1 takehome one 2008. 2 3 month treasury bill rate

Post on 19-Dec-2015

220 views

TRANSCRIPT

11

Takehome OneTakehome One

20082008

22

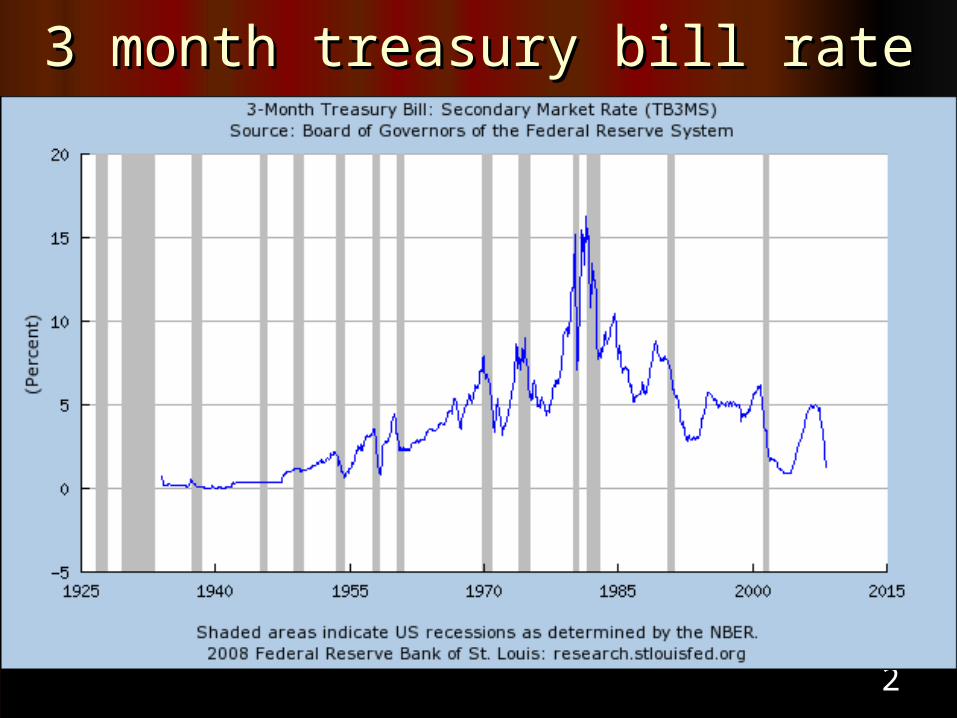

3 month treasury bill rate3 month treasury bill rate

33

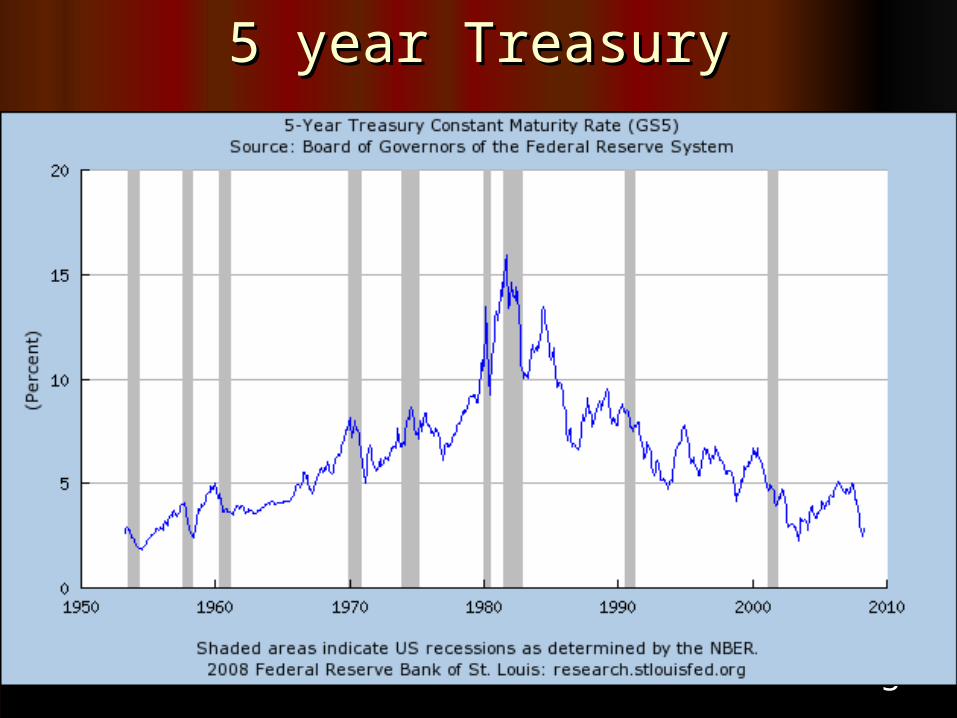

5 year Treasury5 year Treasury

44

0

4

8

12

16

20

55 60 65 70 75 80 85 90 95 00 05

GS5 TB3MS

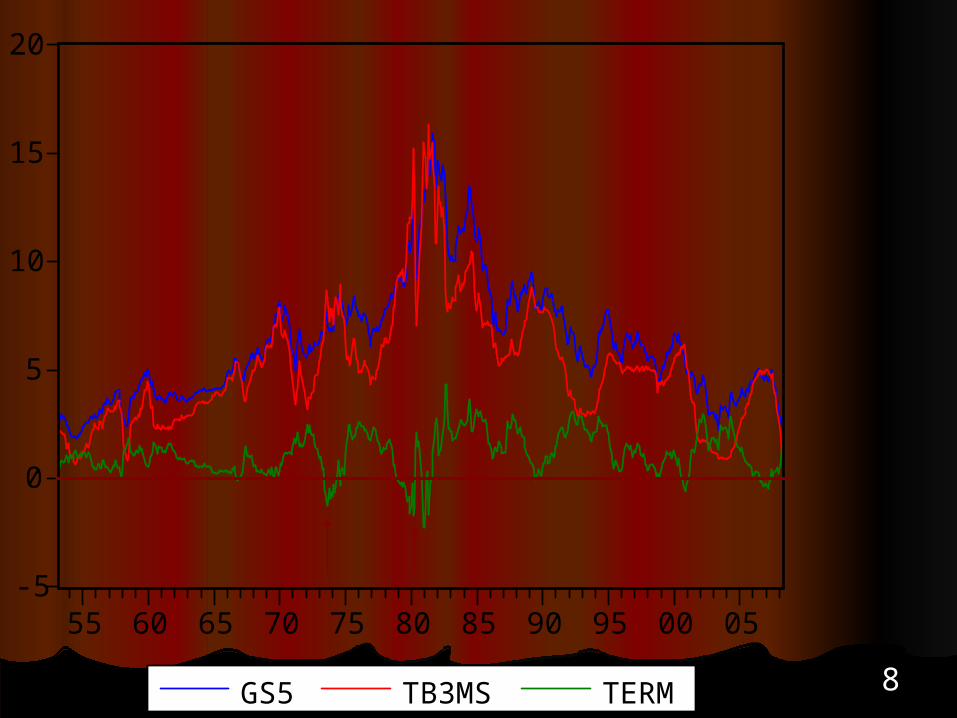

3 month bill and 5 year treasury: April 1953-April 2008

55

66

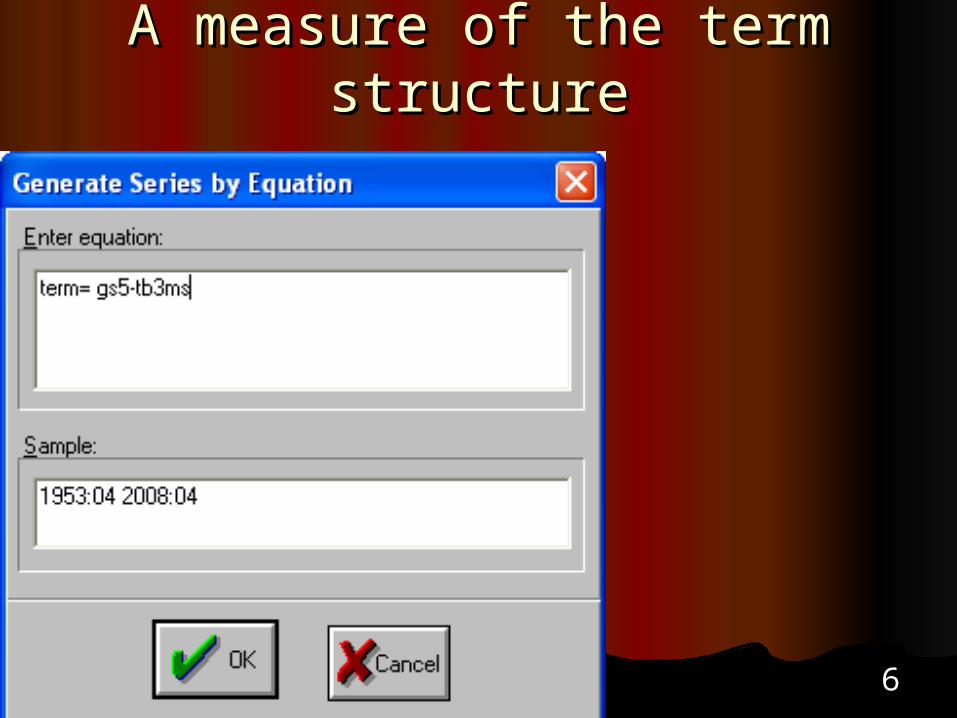

A measure of the term structureA measure of the term structure

77

-4

-2

0

2

4

6

55 60 65 70 75 80 85 90 95 00 05

TERM

term = GS5 - TB3MS

88

-5

0

5

10

15

20

55 60 65 70 75 80 85 90 95 00 05

GS5 TB3MS TERM

99

1. You should try this so that you know at least one way of obtaining time series from FRED. If you have difficulty, an Excel file called Takeone, is available on the class page.2. Generate a time series called term that is the difference between GS5 and TB3MS.3. Is term stationary, i.e. are GS5 and TB3ms co-integrated?4. Is term normally