zhen tian jeff lee visut hemithi

DESCRIPTION

A Deep Analysis of A Random Walk. Zhen Tian Jeff Lee Visut Hemithi. Huan Zhang Diana Aguilar Yuli Yan. Identification. Identification. Unit Root. Log Transformation Trend in Var. Difference Trend in Mean. Pre-Whitening. Pre-Whitening. Unit Root. Model Validation-1. - PowerPoint PPT PresentationTRANSCRIPT

Zhen Tian

Jeff Lee

Visut Hemithi

Huan Zhang

Diana Aguilar

Yuli Yan

A Deep Analysis of A Random WalkA Deep Analysis of A Random Walk

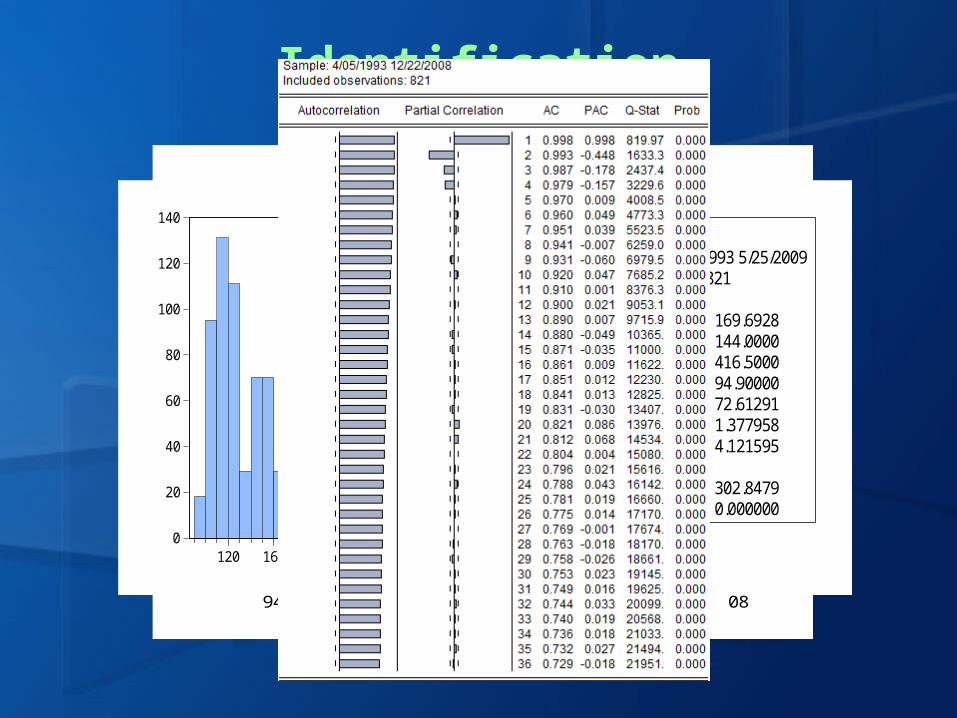

Identification

80

120

160

200

240

280

320

360

400

440

94 96 98 00 02 04 06 08

PRICE

0

20

40

60

80

100

120

140

120 160 200 240 280 320 360 400

Series: PRICESample 4/05/1993 5/25/2009Observations 821

Mean 169.6928Median 144.0000Maximum 416.5000Minimum 94.90000Std. Dev. 72.61291Skewness 1.377958Kurtosis 4.121595

Jarque-Bera 302.8479Probability 0.000000

Identification

80

120

160

200

240

280

320

360

400

440

94 96 98 00 02 04 06 08

PRICE

Unit Root

Null Hypothesis: PRICE has a unit root

Exogenous: Constant

Lag Length: 3 (Fixed)

t-Statistic Prob.*

Augmented Dickey-Fuller test statistic -2.431974 0.1332

Test critical values: 1% level -3.438129

5% level -2.864863

10% level -2.568594

Pre-Whitening

-.15

-.10

-.05

.00

.05

.10

.15

.20

94 96 98 00 02 04 06 08

DLNPRICE

Log Transformation

Trend in Var.

