1q18 analysts - pds.com.ph

TRANSCRIPT

1Q18 Analysts’ Briefing7 May 2018 | The Globe Tower BGC

1Q18 Performance: Record results on strong demand for data and larger subscriberbase

• Increase in EBITDA due to higher revenues andkeeping costs in check

• EBITDA margin of 47%

• Increase in EBITDA offset higher depreciation and non-operating charges

• Momentum continues with data-related servicesrepresenting 58% of total service revenues

Service Revenues

33.6YoY

+8%

EBITDA

15.8 +18%

Net Income After Tax

+18%4.5Cash Dividend

222 .75/sh

x%

Service Revenues

33.2EBITDA

16.1Net Income After Tax

4.7

Pre-PFRS Post-PFRS

• Record Date: May 17, 2018• Payment Date: June 1, 2018

Broad-based revenue growth as market continues shift towards data

Mobile* Home Broadband*

Fixed Line Voice*

Corporate Data*

Total*

Δ1Q17 +9% +11% +4% -18% +8%

3

• Robust prepaid gross acquisitions drive increase insubscriber base

• New product offers drive strong gross acquisitions forfixed wireless service

+17%+8%58.6million

63.3million

Mobile Subscribers Home Broadband Subscribers

1Q17 1Q18

1.19million

1Q17 1Q18

1.40million

Postpaid Prepaid TM Wireless Wired

* Pre-PFRS

Petabytes

53%

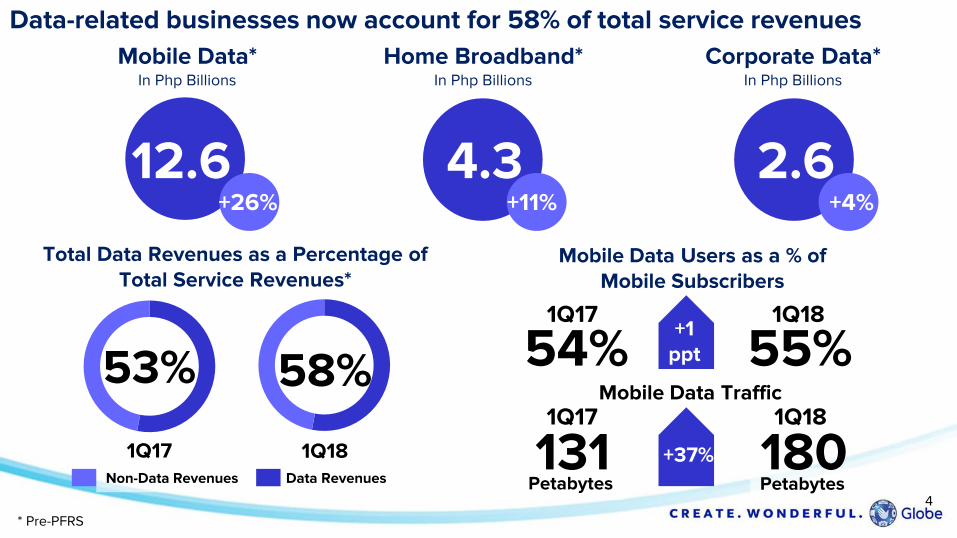

Data-related businesses now account for 58% of total service revenues

Home Broadband*In Php Billions

Corporate Data*In Php Billions

Mobile Data*In Php Billions

Total Data Revenues as a Percentage of Total Service Revenues*

58%

1Q17 1Q18 +35% 180Petabytes

+37%

Mobile Data Users as a % of Mobile Subscribers

Mobile Data Traffic1Q181Q17

55%1Q181Q17 +35%+1

ppt

Non-Data Revenues Data Revenues

12.6 4.3 2.6+26% +11% +4%

4

131

54%

* Pre-PFRS

New products, partnerships and devices geared for the Filipino digital lifestyleGlobe Gaming launched in

partnership with Mineski, Riot

Games, and Garena for esports

Rollout of GCash in more fast food and casual dining outlets, major retailers and gas stations in full swing

