10 case studies compensation summary - cedr · 1 reference case study name 1subject compensation...

TRANSCRIPT

1

Reference

Case Study name Subject1 Compensation £0.00

Compensation to £100.00

2011 Bill shock

Customer was shocked by a bill for £2,975.00 for use of 3G services to down load data whilst on holiday. She acknowledged her son used the phone whilst the family were on holiday and that she had received a warning about the high charges being incurred. The company highlighted information on charges, setting up the 3G phone and warning services they provided. Found. Company’s evidence about all the information they provided, particularly about setting up the 3G device, was compelling. Customer’s claim to be released from an obligation to pay the charges failed.

0.00

2011

Bill shock

Customer ran up a bill of £4,000.00 for data roaming in Egypt. He said that he had never authorised international roaming and the charges were exorbitant, especially as much of the activity had been 'unintentional'. The EU regulations on roaming applied so the charges should be capped. The company maintained that the Customer did authorise it, he had been charged for and paid for international roaming at the same rates on an earlier trip abroad (Columbia), the charges applied were the company's published charges, The customer was responsible for the phone settings (e.g. checking emails and social networking sites) responsible for 'unintentional' roaming and there were warnings about the costs of data roaming in the User Guide and on the iPhone when the roaming facility was turned to 'on'. Found. The charges formed part of the contract price for the available services. Roaming regulations did not apply to roaming in Egypt. The customer had authorised international roaming and the company had provided adequate warnings.

0.00

2011 Bill shock

Customer incurred extremely high charges for accessing data whilst in Turkey which she wished to have reduced or set aside. She maintained that she did not enable data roaming on her handset, she was never informed of the rates for data roaming charges and she did not use her phone to any greater extent than normal while she was in Turkey. The company asserted that the charges were correct, data roaming was automatically turned off on the customer’s handset which necessitated her actively

0.00

1 The customer is sometimes referred to as, C, and the communication and internet service provider as, T, or, ‘the company’.

The Case Studies are summaries of cases they are not the full case. They are merely a guide rather than a precedent. In each case there are circumstances which are particular to that case, which have been considered and have lead to a particular Decision being made by the Adjudicator.

Issue 10

March 2014

Case Studies Compensation Summary

2

Reference

Case Study name Subject1 Compensation £0.00

turning it on, and that the rates for data roaming are clearly set out in its pricing literature.

Found. Customer’s claim failed. She was liable to pay the data roaming charges incurred on her account because the charges for data roaming in Turkey were made clear to the customer when she entered into the contract with the company. The customer actively turned on data roaming on her handset in spite of warnings about the high rate of data roaming charges she would incur. She admitted to having used data whilst in Turkey, and the bills confirmed the extent to which the customer used data whilst she was abroad.

2011 Bill shock

Customer had his phone stolen from his boat in Antigua while he was away. In 10 days a huge bill was run up. The company received reports of unusual activity on the phone and blocked the account, but by then it was too late. The customer said it was the company’s negligence for not detecting the unusual activity and the bill should be reduced to zero. The company maintained the customer should have protected his SIM by a password. Found. While things might be different in EU as a result of the roaming regulation, or because of extenuating circumstances (such as where C was unable for reasons beyond his control to contact T), there were no facts indicating why the customer should not pay. The adjudicator recommended that the company abide by its offer of a 50% reduction in the bill.

0.00

2011 Bill shock

Customer was shocked to receive a bill for more than £250.00 in one month and believed that he was being incorrectly charged for calls to particular mobile numbers. The company asserted it had correctly charged the customer and that its pricing guide stated the mobile numbers called were not charged as UK mobile calls. Found. The customer’s claim was unsuccessful as the company had neither breached any term of its agreement with the customer nor failed in the duty of care it owed to him.

0.00

2011 Bill shock

Customer's SIM card had been stolen whilst he was in Ghana on a business trip although the customer was unaware of the theft as he used a different international SIM card during his trip. He was shocked to receive a bill in the region of £1,000.00. The customer argued that the company should bear the cost of the fraudulent calls as it failed to block his SIM card after the first few fraudulent calls were made and had allowed charges to escalate. The company asserted the contract clearly stated that the customer was responsible for the safe keeping of the SIM card so C should be liable for call charges incurred on his account up to the point the account had been suspended due to high international usage. Found. The customer failed to report the SIM card had been stolen. There were no extenuating circumstances which warranted the terms of the contract being set aside. The contract made the customer liable for the charges incurred on his account, despite the unfortunate circumstances of the case. It was recommended that the company abide by its offer to reduce the charges by £200.00 and arrange a payment plan to allow the customer to pay off the balance in instalments.

0.00

2011 Bill shock

Customer and her husband went on holiday to America. Upon their return they received a bill for £2,970.00 which arose mainly from data charges which were applied through the use of her husband’s iPhone. The customer maintained that her husband did not use his iPhone, in any event the company should have placed a bar on the account and the iPhone should not be able to automatically connect to the Internet when it was not being used. Found. The customer’s claim was dismissed. The evidence identified that the SIM card within the iPhone had made the data connections. As a consequence the charges were properly applied. There were sufficient information and warnings given by the company about the potential for such charges to arise.

0.00

2011 Bill shock Customer wanted company to refund about £1,200.00 on the basis that the company had wrongly charged the customer’s account and had not followed the customer's request (made through an agent) to remove iPhone data bundles from a number of

0.00

3

Reference

Case Study name Subject1 Compensation £0.00

mobile phones. The company’s account note recorded at the time of the request was different to that which the customer thought had been requested. Found. The company had simply acted on an instruction relayed to it by the customer’s agent. The customer had failed to establish an error by the company. The onus was on the customer to produce the written instruction given to the company. Having failed to do so and in the light of an admission by the customer that in any event the company would have calculated data charges correctly in line with its current price guide, there was no basis for the customer seeking a refund.

2011 Bill shock

Customer claimed that the company had wrongly billed her £200.00 for calls not made by her household including calls to India and Italy. The company argued that the bill was correct as it had carried out diagnostic tests and found no fault or mistake. Found. The customer had provided no evidence to support the claim. The tests carried out by the company showed that the calls

were made from the customer's landline. Under the terms of the contract the customer was responsible for calls made using her

landline with or without her knowledge. The claim failed.

0.00

2011 Bill shock

Customer was shocked to receive an exceptionally high bill after he had returned from holiday in Pakistan. Before travelling, he had contacted the company about roaming charges and mobile internet charges. In Pakistan the customer tried his best not to use the facility and disconnected the mobile internet because where he was staying had free broadband. He believed that the amounts he had been charged by the company were incorrect and excessive. The company pointed out that switching off data roaming was something which would be done by the customer. The company provided a number of offers and services in connection with using data roaming when abroad. It also sends a text message when the phone is first connected to a foreign network giving details of costs. It sends additional messages to its customers should they continue to use data. Found. The customer’s claim failed. The company had correctly calculated the bill and had acted in accordance with the terms and conditions of the contract.

