16 20 22 partners the - law society of ireland

TRANSCRIPT

Cover StoryGambling on the stock market

The Irish Stock Market has broken all previous recordsover the last five years, but is it a safe bet for the privateinvestor or just the financial world’s answer to LasVegas? Barry O’Halloran reports

The corporate killing fieldsThose responsible for five major UK disasters which left 473 people deadhave never been brought to justice, but recent proposals to createa new British offence of ‘corporate killing’ could changeall that. Paul Burnley and Kirsty Gomersal explain

Get with the programThe rapid growth of information technology hasleft our copyright laws trailing behind. DenisKelleher discusses the existing protections forsoftware authors and argues the case for reform

Firing your partners theAmerican way

A recent partnership case in the United States turned out to be a pot-boiling tale of greed, fear and fiduciary duties. But such a thing couldn’t happen here, could it? Michael Twomeybegs to differ

The better part of discretionDiscretionary trusts can be useful tax-planning mechanisms, butthe legal and technical issues need careful analysis. EamonnO’Connor outlines their potential benefits

Deals on wheelsWhat’s the best option for financing a new company car? Paul O’Grady looksat the wide range of packages available and gets a steer on good deals fromthe professionals

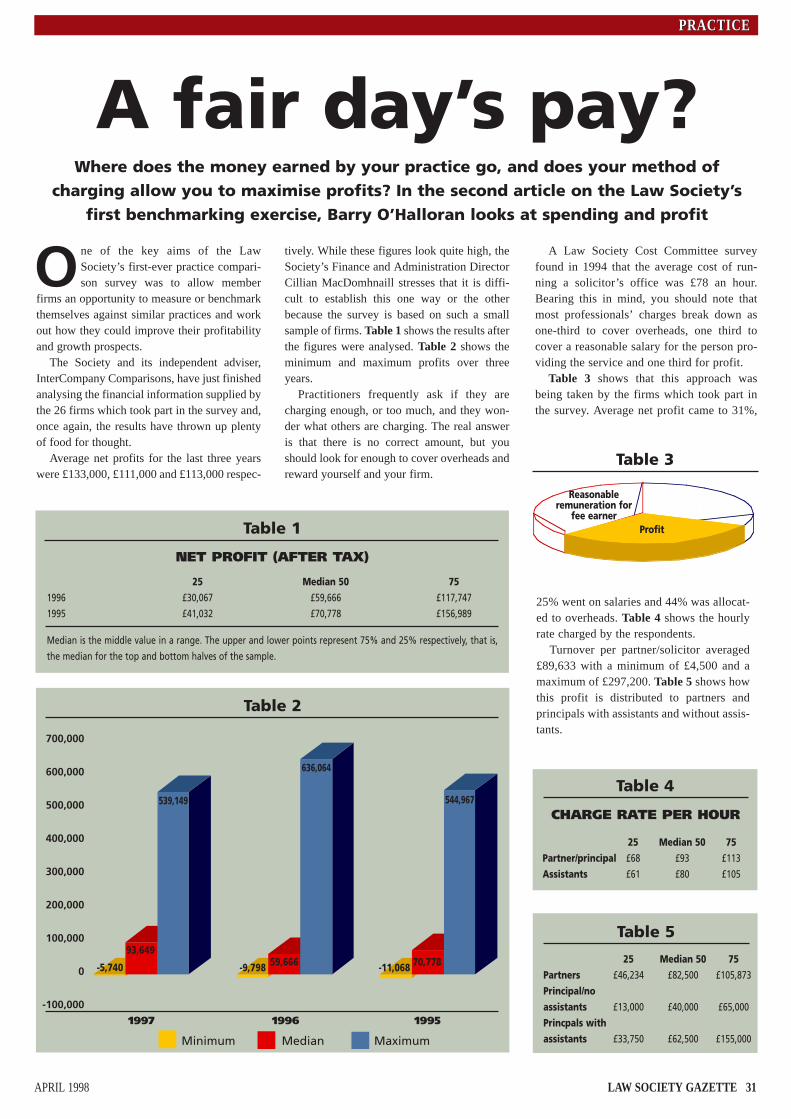

A fair day’s pay?Where does the money earned by your practice go and how can you maximise your profits? The second of two articles on the Law Society’s practice comparison survey

APRIL 1998 LAW SOCIETY GAZETTE 1

CONTENTSCONTENTS

REGULARS

President’s message 3

Viewpoint 4

Letters 7

News 9

Briefing

Council report 33

Committee reports 35

Practice notes 36

Legislation update 37

SBA report and accounts 38

Eurlegal 39

ILT digest 43

People and places 46

Book reviews 51

Professional information 54

12

APRIL 1998APRIL 1998

The views expressed in this publication, save where otherwise indicated, are theviews of contributors and not necessarily the views of the Council of the Law Society.The appearance of an advertisement in this publication does not necessarily indicateapproval by the Law Society for the product or service advertised.

Published at Blackhall Place, Dublin 7, tel: 6710711, fax: 671 0704.

Editorial Board: Dr Eamonn Hall (Chairman), Mary Keane, Ken Murphy, Michael V O’Mahony, Helen Sheehy

Subscriptions: £45 Volume 92, number 3

Editor: Conal O’Boyle MA

Reporter: Barry O’Halloran

Designer: Nuala Redmond

Editorial Secretaries: Andrea MacDermott, Catherine Kearney

Advertising: Seán Ó hOisín, tel/fax: 837 5018, mobile: 086 8117116,10 Arran Road, Dublin 9. E-mail: [email protected]

Printing: Turners Printing Company Ltd, Longford

16

20

22

28

24

31

Rochford BradyLegal Services Ltd

Rochford Brady are Ireland’s largest Lawsearchers and second largest Town Agents (but catching up daily).

Rochford Brady are the only Lawsearchers/Town Agents to have been awarded the ISO 9002 Quality Service Mark.

Rochford Brady are the only Lawsearchers/Town Agents with Professional Indemnity Insurance of £2 million.

Rochford Brady are the only Lawsearchers who carry out planning searches in all counties.

Rochford Brady are the firm chosen by the current planning tribunal. Only Rochford Brady could handle a job of this size.

If you are not with Rochford Brady, isn’t it time you changed?

Phone: 1850 529732 (20 lines)

Fax: 1850 762436 (5 lines)

Rochford BradyLegal Services Ltd

Rochford Brady are Ireland’s largest Lawsearchers and second largest Town Agents (but catching up daily).

Rochford Brady are the only Lawsearchers/Town Agents to have been awarded the ISO 9002 Quality Service Mark.

Rochford Brady are the only Lawsearchers/Town Agents with Professional Indemnity Insurance of £2 million.

Rochford Brady are the only Lawsearchers who carry out planning searches in all counties.

Rochford Brady are the firm chosen by the current planning tribunal. Only Rochford Brady could handle a job of this size.

If you are not with Rochford Brady, isn’t it time you changed?

Phone: 1850 529732 (20 lines)

Fax: 1850 762436 (5 lines)

ISO 9002

TOWN AGENTS

LAWSEARCHERS

SUMMONS SERVERS

COMPANY FORMATION

AGENTS

APRIL 1998 LAW SOCIETY GAZETTE 3

PRESIDENT’S MESSAGEPRESIDENT’S MESSAGE

A s you’ll see from the reporton page 9 of this month’sissue, on 11 March I wel-

comed large numbers to the NewHorizons business breakfast hosted bythe Law Society and sponsored byPrice Waterhouse. In my introductionof the guest speaker, Michael Buckley,Managing Director of AIB CapitalMarkets, I indicated that the successof the financial services sector inIreland over the last ten years hadbeen truly remarkable. I pointed out that it had been created by thevision and tenacity of a few and that it was the collective challenge toall of us to ensure its continued success in entrepreneurial mode,unburdened by undue bureaucracy.

I was proud to say then, and to repeat now, that the members of ourprofession have played their part in an active, constructive and concreteway in building and creating this success. As President of your society,I acknowledge and pay tribute to the role of our members who have par-ticipated in this great accomplishment of our times.

Michael Buckley, in his speech, praised the solicitors’ profession forits great role in the creation of that enormous success, the InternationalFinancial Services Centre. He called on our profession to now play arole in its development over the next ten years, and I am glad to reportthat the Council has agreed with my proposal to appoint a task force toreview this area, to liaise with the Government committees and others,and to consider and work positively towards ensuring that the nextdecade will be just as successful as the past ten years.

National Crime ForumI congratulate our colleague, Professor Bryan McMahon, on takingthe chair of this important initiative of the Minister for Justice. I wishhim well on all our behalves in his endeavours. Your society has com-mitted itself to supporting this initiative, and James MacGuill is amember of the forum. The Criminal Law Committee is presentlyworking on a written submission to the forum on behalf of the pro-fession.

Recently there has been a certainamount of criticism of people who havereduced their tax rates by investing inapproved investments which generate taxrelief. I need hardly remind the critics thatmany of the large number of cranes thatare visible from Blackhall Place are aresult of those tax incentives, which havealso contributed to the creation of whathas become known as the Celtic Tiger.

It is unfair to criticise those who havelegitimately invested in investments

which generate tax relief. It is unfortunate that many of the developmentsin this area which were financed by investors who put some of their dis-posal income at risk and were rewarded with a tax saving should now beclassed as tax dodgers. If the reliefs need to be revisited, then by all meansthe reliefs should be revisited – but those that have legitimately takenadvantage of the reliefs offered should not be criticised for doing so.

