17th ceo survey sector key findings pharma & life … · ceos are even more convinced than ......

TRANSCRIPT

Fit for the future17th Annual Global CEO Survey

Key findings in the pharmaceuticals and lifesciences industry

www.pwc.com/ceosurvey

February 2014

PwC

Contents

Page

Sector snapshot 3

Confidence in growth 7

The global rebalancing act 12

Transforming business 17

2February 201417th Annual Global CEO Survey – Key findings in the pharmaceuticals & life sciences industry

PwC

Sector snapshot

3February 201417th Annual Global CEO Survey – Key findings in the pharmaceuticals & life sciences industry

PwC

Sector snapshot

Pharmaceuticals and life sciences CEOs believe thattechnology is transforming the sector and they’re usingstrength in innovation to make the most of it. They’realso focused on regulation and integrity. Facing thetalent challenge is a key priority too, particularly withdemographics and shifts in wealth also radicallyreshaping the sector.

4February 201417th Annual Global CEO Survey – Key findings in the pharmaceuticals & life sciences industry

PwC

Sector snapshot

Technology, demographics, andshifts in wealth are transformingthe sectorPharmaceuticals and life sciencesCEOs are even more convinced thantheir peers that technologicaladvances will transform theirbusinesses in the next five years. Andthey’re more conscious than otherCEOs of the huge role demographicswill play – 72% see it as atransformative trend, compared to60% across the sample. More are alsoexpecting a big impact from globalshifts in economic power.Pharmaceuticals and lifesciences CEOs believetechnology will help more thanhinderOnly around a third of sector CEOsare concerned that the speed oftechnological change may negativelyimpact growth, compared to nearlyhalf of CEOs across the overallsample.

Innovation is a top priority – andprotecting intellectual propertya worry

Sector CEOs are already transformingtheir R&D function to cope withtransformation – 38% say they’vecompleted or have in progress aprogramme to change their R&D andinnovation strategies, more thanacross the sample as a whole. And thesame number believe that their R&Ddepartments are well-prepared for thechallenge.

Too relaxed when it comes tocyber-security?

A surprising 57% of pharmaceuticalsand life sciences CEOs are notconcerned that cyber threats includinglack of data security could threatengrowth. That’s despite a boom in bigdata and data analytics – 79% agreethere’s a need to change strategies inthat regard, although just 23% havealready started.

5February 201417th Annual Global CEO Survey – Key findings in the pharmaceuticals & life sciences industry

PwC

Sector snapshot

Regulation is not all bad

The pharmaceuticals and life sciencesindustry is highly regulated, andnearly four-fiths of CEOs (79%) areconcerned that over-regulation couldput the brakes on growth. That said, afull 72% recognise its value , believingthat their production and/or servicedelivery quality standards improvedover the past 12 months as a result ofregulation.

Integrity is a big issue

The industry is taking safety seriously;more pharmaceuticals and lifesciences CEOs strongly agree that it isimportant to them to ensure theintegrity of their supply chain (76% vs58% overall). And sectors worry aboutthe impact of bribery and corruption.61% believe it could slow downgrowth, compared to 52% of CEOsoverall.

But sector CEOs are positiveabout facing the talent challenge

Only around half of pharmaceuticalsand life sciences CEOs are concernedabout the availability of key skills, thisyear, far fewer than their peers acrossthe sample. Fewer are concernedabout rising labour costs in high-growth markets too. That may bebecause many have already takensteps to revamp their talent strategy tocapitalise on major trends – 43% saythey’ve already begun or completed achange programme, compared to 32%overall.

76%have cut costs

<40%are well-preparedfor change(customer services HR, IT departments)

6February 201417th Annual Global CEO Survey – Key findings in the pharmaceuticals & life sciences industry

PwC

Confidence in growth

of pharmaceuticals and life sciencesCEOs are somewhat or very confidentof growth over 3 years

7February 201417th Annual Global CEO Survey – Key findings in the pharmaceuticals & life sciences industry

PwC

Views on the economy are looking up

32% of pharmaceuticals and lifesciences CEOs believe that the globaleconomy will improve in the next 12months, compared to just 9% last year.And while a third expected to see theeconomic situation worsen last year,this year only 11% are anticipating aglobal decline.

