© blaqwell, inc. 2007 what you should know about the legal business summer, 2007

TRANSCRIPT

© Blaqwell, Inc. 2007

What You Should Know About the Legal Business

Summer, 2007

2

Introduction

Client needs and the modern law firm

Non-economic forces shaping

law firms

Law as a business

Final thoughts

Outline

3

Introduction

Client needs and the modern law firm

Non-economic forces shaping

law firms

Law as a business

Final thoughts

4

Introduction

Four out of five (80%) 2005 Columbia Law School graduates went into private practice, typically in large law firms

Two out of three (66%) law students nationwide who participated in summer associate programs in 2005 accepted offers to work at the same law firm that employed them during their 2L summer

Of law students who join large law firms on graduation

1% depart after the 1st year

14% leave by the end of the 2nd year

37% leave after three years

77% are gone by the end of the 5th year

This means thatIf you choose to be a 2L summer associate at a law firm in 2008, chances are that you will accept a job there and stay for at least a few years. And if you stay longer, will that firm continue to exist and, if so, what will it look like?

This talk is to help you understand the forces that affect evolution of the legal industry and to help you make better choices among firms

5

Legal industry evolution in the US

The legal industry in the US grows in line with GDP but one sector, comprising the largest firms, is growing revenues and profitability far more quickly

This sector is doing so because it has a relatively benign competitive structure. Though there are some characteristics that may make it less attractive over time – e.g., client pricing pressures, technology – continued revenue and profit expansion is likely

Evolution to date has tracked that of comparable professional service industries, though at slower pace

A key feature of the evolution is that the rich are getting richer – top firms are increasing their share of profit and prominence, and widening a gap with also-rans

The next phase of evolution, already beginning, is likely to be toward greater differentiation in which leaders will develop distinctive value propositions vis-à-vis clients and talent

6

The legal industry as a whole grows in line with GDP but the largest 100 firms grow faster than the market

* Total US legal services output for 1996-2000 and 2006 projected from 2000-2005 dataSources: American Lawyer; Federal Reserve Economic Data; Blaqwell analysis

US GDP and Law Firm Revenues (1996-2006)

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

100

316 (Top 100 US firms’ revenue)

184* (Total US legal services output)

171 (US GDP)

10-Year AnnualizedGrowth Rate

Revenue for Top 100 Firms 12.2 %

Total US Legal Services Output* 6.3 %

US GDP 5.5 %

7

For largest 100 US firms, growth in revenue and profits over past seven years has been extraordinary

11.4 12.213.5

15.317.1

19.121.6

2000 2001 2002 2003 2004 2005 2006

31.135.1

38.141.7

4650.9

56.7

2000 2001 2002 2003 2004 2005 2006

CAGR 11.2%CAGR 10.5%

Total Profitsof US Top 100

($ billions)

Total Revenueof US Top 100

($ billions)

Note: US Top 100 firms comprise the AmLaw 100 – the top 100 US firms ranked by revenue Sources: American Lawyer, Blaqwell analysis

8

Industrycompetitors

Generally attractiveindustry

New entrants

BuyersSuppliers

This is due to an attractive industry structure for large firms

History of “gentlemanly club” competitionIncreasing competitiveness, fueled by greater investment in, and reward from brandIncreasing focus on relative economicsSegmentation by AmLaw ranking or equivalent

Significant barriers to entry; no substitute products

Increasing stratification of work by valueIncreasing, but still relatively low, price sensitivity for high end workRapid expansion of high-shareholder-value legal needsIncreasing attention to cross-border issuesPressure for alternative billing arrangements for routine work gaining momentum

Talent markets relatively constrained Law school pool not growing Increased partner and associate mobility —lateral hiring up 19% in ’05 but down 11% in ‘06 Highest-level brand name lawyers ( a quite limited number) becoming more mobile and demandingTemp attorney use doubled between ’02-’03, +48% in ’04, +13% in ‘05

TECHNOLOGYCompetitive impact limited todayFocus on next generation softwareKnowledge management becoming more importantMore advanced financial reporting and management solutions adopted

MACROECONOMICSGenerally positive even through market and economic downturns

REGULATIONRapidly increasing impact on value to clientsA source of massive demand growth

Other Industry-Shaping Factors

Sources: AmLaw Lateral Report 2007, NALP, Blaqwell Analysis

9

In contrast to most other industries, legal industry players have not changed significantly in the last 50 years

Sources: “The Wall Street Lawyers,” Fortune (February, 1958), cited in Smigel, 1964.