GCash and Alipay jointly

launch new GCash QR Code

Discover new journeys with

the Samsung Galaxy S9 and

S9+ powered by ThePLAN

Chow King Max’s Group

Primer Group Robinson’s Retail

5

Shell

Jollibee Shakeys

Up by

low single digitfrom 2017 level

Maintained at

~40%

A look back at our Consolidated Outlook for 2018

Up by

mid single digitfrom 2017 level

Increase to

~mid 40%

• All other original guidance items pertaining to capex, gearing and cost considerations remain

upgrade to

upgrade to

Original Revised

6

Revenues

EBITDA MarginEBITDA Margin

Revenues

Financial Highlights

Consolidated Financial Highlights: Revenue growth of 8%, combined with lowersubsidies, depreciation, and non-operating charges led to an 18% increase in NIAT

* OPEX & Subsidy includes interconnect charges** Core Net Income excludes forex, mark-to-market gains and losses, and non-recurring items

8

3M18

(Pre-PFRS)3M17 YoY% 4Q17 QoQ%

3M18

(Post-PFRS)

Gross Service Revenues 33,638 31,122 8% 32,767 3% 33,178

OPEX and Subsidy (17,878) (17,806) 0% (20,065) -11% (17,097)

EBITDA 15,760 13,316 18% 12,702 24% 16,081

EBITDA Margin 47% 43% 39% 48%

Depreciation (7,285) (6,437) 13% (7,396) -2% (7,285)

EBIT 8,475 6,879 23% 5,306 60% 8,796

Non-Op Charges (1,753) (1,320) 33% (2,027) -14% (1,753)

Provision for Tax (2,266) (1,798) 26% (1,175) 93% (2,362)

Net Income 4,456 3,761 18% 2,104 112% 4,681

Core Net Income 4,572 3,681 24% 2,339 95% 4,797

Changes in Accounting Rules for 2018

Item PFRS 9 PFRS 15 Effect Explanation

Service Revenues Decrease in overall service revenues

• Mobile • Decrease in service revenues due to re-allocation as non-service revenues

• Mobile ARPUs will decrease in line with service revenues

• Broadband / Corporate Data

Effect on service and non-service revenues will be relatively immaterial compared to mobile

Non-Service Revenues

• Increase in non-service revenues as the allocation to equipment will be based on standalone selling price

• Sale of equipment is recognized upfront

Cost of Sales / Operating Expenses

• Decrease as subscriber acquisition costs are amortized over contract period instead of up-front

• Increase as subscriber recontracting costs are now included as part of cost of sales instead of operating expenses.

• Increase due to higher provision for bad debts

EBITDA / EBITDA Margin

• Increase as subscriber acquisition costs are amortized over contract period instead of up-front

• Decrease due to higher provisions for bad debts

9

13,316 15,760

2,516 257 136 402 567 300

3M17 EBITDA Inc. in

Revenues

Dec. in

Interconnect

Charges

Dec. in Staff

Costs

Dec. in

Marketing &

Subsidy

Inc. in Network

Costs

Inc. in

Provisions,

Services &

Other OPEX

3M18 EBITDA

YoYPre-PFRS

(in Php Mn)

+18%

EBITDA growth of 18% driven by the increase in revenues and decreases ininterconnect, staffing, and subsidies, partly negated by increased network costsand provisions, services and other opex

10

12,702 15,760

871 89 1,226 384 505 17

4Q17 EBITDA Inc. in

Revenues

Dec. in

Interconnect

Charges

Inc. in Staff

Costs

Dec. in

Marketing &

Subsidy

Dec. in

Network Costs

Dec. in

Provisions,

Services &

Other OPEX

1Q18 EBITDA

QoQPre-PFRS

(in Php Mn)

+24%

Gain in EBITDA tempered by higher depreciation, non-operating charges and taxes,resulting in 18% increase in net income.