distributed?5. Estimate your best autoregressive model for term.6. Estimate your best ARMA model for term through April 2007 and see how well a forecast for this model fits the next 12 months.7. Re-estimate your best model for term through April 2008 and forecast for the remaining months of 2008.

Questions: Takehome OneQuestions: Takehome One

1010

0

20

40

60

80

2 4 6 8 10 12 14 16

Series: GS5Sample 1953:04 2008:04Observations 661

Mean 6.240393Median 5.850000Maximum 15.93000Minimum 1.850000Std. Dev. 2.756402Skewness 0.978683Kurtosis 3.850276

Jarque-Bera 125.4318Probability 0.000000

GS5: Rate for Five Year Treasury

Histogram and Stats for Five Histogram and Stats for Five YearYear

1111

1212

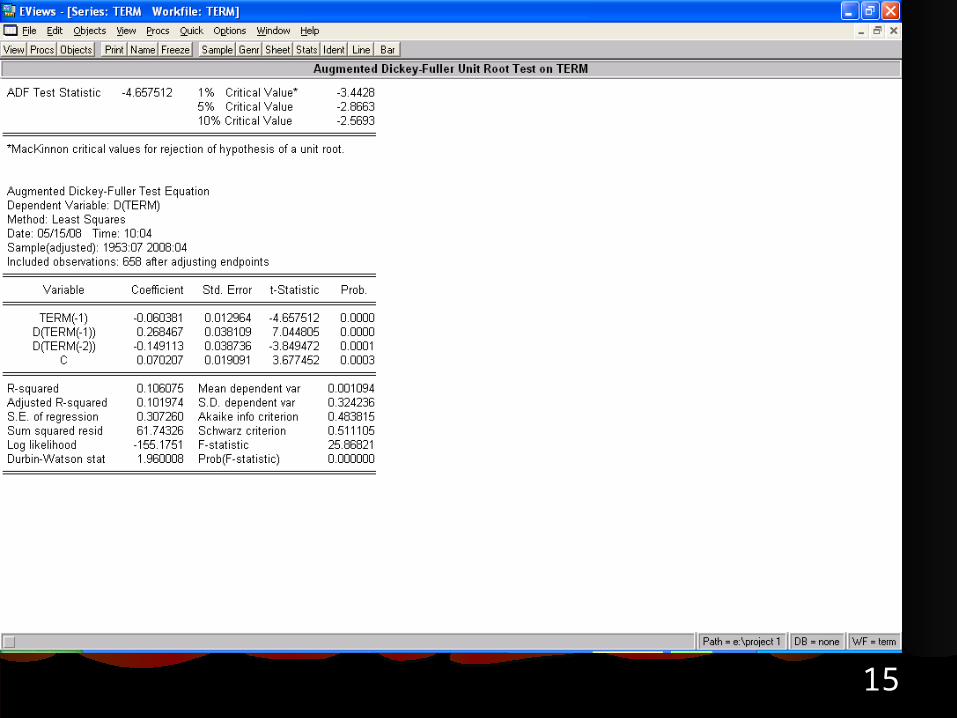

Unit Root test for GS5Unit Root test for GS5

1313

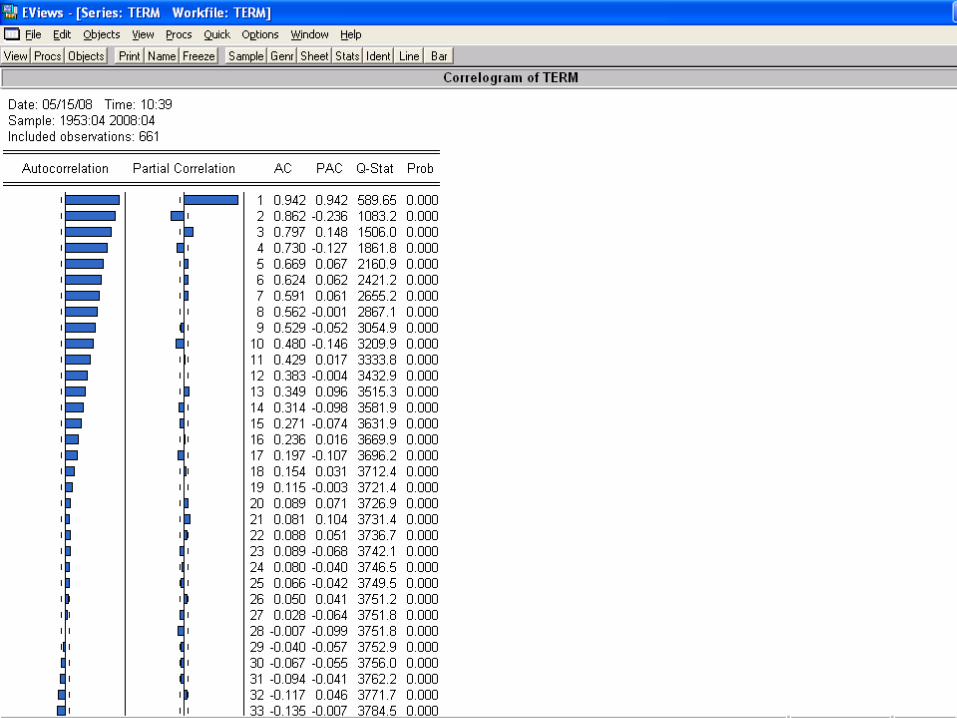

Histogram and Stats for TermHistogram and Stats for Term

0

20

40

60

80

100

-2 -1 0 1 2 3 4

Series: TERMSample 1953:04 2008:04Observations 661

Mean 1.146051Median 1.130000Maximum 4.330000Minimum -2.250000Std. Dev. 0.957974Skewness -0.045212Kurtosis 3.247015

