01 fraserthompson (alphabeta) v4 - hicap...

TRANSCRIPT

UPDATEAsia at the Crossroads:

5 forces transforming Asia-Pacific regionFraser Thompson, AlphaBeta

Email: [email protected]: www.alphabeta.com

YesA: NoB:

WasNapoleonrelativelyshort?1.

1 100USD2 500USD3 1.000USD4 5,000USD5 10,000USD6

1MillionUSD

50,000USD100.000USD200,000USD500,000USD

78910

1A:

3C:

2B:

NoneoftheaboveD:

Howmanywisemenwerementionedinthebible?2.

1 100USD2 500USD3 1,000USD4 5,000USD5 10,000USD6

1MillionUSD

50,000USD100,000USD200,000USD500,000USD

78910

3secondsA:

3monthsC:

3daysB:

3yearsD:

Howlongisthememoryofgoldfish?3.

1 100USD2 500USD3 1,000USD4 5,000USD5 10,000USD6

1MillionUSD

50,000USD100,000USD200,000USD500,000USD

78910

5

Fivemyths

Goodbyetoglobalization1

Growthwillcomefromtheregion’smegacities2

Whenitcomestotourism,it’sallaboutcapturingtheChineseconsumer3

TechnologydisruptionwillbethesameinAsiaaselsewhere4

Wewillreturnto“business-as-usual”afterafewshocks5

Tradedealsarenotdead!

0

30

60

90

120

2014

2012

2010

2008

2006

2004

2002

2000

1998

1996

1994

1992

1990

1988

1986

1984

1982

1980

1978

1976

1974

1972

1970

South-SouthNorth-SouthNorth-North

Numberoftradeagreements(withtradefacilitationcomponents)

6

Whoisinandwhoisout?

RegionalComprehensiveEconomicPartnership(RCEP)

• Cambodia• India• Laos• Myanmar

• HongKong• PapuaNewGuinea• Russia• Taiwan

FreeTradeAreaoftheAsia-Pacific(FTAAP)

• China• Indonesia• Philippines• SouthKorea• Thailand

Trans-PacificPartnership(TPP)• Canada• Chile• Mexico• UnitedStates• Peru

• Australia• Brunei• Japan• Malaysia• NewZealand• Singapore• VietNam

7

TheASEANEconomicCommunity(AEC)movesintoitsnextphase

AECBlueprint2025

Ahighlyintegratedandcohesiveregionaleconomy• Freeflowofgoods• Addressnon-tariffbarriers

• Deepintegrationintradeofservices

• Moreseamlessmovementofinvestment,skilledlabour,businesspersons,andcapital

Competitive,innovative&dynamiccommunity• Digitaltechnology• Innovation• Greentechnology• Goodgovernance• Tacklingcorruption

• Disputeresolution• Enhancedparticipationinglobalvaluechains

Enhancedconnectivityandsectoralcooperation• Focusonstrategicsectoralpriorities

• Infrastructure

Aresilient,inclusive,people-orientedandpeople-centredcommunity• MSMEs• Povertyeradication

• Sub-regionalcooperation

GlobalASEAN• AdriverofregionaleconomicintegrationinEastAsia

• AunitedASEANwithanenhancedroleandvoiceinglobaleconomicforainaddressinginternationaleconomicissues

8

ASEANhasambitiousplansfortourismby2025

• TheGDPcontributionofASEANtourismcouldincreasefrom12%to15%• Tourism’sshareoftotalemploymentcouldincreasefrom3.7%to7%• PercapitaspendingbyinternationaltouristscouldincreasefromUS$877to US$1,500• Increasetheaveragelengthofstayofinternationaltouristarrivalsfrom 6.3 nightsto8 nights.

• Thenumberofaccommodationunitscouldincreasefrom0.51unitsper100headofpopulationinASEANto0.60unitsper100headofpopulation.

9

TourismprogressonIntegration

FDIrestrictionsreduced.SecondmostliberalizedsectorforFDIinASEAN(afterlogistics),althoughconstraintsinsomecountries(e.g.,Thailand)

Visaliberalization.Removalofvisarequirementsforshort-termtravelbyASEANcitizensinmostmemberstates.MovetowardsASEANsinglevisa

Introductionofopenskypolicies.Encouragedintroductionofnewcarriersinroutespreviouslydominatedbynationalincumbents

Vocationaltrainingprograms.Launchofnewtrainingprograms(e.g.,Singapore-MyanmarVocationalTrainingInstitute)

Visaissuesremain.ProgressonASEANBusinessTravelCardislimited.

Restrictionsondomesticairlinecompetition.Domesticroutesareonlyopentonationalcarriers.