Difference

Trend in Mean

Pre-Whitening

0

40

80

120

160

200

240

280

-0.10 -0.05 -0.00 0.05 0.10 0.15

Series: DLNPRICESample 4/05/1993 5/25/2009Observations 820

Mean 0.000574Median -0.000909Maximum 0.161180Minimum -0.098922Std. Dev. 0.019665Skewness 0.259126Kurtosis 11.59559

Jarque-Bera 2533.555Probability 0.000000

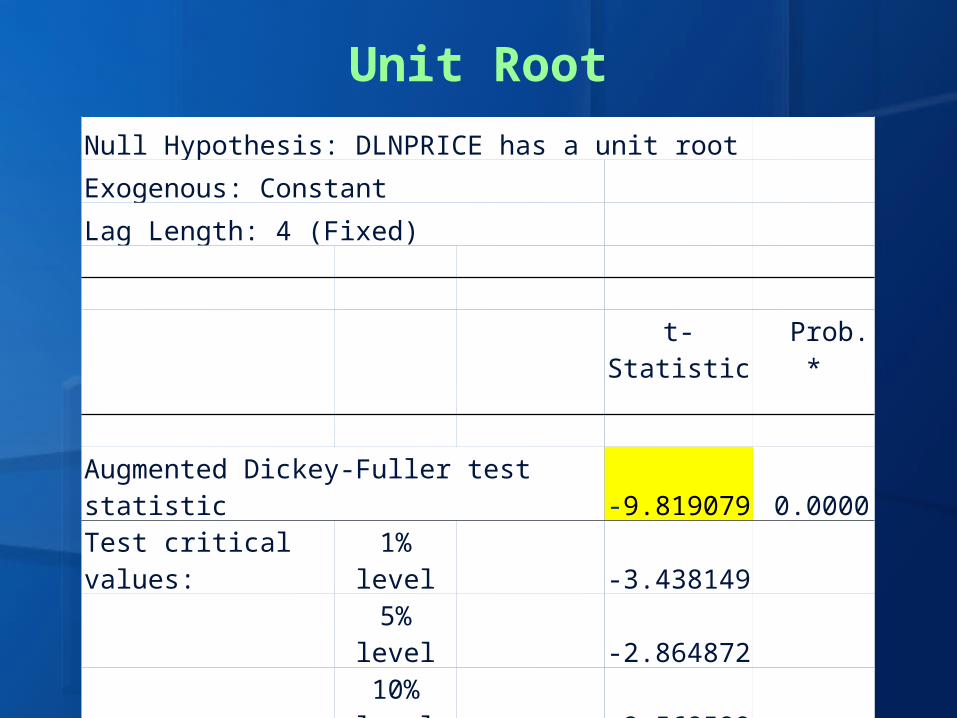

Unit Root

Null Hypothesis: DLNPRICE has a unit root

Exogenous: Constant

Lag Length: 4 (Fixed)

t-Statistic Prob.*

Augmented Dickey-Fuller test statistic -9.819079 0.0000

Test critical values: 1% level -3.438149

5% level -2.864872

10% level -2.568599

Dependent Variable: DLNPRICEMethod: Least SquaresSample (adjusted): 5/17/1993 12/22/2008Included observations: 815 after adjustmentsConvergence achieved after 6 iterationsBackcast: 1/11/1993 5/10/1993

Variable Coefficient Std. Error t-Statistic Prob.

C 0.000421 0.001769 0.238003 0.8119AR(1) 0.503803 0.034771 14.48920 0.0000AR(2) 0.104044 0.039420 2.639331 0.0085AR(3) 0.143444 0.036466 3.933679 0.0001AR(5) -0.124364 0.032993 -3.769439 0.0002MA(8) 0.103332 0.037023 2.791007 0.0054

MA(18) 0.118155 0.036499 3.237194 0.0013

R-squared 0.389743 Mean dependent var 0.000545Adjusted R-squared 0.385211 S.D. dependent var 0.019718S.E. of regression 0.015461 Akaike info criterion -5.492468Sum squared resid 0.193141 Schwarz criterion -5.452073Log likelihood 2245.181 F-statistic 86.00538Durbin-Watson stat 2.000720 Prob(F-statistic) 0.000000