Annual conferenceDue to the unprecedented number of colleagues who wished to attend ourconference in Florence, the organising committee, chaired by Gerry Griffin,and I are very upset at our inability to accommodate all our colleagues. Wehave endeavoured to do as much as possible. I look forward to welcomingall those travelling to Florence. See you at the Piazza Del Duomo.

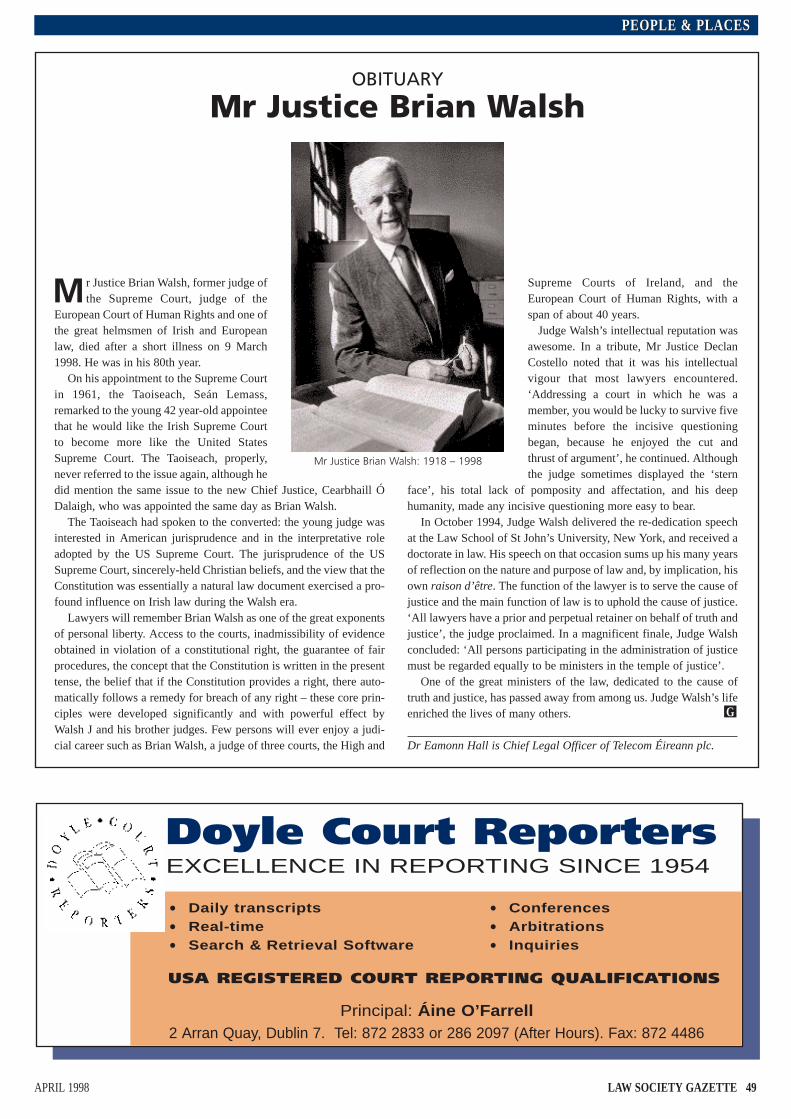

Mr Justice Brian WalshFinally, during the last month the death occurred of Mr Justice Brian Walsh.He was a beacon in the Irish legal profession and helped in particular todevelop the people’s rights under the Constitution. The same words usedlong ago by the Times in an obituary of unparallelled eulogy, referring tothe passing of Christopher Palles, the Lord Chief Baron of the Court of theExchequer in Ireland, appear entirely appropriate: ‘A long, eminent andhonourable life, devoted to the betterment of social institutions and to elu-cidating and clarifying our legal system, has been closed’.

Laurence K ShieldsPresident

Financial services and the legal profession

4 LAW SOCIETY GAZETTE APRIL 1998

VIEWPOINTVIEWPOINT

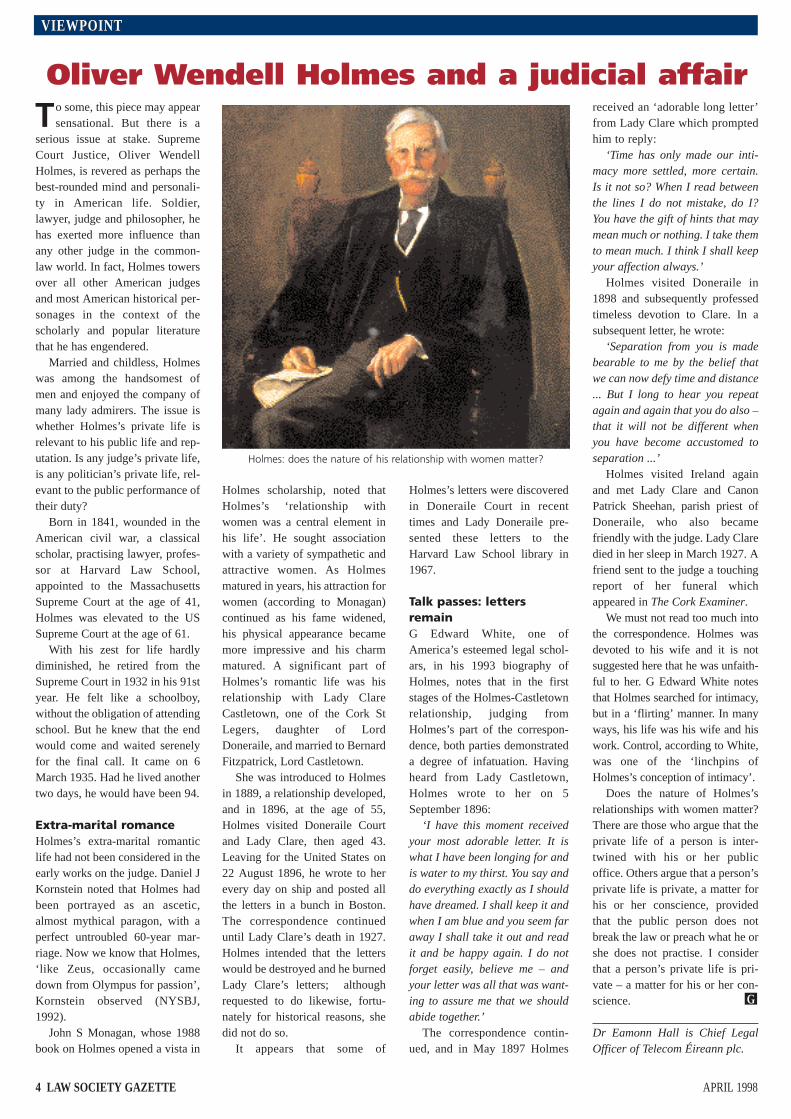

To some, this piece may appearsensational. But there is a

serious issue at stake. SupremeCourt Justice, Oliver WendellHolmes, is revered as perhaps thebest-rounded mind and personali-ty in American life. Soldier,lawyer, judge and philosopher, hehas exerted more influence thanany other judge in the common-law world. In fact, Holmes towersover all other American judgesand most American historical per-sonages in the context of thescholarly and popular literaturethat he has engendered.

Married and childless, Holmeswas among the handsomest ofmen and enjoyed the company ofmany lady admirers. The issue iswhether Holmes’s private life isrelevant to his public life and rep-utation. Is any judge’s private life,is any politician’s private life, rel-evant to the public performance oftheir duty?

Born in 1841, wounded in theAmerican civil war, a classicalscholar, practising lawyer, profes-sor at Harvard Law School,appointed to the MassachusettsSupreme Court at the age of 41,Holmes was elevated to the USSupreme Court at the age of 61.

With his zest for life hardlydiminished, he retired from theSupreme Court in 1932 in his 91styear. He felt like a schoolboy,without the obligation of attendingschool. But he knew that the endwould come and waited serenelyfor the final call. It came on 6March 1935. Had he lived anothertwo days, he would have been 94.

Extra-marital romanceHolmes’s extra-marital romanticlife had not been considered in theearly works on the judge. Daniel JKornstein noted that Holmes hadbeen portrayed as an ascetic,almost mythical paragon, with aperfect untroubled 60-year mar-riage. Now we know that Holmes,‘like Zeus, occasionally camedown from Olympus for passion’,Kornstein observed (NYSBJ,1992).

John S Monagan, whose 1988book on Holmes opened a vista in

Holmes scholarship, noted thatHolmes’s ‘relationship withwomen was a central element inhis life’. He sought associationwith a variety of sympathetic andattractive women. As Holmesmatured in years, his attraction forwomen (according to Monagan)continued as his fame widened,his physical appearance becamemore impressive and his charmmatured. A significant part ofHolmes’s romantic life was hisrelationship with Lady ClareCastletown, one of the Cork StLegers, daughter of LordDoneraile, and married to BernardFitzpatrick, Lord Castletown.

She was introduced to Holmesin 1889, a relationship developed,and in 1896, at the age of 55,Holmes visited Doneraile Courtand Lady Clare, then aged 43.Leaving for the United States on22 August 1896, he wrote to herevery day on ship and posted allthe letters in a bunch in Boston.The correspondence continueduntil Lady Clare’s death in 1927.Holmes intended that the letterswould be destroyed and he burnedLady Clare’s letters; althoughrequested to do likewise, fortu-nately for historical reasons, shedid not do so.

It appears that some of

Holmes’s letters were discoveredin Doneraile Court in recenttimes and Lady Doneraile pre-sented these letters to theHarvard Law School library in1967.