Still, many pharmaceuticals and lifesciences CEOs are worried aboutcontinued slow or negative growth indeveloped markets (65%). It rankshigher in their list of concerns thandoes a slowdown in high-growthmarkets (57%). That reflects thecontinued importance of maturemarkets, a trend we also see in deallocations.

32

9

11

37

2014

2013

Improve

Decline

53

Base: All respondents 2014 (Pharmaceuticals & life sciences, 119);2013 (Pharmaceuticals & life sciences, 90)Source: PwC 16th Annual Global CEO Survey 2013Source: PwC 17th Annual Global CEO Survey 2014

Q: Do you believe the global economy will improve, stay thesame, or decline over the next 12 months?

Stay the same

56

8February 201417th Annual Global CEO Survey – Key findings in the pharmaceuticals & life sciences industry

PwC

More CEOs expect middle term growth for theircompanies, but not for the industry

Far more pharmaceuticals and lifesciences CEOs – 49% – are very confidentin their company’s growth looking outover the next three years.

That’s a lot higher than those who expectthe industry to grow, though. Just 29% ofpharmaceuticals and life sciences CEOssay they are very confident in theirindustry’s prospects for revenue growthover the next three years.

We saw this pattern in the overall sampleas well. CEOs clearly have confidence intheir ability to growth their ownbusinesses, even if they foresee challengesfor their industries.

Q: How confident are you about your company’s prospects for revenue growthover the next 12 months and three years?

Base: All respondents (Pharmaceuticals & life sciences, 119)

Source: PwC 17th Annual Global CEO Survey 2014

%

Company growth Industry growth

vs.

9February 201417th Annual Global CEO Survey – Key findings in the pharmaceuticals & life sciences industry

3

7

8

13

41

39

49

40

Next 3 years

Next 12 months

Not confident at all Not very confident

Somewhat confident Very confident

PwC

Poor growth indeveloped economies

Pharmaceuticals and lifesciences CEOs are slightlyless worried about thispoor or negative growth indeveloped economies thanthe sample as a whole. It’s“business as usual” forthem as growth rates inthese markets have beenlow for some years now.

Over-regulation, debt & deficit responses, and aslower economy are seen as the top three threats

Percentage who are concernedabout over-regulation

79%

Over-regulation

More than three-quartersof pharmaceuticals and lifesciences CEOs believeover-regulation couldsidetrack growth prospects.That’s far more than acrossthe sample as a whole.

Percentage who are concernedabout government responsesto debt and deficits

76%

Debt and deficitsresponses

Pharmaceuticals and lifesciences CEOs, like theirpeers overall, areconcerned about the abilityof debt-laden governmentsto tackle soaring deficits.It’s a worry that’s beenincreasing over the pastseveral years.

Percentage who are concernedabout poor growth indeveloped economies

65%

10February 201417th Annual Global CEO Survey – Key findings in the pharmaceuticals & life sciences industry

PwC

55

55

57

61

64

64

65

76

79

Lack of stability in capital markets

Exchange rate volatility

Slowdown in high-growth markets

Bribery and corruption

Inability to protect Intellectual property

Increasing tax burden

Continued slow or negative growth indeveloped economies

Government response to fiscal deficit anddebt burden

Over-regulation

But there are also other issues pharmaceuticalsand life sciences CEOs believe could affect growth

• 64% of pharmaceuticals and lifesciences CEOs are concernedabout the increase tax burden,compared 70% of the overallsample.

• Reflecting the importance ofinnovation to the sector, 64% ofpharmaceuticals and life sciencesCEOs are concerned that aninability to protect intellectualproperty will hamper growth, farmore than the 43% across thesample as a whole.

• The sector also worries about theimpact of bribery and corruption.61% believe it could slow downgrowth, compared to 52% of CEOsoverall.

Q: How concerned are you, if at all, about each of the following threats to yourgrowth prospects? Top choices listed

Base: All respondents (Total sample, 1344; Pharmaceuticals & life sciences, 119)

Note: Respondents who stated ‘extremely’ or ‘somewhat’’ concerned.

