zignago vetro group · zignago vetro group company overview borsa italiana star conference 2008 -...

TRANSCRIPT

Zignago Vetro Group

Company Overview

Borsa Italiana

STAR Conference 2008 - Milano

06 March 2008

2

65%

100%

100%

Zignago Holding Group Structure

(A) - Based on 100% of Zignago Vetro Group revenues

Zignago Vetro Group remains one of the priorities i n Zignago Holding future strategy

2006 Zignago Holding Revenues Contribution

Luca Marzotto 20.2Nicolò Marzotto 19.5

Stefano Marzotto 19.3 Marco Donà dalle Rose 17.9 Gaetano Marzotto 16.0 Maria Rosaria Marzotto 2.6

Cristiana Marzotto 2.6Margherita Marzotto 1.9

Zignago Holding S.p.A.

Zignago Vetro Group

Glass containersmanufacturer

Santa Margherita S.p.A.

Wine producer

Real estate

FIMIZ S.r.l.

100%

Industrie Zignago SantaMargherita S.p.A.

Shareholders Stake (%)

Santa

Margherita

23%

Others

11%

Zignago Vetro

66% (A)

3

Milestones

1979 1994-1995 October 2004 June 2007IZSM

establishes Zignago Vetro

S.p.A. conferring its

glass production plants

IZSM establishes Attività Industriali Friuli S.r.l. (51.0%

owned) which acquires a plant

from an insolvency proceeding

IZSM transfers its stakes in Attività Industriali Friuli

and Vetrerie Venete to newly

formed Vetri Speciali

Zignago Vetro becomes a Listed Company in the

Italian Stock Exchange (STAR

Segment)

1950's 1980's 1990's 2002 2004 2006 2007

1950’s 1987 2002 June 2006Zignago Vetro

acquires the 43.5% stake in Vetri Speciali

from IZSM

December 2006IZSM sells its 100%

stake in Zignago Vetro to Zignago

Holding

THE BEGINNING ZIGNAGO VETRO EXPANSION GROUP REORGANIZ ATION

THE BEGINNING ZIGNAGO VETRO EXPANSION GROUP REORGANIZ ATION

Industrie Zignago Santa Margherita (“IZSM”) builds its first glass

production plant (jars and bottles)

Zignago Vetro acquires a plant in Empoli from an insolvency proceeding

Zignago Vetro acquires the

assets of Verreries Brosse

S.A.S from an insolvency proceeding

4

Zignago Vetro Group

� Significant positions in the Food & Beverage, Perfumery & Cosmeticsmarkets, High-end Perfumery and Specialty Glass Containers

� In 2007, Group revenues of €241m (33% generated abroad) and EBITDA of€64m (26.7% margin)

� Most profitable Group within the industry with historically above averagemargins

� The management has experience in the industry and turnarounds

� Strong track record in organic growth and selective acquisitions with a14.1% CAGR over last 3 years

Fast growing and profitable niche glass producer de livering a high and rising ROCE

5

Competitive StrengthsMain FeaturesProducts2007A Size (€m)

Our Presence in Selected Business Segments

� Personalization

� Small-runproduction

Vetri SpecialiHighly customized specialtyglass containers produced invery short runs with strong focuson efficiencySales €43m

� Innovation

� QualityVerreries BrosseExtraordinary high-quality,tailor-made product offeringand efficiency

Focus on high-end perfumerymarket

Sales €45m

Zignago Vetro � Flexibility

Flexibility, efficiency andtechnical know-how key forsuccess

Focus on selected segmentsof food & beverage andcosmetics & perfumery

� QualitySales €158m

6

International Presence with an Italian Footprint

Legend:

Production and distribution DistributionProductionZignago Vetro Verreries Brosse Vetri Speciali

New Jersey, USA Empoli (FI)

Fossalta di Portogruaro (VE)

Barcelona, Spain

San Vito al Tagliamento (PN)

Ormelle (TV)Paris, France

Trento

Benicia, USA

Pergine Valsugana (TN)

Vieux Rouen sur Bresle, France

7

What Makes Us Different?

