02 - banco bice

TRANSCRIPT

Carta del PresidenteLetter from the Chairman

Nuestro DirectorioBoard of Directors

Entorno Económico y FinancieroEconomic and Financial Context

Banco BICE en CifrasBanco BICE in Figures

Informe del Gerente GeneralCEO’s Report

Equipo EjecutivoManagement Team

FilialesSubsidiaries

División CorporacionesCorporate Banking Division

División Empresas y SucursalesSME Banking Division

División PersonasRetail Banking Division

División BICE InversionesAsset and Wealth Management Division

División Finanzas e InternacionalTreasury Division

División Operaciones y TecnologíaOperations and Technology Division

División RiesgosRisk Division

División Transformación DigitalDigital Transformation Division

Marketing y Experiencia de ClientesMarketing and Costumer Experience

Administración, Planificacióny Control de GestiónAdministration, Planning and Control

Fiscalía y ContraloríaLegal Department and Comptroller’s Office

Personas y Desarrollo HumanoHuman Resources

Informe de los Auditores IndependientesIndependent Auditors Report

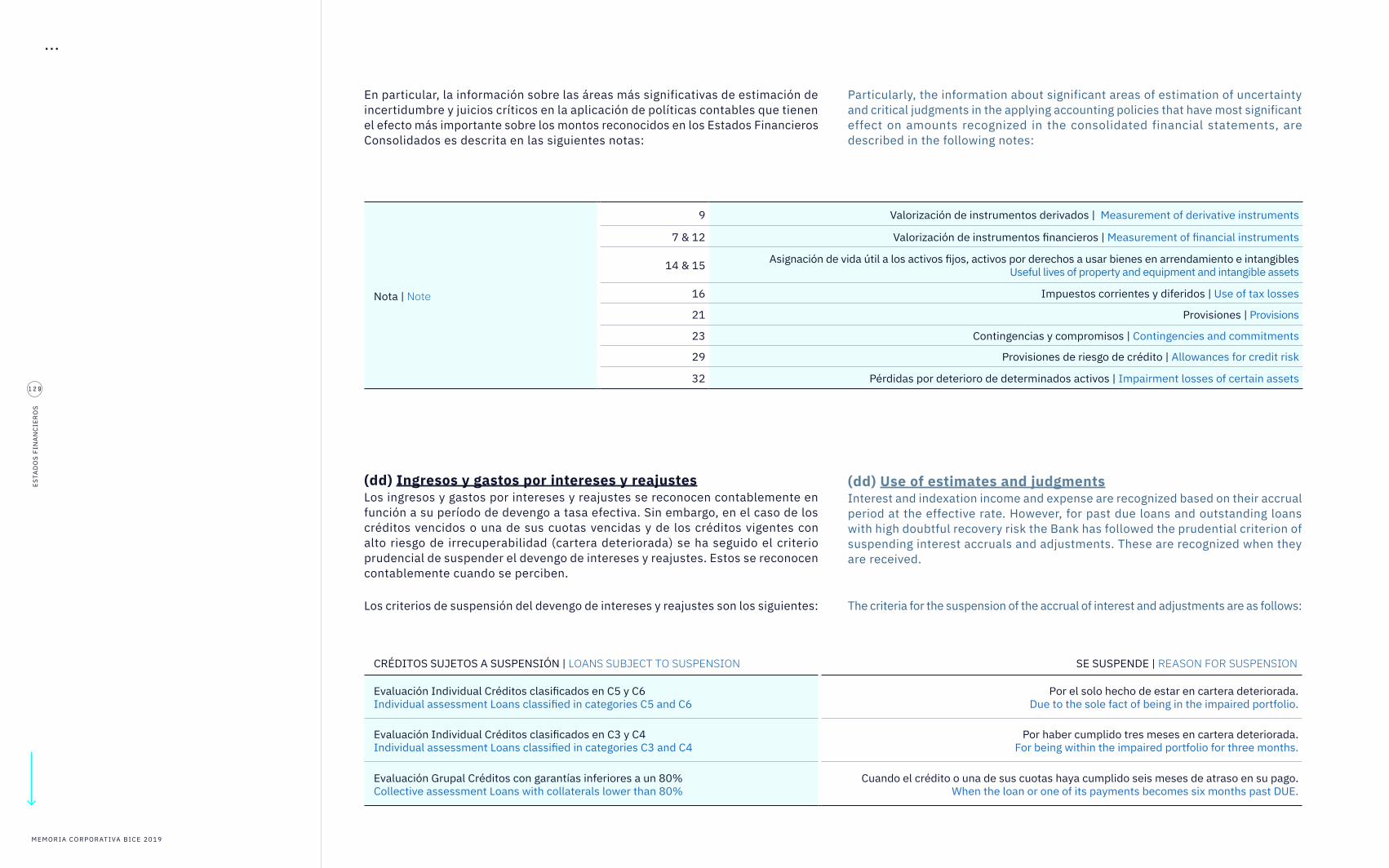

Nota a los Estados Financieros ConsolidadosNotes to the Consolidated Financial Statements

04

07

08

16

18

26

27

29

35

40

46

54

58

62

68

70

78

80

81

94

106

01

EQU

IPO

CO

RP

OR

ATIV

OSE

NIO

R M

ANAG

EMEN

T

02

GES

TIÓ

N C

OM

ERC

IAL

COM

MER

CIAL

PER

FORM

ANCE

03

AP

OYO

A L

A G

ESTI

ÓN

CO

MER

CIA

LSU

PPO

RT F

OR

AREA

S

04

ESTA

DO

S FI

NA

NC

IER

OS

FIN

ANCI

AL R

ESU

LTS

01

C O N L O Q U E T E I M P O R TA

EQ

UIP

O C

OR

PO

RAT

IVO

M E M O R I A CO R P O R ATI VA B I C E 2 0 1 9

4

EQU

IPO

CO

RP

OR

ATIV

O

M E M O R I A CO R P O R ATI VA B I C E 2 0 1 9

4

EQU

IPO

CO

RP

OR

ATIV

O

“Quiero agradecer a nuestros clientes su preferencia y lealtad, y a todas las personas que trabajan en la institución por su compromiso y esfuerzos desplegados en el cumplimiento de sus responsabilidades.”

“I would like to take this opportunity to thank our clients for their preference and loyalty and all our personnel for their commitment and work in fulfilling their responsibilities.”

BERNARDO MATTE L.PRESIDENTE | CHAIRMAN OF THE BOARD

M E M O R I A CO R P O R ATI VA B I C E 2 0 1 9

5

EQU

IPO

CO

RP

OR

ATIV

O

CARTA DEL PRESIDENTELETTER FROM THE CHAIRMAN

Señores Accionistas, Es muy grato dirigirme a ustedes para presentarles la memoria anual y los estados financieros consolidados de Banco BICE y sus sociedades filiales, correspondientes al ejercicio 2019. Los invito a revisar los resultados obtenidos, junto a algunos hechos relevantes del entorno económico y financiero que prevalecieron durante el año.

En 2019, Banco BICE desarrolló sus negocios en un débil escenario económico caracterizado por el bajo dinamismo hasta septiembre y que luego estuvo muy influenciado por la crisis política y social del último trimestre del año. El crecimiento de la actividad nacional fue inferior a lo proyectado a inicio de año y respecto a 2018, con una expansión levemente por sobre 1%. El comercio internacional chileno se debilitó durante 2019, con caídas en los niveles de exportaciones e importaciones de -10% y -16%, respectivamente. El precio promedio del cobre se situó en US$2,7/lb y el petróleo WTI se situó en los US$57 el barril a niveles

promedio. Por su parte, la tasa de desempleo experimentó un alza moderada a nivel nacional, cerrando en 7,0% en el trimestre móvil octubre–diciembre. En tanto, el tipo de cambio observado experimentó un alza de 7% respecto del cierre de diciembre de 2018, cerrando en $744,62. Asimismo, la inflación anual se ubicó en el centro del rango meta establecido por el Banco Central, cerrando en 3,0%.

En materia monetaria, el Banco Central de Chile disminuyó la tasa de instancia en varias oportunidades, acumulando una baja de un punto porcentual, cerrando el año en 1,75%.

Con respecto al negocio de créditos, las colocaciones de la banca registraron un crecimiento real de 7%. En su resultado anual, el sistema financiero incrementó su utilidad neta en 7,2% real respecto a 2018, y obtuvo una rentabilidad sobre patrimonio de 12,1%. Por otra parte, los índices de riesgo aumentaron, el sistema bancario cerró el ejercicio 2019 con un incremento de 12,5% en las provisiones constituidas, lo que significó un gasto en provisiones 36% superior a 2018.

Dear Shareholders,I am very pleased to submit to you the 2019 Annual Report and Consolidated Financial Statements of Banco BICE and its subsidiaries. In this message, I would like to review our results, along with some key aspects of the economic and financial context that prevailed during the year.

In 2019, the Chilean economy performed weakly. During the first nine months, it showed little dynamism and then, in the last quarter, was heavily affected by the country’s political and social crisis. Growth, at slightly above 1%, was slower than expected at the start of the year and down on 2018. Chile’s international trade weakened in 2019, with exports and imports down by 10% and 16%, respectively. Copper averaged US$2.7/lb and the WTI oil price US$57/barrel. The national unemployment rate showed a moderate increase, averaging 7.0% in the last quarter, while the market peso/dollar exchange rate showed an increase of 7% on end-2018, closing at 744.62 pesos, and annual inflation, at 3.0%, was in the middle of the Central Bank’s target range.

Over the course of the year, the Central Bank cut its monetary policy interest rate on several occasions, reducing it by a total of one point to a year-end rate of 1.75%.