Source: PwC 17th Annual Global CEO Survey 2014

%

11February 201417th Annual Global CEO Survey – Key findings in the pharmaceuticals & life sciences industry

PwC

The global rebalancing act

of pharmaceuticals and life sciencesCEOs expect China to be their mainnon-domestic growth market in thecoming year

12February 201417th Annual Global CEO Survey – Key findings in the pharmaceuticals & life sciences industry

PwC

Pharmaceuticals and life sciences CEOs areexpanding more in mature markets

Pharmaceuticals and lifesciences CEOs looking atWestern Europe for planneddeals

More growth confidencein Western Europe

Around a third ofpharmaceuticals and lifesciences CEOs planningdeals have their eyes onWestern Europe when itcomes to transactions.

Pharmaceuticals and lifesciences CEOs expecting amerger, acquisition, JV orstrategic alliance to be in NorthAmerica

North America standsout

Compared to the overallsample, more CEOs whoare planning deals arelooking to North America.Still, interest has declinedfrom last year.

Pharmaceuticals and lifesciences CEOs expectingtransactions in southeast Asia

Asia less appealing

Pharmaceuticals and lifesciences CEOs weremarkedly less likely to beinterested in transactionsin south or south-east Asia,or Australasia.

37%

30%

19%

13February 201417th Annual Global CEO Survey – Key findings in the pharmaceuticals & life sciences industry

PwC

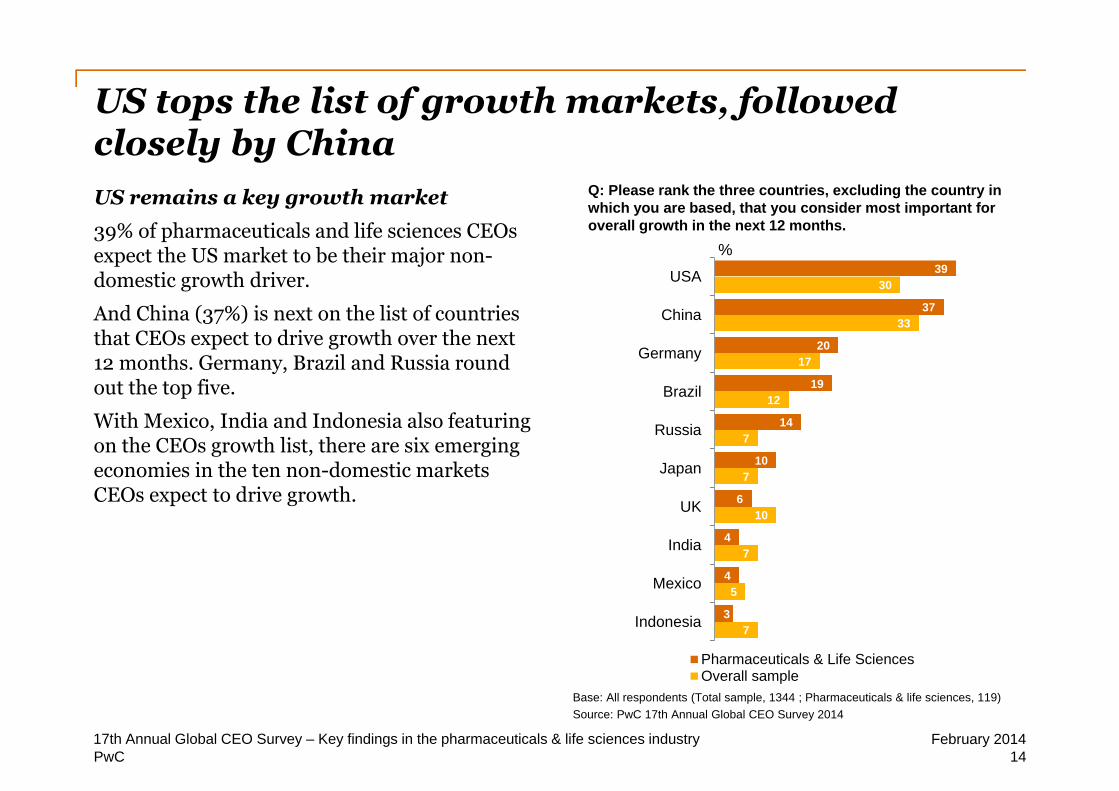

US tops the list of growth markets, followedclosely by China

US remains a key growth market

39% of pharmaceuticals and life sciences CEOsexpect the US market to be their major non-domestic growth driver.