11

3,761 4,456

2,444 848 433 468

3M17 Reported

Net Income

Change in EBITDA Inc. in

Depreciation

Inc. in Non-

operating

expenses

Inc. in Tax 3M18 Reported

Net Income

YoYPre-PFRS

(in Php Mn)

QoQPre-PFRS

(in Php Mn)

+18%

+112%

2,104

4,456 3,058 111 274 1,091

4Q17 Net Income Change in EBITDA Dec. in

Depreciation

Dec. in Non-

operating

expenses

Inc. in Tax 1Q18 Reported

Net Income

2015 2016 2017 2018

Data Business Support Core Others

CAPEX BREAKDOWNIn Php Bn

1Q18 Rollout Update

12

Capital expenditures at approximately Php6.6 billion or USD127 million*, with64% related to data requirements

* Based on FX rate of Php51.887

+508

+59K

LTE SITES

HOME BROADBAND

SUBSCRIBER LINES*

* Composed of wired and wireless

8%

30%

15%

48%

10%

14%

11%

65%

9%

2%

7%

82%

32.136.7

42.5

6.6

20%

14%

2%

64%

Cash Dividends

Rate per Common

Share

Record date:

Payment date:

13

Debt levels remain within covenant ratios

• The financial tests under Globe’s loan agreements include compliance with the following ratios:

• Total Debt-to-Equity not exceeding 2.5:1• Total Debt-to-EBITDA not exceeding 3:1• Debt Service Coverage exceeding 1.3x

22 .75/sh

May 17, 2018

June 1, 2018

YTD March

2018*

YTD Dec

2017

Gross debt (in Php Bn) 127.9 131.5

Gross Debt-to-Equity 1.96x 1.98x

Gross Debt-to-EBITDA 2.25x 2.43x

Debt Service Coverage Ratio 3.09x 3.38x

*Post-PFRS

Globe will divest all or part of its tower assets• UBS appointed as Financial Adviser in project’s preparatory phase

• Towers to be open for lease to potential new and existing players.

• In support of the government’s initiative to open the telco industry to more competition

• To speed up the build and deployment of cellular towers in the Philippines

14

Beginning 1Q18, Globe’s financial reporting will incorporate Philippine FinancialReporting Standard (PFRS) 9, Financial Instruments: Recognition and Measurement,and PFRS 15, Revenue from Contracts with Customers

What is PFRS 9?

PFRS 9, Financial Instruments: Recognition and Measurement,

provides guidance on classifying financial instruments.

What is the impact of adoption of

PFRS 9 to Globe?

The new provisioning methodology,the Expected Credit Loss Model,assigns higher provisions for lowerquality customers (and lowerprovisions for higher qualitycustomers), reflecting the truepicture of portfolio quality based onacquisition, payment behavior, andportfolio outlook.

How will this adjustment be

reflected in Globe’s books?

With the adoption of the modifiedretrospective approach, there will bea deduction to Retained Earnings ofPhp5.58 Billion, net of tax (Php7.98Billion gross) in 1Q 2018.

What is PFRS 15?

What is the impact of adoption of

PFRS 15 to Globe?

How will this adjustment be

reflected in Globe’s books?

PFRS 15, Revenue from Contracts with Customers, provides guidance

on accounting for revenue from contracts with customers.

The new standard changes the long-standing practice of using monthlyservice fees to subsidize upfrontcost of handsets, thus, requiringtelco operators to carry out a"relative fair value" allocationbetween the handset and service.

With the adoption of the modifiedretrospective approach, there will bean addition to retained earningsamounting to Php1.79 Billion, net oftax (Php2.56 Billion gross) as ofMarch 31, 2018.

16

PFRS 15 and 9 Adjustments to Retained Earnings

With Globe’s adoption of the modified retrospective approach, the effects of PFRS 9and 15 on prior year will be booked to Retained Earnings in the Balance Sheet

In Php Mns

Retained Earnings, 12/31/2017 21,708

Add (Deduct) the following:Effect of PFRS 9 (5,587)Effect of PFRS 15 1,790

Retained Earnings, 01/01/2018 17,912

17