Jarque-Bera 1.905692Probability 0.385642

Histogram and Stats for Term = GS5 - TB3ms

1414

1515

1616

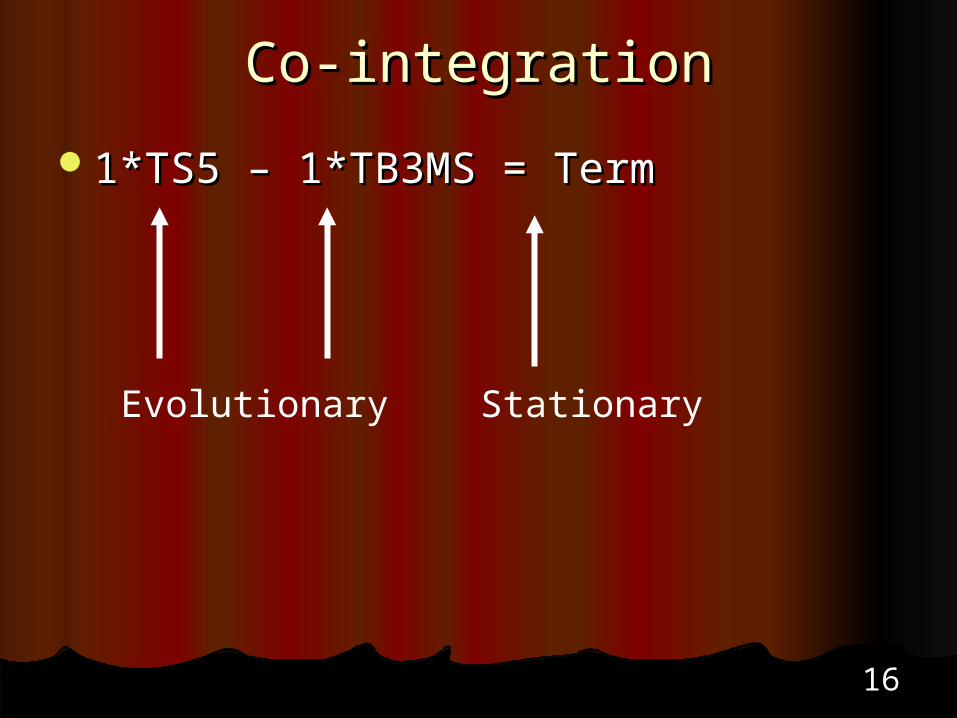

Co-integrationCo-integration

1*TS5 – 1*TB3MS = Term1*TS5 – 1*TB3MS = Term

Evolutionary Stationary

1717

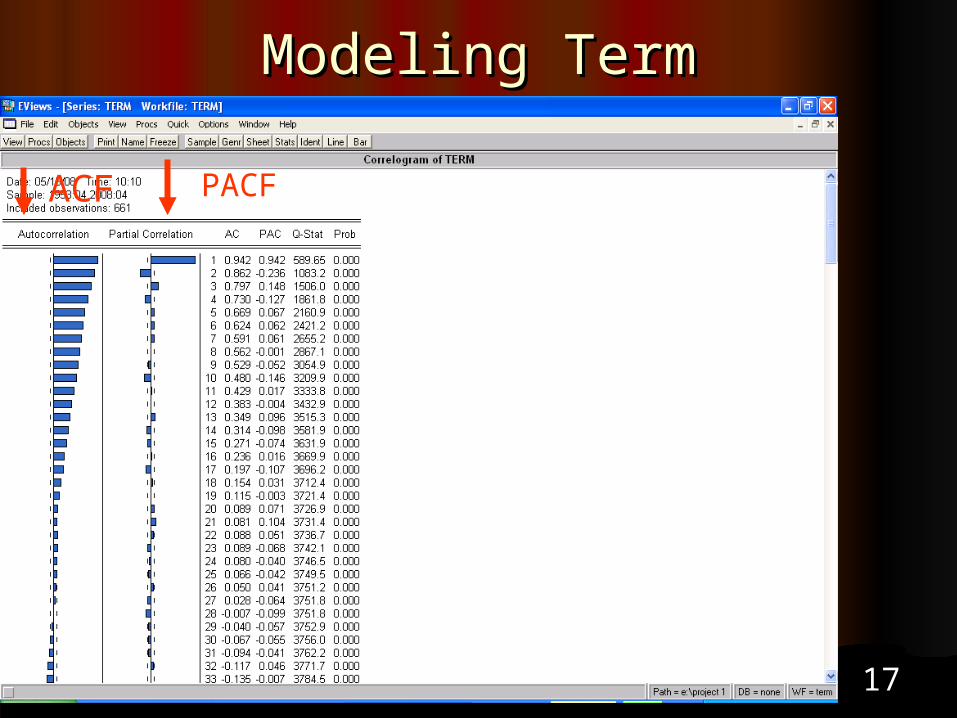

Modeling TermModeling Term

PACFACF

1818

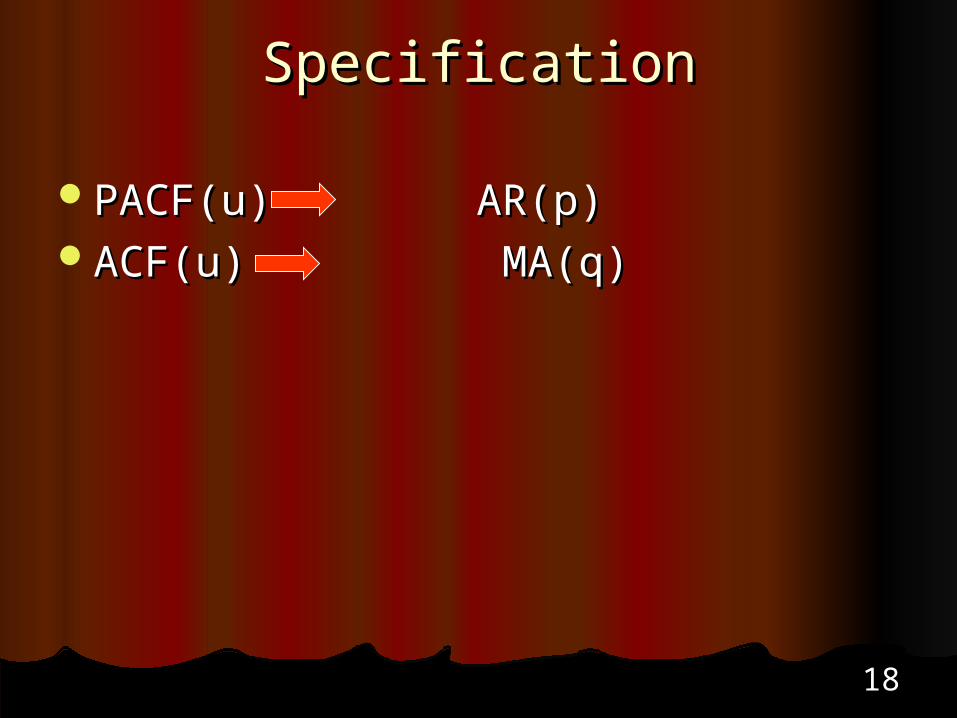

SpecificationSpecification

PACF(u) AR(p)PACF(u) AR(p)ACF(u) MA(q) ACF(u) MA(q)