Talk passes: lettersremainG Edward White, one ofAmerica’s esteemed legal schol-ars, in his 1993 biography ofHolmes, notes that in the firststages of the Holmes-Castletownrelationship, judging fromHolmes’s part of the correspon-dence, both parties demonstrateda degree of infatuation. Havingheard from Lady Castletown,Holmes wrote to her on 5September 1896:

‘I have this moment receivedyour most adorable letter. It iswhat I have been longing for andis water to my thirst. You say anddo everything exactly as I shouldhave dreamed. I shall keep it andwhen I am blue and you seem faraway I shall take it out and readit and be happy again. I do notforget easily, believe me – andyour letter was all that was want-ing to assure me that we shouldabide together.’

The correspondence contin-ued, and in May 1897 Holmes

received an ‘adorable long letter’from Lady Clare which promptedhim to reply:

‘Time has only made our inti-macy more settled, more certain.Is it not so? When I read betweenthe lines I do not mistake, do I?You have the gift of hints that maymean much or nothing. I take themto mean much. I think I shall keepyour affection always.’

Holmes visited Doneraile in1898 and subsequently professedtimeless devotion to Clare. In asubsequent letter, he wrote:

‘Separation from you is madebearable to me by the belief thatwe can now defy time and distance... But I long to hear you repeatagain and again that you do also –that it will not be different whenyou have become accustomed toseparation ...’

Holmes visited Ireland againand met Lady Clare and CanonPatrick Sheehan, parish priest ofDoneraile, who also becamefriendly with the judge. Lady Claredied in her sleep in March 1927. Afriend sent to the judge a touchingreport of her funeral whichappeared in The Cork Examiner.

We must not read too much intothe correspondence. Holmes wasdevoted to his wife and it is notsuggested here that he was unfaith-ful to her. G Edward White notesthat Holmes searched for intimacy,but in a ‘flirting’ manner. In manyways, his life was his wife and hiswork. Control, according to White,was one of the ‘linchpins ofHolmes’s conception of intimacy’.

Does the nature of Holmes’srelationships with women matter?There are those who argue that theprivate life of a person is inter-twined with his or her publicoffice. Others argue that a person’sprivate life is private, a matter forhis or her conscience, providedthat the public person does notbreak the law or preach what he orshe does not practise. I considerthat a person’s private life is pri-vate – a matter for his or her con-science.

Dr Eamonn Hall is Chief LegalOfficer of Telecom Éireann plc.

G

Oliver Wendell Holmes and a judicial affair

Holmes: does the nature of his relationship with women matter?

APRIL 1998 LAW SOCIETY GAZETTE 5

VIEWPOINTVIEWPOINT

A lmost without you realisingit, European Community

law comes before the averagelawyer on a daily basis, regardlessof his or her areas of practice.Apart from competition law, agri-culture and customs matters, thiscontact with Community law willbe through EC directives. Yet,since directives are implementedthrough national legislation, thelikelihood is that most lawyerswill look only at the relevant Actor statutory instrument and willnot think it worthwhile to be both-ered looking at the EC directiveon which the national law isbased. This might seem logical.But there are times when the useof Community law will benefityour client greatly.

Interpreting national lawAdmittedly, it is national legisla-tion which is generally the sourceof your client’s legal rights andobligations. But it is importantalways to remember that thenational law must be interpretedand applied so as to be consistentwith any underlying EC directive.Indeed, the European Court hasruled that, when interpreting andapplying national law, everynational court must presume thatthe State had the intention of ful-filling entirely the obligationsarising from the directive con-cerned.

Three questions should arise inthe mind of the inquiring lawyer:first, is there an EC directive gov-

erning the matter in issue? sec-ond, what interpretation is to begiven to the directive in question?and, third, does the national lawproperly implement the direc-tive? While it is generally recog-nised that the national law mustbe interpreted in line with thedirective, what is often ignored isthe problem of interpretation ofthe directive itself.

The rules governing interpre-tation of directives are relativelyclear: Community legislation isto be interpreted teleologically –that is, by having regard to itsobjectives; it is to be interpretedso as to be consistent with the ECTreaty and with general princi-ples of Community law such asproportionality. Derogations arenormally to be interpreted strict-ly: reference should be made tothe preamble of the legislation todetermine its meaning and pur-pose.

Different versionsMost importantly, however, it isoften not enough to look solely atthe English language version of adirective in order to grasp itsmeaning. EC legislation is draft-ed in each of the official lan-guages of the Community, all ofwhich are equally authentic. Aninterpretation of a provision ofEC law thus involves a compari-son of the different language ver-sions in order to arrive at a com-mon, or ‘proper’, meaning.

Now, admittedly, most lawyers

are not going to go to the trouble,each and every time they arefaced with a question of law, oftracking down 11 different lan-guage versions of a directive. Butjust consider the following sce-nario which formed the basis of ajudgment of the European Courtof Justice a few months ago.

Council Directive 79/112/EECconcerns the labelling of food-stuffs. The English language ver-sion stipulated such labellingmust indicate the ‘name andaddress of the manufacturer orpackager, or of a seller estab-lished within the Community’.However, the Italian versionomitted the comma and requiredthe indication of the ‘name andaddress of the manufacturer orpackager or of a seller establishedwithin the Community’. The

implementing Italian decree fol-lowed this version. Thus, on theface of it, the Italian legislationwas wholly in conformity withthe directive.

Clever defenceA problem was spotted by aclever defence lawyer when hisclient was prosecuted by theItalian authorities for selling acertain foodstuff, the labelling ofwhich indicated solely the nameand address of the producer whowas established outside theCommunity. By comparing thedifferent language versions inEnglish, French, Dutch andGerman, the Court of Justicedeclared that the comma was vitalto establishing the proper inter-pretation. Thus, the condition ofestablishment within theCommunity applied only to thereseller, and not to the manufac-turer or packager. The defendantwas acquitted.

Unfortunately, it is not uncom-mon for EC legislation to be poor-ly worded or badly translated. It isa sad fact of life that the carewhich goes into the drafting of thefinal version of Irish or Britishlegislation is not always emulatedby the Community institutions.The vigilant lawyer shouldalways bear this in mind.

Conor Quigley is a barrister prac-tising at Brick Court Chambers,Brussels and London, specialisingin European Union law.

G

A comma can make all the difference in European terms

New edition. Available in Word 6 and WordPerfect 5.1Price per disk (incl p&p): £5 + 1.05 (VAT): £6.05

PRECEDENT FAMILY LAW DECLARATION FORMS – DISKThe Law Society, Blackhall Place, Dublin 7. Fax: (credit card payments only) 671 0704.

Please supply disk(s). (Disk suitable for Word 6 or WordPerfect 5.1)

I enclose a cheque for £ OR you are authorised to debit £ to my credit card(Access, Visa, Mastercard or Eurocard only)

Card Type: Card No: Expiry Date:

Name:

Firm address

LAW SOCIETYCONVEYANCINGCOMMITTEE

PRECEDENT FAMILY LAW DECLARATION FORMS – ON DISKNOWAVAILABLE on

DISK

Conor Quigley: not uncommon forEU law to be poorly worded

Letters

APRIL 1998 LAW SOCIETY GAZETTE 7

VIEWPOINTVIEWPOINT

From: Irene Lynch, Departmentof Law, University College Cork

Iwas very surprised, as indeedwere a number of my col-

leagues, to see the first headlineon the March Gazette: Your GirlFriday: how to find the best legalsecretaries.

Describing a highly skilled,usually extremely hardworking,member of staff of any solicitor’soffice in such pejoratively sexistterms is so blatantly discriminato-ry as to be almost laughable. Notonly that, the editorial team in theLaw Society do not seem to be

aware of the terms of theEmployment Equality Act, 1977which prohibits employers fromdescribing any particular post interms which imply that it is onlysuitable for a man or a woman. Ifwe find such low editorial stan-dards in the Law Society, whatcan we expect elsewhere?

The editor replies:As far as we are aware, the termsof the Employment Equality Act,1977 do not apply to magazineheadlines. Nevertheless, it’s goodto know that political correctnessis alive and kicking in Cork.

From: Patrick J Farrell, Patrick JFarrell and Co, Co Kildare

Iwrote to a well-known Dublinmedical consultant some years ago

for a report on a young nurse whowas struck by a car while cycling towork. In due time the report arrivedwith a covering note which stated: ‘Ihave looked very carefully and thereis no sign of her’.

After reading this sentence sev-eral times and failing to make anysense of it, my own letter request-ing the report caught my eye. In thecourse of it, my typist had written:‘She was injured and is still underyour car’!

From: McCann FitzGerald, Dublin

The following was obtained offthe Internet and claims to beactual statements made duringcourt cases.

Judge: ‘I know you, don’t I?’Defendant: ‘Uh, yes’.

Judge: ‘All right, how do I knowyou?’Defendant: ‘Judge, do I have to tellyou?’Judge: ‘Of course. You might beobstructing justice not to tell me’.Defendant: ‘Okay. I was your bookie’.

From a defendant representing himself:Defendant: ‘Did you get a goodlook at me when I stole your purse?’Victim: ‘Yes. I saw you clearly. Youare the one who stole my purse’.Defendant: ’I should have shot youwhile I had the chance’.

Judge: ‘The charge here is theft offrozen chickens. Are you the defen-dant?’Defendant: ‘No, sir, I’m the guy whostole the chickens’.

Lawyer: ‘How do you feel aboutdefense attorneys?’Juror: ‘I think they should all bedrowned at birth’.Lawyer: ‘Well, then, I think youare obviously biased for the prose-

cution’.Juror: ‘That’s not true. I think prose-cutors should be drowned at birthtoo’.

