zambia country strategy paper 2017-2021 combined … · 2019-06-29 · african development bank...

TRANSCRIPT

AFRICAN DEVELOPMENT BANK GROUP

ZAMBIA

COUNTRY STRATEGY PAPER 2017-2021 COMBINED WITH THE 2017 COUNTRY

PORTFOLIO PERFORMANCE REVIEW

Prepared by: RDGS/COZM DEPARTMENTS

August 2017

FISCAL YEAR

01 January to 31 December

CURRENCY EQUIVALENTS

(August 2017)

National Currency: Zambia Kwacha (ZMW)

UA 1.00 = USD 1.40775

UA 1.00 = ZMW 12.5252

USD 1.00 = ZMW 8.8973

Sovereign Credit Rating (B- Fitch / B- S&P / B3- Moody’s)

ACRONYMS AND ABBREVIATIONS

ADF African Development Fund

ADB African Development Bank

AGTF Africa Growing Together Fund

BDEV Independent Development Evaluation

DBSA Development Bank of South Africa

CODE Committee on Operations and Development Effectiveness

COMESA Common Market for Eastern and Southern Africa

COZM Country Office Zambia

CP Cooperating Partner

CPPR Country Portfolio Performance Review

CSP Country Strategy Paper

DHS Demographic and Health Survey

EAC East African Community

FDI Foreign Direct Investment

GAFSP Global Agriculture and Food Security Program

GCI Global Competitiveness Index

GDP Gross Domestic Product

GEF Global Environment Facility

GNI Gross National Income

GRZ Government of the Republic of Zambia

HDI Human Development Index

HIV/AIDS Human Immunodeficiency Virus / Acquired Immuno-Deficiency Syndrome

IDC Industrial Development Corporation

IFI International Financing Institution

IFMIS Integrated Financial Management Information System

IMF International Monetary Fund

IOP Indicative Operational Plan

IPP Independent Power Producer

MDB Multilateral Development Bank

MDG Millennium Development Goals

MIC Middle Income Country

MTEF Medium Term Expenditure Framework

NDP National Development Plan

NTF Nigeria Trust Fund

OSBP One-Stop-Border-Post

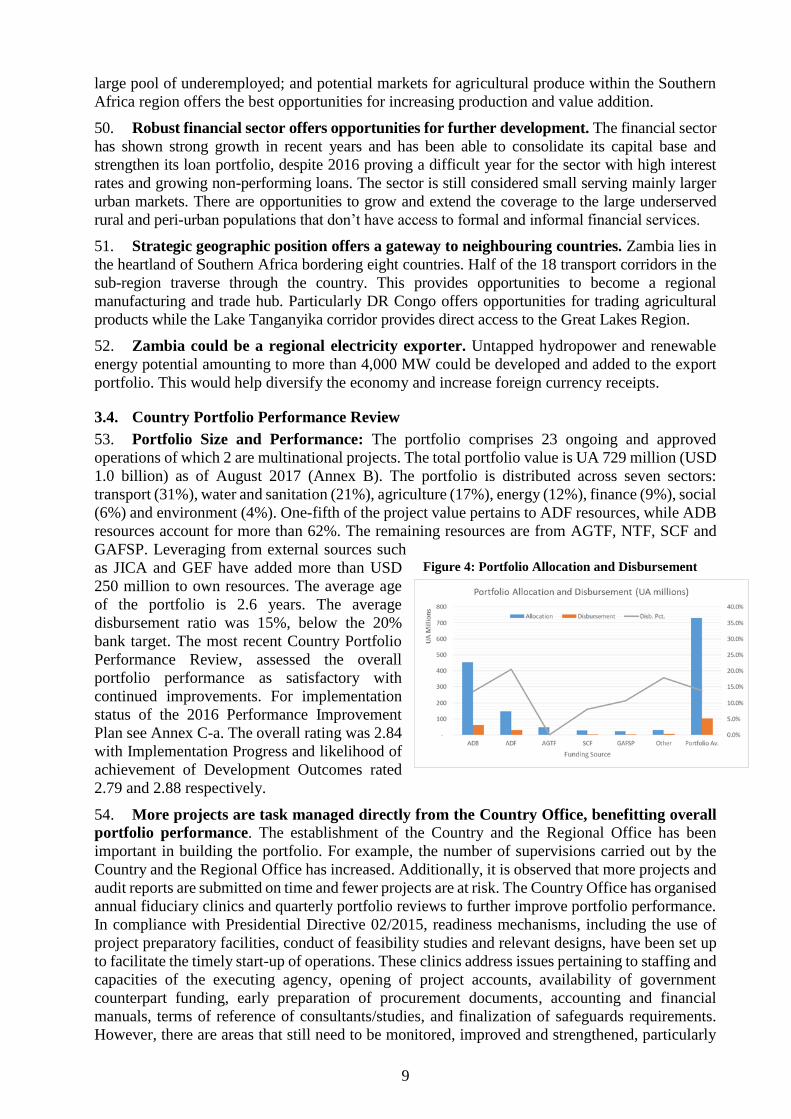

PAF Performance Assessment Framework

PBO Policy Based Operation

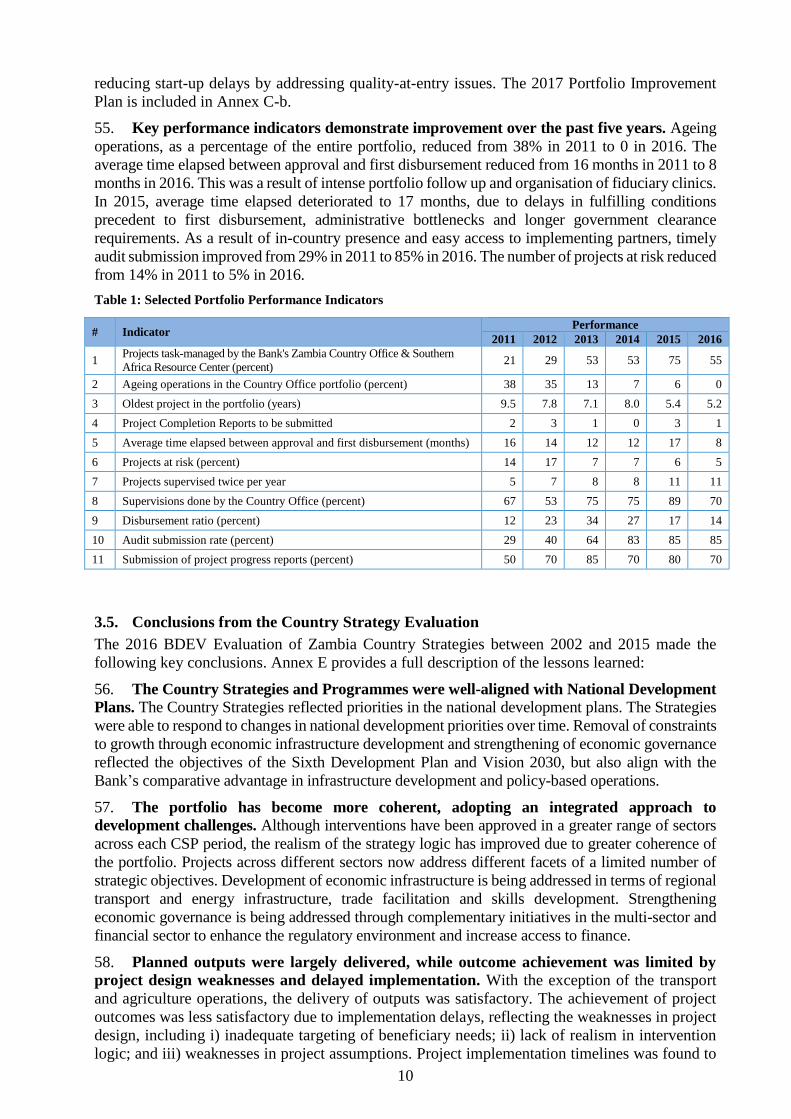

PFM Public Financial Management

PIU Project Implementation Unit

PRBS Poverty Reduction Budget Support

PSD Private Sector Development

RDGS Southern Africa Regional Development and Business Delivery Office

RRC Regional Resource Centre

R-SNDP Revised Sixth National Development Plan 2013-2016

SACMEQ Southern and Eastern Africa Consortium for Monitoring Education Quality

SADC Southern Africa Development Community

SCF Strategic Climate Fund

SI Statutory Instrument

SNDP Sixth National Development Plan 2011-2015

UA Unit of Account

USD United States Dollars

ZESCO Zambia Electricity Supply Company

ZMW Zambian Kwacha

ZAMBIA MAP

Source: Nations Online Project, www.nationsonline.org/oneworld/map/zambia

TABLE OF CONTENTS

EXECUTIVE SUMMARY ...................................................................................................... i

1. INTRODUCTION ......................................................................................................... 1

