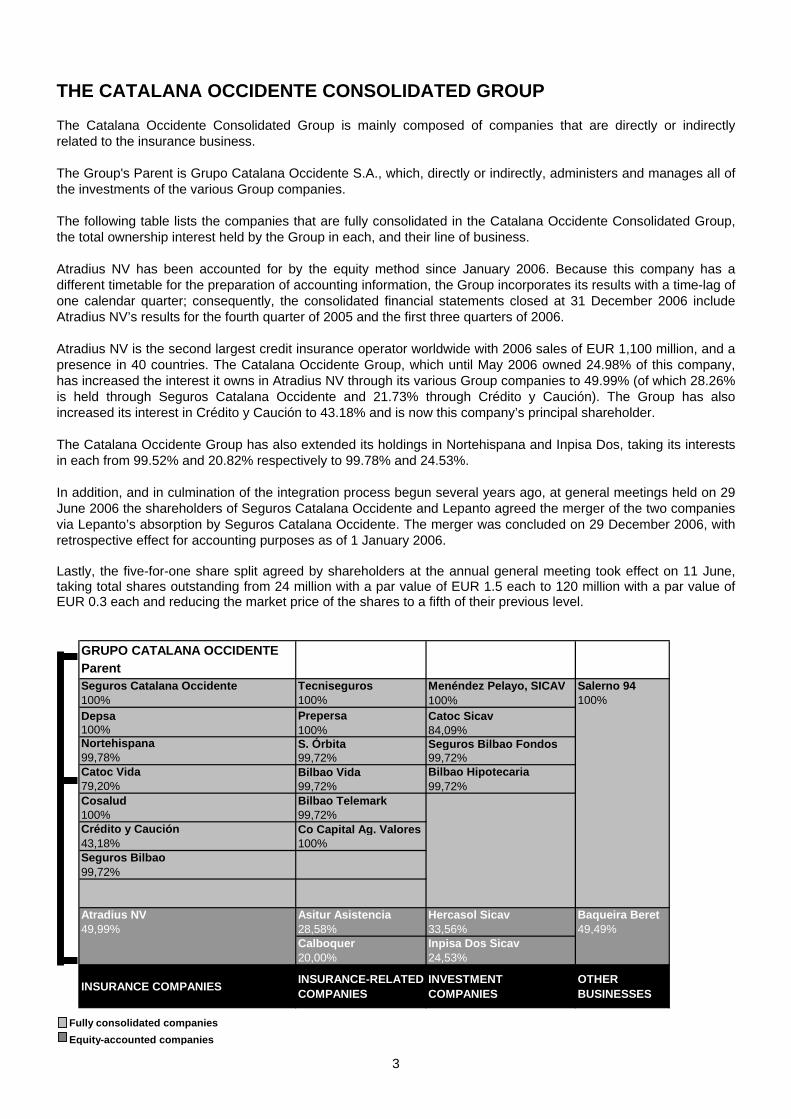

THE CATALANA OCCIDENTE CONSOLIDATED GROUP The Catalana Occidente Consolidated Group is mainly composed of companies that are directly or indirectly related to the insurance business. The Group's Parent is Grupo Catalana Occidente S.A., which, directly or indirectly, administers and manages all of the investments of the various Group companies. The following table lists the companies that are fully consolidated in the Catalana Occidente Consolidated Group, the total ownership interest held by the Group in each, and their line of business. Atradius NV has been accounted for by the equity method since January 2006. Because this company has a different timetable for the preparation of accounting information, the Group incorporates its results with a time-lag of one calendar quarter; consequently, the consolidated financial statements closed at 31 December 2006 include Atradius NV’s results for the fourth quarter of 2005 and the first three quarters of 2006. Atradius NV is the second largest credit insurance operator worldwide with 2006 sales of EUR 1,100 million, and a presence in 40 countries. The Catalana Occidente Group, which until May 2006 owned 24.98% of this company, has increased the interest it owns in Atradius NV through its various Group companies to 49.99% (of which 28.26% is held through Seguros Catalana Occidente and 21.73% through Crédito y Caución). The Group has also increased its interest in Crédito y Caución to 43.18% and is now this company’s principal shareholder. The Catalana Occidente Group has also extended its holdings in Nortehispana and Inpisa Dos, taking its interests in each from 99.52% and 20.82% respectively to 99.78% and 24.53%. In addition, and in culmination of the integration process begun several years ago, at general meetings held on 29 June 2006 the shareholders of Seguros Catalana Occidente and Lepanto agreed the merger of the two companies via Lepanto’s absorption by Seguros Catalana Occidente. The merger was concluded on 29 December 2006, with retrospective effect for accounting purposes as of 1 January 2006. Lastly, the five-for-one share split agreed by shareholders at the annual general meeting took effect on 11 June, taking total shares outstanding from 24 million with a par value of EUR 1.5 each to 120 million with a par value of EUR 0.3 each and reducing the market price of the shares to a fifth of their previous level.

GRUPO CATALANA OCCIDENTEParent Seguros Catalana Occidente Tecniseguros Menéndez Pelayo, SICAV Salerno 94100% 100% 100% 100%Depsa Prepersa Catoc Sicav100% 100% 84,09%Nortehispana S. Órbita Seguros Bilbao Fondos99,78% 99,72% 99,72%Catoc Vida Bilbao Vida Bilbao Hipotecaria79,20% 99,72% 99,72%Cosalud Bilbao Telemark100% 99,72%Crédito y Caución Co Capital Ag. Valores43,18% 100%Seguros Bilbao99,72%

Atradius NV Asitur Asistencia Hercasol Sicav Baqueira Beret49,99% 28,58% 33,56% 49,49%

Calboquer Inpisa Dos Sicav20,00% 24,53%

INSURANCE COMPANIES INSURANCE-RELATED COMPANIES

INVESTMENT COMPANIES

OTHER BUSINESSES

Fully consolidated companiesEquity-accounted companies

4

YEAR’S SUMMARY AND KEY DATA The Group had one of its best years ever in 2006. Consolidated profit and profit attributable to the Parent Company totalled EUR 250 million and EUR 191 million respectively, equating to advances of 42.2% and 39.1% on the already strong figures posted in 2005. Technical profit remained at a level similar to the prior year, thanks to a good business performance and excellent combined ratios in all non-life insurance lines. Equity-accounted investee Atradius NV was included in the scope of consolidation for the first time in 2006, with a consequent impact on the Group’s financial result that more than justified the decision to increase its interest in the associate. Total income rose to EUR 2,419 million, up 9.0%. Of this total, EUR 1.936 million corresponds to premiums billed, which were up 4.0%, EUR 138 million relates to pension plans and mutual funds, which advanced 43.0%, and EUR 345 million came from returns on investments, which showed a 31.6% increase. On the markets, 2006 was also a good year for Catalana Occidente. Having began the year at a price of EUR 14.72 (*), by the year-end the share had surged to EUR 27.45 per share — an annual rerating of EUR 12.73 per share, or return of 86.5%. The outlook and lines of action for 2007 remain generally the same as in prior years and, therefore, we continue working to boost internal growth, by developing our network of agents, to maintain current technical margins, which we consider to be extremely satisfactory, and to contain expenses by harnessing synergies between the various Group companies. Consequently, and given current trends on the financial markets, in 2007 we except to improve on the results we achieved in 2006, although, in a scenario of rising combined ratios, this will be largely dependant on our technical margins and ability to contain costs as synergies between the various Group companies are transformed into cost savings. (*) Price recalculated on the basis of 120,000,000 shares.

5

The table of key data above includes figures for 2004, 2005 and 2006 calculated on the basis of IFRSs. For the purposes of comparison with previous years, the table also includes historical data from 2002 to 2005 prepared according to Spanish GAAP. To prepare the information contained in this directors’ report, in accordance with the terms stated in the section on the application of International Accounting Standards, the standards approved at each of the 2004, 2005 and 2006 year-ends have been taken into account. This means that, for the data relating to the 2004 year-end, IFRSs 32 and 39 on the measurement of assets have not been taken into consideration.

% Change2002 2003 2004 2005 2004 2005 2006 04-05

INCOME- PREMIUMS M. € 1,298 1,300 1,730 1,862 1,730 1,862 1,936 4.0- PENS. PLAN AND MUTUAL FUND CONTRIBUTIONS M. € 24 31 60 97 60 97 138 43.0TOTAL PREMIUMS AND CONTRIBUTIONS M. € 1,322 1,331 1,790 1,959 1,790 1,959 2,074 5.9- INVESTMENT RETURNS M. € 165 194 238 229 253 261 345 31.6TOTAL INCOME M. € 1,487 1,525 2,028 2,188 2,043 2,220 2,419 9.0

EQUITY- SHARE CAPITAL M. € 36 36 36 36 36 36 36 -- EQUITY RESERVES AND VALUATION ADJUSTMENTS M. € 231 257 472 583 485 950 1,307 37.6TOTAL EQUITY M. € 267 293 508 619 521 986 1,343 36.2

TECHNICAL PROVISIONS M. € 2,970 3,159 4,447 4,746 4,399 4,613 4,864 5.4

TOTAL EQUITY ANDTECHNICAL PROVISIONS M. € 3,237 3,452 4,955 5,365 4,920 5,599 6,207 10.9

DISPOSABLEEQUITY M. € 681 750 863 1,057 979 1,246 1,667 33.8

E TOTAL FUNDS UNDER MANAGEMENT M. € 3,194 3,584 5,163 5,975 5,322 6,073 6,910 13.8

F CONSOLIDATED PROFIT M. € 41.0 76.4 113.9 145.4 127.5 175.5 249.5 42.2

NET PROFIT ATTRIBUTABLE TO MINORITY INTERESTS M. € 11.0 26.3 23.3 27.6 23.9 37.9 58.1 53.3TO PARENT COMPANY M. € 30.0 50.1 90.6 117.8 103.6 137.6 191.4 39.1

DATA PER SHAREPROFIT ATTRIBUTED TO PARENT € 0.25 0.42 0.76 0.98 0.86 1.15 1.59 39.1DIVIDEND PER SHARE € 0.20 0.20 0.20 0.29 0.22 0.29 0.40 37.0PAY-OUT % 77.6 48.9 29.7 29.7 25.9 25.5 25.2 -1.2

G

H

A

B

C

D

KEY DATA

IFRSsLOCAL SPANISH STANDARDS

6

GRUPO CATALANA OCCIDENTE, S.A. AND SUBSIDIARIES Consolidated Directors’ Report

7

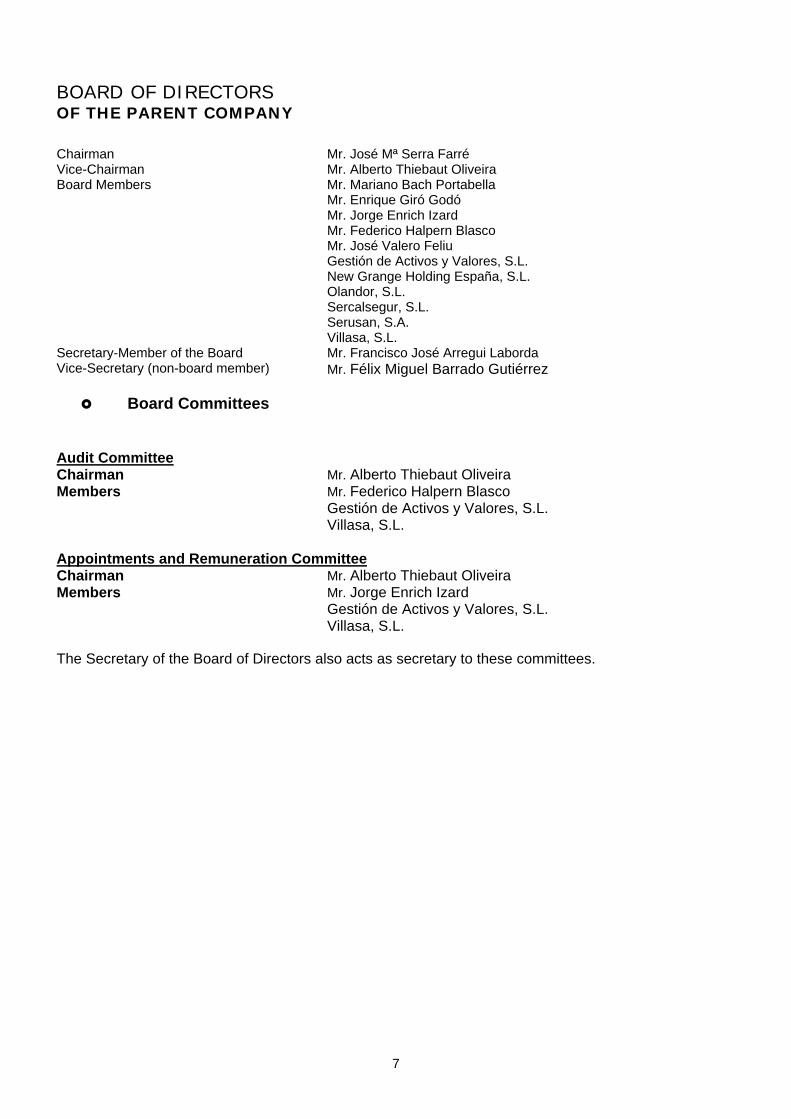

BOARD OF DIRECTORS OF THE PARENT COMPANY

Chairman Mr. José Mª Serra Farré Vice-Chairman Mr. Alberto Thiebaut Oliveira Board Members Mr. Mariano Bach Portabella Mr. Enrique Giró Godó Mr. Jorge Enrich Izard Mr. Federico Halpern Blasco Mr. José Valero Feliu Gestión de Activos y Valores, S.L. New Grange Holding España, S.L. Olandor, S.L. Sercalsegur, S.L. Serusan, S.A. Villasa, S.L. Secretary-Member of the Board Mr. Francisco José Arregui Laborda Vice-Secretary (non-board member) Mr. Félix Miguel Barrado Gutiérrez

Board Committees Audit Committee Chairman Mr. Alberto Thiebaut Oliveira Members Mr. Federico Halpern Blasco Gestión de Activos y Valores, S.L. Villasa, S.L. Appointments and Remuneration Committee Chairman Mr. Alberto Thiebaut Oliveira Members Mr. Jorge Enrich Izard Gestión de Activos y Valores, S.L. Villasa, S.L. The Secretary of the Board of Directors also acts as secretary to these committees.

8

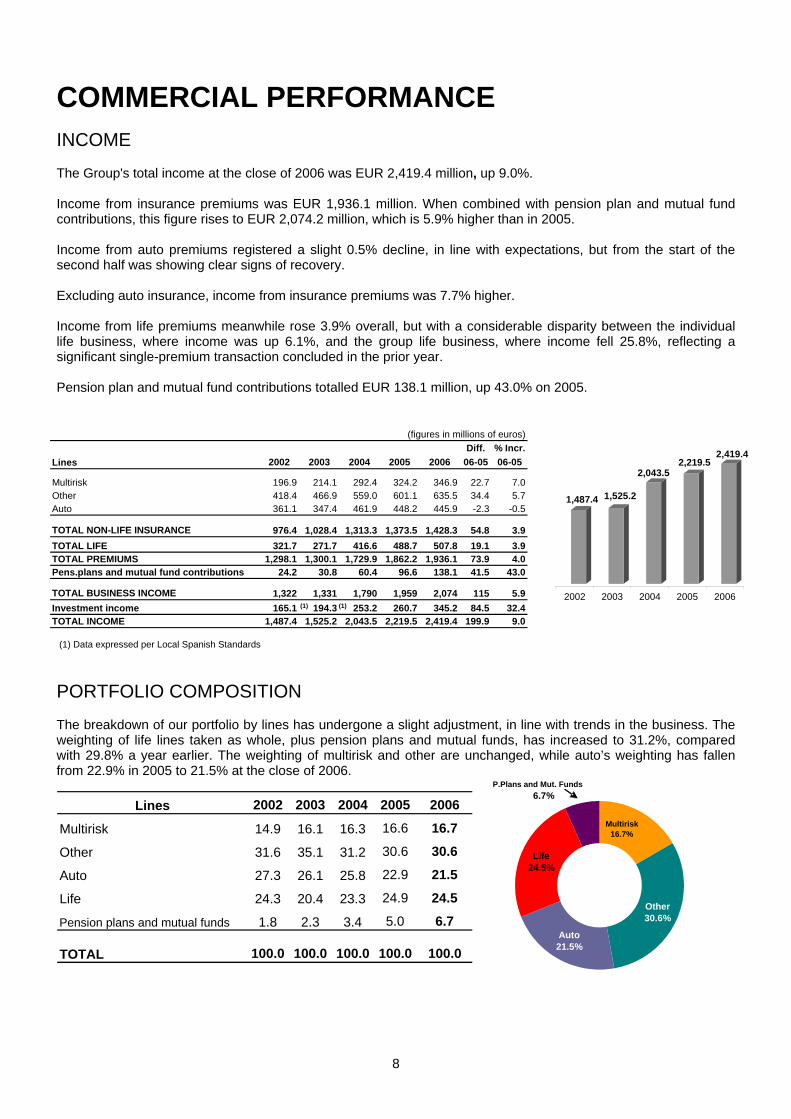

COMMERCIAL PERFORMANCE INCOME The Group's total income at the close of 2006 was EUR 2,419.4 million, up 9.0%. Income from insurance premiums was EUR 1,936.1 million. When combined with pension plan and mutual fund contributions, this figure rises to EUR 2,074.2 million, which is 5.9% higher than in 2005. Income from auto premiums registered a slight 0.5% decline, in line with expectations, but from the start of the second half was showing clear signs of recovery. Excluding auto insurance, income from insurance premiums was 7.7% higher. Income from life premiums meanwhile rose 3.9% overall, but with a considerable disparity between the individual life business, where income was up 6.1%, and the group life business, where income fell 25.8%, reflecting a significant single-premium transaction concluded in the prior year. Pension plan and mutual fund contributions totalled EUR 138.1 million, up 43.0% on 2005.