1957 Rank Largest NY Law Firms in 1957

Today’s AmLaw

Top 20 Top 1001 Shearman & Sterling 2 Cravath 3 White & Case 4 Dewey Ballantine 5 Simpson Thacher 6 Davis Polk 7 Milbank Tweed 8 Cahill Gordon 9 Sullivan & Cromwell

10 Chadbourne, Parke 11 Breed Abbott (merged with Winston & Strawn in 2000) NA NA12 Winthrop Stimson (merged with Pillsbury in 2001) NA NA13 Cadwalader, Wickersham 14 Willkie Farr 15 Donovan Leisure (disbanded in 1998) NA NA16 Lord, Day & Lord (disbanded in 1994) NA NA17 Dwight Royall (became Rogers & Wells, merged with C. Chance in ‘00) NA NA18 Mudge Rose (disbanded in 1996) NA NA19 Kelley Drye

20 Paul Weiss 21 Cleary Gottlieb

10

The competition to attract the best talent is fierce

0

20,000

40,000

60,000

80,000

100,000

120,000

Applicants to ABA approved law schools

Admitted Applicants

Matriculants

$0 k

$30 k

$60 k

$90 k

$120 k

$150 k

$180 k

Sources: Law School Admission Council 2006 data; “Salary Trends: A 15 Year Overview”, NALP bulletin, July 2005; NALP Associate Salary Surveys

* = change in data collection procedures began this year

** = preliminary data

Median Starting Salary for Firms with 501+ Lawyers

Law School Applicationsand Matriculation

11

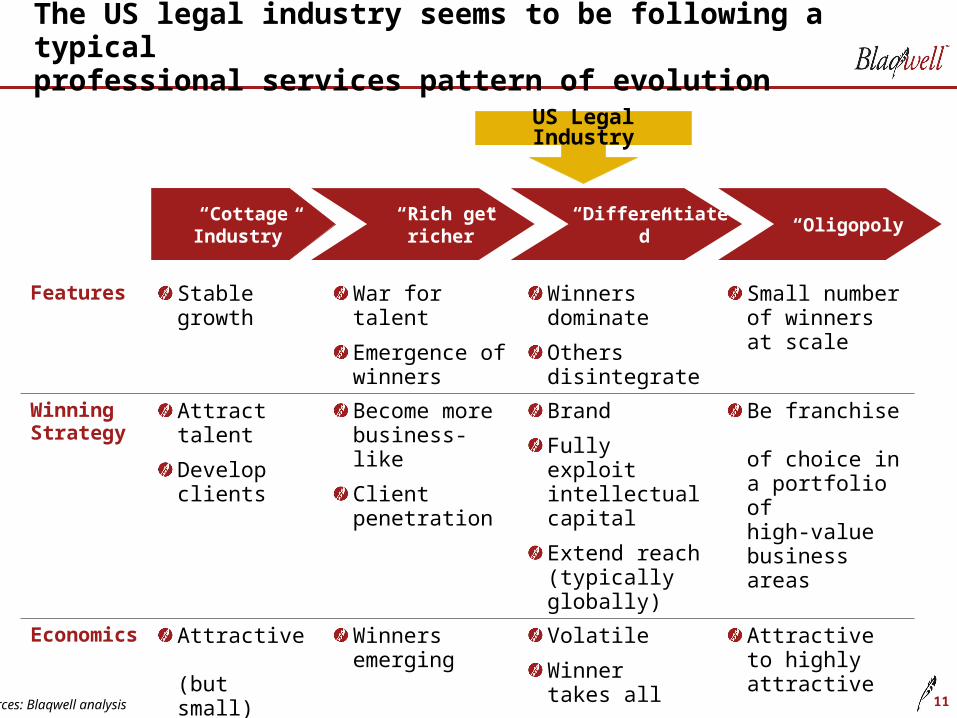

The US legal industry seems to be following a typical professional services pattern of evolution

Features Stable growth War for talent

Emergence of winners

Winners dominate

Others disintegrate

Small number of winners at scale

Winning Strategy

Attract talent

Develop clients

Become more business- like

Client penetration

Brand

Fully exploit intellectual capital

Extend reach (typically globally)

Be franchise of choice in a portfolio of high-value business areas

Economics Attractive (but small)

Winners emerging

Volatile

Winnertakes all

Attractive to highly attractive

US Legal Industry

“Cottage Industry”

“Rich get richer” “Differentiated” “Oligopoly”

Sources: Blaqwell analysis

12

Introduction

Client needs and the modern law firm

Non-economic forces shaping

law firms

Law as a business

Final thoughts

13

Why do law firms evolve?