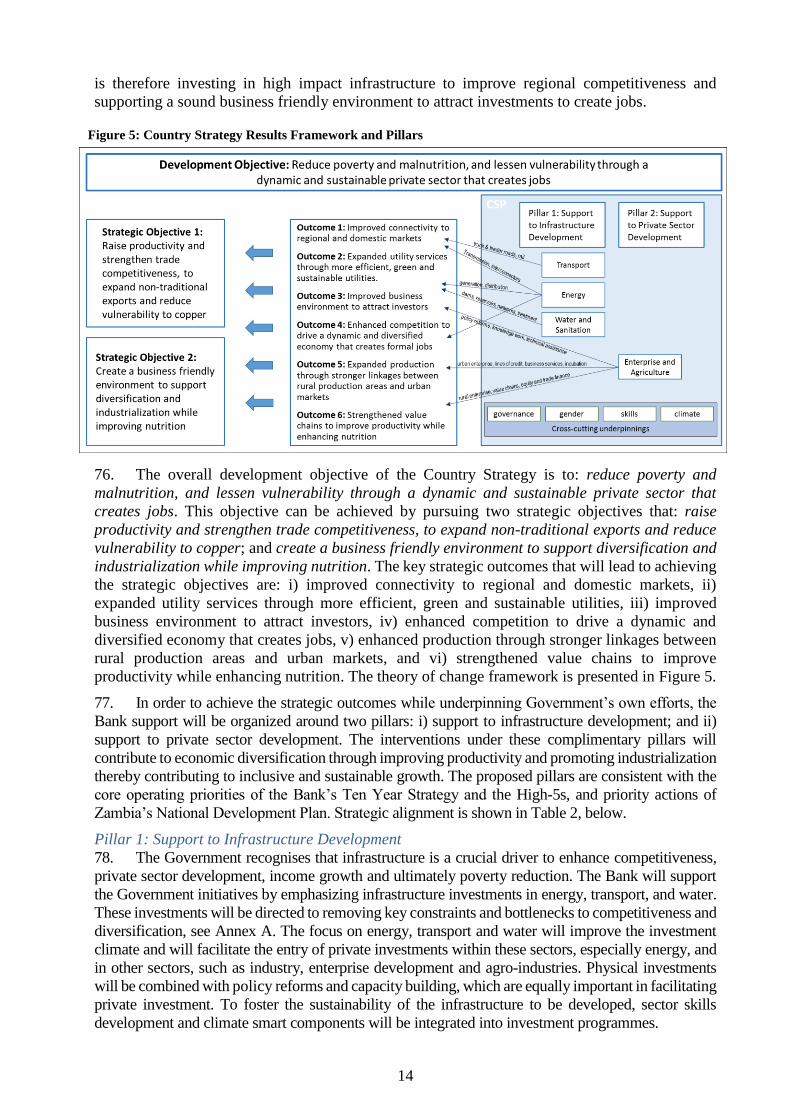

2. COUNTRY CONTEXT ................................................................................................ 1

2.1. Political Trends ....................................................................................................... 1 2.2. Economic Trends .................................................................................................... 2 2.3. Social and Poverty Trends ...................................................................................... 4

3. STRATEGIC OPTIONS ............................................................................................... 5

3.1. Country Strategic Framework ................................................................................ 5 3.2. Aid Coordination, Alignment and Harmonization ................................................. 7 3.3. Challenges and Opportunities ................................................................................ 7 3.4. Country Portfolio Performance Review ................................................................. 9 3.5. Conclusions from the Country Strategy Evaluation ............................................. 10

3.6. Lessons Learned ................................................................................................... 11

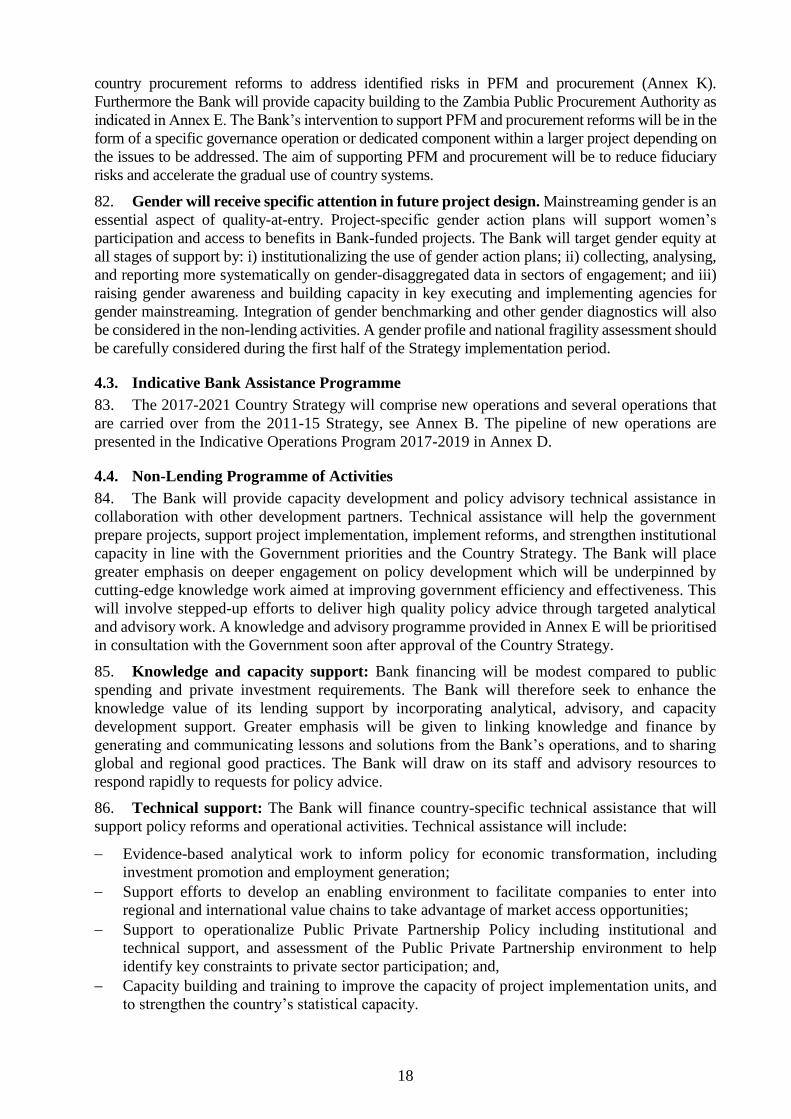

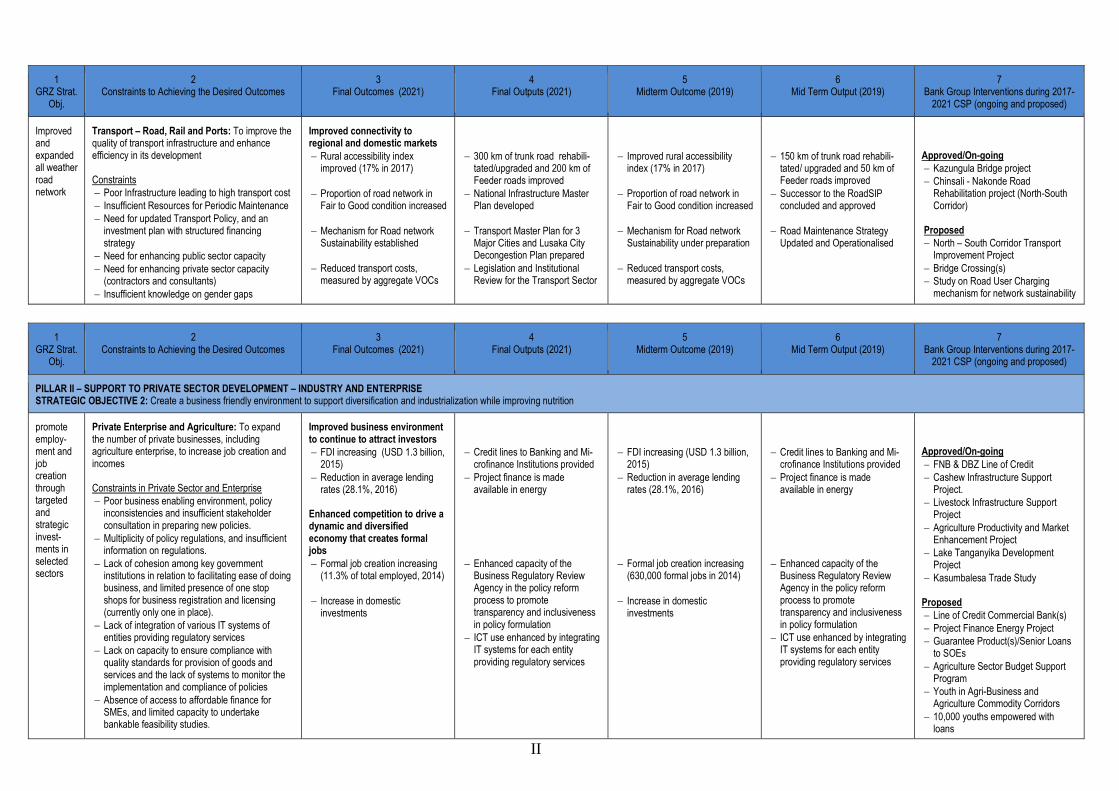

4. BANK GROUP STRATEGY FOR THE COUNTRY ............................................. 12

4.1. Rationale and Strategic Selectivity ....................................................................... 12 4.2. Development and Strategic Objectives and Outcomes ........................................ 13 4.3. Indicative Bank Assistance Programme ............................................................... 18 4.4. Non-Lending Programme of Activities ................................................................ 18