0.00

2011 Price plan

Customer contracted a phone and broadband service from the company but her recollection of the price plan differed from that of the company’s. She contended that monthly bills did not reflect her recollection of the plan and the bills should be reduced by £200.00. The company contended that the bills were correct. Found. The price plan described by the company was more advantageous to the customer than her recollection. Bills conformed to the price plan. However, the company had not responded very well to the customer's complaints and questions. There was a breach of the duty of care and nominal compensation was awarded for inconvenience.

25.00

2011 Bill shock

The customer used premium rate multimedia services which he thought were included in his package and ran up a bill of £814.59 in a month. The company had offered to reduce the charges to £250.00 and give the customer 6 months to pay in instalments at £140.00 per month. The customer did not agree as he could not afford this amount although the company had informed a debt collection agency that the customer had agreed and it applied a termination charge of £479.96. The customer contended that he had received poor customer service. Found. The company had been in breach of its duty of care to provide a reasonable customer service. £40.00 compensation was awarded reducing the bill to (£814.59-£40.00) £774.59. As the entire contract value was (£35.00 per month x 24 months) £840.00 and C had almost reached this in charges of £814.59, applying a termination charge of £479.96 was excessive so the termination charge should be waived. C should pay off the balance in instalments: £61.59 followed by 23 monthly payments of £31.00. Upon receipt of the first payment of £61.59, T should remove the account from the debt collection agency and reset C’s credit file default.

40.00

10:08 Overcharging C overcharged and suffered inconvenience because T delayed cancelling service. 50.00

4

Reference

Case Study name Subject1 Compensation £0.00

Found. T had not provided reasonable customer service. T apologised and explained a mistake had been made.

18:04 What was agreed? The customer complained that he had negotiated with the company for the supply of a package which included high definition television channels for £76.50 per month but after installation had taken place the channels were not received. The company maintained that the HD channels were not part of the package. The customer claimed compensation of £50.00 together with the provision of the HD channels. Found. The customer had provided clear evidence that the provision of the HD channels had been agreed between the customer and the company. Consequently the company were obliged to provide those channels as part of the customer’s package and pay £50.00 compensation to the customer for the frustration and inconvenience it had caused him.

50.00

18:11 Faulty equipment The customer complained that a handset provided by the company had developed a fault but the company had not responded to his complaint. The company maintained that as the faulty equipment was out of scope of CISAS the customer's complaint should not be considered by CISAS. Found. Whilst the customer's complaint about the faulty handset fell outside the scope of CISAS, however, the complaint about the way in which the company dealt with his complaint was within scope. The customer had submitted a copy of an acknowledgement letter that he had received from the company stating that it would send him a response once it had looked into his complaint. The company did not provide the customer with the promised response.

50.00

05:13 Dispute over £3 C upgraded to broadband service from dial up service which T continued to charge for. Found. T had not properly explained its services and not provided CISAS reference number. Dispute over £3.00. C should bear some responsibility for pursuing such small sum and not acting sooner to stop the double charging.

55.00

19:11 Cold calling a vulnerable customer

The customer (who was 85 years of age and suffered from hearing loss, sight impairment and had a heart problem) received a cold call from the company offering a reduced call package. She outlined her condition and age during the initial sales call but was confused about the identity of the company. The customer complained that the company employed aggressive sales tactics. She had attempted six times to cancel the agreement but the company would only accept cancellation once the customer was outside of the cooling off period and charged an early cancellation fee. Found. The company’s call recordings were useful: during the calls the company explained that it was not, “BT”,

also the customer repeatedly called within the cooling off period to cancel. The tone of the calls to an obviously vulnerable customer was unacceptable. A company’s duty of care is of the utmost importance when dealing with clearly vulnerable customers. The Adjudicator found that the company was in breach of its duty of care and contractual obligations by failing to accept the customer’s first cancellation request. The company was directed to remove all early cancellation fees, pay compensation of £57.00 and apologise to the customer for its poor customer service.

57.00

11:06 Television service C was without broadband and television for six weeks. CISAS not normally consider complaints about television services but T agreed to use the scheme. C claimed compensation of more than £1,700.00 calculated at his hourly business rate. Found. C had suffered frustration by T’s breach of duty of care to provide reasonable customer service. Not appropriate to use C’s business rates to calculate compensation for a domestic service.

60.00

17:08 Conflicting evidence C complained that her broadband speed was very slow and as a consequence she decided to transfer to another service 70.00

5

Reference

Case Study name Subject1 Compensation £0.00

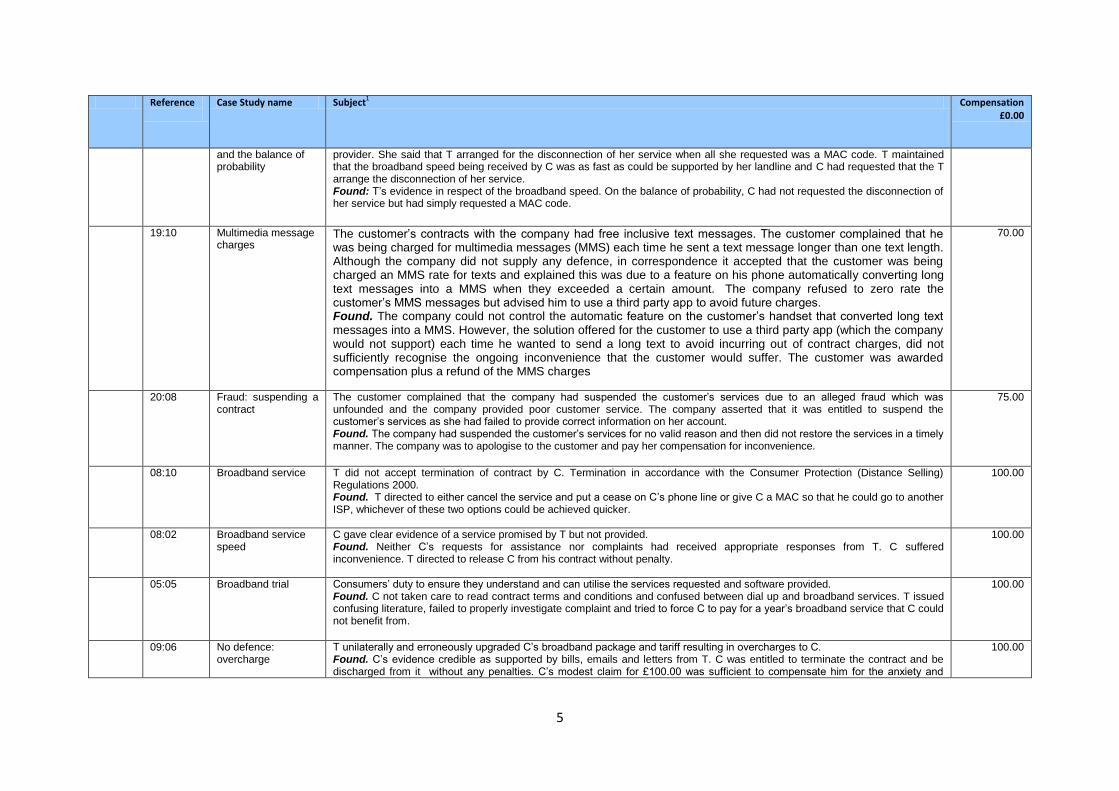

and the balance of probability

provider. She said that T arranged for the disconnection of her service when all she requested was a MAC code. T maintained that the broadband speed being received by C was as fast as could be supported by her landline and C had requested that the T arrange the disconnection of her service. Found: T’s evidence in respect of the broadband speed. On the balance of probability, C had not requested the disconnection of her service but had simply requested a MAC code.