(1) Data expressed per Local Spanish Standards PORTFOLIO COMPOSITION The breakdown of our portfolio by lines has undergone a slight adjustment, in line with trends in the business. The weighting of life lines taken as whole, plus pension plans and mutual funds, has increased to 31.2%, compared with 29.8% a year earlier. The weighting of multirisk and other are unchanged, while auto’s weighting has fallen from 22.9% in 2005 to 21.5% at the close of 2006.

Lines 2002 2003 2004 2005 2006

Multirisk 14.9 16.1 16.3 16.6 16.7

Other 31.6 35.1 31.2 30.6 30.6

Auto 27.3 26.1 25.8 22.9 21.5

Life 24.3 20.4 23.3 24.9 24.5

Pension plans and mutual funds 1.8 2.3 3.4 5.0 6.7

TOTAL 100.0 100.0 100.0 100.0 100.0

Life24.5%

Multirisk16.7%

Other30.6%

Auto21.5%

P.Plans and Mut. Funds6.7%

Diff. % Incr.Lines 2002 2003 2004 2005 2006 06-05 06-05

Multirisk 196.9 214.1 292.4 324.2 346.9 22.7 7.0Other 418.4 466.9 559.0 601.1 635.5 34.4 5.7Auto 361.1 347.4 461.9 448.2 445.9 -2.3 -0.5

TOTAL NON-LIFE INSURANCE 976.4 1,028.4 1,313.3 1,373.5 1,428.3 54.8 3.9TOTAL LIFE 321.7 271.7 416.6 488.7 507.8 19.1 3.9TOTAL PREMIUMS 1,298.1 1,300.1 1,729.9 1,862.2 1,936.1 73.9 4.0Pens.plans and mutual fund contributions 24.2 30.8 60.4 96.6 138.1 41.5 43.0

TOTAL BUSINESS INCOME 1,322 1,331 1,790 1,959 2,074 115 5.9Investment income 165.1 194.3 253.2 260.7 345.2 84.5 32.4TOTAL INCOME 1,487.4 1,525.2 2,043.5 2,219.5 2,419.4 199.9 9.0

(figures in millions of euros)

(1) (1)

1,487.4 1,525.2

2,043.52,219.5

2,419.4

2002 2003 2004 2005 2006

9

GEOGRAPHICAL DISTRIBUTION The Catalana Occidente Group has a broad presence throughout Spain, with 1,037 offices at the close of 2006. In the course of 2006, Lepanto’s business was absorbed by Seguros Catalana Occidente. As a result both its agent sales network and the sales staff supervising the network have now been integrated into Seguros Catalana Occidente’s organisational structure. Accordingly, at the close of 2006, 14 former Lepanto offices that, because of their location, where deemed to duplicate those of Seguros Catalana Occidente were closed. The map below shows the distribution of the Group's offices across Spain, along with premiums billed and the percentage of volume business in Spain accounted for by each autonomous community. The Group has a particularly strong presence in the Mediterranean and Cantabrian coastal regions, reflecting, in the first case, the historical focus of the Group’s business development, and in the second, the greater volume of business generated in this region following the incorporation of Grupo de Seguros Bilbao

79 OfficesEUR 108.8 M.

5.2%

31 OfficesEUR 44,5M.

2.1%

15 OfficesEUR 26,6M.

1.3%

107 OfficesEUR 207,4 M.

10%

16 OfficesEUR 19,4 M.

0,9%

16 OfficesEUR 39,6 M.

1.9%

269 OfficesEUR 682,1 M.

32.9%

31 OfficesEUR 37,5M.

1,8%

50 OfficesEUR 47,9 M.

2.3%

59 OfficesEUR 68,4 M.

3.3%

53 OfficesEUR 228,6 M.

11%

12 OfficesEUR 16.8 M.

0,8%

111 OfficesEUR 204,7 M.

9.9%

114 OfficesSEUR 240,1 M.€

11.6%

45 OfficesEUR 68,9 M.€

3.3%

5 OfficesEUR 5 M.

0.1%

20 OfficesEUR 25.1 M.

1.2%

4 OfficesEUR 4.8 M.

0.2% SALES NETWORK – AGENTS The Catalana Occidente Group distributes its products mainly through highly qualified insurance agents who work exclusively with the Group. As in previous years, in 2006 initiatives were concentrated both on increasing the number of agents and improving productivity levels in sales activities. In addition, extensive employee training, the use of best sales practice across our network, product enhancements, competitive price/benefit ratios and systematic application of cutting-edge technologies all help ensure ongoing improvements in the productivity of our agents network every year. The Group also distributes its product and services through other agency or similar sales channels, including traditional agents and brokers. It also has a number of niche sales networks that are tailored to specific products, geographical areas or market segments.

EVOLUCIÓN COMERCIAL

10

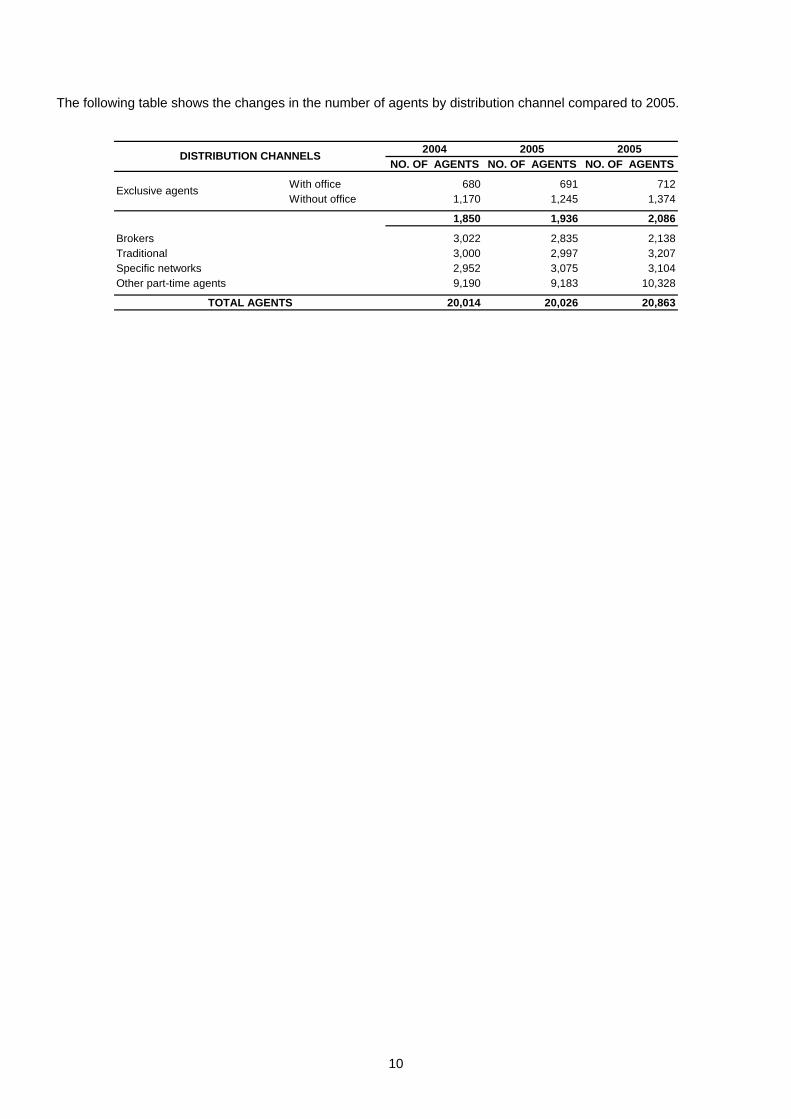

The following table shows the changes in the number of agents by distribution channel compared to 2005.

2004 2005 2005NO. OF AGENTS NO. OF AGENTS NO. OF AGENTS

With office 680 691 712Without office 1,170 1,245 1,374

1,850 1,936 2,086

Brokers 3,022 2,835 2,138Traditional 3,000 2,997 3,207Specific networks 2,952 3,075 3,104Other part-time agents 9,190 9,183 10,328

20,014 20,026 20,863

Exclusive agents

DISTRIBUTION CHANNELS

TOTAL AGENTS

11

INCOME STATEMENT 2004 2005 2006 % Incr.Premiums 1,729.9 1,862.2 1,936.2 4.0 Premiums acquired 1,720.7 1,853.8 1,915.0 3.3 Technical cost 1,394.6 1,427.1 1,482.1 3.9TECHNICAL RESULT 326.1 426.7 432.9 1.5As a % of premiums acquired 19.0% 23.0% 22.6%Expenses 239.9 256.2 264.1 3.1As a % of premiums acquired 13.9% 13.8% 13.8%TECHNICAL RESULT AFTER EXPENSES 86.2 170.5 168.8 -1.0As a % of premiums acquired 5.0% 9.2% 8.8%FINANCIAL RESULT (*) 75.0 62.4 135.5 117.3As a % of premiums acquired 4.2% 4.0% 7.1%PROFIT BEFORE TAXES 161.2 232.9 304.3 30.7As a % of premiums acquired 9.4% 12.6% 15.9%Corporation Tax 33.7 57.4 54.8 -4.4As a % of premiums acquired 2.0% 3.1% 2.9%PROFIT AFTER TAXES 127.5 175.5 249.5 42.2As a % of premiums acquired 7.4% 9.5% 13.0%ATTRIBUTABLE PROFIT 103.6 137.6 191.4 39.1 (*) Includes income and expenses from the non-technical account

(figures in millions of euros)

PROFIT FOR THE YEAR AND PROPOSED DISTRIBUTION PROFIT FOR THE YEAR The Catalana Occidente Consolidated Group recorded net profit of EUR 249.5 million in 2006, an advance of 42.2% on the EUR 175.5 million recognised in 2005. Profit attributable to the Parent amounted to EUR 191.4 million, up 39.1% on the 2005 figure of EUR 137.6 million. The significant earnings advances that the Group has posted for the second year running are underpinned by both good technical results, including excellent combined ratios, and strong financial results, in particular the contribution to earnings of investments in insurance companies incorporated within the scope of consolidation in the past few years. The following table shows the main items in the income statement for 2006, along with comparable data for the two previous years.

CHANGES IN CONSOLIDATED AND ATTRIBUTABLE PROFIT (*)

191.4

249.5

175.5

76.4

127.5

41.0

137.6

103.6

50.130.00

20406080

100120140160180200220240260280

2002 2003 2004 2005 2006

CONSOLIDATED PROFIT

ATTRIBUTED PROFIT

(*) Figures for 2002 and 2003 are calculated under Spanish GAAP. Figures for 2004, 2005 and 2006 are calculated on the basis of IFRSs.

12

PROPOSED DISTRIBUTION OF PROFIT The individual net profit of Grupo Catalana Occidente, S.A. was EUR 64.9 million. The following distribution will be proposed to shareholders at the Annual General Meeting: To dividends 48,000,000 To reserves 16,878,991

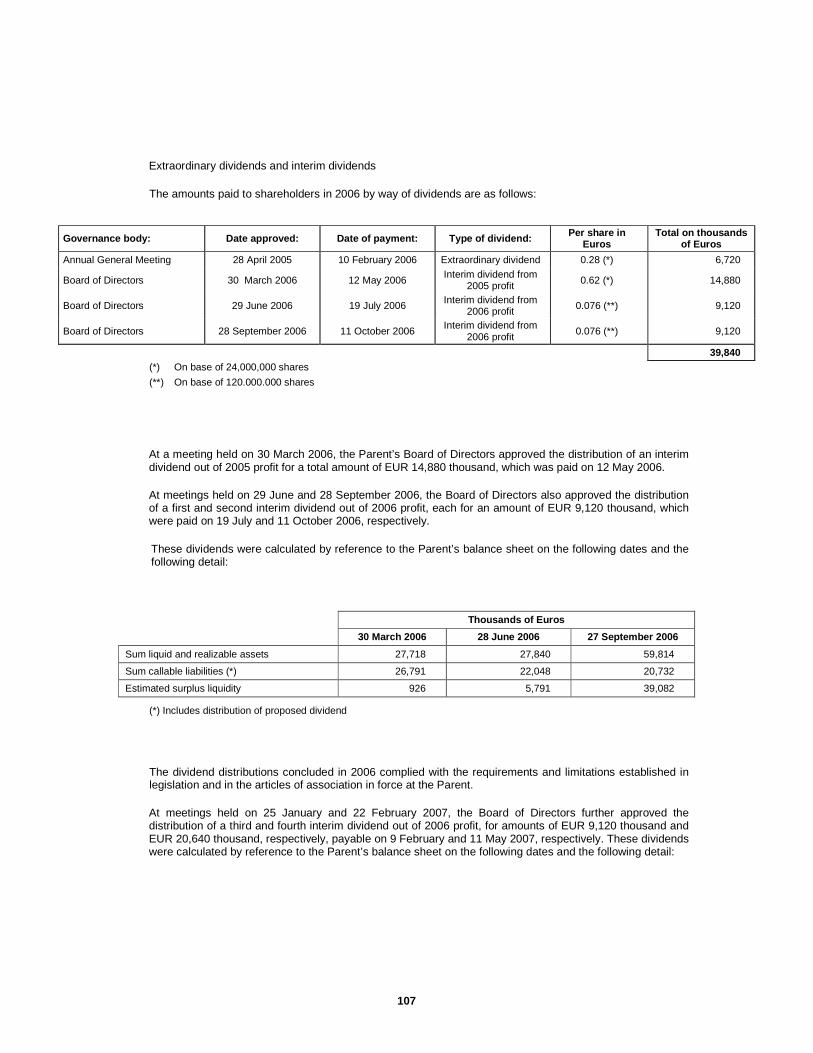

Total 64,878,991

SHAREHOLDER REMUNERATION In July and October 2006, and in February 2007, Grupo Catalana Occidente S.A. distributed interim dividends out of 2006 profit of EUR 0.076 per share. The total amount thus distributed was EUR 27,360,000. The Board of Directors has also resolved to distribute a further interim dividend of EUR 0.172 per share in May 2007, which will take the total distribution to EUR 20,640,000. At the Annual General Meeting, the Board of Directors intends to propose the distribution from 2006 earnings of a total dividend of EUR 0.4 per share, which is 37.0% more than the EUR 0.292 per share (*) distributed in the prior year. These dividends will be settled in full following distribution of the fourth interim dividend detailed above in May 2007. (*) Recalculated on the basis of 120 million shares.

% Incr.

July 2006 1st Interim dividend against 2006 profits 0.076 €

October 2006 2nd Interim dividend against 2006 profits 0.076 € 35.7%

February 2007 3rd Interim dividend against 2006 profits 0.076 €

May 2007 4th Interim dividend against 2006 profits 0.172 € 38.7%

TOTAL 0.400 € 37.0%

TOTAL DIVIDEND 48,000,000 €

Dividends Paid

13

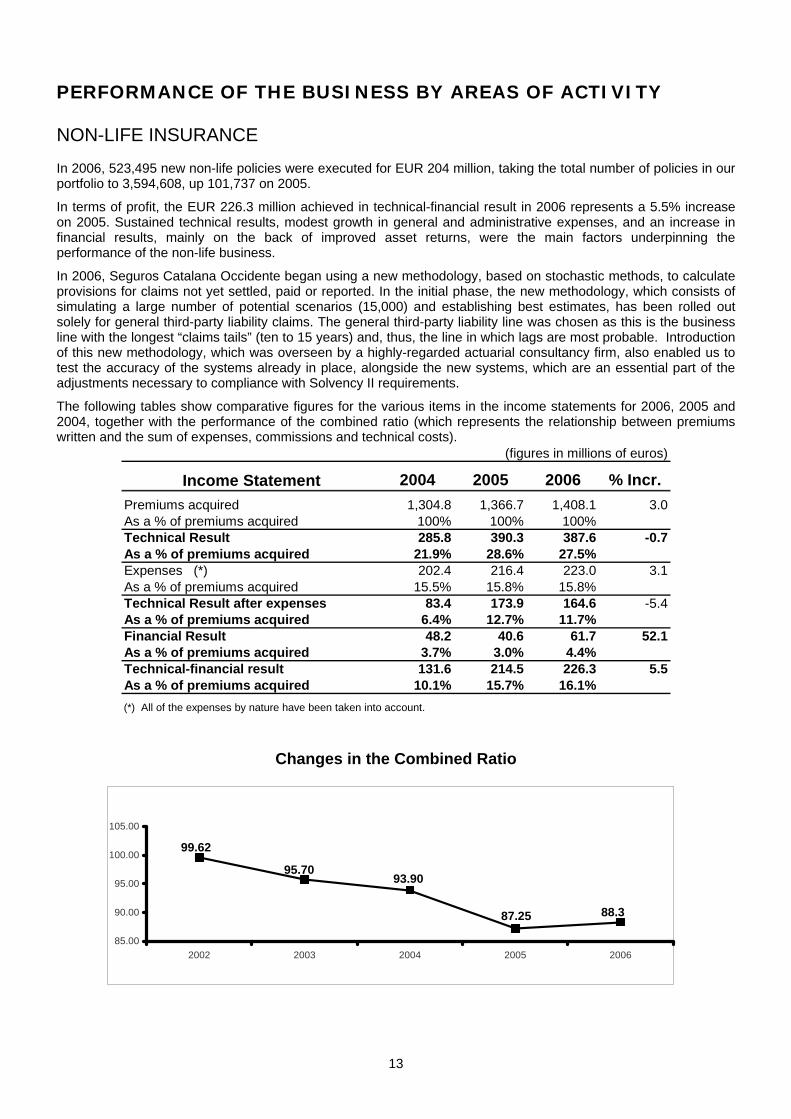

PERFORMANCE OF THE BUSINESS BY AREAS OF ACTIVITY NON-LIFE INSURANCE In 2006, 523,495 new non-life policies were executed for EUR 204 million, taking the total number of policies in our portfolio to 3,594,608, up 101,737 on 2005. In terms of profit, the EUR 226.3 million achieved in technical-financial result in 2006 represents a 5.5% increase on 2005. Sustained technical results, modest growth in general and administrative expenses, and an increase in financial results, mainly on the back of improved asset returns, were the main factors underpinning the performance of the non-life business. In 2006, Seguros Catalana Occidente began using a new methodology, based on stochastic methods, to calculate provisions for claims not yet settled, paid or reported. In the initial phase, the new methodology, which consists of simulating a large number of potential scenarios (15,000) and establishing best estimates, has been rolled out solely for general third-party liability claims. The general third-party liability line was chosen as this is the business line with the longest “claims tails” (ten to 15 years) and, thus, the line in which lags are most probable. Introduction of this new methodology, which was overseen by a highly-regarded actuarial consultancy firm, also enabled us to test the accuracy of the systems already in place, alongside the new systems, which are an essential part of the adjustments necessary to compliance with Solvency II requirements. The following tables show comparative figures for the various items in the income statements for 2006, 2005 and 2004, together with the performance of the combined ratio (which represents the relationship between premiums written and the sum of expenses, commissions and technical costs).