Lending by the banking system grew by 7% in real terms in 2019. The financial system’s net profits showed a real increase of 7.2% on the previous year, giving a return on equity of 12.1%. Risk indicators increased and the banking system closed the year with a 12.5% increase in provisions, implying a 36% increase in expenditure on provisions as compared to 2018.

In this context, Banco BICE reported a net profit of 69,144 million pesos and a return on equity of 11.5%, with a nominal 13% increase in loans and accounts receivable from clients. As of the end of the year, it had a market share of around 3.2%.

Banco BICE’s index of risk over total lending increased slightly to 1.29%, a figure well below the average for the financial system, and total provisions were

11,5%Rentabilidad sobre el patrimonio de Banco BICE.

Banco BICE’s return on equity.

M E M O R I A CO R P O R ATI VA B I C E 2 0 1 9

6

EQU

IPO

CO

RP

OR

ATIV

O

En este contexto, Banco BICE tuvo una utilidad neta en el ejercicio 2019 de $69.144 millones y una rentabilidad sobre patrimonio de 11,5%, con un crecimiento nominal de los créditos y cuentas por cobrar a clientes de 13%, cerrando el año con una participación de mercado en torno al 3,2%.

Asimismo, el índice de riesgo sobre el total de colocaciones de Banco BICE aumentó levemente a 1,29%, cifra muy inferior al promedio del sistema financiero, y mantiene provisiones totales equivalentes al 1,95% del total de préstamos, finalizando el año con una razón de cobertura de provisiones sobre la cartera morosa de más de 90 días de 6,08 veces, situándose como la institución con mayor índice de cobertura del sistema (cuya cobertura promedio es 1,43 veces).

En la gestión anual del Banco y sus empresas filiales, cabe destacar el crecimiento de la base de clientes corporativos y del mercado de personas, el aporte a resultados de las sociedades filiales y finalmente, la favorable calificación obtenida por el Banco de parte de sus propios clientes, distinguiéndolo una vez más, entre los

equivalent to 1.95% of total loans. As of the end of the year, this gave a coverage ratio of loans past due for more than 90 days that, at 6.08 times, was the highest in the industry (where it averaged 1.43 times).

Key features of the Bank and subsidiaries’ performance in 2019 included substantial growth of its corporate and individual client base. Additionally, we also saw a significant increase in the contributions of the Bank’s subsidiaries and we were able to maintain our favorable rating in terms of customer service, ranking as one of the countries’ best banks in this respect.

I would like to comment on the coordinated cultural work being carried out within the Bank and its subsidiaries in terms of “transforming” the way some things

Banco BICE tuvo una utilidad neta en el ejercicio 2019 de $69.144 millones, con un crecimiento nominal de los créditos y cuentas por cobrar a clientes de 13%.

Banco BICE reported a net profit of 69,144 million pesos and a return on equity of 11.5%, with a nominal 13% increase in loans and accounts receivable from clients.

BERNARDO MATTE LARRAÍN Presidente / Chairman of the Board

mejores en calidad de servicio entre todos los bancos que operan en el país.

Quisiera comentar el coordinado trabajo cultural que se está llevando al interior del Banco y sus filiales, en cuanto a “transformar” la forma en que se han hecho históricamente algunas cosas. Me refiero a un nuevo enfoque de organización de equipos, a nuevos cuestionamientos y uso de datos, a nuevas formas de desarrollar productos y de combinar distintas tecnologías, todo al servicio de la innovación, para generar una mejor propuesta de valor para nuestros clientes, en un marco de seguridad y responsabilidad como ha sido siempre característico del BICE.

Al concluir, y a nombre del Directorio de Banco BICE que presido, quiero agradecer a nuestros clientes su preferencia y lealtad, y a todas las personas que trabajan en la institución por su compromiso y esfuerzos desplegados en el cumplimiento de sus responsabilidades.

Atentamente,

have historically been done. I am referring to a new approach to the organization of teams, new questionings and use of data and new ways of developing products and of combining different technologies, all at the service of innovation, in order to generate a better value proposition for our clients, in a framework of the security and responsibility that have always characterized BICE.

Finally, on behalf of the Board of Directors of Banco BICE which I chair, I would like to take this opportunity to thank our clients for their preference and loyalty and all our personnel for their commitment and work in fulfilling their responsibilities.

Yours sincerely,

M E M O R I A CO R P O R ATI VA B I C E 2 0 1 9

7

EQU

IPO

CO

RP

OR

ATIV

O

7

M E M O R I A CO R P O R ATI VA B I C E 2 0 1 9

NUESTRO DIRECTORIOBOARD OF DIRECTORS

01 02

05

08

04

07

03

06

09

01

02

03

04

05

06

07

08

09

BERNARDO MATTE L.PRESIDENTE | CHAIRMAN OF THE BOARD

JUAN EDUARDO CORREA G.VICEPRESIDENTE | VICE CHAIRMAN

KATHLEEN C. BARCLAYDIRECTORA | DIRECTOR

VICENTE MONGE A.DIRECTOR | DIRECTOR

JUAN CARLOS EYZAGUIRRE E.DIRECTOR | DIRECTOR

BERNARDO FONTAINE T.DIRECTOR | DIRECTOR

JOSÉ MIGUEL IRARRÁZAVAL E.DIRECTOR | DIRECTOR

RENÉ LEHUEDÉ F.DIRECTOR | DIRECTOR

RODRIGO DONOSO M.DIRECTOR | DIRECTOR

M E M O R I A CO R P O R ATI VA B I C E 2 0 1 9

8

EQU

IPO

CO

RP

OR

ATIV

O

ENTORNO ECONÓMICO Y FINANCIEROECONOMIC AND FINANCIAL ENVIRONMENT

El panorama económico global de 2019 inició el año con cierto pesimismo, anclado en el peligro de que un recrudecimiento de las tensiones comerciales entre Estados Unidos y China fuera más allá de lo contemplado en los pronósticos. A ello se añadía las negociaciones de salida del Reino Unido de la Unión Europea.

Por el lado del crecimiento global, en marzo la OCDE señaló que estimaba expansiones del crecimiento mundial de 3,3% y 3,4% para el 2019 y 2020, cifras inferiores al promedio de 3,7% de los dos años previos. El Banco Central estimaba que socios comerciales de Chile también se expandirían cerca de estos valores, con una expansión de China en torno al 6% en 2019 y 2020. Actualmente, el FMI estima que el crecimiento mundial fue de solo 2,9% en 2019.

Ya transcurrido gran parte del 2019 se hizo evidente que los efectos de la guerra comercial entre Estados Unidos y China estaban teniendo un efecto más global de lo esperado inicialmente, como lo refleja la debilidad del comercio mundial y de la actividad manufacturera. Todo ello afectó de manera importante las expectativas

y las decisiones de inversión en diversos países, toda vez que el recrudecimiento del conflicto está incrementando la desconfianza por la imposibilidad de predecir los cambios de tono, anuncios y contramedidas.

La incertidumbre en torno a las políticas comerciales, las tensiones geopolíticas y la tensión idiosincrásica en las principales economías de mercados emergentes siguieron imponiendo lastres a la actividad económica mundial, en especial la manufactura y el comercio. La agudización del descontento social en varios países, no solo en Chile, planteó nuevos desafíos, al igual que lo hicieron desastres de índole meteorológica: desde huracanes en el Caribe, hasta sequía e incendios forestales en Australia, inundaciones en África oriental y sequía en el sur de África.

A pesar de la continua creación de empleo (en ciertos casos en un entorno en que las tasas de desempleo ya estaban en mínimos históricos), la inflación subyacente de los precios al consumidor siguió siendo leve en las economías avanzadas. Se suavizó aún más en la mayoría de las economías de mercados emergentes en

At the beginning of 2019, there was a degree of pessimism about the global economic outlook, due mainly to the risk that a resurgence of trade tensions between the United States and China could have an impact beyond that already envisaged in forecasts. There was, in addition, concern about the United Kingdom’s negotiations to exit the European Union.

In March, the OECD forecast global growth of 3.3% in 2019 and 3.4% in 2020, down from an average of 3.7% in the previous two years. The Chilean Central Bank, in turn, estimated that the country’s trading partners would expand in line with this forecast, with China growing by around 6% in 2019 and 2020. Currently, the IMF estimates that global growth in 2019 reached only 2.9%.

Later in the year, it became clear that the trade war between the United States and China was having a more global effect than initially anticipated, negatively affecting world trade and manufacturing activity. All this had a significant impact

on expectations and investment decisions in various countries as the resurgence of the conflict undermined confidence, given the impossibility of predicting changes in tone, announcements and countermeasures.

Uncertainty about trade policies, geopolitical tensions and idiosyncratic tensions in the main emerging market economies continued to have a negative effect on global economic activity, particularly manufacturing and trade. The intensification of social discontent in a number of countries, not only Chile, posed new challenges. This was compounded by climate-related disasters, ranging from hurricanes in the Caribbean to drought and forest fires in Australia, floods in eastern Africa and drought in southern Africa.

Despite ongoing job creation (in some cases with unemployment rates already at historical lows), core consumer price inflation remained low in the advanced economies and, in most emerging economies, was further contained by a more

2,9%Crecimiento mundial en 2019, estimado por el FMI.

Estimated world growth in 2019, according to the IMF

M E M O R I A CO R P O R ATI VA B I C E 2 0 1 9

9

EQU

IPO

CO

RP

OR

ATIV

O

medio de una actividad más moderada. El debilitamiento de la demanda redujo los precios de los metales y de la energía, lo cual puso freno al nivel general de inflación. El FMI estima que en las economías avanzadas, la inflación pase de un 2,0% en 2018 a 1,5% en 2019, y en las economías de mercados emergentes y en desarrollo, de 4,8% a 4,7%.