And China (37%) is next on the list of countriesthat CEOs expect to drive growth over the next12 months. Germany, Brazil and Russia roundout the top five.

With Mexico, India and Indonesia also featuringon the CEOs growth list, there are six emergingeconomies in the ten non-domestic marketsCEOs expect to drive growth.

7

5

7

10

7

7

12

17

33

30

3

4

4

6

10

14

19

20

37

39

Indonesia

Mexico

India

UK

Japan

Russia

Brazil

Germany

China

USA

Pharmaceuticals & Life SciencesOverall sample

Base: All respondents (Total sample, 1344 ; Pharmaceuticals & life sciences, 119)

Source: PwC 17th Annual Global CEO Survey 2014Source: PwC 17th Annual GlobalCEO Survey 2014

14February 201417th Annual Global CEO Survey – Key findings in the pharmaceuticals & life sciences industry

Q: Please rank the three countries, excluding the country inwhich you are based, that you consider most important foroverall growth in the next 12 months.

%

PwC

New strategic alliances or joint ventures are themain restructuring activities planned

The pharmaceutical and life sciencesindustry’s appetite for collaborative co-creation continues. The sector’s CEOs aremore likely than other industries to belooking at alliances, JVs or outsourcing.

When it comes to M&A, they’re keepingthings close to home, with less desire forcross-border deals than their peers inother industries.

8

13

14

21

23

25

44

10

11

17

18

25

32

53

End an existing strategic alliance orjoint venture

Sell majority interest in a business orexit a significant market

“Insource” a previously outsourcedbusiness process or function

Complete a cross-border M&A

Complete a domestic M&A

Outsource a business process orfunction

Enter into a new strategic alliance orjoint venture

Pharmaceuticals & life sciences

Overall sample

Q: Which, if any, of the following restructuring activities do youplan to initiate in the coming twelve months? (cost reduction notlisted)

Base: All respondents (Overall sample, 1344, Pharmaceuticals & life sciences, 119)

Source: PwC 17th Annual Global CEO Survey 2014

15February 201417th Annual Global CEO Survey – Key findings in the pharmaceuticals & life sciences industry

%

PwC

Half of pharmaceuticals and life sciences CEOs areactively changing their transaction strategies

Pharmaceuticals and lifesciences CEOs are aheadof the curve when itcomes to changeprogrammes aroundtheir transactionstrategies. Over onequarter (28%) haveprogrammes completedor underway, comparedto 21% cross-industry,while a further 22%have firm plans to takeaction.

13%

13%

24%

19%

20%

22%

21%

28%

Recognise need to change

Developing strategy to change

Concrete plans to implement changeprogrammes

17%

Base: All respondents (Total sample, 1344; Pharmaceuticals & life sciences 119)

Source: PwC 17th Annual Global CEO Survey 2014

Pharmaceuticals &life sciences

Overall sample

Q: In order to capitalise on the two-three global trends which you believe will mosttransform your business over the five years, to what extent are you currentlymaking changes, if any, in the following areas? (M&A, joint ventures or strategicalliances ).

No needto change

14%

16February 201417th Annual Global CEO Survey – Key findings in the pharmaceuticals & life sciences industry

ActionAspiration

PwC

Transforming business

The biggest trend is theageing population. This is going tocreate both a massive risk and amassive opportunity for the world ...The IT explosion and what we areworking on right now is going tolend itself to managing thechallenges that come with the ageingpopulation.

Joseph Jimenez

CEO, Novartis

February 201417th Annual Global CEO Survey – Key findings in the pharmaceuticals & life sciences industry17

PwC

CEOs recognise that global trends aretransforming businessHeaded up by technological advances

Nearly 90% ofpharmaceuticals and lifesciences CEOs identifiedtechnological advances suchas the digital economy,social media, mobiledevices and big data as keytrends transforming theirbusiness.

More than half also pointedto demographic fluctuationsand global shifts ineconomic power, in linewith the global sample.

89%Technologicaladvances

68%Shifts in globaleconomic power

72%Demographicshifts

Q: Which of the following global trends do you believe will transform your businessthe most over the next five years? (Top trends pharmaceuticals & life sciencesCEOs ranked in their top 3.)