Income Statement 2004 2005 2006 % Incr.Premiums acquired 1,304.8 1,366.7 1,408.1 3.0As a % of premiums acquired 100% 100% 100%Technical Result 285.8 390.3 387.6 -0.7As a % of premiums acquired 21.9% 28.6% 27.5%Expenses (*) 202.4 216.4 223.0 3.1As a % of premiums acquired 15.5% 15.8% 15.8%Technical Result after expenses 83.4 173.9 164.6 -5.4As a % of premiums acquired 6.4% 12.7% 11.7%Financial Result 48.2 40.6 61.7 52.1As a % of premiums acquired 3.7% 3.0% 4.4%Technical-financial result 131.6 214.5 226.3 5.5As a % of premiums acquired 10.1% 15.7% 16.1%(*) All of the expenses by nature have been taken into account.

(figures in millions of euros)

Changes in the Combined Ratio

99.62

95.7093.90

87.25 88.3

85.00

90.00

95.00

100.00

105.00

2002 2003 2004 2005 2006

14

MULTIRISK INSURANCE The products includes in this business line are home/family, retail, shared buildings (communities), offices and SMEs Overall trends in these lines were very positive, reducing the combined ratio to 90.2% of premiums written, from 92.5% in 2005, which is a reduction of 2.3 percentage points. This movement in the combined ratio attests to solid and stable trends in the claims rate and in the costs associated with these products as a whole. The current level of our ratio (around 90%) puts us in the best possible position for growth in all these lines. Technical-financial result was EUR 44.5 million, up 46.9% on the 2005 figure of EUR 30.3 million. The following tables show the changes in the main figures for this group of lines.

2004 2005 2006 % Incr.

Policies sold 173,252 175,520 179,706 2.4Policies in the portfolio 1,298,319 1,329,562 1,359,586 2.3

Premiums sold € M. 44 47 52 9.9Premiums billed € M. 292 324 347 7.0

Claim counts 309,166 317,183 329,960 4.0Claim frequency (no.of claims per 100 policies) 24.1 24.1 24.5 1.7Average cost of claims Euros 468.2 528.8 516.5 -2.3

Total technical provisons € M. 251 276 292 5.8

% technical costs % 55.3 56.9 54.1 -4.8% commissions % 20.2 19.8 20.6 3.8% general expenses % 16.9 15.8 15.5 -2.0% Total = Combined ratio % 92.4 92.5 90.2 -2.5

Income Statement 2004 2005 2006 % Incr.Premiums acquired 284.4 313.4 336.3 7.3As a % of premiums acquired 100% 100% 100%Technical result 69.0 73.2 85.2 16.4As a % of premiums acquired 24.2% 23.4% 25.3%Expenses 47.3 49.6 52.1 5.0As a % of premiums acquired 16.6% 15.8% 15.5%Technical result after expenses 21.7 23.6 33.1 40.6As a % of premiums acquired 7.6% 7.5% 9.8%Financial result 7.6 6.7 11.4 69.2As a % of premiums acquired 2.7% 2.1% 3.4%Technical income - financial result 29.3 30.3 44.5 46.9As a % of premiums acquired 10.3% 9.6% 13.2%

(figures in millions of euros)

15

90.292.4392.66

99.199.3

75.00

80.00

85.00

90.00

95.00

100.00

105.00

2002 2003 2004 2005 2006

Changes in the Combined Ratio

AUTO INSURANCE The auto business' performance in the year was uneven, as mentioned earlier in this report. At the close of 2006, at EUR 446 million, sales in this line were a slight 0.5% down on the 2005 level. Despite this decline, sales trends were very positive, as the table below shows, with net increases in the number of premiums from March onwards. Albeit with a certain time lag, premiums billed also showed monthly advances from the second half, although in the full-year figures these advances are offset by the declines recorded in the first six months. The combined ratio rose to 94.5% — a 4.9 point uptick attributable to, firstly, the fact that overall premiums billed were practically the same as in the previous year, and, secondly, the fact that costs (claims and expenses) increased modestly, reflecting both inflation and an increased number of claims due to the increased number of vehicles insured. Technical-financial result was EUR 47 million, compared with EUR 64.9 million in 2005. The following tables show the changes in the main figures for this group of lines.

2004 2005 2006 % Incr.

Policies sold 159,453 187,206 212,492 13.5Policies in the portfolio 1,154,138 1,136,173 1,155,295 1.7

Premiums sold € M. 80 82 90 9.8Premiums billed € M. 462 448 446 -0.5

Claim counts 261,320 249,874 244,864 -2.0Claim frequency (no.of claims per 100 policies) 22.2 21.8 22.5 3.2Average cost of claims Euros 1,218.6 1,077.7 1,054.4 -2.2

Total technical provisons € M. 649 621 605 -2.6

% technical costs % 69.5 59.3 62.2 4.8% commissions % 12.0 12.2 13.2 8.4% general expenses % 17.0 18.1 19.1 5.4% Total = Combined ratio % 98.5 89.6 94.5 5.4

16

Changes in the Combined Ratio

94.589.6

98.5101.2

104.6

75.00

80.00

85.00

90.00

95.00

100.00

105.00

110.00

2002 2003 2004 2005 2006

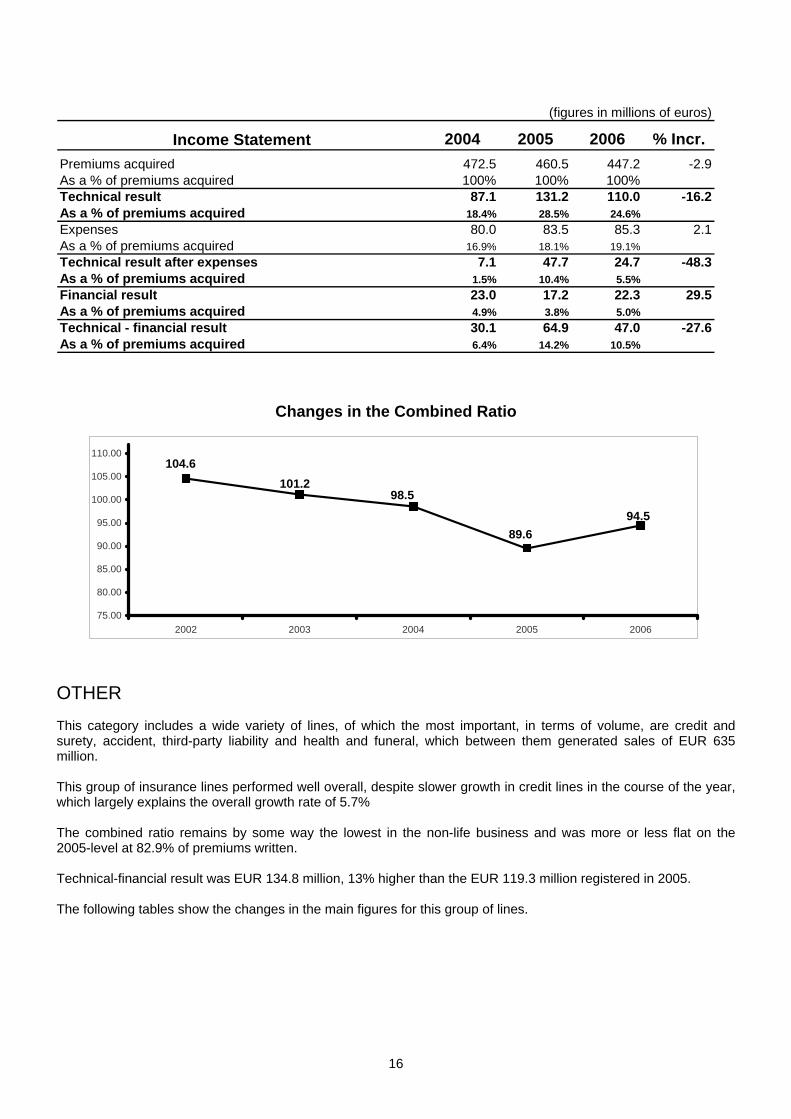

OTHER This category includes a wide variety of lines, of which the most important, in terms of volume, are credit and surety, accident, third-party liability and health and funeral, which between them generated sales of EUR 635 million. This group of insurance lines performed well overall, despite slower growth in credit lines in the course of the year, which largely explains the overall growth rate of 5.7% The combined ratio remains by some way the lowest in the non-life business and was more or less flat on the 2005-level at 82.9% of premiums written. Technical-financial result was EUR 134.8 million, 13% higher than the EUR 119.3 million registered in 2005. The following tables show the changes in the main figures for this group of lines.

Income Statement 2004 2005 2006 % Incr.Premiums acquired 472.5 460.5 447.2 -2.9As a % of premiums acquired 100% 100% 100%Technical result 87.1 131.2 110.0 -16.2As a % of premiums acquired 18.4% 28.5% 24.6%Expenses 80.0 83.5 85.3 2.1As a % of premiums acquired 16.9% 18.1% 19.1%Technical result after expenses 7.1 47.7 24.7 -48.3As a % of premiums acquired 1.5% 10.4% 5.5%Financial result 23.0 17.2 22.3 29.5As a % of premiums acquired 4.9% 3.8% 5.0%Technical - financial result 30.1 64.9 47.0 -27.6As a % of premiums acquired 6.4% 14.2% 10.5%

(figures in millions of euros)

17

2004 2005 2006 % Incr.

Policies sold 110,191 116,149 131,297 13.0Policies in the portfolio 999,007 1,027,136 1,079,727 5.1

Premiums sold € M. 53 58 62 7.0Premiums billed € M. 559 602 635 5.7

Claim counts 127,288 136,344 149,400 9.6Claim frequency (no.of claims per 100 policies) 13.1 13.5 14.2 5.2Average cost of claims Euros 2,161.8 2,235.7 2,172.6 -2.8

Total technical provisons € M. 862 750 820 9.3

% technical costs % 63.9 55.9 56.2 0.6% commissions % 12.4 12.8 13.0 1.7% general expenses % 13.7 14.0 13.7 -2.3% Total = Combined ratio % 90.0 82.7 82.9 0.3

Income Statement 2004 2005 2006 % Incr.Premiums acquired 547.9 593.0 624.6 5.3As a % of premiums acquired 100% 100% 100%Technical result 129.7 185.9 192.4 3.5As a % of premiums acquired 23.7% 31.4% 30.8%Expenses 75.1 83.2 85.6 2.9As a % of premiums acquired 13.7% 14.0% 13.7%Technical result after expenses 54.6 102.7 106.7 4.0As a % of premiums acquired 10.0% 17.3% 17.1%Financial result 17.6 16.6 28.1 69.3As a % of premiums acquired 3.2% 2.8% 4.5%Technical - financial result 72.2 119.3 134.8 13.0As a % of premiums acquired 13.2% 20.1% 21.6%

(figures in millions of euros)

Changes in the Combined Ratio

95.00

89.70 90.00

82.70 82.90

75.00

80.00

85.00

90.00

95.00

100.00

2001 2002 2003 2004 2005

18

REINSURANCE Outward reinsurance premiums totalled EUR 219.3 million, a slight 2.7% fall on 2005. This fall contrasts with a 4% increase in business recorded and is a testament to the policy of increasing business retention we have implemented in the last few years given the quality of our risk portfolio. The Group continues to maintain and, in some cases, to surpass, where possible, the rating of the reinsurance companies in the various reinsurers panels. In particular, Münchener, General Re and Swiss Re, which are the main lead insurers in our reinsurers panels, have A+, AAA and AA ratings, respectively. The other companies’ ratings are between AAA and A-. The following table shows the main figures relating to outward reinsurance.

Income 2004 2005 2006 % Incr.

Outward premiums € M. 226.1 225.4 219.3 -2.7

Increase in provision for unearned premiums € M. -6.2 -0.1 -4.2

Commissions € M. 69.2 67.4 70.4 4.5

Cost of outward reinsurance € M. 163.1 158.1 153.1 -3.2

Loss ratio % 121.0 121.1 128.9 6.4

Total cost of reinsurance € M. 42.1 37.0 24.2 -34.6

19

LIFE, PENSION PLANS AND MUTUAL FUNDS Turnover and Results All life products, irrespective of whether the financial risk is borne by the Group or by the policyholder, are included in this line. Because of their similar features to life products, pension plans and mutual funds are also included in this line.

Sales of this group of products were 10.2% higher overall, at EUR 646 million. Of this total, EUR 508 million was generated by premiums while EUR 1378 million came from contributions to pension plans and mutual funds. Technical-financial result was EUR 20.5 million, up 21.6% on 2005. The following table shows the main figures for the line.

2004 2005 2006 % Incr.

Policies sold, pension plans and mutual funds 95,391 103,142 109,919 6.6Policies in the portfolio 435,985 437,562 457,700 4.6

Premiums sold, pension plan and mutual fund contributions € M. 246 317 386 21.8Premiums billed € M. 417 488 508 4.1

Claim count 53,332 63,145 65,591 3.9

Volume of managed funds in:

Mathematical provisions and unpaid claims € M. 2,542.4 2,667.0 2,775.0 4.0 Pension plans and mutual funds € M. 285.8 361.0 474.0 31.3

Income Statement 2004 2005 2006 % Incr.Premiums acquired 415.9 486.9 506.9 4.1As a % of premiums acquired 100.0% 100.0% 100.0%Technical result 40.3 36.3 45.3 24.6As a % of premiums acquired 9.7% 7.5% 8.9%Expenses 37.4 39.7 41.0 3.2As a % of premiums acquired 9.0% 8.2% 8.1%Technical result after expenses 2.9 -3.4 4.3 -As a % of premiums acquired 0.7 -0.7 0.8Financial result 21.5 20.3 16.2 -20.0As a % of premiums acquired 5.2% 4.2% 3.2%Technical-financial result 24.4 16.9 20.5 21.6As a % of premiums acquired 5.9% 3.5% 4.0%

(figures in millions of euros)

20

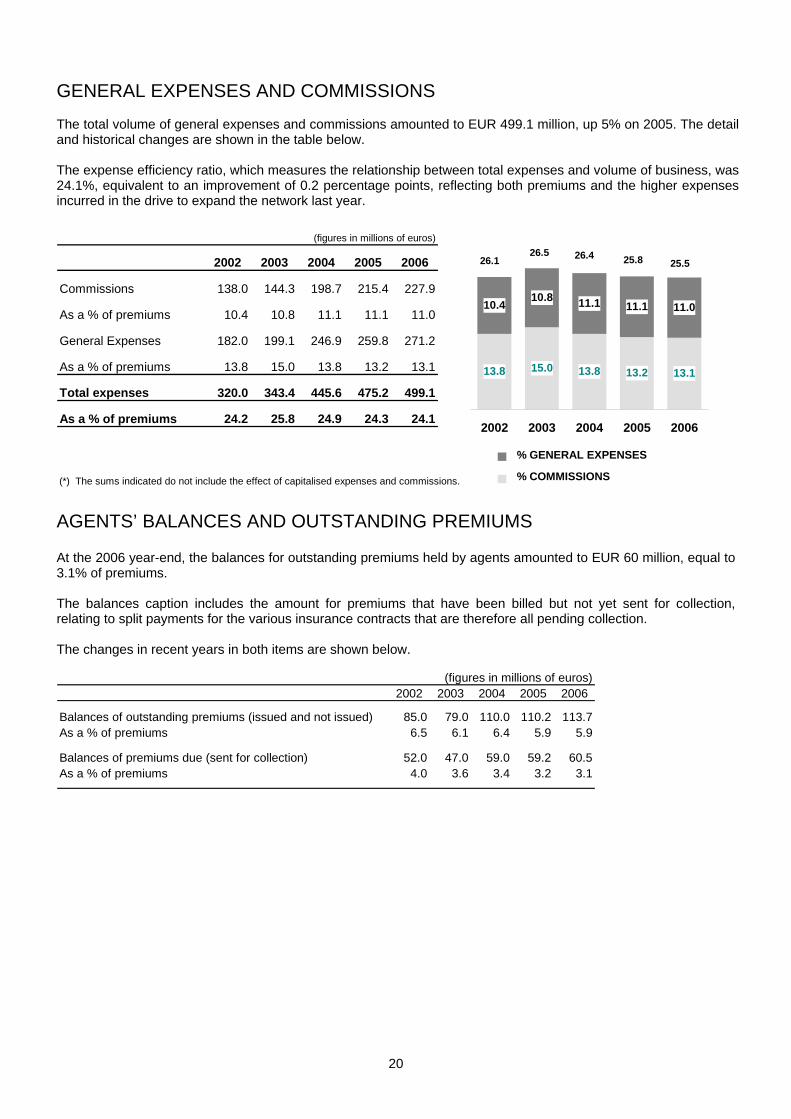

GENERAL EXPENSES AND COMMISSIONS The total volume of general expenses and commissions amounted to EUR 499.1 million, up 5% on 2005. The detail and historical changes are shown in the table below. The expense efficiency ratio, which measures the relationship between total expenses and volume of business, was 24.1%, equivalent to an improvement of 0.2 percentage points, reflecting both premiums and the higher expenses incurred in the drive to expand the network last year.