En medio de registros inflacionarios mayormente contenidos, la política monetaria global ha seguido tornándose más expansiva. En el mundo desarrollado destacan las acciones en Estados Unidos y la Eurozona. En octubre, la Fed efectuó su último recorte de la tasa rectora, el tercero del año. Aunque el mercado continúa apostando por rebajas adicionales, las perspectivas se han moderado, en línea con datos más favorables y una comunicación por parte de la autoridad monetaria de que los niveles actuales hasta ahora serían apropiados. El Banco Central Europeo implementó una serie de estímulos, como la reducción de su tasa de interés y la reanudación del programa de compra de activos. En el bloque emergente, la política monetaria en China se ha vuelto más laxa en el margen, incluyendo

recortes a la tasa de corto plazo y la de facilidad de préstamos de mediano plazo. En América Latina, varias economías igualmente bajaron sus tasas de política monetaria, como Brasil, México, Perú y Chile.

Respecto a las materias primas, los precios del petróleo han sido volátiles. El crudo WTI registró un promedio de USD 57 en el año frente a USD 65 registrado el año anterior, resultado sin embargo, muy semejante al que estimara el Banco Central al cierre de 2018. El cobre por su parte registró un promedio de USD 2,7 la libra frente a USD 2,3 de 2018 y USD 2,85 que estimara la autoridad monetaria a fines del año anterior.

La Economía ChilenaTras cerrar el 2018 con un crecimiento económico del 4%, las expectativas para el 2019 eran altas, aunque no estaban exentas de cierta incertidumbre. La cifra significó la mayor expansión del país en los últimos cinco años, pero estaba

moderate level of activity. The general level of inflation was, moreover, capped by the impact of weaker demand on the prices of metals and energy. The IMF estimates that, in the advanced economies, inflation dropped from 2.0% in 2018 to 1.5% in 2019 and, in emerging market and developing economies, from 4.8% to 4.7%.

In this context of mostly contained inflation, global monetary policy continued to become more expansive, as seen in the United States and the Eurozone. The US Federal Reserve’s latest cut in its policy rate in October was the third of the year. Although the market continues to expect further reductions, the outlook has moderated in line with more favorable data and the Fed’s indication that, for time being, the policy rate appears to be at an appropriate level. The European Central Bank implemented a series of stimulus measures, such as the reduction of its interest rate and the resumption of its asset purchase program. In the case of emerging market economies, China has relaxed its monetary policy in the margin,

including cuts in the short-term rate and that on its medium-term lending facility. In Latin America, a number of countries, including Brazil, Mexico, Peru and Chile, also lowered their monetary policy rates.

In the case of raw materials, oil prices have been volatile. The annual average WTI crude price dropped from US$65 in 2018 to US$57 in 2019, a level very similar to the estimated by the Chilean Central Bank at the end of 2018. Copper averaged US$2.7 per pound as compared to US$2.3 in 2018 and the US$2.85 estimated by the Central Bank at the end of 2018.

The Chilean EconomyIn the wake of the Chilean economy’s 4% growth in 2018, expectations for 2019 were high, albeit not immune to uncertainty. Growth in 2018 was the highest in five years, but there was uncertainty internationally, due to the trade war between

M E M O R I A CO R P O R ATI VA B I C E 2 0 1 9

10

EQU

IPO

CO

RP

OR

ATIV

O

presente la incertidumbre a nivel internacional, producto de la guerra comercial entre Estados Unidos y China, y la desaceleración que estaba anotando la actividad local hacían la tarea compleja. Así y todo, el gobierno inició el 2019, apostando por un crecimiento de 3,8%, mientras el Banco Central lo hacía entre 3,25% y 4,25%. Actualmente, el Banco Central prevé que la economía chilena anotará, el 2019, su peor crecimiento desde la crisis subprime, estimándose una variación en torno al 1,0%, con un crecimiento de la inversión bruta de capital fijo de 2,5% frente al 4,7% que se expandiera el 2018.

Durante todo el 2019, se fue ajustando a la baja el crecimiento. El primer semestre terminó anotando una expansión de 1,75% y Hacienda justificó este débil desempeño como la “tormenta perfecta”, tanto a nivel local como internacional. Aún así seguía optimista, apuntando a un crecimiento del 3,2% para fin de año. Luego, a inicios de octubre y apegándose a las proyecciones del mercado, Hacienda fijó la proyección de crecimiento entre 2,4% y 2,9%.

En el IPoM del primer trimestre 2019, el Banco Central se refirió a que la principal diferencia respecto del escenario base de diciembre se había dado en la inflación local (medida por el IPC de referencia calculado por el INE) la cual se ubicaba significativamente por debajo de lo previsto. El menor registro de inflación era coherente con un traspaso de la depreciación del peso menor a lo esperado, así como con la presencia de factores de oferta que sugieren que las holguras son mayores que lo estimado, destaca el efecto de la inmigración en la fuerza laboral. Con ello la autoridad monetaria justificó un retiro del estímulo monetario más pausado que lo anteriormente comunicado por el Consejo, reconociendo implícitamente que su estimación de crecimiento había sido más optimista que lo que se estaba dando en la realidad. Ello justificaba el aumento que hiciera a fines de enero de la TPM de 2,75% a 3,0%, que finalmente debió revertir en junio al bajarla 50 puntos base y otros 25 puntos en septiembre, a parte de los 25 puntos que decidiera a fines de octubre, cerrando el año en 1,75%.

the United States and China, and the Chilean economy was slowing, making the situation more complex. Nonetheless, at the beginning of the year, the government forecast 3.8% growth in 2019 in line with the Central Bank’s forecast of between 3.25% and 4.25%. Currently, the Central Bank estimates that growth was, in fact, around 1%, its lowest level since the subprime crisis, while gross fixed capital formation expanded by only 2.5%, down from 4.7% 2018.

Throughout 2019, growth forecasts were adjusted downwards. In the first half, activity grew by 1.75%, a weak performance that the Finance Ministry justified as the result of a “perfect storm”, both locally and internationally. It nonetheless remained optimistic, forecasting growth of 3.2% over the whole year. At the beginning of October, however, it reduced its forecast to between 2.4% and 2.9%, bringing it into line with market forecasts.

In its Quarterly Monetary Report (IPoM) for the first quarter of 2019, the Central Bank indicated that the main difference with respect to its December baseline scenario was local inflation (measured using the consumer price index, calculated by the National Institute of Statistics), which was significantly lower than expected. This was consistent with a lower than expected pass-through of the peso’s depreciation to prices as well as the presence of supply factors suggesting that the economy had more slack than estimated, due partly to the impact of immigration on the labor force. In light of this, the Central Bank opted for a more gradual withdrawal of monetary stimulus than previously indicated by its Board, implicitly recognizing that its growth forecast had proved optimistic. At the end of January, it increased the monetary policy rate from 2.75% to 3.0% but, in June, announced a cut of 50 basis points. This was followed by a further 50-point cut in September and a 25-point cut at the end of October, taking the rate to a year-end 1.75%.

El gobierno inició el 2019, apostando por un crecimiento de 3,8%, mientras el Banco Central lo hacía entre 3,25% y 4,25%. Actualmente, el Banco Central prevé que la economía chilena anotará, el 2019, su peor crecimiento desde la crisis subprime.

At the beginning of the year, the government forecast 3.8% growth in 2019 in line with the Central Bank’s forecast of between 3.25% and 4.25%. Currently, the Central Bank estimates that growth was, in fact, around 1%, its lowest level since the subprime crisis.

M E M O R I A CO R P O R ATI VA B I C E 2 0 1 9

11

EQU

IPO

CO

RP

OR

ATIV

O

M E M O R I A CO R P O R ATI VA B I C E 2 0 1 9

Este escenario macroeconómico ya complicado sufrió un cambio abrupto a partir de mediados de octubre. La crisis que se inició el 18 de octubre se ha caracterizado por demandas sociales que han llevado a la discusión de cambios institucionales relevantes —como una nueva constitución— y mayores presiones en el gasto fiscal. Este proceso fue acompañado de episodios de violencia significativos y prolongados, los que provocaron importantes disrupciones en el sistema productivo, incidiendo fuertemente en una menor actividad y debilitando el empleo. Ello llevó a un aumento relevante de la incertidumbre y un deterioro de las confianzas. Los mercados financieros se vieron tensionados por fuertes movimientos en los precios, que en algunos casos iban más allá de lo justificable por la mayor percepción de riesgo país, influenciada en gran parte por los rescates de los fondos mutuos de renta fija de largo plazo. Ello llevó a que a que el Banco Central tuviera que adoptar diversas medidas a mediados de noviembre para mejorar la liquidez en pesos y en dólares, además de decidir intervenir el mercado cambiario para mitigar la alta volatilidad del tipo de cambio.

This already complicated macroeconomic situation underwent an abrupt change as from mid-October. The social demands expressed in the crisis that erupted on October 18 have prompted debate about important institutional changes - such as a new constitution - and put pressure on fiscal spending. This process was accompanied by significant and prolonged episodes of violence, which caused important production disruptions, with a strong negative impact on activity that weakened the labor market. This led to a significant increase in uncertainty, undermining confidence. Financial markets were stressed by strong price movements which, in some cases, went beyond what could be justified by a heightened perception of country risk and reflected withdrawals from long-term fixed-income mutual funds. In mid-November, the Central Bank had to adopt a number of measures to support liquidity in pesos and dollars and decided to intervene the foreign exchange market to mitigate exchange rate volatility.

Finalmente, la economía chilena cerró el año con una inflación de 3,0%, justo en la media del rango meta del Baco Central, pero con un alza del tipo de cambio de 8,3%, tomando como base los precios de cierre de cada año.

