logicamms · petromod businesses were also closed, freeing up more than $1.5 million in working...

TRANSCRIPT

CLEAR FOCUSANNUAL REPORT 2017

LO

GIC

AM

MS

AN

NU

AL

RE

PO

RT

20

17

Our business ........................................................................................................ 1FY2017 performance summary ....................................................................... 2FY2018 business priorities ................................................................................ 2Chairman’s Report .............................................................................................. 5Chief Executive Officer’s Report ...................................................................... 7Board and management ................................................................................... 9Corporate Governance Statement ................................................................ 10Directors' Report............................................................................................... 11 Principal activities ....................................................................................................................11

Operating and Financial Review ....................................................................................11

Information on Directors ....................................................................................................14

Information on Company Secretary ............................................................................15

Meetings of Directors ............................................................................................................15

Remuneration Report – audited ....................................................................................16

Indemnification and insurance of officers and auditors ........................................................................................................24

Non-audit services ..................................................................................................................24

Proceedings on behalf of the Company ...................................................................25

Auditor's Independence Declaration ..........................................................................25

Rounding of amounts ...........................................................................................................25

Financial statements ........................................................................................ 26 Consolidated statement of profit or loss

and other comprehensive income ...............................................................................27

Consolidated statement of financial position........................................................28

Consolidated statement of changes in equity ......................................................29

Consolidated statement of cash flows .......................................................................30

Notes to the financial statements .................................................................................31

Directors Declaration ....................................................................................... 63Independent Auditor’s Report ....................................................................... 64Auditor’s Independence Declaration ............................................................ 71ASX information ............................................................................................... 72

CONTENTS

Purpose of the annual report

The purpose of this annual report is to explain LogiCamms’ strategy and operations, and the performance of the business during FY2017. The report also sets out our strategic objectives and business priorities for FY2018.

1LogiCamms 2017 Annual Report

OUR BUSINESS

LogiCamms provides professional engineering and

environmental consulting services, and competency training.

We work with asset owners and operators in three major market

segments: hydrocarbons, minerals and metals, and infrastructure.

The focus of our work is to help our clients to reduce costs and

improve the performance of their assets, with an emphasis on

brownfield or operating facilities.

Our vision Our purpose Our values

To be a market leader delivering outstanding customer solutions

To enhance the value and performance of assets

Can Do Approach Teamwork Integrity Delivering Quality Results Commitment to People

NEW PLYMOUTH

BRISBANE

MELBOURNE

ADELAIDE

PERTH

MACKAY

WHYALLA

LogiCamms 2017 Annual Report2

FY2017 PERFORMANCE SUMMARY

FY2018 BUSINESS PRIORITIES

OPERATIONAL PERFORMANCE• Completed organisation restructure to re-base the business

for FY18 and beyond by:

- concentrating on our core strengths in automation, electrical instrumentation and controls, and engineering procurement and commissioning (EPC) projects

- re-balancing client facing resources and corporate overheads for the current market

- reducing annualised operating costs by $10.5 million (at a one-off cash cost of $2.1 million recognised in FY17) with savings to be realised in FY18 and beyond

- closing low margin Hunter Valley and Petromod businesses.

• Expanded portfolio of Master Service Agreements which make LogiCamms a pre-qualified supplier with these clients. Approximately 35 of these agreements are actively delivering an increase in firm work orders.

• Progressed development and commercialisation of our suite of new technology products. These projects build on our acknowledged expertise in control systems, and are reaching a critical level of maturity and client acceptance.

• Increased the term and approved limit on our banking facilities to support current order book growth and the working capital needs of the business, with the support of NAB.

• The Company entered FY18 with more than $25 million in work in hand at 30 June 2017, and has won a further $13 million in new work in FY18 as client spending deferred in FY17 begins to convert to revenue.

• Re-based business is positioned to capitalise on a recent uplift in client spending in our core market segments:

- Minerals and Metals: Increased commodity prices are encouraging investments in new projects to unlock productivity gains and catch up on deferred capital expenditure on operating assets

- Infrastructure: Increasing new project investments by governments and private sector organisations. LogiCamms is expanding services into new infrastructure markets in water and agribusiness

- Hydrocarbons: LogiCamms continues to focus on major projects with upstream gas producers.

• Build on the portfolio of Master Service Agreements to pursue new project and revenue opportunities with existing and new clients.

• Leverage our specialist expertise in control systems integration, automation and electrical installation and commissioning to pursue opportunities in our traditional market segments and selected new growth sectors and markets.

• Explore new commercial models including collaborations and partnerships with asset owners and other service providers, to increase revenue and margins.

• Accelerate development and commercialisation of our technology products and commercial models, to increase the share of revenue from value-based services rather than traditional professional fees contracts.

• Become an employer of choice in the consulting engineering market by offering staff the right mix of challenging project work, personal and technical development opportunities, monetary and non-monetary benefits, and a safe, social and inclusive place to work.

1 Underlying EBITDAI is not an IFRS measure and is not audited. It is calculated by adjusting statutory net profit after tax by adding back interest, tax, depreciation, amortisation and goodwill impairment.

12 months to 30 June 2017 FY17 ($m) FY16 ($m)

Revenue 81.1 108.2

NPAT (23.6) (38.1)

EBITDAI1 (8.1) (8.4)

3LogiCamms 2017 Annual Report

LogiCamms 2017 Annual Report4 LogiCamms 2017 Annual Report4

The business is now well positioned to capitalise on increasing client activity in our traditional engineering, training and environmental consultancy businesses, and we have started the new financial year with improving order book momentum.

LogiCamms reported a statutory net loss after tax of $23.6 million, which compares with a loss of $38.1 million for the previous year. This includes a goodwill impairment of $11.0 million which does not impact on the cash position of the Company.

The Board has taken the prudent decision not to recommend an interim or final dividend for the 2016-17 financial year.

The Company has a cautiously optimistic outlook for the year ahead, after the re-structuring of the business and taking into account recent order book growth. Market conditions for our clients are also improving with increased commodity prices and commitments by public and private sector organisations to a number of new infrastructure developments.

The Board has taken the opportunity to consider the composition of skills required to guide the business through its current opportunities and challenges.

Charles Rottier is an experienced engineering and construction executive with extensive experience in Australia and internationally. His appointment in September 2017 as an independent non-executive director complements the existing Board skills set, and brings first-hand knowledge of the dynamics of our core market segments to guide strategic decision making.

I would like to thank the staff of LogiCamms for their continued hard work and focus during a year of adjustment within the business. They continue to deliver high quality engineering solutions for our clients, which underpin the success of the business. Thank you also to the Company’s leadership and directors who have steered the business through necessary changes to return LogiCamms to profitable growth.

On behalf of the Board, I would also like to thank our clients and shareholders for their continued support of the business through the financial year and into the future.

Peter Watson Chairman

LogiCamms responded decisively to continued tough market conditions during 2016-17, with our new management team restructuring the business to reduce operating costs, re-balance our workforce and re-focus on our core strengths.

CHAIRMAN’S REPORT

5LogiCamms 2017 Annual Report 5LogiCamms 2017 Annual Report

LogiCamms 2017 Annual Report6 LogiCamms 2017 Annual Report6

I have also spent time talking to our employees and shareholders about the challenges and opportunities facing the business. This has been an invaluable exercise, giving us an up-to-date and informed perspective on the market, and a solid foundation for the work to re-set the business for the future.

Given the nature of our business, safety is always our first and most important priority. I am pleased to say that we reported no lost time injuries in FY17 for the first time in recent years. This can be attributed to a consistent focus across the business on injury prevention, early incident reporting and responsible injury management. However, this positive result was tempered by the fact that our FY17 Total Recordable Injury Rate was 3.59. While none of these were significant injuries, they were still distressing for the people involved and entirely preventable, which shows that safety must remain our foremost day-to-day priority.

Our safety focus for FY18 is to build on this momentum by engaging everyone across the business to create a “hearts and minds” movement to strengthen our individual and collective values towards safety, health & wellbeing, quality and environmental sustainability.

During the financial year, we reported no environmental incidents and attained ISO 14001 (Environmental Management) for all of our Australian operations. This reinforces that we are on the right path to environmental sustainability and best practice.

The restructuring of the business has concentrated our activities on the core strengths for which LogiCamms has long been recognised, in automation, electrical instrumentation and controls, and engineering procurement and commissioning (EPC) projects. We have secured more than 50 Master Service Agreements (MSAs) with clients, which position us as a pre-qualified supplier in our core areas of expertise. Approximately 35 of these agreements are actively delivering an increase in firm work orders.

During the second half of the financial year, we also restructured the business to reduce operating costs and align our workforce to suit prevailing market conditions. At the outset of FY17, the cost base of the business had been set for a budget to achieve revenue of more than $100 million. However, projects that had been anticipated for FY17 were deferred into the following year or converted into revenue more slowly than we had forecast.

