1 environment accounting and the business - pearson · each chapter. key questions are ......

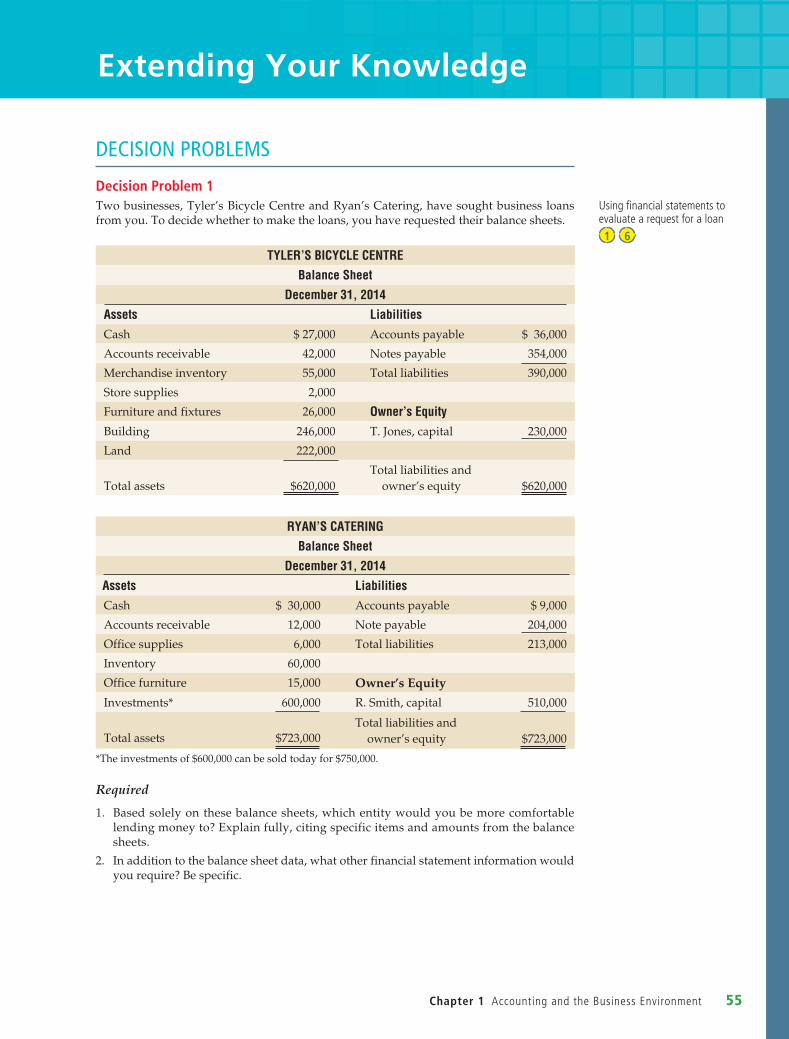

TRANSCRIPT

1 Defineaccounting,anddescribetheusersofaccountinginformation

LEARNING OBJECTIVESKEY QUESTIONS

Accounting and the Business

Environment1

Why is accounting important, and who uses the information?

Why is it important for accountants to be ethical? 2 Explainwhyethicsandrulesofconductarecrucialinaccountingandbusiness

In what form can we set up a company? 3 Describeanddiscusstheformsofbusinessorganizations

What are the rules of accounting, and why do we need them?

How do business transactions affect the accounting records of a company?

What financial statements are prepared by a company, and how do we create them?

4 Explainthedevelopmentofaccountingstandards,anddescribetheconceptsandprinciples

5 Describeandusetheaccountingequationtoanalyzebusinesstransactions

6 Prepareandevaluatethefinancialstatements

Learning Objectivesarea“roadmap”showingwhatwillbecoveredandwhatisespeciallyimportantineachchapter.

Key Questions arequestionsabouttheimportantconceptsinthechapterexpressedineverydaylanguage.

M01_HORN0096_01_SE_C01.indd 2 10/4/12 1:11 PM

3

Lisa Hunter graduated from university with a degree in environmental studies. She then went to work with an environmental consulting company and gained extensive expe-rience in the area of environmental sustainability. Lisa soon came to realize that many

businesses were starting to recognize the benefits of advancing their environmental per-formance and were seeing increasing opportunities to participate in the green economy. For these companies, the financial implications of “going green” were significant.

Lisa decided to go back to university to pursue an accounting designation. Within three years, she had successfully completed all the requirements and became designated as a professional accountant.

Lisa started her own consulting firm to combine her passion for environmental sus-tainability with her recently developed accounting skills. She named her new company “Hunter Environmental Consulting.” She was now an entrepreneur! She realized she needed to develop a business plan, secure clients, set up an office, and hire staff.

Lisa’s first year in business was stressful and successful. Her work in the first year was primarily in the area of energy efficiency and how her clients could reduce their energy consumption and their energy costs.

“My previous training and experience gave me the confidence to know that I could be successful in this field. However, I did not realize how carefully you have to watch the books—costs can get out control in a hurry if you are not careful!”

Achapter-opening storyshowswhythetopicsinthechapterareimportanttorealcompaniesandbusinesspeople.Werefertothisstorythroughoutthechapter.

M01_HORN0096_01_SE_C01.indd 3 10/4/12 1:11 PM

4 Part 1 TheBasicStructureofAccounting

ConnECting ChAptEr 1

Defineaccounting,anddescribetheusersofaccountinginformation

Explainwhyethicsandrulesofconductarecrucialinaccountingandbusiness

Describeanddiscusstheformsofbusinessorganizations

Explainthedevelop-mentofaccountingstandards,anddescribetheconceptsandprinciples

Describeandusetheaccountingequationtoanalyzebusinesstransaction

Prepareandevalu-atethefinancialstatements

Why is accounting important, and who uses the information? page 5

Why is it important for accountants to be ethical? page 7

In what form can we set up a company? page 9

What are the rules of accounting, and why do we need them? page 11

How do business transactions affect the accounting records of a company? page 16

What financial statements are prepared by a company, and how do we create them? page 23

Accounting:TheLanguageofBusiness,page5

EthicalConsiderationsinAccountingandBusiness,page7

FormsofBusinessOrganizations,page9

AccountingConcepts,page11

TheAccountingEquation,page16

TheFinancialStatements,page23

DecisionMakers:TheUsersofAccountingInformation,page 5

OtherConsiderationsinFinancialStatementPreparation,page13

AccountingforBusinessTransactions,page 17

RelationshipsamongtheFinancialStatements,page 24

TheHistoryofAccounting,page7

EvaluatingBusinessTransactions,page22

MyAccountingLab

RelationshipsamongtheFinancialStatements

MyAccountingLab • DemoDoc:BasicTransactions • StudentPowerPointSlides • AudioChapterSummary • AvarietyofvideosonChapter1topics.

AllMyAccountingLabresourcesarefoundbyclickingonChapterResourcesandthenMultimediaLibrary.

TheSummaryforChapter1appearsonpage30.Accounting Vocabularywithdefinitionsappearsonpage33.

1 2 3 4 5 6

role does accounting play in Lisa Hunter’s situation? Lisa hadtodecidehowtoorganizehercompany.Shesetupherbusinessasapropri-etorship—a single-owner company—with herself as the owner. As her busi-ness grows, she may decide to expand it by taking on a partner. She mightalsochooseto incorporate—that is, toformacorporation. Inthischapter,wediscussallthreeformsofbusinessorganization:proprietorships,partnerships,andcorporations.

Youmayalreadyknowvariousaccounting termsandrelationships,becauseaccountingaffectspeople’sbehaviourinmanyways.Thisfirstaccountingcoursewillsharpenyour focusbyexplaininghowaccountingworks.Asyouprogressthroughthiscourse,youwillseehowaccountinghelpspeoplelikeLisaHunter—andyou—achievebusinessgoals.

What

Connecting Chapter “X”appearsatthebeginningofeachchapterandgivesaguidetothecontentofthechapterwithpagerefer-ences,aswellasreferencestoMyAccountingLabsoyoucanconnecttowhatyouneedquicklyandeasily.

M01_HORN0096_01_SE_C01.indd 4 10/4/12 1:11 PM

Chapter 1 AccountingandtheBusinessEnvironment 5

Accounting: the Language of Business

Accountingistheinformationsystemthatmeasuresbusinessfinancialactivities,processes that information into reports, and communicates the results to deci-sionmakers.Forthisreasonitiscalled“thelanguageofbusiness.”Thebetteryouunderstandthelanguage,thebetteryourdecisionswillbe,andthebetteryoucanmanagefinancialinformation.Itisgenerallyrecognizedthatbusinessmanagersbelieveitismoreimportantforuniversitystudentstolearnaccountingthananyotherbusinesssubject.Decisionsconcerningpersonalfinancialplanning,educa-tionexpenses,loans,carpayments,incometaxes,andinvestmentsarebasedontheinformation systemthatwecallaccounting.

Financialstatementsareakeyproductofanaccountingsystemandprovideinformation that helps people make informed business decisions. Financial statements report on a business in monetary terms. Is my business making aprofit?ShouldIhireassistants?AmIearningenoughmoneytoexpandmybusi-ness?Answeringbusinessquestionsliketheserequiresaknowledgeoffinancialstatements.

Studentssometimesmistakebookkeepingforaccounting.Bookkeepingisapro-ceduralelementofaccounting,justasarithmeticisaproceduralelementofmath-ematics (or just as skating is a procedural element of hockey). There are manyaccountingsoftwarepackagesthatwillhandledetailedbookkeeping—inhouse-holds,businesses,andorganizationsofalltypes.Exhibit1–1illustratestheroleofaccountinginbusiness.Theprocessstartsandendswithpeoplemakingdecisions.

LO 1Whyisaccountingimportant,andwhousestheinformation?

IFRS

The Accounting System: The Flow of InformationExhibit 1–1

Decision Makers: the Users of Accounting information

Decisionmakersneedinformation.Themoreimportantthedecision,thegreaterthe need for information. Virtually all businesses and most individuals keepaccountingrecordstoaiddecisionmaking.Herearesomedecisionmakerswhouseaccountinginformation.

Individuals Peopleuseaccounting information inday-to-dayaffairs tomanagebankaccounts,evaluate jobprospects,make investments,andevenindecidingwhethertoleaseorbuyanewcar.

Businesses Business owners and managers use accounting information to setgoalsfortheirorganizations.Theyevaluatetheirprogresstowardthosegoals,and

BoldfacedwordsarenewtermsthatareexplainedhereanddefinedintheAccountingVocabularysectionatthe endofthischapterandtheGlossaryattheendofthebook.

LearningObjectivesinthemarginsignalthebeginningofthesectionthatcoversthelearning-objectivetopic.LookfortheLearningObjectivewhenyouwanttoreviewthistopic.

Exhibitssummarizekeyideasinavisualway.

M01_HORN0096_01_SE_C01.indd 5 10/4/12 1:11 PM

6 Part 1 TheBasicStructureofAccounting

theytakecorrectiveactionwhenitisnecessary.Forexample,LisaHuntermakesdecisionsbasedonaccountinginformation.Sheknowstheamountofrevenuethatwillbeearned,sincesheandherclientwillagreeonafeefortheconsultingworkshewillperform.Sheneedstodeterminethescopeofthework,howmanyconsul-tantsshewillrequire,andhowmanyhoursitwilltaketocompletetheproject.Sheneedstomakesurethathercostsdonotexceedthefeeshewillreceivefromherclientifshewantstomakesurethatshemaintainsaprofitablebusiness.

Investors Outsideinvestorsoftenprovidethemoneyabusinessneedstobeginoperations.Todecidewhether to invest,potential investorspredict theamountofincometobeearnedontheirinvestment.Thisevaluationmeansanalyzingthefinancial statements of the business and keeping up with developments in theworldofbusiness.

Creditors Beforelendingmoney,creditors(lenders)suchasbanksevaluatetheborrower’sabilitytomakescheduledpayments.Thisevaluationincludesareportoftheborrower’sfinancialpositionandapredictionoffutureoperations,bothofwhicharebasedonaccountinginformation.