19:10 Multimedia message

charges The customer’s contracts with the company had free inclusive text messages. The customer complained that he was being charged for multimedia messages (MMS) each time he sent a text message longer than one text length. Although the company did not supply any defence, in correspondence it accepted that the customer was being charged an MMS rate for texts and explained this was due to a feature on his phone automatically converting long text messages into a MMS when they exceeded a certain amount. The company refused to zero rate the customer’s MMS messages but advised him to use a third party app to avoid future charges. Found. The company could not control the automatic feature on the customer’s handset that converted long text messages into a MMS. However, the solution offered for the customer to use a third party app (which the company would not support) each time he wanted to send a long text to avoid incurring out of contract charges, did not sufficiently recognise the ongoing inconvenience that the customer would suffer. The customer was awarded compensation plus a refund of the MMS charges

70.00

20:08 Fraud: suspending a contract

The customer complained that the company had suspended the customer’s services due to an alleged fraud which was unfounded and the company provided poor customer service. The company asserted that it was entitled to suspend the customer’s services as she had failed to provide correct information on her account. Found. The company had suspended the customer’s services for no valid reason and then did not restore the services in a timely manner. The company was to apologise to the customer and pay her compensation for inconvenience.

75.00

08:10 Broadband service T did not accept termination of contract by C. Termination in accordance with the Consumer Protection (Distance Selling) Regulations 2000. Found. T directed to either cancel the service and put a cease on C’s phone line or give C a MAC so that he could go to another ISP, whichever of these two options could be achieved quicker.

100.00

08:02 Broadband service speed

C gave clear evidence of a service promised by T but not provided. Found. Neither C’s requests for assistance nor complaints had received appropriate responses from T. C suffered inconvenience. T directed to release C from his contract without penalty.

100.00

05:05 Broadband trial Consumers’ duty to ensure they understand and can utilise the services requested and software provided. Found. C not taken care to read contract terms and conditions and confused between dial up and broadband services. T issued confusing literature, failed to properly investigate complaint and tried to force C to pay for a year’s broadband service that C could not benefit from.

100.00

09:06 No defence: overcharge

T unilaterally and erroneously upgraded C’s broadband package and tariff resulting in overcharges to C. Found. C’s evidence credible as supported by bills, emails and letters from T. C was entitled to terminate the contract and be discharged from it without any penalties. C’s modest claim for £100.00 was sufficient to compensate him for the anxiety and

100.00

6

Reference

Case Study name Subject1 Compensation £0.00

inconvenience he had gone through.

11.10 Charges C making many telephone calls and writing many letters but T gave poor customer service. Found. Breach of the duty of care by T to C.

100.00

17.07 Insufficient evidence

C claimed £4,000 as a result of T not putting in place a new contract. He did not notice the error until nearly five months later when he checked his bills. T admitted that it had failed to put the new agreement in place, but had recalculated the bills and applied a £50 credit to C’s account. C did not pay the balance and T disconnected the services. Found. C had not provided any build up to the £4,000 claimed or evidence of bank charges incurred, despite being requested to do so by T. C was awarded a fraction of the amount claimed as C had provided insufficient evidence.

100.00

14:02

Moving house

C cancelled broadband and telephone as he was moving house. He was due a small credit of £4.19. Nothing happened, the credit was not paid and T continued to bill for the unwanted service being provided to the old address of C. C was concerned that non-payment would lead to credit blacklisting. Found. C’s claim succeeded.

100.00

18: 05 Services charged for at new and old addresses

The customer complained that he had transferred his services to a new address but the company left the account at the customer’s old address open and continued to charge for services at the old address. The customer only realised what had happened when he found a default on his credit file. The company asserted that the customer had transferred his services to his new address but three days later he requested reconnection at his old address. The company had charged the customer correctly and the default was correct, however, it had taken action to remove the default as a goodwill gesture. Found. The company had reconnected the customer’s services at his old address in error, charged him incorrectly and then applied a default incorrectly. The Adjudicator directed the company to apologise to the customer, pay compensation and ensure that the default was removed from the customer’s credit file.

100.00

18:10 2 year default notice The customer complained that the company had placed a default on his credit file for two years which prevented him from obtaining credit. The company explained that the customer had made a previous application to CISAS which the company had agreed to settle by clearing the default from his credit file. By the time the settlement was agreed the outstanding balance on the customer’s account had been sold to a debt collection agency. It took the company several months to purchase the debt back so that it could be cancelled. Found. Although the company had agreed to clear the default from the customer’s credit file as a goodwill gesture, it caused an unreasonable delay in arranging for the debt to be purchased back and waived approximately five months after the settlement had been agreed. The customer had been caused stress and inconvenience by the company.

100.00

20:01 Compensation in exceptional circumstances although none claimed

The customer tried to send an email to the company that he was transferring his broadband and phone service to another provider but the company’s system would not recognise his email address. He also had problems phoning the company as its menus required him to submit a 9 digit account number but he had an 8 digit account number that the company’s system did recognise. The customer gave up trying to contact the company, relied on his new provider to make the transfer and received a text from the company acknowledging that he was moving. The customer complained that he had then been pestered by the company to pay arrears but how they had accrued was not explained to him, the company insisted its TV box be returned although the customer had not had a TV contract and every time he spoke to the company’s representatives he had to constantly repeat what had happened. The company’s position was that all its customers were required to give 30 days’ notice to cancel their services, a third party (such as a new provider) could not request disconnection of the company’s customer account. Found. The terms and conditions of the service agreement meant that the customer had to give the company 30 days notice to

100.00

7

Reference

Case Study name Subject1 Compensation £0.00

cancel its services although the new provider had advised the customer they would cancel all his services. However the company was required to give a reasonable level of customer service in assisting its customers, this it did not do throughout the dispute. The customer had not claimed compensation. However the circumstances were exceptional and the customer was awarded compensation for the company’s poor level of customer service.

