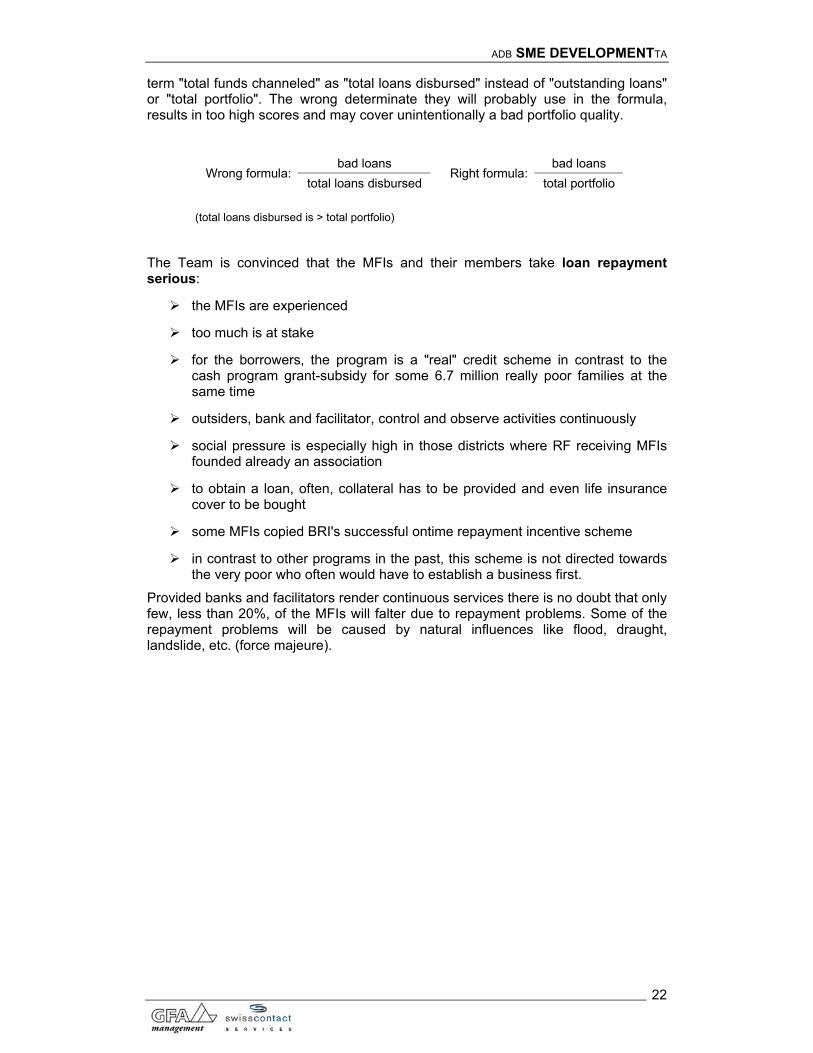

11 evaluation of revolving fund for strenghening micro fin. · kja koperasi jasa audit kpkn kantor...

TRANSCRIPT

ADB SME DEVELOPMENT TA

BACKGROUND REPORT

EVALUATION OF REVOLVING FUND FOR STRENGTHENING MICRO FINANCE INSTITUTIONS

WOLFRAM HIEMANN, ANDI IKHWAN, TIKA NOORJAYA

JULI 2001

Published by: ADB Technical Assistance

SME Development

State Ministry for Cooperatives & SME

Jalan H.R. Rasuna Said Kav.3

Jakarta 12940

Tel: ++62 21 520 15 40

Fax: ++62 21 527 94 82

e-mail: [email protected]

ADB SME DEVELOPMENTTA

I

I. TABLE OF CONTENTS

I. TABLE OF CONTENTS ........................................................................................... I

II. TABLE OF ABBREVIATIONS ...............................................................................IV

III. TABLE OF FIGURES ..............................................................................................V

IV. TABLE OF REFERENCES ....................................................................................VI

V. EXECUTIVE SUMMARY ENGLISH ......................................................................VII

VI. RINGKASAN EKSEKUTIF...................................................................................XIII

1 BACKGROUND .......................................................................................................2

1.1 Fuel Prices and Policies...........................................................................................2

1.1.1 Government Programs From Reduced Fuel Subsidy ...........................................3

1.1.2 Observations of Other Parties ...............................................................................4

1.2 Scope of Assessment ..............................................................................................5

2 THE PROGRAM ......................................................................................................7

2.1 The Environment and Problems Identified Before Program Implementation...........7

2.2 Description and Implementation of the Program......................................................8

2.3 Financial and Contractual Issues.............................................................................9

3 IMPLEMENTATION: FINDINGS AND ASSESSMENT..........................................11

3.1 The RF Concept.....................................................................................................11

3.2 Selecting Number and Type of MFI Participants ...................................................13

3.3 Selecting Handling Banks ......................................................................................13

3.4 Selecting Facilitators..............................................................................................14

3.5 Selecting MFIs .......................................................................................................14

3.6 Handling Banks as WG Member............................................................................17

3.7 Training ..................................................................................................................17

ADB SME DEVELOPMENTTA

II

4 SUCCESS YARDSTICKS......................................................................................18

4.1 Success 1: Disbursement of Funds .......................................................................19

4.2 Success 2: Utilization of RF by MFI members .......................................................20

4.3 Success 3: Repayment ..........................................................................................21

4.4 Impact Monitoring ..................................................................................................23

5 ASSESSMENT OF DUTIES AND PERFORMANCE OF STAKEHOLDERS ........24

5.1 Government Agencies ...........................................................................................24

5.1.1 National Level......................................................................................................24

5.1.2 Provincial Level ...................................................................................................25

5.1.3 District Level........................................................................................................25

5.2 Facilitators..............................................................................................................26

5.3 Handling Banks (Bank Pelaksana) ........................................................................28

5.3.1 Handling MFI accounts [1-3] ...............................................................................29

5.3.2 Other Financial Services [4, 5] ............................................................................30

5.3.3 Tasks concerning training and guidance [6, 7]....................................................30

5.3.4 Monitoring and supervision [8, 9] ........................................................................31

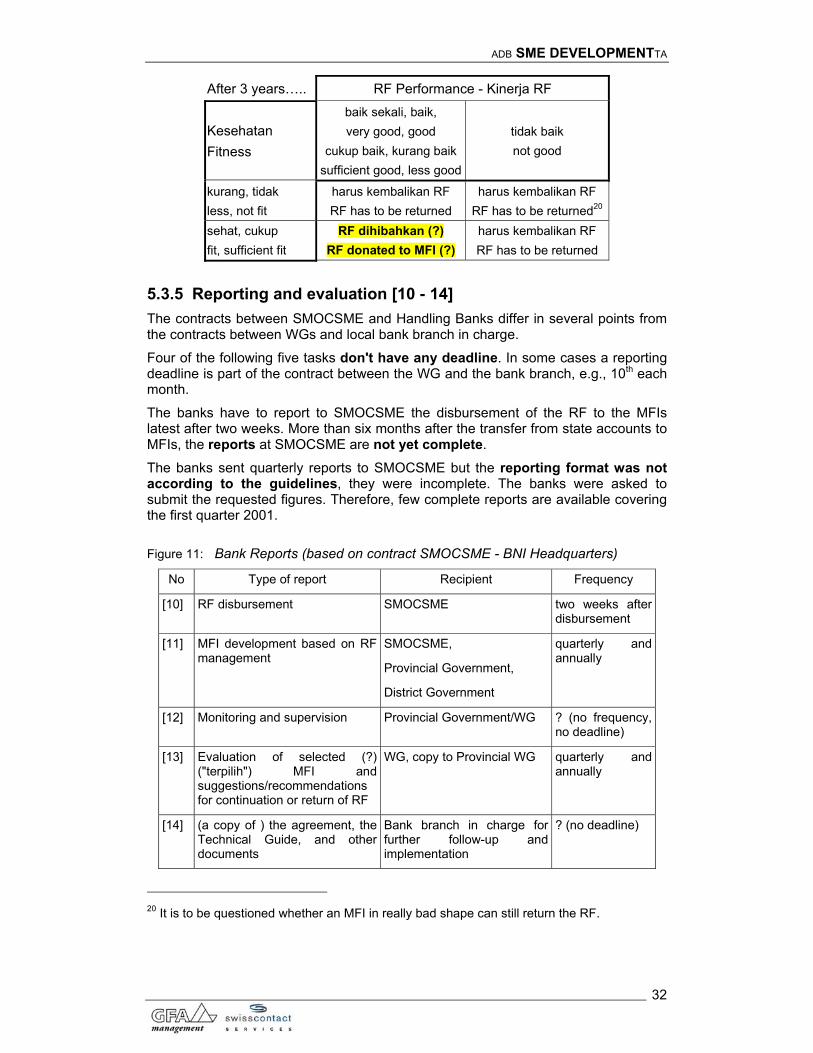

5.3.5 Reporting and evaluation [10 - 14] ......................................................................32

5.3.6 Reasons for Underperformance ..........................................................................34

5.3.7 Handling Fee .......................................................................................................34

5.4 The MFIs................................................................................................................36

5.4.1 Financial Activities...............................................................................................36

5.4.2 Monitoring Loan Repayment ...............................................................................38

5.4.3 Administration and Bookkeeping Issues .............................................................39

5.4.4 MFI Organizations ...............................................................................................39

5.5 Auditors..................................................................................................................40

6 PROGRAM MEASUREMENTS .............................................................................41

7 PNM, AN ALTERNATIVE INSTITUTIONAL SET-UP ............................................44

8 RECOMMENDATIONS..........................................................................................45

8.1 Recommendations for SMOCSME ........................................................................45

8.1.1 Guide Book..........................................................................................................45

ADB SME DEVELOPMENTTA

III

8.1.2 Improved Reporting.............................................................................................47

8.1.3 Improve Monitoring and Introduce Evaluation.....................................................48

8.1.4 Documentation "Lending to MFIs".......................................................................49

8.2 Recommendations Regarding Provincial WG........................................................49

8.3 Recommendations Regarding District WGs ..........................................................50

8.4 Recommendations Regarding Facilitators .............................................................50

8.5 Recommendations for MFIs...................................................................................52

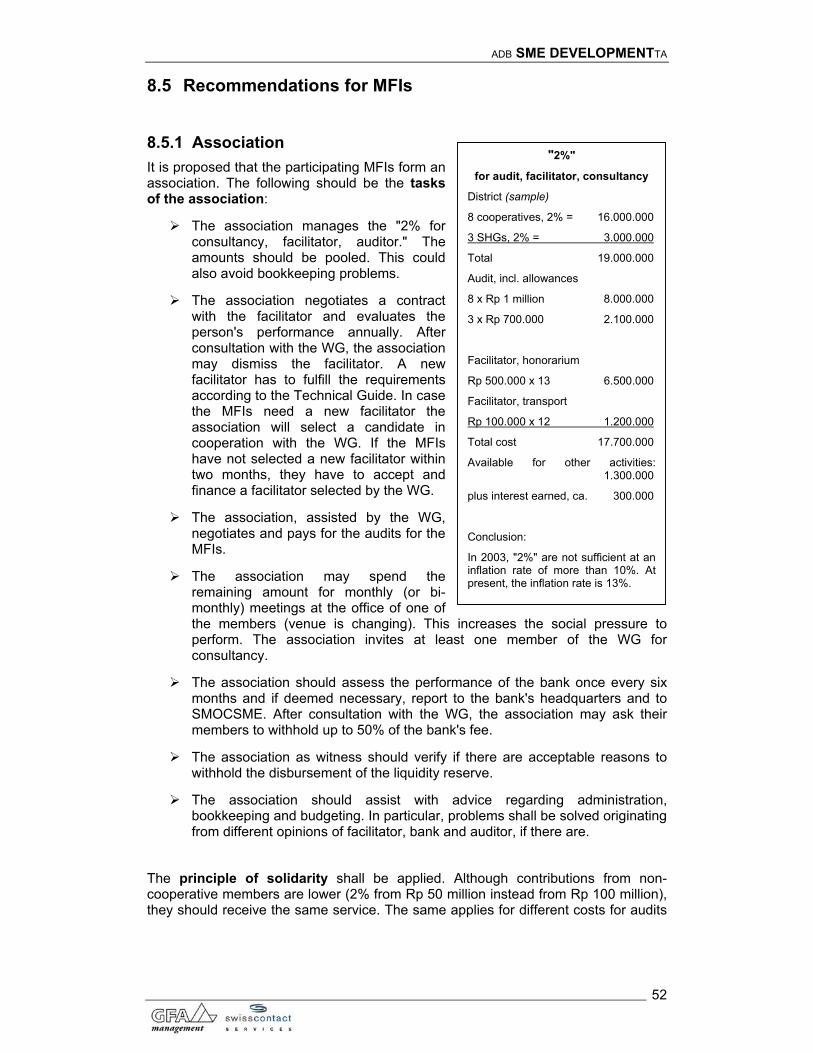

8.5.1 Association ..........................................................................................................52