Government Regulatory Agencies Mostorganizationsfacegovernmentregulation.Forexample,theprovincialsecuritiescommissions,suchastheBritishColumbiaSecuritiesCommissionandtheOntarioSecuritiesCommission,dictatethatbusi-nessessellingtheirsharestoandborrowingmoneyfromthepublicdisclosecer-tainfinancialinformationtotheinvestingpublic.

Taxing Authorities Provincial and federal governments levy taxes on individu-alsandbusinesses.Incometaxiscalculatedbyusingaccountinginformationasastartingpoint.Abusiness’saccountingsystemisrequiredtokeeptrackofpro-vincialsalestax,goodsandservicestax,andharmonizedsalestaxthatacompanycollectsfromitscustomersandpaystoitssuppliers.Businessesusetheseaccount-ingrecordstohelpthemdeterminetheirtaxesthatmustbepaidtotheprovincialandfederalgovernments.

Not-for-profit Organizations Not-for-profitorganizationssuchaschurches,hospi-tals,governmentagencies,universities,andcolleges,whichoperateforpurposesotherthantoearnaprofit,useaccountinginformationtomakedecisionsrelatedtotheorganizationinmuchthesamewaythatprofit-orientedbusinessesdo.

Other Users Employeesandlabourunionsmaymakewagedemandsbasedontheaccountinginformationthatshowstheiremployer’sreportedincome.Consumergroupsandthegeneralpublicarealso interested in theamountof incomethatbusinessesearn.Andnewspapersmayreport“animprovedprofitpicture’’ofamajor company as it emerges from economic difficulties. Such news, based onaccountinginformation,relatestothecompany’shealth.

Financial Accounting and Management AccountingUsersofaccountinginformationareadiversepopulation,buttheymaybegroupedasexternalusersorinternalusers.Thisdistinctionallowsustoclassifyaccountingintotwofields—financialaccountingandmanagementaccounting.

Financial accounting provides information to people outside the company.Creditors and outside investors, for example, are not part of the day-to-daymanagement of the company. Likewise, government agencies and the generalpublicareexternalusersofacompany’saccountinginformation.Thisbookdealsprimarilywithfinancialaccounting.

Management accountinggenerates informationfor internaldecisionmakers,such as company executives, department heads, university deans, and hospitaladministrators.

Exhibit1–2showshowfinancialaccountingandmanagementaccountingareusedbyHunterEnvironmentalConsulting’sinternalandexternaldecisionmakers.

M01_HORN0096_01_SE_C01.indd 6 10/4/12 1:11 PM

Chapter 1 AccountingandtheBusinessEnvironment 7

the history and Development of Accounting

Accountinghasalonghistory.Somescholarsclaimthatwritingaroseinordertorecordaccountinginformation.Accountingrecordsdatebacktotheancientcivi-lizationsofChina,Babylonia,Greece,andEgypt.Therulersofthesecivilizationsusedaccountingtokeeptrackofthecostoflabourandmaterialsusedinbuildingstructureslikethegreatpyramids.Theneedforaccountinghasexistedaslongastherehasbeenbusinessactivity.

Accountingdevelopedfurtherasaresultoftheinformationneedsofmerchantsinthecity-statesofItalyduringthe1400s. Inthatbusycommercialclimate, themonkLucaPacioli,amathematicianandfriendofLeonardodaVinci’s,publishedthefirstknowndescriptionofdouble-entrybookkeepingin1494.

IntheIndustrialRevolutionofthe19thcentury,thegrowthofcorporationsspurredthe development of accounting. The corporation owners—the shareholders—were no longer necessarily the managers of their business. Managers had tocreateaccountingsystemstoreporttotheownersandgovernmenthowwelltheirbusinessesweredoing.Becausemanagerswanttheirperformancetolookgood,societyneedsawaytoensurethatthebusinessinformationprovidedisreliable.To meet this need, generally accepted accounting principles were developed.Thesewillbediscussedinmoredetailshortly.

Asrequiredinothersegmentsofsociety,accountingmustbepractisedinanethicalmanner.Welooknextattheethicaldimensionofaccounting.

How Financial Accounting and Management Accounting Are UsedExhibit 1–2

HunterEnvironmental

Consultingproprietorship

Hunter’s company lostmoney on its firstconsulting project.Management accountinginformation would be used to help Hunterdetermine costs and theamount she should charge for a consulting project.

A bank manager would use financial accounting informationto decide whether to lend money to Hunter’scompany to expand the business.

Just Checking questionsappearattheendofeachLearningObjective,allowingyoutotestyourmasteryoftheconceptsinthisLearningObjectivebeforemovingontothenextone.ThesolutionsappearattheendofthechapterandonMyAccountingLab.

Ethical Considerations in Accounting and Business

Ethical considerations affect all areas of accounting and business. Investors,creditors,andregulatorybodiesneedrelevantandreliable informationaboutacompany.Naturally,companieswant tomake themselves lookasgoodaspos-sibletoattractinvestors,sothereisapotentialforconflict.Anauditisafinancial

LO 2Whyisitimportantforaccountantstobeethical?

IFRS

1. Whatisaccounting?

2. Namethreedecisionmakersthatrelyonfinancialinformation,andbrieflydescribehowtheyuseit.

3. Whatisthedifferencebetweenfinancialaccountingandmanagementaccounting?

Just Checking Solutions appear at the end of this chapter and on MyAccountingLab.

JUST CHECKING MyAccountingLab

M01_HORN0096_01_SE_C01.indd 7 10/4/12 1:11 PM

8 Part 1 TheBasicStructureofAccounting

examination.Auditsareconductedbyindependentaccountantswhoexpressanopinion on whether or not the financial statements fairly reflect the economiceventsthatoccurredduringtheaccountingperiod.Itisvitalthatcompaniesandtheirauditorsbehaveinanethicalmanner.Exhibit1–3illustratestherelationshipamong accounting and business entities that are public companies (companiesthatsellsharesofstocktoinvestors).

Relationship among Accounting and Business EntitiesExhibit 1–3

Provincial securities commissionsoversee operations of public companies

Decision makersinclude investors,creditors, andregulatoryorganizations

Public companiessell shares toinvestors, borrowmoney, and issuefinancial reports

Independentaccounting firmsperform audit,compliance, andadvisory services

Unfortunatelyfortheaccountingprofession,accountingscandalsinvolvingbothpubliccompaniesandtheirauditorshavemadetheheadlinesoverthepastfifteenyears.Attheturnofthiscentury,EnronCorporation,whichwastheseventh-largestcompanyintheUnitedStates, issuedmisleadingfinancialstatements.Enronwasforcedintobankruptcyanditsauditors’actionswerequestioned.TheimpactoftheEnronbankruptcywasfeltbymanydifferentparties,includingEnronshareholders,whosawtheirinvestmentsbecomeworthless;employeeswholosttheir jobsandtheirpensions;andtheaccountingprofession,whichlostsomeofitsintegrityandreputation as gatekeepers and stewards for the investing public. This situationshockedthebusinesscommunityandcausedinvestorstoquestionthereliabilityoffinancialinformation.

Sincethefinancialhealthofacompanyisimportanttomanydifferentgroupsofusers,theseusersmustbeconfidentthattheycanrelyonthefinancialinformationtheyaregivenwhentheyaremakingdecisions.Toincreaseusers’confidence,theaccountingprofessionandother interestedstakeholdergroupsmade importantchangesoverthepastdecadetoimprovethequalityofthefinancialinformationprovided.Wewilldescribethesechangeslaterinthischapter.

The Professional Accounting Bodies and Their Standards of Professional ConductThe members of the four accounting organizations in Canada—CharteredAccountants (CAs), Certified General Accountants (CGAs), Certified Manage-mentAccountants(CMAs)andCharteredProfessionalAccountants(CPAs)—areallgovernedbyrulesofprofessionalconductcreatedbytheirrespectiveorganiza-tions.Manyoftherulesapplywhetherthemembersarepublicaccountantswork-inginpublicpracticeorprivateaccountantsworkinginindustryorgovernment.Theserulesconcerntheconfidentialityofinformationtheaccountantisprivyto,maintenanceofthereputationoftheprofession,theneedtoperformaccountancyworkwithintegrityandduecare,competence,refusaltobeassociatedwithfalseormisleadinginformation,andcompliancebytheaccountantwithprofessionalstandards.Other rulesareapplicableonly to thosemembers inpublicpractice,anddealwiththingsliketheneedforindependence,andhowtoadvertise,seekclients,andconductapractice.

M01_HORN0096_01_SE_C01.indd 8 10/4/12 1:11 PM

Chapter 1 AccountingandtheBusinessEnvironment 9

The rulesofprofessional conduct serveboth themembersof theaccountingbodies and the public. The rules serve members by setting standards that theymustmeet,andprovidingabenchmarkagainstwhichtheywillbemeasuredbytheirpeers.Thepublicisservedbecausetherulesofprofessionalconductprovideitwithalistofthestandardstowhichthemembersofthebodyadhere.Thishelpsthepublicdetermineitsexpectationsofmembers’behaviour.However,therulesofprofessionalconductshouldbeconsideredaminimumstandardofperformance;ideally,themembersshouldcontinuallystrivetoexceedthem.

Throughoutthisbook,weprovideseveralproblemsthatallowyoutoconsiderethicaldilemmas.Considerthemcarefully.Theperceptionthataccountantsfollowthehigheststandardofprofessionalconductmustalsobethereality.Intoday’sbusinessclimate,behavinginanethicalmanneriscrucial.

Codes of Business Conduct of CompaniesMany companies have codes of conduct that apply to their employees in theirdealingswitheachotherandwiththecompanies’suppliersandcustomers.Someofthesecompaniesmentiontheircodeintheirannualreportorontheirwebsite.Forexample,VancouverCitySavingsCreditUnionstatesonitswebsite:

Our Values

Integrity: Weactwithcourage,consistencyandrespecttodowhatishonest,fairandtrustworthy.Innovation: Weanticipateandrespondtochallengesandchangingneedswithcreativity,enthusiasmanddetermination.Responsibility: We are accountable to our members, employees, colleaguesandcommunitiesfortheresultsofourdecisionsandactions.

Source: From Vancouver City Savings Credit Union’s website, www.vancity.com (accessed May25,2012)

Thecompanyindicatestoitsemployeesandtothegeneralpublichowmanage-mentexpectsemployeestobehave.

4. What isanaudit,andwhyis it important that itbeperformedby independentaccountants?

5. Whydotheprofessionalaccountingbodiesestablishrulesofprofessionalconductfortheirmembers?

6. Refer to theStudentPolicies,Bylaws,andCodesofConductofyourcollegeoruniversity.Whydothesepoliciesexist?

Just Checking Solutions appear at the end of this chapter and on MyAccountingLab.

JUST CHECKING

Forms of Business organizations

Abusinesscanbeorganizedasa

• Proprietorship• Partnership• Corporation

Youshouldunderstandthedifferencesamongthethree.

Proprietorship Aproprietorshiphasasingleowner,calledtheproprietor,whooftenmanagesthebusiness.Proprietorshipstendtobesmallretailstores,res-taurants,andservicebusinesses,butalsocanbeverylarge.Fromanaccounting

LO 3Inwhatformcanwesetupacompany?

IFRS

MyAccountingLab

M01_HORN0096_01_SE_C01.indd 9 10/4/12 1:12 PM

10 Part 1 TheBasicStructureofAccounting

viewpoint,eachproprietorshipisdistinctfromitsowner.Thus,theaccountingrecordsoftheproprietorshipdonotincludetheproprietor’spersonalaccount-ingrecords.However,fromalegalperspective,thebusinessistheproprietor,so if thebusiness cannotpay itsdebts, lenders can take theproprietor’sper-sonalassets(cashandbelongings)topaytheproprietorship’sdebt.Inthisbook,westartwithaproprietorshipbecausemanystudentsorganizetheirfirstbusi-nessthatway.

Partnership A partnership joins two or more individuals together asco-owners.Eachownerisapartner.Manyretailstoresandprofessionalorga-nizations of physicians, lawyers, and accountants are partnerships. Mostpartnershipsaresmallandmedium-sized,butsomearequite large; therearepublicaccountingfirmsandlawfirmsinCanadawithseveralhundredpartners.Accountingtreatsthepartnershipasaseparateorganizationdistinctfromthepersonalaffairsofeachpartner.Butagain,fromalegalperspective,apartner-shipisthepartnersinamannersimilartoaproprietorship.Ifthepartnershipcannotpayitsdebts,lenderscantakeeachpartner’spersonalassetstopaythepartnership’sdebts.