4.5. Financing of the Strategy ..................................................................................... 19 4.6. Monitoring and Evaluation of Bank Group Operations ....................................... 19

4.7. Country Dialogue Issues ...................................................................................... 20 4.8. Potential Risks and Mitigation Measures ............................................................. 20

5. CONCLUSION AND RECOMMENDATION ......................................................... 21

LIST OF ANNEXES

ANNEX A: INDICATIVE RESULTS FRAMEWORK

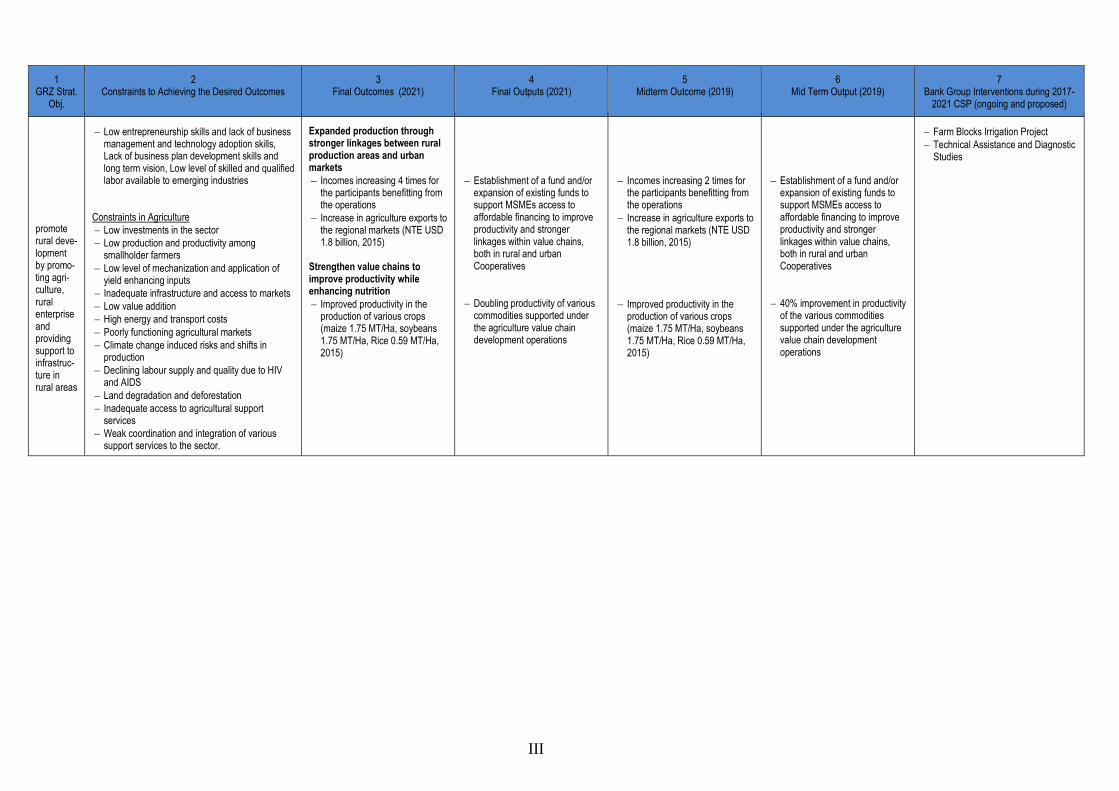

ANNEX B: BANK PORTFOLIO STATUS AS OF 01 AUGUST 2017

ANNEX C-a: PORTFOLIO PERFORMANCE IMPROVEMENT PLAN 2016 – STATUS

OF IMPLEMENTATION

ANNEX C-b: 2017 COUNTRY PORTFOLIO IMPROVEMENT PLAN

ANNEX D: INDICATIVE LENDING PROGRAM 2017-2019

ANNEX E: INDICATIVE NON-LENDING PROGRAM

ANNEX F: LESSONS LEARNED

ANNEX G: SELECTED ECONOMIC AND FINANCIAL INDICATORS

ANNEX H: PROGRESS TOWARDS ACHIEVING MILLENNIUM DEVELOPMENT

GOALS

ANNEX I: COMPARATIVE SOCIO ECONOMIC INDICATORS

ANNEX J: RISK AND DEBT ANALYSIS

ANNEX K: SUMMARY OF FIDUCIARY RISK ASSESSMENT REPORT 2016

ANNEX L: DIVISION OF LABOR

ANNEX M: ANALYTICAL REPORTS CONSULTED

LIST OF TABLES

Table 1: Selected Portfolio Performance Indicators ................................................................ 10

Table 2: Country Strategy Alignment with National Development Plan, 10-Year Strategy, and

High 5s ....................................................................................................................... 15

Table 3: Key debt indicators for selected years

Table 4: Public Expenditure and Financial Analysis trends between 2005 and 2016 Table 5: 2016 Public Financial Management Scores (based on PEFA framework)

LIST OF FIGURES

Figure 1: Competitiveness Indicators for Selected Countries .................................................... 2 Figure 2: Selected macroeconomic trends ................................................................................. 3 Figure 3: Key Strategic Growth Areas ....................................................................................... 5 Figure 4: Portfolio Allocation and Disbursement ...................................................................... 9 Figure 5: Country Strategy Results Framework and Pillars ..................................................... 14

Figure 6: Composition of External Debt (2016, pct.) Figure 7: Redemption Profile as at end-2016 (K billions)

LIST OF TEXT BOXES

Box 1: Recent Development in Energy Reforms ....................................................................... 6 Box 2: Employment and Education ........................................................................................... 8 Box 3: Alignment and Selectivity Criteria ............................................................................... 12

Box 4: Main Conclusions from the Bank Dialogue Mission ................................................... 13 Box 5: Indicative financing the Country Strategy .................................................................... 19

i

EXECUTIVE SUMMARY

1. The new Country Strategy was prepared between 2015 and 2017 when the Zambian

economy faced some of its worst macroeconomic and fiscal challenges since the 1980’s.

The 10-year period before 2011-12 was characterized by high growth averaging 7.4% per

annum and large foreign direct investments into a mineral-driven copper economy. The overall

fiscal performance reached a new low with a deficit of 10% of GDP in 2016. The Country

Strategy preparation process started in 2015, but faced substantial slippages due to delays in the

adoption of a new annotated format for the Bank’s Country Strategy Papers and a parallel

process of finalising the evaluation of Country Strategies for Zambia between 2002 and 2015.

The 2017-2021 Country Strategy framework and strategic pillars were finally endorsed by

CODE on November 14th, 2016, in a meeting that also discussed the achievements and lessons

from the previous CSP 2011-2015 and the Country Portfolio Performance Review. CODE

members recommended during the meeting that within the pillars there was a need for greater

selectivity, expansion of the macroeconomic and debt analysis, diversification of economic and

energy sectors, and strong focus on sustainability.

2. Despite being a middle income country, poverty continues to exceed 54% with rural

poverty around 77%. Social indicators are improving, but continue to mimic those in low

income countries. A key challenge has been the absence of inclusive growth and formal job

creation which stands at only 11% of the active labour force. Addressing the creation of

productive employment opportunities for the rising population is key to increasing

inclusiveness. Tackling structural impediments are therefore critical to unlock the private

sector. The past mineral-driven and public-sector led growth model therefore needs to be

transformed to stimulate broad based private sector led growth. Zambia’s National

Development Plan 2017-2021 recognizes the need for a new model for economic development

that aims to create a resilient diversified economy for sustained advanced growth and socio-

economic development. This approach entails Government to facilitate a business friendly

environment through structural reforms and regulatory adjustments while seeking to support

private-sector investments in high impact infrastructure.

3. The National Development Plan also recognizes that tackling infrastructure

bottlenecks will promote development and support growth in the private sector and lower

business costs. Only 25% of households have access to electricity of which rural access is even

lower at a meagre 3%. Reforming the power sector and facilitating investments to increase

generation, transmission and distribution capacity will help expand rural electrification and

support the growing demand from industry and urban households. The limited and poor linkages

between rural production areas and urban markets hampers private sector growth. Strengthening

these linkages will create more business and market opportunities. Access to safe water stands at

65% while access to improved sanitation is only 44%. Improving these indicators is a priority for

Government to contribute to a healthy and productive population.

4. Apart from attracting the private sector, the Government will be focused on

consolidating the budget during the next five years. Zambia Plus, the Government’s medium

term Economic Recovery Program from 2016, aims to restore budget credibility by reducing the

deficit to sustainable levels. Zambia Plus also aims to ensure greater economic stability, growth and

job creation through policy consistency to raise market confidence for sustained private sector

investment. This year, 2017, already looks to be a turning point with higher copper prices,

expanding mining production, improved agriculture harvest, stable exchange rates, low

inflation, and decelerating debt accumulation. Finally, Zambia Plus sets out some bold and

important reforms that among other things aims to reduce costly subsidies while shielding the

most vulnerable.

5. The Country Strategy 2017-21 proposes the Bank Group interventions for the next five

years based on discussions with key stakeholders in the country, and taking into account the

ii

lessons and recommendations emanating from previous Country Strategies. The Strategy also

considers the reclassification to Blend in 2014, which made considerable non-concessional (ADB)

resources available in excess of USD 1 billion. The Strategy therefore seeks a broader mandate than

previous Strategies in order to allow operational flexibility and adjustments to changes in

Government priorities.

