1 worksheet s-10 - healthcare financial...

TRANSCRIPT

Worksheet S-10FY’s 2014 - 2018

E D G U E R R E R OO C T O B E R 1 7 , 2 0 1 7

TAHFA & HFMA South Texas Fall Symposium

1

Agenda2

FY2018 Highlights

Cost Report instructions: 9/29/2017 update

Medlearn Examples

Modeling Uncompensated Care Factor 3

Q & A’s

Regulatory Update – UC-DSH Highlights3

CMS-1677-F published August 14, 2017 Factor 2 change in uninsured population from CBO estimates to CMS’ Office of

Actuary

Incorporate FY14 Worksheet S-10 “Tipping point” reached

Defined uncompensated care consists of charity care and bad debt expense

Implementing trim methodology to address aberrant cost-to-charge ratios as well as potentially aberrant uncompensated care costs that exceed a threshold of 50 percent of total operating costs

Scaling factor applied to ensure paid UC-DSH is consistent with estimated amount available Overpaid providers $5.016M in FY17

Data is still suspect and no audit process in place

Regulatory Update: The Numbers Game4

Factor 1 – Total available DSH payments FY2016 = $14.4B FY2017 = $15.2B FY2018 = $15.5B

Factor 2 – Percentage Change in Uninsured Population CMS data assumptions change from Congressional Budget Office (CBO)

estimated to Office of the Actuary (OACT) FY2016 = $6.41B FY2017 = $5.99B FY2018 = $6.77B

Factor 3 – Allocation Basis FY12 and FY13 Medicaid Days FY13 and FY14 SSI Days FY14 Worksheet S-10

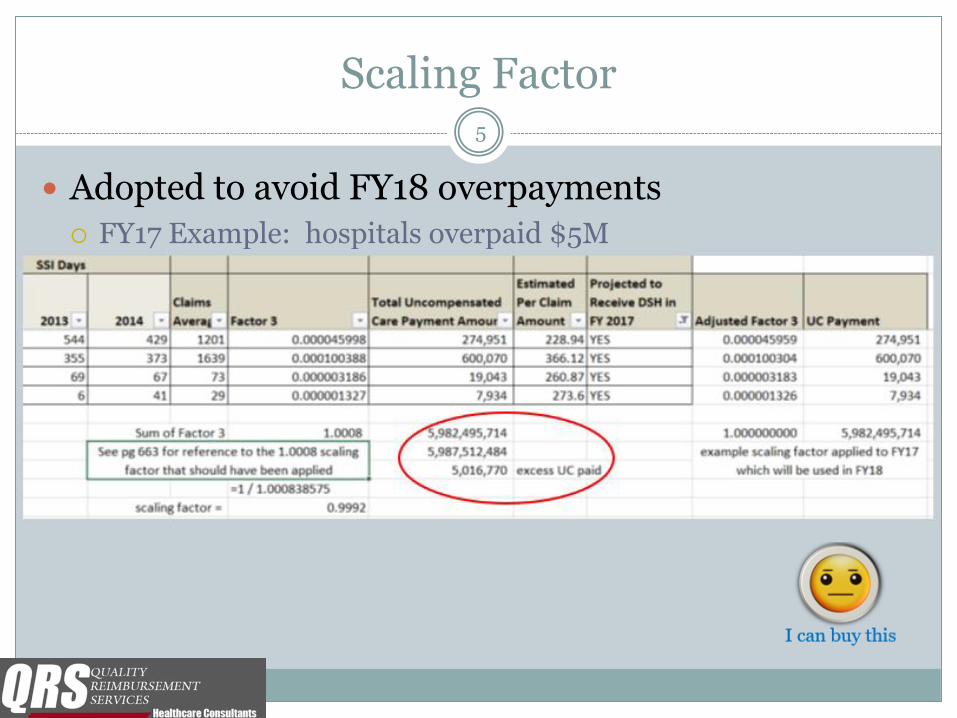

Scaling Factor5

Adopted to avoid FY18 overpayments

FY17 Example: hospitals overpaid $5M

Regulatory Update: Transmittal 11CMS-1677-CN published September 29, 2017

6

Revised the instructions for line 20 for subsection (d) Puerto Rico hospitals, charity care and uninsured discounts. Must meet hospital’s charity care policy or FAP. T10: Charity care--Health services for which a hospital demonstrates that the patient is unable to pay. T11: Charity Care and Uninsured Discounts--Charity care and uninsured discounts result from a hospital's policy to

provide all or a portion of services free of charge to patients who meet the hospital's charity care policy or FAP.

Modified the calculation and clarified the instructions on line 21, column 2, for insured patients and non-covered charges for insured patients for days exceeding a length-of-stay limit.

Clarified the instructions for line 22.

Clarified that the amount reported on line 26 is net of recoveries.

Added line 27.01 to capture Medicare allowable bad debt for the entire facility.

Modified the instructions for line 28 to only capture the non-Medicare bad debt expense.

