1 us energy market: uni- and bivariate extreme value analysis nik tuzov purdue university ntuzov/ m....

TRANSCRIPT

1

US Energy Market: US Energy Market: uni- and bivariate uni- and bivariate

Extreme Value analysisExtreme Value analysisNik TuzovNik Tuzov

Purdue UniversityPurdue University

http://www.stat.purdue.edu/~ntuzov/http://www.stat.purdue.edu/~ntuzov/

M. Pilar MunozM. Pilar MunozTechnical University of CataloniaTechnical University of Catalonia

[email protected]@upc.edu

22

Structure of US Energy MarketStructure of US Energy Market

Electricity and n/gas are traded at Electricity and n/gas are traded at many locations, but only a few of many locations, but only a few of them are tied to energy derivativesthem are tied to energy derivatives

Physically, trading happens every Physically, trading happens every day but exchanges are closed on day but exchanges are closed on weekendsweekends

Live example:Live example: http://www.powerlytix.com/frontend/landingpage/Power.shtmlhttp://www.powerlytix.com/frontend/landingpage/Power.shtml

33

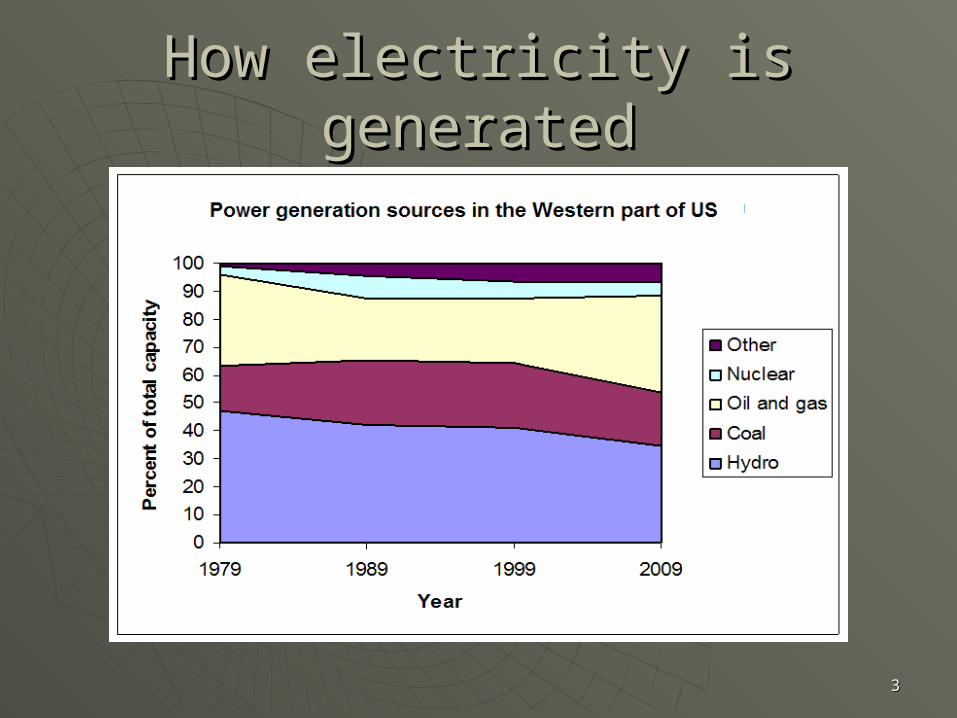

How electricity is generatedHow electricity is generated

44

Possible important factorsPossible important factors Precipitation (for hydro-plants)Precipitation (for hydro-plants) Temperature (affects demand)Temperature (affects demand) Natural Gas priceNatural Gas price Fuel Oil / Heating Oil priceFuel Oil / Heating Oil price Coal priceCoal price Nuclear Fuel PriceNuclear Fuel Price Cost of power plant emissions (emission Cost of power plant emissions (emission

allowances can be purchased via emission allowances can be purchased via emission derivatives)derivatives)

??????

55

Our objectiveOur objective

To check what variables influence To check what variables influence the power price, in particular at the power price, in particular at extreme levelsextreme levels

66

Market Data: NYMEX, CCXMarket Data: NYMEX, CCX

We will utilize daily spot prices from We will utilize daily spot prices from Oct 2001 to March 2008Oct 2001 to March 2008

Data quality issues: Data quality issues: • Daily spot data are not always availableDaily spot data are not always available• Have to construct reasonable Have to construct reasonable

benchmarks (e.g., for nuclear fuel)benchmarks (e.g., for nuclear fuel)• Short history (emission derivatives)Short history (emission derivatives)

77

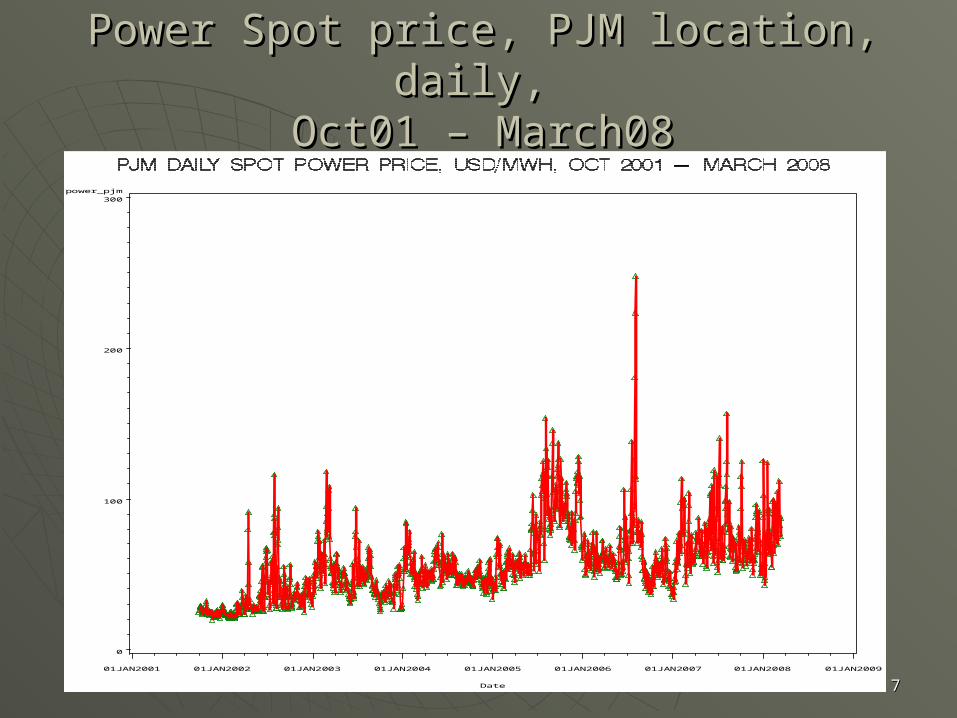

Power Spot price, PJM location, daily, Power Spot price, PJM location, daily, Oct01 – March08Oct01 – March08