6. The Country Strategy 2017-2021 has a stronger emphasis on private sector

development to support the industrialization and jobs creation agenda. The overall

development objective aims to: reduce poverty and lessen vulnerability through a dynamic and

sustainable private sector that creates jobs. This objective is achieved by pursuing two strategic

goals that: i) raise productivity and strengthen trade competitiveness, to expand non-traditional

exports and reduce vulnerability to copper; and ii) create a business friendly environment to

support diversification and industrialisation while improving nutrition. To achieve these

objectives two pillars are proposed. Pillar 1, Support to Infrastructure Development, will

include support to water and sanitation, energy and transport. This pillar is aligned to the Banks

Ten-Year Strategy priority area of infrastructure development, and scaling up High 5s of Light-

up and Power Africa. Pillar 2, Support to Private Sector Development, will underscore key

private sector areas, enterprise development and agriculture. This pillar is aligned to the Ten-

Year Strategy priority area of agriculture and food security, and scaling up High 5s of Feed

Africa and Industrialise Africa.

7. The Country Strategy will screen cross-cutting themes in the project design.

Evaluation recommendations suggested that a stronger attempt is made on promoting inclusive

and green growth while improving the mainstreaming of gender. The Strategy will concentrate

on cross-cutting areas that can be categorized in the following four themes: Gender; Climate;

Skills and Technology; and Economic and Governance Reforms. When preparing projects each

of these areas will be screened, reviewed and considered in the design and formulation of projects.

Certain cross-cutting areas will be more relevant for some operations than for others.

8. A project pipeline was developed in discussions with Government amounting to USD

1.2 billion taking into account the available funding. Apart from lending the Bank will also

increase its focus on non-lending operations. The Bank will place greater emphasis on policy

dialogue which will be underpinned by cutting-edge knowledge work. Technical assistance will

support preparation of projects, project and reform implementation, and strengthen institutional

capacity in line with the Government priorities. The Bank will provide capacity development

and policy advisory assistance in collaboration with other development partners.

9. The Bank portfolio in Zambia comprises 23 ongoing and approved operations of

which 2 are multinational. The net portfolio value is UA 729 million (USD 1.0 billion). The

three largest sectors in the portfolio include transport, water and sanitation, and agriculture.

More than 62% of funding is now from ADB resources. The average disbursement ratio is 15%

with an average project age of 2.6 years. The most recent Country Portfolio Performance

Review assessed the overall portfolio performance as satisfactory with a positive improvement

trend. More projects are increasingly task managed directly from the Country Office and the

Regional Resource Centre, benefitting overall portfolio performance.

10. The Boards of Directors are hereby requested to consider and approve Zambia’s

Country Strategy 2017– 2021.

1

1. INTRODUCTION

11. This paper proposes the Bank Group’s intervention strategy in Zambia for 2017 to 2021. The

Strategy is based on discussions with the Government, Cooperating Partners, the Private Sector,

civil society, and the lessons and recommendations emanating from the Independent Development

Evaluation 2002-2015 and the Zambia Country Strategy 2011-15 Completion Report. The Strategy

also takes into account the comments from CODE on the need for greater selectivity, expansion

of the macroeconomic analysis and debt sustainability, energy diversification, and sustainability

of interventions. The Strategy takes into account Zambia’s MIC status and the transition to Blend

in 2014, making considerable non-concessional resources available. The Strategy therefore seeks

a broader mandate in order to allow operational flexibility subject to the Government’s priorities.

12. Based on the conclusions and the recommendations of the Evaluation, the Country Strategy

2017-2021 proposes a stronger emphasis on private sector development. The development objective

aims to build a conducive investment environment for sustainable development to create jobs, reduce

poverty and malnutrition, and lessen vulnerability. The Evaluation also established the need to

continue to address infrastructure bottlenecks (Pillar 1: Support to Infrastructure Development) in

addition the dialogue mission confirmed Governments reorientation towards the private sector to

create jobs (Pillar 2: Support to Private Sector Development). These pillars aim to: i) raise

productivity and strengthen trade competitiveness, to expand non-traditional exports and reduce

vulnerability to copper, and ii) create a business friendly environment to support diversification and

industrialization while improving nutrition. The Strategy is aligned with the Government’s long term

Vision 2030 and the Seventh National Development Plan 2017-2021, and has taken Bank policies,

priorities and strategies into account. The High 5s are mainly addressed through Light-up and Power,

Feeding and Industrialising Africa.

13. Following the introduction, the paper is structured as follows: Chapter 2 presents the country

context from the political, economic, and social standpoints. Chapter 3 presents the strategic

options, including aid coordination and the Bank’s positioning in the country. Chapter 4 presents

the Bank’s intervention strategy for Zambia from 2017 to 2021. Chapter 5 concludes this paper

and presents the recommendation submitted to the Board.

2. COUNTRY CONTEXT

2.1. Political Trends

14. Zambia has remained peaceful and politically stable since independence, while public

institutions continue to mature. Multiparty elections were introduced in 1991, with the Movement

for Multiparty Democracy emerging as the governing party. Presidential, parliamentary and local

government elections have been held every five years. The MMD retained power for 20 years under

three presidents. At the national elections in 2011, the Patriotic Front under Michael Sata’s

leadership, defeated the MMD. His presidency was cut short due to illness after which PF front-

runner Edgar Lungu, was elected in 2015. General elections were held in August 2016 under a new

constitution. Edgar Lungu, retained his presidency, being the first president elected under a 50

percent plus one vote system and with a Vice President as running mate. The elections and the

aftermath have been characterised by waning political space for the opposition parties. This has been

most evident with the arrest of the opposition leader in April 2017 and the subsequent treason charge

for blocking the presidential motorcade.

15. Zambia is slowly improving good governance while strengthening its actions to tackle

corruption. The 2016 Mo Ibrahim Index (good governance), indicates a marginal improvement

from 58.0 in 2011 to 58.8 in 2015. Of the four areas monitored, two have shown improvements: rule

of law, and human development, while participation and human rights, and sustainable economic

opportunity has deteriorated. The Government has managed to improve accountability from 39.3 in

2011 to 42.5 in 2015. Despite these positive trends, the 2015 Transparency International Corruption

Index still places Zambia in the middle group (ranked 76) with a low score of 38/100.

2

16. Zambia faces limited fragility and transitional challenges. There are some factors that

could develop adversely over time if not addressed. It has been observed there is some degree of

political intolerance and exclusion of the media in political processes, relatively high urban youth

unemployment, and high dependence on the mining sector for reserves. Failing to address these

factors could affect overall economic performance, and lead to social and political instability.

2.2. Economic Trends

17. Between 2000 and 2010, the economy achieved impressive growth averaging 7.4% per

annum driving Zambia above the threshold for Middle Income Countries. Growth was driven

by investments in the mining sector spilling into construction, transport, communications, wholesale

and retail. High growth was facilitated by favourable copper prices underpinned by demand from

China, and increasing trade in the region. The global financial crisis during 2008/9 initially had

limited effects on the Zambian economy. The main transmission of instability was through falling

copper prices after 2011 that led to a slower growth trajectory (see Annex G and I for indicators).

18. The reduction in copper prices, and abnormal rainy seasons in 2014/5 and 2015/6

affected growth in mining and agriculture. The poor rains especially in the south of the country

reduced electricity generation from major hydro power plants. Combined with excess exchange

rate volatility and inflationary pressure in 2015 and 2016, wholesale and retail trade, financial

services, and transportation services were also affected. Real growth declined to 3.2% in 2016

putting real per capita growth at just 0.2%.

19. Although agriculture remains a small sector, it employs more than 2.9 million out of

5.9 million in employment. Agriculture is only the sixth largest (7.1% of GDP) sector. Wholesale

and retail trade employs 690,000 and is by far the largest sector, 22.6% of GDP. Mining, 10.5%;

construction, 10.2%; and manufacturing, 8.3% of GDP. Mining employs 82,000, construction

employs 183,000 while manufacturing 234,000. Education is fifth accounting for 7.6% of GDP

while employing more than 132,000 teachers creating substantial formal employment. There are

630,000 formally employed of which more than 1/3 are in central and local government.

20. Zambia remains a preferred investment destination in the region by many investors that

see the country as peaceful and with limited internal conflicts. Despite the slowing economy,

Zambia continues to attract foreign investors. In 2015, FDI amounted to USD 1.3 billion a reduction

from USD 2.1 billion in 2014. In previous years, mining received more than two thirds of investments,

but in 2015 manufacturing surpassed mining, receiving USD 604 million, compared to mining’s USD

325 million. Over the past decade, Government has taken several initiatives to improve the country’s

investment climate. Zambia was listed among the top-10 reformers in 2010, and ranked 98 out of 190

economies in the 2017 Doing Business ranking. Zambia has made good progress in the areas of ease

of starting a business, getting credit, paying taxes and dealing with construction permits. Six issues

stand out as far from best practice: i) trading across borders (rank 161), ii) getting electricity (rank

153), iii) resolving insolvency (rank 83), iv) enforcing contracts (rank 135), v) registering property

(rank 145) and vi) protecting minority investors (ranking 87). According to the 2016 GCI Zambia is

in the bottom fifth, ranked 118 out of 138 economies.