8.5.2 Prevention of Fraud, Handling of Arrears and Bad Debt.....................................53

8.6 Recommendations Regarding Handling Banks .....................................................55

8.7 Recommendations for Training..............................................................................56

8.8 Recommendations Regarding Institutional Set-up.................................................59

9 ANNEXES..............................................................................................................60

9.1 ANNEX 1: Impact Analysis ....................................................................................60

9.2 ANNEX 2 : Objectives and Indicators ....................................................................64

9.3 ANNEX 3: Success Supporting Factors.................................................................66

9.4 ANNEX 4: Performance Evaluation .......................................................................67

9.5 ANNEX 5: RF Performance Assessment (Calculation) ........................................68

9.5.1 Scoring ................................................................................................................68

9.5.2 Example for MFI RF Performance Assessment ..................................................68

ADB SME DEVELOPMENTTA

IV

II. TABLE OF ABBREVIATIONS

BDS Business Development Services

BMT Baitul Maal Wa Tanwil, Islamic SHG

BPR Bank Perkreditan Rakyat, Rural Bank

DWG District Working Group

IFI Informal Financial Institutions, i.e. those set up by NGOs and independent savings and credit group members

KJA Koperasi Jasa Audit

KPKN Kantor Perbendaharaan dan Kas Negara, Government cashier office

KSP Koperasi Simpan Pinjam, single purpose savings and credit cooperative

KUD Koperasi Unit Desa, incorporated multipurpose village cooperative

LEPMM (Program) Lembaga Ekonomi Produktif Masyarakat Mandiri

MFI Micro Finance Institutions, i.e. cooperatives and SHGs (self-help groups, "informal financial institutions (IFI)")

OCSME Office of Cooperatives and Small Medium Enterprises

PHBK Proyek Hubungan Bank dengan Kelompok, Project Linking Banks and Self-Help Groups

RF Revolving fund

SHG Self-Help Group, here: savings and credit groups, a grassroots movement, identical with non-incorporated MFIs

SMERU Social Monitoring Early Respond Unit, an international sponsored research institute (1998 in the framework of monitoring social safety net), meanwhile independent

SMERU Social Monitoring Early Respond Unit, an international sponsored research institute (1998 in the framework of monitoring social safety net), meanwhile independent

SMOCSME State Ministry of Cooperatives and Small Medium Enterprises

USP-Kop Usaha Simpan Pinjam Koperasi, the autonomous (separate balance sheet) savings and credit unit of a multipurpose cooperative

WG Working Group on district level (Pokja, Kelompok Kerja)

ADB SME DEVELOPMENTTA

V

III. TABLE OF FIGURES

Figure 1: Price Developments for gasoline ,exchange rate, and price of crude oil ...........2 Figure 2: Fuel subsidy from FY 91/92 – FY 2001 .............................................................3 Figure 3: Three types of compensation regarding reduced fuel subsidies .......................4 Figure 4: Location of evaluation by SMERU.....................................................................5 Figure 5: Location of the survey........................................................................................6 Figure 6: Utilization of fee per annum.............................................................................10 Figure 7: Criteria of participants......................................................................................15 Figure 8: Distances (km) to MFIs....................................................................................16 Figure 9: RF: Disbursement through BNI per March 2001 .............................................19 Figure 10: Honorarium of Facilitators ................................................................................27 Figure 11: Bank Reports (based on contract SMOCSME - BNI Headquarters)................32 Figure 12: Bank Reporting Requirements: Contract WG Bantul - BPD Bantul branch .....33 Figure 13: Allocation of Costs for Auditors and Facilitators...............................................40 Figure 14: Reporting institution: Facilitator (sample).........................................................47 Figure 15: Scoring Realized Benefits versus Expectations before taking up the loan. .....49 Figure 16: Credit Sheet (sample) ......................................................................................54 Figure 17: Scheduling Training "Fitness Appraisal" ..........................................................58

ADB SME DEVELOPMENTTA

VI

IV. TABLE OF REFERENCES

Author Title BRI Laporan Triwulanan I/2001 Perkembangan Dana Bergulir

Subsidi BBM oleh KSP/USP-Kop dan LKM

Deputi Menteri Negara Koperasi & UKM Bidang Pembiayaan

Konsep Kebijakan Pengembangan KSP/USP-KOP dan LKM, , Jakarta Maret 2001

LKM - Handling Bank Naskah Perjanjian antara LKM dengan Bank tentang Perkuatan Lembaga Keuangan Mikro…(BRI Purwakarta)

Menteri Negara Urusan Koperasi dan Usaha Kecil dan Menengah

Naskah Kesepakatan Bersama antara Menteri Negara Urusan Koperasi dan Usaha Kecil dan Menengah tentang Perkuatan Koperasi Simpan Pinjam/Unit Simpan Pinjam Koperasi (KSP/USP KOP) dan Lembaga Keuangan Mikro (LKM) dengan Bantuan Dana Bergulir dari Subsidi BBM Terarah 27 Oktober 2000

Menteri Negara Urusan Koperasi dan Usaha Kecil dan Menengah

Petunjuk Pelaksanaan Evaluasi Kinerja Dana Bergulir dari Hasil Pengurangan Subsidi BBM Terarah

Keputusan Menteri Negara Koperasi dan UKM Nomor 03/KEP/MENEG/I/2001, 16 Januari 2001

SMERU Research Institute

Has the Reallocation of Fuel Subsidies Addressed Community Concerns?, Newsletter Nr. 02 Mar-April 2001

WG/Pokja - Handling Bank/Bank Pelaksana

Naskah Kesepakatan antara Kelompok Kerja Dana Bergulir Kabupaten dengan Bank tentang Perkuatan KSP/USP-Kop dan LKM (BNI - Kab. Bojonegoro)

ADB SME DEVELOPMENTTA

VII

V. EXECUTIVE SUMMARY ENGLISH

Background In October 2000, the Indonesian Government, pressured by an agreement with the IMF, increased fuel prices. Fuel price subsidies ballooned from Rp 1.4 trillion (about US$ 600 million) in fiscal year 1996/1997 to Rp 51.1 trillion (approximately $5.3 billion) in fiscal year 2000 (April - December = 9 months only). The fuel price increase resulted in reduction of subsidies but a burden for the low-income strata of the population. The Government allocated from these savings Rp 350 billion (about $40 million) to a Revolving Fund (RF).

In October 2000, the Government of Indonesia through the Office of the State Ministry of Cooperative Affairs and Small Medium Enterprises (SMOCSME) introduced a program called "Strengthening Savings and Credit Cooperatives, Savings and Credit Units of Cooperatives and Micro Finance Institutions Assisted with a Revolving Fund from Fuel Subsidies." A revolving fund (RF) shall strengthen selected non-bank micro financial institutions (MFIs) so that they achieve scale and professionalism enabling them to continuously borrow to low income people in their community and finally qualify as debtors for commercial banks.

A 3-year RF should be channeled to at least 350,000 micro entrepreneurs and farmers (maximum individual loan amount: Rp 1 million) through

2,925 MFIs being registered as a cooperative; they received Rp 100 million ($11,000) each to be channeled as micro loans to at least 90 members;

1,000 non-registered MFIs received Rp 50 million each for at least 45 borrowers.

The MFIs pay quarterly a 4% interest/fee. The "Handling Bank" keeps 1% for its services, 2.5% are added to the MFIs' blocked "liquidity reserve", and 0.5% are reserved to cover costs for auditing the MFIs, for the facilitator and for consultancy, advice and guidance ("pembinaan").

On Central level, SMOCSME concluded agreements with three national "Handling Banks" (BRI, BNI, Bukopin) and 23 Provincial Development Banks (BPD), the "crucial partner" (Deswandhy, Deputy Minister SMOCSME). They were given the important tasks to safeguard the RF: involvement in selecting MFIs, training MFI personnel, guidance, monitoring and supervision as well as monthly reporting on the development and performance of these MFIs over a 3-year period.

In nearly all (341) participating districts in Indonesia, the Offices for Cooperatives and SME (OCSME) organized Working Groups (WGs). The WGs concluded mirroring contracts with bank branch managers and with about 9 to 13 selected MFIs. In addition, a facilitator with community development experience was selected to support and bridge between MFIs, banks and government agencies. The banks concluded also contracts with the MFIs.

The 3-4-month preparation and socialization phase started in September 2000. The Revolving Fund (RF) was released in December.

Scope of Assessment During July 2001, the Financial Team of ADB Technical Assistance to SME Development and two resource persons assessed the implementation and performance of the program.

ADB SME DEVELOPMENTTA

VIII

More than six months after release of the funds to the MFIs, the Team interviewed representatives in 7 provinces (four islands) originating from:

2 Jakarta-located headquarters of banks with a nationwide branch network, namely BRI and BNI, both together accounting for nearly two thirds of the scheme's participants

3 headquarters of Provincial Development Banks

8 bank branches keeping accounts of the participants

6 district offices of the Ministry of Cooperatives and SME

8 single-purpose credit and savings cooperatives

6 multi-purpose cooperatives with an autonomous savings and credit unit

7 non-registered savings and credit cooperatives

Experience was shared with 7 facilitators.

The Team asked for and received copies of all relevant contracts, instructions and guidelines concerning the implementation of the program.

On July 20, the Team discussed preliminary findings with Mr. Agus Muharram , Assistant to Mr. Deswandhy, Deputy Minister SMOCSME, who is in charge of the program. On July 26, the Team had the opportunity to discuss the findings with the Finance Task Force and with representatives from banks involved in the RF.

The Team members extend their thanks to all institutions for their readiness to accept the Team on shortest notice, to make available the documents and to assist with logistic support. The Team members enjoyed a frank atmosphere. Most of all the Team has to extend its praise to the staff of the visited institutions who trustfully not only answered the seemingly endless questions but also shared their experience and aspirations.