A lawyer’s function, and the structure in which his activity is best organized, depends both on what corporations – that is, the clients – are doing and on the structures in which clients’ activities are being carried out

As a result of profound changes in the underlying configuration of markets and technology, corporations and their corresponding structures may change dramatically

Hence, both the lawyer’s function and the structure of the profession change dramatically from time to time in response to changes in clients’ markets

14

Phase 1 (Competition) - Mid- to late-19th century

Competition amongst small ventures

Lawyers active in promotion of companies, negotiating rights-of-way, collection of debts and other routine activities

Strategic litigation an extension of competition – challenges to patents, mining claims, or franchises

Peddling influence and seeking favors in state capitals

“Hustling, aggressive, scrappy, opportunistic, ethically corner-cutting kind of practice”

Phase 2 (Consolidation) - First quarter of 20th century

Many large industries came to be dominated by a few giant firms

Lawyers negotiated alliances, trusts, holding company structures, including increasingly complex corporate debt and equity instruments

Many leading corporate lawyers left litigation

Redesign of legal system to legalize consolidations

Sources: “The Legal Profession,” Robert Gordon

Evolution of legal practice in America

15

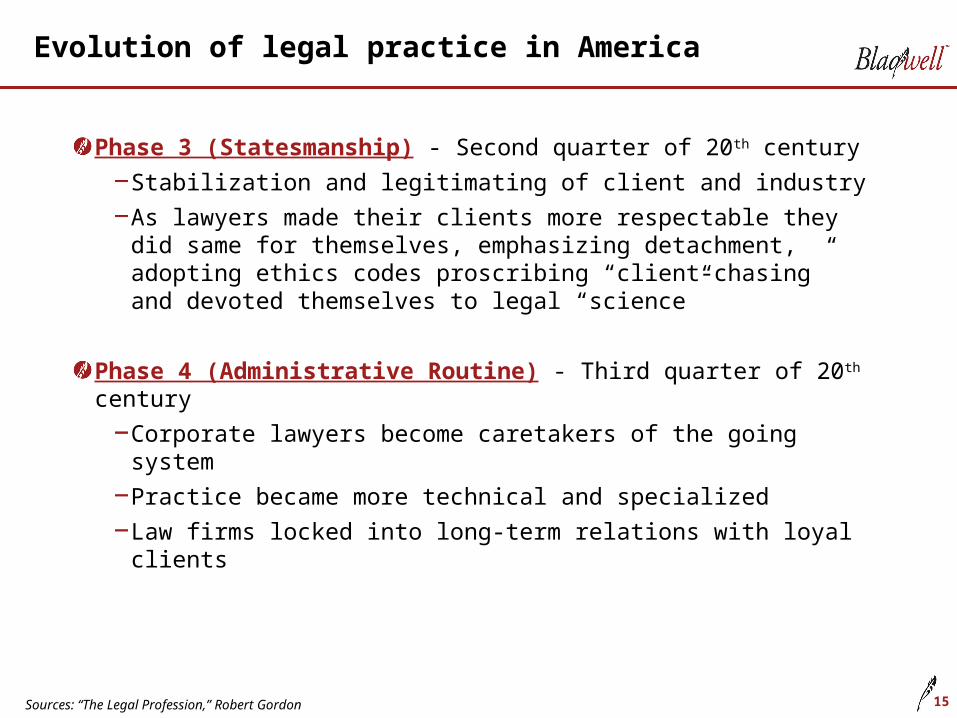

Phase 3 (Statesmanship) - Second quarter of 20th century

Stabilization and legitimating of client and industry

As lawyers made their clients more respectable they did same for themselves, emphasizing detachment, adopting ethics codes proscribing “client-chasing” and devoted themselves to legal “science”