The business was unable to replace the significant volume of work on the Roy Hill iron ore project that concluded in FY16 after contributing revenue of more than $30 million in that year. In addition, intense competition negatively impacted both our sell rates and gross margins.

We took a number of actions to address these challenges to the business.

Between June and August 2017, we reduced the workforce by a total of 80 roles from corporate overheads and non-reimbursable labour through a combination of the restructuring and natural attrition. Our workforce at the end of the financial year totalled approximately 405 full-time equivalent roles, down from 450 in the previous financial year. These changes reduced labour costs by $8.8 million.

We also undertook a comprehensive review of overheads, generating savings of $1.7 million across IT and communications, premises and other general and administrative expenses.

These changes will reduce total operating costs by $10.5 million. One-off restructuring costs of $2.1 million were recognised in FY17, and the cost savings will be realised in FY18. The low-margin Hunter Valley and Petromod businesses were also closed, freeing up more than $1.5 million in working capital.

All of these changes have effectively re-based the business for FY18 and beyond. We are a more focused and streamlined business, with a consulting workforce and overhead structure that is closely aligned to the current pipeline of opportunities.

In the early months of FY18, we have begun to see the benefits of restructuring the business and reinforcing our value proposition that spans from environmental consulting through engineering design, project management and commissioning, to competency training.

In our traditional market segments, we are beginning to see an upward shift in client spending. Increasing commodity prices are giving clients in the Minerals and Metals segment greater confidence to invest in projects that unlock productivity gains and catch up on deferred capital expenditure on brownfield assets. In the infrastructure segment, governments and private sector organisations are increasing their investments in new projects. Through the financial year, the Company continued to expand its services into new areas of the infrastructure segment, carrying out a significant volume of work for water utilities in Queensland, South Australia and Western Australia, and in agribusiness for Viterra.

Since my appointment as CEO in February 2017, I have spent a great deal of time connecting with our clients to understand the factors that currently drive their businesses.

CHIEF EXECUTIVE OFFICER’S REPORT

7LogiCamms 2017 Annual Report 7LogiCamms 2017 Annual Report

LogiCamms 2017 Annual Report8

To access new opportunities within these traditional market segments, we have also pursued a number of strategic partnerships. Already this strategy has led to some exciting developments, with the Company winning a role on Northconnex, Australia’s longest road tunnel project, in New South Wales. We have also signed an agreement with Dassault Systèmes to jointly pursue technical and business opportunities in the natural resources, energy and utilities, and life sciences industries.

We have also continued to invest in developing new technology solutions that build on our recognised expertise in control systems, and which offer our clients innovative ways to improve the performance of their operating assets.

These products are beginning to reach a critical level of maturity and client acceptance, and we secured our first significant commercial contract for LogiCamms’ proprietary Automated Infrastructure Design Engine (AIDE) with a blue-chip CSG producer. AIDE was developed by our software engineers and GIS (Geographic Information Systems) specialists to reduce design time and costs for linear infrastructure projects such as gas pipelines and telecommunication, road, rail and energy networks.

In addition, our in-field data capture and tracking solution, Stacks On, is currently undergoing proof of concept trials with a major ASX-listed client. This product allows clients to optimise the performance of materials stockpiles and we are targeting first commercial contracts in FY18.

The commercial models for these solutions are based on sharing the value they create for clients rather than traditional professional fees, and offer potential to develop new, higher margin revenue streams.

These developments are contributing to strengthening order book momentum for the business. At the end of the FY17 year, the Company reported Work in Hand of $25.1 million, which equates to approximately 33 per cent of forecast FY18 engineering consulting revenue. Since the year end, we have also secured new contract wins totalling more than $13 million. LogiCamms is actively recruiting specialist engineering and technology resources to support this growth in our order book. We have also had the support of NAB to increase both the term and approved limit of our banking facility, to support this order book growth and the working capital needs of the business.

We continue to refine the Company’s strategic direction and position the business to capitalise on prevailing market conditions. An updated strategic plan is being developed under the theme of Clear Focus, concentrating on the value proposition, markets and alliance partners to profitably grow the business and as a result, create greater value for shareholders. The plan will outline actions to develop our strong market position in the core professional consulting and engineering services, broaden our services and capabilities through the investments in technology products and new commercial models, and expand into new growth industries and segments in which we have a defined competitive advantage.

I am optimistic about the performance of the business and the market outlook for FY18. I am also pleased that we have maintained the support of our employees, clients, financiers and shareholders as we have managed the transition to strengthen the competitive position of the business. Thank you for your continued support for LogiCamms.

Flora Furness Chief Executive Officer

9LogiCamms 2017 Annual Report

BOARD AND MANAGEMENT

Peter WatsonNon-Executive Chairman

Peter is a business leader with more than 30 years of experience in engineering, construction and services. He has a strong background in achieving growth for businesses on local and international scale.

• Joined LogiCamms 2011

• Former CEO of Transfield Services (ASX: TSE)

• Chairman, Regional Rail Link Victoria and AssetCo

Peter WallNon-Executive Director

Peter is a founding Board member of LogiCamms and has decades of experience in management and board positions, with a focus on human resources and corporate governance.

• Joined LogiCamms in 2007

• Long standing tenure at S. Smith & Sons (The Yalumba Wine Company) and role in international trade facilitation for the wine industry

Richard Robinson Non-Executive Director

Richard has extensive experience in the oil and gas industry in Australia and Papua New Guinea in project management, operations and commercial roles in upstream and downstream sectors. He has also been a consultant in the oil and gas, engineering and construction industries.

• Joined LogiCamms in 2015

• Former Executive General Manager at Oil Search (ASX: OSH)

• Chairman of Kina Petroleum Limited (ASX:KPL)

Charles Rottier Non-Executive Director

Charles is a senior manager with extensive management and project experience in local and international engineering, construction and maintenance services companies. He has managed successful businesses with operations in Australia, PNG, Asia, and the Americas.

• Joined LogiCamms in September 2017

• Former CEO, Austin Engineering (ASX: ANG)

• Former Executive General Manager at Transfield Services (ASX: TSE)

Management

Flora FurnessChief Executive Officer

Dan DreweChief Financial Officer

Iulius MincuDirector, Innovation Technology & Asset Performance

Chief Operating OfficerRole currently being recruited

CORPORATE GOVERNANCE STATEMENTFor the year ended 30 June 2017

LogiCamms Limited and the Board are committed to achieving

and demonstrating the highest standards of corporate

governance. LogiCamms Limited has reviewed its corporate

governance practices against the Corporate Governance Principles

and Recommendations (3rd edition) published by the ASX

Corporate Governance Council. The 2017 corporate governance

statement is dated as at 30 June 2017 and reflects the corporate

governance practices in place throughout the 2017 financial year.

The 2017 corporate governance statement was approved by the

board on 12 September 2017. A description of the group’s current

corporate governance practices is set out in the group’s corporate

governance statement which can be viewed at

www.logicamms.com.au/investor-relations/corporategovernance.

LogiCamms 2017 Annual Report10

11LogiCamms 2017 Annual Report

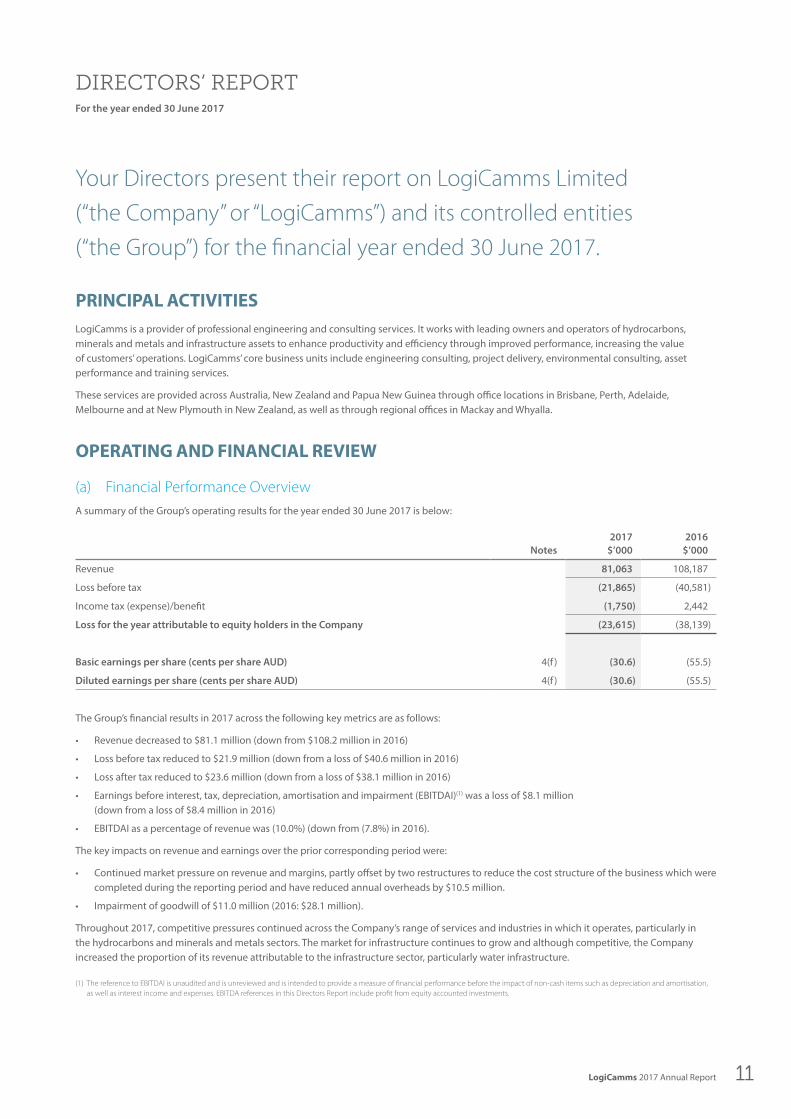

DIRECTORS’ REPORTFor the year ended 30 June 2017

Your Directors present their report on LogiCamms Limited

(“the Company” or “LogiCamms”) and its controlled entities

(“the Group”) for the financial year ended 30 June 2017.