Main Findings The RF concept is almost excellent. It involves the Government and private business oriented parties, the MFIs and the banks. The MFIs pay for business development services: the facilitators, training and guidance from banks (consultancy) and external auditors. Another quite unique feature is the effort to continuously measure impact. A concept for the utilization of data or monitoring results could, however, not be presented. Several questions, e.g. relating to the management of the 0.5% (2% p.a.) fee, namely costs for audit, facilitator and consultancy, are discussed controversially. The parties can not differ between rules that are allowed to be adjusted according to local conditions and other rules that are not negotiable on local level. The concept has still a "foggy" end. According to the Technical Guide, the RF will be donated to well-performing MFIs after three years. The contract between MFIs and the District Working Group offer only a prolongation.

The Team deemed it too early to judge if the MFIs have also already been strengthened considerably in non-financial fields. However, considering few efforts with regard to training and consultancy, it is quite doubtful.

The implementation of the program by SMOCSME was dictated by time pressure. This resulted in weaknesses in the preparation and socialization of the program. For example, training material was not developed and bank branches received instructions on reporting only in February 2001. Monitoring and reporting tools were developed (reportedly by one

ADB SME DEVELOPMENTTA

IX

of the appointed banks) and their use instructed without having them tested in the field. Management of filing, documentation, reporting, supervision and monitoring on Central level is poor.

The Working Groups on District level executed the selection of participants, the MFIs, in a transparent and objectively verifiable way although some successful candidates did not fulfill all selection criteria. Only few large MFIs (assets more than Rp 500 million) received the loan. Most, but not all of the MFIs are located within 15 km from the district capital. The offices of the SMOCSME played an active role. They are now rather handicapped by the absence of operational funds, reallocation of staff and premises due to decentralization. They would be less involved would not the facilitator continuously keep contact with the staff in charge.

The facilitators were found to be sufficiently qualified. They are well received by the MFIs. They act not only as a consultants but also as discussion partners and catalysators. They are involved in the development of about ten similar units. They know the internal problems and are disseminating best practices and experiences. Continuous supervision by an outsider is certainly contributing to a higher standard of financial "hygiene." The job description could be more specific. A fixed honorarium is considered problematic if the facilitator has to pay transport from his own pocket. Transport is a particular problem if the facilitator owns no motorcycle. MFIs pay the honorarium for the facilitator therefore they should have a vote when (re-) negotiating the contract or employing the facilitator. Both, the WG and the MFIs should agree on the facilitator.

The MFIs (KSP/USK-Kop, LKM) have been found to be very enthusiastic. Finally, they did not receive a "dropping" but they were successfully competing with other MFIs. They are engaged and understand rather well the intentions of the RF. They are cautious in their credit operation but do not exclude really small entrepreneurs without collateral from taking a loan. Serious administrative deficiencies were identified. They refer to credit contracts and how loan repayments are recorded. Most MFIs do not know the amount of loans in arrears, thus effectively preventing easy portfolio quality calculation. They do not mind being supervised and controlled because they see the opportunity to learn and improve. It is noteworthy and encouraging that in several districts the participants formed associations.

The majority of borrowers, mostly micro entrepreneurs, could increase the welfare of the family. Many took up less than the maximum Rp 1 million. The MFIs offer a loan in the right size, more than they could get from traditional savings and credit groups but less than banks would like to extend to cover their transaction costs. The MFIs have their roots in the community, and they allow the required repayment flexibility at low cost, in particular if compared with the alternative moneylenders.

The "crucial partner", the banks, failed in a disastrous way to perform. They receive from the MFIs (finally from the work of thousands of small entrepreneurs) about Rp 14 billion annually for their task but they do not execute it. No bank has been met employing additional staff for the program on district level although the MFIs pay about Rp 40 million annually to the appointed district bank branch for services they do not receive. Banks shortened the training from one week to one day. They visit the MFIs about once in 6 months, some bank officers do even not know the location of the MFIs' premises. The banks have to prepare performance evaluation reports. Only very few reports arrived at

ADB SME DEVELOPMENTTA

X

the SMOCSME. Nearly all reports contained wrong figures, most of all because bank officers do not report problems related to the forms. The Team heard also that some banks are hesitant to advice MFIs, in particular bigger ones, because they are competing for the same clientele. Another bank did not see the threat but the opportunity: Based on a recommendation of the MFI, it took over several debtors who needed higher loan amounts than the MFI could make available. The MFI lost big risks and has now more funds available to finance additional small entrepreneurs!

The Team assessed whether the fee for the Handling Bank is sufficient. On average, banks earn about Rp 40 million per year. It is costly to conduct visits to MFIs at a distance of more than 1-hour travel. However, seen apart from thinly populated areas and small islands, the average distance is less than half-hour travel. Banks can easily earn a gross on-top profit of more than 100%.

It is also questioned whether the bank staff is qualified for the job. Normally bank people are not trained to advice other financial institutions. They may be not familiar anymore with the non-computerized bookkeeping procedures and simple credit contracts. Credit analysts learn to assess non-financial enterprises based on 5 C (character, condition, collateral, capital, capacity) but not financial institutions based on CAMEL (capital, assets, management, earnings, liquidity).

Main Recommendations Recommendations for SMOCSME It is recommended that SMOCSME develops a "Guide Book to the RF" in which problems and solutions for problems are presented. This book should also answer all questions regarding ownership and management of the RF after end of 2003. Every MFI should own two copies of this book. The MFIs can finance these books from interest earned on the various RF accounts (According to the Technical Guideline interest earned on the "liquidity reserve" account belongs to the MFIs. However, a respective clausula is not part of the contract between the District WG and MFIs.)

The entire reporting system needs to be reviewed including type, frequency and recipient of reports. In order to obtain meaningful data, a review of the evaluation scheme for MFIs and test trials are an absolute necessity before starting national implementation. Bank staff needs to be trained to cope with the monthly and quarterly performance and fitness evaluation formats. A manual with forms, samples how to use them, and explanations regarding the necessity of obtaining the data has to be sent to banks and MFIs. The portfolio quality calculation ("repayment") and data collection for the impact analysis needs to be made easier (principle: "simple and dirty"). Payments to banks for their services should also be linked to on-time reporting.

One reason for connecting banks with MFIs through training, consultancy and reporting is that after three years, banks should not anymore regard MFIs as a "strange animal" but as qualified potential debtors. It is proposed that together with banks schemes are developed that allow banks prudential lending to MFIs as companies without individuals rendering collateral thus risking their private property.

The Team learned that in due time a Consultant will be engaged to elaborate proposals for improving monitoring of the RF. The Team backs this efforts and urges immediate implementation and appropriate, thorough training of the staff who will handle this field in future. One of Indonesia's assets is its richness in micro finance schemes. The RF adds to this an exciting new product. Every district could allow at least one student to write a thesis on the RF in that district. It is proposed that universities be invited to take part in the evaluation of data.

ADB SME DEVELOPMENTTA

XI

Recommendations for District WGs Independent from how the Government has booked the disbursement of the RF to the MFIs, legally, the Government is probably still owner of the RF. The MFIs use the RF based on a contract in which the word credit is not used to describe the character of the RF. Until end of 2003, the District WG will regularly be involved with the management of the RF and the relationship between bank, facilitator and MFIs. It is recommended that a budget should be made available for the activities of the WG. It is proposed to assess, if the 2.5% per quarter for the "liquidity fund" should be transferred to an account kept by the WG. The WG would, after receiving the bank's evaluation release the liquidity fund. The interest earned on this account, about Rp 3 million per year, would be available to finance WG activities. This procedure does not create new dependencies because the MFIs depend already now on the WG's recommendation to utilize the liquidity fund.

It is recommended that the District WG facilitates the founding of an association of the RF participants, to exchange experience and discuss joint financial problems, e.g. the use of the 2% p.a. fee allocated to audit, consultancy, and facilitator.

Recommendations for Facilitators Nobody controls the facilitators' day-to-day activities. The facilitators' job description needs to state clearly how often they should visit MFIs. The facilitators should be obliged to enter name and activity in the MFI's visitor book or a separate book. The facilitators should also keep records on their activities, which are to be countersigned by MFIs. It is proposed that the District Government offers them a desk and allows the use of a computer for his reports. The honorarium, or a lumpsum for fuel, should consider necessary costs for transport in order to make sure that also distant MFIs are visited only regularly.

Recommendations for MFIs The majority of MFIs fail because of non-performing loans (NPL). Following are proposals in order that NPLs do not remain undetected and become a problem in the future.

All MFIs should use credit contracts (one page) following minimum standards, among others clearly stating when installments are due, separately for principal and interest (except for loans with daily repayment), and the final date for repayment. A clausula in this contract shall reserve the Government's right to collect the loan.

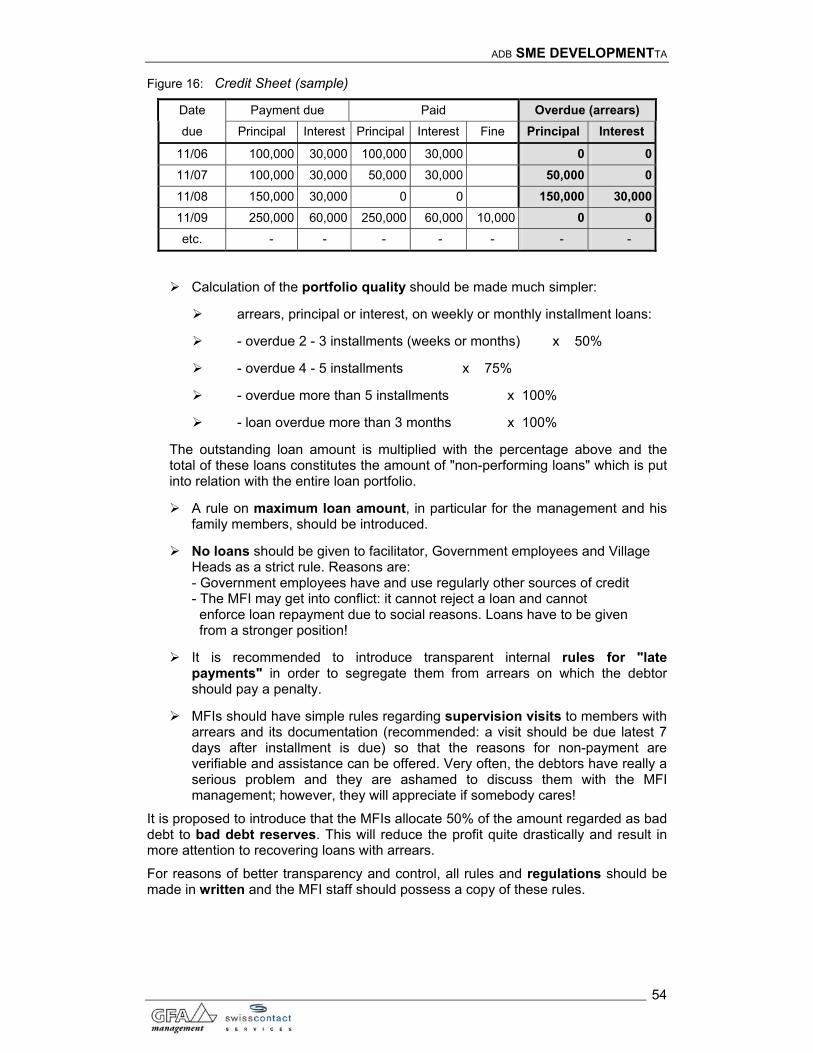

Arrears should be calculated and presented at the end of each month.