Weaklabourmobility.Verylimitedprogressontourism-relatedlabourmobilityinASEANdespitebeinghavingmutualrecognitionagreements.

10

11

TheASEANSingleAviationMarketisaworkinprogress!

Whathasbeenachieved?ü Whathasbeenachieved?û

3rdfreedom

7thfreedom

Therighttoflyfromone’sowncountrytoanother

Therighttoflybetweentwoforeigncountrieswhilenotofferingflightstoone'sowncountry

4thfreedom

8thfreedom

Therighttoflyfromanothercountrytoone’sown

Therighttoflyinsideaforeigncountry,continuingtoone'sowncountry

5thfreedom

9thfreedom

Therighttoflybetweentwoforeigncountriesonaflightoriginatingorendinginone'sowncountry

Therighttoflyinsideaforeigncountrywithoutcontinuingtoone'sowncountry

12

ASEANcountriesstillimposevisarequirementsforshortbusinessvisits

Brunei Indonesia Singapore Thailand VietnamCambodia Laos Malaysia Myanmar PhilippinesASEANmemberstates

VisaonarrivalVisarequiredinadvance Novisarequired

Nationality

Japan

China

India

UK

US

Korea

Germany

France

Canada

Australia

13

ASEANisbuildingintegratedtripplanningfacilitiesandsupportingthedevelopmentofe-visas

• TheWesternAustraliawebsitehasspecificitinerarieslistedontheirwebsitewhichhelpstravelersplantheirtripbetter

• Theyalsohaveaneventssectionsthatliststhevariouspopulareventsandleadsyoutothelinktobookticketstotheevents

• Thewebsitealsohastheoptiontotranslateitintomultiplelanguages

WesternAustraliatourismwebsite Turkeytourismwebsite

• InformationtabontheTurkeytourismwebsiteprovidesinformationonthee-visaeligibilityandprocess

• Theapplicationfore-visaisintegratedintothewebsite• Itletsyouapplyforthevisa,makepaymentandthendownloadtheapprovedvisainstantaneously

• Alsohasoptionstotranslateintocommonlanguagesi.e.Spanish,Germanetc.

14

Fivemyths

Goodbyetoglobalization1

Growthwillcomefromtheregion’smegacities2

Whenitcomestotourism,it’sallaboutcapturingtheChineseconsumer3

TechnologydisruptionwillbethesameinAsiaaselsewhere4

Wewillreturnto“business-as-usual”afterafewshocks5

15

Nottheusualsuspects:middleweights,notmegaregions,aregrowingfastestinASEAN

Source: AlphaBetaregionaldatabase

CompoundannualgrowthrateofrealGDPShareofrealGDP2015

ShareofPop.2015#ofregions20152010-2015 2015-2020

5.0

5.0

5.1

4.2

4.8

5.7

MegaRegions5millionandabove

LargeMiddleweights1million– 5million

SmallMiddleweights500,000– 1million

Total

RuralRegionsBelow300,000

SmallRegions300,000– 500,000

6.9

5.8

5.5

6.0

5.5

6.0

32% 48%184

33% 11%8

16% 22%191

11% 10%448

8% 9%143

974

16

Don’tthinkaboutcountrieswhenitcomestogrowth–ThinkaboutcitiesGDPgrowth2010-2015CAGRPercent

1 Regionswith>500,000people.

3

5

5

6

6

6

8

9

9

11

145

8

6

15

108

10

12

23

ASEANaveragegrowth(5.5)

Thailand

Singapore

Malaysia

VietNam

Indonesia

Philippines

Brunei

LaoPDR

Cambodia

Myanmar

Fastestgrowingregion1Averagecountrygrowthrate Differenceingrowthrate;Percent

12

3

1

N/A

4

9

1

3

11

N/A

17

Whatisdrivingthegrowthofthemiddleweightregions?

Percentofuppermiddle– Weightregionswheregrowthdriverisoflargeormediumimportance1,Percent

1 Onlyincludesregionswithapopulationofmorethan1millioninhabitants

MediumLarge

30

12

12

18

10

42

30

22

14

14

34

Satelliteregion

Naturalresources

Tourism 32

24Growingconsumerbase

42

Trade&FDI 72

18

Examples

Mid-sizemiddle-weights Country

Growth rate(2009-13;percent)

Rich innaturalresources

Trade andFDI Tourism

Satelliteregion

Growingconsumerbase

Cebu4.4million

Karawang2.2million

Bandung3.4million

ChiangRai1.2million

Makassar1.4 million

Largefocus Mediumfocus

9.4

8.7

8.6

8.1

8.8

19

Fivemyths

Goodbyetoglobalization1

Growthwillcomefromtheregion’smegacities2

Whenitcomestotourism,it’sallaboutcapturingtheChineseconsumer3

TechnologydisruptionwillbethesameinAsiaaselsewhere4

Wewillreturnto“business-as-usual”afterafewshocks5

20

TourismisboominginASEAN,particularlyfromincreasingintra-ASEANvisitorsTouristarrivalsintoASEAN