Perspectivas para 2020Las perspectivas para la economía mundial según el FMI se proyectan optimistas a pesar de una leve corrección a la baja respecto a su informe de octubre, ya que se estima pasar de un crecimiento de 2,9% en 2019 a 3,3% en 2020 y a 3,4% en 2021. La revisión a la baja se debe, principalmente, a resultados inesperados negativos de la actividad económica en unas pocas economías de mercados emergentes, en particular India, que dieron lugar a una revaluación de las perspectivas de crecimiento correspondientes a los próximos dos años. En unos pocos casos, esta revaluación también tiene en cuenta los efectos del mayor malestar social. El impacto que indudablemente tendrá el coronavirus, agrega un mayor sesgo a la baja.

The Chilean economy closed the year with an inflation rate of 3.0%, exactly in the middle of the Central Bank’s target range, but an exchange rate that was up by 8.3% on end-2018.

Outlook for 2020The IMF is optimistic about the outlook for the world economy, despite a slight downward correction with respect to its October report. It anticipates that world growth will reach 3.3% in 2020 and 3.4% in 2021, up from 2.9% in 2019. Its downward correction mainly reflected unexpected negative results for economic activity in a few emerging market economies, particularly India, which led it to reassess the prospects for growth over the next two years. In a few cases, this re-evaluation also took into account the impact of increased social discontent. The impact that coronavirus will have implies a greater downward bias.

Las perspectivas para la economía mundial según el FMI se proyectan optimistas, ya que se estima pasar de un crecimiento de 2,9% en 2019 a 3,3% en 2020 y a 3,4% en 2021.

The IMF is optimistic about the outlook for the world economy, despite a slight downward correction with respect to its October report. It anticipates that world growth will reach 3.3% in 2020 and 3.4% in 2021, up from 2.9% in 2019.

M E M O R I A CO R P O R ATI VA B I C E 2 0 1 9

12

EQU

IPO

CO

RP

OR

ATIV

O

Por el lado positivo, la actitud de los mercados se ha visto estimulada por indicios de que la actividad manufacturera y el comercio internacional están llegando a un punto de inflexión, por una reorientación general hacia una política monetaria acomodaticia, por noticias intermitentemente favorables acerca de las negociaciones comerciales entre Estados Unidos y China, y por menores temores de que se produzca un brexit sin acuerdo.

La evolución, desde el cuarto trimestre de 2019, deja entrever un conjunto de riesgos para la actividad mundial menos sesgado a la baja. Estas incipientes señales de estabilización podrían persistir y a la larga reforzar el vínculo entre el gasto de consumo, que sigue siendo resiliente, y un repunte del gasto de las empresas.

No obstante, los riesgos a la baja siguen siendo importantes e incluyen la agudización de las tensiones geopolíticas, particularmente entre Estados Unidos e Irán, el aumento del malestar social, un nuevo empeoramiento de las relaciones entre Estados Unidos y sus socios comerciales, y una profundización de las

On the positive side, the markets have been encouraged by signs that manufacturing activity and international trade are reaching a point of inflection as well as by a general move towards an accommodating monetary policy, intermittently favorable news about the trade negotiations between the United States and China and reduced fears of a no-deal Brexit.

The international economy’s performance since the last quarter of 2019 suggests a reduction in downside risks. These emerging signs of stabilization could persist and, in the long run, strengthen the link between consumer spending, which remains resilient, and a recovery of corporate spending.

However, the downside risks remain significant and include an intensification of geopolitical tensions, particularly between the United States and Iran, an increase in social discontent, a new worsening of relations between the United States and its trading partners, and a deepening of economic frictions between other countries.

fricciones económicas entre otros países. Y recientemente se agrega los efectos aún no dimensionados de coronavirus en China.

Las señales incipientes de estabilización reforzaron la actitud en los mercados financieros, que ya se había visto afianzada por recortes de las tasas de los bancos centrales. Los mercados parecen haber interiorizado las perspectivas para la política monetaria de Estados Unidos y la decisión de la Reserva Federal de poner la orientación futura de esa política en «compás de espera», tras haber efectuado tres recortes en el segundo semestre de 2019.

El perfil de crecimiento también depende de que las economías de mercados emergentes, relativamente saludables, mantengan su desempeño sólido, aun cuando las economías avanzadas y China continúan desacelerándose gradualmente hacia sus tasas de crecimiento potencial. Se espera que los efectos de la sustancial distensión monetaria en las economías avanzadas y de mercados emergentes en 2019 continúen propagándose en la economía mundial en 2020.

A further risk has also emerged recently in the form of the not yet dimensioned effects of the coronavirus outbreak in China.

The incipient signs of stabilization reinforced the attitude of financial markets, which had already been strengthened by cuts in central bank rates. The markets appear to have internalized the outlook for monetary policy in the United States and the Federal Reserve’s “wait and see” stance, following its three rate cuts in the second half of 2019.

The growth profile also depends on the relatively healthy emerging market economies maintaining their solid performance, even though the advanced economies and China continue to decelerate gradually to their potential growth rates. The effects of the significant relaxation of monetary policy seen in advanced and emerging market economies in 2019 are expected to continue permeating the world economy in 2020. The IMF estimates that, without this monetary stimulus,

M E M O R I A CO R P O R ATI VA B I C E 2 0 1 9

13

EQU

IPO

CO

RP

OR

ATIV

O

Sin este estímulo monetario, el FMI estima que el crecimiento mundial para 2019 y la proyección para 2020 habrían sido 0,5 puntos porcentuales más bajas en cada año. Hasta antes de los efectos del coronavirus, se proyectaba que la recuperación mundial fuera acompañada de un repunte del crecimiento del comercio gracias a una recuperación de la demanda y la inversión internas en particular, así como a la disipación de ciertos lastres temporales en los sectores automotor y de tecnología. Actualmente esta situación podría ser diametralmente distinta.

En las economías avanzadas, se proyecta que el crecimiento se estabilice en 1,6% en 2020–21. En Estados Unidos, se prevé que el crecimiento se modere de 2,3% en 2019 a 2% en 2020 y luego a 1,7% en 2021. La moderación obedece a un retorno a una orientación fiscal neutral y el impulso cada vez menor derivado del relajamiento de las condiciones financieras.

global growth in 2019 and its forecast for 2020 would both have been a half-point lower. Before the coronavirus outbreak, it was expected that the recovery of the world economy would be accompanied by a rebound in the growth of trade, thanks to a recovery of domestic demand and investment and the disappearance of some temporary obstacles to the growth of the automobile and technology sectors. The situation could now be diametrically different.

Growth in the advanced economies is forecast to stabilize at 1.6% in 2020-21. In the United States, it is expected to moderate from 2.3% in 2019 to 2% in 2020 and 1.7% in 2021, reflecting a return to a neutral fiscal stance and the weakening impact of the relaxation of financial conditions.

En América Latina se proyecta que el crecimiento se recupere de un 0,1% estimado en 2019 a 1,6% en 2020 y 2,3% en 2021. En esta proyección se compensan menores perspectivas de crecimiento en México y Chile.

In Latin America, it is expected to recover from an estimated 0.1% in 2019 to 1.6% in 2020 and 2.3% in 2021. A drop in forecasts for Mexico and Chile is offset by an upward review of the forecast for Brazil in 2020.

Se proyecta que el crecimiento en la zona del euro repuntará de 1,2% en 2019 a 1,3% en 2020 y a 1,4 en 2021. Las mejoras proyectadas de la demanda externa facilitan el afianzamiento previsto del crecimiento. En el Reino Unido se espera que el crecimiento se estabilice en 1,4% en 2020 y que suba a 1,5% en 2021. El pronóstico de crecimiento supone una salida ordenada de la Unión Europea el 31 de enero, seguida de una transición gradual hacia una nueva relación económica.

En el grupo de las economías de mercados emergentes y en desarrollo, se prevé que el crecimiento aumente a 4,4% en 2020 y a 4,6% en 2021, desde un nivel estimado de 3,7% en 2019. En América Latina se proyecta que el crecimiento se recupere de un 0,1% estimado en 2019 a 1,6% en 2020 y 2,3% en 2021. En esta proyección se compensan menores perspectivas de crecimiento en México y Chile, con una revisión al alza del pronóstico de 2020 para Brasil, gracias a una mejora de la actitud tras la aprobación de la reforma de las pensiones y la disipación de las perturbaciones de la oferta en el sector minero.

Growth in the Eurozone is forecast to increase from 1.2% in 2019 to 1.3% in 2020 and 1.4% in 2021, thanks to an expected improvement in external demand. In the United Kingdom, growth is expected to stabilize at 1.4% in 2020 and rise to 1.5% in 2021, assuming an orderly exit from the European Union on January 31 and a gradual transition to a new economic relationship.

In the emerging market and developing economies, growth is forecast to reach 4.4% in 2020 and 4.6% in 2021, up from an estimated 3.7% in 2019. In Latin America, it is expected to recover from an estimated 0.1% in 2019 to 1.6% in 2020 and 2.3% in 2021. A drop in forecasts for Mexico and Chile is offset by an upward review of the forecast for Brazil in 2020, thanks to improved prospects for approval of this country’s proposed pension reform and the dissipation of supply-side disturbances in the mining sector.

M E M O R I A CO R P O R ATI VA B I C E 2 0 1 9

14

EQU

IPO

CO

RP

OR

ATIV

O

Economía ChilenaEl escenario macroeconómico sufrió un cambio abrupto a partir de mediados de octubre del año pasado. El actual escenario presenta un grado de incertidumbre mayor que el habitual, tanto por las dudas respecto de la duración de las disrupciones, como por la evolución de la situación política y los fundamentos de mediano plazo. La información disponible muestra un aumento relevante de la incertidumbre y un deterioro de las confianzas que estarían amplificando estos efectos. Un factor clave en la evolución futura de la economía será la confianza de hogares y empresas, y su relación con desempeño del mercado laboral, el consumo y la inversión. En lo referente al consumo, diversas encuestas muestran que la confianza de las personas se deterioró de manera significativa posterior al 18 de octubre.