Judge: ‘Is there any reason youcould not serve as a juror in thiscase?’Juror: ‘I don’t want to be away frommy job that long’.Judge: ‘Can’t they do without you atwork?’Juror: ‘Yes, but I don’t want them toknow it’.

Defendant: ‘Judge, I want you toappoint me another lawyer’.Judge: ‘Why?’Defendant: ‘Because the PublicDefender isn’t interested in mycase’.Judge (to Public Defender): ‘Do youhave any comment on the defen-dant’s motion?’Public Defender: ‘I’m sorry, YourHonor, I wasn’t listening’.

Judge: ‘Please identify yourself forthe record’.

Defendant: ‘Colonel EbenezerJackson’.Judge: ‘What does the “Colonel”stand for?’Defendant: ‘Well, it’s kinda like the“Honorable” in front of your name.Not a damn thing’.

Judge: ‘You are charged with habit-ual drunkenness. Have you anythingto say in your defense?’Defendant: ‘Habitual thirstiness?’

Defendant (after being sentencedto 90 days in jail): ‘Can I address thecourt?’Judge: ‘Of course’.Defendant: ‘If I called you a son of abitch, what would you do?’Judge: ‘I’d hold you in contemptand assess an additional five days injail’.Defendant: ‘What if I thought youwere a son of a bitch?’Judge: ‘I can’t do anything aboutthat. There’s no law against think-ing’.Defendant: ‘In that case, I thinkyou’re a son of a bitch’.

Dumb and dumber

Patrick J Farrell wins the bottle of champagne this month

From: TM Treston, Brisbane,Australia

My wife and I are giving con-sideration to spending a

period of ten to 12 weeks inIreland. The period we have inmind would be the months July toNovember inclusive. We wouldnot wish to stay in a large city. Thethought has occurred to us thatthere may be Irish practitionerswho would welcome the opportu-nity to spend an extended holidayin Australia. If so, a houseexchange proposal might appeal tothem. Anyone interested in such a

Low standards in highplaces

Anyone for a houseexchange?

suggestion can contact me at thefollowing address: TM Treston,Quinlan Miller & Treston,Solicitors, Commonwealth BankBuilding, 240 Queen Street,Brisbane 4000, Australia (tel: +073229 4366, fax: +07 3221 0015).

Your viewsYour letters make your magazine and may influenceyour Society. Send your let-ters to the Editor, LawSociety Gazette, BlackhallPlace, Dublin 7, or you canfax us on 01 671 0704.

Talk to your nearest Ulster Bank about thespecial LOW COST FINANCE offer forLawLink and SecureMail installation costs

FOR FURTHER INFORMATION CONTACT LAWLINK AT: 19 Fitzwilliam Square, Dublin 2. Tel: 01-6766222, Fax 6615398. SecureMail: [email protected]. 11 Emmet Place, Cork. Tel: 021-271044, Fax: 021-272088. SecureMail: [email protected] Fitzroy Sq., London WIP5AH. Tel: 0171-3801500, Fax: 0171-3801550. SecureMail:[email protected].

Lawlink is a joint venture between the Law Society of Irelandand IFG Group Plc. The range of services provided are:

LawLink IrelandProvides direct on line access to the Companies Office, the Companies FormationsInternational (an alternative company information database), the Land Registry, theLegal Diary, Judgements (Company and Personal) InfoLink* – News (national andinternational), News Wires, Stock Exchange information, Foreign exchange infor-mation, Reports on markets, countries, industries, companies

LawLink UK*Provides direct on line access to UK Companies House, UK Land Registry, UKPatent Office, Laserform (electronic forms updating), CompanyLink in conjunctionwith RM and the Companies House, Court Listing and Infolink (see above)

SecureMailThe industry standard for the legal profession. LawLink provides a private andsecure electronic messaging service for both Ireland and England

Training*LawLink now has state of the art training centres in Dublin, Cork and Limerickoffering a variety of technology courses

Hardware and SoftwareLawLink supplies its customers comprehensive hardware and software. Novell, NT,Microsoft Office, Lotus, Accr, Hewlett Packard, Compaq, Epson and many more

Web Development*A growing medium for the Legal Profession. LawLink will consult on and designsolutions for our clients. Watch out for a new service being launched next month

*New services

LAWLINK

APRIL 1998 LAW SOCIETY GAZETTE 9

NEWSNEWS

Lawyers have a key role to playin growing Ireland’s lucrative

international financial servicessector, according to MichaelBuckley, Managing Director ofAIB Capital Markets. Speaking atthe latest Law Society NewHorizons business breakfast inDublin’s RDS, he said the indus-try had grown by 15% last yearand is set to double in size overthe next five years.

‘The legal profession has avery important role to play inassisting the Irish authorities withdefining suggested regulatoryreform as well as in proposingnew legislation which willincrease Ireland’s competitive-ness’, he said.

He also pointed out that manysolicitors are directly involvedand employed in the InternationalFinancial Services Centre (IFSC),as well as the industry generally.His own firm employs at least 20practitioners in non-traditionalwork such as securities, treasury,funds and custodial services.

In his talk, The IFSC – whereto from here?, Buckley warned

Lawyers ‘key to IFSC growth’ BRIEFLYSoftware changes hands IVUTEC, the Irish-based profes-

sional practice management

software developer, has taken

over the Italax program from

Orchard Software Ltd. Italax

claims to be the most commonly-

used software in Irish solicitors’

firms. The company’s managing

director Dermot Mooney has

pledged to develop the program

while keeping it easy to use.

EU legal programme The Council of the Bars and Law

Societies of the EU will launch

The programme of legal and

judicial co-operation on 15 June

next. The project is designed to

respond to the EU’s need to

train legal practitioners in the

legal and judicial co-operation

in Europe. For further informa-

tion, contact Cristina Coteanu-

Bompard, Council of the Bars

and Law Societies of the

European Community, Rue

Washington 40, B-1050 Brux-

elles (tel: 0032 2 640 4274).

Banking seminars in MayCardiff-based consultants Lawyers’

Planning Services are holding two

half-day seminars in Blackhall Place,

Dublin, on 21 May. The seminars,

Your real bottom-line and How to

improve your banking cost stg£175

but anyone booking both seminars

gets an automatic 10% discount

(tel: 0044 222 398161).

Volunteers needed to manenterprise standThe Law Society has taken a stand at

the Enterprise Experience ‘98 exhibi-

tion which runs from Friday 24 April

to Sunday 26 April in the National

Exhibition Centre at Cloghran, near

Dublin Airport. The stand is the ini-

tiative of the Image of the Profession

Committee which feels that the

Society should be more proactive in

publicising the services the profes-

sion can supply to entrepreneurs.

Volunteers are urgently required to

man the stand for shifts of about

two hours. Anyone interested in

helping out should contact Andrea

MacDermott or Catherine Kearney

on 01 671 0711.

that new incentives and productswould have to be offered topotential IFSC companies beforethe marketing deadline expires inDecember 2000. He argued thatafter this date, few companieswill want to set up in the IFSCuntil corporation tax is slashed to12.5%. ‘This will create a market-ing void unless we rethink whatthe IFSC has to offer and putsome new products and incentives

on the table’, he said.He called for the laws relating

to the funds industry to bereviewed and reformed to ensurethat this country stays an attrac-tive location in which to set upand administer funds.

The New Horizons programmeis organised by the Law Society’sCareer Development Committeeand sponsored by accountantsPrice Waterhouse.

The Law Society is due to pub-lish a guide to the ISO quality

management system shortly. ISO9000 and legal practices, pro-duced by the Society’s PracticeManagement Committee, will beavailable for distribution over thecoming weeks.

The guide gives an overviewof the international quality stan-dard and what members will needto do to get accreditation. Itdescribes the benefits of ISO,which include:● More effective staff training● Better communication

through a standardised prac-tice system for practice man-agement

● Better public relations● More satisfied clients● Lower costs through lower

insurance premiums andgreater efficiency in accredit-ed firms.

Members should note that thestandard does not purport to offersuperior legal advice; rather, itmakes it clear to customers that afirm’s management is organised

Society to publish ISO guideand consistent. Further informa-tion about the guide is availablefrom Liz O’Brien, MemberServices Executive (tel: 01 6710711).

Internet provider LawLink is

expanding into the Britain. The

company, which provides a

secure e-mail service for solicitors

in this country, launched its UK

service at the recent solicitors’

technology exhibition in

Birmingham’s NEC.

LawLink is 30% owned by the

Law Society of Ireland, which has

endorsed its SecureMail e-mail

service as the industry standard

for Irish lawyers. According to

LawLink director Stewart

Thompson, the company is now

discussing the possibility of hav-

ing its services endorsed as the

industry standard in Britain with

the Law Society of England and

Wales, and the Law Society of

Scotland.

An estimated 350 Irish firms

are currently using the service,

with approximately 40 joining

each month. It is also being used

by the Department of Health, and

several banks and building soci-

eties.

LawLink connects to UK

Law Society President Laurence K Shields (centre) with Price WaterhouseManaging Partner Donal O’Connor and guest speaker Michael Buckley at

the New Horizons business breakfast

LAW SOCIETYCREDIT CARD

DESIGNED EXCLUSIVELY FOR SOLICITORS

THE CREDIT CARD YOU’VEBEEN WAITING FOR…

Please send me full details and a Priority Request Form for the Law Society Credit Card

Name

Address

Home Telephone Number

Please note, NO STAMP REQUIRED. Send this coupon to: Law Society of Ireland Visa Card, Priority Applications, MBNA Ireland, FREEPOST, PO Box 5898, Dublin 2. (Ref: 08GH).