PRINCIPAL ACTIVITIESLogiCamms is a provider of professional engineering and consulting services. It works with leading owners and operators of hydrocarbons, minerals and metals and infrastructure assets to enhance productivity and efficiency through improved performance, increasing the value of customers’ operations. LogiCamms’ core business units include engineering consulting, project delivery, environmental consulting, asset performance and training services.

These services are provided across Australia, New Zealand and Papua New Guinea through office locations in Brisbane, Perth, Adelaide, Melbourne and at New Plymouth in New Zealand, as well as through regional offices in Mackay and Whyalla.

OPERATING AND FINANCIAL REVIEW

(a) Financial Performance OverviewA summary of the Group’s operating results for the year ended 30 June 2017 is below:

Notes2017

$’0002016

$’000

Revenue 81,063 108,187

Loss before tax (21,865) (40,581)

Income tax (expense)/benefit (1,750) 2,442

Loss for the year attributable to equity holders in the Company (23,615) (38,139)

Basic earnings per share (cents per share AUD) 4(f ) (30.6) (55.5)

Diluted earnings per share (cents per share AUD) 4(f ) (30.6) (55.5)

The Group’s financial results in 2017 across the following key metrics are as follows:

• Revenue decreased to $81.1 million (down from $108.2 million in 2016)

• Loss before tax reduced to $21.9 million (down from a loss of $40.6 million in 2016)

• Loss after tax reduced to $23.6 million (down from a loss of $38.1 million in 2016)

• Earnings before interest, tax, depreciation, amortisation and impairment (EBITDAI)(1) was a loss of $8.1 million (down from a loss of $8.4 million in 2016)

• EBITDAI as a percentage of revenue was (10.0%) (down from (7.8%) in 2016).

The key impacts on revenue and earnings over the prior corresponding period were:

• Continued market pressure on revenue and margins, partly offset by two restructures to reduce the cost structure of the business which were completed during the reporting period and have reduced annual overheads by $10.5 million.

• Impairment of goodwill of $11.0 million (2016: $28.1 million).

Throughout 2017, competitive pressures continued across the Company’s range of services and industries in which it operates, particularly in the hydrocarbons and minerals and metals sectors. The market for infrastructure continues to grow and although competitive, the Company increased the proportion of its revenue attributable to the infrastructure sector, particularly water infrastructure.

(1) The reference to EBITDAI is unaudited and is unreviewed and is intended to provide a measure of financial performance before the impact of non-cash items such as depreciation and amortisation, as well as interest income and expenses. EBITDA references in this Directors Report include profit from equity accounted investments.

LogiCamms 2017 Annual Report12

DIRECTORS’ REPORTFor the year ended 30 June 2017

OPERATING AND FINANCIAL REVIEW (CONTINUED)

(a) Financial Performance Overview (continued)The Company also secured its first commercial revenue emanating from prior year investments in its technology and innovation business. The Company has secured an ongoing contract for the use of its proprietary Automated Infrastructure Design Engine (“AIDE”) with a blue-chip CSG Company. A number of other clients are evaluating or are currently in the proof of concept phase with a range of products with the commercial models being value-based rather than on a traditional reimbursable basis.

During the 2017 financial year, the Company delivered reduced revenue of $81.1 million, compared to $108.2 million in 2016. Our key focus for cost efficiencies, in line with the down turn in the market, was to reduce our overhead costs in areas that impact our ability to improve revenue performance. The Company achieved annualised labour cost savings of $8.8 million during the reporting period, at a one-off cash cost of $2.1 million.

In addition to the restructure, the low-margin Hunter Valley and Petromod businesses were closed as at 31 July 2017, freeing up over $1.5 million of working capital. A full review of overheads was also conducted, with further savings of $1.7 million identified across IT and communications, premises costs and other general and administrative expenses. The benefit of these savings will impact the 2018 financial year.

(b) Performance Across MarketsThe Company operates across three key markets, being hydrocarbons, minerals and metals and infrastructure. Hydrocarbons again was responsible for most of the work at 57% of revenue (up from 48% the previous year) which reflected continued work with upstream gas producers such as Santos, Origin Energy, Oil Search, BP and Vector.

Steady growth was achieved through the Company’s continued expansion of its services into the infrastructure sector. Notably, a significant volume of work was carried out for water utilities, including SA Water and Watercorp and agri-business for Viterra. Infrastructure now accounts for 16% of revenue, up from 13% in the 2016 financial year and is expected to grow substantially in the 2018 financial year.

Minerals and Metals revenue remained steady following the completion of the Roy Hill project in quarter three in the last financial year. Greater than 50% of the revenue has come from work carried out for iron ore clients such as Rio Tinto, Roy Hill, Fortescue and BHP.

The Company’s work in international markets was focused primarily around existing operations in New Zealand, as well as an increasing workflow out of Papua New Guinea. Ad hoc projects were conducted in Asia, predominately through Competency Training, our wholly owned Registered Training Organisation.

(c) Market Review and OutlookThe market for services to the hydrocarbons and minerals and metals markets continues to be highly competitive, however, within those markets, there remain significant opportunities for LogiCamms to apply its asset performance and engineering services to enable its customers to extract more value from existing assets.

The outlook in the hydrocarbons and minerals and metals sectors in Australia and New Zealand has seen marked improvement in recent months, driven by higher commodity prices, with requests for proposals and specialist capability by clients seeking to extract productivity improvements and undertake work that has been deferred from prior periods. In addition, greenfield and brownfield opportunities in infrastructure continue to be a core focus of the Company in the upcoming financial year.

As a result of the restructure process undertaken throughout the 2017 financial year, the Company is well positioned to deliver cost effective solutions to its customers as market conditions improve and clients are looking to invest in productivity improvements and sustaining capital and operating expenditure.

The key drivers of future revenue and earnings growth are:

• LogiCamms has over 50+ Master Services Agreements (“MSA’s”) secured with clients, providing a pipeline of sustainable work to support the core engineering disciplines

• Expanding our existing capabilities and strengths into non-traditional markets and regions including renewables, transport, defence, rail and agri-business, and geographically into NSW and Victoria

• Continued development and commercialisation of the Company’s innovative technology products including the Automated Infrastructure Design Engine (“AIDE”), drone-based survey and data analysis capability (“Ninox Robotics”) and in-field data capture and tracking tool (“StacksOn”)

• Leveraging value adding, higher margin opportunities generated by our collaborations and partnerships with asset owners and other service providers

• Utilising our end-to-end project capabilities, from environmental consulting, through engineering, procurement, commissioning, maintenance and training to generate synergistic opportunities to add value to our client’s operations

• Disciplined and focused approach to resource planning and overhead cost management

13LogiCamms 2017 Annual Report

OPERATING AND FINANCIAL REVIEW (CONTINUED)

(d) Working Capital ManagementThe group had negative operating cash flows of $9.2 million (2016: outflow of $8.3 million) primarily as a result of the continuation of poor market conditions. The Company has focused strongly on working capital management during the year. Debtors days outstanding and WIP aging have both reduced significantly. Outstanding debtors balances greater than 30 days have been reduced to less than $0.6 million (4.5%) at 30 June 2017.

During the year, the Company borrowed $4.0 million under its working capital facility with the National Australia Bank (“NAB”) and raised $4.5 million in equity. These funds were used for restructure costs and general working capital requirements, with $5.0 million remaining in cash at bank at 30 June 2017 and headroom available under the working capital facility was $1.0 million.

Subsequent to the end of the year, the limit on the Company’s working capital facility was increased by $4.0 million to provide additional headroom for general working capital requirements and to fund growth.

(e) Statement of Financial PositionThe Company’s total assets decreased to $51.0 million in 2017 (2016: $68.5 million) primarily from the impairment of goodwill. The end of year cash balance of $5.0 million was reduced from $6.6 million in 2016.