20:02 SIM cards mix up

The customer, a pensioner, complained to the company many times about unusual amounts added to her bill for unwanted emails and maps received on a new tablet. The company replaced the tablet but the customer could not make the SIM card slot on the new tablet work properly. The company thought that the customer may have mixed up the tablet’s SIM card (for mobile broadband without inclusive texts and calls) with other mobile phone SIM cards she had and had used the wrong SIM card in the wrong device. As the customer refused to pay the £1,000.00 plus outstanding bills, the company passed them to debt collectors explaining that the itemised bills for text messages, photo messages and phone calls were accurate and had been produced from information via the customer’s tablet SIM card. Found. Issues about faulty equipment were out of scope of CISAS but also the customer had provided insufficient evidence that the new tablet was faulty. It was the responsibility of the customer how she used her SIM cards. The bills were a correct reflection of what services the customer used and she was responsible for paying them. She chose not to pay them and consequently the company could take action to recover the amount due to it. However during the course of the CISAS adjudication the customer received a letter from the company’s debt collectors threatening legal proceedings if the disputed amount was not paid within 7 days. The Adjudicator found that the company had a duty of care to the customer to act reasonably and it was responsible for the actions of its agents, the debt collectors. Those actions amounted to a breach of the company’s duty of care for which it was directed to apologise and pay compensation to the customer.

100.00

Compensation from £101.00 to £500.00

08:05 18 weeks without internet

After 18 weeks C was without a broadband service as T tried unsuccessfully to deal with connection problems but T continued to deduct a monthly subscription. C was frustrated trying to contact T to the extent that C telephoned T’s helpline at 4.30am in the morning as it was the only time she could get through. C suffered anxiety and inconvenience caused by the failings of T. Found. C’s claim succeeded.

150.00

15:02

Direct debit

C decided to terminate his services with T and move to another service provider. T disconnected his services early without authorisation, re-instated the direct debit without C’s authorisation and took two payments from his account. Found. C’s claim succeeded.

150.00

14:10

Services not transferred to new home in time

T did not transfer its telephone and broadband service to C’s new home by an agreed date. Found. C’s claim succeeded

161.49

08:12 Poor service T without C’s authorisation upgraded C’s broadband service accidentally making C’s email address inoperable. T took 76 days to restore the email service. When C phoned T to cancel the anti-spam package on the email service, T cancelled the whole account and refused to reinstate it. Found. T had not provided a reasonable service.

195.00

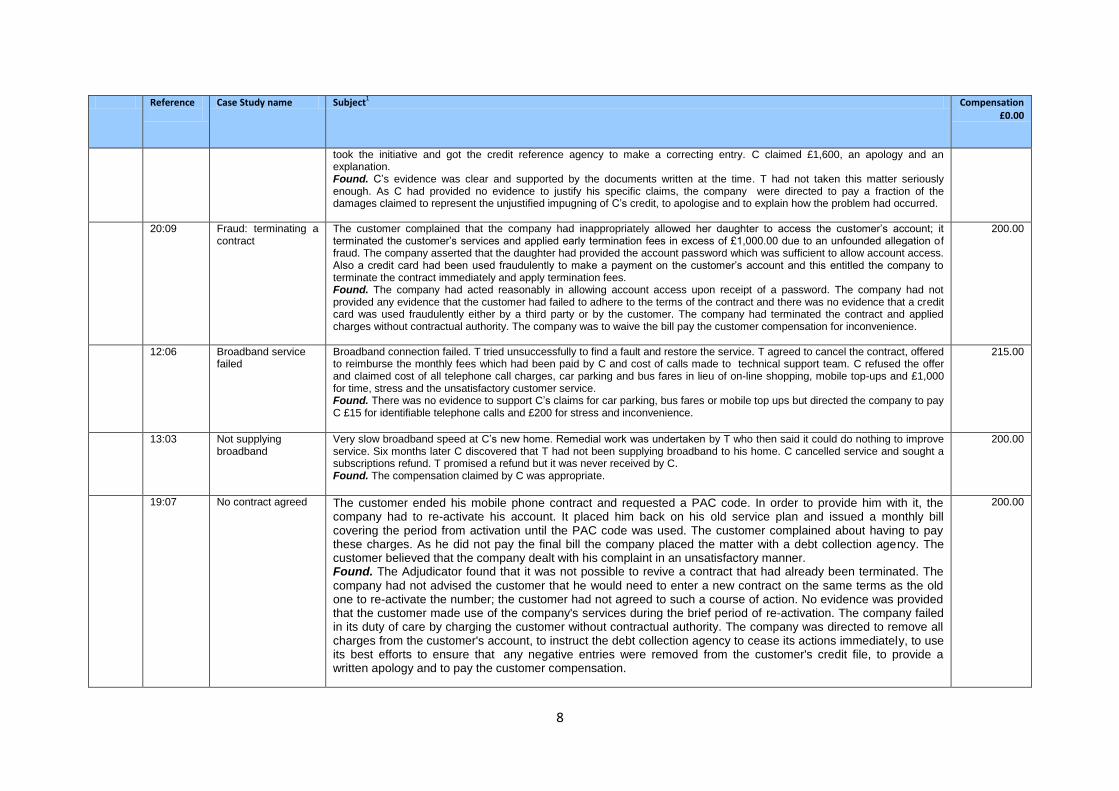

17:06 Evidence accepted C terminated a contract about two years earlier but later found that T had made an incorrect credit reference about him. T admitted this but over the course of several months did not do anything about it as they thought it was only an internal matter. C

200.00

8

Reference

Case Study name Subject1 Compensation £0.00

took the initiative and got the credit reference agency to make a correcting entry. C claimed £1,600, an apology and an explanation. Found. C’s evidence was clear and supported by the documents written at the time. T had not taken this matter seriously enough. As C had provided no evidence to justify his specific claims, the company were directed to pay a fraction of the damages claimed to represent the unjustified impugning of C’s credit, to apologise and to explain how the problem had occurred.

20:09 Fraud: terminating a contract

The customer complained that the company had inappropriately allowed her daughter to access the customer’s account; it terminated the customer’s services and applied early termination fees in excess of £1,000.00 due to an unfounded allegation of fraud. The company asserted that the daughter had provided the account password which was sufficient to allow account access. Also a credit card had been used fraudulently to make a payment on the customer’s account and this entitled the company to terminate the contract immediately and apply termination fees. Found. The company had acted reasonably in allowing account access upon receipt of a password. The company had not provided any evidence that the customer had failed to adhere to the terms of the contract and there was no evidence that a credit card was used fraudulently either by a third party or by the customer. The company had terminated the contract and applied charges without contractual authority. The company was to waive the bill pay the customer compensation for inconvenience.