For further details and a Priority Request form call FREEPHONE quoting ref: 08GG

1800 409 511

Law Society Member Services announcesthe launch of the Law Society’s CreditCard. Now you can take full advantageof a comprehensive range of benefits

MORE FREEDOM...● Credit limit up to £15,000 for

Standard Cards and £25,000 forGold Cards

● Free Credit Card Cheque Book

MORE PRIVILEGES...● Up to £100,000 free Travel Accident

Insurance● Free Purchase Protection Insurance● 24 Hour Freephone Customer Service

from anywhere in the world● Free lost card registration● No liability for lost or stolen cards

MORE FOR YOUR MONEY...● No annual fee● Low APR for purchases – only

19.9% APR (variable)● 9.9% APR for balance transfers fixed

for six months

MORE REASONS TOSAY YES...Use your Law Society Credit Card topay for Law Society services such asCLE courses, consultation room hire, publications etc .… indeed any serviceavailable through Member Services andyour name will be entered into a freeprize draw at the end of the year.

The Law Society of Ireland Visa Card is issued by MBNA International Bank Limited, incorporated in England and Wales under number 2783251. Registered office: StansfieldHouse, Chester Business Park, Wrexham Road, Chester CH4 9QQ. Registered as a branch in Ireland under number E3873 as 23 St. Stephen’s Green, Dublin 2. Credit is avail-able subject to status, only to ROI residents aged 18 or over. Written quotations available on request.

APRIL 1998 LAW SOCIETY GAZETTE 11

NEWSNEWS

BRIEFLY

Would you credit it?In the month since the Law

Society launched its credit card,

476 members applied for the

Visa card and most of these

have already been approved.

Several have been issued and

the holders are using them. The

card offers a credit limit of up

to £15,000 standard and

£25,000 gold. There is free pur-

chase protection insurance, no

liability for lost or stolen cards,

no annual fee, and 19.9%

annual percentage rate (vari-

able). Anyone using the card

for anything available from

Members’ Services will have

their name entered in a free

prize draw at the end of the

year.

Family lawyers to uniteThe fifth Family Lawyers’

Association annual conference

and AGM will be held in the

Great Southern Hotel, Rosslare,

Wexford, from 15 to 17 May

1998. The conference will focus

on two issues: the Children Act,

1997, and non-marital co-habi-

tation and the law. For further

information, contact Mark

Graham, Ormond Quay Law

Centre, Dublin 1 (tel: 01

8724133), Jennifer Curry (tel: 01

829 0000) or Sora O’Doherty,

Law Library (tel: 01 7023989).

Copyright crooks face five-year jail termsBreaches of copyright law will earn

prison sentences of up to five years

for offenders under a new law set

to be enacted by next July. Trade

and Consumer Affairs Minister Tom

Kitt revealed recently that the

Government has approved tough

new penalties for criminals who

flout intellectual property rights.

The newly-drafted Copyright

(Amendment) Bill, 1998 proposes to

jail offenders for up to five years, or

fine them to a maximum of

£100,000, or both. Kitt vowed that

the Bill would be passed no later

than July of this year.

(See also Get with the program,

p20)

Apprentices are due a pay increase

following the Law Society

Council’s approval of a revised rec-

ommended salary scale. The new

recommended rates are: £135

gross a week for the first six

months after completing the pro-

fessional course, £145 gross a

week for the second six months,

and £155 gross a week for the

remaining period. While there is

no strict obligation on a master to

pay an apprentice before the

apprentice attends a professional

course, the Council recommends

that the apprentice be paid £105

gross a week. These rates came

into force from 1 March.

Pay boost for apprentices

Law Society Director GeneralKen Murphy has hit out at alle-

gations that solicitors will refuse tosue their fellow professionals. Theclaim, made during a recent casein Galway District Court, wasdenied this month by Murphy, whorejected suggestions that membersoperate a protective practiceamong themselves.

‘There are always solicitorsavailable to sue other solicitors inmeritorious cases’, he said. ‘Anymember of the public whobelieves their solicitor has beennegligent or who believes theyhave a good case to bring againsta solicitor for any reason can con-tact the Law Society, which main-tains a panel of solicitors who areprepared to act in such cases’.

‘The names of solicitors in thelocality who are prepared to act insuch cases will be supplied.Whenever a good cause of actionlies against a solicitor, another

solicitor will always be found, withthe assistance of the Law Society ifnecessary, to institute proceedingsand bring the case to court’, he said.

The ‘protective practice’ claimwas made during a hearing inGalway District Court in whichAthenry private investigator AlfredDoherty was attempting to recover£1,420 in fees from local firm, VPShields and Son. Doherty com-plained to the court that he hadbeen told by his solicitor that it was‘doubtful’ if any law firm wouldtake a case against another. He wasforced to represent himself.

Judge Albert O’Dea said it was‘outrageous’ that any solicitor wouldmake such a statement, and con-demned lawyers for operating whathe claimed was a protective practice.

Solicitors’ protective practice denied

Conveyancing solicitors actingfor the vendors of a property

now owe a duty of care to the pur-chaser following the recent prece-dent-setting Doran judgment,where a couple who bought a£25,000 site in Wicklow won theright to sue the vendor’s solicitorsafter an eight-year court battle.

New duty of care on conveyancersIn the Supreme Court, Mr

Justice Keane ruled that Terenceand Maureen Doran were oweda duty of care by Bray solicitorsJoseph Maguire and Co, the firmthat acted for the sellers in thedeal. Mr Justice Keane said thatwhere a vendor’s solicitors wereaware that a neighbour had

already made claims over theland, and that there was a threatof litigation, they at leastassumed some responsibility forthe information about theseclaims.

A fuller examination of thislandmark case will appear in nextmonth’s Gazette.

Law Society Director GeneralKen Murphy and Minister for

Defence Michael Smith have bothwelcomed the Government deci-sion to proceed with the drafting oflegislation to amend the law onsolicitor advertising.

‘The proposal to amend the lawrepresents a pragmatic compro-mise. While some advertising willremain, it will have to conform to aspecific format’, the Minister said.

In January, the Law SocietyCouncil unanimously agreed tosupport legislation to ban solicitoradvertising for personal injurywork.

‘The Society believes that thisadvertising has greatly diminished

Society and Smith welcome ad curbsthe public esteem in which the pro-fession is held’, said Murphy.‘Maybe we will hear the ambulance-chaser jibe less frequently in future’.

He confirmed that the Society

had held a number of meetingswith the Department of Justice onthe draft legislation. ‘However, itis very much the Government’sBill, not the Society’s’, he said.

Ken Murphy: ‘there are alwayssolicitors available to sue other

solicitors’

12 LAW SOCIETY GAZETTE APRIL 1998

Betting on the stock market seems like the ultimate gamble.Prices fluctuate every day, leaving some investors countingtheir winnings and others counting the cost of an expensiveflutter. Worse still, a ‘Black Monday’ style crash can wipemillions off the value of shares, leaving companies and their

stakeholders reeling.On the face of it, many other investment options seem safer than going

into this financial answer to Cheltenham, but is that actually the case? Infact, it’s not. The stock market offers the best chance of getting a goodreturn for any investor willing to look at the long to medium term.

In Britain, City guru and group economic adviser to Barclays, MichaelHughes, produces a yearly study comparing share performance with thatof Government bonds – traditionally the safest bet for an investor. His lat-est findings show that the chances of stocks outperforming these safe betsare as high as 96%.

Risk for returnsTaking any period of ten years since 1918, he says that gilts have beatenshares only three times, and cash investments have only given a betterreturn than the stock market on two occasions. So it seems there is nocontest if you are prepared to stick it out for the long term.

The story in this country is much the same. According to MarkDonnelly of Goodbody Stockbrokers’ private clients’ service, dependingon the circumstances, shares can be an attractive alternative. ‘Over thelonger term they have consistently outperformed other investments likecash and property’, he says.

Shares are the riskiest type of investment and to take such a risk youhave to get a high return. Obviously some stocks will collapse and otherswill rocket ahead. But in the long term, they still offer a high return.

Last year, shares on the Irish Stock Market increased in value by 50%.In other words, every £1 invested at the beginning of 1997 was worth£1.50 by the beginning of this year. Davy Stockbrokers’ Guide to theIrish equity market shows that the market’s value has more than tripledover the last five years, earning investors an average annual return of 30%over the same period.

Comparing last year’s market performance with what you would havereceived on deposit, which would only be around 5% to 6% at the most,it is clear that shares can be very worthwhile.

The Irish Stock Market has broken all previous records over the last five years.

But is it a safe bet for the privateinvestor or just the financial world’s

answer to Las Vegas? Barry O’Hallorandons his red braces and finds out

GamGam

market

APRIL 1998 LAW SOCIETY GAZETTE 13

COVER STORY

At this stage, opinion is divided on whether the market can keepsteaming ahead in this fashion. Some are predicting that the ISEQ indexof Irish shares will break new records this year, while others say thatprices are already over-stretched and that the only way the index can gois down. But market analysts are a bit like astrologers – no two of themwill come up with the same predictions.

Dealers say that the value of some stocks is stretched at the moment,so there could be some volatility in the short term, but they stress thatthere are plenty of stocks that still offer good value. Also, there may bea number of them that do not look attractive just at the moment, but maybe attractive in the long term.

So the real secret of success on the markets is not to go in hoping tomake a quick killing, but to invest for the medium or long term. Yourinvestment will go through highs and lows, but if you hang in there itshould ultimately reward you for your patience.

The dominant investors on the Irish market are the big financial insti-tutions, pension funds and life companies. But dealers say there is plen-ty of anecdotal evidence to indicate that more and more private individ-uals are now putting their spare cash on publicly-quoted companies.