El Banco Central espera que el mayor impulso fiscal que genero las demandas sociales, unido a la ya alta expansividad de la política monetaria, ayudará a

contener el deterioro de la economía, con lo que luego de una contracción de 2,5% estimada para el cuarto trimestre del 2019, crecerá entre 0,5 y 1,5% el 2020. Asimismo, la autoridad monetaria estima que esta desaceleración presionará a la baja a la inflación, lo que la permitirá mantener contenido los efectos más persistentes de la depreciación idiosincrática del peso. El mercado lo cree así y mantiene las expectativas para éste y el próximo año solo levemente por sobre el 3,0%, con una Tasa de Política Monetaria (TPM) que se mantendrá en los niveles actuales (1,00%).

Tanto la evolución del mercado laboral como de la inversión serán factores claves en las expectativas y evolución futura de la economía. De mantenerse la relación histórica entre la demanda de trabajo y la actividad, es probable que la tasa de desempleo pueda superar el 10% en 2020. En cuanto a la inversión, el Banco Central corrigió de forma relevante su proyección, estimando una caída del orden 4% en 2020. Ello responde a un descenso significativo de la inversión privada no minera. Esto es coherente con la mayor incertidumbre y el agudo

Outlook for the Chilean EconomyChile’s macroeconomic outlook changed abruptly in mid-October 2019 and is currently more than usually uncertain, due both to doubts about the duration of the disruptions and the evolution of the political situation and the economy’s medium-term fundamentals. The available information indicates that these factors are being amplified by a significant increase in uncertainty and a deterioration in confidence. The confidence of households and companies, and their relationship with the performance of the labor market, consumption and investment will be key for the economy’s evolution. In the case of consumption, different surveys show that people’s confidence has deteriorated significantly since October 18.

The Central Bank anticipates that higher fiscal spending in response to social demands, together with an already very expansive monetary policy, will help to

contain the deterioration of the economy. Following an estimated 2.5% contraction in the last quarter of 2019, it is forecasting growth of between 0.5% and 1.5% in 2020. It anticipates that this slowdown will exert downward pressure on inflation, helping to contain the more persistent effects of the peso’s idiosyncratic depreciation. The market shares this view and expects inflation to remain anchored at around 3% in 2020 and 2021, with the monetary policy interest rate held at its present level of 1.00%.

The evolution of the labor market and investment will be key for both expectations and the evolution of the economy. If the historical relationship between demand for labor and activity continues to hold, an unemployment rate of over 10% is likely in 2020. On investment, the Central Bank has made a significant correction to its forecasts and now anticipates a contraction of around 4% in 2020. This assumes

M E M O R I A CO R P O R ATI VA B I C E 2 0 1 9

15

EQU

IPO

CO

RP

OR

ATIV

O

deterioro de la confianza empresarial y los mayores costos que enfrentan las empresas en diversos ámbitos, entre ellos, el efecto de la depreciación del peso en el costo de la maquinaria importada y el deterioro de las condiciones financieras, incluyendo la caída de la bolsa y las alzas de tasas de interés y spreads corporativos, aun cuando estos dos últimos han tendido a la normalidad. Ayudarán en todo caso, parcialmente, los grandes proyectos de inversión mineros ya iniciados y el significativo aumento de la inversión pública.

El Banco Central proyecta que durante el 2020 la inflación alcanzará niveles promedio cercanos a 4% y de 3,6% respecto a diciembre 2019, respondiendo mayormente a la depreciación idiosincrática del peso, lo que lleva a que el grado de traspaso a la inflación sea mayor al promedio. Esto, toda vez que en estas circunstancias no se verifican factores amortiguadores, como el descenso

de los precios en dólares de productos importados que se produce ante una apreciación global del dólar. Aun así, el mercado está más optimista y está fijando la inflación cerca del 3%, en parte sustentada en una menor demanda por efecto de una débil actividad y mercado laboral, que frenara la presión alcista de la depreciación del peso.

Dentro de este panorama comienza a ser relevante la evolución de las finanzas públicas, que está siendo afectado por la desaceleración económica y el mayor gasto fiscal como consecuencia de las demandas sociales. El déficit fiscal efectivo alcanzó al 2,8% del PIB en 2019, estimándose, tal vez optimistamente, que llegará al 4,6% en 2020, con un aumento del gasto de 9,8%. La deuda bruta estaría representada por un 27,9% del PIB al cierre de 2019, la más alta desde 1993.

an important decrease in private non-mining investment. This is consistent with greater uncertainty, the sharp deterioration of business confidence and the higher costs faced by companies in various spheres, including the effect of the peso’s depreciation on the cost of imported machinery and the deterioration of financial conditions. The latter include the drop in share prices and higher interest rates and corporate spreads, although they have tended to normalize. The impact of these factors will, however, be partially offset by the large mining investment projects already underway and a significant increase in public investment.

The Central Bank is forecasting that inflation will average close to 4% in 2020 and reach 3.6% with respect to December 2019. This would be the result mainly of the idiosyncratic depreciation of the peso, with a higher than average pass-through

to inflation, assuming the absence of mitigating factors such as a decrease in the dollar price of imported products in response to a global appreciation of the dollar. The market is nonetheless more optimistic, anticipating inflation of around 3% on the grounds that weak activity and a weak labor market will dampen demand, thereby offsetting the upward pressure of peso depreciation.

In this context, the evolution of public finances will be relevant. They are being affected by the economic slowdown and increased spending to address social demands. In a perhaps optimistic forecast, the effective fiscal deficit, which was running at 2.8% of GDP in 2019, is projected to reach 4.6% in 2020, with spending rising by 9.8%. At the end of 2019, gross debt was running at an estimated 27.9% of GDP, its highest level since 1993.

El Banco Central proyecta que durante el 2020 la inflación alcanzará niveles promedio cercanos a 4% y de 3,6% respecto a diciembre 2019.

The Central Bank is forecasting that inflation will average close to 4% in 2020 and reach 3.6% with respect to December 2019.

27,9%Deuda Bruta del PIB al cierre de 2019.

Gross debt at the end of 2019.

M E M O R I A CO R P O R ATI VA B I C E 2 0 1 9

16

EQU

IPO

CO

RP

OR

ATIV

O

BANCO BICE EN CIFRASBANCO BICE IN FIGURES

MM$ 2015 2016 2017 2018 2019

ESTADO DE RESULTADOS: | INCOME STATEMENT:

Ingreso operacional neto | Net Operating Revenues 158.342 177.290 193.330 198.542 214.384

Gastos operacionales | Operating Expenses -91.025 -94.064 -102.155 -112.487 -119.921

Resultado operacional | Operating Income 67.317 83.226 91.175 86.055 94.463

Utilidad consolidada del ejercicio | Consolidated Annual Profit 57.009 67.678 71.222 67.040 69.144

SALDOS DE BALANCE: | BALANCE SHEET:

Créditos y cuentas por cobrar a clientes |Loans and Accounts Receivable from Clients 4.000.923 4.299.167 4.722.675 5.443.369 6.148.215

Instrumentos para negociación | Securities Held for Trading 248.355 557.828 646.140 407.754 607.592

Total Activos | Total Assets 5.457.023 5.815.487 6.620.435 7.404.573 8.593.893

Depósitos vista y otras obligaciones a la vista | Demand Deposits and Other Demand Liabilities 856.268 899.275 997.111 1.104.005 1.380.960

Depósitos y otras captaciones a plazo | Time Deposits and Other Time Liabilities 2.601.582 2.900.227 3.032.261 3.356.752 4.052.414

Instrumentos de deuda emitidos | Debt Instruments Issued 956.484 1.040.991 1.328.284 1.544.247 1.652.842

Patrimonio | Equity 407.705 455.763 505.349 552.494 601.068

Reinversión de utilidades | Profit Reinvestment Ratio 70% 70% 70% 70% 70%

Clasificación de riesgo local (Fitch, Feller) | Local Credit Rating (Fitch, Feller) AA AA AA AA AA

Clasificación de riesgo internacional | International Credit Rating BBB+ BBB+ BBB+ BBB+ BBB+

M E M O R I A CO R P O R ATI VA B I C E 2 0 1 9

17

EQU

IPO

CO

RP

OR

ATIV

O

MM$ 2015 2016 2017 2018 2019

PRINCIPALES ÍNDICES ANUALES: | PRINCIPAL ANNUAL INDICATORS:

Rentabilidad sobre patrimonio | Return on Equity 14,0% 14,8% 14,1% 12,1% 11,5%

Rentabilidad sobre activos | Return on Assets 1,0% 1,2% 1,1% 0,9% 0,8%

Índice de basilea | Basel Ratio 13,5% 14,0% 13,6% 13,3% 12,6%

Índice de riesgo | Risk Ratio 1,12% 1,06% 0,96% 1,05% 1,11%

Cartera morosa sobre cartera total | Past Due Loans over Total Loans 0,26% 0,15% 0,25% 0,26% 0,34%

Cobertura provisiones totales sobre cartera morosa | Total Provisions over Past Due Loans 8,18 13,76 7,64 7,25 6,08

OTRA INFORMACIÓN RELEVANTE: | OTHER INFORMATION:

Número de cuentas corrientes | N° of Current Accounts 78.752 86.827 93.726 100.091 106.651