Outperform market growth

Maximise ROCE & profitability

Competitive advantage

Unique positioning and economic returns thanks to a distinctive business model

8

State-of-the-art,flexible manufacturing plants

Flexible and Efficient Production Process Drives Profi tability

Multi-skilled,flexible workforce

React promptly to marketchanges and requests

Move towards moreprofitable market segments

Flexible,efficient production

Flexible,efficient production

9

Process InnovationProduct Innovation

Constant Innovation Boosts Sales

� New products equal to ca. 14% oftotal products

� Highly personalized and complexshapes

� State-of-the-art and in-housetechnology

� High know-how in moulds designingand process development

10

Provider of Top Glass Solutions not Simply Quality Glass Containers

Corporate culture committed to highest quality of p roducts and customer service

� Designers’ ideas into feasible products

� Continuous improvement of plants’operations

� Quality control over the whole process

Quality of Products Quality of Customer Service

� Prompt response to requests

� Tailor-made product offering

� Flexible planning

� On-time deliveries

11

80%16%Vetri Speciali

50%49%Verreries Brosse

67%15%Zignago Vetro

Customerloyalty 1

Concentrationrate of first 5

clients

Loyalty of customers retained by:

� Meeting and anticipating their needs� Building effective partnerships

Excellent Longstanding Client Relationships and Goo dRevenues Visibility

1 % of clients present also the 2 previous years (data referred to 2007)

12

� Fully exploit Verreries Brosse brand potentialadopting Zignago Vetro state-of-the-art technology,flexible and efficient approach

Verreries Brosse: A Successful Turnaround Story

Rethinking of strategy

Zignago Vetro acquired Verreries Brosse in2002 following an insolvency proceeding and

turned it into a successful business

� Sales per employee increased from ca. €64,000in 2002 to ca. €136,000 in 2007

� Verreries Brosse sold 14m units in 2002, and47.5m in 2007

Experienced management team with the ability to cap italise on future acquisition opportunities

Capex trend (€m)

Intermediate achievements

8,9

2,54,1

2,94,6

2,4

2002 2003 2004 2005 2006 2007

18,0

24,929,8 30,9

36,3

45,2

9%

13%

16%17% 17%

21%

10

20

30

40

50

60

70

2002 2003 2004 2005 2006 20070%

5%

10%

15%

20%

25%

Revenues (€m) EBITDA margin (%)

13

Italian Food & Beverage Market

� Fast-growing demand in the winesegment boosted by strong exports

� Rebounding demand in the foodsegment

� Increasing demand for higherquality of product and service

� Large multinational competitorsfocused on commodity products andstandardizing service

Source: Zignago Vetro Group

Large multinational comps are focused on volumes an d standardised production,whereas Zignago Vetro is focused on selective segme nts requiring flexibility and service

0

200

400

600

800

1000

1200

1400

1600

1800

2004 2006 2009

04-06CAGR

+3.6%

06-09CAGR

+4.8%

Zignago Vetro04-06 CAGR +4.6%

(€m

)

