10 c h a p t e r bond prices and yields second edition fundamentals of investments valuation &...

Post on 22-Dec-2015

216 views

TRANSCRIPT

1010C h a p t e r

Bond Prices and YieldsBond Prices and Yields

second edition

Fundamentals

of InvestmentsValuation & Management

Charles J. Corrado Bradford D. Jordan

McGraw Hill / Irwin Slides by Yee-Tien (Ted) Fu

2002 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw Hill / Irwin

10 - 2

Bond Prices and Yields

Our goal in this chapter is to understand the relationship between bond prices and yields, and to examine some of the fundamental tools of bond risk analysis used by fixed-income portfolio managers.

Goal

2002 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw Hill / Irwin

10 - 3

Bond Basics A bond essentially is a security that offers the investor a

series of fixed interest payments during its life, along with a fixed payment of principal when it matures.

So long as the bond issuer does not default, the schedule of payments does not change.

When originally issued, bonds normally have maturities ranging from 2 years to 30 years, but bonds with maturities of 50 or 100 years also exist.

Bonds issued with maturities of less than 10 years are usually called notes.

A very small number of bond issues have no stated maturity, and these are referred to as perpetuities or consols.

2002 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw Hill / Irwin

10 - 4

Bond Basics

U.S. Treasury bonds are straight bonds. Special features may be attached, creating convertible bonds, “putable”

bonds, “putable” bonds have a put feature that grants bondholders the right to sell their bonds back to the issuer at a special put price.

Straight bondAn IOU that obligates the issuer to pay to the bondholder a fixed sum of money (called the principal, par value, stated value or face value) at the bond’s maturity, along with constant, periodic interest payments (called coupons) during the life of the bond.

2002 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw Hill / Irwin

10 - 5

Bond Basics

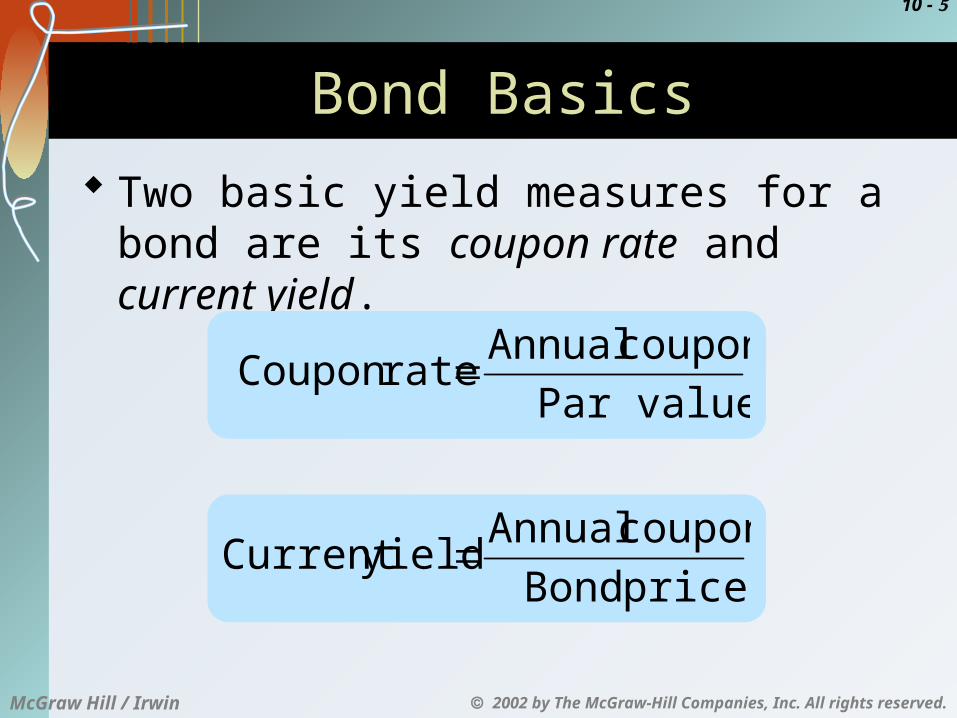

Two basic yield measures for a bond are its coupon rate and current yield.