1919

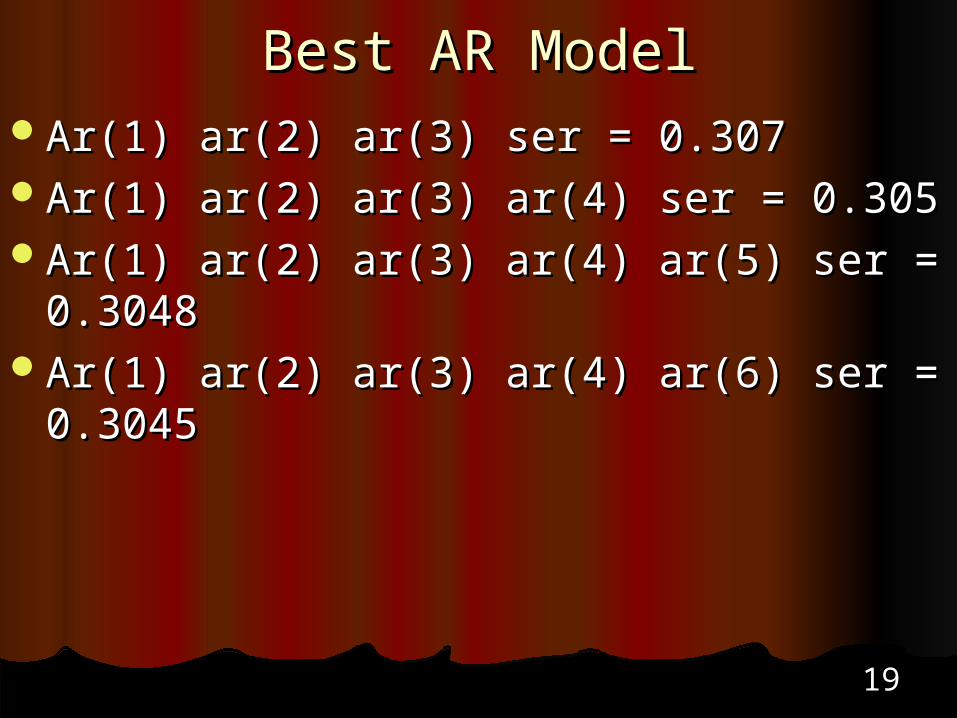

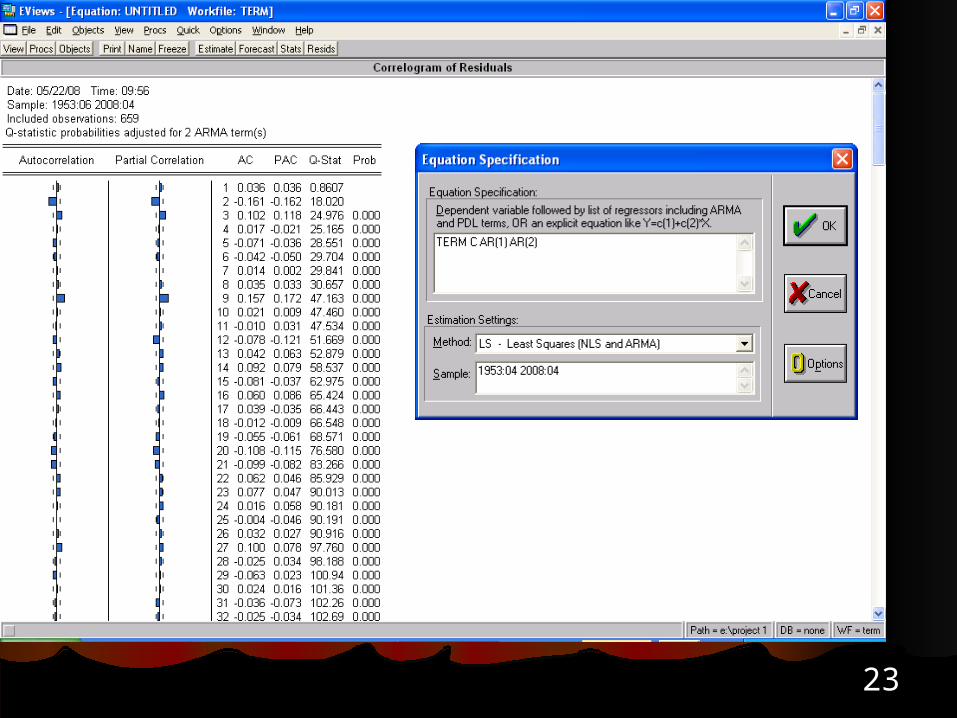

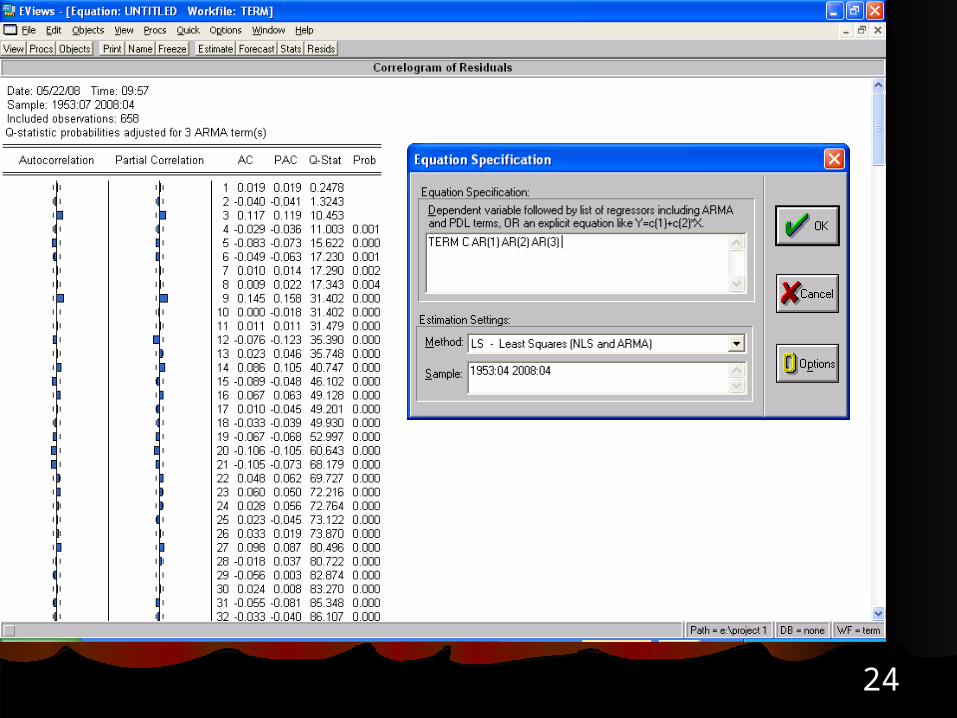

Best AR ModelBest AR ModelAr(1) ar(2) ar(3) ser = 0.307Ar(1) ar(2) ar(3) ser = 0.307Ar(1) ar(2) ar(3) ar(4) ser = 0.305Ar(1) ar(2) ar(3) ar(4) ser = 0.305Ar(1) ar(2) ar(3) ar(4) ar(5) ser = 0.3048Ar(1) ar(2) ar(3) ar(4) ar(5) ser = 0.3048Ar(1) ar(2) ar(3) ar(4) ar(6) ser = 0.3045Ar(1) ar(2) ar(3) ar(4) ar(6) ser = 0.3045

2020

2121

2222

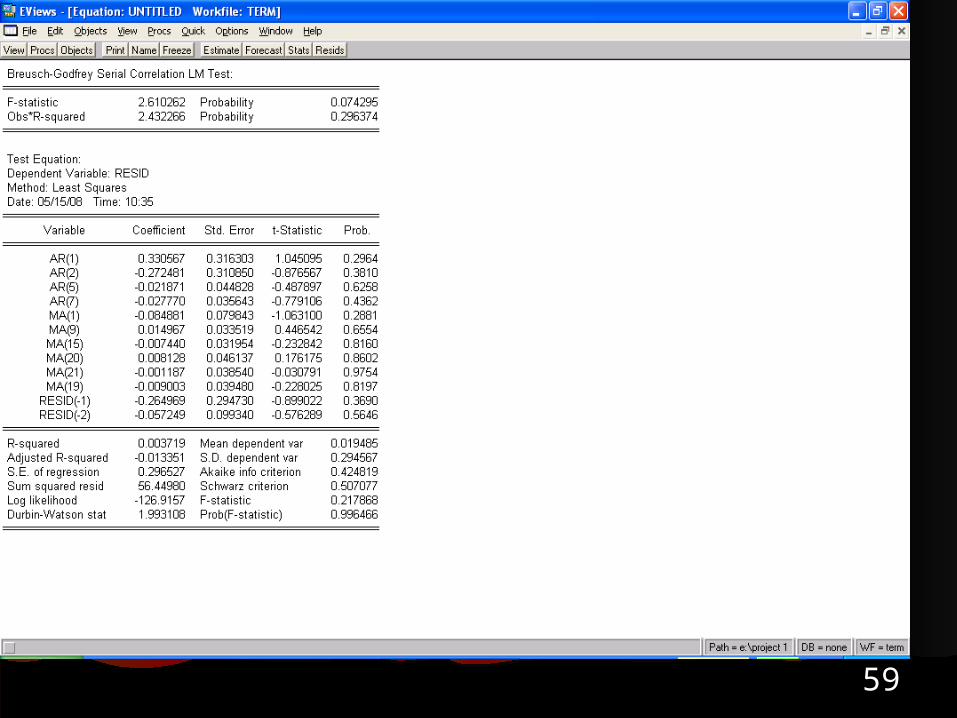

SpecificationSpecificationAr(1) ar(2) : look at residualsAr(1) ar(2) : look at residualsAr(1) ar(2) ar(3) : look at residualsAr(1) ar(2) ar(3) : look at residualsAr(1) ar(2) ar(3) ma(3) : look at Ar(1) ar(2) ar(3) ma(3) : look at

residualsresidualsAr(1) ar(2) ar(3) ma(3) ma(9) : look at Ar(1) ar(2) ar(3) ma(3) ma(9) : look at

residualsresidualsADD MA(15)ADD MA(15)ADD MA(20)ADD MA(20)ADD MA(21), ser = 0.295ADD MA(21), ser = 0.295

2323

2424

2525

2626

2727

2828

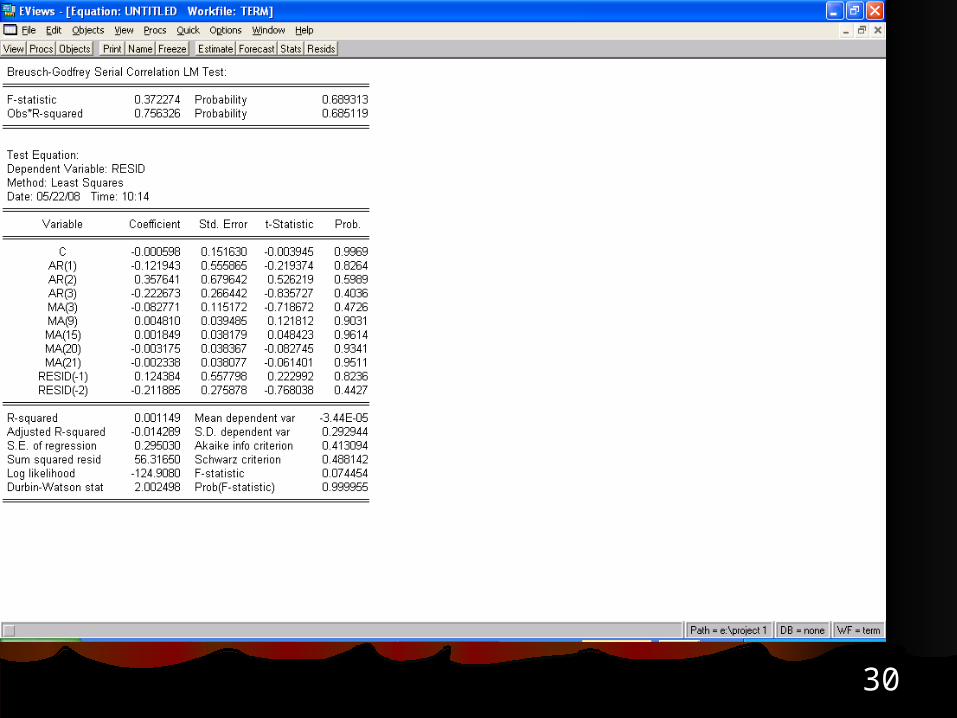

ValidationValidationCorrelogram of residualsCorrelogram of residualsActual, fitted & residual graphActual, fitted & residual graphSerial correlation testSerial correlation testHistogram of residualsHistogram of residuals