Phase 4 (Administrative Routine) - Third quarter of 20th century

Corporate lawyers become caretakers of the going system

Practice became more technical and specialized

Law firms locked into long-term relations with loyal clients

Sources: “The Legal Profession,” Robert Gordon

Evolution of legal practice in America

16

Phase 5 (Destabilization and reconfiguration) – Last quarter 20th century

International competition, new mobility of capital, and volatility of market for corporate control

Legal relationships characterized by cost-cutting

New style of corporate practice

“ruthlessly competitive, powered almost exclusively by the drive for profits, so demanding as to leave no time or energy for other commitments, very lucrative for lawyers and firms who succeed but also very anxiety producing because so many fail, and mostly indifferent to social responsibility and public values”

Sources: “The Legal Profession,” Robert Gordon

Evolution of legal practice in America

17

Features of the American profession

Although a single profession, lawyers in different kinds of practice receive a wide range of prestige and reward

LOWEST STATUS

Practice solo or in small partnerships

Represent individuals in trouble and without much money

Frequently of recent immigrant origin

ELITE

Partners in big city law firms doing specialized work for corporations

Top graduates of elite law schools

Predominantly white male

MIDDLE

Miscellaneous work for middle class individuals

Personal injury, real estate, estate planning, divorce

Human Suffering

Prestige and Reward

18

What do law firms do?

Before 1900 leading lawyers were rarely exclusively “corporate” lawyers or litigators. Big Deals, Big Cases, and Big State have created the need for specialist work and given rise to modern multi-specialist firms.

Today the work of the bar varies in interest, complexity and importance

Corporate

Regulatory compliance and

contract administration

Design and negotiation of new

structures of contractual or

regulatory architecture

Litigation

Routine processing of low-stakes

repetitive litigation

Huge “bet-the-company” cases in

bankruptcy, antitrust and mass tort

defenses

Regulatory

Processing routine

applications for administrative

orders

Designing and drafting

legislative and administrative

frameworks

Value

Low

High

19

Introduction

Client needs and the modern law firm

Non-economic forces shaping

law firms

Law as a business

Final thoughts

20

Law as a profession

The tasks of professions are to address human problems amenable to solution by application of expert service. They may be individual problems or problems for groups. The degree of resort to experts varies from problem to problem, from society to society, and from time to time

The function of the professionals is to classify a problem (“diagnosis”), to reason about it (“inference”), and to take action on it (“treatment”)

Why is it that lawyers, rather than accountants or consultants or bankers, solve particular problems? Or do they?

21

Control of asymmetric relationships / monopoly control

“Asymmetry of expertise” requires client to trust professional and professional to respect both client and colleagues. The “project” of the profession is to ensure maintenance of this collegiality and trust and it does so by various institutional forms – educational requirements, associations, licensure, ethics codes – and assumes that only those who conform will be entitled to deliver the expert advice

Professions do not serve disembodied social needs but rather impose both the definition of needs and the manner of service on atomized customers. Dominance and autonomy, not collegiality and trust, are the true hall marks of a profession. The “project” of the profession is to secure the goal of economic monopoly

Neither approach provides a complete answer to the relationship between organized law and society

22

The disappearing middle market

Perception of lawyers as professionals with unique qualifications has led to a privileged position in society

A monopoly to perform certain professional activities – most important, to represent others before the courts

Many rules have evolved to ensure the ability of lawyers to carry out the tasks of their profession effectively. The most important of these are:

The right to privileged communication with clients

The burden of confidentiality imposed upon such communication

Rules relating to potential conflict among clients or potential clients

A prohibition on sharing profit with non-lawyers

23

The purpose of ethics

The first ABA ethics code of 1908 stressed the lawyer’s fidelity to the public purposes of the legal system as well as to clients

Since then, every revision of the code has moved it further away from the obligation to balance client’s interests against obligations to the legal system, towards almost-exclusive duties of loyalty, confidentiality, and zealous advocacy of clients

The lawyer must press in his client’s favor every plausibly arguable construction of the law and the known facts. He has almost no affirmative duties to assist adversaries, tribunals, or regulatory agencies to gather facts; to restrain clients from perjury or fraud; or to urge his clients to comply with laws or regulations