Calculation of the portfolio quality has to be made much simpler.

A rule on maximum loan amount, in particular for the management and his family members, should be introduced.

It is recommended to introduce internal rules for "late payments" in order to segregate them from arrears on which the debtor should pay a penalty.

MFIs should have simple rules regarding supervisory visits, and their documentation, to members with arrears so that the reasons for non-payment are verifiable.

It is recommended that MFIs apply the same conditions to loans financed from the RF as those financed from members' savings.

ADB SME DEVELOPMENTTA

XII

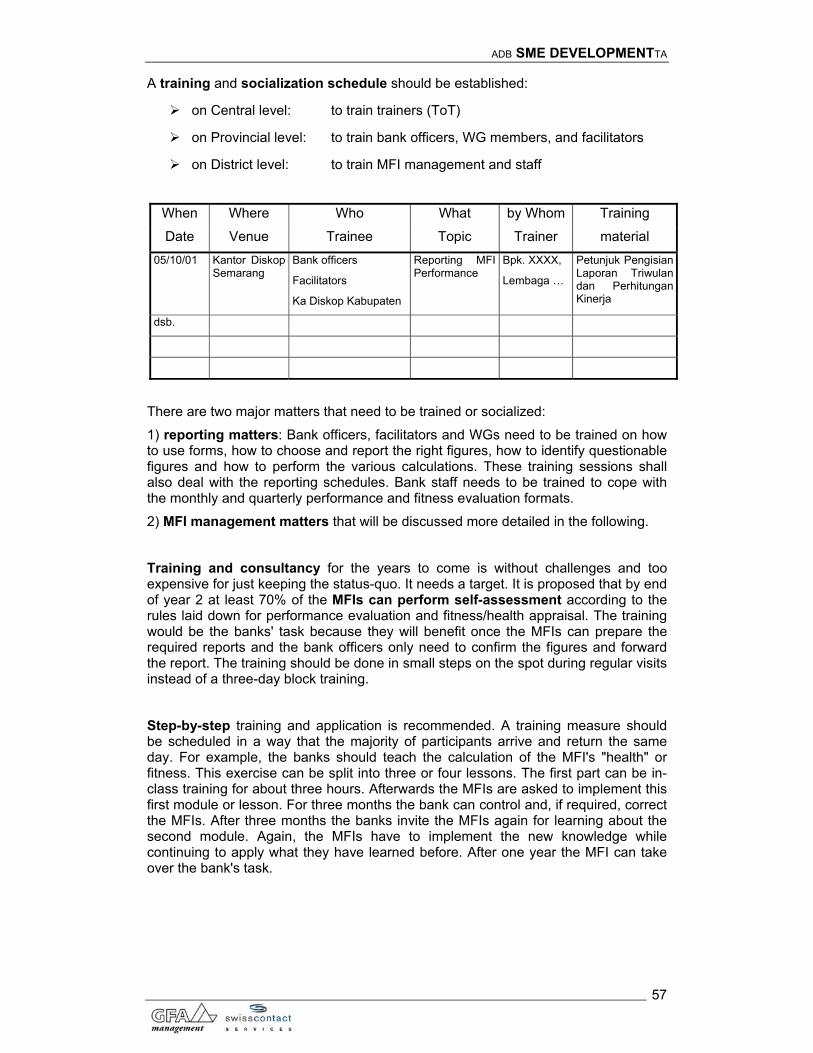

Training and consultancy for the years to come is without challenges and too expensive for just keeping the status quo. It needs a target. It is proposed that by end of year 2 at least 70% of the MFIs can perform self-assessment according to the rules laid down for performance evaluation and fitness. The training would be the bank's task because they will benefit if the MFI can prepare the required reports and the bank officers only need to confirm and forward the report. The training should be done in small steps on the spot during regular visits.

Two urgent training requirements refer to (a) differences between loan disbursement and outstanding loans in liquidity calculations and balance sheets and (b) interest calculation (flat, declining) and the effect of delayed loan repayment on effective interest and interest income.

Recommendations regarding Handling Banks The contract with Handling Banks needs to be assessed. The present system of paying banks, based on good trust without proper control of activities, should be abolished. It is recommended that banks do only receive the fee if they have performed their duty according to contract. It is acknowledged that in remote areas Rp 40 million might not be cost covering, if proper service is provided. This can be compensated with urban districts (municipalities) were distances average far below 10 km. The additional costs could be compensated with lower fees for small districts. Only MFIs and the District WG are in the position to judge, whether banks fulfilled the contractual obligations. Fees should only be released to banks, if the District WG and the MFIs consent.

In contrast to the facilitator and the MFIs, banks on district level were not selected but appointed. As the bank staff is burdened without receiving a reward (and punishment may not loom), one should consider the introduction of a split fee, where a part of the money is directly earned by bank staff when visiting the MFIs. Another possibility to overcome the lack of engagement may be to invite (or even to tender) other banks in the district to participate.

The Team proposes training bank officers in charge for the RF.

Recommendation regarding institutional Set-up It is recommended that in future, all financial Government programs directed towards small financial institutions should involve PNM in order to centralize experience and expertise. The level of involvement may change from case to case

ADB SME DEVELOPMENTTA

XIII

VI. RINGKASAN EKSEKUTIF

Latar belakang Dalam bulan Oktober 2000, tekanan terhadap Pemerintah Indonesia oleh sebuah perjanjian dengan IMF mengakibatkan harga BBM naik. Subsidi BBM yang dalam tahun anggaran 1996/1997 hanya Rp 1,4 triliun (waktu itu sekitar US$ 600 million) kemudian naik dengan pesat mencapai Rp 51,1 triliun (sekitar US$ 5.3 miliar) dalam tahun anggaran 2000 (April - Desember = 9 bulan). Naiknya harga BBM akan mengurangi subsidi BBM, tetapi menimbulkan beban terhadap kelompok penduduk berpendapatan rendah. Pemerintah mengalokasikan penghematan tersebut sebesar Rp 350 miliar (sekitar US$ 40 juta) untuk dana bergulir.

Dalam bulan Oktober 2000, Pemerintah Indonesia melalui Kantor Menteri Negara Koperasi dan UKM meluncurkan sebuah program yang disebut sebagai “Penguatan Koperasi Simpan Pinjam/Unit Simpan Pinjam dan Lembaga Keuangan Mikro Melalui Dana Bergulir Kompensasi Subsidi BBM”. Dana bergulir akan memperkuat Lembaga Keuangan Mikro Bukan Bank (LKM Non Bank) sehingga lembaga tersebut dapat mencapai skala dan profesionalisme untuk mampu terus memberikan pinjaman kepada penduduk berpendapatan rendah di lingkungannya dan pada akhirnya memenuhi kualifikasi sebagai peminjam dari bank umum.

Selama 3 tahun dana bergulir akan disalurkan minimal kepada sekitar 350.000 pengusaha mikro dan petani (dengan maksimum pinjaman maksimum Rp 1 juta per orang) melalui:

2.925 KSP/USP yang akan memperoleh dana sebesar Rp 100 juta (US$ 9,000) per KSP/USP yang akan disalurkan sebagai kredit mikro minimal kepada 90 orang anggota;

1.000 LKM (pra koperasi atau lembaga semacam koperasi tetapi belum mempunyai badan hukum) yang memperoleh dana sebesar Rp 45 juta per LKM yang disalukan kepada minimal 45 peminjam

LKM membayar "fee/bunga" 4% per triwulan. Bank Pengelola akan memperoleh 1% atas jasanya, 2,5% sebagai “cadangan likuiditas terbeku” LKM, dan 0,5% dipergunakan untuk menutupi biaya audit, honorarium fasilitator, dan untuk konsultasi, saran dan petunjuk (pembinaan).

Pada tingkat pusat, Kantor Menteri Negara Koperasi dan UKM memutuskan untuk bekerjasama dengan 3 “bank nasional pengelola” (BRI, BNI, dan BUKOPIN) dan 23 Bank Pembangunan Daerah (BPD), “pemegang peranan krusial” (Deswandhy, Deputy Pembiayaan Kantor Menteri Negara Koperasi dan UKM). Bank mempunyai tugas yang penting dalam pelaksanaan program dana bergulir, yaitu: (i) ikut serta dalam seleksi LKM, (ii) melatih pengelola LKM, dan (iii) memberikan petunjuk, melakukan monitoring dan pembinaan sebagai bahan untuk laporan bulanan terhadap perkembangan dan kinerja KSP/USP dan LKM selama 3 tahun.

Hampir semua (341) kabupaten/kota di Indonesia ikut serta, dan Dinas Koperasi dan UKM di kabupaten/kota mengelola kelompok kerja (Pokja) yang membuat kontrak kerjasama dengan pengelola kantor cabang bank dan dengan sekitar 9 hingga 13 LKM terpilih. Kemudian, seorang fasilitator yang mempunyai pengalaman dalam pengembangan masyarakat dipilih untuk mendukung dan penghubung antara LKM,

ADB SME DEVELOPMENTTA

XIV

bank, dan lembaga pemerintah. Bank juga membuat kontrak kerjasama dengan LKM.

Tahapan persiapan dan sosialisasi dilaksanakan sekitar 3-4 bulan, sejak September 2000. Dana bergulir disalurkan pada bulan Desember 2000.

Ruang lingkup penilaian Selama bulan Juli 2001, Tim Kelompok Kerja Keuangan ADB SME Development TA dan 2 orang nara sumber melakukan penilaian mengenai pelaksanaan dan kinerja program ini. Setelah 6 bulan dana bergulir ini disalurkan kepada LKM, tim melakukan wawancara dengan beberapa pihak yang terkait dengan program ini di 7 propinsi yang berasal dari:

2 kantor pusat dari bank umum yang berlokasi di Jakarta dengan jaringan kantor cabang hampir di seluruh Indonesia, yaitu BRI dan BNI, dimana kedua bank ini memperoleh alokasi dana untuk sekitar 2/3 dari KSP/USP dan LKM yang ikut serta dalam program ini

3 kantor pusat BPD

8 kantor cabang bank dimana rekening KSP/USP dan LKM tersimpan

6 Kantor Dinas Koperasi dan UKM Kabupaten/Kota

8 KSP

6 USP

7 LKM

Tukar pengalaman dengan 7 orang fasilitator

Tim berdiskusi dan menerima salinan dari dokumen yang relevan dalam pelaksanaan program ini, seperti kontrak, instruksi, dan petunjuk teknis.

Pada tanggal 20 Juli 2001, temuan awal penilaian ini didiskusikan dengan Bapak Agus Muharram, Asisten Deputy Pembiayaan selaku Ketua Pelaksana Penyaluran Dana Subsidi BBM Pokja Pusat. Pada tanggal 26 Juli 2001, tim memperoleh kesempatan untuk mendiskusikan temuan–temuan dengan Anggota Satuan Tugas Keuangan dan wakil dari bank pelaksana.

Tim mengucapkan terima kasih kepada semua lembaga yang mau menerima tim meskipun dengan pemberitahuan yang sangat singkat, menyediakan seluruh dokumen yang diperlukan, dan memberikan bantuan logistik. Anggota tim merasa senang dengan suasana yang ada. Hampir semua anggota tim merasa staf dari lembaga yang dikunjungi telah memberikan jawaban yang terpercaya dan tidak hanya sekedar memberikan jawaban terhadap pertanyaan yang ada, tetapi juga melakukan tukar pengalaman dan pendapat.