At least one reason for this is the poor return offered by cash deposits.Low interest rates may be good news for borrowers, but they are bad forsavers, some of whom are earning only small amounts on the money theyhave left on deposit with the banks. ‘Because we have low inflation andlow interest rates, we are seeing more and more people moving their cashinto equities’, says Goodbody’s Mark Donnelly.

Getting in the doorSo if you are thinking of joining this rush to the trading floor, how do youget in the door? Most stockbrokers have a private clients’ service whichspecialises in dealing with individual investors. They will advise you onwhere to put your money and will act as your dealer, which means theywill buy and sell shares on your behalf.

You can allow the broker full discretion to make all the investmentdecisions. In this situation, they have to follow rigorous guidelines relat-ing to income, risk, tax and other issues as set down by the client. Thebrokers also have to notify any change to the investor.

The other option is an advice service. Here, the brokers act as advis-ers, taking into account the same requirements mentioned above. In this

mblingmarketstock

on thembling

stock

Advance Booking FormFee: £55 per person, £550 per table of 10 or £35 per solicitor qualified less less than three years. (There are only 100 reduced-pricetickets availabe and they will be issued on a first-come basis)

Please reserve place(s) @ £ or table(s) for the Law Society Celebration Ball onFriday, 17 July 1998, at Blackhall Place.

Name Firm

Address

DX Tel Fax

Cheque enclosed: £ £55 per person, £550 per table of 10 or £35 <3yrs qualified.

Or debit the following credit cardName of cardholder:

Card No: Expiry Date:

Return to: Elizabeth O’Brien, The Law Society, Blackhall place, Dublin 7. Telephone (01) 671 0711, Fax (01) 671 0704.

LAW SOCIETY

Celebration BallTHIS YEAR THE SOCIETY CELEBRATES

20 years AT BLACKHALL PLACE.

TO MARK THE OCCASION A CELEBRATION

BALL WILL BE HELD IN A MAGNIFICENT

MARQUEE ON THE GROUNDS ON FRIDAY,

17 JULY 1998.

PRE-DINNER RECEPTION

SUMPTUOUS BANQUET

DANCING TO PADDY COLE AND THE ALLSTARS

AND FOR THE NIGHT OWLS - 2FM DJ BOB CONWAY ‘TILL LATE

DRESS – BLACK TIE

Enjoy a wonderful evening with friends,

clients or colleagues

case, the final decision is up to you, andonce your mind is made up the brokers acton your instructions.

In both situations, the brokers shouldprovide you with regular valuations ofyour investment. It’s also worth notingthat if you do not want your name on theshareholders’ register, which is a publicdocument, stockbrokers will provide anominee to hold the stake for your benefit.

On the other hand, if the deal is a one-off – for example, if you are sellingNorwich Union shares granted to you lastyear before the company’s flotation – thenyou can opt for a straightforward execu-tion service. Here, the intermediary has noinvolvement beyond simply buying orselling shares on your instructions and tak-ing a commission.

Dealers recommend that to get the bestvalue you should have at least £10,000 toinvest. The advantage of having a comparatively large sum like this toplay with is that it gives the broker the chance to spread the cash througha number of stocks in a bid to minimise risk and maximise earnings.However, not all private individuals have this kind of money, and it is notthat unusual for people to invest much smaller amounts.

Different dealsObviously, brokers are not philanthropists, and all charge commissionsfor their services. These may vary according to the amount of moneyyou are investing and the level of business you do with the company.For example, charges could range from 1.65% on the first £10,000, 1%up to £20,000 and 0.5% after that. But this should not be taken as a hardand fast rule.

Brokers will offer different deals depending on the kind of service youare looking for and the amount of money you are investing, so it makessense to shop around. Also, you should ensure that any investment inter-mediaries you deal with are properly accredited.

The market itself is divided into a number of sectors, basically:● Industrials, which includes companies like Smurfit and CRH● Financials, made up of the banks and insurance companies such as

Irish Life● Food, mainly the large co-ops which have been floated over the last 15

years, for example, Kerry and Golden Vale, and ● Exploration, which includes a range of Irish companies involved in

mining and exploration either at home or abroad.

Not all of the listed companies fit precisely into these sectors, whichthemselves are only broad categories whose overall performance may notreflect how particular stocks are doing. The official gauge for measuringequity performance is the ISEQ index, which is compiled by the IrishStock Exchange. It includes all shares listed on the official market andthe Developing Companies Market (DCM). Most of these are registeredin Ireland, but it also includes nine Northern Irish companies with a list-ing in Dublin.

The index is based on the quoted companies’ market capitalisation,which varies according to their share price. A company’s market capital-isation is the total value of all the shares if they were cashed in at thesame time. The ISEQ is updated regularly, one of the latest stocks to beincluded was British-based Norwich Union, the mutual which floatedlast June, delivering a windfall to thousands of Irish savers.

When it actually comes to putting your money somewhere, there area number of things that advisers take into account. Because the success

of your investment depends purely onhow the stock performs, which in turndepends directly on how profitable thecompany is likely to be, then you look atyour chosen investment’s prospects forthe future.

This may be easy to work out. Forexample, any company in the constructionindustry is doing well out of the buildingboom and is probably a good bet for thecoming year at least. But it is not so easywhen you consider that most of the com-panies quoted in Dublin have large inter-ests in other countries and in parts of theworld where the economy is either morevolatile than here, or is just not performingas well.

Market analysts say that any businessactive in this economy has good prospects,but that should not be the only factor thatinfluences the choice of investment. ‘We

would say that companies with a lot of exposure in the Irish economy areobviously good value at the moment’, one says. ‘But that’s not all youshould look at. We also look at how well-managed a company is and atits strategy for future growth. At the moment, most Irish shares representgood value. Companies like Kerry, CRH, and Waterford/Wedgwoodremain attractive’, he adds.

Davy Stockbroker’s forecast for this year predicts that the smallerstocks are likely to out-perform all others on the market over the next 12months, leaving even giants like AIB and Smurfit in the shade. The firmis backing companies like Arnotts, Jury’s, Ryanair and United Drug tomake big gains in 1998.

Of the larger companies, Davy says that Smurfit, Waterford,Clondalkin, Fyffes and Lamont should do well, while the brokers say thatin the financial sector insurance companies offer a cheap alternative tothe banks, whose strong performances have pushed up their prices.

The DCM may also offer good opportunities. This is an alternativemarket designed for smaller, newly or recently-floated companies whichdo not qualify for a full listing. The volumes, or amount, of shares trad-ed by each DCM company tend to be smaller and prices may also becheaper.

It can offer good prospects to private investors. One of the DCM’srecent success stories was recruitment specialist Marlborough plc whichwas floated last October and subsequently applied for a full listing aftertaking over a British firm, Walker Hamill. Its share price almost doubledduring that period and the company earned a very good return for itsinvestors.

Taxing thoughtsAny income you make from an investment is subject to tax. Dividendspaid to you on your shares by the company qualify for income tax, whileprofits from selling shares qualify for capital gains tax (CGT). But youcan cut your liability by putting your money in a special portfolio invest-ment account. This is a scheme designed to encourage private investorsto invest in Irish stocks by offering them tax breaks.

A single person is allowed to place up to £75,000 in a special portfo-lio, while married people are limited to £150,000. Both income and cap-ital gains are taxed at 10%. Thus, if someone places £10,000, and thevalue of their holding increases by £1,000, they pay £100 CGT, or if theyreceive £2,000 in dividend income, they pay £200 in income tax.

So it does seem that using your spare cash to stock up on shares is agood idea. In any case, you have to admit that playing the market is like-ly to be far more exciting than putting your money in the post office. G

APRIL 1998 LAW SOCIETY GAZETTE 15

COVER STORYCOVER STORY

The Stock Market: the ultimate gamble?

16 LAW SOCIETY GAZETTE APRIL 1998

Ten years ago 167 people died inthe tragedy on the Piper Alpha oilrig. In 1987, 31 people were killedin the King’s Cross fire, while 35people perished in the Clapham

rail crash of 1988. The sinking of the Herald ofFree Enterprise in 1987 resulted in 188 deathswhile the sinking of the Marchioness two yearslater saw 51 people lose their lives.

Remarkably, in each instance, no successfulprosecution for manslaughter against the com-pany or the individuals who make up the com-pany was able to be mounted in the UnitedKingdom. Why is that so? It took a furthertragedy last year – the Southall rail crash inwhich seven people died and 160 were injured– for the British Government to act. Moveshave now been made which, in future, shouldmake it easier to prosecute UK firms formanslaughter and potentially to bring to justicethose responsible for the deaths.

The British Home Secretary, Jack Straw,supported by Deputy Prime Minister, JohnPrescott, is pressing for the introduction of anew offence of ‘corporate killing’. Companydirectors could also be prosecuted and be liablefor unlimited fines and imprisonment if theyare found to have failed to ensure the healthand safety of those affected by their activities.

Controlling mindThe present UK law demands that, in prosecut-ing a corporation for manslaughter, it is neces-sary to identify a ‘controlling mind’ and, assuch, it has been notoriously difficult to pinpointone person who caused the death or deaths.

The failure of the law to avenge those killedby management failures has been criticised forsome time. There has been a great deal of spec-ulation about the criminal law’s ability to protectemployees and the public from the activities ofcorporations and to punish corporate offenders.Recommendations for the creation of an offenceof ‘killing by gross carelessness’ to replace thepresent offence of corporate manslaughter weremade by the Law Commission in March 1996after many years of discussion and debate.

In the eyes of the greatBritish public those

responsible for five majordisasters which left 473people dead and many

others injured have neverbeen brought to justice.