Par value

coupon AnnualrateCoupon

price Bond

coupon AnnualyieldCurrent

2002 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw Hill / Irwin

10 - 6

Bond Basics

example1, suppose a $1,000 par value bond pays semiannual coupons of $40. The annual coupon is then $80, and stated as a percentage of par value the bond's coupon rate is

$80 / $1,000 = 8%. example2, suppose a $1,000 par value bond

paying an $80 annual coupon has a price of $1,032.25.

The current yield is $80 / $1,032.25 = 7.75%.

2002 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw Hill / Irwin

10 - 7

Straight Bond Prices and Yield to Maturity

Yield to maturity (YTM)The discount rate that equates a bond’s price with the present value of its future cash flows.

2002 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw Hill / Irwin

10 - 8

Straight Bond Prices and Yield to Maturity

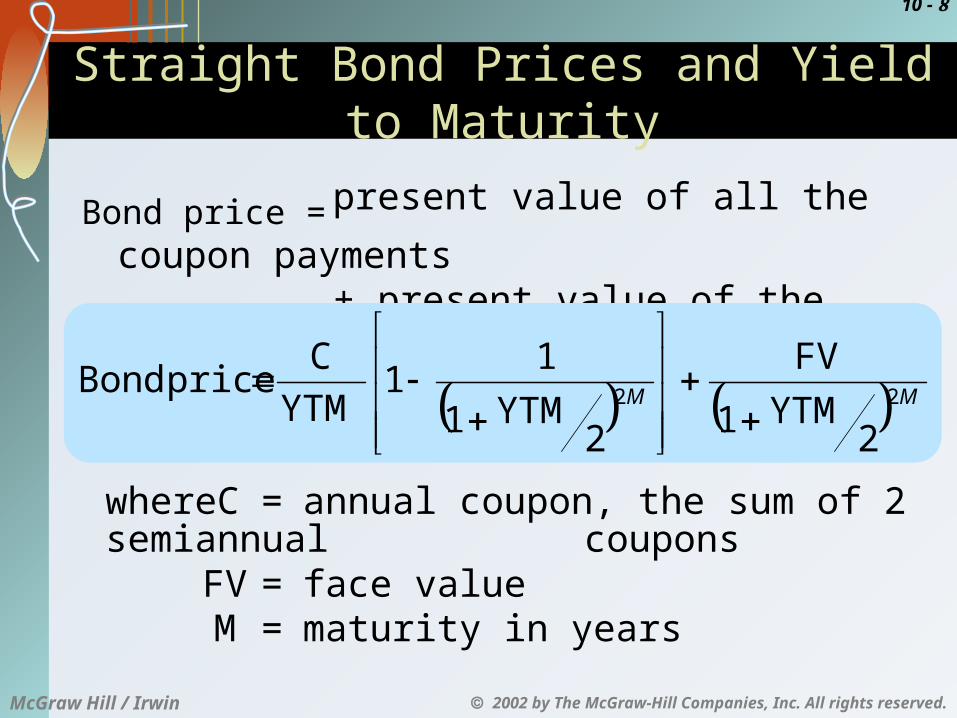

Bond price = present value of all the coupon

payments+ present value of the principal

payment

MM 22

2YTM1

FV

2YTM1