2002 2003 2004 2005 2006

Commissions 138.0 144.3 198.7 215.4 227.9

As a % of premiums 10.4 10.8 11.1 11.1 11.0

General Expenses 182.0 199.1 246.9 259.8 271.2

As a % of premiums 13.8 15.0 13.8 13.2 13.1

Total expenses 320.0 343.4 445.6 475.2 499.1

As a % of premiums 24.2 25.8 24.9 24.3 24.1

(*) The sums indicated do not include the effect of capitalised expenses and commissions.

(figures in millions of euros)

13.8 15.0 13.8 13.2

10.410.8 11.1 11.1 11.0

13.1

2002 2003 2004 2005 2006

26.126.5 26.4 25.8 25.5

% COMMISSIONS

% GENERAL EXPENSES

AGENTS’ BALANCES AND OUTSTANDING PREMIUMS At the 2006 year-end, the balances for outstanding premiums held by agents amounted to EUR 60 million, equal to 3.1% of premiums. The balances caption includes the amount for premiums that have been billed but not yet sent for collection, relating to split payments for the various insurance contracts that are therefore all pending collection. The changes in recent years in both items are shown below.

2002 2003 2004 2005 2006

Balances of outstanding premiums (issued and not issued) 85.0 79.0 110.0 110.2 113.7As a % of premiums 6.5 6.1 6.4 5.9 5.9

Balances of premiums due (sent for collection) 52.0 47.0 59.0 59.2 60.5As a % of premiums 4.0 3.6 3.4 3.2 3.1

(figures in millions of euros)

21

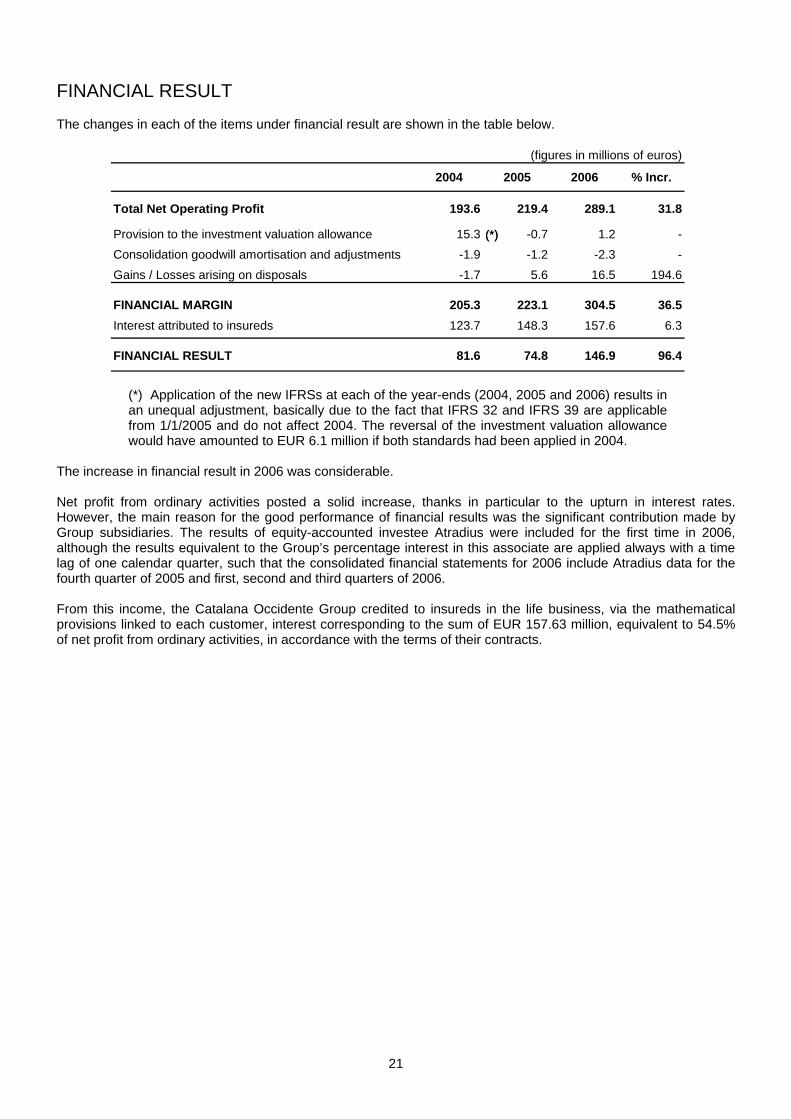

FINANCIAL RESULT The changes in each of the items under financial result are shown in the table below.

2004 2005 2006 % Incr.

Total Net Operating Profit 193.6 219.4 289.1 31.8

Provision to the investment valuation allowance 15.3 -0.7 1.2 -Consolidation goodwill amortisation and adjustments -1.9 -1.2 -2.3 -Gains / Losses arising on disposals -1.7 5.6 16.5 194.6

FINANCIAL MARGIN 205.3 223.1 304.5 36.5Interest attributed to insureds 123.7 148.3 157.6 6.3

FINANCIAL RESULT 81.6 74.8 146.9 96.4

(figures in millions of euros)

(*)(*)

(*) Application of the new IFRSs at each of the year-ends (2004, 2005 and 2006) results in an unequal adjustment, basically due to the fact that IFRS 32 and IFRS 39 are applicable from 1/1/2005 and do not affect 2004. The reversal of the investment valuation allowance would have amounted to EUR 6.1 million if both standards had been applied in 2004.

The increase in financial result in 2006 was considerable. Net profit from ordinary activities posted a solid increase, thanks in particular to the upturn in interest rates. However, the main reason for the good performance of financial results was the significant contribution made by Group subsidiaries. The results of equity-accounted investee Atradius were included for the first time in 2006, although the results equivalent to the Group’s percentage interest in this associate are applied always with a time lag of one calendar quarter, such that the consolidated financial statements for 2006 include Atradius data for the fourth quarter of 2005 and first, second and third quarters of 2006. From this income, the Catalana Occidente Group credited to insureds in the life business, via the mathematical provisions linked to each customer, interest corresponding to the sum of EUR 157.63 million, equivalent to 54.5% of net profit from ordinary activities, in accordance with the terms of their contracts.

22

BALANCE SHEET PERFORMANCE BALANCE SHEET Movement in the balance sheet and the main component asset and liability headings are summarised in the table below. To interpret this data correctly, it must be remembered that, in its application of IFRSs, the Catalana Occidente Consolidated Group has elected to continue recognising all property investments at amortised cost rather than at market value, and that this situation is reflected in the balance sheet below.

2004 2005 2006

Intangible Assets and Property, Plant and Equipment 371.6 376.4 393.1Investments 4,190.7 5,088.8 5,673.9Reinsurance Share of Technical Provisions 302.4 292.8 296.6Deferred Tax Assets 24.3 24.3 14.1Receivables 252.5 258.7 297.6Prepayments and Accrued Income and Other 118.4 115.5 106.6

T O T A L A S S E T S 5,259.9 6,156.5 6,781.9

Equity 521.2 985.6 1,343.2Technical Provisions 4,398.7 4,613.1 4,863.8Other Provisions 63.1 70.8 78.4Deposits received for outward reinsurance 57.7 56.1 52.3Deferred Tax Liabilities 2.6 188.1 194.0Payables 203.4 229.6 236.9Accrued Expenses and Deferred Income and Other 13.2 13.2 13.3T O T A L E Q U I T Y A N D L I A B I L I T I E S 5,259.9 6,156.5 6,781.9

(figures in millions of euros)

A S S E T S

E Q U I T Y A N D L I A B I L I T I E S

Balance Sheet

23

CHANGE IN EQUITY At the close of 2006, the Catalana Occidente Consolidated Group had equity of EUR 1,344.1 million, which was EUR 358.5 million more than at the close of 2005.

EQUITY at 31/12/2005 985.6

(+) Consolidated results for 2006 249.5

(+) Dividends paid -39.8

(+) Movement treasury shares +/- results -4.2

(+) Change in Valuation Adjustments (capital gains) 47.6

(+) Change in pension funds -4.2

(+) Changes valuation of holdings in subsidiaries 108.7

TOTAL movements for the year 357.6

TOTAL EQUITY at 31/12/2006 1,343.2

(figures in millions of euros)

TREASURY SHARES In 2006, the subsidiary Salerno 94 S.A. acquired 289,765 shares and sold 103,170 shares in Grupo Catalana Occidente, thereby increasing the volume of its investment by EUR 5,145,457 and consequently recording an addition to the restricted reserve under Article 79 of Consolidated Spanish Corporations Law for the same amount. At year-end the Group owned 1.60% of its own shares. In accordance with the new IFRSs, gains or losses on the disposal of treasury shares must be adjusted and may not be accounted for as an increase in profit or loss for the year, as appropriate, but must be recognised directly as an increase or decrease in Equity. TECHNICAL PROVISIONS AND COVERAGE International Financial Reporting Standards establish no specific criteria relating to technical provisions and their coverage. To ensure continuity with information published prior to application of IFRSs, the Catalana Occidente Consolidated Group has prepared the following information on technical provisions and coverage using methodologies established under Spanish GAAP but amounts drawn from the consolidated figures prepared under IFRSs. On this basis, the Group has assumed commitments with third parties, which are recognised under technical provisions and corrected for other receivables and payables, in the amount of EUR 4,634.3 million. Eligible asset totalled EUR 6,222.0 at the close of 2006. This amount represents the market value of the assets as determined in accordance with established measurement criteria. It may be deduced from the above that the Group’s assets exceed its liabilities by EUR 1,587.7 million, with the coverage surplus having thus increased by EUR 232.5 million relative to the prior-year level.

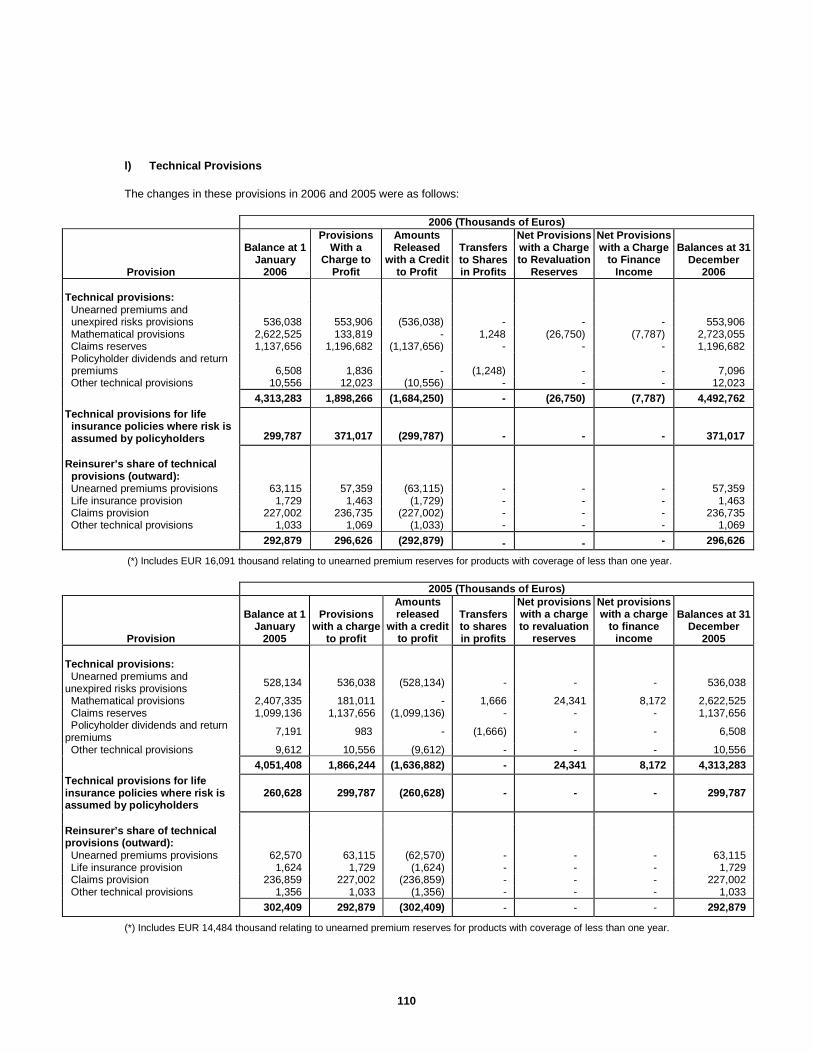

24

The status of coverage by technical provisions at the close of 2006 and the changes over the past few years are shown in the following table.

2004 2005 2006

Technical provisions to be materialised 4,161.0 4,377.2 4,635.0

Eligible assets 4,990.0 5,731.7 6,222.0

Coverage surplus 829.0 1,354.5 1,587.0

(figures in millions of euros)

SOLVENCY MARGIN As in the case of technical provisions detailed above, IFRSs also establish no specific criteria for calculating the minimum capital requirement necessary to the activities performed on the basis of risks assumed. Until the new Solvency II requirements are formalised and a new methodology for their calculation is available, the Group has applied the methodology established in the current private insurance regulations, using data prepared in accordance with IFRSs. The following table shows movement in the consolidated solvency margin over the past three years.

2004 2005 2006

Disposable equity 979.4 1,245.8 1,666.7

Minimum solvency margin 327.5 321.5 337.5

Surplus solvency margin 651.9 924.3 1,329.2

Disposable equity as a % of minimum requirement 299.1 387.5 493.8

(figures in millions of euros)

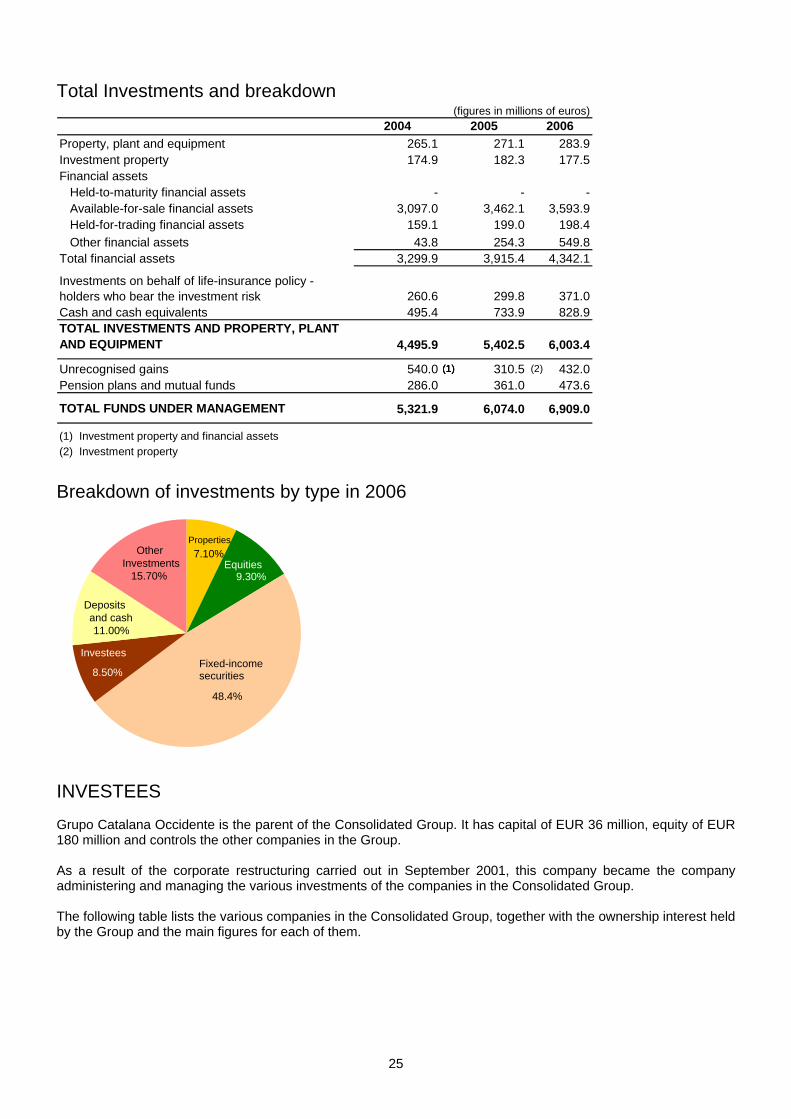

INVESTMENTS AND FUNDS UNDER MANAGEMENT Total investments made by the Group amounted to EUR 6.004 million, up 11.1% on 2005. Including investments corresponding to pension plans and mutual funds, and unrecognised capital gains on property, total funds under management come to EUR 6,910 million, up 13.8%. It should be taken into account that IFRS 32 and 29 on the measurement of assets were not applied in 2004. It must also be taken into account that the application of IAS 16 and IAS 40 on the measurement of investment property, also allows various options, from measuring properties at amortised cost, as under Spanish legislation, to measuring some or all of them at market value. In this first stage of application of IFRSs, the Group has chosen to measure properties at amortised cost as this is the most prudent option and because, under the above-mentioned IFRS, properties can always be restated to market value, but may not be accounted for at amortised cost once the values have been restated. At the 2004, 2005 and 2006 year-ends, unrecognised gains on properties amounted to EUR 258 million, EUR 310 million and EUR 432 million respectively.