14

0

200

400

600

800

1000

1200

1400

1600

2004 2006 2009

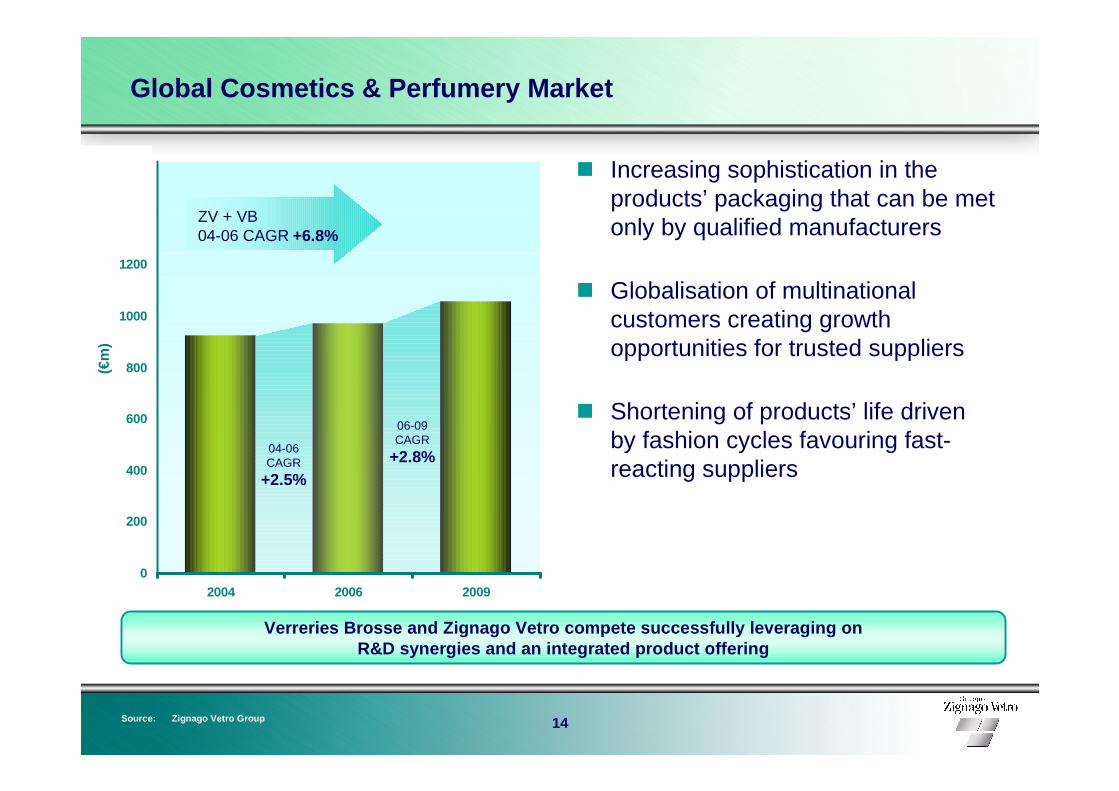

Global Cosmetics & Perfumery Market

� Increasing sophistication in theproducts’ packaging that can be metonly by qualified manufacturers

� Globalisation of multinationalcustomers creating growthopportunities for trusted suppliers

� Shortening of products’ life drivenby fashion cycles favouring fast-reacting suppliers

Source: Zignago Vetro Group

Verreries Brosse and Zignago Vetro compete successf ully leveraging onR&D synergies and an integrated product offering

04-06CAGR

+2.5%

06-09CAGR

+2.8%

ZV + VB04-06 CAGR +6.8%

(€m

)

15

0

100

200

300

400

500

600

700

800

2004 2006 2009

Global Specialty Glass Containers Market

� New, high-growing business

� Increasing demand fuelled by moresophisticated customer marketingfor premium lines(e.g. in wines and spirits)

� Robust demand for small quantitiesand special shapes and colours

� Premium positioning

Source: Zignago Vetro Group

Unique range of products and experienced sales forc e enable Vetri Specialito meet special needs of a more sophisticated marke t

04-06CAGR

+8.1%

06-09CAGR

+8.5%

Vetri Speciali05-06 CAGR +4.5%

(€m

)

16

Growth &Profitability

MarketOpportunities

Zignago VetroGroups’ Model

+

Zignago Vetro Group: Positioned for Growth

Flexibility, efficiency, innovation and quality are key competitive advantages

Opportunities and room for fast moving players to o utperform

External growth opportunities

17

10,716,8 15,4

24,9

6,6%

8,7%

7,4%

10,4%

0

5

10

15

20

25

30

2004 2005 2006 20072%

4%

6%

8%

10%

Net Results (€m) Margin (%)

2.5

162,1 192,6 209,4 240,7

0

50

100

150

200

250

300

2004 2005 2006 2007

Strong Track-record of Revenues Growth and Top of the M arketProfitability

Revenues (€m) EBITDA (€m)

EBIT (€m) Net Result (€m)

Source: Zignago Vetro Group

Y-o-YGrowth

+18.8%

Y-o-YGrowth

+8.7% 39,649,9 53,8

64,3

24,4%

25,7%

26,7%25,9%

20

30

40

50

60

70

2004 2005 2006 200720%

25%

EBITDA (€m) Margin (%)