This tendency, coupled with the perception of law as a business, is leading to some serious issues within the profession

24

Introduction

Client needs and the modern law firm

Non-economic forces shaping

law firms

Law as a business

Final thoughts

25

The disappearing middle market

Law as a business

Modern law firms organize themselves as businesses and that, as with all other businesses, they are motivated to maximize the return to the owners of the business

To understand what you can expect from a law firm, you need to begin to understand how law firms make money and how you fit into the productive machine that is a law firm

26

Importance of profit per equity partner (PPP)

If the most important function of the law firm is to maximize return to the proprietors of the business it follows that Profit per Partner (“PPP”) must be the best measure of comparative success among competing law firms

This does indeed turn out to be the case

Most widely followed measure by commentators

Safe harbor for clients -- proxy for quality

Fundamental to attract best talent

27

Top 20 firms by PPP (2006)

Rank Firm PPEP

1 Wiley Rein* $4,434,426

2 Wachtell $3,974,026

3 Cravath $3,017,241

4 Cadwalader $2,901,316

5 Sullivan & Cromwell $2,820,122

6 Cahill Gordon $2,571,429

7 Simpson Thacher $2,496,914

8 Paul, Weiss $2,495,413

9 Quinn Emanuel $2,433,824

10 Kirkland $2,268,868

Rank Firm PPEP

11 Milbank, Tweed $2,166,667

12 Schulte $2,157,895

13 Cleary Gottlieb $2,118,785

14 Skadden $2,091,837

15 Willkie Farr $2,032,520

16 Dechert $1,988,166

17 Weil, Gotshal $1,900,000

18 Latham $1,856,448

19 Davis Polk $1,819,728

20 Debevoise $1,806,818

Note: Indicates the firm received high contingency fees during the year

Sources: AmLaw 100, Blaqwell analysis

28

Consistency in top 20 firms

Rank

Firm PPEP 2006 1996 1986

Wiley Rein* $4,434,426 1 -- --

Wachtell $3,974,026 2 3 1

Cravath $3,017,241 3 1 2

Cadwalader $2,901,316 4 18 25

Sullivan & Cromwell $2,820,122 5 4 6

Cahill Gordon $2,571,429 6 2 3

Simpson Thacher $2,496,914 7 5 8

Paul, Weiss $2,495,413 8 14 15

Quinn Emanuel $2,433,824 9 -- --

Kirkland $2,268,868 10 11 12

Milbank, Tweed $2,166,667 11 16 18

Schulte $2,157,895 12 21 --

Cleary Gottlieb $2,118,785 13 9 14

Skadden $2,091,837 14 8 4

Willkie Farr $2,032,520 15 10 11

Dechert $1,988,166 16 58 72

Weil, Gotshal $1,900,000 17 15 7

Latham $1,856,448 18 13 8

Davis Polk $1,819,728 19 6 5

Debevoise $1,806,818 20 7 16

Note: Indicates the firm received high contingency fees during the year

Sources: AmLaw 100, Blaqwell analysis

29

Cash generation

Because firms charge for the time of their professionals on an hourly basis, it is possible to calculate how much revenue they can generate (“maximum fee capacity”). The result is a function of the number of professionals at different levels in the organization, their utilization on billable work, and their respective charge-out rates.

Note: Indicates firm with leverage of 2 associates to 1 partner working at maximum capacity

Sources: Blaqwell analysis

Level of Organization# of

ProfessionalsTarget Hours

Hourly Rate (US$)

Fee Capacity (US$)

Equity Partner 20 2,000 650 26,000,000

Non-Equity Partner 5 2,400 500 6,000,000

Sr. Associate 5 2,400 400 4,800,000

Mid-Level Associate 15 2,200 300 9,900,000

Jr. Associate 30 2,000 200 12,000,000

Legal Staff 75 58,700,000

Paralegals 10 1,500 125 1,875,000

Total 85 60,575,000

30

Maximum fee capacity

Maximum fee capacity is a budgetary device, not a ceiling on the amount of revenue that a firm can generate

An organizing technique to enable firm to predict and manage firm revenue on basis of assumptions relating to number of fee earners, hours that each of them will work, rates they will charge and success in billing and collection

Realizing maximum fee capacity requires the firm to balance

Maximizing billable hours recorded by each lawyer within the firm (“Utilization”)

Maximizing rate charged to clients for each billable hour recorded (“Charging Rates”)

Maximizing realization of revenue for each recorded hour (“Realization Rate”)

Optimizing the mix of senior and junior time spent in the execution of each engagement (“Leverage”)

31

The bottom line: from fee capacity to PPP (the return to the proprietors)

Fee capacity must be converted into PPP. This is a multi-stage process involving lawyers and managers. Law firms seek to optimize the conversion and, in so doing, affect every aspect of practice.