Temuan utama Konsep dana bergulir sangat baik. Program ini melibatkan pemerintah dan swasta, kelompok yang berorientasi bisnis, LKM, dan bank. LKM membayar untuk jasa pengembangan usaha yang diterima: fasilitator, pelatihan dan petunjuk dari bank (konsultasi) dan audit eksternal. Pengukuran dampak secara terus menerus merupakan suatu kegiatan yang baik. Konsep untuk menggunakan data atau hasil monitoring sampai saat ini belum dapat dilakukan. Beberapa pertanyaan seperti

ADB SME DEVELOPMENTTA

XV

pengelolaan fee 0,5% per triwulan (2% per tahun) yang diperuntukkan sebagai biaya audit, fasilitator dan konsultasi masih mengandung diskusi yang kontroversial. Pihak yang terlibat di daerah tidak dapat membedakan antara aturan yang dapat disesuaikan berdasarkan kondisi setempat dan aturan lain yang dapat dinegosiakan di tingkat daerah. Pada akhirnya konsep ini masih mengandung “kabut”. Berdasarkan pedoman teknis, dana bergulir akan dihibahkan kepada LKM yang mempunyai kinerja baik setelah 3 tahun. Perjanjian Kerjasama antara LKM dengan Pokja kabupaten/kota hanya menawarkan perpanjangan kerjasama tsb.

Tim ini merasa terlalu dini untuk menilai jika KSP/USP dan LKM sudah sangat diperkuat sekali dalam bidang non keuangan. Bagaimanapun, mengingat upaya yang sedikit sekali dalam konsultasi dan pelatihan, sungguh diragukan.

Pelaksanaan program ini oleh Kantor Menteri Negara Koperasi dan UKM menghadapi tekanan waktu. Akibatnya terdapat kelemahan dalam persiapan dan sosialisasi program. Sebagai contoh, materi pelatihan tidak dipersiapkan dan kantor cabang bank baru menerima surat keputusan mengenai evaluasi sebagai bahan laporan baru pada bulan Februari 2001. Alat untuk melakukan monitoring dan pelaporan telah dipersiapkan (hanya dilaporkan oleh satu bank) dan digunakan tanpa dicoba terlebih dahulu di lapangan. Pengelolaan file, dokumen, laporan, pembinaan dan monitoring di tingkat pusat lemah.

Pokja kabupaten/kota melakukan seleksi terhadap calon peserta (KSP/USP dan LKM) dengan transparan dan melakukan verifikasi secara objektif, meskipun ada beberapa kandidat yang terpilih tidak memenuhi seluruh kriteria seleksi. Hanya sedikit LKM besar (asset lebih besar dari Rp 500 juta) yang menerima dana bergulir ini. Sebagian besar, tetapi tidak semua lokasi LKM berjarak tidak lebih dari 15 km dari ibukota kabupaten/kota. Kantor Dinas Koperasi dan UKM kabupaten/kota melakukan peran aktif. Saat ini Pokja kabupaten/kota menghadapi kendala berupa: (i) tidak adanya dana operasional, dan (ii) realokasi staf dan dasar pemikiran yang disebabkan karena pelaksanaan otonomi daerah. Keterlibatan Pokja pasti akan berkurang jika fasilitator secara terus menerus menghubungi anggota Pokja.

Fasilitator yang ditemui cukup mempunyai kemampuan. Dapat diterima dengan baik oleh LKM. Fasilitator tidak hanya sebagai konsultan, tetapi juga berfungsi sebagai teman diskusi dan memberikan motivasi. Mereka terlibat aktif dalam pengembangan sekitar 10 lembaga penerima, persoalan internal yang dihadapi dan mendiseminasikan praktek dan pengalaman terbaik. Pembinaan yang berkelanjutan yang dilakukan orang luar tentu saja mempunyai kontribusi terhadap pencapaian standar kesehatan yang lebih tinggi. Honorarium yang tetap akan menimbulkan masalah jika fasilitator harus membayar biaya transport sendiri, utamanya bagi fasilitator yang tidak mempunyai sepeda motor. LKM membayar honor fasilitator sehingga LKM seharusnya mempunyai suara bila dilakukan negosiasi kontrak atau akan memilih fasilitator. Keduanya, Pokja kabupaten/kota dan LKM seharusnya memberikan persetujuan terhadap fasilitator.

KSP/USK-Kop dan LKM yang ditemui sangat antusias. Akhirnya, LKM tidak menerima “bantuan”, tetapi mereka telah memenangkan kompetisi dengan LKM yang lain. LKM menggunakan dan memberikan perhatian dengan baik terhadap dana bergulir. Mereka berhati-hati dalam penyaluran kredit dengan tetap meminta agunan, namun tidak menutup kesempatan kepada pengusaha sangat kecil yang

ADB SME DEVELOPMENTTA

XVI

tidak memiliki agunan. Kelemahan administrasi yang cukup serius diidentifikasi pada LKM sehubungan dengan perjanjian kredit dan caranya untuk mencatat pembayaran cicilan. Sebagian besar LKM tidak mengetahui jumlah tunggakan kredit, akibatnya menghalangi mereka membuat perhitungan kualitas portfolionya secara efektif. Mereka tidak merasa diberatkan dengan pembinaan dan pengawasan, karena mereka melihat ada peluang untuk belajar dan memperbaiki. Perlu disampaikan perkembangan yang membesarkan hati yaitu LKM di beberapa kabupaten/kota membentuk paguyuban atau asosiasi.

Sebagian besar peminjam, adalah pengusaha mikro, dan mungkin dapat meningkatkan kesejahteraan keluarganya. Pinjaman yang diterima sebagian kurang dari Rp 1 juta. LKM memberikan pinjaman dengan jumlah yang sesuai, lebih besar dari pinjaman tradisionil yang dapat diterima dari arisan atau kelompok simpan pinjam, tetapi lebih kecil dibandingkan yang suka diberikan oleh bank, antara lain karena pertimbangan biaya transaksi. LKM mempunyai basis di masyarakat dan menerapkan pembayaran pinjaman yang fleksibel dengan biaya yang rendah, utamanya jika dibandingkan dengan pelepas uang.

Bank Pelaksana. “Pihak yang krusial”, bank, gagal dalam menunjukkan kinerjanya. Bank menerima dari LKM sekitar Rp 14 milyar per tahun (yang bersumber dari kerja ribuan pengusaha kecil) untuk tugas yang ditentukan, tetapi mereka tidak melakukan. Tidak ada bank yang ditemui mempekerjakan staf tambahan untuk program ini di kabupaten/kota, meskipun LKM membayar sekitar Rp 40 juta per tahun kepada kantor cabang bank untuk jasa yang mereka, LKM, tidak terima. Bank mempersingkat waktu pelatihan dari satu minggu yang ditentukan menjadi satu hari. Mereka berkunjung kepada LKM hanya satu kali dalam 6 bulan, dan beberapa petugas bank tidak mengetahui lokasi KSP/USP yang ikut dalam program ini. Bank telah menyiapkan laporan evaluasi kinerja. Hanya sedikit laporan yang sesuai dengan pedoman evaluasi sampai kepada Kantor Menteri Negara Koperasi dan UKM. Hampir semua laporan mengandung informasi yang salah, dimana penyebab utamanya adalah petugas bank tidak memberikan informasi tentang masalah yang dialami dalam penggunaan formulir yang tersedia. Tim mendengar juga bahwa beberapa bank enggan untuk memberikan pembinaan kepada LKM, utamanya yang besar, karena mereka berkompetisi untuk nasabah yang sama. Bank yang lain tidak melihat pembinaan terhadap LKM sebagai ancaman, tetapi sebagai peluang. Misalnya, berdasarkan rekomendasi dari LKM, bank dapat membiayai beberapa peminjam yang membutuhkan pinjaman lebih besar dari yang mampu disediakan LKM. LKM kehilangan resiko besar dan sekarang lebih banyak dana tersedia untuk memberikan tambahan dana kepada pemohon pinjaman mikro.

Tim menilai fee untuk bank pelaksana cukup. Secara rata-rata, cabang bank memperoleh pendapatan Rp 40 juta per tahun. Biaya yang cukup besar diperlukan untuk melakukan kunjungan kepada LKM yang mempunyai waktu tempuh diatas satu jam perjalanan. Meskipun demikian, hampir sebagian besar KSP/USP dan LKM berlokasi dengan jarak tempuh rata-rata kurang dari setengah jam. Bank dengan mudah dapat memperoleh keuntungan kotor lebih dari 100%.

Juga menjadi pertanyaan, apakah petugas bank mampu untuk melaksanakan tugas ini. Pada umumnya petugas bank tidak dilatih untuk memberikan nasihat kepada lembaga keuangan non bank. Mereka mungkin tidak familiar dengan prosedur sistem pembukuan yang tidak menggunakan komputer dan kontrak kredit sederhana. Analis kredit belajar untuk melakukan penilaian kepada perusahaan non lembaga keuangan berdasarkan prinsip 5C (karakter, kondisi usaha, agunan, modal, kapasitas) tetapi

ADB SME DEVELOPMENTTA

XVII

tidak untuk lembaga non keuangan berdasarkan CAMEL (modal, asset, manajemen, pendapatan/hasil usaha, dan likuiditas).

Rekomendasi utama Rekomendasi untuk Kantor Menteri Negara Koperasi dan UKM Direkomendasikan agar Kantor Menteri Negara Koperasi dan UKM mencetak “Buku Petunjuk Dana Bergulir” yang menjelaskan masalah dan jalan keluar untuk masalah yang ada. Buku ini juga dapat menjawab semua pertanyaan yang berkaitan dengan kepemilikan dan pengelolaan dari dana bergulir setelah akhir tahun 2003. Setiap LKM sebaiknya memiliki 2 eksemplar. LKM dapat membiayai buku ini dari bunga yang diperoleh dari beberapa rekening LKM yang ada di bank (Berdasarkan petunjuk teknis, bunga yang diperoleh dari cadangan likuiditas yang ada direkening LKM menjadi milik LKM. Meskipun demikian, klausul ini tidak termasuk dalam naskah kerjasama antara Pokja kabupaten/kota dengan dan LKM).

Sistem pelaporan yang ada perlu dikaji kembali termasuk bentuk, frekuensi dan penerima laporan. Agar laporan dapat mengandung data yang berarti, perlu dikaji kembali skema evaluasi LKM dan diuji coba terlebih dahulu sebelum dilaksanakan secara nasional. Pegawai bank perlu untuk dilatih agar dapat membuat laporan kinerja bulanan dan triwulanan yang sesuai dengan format evaluasi. Sebuah manual dengan bentuk dan contoh bagaimana menggunakannya, dan menjelaskan bagaiman data diperoleh harus dikirim kepada bank dan LKM. Perhitungan kualitas portfolio (“pembayaran kembali") dan data yang diperlukan untuk melakukan analisa dampak perlu dibuat lebih sederhana (prinsip: “sederhana dan kasar”). Pembayaran kepada bank untuk jasa yang diberikan seharusnya terkait dengan penyampaian laporan yang tepat waktu.

Salah satu alasan untuk menghubungkan bank dengan LKM melalui pelatihan, konsultasi dan laporan agar setelah 3 tahun bank tidak lagi melihat LKM sebagai “binatang aneh”, tetapi sebagai calon peminjam yang memiliki kemampuan. Untuk itu disarankan bersama dengan bank, program ini dikembangkan mengikuti prinsip kehati-hatian bank dalam penyaluran kredit kepada dan LKM dengan prinsip hati-hati sebagai perusahaan tanpa harus pengurus atau anggota LKM menyediakan agunan.