2929

3030

3131

0

40

80

120

160

-2.0 -1.5 -1.0 -0.5 0.0 0.5 1.0 1.5 2.0

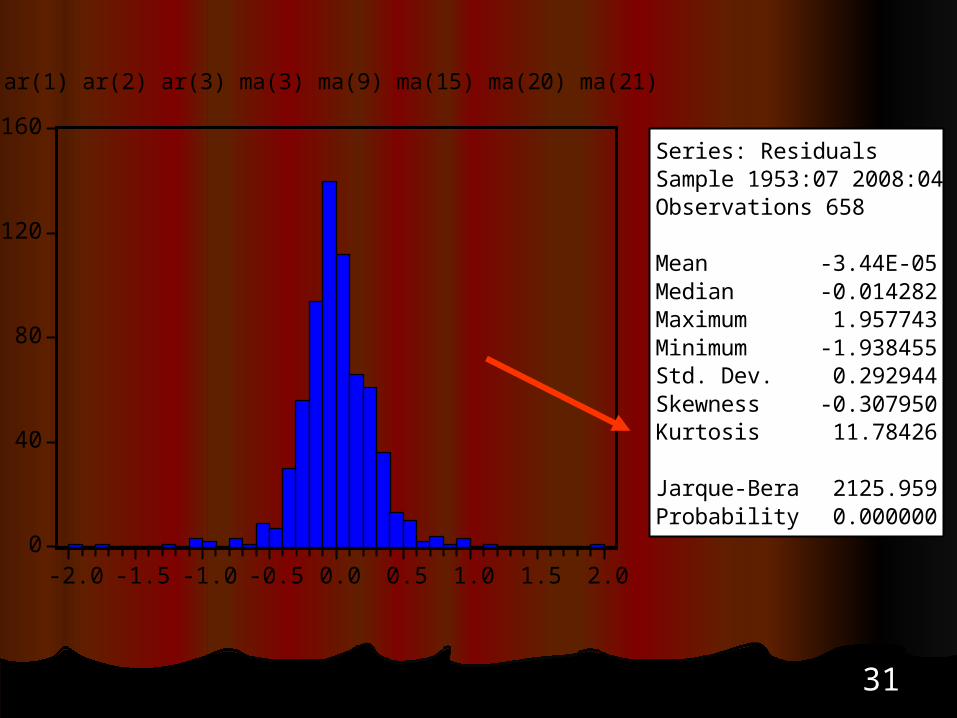

Series: ResidualsSample 1953:07 2008:04Observations 658

Mean -3.44E-05Median -0.014282Maximum 1.957743Minimum -1.938455Std. Dev. 0.292944Skewness -0.307950Kurtosis 11.78426

Jarque-Bera 2125.959Probability 0.000000

ar(1) ar(2) ar(3) ma(3) ma(9) ma(15) ma(20) ma(21)

3232

Within Sample ForecastingWithin Sample Forecasting

Re-estimate model from 1953:04 -Re-estimate model from 1953:04 -2007:042007:04

3333

-2

-1

0

1

2

3

07:05 07:07 07:09 07:11 08:01 08:03

TERMF ± 2 S.E.

Forecast: TERMFActual: TERMSample: 2007:05 2008:04Include observations: 12

Root Mean Squared Error 0.301040Mean Absolute Error 0.208092Mean Abs. Percent Error 60.36766Theil Inequality Coefficient 0.261678 Bias Proportion 0.148157 Variance Proportion 0.158776 Covariance Proportion 0.693066

In sample forecast: 2007:04-In sample forecast: 2007:04-2008:042008:04

3434

3535

Sample: 2005:01 – 2008:04

Quick menu: show

3636

In sample forecastIn sample forecast

-2

-1

0

1

2

3

05:01 05:07 06:01 06:07 07:01 07:07 08:01

TERMFORECAST

FORECAST+2*SEFFORECAST-2*SEF

In sample forecast

3737

Out of sample forecastOut of sample forecastProcs: expand 1953:04 – 2008:12Procs: expand 1953:04 – 2008:12Sample 1953:04 – 2008:12Sample 1953:04 – 2008:12

3838

Out of Sample ForecastOut of Sample Forecast

0

1

2

3

4

08:05 08:06 08:07 08:08 08:09 08:10 08:11 08:12

TERMF ± 2 S.E.

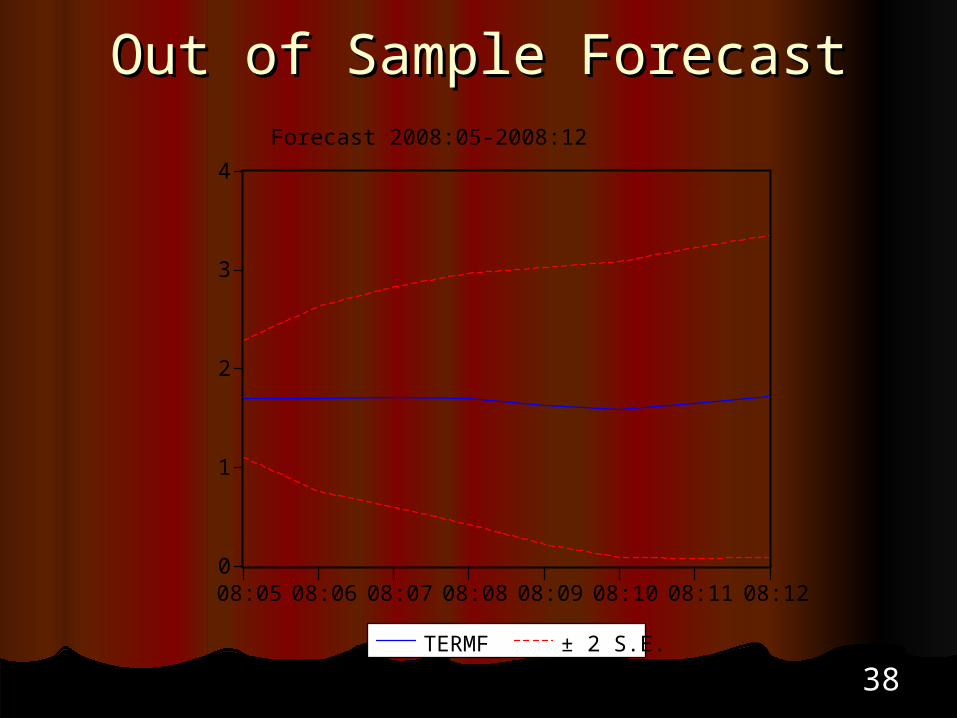

Forecast 2008:05-2008:12

3939

4040

Out of Sample ForecastOut of Sample Forecast

-1

0

1

2

3

4

00 01 02 03 04 05 06 07 08

TERMFORECAST

FORECAST+2*SEFFORECAST-2*SEF

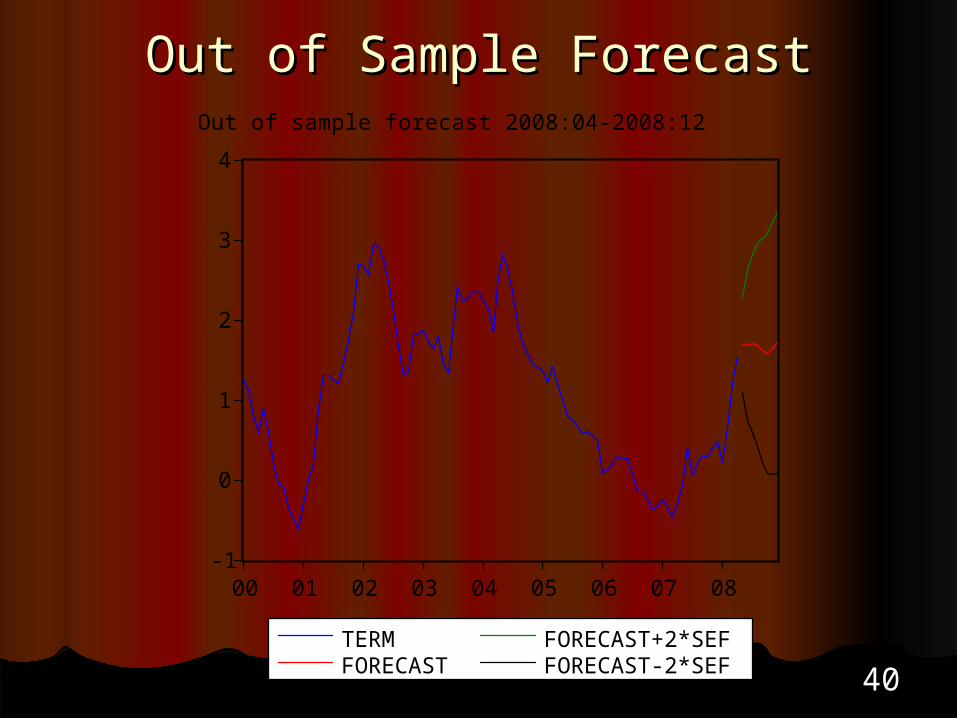

Out of sample forecast 2008:04-2008:12

4141

ARCHARCH

0

40

80

120

160

-2.0 -1.5 -1.0 -0.5 0.0 0.5 1.0 1.5 2.0

Series: ResidualsSample 1953:07 2008:04Observations 658

Mean -3.44E-05Median -0.014282Maximum 1.957743Minimum -1.938455Std. Dev. 0.292944Skewness -0.307950Kurtosis 11.78426