11

YTM

CpriceBond

where C = annual coupon, the sum of 2 semiannual coupons

FV = face valueM = maturity in years

2002 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw Hill / Irwin

10 - 9

Straight Bond Prices and Yield to Maturity

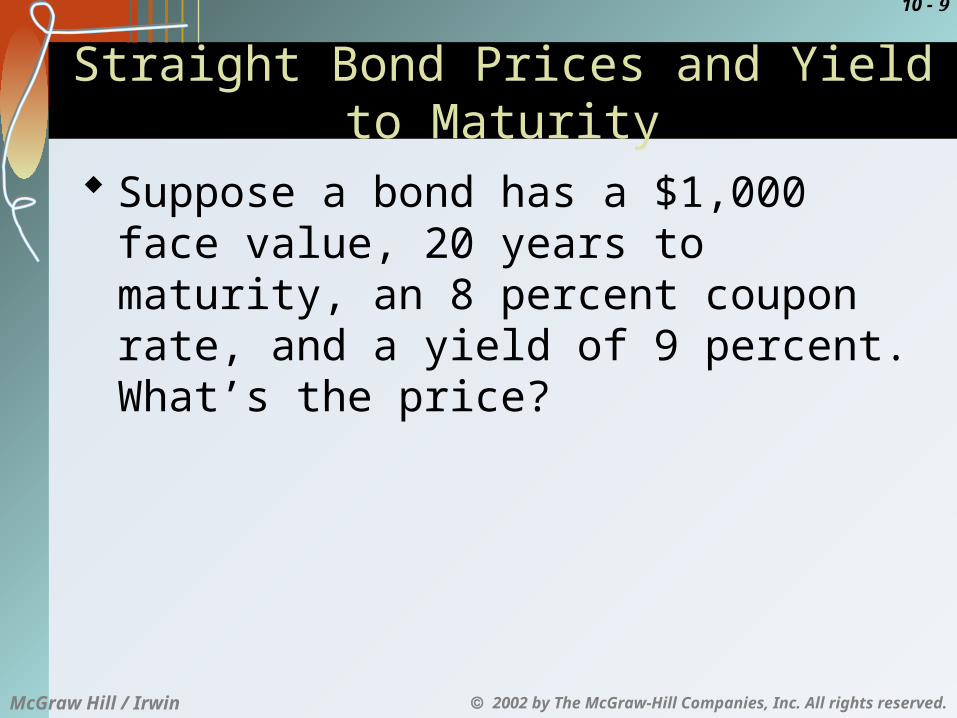

Suppose a bond has a $1,000 face value, 20 years to maturity, an 8 percent coupon rate, and a yield of 9 percent. What’s the price?

2002 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw Hill / Irwin

10 - 10

At simple interest: P = A/(1 + nr) At interest compounded annually: P = A/(1 + r)n At interest compounded q times a year: P = A/(1 + r/q)nq

2002 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw Hill / Irwin

10 - 11

Straight Bond Prices and Yield to Maturity

2002 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw Hill / Irwin

10 - 12

Premium and Discount Bonds

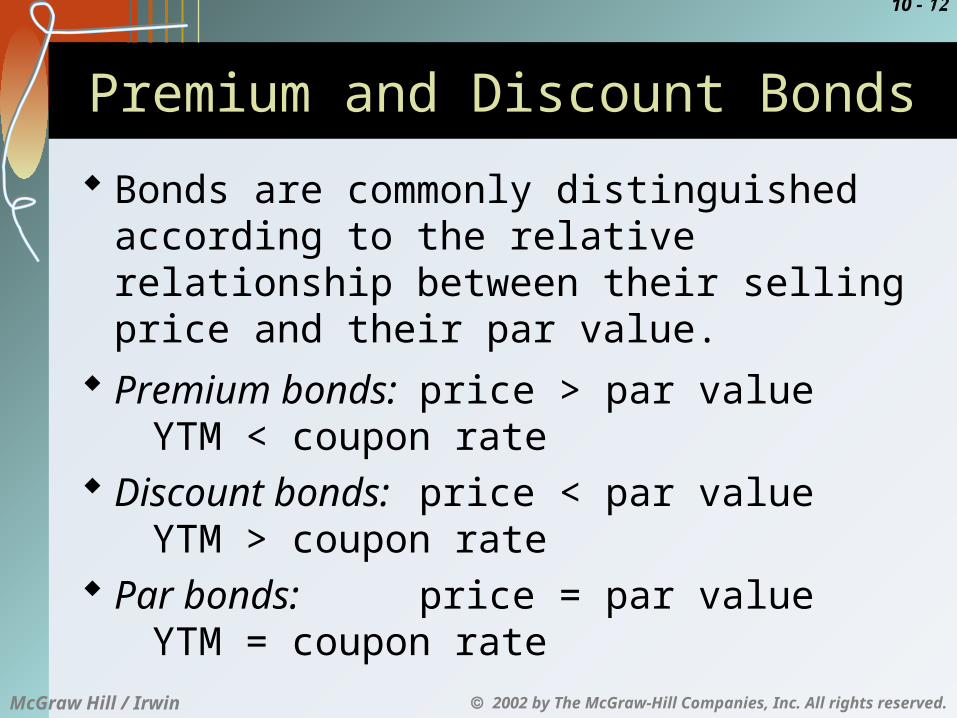

Bonds are commonly distinguished according to the relative relationship between their selling price and their par value.