Modified the calculation for line 29.

FY14 and FY15 cost reports - resubmission extended to October 31, 2017

Cost Report Edits7

Edit # Description Level Purpose

14005S Worksheet S-10 line 20, column 3 must be less than Worksheet C, line 200, column 8.

1 Charity charges cannot exceed total charges

14010S For each column, if Worksheet S-10, line 22 is greater than line 21, then line 23 must be zero.

1 Charity payments cannot exceed cost

14015S If Worksheet S-10, line 27.01 is greater than zero, then line 26 must be greater than line 27.01, and line 27 must be less than 27.01.

1 Total facility bad debt must exceed Medicare reimbursable and allowable bad debt

14020S If Worksheet S-10, line 26 is zero then line 27.01 must be zero.

1 No Medicare bad debt if total facility bad debt is zero

Cost Reporting Periods8

Periods beginning prior to 10/1/2016

Periods beginning on or after 10/1/2016

Line 20 “…measured at full charges, for patients, including uninsured patients, who are given a full or partial discount based on the hospital 's charity care policy or FAP for healthcare services delivered during..”

“Enter the actual charge amounts for the entire facility (except physician and other professional services) , of uninsured patients who were given a full or partial discounts…"

Ln 20, col 1(uninsured)

"... charges for non-covered services* provided to patients eligible for Medicaid or other indigent care programs if such inclusion is specified in the hospital 's charity care policy or FAP and the patient meets the hospital's policy criteria."

"...charges for non-covered services* provided to patients eligible for Medicaid or other indigent care programs, if such inclusion is specified in the hospital 's charity care policy or FAP and the patient meets the hospital's policy criteria. The total charges or the portion of total charges is the amount the patient is not responsible for paying...“

Ln 20, col 2(insured)

"... non-covered charges for days exceeding a length-of-stay limit for patients covered by Medicaid or other indigent care programs if such inclusion is specified in the hospital's charity care policy or FAP and the patient meets the hospital's policy criteria."

"...non-covered charges for days exceeding a length-of-stay limit for patients covered by Medicaid or other indigent care programs if such inclusion is specified in the hospital's charity care policy or FAP and the patient meets the hospital's policy criteria."

Line 20 cols 1 & 2

"... do not reduce charges by any payments made for the patient liability; instead report these amounts on line 22."

“Do not record on line 20 net charity care charges; line 20 must include all charges and line 22 must include all receipts.”

* Patient is uninsured for these services

Cost Reporting Periods – Con’t9

Periods beginning prior to 10/1/2016

Periods beginning on or after 10/1/2016

Line 21 (Charity Cost)

Enter in column 1, the cost of patients approved for charity care and uninsured discountsby multiplying line 20, column 1 , times the CCR on line 1. Enter in column 2, the deductibles and

coinsurance not subject to the CCR on line 1 (line 20 minus line 25) plus the non-covered chargesfor insured patients for days exceeding a length-of-stay limit that are subject to the CCR on line 1

(line 25 multiplied by line 1 ) .

Line 22(Payments)

"...enter payments received or expected to be received from patients who have been approved for charity care or uninsured discounts for healthcare services delivered during this cost reporting period."

"...charity care charges or uninsured discounts reported on line 20 include amounts written off with no expectation of payment. Enter all payments received during this cost reporting period, regardless of when the services were provided, from patients for amounts previously written off on line 20 as charity care or uninsured discounts.“ (MedLearn #6)"Do not include grants or other mechanisms of funding for charity care on line 22."

"Payments entered on this line must not exceed charity care or uninsured discount amounts written off in the cost reporting period.“

"Do not include payments received that represent a patient 's liability, or amounts that were not previously written off on line 20 as charity care or uninsured discounts.“(MedLearn #7)

Cost Reporting Periods – Con’t10

Periods beginning prior to 10/1/2016

Periods beginning on or after 10/1/2016

Line 23(Net cost of Charity) For each column, if the amount on line 22 is greater than line 21, enter zero. (Edit 14010S)

Line 26(Total Facility BD)

Enter the total facility (entire hospital complex) amount of bad debts (Medicare bad debts and non-Medicare bad debts), net of recoveries, written off during this cost reporting period on balances owed by patients regardless of the date of service.

Line 27.01(Allowable Mcare

Bad Debts)

"New line: Enter the total facility (entire hospital complex) Medicare allowable bad debts as the sum of….(W/S E Series various lines). The amount entered on this line must also be included in the amount on line 26.”

(Amounts are stated at 65% reimbursement rate.)

Line 28 Calculate the non-Medicare bad debt expense by subtracting line 27.01 from line 26. (Subtracts only the allowable Medicare bad debt, i.e. 35% reduction is included in bad debt expense calc for UC Cost for line 30.)

Line 29 The cost of non-Medicare bad debt expense is calculated by multiplying line 28 by the CCR on line 1. The cost of non-reimbursable Medicare bad debt expense is calculated by subtracting line 27 from line 27. 01 (this amount is not multiplied by the

CCR on line 1). Enter the sum of the non-Medicare bad debt expense and the non-reimbursable Medicare bad debt expense."