power _ pj m

0

100

200

300

Dat e

01J AN2001 01J AN2002 01J AN2003 01J AN2004 01J AN2005 01J AN2006 01J AN2007 01J AN2008 01J AN2009

88

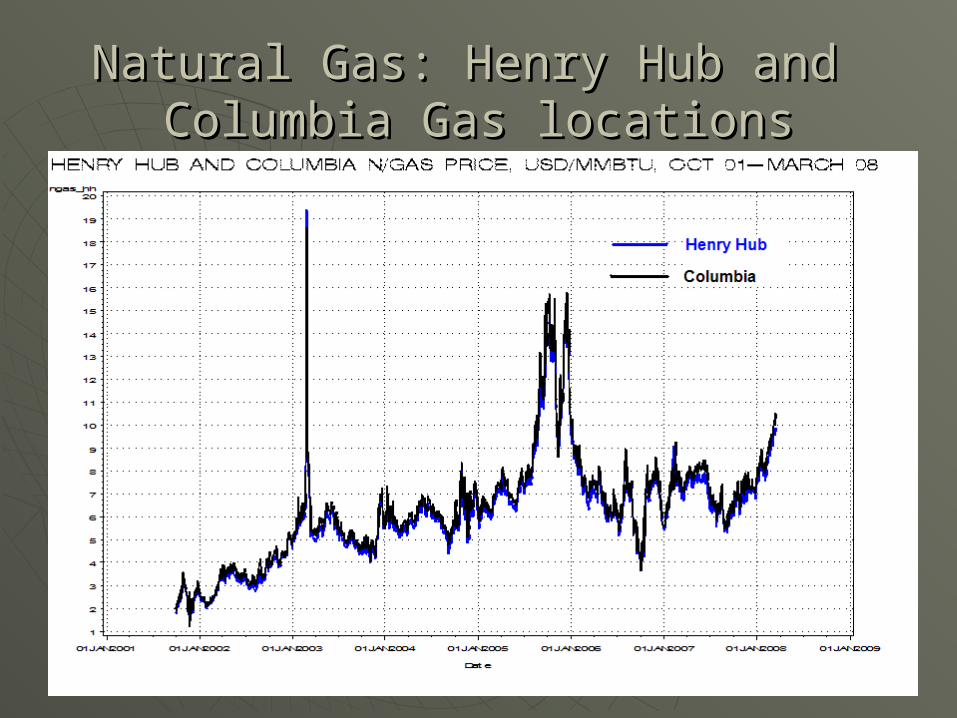

Natural Gas: Henry Hub and Natural Gas: Henry Hub and Columbia Gas locationsColumbia Gas locations

99

Heating Oil Heating Oil (similar in composition to Diesel fuel )(similar in composition to Diesel fuel )