21. Rising expenditures and insufficient

revenues have led to deterioration of the

fiscal deficit. When PF took office, the

election promise was to increase public

investments in transport and energy while

putting more money in people’s pockets. This

led to a 45% wage adjustment for public

employees in 2013 pushing the wage bill to

over 61% of domestic tax revenues in 2014.

This entailed faster growth in expenditures

while revenues couldn’t keep up. The fiscal

deficit deteriorated reaching 10% of GDP in 2016 (commitment basis). During 2015 and 2016

Figure 1: Competitiveness Indicators for Selected Countries

3

arrears grew to 8.8% of GDP as public service providers and contractors where not being paid. The

Government acknowledges the need for fiscal consolidation, but has been slow to adjust. With the

2016 elections behind us there is increased optimism that Government will now be able to tighten

fiscal policy and pursue fiscal consolidation.

22. Borrowing to finance public infrastructure investments and fill gaps in the national

budget have increased public debt levels in recent years. Total debt stocks are estimated to

increase to about 56% of GDP in 2016 from 26% in 2012, with external debt accounting for 70%

of total debt. Zambia has accessed a total of USD 3 billion on international financial markets since

2012 in addition to concessional and non-concessional borrowing. The cost of Eurobond finance

has risen from 5.3% in 2012 to over 9% in 2015 adding to higher debt service payments. The sharp

depreciation of the Kwacha in 2015 increased external debt levels in kwacha terms, but also

increased debt servicing to an estimated 17% of domestic revenues in 2016. The risk of external

debt distress was therefore adjusted to moderate given the deterioration in debt dynamics (IMF,

Figure 2: Selected macroeconomic trends

4

2015). Under the baseline and alternative scenarios, all external debt sustainability indicators

remain below their applicable thresholds, but the debt-service-to-revenue ratio breaches the

threshold under various external shocks. Breaches coincide with Eurobond repayments during

2024 to 2028 period. Zambia’s overall public sector debt dynamics are sustainable under the

baseline. However, the large primary balance deficit underscores the need for improving the fiscal

position. Annex J provides additional analysis on the debt dynamics for the next five years.

23. Zambia is committed to an open, liberal trade regime and has put efforts into deepening

regional integration through regional and multilateral arrangements. This has been important

in promoting exports and to some extent economic diversification. Exports to the eight neighbouring

countries and South Africa increased from USD 1.3 billion in 2010 to USD 1.6 billion in 2015, while

imports increased from USD 3.3 billion to USD 3.9 billion. Trade with Congo DR peaked in 2013,

but still maintains a high level with USD 1.5 billion while South African trade amounts to USD 3.1

billion. Zambia hosts the headquarters of COMESA and remains active in SADC. Zambia has

affirmed its forward commitment to inter-regional trade by participating in the COMESA-EAC-

SADC-tripartite trade market. Zambia has also adopted a policy to establish one stop border posts

and trade centres at all its major borders as a way of expediting intra-regional and international trade.

24. This year, 2017, looks to be a turning point with increasing copper prices, expansion of

mining production, expectations of an improved agriculture harvest, stable exchange rate and

inflation and decelerating debt accumulation. The improved rains have ended load shedding from

8-10 hours per day in 2015/16 while new and rehabilitated mines will be ramping up production by

8-16% in the medium term. In 2016 the Government launched its Economic Recovery Program that

will focus on greater domestic resource mobilisation, improving fiscal governance, restoring budget

credibility and raising the confidence of the private sector. These reforms are needed to stimulate

growth in the economy. In the medium term, the economy is expected to exceed 4% growth, inflation

remaining within 6-9% range, and currency depreciation mirroring low inflation.

2.3. Social and Poverty Trends

25. Poverty remains endemic and widespread with gains in social and human development

lagging behind. Zambia’s high economic growth rate has not translated into equitable wealth

distribution. Poverty levels are high, with more than 54% of the population living below the

poverty line in 2015. Poverty remains predominantly geographically defined, with poverty highest

in rural areas at about 77% compared to 23% in urban areas. Poverty prevalence is higher in the

rural and remote areas, but the concentration of poverty is often located in urban areas. Urban

poverty incidence could rise in the future as urban population continues to grow while employment

opportunities are not created fast enough to follow suit. Evidence from Zambia indicates that the

level of education is important in reducing the risk of becoming poor. The 2015 HDI ranks Zambia

139. The score was 0.586 up from 0.555 in 2010 moving Zambia into medium developed countries

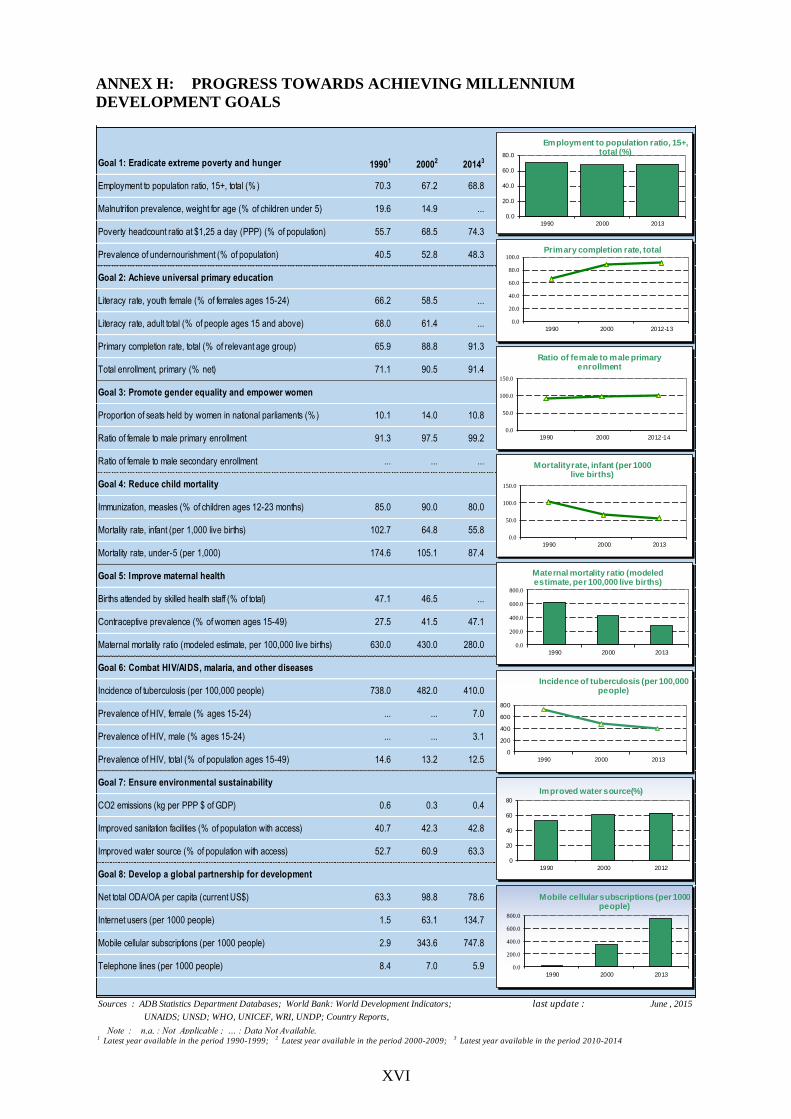

and above the average for Sub-Saharan Africa (0.502). Annex H provides data on MDG progress.

26. Gender equality is improving, but remains low in the region. The Gender Inequality

Index interprets loss in human development due to inequality between female and male

achievements in three dimensions: reproductive health, empowerment and economic activity.

Zambia has a low Gender Inequality Index of 0.587, ranking it 132 out of 154 countries. Female

participation in the labour market is 73% compared to 86% for men. In parliament, women only

occupy 18% of seats. This is well below the SADC target of 50% representation. In 2015, the first

female Vice President was appointed, and female participation in cabinet increased to 29%.

27. Primary school net enrolment has remained consistently above 95% for both girls and

boys, but quality of education lags behind. The 2014 national figures indicate that the combined

net enrolment is 100% for boys and girls. Primary school completion rates have increased reaching

over 99% in 2014. At the secondary school level school infrastructure and qualified teachers

remains in short supply. Net attendance rates are low, 38% for boys and 36% for girls. Pass rates

are low at only 60%, while dropout rates in lower secondary school reach as high as 39% in 2009

according to UNESCO. The quality of education is low according to studies from SACMEQ.

5

Particularly math and reading skills are poor compared to the region. Other areas contributing to

low quality are the high student-teacher ratio, limited access to teaching materials and resources,

and insufficient number of classrooms.

28. Maternal and child health outcomes are improving, while better access to treatment is

addressing the spread of HIV and AIDS. The 2014 DHS indicates that maternal mortality has

fallen to 398 deaths per 100,000 from 591 deaths per 100,000 in 2007. Improvements in other

areas include use of family planning services, reduction in child and infant mortality, and increase

in exclusive breastfeeding. Chronic malnutrition still remains a concern with prevalence above

40% in 2015, the second highest in Southern Africa. The Government target is to reduce stunting

to 30%. HIV and AIDS prevalence rates are decreasing in Zambia. The rate of HIV transmission

from mother to child has been halved to 12% in 2014 from 24% in 2009. This is attributed to

universal coverage of ARV treatment. Young women are still most at risk of being infected.