MedLearn Examples: 1-3Article Number SE17031

11

Examples 1-3 Assumptions Cost reporting period is on or after 10/1/2016

Charity care policy based on sliding scale of 25% to 100% of patient liability

Insured patient owes $100 deductible for allowable services

Patient applies and is approved for 25% charity

Example 1: Unpaid Insured Patient Liability

Hospital deems $25 as charity care and records amount on line 20, column 2

Remaining balance of $75 may subsequently be classified as charity care or bad debt, but not both.

MedLearn Examples: 1-3 Con’tArticle Number SE17031

12

Example 2: Partial Payment of Insured Patient Liability

Hospital deems $25 as charity care and records amount on line 20, column 2

Patient pays $35 of remaining $75 patient liability.

Remaining $40 can be classified as charity care or bad debt, but not both

If determined to be charity care, amount is recorded on line 20, column 2

If determined to be bad debt, amount is recorded on line 26

MedLearn Examples: 1-3 Con’tArticle Number SE17031

13

Example 3: Partial Payment of Medicare Patient Liability

Hospital deems $25 as charity care and records amount on line 20, column 2

Hospital makes reasonable collection effort on $75 patient liability

Patient pays $35 of remaining $75 patient liability

Hospital determines $40 as Medicare bad debt, recorded on line 26 as hospital bad debt and allowable Medicare bad debt on line 27.01 (gross)

Medicare reimbursable bad debt of $26 ($40 x 65% reimb rate) reflected on line 27

MedLearn Example 4Article Number SE17031

14

Example 4: Partial Payment by Uninsured Patient

Cost reporting period begins on or after 10/1/2016

Charity care policy based on sliding scale of 25% to 100% of patient liability

Patient has $1,000 liability and qualifies for 60% charity

Hospital records $600 as charity on line 20, column 1

Patient pays $100 of remaining $400 liability

Patient does not pay remaining $300, hospital determines amount to be bad debt and records it line 26

Amount paid of $100 is not reported on W/S S-10 since it was a payment toward patient liability, i.e. paid before write off to bad debt

MedLearn Example 5Article Number SE17031

15

Example 5: Partial Payment by Uninsured Patient

Cost reporting period begins prior to 10/1/2016

Charity care policy based on sliding scale of 25% to 100% of patient liability

Patient has $1,000 liability and qualifies for 60% charity

Hospital records $1,000 as charity on line 20, column 1

Remaining $400 liability recorded on line 22 (as an expected payment)

Patient pays $100 of remaining $400 liability

Patient does not pay remaining $300, hospital determines amount to be bad debt and records it line 26

Amount paid of $100 is not reported on W/S S-10 since it was a payment toward patient liability, i.e. paid before write off to bad debt

MedLearn Example 6Article Number SE17031

16

Example 6: Partial Payment by Uninsured Patient

Cost reporting period begins prior to 10/1/2016; payment made during cost reporting period after 10/1/2016

Charity care policy based on sliding scale of 25% to 100% of patient liability

Patient has $1,000 liability and qualifies for 60% charity

Hospital records $1,000 as charity on line 20, column 1 Hospital did not record remaining $400 liability on line 22 as required

The $400 is expected payment

Patient pays $100 during cost reporting period after 10/1/2016 Payment must be recorded on line 22 as a reduction of amount previously

deemed charity

MedLearn Example 7Article Number SE17031

17

Example 7: Uninsured Patient Qualifies for Uninsured

Discount

Cost reporting period begins after 10/1/2016

Uninsured patient owes $100 for allowable hospital service

Hospital has FAP of 30% discount for all uninsured patients

Patient qualifies for $30 discount and records it on line 20, column 1

If $70 remains uncollected and deemed as bad debt, record on line 26

Same scenario in cost reporting period prior to 10/1/2016

Full charges of $100 recorded on line 20, col 1, expected payment of $70 recorded on line 22 as expected payment

If $70 remains uncollected and deemed as bad debt, record on line 26

MedLearn Example 8Article Number SE17031

18

Example 8: Cost of Insured Patients Approved for Charity Cost reporting period begins after 10/1/2016

Cost-to-charge ratio (CCR) is 0.31

Medicaid charges for length-of-stay limit recorded on line 20, column 2, in the amount of $10,000

Charity charges for deductible and coinsurance of $550,000 also recorded on line 20, column 2

Net amount on line 20, column is $560,000

Hospital answers “yes” on line 24 and reports $10,000 on line 25 Cost of charity per line 21 as follows:

$10,000 length-of-stay charges x 0.31 CCR = $3,100 plus

$550,000 deductibles and coinsurance not subject to CCR

Total cost of Insured charity per column 2 = $553,100

Modeling Your Data19

Modeling Your Data: Texas20

Modeling Your Data: Texas ProjectionsData Source: FY17

21