oi l

0

100

200

300

400

Dat e

01J AN2001 01J AN2002 01J AN2003 01J AN2004 01J AN2005 01J AN2006 01J AN2007 01J AN2008 01J AN2009

1010

CoalCoalcoal

20

30

40

50

60

70

80

90

Dat e

01J AN2001 01J AN2002 01J AN2003 01J AN2004 01J AN2005 01J AN2006 01J AN2007 01J AN2008 01J AN2009

1111

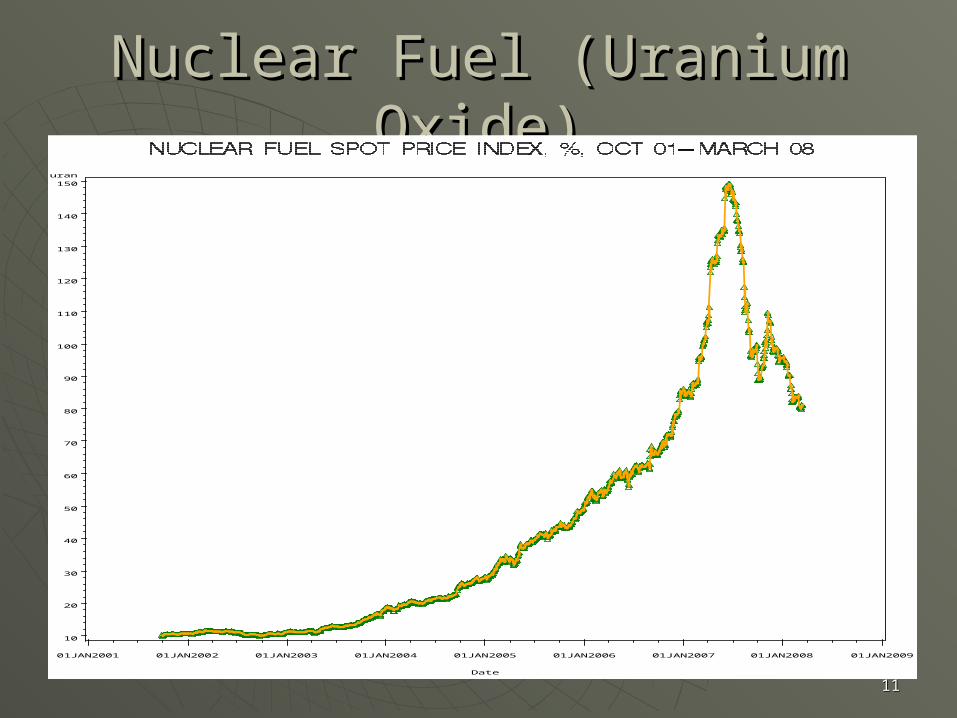

Nuclear Fuel (Uranium Oxide)Nuclear Fuel (Uranium Oxide)ur an

10

20

30

40

50

60

70

80

90

100

110

120

130

140

150

Dat e

01J AN2001 01J AN2002 01J AN2003 01J AN2004 01J AN2005 01J AN2006 01J AN2007 01J AN2008 01J AN2009

1212

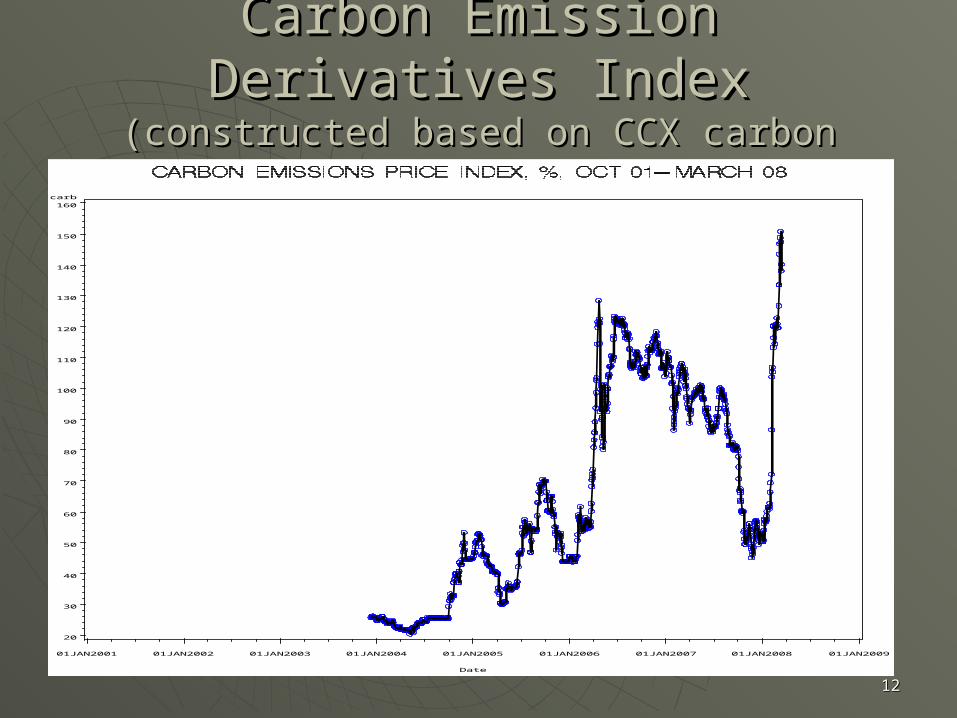

Carbon Emission Derivatives IndexCarbon Emission Derivatives Index(constructed based on CCX carbon vintages)(constructed based on CCX carbon vintages)

car b

20

30

40

50

60

70

80

90

100

110

120

130

140

150

160

Dat e

01J AN2001 01J AN2002 01J AN2003 01J AN2004 01J AN2005 01J AN2006 01J AN2007 01J AN2008 01J AN2009

1313

Sulfur and Nitrogen Emission Indices (CCX)Sulfur and Nitrogen Emission Indices (CCX)sul f