29. Two-thirds of the population do not have access to electricity. Less than 4% of households

in rural areas have access while 68% of urban households have access. The absence of energy

reforms and cost-reflective electricity tariffs has discouraged investments and led to insufficient supply

of generation capacity. This is evident with electricity generation that has been affected by two

droughts and the overuse of water at the critical Kariba Hydro Power Station. Growing demand for

electricity currently outstrips available supply.

30. Access to potable water is still below the required amounts for a sanitary and disease-free

environment, while sanitation and drainage systems in many areas are still underdeveloped. The

average consumption of water for drinking and other domestic use is not more than 20 liters per day

per rural household, i.e. approximately 5 liters per person per day (UNCTAD, 2006). Poor water

supply and sanitation services in peri-urban areas cause annual outbreaks of waterborne diseases

during the rainy season. This not only places a heavy economic burden on already impoverished

communities, but also on public health services. According to WHO/UNICEF more than 56% of the

population is still without access to improved sanitation facilities. Poorly constructed drainage systems

are inefficient during the rainy season leading to waterlogs on the roads or in market places.

3. STRATEGIC OPTIONS

3.1. Country Strategic Framework

31. Vision 2030 projects Zambia to become a prosperous

middle income nation through infrastructure and human

resource development to stimulate creation of wealth and

jobs. The development aim is set forth in Vision 2030,

providing a framework for Zambia’s aspirations. The Seventh

National Development Plan provides the overall strategic

direction and investment priorities for 2017-2021.

32. The NDP uses an integrated approach and sets out the

principles of accountability, efficient resource allocation and

effective utilization of resources. The overarching goal is

creating a resilient diversified economy for sustained

advanced growth and socio-economic development. The plan

rests on five pillars: i) economic diversification and job

creation; ii) reducing inequalities; iii) tackling poverty and

vulnerabilities; iv) enhancing human development; and v)

strengthening governance for diversification. The plan

recognizes key strategic growth areas, Figure 3. Agriculture is the major employer in the country,

while reliable infrastructure is vital to economic development promoting inclusive growth. By

raising labour productivity and lowering production costs, infrastructure will enhance economic

activity and contribute to creating jobs. While investing in infrastructure is a pre-requisite for

Figure 3: Key Strategic Growth Areas

6

achieving growth, Government also sees investments in health, education, water and sanitation as

critical for inclusive and sustainable growth in the long term.

33. Sufficient electricity generation will be important

for future development. The Government recognizes that

the energy sector is critical for powering businesses,

mining, manufacturing and the economy as a whole (2008

National Energy Policy and the 2017 Electricity Reform

Road Map). Energy reforms are high on the Governments

agenda and are needed to attract private sector through

Independent Power Producers and institutional investors

which will help to achieve the country’s generation targets

while creating a competitive environment for improving

efficiency, Box 1. Investments will be needed, to ensure

future generation surplus while expanding access. With

abundant water and other renewable energy resources

available, the Government aims to turn Zambia into an electricity exporter.

34. To reduce transport costs, good quality and expanded transport is key to linking the

country’s provinces and districts. The Government prioritises the development of the main

transport corridors as stated in the National Transport Policy and the Road Sector Framework 2012-

2022. Link 8000 plans to construct and rehabilitate 8000 km of trunk and main roads. The Pave

Zambia 2000 aims to pave urban roads in 17 districts across the country, and L400 aims to

rehabilitate the road network in Lusaka. Implementation has been mixed as a result of the fiscal

pressures. A national infrastructure master plan has been developed in 2017. A shift from rail to road

presents advantages in the cost to government through reduced maintenance costs. Shifting cargo to

rail would result in reduced traffic loads mitigating premature road failures and help provide good

road transport. Viable business models will need to be explored while private sector investment

would be required to supplement the government’s limited resources into rail transport systems.

35. The Government aims to establish an agriculture sector that is commercially oriented,

competitive, productive, diversified, and driven by principles of equity and sustainability. The development of agriculture, livestock, fisheries and forestry are considered national

development priorities. The Agriculture Policy sees these priorities as key drivers in creating jobs,

enhancing inclusive growth, addressing climate change, and diversifying the economy. In the area

of agricultural diversification, the Government intends to promote cash crops such as cotton,

cashew nuts, soya beans, cassava, horticulture and rice. Government is also actively supporting

farmers to exploit investment opportunities in dairy, beef, small ruminants, poultry and

aquaculture value chains. Government is further supporting aquaculture parks to improve the

availability of fingerlings, while encouraging the private sector to participate in the establishment

of fish feed plants, freezing facilities, and offering fiscal incentives to the aquaculture sub-sector.

36. The development of a dynamic private sector is key to creating the hundred thousand jobs

needed to keep up with annual entry into the labour market. Economic diversification will lead to

lower copper dependency and vulnerability to external shocks. The Private Sector Development and

Competitiveness Strategy and the 2013 Industrialisation and Jobs Creation Strategy are critical

Government documents outlining the diversification strategy. Diversification will require, among

others, improving technology and innovation, improving skills, raising productivity, ensuring low cost

inputs, and establishing marketing and distribution channels. Expanding and growing micro, small and

medium sized enterprises through business development services and affordable access to finance and

promoting partnerships between local and international firms will also be important. The 2015 Youth

Policy promotes skilled, enlightened, and economically empowered youth to impact national

development. In 2014, the IDC was created to take ownership of 34 State Owned Enterprises to

commercialize and attract foreign partners/investors. Multi-facility economic zones are being

developed. These zones provide investor incentives to attract local and foreign investors.

Government took bold steps in November 2016

by increasing fuel prices by more than 40% to

ensure cost-reflectivity on fuel imports. As of May

2017, non-mining electricity tariffs were raised by

an initial 50% contributing to improvement in

ZESCO cash flows (and a reduction of indirect

subsidies). An additional 25% increase is planned

for September 2017 as well as negotiations with

mining houses is nearing a conclusion that will

raise their tariffs to an average of 9.3 US-

cents/kWh. These measures will help to reduce

pressure on the fiscal deficit in the medium term.

Box 1: Recent Development in Energy Reforms

7

3.2. Aid Coordination, Alignment and Harmonization

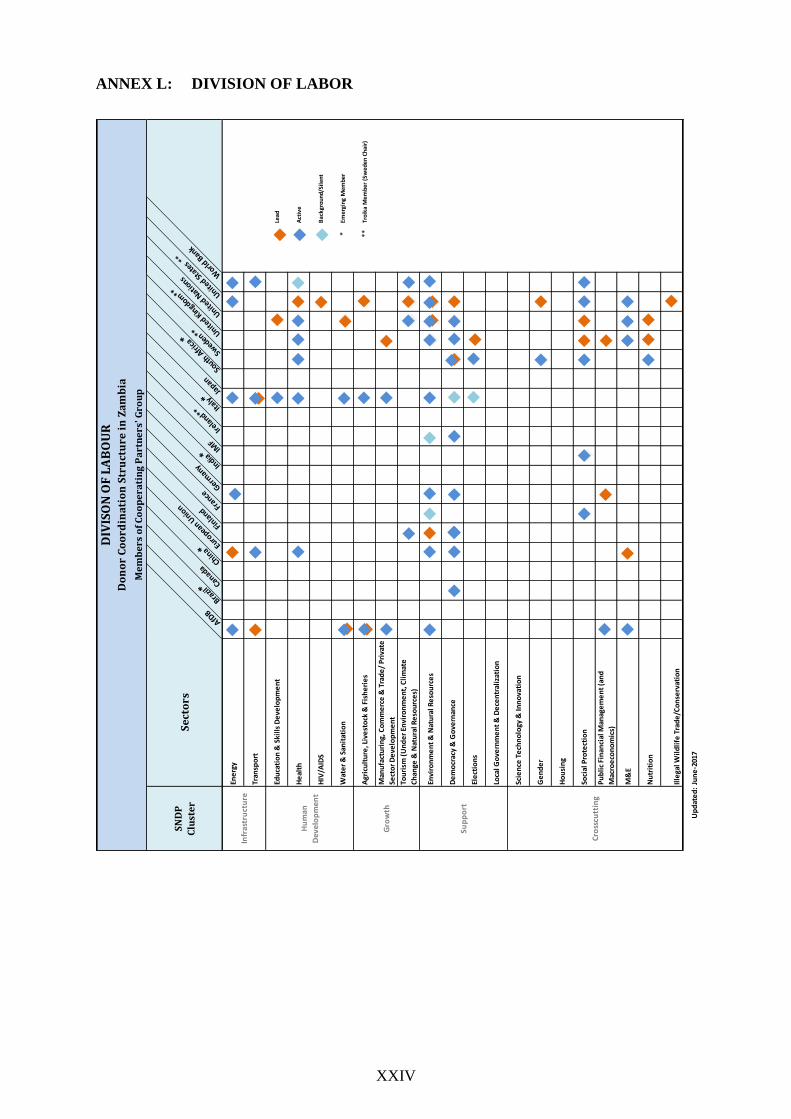

37. The Joint Assistance Strategy 2011-15 and the Division of Labour are the main aid

coordination instruments. The Strategy sets out the Cooperating Partners support to the NDPs,

provides the medium term framework to realize the aid principles, and aligns development to the

Aid Policy and Strategy. For coordination purposes the Division of Labour is regularly updated

and included in Annex L. As the Joint Assistance Strategy remains relevant and valid there are no

immediate plans to have this revised.