Corporation A corporation is a business owned by shareholders. These arethe peopleorothercorporationswhoownsharesofownershipinthebusiness.The corporation is the dominant form of business organization in Canada.Althoughproprietorshipsandpartnershipsaremorenumerous,corporationsengageinmorebusinessandaregenerallylargerintermsoftotalassets,income,andnumberofemployees.InCanada,generally,corporationsmusthaveLtd.orLimited, Inc.orIncorporated,orCorp.orCorporationintheirlegalnameto indi-catethattheyareincorporated.Corporationsneednotbelarge;abusinesswithonlyafewassetsandemployeescouldbeorganizedasacorporation.

Fromalegalperspective,acorporationisformedwhenthefederalgovernmentoraprovincialgovernmentapprovesitsarticlesofincorporation.Unlikeapropri-etorshiporapartnership,onceacorporationisformed,itisalegalentityseparateanddistinct from itsowners.Thecorporationoperatesasan“artificialperson”thatexistsapartfromitsownersandthatconductsbusinessinitsownname.Thecorporationhasmanyoftherightsthatapersonhas.Forexample,acorporationmaybuy,own,andsellproperty.Thecorporationmayenterintocontractsandsueandbesued.

Since corporations are entities separate from their owners, they willprepare financial reports separate from their owners. Over the years, theaccounting profession has developed accounting and reporting standardsthatcorporationsmustfollowwhenpreparingtheirfinancialreports.Wewillexaminethemingreaterdetailinthenextsectionofthischapter.Corporationsdiffer significantly from proprietorships and partnerships in another way.If a proprietorship or partnership cannot pay its debts, lenders can take theowners’personalassetstosatisfythebusiness’sobligations.Butifacorporationgoesbankrupt,lenderscannottakethepersonalassetsoftheshareholders.Thislimited personal liability of shareholders for corporatedebts explainswhycor-porationsaresopopularcomparedtoproprietorshipsandpartnerships,whichhaveunlimited personal liability.Exhibit1–4showstheformationandownershipofacorporation.

Another factor for corporations is the division of ownership into individualshares.CompaniessuchasWestJet,CanadianImperialBankofCommerce,andCanadianTireCorporation,Limited,haveissuedmillionsofsharesofstockandhave tensof thousandsof shareholders.An investorwithnopersonal relation-shipeithertothecorporationortoanyothershareholdercanbecomeanownerbybuying30,100,5,000,oranynumberofsharesofitsstock.Formostcorpora-tions,theinvestormaysellthesharesatanytime.Itisusuallyhardertosellone’sinvestmentinaproprietorshiporapartnershipthantosellone’sinvestmentinacorporation.

Aproprietorshipandapartnership(Ch.12)arenotlegalentitiesseparatefromtheirowners,sotheincomefromproprietorshipsandpartnershipsistaxabletotheirowners,nottothebusiness.Butinaccounting,theownerandthebusinessareconsideredseparateentities,andseparaterecordsarekeptforeach.Acorporation(Ch.13)isaseparatelegalentity.Thecorporationistaxedonitsincome,andtheownersaretaxedonanyincometheyreceivefromthecorporation.

KEY POINTS

Key Pointshighlightimportantdetailsfromthetextandaregoodtoolsforreviewingconcepts.

Exhibit 1–4

Federal or provincialgovernment approves Articles of Incorporation

Shareholders invest incorporations

Corporations Examples includeWestJet Airlines Ltd.Canadian Western BankSun-Rype Products Ltd.

The Formation and Ownership of a Corporation

M01_HORN0096_01_SE_C01.indd 10 10/4/12 1:12 PM

Chapter 1 AccountingandtheBusinessEnvironment 11

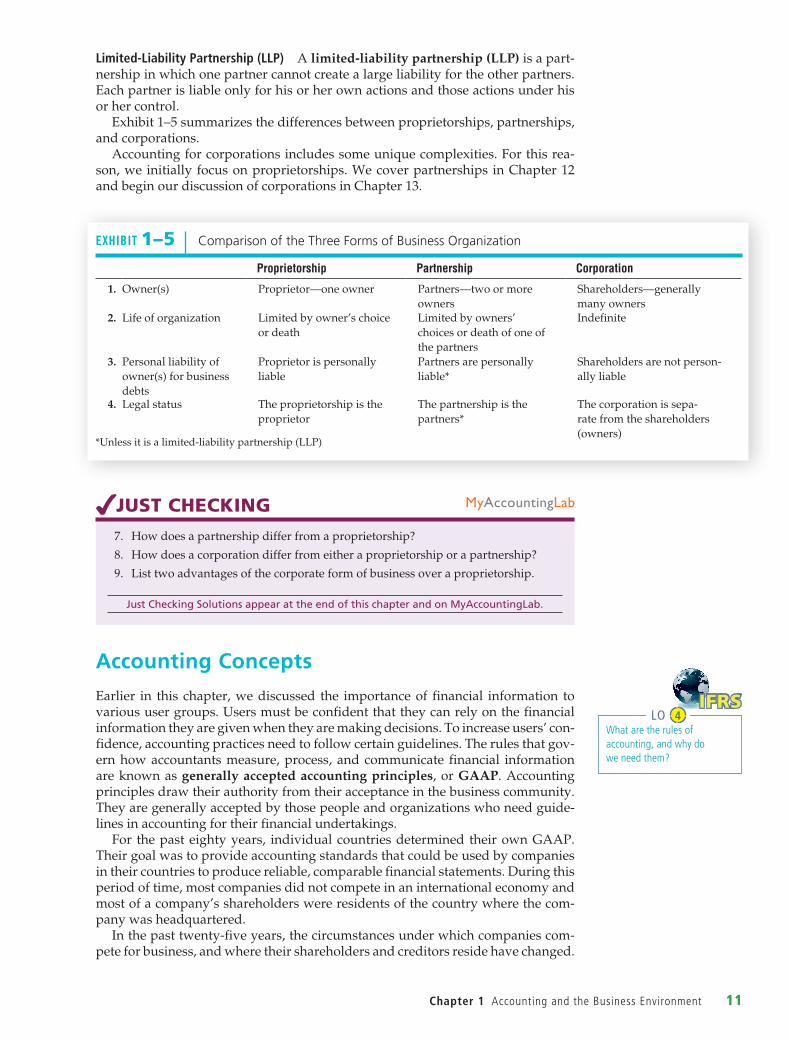

Limited-Liability Partnership (LLP) Alimited-liability partnership (LLP)isapart-nershipinwhichonepartnercannotcreatealargeliabilityfortheotherpartners.Eachpartnerisliableonlyforhisorherownactionsandthoseactionsunderhisorhercontrol.

Exhibit1–5summarizesthedifferencesbetweenproprietorships,partnerships,andcorporations.

Accountingforcorporationsincludessomeuniquecomplexities.Forthisrea-son,weinitially focusonproprietorships.Wecoverpartnerships inChapter12andbeginourdiscussionofcorporationsinChapter13.

7. Howdoesapartnershipdifferfromaproprietorship?

8. Howdoesacorporationdifferfromeitheraproprietorshiporapartnership?

9. Listtwoadvantagesofthecorporateformofbusinessoveraproprietorship.

Just Checking Solutions appear at the end of this chapter and on MyAccountingLab.

JUST CHECKING

Exhibit 1–5 Comparison of the Three Forms of Business Organization

Proprietorship Partnership Corporation

1. Owner(s) Proprietor—oneowner Partners—twoormoreowners

Shareholders—generallymanyowners

2. Lifeoforganization Limitedbyowner’schoiceordeath

Limitedbyowners’choicesordeathofoneofthepartners

Indefinite

3. Personalliabilityofowner(s)forbusinessdebts

Proprietorispersonallyliable

Partnersarepersonallyliable*

Shareholdersarenotperson-allyliable

4. Legalstatus Theproprietorshipistheproprietor

Thepartnershipisthepartners*

Thecorporationissepa-ratefromtheshareholders(owners)

*Unlessitisalimited-liabilitypartnership(LLP)

Accounting Concepts

Earlier in this chapter,wediscussed the importanceof financial information tovarioususergroups.Usersmustbeconfidentthattheycanrelyonthefinancialinformationtheyaregivenwhentheyaremakingdecisions.Toincreaseusers’con-fidence,accountingpracticesneedtofollowcertainguidelines.Therulesthatgov-ernhowaccountantsmeasure,process, andcommunicate financial informationareknownasgenerally accepted accounting principles,orGAAP.Accountingprinciplesdrawtheirauthorityfromtheiracceptanceinthebusinesscommunity.Theyaregenerallyacceptedbythosepeopleandorganizationswhoneedguide-linesinaccountingfortheirfinancialundertakings.

For thepasteightyyears, individualcountriesdetermined theirownGAAP.Theirgoalwastoprovideaccountingstandardsthatcouldbeusedbycompaniesintheircountriestoproducereliable,comparablefinancialstatements.Duringthisperiodoftime,mostcompaniesdidnotcompeteinaninternationaleconomyandmostofacompany’sshareholderswereresidentsofthecountrywherethecom-panywasheadquartered.

Inthepasttwenty-fiveyears,thecircumstancesunderwhichcompaniescom-peteforbusiness,andwheretheirshareholdersandcreditorsresidehavechanged.

LO 4Whataretherulesofaccounting,andwhydowe needthem?

IFRS

MyAccountingLab

M01_HORN0096_01_SE_C01.indd 11 10/4/12 1:12 PM

12 Part 1 TheBasicStructureofAccounting

Manymorebusinesseseitherpurchaseorsell inmarketsoutside theircountry,andshareholdersofcompaniescanresideanywhereintheworld.Theadventoftechnologyhasgreatlyaidedthisexpansion.

Untilrecently,however,GAAPhadnotkeptupwiththechangesinthewaycompaniesdobusiness.Accountingstandardswerestillnational.Itmeantinves-torsandcreditorswhohadbusinessdealingsindifferentareasoftheworldhadtounderstandvariousaccountingstandards.Althoughmanyofthestandardsweresimilaramongcountries,therewerealsomanysignificantdifferences.Forexam-ple,aCanadiancompanythatsolditssharesonastockexchangeintheUnitedStates actually had to prepare one set of financial statements under CanadianGAAPandanotherunderUnitedStatesGAAPor,atleast,provideareconciliationfromonetotheother.Thisduplicationwasinefficientandcostly.

Given the likelihood that companies would continue to expand globally, agroupofcountriesstartedtoworktogetheronaccountingstandardswithagoalofdevelopinginternationalaccountingstandardsthatcouldbeappliedanywherein the world. This group formed the International Federation of Accountantsand developed International Financial Reporting Standards, or IFRS, as wemorecommonlyrefertothem.Thesestandardshavenowbeenacceptedbyover110 countriesintheworld.Canadaadoptedthesestandardsin2011forcompaniesthatqualifyaspubliclyaccountableenterprises.

Publicly accountable enterprises, generally speaking, are companies thatarepubliclytradedorforwhichastrongpublicinterestexists.InCanada,pub-licly accountable enterprises are small in number but contribute heavily to oureconomy.

TheIFRSstandardsaremuchmorecomplexthanmanyCanadianbusinessesrequire in preparing their financial statements. Most Canadian businesses aresmalltomediuminsizeandareprivatelyowned.Themostsignificantusersoftheirfinancialinformationaretheircreditors(likelytheirbank)andthegovern-ment(forcomputingincometaxesandsalestaxes).Consequently,asecondsetofaccountingstandards,Accounting Standards for Private Enterprises,orASPE,wasdevelopedforthesetypesofbusinesses.