Tim ini memperoleh informasi bahwa dalam waktu dekat sebuah konsultan akan dipekerjakan untuk mempersiapkan proposal guna memperbaiki monitoring dari dana bergulir. Tim menganggap ini penting dan dapat dilaksanakan dalam waktu singkat dan sesuai, melalui pelatihan kepada pegawai yang akan melaksanakan program ini di lapangan di masa yang akan datang. .Salah satu kekayaan Indonesia adalah kaya dengan skema dan program keuangan mikro. Dana bergulir menambah program ini dengan produk yang menarik. Setiap kabupaten/kota sebaiknya ada satu mahasiswa yang menulis tesis mengenai dana bergulir ini. Diusulkan agar perguruan tinggi diundang untuk ikut serta dalam evaluasi data.

Rekomendasi untuk Pokja kabupaten/kota Terlepas dari cara bagaiman pemerintah mencatatkan penyaluran dana bergulir kepada LKM, secara legal pemerintah masih tetap menjadi pemilik dari dana bergulir. LKM menggunakan dana ini berdasarkan kontrak kerjasama dimana kata kredit tidak digunakan untuk menggambarkan karakter dari dana bergulir. Hingga akhir tahun 2003, Pokja kabupaten/kota akan terus terlibat dalam pengelolaan dana bergulir dan berhubungan dengan bank, fasilitator, dan LKM. Direkomendasikan agar

ADB SME DEVELOPMENTTA

XVIII

anggaran dapat disediakan untuk aktivitas dari Pokja kabupaten/kota. Sebuah usulan yang memerlukan penilaian, jika dana 2,5% sebagai cadangan likuiditas dapat ditransfer kepada sebuah rekening yang dikelola oleh Pokja kabupaten/kota. Pokja setelah memperoleh evaluasi dari bank baru dapat memutuskan untuk mencairkan dana ini. Bunga yang diperoleh dalam rekening ini yang diperkirakan sekitar Rp 3 juta per tahun dapat digunakan untuk membiayai operasional Pokja kabupaten/kota. Mekanisme ini tidak menciptakan ketergantungan baru sebab LKM saat ini juga tergantung kepada rekomendasi dari Pokja kabupaten/kota untuk menggunakan dana cadangan likuiditas.

Direkomedasikan agar Pokja kabupaten/kota dapat memfasilitasi pendirian asosiasi penerima dana bergulir, dalam rangka tukar pengalaman dan mendiskusikan persoalan keuangan bersama, seperti alokasi dari penggunaan dana 2% yang dialokasikan untuk audit, konsultasi, dan fasilitator.

Rekomendasi untuk fasilitator Tidak ada yang mengawasi fasilitator. Deskripsi uraian kerja dari fasilitator mengenai waktu/frekuensi kunjungan kepada LKM harus ditentukan dengan jelas. Fasilitator diminta untuk menuliskan nama dan aktivitasnya dalam buku tamu LKM atau pada buku yang terpisah. Fasilitator juga harus mencatat aktivitas yang dilakukan dan diketahui oleh LKM dengan membubuhkan tanda tangan. Diusulkan agar pemerintah daerah (kabupaten/kota) dapat menyediakan meja dan komputer bagi fasilitator untuk membuat laporan. Honor atau dana tetap untuk BBM harus cukup tersedia sebagai biaya transport dalam rangka menjamin agar LKM yang jauh dapat secara teratur dikunjungi.

Rekomendasi untuk LKM Pengalaman menunjukkan pada umumnya LKM gagal karena persoalan kredit macet. Agar kondisi ini tidak terjadi pada program ini dan dapat dideteksi dengan cepat sehingga tidak menimbulkan masalah di kemudian hari, maka direkomendasikan sejumlah usulan:

Semua LKM sebaiknya menggunakan perjanjian kredit (satu halaman) yang mengikuti standar minimum, antara lain jelas mengenai waktu pembayaran jatuh tempo, dipisahkan antara pokok dan bunga (kecuali untuk pinjaman dengan pembayaran harian), dan tanggal akhir untuk pembayaran. Penambahan klausul ini dalam kontrak merupakan jaminan bagi pemerintah yang benar untuk mengumpulkan pinjaman.

Tunggakan harus diperhitungkan dan dilaporkan pada setiap akhir bulan.

Perhitungan dari kualitas pinjaman harus dibuat lebih sederhana.

Aturan untuk jumlah pinjaman maksimum, utamanya untuk anggota secara berkelompok atau keluarga harus ditetapkan.

Direkomendasikan untuk membuat aturan internal mengenai “pembayaran yang terlambat” dalam rangka memisahkan antara debitur yang memiliki tunggakan dan akan diberikan sanksi.

LKM seharusnya mempunyai aturan yang sederhana mengenai kunjungan dan didokumentasikan, kepada anggota yang mempunyai tunggakan sehingga alasan untuk tidak membayar dapat diverifikasi.

ADB SME DEVELOPMENTTA

XIX

Direkomendasikan bahwa LKM menerapkan aturan yang sama untuk pinjaman kepada anggota yang dananya berasal dari dana bergulir subsidi BBM dan yang dikumpulkan dari simpanan anggota.

Pelatihan dan konsultasi untuk waktu yang akan datang tanpa perubahan dan tantangan dan tentunya mahal hanya dalam rangka mempertahankan kondisi yang ada. Diperlukan target. Diusulkan pada akhir tahun kedua minimal 70% dari LKM dapat melakukan penilaian sendiri tentang kinerjanya berdasarkan aturan yang terdapat dalam format evaluasi kinerja. Pelatihan ini akan menjadi tugas bank karena mereka akan memperoleh manfaat jika LKM dapat mempersiapkan laporan yang diperlukan dan pegawai bank hanya perlu untuk melakukan konfirmasi dan mengirimkan laporan ini. Pelatihan ini sebaiknya dilaksanakan dalam tahap kecil pada saat kunjungan dilakukan.

Dua jenis pelatihan diperlukan berdasarkan kepada (a) perbedaan antara penyaluran pinjaman dan baki debet pinjaman dalam perhitungan likuiditas dan neraca, dan (b) perhitungan tingkat bunga (tetap atau menurun) dan pengaruh dari pembayaran pinjaman yang terlambat terhadap tingkat bunga efektif dan pendapatan bunga.

Rekomendasi untuk bank pelaksana Kontrak untuk bank pelaksana perlu untuk dinilai. Saat ini pembayaran kepada bank berdasarkan kepada kepercayaan tanpa ada kontrol yang yang ketat terhadap kegiatan, sebaiknya dihapuskan. Direkomendasikan bank hanya dapat menerima pembayaran jasa jika tugasnya dilaksanakan sesuai dengan yang terdapat di kontrak. Dapat dipahami jika untuk wilayah yang sulit nilai Rp 40 juta mungkin tidak akan menutupi biaya, jika pelayanan yang baik disediakan. Kondisi ini dapat dikompensasi dari LKM yang jaraknya kurang dari 10 km dari kantor bank. Tambahan biaya dapat dikompensasi dengan fee yang rendah untuk kabupaten/kota kecil. Hanya LKM dan Pokja kabupaten/kota yang dapat memberikan penilaian, apakah bank memenuhi kawajiban seperti yang terdapat dalam kontrak. Pembayaran fee hanya dapat diberikan kepada bank, jika Pokja kabupaten/kota dan KSP/USP dan LKM memberikan persetujuan.

Berbeda dengan fasilitator dan KSP/USP dan LKM, bank di kabupaten/kota tidak dipilih tetapi ditunjuk. Petugas bank memperoleh beban tambahan tanpa menerima penghargaan (dan mungkin memperoleh sanksi), dimana mulai dapat diperkenalkan untuk memisahkan fee yang diterima bank dan langsung diberikan kepada pegawai bank yang melakukan kunjungan kepada LKM. Kemungkinan lain untuk mengatasi permasalahan yang ada adalah mengundang (atau melakukan tender) bank lain dalam wilayah kabupaten/kota untuk berpartisipasi.

Tim mengusulkan untuk memberikan pelatihan kepada petugas bank yang akan ikut serta dalam program dana bergulit

Rekomendasi untuk penentuan kelembagaan Direkomendasikan dalam masa yang akan datang, seluruh kredit program pemerintah yang akan disalurkan kepada lembaga keuangan kecil agar mengikutsertakan PT. Permodalan Nasional Madani (PNM) dalam rangka memberikan pengalaman dan keahlian. Tingkat keikutsertaannya dapat berubah untuk setiap kasus.

ADB SME DEVELOPMENTTA

2

1 BACKGROUND

In October 2000, the Government of Indonesia introduced a program called "Strengthening Savings and Credit Cooperatives, Savings and Credit Units of Cooperatives and Micro Finance Institutions Assisted with a Revolving Fund from Fuel Subsidies." The program is not a genuine Government credit program.

Throughout the various documents, the term "credit" is deliberately avoided. The revolving fund (RF) is made available to strengthen selected non-bank microfinance institutions (MFIs1) all over Indonesia. The MFIs shall achieve a level of professionalism, and income, that enables them to continuously lend to low income people in their community. If these MFIs can perform satisfactory over a three-year period the Revolving Fund will remain to be revolved within the MFI. Otherwise, the fund shall be made available or "revolved" to other MFIs.

1.1 Fuel Prices and Policies

This program was meant as an anticipation of an October 2000 fuel price increase. The Government of Indonesia, an OPEC member, owns the oil company Pertamina and the wholesale distribution network. Traditionally, the nationwide fixed retail prices for several types of fuel, in particular kerosene, diesel, and, until the mid-90s, gasoline, were subsidized. Indonesia imported these products because demand exceeded the national refinery capacity. Local prices did not immediately follow movements on world markets for crude oil, fuel and currencies. From December 1998 until September 2000, crude oil prices increased about 220% (in $ terms). Since July 1997, the $-exchange rate for the Indonesian Rupiah slipped from 2,400 to 11,5002. Mathematically, this would have justified nearly a 6.7-fold fuel price increase for the period July 1997 - September 2000.3 The decent October 2000 increase of about 15% for oil products reduced subsidies. Indonesian consumers still pay a fraction of prices people pay in neighboring countries.

Figure 1: Price Developments for gasoline, exchange rate, and price of crude oil

Year Gasoline price/liter

$ exchange rate

$/barrel $c/ liter

Remarks

1980 Rp 100 Rp 625 30 16,0 1997, June Rp 700 Rp 2,400 18 29,2 Start of crisis 1998, May Rp 1,200 Rp 6,000 13 20,0 fuel price increase triggers riots 1998, June Rp 1,000 Rp 15,000 12 6,7 Habibie succeeds Pres. Suharto 1999, October Rp 1,000 Rp 7,000 13 14,3 President Abdurrahman Wahid 2000, October Rp 1,150 Rp 8,900 32 12,8 fuel price increase 2001, June Rp 1,450 Rp 11,500 Feb: 26 12,6 fuel price increase 2001, July Rp 1,450 Rp 9,800 14,8 President Megawati 2001, August Rp 1,450 Rp 8,450 17,2

1 In this report Cooperatives engaged in financial services are regarded as MFIs.

2 The exchange rate for the Indonesian Rupiah is quite volatile in both directions allowing daily moves of more than 5%. During the past 12 months, one US$ bought between Rp 8,500 and Rp 12,000.