Premium bonds: price > par valueYTM < coupon rate

Discount bonds: price < par valueYTM > coupon rate

Par bonds: price = par valueYTM = coupon rate

2002 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw Hill / Irwin

10 - 13

Premium and Discount Bonds

2002 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw Hill / Irwin

10 - 14

Premium and Discount Bonds

In general, when the coupon rate and YTM are held constant …

for discount bonds: the longer the term to maturity, the greater the discount from par value, and

for premium bonds: the longer the term to maturity, the greater the premium over par value.

2002 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw Hill / Irwin

10 - 15

Premium and Discount Bonds

Example 10.2: Premium and Discount Bonds. Suppose a bond has a $1,000 face value, with eight years to maturity and a 7 percent coupon rate. If its yield to maturity is 9 percent, does this bond sell at a premium or discount? Verify your answer by calculating the bond’s price.

Since the coupon rate is smaller than the yield, this is a discount bond.

2002 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw Hill / Irwin

10 - 16

Premium and Discount Bonds Example 10.3: Premium Bonds Consider two bonds,

both with a 9 percent coupon rate and the same yield to maturity of 7 percent, but with different maturities of 5 and 10 years. Which has the higher price? Verify your answer by calculating the prices.

First, since both bonds have a 9 percent coupon and a 7 percent yield, both bonds sell at a premium. Based on what we know, the one with the longer maturity will have a higher price.

We can check these conclusions by calculating the prices as follows:

2002 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw Hill / Irwin

10 - 17

Premium and Discount Bonds

2002 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw Hill / Irwin

10 - 18

Premium and Discount Bonds

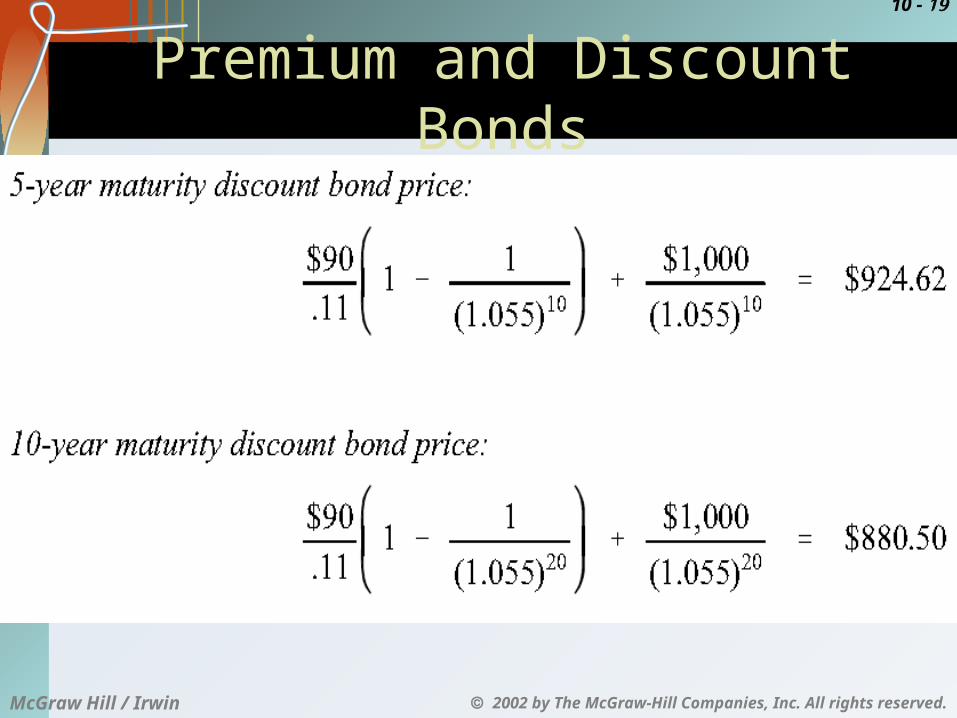

Example 10.4: Discount Bonds Now consider two bonds, both with a 9 percent coupon rate and the same yield to maturity of 11 percent, but with different maturities of 5 and 10 years. Which has the

higher price? Verify your answer by calculating prices.