300

400

500

600

700

800

900

1000

1100

1200

1300

1400

1500

1600

1700

Dat e

01J AN2001 01J AN2002 01J AN2003 01J AN2004 01J AN2005 01J AN2006 01J AN2007 01J AN2008 01J AN2009

ni t r o

0

100

200

300

Dat e

01J AN2001 01J AN2002 01J AN2003 01J AN2004 01J AN2005 01J AN2006 01J AN2007 01J AN2008 01J AN2009

1414

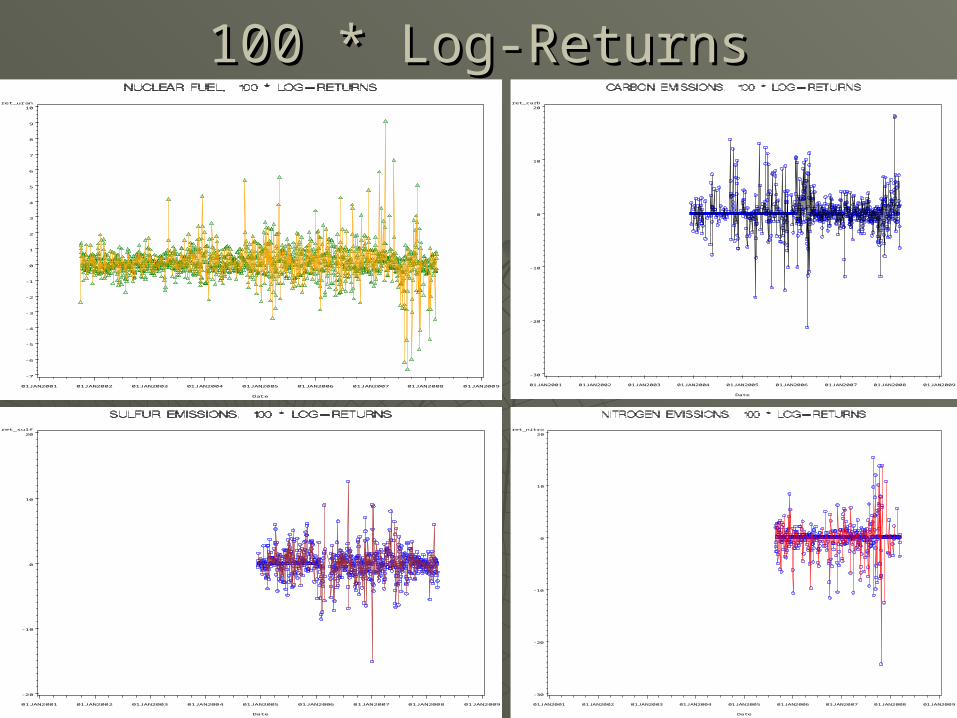

100 * Log-Returns100 * Log-Returnsr et _ power _ pj m

- 90

- 80

- 70

- 60

- 50

- 40

- 30

- 20

- 10

0

10

20

30

40

50

60

70

80

90

100

Dat e

01J AN2001 01J AN2002 01J AN2003 01J AN2004 01J AN2005 01J AN2006 01J AN2007 01J AN2008 01J AN2009

r et _ ngas_ hh

- 60

- 50

- 40

- 30

- 20

- 10

0

10

20

30

40

50

60

70

Dat e

01J AN2001 01J AN2002 01J AN2003 01J AN2004 01J AN2005 01J AN2006 01J AN2007 01J AN2008 01J AN2009

r et _ oi l

- 10

0

10

20

Dat e

01J AN2001 01J AN2002 01J AN2003 01J AN2004 01J AN2005 01J AN2006 01J AN2007 01J AN2008 01J AN2009

r et _ coal

- 20

- 10

0

10

20

Dat e

01J AN2001 01J AN2002 01J AN2003 01J AN2004 01J AN2005 01J AN2006 01J AN2007 01J AN2008 01J AN2009

1515

100 * Log-Returns100 * Log-Returnsr et _ ur an

- 7

- 6

- 5

- 4

- 3

- 2

- 1

0

1

2

3

4

5

6

7

8

9

10

Dat e

01J AN2001 01J AN2002 01J AN2003 01J AN2004 01J AN2005 01J AN2006 01J AN2007 01J AN2008 01J AN2009

r et _ car b

- 30

- 20

- 10

0

10

20

Dat e

01J AN2001 01J AN2002 01J AN2003 01J AN2004 01J AN2005 01J AN2006 01J AN2007 01J AN2008 01J AN2009

r et _ sul f

- 20

- 10

0

10

20

Dat e

01J AN2001 01J AN2002 01J AN2003 01J AN2004 01J AN2005 01J AN2006 01J AN2007 01J AN2008 01J AN2009

r et _ ni t r o

- 30

- 20

- 10

0

10

20

Dat e

01J AN2001 01J AN2002 01J AN2003 01J AN2004 01J AN2005 01J AN2006 01J AN2007 01J AN2008 01J AN2009

1616

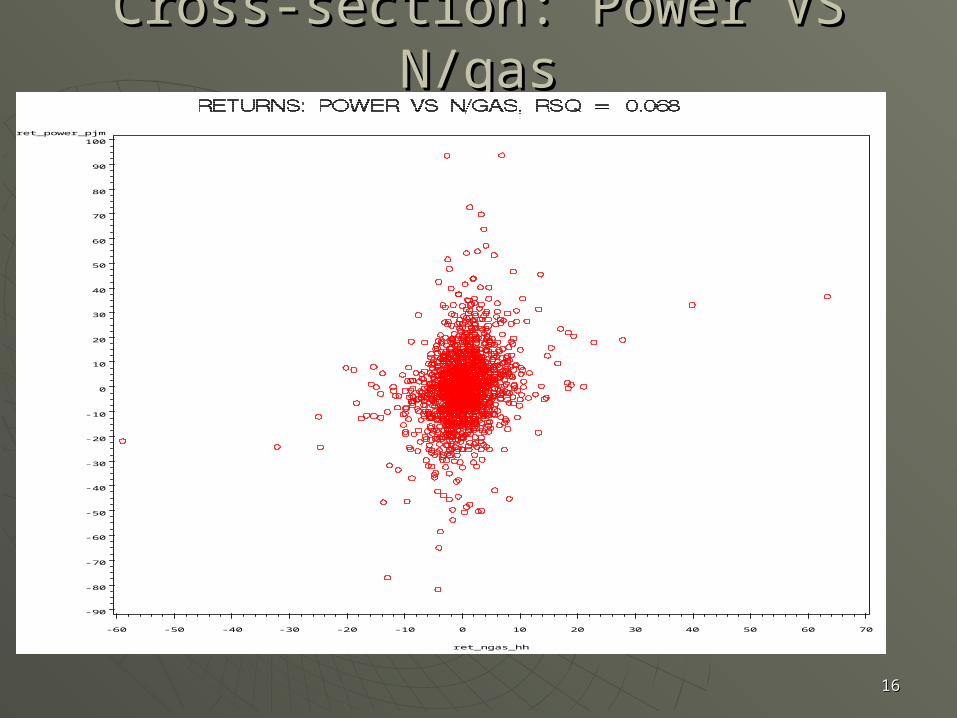

Cross-section: Power VS N/gasCross-section: Power VS N/gas

r et _ power _ pj m

- 90

- 80

- 70

- 60

- 50

- 40

- 30

- 20

- 10

0

10

20

30

40

50

60

70

80

90

100

r et _ ngas_ hh

- 60 - 50 - 40 - 30 - 20 - 10 0 10 20 30 40 50 60 70

1717

Cross-section: Power VS OilCross-section: Power VS Oilr et _ power _ pj m

- 90

- 80

- 70

- 60

- 50

- 40

- 30

- 20

- 10

0

10

20

30

40

50

60

70

80

90

100

r et _ oi l

- 10 0 10 20

1818

Cross-sectional analysisCross-sectional analysis

Other scatterplots are similar with a very Other scatterplots are similar with a very low Rsqlow Rsq

““Naïve” regression of returns Naïve” regression of returns

Power = b0 + b1 * N/gas + b2 * Oil + b3 * Coal + b4 * Nuclear + Power = b0 + b1 * N/gas + b2 * Oil + b3 * Coal + b4 * Nuclear + b5 * Carbon + b6 *Sulfur + b7 * Nitrogen + Errorb5 * Carbon + b6 *Sulfur + b7 * Nitrogen + Error

Has Rsq of 6-10%, all of it due to N/gasHas Rsq of 6-10%, all of it due to N/gas

More advanced analysis to followMore advanced analysis to follow

1919

Univariate Time Series analysis - PowerUnivariate Time Series analysis - Power

- 90 - 80 - 70 - 60 - 50 - 40 - 30 - 20 - 10 0 10 20 30 40 50 60 70 80 90 100

0

5

10

15

20

25

30

35

40

Percent

r et _ power _ pj m

- 4 - 3 - 2 - 1 0 1 2 3 4

- 100

- 75

- 50

- 25

0

25

50

75

100

ret_power_pjm

Nor mal Quant i l es

2020

Univariate Time Series analysis - PowerUnivariate Time Series analysis - Power

2121

AR(p,q)-GARCH(p’,q’), EGARCH, AR(p,q)-GARCH(p’,q’), EGARCH, GARCH-m with normal and GARCH-m with normal and

t-distributions have been fitted t-distributions have been fitted

(SAS proc autoreg)(SAS proc autoreg)

Best model: AR(5,6) – GARCH(1,1), Best model: AR(5,6) – GARCH(1,1), normal, 10 non-zero parametersnormal, 10 non-zero parameters