25

Fixed-income securities

48.4%

Equities9.30%

Properties7.10% Other

Investments15.70%

Deposits and cash11.00%

Investees

8.50%

Total Investments and breakdown

2004 2005 2006Property, plant and equipment 265.1 271.1 283.9Investment property 174.9 182.3 177.5Financial assets Held-to-maturity financial assets - - - Available-for-sale financial assets 3,097.0 3,462.1 3,593.9 Held-for-trading financial assets 159.1 199.0 198.4 Other financial assets 43.8 254.3 549.8Total financial assets 3,299.9 3,915.4 4,342.1

Investments on behalf of life-insurance policy -holders who bear the investment risk 260.6 299.8 371.0Cash and cash equivalents 495.4 733.9 828.9TOTAL INVESTMENTS AND PROPERTY, PLANT AND EQUIPMENT 4,495.9 5,402.5 6,003.4

Unrecognised gains 540.0 310.5 432.0Pension plans and mutual funds 286.0 361.0 473.6

TOTAL FUNDS UNDER MANAGEMENT 5,321.9 6,074.0 6,909.0

(1) Investment property and financial assets(2) Investment property

(figures in millions of euros)

(1) (2)(1)(1)

Breakdown of investments by type in 2006

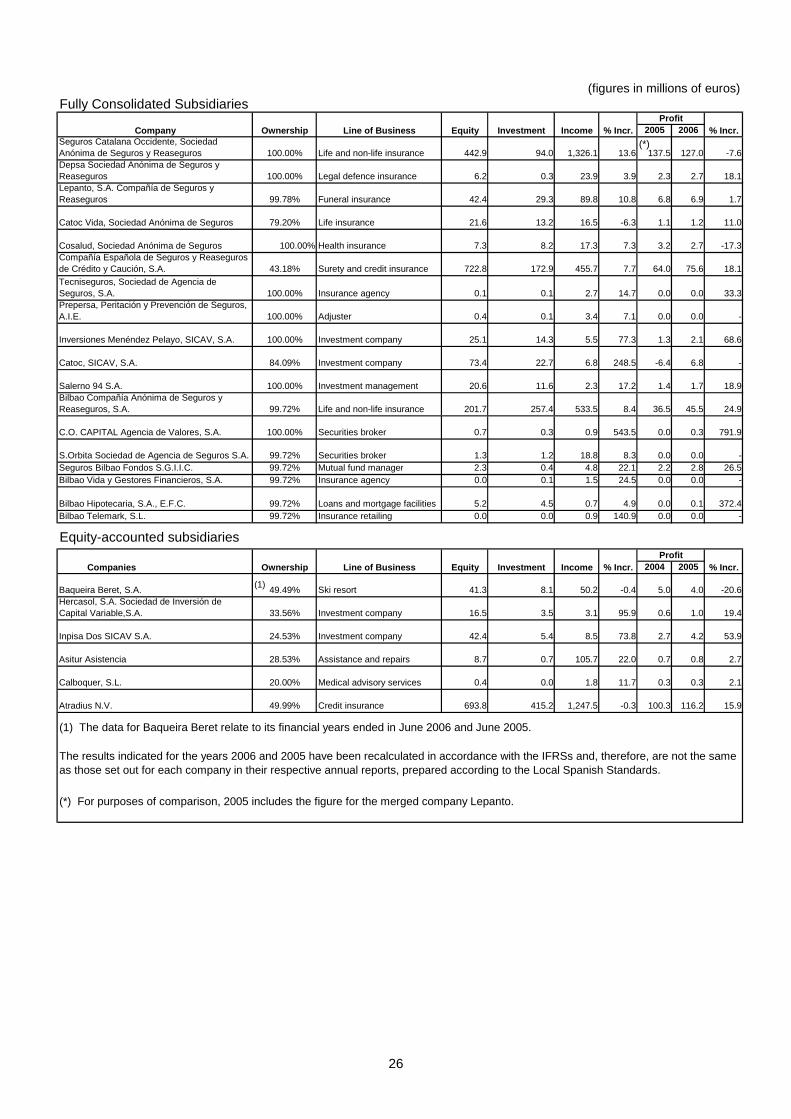

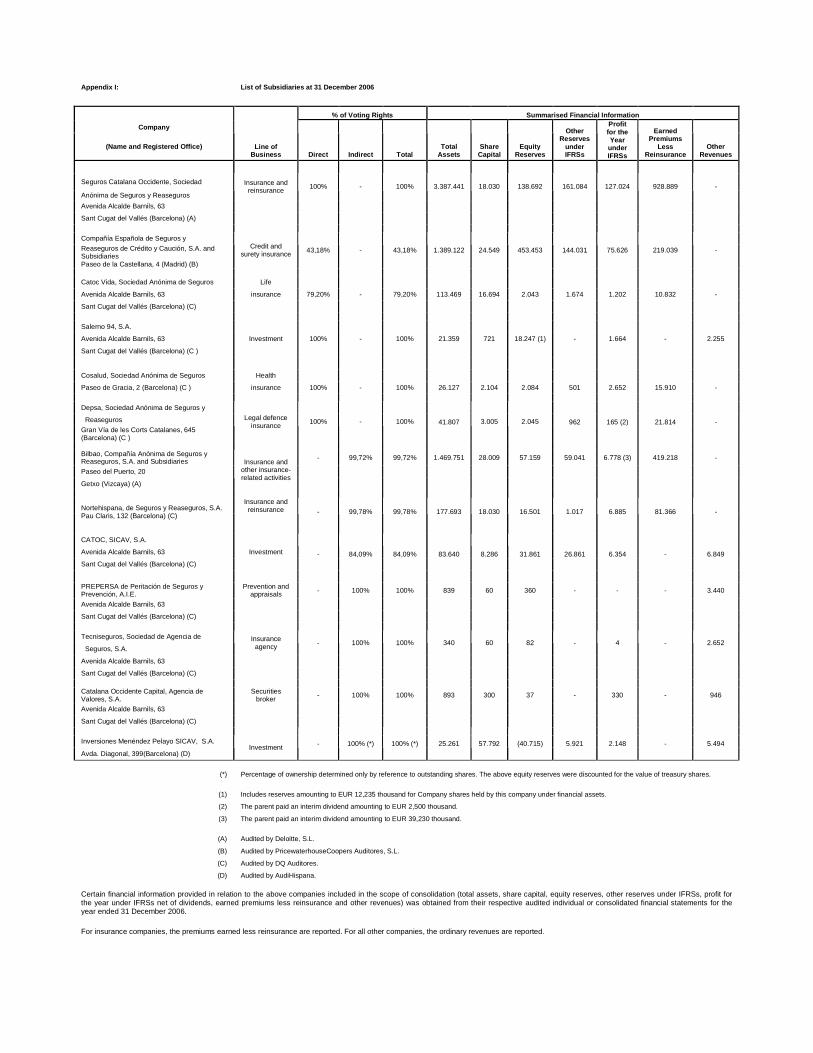

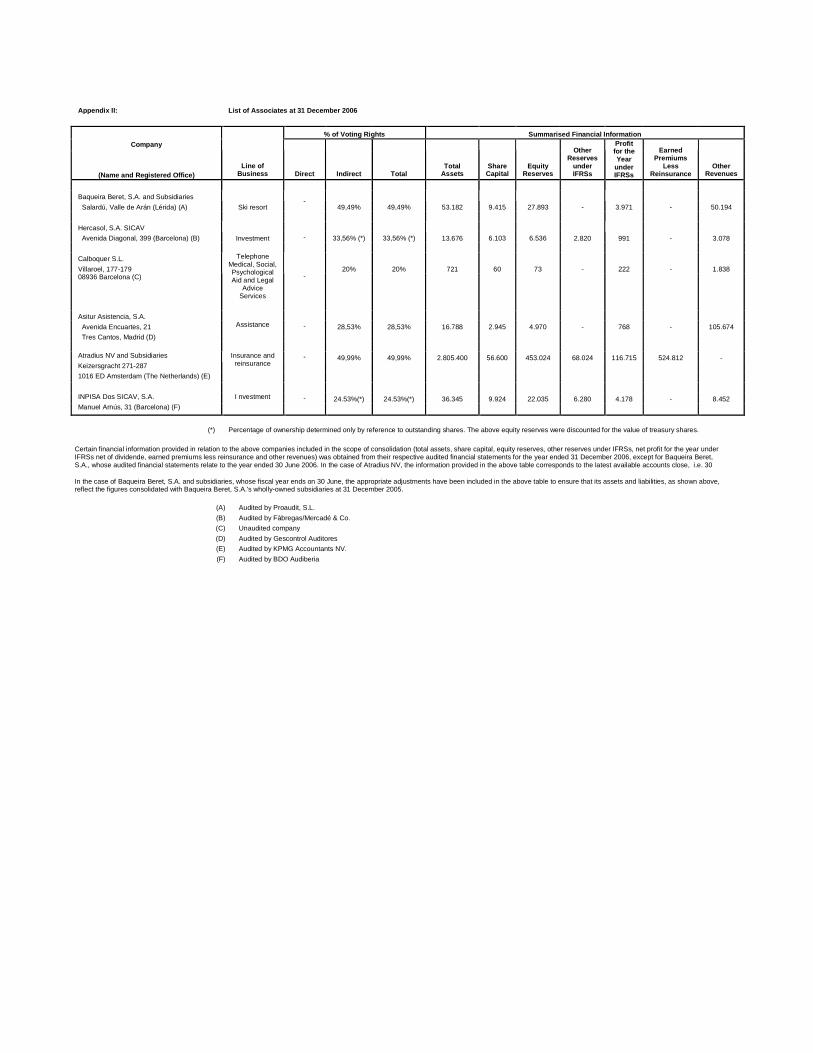

INVESTEES Grupo Catalana Occidente is the parent of the Consolidated Group. It has capital of EUR 36 million, equity of EUR 180 million and controls the other companies in the Group. As a result of the corporate restructuring carried out in September 2001, this company became the company administering and managing the various investments of the companies in the Consolidated Group. The following table lists the various companies in the Consolidated Group, together with the ownership interest held by the Group and the main figures for each of them.

26

2005 2006Seguros Catalana Occidente, Sociedad Anónima de Seguros y Reaseguros 100.00% Life and non-life insurance 442.9 94.0 1,326.1 13.6 137.5 127.0 -7.6Depsa Sociedad Anónima de Seguros y Reaseguros 100.00% Legal defence insurance 6.2 0.3 23.9 3.9 2.3 2.7 18.1Lepanto, S.A. Compañía de Seguros y Reaseguros 99.78% Funeral insurance 42.4 29.3 89.8 10.8 6.8 6.9 1.7

Catoc Vida, Sociedad Anónima de Seguros 79.20% Life insurance 21.6 13.2 16.5 -6.3 1.1 1.2 11.0

Cosalud, Sociedad Anónima de Seguros 100.00% Health insurance 7.3 8.2 17.3 7.3 3.2 2.7 -17.3Compañía Española de Seguros y Reaseguros de Crédito y Caución, S.A. 43.18% Surety and credit insurance 722.8 172.9 455.7 7.7 64.0 75.6 18.1Tecniseguros, Sociedad de Agencia de Seguros, S.A. 100.00% Insurance agency 0.1 0.1 2.7 14.7 0.0 0.0 33.3Prepersa, Peritación y Prevención de Seguros, A.I.E. 100.00% Adjuster 0.4 0.1 3.4 7.1 0.0 0.0 -

Inversiones Menéndez Pelayo, SICAV, S.A. 100.00% Investment company 25.1 14.3 5.5 77.3 1.3 2.1 68.6

Catoc, SICAV, S.A. 84.09% Investment company 73.4 22.7 6.8 248.5 -6.4 6.8 -

Salerno 94 S.A. 100.00% Investment management 20.6 11.6 2.3 17.2 1.4 1.7 18.9Bilbao Compañía Anónima de Seguros y Reaseguros, S.A. 99.72% Life and non-life insurance 201.7 257.4 533.5 8.4 36.5 45.5 24.9

C.O. CAPITAL Agencia de Valores, S.A. 100.00% Securities broker 0.7 0.3 0.9 543.5 0.0 0.3 791.9

S.Orbita Sociedad de Agencia de Seguros S.A. 99.72% Securities broker 1.3 1.2 18.8 8.3 0.0 0.0 -Seguros Bilbao Fondos S.G.I.I.C. 99.72% Mutual fund manager 2.3 0.4 4.8 22.1 2.2 2.8 26.5Bilbao Vida y Gestores Financieros, S.A. 99.72% Insurance agency 0.0 0.1 1.5 24.5 0.0 0.0 -

Bilbao Hipotecaria, S.A., E.F.C. 99.72% Loans and mortgage facilities 5.2 4.5 0.7 4.9 0.0 0.1 372.4Bilbao Telemark, S.L. 99.72% Insurance retailing 0.0 0.0 0.9 140.9 0.0 0.0 -

2004 2005

Baqueira Beret, S.A. 49.49% Ski resort 41.3 8.1 50.2 -0.4 5.0 4.0 -20.6Hercasol, S.A. Sociedad de Inversión de Capital Variable,S.A. 33.56% Investment company 16.5 3.5 3.1 95.9 0.6 1.0 19.4

Inpisa Dos SICAV S.A. 24.53% Investment company 42.4 5.4 8.5 73.8 2.7 4.2 53.9

Asitur Asistencia 28.53% Assistance and repairs 8.7 0.7 105.7 22.0 0.7 0.8 2.7

Calboquer, S.L. 20.00% Medical advisory services 0.4 0.0 1.8 11.7 0.3 0.3 2.1

Atradius N.V. 49.99% Credit insurance 693.8 415.2 1,247.5 -0.3 100.3 116.2 15.9

(figures in millions of euros)

The results indicated for the years 2006 and 2005 have been recalculated in accordance with the IFRSs and, therefore, are not the same as those set out for each company in their respective annual reports, prepared according to the Local Spanish Standards.

(*) For purposes of comparison, 2005 includes the figure for the merged company Lepanto.

Fully Consolidated SubsidiariesProfit

Equity Investment Income % Incr. % Incr.Line of Business Company

Equity-accounted subsidiaries

Ownership

Ownership Equity

(1) The data for Baqueira Beret relate to its financial years ended in June 2006 and June 2005.

% Incr.Investment Income % Incr.Profit

Companies Line of Business

(1)

(*)

27

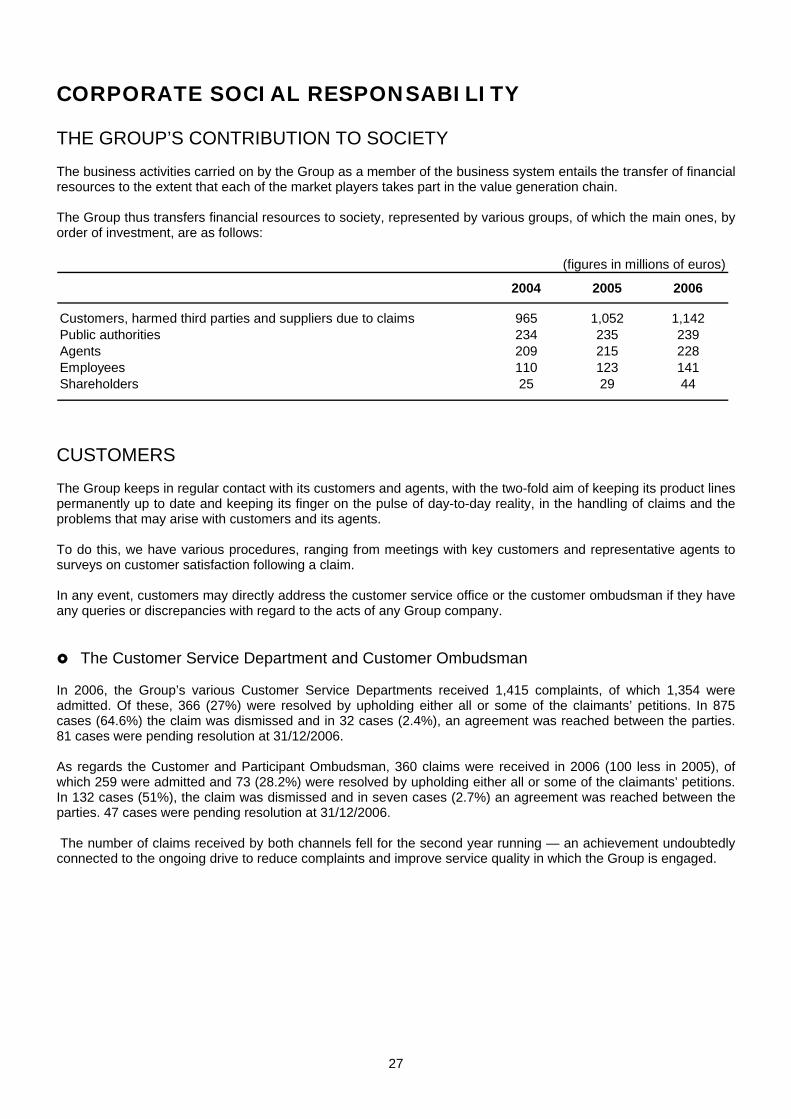

CORPORATE SOCIAL RESPONSABILITY THE GROUP’S CONTRIBUTION TO SOCIETY The business activities carried on by the Group as a member of the business system entails the transfer of financial resources to the extent that each of the market players takes part in the value generation chain. The Group thus transfers financial resources to society, represented by various groups, of which the main ones, by order of investment, are as follows:

2004 2005 2006

Customers, harmed third parties and suppliers due to claims 965 1,052 1,142Public authorities 234 235 239Agents 209 215 228Employees 110 123 141Shareholders 25 29 44

(figures in millions of euros)

CUSTOMERS The Group keeps in regular contact with its customers and agents, with the two-fold aim of keeping its product lines permanently up to date and keeping its finger on the pulse of day-to-day reality, in the handling of claims and the problems that may arise with customers and its agents. To do this, we have various procedures, ranging from meetings with key customers and representative agents to surveys on customer satisfaction following a claim. In any event, customers may directly address the customer service office or the customer ombudsman if they have any queries or discrepancies with regard to the acts of any Group company. The Customer Service Department and Customer Ombudsman

In 2006, the Group’s various Customer Service Departments received 1,415 complaints, of which 1,354 were admitted. Of these, 366 (27%) were resolved by upholding either all or some of the claimants’ petitions. In 875 cases (64.6%) the claim was dismissed and in 32 cases (2.4%), an agreement was reached between the parties. 81 cases were pending resolution at 31/12/2006. As regards the Customer and Participant Ombudsman, 360 claims were received in 2006 (100 less in 2005), of which 259 were admitted and 73 (28.2%) were resolved by upholding either all or some of the claimants’ petitions. In 132 cases (51%), the claim was dismissed and in seven cases (2.7%) an agreement was reached between the parties. 47 cases were pending resolution at 31/12/2006. The number of claims received by both channels fell for the second year running — an achievement undoubtedly connected to the ongoing drive to reduce complaints and improve service quality in which the Group is engaged.