These are both discount bonds. (Why?) The one with the shorter maturity will have a higher price. To check, the prices can be calculated as follows:

2002 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw Hill / Irwin

10 - 19

Premium and Discount Bonds

2002 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw Hill / Irwin

10 - 20

Relationships among Yield Measures

Since the current yield is always between the coupon rate and the yield to maturity (unless the bond is selling at par) …

for premium bonds: coupon rate > current yield > YTM

for discount bonds:coupon rate < current yield < YTM

for par value bonds:coupon rate = current yield = YTM

2002 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw Hill / Irwin

10 - 21

A note on bond price quotes

Clean price : the price of a bond net of accrued interest , this the price that is typically quoted .

Dirty price : the price of a bond including accrued interest , also known as the full or invoice price , this is the price the buyer actually pays .

2002 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw Hill / Irwin

10 - 22

Calculating Yields

To calculate a bond’s yield given its price, we use the straight bond formula and then try different yields until we come across the one that produces the given price.

MM 22

2YTM1

FV

2YTM1

11

YTM

CpriceBond

To speed up the calculation, financial calculators and spreadsheets may be used.

2002 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw Hill / Irwin

10 - 23

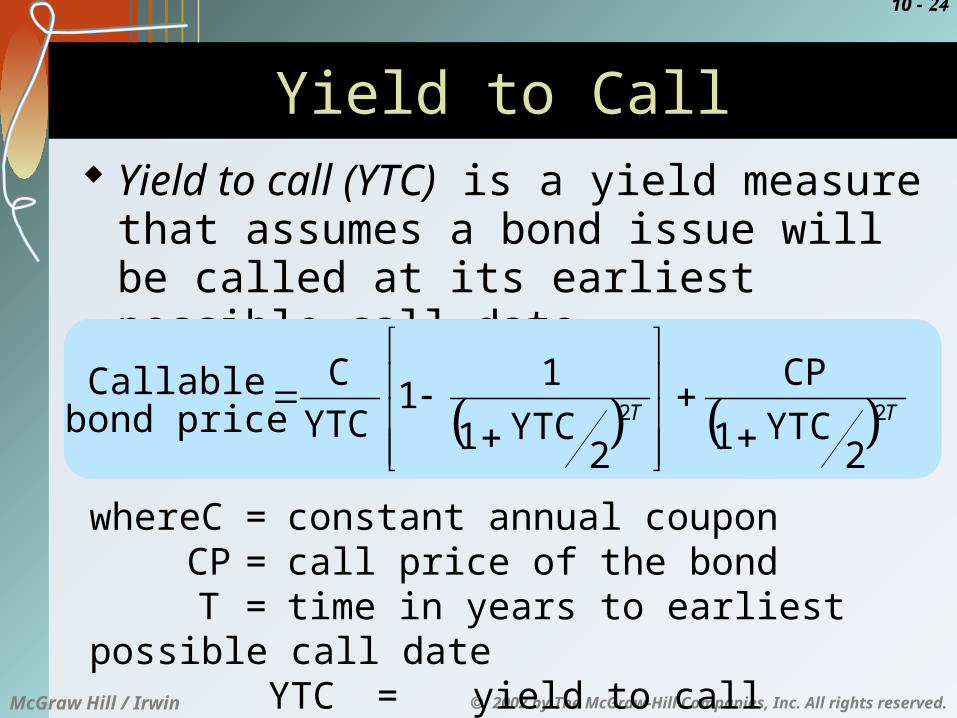

Yield to Call

A callable bond allows the issuer to buy back the bond at a specified call price anytime after an initial call protection period, until the bond matures.

2002 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw Hill / Irwin

10 - 24

Yield to Call Yield to call (YTC) is a yield measure that

assumes a bond issue will be called at its earliest possible call date.

where C = constant annual couponCP = call price of the bondT = time in years to earliest possible call date

YTC = yield to call assuming semiannual coupons

TT 22

2YTC1

CP

2YTC1

11

YTC

C

Callable

bond price

2002 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw Hill / Irwin

10 - 25

Interest Rate Risk

The yield actually earned or “realized” on a bond is called the realized yield, and this is almost never exactly equal to the yield to maturity, or promised yield.

Interest rate riskThe possibility that changes in interest rates will result in losses in a bond’s value.