TheprimaryreasonforthedevelopmentofASPEisusers’accesstoacompa-ny’sfinancialinformation.Forsmaller,privatebusinesses,whethertheyarepro-prietorships,partnerships,orcorporations,thevarioususergroupsthatinteractwiththecompanytypicallyhavebetteraccesstotheownersandmanagersofthecompany.Therefore,theusersdonotneedasmuchinformationfromthefinancialstatements,whichmakesrecordkeepingandfinancial-statementproductionlesscostlyforprivatecompanies.Ifabankerhasaquestionaboutaprivatecompany’spurchasesofequipment,thebankercanasktheownerdirectly.However,manyoftheusergroupswhoneedfinancialinformationaboutlarger,publiclytradedcompaniesdonothavethesameaccesstothemanagersand,therefore,needmoreinformationinthefinancialstatements.FinancialstatementspreparedusingIFRSprovidethisadditionalinformation.ThefocusofthistextbookwillbeASPE,withIFRSmaterialappearingasthefinalLearningObjectiveineachchapter.

ItisimportanttorememberthatpubliclyaccountableenterprisesmustfollowIFRS.Otherfor-profitenterprisescanfolloweitherASPEorcanchoosetofollowIFRS.Forexample,acompanyplanningtotradeitssharesonastockexchangeinthefuturemightchoosetofollowIFRSearlierforasmoothtransition.

Both IFRS and ASPE are prepared under the authority of the AccountingStandardsBoardandarepublishedaspartoftheCanadianInstituteofCharteredAccountants(CICA)Handbook.Thesestandardsareverydetailedandcomplete,andasyoubecomemoreknowledgeableinaccounting,youwillneedtobecomefamiliarwithmanyofthem.

ItisinterestingtonotethatbothIFRSandASPEare“principles-based.”Thismeansthatstandardscannotpossiblybedevelopedforeveryaccountingtransac-tionacompanywillencounter,sotheaccountantmustuseprofessionaljudgmentin somecircumstances.Professional judgment is anacquired skill—youneedagoodknowledgeofaccountingstandardsandmanyyearsofexperienceinorder

M01_HORN0096_01_SE_C01.indd 12 10/4/12 1:12 PM

Chapter 1 AccountingandtheBusinessEnvironment 13

toexercisesoundprofessionaljudgment.However,itisimportanttonotethatthestartingpointinacquiringprofessionaljudgmentisasolidunderstandingoftheconceptsofaccounting.

IntheHandbook,theintroductiontoboththeASPEandIFRSsectionsdiscussfinancial statement concepts in some detail. These are the concepts on whichASPEandIFRSarebased.Consequently,wewillnowintroducesomeofthemoreimportantfundamentalconceptsinaccounting.

Framework for Financial ReportingFundamental accounting concepts form the basis of how accounting should bedoneandreportedtousers.Exhibit1–6providesahierarchyoffinancialstatementconcepts.Thisistheframeworkforfinancialreporting.Asthepyramidshapeindi-cates,thefinancialreportsissuedbyacompanyaretheendproductdesignedtosatisfythefinancial-informationneedsofvarioususergroups,andtheyarebuiltonastrongfoundationofaccountingprinciples.Let’slookmorecloselyateachlevel.

A Hierarchy of Financial-Statement ConceptsExhibit 1–6

Recognition and Measurement Criteria, and Constraints

Considerations Principles Constraints Economic Entity Recognition Criteria Cost/BenefitGoing Concern Revenue MaterialityStable Monetary Unit Expense Measurement Cost Other bases (used in limited circumstances) Disclosure

Elements of Financial Statements

Assets Liabilities Equity Revenue and Gains and Expenses Losses

Qualitative Characteristics ofAccounting Information

Relevance ReliabilityComparability Understandability

Objective of Financial Reporting

Communicate useful information to users

LEVEL

1.

2.

3.

4.

Level 1:Exhibit1–6showsthattheprimaryobjectiveoffinancialstatementsistocommunicateinformationthatisusefultoinvestors,creditors,andotherusersinmakinginvestmentdecisionsorassessingthesuccessofacompany.Whatdoesthismean?Ideally,thefinancialinformationprovidedshouldallowaninterestedusertomakedecisionsaboutitsongoingfinancialrelationshipwithanorganization.

Level 2:Thequalitativecharacteristicsofusefulfinancialinformationidentifythetypesofinformationthatarelikelytobethemostusefultothevarioususersoffinancial reports, whichare existingandpotential investors, lenders, andothercreditors. The four characteristics identified are understandability, relevance,reliability,andcomparability.

M01_HORN0096_01_SE_C01.indd 13 10/4/12 1:12 PM

14 Part 1 TheBasicStructureofAccounting

• Theinformationmustbeunderstandabletousersiftheyaretobeabletouseit.• Relevantfinancialinformationiscapableofmakingadifferenceinthedecisions

made by users. To be relevant, the information must allow users to predictfutureoutcomesorprovide feedbackaboutpreviousmanagementdecisions,or both.

• Financialinformationisonlyusefulifitisreliable.Informationisreliablewhenitaccuratelyrepresentstheimpactofthetransactionsthataresummarizedinthefinancialstatements,andisfreeoferrorandbias.

• Thecomparabilitycharacteristicfocusesontherelationshipbetweentwopiecesofinformationratherthanaparticularpieceofinformation.Itenablesuserstoidentifysimilaritiesanddifferencesbetweentheinformationprovidedbytwosetsoffinancialstatements.

Let’s take a moment to understand the role of these characteristics. Assumethatyouhavedecidedthatyouwouldliketoinvestsomeofyoursavingsinthesharesofacompany.Howwouldyoudecideonacompanyto invest in?Yourstartingpointwouldlikelybethefinancialstatements.Youarehopingthat thefinancialstatementsarereliable(thattheinformationreportedaccuratelyreflectsthetransactionsofthecompany)andthattheinformationisrelevant(itprovidesinformationuponwhichyoucanbaseyourinvestmentdecision).Youmightwanttomeasuretheresultsofthecompanyagainstitsresultsinpreviousyearsoryoumightliketocomparetheresultsofonecompanyagainsttheresultsofanothercompanyinthesameindustry(comparability).

Ifthesecharacteristicsareinplace, itmakesyourinvestmentdecisionalittleeasier.Certainlythereisotherinformationthatyoumaywanttostudybeforeyoumakeyourdecision,butthefinancialstatementsareagoodstartingpoint.

Level 3:Elements of financial statementsarethebasiccategoriesofitemsportrayedonthefinancialstatementstomeettheobjectivesoutlinedinLevel1.Wewilllearnmoreabouttheseitemslaterinthischapter.

Level 4:Thisleveloutlinessomebasicconsiderations,principles,andconstraintsthataccountantsrelyuponwhenproducingthefinancialinformationrequiredtosatisfytheneedsofusersoutlinedinLevel1.Theeconomicentity,goingconcern,andstablemonetaryunitconsiderationsarebasicassumptionsusedinbothASPEandIFRS.

Inaccounting,anentityisanorganizationorasectionofanorganizationthatstands apart from other organizations and individuals as a separate economicunit.Eachentityisaccountedforseparately.Thisappliesinsituationswhereyoukeepyourbusiness’saccountingseparatefromyourpersonalaccountingsothatyoucanevaluatethesuccessofyourbusiness.Italsoappliesinsituationswherecompanieskeepeachdepartment’saccountingseparatefromalltheotherdepart-mentstoassessandevaluatetheperformanceofeachdepartment.Resultsforeachdepartmentcanthenbecombinedtocreateresultsforthewholeorganization.

Whenaccountantsrecordfinancialinformation,theyassumethattheentityonwhichtheyarereportingisgoingtobeinbusinessfortheforeseeablefuture.Thisgoing-concern assumptionisimportantbecauseitimpactsthewaywemeasurecertaintransactions.Forexample,awarehousecosting$100,000maybevaluabletoacompanybecauseitexpectstouseitforthenexttenyears,sothecompanyrecordsthecostofthewarehouseasthe$100,000itpaid.However,ifthecompanywasforcedtosellthewarehousetomorrowbecauseitwasgoingoutofbusiness,itmightonlybeabletoget$50,000foritbecauseitisforcedtoacceptwhateverpriceitcangetforthewarehouse.Inthissituation,thecostofthewarehouseshouldbe$50,000.Thegoing-concernassumptionallowsthecompanytorecordthe$100,000costofthewarehousewhenitispurchased.Wewilldiscussthisassumptionasnecessaryinfuturechapters.

InCanada,accountantsrecordtransactionsindollarsbecausethedollaristhemeasureweusewhenwemakepurchasesandsales.However,unlikeothermea-sureslikeakilometeroratonne,thevalueofadollarcanchangeovertime.Arise

M01_HORN0096_01_SE_C01.indd 14 10/4/12 1:12 PM

Chapter 1 AccountingandtheBusinessEnvironment 15

inthegenerallevelofpricesiscalledinflation.Duringinflation,adollarwillpur-chaselessmilk,lesstoothpaste,andlessofothergoodsovertime.Whenpricesarerelativelystable—whenthereislittleinflation—thepurchasingpowerofmoneyisalsostable.Whenthedollar’spurchasingpowerisrelativelystable,thestable monetary unit assumptionallowsaccountantstoignoretheeffectofinflationintheaccountingrecords.Itallowsaccountantstoaddandsubtractdollaramountsforactivitiesthathappenedatdifferenttimes.

Toproducethefinancialinformationthatusersneed,accountantsmustfollowrecognition criteriaandprinciples tomeasureanddisclose (or report) financialinformation, as shown in Level 4 of Exhibit 1–6. Recognition is the process ofincludinganiteminthefinancialstatementsofacompany.Howdoesanaccoun-tantdecidewhenanitemshouldberecognizedinthefinancialstatements?ThecriteriafordeterminingwhenanitemshouldberecognizedareexaminedlaterinthischapterandinmoredetailinChapter3.

Measurement is the process of determining the amount at which an item isrecognized in the financial statements. There are a number of bases on whichanamountcanbemeasured.Financialstatementsarepreparedprimarilyusingthehistorical-costbasisofmeasurement,commonlycalledthecost principle.Thecost principle of measurementstatesthatacquiredassetsandservicesshouldberecordedattheiractualcost(alsocalledhistorical cost).Eventhoughthepurchasermaybelievethepricepaidisabargain,theitemisrecordedatthepriceactuallypaidandnotatthe“expected”cost.

The cost principle of measurement also holds that the accounting recordsshouldcontinuereportingthehistoricalcostofanassetforaslongasthebusinessholdstheasset.Why?Becausecostisareliablemeasure.

Otherbasesofmeasurementcanbeusedbutonlyinlimitedcircumstances.Inparticularcircumstances,wemayusereplacementcost,realizablevalue,orpres-entvalue.Theseotherbasesofmeasurementwillbediscussedonlyasneededinfuturechapters.

Level 4 inExhibit 1–6also includes twoconstraints that accountantsmustconsiderwhentheyareproducingfinancialinformation.Thefirstconstraintisthat thebenefitsof the informationproducedshouldexceedthecostsofpro-ducingtheinformation.Thesecondconstraintismateriality.Apieceofinfor-mationismaterialifitwouldaffectadecisionmaker’sdecision.Materialityisnotdefinedinthestandardsbutisamatteroftheinformationpreparer’sjudg-ment.Forexample,informationaboutinventoryisimportanttousersofRonaHardware’s financial statements, since a change in inventory could change adecisionmaker’sdecisionaboutinvestinginRonaorsellingproductstoRona.Thus,suchinformationwouldbeprovidedtodecisionmakers.However,infor-mationabout theoffice suppliesatRonawouldnot likelychange the invest-mentdecisionofaRonafinancial-statementuser,sodetailsofsuchinformationarenotprovided.

Exhibit 1–6 summarizes thekeypoints for recordingand reporting financialinformation:Foranyfinancialtransactionorsituation,theGAAPinLevel4areused as guidelines for classifying the transaction’s financial data into the stan-dard financial-statementelementsshown inLevel3. If theseelementsmeet theLevel-2qualitativecharacteristicsofaccountinginformation,theyarecombinedinto financial statements that meet the Level-1 objective of reporting financialinformationusefulforusers.FinancialinformationcanbereportedtousersusingeitherASPEorIFRS,dependingonwhetherthecompanyisapubliclyaccountableenterprise(mustuseIFRS)ornot(canuseASPEorIFRS).