Univariate Time Series analysis - PowerUnivariate Time Series analysis - Power

2222

Diagnostics for standardized residuals - PowerDiagnostics for standardized residuals - Power

2323

Diagnostics for standardized residuals - PowerDiagnostics for standardized residuals - Power

- 4 - 3 - 2 - 1 0 1 2 3 4

- 6

- 4

- 2

0

2

4

6

8

std_res

Nor mal Quant i l es

Serial correlation is much reduced, but Serial correlation is much reduced, but fat tails persistfat tails persist

2424

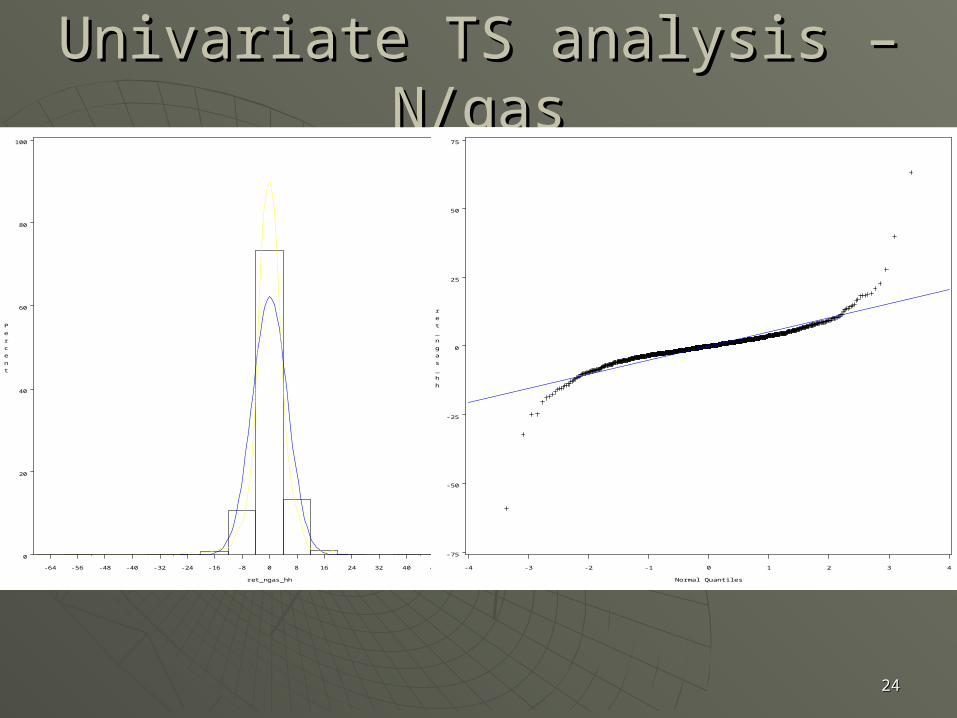

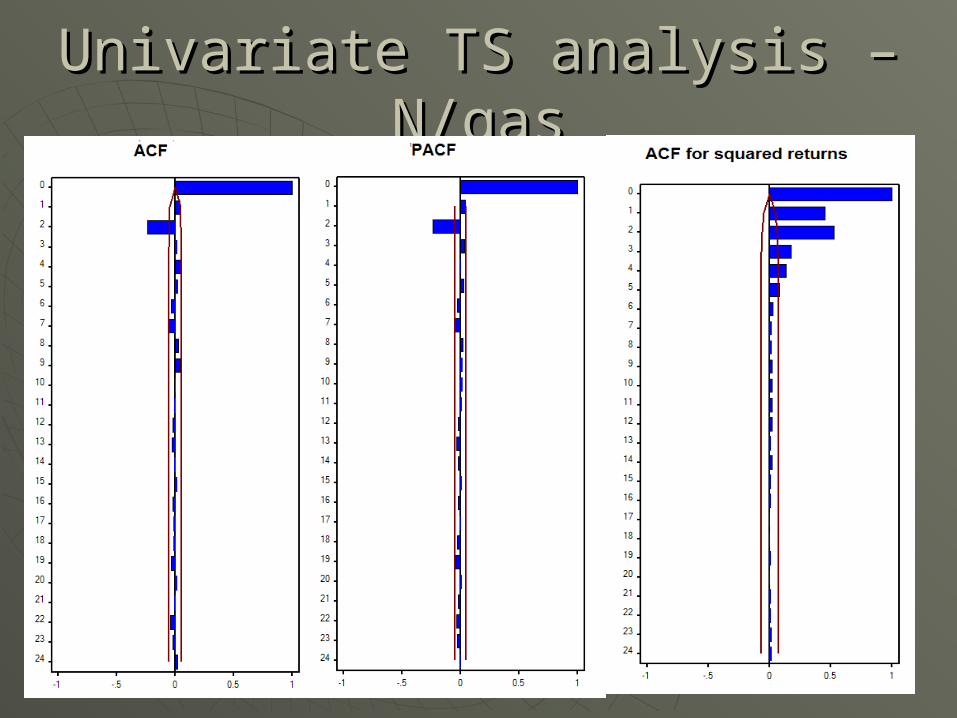

Univariate TS analysis – N/gasUnivariate TS analysis – N/gas

- 64 - 56 - 48 - 40 - 32 - 24 - 16 - 8 0 8 16 24 32 40 48 56 64

0

20

40

60

80

100

Percent

r et _ ngas_ hh

- 4 - 3 - 2 - 1 0 1 2 3 4

- 75

- 50

- 25

0

25

50

75

ret_ngas_hh

Nor mal Quant i l es

2525

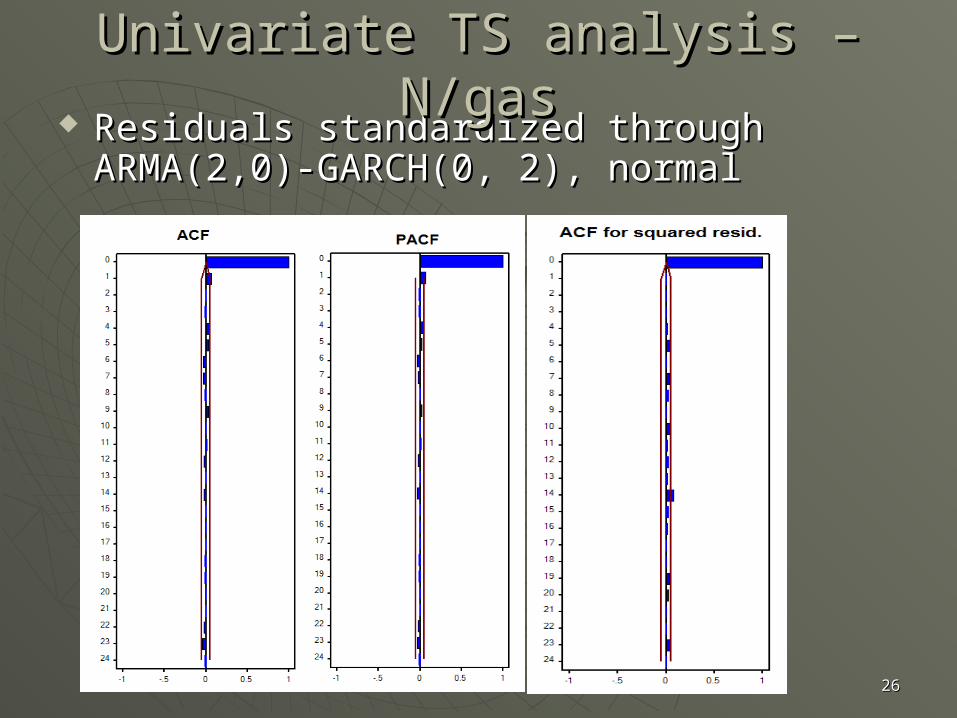

Univariate TS analysis – N/gasUnivariate TS analysis – N/gas