Base: All respondents (Total sample, 1344; Pharmaceuticals & life sciences, 119).Source: PwC 17th Annual Global CEO Survey

18February 201417th Annual Global CEO Survey – Key findings in the pharmaceuticals & life sciences industry

PwC

And pharmaceuticals and life sciences CEOsrecognise they’ll need to change in response

Q: To what extent are you currently making changes, if any, in the following areas?

Base: All respondents (Pharmaceuticals & life sciences, 119)

Source: PwC 17th Annual Global CEO Survey 2014

19February 201417th Annual Global CEO Survey – Key findings in the pharmaceuticals & life sciences industry

43

24

23

22

19

18

18

18

14

12

11

9

8

39

37

39

47

56

57

50

40

55

46

48

50

49

16

38

34

28

23

23

29

38

28

40

40

40

43

60% 40% 20% 0% 20% 40% 60% 80%

Location of key operations or headquarters

Corporate governance

Investment in production capacity

Supply chain

Use and management of data and data analytics

Channels to market

Approach to managing risk

R&D and innovation capacity

M&A strategies, joint ventures or strategic alliances

Technology investments

Organisational structure/design

Customer growth and retention strategies

Talent strategies

No need to change Recognise need/developing strategy/concrete plans to change Change programme underway or completed

Aspiration Action

PwC

Pharmaceuticals and life sciences CEOs areembracing innovation and technological change

• More pharmaceuticals and life sciences CEOs (44% vs.35% overall) see product and service innovation as theirmain route to growth.

• The sector’s CEOs are confident in their ability to keepup with a changing world. Just 32% of pharmaceuticalsand life sciences CEOs are concerned about the speed oftechnological change – lower than across the overallsample (47%).

• And more believe that their R&D department is ready tocope. 38% say it’s well-prepared, compared to 28%overall.

In other research,* we’ve foundthat the most successful CEOsare doing three things to‘industrialise’ innovation – i.e.,to make it repeatable,dependable and scalable.

They’re focusing onbreakthrough innovation in allits forms; putting disciplinedinnovation techniques in place;and collaborating much moreactively.

We think it’s important torecognise that innovationmeans more than new productdevelopment. It can also helpimprove processes, or createnew services or businessmodels.

20February 201417th Annual Global CEO Survey – Key findings in the pharmaceuticals & life sciences industry

* PwC’s Breakthrough innovation and growth

PwC

And they’re already emphasising technology’srole in innovation

21February 201417th Annual Global CEO Survey – Key findings in the pharmaceuticals & life sciences industry

“We have to fully utilise new technologieslike bioinformatics, like immunotherapyagainst cancer. There are many emergingtechnologies we must get to grips withright now in order to be able to capitaliseon them in 10 years’ time.”

“For Novartis it’s all about science-based innovation. We have manycompetitors who fail at innovation. Iexpect that in five years from nowwe will have extended our lead ininnovation. We continue to invest inresearch and development andtherefore I expect to accelerate ourgrowth, because we will come upwith some very innovativeproducts.”

Joseph JimenezCEO, Novartis

PwC

But while more than half have plans, just over onethird have acted

There’s a glaring gapbetween

Aspirations

and

Actions

17th Annual Global CEO Survey – Key findings in the pharmaceuticals & life sciences industry22

February 2014

Q: Which, if any, of these national outcomes is your organisation focusing on as a priority over the next three years?Q: To what extent are you currently making changes, if any, in the following areas?Base: All respondents (Total sample, 1,344; Pharmaceuticals & life sciences, 119) Aspirations responses include: recognise need to change,developing strategy to change, concrete plans to implement change programmes, and change programme underway or completed.Source: PwC 17th Annual Global CEO Survey 2014

53% 78%

Most pharmaceuticals & life sciences CEOs want to improve their company’sability to innovate

86%

40%Have started or

completedchanges

38%Have started or

completedchanges

Develop an innovationecosystem

Alter R&D and innovationcapacity

Change technologicalinvestments

PwC

But there’s work to do to in both areas

While nearly four in tenpharmaceuticals and lifesciences CEOs told us thattheir R&D functions are well-prepared for change, justover a quarter show the sameconfidence in theirorganisation’s ITdepartment.