38. The high level aid architecture is well structured and institutionalized through the CP

Group led by a Troika. The Troika holds monthly meetings with the Secretary to the Treasury,

the Permanent Secretary of Planning and their teams. In addition, Joint Sector Working Groups

hold regular meetings that provide a platform for policy dialogue. Issues that cannot be resolved

at working group level can be elevated to the CP group. The Bank is active in the CP group and

led the Troika in 2012. The Bank participates in relevant working groups and has previously

chaired the following working groups: transport (since 2014), agriculture (2013), water and

sanitation (2012 and 2015) and monitoring and statistics (2014 and 2015).

39. Country dialogue is carried out at various levels of Government. The CP Group leads the

high-level dialogue with Government. The Bank, through the Resident Representative, the Country

Programme Officer and the Country Economist, engage with Government, particularly the Ministry

of Finance, Ministry of Planning, and the Bank of Zambia, at relevant entry points. Sector staff are in

regular contact with their counterparts and participate in the activities of various sector working groups.

40. Development aid from traditional bilateral donors is declining. Over the past 15 years

development aid has fallen from 23 to 4% of GNI. In 2015, total bilateral aid fell to USD 572

million while multilateral aid amounted to USD 311 million. About 4/5 of aid ends in health and

social sectors. The waning development assistance is being filled by increased foreign direct

investment and by accessing international credit markets. Emerging development partners from

China and South Africa (i.e. DBSA) are increasing support.

3.3. Challenges and Opportunities

41. The main challenges stem from the infrastructure gaps that remain in transport, energy, and

water and sanitation. These sectors are key enablers for private sector and human development.

Keeping up with the growing demand for electricity is crucial to avoid load shedding. Other

challenges stem from limited diversification and the high dependence on copper. Growing demand

in domestic and regional markets offer opportunities in agriculture and manufacturing, but limited

policy consistency and coordination have led to private sector uncertainty, reducing potential

investment and growth. The private sector regulatory framework is therefore a crucial component

that must be accommodative to attract investors and support local businesses, benefiting employment

generation and consumers. Skilled and qualified labor are key to promote innovation, increase

productivity, and improve efficiency in production and business.

Challenges and Weaknesses

42. Infrastructure deficits increase business costs and lower the quality of services. The high

cost of transport and demanding non-tariff trade barriers reduces the potential of regional trade. The

limited maintenance and poor quality of roads has increased the cost of transport to as much as 40%

of the value of goods. It is estimated that 87% of trunk roads are in good condition compared to less

than 10% of feeder roads. One stop border posts support the flow of goods, but non-tariff trade

barriers still increases trade costs. Competitive and efficient transport corridors are critical to

growing the economy. Limited investment in electricity infrastructure affected power supply in 2015

and 2016 impacting business. An inefficiently performing utility, energy tariffs set below the cost of

supply, and scarce reforms has led to underinvestment in the sector. Sustainable service delivery and

reliability of water supply and sanitation is affected by deteriorating infrastructure. Pressure on

access to water and sanitation will continue to grow due to urbanization and unplanned expansion

of peri-urban areas. Maintaining existing infrastructure and enhancing management, project

appraisal, and planning are critical skills for developing future quality infrastructure.

8

43. High dependency on copper for export earnings increases vulnerability to commodity

shocks. The country remains highly dependent on copper earnings for 60-70% of its foreign currency

reserves. When copper prices slump this increases the risk of macro-economic instability. Although

non-traditional exports have grown in the past few years there is need to diversify and expand the

production base of the economy while increasing the basket of goods that can be exported.

44. Policy uncertainty and predictability lowers appetite for investment and private sector

expansion. Red tape, bureaucratic procedures, limited information of licensing requirements in

certain industries, low government capacity and service mindedness, low entrepreneurship capacity

and access to information on market conditions, and high interest rates constrains private sector

development. Cumbersome licensing and inspection procedures adds to company costs while

smaller businesses often can’t attain compliance with regulations due to the lack of capacity and

knowledge of the regulations. Policies and regulations are often prepared without private sector

consultation leading to suboptimal outcomes. Although private sector reforms are on-going

implementation is often constrained by insufficient resources, weak capacity and inadequate inter-

ministerial coordination. A predictable business environment with access to market information will

increase investment and boost private sector activity creating (formal) jobs.

45. Inadequate skills and skills mismatch reduces innovation, and maintains low productivity

and competitiveness. Low quality of general education affects the quality of technical and academic

skills. Poor coordination and planning leads to a mismatch

between skills supplied and skills demanded. The limited skills

reduces the potential uptake of innovation, reducing

productivity and competitiveness of local firms. The labour

market lacks flexibility, while being oriented towards protecting

the rights of workers. This implies that firms have less incentive

to employ permanent employees if it is difficult to adjust the

workforce based on the market conditions. The informal sector

accounts for 89% of employment. For Zambia to finance and

develop more rapidly there is need for a higher degree of

formalization to broaden the tax base and collect more revenues

for public investments and operations.

46. Changing climate is expected to increase the number of extreme weather events, with

longer dry spells or more severe rains, that may cause drought, waterlogging, or flooding.

47. Poverty remains endemic in rural areas and growing risk of poverty in urban

communities. Scarce opportunities and limited economic participation in rural areas maintains

high levels of poverty and poor quality of life. The sluggish (formal) job growth in urban

communities will add to urban poverty in the future, leading to increasing inequality, which left

unattended, could lead to more serious social inequalities.

Strengths and Opportunities

48. More than a decade of macro stability has helped grow the consumer market providing

local opportunities for services and manufacturing. Zambia enjoyed high growth and macro

stability from 2000. This was attributed to effective implementation of macro policies and

privatization that boosted the economy and provided room for further development. Despite poverty

remaining a challenge, growth has increased purchasing power for a growing group of Zambians

further expanding the domestic market. This provides increased opportunities for local production,

manufacturing, and services creation.

49. Agriculture provides an opportunity for diversifying away from mineral dependency.

Primary agriculture contributes about 35% to the country’s total non-traditional exports and about

10% of the total export earnings for the country. Agriculture is widely acknowledged as one of the

top priorities for economic diversification from mineral dependency. The availability of large

tracts of unutilized fertile soils; abundant water resources; conducive climate for agriculture; a

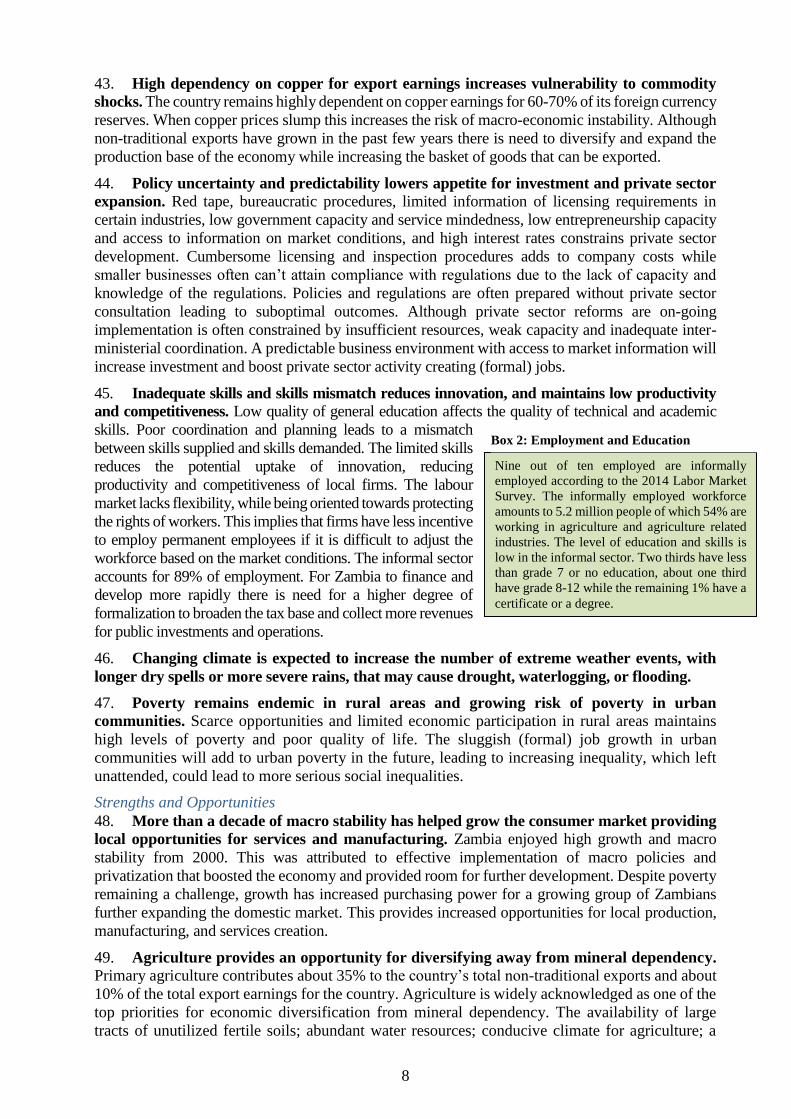

Nine out of ten employed are informally

employed according to the 2014 Labor Market

Survey. The informally employed workforce

amounts to 5.2 million people of which 54% are

working in agriculture and agriculture related

industries. The level of education and skills is

low in the informal sector. Two thirds have less

than grade 7 or no education, about one third

have grade 8-12 while the remaining 1% have a

certificate or a degree.