2002 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw Hill / Irwin

10 - 26

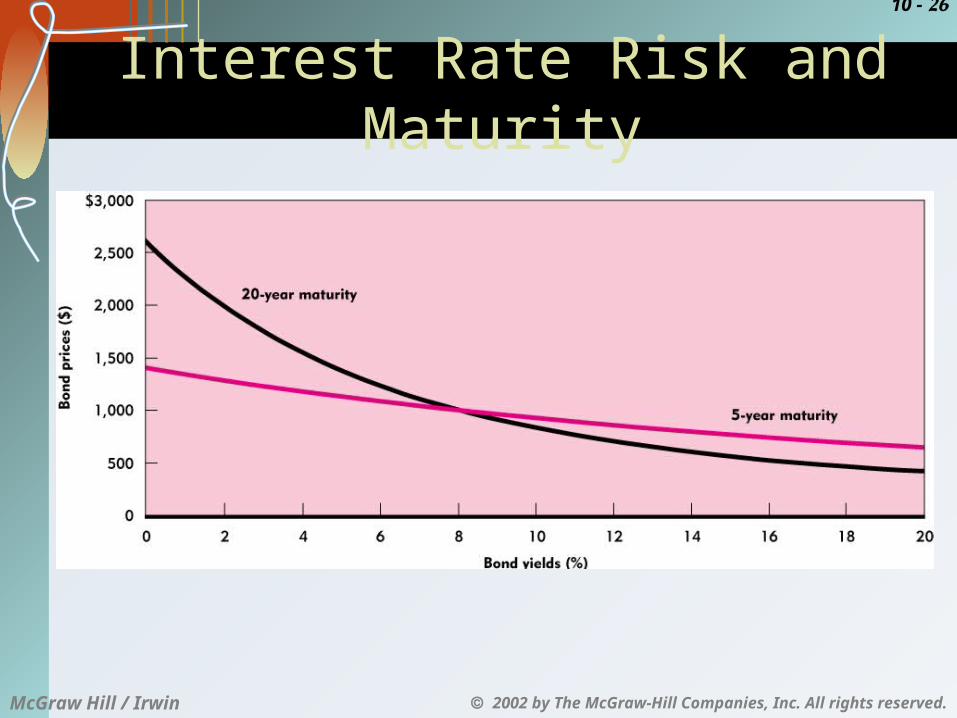

Interest Rate Risk and Maturity

2002 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw Hill / Irwin

10 - 27

Reinvestment Risk

A simple solution is to purchase zero coupon bonds. In practice however, U.S. Treasury STRIPS are the only zero coupon bonds issued in sufficiently large quantities, and they have lower yields than even the highest quality corporate bonds.

Reinvestment rate riskThe uncertainty about future or target date portfolio value that results from the need to reinvest bond coupons at yields not known in advance.

2002 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw Hill / Irwin

10 - 28

Price Risk versus Reinvestment Rate Risk

Interest rate increases act to decrease bond prices (price risk) but increase the future value of reinvested coupons (reinvestment rate risk), and vice versa.

Price riskThe risk that bond prices will decrease. Arises in dedicated portfolios when the target date value of a bond or bond portfolio is not known with certainty.

2002 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw Hill / Irwin

10 - 29

Immunization

It is possible to engineer a portfolio such that price risk and reinvestment rate risk offset each other more or less precisely.

ImmunizationConstructing a portfolio to minimize the uncertainty surrounding its target date value.

2002 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw Hill / Irwin

10 - 30

Chapter Review

Bond Basics Straight Bonds Coupon Rate and Current Yield

Straight Bond Prices and Yield to Maturity Straight Bond Prices Premium and Discount Bonds Relationships among Yield Measures

2002 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw Hill / Irwin

10 - 31

Chapter Review

More on Yields Calculating Yields Yield to Call

Interest Rate Risk and Malkiel’s Theorems Promised Yield and Realized Yield Interest Rate Risk and Maturity Malkiel’s Theorems

2002 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw Hill / Irwin

10 - 32

Chapter Review

Duration Macaulay Duration Modified Duration Calculating Macaulay’s Duration Properties of Duration

Dedicated Portfolios and Reinvestment Risk Dedicated Portfolios Reinvestment Risk

2002 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw Hill / Irwin

10 - 33

Chapter Review

Immunization Price Risk versus Reinvestment Rate Risk Immunization by Duration Matching Dynamic Immunization