But recent proposals fromthe UK’s Law Commissionto create a new offence of

‘corporate killing’ couldsoon change all that, asPaul Burnley and Kirsty

Gomersal explain

corporatekillin

The

killin

APRIL 1998 LAW SOCIETY GAZETTE 17

CRIMINALCRIMINAL

The reason for the law’s failure is that thecurrent offence has developed case by case overthe centuries and is still tainted by preconcep-tions which existed in the 17th century. It wasnot until the early part of this century that theprocedural rule that a defendant had to appear inthe dock to answer a charge was defeated bylegislation which stated that corporations couldappear in court and plead through a representa-tive. Until that time, the fact that a corporationcould not physically appear in court excludedthem from criminal jurisdiction.

‘Who is to blame?’It was also thought that a company could notbe guilty of a crime as it had no body or mindand therefore could not have a guilty intent. Itis only recently that the law has been furtherrefined so that a company can be found crimi-nally responsible for the acts of those repre-senting the directing mind and will of the com-pany and who effectively controlled what thecompany did. This has still not satisfied thepress or the public. ‘Who is to blame’ stillechoes down the corridors of coroner’sinquests and public hearings into a tragedy.

The present corporate offence is that of‘involuntary manslaughter’. It is not possibleto prosecute a company for voluntarymanslaughter or murder as the penalty isimprisonment and a company cannot be sent tojail. Involuntary manslaughter covers caseswhere there was no intention to kill or causeserious injury, but the law considers that theperson causing death was in some other way toblame. A conviction for manslaughter is possi-ble as it is punishable by a fine. It is necessaryto prove that the decisions made by the direct-ing mind of the company (or the failure tomake decisions) caused the fatality.

So far in the UK only a handful of caseshave been brought to trial for corporatemanslaughter. In May 1992, P&O Ferries wastried for manslaughter following the sinking ofthe Herald of Free Enterprise off Zeebrugge in1987. Mr Justice Sheen, who conducted a fullinvestigation into the disaster and its causes,

concluded that the fault lay with the directorswhom he described as a ‘vacuum at the centreof the company’. The company was describedas being infected ‘with the disease of sloppi-ness’ from top to bottom. At the coroner’sinquest, despite the direction from the coroner,the jury returned a verdict of unlawful killing.

The subsequent trial of the company andseveral individuals was stopped by the judgeeven before the prosecution had closed its case.The Crown failed to prove the key element:that directors and senior managers (the peoplerepresenting the controlling mind of the com-pany) had formed the necessary criminal intentor had acted in a grossly negligent way in thatthey ought to have known that there was a seri-ous and obvious risk that the ship would sailwith open bow doors. In essence, for the com-pany to be convicted of manslaughter, the indi-vidual defendants would also have to be guilty.

Despite the damning Sheen Inquiry, it wasalways going to be an uphill struggle to provethe case against P&O. The overwhelming dif-ficulty was identifying the ‘controlling mind’.The more diffuse the corporate structure, themore difficult this can be to define. However,the decision by the British Director of PublicProsecutions to prosecute the company washailed as a major step towards corporateaccountability and gave the courts the opportu-nity to confirm that, where the evidential bur-den was discharged, the offence of manslaugh-ter could be established against a company.

First successful prosecutionThe first successful prosecution for corporatemanslaughter occurred in December 1994.After four young people drowned in the LymeBay canoeing tragedy, the company responsi-ble for their fatal trip (OLL Limited) was con-victed of corporate manslaughter and fined£60,000. In this instance, it was possible toidentify a ‘controlling mind’. The company’smanaging director, Peter Kite, was also foundguilty of the children’s manslaughter and jailedfor three years. He was said to be grossly neg-ligent in ignoring the warnings of former

ing fieldsing

APRIL 1998 LAW SOCIETY GAZETTE 19

CRIMINALCRIMINAL

employees who left because of concerns aboutsafety at the centre; he was also said to have pro-vided inadequate training and to have employedinsufficiently qualified people.

A further successful prosecution was securedin September 1996 when Jackson Transport(Ossett) Limited and its former managing direc-tor were found guilty in Bradford Crown Courtfollowing the death of an employee who hadbeen cleaning chemical residues from a tanker.Alan Jackson was sentenced to one year’simprisonment.

Both Jackson and the company were alsofound guilty of two offences under the Healthand Safety at Work Act 1974 (HSWA) for failureto secure the safety of employees. The Act con-tains similar provisions for failing to ensure thesafety of third parties, for example, customers.Such a conviction carries an unlimited fine fol-lowing conviction in the Crown Court and apotential two-year jail sentence for a directorfound guilty of the offence. It is also possible fora director convicted in the Crown Court to be dis-qualified from acting as a director for up to fiveyears. This represents a potential ‘double wham-my’ for companies and a ‘triple whammy’ fordirectors. It remains to be seen whether compa-nies will be prosecuted under both the HSWA andany new offence, but it is likely that the impetusfor a prosecution for corporate manslaughter willbe used where prosecution under the HSWAseems inappropriate or inadequate.

The Law Commission’s proposed newoffence of ‘corporate killing’ is defined askilling by gross carelessness or where the con-duct falls well below what could reasonably beexpected. A company would be liable underthis offence if a management failure resulted indeath and that failure constituted conductwhich failed to ensure the health and safety ofthose affected by the company’s conduct. Theconvicted company would be liable to anunlimited fine and to remedy the fault whichled to be accident.

Genuine corporate liabilityThe conviction of companies responsible fordeaths should be easier under the proposednew offence. A successful conviction will nolonger depend on the identification of the‘directing mind’; rather, the question will bewhether the corporation was grossly careless inthat it should have been aware that there was arisk of death or serious injury and, secondly,that its conduct fell well below what could rea-sonably be demanded in dealing with the risk.There should now be genuine corporate liabili-ty as opposed to individual liability. What is‘reasonable’ will depend on the individual cir-cumstances of each case and will be a matterfor a jury, but it will include factors such as thecost and practicality of taking steps to reduceor eliminate the prevalent risk.

If the proposals are implemented, it will be

the conduct of the company which is ques-tioned as opposed to the status and identifica-tion of those responsible for it.

So what about prosecuting individual direc-tors for manslaughter? The Law Commissionmakes no suggestions about this, but it is like-ly, given the present mood of the British courts,that such prosecutions will continue alongsidecorporate prosecutions. However, while thechange in the law with regard to the corporateoffence may result in more successful prosecu-tions, it is unlikely that the situation willchange with regard to those ultimately respon-sible for any death. How far that will satisfypublic anger remains to be seen.

In a large diffuse company, such as P&O, itcan be difficult to identify those ultimately atfault. It is undoubtedly easier for a director of asmall company to be prosecuted because themanagement structure is simpler and he ismore easily identifiable. So while companiesface the stigma of being branded corporatekillers, senior executives of large companiesare unlikely to be pursued. Strange as it mayseem, it is the directors of smaller businesseswho are more likely to face a custodial sen-tence than the directors of large companieswho may be just as liable – if not more so.

Paul Burnley is a partner and Kirsty Gomersalis a solicitor in the Leeds office of the UK lawfirm Eversheds.

G

Solve your storage problems with a new-style Gazettemagazine binder. Each easy-to-use binder takes a year’sworth of issues and is finished in blue leatherette with theGazette logo in gold on the front and spine.

EACH BINDER COSTS £7.95 PLUS £1.20 POST AND PACKAGE (FOR ORDERS OFBETWEEN FIVE AND TEN BINDERS, A SPECIAL ALL-IN POSTAGE RATE OF £5.50APPLIES)

Keep your magazines safe with a newGazette binder

To order your magazine binder, please fill in the form below.

Please send me magazine binders at £7.95 plus £1.20 p&p(special p&p rate of £5.50 for orders of between five and ten binders)

I enclose my cheque for £

Please charge my Access Visa Mastercard Eurocard

Credit card number

Expiry date:

Name:

Address:

Telephone:

Signature:

Please return to Law Society Gazette, Blackhall Place, Dublin 7.

MONTH/YEAR

Technology’s rapid surge ahead has left our

copyright laws trailingbehind the times. Denis

Kelleher outlines theexisting protections for

computer programauthors and argues the

case for reform

20 LAW SOCIETY GAZETTE APRIL 1998

Computer programs are valuablecommodities which cost millionsof pounds to create but just a fewpence to copy. The great demandfor new programs and the high

rewards for their creators make this a veryfinancially rewarding industry for anyoneinvolved. But if a computer program is success-ful, then many people will try to copy it. Theymay reproduce the whole program and sell itwithout giving the author any royalties, or theymay copy parts of it to improve their own com-peting programs.

In Ireland, computer programs are protectedby copyright law in the same way as literaryworks such as books. This is a very strong pro-tection but the law is convoluted. Computer pro-grams derive their basic protection from an EUdirective implemented in Ireland as SI 26/1993,which essentially protects computer programs asliterary works under the Copyright Act, 1963.

This means that anyone wishing to assert hisrights over a computer program, or a part of it,has to refer to three separate laws to establishthose rights. Conflicts and contradictionsinevitably arise between the different provisions,a problem compounded by the fact that the EU iscommitted to comprehensively amending copy-right law.

The anticipated arrival of EU legislation andthe need for Ireland to agree to revisions of theBerne convention and the new World TradeOrganisation (WTO) treaty on copyright maytempt the Irish legislature to wait before reform-ing our law. This ignores the fact that theCopyright Act, 1963 was never written for com-puter programs or the other products now beingcreated for the Internet and other technologies. Itis badly out of date and in need of reform.