This course will expose you to the generally accepted methods of account-ing.Webegin thediscussionofGAAP in this sectionand introduceadditionalassumptionsandprinciplesasneededthroughoutthebook.Throughoutthetext,wewilllinktheaccountinginthatchaptertotheframeworkforfinancialreport-ing using Why It’s Done This Way boxes. The hierarchy of financial statementconceptsformingtheframeworkforfinancialreportingfromExhibit1–6isshownonthebackinsidecoverofthistextbookforeasyreference.

M01_HORN0096_01_SE_C01.indd 15 10/4/12 1:12 PM

16 Part 1 TheBasicStructureofAccounting

the Accounting Equation

Financial statements tell us how a business is performing and where it stands.Theyarethefinalproductoftheaccountingprocess.Buthowdowearriveattheitemsandamountsthatmakeupthefinancialstatements?Themostbasictooloftheaccountantistheaccounting equation.Itmeasurestheresourcesofabusinessandtheclaimstothoseresources.

Assets and LiabilitiesAssetsareeconomicresourcescontrolledbyanentitythatareexpectedtobenefitthebusinessinthefuture.Cash,officesupplies,merchandiseinventory,furniture,land,andbuildingsareexamplesofassets.

Claimstothoseassetscomefromtwosources.Liabilitiesaredebtsthatarepay-abletooutsiders.Theseoutsidepartiesarecalledcreditors.Forexample,acreditorwhohaslentmoneytoabusinesshasaclaim—alegalright—toapartoftheassetsuntil the business pays the debt. Many liabilities have the word payable in theirtitles.Examples includeAccountsPayable,NotesPayable,andSalariesPayable.Insiderclaimstothebusinessassetsareowners’claimscalledowner’s equityorcapital.Anowner’s claim to someof theentity’sassetsbeginswhen theownerinvestsinthebusiness.

TheaccountingequationinExhibit1–7showshowassets,liabilities,andown-er’sequityarerelated.Assetsappearontheleftsideoftheequation.Thelegalandeconomicclaimsagainsttheassets—theliabilitiesandowner’sequity—appearontherightsideoftheequation.AsExhibit1–7shows,the two sides must be equal:

Economic Resources Claims to Economic Resources(Outsiders) (Insiders)

Assets 5 Liabilities 1 Owner’s Equity

Owner’s EquityOwner’s equityistheamountofanentity’sassetsthatremainsaftertheliabilitiesaresubtracted.Forthisreason,owner’sequityisoftenreferredtoasnet assets,andtheaccountingequationcanbewrittentoshowthis:

Assets 2 Liabilities 5 Owner’s Equity

10. Explainwhyfinancialinformationmustbebothrelevantandreliable.

11. Supposeyouareconsideringthepurchaseoflandforfutureexpansion.Thesellerisasking$200,000forlandthatcosther$100,000.Anappraisalshowsthelandhasavalueof$180,000.Youfirstoffer$160,000.Thesellercounterofferswith$190,000.Finally,youandtheselleragreeonapriceof$185,000.Whatdollaramountforthislandisreportedonyourfinancialstatements?Whichaccountingconsiderationorprincipleguidesyouranswer?

12. Supposeyouownacompanythatdeliversnewspapers.Thecompanyownstwotrucksthatareusedfordeliveringthepapers.Youhavedecidedthatyouneedanewcarformainlypersonalpurposesbutyouwantthecompanytobuyitforyou.Isthisappropriate?Nametheconsiderationorprinciplethatmustbeconsidered.

Just Checking Solutions appear at the end of this chapter and on MyAccountingLab.

JUST CHECKING

LO 5Howdobusinesstransactionsaffecttheaccountingrecordsofacompany?

IFRS

Exhibit 1–7

The Accounting Equation

Assets �

Assets

Liabilities�

Owner’sEquity

Owner’sEquity

Liabilities

Increasesincasharenotalwaysrevenues.Cashalsoincreaseswhenacompanyborrowsmoney,butborrowingmoneycreatesaliability—notarevenue.Revenueresultsfromrenderingaserviceorsellingaproduct,notnecessarilyfromthereceiptofcash.

KEY POINTS

MyAccountingLab

M01_HORN0096_01_SE_C01.indd 16 10/4/12 1:12 PM

Chapter 1 AccountingandtheBusinessEnvironment 17

Thepurposeofbusinessistoincreaseowner’sequitythroughrevenues,whichare amounts earned by delivering goods or services to customers. Revenuesincrease owner’s equity because they increase the business’s assets but not itsliabilities.Asaresult,theowner’sshareofbusinessassetsincreases.Examplesofrevenue includesales revenue fromsellinggoods, service revenue fromsellingservices, interest revenue fromsavingmoney inabank, anddividend revenuefrominvestinginsharesofstock.Exhibit1–8showsthatownerinvestmentsandrevenuesincreasetheowner’sequityofthebusiness.

Exhibit1–8alsoshows thatownerwithdrawalsandexpensesdecreaseown-er’sequity.Owner withdrawals are thoseamountsor resources removed fromthebusinessbytheowner.Withdrawalsaretheoppositeofownerinvestments.Expenses are decreases in owner’s equity that occur from using or consumingassetsorincreasingliabilitiesinthecourseofdeliveringgoodsandservicestocus-tomers.Expensesarethecostofdoingbusinessandaretheoppositeofrevenues.Expensesincludethecostofofficerent;interestpayments;salariesofemployees;insurance;advertisements;propertytaxes;utilitypaymentsforwater;electricity;gas;andsoforth.

AccountnamesfordifferenttypesofbusinessesaregiveninAppendixBattheendofthisbook.

Transactions that Increase and Decrease Owner’s EquityExhibit 1–8

INCREASEOWNER’S EQUITY

DECREASE

Owner Investmentsin the Business

Revenues

Owner Withdrawalsfrom the Business

Expenses

Decreasesincasharenotalwaysexpenses.Cashdecreaseswhenlandispurchased,forexample,butthepurchasealsoincreasestheassetLand,whichisnotanexpense.Expensesresultfromusinggoodsorservicesinthecourseofearningrevenue,notnecessarilyfromthepaymentof cash.

KEY POINTS

Accounting for Business transactions

Accountingisbasedontransactions,notopinionsordesires.Atransactionisanyeventthataffectsthefinancialpositionofthebusinessentityandcanbemeasuredreliably.Manyeventsmayaffecta company, includingelectionsandeconomicbooms.Accountantsdonotrecordtheeffectsof theseeventsbecause theycan-notbemeasuredreliably.Anaccountantrecordsastransactionsonlyeventswithdollaramountsthatcanbemeasuredreliably,suchaspurchasesandsalesofmer-chandise inventory,paymentof rent, andcollectionof cash fromcustomers. InExhibit1-1onpage5,transactionsarethemiddlestepintheflowofinformationinanaccountingsystem.

Toillustrateaccountingforbusinesstransactions,let’sgobacktoouropeningstoryandtracethetransactionsforLisaHunter’scompany,HunterEnvironmentalConsulting(HEC),inthefirstyearofherbusiness.Wewillconsider11eventsandanalyzeeachintermsofitseffectontheaccountingequationofHEC.Remember that the accounting equation must always remain in balance.Transactionanalysisistheessenceofaccounting.

Transaction 1: Starting the Business Hunterinvests$250,000ofhermoneytostartthebusiness.Specifically,shedeposits$250,000inabankaccountentitledHunterEnvironmentalServices.

Atransactionisaneventthatmustalwayssatisfythesetwoconditions:

1. Itaffectsthefinancialpositionofabusinessentity,and

2. Itcanbereliablyrecordedintheaccountingrecords.

KEY POINTS

M01_HORN0096_01_SE_C01.indd 17 10/4/12 1:12 PM

18 Part 1 TheBasicStructureofAccounting

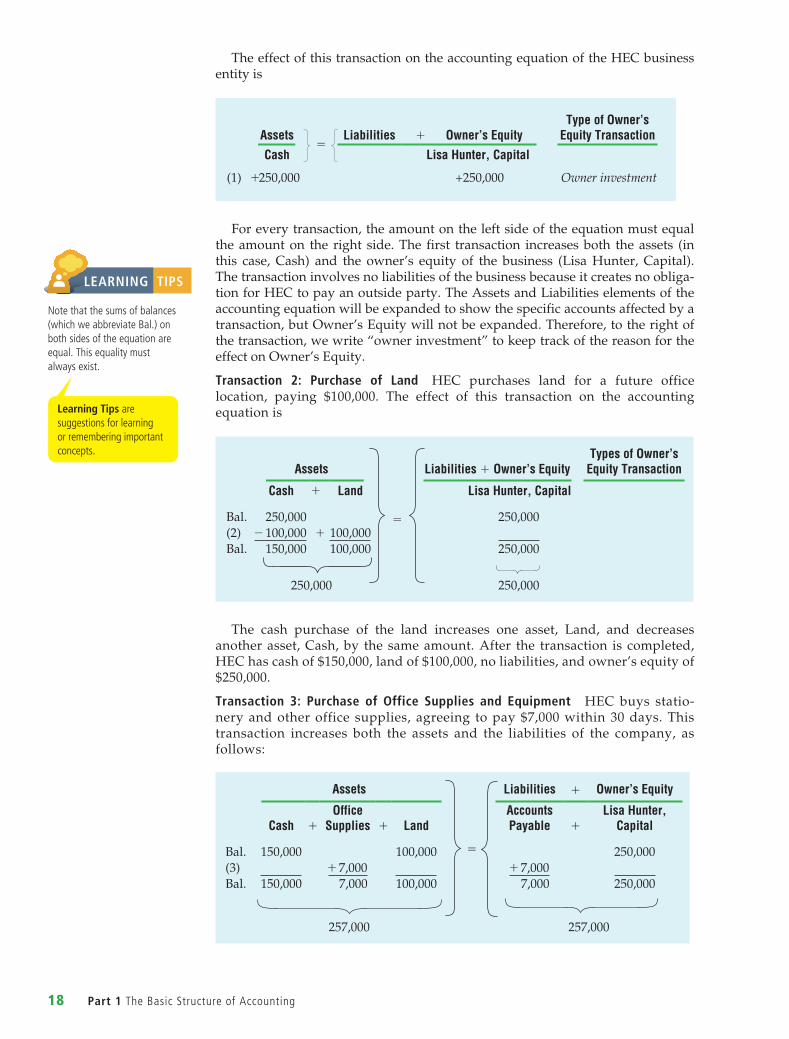

TheeffectofthistransactionontheaccountingequationoftheHECbusinessentityis

Assets 5

Liabilities 1 Owner’s EquityType of Owner’s

Equity Transaction

Cash Lisa Hunter, Capital

(1) +250,000 +250,000 Owner investment

Foreverytransaction,theamountontheleftsideoftheequationmustequalthe amount on the right side. The first transaction increases both the assets (inthis case, Cash) and the owner’s equity of the business (Lisa Hunter, Capital).Thetransactioninvolvesnoliabilitiesofthebusinessbecauseitcreatesnoobliga-tionforHECtopayanoutsideparty.TheAssetsandLiabilitieselementsoftheaccountingequationwillbeexpandedtoshowthespecificaccountsaffectedbyatransaction,butOwner’sEquitywillnotbeexpanded.Therefore,totherightofthetransaction,wewrite“ownerinvestment”tokeeptrackofthereasonfortheeffectonOwner’sEquity.

Transaction 2: Purchase of Land HEC purchases land for a future officelocation, paying $100,000. The effect of this transaction on the accountingequationis

Assets Liabilities 1 Owner’s EquityTypes of Owner’s

Equity Transaction

Cash 1 Land Lisa Hunter, Capital

Bal. 250,000 5 250,000(2) -100,000 + 100,000Bal. 150,000 100,000 250,000

250,000 250,000

The cash purchase of the land increases one asset, Land, and decreasesanotherasset,Cash,by the sameamount.After the transaction is completed,HEChascashof$150,000,landof$100,000,noliabilities,andowner’sequityof$250,000.

Transaction 3: Purchase of Office Supplies and Equipment HEC buys statio-neryandotheroffice supplies, agreeing topay$7,000within30days.Thistransaction increases both the assets and the liabilities of the company, asfollows:

Assets Liabilities 1 Owner’s Equity

Cash 1Office

Supplies 1 LandAccounts Payable 1

Lisa Hunter, Capital

Bal. 150,000 100,000 5 250,000(3) +7,000 +7,000Bal. 150,000 7,000 100,000 7,000 250,000

257,000 257,000

LEARNING TIPS

Notethatthesumsofbalances(whichweabbreviateBal.)onbothsidesoftheequationareequal.Thisequalitymustalwaysexist.