2626

Residuals standardized through Residuals standardized through ARMA(2,0)-GARCH(0, 2), normalARMA(2,0)-GARCH(0, 2), normal

Univariate TS analysis – N/gasUnivariate TS analysis – N/gas

2727

same problem as with power returnssame problem as with power returns

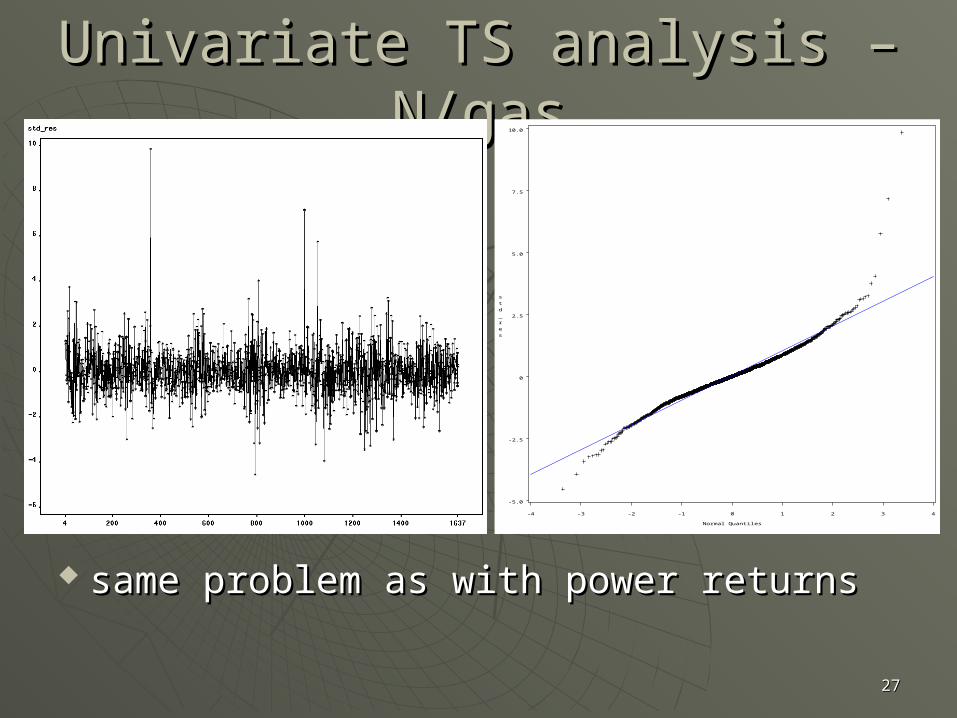

Univariate TS analysis – N/gasUnivariate TS analysis – N/gas

- 4 - 3 - 2 - 1 0 1 2 3 4

- 5. 0

- 2. 5

0

2. 5

5. 0

7. 5

10. 0

std_res

Nor mal Quant i l es

2828

Extreme Value analysisExtreme Value analysis

Interested in extremely negative power Interested in extremely negative power returnsreturns

Therefore, will utilize standardized Therefore, will utilize standardized residuals of power and n/gas series residuals of power and n/gas series multiplied by (-1)multiplied by (-1)

Apply Peaks-Over-Threshold (POT) to Apply Peaks-Over-Threshold (POT) to power and n/gas separately and then power and n/gas separately and then jointlyjointly