Número de cuentas vista | N° of Sight Accounts 51.760 55.783 52.860 54.892 55.893

Número de depósitos a plazo | N° of Time Deposits 20.023 24.440 23.809 25.249 25.141

Número de tarjetas de crédito | N° of Credit Cards 42.272 46.510 49.892 53.050 54.909

Número de partícipes en fondos mutuos | N° of Mutual Fund Holders 41.506 42.295 44.421 46.960 47.940

Número de empleados | N° of Employees 1.284 1.336 1.374 1.381 1.426

Número de sucursales | N° of Branches 27 27 28 26 26

Fondos Administrados por BICE Inversiones Administradora General de Fondos S.A. | Administradora General de Fondos S.A. 1.786.960 2.116.781 2.430.751 2.524.894 2.890.497

Acciones en custodia BICE Inversiones |Shares held in custody by BICE Inversiones 387.798 534.051 944.981 1.153.958 1.350.051

M E M O R I A CO R P O R ATI VA B I C E 2 0 1 9

18

EQU

IPO

CO

RP

OR

ATIV

O

M E M O R I A CO R P O R ATI VA B I C E 2 0 1 9

“Durante el año 2019 se cumplió el tercer año del plan estratégico de mediano plazo 2017-2021 el cual fue establecido de acuerdo a los siguientes objetivos: la rentabilidad y excelencia en el servicio a partir de la segmentación del mercado, la atención diferenciada y especializada según las necesidades de cada tipo de cliente, el desarrollo de nuevos y mejores productos y servicios, el adecuado control del riesgo de crédito, la eficiencia operacional, la necesaria Transformación Digital y cultural que estamos implementando, y el desarrollo y motivación del personal que integra la organización.”

“In 2019, the Bank completed the third year of its 2017-2021 medium-term strategic plan. Its objectives are profitability and excellence of service, based on market segmentation, differentiated and specialized services tailored to the needs of each type of client, the development of new and better products and services, proper control of credit risk, operational efficiency, the necessary digital and cultural transformation we are implementing, and the development and motivation of the people who make up the organization.”

ALBERTO SCHILLING R.GERENTE GENERAL | CEO

M E M O R I A CO R P O R ATI VA B I C E 2 0 1 9

19

EQU

IPO

CO

RP

OR

ATIV

O

INFORME DEL GERENTE GENERALCEO’S REPORT

El año 2019 fue un período satisfactorio en cuanto a resultados para Banco BICE y sus filiales, con una utilidad neta consolidada de $69.136 millones, 3,1% superior a la obtenida en 2018, y una rentabilidad sobre patrimonio de 11,5%.

Durante el año 2019 se cumplió el tercer año del plan estratégico de mediano plazo 2017-2021 el cual fue establecido de acuerdo a los siguientes objetivos: la rentabilidad y excelencia en el servicio a partir de la segmentación del mercado, la atención diferenciada y especializada según las necesidades de cada tipo de cliente, el desarrollo de nuevos y mejores productos y servicios, el adecuado control del riesgo de crédito, la eficiencia operacional y el desarrollo y motivación del personal que integra la organización. En esa línea y como parte de nuestro plan de mediano plazo, se creó durante el año nuestra Gerencia de Transformación Digital junto con nuestro primer Laboratorio Digital, buscando fortalecer las metas antes mencionadas, acelerando nuestro proceso de cambio y adaptación al entorno competitivo al que nos enfrentamos.

La División Corporaciones inició el 2019 un proceso de transformación, poniendo a nuestros clientes en el centro de nuestro quehacer, ofreciendo productos innovadores de acuerdo a sus necesidades, destacándonos por la excelencia en la ejecución y con el firme objetivo mejorar su experiencia en servicios financieros.

En la División Empresas y Sucursales el foco ha sido brindar una atención personalizada, simple y rápida a nuestros clientes, con un servicio de calidad basada en la atención de nuestros ejecutivos comerciales. El año 2019 fue un año de avances relevantes en la automatización de procesos y en la entrega de productos y servicios completamente digitales.

La División Personas e Hipotecario continuó con su proceso de crecimiento sostenido durante el 2019, manteniendo un servicio de excelencia mediante soluciones integrales, flexibles y convenientes para satisfacer los diferentes requerimientos de los clientes.

Los volúmenes de negocios en colocaciones y clientes nuevos estuvieron en

2018 was a satisfactory year as regards the results of Banco BICE and its subsidiaries, which reported a net consolidated profit of 69,136 million pesos, up by 3.1% on 2018, and a return on equity of 11.5%.

In 2019, the Bank completed the third year of its 2017-2021 medium-term strategic plan. Its objectives are profitability and excellence of service, based on market segmentation, differentiated and specialized services tailored to the needs of each type of client, the development of new and better products and services, proper control of credit risk, operational efficiency and the development and motivation of the people who make up the organization. In line with this and as part of our medium-term plan, the Bank established a Digital Transformation area in 2019, along with our first Digital Laboratory, seeking to strengthen achievement of these goals and accelerate our process of change and adaptation to the competitive environment we now face.

The Corporate Banking Division embarked on a transformation process in 2019, putting our clients at the center of the way we do business, offering innovative products tailored to their needs and standing out for excellence of service, with the clear objective of improving clients’ experience of financial services.

The SME Banking Division’s priority was to provide clients with a rapid, simple and personalized response, anchored in the quality of service offered by our marketing executives. In 2019, the Division achieved important progress on the automation of processes and the offer of wholly digital products and services.

The Retail Banking and Mortgage Division continued to show sustained growth in 2019, maintaining its excellent service with integrated, flexible and attractive solutions to satisfy customers’ different needs.

Gross loans volume and new clients were in line with targets, reflecting an

11,5%Rentabilidad sobre el patrimonio de Banco BICE.

Banco BICE’s return on equity.

M E M O R I A CO R P O R ATI VA B I C E 2 0 1 9

20

EQU

IPO

CO

RP

OR

ATIV

O

línea con lo presupuestado, debido a un mayor énfasis en una oferta proactiva y de disponibilidad inmediata en todos los canales.

La División BICE Inversiones, que concentra los servicios especialistas de administración de fondos mutuos y de inversión, corretaje de valores y administración de carteras, alcanzó durante 2019 un monto promedio administrado en activos de terceros superior a los $6,76 billones (en torno a los US$ 9.026 millones). Además, se continuó enfatizando el desarrollo de su estrategia comercial, sustentada en una oferta multiproducto y asesoría especializada a sus distintos segmentos de clientes: Personas, Empresas, Altos Patrimonios e Institucionales.

La cabal, oportuna y efectiva administración de los riesgos es uno de los aspectos básicos de la estrategia de negocios de Banco BICE. Considerando los distintos mercados y actividades que realiza el Banco y sus filiales, la gestión de riesgos es diferenciada e integral, para lo cual se cuenta con políticas y procesos aprobados

por el Directorio. En términos de logros y desempeño, durante el último periodo, los indicadores de gestión y de eficiencia de riesgo de crédito se mantuvieron en niveles superiores a los de la industria.

La División Finanzas e Internacional mantuvo su rol corporativo de administrar la liquidez del Banco y de sus filiales, con el objeto de apoyar el crecimiento de las colocaciones, además de administrar en forma rentable los descalces del balance. Por otra parte, a través de la mesa de distribución, se continuó con el crecimiento en la venta de productos de tesorería a nuestros clientes, creciendo en el número de operaciones con los clientes, en los volúmenes transados y en los ingresos obtenidos en este negocio. Del mismo modo, se continuó con la generación de resultados financieros, por medio de la toma de descalces en el balance, la toma de posiciones y la actividad de trading en tasas de interés y tipo de cambio. Se inició también la construcción de un libro de inversiones en bonos corporativos, esperando generar un ingreso de devengo por sobre el costo de fondeo de los mismos. Por su parte, el área internacional mantuvo una estrecha relación con bancos corresponsales

Los volúmenes de negocios en colocaciones y clientes nuevos estuvieron en línea con lo presupuestado, debido a un mayor énfasis en una oferta proactiva y de disponibilidad inmediata en todos los canales.

Gross loans volume and new clients were in line with targets, reflecting an increased emphasis on the proactive offer of products and their immediate availability across all channels.

increased emphasis on the proactive offer of products and their immediate availability across all channels.

The Asset and Wealth Management Division (BICE Inversiones) is responsible for the Bank’s specialized mutual and investment fund administration services and its stock brokerage and portfolio administration services. In 2019, it managed third-party assets averaging over 6.76 billion pesos (some US$9,026 million). It also continued to focus on the development of its commercial strategy, which is based on the offer of multiple products and specialized advice to its different segments of clients: persons, companies, high-net-worth clients and institutional clients.

The full, timely and effective management of risks is one of the key aspects of Banco BICE’s business strategy. Taking into account the different markets in which the Bank and its subsidiaries operate and their different activities, risk is

managed in a differentiated and comprehensive manner, based on policies and processes approved by the Board of Directors. As regards achievements and performance, credit risk management and efficiency indicators remained above those of the industry in general.