3 In June 1997, the Indonesian crude oil price (ICP) was $ 17.9/barrel

ADB SME DEVELOPMENTTA

3

1.1.1 Government Programs From Reduced Fuel Subsidy Fuel subsidy increased as a result of constant rupiah prices for fuel in the wake of higher prices for crude oil and the de-fakto devaluation. Based on an Letter of Intent with IMF, Indonesia agreed to reduce the ballooning burden and increase domestic fuel prices.

Figure 2: Fuel subsidy from FY 91/92 – FY 2001

Subsidy Rp billion

Subsidy $ billion

Fiscal Year

930 467 FY 91/92 March 692 336 FY 92/93 March 1,280 607 FY 93/94 March 687 312 FY 94/95 March 0 0 FY 95/96 March 1,416 594 FY 96/97 March 9,814 2,111 FY 97/98 March 28,607 3,565 FY 98/99 March 40,923 5,764 FY 99/00 March 51,135 5,329 2000 April-Dec (9 months) 41,304 4,303 2001 Budget (Rp/$: 9,600)

To soften the people's burden, the Government allocated "from reduced subsidies" Rp 800 billion (about $ 90 million)4 to three programs aimed at supporting the lower income strata:

individual Rp 30,000 (about $3.3) cash transfers to poor households to compensate for the fuel price increase for three months

community empowerment programs generating employment opportunities by supporting infrastructure projects (PPM Prasarana)

revolving funds to support the development of savings and credit activities of cooperatives and community groups in their effort to enhance the activities of small business people, farmers, fisherfolk, craftsmen and other low-income groups through micro loans

The figures in the table below show that cash transfers to compensate for increased fuel prices have reached many people (about 15% of the population) although the financial impact was probably very short lasting. It arrived however at an extremely strategic moment, namely before the Hari Raya Idul Fitri holidays (27/28 December). The community employment program could have engaged about 700,000 persons (or about 5% of the families living outside Java) for one month. Advantages from improved infrastructure may last for several years depending on availability of funds for maintenance. The impact of the revolving fund, being constantly monitored, may also last for years to come depending on the fund's management, its supervision and operation. Borrowers, through their interest payments, finance the MFIs' maintenance costs and even allow the institution, the fund, and its positive impact to grow.

4 This is less than 2% of fuel subsidies. The Rp 0.8 trillion program compares with Rp 648 trillion debt obligation to re-capitalize Bank Indonesia, state banks and commercial banks.

ADB SME DEVELOPMENTTA

4

Figure 3: Three types of compensation regarding reduced fuel subsidies

Measure Amount Beneficiaries

Cash transfer (about $3.3 per beneficiary)

Rp 200 billion 6.7 million recipients

(47% of poor families)

Community employment and infrastructure program

Rp 250 billion 14.7 million working days (equivalent to 58,800 man-years at 250 days/year)

in 5,097 villages (out of more than 60,000 in all Indonesia) in 250 sub-districts, 55 districts, 15 provinces (outside Java only)

Revolving fund for MFIs

max. individual loan to member: Rp 1 million ($110)

Rp 350 billion more than 350,000 small entrepreneurs (out of about 40 million)

through strengthening microfinance institutions (MFI), the "participants":

- 2,925 savings and credit cooperatives

- 1,000 informal financial institutions

(savings and credit self-help groups, SHG)

341 districts, 26 provinces

Proposal for 2001

Revolving fund Rp 56.3 billion 50,000 small entrepreneurs

- 1,000 MFIs

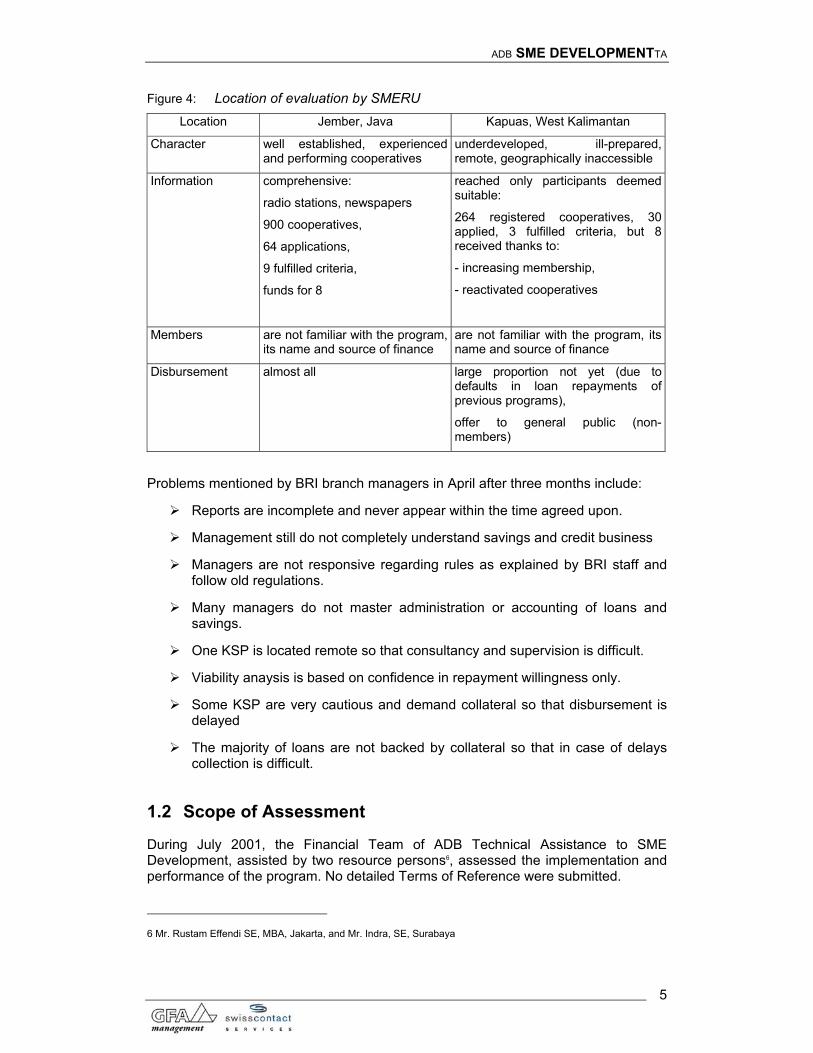

1.1.2 Observations of Other Parties An early evaluation, executed in February 2001 by SMERU5, hinted to that the cash subsidy program might have given many poor people a relief, in particular as the money was disbursed before Hari Raya Idul Fitri. The timing for the infrastructure program was considered less appropriate as people are busy and can generate alternative income throughout the fasting month. The business loans for small entrepreneurs were mostly disbursed after Hari Raya in order to prevent diversion to consumptive use.

5 The SMERU Research Institute, No 02: Mar-Apr/2001, Spotlight On; www.smeru.or.id/newslt/ed14/spot14.htm

ADB SME DEVELOPMENTTA

5

Figure 4: Location of evaluation by SMERU

Location Jember, Java Kapuas, West Kalimantan

Character well established, experienced and performing cooperatives

underdeveloped, ill-prepared, remote, geographically inaccessible

Information comprehensive:

radio stations, newspapers

900 cooperatives,

64 applications,

9 fulfilled criteria,

funds for 8

reached only participants deemed suitable:

264 registered cooperatives, 30 applied, 3 fulfilled criteria, but 8 received thanks to:

- increasing membership,

- reactivated cooperatives

Members are not familiar with the program, its name and source of finance

are not familiar with the program, its name and source of finance

Disbursement almost all large proportion not yet (due to defaults in loan repayments of previous programs),

offer to general public (non-members)

Problems mentioned by BRI branch managers in April after three months include:

Reports are incomplete and never appear within the time agreed upon.

Management still do not completely understand savings and credit business

Managers are not responsive regarding rules as explained by BRI staff and follow old regulations.

Many managers do not master administration or accounting of loans and savings.

One KSP is located remote so that consultancy and supervision is difficult.

Viability anaysis is based on confidence in repayment willingness only.

Some KSP are very cautious and demand collateral so that disbursement is delayed

The majority of loans are not backed by collateral so that in case of delays collection is difficult.

1.2 Scope of Assessment

During July 2001, the Financial Team of ADB Technical Assistance to SME Development, assisted by two resource persons6, assessed the implementation and performance of the program. No detailed Terms of Reference were submitted.

6 Mr. Rustam Effendi SE, MBA, Jakarta, and Mr. Indra, SE, Surabaya

ADB SME DEVELOPMENTTA

6

More than six months after release of the RF to the MFIs, the Team interviewed stakeholders in 7 provinces on four islands:

2 Jakarta-located headquarters of banks with a nationwide branch network, namely BRI and BNI, both together overseeing nearly two thirds of the scheme's participants

3 headquarters of Provincial Development Banks

8 bank branches keeping accounts of the participating MFIs

6 district Offices of Cooperatives and SME (OCSME), as representatives of the District Working Groups (WG)

8 single-purpose credit and savings cooperatives, including two BMT

6 multi-purpose cooperatives with an autoomous savings and credit unit

7 non-registered savings and credit cooperatives

7 facilitators

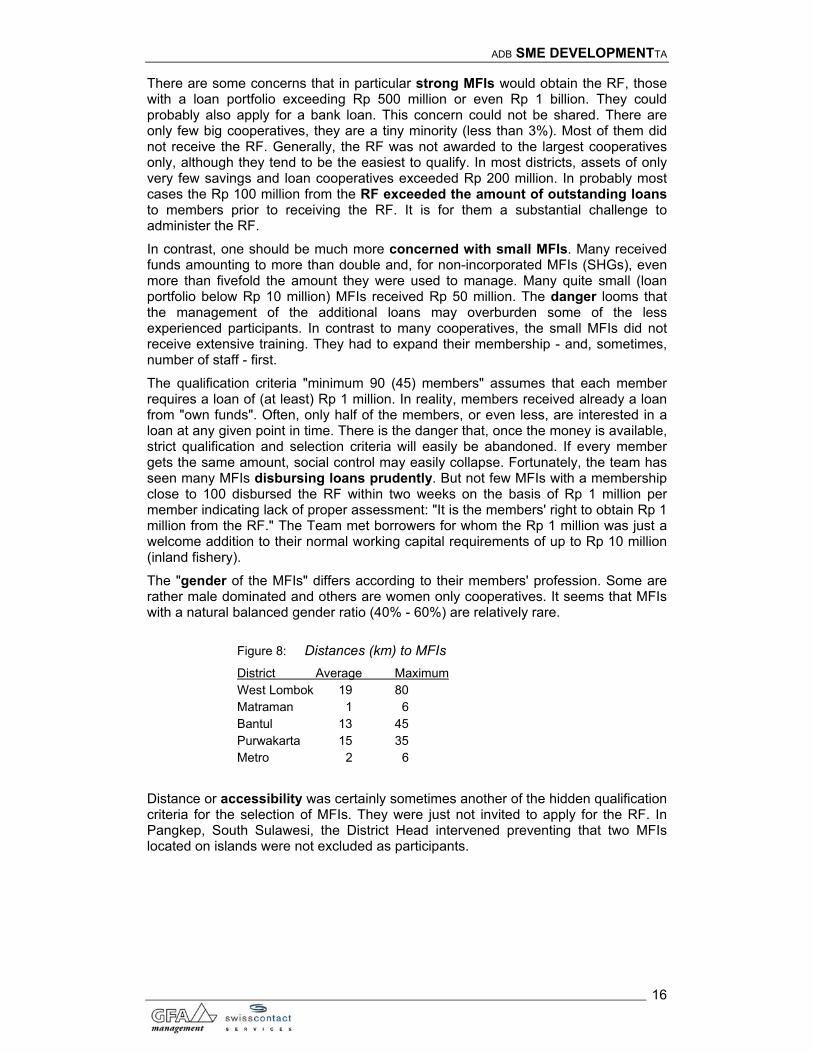

Figure 5: Location of the survey

Location Jakarta Lampung West Java NTB Yogya-

karta South

Sulawesi East Java

Institution Kota Metro

Lampung Tengah

Purwakarta

Lombok Barat

Kota Mataram

Bantul Pangkep Sidoarjo

Dinas Koperasi 1 1 1 1 1 1

Facilitator 1 1 1 1 1 1 1

Bank HQ Jakarta

BRI

BNI

HQ BPD 1 1 1

Branch BNI BPD BRI BPD BPD BPD BRI Bukopin

KSP 3 1 1 1 1 1

USP-Kop 2 2 1 1

LKM 1 1 1 2 1 1

Those few districts the team visited are, if compared to the national average, areas with high population density. The development of the program might differ in districts that have difficult access and few suitable MFIs applying to take part in the scheme. The Team was committed to submit results within three weeks and could therefore not embark on exhilarating boat trips through the forests of Kalimantan. The Team met with few of the final RF recipients, the low-income population, as the attention focused on strengthening MFIs (see Annex Itinerary).