2929

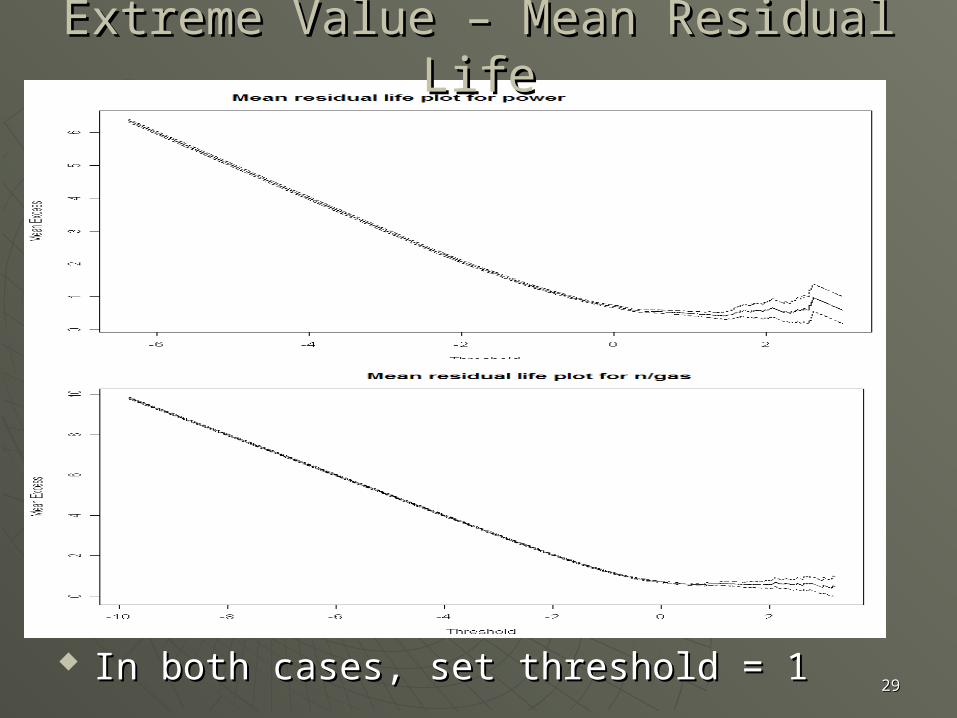

In both cases, set threshold = 1In both cases, set threshold = 1

Extreme Value – Mean Residual LifeExtreme Value – Mean Residual Life

3030

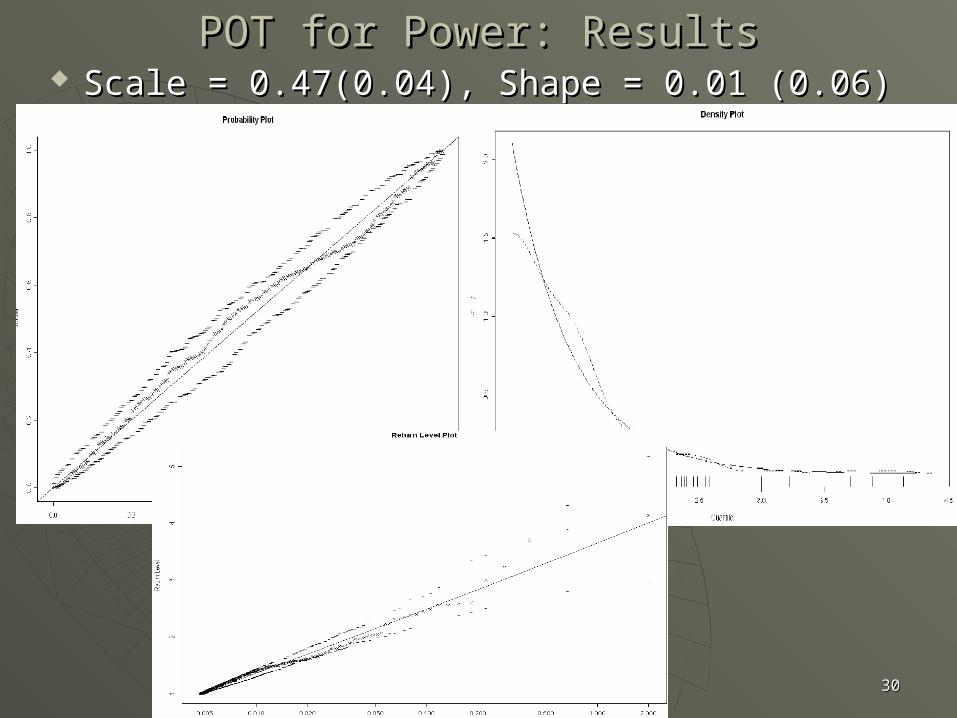

POT for Power: ResultsPOT for Power: Results Scale = 0.47(0.04), Shape = 0.01 (0.06)Scale = 0.47(0.04), Shape = 0.01 (0.06)

3131

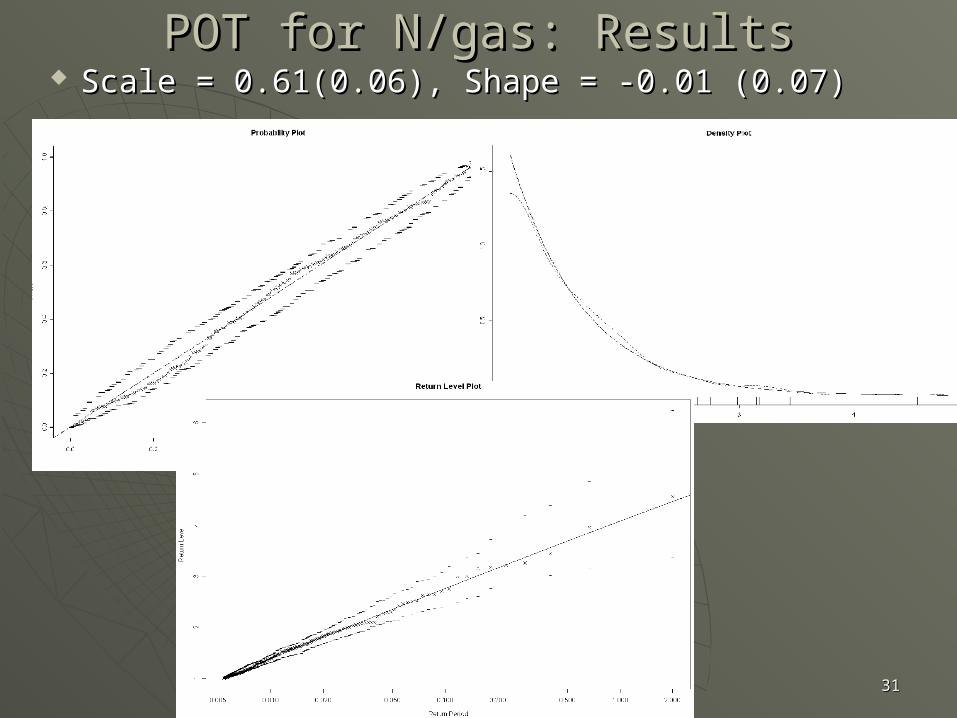

POT for N/gas: ResultsPOT for N/gas: Results Scale = 0.61(0.06), Shape = -0.01 (0.07)Scale = 0.61(0.06), Shape = -0.01 (0.07)