The Treasury Division continued to fulfill its corporate role of managing liquidity for the Bank and its subsidiaries in order to support the growth of lending whilst also profitably managing balance sheet mismatches. Sales of Treasury products to clients through the trading desk continued to grow in terms of the number of operations with clients, the volumes traded and the resulting earnings. The Division also continued to generate financial earnings through balance sheet mismatches and by taking positions and trading in interest and exchange rates. In addition, the international area maintained close relations with correspondent banks and multilateral organizations so as to serve clients who operate with

M E M O R I A CO R P O R ATI VA B I C E 2 0 1 9

21

EQU

IPO

CO

RP

OR

ATIV

O

y otros organismos multilaterales, para asegurar una buena atención de clientes que operan con contrapartes en el exterior. Quisiera mencionar la decisión de crear nuestra gerencia de Transformación Digital, gerencia encargada de apoyarme en los esfuerzos, especialmente de cambio y transformación cultural y organizacional al interior del banco y filiales, de modo de ir adoptando crecientemente formas de aproximación a la solución de problemas y desafíos, con equipos multidisciplinarios, con alta autonomía, capaces de producir avances concretos en rápidos ciclos iterativos y de incorporar tempranamente las experiencias de usuarios en el desarrollo de las tareas. Estoy seguro de que el estilo histórico de disciplina y preocupación por un trabajo bien hecho y centrado en el cliente, unido a esta “nueva forma de trabajar” nos traerán grandes satisfacciones a futuro.

Finalmente, en el Premio Nacional de Satisfacción de Clientes ProCalidad 2019, el cual destaca la excelencia en el ámbito de la atención y los servicios al cliente, Banco BICE fue distinguido con el primer lugar dentro del sector Bancos Medios. A este reconocimiento se suma el premio “Mejor de los Mejores”, de la categoría Contractual.

counterparties overseas. I would like to mention the decision to create our Digital Transformation area, which will support me, particularly as regards change and the cultural and organizational transformation of the Bank and its subsidiaries, as we increasingly seek to address problems and challenges through highly autonomous multidisciplinary teams, able to produce concrete advances in rapid iterative cycles and ensure early incorporation of users’ experiences in the implementation of tasks. I am sure that our longstanding tradition of discipline and care for a job well done and focused on the client, together with this “new way of working”, will bring us great satisfaction in the future.

Finally, Banco BICE was awarded first place in the mid-sized banking category of the National ProCalidad Customer Satisfaction Prize 2019 for excellence in customer attention and services. In addition, it received the “Best of the Best” award in the Contractual category.

Análisis Financiero de los ResultadosLos activos del Banco y sus filiales aumentaron en un 16,1% respecto del año 2018. Por su parte, los principales activos rentables del Banco (créditos y cuentas por cobrar a clientes + instrumentos para negociación + instrumentos de inversión disponibles para la venta), medidos como saldos al cierre del ejercicio, aumentaron $841.4 mil millones, esto es, un 12,3%. Ello se traduce en un crecimiento de los créditos y cuentas por cobrar a clientes de $704,8 mil millones, equivalentes a un 12,9%, y a un incremento del 9,5% en los instrumentos para negociación e instrumentos disponibles para la venta.

La evolución de las colocaciones fue, principalmente, el resultado de un crecimiento del 13,6% en los préstamos comerciales, del 11,2% en los créditos hipotecarios de vivienda y del 9,3% en los créditos de consumo.

En materia de pasivos, destacan el incremento del 25,1% experimentado por los depósitos y otras obligaciones a la vista, y 20,7% de los depósitos y otras

Financial Analysis of ResultsThe assets of the Bank and its subsidiaries increased by 16.1% compared to 2018. Its principal earning assets (loans and accounts receivable from clients + held-for-trading securities + securities available for sale) measured as year-end balances increased by 841,400 million pesos, or 12.3%, with loans and accounts receivable from clients rising by 704,800 million pesos, or 12.9%, while securities for trading and available for sale were up by 9.5%.

The evolution of lending was explained principally by increases of 13.6%, 11.2% and 9.3% in corporate loans, residential mortgages and consumer lending, respectively.

In the case of liabilities, demand deposits and other sight liabilities were up by 25.1%, time deposits and other time liabilities by 20.7% and debt instruments corresponding to the issue of regular and subordinate bonds by 7.1%.

M E M O R I A CO R P O R ATI VA B I C E 2 0 1 9

22

EQU

IPO

CO

RP

OR

ATIV

O

Créditos a clientesLoans to clients

Instrumentos para negociaciónSecurities for trading

Instrumentos disponiblespara la ventaSecurities available for sale

Activos rentablesEarning assets

1. ACTIVOS RENTABLES BANCO BICE (MMM$) EARNING ASSETS BANCO BICE

6.2295.511

608408

810887

7.6476.805

2019

2019

2019

2019

2018

2018

2018

2018

M E M O R I A CO R P O R ATI VA B I C E 2 0 1 9

23

EQU

IPO

CO

RP

OR

ATIV

O

2. PRINCIPALES COLOCACIONES BANCO BICE (MMM$) PRINCIPAL LENDING BANCO BICE

ComercialesCommercial

ViviendaResidential Mortgages

ConsumoConsumer

4.957,64.364,8

1.105,4994,3

165,7151,6

20192019 2019

2018

2018 2018

M E M O R I A CO R P O R ATI VA B I C E 2 0 1 9

24

EQU

IPO

CO

RP

OR

ATIV

O

captaciones a plazo, así como el aumento del 7,1% en instrumentos de deuda correspondiente a la emisión de bonos corrientes y subordinados.

Al 31 de diciembre de 2019, el patrimonio efectivo de Banco BICE alcanzó a $ 842.548 millones y los activos ponderados por riesgo sumaron $6.691.329 millones. Como consecuencia, el Índice de Basilea al cierre de 2019 se situó en 12,6%, indicador que permite al Banco enfrentar adecuadamente las proyecciones de crecimiento del año 2020.

En el ejercicio 2019, el Banco obtuvo ingresos operacionales consolidados por $240.738 millones, que representa un incremento del 12,1% en relación con el año anterior. El gasto en provisiones por riesgo de crédito, incluyendo las provisiones adicionales, aumentó en un 62,9% debido a un índice de riesgo que aumentó a niveles de 1,11%. La razón de cobertura de provisiones totales a cartera morosa cerró en 6,1 veces.

Por su parte, los gastos operacionales registraron un aumento del 6,6%, consecuencia de lo anterior, el resultado operacional aumentó en un 9,8% respecto de 2018. Finalmente, la utilidad neta aumentó en un 3,1%.

As of 31 December 2019, Banco BICE had an effective net worth of 842,548 million pesos while its risk-weighted assets reached 6,691,329 million pesos. This gave an end-year Basel ratio of 12.6%, putting the Bank on an adequate footing for its projected growth in 2020.

In 2019, the Bank’s consolidated operating revenues reached 240,738 million pesos, up by 12.1% on the previous year. Expenditure on provisions for credit risk, including additional provisions, increased by 62.9%, reflecting an increase in the Bank’s risk ratio to 1.11%. At the end of the year, total provisions represented 6.1 times past due loans.

Operating expenses increased by 6.6% while operating income was up by 9.8% on 2018. Finally, net profits increased by 3.1%.

Depósitos a la vistaDemand deposits

Depósitos y otras a plazoTime deposits and other time liabilities

Instrumentos de deuda Debt Instruments

Obligaciones con bancosLiabilities to banks

OtrosOthers

3. PRINCIPALES PASIVOS BANCO BICE (MMM$) PRINCIPAL LIABILITIES BANCO BICE

1.3811.104

4.0523.357

1.6531.544

296297

1.2121.102

2019

2019

2019

2019

2019

2018

2018

2018

2018

2018

M E M O R I A CO R P O R ATI VA B I C E 2 0 1 9

25

EQU

IPO

CO

RP

OR

ATIV

O

MM$ 2018 2019 VAR Ingresos operacionales | Operating Revenues 214.717 240.738 12,1%

Provisiones por riesgo de crédito | Allowance account for credit risk -16.175 -26.354 62,9%

INGRESO OPERACIONAL NETO | NET OPERATING REVENUES 198.542 214.384 8,0%

Gastos operacionales |Operating expenses -112.487 -119.921 6,6%

RESULTADO OPERACIONAL | OPERATING INCOME 86.055 94.463 9,8%

Resultado por inversión en sociedades | Profit from investment in related companies 141 133 -5,7%

Impuesto a la renta |Income tax -19.156 -25.452 32,9%

Utilidad consolidada del ejercicio | Consolidated profit for the period 67.040 69.144 3,1%

Atribuible a tenedores patrimoniales | Attributable to Shareholders 67.031 69.136 3,1%

Interés minoritario | Non-Controlling Interests 9 8 -11,1%

Patrimonio |Equity 552.533 601.111 8,8%

Los gastos operacionales registraron un aumento del 6,6%, consecuencia de lo anterior, el resultado operacional aumentó en un 9,8% respecto de 2018. Finalmente, la utilidad neta aumentó en un 3,1%.

Operating expenses increased by 6.6% while operating income was up by 9.8% on 2018. Finally, net profits increased by 3.1%.