200.00

12:06 Broadband service failed

Broadband connection failed. T tried unsuccessfully to find a fault and restore the service. T agreed to cancel the contract, offered to reimburse the monthly fees which had been paid by C and cost of calls made to technical support team. C refused the offer and claimed cost of all telephone call charges, car parking and bus fares in lieu of on-line shopping, mobile top-ups and £1,000 for time, stress and the unsatisfactory customer service. Found. There was no evidence to support C’s claims for car parking, bus fares or mobile top ups but directed the company to pay C £15 for identifiable telephone calls and £200 for stress and inconvenience.

215.00

13:03 Not supplying broadband

Very slow broadband speed at C’s new home. Remedial work was undertaken by T who then said it could do nothing to improve service. Six months later C discovered that T had not been supplying broadband to his home. C cancelled service and sought a subscriptions refund. T promised a refund but it was never received by C. Found. The compensation claimed by C was appropriate.

200.00

19:07 No contract agreed The customer ended his mobile phone contract and requested a PAC code. In order to provide him with it, the company had to re-activate his account. It placed him back on his old service plan and issued a monthly bill covering the period from activation until the PAC code was used. The customer complained about having to pay these charges. As he did not pay the final bill the company placed the matter with a debt collection agency. The customer believed that the company dealt with his complaint in an unsatisfactory manner. Found. The Adjudicator found that it was not possible to revive a contract that had already been terminated. The

company had not advised the customer that he would need to enter a new contract on the same terms as the old one to re-activate the number; the customer had not agreed to such a course of action. No evidence was provided that the customer made use of the company's services during the brief period of re-activation. The company failed in its duty of care by charging the customer without contractual authority. The company was directed to remove all charges from the customer's account, to instruct the debt collection agency to cease its actions immediately, to use its best efforts to ensure that any negative entries were removed from the customer's credit file, to provide a written apology and to pay the customer compensation.

200.00

9

Reference

Case Study name Subject1 Compensation £0.00

19:08 Default notice The customer had an outstanding balance on his account which he queried and sought access to his bills. He complained that the company did not answer his questions and had recorded a default on his credit file for non-payment without first sending him a default notice. The company said that it had responded to the customer’s queries and the default notice would have been sent out automatically. It was unable to provide the customer with access to his bills as this information was no longer available. Found. The company did not provide the customer with a default notice as required before entering a default on his credit file. Therefore, although the debt was correct and owing the default should not have been recorded. The company was directed to apologise to the customer, remove any negative entry on the customer’s credit file which related to the outstanding balance on his account and pay the customer compensation. The customer’s claim for access to his bills did not succeed as the company had explained why it could not provide them.

200.00

19:05 Customer’s change of mind

The customer contacted the company and agreed that she would receive its broadband services. Two days later the customer changed her mind and telephoned the company cancelling the earlier agreement. She complained that the company had not followed her instructions and instead it started the process of transferring the services from her existing service provider. The customer suffered a great deal of inconvenience and expense for which she claimed £5,000.00 compensation because she was unable to reserve her daughter’s accommodation at university. The company denied that it had acted as alleged by the customer and in any event the damages which she sought could not be recovered. Found. The company should not have begun transferring the customer’s broadband service away from her existing

service provider. By doing so the company had acted in breach of the duty of care which it owed to the customer. The majority of the compensation claimed by the customer could not be recovered because it was too remote and not reasonably foreseeable. However the customer had suffered some frustration and inconvenience as a consequence of the company’s failings and she was awarded compensation.

225.00

05:03 Reasonable procedure not followed

C ordered a broadband service but was unable to connect. Found. T knowingly failed to provide a service, did not follow its own procedures to refer problem to second level team and attempted to deny C access to a means of resolving the dispute both technically and administratively while at the same time charging for that service causing C inconvenience.

250.00

06:08 Wrong debts C had broadband service for less than 1 month. T continued to debit C’s bank account each month. C was forced to close her bank account to stop monies being taken. Found. T was directed to refund C all disputed sums debited from C’s bank account and pay compensation.

250.00

07:09 Inconvenience damages

Agreement for services by which C would have enjoyment, peace of mind and would not be overcharged. T overcharged C at mobile phone rates instead of landline rates for calls to Jamaica. T took more from C’s bank account on a direct debit than C expected resulting in bank making an extra charge because there was not enough money in C’s account to cover it. Found. C inconvenienced by T’s failure.

250.00

13:09 Moving broadband providers

C terminated contract before moving to next door property. C arranged for broadband services at his new property with a different service provider. A short time after receiving a bill from T for alleged outstanding charges C’s new broadband connection was suspended. Debt collectors pursued the customer. T acknowledged it had confused C’s account but it had no record of C

250.00

10

Reference

Case Study name Subject1 Compensation £0.00

cancelling the contract. T apologised. Found. T was directed to cancel the outstanding bill, to instruct its debt collection agents to stop pursuing C, to pay C’s reasonable set up costs with another broadband provider, to investigate and explain in writing why the customer’s line was cut off and to pay compensation.

15:08 Porting a number C had been promised by T that he could port his number to his new address but the number was not ported. Found. C’s claim succeeded.

250.00

12:08 Compensation for lost landline and broadband

Customer lost landline phone for two weeks and broadband for four weeks. The company accepted there had been a service failure as well as poor customer service and offered £300 compensation which the customer rejected claiming £1,000.00. Found. The company’s offer of £300.00 was reasonable.

300.00

06:03 Hard of hearing C was hard of hearing and found it difficult to communicate with T by telephone. C used T’s Anytime service, opened a different account then requested termination of the account. T took 6 months to terminate the account which was far too long. Found. C was disadvantaged when seeking technical support from T because he was continually referred to a telephone help line when he had difficulty in hearing what was being said to him.

300.00

07:08 Providing broadband C took up T’s broadband offer which could consolidate his three dedicated lines for home telephone, fax/telephone and computer into two lines, giving an improved level of speed and service without inconvenience. C requested the broadband service be provided on his dedicated home computer line but T provided it to the dedicated home telephone line. Found. It cost C more money for a service he did not receive, he spent a significant amount of time trying to sort out a problem not of his making and he was inconvenienced.

300.00

13:10 Broadband in non-cable area

Customer asked the company to transfer broadband service to his new home. As the customer was moving to a non-cable area she was told by the company to obtain a line from others and then broadband could be provided over that. The customer did so, but broadband service never provided by the company. Bills accumulated at the old address. Customer terminated the contract after being without broadband service for more than six months. Found. The order went through the non-cable division of the company but there were problems between their cable and non-cable divisions. The company was directed to apologise and pay compensation.