4%4%4%

12%

30%

46% OtherAmericaOceaniaEuropeAsia(exASEAN)Intra-ASEAN

21

Manyplannedregionalinfrastructureprojectswillsupportthisgrowth

7

43

11

1

1

1

12

2

1 3

9

2

2

5

4

21

ThailandIndonesia

3

Malaysia

7

VietNam Brunei

2

Cambodia

2

Myanmar

2

Laos Total

1

39

2

Philippines

9

2

Road Rail Port EnergyAirportNumberofplannedPPPinfrastructureprojectsinASEAN

22

Fivemyths

Goodbyetoglobalization1

Growthwillcomefromtheregion’smegacities2

Whenitcomestotourism,it’sallaboutcapturingtheChineseconsumer3

TechnologydisruptionwillbethesameinAsiaaselsewhere4

Wewillreturnto“business-as-usual”afterafewshocks5

AnumberofuniqueaspectsinAsiawillinfluencetechnologydisruptionAsiacontext

Rapidlygrowingaffluentmiddleclass

Techlovingpopulation

Supplychainfragmentation

Skillsconstraints

Lowstartingpoint

• ASEANisthe2nd largestfacebookmarket

• AsidefromBruneiandSingapore,>50%ofallgrocerymarketsinASEANarestillconsideredtraditionalgroceryretailers.

• Only~20%ofpopulationabove25havecompletedsecondaryschooling

• <50%broadbandpenetrationinallcountriesexceptSingapore

• Consumingclasswilldouble inASEANby2030

• Bigdatatechniquestounderstandbuyingbehavior

• Socialmediastrategybecomescoretogrowth

• InternetofThingsallowstransformationofsupplychain

• Technologyempoweringworkersbyupskillingthem,orenablingthemtoachievesimilarimpactwithoutobtainingahighskill-level

• Lowwagecostsmaylimitdisplacement• Opportunityfordigitalleapfrogging

KeyfactsinASEAN Implicationsfortourism

23

TechnologywillcontinuetogiverisetoinnovativenewentrantsanddisruptincumbentsMusicindustryexample

NewtrendsemergeInnovativestartupscreatedisruptivebusinessmodels

Earlyadoptersstartembracingthenewmodels

Advancedincumbentsstartadaptingtothenewmodel

Mainstreamcustomersadopt

Laggardincumbentsdie

Advancedincumbents&established“start-ups”constitutethenewnormal

TimeDigitallynascent Emergingorontheadoptioncurve Newnormal

TippingpointIllegalupstart

provesdownloadpotential(1999)

Rentalandpurchasingmodels

Incumbentsfromproductionandretail

Traditionalretailers

24

5testsoftechnologicalreadiness

Doesyourcompanycultureallowyourteamtoundertakeboldtechnologyinitiatives?4

Doyouhavethepeopleinplacetodaytosupportwhereyouneedtogoto?Howdoyoumanagethetransitionforthosewhowillbedisplaced?5

Haveyoufullyintegrateddigitalinitiativesintoyourstrategicplanningprocess?2

3 Whichdisruptorsaresettochangeyourindustrylandscape?AretheyaNapsteroraSpotify?

1 Canyounamethreetofivetechnologiesthatposethebiggestrisksoropportunitiestoyourbusiness?Aretheydifferentthanoneyearorthreeyearsago?

25

26

Fivemyths

Goodbyetoglobalization1

Growthwillcomefromtheregion’smegacities2

Whenitcomestotourism,it’sallaboutcapturingtheChineseconsumer3

TechnologydisruptionwillbethesameinAsiaaselsewhere4

Wewillreturnto“business-as-usual”afterafewshocks5

27

ExecutivesoperatinginAsiaconsidergeopoliticalinstabilitytobethebiggestpotentialrisktoglobaleconomicgrowthWhatriskstoeconomicgrowthwillbepresentintheglobaleconomyoverthenext12months?

5

11

11

10

22

30

33

34

38

68

Increasedeconomicvolatility

GeopoliticalInstability

Transitionsofpoliticalleadership

Domesticpoliticalconflicts

Newassetbubbles

Increasedvolatilityofexchangerates

Lackofaccesstocredit

Insufficientgovernment-policysupport

Lowconsumerdemand

Oneormoredefaultsonsovereignbond

8

12

19

15

21

20

22

36

37

68

4

4

13

12

26

16

28

35

39

77

8

11

16

17

29

19

18

31

25

82

9

10

16

21

13

18

19

33

35

75

China India Asia-Pacificcountries Europe NorthAmerica

28

Whataresomeoftheriskstogrowth?