Base: All respondents (Pharmaceuticals & life sciences, 119)

Source: PwC 17th Annual Global CEO Survey 2014

Q: Thinking about the changes you are making to capitalise on transformativeglobal trends, to what degree are the following areas of your organisationprepared to make these changes?

23February 201417th Annual Global CEO Survey – Key findings in the pharmaceuticals & life sciences industry

38% 26%

R&D IT

Well-prepared

Somewhat prepared, not prepared, don’t know or refused

PwC

More pharmaceuticals and life sciences CEOs aretaking on staff than letting them go

say headcountwill increase(50% overall)

say headcountwill stay the

same(29% overall)

say headcountwill decrease(20% overall)

Nearly half ofpharmaceuticals and lifesciences CEOs sayheadcount will increase inthe coming 12 months. Butthis is less than the overallsample predicts.

A quarter expect to reducetheir workforce, comparedto one fifth overall.

24February 201417th Annual Global CEO Survey – Key findings in the pharmaceuticals & life sciences industry

PwC

And CEOs are concerned about developing aworkforce that can cope with a changing world

Talent is one of the main engineof business growth. So one ofthe biggest issues CEOs face, asthese huge demographicchanges occur, is finding andsecuring the workforce oftomorrow – particularly theskilled labour they need to taketheir organisations forward.

• 51% of pharmaceuticals and life sciences CEOs areworried about the availability of key skills. It’s acontinuing concern. As consumerisation dramaticallychanges the delivery of healthcare, old business modelsneed to change, and that includes people and skills.

• 37% of pharmaceuticals and life sciences CEOs believethat creating a skilled workforce should be a governmentpriority, but only 19% believe that the government hasbeen effective.

• So many are taking action themselves – 64% say acreating a skilled workforce is a priority for theircompany.

25February 201417th Annual Global CEO Survey – Key findings in the pharmaceuticals & life sciences industry

PwC

In response, pharmaceuticals and life sciencesCEOs are transforming their talent strategies

Pharmaceuticals and lifesciences CEOs over-whelmingly agree they’llneed to change theirtalent strategies to copewith future trends. 43%are already doing so,compared to under athird of CEOs across theoverall sample.

And 38% believe theirHR departments arewell-prepared to makechanges, compared to30% overall.

12%

10%

22%

14%

27%

24%

32%

43%

Recognise need to change

Developing strategy to change

Concrete plans to implement change programmes

Change programme underway or completed

6%

Action

Base: All respondents (Total sample, 1344; Pharmaceuticals & life sciences, 119)

Source: PwC 17th Annual Global CEO Survey 2014

Pharmaceuticals& life sciences

Overallsample

Q: In order to capitalise on the two-three global trends which you believe will mosttransform your business over the five years, to what extent are you currentlymaking changes, if any, in the following areas? (talent strategies ).

No needto change

8%

26February 201417th Annual Global CEO Survey – Key findings in the pharmaceuticals & life sciences industry

Aspiration

PwC

The sector’s CEOs also need to serve consumers innew ways

• The world is getting wealthier: the number of middle-class consumers is projected to rise dramatically over thenext 15 years, especially in Asia.

• But major inequalities in income remain. Averageincomes in the E7 countries are still less than a third ofthose in the G7 countries, for example.

• And the shift in the balance of economic power is makingit easier for emerging-market competitors to fight for thesame consumers that mature-market companies aretargeting.

CEOs face three key challenges.They have to chase a movingtarget, as consumers evolve indifferent ways in differentmarkets. They have to addressthe needs of more diverse – anddemanding – customersegments. And they have to fightoff increasingly intensecompetition.

27February 201417th Annual Global CEO Survey – Key findings in the pharmaceuticals & life sciences industry

The general population as a stakeholder has probablymade the biggest shift in terms of their expectations.They don’t care what is legal, they care about what isright. What is right is what they perceive as goodethical behaviour.

Joseph Jimenez, CEO, Novartis

PwC

So they’re focusing on customer retention andchannels to market

The vast majority ofpharmaceuticals and lifesciences CEOs plan tochange their customergrowth and retentionstrategies – with nearlytwo-thirds actively engagedalready.