300.00

08:04 No broadband C’s broadband service disconnected by T due to telephone line (owned by another provider) being upgraded. Telephone line could not take the enhanced service. Found. T could not use problems with the line as an excuse to avoid responsibility. If a provider fails to provide what has been agreed and charged for it is in breach of contract and has no right to demand or to take money for something it does not provide. Exclusion clauses in the contract were void under the Unfair Contract Terms Act 1977 and the Unfair Terms in Consumer Contracts Regulations 1999. T was directed to cancel its contract with C, remove its marker from the telephone line, repay all sums paid by C after the broadband service failed, cancel any outstanding invoices and pay C compensation. The stress exacerbated C’s psychiatric condition; compensation for personal injury was outside the scope of CISAS.

350.00

15:01

Mis-selling unsuitable package

C, represented by his daughter, was over 80 years old and died during the course of the application to CISAS. Found. T had not properly charged him, not provided details of the agreement between them and had mis-sold him a package which was not suitable for his needs.

350.00

11

Reference

Case Study name Subject1 Compensation £0.00

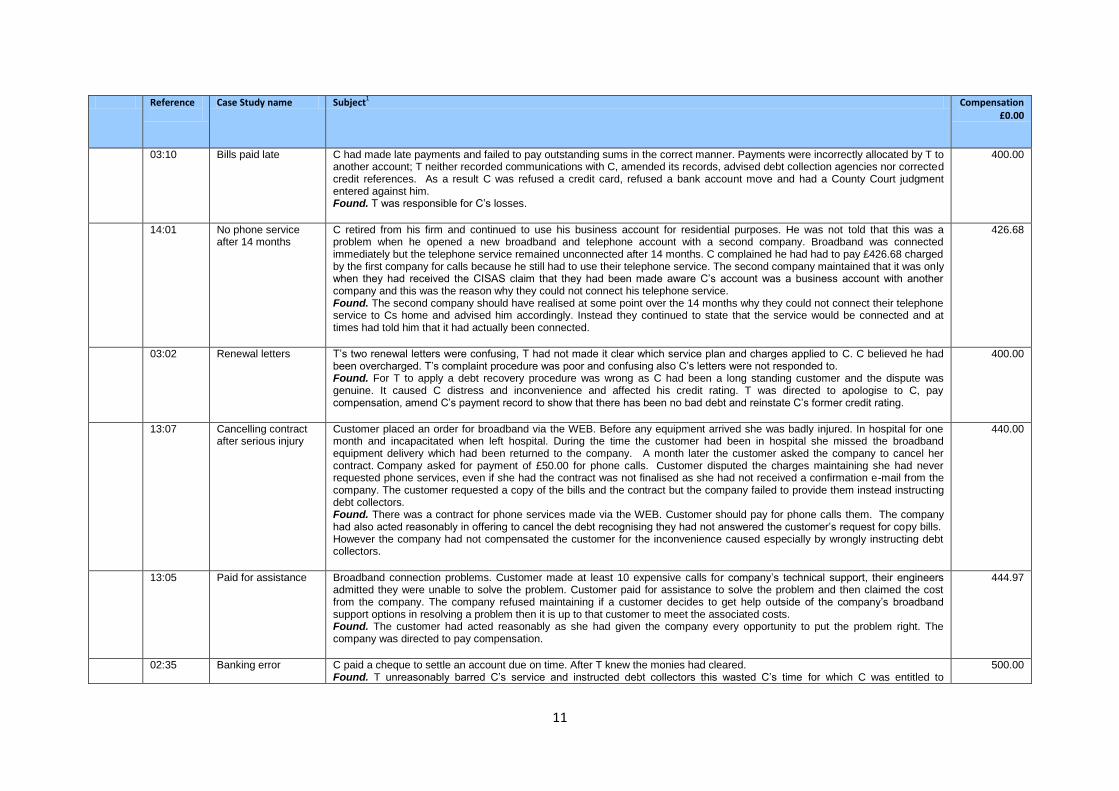

03:10 Bills paid late C had made late payments and failed to pay outstanding sums in the correct manner. Payments were incorrectly allocated by T to another account; T neither recorded communications with C, amended its records, advised debt collection agencies nor corrected credit references. As a result C was refused a credit card, refused a bank account move and had a County Court judgment entered against him. Found. T was responsible for C’s losses.

400.00

14:01 No phone service after 14 months

C retired from his firm and continued to use his business account for residential purposes. He was not told that this was a problem when he opened a new broadband and telephone account with a second company. Broadband was connected immediately but the telephone service remained unconnected after 14 months. C complained he had had to pay £426.68 charged by the first company for calls because he still had to use their telephone service. The second company maintained that it was only when they had received the CISAS claim that they had been made aware C’s account was a business account with another company and this was the reason why they could not connect his telephone service. Found. The second company should have realised at some point over the 14 months why they could not connect their telephone service to Cs home and advised him accordingly. Instead they continued to state that the service would be connected and at times had told him that it had actually been connected.

426.68

03:02 Renewal letters T’s two renewal letters were confusing, T had not made it clear which service plan and charges applied to C. C believed he had been overcharged. T’s complaint procedure was poor and confusing also C’s letters were not responded to. Found. For T to apply a debt recovery procedure was wrong as C had been a long standing customer and the dispute was genuine. It caused C distress and inconvenience and affected his credit rating. T was directed to apologise to C, pay compensation, amend C’s payment record to show that there has been no bad debt and reinstate C’s former credit rating.

400.00

13:07 Cancelling contract after serious injury

Customer placed an order for broadband via the WEB. Before any equipment arrived she was badly injured. In hospital for one month and incapacitated when left hospital. During the time the customer had been in hospital she missed the broadband equipment delivery which had been returned to the company. A month later the customer asked the company to cancel her contract. Company asked for payment of £50.00 for phone calls. Customer disputed the charges maintaining she had never requested phone services, even if she had the contract was not finalised as she had not received a confirmation e-mail from the company. The customer requested a copy of the bills and the contract but the company failed to provide them instead instructing debt collectors. Found. There was a contract for phone services made via the WEB. Customer should pay for phone calls them. The company had also acted reasonably in offering to cancel the debt recognising they had not answered the customer’s request for copy bills. However the company had not compensated the customer for the inconvenience caused especially by wrongly instructing debt collectors.

440.00

13:05 Paid for assistance

Broadband connection problems. Customer made at least 10 expensive calls for company’s technical support, their engineers admitted they were unable to solve the problem. Customer paid for assistance to solve the problem and then claimed the cost from the company. The company refused maintaining if a customer decides to get help outside of the company’s broadband support options in resolving a problem then it is up to that customer to meet the associated costs. Found. The customer had acted reasonably as she had given the company every opportunity to put the problem right. The company was directed to pay compensation.

444.97

02:35 Banking error C paid a cheque to settle an account due on time. After T knew the monies had cleared. Found. T unreasonably barred C’s service and instructed debt collectors this wasted C’s time for which C was entitled to

500.00

12

Reference

Case Study name Subject1 Compensation £0.00

compensation. No compensation for business losses as C had not proved them and T did not know the service was for business use.