Fee Capacity

Revenue or

Gross Margin

DirectCost

ContributionMargin

Overhead

Operating Profit

InvestmentCosts

NetIncome

Unconverted Fee Capacity & Uncollected

Bills Net IncomeNumber Of

Equity Partners

PPP=

Sources:Blaqwell analysis

32

Limited ways to improve PPP

Hours

Rates

Leverage

33

Controlling hours

1 Necessary activities included are Sleeping (365x8), Eating (365x3), Bodily (365x1), Errands (365x1)2 Discretionary activities included are Exercise, Family, Illness, Hobbies, Romance, Vacation, Continuing Education

Activity Case I Case II Case III

Total Hours Per Year 8,760 8,760 8,760

Necessary 1 4,745 4,745 4,745

Remaining Hours 4,015 4,015 4,015

Working Hours 2,500 3,000 3,500

(Billable Hours 1,667 2,000 2,333

Discretionary 2 1,515 1,015 515

Hours Per Day (weeks) 4.2 (9) 2.8 (6) 1.4 (3)

Sources:Blaqwell analysis

34

Controlling rates

Sources: Inside Counsel 17th Annual Survey of General Counsel July 2006

52% of general counsel reported

“reduce cost” as the most important

thing firms could do to improve their

client relationships52%

35

Controlling leverage

Firm PPEP Leverage 2000 (EP’s/ lawyers

Leverage 2006 (EP’s/ lawyers)

Wachtell $3,974,026 1.03 2.51

Cravath $3,017,241 3.30 4.67

Cadwalader $2,901,316 3.62 7.30

Sullivan & Cromwell $2,820,122 2.90 3.51

Cahill Gordon $2,571,429 2.83 3.84

Simpson Thacher $2,496,914 3.20 4.12

Paul, Weiss $2,495,413 3.18 5.26

Kirkland & Ellis $2,268,868 4.17 5.21

Milbank, Tweed $2,166,667 3.60 4.16

Schulte $2,157,895 3.43 5.24

Cleary Gottlieb $2,118,785 2.79 4.61

Skadden $2,091,837 3.77 4.31

Willkie Farr $2,032,520 2.53 4.21

Dechert $1,988,166 2.18 5.31

AmLaw 100 average: 2.77 4.13

Sources:AmLaw 100, Blaqwell analysis

36

Note: 1994 is the first year for which AmLaw reports non-equity partner figures

Sources: AmLaw, Blaqwell analysis.

Adjusting the partnership structure: growth of non-equity partnership in the AmLaw 100

8078

73

45

33.7%

13.3%

31.4%

22.2%

0

20

40

60

80

100

1994* 2000 2005 2006

Am

La

w F

irm

s

0%

10%

20%

30%

40%

% T

ota

l Pa

rtn

ers

Firms with NEP's Total NEP's as % of all partners

37

Introduction

Client needs and the modern law firm

Non-economic forces shaping

law firms

Law as a business

Final thoughts

38

The disappearing middle market

The profession is increasingly troubled as traditional values clash with the imperative to make money

Many lawyers are disaffected

Public regard for lawyers is low

Many lawyers do not enjoy the quality or the quantity of their work

Loss of professionalism

Hyper-adversarial behavior

Incivility

Ethical corner-cutting

Greed

Competition and loss of autonomy

39

Final words

Lawyers never stop learning

To be successful you will need to develop the following capabilitiesMaturity and judgmentWork ethicInitiative and entrepreneurshipInnovationAttitudePrior career successInterpersonal skillsLeadershipTeamworkCross-cultural exposure/ sensitivity

These are not all learned at Law School – your first employer is the next stop along the path to attaining these capabilities

Choose wisely

© Blaqwell, Inc. 2007

What You Should Know About the Legal Business

Summer, 2007