The net assets of the Group have reduced to $24.8 million at 30 June 2017 from $43.6 million at 30 June 2016. This decrease is primarily the result of the impairment to goodwill combined with continued operating losses.

The Company’s total liabilities increased to $26.2 million (2016: $24.9 million), due to borrowings under the working capital facility.

The Company has utilised $5.2 million of its current $12.5 million bank guarantee and bonding facilities (2016: utilised $7.4 million of $17.0 million).

Declared after end of year

No dividends were declared after the balance sheet date.

(f ) Key Strategic GoalsThe Company operates various business lines, including core engineering services (comprising design, onsite maintenance, installation and commissioning services) and specialist businesses, including Asset Performance (incorporating the Technology & Innovation business), Competency Training and Monarc Environmental.

The Company’s key strategic goals include:

• Building on the extensive portfolio of MSA’s to drive opportunities with new and existing clients

• Increasing revenue and margins by exploring new commercial models including collaborations and partnerships with asset owners and other service providers

• Leveraging its traditional expertise in control systems integration, automation and electrical installation and commissioning into the growth sectors of the economy, including renewables, transport, defence, rail and agri-business, and geographically into NSW and Victoria

• Accelerating the commercialisation of products developed by its technology and innovation business, increasing its share of revenue from value based services rather than traditional reimbursable-based contracts

• Becoming an employer of choice in the engineering consulting market by offering staff the right mix of challenging project work, personal and technical development opportunities, monetary and non-monetary benefits and a safe, social and inclusive place to work

The Company continues to refine its strategic direction under the theme of Clear Focus, concentrating on value proposition, markets, and alliance partners to maximise shareholder value through profitable expansion of the business in FY18 and beyond.

(g) Significant RisksThe Company is subject to a number of external, business, financial and operational risks. As LogiCamms is a service provider to the hydrocarbons, minerals and metals and infrastructure industries, any exposure that those industries have to risk factors will have some impact on LogiCamms’ business. Although LogiCamms has in place strategies to mitigate the impact of this, such as industry and service diversification, the volatility and uncertainty from such events may impact the nature and timing of work under contract.

LogiCamms is also subject to other external risks such as currency exchange movements, changes in demand for key commodities (including iron ore, oil and gas) and political risk. The majority of LogiCamms’ revenues are based in Australia and New Zealand and both revenue and associated costs are denominated in Australian and New Zealand dollars, and as such, foreign currency risks are somewhat reduced.

As a professional services business, the attraction, retention and investment in our people is critical to the success of the business. LogiCamms manages the risks associated with a people-based business through significant investment in training, attraction and retention strategies.

DIRECTORS’ REPORTFor the year ended 30 June 2017

LogiCamms 2017 Annual Report14

OPERATING AND FINANCIAL REVIEW (CONTINUED)

(g) Significant Risks (continued)The Company also faces risks in its relationship with customers. In order to optimise the delivery of services to customers, the Company has in place a robust risk management and governance framework that applies to the assessment, tender and delivery of customer projects.

LogiCamms is exposed to financial risks, which are partly inter-dependent on the external and business risks mentioned above. Significant investment has occurred in the development of risk and financial management systems and processes available to the business. Further, LogiCamms manages working capital closely to ensure minimal volatility in results and the appropriate delivery of services within commercial agreed terms.

In relation to the operational risks to the business, LogiCamms has a strong focus on ensuring that work is carried out on terms that satisfy the Company’s internal policies relevant to appropriate return and risk. LogiCamms has a focus on long term sustainable projects and relationships and applies margins to work accordingly.

The Company also has detailed procedures in place to ensure that the Company is staffed efficiently and that its people are working at a level of business that balances the goal of strong margins with that of ensuring the Company’s people are working in an environment that encourages sustainable personal development and growth opportunities.

The Company maintains a register of key risks and has in place crisis management and disaster recovery plans.

INFORMATION ON DIRECTORSThe Directors in office at any time during or since the end of the year were:

Mr Peter Watson Independent Non-Executive Director and Chairman

Appointed 2 June 2011. Year last re-elected: 2016.

Experience Peter Watson has 30 years of international experience in engineering, construction and services industries. As former Chief Executive Officer of Global Services Group, Transfield Services (ASX: TSE) from 1999 to 2009 (now known as Broadspectrum), Peter stewarded the company through its listing in 2001 and led its transformation from a local operator to a global business. Since 2009 Peter has served on a number of boards including Save the Children Pty Ltd, AssetCo Pty Ltd, Zinfra Pty Ltd, and Ross River Solar Farm Pty Ltd. Peter is a member of the AICD, Institute of Engineers Australia, and is a fellow of ATSE.

Peter is a member of the Nomination and Remuneration Committee, and a member of the Audit and Risk Committee.

Current directorships held in other listed entities

Watpac Limited

Mr Peter Wall Independent Non-Executive Director

Appointed 8 October 2007. Year last re-elected: 2015.

Experience Peter has extensive management expertise, including a focus on human resources and corporate governance. Peter had a long tenure at S. Smith & Son (The Yalumba Wine Company); is a former board member of SA WorkCover Corporation and Chairman of the South Australian Vocational Employment Education & Training Board. Peter is Chair of the Nomination & Remuneration Committee, and Chair of the Audit and Risk Committee.

Current directorships held in other listed entities

None

Mr Richard Robinson Independent Non-Executive Director

Appointed 26 May 2015. Year last re-elected: 2015

Experience Richard Robinson has nearly 40 years’ experience in the Oil & Gas industry in Australia and Papua New Guinea. Richard’s experience covers project, operations and commercial management in the upstream, downstream and associated service sectors. Richard held senior roles for more than 10 years at Oil Search Limited, retiring from his role as Executive General Manager in 2013. He has since held a number of Non-Executive Director and consulting roles within the Oil & Gas, engineering and construction sectors.

Richard is a member of the Nomination & Remuneration Committee, and a member of the Audit & Risk Committee.

Current directorships held in other listed entities

Chairman of Kina Petroleum Limited having been appointed as a Non-Executive director in 2013.

DIRECTORS’ REPORTFor the year ended 30 June 2017

15LogiCamms 2017 Annual Report

DIRECTORS’ REPORTFor the year ended 30 June 2017

INFORMATION ON DIRECTORS (CONTINUED)

Mr Steve Banning Managing Director

Reappointed 2 March 2015. Resigned 22 February 2017.

Experience Steve Banning has extensive experience across the resources and energy industry. Prior to his role as Managing Director at LogiCamms, he was Managing Director of Epic Energy from 2007 until 2011. In his role as MD of Epic Energy, Steve led the business through a period of significant growth. Steve’s other roles have included General Manager Commercial of Epic Energy, Group Manager of Duke Energy and various roles within ExxonMobil.

Steve has a Bachelor of Science (Honours).

Steve Banning was re-appointed as Managing Director on 2 March 2015.

Current directorships held in other listed entities

None

INFORMATION ON COMPANY SECRETARYThe role of Company Secretary was held by two individuals throughout the financial year ended 30 June 2017.

Paul Bowker was appointed to the position of Company Secretary 2011 and also held the position of Director - Corporate Development until his resignation from the company and as Company Secretary on 17 February 2017.

David Shaw was appointed to the position of Company Secretary on 17 February 2017 and also holds the position of Legal Counsel at LogiCamms, a role in which he has served since joining LogiCamms in 2012. David holds a Bachelor of Laws and has a legal and compliance background gained from working in the corporate sector in Australia, including with Mills Oakley Lawyers and Ebsworth Lawyers.

MEETINGS OF DIRECTORSThe number of Directors’ meetings (including meetings of committees of Directors) and number of meetings attended by each of the Directors of the Company during the financial year are:

Director Board MeetingsAudit & Risk

Committee Meetings

Nomination and Remuneration

Committee MeetingsProject

Committee Meetings

A B A B A B A B

Peter Watson 19 19 4 5 5 5 NA NA

Richard Robinson 16 19 5 5 4 5 5 5

Peter Wall 19 19 5 5 5 5 NA NA

Steve Banning 11 11 3 3 3 3 2 3

A = Number of meetings attended B = Number of meetings held during the time the Director was a member of the Board or Committee

LogiCamms 2017 Annual Report16

DIRECTORS’ REPORTFor the year ended 30 June 2017

REMUNERATION REPORT – AUDITEDThe Directors present the LogiCamms 2017 remuneration report, outlining key aspects of our remuneration policy and framework, and remuneration awarded this year. This Remuneration Report outlines the Key Management Personnel (KMP) remuneration arrangements of the Group in accordance with the requirements of the Corporations Act 2001 and its Regulations. For the purpose of this report KMP of the Group are defined as those persons having authority and responsibility for planning, directing and controlling the major activities of the Group, directly or indirectly, including any Director (whether executive or otherwise).