Similarly, most are lookingto refine channels tomarket, with half takingaction in this area.

9%

7%

17%

24%

24%

27%

40%

23%

Recognise need to change

Developing strategy to change

Concrete plans to implement change programmes

Change programme underway or completed

9%

Base: All respondents (Total sample, 1344; Pharmaceuticals & life sciences, 119)

Source: PwC 17th Annual Global CEO Survey 2014

Customergrowth andretentionstrategies

Channelsto market

Q: In order to capitalise on the two-three global trends which you believe will mosttransform your business over the five years, to what extent are you currentlymaking changes, if any, in the following areas? (two listed).

No needto change

18%

28February 201417th Annual Global CEO Survey – Key findings in the pharmaceuticals & life sciences industry

Aspiration Action

PwC

And they’re preparing their organisations toadapt

The customer-focuseddepartments ofpharmaceuticals and lifesciences companies are morelikely than the overall sampleto be well-prepared forchange.

Nearly half the salesdepartments are up to speedin this area, with customerservice and marketing/brandmanagement followingclosely behind.

40%

Base: All respondents (Pharmaceuticals & life sciences, 119)

Source: PwC 17th Annual Global CEO Survey 2014

45%

Q: Thinking about the changes you are making to capitalise on transformativeglobal trends, to what degree are the following areas of your organisationprepared to make these changes?

29February 201417th Annual Global CEO Survey – Key findings in the pharmaceuticals & life sciences industry

38%

Well-prepared

Somewhat prepared, not prepared, don’t know or refused

Sales Marketing & brand management

Customer service

PwC

About PwC’s 17th Annual Global CEO Survey

In ‘Fit for the future: Capitalising onglobal trends’, we also explore threeforces that business leaders think willtransform their business in the nextfive years: technological advances,demographic changes and globaleconomic shifts. We show how thesetrends, and more importantly theinterplay between them, are creatingmany new – but challenging -opportunities for growth through:creating value in totally new ways;developing tomorrow’s workforce;and serving the new consumers.

We also show how, in responding tothese trends, CEOs have theopportunity to help solve importantsocial problems.

In short, the demands being placed onbusiness leaders to adapt to thechanging environment are increasingexponentially; CEOs are having tobecome hybrid leaders who cansuccessfully run the business of todaywhile creating the business oftomorrow.

This sector key findings report takes acloser look at responses frompharmaceuticals and life sciencesCEOs. It is based on 119 interviews,conducted in 40 countries around theworld. We also cite more in-depthconversations with two sector CEOs.

Pharmaceuticals & lifesciences respondents

In countries across theworld

We surveyed 1,344 business leadersacross 68 countries around the world,in the last quarter of 2013, andconducted further in-depth interviewswith 34 CEOs.

Our overall survey sees a leap in CEOs’confidence in the global economy –but caution as to whether this willtranslate into better prospects fortheir own companies. The search forgrowth is getting more and morecomplicated as opportunities in bothdeveloped and emerging economiesbecomes more nuanced, leading CEOsto revise the portfolio of overseasmarkets they will focus on.

30February 201417th Annual Global CEO Survey – Key findings in the pharmaceuticals & life sciences industry

PwC

For more information, please contact:

Acknowledgements

Our thanks to the following CEO quotedin this document.

Joseph Jimenez, CEO

Novartis, Switzerland

Michael F. Swanick Marina Bello Valcarce Dr Sally Drayton

Global Leader+1 267 330 [email protected]

Global Marketing & KnowledgeManagement+44 20 7212 [email protected]

Global KnowledgeManagement+44 207 212 [email protected]

Download the main report,access the results and explorethe CEO interviews from our17th Annual Global CEOSurvey online atwww.pwc.com/ceosurvey

Clickhere toexploresectordata

online

Clickhere tovisit our

sectorwebsite

31February 201417th Annual Global CEO Survey – Key findings in the pharmaceuticals & life sciences industry

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the informationcontained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of theinformation contained in this publication, and, to the extent permitted by law, PwC does do not accept or assume any liability, responsibility or duty of care for any consequencesof you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

© 2014 PwC. All rights reserved. PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please seewww.pwc.com/structure for further details.