28

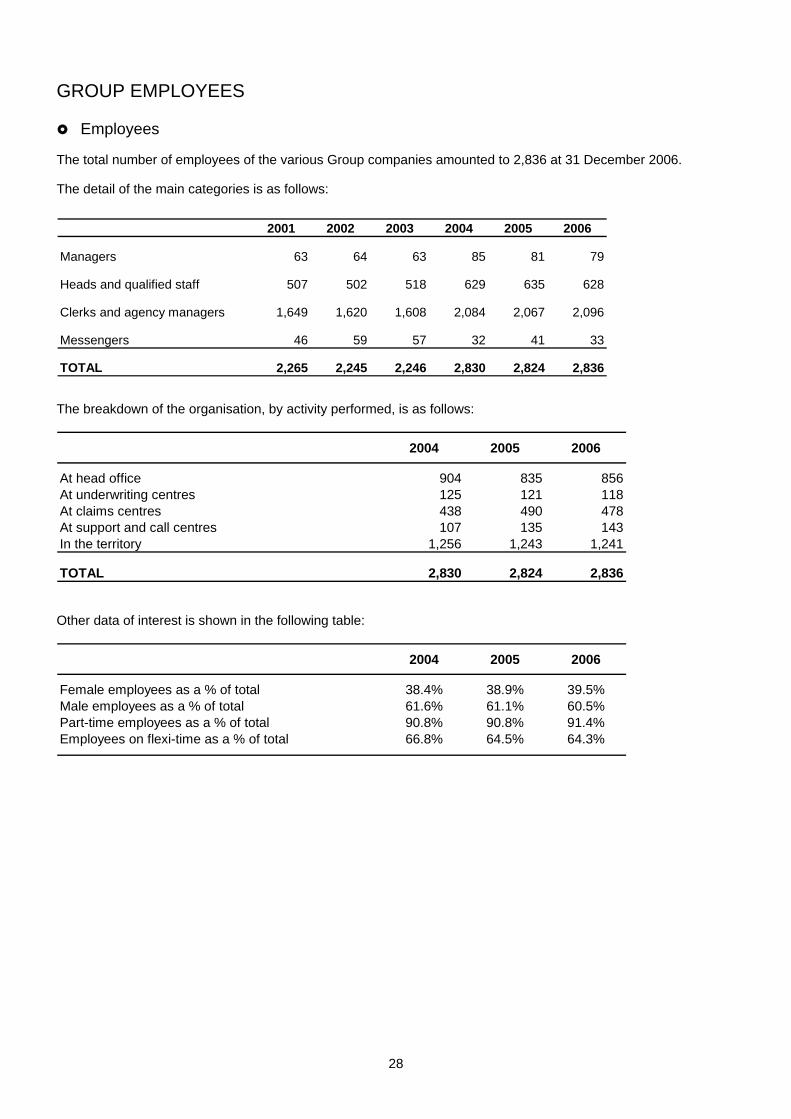

GROUP EMPLOYEES Employees

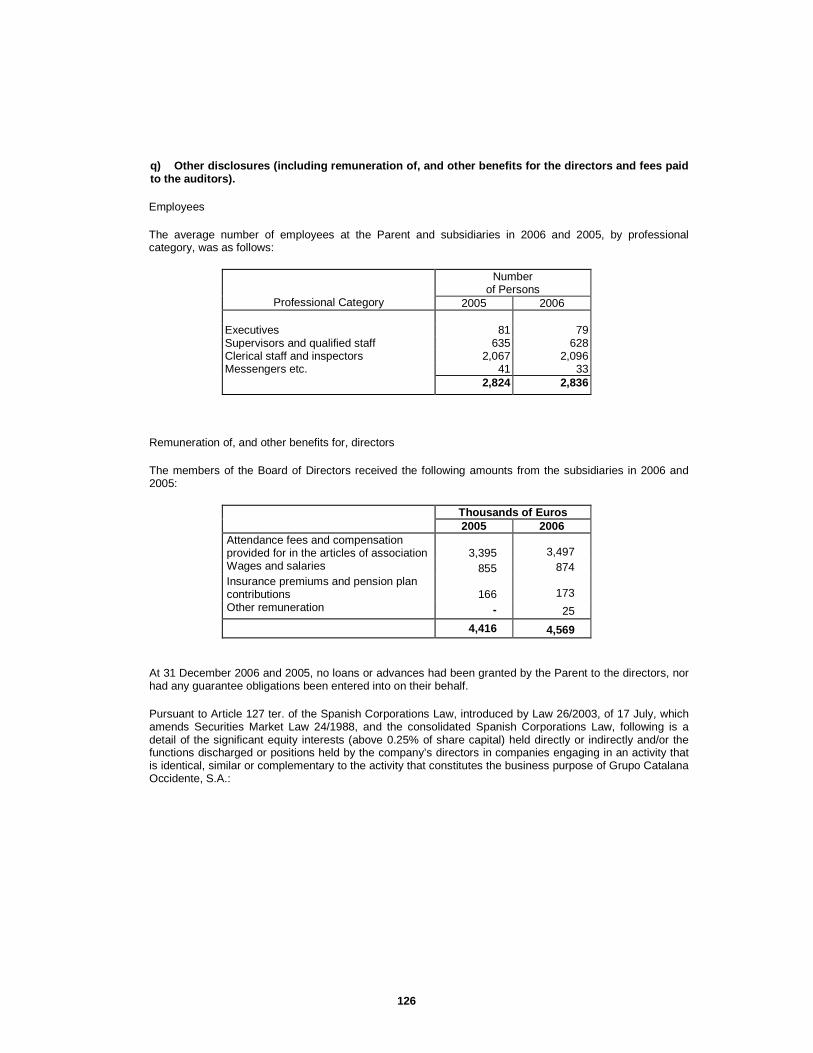

The total number of employees of the various Group companies amounted to 2,836 at 31 December 2006. The detail of the main categories is as follows:

The breakdown of the organisation, by activity performed, is as follows:

2004 2005 2006

At head office 904 835 856At underwriting centres 125 121 118At claims centres 438 490 478At support and call centres 107 135 143In the territory 1,256 1,243 1,241

TOTAL 2,830 2,824 2,836 Other data of interest is shown in the following table:

2004 2005 2006

Female employees as a % of total 38.4% 38.9% 39.5%Male employees as a % of total 61.6% 61.1% 60.5%Part-time employees as a % of total 90.8% 90.8% 91.4%Employees on flexi-time as a % of total 66.8% 64.5% 64.3%

2001 2002 2003 2004 2005 2006

Managers 63 64 63 85 81 79

Heads and qualified staff 507 502 518 629 635 628

Clerks and agency managers 1,649 1,620 1,608 2,084 2,067 2,096

Messengers 46 59 57 32 41 33

TOTAL 2,265 2,245 2,246 2,830 2,824 2,836

29

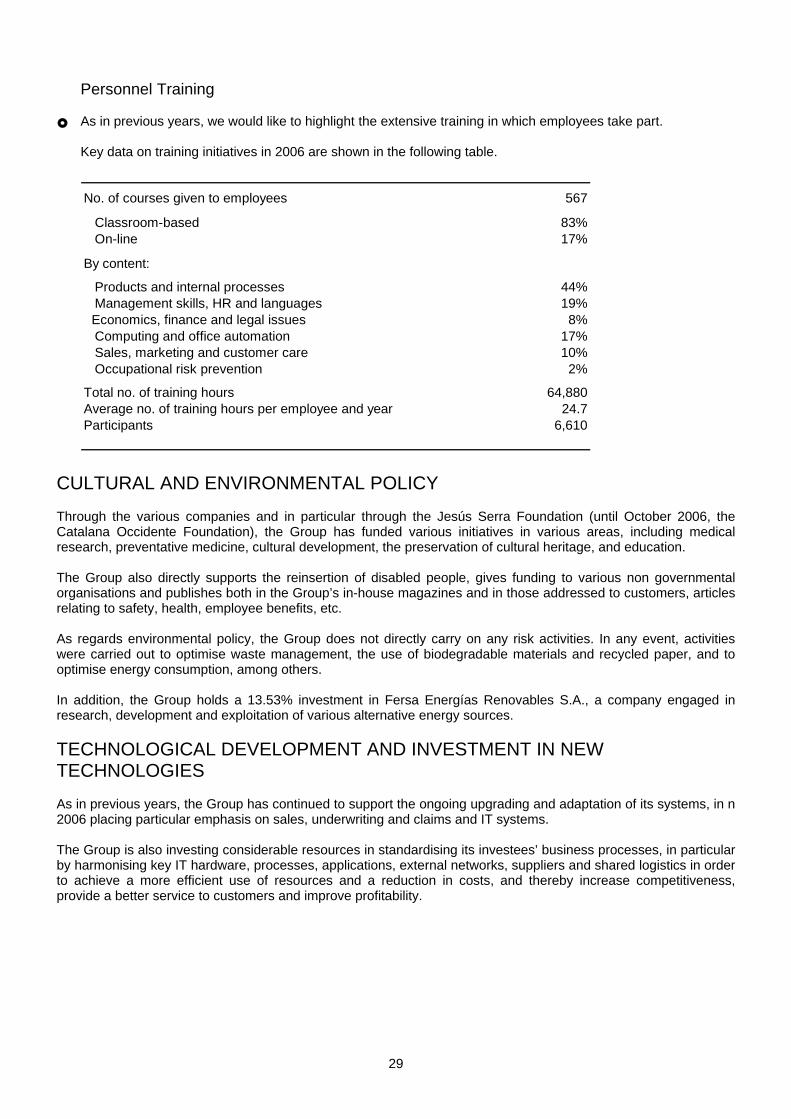

Personnel Training As in previous years, we would like to highlight the extensive training in which employees take part. Key data on training initiatives in 2006 are shown in the following table.

No. of courses given to employees 567

Classroom-based 83% On-line 17%

By content:

Products and internal processes 44% Management skills, HR and languages 19% Economics, finance and legal issues 8% Computing and office automation 17% Sales, marketing and customer care 10% Occupational risk prevention 2%

Total no. of training hours 64,880Average no. of training hours per employee and year 24.7Participants 6,610

CULTURAL AND ENVIRONMENTAL POLICY Through the various companies and in particular through the Jesús Serra Foundation (until October 2006, the Catalana Occidente Foundation), the Group has funded various initiatives in various areas, including medical research, preventative medicine, cultural development, the preservation of cultural heritage, and education. The Group also directly supports the reinsertion of disabled people, gives funding to various non governmental organisations and publishes both in the Group’s in-house magazines and in those addressed to customers, articles relating to safety, health, employee benefits, etc. As regards environmental policy, the Group does not directly carry on any risk activities. In any event, activities were carried out to optimise waste management, the use of biodegradable materials and recycled paper, and to optimise energy consumption, among others. In addition, the Group holds a 13.53% investment in Fersa Energías Renovables S.A., a company engaged in research, development and exploitation of various alternative energy sources. TECHNOLOGICAL DEVELOPMENT AND INVESTMENT IN NEW TECHNOLOGIES As in previous years, the Group has continued to support the ongoing upgrading and adaptation of its systems, in n 2006 placing particular emphasis on sales, underwriting and claims and IT systems. The Group is also investing considerable resources in standardising its investees’ business processes, in particular by harmonising key IT hardware, processes, applications, external networks, suppliers and shared logistics in order to achieve a more efficient use of resources and a reduction in costs, and thereby increase competitiveness, provide a better service to customers and improve profitability.

30

INTERNAL CONTROL. Risk Control Systems The Group has an internal control system that focuses on control of the various risks involved in the business. It consists of the following: • A set of rules and procedures applicable to the entire organisation. • Internal control procedures, with appropriate authorisation levels and the required segregation of functions,

established for the various management areas, • The performance of various external audits. • External consulting support for areas requiring such support. • A structured information system. • An internal audit unit which periodically performs audits according to the risk levels. This system enables appropriate RISK CONTROL to be performed reasonably, and is aimed at covering the SOLVENCY II considerations and, therefore, has been divided into the following three risk groups: Technical Risks and risks inherent to the insurance business

These are generated in policy underwriting, claims management based on deviations in costs or frequencies, changes in the provision for future obligations generated by the coverage offered and deviations in management costs. The actions undertaken to monitor and control these risk principally include: • Implementing appropriate technical standards for policy underwriting purposes. • Analysing products to determine the sufficiency of premiums or technical provisions. • Contracting the necessary reinsurance cover, pursuant to a policy that allows for an increase in retained

business, subject to size and solvency considerations. For outward reinsurance, only companies with a high solvency level and the required financial and management capacities are used.

• Policy and initiatives relating to returns on policies.

Financial Risks • Assets in the various portfolios managed are classified according to their characteristics (required return, risk,

liquidity, etc). • Analysis of ALM in relation to the obligations acquired with the insureds. • Analysis and monitoring of credit risk (investments below investment grade require express approval) and

tracking concentration risk on managed portfolios. • Direct supervision by the risk department.

Operational Risks

This is a different type of risk, divided into five broad groups, described separately: • General risks. This encompasses legal, technological and strategic risks. These risks are mitigated with the

support of the systems in the areas in question and the assistance of external consultants. • IT risks. Each year, a general audit of the IT area is performed by an external consultancy specialised in

preventing unauthorised access. The Group has a Business Continuity Plan and a backup centre. To test the efficiency of the plan and the centre, a simulation exercise was performed in the course of 2006.

• Human resources risks. There are emergency and building evacuation plans and occupational risk audits are carried out periodically.

• Commercial risks. These include the risks associated with commercial practices and sales systems. Controls are performed by the various sales managers, the Control Department and the Internal Audit department.

• Errors and misstatements. This item includes errors and misstatements, as well as internal and external fraud. Controls are performed by the Group’s various operational managers, and in particular by the Control and Internal Audit departments.

31

OUTLOOK FOR 2007: Strategy and Objectives. The Catalana Occidente Group has a formal, participatory planning system which culminates in the distribution of the Group’s Strategic Plan and annual guidelines for all the members of the organisation, which sets in motion a process for the creation of Action Plans and Budgets. The above Annual Guidelines focus on the objectives which, for 2007, we believe to be a priority for achieving our strategy in the medium and long term which, evidently, would not vary from those set in the last few years, apart from the intensity with which they will be carried out, the level of effectiveness forecast and the costs associated with the whole process. In this respect, the lines of action relating to the Guidelines for 2007 concentrate on the following issues:

1.- Consolidating in 2007 the improvement in net policy capture and increase in net agents achieved in 2006. 2.- Reviewing and adapting our offering to customers’ and agents’ demands and, in particular, promoting sales

in the Auto and Projected Life Premiums. 3.- Controlling the performance of Technical Margin by combining the objectives concerning the profitability of

products with those concerning the competitiveness of our offering. We will be paying particular attention to the improvement in the financial results of each product line.

4.- Lastly, continuing to contain expenses, by matching the management of resources with the objectives set, with a clear and determined support for the creation of the network and improving efficiency, promoting savings plans and taking advantage of synergies among the various Group companies.