05:18 Communications provider transfer

C placed an order for broadband which she cancelled a month later as she was entitled to do. T took five weeks to transfer C’s line to another communications provider during which C did not have internet access also C was without phone access for several days. Found. T was directed to reimburse C for phone charges and pay compensation.

500.00

12:07 Paying to avoid poor credit rating. CISAS rule 5(g) applied

C paid an overcharge of £10.32 by cheque and account ended but T pursued her via its debt collectors who forced her to pay £10.32 again. Found. C had been confused and frightened about her credit rating and what the debt collectors would do. A rebate of £640.00 was due for overcharging, a refund of fees due to poor service, £30.00 compensation a month for inconvenience caused by poor service plus £150.00 for upset and inconvenience caused by the company’s negligent instruction of debt collectors. However, under CISAS rule 5(g) the award was limited to the amount claimed by C which was £500.00.

500.00

15:06 Mobile barring service

C paid for a mobile barring service on her landline to avoid her son incurring high bills. T had not assisted C when she asked if call barring was working although T’s records showed they knew it was being avoided. T had not barred calls to mobiles. T had billed 4 months late which meant C did not appreciate the costs she was incurring. Found. C’s claim succeeded.

500.00

17.01 The balance of probability

The customer complained that she had requested cancellation of her contract by e-mail but the company would not accept the request. The company explained that because the request was received by e-mail it did not accept it as a secure form of communication. The company continued to leave the customer’s account active and charged her monthly fees. The bills were not paid as the customer had cancelled her direct debit mandate so the company referred her details to a debt collection agency. Found. On the balance of probability the customer had given proper notice to cancel her account using a valid form of communication. As the company did not cancel the account, continued to charge her and referred her details to a debt collection agency then the company breached the terms of its contract and failed in its duty of care to the customer. The company was directed to pay the customer compensation, give her a written apology, clear the charges after the date on which her account should have been cancelled and clear the negative entries from the customer’s credit file.

500.00

18:03 Establishing amount lost

The customer was a small family run business which claimed compensation for business loss of £19,000.00 because their telephone line was mistakenly targeted by the company for transfer. The customer lost the use of their phone and internet service for over a month making it impossible for them to trade as they were predominantly an internet and email based business. The customer also lost several contracts during the month it took to reinstate the line. The company accepted it had processed an order on the customer’s phone line in error as a result of information supplied to the company by another customer. The company had received instructions from the other customer to take over a phone line in the new premises that they were moving into. The address of the new premises given by the other customer had a small error as the final letter of the postcode was incorrect. This as well as a similarity in road names and premises numbers meant that the wrong address was targeted by the company and the wrong phone line was selected to be taken over. The company, who had not intended to disrupt the customer’s phone and broadband services, made a goodwill offer of £500.00 but it was not acceptable to the customer. Found. The Adjudicator found that the loss of the customer’s service amounted to a failure of duty of care by the company in correctly checking information to prevent the customer being subject to an erroneous line takeover. Such a loss of service as was experienced by the customer could be expected to have a significant impact on a small family business and the customer had provided reference numbers to contracts lost amounting to £14,000.00. Under CISAS rules the maximum claim is £5,000.00 also

500.00

13

Reference

Case Study name Subject1 Compensation £0.00

the customer must justify any claim for compensation. However, the customer had not provided sufficient documentation, an explanation or calculation to fully support their claim for loss of business and financial loss. In the circumstances the offer of £500.00 made by the company did not appear unreasonable (though had detailed documented information and evidence been provided by the customer then the customer may have been entitled to additional compensation).

18:09 5 year default notice The customer complained that the company had waived the customer’s outstanding balance but had not removed the default placed on his credit file. Five years later the customer received a number of rejections from potential creditors including failing to get his house re-mortgaged. He was advised to check his credit file and contacted the company. Months passed before the company arranged to have the default notice removed. Found. The customer had suffered inconvenience through the company not having acted in a timely manner.

500.00

Compensation from £501.00 to £999.00

08:06 No internet connection

Product of another provider used by T on C’s telephone line caused loss of C’s internet and e-mail service. T debited C’s debit card with monthly subscriptions without C’s permission. Found. T’s action highly inappropriate. T was directed to refund C the monthly subscriptions, release C from the contract without any payment, provide a MAC, remove any offending products from line and ensure C’s credit rating was not adversely affected.

600.00

10.10 Unauthorised access Cost of unauthorised access to C’s telephone, broadband and television cables added by T to C’s bills. C asked T to terminate the services and investigate who was accessing the cables. Found. T did little to help and failed in its duty of care. T was directed to suspend C’s services at no cost to C, liaise with C and carry out a detailed investigation into C’s problems, suspend the actions of debt collection agency pending results of the investigations and pay compensation.

600.00

11.01 Billing and wrong use of direct debit

C succeeded in a billing complaint against T and awarded £600.00. T then took more money by direct debit from C. Found. C’s complaint succeeded. T’s actions were an extremely serious breach of contract and duty of care.

600.00

13:08 Account not terminated

C sent letter terminating two telephone accounts. T’s records showed only one contract was to be terminated, this they did and chased C for payment of the other account. C’s credit record was blighted. Found. The letter referred to both accounts. Extremely serious thing to publicise an alleged credit default because it can damage C’s personal reputation, and ability to pay his way through life. It is to be expected that C will suffer from a bad credit entry. It is fair and reasonable to compensate customers for the mere fact that a wrong entry was made, regardless of whether they suffer actual financial loss as a result. Compensation awarded and T was directed to give an explanation and a full apology.

600.00

02:14 Inaccurate records T billed C £900. 00 in one month. Found. More likely than not C did not make all the billed calls because of their timings and shear volume. Serious doubts about the integrity of T’s records.

602:15

14:03 Two accounts set up accidently

A duplicate account had accidentally been set up when an earlier broadband problem had been resolved. C was unaware that an additional direct debit was being taken by T and had not authorised any additional payment. Found. C’s claim succeeded. A full repayment should be made by T to C.

607.02

10:07 Lost business C experienced problems with mail forwarding which T failed to resolve. C asked for a smooth domain transfer which T took 3 750.00

14

Reference

Case Study name Subject1 Compensation £0.00

revenue months to confirm. Breach of contract or a breach of duty of care by T. C estimated lost business revenue of more than £30,000.00 and claimed the maximum of £5,000.00 under CISAS but failed to submit evidence supporting the amounts. Found. Compensation awarded only for inconvenience and the time and energy expended by C in trying to get the problem resolved.

13:01 Inadequate broadband and defective router

Defective router and inadequate broadband service for about a month. The router caused breaches of security by making the contents of the customer’s computer available to other users. The customer (who was studying for his exams at the time and needed the internet to prepare) was badly affected by the countless attempts to make the service work with the assistance of the company’s technical department. Company was directed to pay compensation for lack of service, vexation and inconvenience.