The report is structured as follows:

(a) Overview of the Company’s approach to executive reward

(b) Governance of remuneration arrangements

(c) Elements of remuneration

(d) Consequences of performance on shareholder wealth

(e) Remuneration expenses for executive KMP

(f ) Contractual arrangements for executive KMP

(g) Non-executive director arrangements

(a) Overview of the Company’s approach to executive rewardThe Board has adopted a remuneration policy that takes into account the current size and nature of the Company’s operations.

Remuneration of KMPs is set at levels to reflect market conditions and encourage the continued services of KMP’s including by benchmarking KMP remuneration to determine where roles are currently positioned, reviewing base salary, short-term incentives and long-term incentives.

The Group’s remuneration strategy recognises and rewards performance in a way that is consistent with general practices in the markets in which the Group operates. The Group’s remuneration philosophy is focused on the following key principles:

• Alignment to sustainable long-term value creation

• Assist the attraction and retention of highly skilled employees

• Be competitive within the global markets in which the Group operates

• Alignment is best achieved through significant levels of equity ownership

• Provide high rewards for true outperformance

• Simple and transparent remuneration framework

• Consistent remuneration framework across the organisation

• Strategically align talent and succession planning for future growth

This report specifically sets out remuneration information for the key people who can directly influence the long term strategic direction of the Company and had the authority for planning, directing and controlling the affairs of the Group during the financial year ended 30 June 2017. They include the Chief Executive Officer and other key executives and Non-Executive Directors, of the Company as set out below:

Non-executive and executive Directors (see page 9 for details about each Director)

Name Position

Peter Watson Chairman

Peter Wall Non-executive Director

Richard Robinson Non-executive Director

Steve Banning Managing Director (until 22 February 2017)

17LogiCamms 2017 Annual Report

REMUNERATION REPORT – AUDITED (CONTINUED)

(a) Overview of the Company’s approach to executive reward (continued)

Other key management personnel

Name Position

Flora Furness Director – Deliver (until 22 February 2017), Chief Executive Officer (from 22 February 2017)

Dan Drewe Chief Financial Officer (from 09 June 2017)

Iulius Mincu Director – Hydrocarbons (until 17 March 2017) Director – Technology, Innovation and Asset Performance (from 17 March 2017)

Steve Banning Managing Director (until 22 February 2017)

Paul Bowker Director – Corporate Development (until 17 February 2017)

Craig White Interim Chief Financial Officer (from 17 February 2017 until 09 June 2017)

Except as noted, the named persons held their current position for the whole of the financial year and to the date of this report.

(b) Remuneration governanceTo determine the remuneration of its KMP the Company has a Nomination and Remuneration Committee. The Committee makes recommendations to the Board in relation to the remuneration of KMP, including the fixed and at risk components of remuneration. Based on the information and recommendations provided by the Committee, the Board applies its discretion to determine remuneration, including any changes to fixed components of KMP remuneration as well as any awards under the STI and LTI Plans. The Committee assists the Board in establishing human resources and compensation policies and practices including the specific remuneration (including base pay, incentive payments, bonuses, equity awards, superannuation, retirement rights, termination payments and services contracts) of the Chief Executive Officer and other KMP. The proceedings of each Committee meeting are reported directly to the Board. The Chairman of the Committee shall be a Non-Executive Director, with all other members being members of the Board. The Chief Executive Officer is invited to attend Committee meetings.

The primary objective of LogiCamms’ executive remuneration strategy is creating a framework that supports sustainable growth over the long term, recognising that this is in the interest of all stakeholders. This framework seeks to reward, retain, and motivate senior executives in a manner aligned with shareholders.

(c) Elements of remunerationRemuneration and other terms of employment for the Chief Executive Officer and other executive KMP are formalised in Executive Service Agreements and incentive plans. The total remuneration packages for these KMP contain:

• A fixed component – Base salary including superannuation. This is expressed as a specific amount that the executive may take in a form agreed with the Company and is determined based on market reference, the scope and nature of the individual’s role, their performance and experience.

• At-risk components – The Board considers that the financial and operational performance and prospects of the Company are strongly linked to creating shareholder wealth. Accordingly, the Board has put in place at-risk components to remuneration based on success in delivering on pre-defined targets. For 2017, at-risk components were in the form of:

– Short Term Incentive (STI) – payable in cash and ordinary shares. Outcomes based on LogiCamms financial and operational performance over the 2017 financial period, in addition to individual performance measures; and

– Long Term Incentives (LTI) – payable through the issue of Performance Rights and Performance Options. These LTI instruments are issued for the purposes of aligning KMP interests with those of shareholders by rewarding long term sustainable shareholder value creation. LTI outcomes for 2017 were based on strategic performance measures.

(i) Fixed annual remuneration (FR)

The fixed remuneration component of salaries includes a base salary and superannuation. Fixed remuneration may be allocated at the executive’s discretion to cash, superannuation (subject to legislative minimum), motor vehicles and certain other benefits. The fixed remuneration component is determined based on the scope and nature of the individual’s role, their performance and experience.

DIRECTORS’ REPORTFor the year ended 30 June 2017

LogiCamms 2017 Annual Report18

REMUNERATION REPORT – AUDITED (CONTINUED)

(c) Elements of remuneration (continued)

(ii) Short-term incentives

Under the terms of the STI for 2017, each participant had an annual target STI award based on a percentage of base salary for the year. Payment of the individual’s target STI was dependent on performance against the key metrics set out in the table below.

For financial year 2017, KMP had a maximum STI opportunity ranging from 20% to 50% of their fixed remuneration where targets are met. However, if the threshold performance for a measure is not met, the payment may be reduced.

The STI payment is subject to the participant being employed with the Company at the time the STI is due to be paid.

STI awards are determined after a review of performance against the key performance drivers by the Board at the end of the financial year.

Award criteria for STI

The award criteria for the STI are based on achievement against the Performance Objectives for the Company for the 2017 financial year. The table below sets out the criteria and performance against those criteria:

FY17 Scorecard Weight Position

Financial 50% Revenue, EBITDA, Capital and Cash Management

Operational 50% Reimbursability (proportion of billable hours), Staff Turnover, Training and Diversity

The Nomination and Remuneration Committee have reviewed the performance of the KMP against the above criteria. Based on the performance of the Group no STI was awarded.

The award criteria for the 2018 STI are based on achievement against the Performance Objectives for the Company for the 2018 financial year. Awards under the 2018 STI are to be paid in the form of cash and ordinary shares in a combination to be determined by the Board. The table below sets out the award criteria.

FY18 Scorecard Weight Position

Financial – EBITDAI 50% Earning Before Interest, Taxes, Depreciation, Amortisation and Impairment

Financial – OCAT 30% Operating Cashflow After Tax

Operational 20% Health, Safety, Environment and Quality

The Board has discretion to make a determination on individual performance of a KMP and apply such determination as a modifier to increase or decrease the STI payable.

(iii) Long-term incentives

For the 2017 financial year, each of the executive KMP listed in (a) above was eligible to participate in the LTI Plan, awards for which can be made in the form of Performance Rights or Performance Options.

Award criteria for LTI

Due to the change in Key Management Personnel during the year and the financial performance of the Group, no LTI award criteria were set and no LTI was awarded for the financial year ended 30 June 2017.

DIRECTORS’ REPORTFor the year ended 30 June 2017

19LogiCamms 2017 Annual Report

DIRECTORS’ REPORTFor the year ended 30 June 2017

REMUNERATION REPORT – AUDITED (CONTINUED)

(c) Elements of remuneration (continued)

Proportions of fixed and at risk remuneration

The table below sets out LogiCamms’ target mix of fixed and at risk (STI & LTI) components for each of the executive KMP for 2017 as a percentage of total remuneration:

Name Title Fixed Remuneration

STI LTI

Flora Furness Chief Executive Officer 50% 20% 30%

Dan Drewe Chief Financial Officer 100% – –

Iulius Mincu Director – Technology, Innovation and Asset Performance

62.5% 18.75% 18.75%

Craig White Interim Chief Financial Officer 100% – –

(d) Consequences of performance on shareholder wealthIn considering the Group’s performance and benefits for shareholder wealth, the Nomination and Remuneration Committee has had regard to a number of factors including profit (as determined under Australian Accounting Standards), dividends, earnings per share (EPS), return on equity and the performance of the share price.

The Nomination and Remuneration Committee has regard to the following indices in respect of the 2017 financial year and the previous four financial years.

2017 2016 2015 2014 2013

Profit/(loss) for the year attributable to owners of the Company ($’000)

(23,615) (38,139) 8,336 5,006 11,096

EBITDAI ($'000) (8,133) (8,409) 12,057 6,724 14,060

Dividends payments ($'000) – 2,410 4,884 4,545 6,307

Basic earnings per share (cents) (31) (56) 12 7 17

Increase/(decrease) in share price ($) (0.22) (0.31) (0.13) (0.48) 0.21

Return on equity % (95) (87) 10 6 14

Earnings before interest, tax, depreciation, amortisation and impairment (EBITDAI) was a loss of $8.1 million, down from a loss of $8.4 million in 2016.