Learning Tips aresuggestionsforlearningorrememberingimportantconcepts.

M01_HORN0096_01_SE_C01.indd 18 10/4/12 1:12 PM

Chapter 1 AccountingandtheBusinessEnvironment 19

The asset affected is Office Supplies, and the liability is called an account payable. A payable is always a liability. Because HEC is obligated to pay $7,000in the futurebutsignsnoformalpromissorynote,werecordthe liabilityasanAccountPayable.(Ifapromissorynotehadbeensigned,wewouldhaverecordedtheliabilityasaNote Payable.)

Transaction 4: Earning of Service Revenue HECearnsservicerevenuebyprovid-ing environmental consulting services for clients. Assume the business earns$30,000andcollectsthisamountincash.TheeffectontheaccountingequationisanincreaseintheassetCashandanincreaseinLisaHunter,Capital,asfollows:

Assets Liabilities 1 Owner’s EquityType of Owner’s

Equity Transaction

Cash 1Office

Supplies 1 LandAccounts Payable 1

Lisa Hunter, Capital

Bal. 150,000 7,000 100,000 5 7,000 250,000Service revenue(4) +30,000 +30,000

Bal. 180,000 7,000 100,000 7,000 280,000

287,000 287,000

Arevenuetransactioncausesthebusinesstogrow,asshownbytheincreaseintotalassetsandinthesumoftotalliabilitiesplusowner’sequity.AcompanylikeRONAorCanadianTirethatsellsgoodstocustomers isamerchandisingbusi-ness.Itsrevenueiscalledsales revenue.Incontrast,HECperformsservicesforcli-ents.HEC’srevenueiscalledservice revenue.

Transaction 5: Earning of Service Revenue on Account HECperformsconsultingservicesforclientswhodonotpayimmediately.Inreturnfortheservices,HECissuesaninvoiceandtheclientswillpaythe$25,000amountwithinonemonth.ThisamountowedtoHECisanassettoHEC,anaccountreceivablebecausethebusinessexpectstocollectthecashinthefuture.Inaccounting,wesaythatHECperformedthisserviceon accountandearnedtherevenue.Performingtheservice,not collecting thecash,earns the revenue.This$25,000of service revenue isasrealan increase in thewealthofHEC’sbusinessas the$30,000of revenue thatwascollectedimmediatelyinTransaction4.HECrecordsanincreaseintheassetAccounts Receivable and an increase in Service Revenue, which increases LisaHunter,Capital,asfollows:

Assets Liabilities 1 Owner’s EquityType of Owner’s

Equity Transaction

Cash 1Accounts

Receivable 1Office

Supplies 1 LandAccounts Payable 1

Lisa Hunter, Capital

Bal. 180,000 7,000 100,000 5 7,000 280,000Service revenue(5) +25,000 +25,000

Bal. 180,000 25,000 7,000 100,000 7,000 305,000

312,000 312,000

Transaction 6: Payment of Expenses Duringthemonth,HECpays$12,000incashexpenses:officerent,$4,000(HECpurchasedlandtobuildanofficeinthefuture(transaction 2), but the company is renting fully furnished office space in the

Allreceivablesareassets.Allpayablesareliabilities.

KEY POINTS

M01_HORN0096_01_SE_C01.indd 19 10/4/12 1:12 PM

20 Part 1 TheBasicStructureofAccounting

meantime);employeesalaries,$6,500(forafull-timeassistantandajuniorconsul-tant);andtotalutilities,$1,500.Theeffectsontheaccountingequationare

Expenses have the opposite effect of revenues. Expenses cause the business toshrink,asshownbythedecreasedbalancesoftotalassetsandowner’sequity.

Eachexpenseshouldberecordedinaseparatetransaction.Here,forsimplic-ity,theexpensesarelistedtogether.Alternatively,wecouldrecordthecashpay-mentinasingleamountforthesumofthosethreeexpenses,$12,000($4,000+$6,500+$1,500).Ineithercase,the“balance”oftheequationholds,asweknowitmust.

Transaction 7: Payment on Account HECpays$5,000tothestorefromwhichitpur-chased$7,000worthofofficesuppliesinTransaction3.Inaccounting,wesaythatthebusinesspays$5,000on account.TheeffectontheaccountingequationisadecreaseintheassetCashandadecreaseintheliabilityAccountsPayableasfollows:

Assets Liabilities 1 Owner’s Equity

Cash 1Accounts

Receivable 1Office

Supplies 1 LandAccounts Payable 1

Lisa Hunter, Capital

Bal. 168,000 25,000 7,000 100,000 5 7,000 293,000

(7) - 5,000 -5,000

Bal. 163,000 25,000 7,000 100,000 2,000 293,000

295,000 295,000

The payment of cash on account has no effect on the asset Office Suppliesbecausethepaymentdoesnotincreaseordecreasethesuppliesavailabletothebusiness.Likewise, thepaymentonaccountdoesnotaffectexpenses.HECwaspayingoffaliability,notanexpense.

Transaction 8: Personal Transaction LisaHunterremodelsherhomeatacostof$30,000,payingcashfrompersonalfunds.ThiseventisnotatransactionofHEC.IthasnoeffectonHEC’sbusinessaffairsand,therefore,isnotrecordedbythebusi-ness.ItisatransactionoftheHunterpersonalentity,nottheHECbusinessentity.Wearefocusingnowsolelyonthebusinessentity,andthiseventdoesnotaffectit.Thistransactionillustratestheeconomic-entityconsideration.

Transaction 9: Collection on Account InTransaction5,HECperformedconsult-ing services for clients on account. The business now collects $15,000 from a

Assets Liabilities 1 Owner’s EquityType of Owner’s

Equity Transaction

Cash 1Accounts

Receivable 1Office

Supplies 1 LandAccounts Payable 1

Lisa Hunter, Capital

Bal. 180,000 25,000 7,000 100,0005

7,000 305,000Rent expenseSalaries expenseUtilities expense

(6) -4,000 -4,000-6,500 -6,500-1,500 -1,500

Bal. 168,500 25,000 7,000 100,000 7,000 293,000

300,000 300,000

M01_HORN0096_01_SE_C01.indd 20 10/4/12 1:12 PM

Chapter 1 AccountingandtheBusinessEnvironment 21

client.Wesaythatitcollectsthecashon account.ItwillrecordanincreaseintheassetCashandadecreaseintheassetAccountsReceivable.Shoulditalsorecordanincreaseinservicerevenue?No,becauseHECalreadyrecordedtherevenuewhen it performed the service in Transaction 5. The effect on the accountingequationis

Assets Liabilities 1 Owner’s Equity

Cash 1Accounts

Receivable 1Office

Supplies LandAccounts Payable 1

Lisa Hunter, Capital

Bal. 163,000 25,000 7,000 100,000 5 2,000 293,000(9) +15,000 -15,000Bal. 178,000 10,000 7,000 100,000 2,000 293,000

295,000 295,000

Totalassetsareunchangedfromtheprecedingtransaction’stotal.Why?BecauseHECmerelyexchangedoneassetforanother.

Transaction 10: Sale of Land Lisasells50%ofthelandpurchasedinTransaction2.Thesalepriceof$50,000isequaltoHEC’scostoftheland.HECsellsthelandandreceives$50,000cash,andtheeffectontheaccountingequationis

Assets Liabilities 1Owner’s Equity

Cash 1Accounts

Receivable 1Office

Supplies 1 LandAccounts Payable 1

Lisa Hunter, Capital

Bal. 178,000 10,000 7,000 100,000 5 2,000 293,000(10) + 50,000 - 50,000Bal. 228,000 10,000 7,000 50,000 2,000 293,000

295,000 295,000

Transaction 11: Withdrawing of Cash Lisawithdraws$6,000cashforherpersonaluse.Theeffectontheaccountingequationis

Assets Liabilities 1 Owner’s EquityType of Owner’s

Equity Transaction

Cash 1Accounts

Receivable 1Office

Supplies 1 LandAccounts Payable 1

Lisa Hunter, Capital

Bal. 228,000 10,000 7,000 50,000 5 2,000 293,000Owner withdrawal- 6,000 -6,000

Bal. 222,000 10,000 7,000 50,000 2,000 287,000

289,000 2,89,000

Hunter’s withdrawal of $6,000 cash decreases the asset Cash and also theowner’sequityofthebusiness.

Owner withdrawals do not represent a business expense because the cash is used for the owner’s personal affairs unrelated to the business.Werecordthisdecreaseinowner’sequityasWithdrawalsorDrawings.Thedoubleunderlinesbeloweachcolumnindicateafinaltotalafterthelasttransaction.

M01_HORN0096_01_SE_C01.indd 21 10/4/12 1:12 PM

22 Part 1 TheBasicStructureofAccounting

Exhibit 1–9 Analysis of Transactions of Hunter Environmental Consulting

Evaluating Business transactions

Exhibit1–9summarizesthe11precedingtransactions.PanelAoftheexhibitliststhedetailsofthetransactions,andPanelBpresentstheanalysis.Asyoustudytheexhibit,notethateverytransactionmaintainstheequalityoftheequation

Assets 5 Liabilities 1 Owner’s Equity

MyAccountingLab

Accounting Cycle Tutorial

1. BalanceSheetAccountsandTransactionspages1–12

2. IncomeStatementAccountsandTransactionspages1–6

ThesereferencestoMyAccountingLabareremindersthatyoucanreviewthesetopicsusingtheAccountingCycleTutorialsonMyAccountingLab.

PANEL A: DETAILS OF TRANSACTIONS(1) Thebusinessrecordedthe$250,000cashinvestmentmadebyLisaHunter.(2) Paid$100,000cashforland.(3) Bought$7,000ofofficesuppliesonaccount.(4) Received$30,000cashfromclientsforservicerevenueearned.(5) Performedservicesforclientsonaccount,$25,000.(6) Paidcashexpenses:rent,$4,000;employeesalary,$6,500;utilities,$1,500.(7) Paid$5,000ontheaccountpayablecreatedinTransaction3.(8) RemodelledHunter’spersonalresidence.Thisisnotatransactionofthebusiness.(9) Collected$15,000ontheaccountreceivablecreatedinTransaction5.(10) Soldlandforcashequaltoitscostof$50,000.(11) Thebusinesspaid$6,000cashtoHunterasawithdrawal.

PANEL B: ANALYSIS OF TRANSACTIONS

Assets Liabilities 1 Owner’s EquityType of Owner’s

Equity Transaction

Cash Accounts

Receivable Office

Supplies Land

Accounts Payable

Lisa Hunter, Capital

(1) +250,000 +250,000 Owner investmentBal. 250,000 250,000(2) -100,000 +100,000Bal. 150,000 100,000 250,000(3) +7,000 +7,000Bal. 150,000 7,000 100,000 7,000 250,000(4) +30,000 +30,000 Service revenueBal. 180,000 7,000 100,000 7,000 280,000(5) +25,000 +25,000 Service revenueBal. 180,000 25,000 7,000 100,000 7,000 305,000(6) -4,000 5 -4,000 Rent expense

-6,500 -6,500 Salaries expense-1,500 -1,500 Utilities expense

Bal. 168,000 25,000 7,000 100,000 7,000 293,000(7) -5,000 -5,000Bal. 163,000 25,000 7,000 100,000 2,000 293,000(8) Notatransactionofthebusiness(9) +15,000 -15,000Bal. 178,000 10,000 7,000 100,000 2,000 293,000(10) +50,000 -50,000Bal. 228,000 10,000 7,000 50,000 2,000 293,000(11) -6,000 -6,000 Owner withdrawalBal. 222,000 10,000 7,000 50,000 2,000 287,000

289,000 289,000

1 1 11

M01_HORN0096_01_SE_C01.indd 22 10/4/12 1:12 PM

Chapter 1 AccountingandtheBusinessEnvironment 23

the Financial Statements

Once the analysis of the transactions is complete, what is the next step in theaccountingprocess?Howdoesabusinesspresenttheresultsofthetransactions?Wenowlookatthefinancial statements,whicharetheformalreportsofanentity’sfinancialinformation.Theprimaryfinancialstatementsarethe:

• Incomestatement• Statementofowner’sequity• Balancesheet• Cashflowstatement

Income Statement The income statementpresentsasummaryof therevenuesandexpensesofanentityforaspecificperiodoftime,suchasamonthorayear.The income statement, also called the statement of earnings or statement of operations,islikeavideooftheentity’soperations—amovingfinancialpictureofbusinessoperationsduringtheperiod.Theincomestatementholdsperhapsthemostimportantsinglepieceofinformationaboutabusiness—itsnet income or net loss.Businesspeopleruntheirbusinesseswiththeobjectiveofhavingmorerevenuesthanexpenses.Anexcessoftotalrevenuesovertotalexpensesiscallednet income,net earnings,ornet profit.Iftotalexpensesexceedtotalrevenues,theresultiscalledanet loss.