Jarque-Bera 2125.959Probability 0.000000

4242

4343

-4

-2

0

2

4

6

55 60 65 70 75 80 85 90 95 00 05

TERM RESQ

ARCH: Noisy Residuals when term goes negative

ARCH: when Inverted Term ARCH: when Inverted Term StructureStructure

4444

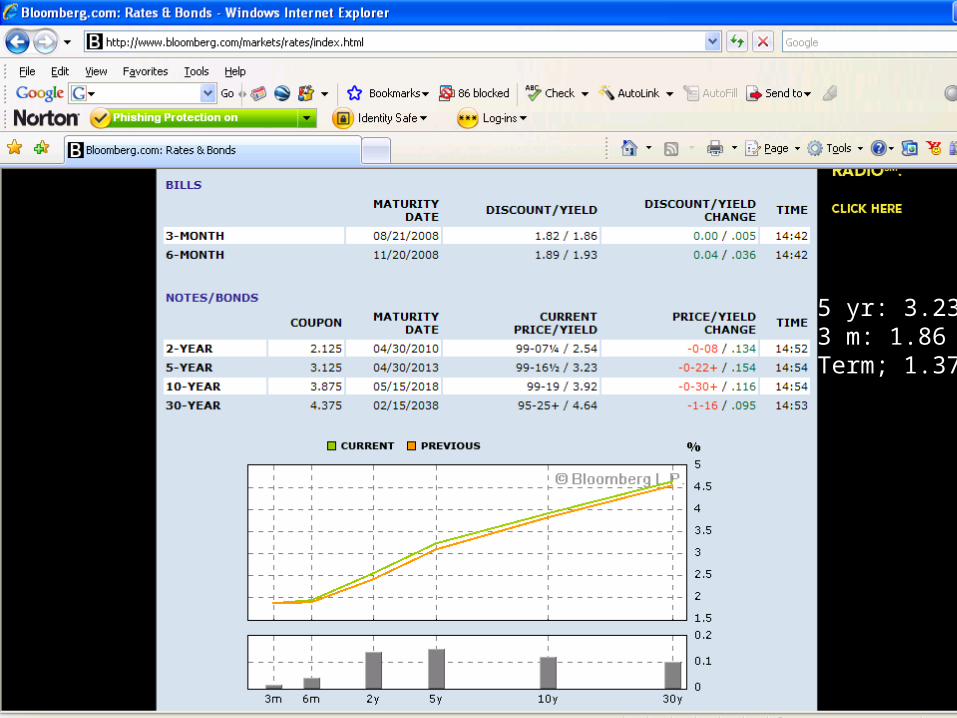

5 yr: 3.233 m: 1.86Term; 1.37

4545

Estimate ARCH/GARCHEstimate ARCH/GARCH

4646

4747

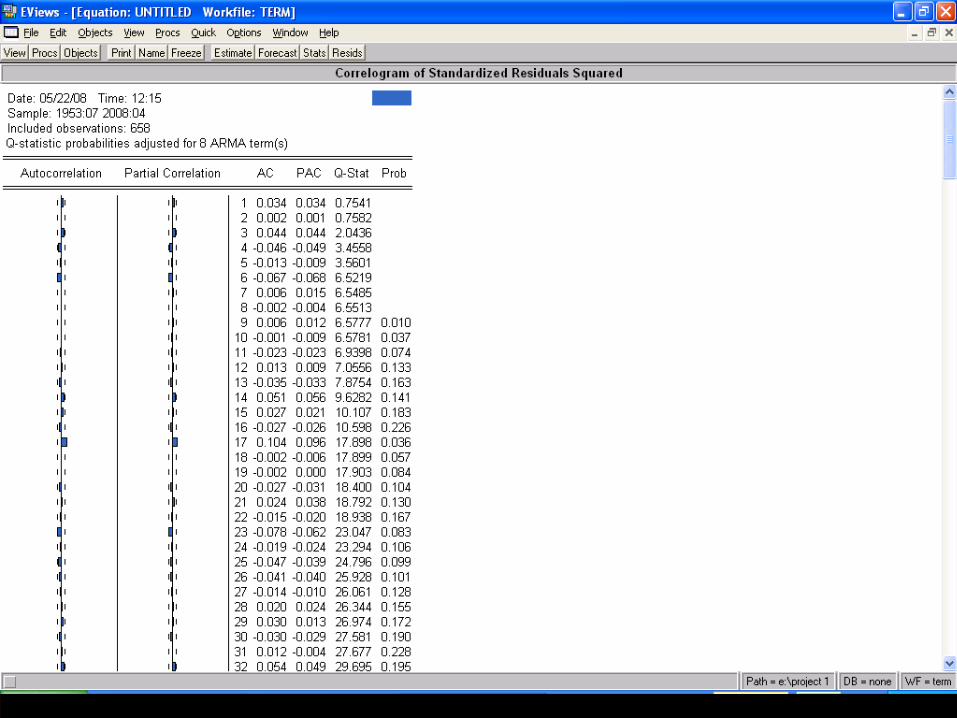

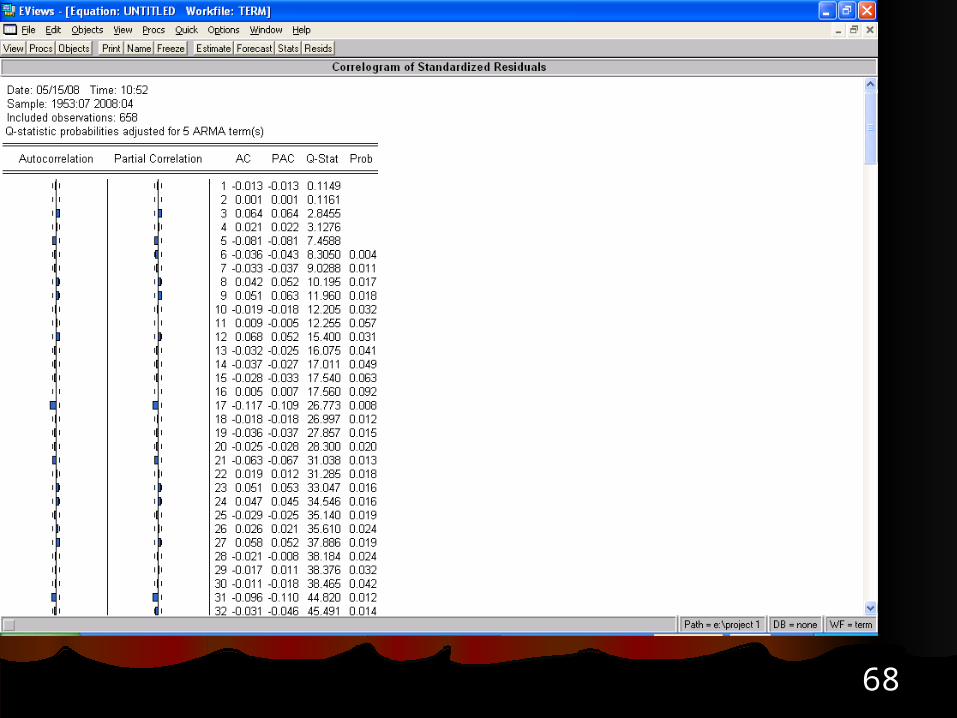

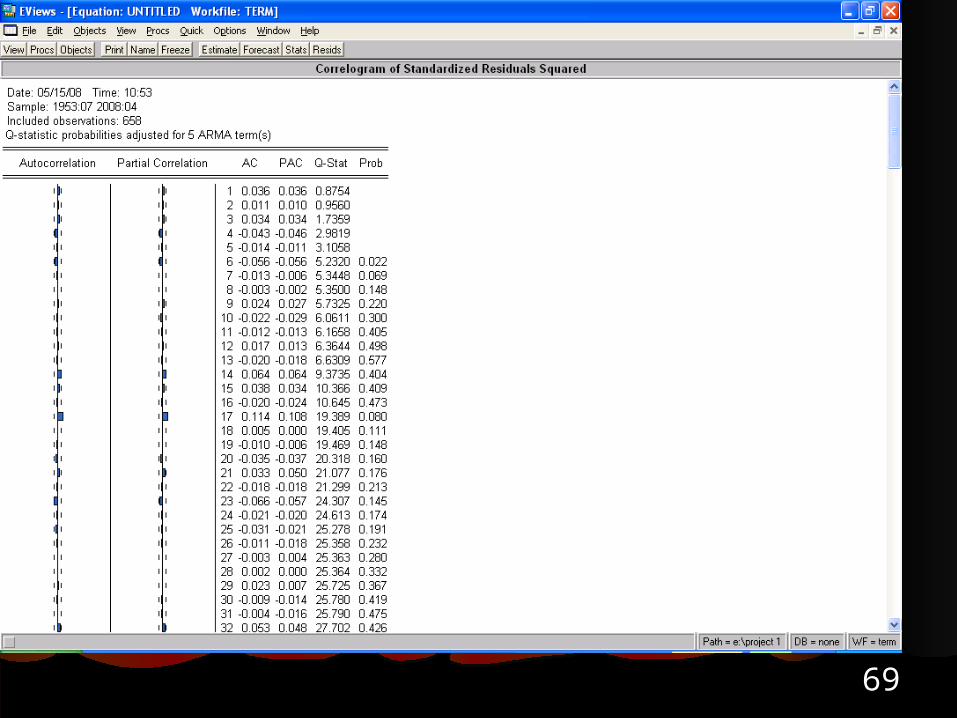

DiagnosticsDiagnosticsCorrelogram of standardized Correlogram of standardized

residuals residuals Actual, fitted, residual graphActual, fitted, residual graphcorrelogram of standardized correlogram of standardized