Model Validation-1

-.12

-.08

-.04

.00

.04

.08

.12

.16

-.2

-.1

.0

.1

.2

1994 1996 1998 2000 2002 2004 2006 2008

Residual Actual Fitted

0

50

100

150

200

250

300

-0.10 -0.05 -0.00 0.05 0.10 0.15

Series: ResidualsSample 5/17/1993 12/22/2008Observations 815

Mean 4.29e-06Median -0.000768Maximum 0.145377Minimum -0.113527Std. Dev. 0.015404Skewness 0.656675Kurtosis 17.17994

Jarque-Bera 6886.600Probability 0.000000

Model Validation-2

Breusch-Godfrey Serial Correlation LM Test:

F-statistic 0.105569 Prob. F(2,806) 0.899825

Obs*R-squared 0.213376 Prob. Chi-Square(2) 0.898806.000

.004

.008

.012

.016

.020

.024

1994 1996 1998 2000 2002 2004 2006 2008

RESIDSQ

Model Validation-ARCH GARCH (1)

ARCH GARCH (2)Dependent Variable: DLNPRICEMethod: ML - ARCH (Marquardt) - Normal distribution

MA backcast: 1/11/1993 5/10/1993, Variance backcast: ONGARCH = C(8) + C(9)*RESID(-1)^2 + C(10)*GARCH(-1)

Coefficient Std. Error z-Statistic Prob.