Statement of Owner’s Equity Thestatement of owner’s equitypresentsasum-maryofthechangesthatoccurredintheentity’sowner’s equityduringaspecificperiodoftime,suchasamonthorayear.

Increasesinowner’sequityarisefrom:

• Ownerinvestments• Netincome(revenuesexceedexpenses)

Decreasesinowner’sequityarisefrom:

• Ownerwithdrawals• Netloss(expensesexceedrevenues)

13. a. Iftheassetsofabusinessare$75,000andtheliabilitiestotal$65,000,howmuchistheowner’sequity?

b. Iftheowner’sequityinabusinessis$50,000andtheliabilitiesare$20,000,howmucharetheassets?

14. Indicatewhethereachaccountlistedbelowisa(n)asset(A),liability(L),owner’sequity(OE),revenue(R),orexpense(E)account.

AccountsReceivable _____

ComputerEquipment_____

S.Scott,Capital _____

RentExpense _____

Supplies _____

S.Scott,Withdrawals _____

JUST CHECKING

SalariesExpense _____

ConsultingServiceRevenue_____

Cash _____

NotesPayable _____

SuppliesExpense _____

AccountsPayable _____

15. Acustomerpaysadepositof$20,000toyourcompanyforaservicethatyouwill begin to provide six months from now. How do you account for thistransaction?

Just Checking Solutions appear at the end of this chapter and on MyAccountingLab.

LO 6Prepareandevaluatethefinancialstatements

MyAccountingLab

IFRS

M01_HORN0096_01_SE_C01.indd 23 10/4/12 1:12 PM

24 Part 1 TheBasicStructureofAccounting

Net income or net loss comes directly from the income statement. Ownerinvestmentsandwithdrawalsarecapitaltransactionsbetweenthebusinessanditsowner,sotheydonotaffecttheincomestatement.

Balance Sheet Thebalance sheetlistsalltheassets,liabilities,andowner’sequityofanentityasofaspecificdate,usuallytheendofamonthorayear.Thebalancesheetislikeasnapshotoftheentity.Forthisreason,itisalsocalledthestatement of financial position.

Cash Flow Statement The cash flow statement reports the cash coming in(cash receipts) and the cash going out (cash payments or disbursements) during aperiod.Businessactivities result inanet cash inflow (receiptsgreater thanpay-ments)oranetcashoutflow(paymentsgreaterthanreceipts).Thecashflowstate-mentshowsthenet increaseordecrease incashduringtheperiodandthecashbalanceattheendoftheperiod.WefocusonthecashflowstatementinChapter17.

Computersandsoftwareprogramshavehadasignificantimpactontheprepa-rationofthefinancialstatements.Financialstatementscanbeproducedinstanta-neouslyafterthedatafromthefinancialrecordsareenteredintothecomputer.Ofcourse,inmanualandcomputerizedaccountingsystems,anyerrorsthatoccurinthefinancialrecordswillbepassedontothefinancialstatements.Forthisreason,thepersonresponsibleforanalyzingtheaccountingdataiscriticaltotheaccuracyofthefinancialstatements.

Financial Statement HeadingsEachfinancialstatementhasaheading,whichgivesthreepiecesofdata:

• The proper name of the business (in our discussion, Hunter EnvironmentalConsulting)

• Thefullnameoftheparticularstatement• Thedateortimeperiodcoveredbythestatement

Abalancesheet takenat theendofyear2013wouldbedatedDecember31,2013.AbalancesheetpreparedattheendofMarch2014isdatedMarch31,2014.

Anincomestatementorastatementofowner’sequitycoveringayearendingonDecember31,2013,isdated“FortheYearEndedDecember31,2013.”Amonthlyincome statement or statement of owner’s equity for September 2014 has in itsheading “For the Month Ended September 30, 2014” or simply “For the MonthofSeptember2014.”Incomemustbeidentifiedwithaparticulartimeperiod.ThisisbecauseifDecember31,2013appearedintheheadingofthesestatements,youwouldnotknowwhetherthenetincomeamountwasgoodorbadunlessyouknewthetimeperiodcoveredbythestatements.Thenetincomeamountcouldbegoodifthetimeperiodwereoneday,butitcouldbebadifthetimeperiodwereoneyear.

relationships among the Financial Statements

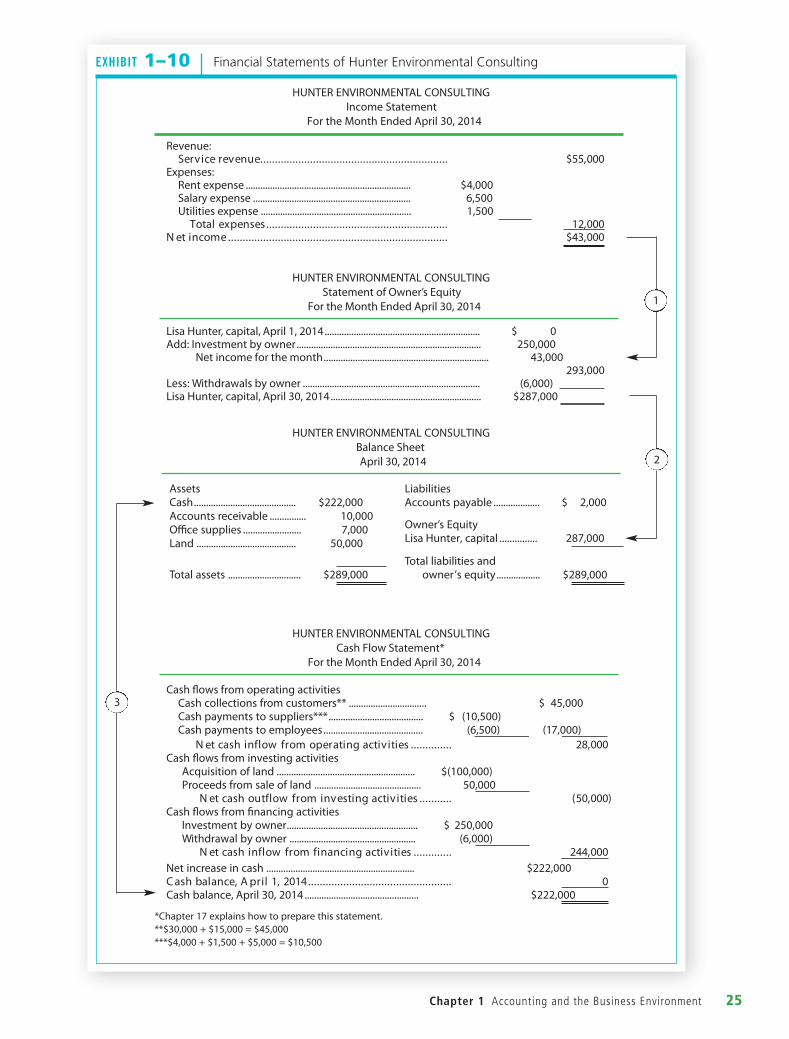

Exhibit1–10onpage25illustratesallfourfinancialstatements.Theirdatacomefrom the transaction analysis in Exhibit 1–9. We are assuming the transactionsoccurredduringthemonthofApril2014.Studytheexhibitcarefully,becauseitshowstherelationshipsamongthefourfinancialstatements.

ObservethefollowinginExhibit1–10:

1. Theincome statementforthemonthendedApril30,2014,a. Reportsallrevenuesandallexpensesduringtheperiod.Expensesareoften

listedalphabetically,butcanalsobe listed indecreasingorderofamount,withthelargestexpensefirst.

b. Reportsnet incomeoftheperiodiftotalrevenuesexceedtotalexpenses,asinthecaseofHEC’soperationsforApril.Iftotalexpensesexceedtotalrevenues,anet lossisreportedinstead.

M01_HORN0096_01_SE_C01.indd 24 10/4/12 1:12 PM

Chapter 1 AccountingandtheBusinessEnvironment 25

Financial Statements of Hunter Environmental ConsultingExhibit 1–10

1

2

Statement of Owner’s EquityFor the Month Ended April 30, 2014

Lisa Hunter, capital, April 1, 2014................................................................ $ 0Add: Investment by owner............................................................................ 250,000

Net income for the month.................................................................... 43,000293,000

Less: Withdrawals by owner ......................................................................... (6,000)Lisa Hunter, capital, April 30, 2014.............................................................. $287,000

Cash Flow Statement*For the Month Ended April 30, 2014

Cash �ows from operating activitiesCash collections from customers** ................................ $ 45,000Cash payments to suppliers***....................................... $ (10,500)Cash payments to employees......................................... (6,500) (17,000)

000,82..............seitivitca gnitarepo morf wolfni hsac teNCash �ows from investing activities

Acquisition of land ......................................................... $(100,000)Proceeds from sale of land ............................................ 50,000

)000,05(...........seitivitca gnitsevni morf wolftuo hsac teNCash �ows from nancing activities

Investment by owner...................................................... $ 250,000Withdrawal by owner .................................................... (6,000)

000,442.............seitivitca gnicnanif morf wolfni hsac teNNet increase in cash ............................................................. $222,000

0.................................................4102 ,1 lirpA ,ecnalab hsaCCash balance, April 30, 2014............................................... $222,000

*Chapter 17 explains how to prepare this statement.**$30,000 + $15,000 = $45,000***$4,000 + $1,500 + $5,000 = $10,500

HUNTER ENVIRONMENTAL CONSULTING

HUNTER ENVIRONMENTAL CONSULTING

HUNTER ENVIRONMENTAL CONSULTING

HUNTER ENVIRONMENTAL CONSULTING

Income Statement For the Month Ended April 30, 2014

Revenue:000,55$................................................................eunever ecivreS

Expenses:Rent expense .................................................................... $4,000Salary expense ................................................................. 6,500Utilities expense .............................................................. 1,500

000,12..............................................................sesnepxe latoT000,34$...........................................................................emocni teN

AssetsCash.......................................... $222,000Accounts receivable ............... 10,000O�ce supplies ........................ 7,000Land ......................................... 50,000

Total assets .............................. $289,000

LiabilitiesAccounts payable ................... $ 2,000

Owner’s EquityLisa Hunter, capital ............... 287,000

Total liabilities andowner’s equity.................. $289,000

Balance SheetApril 30, 2014

3

M01_HORN0096_01_SE_C01.indd 25 10/4/12 1:12 PM

26 Part 1 TheBasicStructureofAccounting

2. Thestatement of owner’s equityforthemonthendedApril30,2014,a. Openswiththeowner’scapitalbalanceatthebeginningoftheperiod.b. Adds investment by the owner andaddsnet income (or subtractsnet loss, as

thecasemaybe).Netincome(ornetloss)comesdirectlyfromtheincomestatement(seearrow1inExhibit1–10).

c. Subtracts withdrawals by the owner. The parentheses around an amountindicateasubtraction.

d.Endswiththeowner’scapitalbalanceattheendoftheperiod.3. Thebalance sheetatApril30,2014,theendoftheperiod,

a. Reportsallassets,allliabilities,andowner’s equityofthebusinessattheendoftheperiod.

b. Reportsthattotalassetsequalthesumoftotal liabilitiesplustotalowner’sequity.

c. Reportstheowner’sendingcapitalbalance,takendirectlyfromthestatementofowner’sequity(seearrow2).