3232

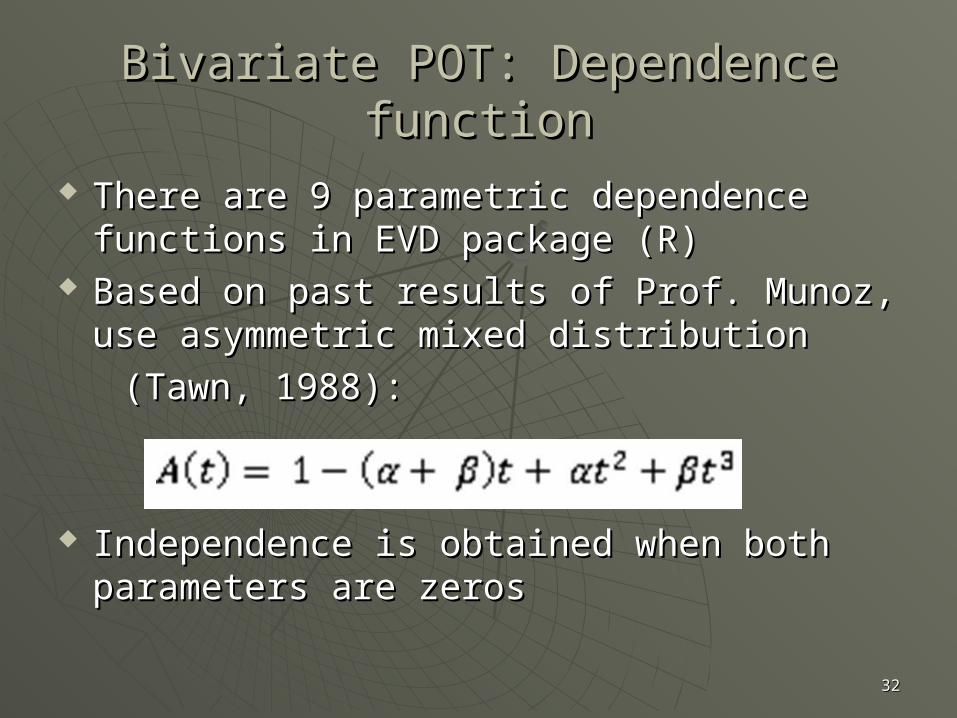

Bivariate POT: Dependence functionBivariate POT: Dependence function

There are 9 parametric dependence There are 9 parametric dependence functions in EVD package (R)functions in EVD package (R)

Based on past results of Prof. Munoz, use Based on past results of Prof. Munoz, use asymmetric mixed distribution asymmetric mixed distribution

(Tawn, 1988):(Tawn, 1988):

Independence is obtained when both Independence is obtained when both parameters are zerosparameters are zeros

3333

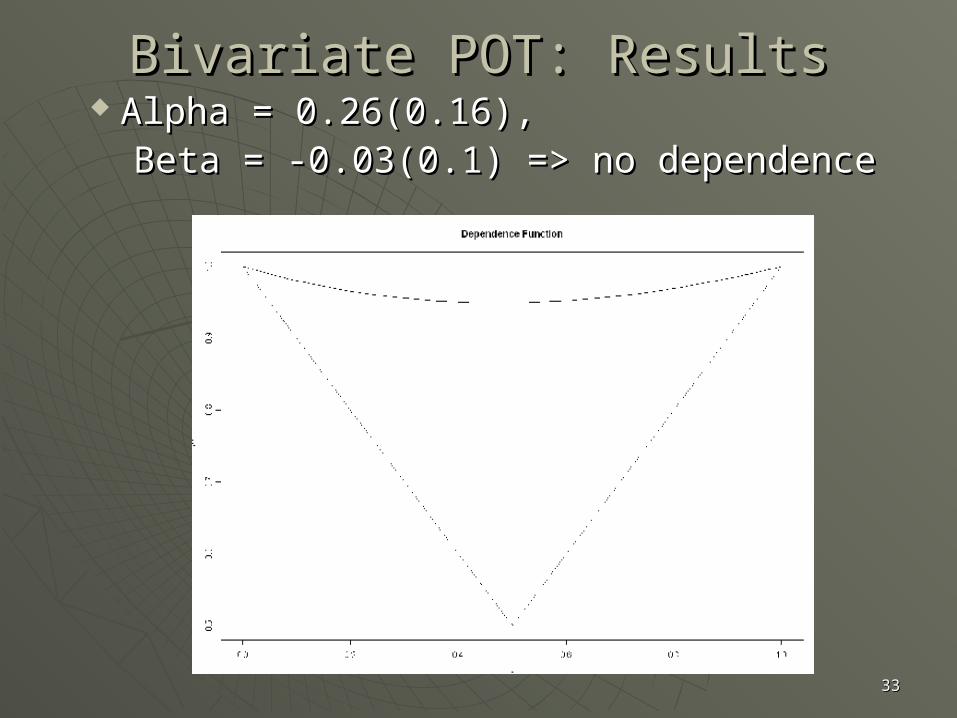

Bivariate POT: ResultsBivariate POT: Results Alpha = 0.26(0.16), Alpha = 0.26(0.16), Beta = -0.03(0.1) => no dependenceBeta = -0.03(0.1) => no dependence

3434

Bivariate POT: ResultsBivariate POT: Results

However, there can be dependence in the bottom-left However, there can be dependence in the bottom-left corner corner

3535

Further researchFurther research

Investigate the rest of dataInvestigate the rest of data Look into other types of dependence Look into other types of dependence

functionsfunctions Incorporate temperature and Incorporate temperature and

precipitation variablesprecipitation variables Try to model volatility of power Try to model volatility of power

returns using the other variablesreturns using the other variables

3636

Data sources & ReferencesData sources & References Bloomberg (terminal access)Bloomberg (terminal access)

Exchanges:Exchanges:

• http://www.nymex.com/index.aspxhttp://www.nymex.com/index.aspx

• http://www.chicagoclimatex.com/http://www.chicagoclimatex.com/

US power and n/gas real time grids:US power and n/gas real time grids: http://www.powerlytix.com/frontend/landingpage/Power.shtmlhttp://www.powerlytix.com/frontend/landingpage/Power.shtml

Presentation of Prof. Munoz:Presentation of Prof. Munoz: http://www.samsi.info/200708/risk/presentations/0124/pilar%20munoz-gracia.pdfhttp://www.samsi.info/200708/risk/presentations/0124/pilar%20munoz-gracia.pdf

Other Web sources:Other Web sources: • www.pjm.comwww.pjm.com

• http://www.ferc.gov/http://www.ferc.gov/

• https://www.theice.com/indices.jhtmhttps://www.theice.com/indices.jhtm