18,627,1 31,3

42,9

11,5%

14,1% 14,9%17,8%

05

1015202530354045

2004 2005 2006 20070%

5%

10%

15%

EBIT (€m) Margin (%)

Y-o-YGrowth

+14.9%

1.1

Extraordinary Items

1.2

18

Solid Balance Sheet 1 to Support Organic and External Growth

1 Aggregated data is shown in 2004 and 2005

132,5 132,1 121,9 123,2

0

20

40

60

80

100

120

140

160

2004 2005 2006 2007

Net Capital Employed (€m) Net Working Capital (€m)

Net Equity (€m)

34,846,2 42,9 39,9

21,4% 20,5%

16,6%

24,0%

0

10

20

30

40

50

60

2004 2005 2006 20070%

4%

8%

12%

16%

20%

24%

Net working Capital (€m) on sales (%)

Net Financial Debt (€m)

102,1 108,8

61,377,2

0

20

40

60

80

100

120

2004 2005 2006 2007

30,4 23,3

60,546

0

20

40

60

80

2004 2005 2006 2007

Source: Zignago Vetro Group

19

Capex (€m) Cash Flow from Operations (€m)

High and Stable Cash Flow From Operations

Capex mainly depends on furnaces refurbishment and capacity increase

Pay-out ratio: approximately 70%, without extraordi nary operations

11,0

16,7

8,5

20,5

21,5

0

5

10

15

20

25

30

35

2004 2005 2006 2007

Net Capex related toVetri Speciali acquisition

Source: Zignago Vetro Group

32,8 33,236,6 38,0

0

5

10

15

20

25

30

35

40

2004 2005 2006 2007

20

34,442,1

25,3% 26,6%

05

1015202530354045

2006 20070%

5%

10%

15%

20%

25%

EBITDA (€m) Margin (%)

9,9

19,8

12,5%

7,3%

0

5

10

15

20

25

2006 20070%

2%

4%

6%

8%

10%

12%

16,4

5,30

5

10

15

20

2006 2007

135,9158,1

020406080

100120140160

2006 2007

2007 ZV results

Revenues (€m) EBITDA and margin evolution

Net result (€m) Net Financial Debt (€m)

+16.3%

1,2

Net result (€m) Extraordinary Items Margin (%)

21

45,236,3

51015202530354045

2006 2007

2007 VB results

Revenues (€m) EBITDA and margin evolution

Net result (€m) Net Financial Debt (€m)

+24.3%

16,012,3

0

5

10

15

20

2006 2007

6,29,4

17,0%

20,7%

0

2

4

6

8

10

12

2006 20070%

5%

10%

15%

20%

EBITDA (€m) Margin (%)

3,2

1,1

3,0%

7,1%

0

1

2

3

4

2006 20070%

3%

6%

Net result (€m) Margin (%)

22

2007 VS results (43,5%)

Revenues (€m) EBITDA and margin evolution

Net result (€m) Net Financial Debt (€m)

28,1 28,4

0

10

20

30

40

2006 2007

4,35,1

11,9%10,8%

0

1

2

3

4

5

2006 20070%

3%

6%

9%

12%

Net result (€m) Margin (%)

13,2 13,2

30,6%33,1%

0

5

10

15

2006 20070%

5%

10%

15%20%

25%

30%

35%

EBITDA (€m) Margin (%)

43,239,8

10

20

30

40

2006 2007

+8.3%

23

Strategic Guidelines

MarketCorporate

Focus on higher valueadded and fast growing

segments

Strengthen competitivebarriers

Increase sophisticatedclients

Continuousimprovement of businessmodel

Commitment to organicand external growthopportunities

Optimise and expandproduction capacity

Growth+

HighProfitability

24

GROWTH + HIGH PROFITABILITY

Zignago Vetro Group’s Highlights

Highly skilled management team with experience in c reating value and turnarounds

Financial flexibility with a solid balance sheet an d strong cash flow to supportgrowth opportunities and dividend distribution

Distinctive business model to boost sales, profitab ility and competitive barriers

Value creation for shareholders