EBITDAI is considered one of the key financial performance targets in setting the STI as EBITDAI is a measure of free cash flow excluding the impact of financing, non-cash accounting adjustments and tax treatments. It is considered to be a measure of the operating performance of the business that is most influenced by management decisions. EBITDAI amounts for 2013 to 2017 have been calculated by adjusting net profit calculated in accordance with Australian Accounting Standards (AASBs) and adding back net finance expenses, tax expense, depreciation, amortisation and impairment charges.

The overall level of executive KMP compensation takes into account these and other factors in assessing the performance of the Group and executive KMP over a number of years. When comparing financial year 2017 to financial year 2016, the Group continued to experience significant EBITDAI losses. The Nomination and Remuneration Committee has determined that no STI be awarded under the 2017 STI plan.

LogiCamms 2017 Annual Report20

DIRECTORS’ REPORTFor the year ended 30 June 2017

REMUNERATION REPORT – AUDITED (CONTINUED)

(e) Remuneration expenses for executive KMPDetails of the nature and amount of each major element of remuneration of each of the Key Management Personnel are:

Fixe

d

rem

uner

atio

nVa

riab

le

rem

uner

atio

nPr

opor

tion

of

rem

uner

atio

n pe

rfor

man

ce

rela

ted %

Valu

e of

op

tions

and

ri

ghts

as

prop

ortio

n of

re

mun

erat

ion %

Nam

eYe

ar

Cash

sa

lary

$

Non

-m

onet

ary

bene

fits $

Post

- em

ploy

men

t be

nefit

s Te

rmin

atio

n be

nefit

s %

Opt

ions

an

d ri

ghts

$To

tal $

Non

-Exe

cutiv

e D

irect

ors

Pete

r Wat

son

2017

140,

000

––

––

140,

000

––

20

1614

0,00

0–

––

10,9

5515

0,95

5–

7.3%

Pete

r Wal

l20

1780

,000

––

––

80,0

00–

–

20

1680

,323

––

––

80,3

23–

–

Rich

ard

Robi

nson

2017

75,0

00–

––

10,4

2185

,421

–12

.2%

20

1675

,000

––

––

75,0

00–

–

Gile

s Eve

rist (

resig

ned

5 D

ecem

ber 2

015)

2016

42,5

00–

––

–42

,500

––

Tota

l Non

-Exe

cutiv

e D

irect

or re

mun

erat

ion

2017

295,

000

––

–10

,421

305,

421

20

1633

7,82

3–

––

10,9

5534

8,77

8

Exec

utiv

e D

irect

ors

Stev

e Ba

nnin

g (re

tired

22

Febr

uary

201

7)20

1739

8,62

63,

900

22,6

9290

,000

(1,3

92)

513,

826

–(0

.3%

)

20

1650

4,59

2–

36,2

48–

164,

309

705,

149

23.3

%23

.3%

Exec

utiv

es

Flor

a Fu

rnes

s (a

ppoi

nted

22

Febr

uary

201

7)20

1735

6,66

16,

500

27,2

32–

90,0

0048

0,39

318

.7%

18.7

%

20

1631

8,90

1–

22,0

00–

36,0

0037

6,90

19.

6%9.

6%

Paul

Bow

ker (

resi

gned

17

Febr

uary

201

7)20

1720

4,23

03,

900

21,5

7717

0,19

2(2

9,25

0)37

0,64

9(7

.9%

)(7

.9%

)

20

1630

7,63

0–

30,7

84–

45,7

5038

4,16

411

.9%

11.9

%

Iuliu

s M

incu

2017

315,

946

2,31

030

,015

–35

,000

383,

271

9.1%

9.1%

20

1631

9,63

5–

30,3

65–

35,0

0038

5,00

09.

1%9.

1%

Crai

g W

hite

(app

oint

ed 1

7 Fe

brua

ry 2

017,

re

sign

ed 0

9 Ju

ne 2

017)

2017

134,

116

2,60

012

,113

–-

148,

829

––

Dan

Dre

we

(app

oint

ed 0

9 Ju

ne 2

017)

2017

9,23

0–

877

––

10,1

07–

–

Dav

id H

arris

(res

igne

d 1

Apr

il 20

16)

2016

235,

383

–15

,773

166,

460

–41

7,61

6–

–

Tota

l exe

cutiv

e di

rect

ors

and

exec

utiv

es20

171,

418,

809

19,2

1011

4,50

626

0,19

294

,358

1,90

7,07

5

2016

1,68

6,14

1–

135,

170

166,

460

281,

059

2,26

8,83

0

Tota

l KM

P Re

mun

erat

ion

2017

1,71

3,80

919

,210

114,

506

260,

192

104,

779

2,21

2,49

6

2016

2,02

3,96

4–

135,

170

166,

460

292,

014

2,61

7,60

8

21LogiCamms 2017 Annual Report

REMUNERATION REPORT – AUDITED (CONTINUED)

(e) Remuneration expenses for executive KMP (continued)

Equity instruments

KMP disclosed below were issued Performance Rights as detailed below that impact on compensation in the 2017 or subsequent reporting periods. The service or performance criteria used to determine the number of Performance Rights issued is set out earlier in this report in the discussion of the Company’s LTI Plan.

No terms of equity-settled share-based payment transactions have been altered or modified by the issuing entity since the date of grant. All Performance Rights were provided at no cost to the recipients. Performance Rights expire on the earlier of their expiry date or termination of the individual’s employment.

Analysis of incentives included in remuneration

Details of the vesting profile of the Performance Rights granted to KMP and impacting on compensation in the 2017 reporting period as at the date of this report, or subsequent reporting periods that are still outstanding are detailed below.

Name Instrument NumberGrant Date

Fair Value per

instrument at grant date

Vested in Year

Forfeited in Year

Number at reporting

date

Financial Years

in which Grant Vests

Steve Banning Performance Rights 166,667 2-Mar-15 $0.80 50% 50% – 2017-8

Performance Rights 69,444 26-Aug-15 $0.60 – 100% – 2017

Performance Rights 346,154 28-Sep-16 $0.39 – 100% – 2017

Performance Rights 346,154 28-Sep-16 $0.39 – 100% – 2018

Paul Bowker Performance Rights 48,750 26-Aug-15 $0.60 – 100% – 2017

Performance Rights 138,462 28-Sep-16 $0.39 – 100% – 2017

Performance Rights 138,462 28-Sep-16 $0.39 – 100% 2018

Flora Furness Performance Rights 138,462 28-Sep-16 $0.39 100% – – 2017

Performance Rights 138,462 28-Sep-16 $0.39 – – 138,462 2018

Iulius Mincu Performance Rights 134,615 28-Sep-16 $0.39 100% – – 2017

Performance Rights 134,615 28-Sep-16 $0.39 – – 134,615 2018

Richard Robinson Performance Rights 16,667 24-Nov-16 $0.44 100% – – 2017

Performance Rights 16,666 24-Nov-16 $0.44 – – 16,666 2018

The performance period for rights issued 28 September 2016, shown above, under the 2016 LTI awards is the year from 1 July 2015 to 30 June 2016. The Performance Rights vest into shares for no further consideration on a 1 for 1 basis subject to tenure at the time of vesting. The form of the share based payments for Steve Banning for 2016 were subject to approval by resolution of the shareholders at the 2016 AGM. The resolution was not passed and the shares were forfeited.

Other terms

Performance Rights granted under the LTI Plan carry no voting or dividend entitlements. Currently, based on the number of Performance Rights issued and held pursuant to the LTI Plan, should all of these securities convert to shares they would represent 0.2% of the Company’s issued share capital.

Exercise of Options or Performance Rights

During the period 138,462 shares were issued to Flora Furness with a fair value at grant date of $0.39, 16,667 shares were issued to Richard Robinson with a fair value at grant date of $0.44 and 83,334 shares were issued to Steve Banning with a fair value at grant date of $0.80. All shares issued were on the conversion of Performance Rights granted in the current or prior years as compensation. No exercise price was payable on the conversion of the Performance Rights. The Performance Rights were all STI awards in respect of the 2016 financial year.