RESULTADOS CONSOLIDADOS BANCO BICEBANCO BICE CONSOLIDATED INCOME

M E M O R I A CO R P O R ATI VA B I C E 2 0 1 9

26

EQU

IPO

CO

RP

OR

ATIV

O

26

EQU

IPO

CO

RP

OR

ATIV

O

M E M O R I A CO R P O R ATI VA B I C E 2 0 1 9

EQUIPO EJECUTIVOMANAGEMENT TEAM

ALBERTO SCHILLING R.GERENTE GENERAL | CEO

PAUL ABOGABIR M.GERENTE DIVISION TRANSFORMACIÓN DIGITAL | HEAD OF DIGITAL TRANSFORMATION DIVISION

RODRIGO ÁLVAREZ S.GERENTE DIVISIÓN FINANZAS E INTERNACIONAL | HEAD OF TREASURY DIVISION

JOSÉ PEDRO BALMACEDA M.GERENTE DIVISIÓN RIESGOS | HEAD OF RISK DIVISION

EDUARDO BARRIENTOS B.CONTRALOR | COMPTROLLER

MARCELO CLEMENTE C.GERENTE DIVISIÓN OPERACIONES Y TECNOLOGÍA | HEAD OF OPERATIONS AND TECHNOLOGY DIVISION

RONY JARA A.FISCAL | LEGAL COUNSEL

PABLO JEREZ H. (INGRESÓ EN FEBRERO 2020, REEMPLAZANDO A ANDRÉS ROCHETTE G.)GERENTE DE PLANIFICACIÓN, ADMINISTRACIÓN Y CONTROL DE GESTIÓN | HEAD OF PLANNING, ADMINISTRATION AND CONTROL

MÁXIMO LATORRE E.GERENTE DIVISIÓN BICE INVERSIONES | HEAD OF ASSET AND WEALTH MANAGEMENT DIVISION

ALICE MARTINS G. (INGRESÓ EN DICIEMBRE 2019, REEMPLAZANDO A FRANCISCO GUZMÁN B.)GERENTE DE MARKETING Y EXPERIENCIA DE CLIENTES | HEAD OF MARKETING AND CUSTOMER EXPERIENCE

CLAUDIA MIRANDA R.GERENTE DIVISIÓN EMPRESAS Y SUCURSALES | HEAD OF SME BANKING DIVISION

ROBERT PUVOGEL L.GERENTE DIVISIÓN CORPORACIONES | HEAD OF CORPORATE BANKING DIVISION

CORNELIO SAAVEDRA C.GERENTE DIVISIÓN PERSONAS E HIPOTECARIO | HEAD OF RETAIL BANKING DIVISION

GINNY WALKER C.GERENTE DE PERSONAS Y DESARROLLO HUMANO | HEAD OF HUMAN RESOURCES

01

02

03

04

05

06

07

08

09

10

11

12

13

14

01

08 11

02

05

09

12

03

06

10

13

04 07

14

M E M O R I A CO R P O R ATI VA B I C E 2 0 1 9

27

EQU

IPO

CO

RP

OR

ATIV

O

M E M O R I A CO R P O R ATI VA B I C E 2 0 1 9

FILIALES SUBSIDIARIES

FEDERICO DÍAZ G.GERENTE GENERAL BICE FACTORING S.A. | GENERAL MANAGER. BICE FACTORING S.A.

GERARDO EDWARDS S.GERENTE GENERAL BICE CORREDORES DE SEGUROS LTDA. | GENERAL MANAGER, BICE CORREDORES DE SEGUROS LTDA.

CRISTIÁN GAETE P.GERENTE GENERAL BICE INVERSIONES CORREDORA DE BOLSA S.A. | GENERAL MANAGER, BICE INVERSIONES CORREDORA DE BOLSA S.A.

PATRICIO SANDOVAL F.GERENTE GENERAL BICE AGENTE DE VALORES LTDA. | GENERAL MANAGER, BICE AGENTE DE VALORES LTDA.

JAVIER VALENZUELA G.GERENTE GENERAL BICE INVERSIONES ADMINISTRADORA GENERAL DE FONDOS S.A. | GENERAL MANAGER, BICE INVERSIONES ADMINISTRADORA GENERAL DE FONDOS S.A.

01

02

03

04

05

01

02

03 04

05

GE

STIÓ

N C

OM

ER

CIA

L

02

T U S P R OY E C T O S

29

GES

TIÓ

N C

OM

ERC

IAL

M E M O R I A CO R P O R ATI VA B I C E 2 0 1 9

DIVISIÓN CORPORACIONESCORPORATE BANKING DIVISION

La División Corporaciones de Banco BICE está integrada por las áreas de Corporaciones y Grupos Económicos, Negocios y Financiamiento de Proyectos, Grandes Empresas Industrias y Servicios, Instituciones Financieras e Infraestructura, Grandes Empresas Inmobiliaria y Construcción y Servicios Transaccionales.

Nuestra misión es ser referente de mercado en la calidad de servicio y experiencia de nuestros clientes, con un foco en el crecimiento de los ingresos que generamos en nuestras relaciones comerciales.

Para lograr nuestros objetivos de largo plazo, el año 2019 iniciamos un proceso de transformación, poniendo a nuestros clientes en el centro de nuestro quehacer, ofreciendo productos innovadores de acuerdo a sus necesidades, destacándonos por la excelencia en la ejecución y con el firme objetivo mejorar su experiencia en servicios financieros.

Robert Puvogel L.Gerente División CorporacionesHead of Corporate Banking Division

Paulo García M.Gerente Grandes Empresas, Sector Industrias y Servicios Manager for Large companies, Industries and Services Sector

Ignacio Hernández M.Gerente Grandes Empresas, Sector Inmobiliario y Construcción Manager for Large Companies, Real Estate and Construction Sector

Sebastián Pinto E.Gerente Corporaciones Corporations Manager

Rodrigo Violic G.Gerente de Negocios y Financiamiento de Proyectos Business and Project Financing Manager

Mónica Cornú P.Subgerente Instituciones Financieras e Infraestructura Manager for Financial Institutions and Infrastructure

Banco BICE’s Corporate Banking Division comprises the following areas: Corporations and Economic Groups, Business and Project Financing, Large Industrial and Service Companies, Financial Institutions and Infrastructure, Large Real Estate and Construction Companies, and Transactional Services.

Its mission is to be a reference in the market for service quality and customer experience, with a focus on growing the income generated through its commercial relations.

In pursuit of its long-term objectives, the Division embarked on a transformation process in 2019, putting its clients at the center of how it does business, offering innovative products tailored to their needs and standing out for the excellence of its services, with the clear objective of improving clients’ experience of financial services.

M E M O R I A CO R P O R ATI VA B I C E 2 0 1 9

30

GES

TIÓ

N C

OM

ERC

IAL

29%Aumentaron las colocaciones respecto del año 2018.

Financial Loans increased compared to 2018

Corporaciones y Grupos EconómicosEl 2019 fue un año complejo, marcado por una importante disminución de las tasas de largo plazo y altos niveles de competencia del mercado financiero. Lo anterior generó una alta demanda por refinanciamientos de créditos, los que, en algunos casos, no fue posible retener impactando negativamente el stock de colocaciones del primer semestre. Sin embargo, una activa gestión comercial, gracias a varios financiamientos estructurados, permitió revertir esta situación, aumentando las colocaciones en torno al 29% respecto del año 2018.

En el ámbito de las soluciones tecnológicas, se implementó un desarrollo para un importante emisor de tarjetas de crédito, que permite a sus clientes realizar en línea la solicitud y el abono de créditos.

Instituciones Financieras e InfraestructuraDurante 2019, la gerencia de Instituciones Financieras e Infraestructura experimentó un fuerte crecimiento en colocaciones, saldos vista y margen financiero, dado que esta área reúne la experiencia y reconocimiento en el desarrollo de soluciones a la medida para los diferentes clientes financieros, con el conocimiento y capacidad de financiamiento y estructuración en el mundo de la infraestructura local.

Esta gerencia es un referente en el mercado en atención a las instituciones financieras, desarrollando diversos financiamientos y servicios a la medida de cada uno de los ellos. Asimismo, durante 2019 ha visto incrementada su presencia en el sector Infraestructura, participando en diferentes licitaciones y financiamientos, lo que lo llevó a concretar financiamiento para Vías Chile en Autopista Los Libertadores y Autopista Rutas del Pacífico.

Corporations and Economic Groups2019 was a complex year, marked by a significant decrease in long-term interest rates and intense competition in the financial market. There was, as a result, high demand for credit refinancing and, in some cases, it was not possible to retain the business, which negatively impacted the stock of lending in the first half of the year. However, active commercial management, thanks to several structured financing operations, meant that it was possible to turn the situation around and end the year with lending up by 29% on 2018.

In the case of technological solutions, a solution for a major credit card issuer was developed to allow its customers to apply for and repay loans online.

Financial Institutions and InfrastructureIn 2019, the Financial Institutions and Infrastructure area achieved strong growth of lending, sight balances and financial margin. This reflected its experience and track record in the development of tailored financial solutions for different clients, its knowledge of the local infrastructure sector and capacity to serve its financing and structuring needs.

The area has become a reference in the market for attending financial institutions, developing different types of financing and services in line with the needs of each of its clients. In addition, it increased its presence in the infrastructure sector, participating in different tenders and requests for financing as a result of which it provided financing for Vías Chile (Los Libertadores and Rutas del Pacífico Highways).

M E M O R I A CO R P O R ATI VA B I C E 2 0 1 9

31

GES

TIÓ

N C

OM

ERC

IAL

En resumen, durante 2019, el número de clientes creció en un 10,55%, las colocaciones en un 20,85%, alcanzando aproximadamente MM$785.720, mientras que los saldos vista crecieron un 46,0% y margen Financiero, un 30%.

Sector Inmobiliario y ConstrucciónEn el 2019, la gerencia tuvo un cambio en el modelo de negocio, reestructurando el área. Se ha buscado dar mayor fuerza a sus integrantes, además de modificar ciertas metodologías de trabajo, con el objeto de convertirnos un equipo de trabajo más eficiente en la resolución de las necesidades de nuestros clientes. El resultado ha sido considerablemente favorable, debido a que hemos crecido, tanto en el número de clientes como en el número de proyectos, traduciéndose esto en mayores volúmenes de colocaciones.

La gerencia está fuertemente comprometida y alineada con la Transformación Digital, cultura organizacional implementada por el Banco. Sabemos que es de suma importancia desarrollar nuevas competencias y habilidades digitales para generar valor, tanto para nuestros clientes como para el área.

Tenemos claro que el año 2020 será un año de grandes desafíos, por lo que debemos mantenernos cerca nuestros clientes y conocer claramente sus necesidades, y de este modo, generar soluciones financieras creativas y a la medida, además de lograr sinergias crecientes con otras áreas de negocio global del Banco y filiales.