32

STANDARDS AND LEGISLATION INTERNATIONAL ACCOUNTING STANDARDS A description is provided below of the International Accounting Standards taken into account in the preparation of this financial information. SCOPE OF CONSOLIDATION IAS 28, Accounting for investments in associates. Significant influence is presumed to exist and, therefore, companies in which between 20% and 50% of the voting rights are directly or indirectly held, are consolidated using the equity method. As local regulations set this limit at 3% in the case of listed companies, companies that fall within the 3% to 20% band are excluded from consolidation, i.e. the following companies: Mackerel SICAV, BBVA Catalana Cartera SICAV and Fersa Energías Renovables S.A. INCOME STATEMENT AND BALANCE SHEET IFRS 3 (previously IAS 22) - Business Combinations: This standard establishes that Consolidation Goodwill is not subject to periodical amortisation but to impairment analysis processes (or evaluation of the decline in value of the investment). Local Spanish standards stipulate that goodwill must be amortised within a period of 5, 10 or 20 years. The goodwill arising on the acquisition of Lepanto and Seguros Bilbao is amortised over 10 years and the goodwill in Baloise, over five years. No decline has been detected in the value of the above investments and, therefore, the amounts amortised in 2004 and 2005 under local standards have been adjusted with a credit to income in each year. IFRS 4 - Insurance Contracts Introductory paragraph 4 and paragraph 14 stipulate that technical provisions for future claims and, specifically, the current Equalisation Provision, may not be recognised. The Group has reversed any existing provisions at year-end, following deduction of income tax, giving rise to greater equity. No effects arising from the reclassification of life products as financial products have been detected, or any shortfalls in mathematical provisions as a result of liability adequacy tests. Under paragraph 30, unrealised gains on financial assets allocated to life policies are attributable to the insureds at the same proportion as the income effectively realised on such policies is allocated. According to this accounting policy, known as Shadow Accounting, the insureds’ related Shares in Future Profits have been allocated as the balancing entry for the Equity arising from gains on financial assets. IAS 12 - Corporation tax. The net tax effect of the changes arising from the accounting of the other IASs, particularly the effect on equity, must be recognised. IAS 18 - Revenues. The origination fees for the creation of mortgage loans have been recalculated. IAS 19 - Employee benefits. The employee retirement commitments have been restated. IAS 32 - Financial instruments: Disclosure and presentation: Under this IAS, the cost of treasury shares must be deducted from capital instead of being classified as an Investment. In addition, any gains on the disposal of treasury shares must be eliminated in the consolidation processes. IAS 36 - Impairment of assets: The allowances for bad debts and outstanding premiums have been restated. IAS 37 - Provisions, contingent liabilities and contingent assets: The provisions for liabilities and charges have been restated. IAS 39 - Financial Instruments: Recognition and Measurement: Under this IAS, certain assets and liabilities may be measured at market value in certain portfolios defined for that purpose. Although it also allows assets with a defined maturity to be recognised at amortised historical cost, this standard is very stringent with respect to the principle concerning the holding period for the assets classified in this type of portfolios. Therefore, the Group has chosen to classify practically all of its investment securities as marked-to-market securities, thereby giving rise to a substantial amount of gains which, upon first-time application of IASs, net of taxes, are recognised in equity. IAS 16 - Property, Plant and Equipment and IAS 40 - Investment Property. Under these IASs, properties may be, but need not be, measured at market value, which would have resulted in the emergence of gains totalling EUR 310.5 million for accounting purposes. These standards provide for a separate reporting treatment for properties for

33

own use, which are broken down under Property, Plant and Equipment, and for properties leased to third parties, which are reported as investment property. CHANGES MADE TO IFRSs Various amendments and reinterpretations were made to the previously published IFRSs in 2006, of which the most important are as follows: IAS 19: Amendment of criteria used to recognise employee benefits IAS 39: Recognition and measurement of financial instruments IFSR 4: Interpretation of Insurance Contract (Crédito) IFSR 7: Disclosures. Replaces IAS 32. APPLICATION DATES All of the International Standards except IAS 32, IAS 39 and IFRS 4 are applicable from the opening balance sheet for 2004, i.e. from 1 January 2004. IAS 32, IAS 39 and IFRS 4 are applicable from the opening balance sheet for 2005, i.e. from 1 January 2005. Optionally, companies are authorised to apply them from 1 January 2004 provided that the companies themselves and their auditors guarantee the accuracy of the adjustments resulting from their application in 2004. INTERNATIONAL STANDARDS: WHAT THE INITIALS MEAN The standards published until June 2003 are called IASs (International Accounting Standards) in English and NICs in Spanish (Normas Internacionales de Contabilidad). Those published since that date are called IFRSs (International Financial Reporting Standards) in English and NIIFs in Spanish (Normas Internacionales de Información Financiera). SOLVENCY MARGIN AND COVERAGE OF PROVISIONS To date, IFRSs have provided neither a quantified solvency level for insurance companies nor criteria for the coverage of technical provisions The Group has elected to calculate both its solvency margin and coverage of technical provisions using the methodology established under Spanish GAAP, calculating certain financial balances in accordance with the criteria established under IFRSs.

34

STOCK MARKET DATA

SHARE PRICE (euros per share)Start of year 14.72 1/01/2006Low 14.72 1/01/2006High 27.85 28/12/2006Year-end 27.45 31/12/2006Average 22.02 2006

STOCK MARKET RATIOSPER (price at 31/12/2006 / attributable earnings per share) 17.2 31/12/2006Yield (2006 dividend / price, %) 1.5% 31/12/2006Renturn (Dividends 2006 / average trading price) 1.9% 2006Pay-Out (2005 dividend / 2005 attributable profit, %) 25.2% 2006

PROFITABILITY RATIOSROE (2006 attributable profit / 2006 average equity, %) 23.6% 2006ROE (2006 attributable profit / equity at 12/2006, %) 21.2% 31/12/2006

OTHER DATA (in euros)No. of shares 120,000,000 31/12/2006Par value per share 0.3 31/12/2006Daily average trading volume (no. of shares) 118,820 01/01/2006 - 31/12/2006Daily average trading volume (thousands of euros) 2,550,475 01/01/2006 - 31/12/2006Dividend per share 0.4 31/12/2006

14.72 euros(73.6 euros)

8.80 euros(44.00 euros)

4.93 euros (24.65 euros)

3.99 euros (19.95 euros)

27.45 euros

Comparative performance of the market price of Grupo Catalana Occidente with the IBEX 35 and the Dow Jones Europe Stoxx Insurance indexes

CATALANA OCCIDENTEIBEX 35DOW JONES EUROPE STOXX INSURANCE

31/12/2002 31/12/200431/12/2003 31/12/2005Base 100 at 31/12/2001

31/12/2006

35

AUDIT At the Annual General Meeting of the Consolidated Group’s Parent held on 25 May 2006, shareholders resolved to renew the appointment of DELOITTE, S.L. as auditors of the individual Company and of the Consolidated Group, for 2006. This firm also audits the subsidiaries Seguros Catalana Occidente, Sociedad Anónima de Seguros y Reaseguros and Bilbao, Compañía Sociedad Anónima de Seguros y Reaseguros, S.A., this latter company, under a resolution of its Annual General Meeting held on 8 June 2005, for an initial period of three years. DQ Auditores S.L. audits the other subsidiaries which were fully consolidated, and those relating to the pension funds, for an initial period of three years, running from 2005, with the exception of Compañía Española de Seguros y Reaseguros de Crédito y Caución, S.A., which is audited by PricewaterhouseCoopers Auditores, S.L., and Inversiones Menéndez y Pelayo, SICAV, S.A., which is audited by Audihispana Auditores Consultores, S.A.

36

GRUPO CATALANA OCCIDENTE, S.A. AND SUBSIDIARIES Consolidated Financial Statements for the year ended 31 December 2006, prepared in accordance with International Financial Reporting Standards

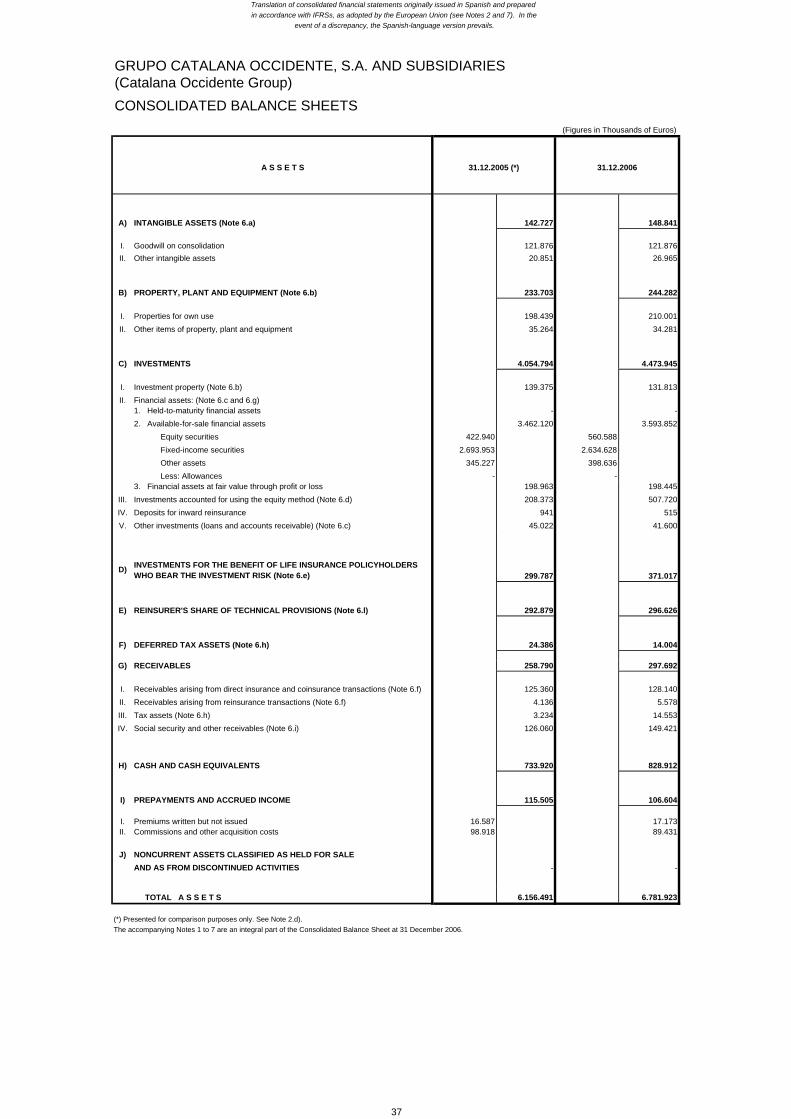

GRUPO CATALANA OCCIDENTE, S.A. AND SUBSIDIARIES (Catalana Occidente Group)CONSOLIDATED BALANCE SHEETS

A S S E T S 31.12.2005 (*) 31.12.2006

A) INTANGIBLE ASSETS (Note 6.a) 142.727 148.841

I. Goodwill on consolidation 121.876 121.876II. Other intangible assets 20.851 26.965

B) PROPERTY, PLANT AND EQUIPMENT (Note 6.b) 233.703 244.282

I. Properties for own use 198.439 210.001II. Other items of property, plant and equipment 35.264 34.281

C) INVESTMENTS 4.054.794 4.473.945

I. Investment property (Note 6.b) 139.375 131.813II. Financial assets: (Note 6.c and 6.g)

1. Held-to-maturity financial assets - -2. Available-for-sale financial assets 3.462.120 3.593.852 Equity securities 422.940 560.588 Fixed-income securities 2.693.953 2.634.628 Other assets 345.227 398.636 Less: Allowances - -3. Financial assets at fair value through profit or loss 198.963 198.445

III. Investments accounted for using the equity method (Note 6.d) 208.373 507.720IV. Deposits for inward reinsurance 941 515V. Other investments (loans and accounts receivable) (Note 6.c) 45.022 41.600

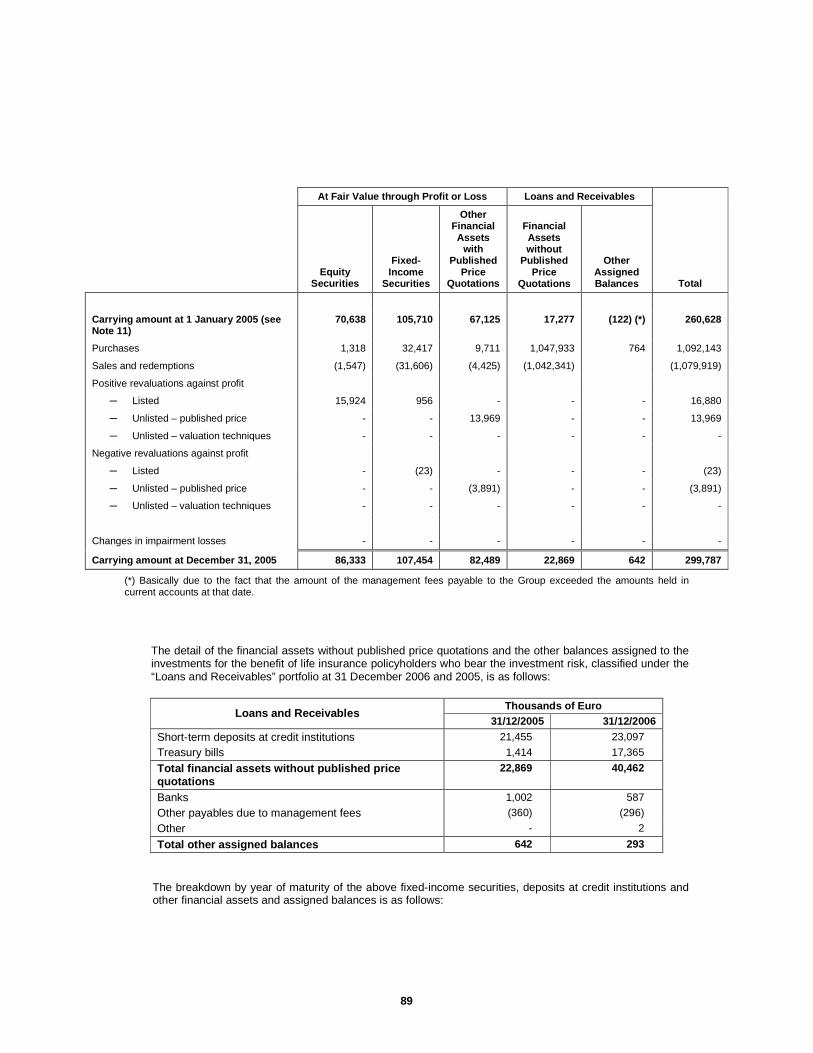

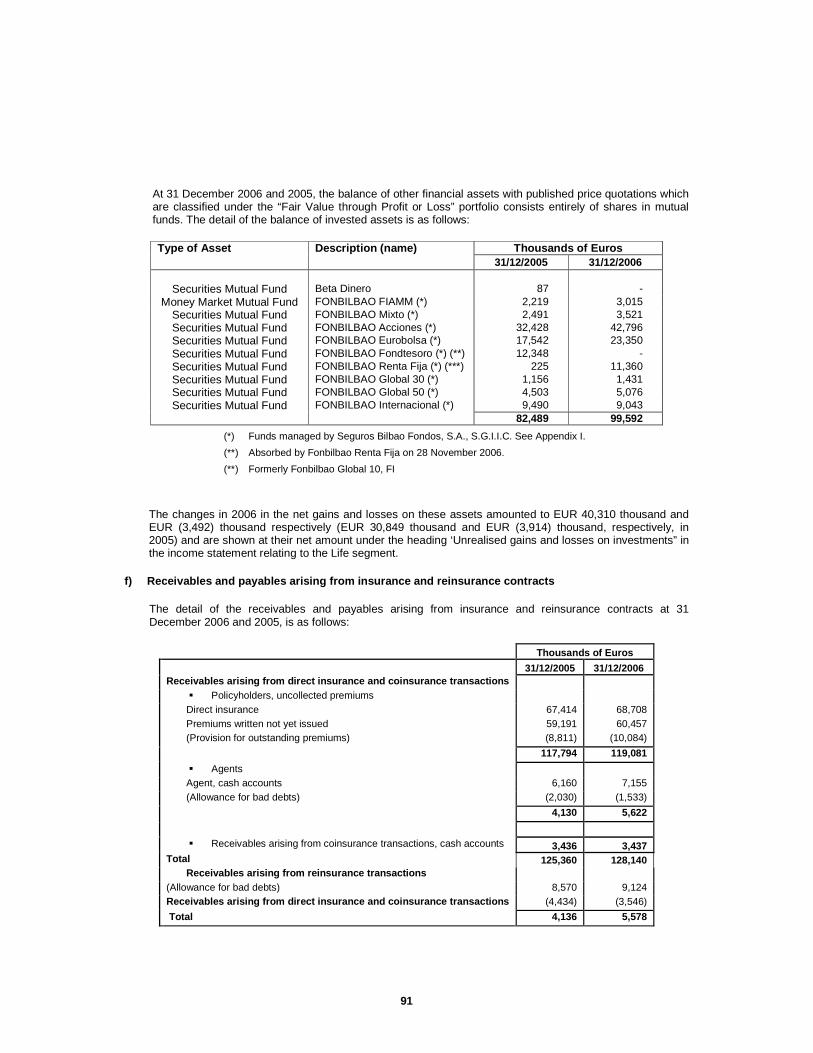

D) INVESTMENTS FOR THE BENEFIT OF LIFE INSURANCE POLICYHOLDERS WHO BEAR THE INVESTMENT RISK (Note 6.e) 299.787 371.017

E) REINSURER'S SHARE OF TECHNICAL PROVISIONS (Note 6.l) 292.879 296.626

F) DEFERRED TAX ASSETS (Note 6.h) 24.386 14.004

G) RECEIVABLES 258.790 297.692

I. Receivables arising from direct insurance and coinsurance transactions (Note 6.f) 125.360 128.140II. Receivables arising from reinsurance transactions (Note 6.f) 4.136 5.578III. Tax assets (Note 6.h) 3.234 14.553IV. Social security and other receivables (Note 6.i) 126.060 149.421

H) CASH AND CASH EQUIVALENTS 733.920 828.912

I) PREPAYMENTS AND ACCRUED INCOME 115.505 106.604

I. Premiums written but not issued 16.587 17.173II. Commissions and other acquisition costs 98.918 89.431

J) NONCURRENT ASSETS CLASSIFIED AS HELD FOR SALEAND AS FROM DISCONTINUED ACTIVITIES - -

TOTAL A S S E T S 6.156.491 6.781.923

(*) Presented for comparison purposes only. See Note 2.d).The accompanying Notes 1 to 7 are an integral part of the Consolidated Balance Sheet at 31 December 2006.

Translation of consolidated financial statements originally issued in Spanish and prepared in accordance with IFRSs, as adopted by the European Union (see Notes 2 and 7). In the

event of a discrepancy, the Spanish-language version prevails.