Programs written by Irish people are protectedby the Act and programs written by Europeanshave to be protected under Irish and Europeanlaw. But the Copyright (Foreign Countries)Order, implemented in 1996, extends the Act’sprotection to literary works first published, eitherbefore or after the making of the order, in anycountry of the Berne Union, the Universal copy-right convention or the WTO, includingAmerica, where most programs are written.

This was passed because the 1963 Act’sdrafters never thought that marketing andexploiting the works of American authors of anykind would be a multi-million pound industry inIreland over 30 years later and that it would beused to protect that business. In the same way, if

Get with tGet with t

APRIL 1998 LAW SOCIETY GAZETTE 21

TECHNOLOGYTECHNOLOGY

the drafters and legislators of 1963 had evenheard of a computer program they would nothave realised that the Act would in time be usedto protect 1990s’ technology. Using the Act toprotect modern technology is inappropriate andit would have been better to introduce a newCopyright Act in 1993 rather than relying on thesticking plaster of a statutory instrument.

One difficulty caused by the Act is containedin section 27(3). This makes it an offence toknowingly make or hold a plate (defined as‘including a stereotype, stone, block, mould,matrix, transfer, negative or other appliance’). Itis unclear whether or not holding a computerprogram or a part of a computer program forcopying would be an offence.

Trivial penaltiesAt any rate the penalties are trivial when com-pared with the sums which may be made by sell-ing pirated copies. Anyone summarily convict-ed of selling or distributing infringing copiesshall be liable to a fine of £100 per copy on hisfirst offence and in any other case liable to thesame fine or to imprisonment for not more thansix months. But the fine cannot exceed £1,000.

This leniency should be contrasted with thesituation in the United States where theCopyright Felony Act 1992 provides that a per-son who ‘wilfully and for purposes of commer-cial advantage or financial gain reproduces ordistributes within a 180-day period at least tenunauthorised copies ... of one or more copy-righted works with a collective value of morethan $2,500’ will face up to five years in prisonand a fine of $250,000 for a first offence.

But the major challenge for Irish courts is thetask of devising a test for deciding whether ornot a computer program has been copied fromanother. This probably cannot be met by legisla-tion. Copyright disputes may take two basicforms. In the first, a work is pirated or simplycopied with no effort made to disguise it. Thechallenge is not to prove that copying occurred,but to catch the pirate. The second is more com-plex: here, elements of one computer programwill be copied and included in another to com-pete with the original. The alleged copier will beeasy to identify, but proving that they havecopied may be difficult.

The test for deciding whether or not copyingoccurred was laid down by Costello J in Housesof Spring Gardens v Point Blank Ltd (1984) IR611 where he adopted a test developed byWilmer LJ in Francis Day and Hunter Ltd v

Bron: ‘In order to constitute repro-duction within the meaning ofthe Act, there must be (a) asufficient degree of objec-tive similarity between thetwo works and (b) somecausal connectionbetween the plaintiffs’and the defendants’work’.

This test is straightfor-ward in itself and it was eas-ily applied in the case, wherethere was a very large degree ofsimilarity between the bullet-proof vestdesigned by the plaintiff and that which thedefendant claimed to have designed. Thus, it waseasy to establish a causal connection between theproducts.

But deciding whether or not one computer pro-gram is sufficiently similar to another is a difficulttask. Programmers learn from one another’s suc-cesses and failures, and the fact that all programsmust run on standard operating systems mean thatsome elements will have to be identical and the1993 regulations specifically allow for this.

Identical elementsJudges and lawyers may find it difficult to decidewhether certain elements are identical andwhether that similarity stems from copying; orwhether programmers used similar methodolo-gies; or whether the elements’ form was deter-mined by other factors, such as the constraints ofthe computer hardware for which the programwas designed.

Unfortunately, American cases do not offerany easy solution. The so-called ‘abstraction-fil-tration-comparison’ test developed there inComputer Associates International Inc v Altai isdifficult to apply and, arguably, by concentratingon the dissection of a program’s elements missesthe wood for the trees.

A major challenge in a computer copyrightdispute will be the difficulty of explaining thetechnology. The courts will rely particularly onthe evidence of experts, and lawyers and judgeswill have to educate themselves so that this doesnot become dependence. The danger in these dis-putes is that the questions will be decided bywhichever side can best explain the technologyrather than on the merits of the case.

Another potential difficulty is that whilelawyers will inevitably try to clarify technologi-cal terms, there is a danger that they will over-

simplify complex issues.Ultimately, time and experi-

ence will allow the courts todeal with computer pro-

grams with the sameease as other areas suchas company law. Butfor now it is importantto realise that protectingcomputer programs rais-

es new questions of lawthat have yet to be dealt

with satisfactorily in Irelandor other jurisdictions.

In spite of these problems, the deter-mination with which computer program ownersintend to pursue those who pirate or plagiarisetheir works should not be doubted. The manag-ing director of an English computer companywas recently sentenced to a two-and-a-half-yearprison sentence after his company sold 46 pirat-ed copies of Novell software.

Both Microsoft and Novell are targetingthose who illegally copy their software inIreland and have won injunctions against thosewhom they believe have been infringing theircopyright. This jurisdiction provides strongcopyright protection for computer programs andother works, but reforms are needed to ensurethat the law is clearly implemented.

Pressure on the Irish Government to reformIrish copyright law is increasing. The US gov-ernment is concerned, and in December 1997the EU published its Proposal for a EuropeanParliament and Council directive on the har-monisation of certain aspects of copyright andrelated rights in the information society. If andwhen this legislation is passed, it will need tobe implemented here, but this can be done bya regulation.

It is unclear how long this will take, but theOireachtas should not be allowed to use it as anexcuse for failing to legislate and reform existingcopyright law. Ultimately, the EU will legislatefor all aspects of copyright and intellectual prop-erty, but this process might take years – if notdecades – to complete. It is unwise and unrealis-tic to expect that a piece of legislation datingback to 1963 will be adequate to deal with all thechanges in both technology and the law whichwill be encountered in the years to come.

Denis Kelleher is a Dublin-based barrister andco-author of Information technology law inIreland (Butterworths, 1997).

G

the programthe program

22 LAW SOCIETY GAZETTE APRIL 1998

T he New York firm of Cadwalader,Wickersham & Taft is supposed to bethe oldest law firm in the United States.

In 1989, James Beasley was admitted as a part-ner to the firm and proved himself to be ‘anextraordinary rainmaker and a skilled litiga-tor’. Beasley was a partner in the firm’s Floridaoffice, and for a number of years after hisarrival the business was very successful – theprofit-share of each partner increasing year-on-year after 1989. But in 1993, the partners’ prof-it-share declined and the Florida office made aloss for the first time since Beasley’s arrival.

This state of affairs upset the ‘younger, moreproductive partners’ who controlled a lot of thefirm’s business, but felt that they were not get-ting credit for it. They decided to turn theirsights on other partners who didn’t bill or hustleat the same pace as themselves. They did this byputting pressure on the firm’s management com-mittee to do something about the fall-off in prof-it-share. The committee came up with ‘ProjectRight Size’ which was ‘aimed at identifying lessproductive partners for elimination from thepartnership’. The project was designed toimprove the continuing partners’ profit-share bysacking some of the most unproductive partnersand keeping the more productive ones.

The watershed was a clandestine all-daymanagement committee meeting. Before themeeting, co-chair Donald Glascoff asked allmembers to submit lists of less productivepartners for discussion. Only five of the 12members chose to submit such a list – all of theFlorida partners appeared on at least three listsand one appeared on all five.

Soon after this meeting, the managementcommittee decided to close the Florida office.The day after this decision was reached, themanagement committee informed the Floridapartners. When the Florida partners refused theoffer of voluntarily withdrawing from the firm

One recent US partnership case has turned out to be a pot-boiling tale of greed, fear, loathing and fiduciary duties. And, as Michael Twomey points out, the

principles of partnership law highlighted by the case of Beasley v Cadwalader,

Wickersham & Taft could equally apply here

Firing youthe Amer

Florida branch of the firm and offered Beasley atransfer to New York.

The Florida court found that the firm’s offerto move Beasley to New York ‘was not a good-faith offer of continued partnership’ and itsactions in ‘deciding to terminate the Floridapartners and to close the Florida office consti-tuted an anticipatory breach of the partnershipagreement’. The court noted that a majority ofthe partners could have amended the agreementto include a power to expel a partner. But for thesake of expediency, the management committeechose to ‘bend to the will of the disgruntledpartners by expelling others to whom they oweda fiduciary duty’.

Cadwalader also claimed that Beasley hadbeen planning to leave the firm anyway – it tran-spired that he had entered discussions in thisregard with some associates, and did not tell hispartners. Cadwalader alleged that Beasley’s fail-ure to reveal his discussions to leave the firm wasa breach of his fiduciary duty to it and that thisdefeated his claim. The Florida court held that itwould not be equitable to allow Beasley’s discus-sions with his associates about leaving the firm tostand as a defence to Cadwalader’s conduct.Judge Cook added an American refinement to themaxim that he who comes to equity must do sowith clean hands when he stated that ‘if Beasleyhad dirt under his fingernails, Cadwalader was upto its elbows in the dung heap’.

It was also alleged by the management com-mittee’s chairman that the firm’s decision regard-ing the Florida partners was not a breach of fidu-ciary duty since it was in the overall interests ofthe firm. He explained his view of the positionprior to the Florida closure as follows: ‘Therewas a fear, there is a fear, there always will be afear, that highly productive partners can leave, goto another place and get more money. And life isnot made up of love; it is made up of fear andgreed and money – how much you get paid in

Firing youthe Amer