DIRECTORS’ REPORTFor the year ended 30 June 2017

LogiCamms 2017 Annual Report22

REMUNERATION REPORT – AUDITED (CONTINUED)

(e) Remuneration expenses for executive KMP (continued)

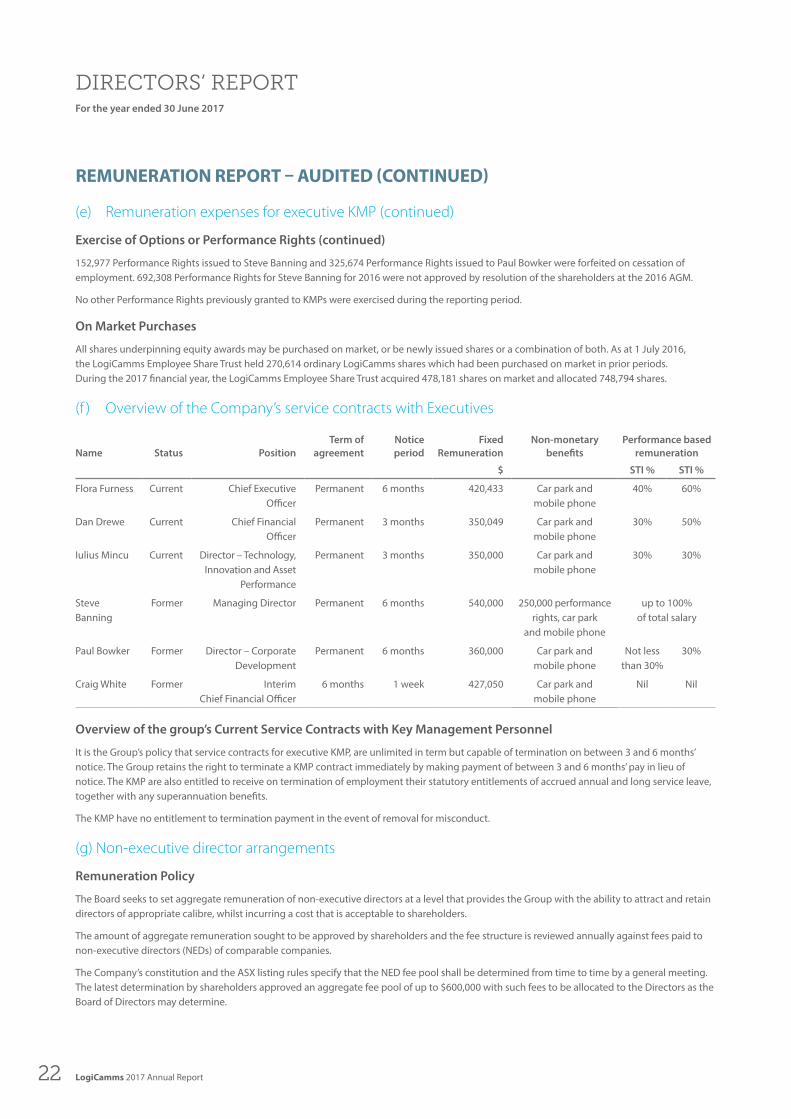

Exercise of Options or Performance Rights (continued)

152,977 Performance Rights issued to Steve Banning and 325,674 Performance Rights issued to Paul Bowker were forfeited on cessation of employment. 692,308 Performance Rights for Steve Banning for 2016 were not approved by resolution of the shareholders at the 2016 AGM.

No other Performance Rights previously granted to KMPs were exercised during the reporting period.

On Market Purchases

All shares underpinning equity awards may be purchased on market, or be newly issued shares or a combination of both. As at 1 July 2016, the LogiCamms Employee Share Trust held 270,614 ordinary LogiCamms shares which had been purchased on market in prior periods. During the 2017 financial year, the LogiCamms Employee Share Trust acquired 478,181 shares on market and allocated 748,794 shares.

(f ) Overview of the Company’s service contracts with Executives

Name Status PositionTerm of

agreementNotice period

Fixed Remuneration

Non-monetary benefits

Performance based remuneration

$ STI % STI %

Flora Furness Current Chief Executive Officer

Permanent 6 months 420,433 Car park and mobile phone

40% 60%

Dan Drewe Current Chief Financial Officer

Permanent 3 months 350,049 Car park and mobile phone

30% 50%

Iulius Mincu Current Director – Technology, Innovation and Asset

Performance

Permanent 3 months 350,000 Car park and mobile phone

30% 30%

Steve Banning

Former Managing Director Permanent 6 months 540,000 250,000 performance rights, car park

and mobile phone

up to 100% of total salary

Paul Bowker Former Director – Corporate Development

Permanent 6 months 360,000 Car park and mobile phone

Not less than 30%

30%

Craig White Former Interim Chief Financial Officer

6 months 1 week 427,050 Car park and mobile phone

Nil Nil

Overview of the group’s Current Service Contracts with Key Management Personnel

It is the Group’s policy that service contracts for executive KMP, are unlimited in term but capable of termination on between 3 and 6 months’ notice. The Group retains the right to terminate a KMP contract immediately by making payment of between 3 and 6 months’ pay in lieu of notice. The KMP are also entitled to receive on termination of employment their statutory entitlements of accrued annual and long service leave, together with any superannuation benefits.

The KMP have no entitlement to termination payment in the event of removal for misconduct.

(g) Non-executive director arrangements

Remuneration Policy

The Board seeks to set aggregate remuneration of non-executive directors at a level that provides the Group with the ability to attract and retain directors of appropriate calibre, whilst incurring a cost that is acceptable to shareholders.

The amount of aggregate remuneration sought to be approved by shareholders and the fee structure is reviewed annually against fees paid to non-executive directors (NEDs) of comparable companies.

The Company’s constitution and the ASX listing rules specify that the NED fee pool shall be determined from time to time by a general meeting. The latest determination by shareholders approved an aggregate fee pool of up to $600,000 with such fees to be allocated to the Directors as the Board of Directors may determine.

DIRECTORS’ REPORTFor the year ended 30 June 2017

23LogiCamms 2017 Annual Report

REMUNERATION REPORT – AUDITED (CONTINUED)

(g) Non-executive director arrangements (continued)

Structure

The remuneration of NEDs consists of directors’ fees and committee fees. NEDs do not receive retirement benefits.

Mr Richard Robinson received a base fee of $75,000 inclusive of superannuation for being a director of the Group. The Board Chairman, Mr Peter Watson, received a base fee of $140,000 inclusive of superannuation for the period. Mr Peter Wall received a base fee of $80,323 inclusive of superannuation due to an additional fee being payable as chair of the Audit Committee and Nomination and Remuneration Committee.

An additional fee may be payable for a Director (except for the Board Chairman) who is a chair of a Board committee. The payment of additional fees for serving on a committee recognises the additional time commitment required by NEDs who serve on sub-committees. NEDs do not participate in the Company’s STI or LTI plans.

Movements in shares

The movement during the reporting year in the number of ordinary shares in the Company held directly, indirectly or beneficially, by KMP, is as follows:

2017 Name

Balance at the start of the

year

Received on vesting of

rights

Other changes during the

year

Balance at the end of the

year

Ordinary shares

Peter Watson 811,029 66,666 39,474 917,169

Peter Wall 200,001 – 39,474 239,475

Richard Robinson – 33,334 – 33,334

Steve Banning (1) 175,827 83,333 39,474 298,634

Paul Bowker (2) 327,876 – – 327,876

Flora Furness – 138,462 – 138,462

Iulius Mincu – 134,615 – 134,615

Craig White – – – –

Dan Drewe – – – –

(1) Steve Banning retired during the period, balance is representative at 28 February 2017. (2) Paul Bowker left during the period, balance is representative at 17 February 2017.

Other changes during the period represents shares acquired by Directors as part of the Share Purchase Plan.

Directors interests

The relevant interest of each Director in the Shares and Performance Rights issued by the Company at the date of this report is as follows:

DirectorOrdinary

SharesPerfromance

Rights

Richard Robinson 33,334 16,666

Peter Wall 239,475 –

Peter Watson 917,169 –

Options and rights granted to Directors and Officers of the Company

During or since the end of the financial year, the Company granted no additional rights over unissued ordinary shares in the Company to the Key Management Personnel.

The Performance Rights require the holder to remain employed by the Company prior to vesting. Performance Rights over unissued ordinary shares in the Company granted in the previous financial year were detailed in the previous Annual Report.

Unissued shares under options

At the date of this report there are no other unissued ordinary shares of the Company under option.