Chinaeconomictransition

Description

• Transitionfrominvestmentledgrowthmodeltoconsumerledmodel

Impactontourism

• MostexposedmarketsincludeMalaysiaandKorea• Indonesialessexposed

SouthChinaSea• “Saber-rattling”fromChina • DropintourismarrivalsfrommainlandChina–

KoreaandTaiwanalreadyimpacted

Debt• Unwindingofhighconsumerdebtlevels

• MalaysiaandThailandhavesomeofhighestdebttodisposableincomelevelsglobally

• Myanmarwithriskstocapitalaccount

USDstrength• AppreciatingUSDplacingpressureoncurrenciespeggedtoUSD

• PotentialslowdowningrowthinHongKong.Korea,Taiwan,Thailand,andVietnamneedtobecareful

Demographics• Reductioninworkingagepopulation • Thailand/Singapore/Korea/Taiwanparticularly

impacted

29

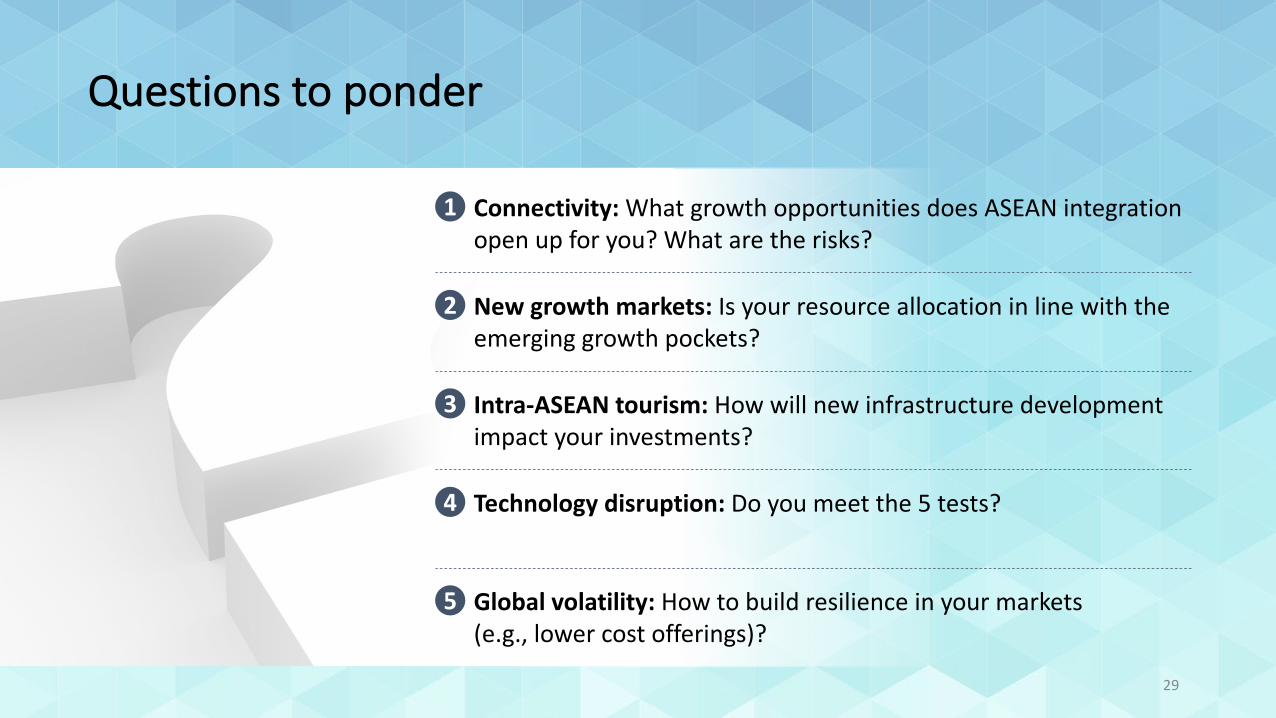

Questionstoponder

Connectivity:WhatgrowthopportunitiesdoesASEANintegrationopenupforyou?Whataretherisks?

1

Intra-ASEANtourism:Howwillnewinfrastructuredevelopmentimpactyourinvestments?

3

Technologydisruption:Doyoumeetthe5tests?4

Newgrowthmarkets:Isyourresourceallocationinlinewiththeemerginggrowthpockets?

2

Globalvolatility:Howtobuildresilienceinyourmarkets(e.g.,lowercostofferings)?

5

UPDATE

Thankyou

30