ADB SME DEVELOPMENTTA

7

2 THE PROGRAM

2.1 The Environment and Problems Identified Before Program Implementation

The Office of the State Ministry of Cooperatives and Small Medium Enterprises (SMOCSME) is the program's designer and promoter. The design is based on vast experience with other programs to support the low-income people, including other micro and small credit schemes:

Cash subsidies and time-limited employment opportunities help people only for a very short period to cover additional expenses for fuel and transport. The higher income is not sustainable.

Small entrepreneurs, including farmers, can sustainably increase their income. They need working capital that banks, for many acceptable reasons, do not or cannot make available.

Several thousand MFIs in Indonesia, rooted in the local community, try to complement where banks do not offer services. They lack working capital and qualified management.

Small entrepreneurs are reliable borrowers unless it concerns a Government "credit" program. Reward and punishment features, loan conditions set by the MFI and not the Government, steady supervision from a respected agency (commercial banks) and independent audits introduced from the very beginning shall underline the different approach compared to previous schemes.

The Government agencies have limited capacity to professionally assist MFI management and to monitor MFIs and their funds. Banks, whose professional task it is to handle loans, are the most suitable and experienced institution to do so.

Besides the professional aspects, namely the financial part, MFIs would need to have a person "translating" between the Government and the banks on the one hand, and the MFIs and their members on the other hand. Small MFIs are community based. Therefore, a community development advisor experienced with savings and credit activities should back the revolving fund scheme.

Small entrepreneurs or MFIs dislike paying for services the banks, facilitators and auditors have to render (BDS) although they could afford paying for them.

ADB SME DEVELOPMENTTA

8

2.2 Description and Implementation of the Program

For more information on objectives and indicators see Annex 2.

Having in mind this background, the Government allocated Rp 350 billion7 to be channeled as a 3-year revolving fund (RF) through

2,925 MFIs being incorporated as a cooperative; they received each Rp 100 million ($11,000) to be channeled as micro loans to at least 90 members

1,000 non-incorporated MFIs or SHGs; they received each Rp 50 million for at least 45 borrowers

in 341 districts in Indonesia.

The program has a distinct regional component. Independent from the number of people, the size of the district, or number of registered cooperatives and other MFIs, each district received about Rp 1 billion for a certain number of incorporated cooperatives and other MFIs. The diversity of the regions results in particular challenges:

uneven quality of participants between and within regions

remote location of MFIs making supervision by banks and control by other agencies difficult

limited experience of bank officers with cooperatives and microfinance institutions

A 3- to 4-month preparation and socialization phase started in September 2000. The Revolving Fund (RF) was released to the Handling Banks8 in December. In nearly all districts that the Team visited, it was common that the MFIs withdraw the RF in January 2001, after the Hari Raya Idul Fitri festivities.

On October 9, 2000, SMOCSME issued the Technical Guide for the implementation of the RF program. This paper explains

the composition, tasks and responsibilities of Working Groups on Central, Provincial and District level

criteria for the selection of a facilitator

criteria for the selection of participating MFIs

criteria for MFI members for receiving a loan from the RF

tasks of Handling Banks

operating the RF

The Technical Guide avoids the term "credit" and uses the term "Revolving Fund Assistance" ("bantuan dana bergulir").

End of October 2000, SMOCSME concluded contracts with Handling Banks, the "crucial partner" (Deswandhy, Deputy Minister SMOCSME), on channeling the RF and on other services for which they receive a 4% p.a. fee payable by the MFIs for 7 This compares with much more than Rp 400,000 billion the government had to spent to bail out the commercial banks (re-capitalization) or Rp 70,000 billion the government has budgeted for interest payment of bonds.

8 The Indonesian term "Bank Pelaksana", used in the Technical Guide, is normally used for Government credit programs in which the bank has full authority to select clients, and bank take over the repayment risk.

ADB SME DEVELOPMENTTA

9

three years based on the amount the banks channeled to the MFIs. In order to achieve scale, one bank branch handles all MFIs in one district. This branch can earn about Rp 32 to Rp 40 million (about $3,500 - $4,500) annually from monitoring the RF and related tasks. BRI, due to its extensive network, received an allocation for about 50% of the 341 districts.

On October 18, SMOCSME issued a decree stipulating the number and type (cooperative or SHG) of MFIs in each district to be selected as RF recipients.

The SMOCSME concluded a contract with Bank Bukopin on training facilitators. This bank is affiliated to the cooperative movement and acknowledged for their capacity and qualification to train MFI people. Together with multi-purpose cooperatives, Bank Bukopin established and manages several hundred MFIs.

The Provincial Working Groups, having only coordinative tasks, organized efficiently the socialization of the program. People from Jakarta presented the RF to representatives of the District Governments.

The District Working Groups (WG) were the backbone of the program during its initial phase. The Bupati (District Head) has been appointed as its chairman, the Head of the Office of Cooperatives and Small Medium Enterprises (OCSME, Dinas Koperasi) is in charge of the routine work. About seven to ten9 WG members represent other Government agencies and the Handling Bank, they include non-formal community leaders, scholars, and NGO-activist. These WGs fulfilled the task to select the facilitator (October) and the MFIs (November).

The WGs announced the availability of the RF (radio, newspapers, direct visits to MFIs) and asked interested MFIs to apply and submit a proposal for the utilization of the RF. Teams were sent to the MFIs to verify the data they submitted in their applications. Based on a catalogue of criteria, the WGs finally awarded the RF to those MFIs that achieved the highest score in their category.

The WGs concluded "cooperation agreements" with the Handling Bank on reporting an on training MFI staff, and with the MFIs on the utilization of the fund. Thus, the assumed capacity of banks to train, advise and supervise the MFIs, and the Government's and other party's commitment to support the low-income strata of the population were combined. The WGs ordered the transfer of the money.

In December 2000 the MFIs opened savings accounts with the Hankdling Bank.

They signed a document (Berita Acara) taking over the responsibility to utilize the fund according to the program's specifications, the prerequisite for money transfer from the Government's account directly to the MFIs' bank accounts. This transparent procedure should make "side streaming" difficult.

2.3 Financial and Contractual Issues

The MFIs could withdraw their allocation of the RF from the bank account whenever they wanted to do so. The main obligation was disbursement of the RF to small entrepreneurs among their members. The maximum individual loan amount to their borrowers should not exceed Rp 1 million ($ 110). The program allows that up to 10% of the fund or Rp 10 million (respectively Rp 5 million) can be used by the MFIs for investment, e.g., premises and equipment. The MFIs have to pay quarterly (some few pay monthly) a 4% "interest/fee" to the Handling Banks. The banks keep 1% as

9 According to the Technical Guide: not more than eight members! Reason is that the budget from Central Government allowed financing only eight people.

ADB SME DEVELOPMENTTA

10

their handling fee, 2.5% are added to the MFI's blocked "liquidity reserve", and 0.5% are allocated to cover costs of audit, facilitator, advice and guidance

Figure 6: Utilization of fee per annum

Cooperative MFI Non-Cooperative MFI (SHG)Payments by % p.a.quarterly annually quarterly annually

Handling fee for bank 4% Rp 1.0 mio. Rp 4.0 mio. Rp 0.50 mio. Rp 2.0 mio. Liquidity reserve "blocked savings"

10% Rp 2.5 mio. Rp 10.0 mio. Rp 1.25 mio. Rp 5.0 mio.

Allocation for audit, facilitator, training

2% Rp 0.5 mio. Rp 2.0 mio. Rp 0.25 mio. Rp 1.0 mio.

Total 16% Rp 4.0 mio. Rp 16.0 mio. Rp 2.00 mio. Rp 8.0 mio.

The survey included two BMTs. One of these MFIs following strict syariah banking rules pays 60% of the profit10, another one does not regard the payment to be interest but "fee".

The MFIs are allowed to withdraw the "liquidity reserve" depending on a positive result of the annual performance evaluation. The release of the "liquidity reserve" is regarded as a short-term incentive for MFIs to perform.

Another obligation of the MFIs is separate accounting for the RF utilization in order to allow easy monitoring. Therefore, members know whether their loan origins from the MFI's "own" resources or from the RF. However, according to the Technical Guide, MFIs shall not apply different loan conditions.

The following contracts govern the rights and obligations of the parties involved in the channeling of the RF: 1. SMOCSME - Handling Banks, headquarters 2. WG - Handling Bank, branch office11 3. WG - MFI 4. WG - Facilitator (Appointment, a kind of contract) 5. MFI - Handling Bank, branch office 6. MFI - Member, individual debtor (credit contract) 7. Treasurer OCSME - MFI (conditions for release of RF from KPKN to the

participants' accounts) According to the Technical Guide, after three years, December 2003, depending on the evaluation of RF performance and institutional fitness appraisal, MFIs may continue to revolve the RF. However, contracts between WGs and MFIs differ. Some even stipulate the repayment of the RF first before any further decision is made.

10 This payment was Rp 3.7 million in the first quarter and Rp 4.2 million in the second quarter and will still increase in the third quarter.

11 It is regarded problematic that the Handling Bank as a member of the WG is in a way concluding a contract with itself.

ADB SME DEVELOPMENTTA

11

3 IMPLEMENTATION: FINDINGS AND ASSESSMENT

The institutional setup is ambitious, in particular during the program's 3-4 months inception phase. Overall, no really serious problems like delays that would have prevented disbursements, gross misallocation, unqualified MFIs or facilitators were met neither could the team identify any.

The implementation, the disbursement of funds, had to be finalized within a short period. The funds had to be channeled to the MFIs' accounts until end of December 2000, the end of the budget year. This target was achieved. The Technical Guide was released in the second week of October 2000 and in less than two months the selection processes took place and funds started to be transferred. Several of the shortcomings can be explained with this time pressure. Fortunately, these shortcomings are still relatively easy to reverse.

3.1 The RF Concept

The scheme or the concept of the RF is convincing and nearly excellent.

Many features that commonly apply to a successful small- or micro-scale credit program characterize it. For example:

The program is not too demanding and it is not loaded with incompatible objectives.