residuals squaredresiduals squaredLM ARCH testLM ARCH test

4848

4949

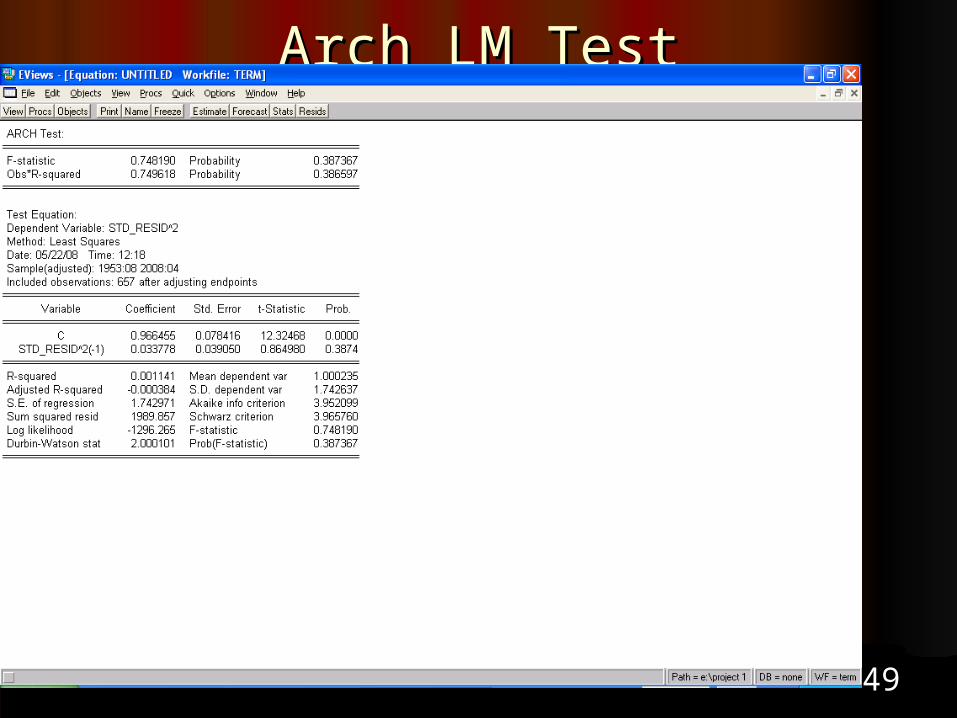

Arch LM TestArch LM Test

5050

0

20

40

60

80

-4 -3 -2 -1 0 1 2 3 4

Series: Standardized ResidualsSample 1953:07 2008:04Observations 658

Mean 0.027893Median 0.028664Maximum 3.760420Minimum -4.166763Std. Dev. 1.000265Skewness 0.016000Kurtosis 4.028786