750.00

Compensation from £1,000.00 to £5,000.00

04:07 Creating problems T created problems by wrongly invoicing C annually in advance, making billing mistakes, not providing accurate bills, wrongfully suspending services, not efficiently using the direct debit facilities given by C and instructing debt collectors. Found. C endured inconvenience and the cost of having to repeatedly correspond with T together with vexation through loss of services.

1,000.00

02:25 Fraud C informed T of fraudulent use of mobile phone number to make calls to many countries associated with questionable activities. T did not take complaint seriously nor offer reasonable assistance or advice. Found. T seriously failed in its duty of care towards C.

1,000.00

12:10 Error making customer un-creditworthy

The customer made un-creditworthy due to the company’s error more than 12 months earlier; their entries on the customer’s credit file were not correct. Found. Company failed to rectify the situation promptly after being notified of the error. The company was directed to pay compensation for the stress and harassment customer suffered for over one year as well as final loss of increased mortgage payment which directly resulted from the failures of the company.

1,285.00

12:03 Barring outgoing calls

Customers had contract with company 1 for home and business until they transferred to company 2. Two years later traffic again passing over network of company 1 but company 1 had no contract to reprove the service. Customers refused to pay bills of company 1 who then barred the customers outgoing calls and placed the matter in the hands of debt collectors. Significant failure of duty of care by company 1 who had also through their debt collectors given notice of legal proceedings after the matter had been referred to CISAS. Found. The disregard of the CISAS adjudication process was in the words of the customers, ‘cynical, needless intimidation... bullying techniques’, which was inexcusable.

1,400.00

12:01 Business loss Customer requested an upgrade to a business package with a static IP address. Constant connection problems for a year. Found. Customer frustrated, received little real assistance from company, and his business suffered losses due to the amount of time unable to connect to the internet.

1,500.00

19:06 Mistake over who contract was with

The sister of a customer took out a mobile phone contract in a retail store in her own name. The customer received a text message stating, 'Thank you for the additional line taken out’, which alerted her to the new number on her existing account. All the paperwork and receipt stated her sister’s name, address and direct debit details. However, when the details had been sent from the store to the company the contract had been mistakenly placed on the

1,962.80

15

Reference

Case Study name Subject1 Compensation £0.00

customer’s account. The company would not allow the customer to change ownership until 3 months had passed so she was bound to a contract she did not take and did not agree to. The company insisted that a change of ownership could only occur once the customer’s sister cooperated. The customer complained that she should not be responsible as she had no right to forcefully make anyone do anything especially when she was not supposed to be the account holder and the error was not her fault. A change of ownership eventually took place. However, the company billed the customer for the second mobile line. The customer claimed a refund of the second mobile line charges of £462.80 together with £2,000.00 compensation for the immense stress she had been placed under by the company. Found. The customer’s sister had taken out a contract for the second mobile line. The company provided no evidence that there was any agreement for a second phone in place with the customer. If the retail store had made an error in its notification to the company then this could only be a matter between the company and the retail store. It was common sense that it could be nothing to do with the customer who was not involved with the transaction. The company took advantage of the family relationship to make the customer responsible for payments on a contract which the company had provided no evidence the customer was liable for. There was a serious failure of duty of care by the company for extending the customer’s existing agreement to include the second mobile line. The company was directed to write a letter of apology to the customer and release the customer from her contract without imposing early termination charges. She was awarded the refund claimed of £462.80 and compensation for stress and inconvenience of £1,500.00 (a total of £1,962.80). The company was directed to confirm in writing that it held a clear credit rating on the customer’s account for the matters dealt with in the adjudication.

08:14 Loss of business C, a small business, cancelled its contract with T who unable to provide a broadband service. T continued to charge C, threatened action from its debt management team, contacted another provider and placed an order for T’s broadband on the line of C. C’s existing contract with the other provider was interrupted for several weeks. Found. T liable for loss of business whilst C was without a broadband connection.

2,000.00

20:05 Package not clearly explained

The customer complained that he had been mis-sold an upgrade mobile phone package when over three months he was billed £3,000.00. He had been led to believe that charges would be capped at £15.00 per month. In its defence the company said nothing about the mis-selling allegation. Found. When the company had sold the upgrade package to the customer it had repeatedly said, ‘...all in £15.00 per month’, and had noted this in its customer account notes. However it had not clearly explained in plain English what the upgrade package included and did not include. The customer did not understand what services were, ‘outside of plan’, and would be billed separately. The company had given the customer the wrong impression that his contract would be a capped service. The company was to refund the customer £2,590.74 and apply a £1,142.30 credit note to the account together with waiving penalty, cancellation and debt recovery charges. The company was to restore service to the customer’s mobile phone though the contract would not be capped or, if the customer preferred, the company was to allow the customer to terminate the contract without penalty.

2,590.74 / 1,142.30

20:07 Stolen SIM card and inaccurate records

The customer complained that she reported her SIM card had been stolen and requested a new one. However when she chased the whereabouts of the new SIM card a week later it was only then that the company blocked the SIM card to prevent further fraudulent activity. The company charged the customer £4,000.00 for the week after the theft; it said the theft was not reported

3,579.67 / 500.00

16

Reference

Case Study name Subject1 Compensation £0.00

and the company had blocked the account of its own accord due to unusual activity on the account. Found. The company had not kept accurate account records so more weight was attached to the customer’s account of events. The customer had reported the theft but the company had not blocked the SIM card for a week and in error continued to charge the customer. The company was d to refund the customer £3,579.67 for charges incurred after the theft had been reported. Also the company should pay £500.00 compensation as the customer was deprived of a significant sum of money over a lengthy period of time.

10.04 Overpayments by small company

C, a small IT company, regularly overcharged by T for broadband and phone services. T did not try to resolve the dispute expeditiously. C provided detailed calculations together with copies of tariff and cap agreements. T did not provide any business contract terms excluding liability for any element of losses arising from overcharging nor did it comment upon losses claimed by C for time spent trying to resolve the dispute which included lengthy attempts by C to communicate with T, evaluate opportunities to move service provider, attempts to stop bank payments and assessing bills manually call by call. Found. T was directed to reimburse C £640.00 for overcharging and £3,000.00 towards C’s total loss.

3,640.00

13:02 Business loss

Having purchased a business and since taking over the account, the customer had numerous problems with the company including the phone line being cut at random without warning, being charged on two accounts for more than 12 months and having hundreds of pounds taken by the company from a bank account which the customer had been unable to retrieve. As a result the customer had bank charges imposed on her due to the wrongful withdrawals, lost business and had spent 27 hours of her time trying unsuccessfully to solve the problems with the company. The company admitted they were at fault. Found. The company was directed to apologise to the customer, to stop sending bills for a service the customer never had, to stop taking money from the customer’s account for that service, to pay compensation and reimburse all the money wrongly withdrawn from the customer’s account.

3,700.00