C 0.000121 0.001162 0.104385 0.9169

AR(1) 0.543373 0.037777 14.38374 0.0000

AR(2) 0.188020 0.038719 4.855993 0.0000

AR(4) -0.095035 0.036572 -2.598555 0.0094

AR(5) 0.006074 0.030310 0.200393 0.8412

MA(9) -0.034453 0.033775 -1.020079 0.3077

MA(18) 0.105656 0.028083 3.762291 0.0002

Variance Equation

C 7.30E-06 1.18E-06 6.189402 0.0000

RESID(-1)^2 0.288911 0.040133 7.198888 0.0000

GARCH(-1) 0.724386 0.031554 22.95716 0.0000

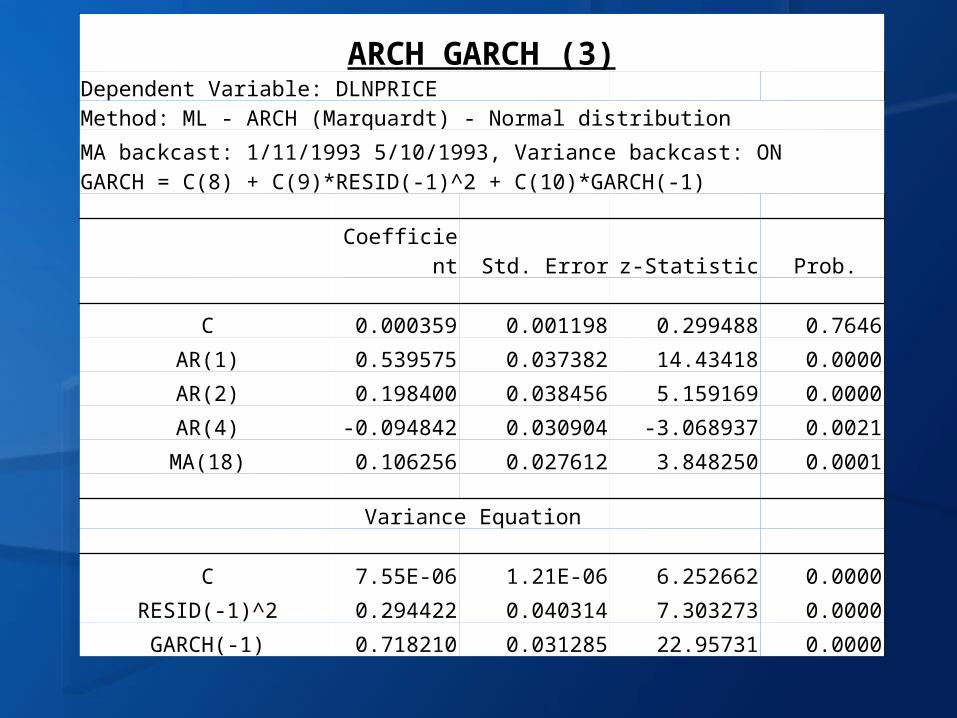

ARCH GARCH (3)Dependent Variable: DLNPRICEMethod: ML - ARCH (Marquardt) - Normal distribution

MA backcast: 1/11/1993 5/10/1993, Variance backcast: ONGARCH = C(8) + C(9)*RESID(-1)^2 + C(10)*GARCH(-1)

Coefficient Std. Error z-Statistic Prob.

C 0.000359 0.001198 0.299488 0.7646

AR(1) 0.539575 0.037382 14.43418 0.0000

AR(2) 0.198400 0.038456 5.159169 0.0000

AR(4) -0.094842 0.030904 -3.068937 0.0021

MA(18) 0.106256 0.027612 3.848250 0.0001

Variance Equation

C 7.55E-06 1.21E-06 6.252662 0.0000

RESID(-1)^2 0.294422 0.040314 7.303273 0.0000

GARCH(-1) 0.718210 0.031285 22.95731 0.0000

Model Validation-ARCH GARCH (3)

Correlogram

Correlogram of Residual2

Histogram

0

20

40

60

80

100

120

-2.50 -1.25 0.00 1.25 2.50 3.75 5.00

Series: Standardized ResidualsSample 5/10/1993 12/22/2008Observations 816

Mean 0.048932Median -0.086097Maximum 5.942007Minimum -2.775767Std. Dev. 0.999207Skewness 1.024413Kurtosis 6.494198

Jarque-Bera 557.8417Probability 0.000000

ARCH Test

ARCH Test:

F-statistic 0.190541 Prob. F(1,812) 0.662583

Obs*R-squared 0.190965 Prob. Chi-Square(1) 0.662115

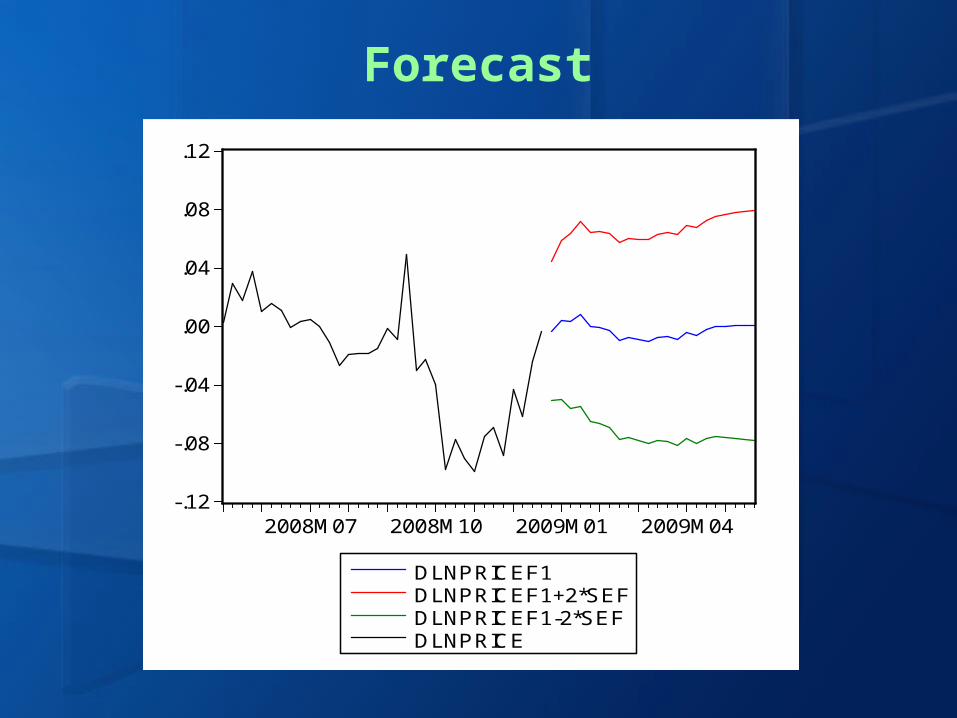

Forecast

-.12

-.08

-.04

.00

.04

.08

.12

2008M07 2008M10 2009M01 2009M04

DLNPRICEF1DLNPRICEF1+2*SEFDLNPRICEF1-2*SEFDLNPRICE

Forecast

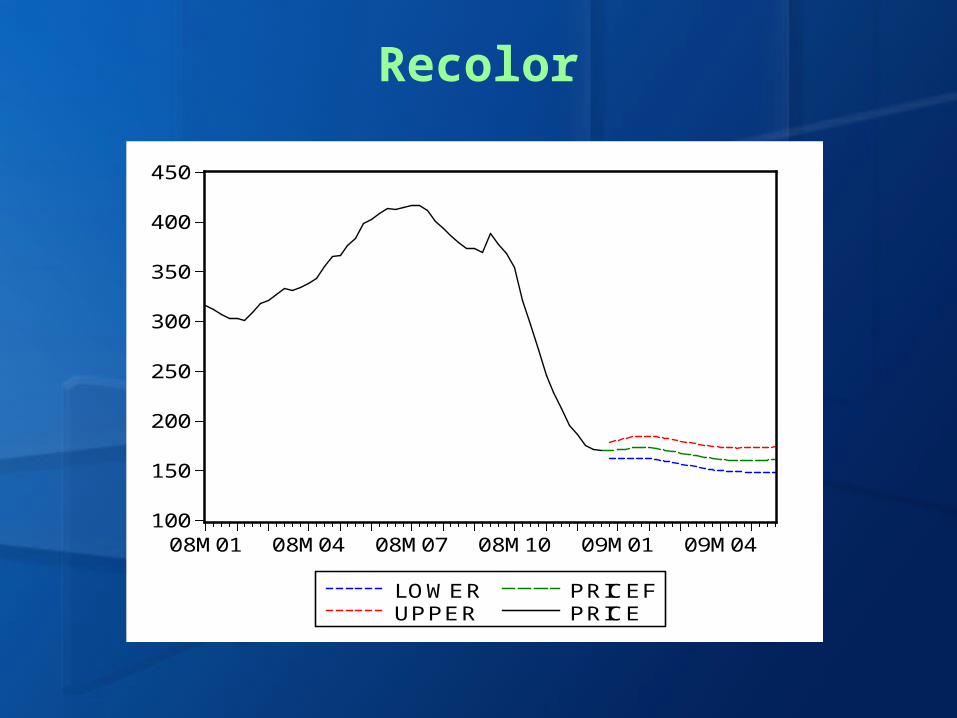

Recolor

100

150

200

250

300

350

400

450

08M01 08M04 08M07 08M10 09M01 09M04

LOWERUPPER

PRICEFPRICE

Comparison

100

150

200

250

300

350

400

450

08M01 08M04 08M07 08M10 09M01 09M04

PRICEALOWER

UPPERPRICEF

A Little Bit Further

-.12

-.08

-.04

.00

.04

.08

.12

2008M07 2008M10 2009M01 2009M04

DLNPRICEF1+2*SEFDLNPRICEF1-2*SEFDLNPRICEF1DLNPRICE

150

200

250

300

350

400

450

2008M07 2008M10 2009M01 2009M04

PRICEFPRICE

UPPERLOWER

Story Behind the Scene

To Investigate the Sources of Shock Geopolitical Events (War & Disasters)

GDP / Mean Personal Income

Vehicle Sales (SUV Sales)

China Petro Consumption

Speculation (Future Contract Price)

Key Bibliography “Causes and Consequences of the Oil Shock of 2007-08”

James D. Hamilton, UCSD (2009)