4. Thecash flow statementforthemonthendedApril30,2014,a. Reportscashflowsfromthreetypesofbusinessactivities(operating, investing,

and financing activities) during the month. Each category of cash-flow ac-tivities includes both cash receipts, which are positive amounts, and cashpayments, which are negative amounts (denoted by parentheses). Eachcategoryresultsinanetcashinfloworanetcashoutflowfortheperiod.WediscussthesecategoriesindetailinChapter17.

b. Reportsanetincreaseincash(oranetdecrease,asthecasemaybe)duringthe month and ends with the cash balance at April 30, 2014. This is theamountofcashtoreportonthebalancesheet(seearrow3).

16. Indicate whether each account listed below appears on the balance sheet (B),incomestatement (I), statementofowner’s equity (OE),or cash flowstatement(CF).Someitemsappearonmorethanonestatement.

AccountsReceivable _____

ComputerEquipment_____

S.Scott,Capital _____

RentExpense _____

Supplies _____

S.Scott,Withdrawals _____

JUST CHECKING

17. Study Exhibit 1–10, which gives the financial statements for Hunter Environ-mentalServices(HEC)atApril30,2014,theendofthefirstmonthofoperations.AnswerthesequestionsaboutHECtoevaluatethebusiness’sresults.a. What was the business’s result of operations for the month of April—a net

income(profit)oranetloss,andhowmuch?Whichfinancialstatementpro-videsthisinformation?

b. HowmuchownercapitaldidthecompanyhaveatthebeginningofApril?Atthe end of April? Identify all the items that changed owner’s capital duringthemonth,alongwiththeiramounts.Whichfinancialstatementprovidesthisinformation?

c. Howmuchcashdoesthecompanyhaveasitmovesintothenextmonth—thatis,May2014?Whichfinancialstatementprovidesthisinformation?

d. HowmuchdoclientsoweHECatApril30?Isthisanassetoraliabilityforthebusiness?Whatdoesthebusinesscallthisitem?

e. HowmuchdoesthebusinessoweoutsidersatApril30?Isthisanassetoraliabilityforthebusiness?Whatdoesthebusinesscallthisitem?

Just Checking Solutions appear at the end of this chapter and on MyAccountingLab.

SalariesExpense _____

ConsultingServiceRevenue_____

Cash _____

NotesPayable _____

SuppliesExpense _____

AccountsPayable _____

MyAccountingLab

M01_HORN0096_01_SE_C01.indd 26 10/4/12 1:12 PM

Chapter 1 AccountingandtheBusinessEnvironment 27

As you review the details of each transaction, think of the names of the accounts that will be affected.

Summary problem for Your review

SamanthaTorresopensahomedesignbusinessinCalgary.Sheisthesoleownerof the proprietorship, which she names Torres Home Design. During the firstmonthofoperations,July2014,thefollowingtransactionsoccurred:

a. Torresinvests$80,000ofpersonalfundstostartthebusiness.b. Thebusinesspurchases,onaccount,officesuppliescosting$2,000.c. TorresHomeDesignpayscashof$56,000toacquireaparcelofland.Thebusi-

nessintendstousethelandasafuturebuildingsiteforitsbusinessoffice.d. Thebusinessprovidesservicesforclientsandreceivescashof$10,000.e. Thebusinesspays$1,500ontheaccountpayablecreatedinTransaction(b).f. Torrespays$6,500ofpersonalfundsforavacationforherfamily.g. Thebusinesspayscashexpensesforofficerent,$2,500,andutilities,$500.h. Thebusinessreturnstothesupplierofficesuppliesthatcost$300.Thewrong

supplieswereshipped.i. Torreswithdraws$3,000cashforpersonaluse.

Required

1. AnalyzetheprecedingtransactionsintermsoftheireffectsontheaccountingequationofTorresHomeDesign.UseExhibit1–9onpage22asaguidebutshowbalancesonlyafterthelasttransaction.

2. Preparetheincomestatement,statementofowner’sequity,andbalancesheetofTorresHomeDesignafterrecordingthetransactions.UseExhibit1–10onpage25asaguide.

SOLUTION1. PanelA:DetailsofTransactions

a.Torresinvested$80,000cashtostartthebusiness.b.Purchased$2,000inofficesuppliesonaccount.c. Paid$56,000toacquirelandasafuturebuildingsite.d.Earnedservicerevenueandreceivedcashof$10,000.e.Paid$1,500onaccount.f. Paidforapersonalvacation,whichisnotatransactionofthebusiness.g.Paidcashexpensesforrent,$2,500,andutilities,$500.h.Returnedofficesuppliesthatcost$300.i. Withdrew$3,000cashforpersonaluse.

Name: Torres Home DesignIndustry: Home design consultingFiscal Period: Month of July 2014

TheSummary Problem forYourReviewisanextensive,challengingreviewprob-lemthatpullstogetherthechapterconcepts.

M01_HORN0096_01_SE_C01.indd 27 10/4/12 1:12 PM

28 Part 1 TheBasicStructureofAccounting

Assets

Office Cash 1 Supplies 1 Land

(a) +80,000(b) +2,000(c) - 56,000 + 56,000(d) + 10,000(e) - 1,500(f) Notabusinesstransaction(g) - 2,500

- 500(h) - 300(i) - 3,000Bal. 26,500 1,700 56,000

84,200

Liabilities

Owner’s Equity

Type of Owner’s Equity Transaction

Accounts Payable

Samantha Torres, Capital

+80,000 Owner investment+2,000

+10,000 Service revenue−1,500

- 2,500 Rent expense- 500 Utilities expense

− 300- 3,000 Owner withdrawal

200 84,000

84,200

Panel B: Analysis of Transactions

For each transac-tion, make sure the accounting equa-tion Assets = Liabilities + Owner’s Equity balances before going on to the next transaction.

2. Financial Statements of Torres Home Design

TORRES HOME DESIGN

Income Statement

For the Month Ended July 31, 2014

Revenue:

Servicerevenue $10,000

Expenses:

Rentexpense $2,500

Utilitiesexpense 500

Totalexpenses 3,000

NetIncome $ 7,000

TORRES HOME DESIGN

Statement of Owner’s Equity

For the Month Ended July 31, 2014

SamanthaTorres,capital,July1,2014 $ 0

Add:Investmentbyowner 80,000

NetincomeforJuly 7,000

87,000

Less:Withdrawalbyowner 3,000

SamanthaTorres,capital,July31,2014 $84,000

=

1

M01_HORN0096_01_SE_C01.indd 28 10/4/12 1:12 PM

Chapter 1 AccountingandtheBusinessEnvironment 29

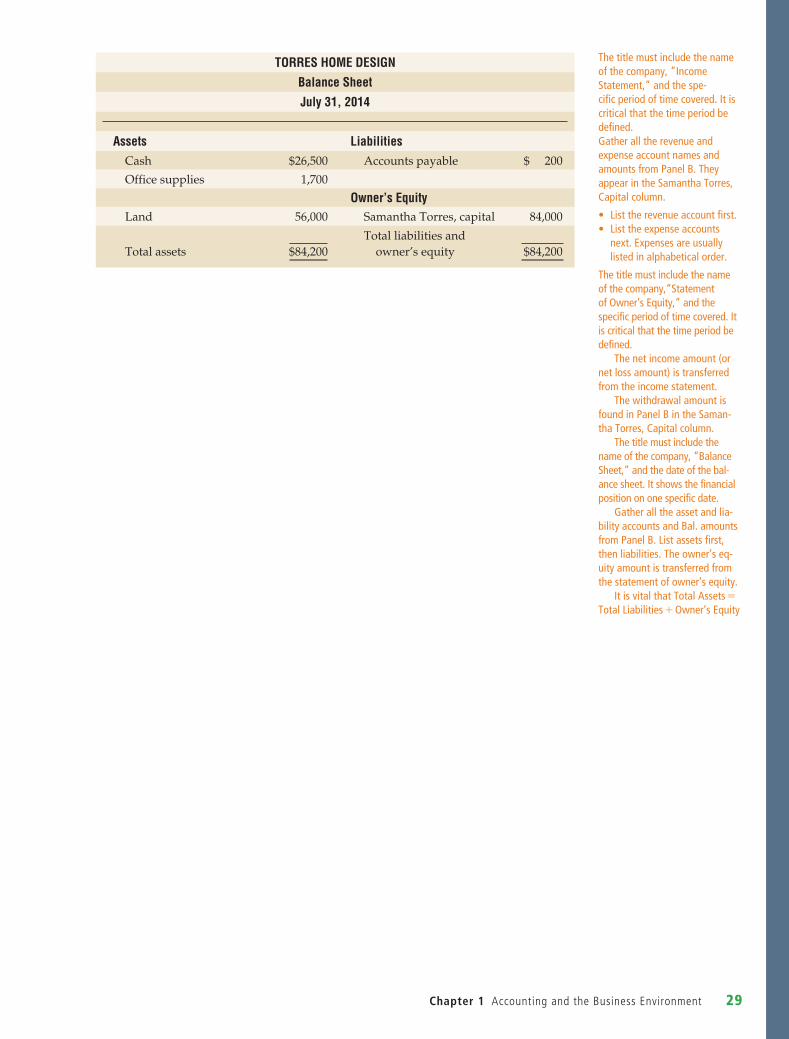

TORRES HOME DESIGN

Balance Sheet

July 31, 2014

Assets LiabilitiesCash $26,500 Accountspayable $200

Officesupplies 1,700

Owner’s EquityLand 56,000 SamanthaTorres,capital 84,000

Totalassets

$84,200

Totalliabilitiesand owner’sequity

$84,200

The title must include the name of the company, “Income Statement,” and the spe-cific period of time covered. It is critical that the time period be defined.Gather all the revenue and expense account names and amounts from Panel B. They appear in the Samantha Torres, Capital column.

• List the revenue account first.• List the expense accounts

next. Expenses are usually listed in alphabetical order.

The title must include the name of the company,“Statement of Owner’s Equity,” and the specific period of time covered. It is critical that the time period be defined.

The net income amount (or net loss amount) is transferred from the income statement.

The withdrawal amount is found in Panel B in the Saman-tha Torres, Capital column.

The title must include the name of the company, “Balance Sheet,” and the date of the bal-ance sheet. It shows the financial position on one specific date.

Gather all the asset and lia-bility accounts and Bal. amounts from Panel B. List assets first, then liabilities. The owner’s eq-uity amount is transferred from the statement of owner’s equity.

It is vital that Total Assets = Total Liabilities + Owner’s Equity

M01_HORN0096_01_SE_C01.indd 29 10/4/12 1:12 PM

30 Part 1 TheBasicStructureofAccounting

Learning Objective 1: Define accounting, and describe the users of accounting information.

Define accounting, and describe the users of accounting information

• Accountingisaninformationsystemformeasuring,processing,andcommunicatingfinancialinformation.

• Asthe“languageofbusiness,”accountinghelpsawiderangeofusersmakebusinessdecisions.

• Examplesofusersincludeindividualinvestors,businesses,governmentagencies,andlenders.

MyAccountingLab Video:

Pg 5

Learning Objective 2: Explain why ethics and rules of conduct are crucial in accounting and business.

Explain why ethics and rules of conduct are crucial in accounting and business

• Ethicalconsiderationsaffectallareasofaccountingandbusiness.• Usersneedrelevantandreliableinformationaboutcompaniestomakedecisions.• TheprofessionalaccountinggroupsinCanadahavecodesofethicsandrulesofconductto

assuresocietythataccountantsbehaveethically

MyAccountingLab Video:

Pg 7

Learning Objective 3: Describe and discuss the forms of business organizations

Describe and discuss the forms of business organizations

• Thethreebasicformsofbusinessorganizationsarethe• proprietorship• partnership(alimited-liabilitypartnership,orLLP,isaspecialformofpartnership),and• corporation.

• AsummaryandcomparisonofthethreeformsaregiveninExhibit1–5onpage11.

MyAccountingLab Video:

Pg 9

Learning Objective 4: Explain the development of accounting standards, and describe the concepts and principles

Explain the development of accounting standards, and describe the concepts and principles

• Accountingconceptsguideaccountantsintheirwork.• Accountingconceptsthatprovidethebasisforaccountingstandardsforprivateenterprises