Jarque-Bera 29.04587Probability 0.000000

Standardized Residuals from GARCH Model

Histogram of Standardized Histogram of Standardized ResidualsResiduals

5151

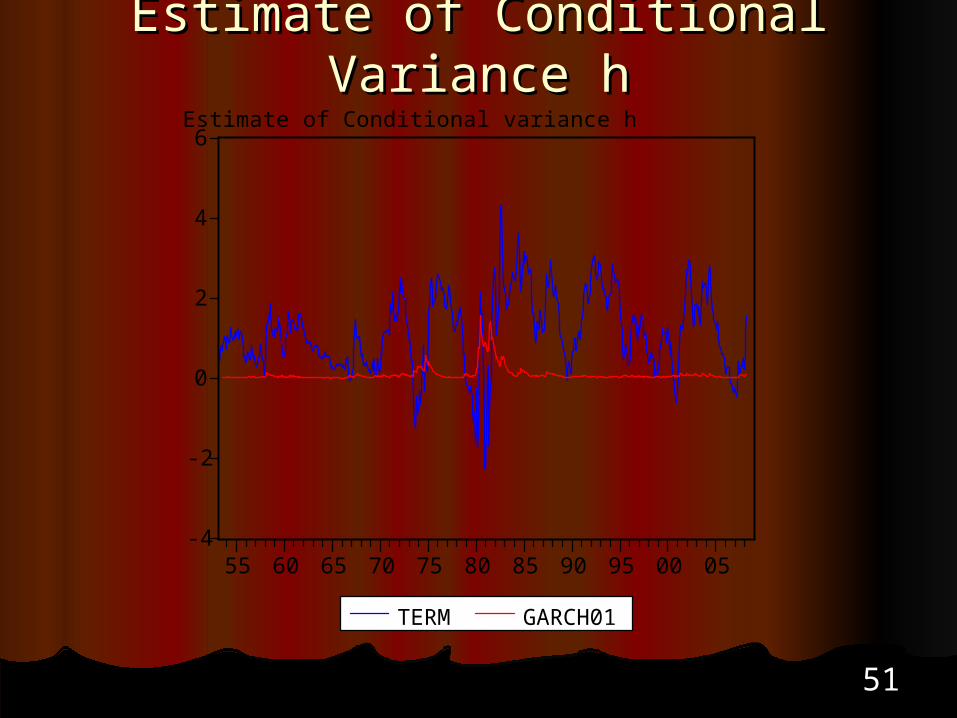

Estimate of Conditional Variance Estimate of Conditional Variance hh

-4

-2

0

2

4

6

55 60 65 70 75 80 85 90 95 00 05

TERM GARCH01

Estimate of Conditional variance h

5252

Estimate of a Simpler Model with Estimate of a Simpler Model with ARCHARCH

5353

5454

-3

-2

-1

0

1

2

3

-4

-2

0

2

4

6

55 60 65 70 75 80 85 90 95 00 05

Residual Actual Fitted

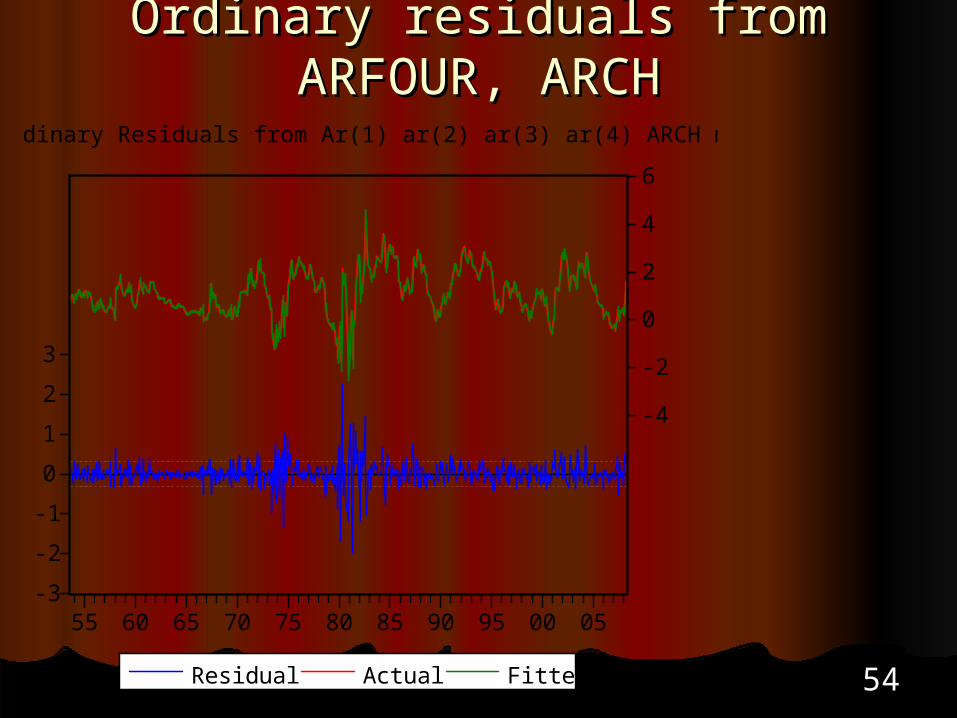

Ordinary Residuals from Ar(1) ar(2) ar(3) ar(4) ARCH model

Ordinary residuals from ARFOUR, Ordinary residuals from ARFOUR, ARCHARCH

5555

AppendixAppendix

5656

Alternative model #1Alternative model #1

5757

5858

5959

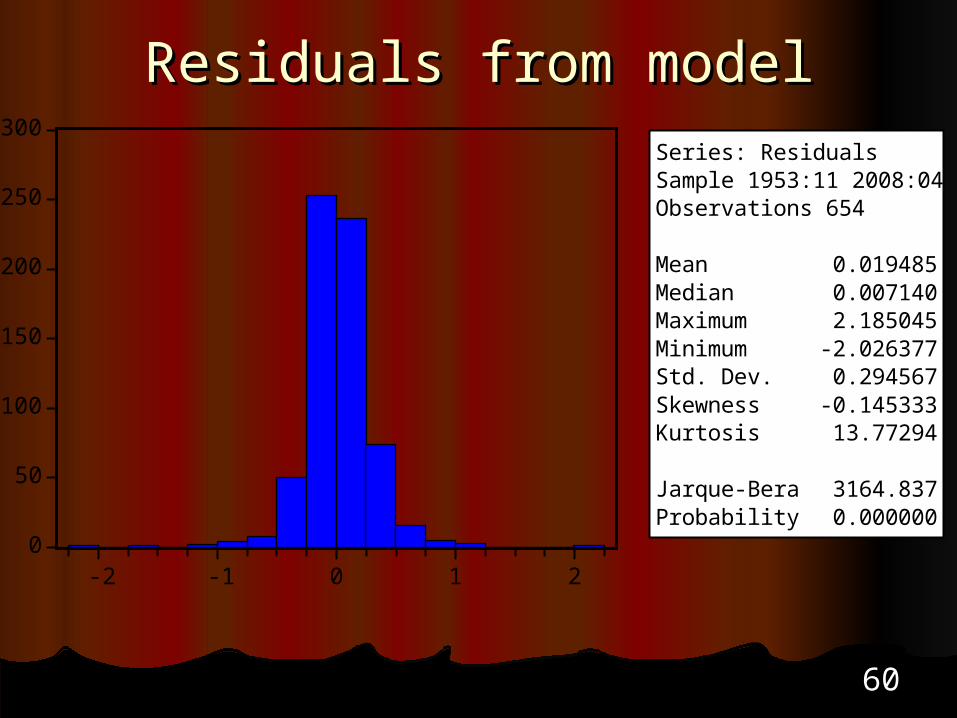

6060

Residuals from modelResiduals from model

0

50

100

150

200

250

300

-2 -1 0 1 2

Series: ResidualsSample 1953:11 2008:04Observations 654

Mean 0.019485Median 0.007140Maximum 2.185045Minimum -2.026377Std. Dev. 0.294567Skewness -0.145333Kurtosis 13.77294

Jarque-Bera 3164.837Probability 0.000000

6161

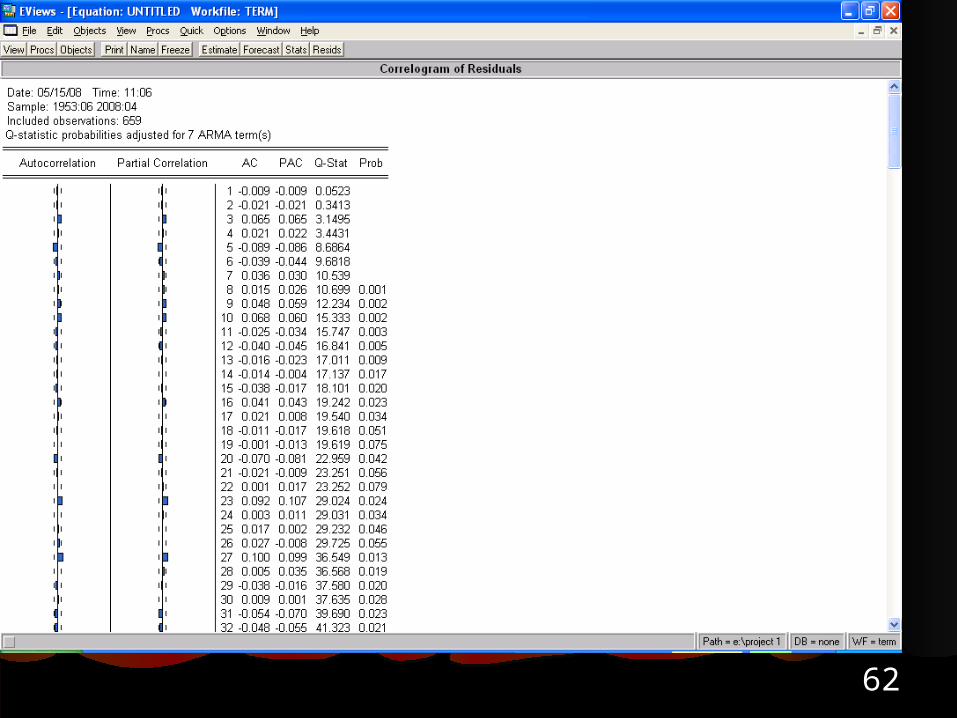

Alternative model #2Alternative model #2

6262

6363

6464

0

40

80

120

160

-1.5 -1.0 -0.5 0.0 0.5 1.0 1.5 2.0

Series: ResidualsSample 1953:06 2008:04Observations 659

Mean -9.24E-05Median -0.010673Maximum 2.113270Minimum -1.736855Std. Dev. 0.294642Skewness -0.025338Kurtosis 11.88345

Jarque-Bera 2166.966Probability 0.000000

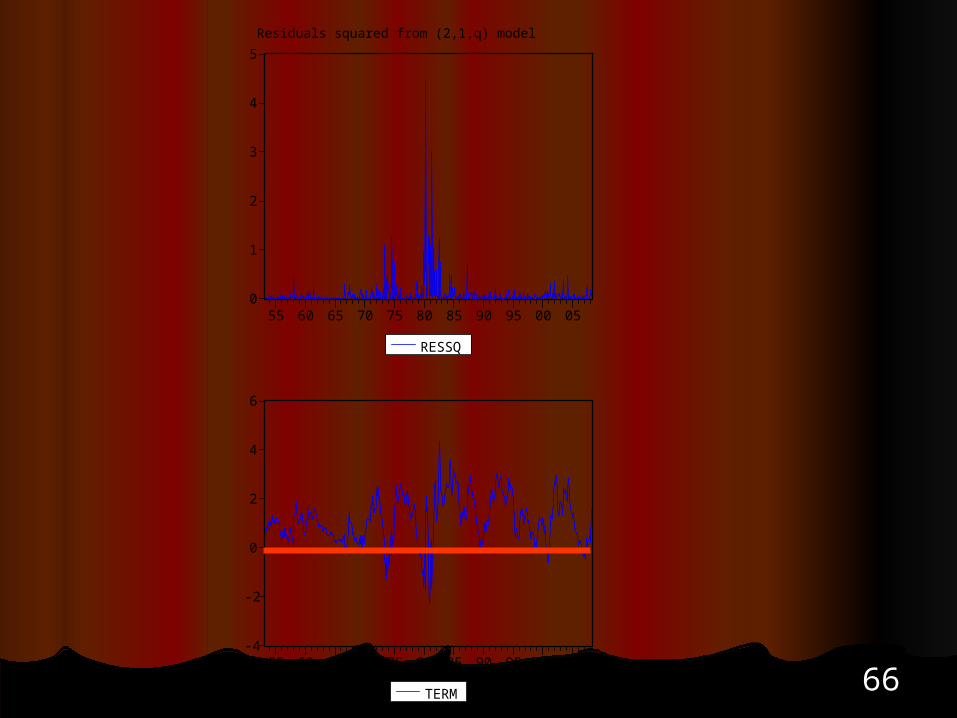

Residulas from (2,1,q) model

6565

Autoregressive Conditional Autoregressive Conditional HeteroskedasticityHeteroskedasticity

6666

0

1

2

3

4

5

55 60 65 70 75 80 85 90 95 00 05

RESSQ

-4

-2

0

2

4

6

55 60 65 70 75 80 85 90 95 00 05

TERM

Residuals squared from (2,1,q) model

6767

6868

6969

7070

0

20

40

60

80

-3.75 -2.50 -1.25 0.00 1.25 2.50 3.75

Series: Standardized ResidualsSample 1953:07 2008:04Observations 658

Mean 0.041163Median 0.028847Maximum 3.840148Minimum -4.563053Std. Dev. 0.999768Skewness -0.040181Kurtosis 4.379016

Jarque-Bera 52.31493Probability 0.000000

Residuals from Arch-Garch Model