(Figures in Thousands of Euros)

37

GRUPO CATALANA OCCIDENTE, S.A. AND SUBSIDIARIES (Catalana Occidente Group)CONSOLIDATED BALANCE SHEETS

E Q U I T Y A N D L I A B I L I T I E S 31.12.2005 (*) 31.12.2006

A) EQUITY 985.591 1.343.218

I. Share capital paid in 36.000 36.000

II. Reserves 357.085 473.603

III. Less : Treasury shares 7.089 12.234

IV. Reserves for valuation adjustments and exchange differences 197.637 236.412

V. Reserves for pensions -4.202

VI. Retained earnings

1. Unallocated prior years' earnings

2. Profit for the year attributable to the Parent 137.591 191.389

a) Consolidated profit 175.503 249.515

b) Profit attributable to minority interests 37.912 58.126

3. Less: Interim dividends 18.240

Equity attributable to the Parent's shareholders (Note 6.j) 721.224 902.728

Minority Interests (Note 6.k) 264.367 440.490

C) TECHNICAL PROVISIONS (Note 6.l) 4.313.283 4.492.762

I. Unearned premiums and unexpired risks provisions 536.038 553.906

II. Life insurance provisions (Note 6.n) 2.622.525 2.723.055

III. Claims provisions 1.137.656 1.196.682

IV. Provisions for policyholder dividends and return premiums 6.508 7.096

V. Other technical provisions 10.556 12.023

TECHNICAL PROVISIONS FOR LIFE INSURANCE POLICIES WHERE RISK IS BORNE BY POLICYHOLDERS (Note 6.e) 299.787 371.017

E) PROVISIONS FOR LIABILITIES AND CHARGES (Note 6.m) 70.788 78.427

F) DEPOSITS RECEIVED FOR OUTWARD REINSURANCE AND RETROCESSIONS 56.057 52.282

G) DEFERRED TAX LIABILITIES (Note 6.h) 188.172 194.026

H) PAYABLES 229.595 236.881

I. Payables arising from direct insurance and coinsurance transactions (Note 6.f) 39.040 40.584

II. Payables arising from reinsurance transactions (Note 6.f) 15.498 9.820

III. Tax liabilities (Note 6.h) 50.895 58.610

IV. Other liabilities (Note 6.i) 124.162 127.867

I) ACCRUED EXPENSES AND DEFERRED INCOME 13.218 13.310

J) LIABILITIES ASSOCIATED WITH NONCURRENT ASSETS CLASSIFIED

AS HELD FOR SALE AND AS FROM DISCONTINUED ACTIVITIES - -

TOTAL E Q U I T Y A N D L I A B I L I T I E S 6.156.491 6.781.923

(*) Presented for comparison purposes only. See Note 2.d).The accompanying Notes 1 to 7 are an integral part of the Consolidated Balance Sheet at 31 December 2006.

Translation of consolidated financial statements originally issued in Spanish and prepared in accordance with IFRSs, as adopted by the European Union (see Notes 2 and 7). In the

event of a discrepancy, the Spanish-language version prevails.

D)

(Figures in Thousands of Euros)

38

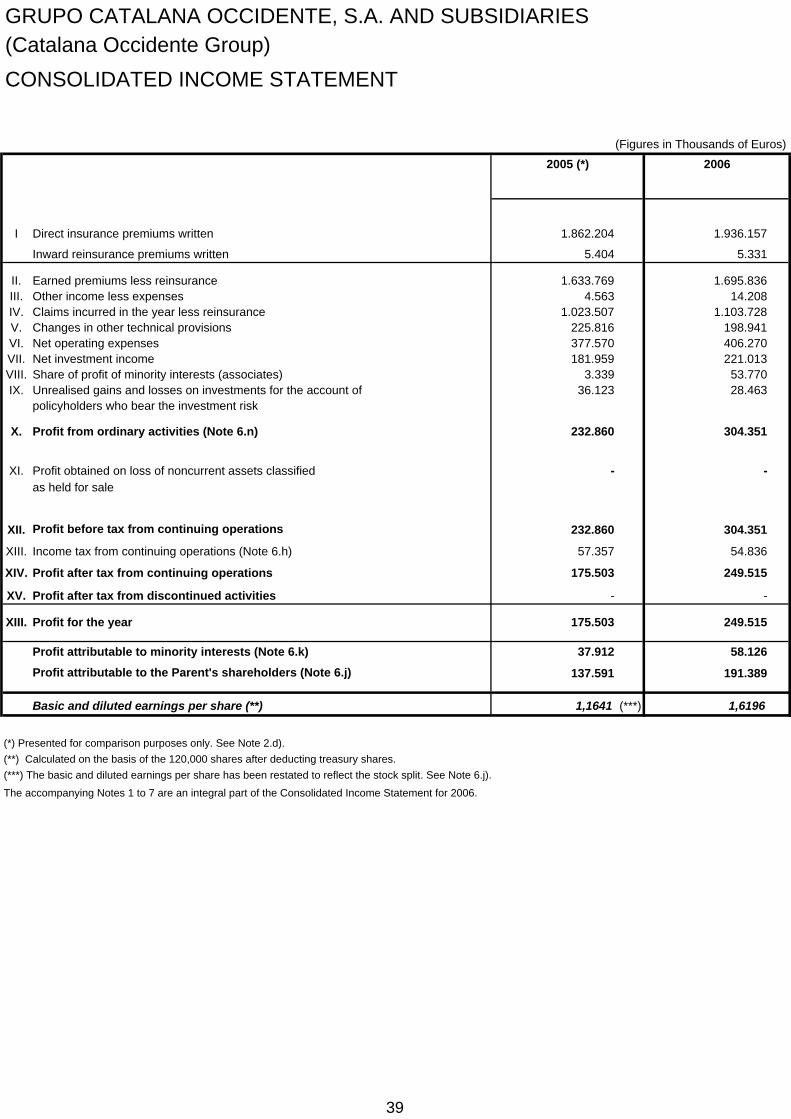

GRUPO CATALANA OCCIDENTE, S.A. AND SUBSIDIARIES (Catalana Occidente Group)CONSOLIDATED INCOME STATEMENT

(Figures in Thousands of Euros)

I Direct insurance premiums written 1.862.204 1.936.157

Inward reinsurance premiums written 5.404 5.331

II. Earned premiums less reinsurance 1.633.769 1.695.836III. Other income less expenses 4.563 14.208IV. Claims incurred in the year less reinsurance 1.023.507 1.103.728V. Changes in other technical provisions 225.816 198.941VI. Net operating expenses 377.570 406.270VII. Net investment income 181.959 221.013VIII. Share of profit of minority interests (associates) 3.339 53.770IX. Unrealised gains and losses on investments for the account of 36.123 28.463

policyholders who bear the investment risk

X. Profit from ordinary activities (Note 6.n) 232.860 304.351

XI. Profit obtained on loss of noncurrent assets classified - -as held for sale

XII. Profit before tax from continuing operations 232.860 304.351

XIII. Income tax from continuing operations (Note 6.h) 57.357 54.836

XIV. Profit after tax from continuing operations 175.503 249.515

XV. Profit after tax from discontinued activities - -

XIII. Profit for the year 175.503 249.515

Profit attributable to minority interests (Note 6.k) 37.912 58.126

Profit attributable to the Parent's shareholders (Note 6.j) 137.591 191.389

Basic and diluted earnings per share (**) 1,1641 (***) 1,6196

(*) Presented for comparison purposes only. See Note 2.d).(**) Calculated on the basis of the 120,000 shares after deducting treasury shares.(***) The basic and diluted earnings per share has been restated to reflect the stock split. See Note 6.j).

The accompanying Notes 1 to 7 are an integral part of the Consolidated Income Statement for 2006.

20062005 (*)

39

(Figures in Thousands of Euros)

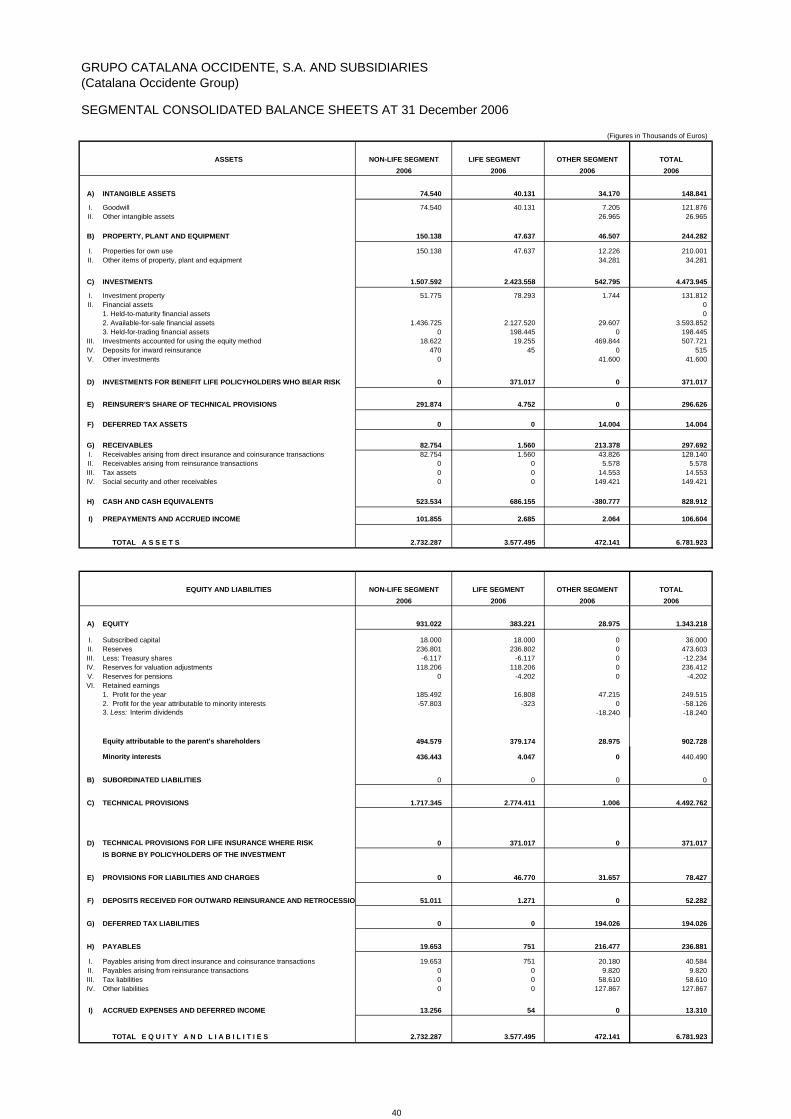

ASSETS LIFE SEGMENT

A) INTANGIBLE ASSETS 74.540 40.131 34.170 148.841

I. Goodwill 74.540 40.131 7.205 121.876II. Other intangible assets 26.965 26.965

B) PROPERTY, PLANT AND EQUIPMENT 150.138 47.637 46.507 244.282

I. Properties for own use 150.138 47.637 12.226 210.001II. Other items of property, plant and equipment 34.281 34.281

C) INVESTMENTS 1.507.592 2.423.558 542.795 4.473.945

I. Investment property 51.775 78.293 1.744 131.812II. Financial assets 0

1. Held-to-maturity financial assets 02. Available-for-sale financial assets 1.436.725 2.127.520 29.607 3.593.8523. Held-for-trading financial assets 0 198.445 0 198.445

III. Investments accounted for using the equity method 18.622 19.255 469.844 507.721IV. Deposits for inward reinsurance 470 45 0 515V. Other investments 0 41.600 41.600

D) INVESTMENTS FOR BENEFIT LIFE POLICYHOLDERS WHO BEAR RISK 0 371.017 0 371.017

E) REINSURER'S SHARE OF TECHNICAL PROVISIONS 291.874 4.752 0 296.626

F) DEFERRED TAX ASSETS 0 0 14.004 14.004

G) RECEIVABLES 82.754 1.560 213.378 297.692I. Receivables arising from direct insurance and coinsurance transactions 82.754 1.560 43.826 128.140II. Receivables arising from reinsurance transactions 0 0 5.578 5.578III. Tax assets 0 0 14.553 14.553IV. Social security and other receivables 0 0 149.421 149.421

H) CASH AND CASH EQUIVALENTS 523.534 686.155 -380.777 828.912

I) PREPAYMENTS AND ACCRUED INCOME 101.855 2.685 2.064 106.604

TOTAL A S S E T S 2.732.287 3.577.495 472.141 6.781.923

EQUITY AND LIABILITIES

A) EQUITY 931.022 383.221 28.975 1.343.218

I. Subscribed capital 18.000 18.000 0 36.000II. Reserves 236.801 236.802 0 473.603III. Less: Treasury shares -6.117 -6.117 0 -12.234IV. Reserves for valuation adjustments 118.206 118.206 0 236.412V. Reserves for pensions 0 -4.202 0 -4.202VI. Retained earnings

1. Profit for the year 185.492 16.808 47.215 249.5152. Profit for the year attributable to minority interests -57.803 -323 0 -58.1263. Less: Interim dividends -18.240 -18.240

Equity attributable to the parent's shareholders 494.579 379.174 28.975 902.728

Minority interests 436.443 4.047 0 440.490

B) SUBORDINATED LIABILITIES 0 0 0 0

C) TECHNICAL PROVISIONS 1.717.345 2.774.411 1.006 4.492.762

D) TECHNICAL PROVISIONS FOR LIFE INSURANCE WHERE RISK 0 371.017 0 371.017IS BORNE BY POLICYHOLDERS OF THE INVESTMENT

E) PROVISIONS FOR LIABILITIES AND CHARGES 0 46.770 31.657 78.427

F) DEPOSITS RECEIVED FOR OUTWARD REINSURANCE AND RETROCESSIO 51.011 1.271 0 52.282

G) DEFERRED TAX LIABILITIES 0 0 194.026 194.026

H) PAYABLES 19.653 751 216.477 236.881

I. Payables arising from direct insurance and coinsurance transactions 19.653 751 20.180 40.584II. Payables arising from reinsurance transactions 0 0 9.820 9.820III. Tax liabilities 0 0 58.610 58.610IV. Other liabilities 0 0 127.867 127.867

I) ACCRUED EXPENSES AND DEFERRED INCOME 13.256 54 0 13.310

TOTAL E Q U I T Y A N D L I A B I L I T I E S 2.732.287 3.577.495 472.141 6.781.923

NON-LIFE SEGMENT OTHER SEGMENT

2006TOTAL

2006 2006LIFE SEGMENT

2006

2006

TOTAL

GRUPO CATALANA OCCIDENTE, S.A. AND SUBSIDIARIES (Catalana Occidente Group)

SEGMENTAL CONSOLIDATED BALANCE SHEETS AT 31 December 2006

NON-LIFE SEGMENT OTHER SEGMENT

2006 20062006

40

(Figures in Thousands of Euros)

ASSETS LIFE SEGMENT

A) INTANGIBLE ASSETS 74.550 40.130 28.047 142.727

I. Goodwill 74.550 40.130 7.196 121.876II. Other intangible assets - - 20.851 20.851

B) PROPERTY, PLANT AND EQUIPMENT 135.680 48.733 49.290 233.703

I. Properties for own use 135.680 48.733 14.026 198.439II. Other items of property, plant and equipment - - 35.264 35.264

C) INVESTMENTS 1.496.056 2.356.557 202.181 4.054.794

I. Investment property 55.023 80.206 4.146 139.375II. Financial assets

1. Held-to-maturity financial assets - - - -2. Available-for-sale financial assets 1.421.804 2.040.316 - 3.462.1203. Held-for-trading financial assets - 198.963 - 198.963

III. Investments accounted for using the equity method 18.339 17.045 172.989 208.373IV. Deposits for inward reinsurance 890 51 - 941V. Other investments - 19.976 25.046 45.022

D) INV. FOR BENEFIT OF LIFE POLICYHOLDERS WHO BEAR RISK - 299.787 - 299.787

F) REINSURER'S SHARE OF TECHNICAL PROVISIONS 287.505 5.374 - 292.879

G) DEFERRED TAX ASSETS - - 24.386 24.386

H) RECEIVABLES 117.793 - 140.997 258.790I. Receivables arising from direct insurance and coinsurance transactions 117.793 - 7.567 125.360II. Receivables arising from reinsurance transactions - 4.136 4.136III. Tax assets - - 3.234 3.234IV. Social security and other receivables - - 126.060 126.060

I) CASH AND CASH EQUIVALENTS 184.136 569.514 -19.730 733.920

J) ACCRUED EXPENSES AND DEFERRED INCOME 110.663 2.535 2.307 115.505

TOTAL A S S E T S 2.406.383 3.322.630 427.478 6.156.491

EQUITY AND LIABILITIES

A) EQUITY 676.004 308.446 1.141 985.591

I. Subscribed capital 18.000 18.000 - 36.000II. Reserves 178.542 178.543 - 357.085III. Less: Treasury shares -3.545 -3.544 - -7.089IV. Reserves for valuation adjustments 98.819 98.818 - 197.637VI. Retained earnings

1. Profit for the year 161.652 12.710 1.141 175.5032. Profit for the year attributable to minority interests -37.612 -300 - -37.9123. Less: Interim dividends - - - -

Equity attributable to the parent's shareholders 415.856 304.227 1.141 721.224

Minority interests 260.148 4.219 - 264.367

B) SUBORDINATED LIABILITIES - - - -

C) TECHNICAL PROVISIONS 1.646.706 2.666.577 - 4.313.283

D) TECHNICAL PROVISIONS FOR LIFE INSURANCE WHERE RISK - 299.787 - 299.787IS BORNE BY POLICYHOLDERS OF THE INVESTMENT

E) PROVISIONS FOR LIABILITIES AND CHARGES - 46.099 24.689 70.788

F) DEPOSITS RECEIVED FOR OUTWARD REINSURANCE AND RETROCESSI 54.395 1.662 - 56.057

G) DEFERRED TAX LIABILITIES - - 188.172 188.172

H) PAYABLES 16.447 - 213.148 229.595