DIRECTORS’ REPORTFor the year ended 30 June 2017

LogiCamms 2017 Annual Report24

DIRECTORS’ REPORTFor the year ended 30 June 2017

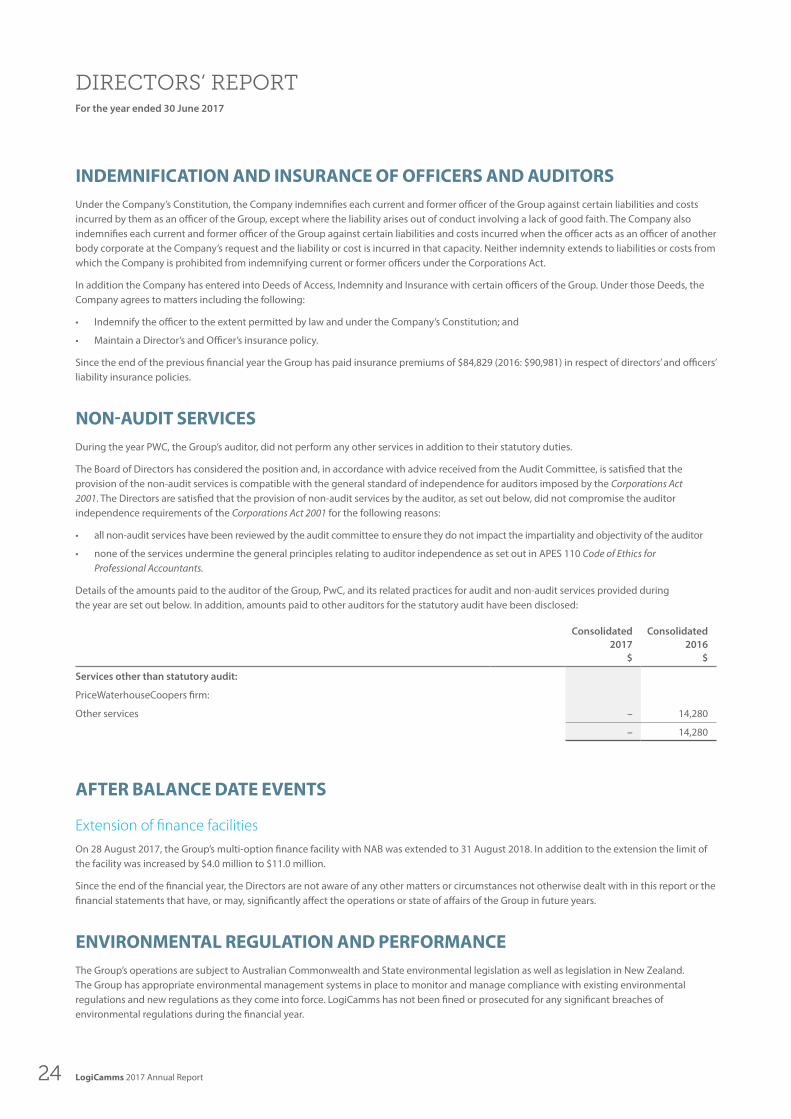

INDEMNIFICATION AND INSURANCE OF OFFICERS AND AUDITORSUnder the Company’s Constitution, the Company indemnifies each current and former officer of the Group against certain liabilities and costs incurred by them as an officer of the Group, except where the liability arises out of conduct involving a lack of good faith. The Company also indemnifies each current and former officer of the Group against certain liabilities and costs incurred when the officer acts as an officer of another body corporate at the Company’s request and the liability or cost is incurred in that capacity. Neither indemnity extends to liabilities or costs from which the Company is prohibited from indemnifying current or former officers under the Corporations Act.

In addition the Company has entered into Deeds of Access, Indemnity and Insurance with certain officers of the Group. Under those Deeds, the Company agrees to matters including the following:

• Indemnify the officer to the extent permitted by law and under the Company’s Constitution; and

• Maintain a Director’s and Officer’s insurance policy.

Since the end of the previous financial year the Group has paid insurance premiums of $84,829 (2016: $90,981) in respect of directors’ and officers’ liability insurance policies.

NON-AUDIT SERVICESDuring the year PWC, the Group’s auditor, did not perform any other services in addition to their statutory duties.

The Board of Directors has considered the position and, in accordance with advice received from the Audit Committee, is satisfied that the provision of the non-audit services is compatible with the general standard of independence for auditors imposed by the Corporations Act 2001. The Directors are satisfied that the provision of non-audit services by the auditor, as set out below, did not compromise the auditor independence requirements of the Corporations Act 2001 for the following reasons:

• all non-audit services have been reviewed by the audit committee to ensure they do not impact the impartiality and objectivity of the auditor

• none of the services undermine the general principles relating to auditor independence as set out in APES 110 Code of Ethics for Professional Accountants.

Details of the amounts paid to the auditor of the Group, PwC, and its related practices for audit and non-audit services provided during the year are set out below. In addition, amounts paid to other auditors for the statutory audit have been disclosed:

Consolidated 2017

$

Consolidated 2016

$

Services other than statutory audit:

PriceWaterhouseCoopers firm:

Other services – 14,280

– 14,280

AFTER BALANCE DATE EVENTS

Extension of finance facilitiesOn 28 August 2017, the Group’s multi-option finance facility with NAB was extended to 31 August 2018. In addition to the extension the limit of the facility was increased by $4.0 million to $11.0 million.

Since the end of the financial year, the Directors are not aware of any other matters or circumstances not otherwise dealt with in this report or the financial statements that have, or may, significantly affect the operations or state of affairs of the Group in future years.

ENVIRONMENTAL REGULATION AND PERFORMANCEThe Group’s operations are subject to Australian Commonwealth and State environmental legislation as well as legislation in New Zealand. The Group has appropriate environmental management systems in place to monitor and manage compliance with existing environmental regulations and new regulations as they come into force. LogiCamms has not been fined or prosecuted for any significant breaches of environmental regulations during the financial year.

25LogiCamms 2017 Annual Report

PROCEEDINGS ON BEHALF OF THE COMPANYNo person has applied to the Court under section 237 of the Corporations Act 2001 for leave to bring proceedings on behalf of the Company, or to intervene in any proceedings to which the Company is a party, for the purpose of taking responsibility on behalf of the Company for all or part of those proceedings.

No proceedings have been brought or intervened in on behalf of the Company with leave of the Court under section 237 of the Corporations Act 2001.

AUDITOR’S INDEPENDENCE DECLARATIONA copy of the auditor’s independence declaration as required under section 307C of the Corporations Act 2001 is set out on page 71.

ROUNDING OF AMOUNTSThe Company is of a kind referred to in ASIC Corporations (Rounding in Financial/Directors’ Reports) Instrument 2016/191 dated 24 March 2016. Amounts in the Directors’ report have been rounded off in accordance with that Legislative Instrument to the nearest thousand dollars, or in certain cases, to the nearest dollar.

This report is made in accordance with a resolution of Directors.

Peter Watson Chairman

Brisbane 30 August 2017

DIRECTORS’ REPORTFor the year ended 30 June 2017

LogiCamms 2017 Annual Report26

27LogiCamms 2017 Annual Report

CONSOLIDATED STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME For the year ended 30 June 2017

Notes2017

$’0002016

$’000

Revenue 4(a) 81,063 108,187

Cost of sales (52,624) (73,520)

Gross profit 28,439 34,667

Other income 4(b) 323 2,001

Business development expenses (6,179) (7,370)

Other expenses (34,020) (37,476)

(11,437) (8,178)

Onerous lease benefit/(expense) 11(b) 668 (4,200)

Results from operating activities (10,769) (12,378)

Finance income 4(c) 4 81

Finance expenses 4(d) (85) (151)

Net finance income (81) (70)

Revaluation / share of net loss of equity accounted investees 9(b) (15) (33)

Impairment charge (11,000) (28,100)

(11,015) (28,133)

Loss before income tax (21,865) (40,581)

Income tax benefit/(expense) 4(e) (1,750) 2,442

Loss for the year attributable to owners of the Company (23,615) (38,139)

Other comprehensive income

Items that may be reclassified to profit or loss

Foreign currency translation differences 325 1,434

Other (26) –

Other comprehensive income for the year, net of tax 299 1,434

Total comprehensive loss for the year attributable to owners of the Company (23,316) (36,705)

Earnings per share

Basic earnings per share (cents per share AUD) 4(f ) (30.6) (55.5)

Diluted earnings per share (cents per share AUD) 4(f ) (30.6) (55.5)

The above Consolidated statement of profit or loss and other comprehensive income should be read in conjunction with the accompanying notes.

LogiCamms 2017 Annual Report28

CONSOLIDATED STATEMENT OF FINANCIAL POSITIONFor the year ended 30 June 2017

Notes2017

$’0002016

$’000

ASSETS

Cash and cash equivalents 5(a) 4,983 6,637

Trade and other receivables 5(b) 18,245 20,832

Current tax asset 4(e) – 508

Total current assets 23,228 27,977

Investments in equity accounted investees 9(b) – 15

Property, plant and equipment 6(a) 2,877 1,851

Deferred tax assets 4(e) 3,328 4,713

Intangible assets 6(b) 21,537 33,801

Other non-current assets – 125

Total non-current assets 27,742 40,505

Total assets 50,970 68,482

LIABILITIES

Trade and other payables 5(c) 7,576 9,471

Borrowings 5(g) 4,000 –

Current tax liability 4(e) 122 –

Employee benefits 5(e) 3,591 4,499

Provisions 5(f ) 3,839 4,807

Deferred income 5(d) 2,242 681

Total current liabilities 21,370 19,458

Trade and other payables 5(c) 1,210 961

Employee benefits 5(e) 839 878

Provisions 5(f ) 2,779 3,560

Total non-current liabilities 4,828 5,399

Total liabilities 26,198 24,857

Net assets 24,772 43,625

EQUITY

Share capital 57,619 53,163

Reserves 2,760 2,435

Accumulated losses (35,607) (11,973)

Total equity attributable to owners of the Company 24,772 43,625