Box 2: Employment and Education

9

large pool of underemployed; and potential markets for agricultural produce within the Southern

Africa region offers the best opportunities for increasing production and value addition.

50. Robust financial sector offers opportunities for further development. The financial sector

has shown strong growth in recent years and has been able to consolidate its capital base and

strengthen its loan portfolio, despite 2016 proving a difficult year for the sector with high interest

rates and growing non-performing loans. The sector is still considered small serving mainly larger

urban markets. There are opportunities to grow and extend the coverage to the large underserved

rural and peri-urban populations that don’t have access to formal and informal financial services.

51. Strategic geographic position offers a gateway to neighbouring countries. Zambia lies in

the heartland of Southern Africa bordering eight countries. Half of the 18 transport corridors in the

sub-region traverse through the country. This provides opportunities to become a regional

manufacturing and trade hub. Particularly DR Congo offers opportunities for trading agricultural

products while the Lake Tanganyika corridor provides direct access to the Great Lakes Region.

52. Zambia could be a regional electricity exporter. Untapped hydropower and renewable

energy potential amounting to more than 4,000 MW could be developed and added to the export

portfolio. This would help diversify the economy and increase foreign currency receipts.

3.4. Country Portfolio Performance Review

53. Portfolio Size and Performance: The portfolio comprises 23 ongoing and approved

operations of which 2 are multinational projects. The total portfolio value is UA 729 million (USD

1.0 billion) as of August 2017 (Annex B). The portfolio is distributed across seven sectors:

transport (31%), water and sanitation (21%), agriculture (17%), energy (12%), finance (9%), social

(6%) and environment (4%). One-fifth of the project value pertains to ADF resources, while ADB

resources account for more than 62%. The remaining resources are from AGTF, NTF, SCF and

GAFSP. Leveraging from external sources such

as JICA and GEF have added more than USD

250 million to own resources. The average age

of the portfolio is 2.6 years. The average

disbursement ratio was 15%, below the 20%

bank target. The most recent Country Portfolio

Performance Review, assessed the overall

portfolio performance as satisfactory with

continued improvements. For implementation

status of the 2016 Performance Improvement

Plan see Annex C-a. The overall rating was 2.84

with Implementation Progress and likelihood of

achievement of Development Outcomes rated

2.79 and 2.88 respectively.

54. More projects are task managed directly from the Country Office, benefitting overall

portfolio performance. The establishment of the Country and the Regional Office has been

important in building the portfolio. For example, the number of supervisions carried out by the

Country and the Regional Office has increased. Additionally, it is observed that more projects and

audit reports are submitted on time and fewer projects are at risk. The Country Office has organised

annual fiduciary clinics and quarterly portfolio reviews to further improve portfolio performance.

In compliance with Presidential Directive 02/2015, readiness mechanisms, including the use of

project preparatory facilities, conduct of feasibility studies and relevant designs, have been set up

to facilitate the timely start-up of operations. These clinics address issues pertaining to staffing and

capacities of the executing agency, opening of project accounts, availability of government

counterpart funding, early preparation of procurement documents, accounting and financial

manuals, terms of reference of consultants/studies, and finalization of safeguards requirements.

However, there are areas that still need to be monitored, improved and strengthened, particularly

Figure 4: Portfolio Allocation and Disbursement

10

reducing start-up delays by addressing quality-at-entry issues. The 2017 Portfolio Improvement

Plan is included in Annex C-b.

55. Key performance indicators demonstrate improvement over the past five years. Ageing

operations, as a percentage of the entire portfolio, reduced from 38% in 2011 to 0 in 2016. The

average time elapsed between approval and first disbursement reduced from 16 months in 2011 to 8

months in 2016. This was a result of intense portfolio follow up and organisation of fiduciary clinics.

In 2015, average time elapsed deteriorated to 17 months, due to delays in fulfilling conditions

precedent to first disbursement, administrative bottlenecks and longer government clearance

requirements. As a result of in-country presence and easy access to implementing partners, timely

audit submission improved from 29% in 2011 to 85% in 2016. The number of projects at risk reduced

from 14% in 2011 to 5% in 2016.

Table 1: Selected Portfolio Performance Indicators

3.5. Conclusions from the Country Strategy Evaluation

The 2016 BDEV Evaluation of Zambia Country Strategies between 2002 and 2015 made the

following key conclusions. Annex E provides a full description of the lessons learned:

56. The Country Strategies and Programmes were well-aligned with National Development

Plans. The Country Strategies reflected priorities in the national development plans. The Strategies

were able to respond to changes in national development priorities over time. Removal of constraints

to growth through economic infrastructure development and strengthening of economic governance

reflected the objectives of the Sixth Development Plan and Vision 2030, but also align with the

Bank’s comparative advantage in infrastructure development and policy-based operations.

57. The portfolio has become more coherent, adopting an integrated approach to

development challenges. Although interventions have been approved in a greater range of sectors

across each CSP period, the realism of the strategy logic has improved due to greater coherence of

the portfolio. Projects across different sectors now address different facets of a limited number of

strategic objectives. Development of economic infrastructure is being addressed in terms of regional

transport and energy infrastructure, trade facilitation and skills development. Strengthening

economic governance is being addressed through complementary initiatives in the multi-sector and

financial sector to enhance the regulatory environment and increase access to finance.

58. Planned outputs were largely delivered, while outcome achievement was limited by

project design weaknesses and delayed implementation. With the exception of the transport

and agriculture operations, the delivery of outputs was satisfactory. The achievement of project

outcomes was less satisfactory due to implementation delays, reflecting the weaknesses in project

design, including i) inadequate targeting of beneficiary needs; ii) lack of realism in intervention

logic; and iii) weaknesses in project assumptions. Project implementation timelines was found to

# Indicator Performance

2011 2012 2013 2014 2015 2016

1 Projects task-managed by the Bank's Zambia Country Office & Southern

Africa Resource Center (percent) 21 29 53 53 75 55

2 Ageing operations in the Country Office portfolio (percent) 38 35 13 7 6 0

3 Oldest project in the portfolio (years) 9.5 7.8 7.1 8.0 5.4 5.2

4 Project Completion Reports to be submitted 2 3 1 0 3 1

5 Average time elapsed between approval and first disbursement (months) 16 14 12 12 17 8

6 Projects at risk (percent) 14 17 7 7 6 5

7 Projects supervised twice per year 5 7 8 8 11 11

8 Supervisions done by the Country Office (percent) 67 53 75 75 89 70

9 Disbursement ratio (percent) 12 23 34 27 17 14

10 Audit submission rate (percent) 29 40 64 83 85 85

11 Submission of project progress reports (percent) 50 70 85 70 80 70

11

be unsatisfactory across all sectors. Progress was made in addressing delays to loan effectiveness

and first disbursement, while challenges arising from multiparty co-financing arrangements was

affected by the need to harmonise terms, conditions and procurement arrangements.

59. The Bank contributed to increasing access to basic services and improving the business

environment while opportunities for upscaling private investment were not leveraged. At the

country level, the Bank contributed to improving access to basic services, including water, sanitation,

power and health. In contrast, efforts to strengthen public financial management were less successful.

Notably, these gains were not only the result of direct investments in each sector. Increased access

to services and business development also resulted from large private sector investments. However,

opportunities to complement and upscale these private investments were not pursued.

60. Political and governance risks are increasingly important factors in the sustainability

of projects. These risks include regulatory changes implemented without consultation,

irregularities in procurement, and lack of political will to address inadequate tariff regimes. For

example, the sustainability of lines of credit projects were limited by the introduction of interest

rate caps and increased capital reserve requirements. Investments in utilities face challenges due

to the absence of cost-reflective tariffs.

61. Activities attempted to promote inclusive and green growth, while opportunities to

mainstream gender were not fully leveraged. Projects attempted to promote sustainable

investment as well as reduce disparities between urban and rural areas. However, opportunities were

not always leveraged to generate business development and employment opportunities for women.

Lines of credit and agriculture projects demonstrated that such initiatives should be supported by

targeted project interventions. More could also be done to promote direct employment opportunities

for women within infrastructure and industrial projects.

3.6. Lessons Learned

The lessons learned from previous CSPs have been taken into account in this Strategy and will be

carefully considered in all future operations.

Quality-at-Entry and Start-up Delays

62. Requiring preconditions to be met at pre-appraisal instead of creating conditions

precedent will reduce start-up delays: Attaining conditions precedent posed difficulties for some

projects, resulting in significant delays. This was often due to requirements about certain

regulations and/or studies to be carried out. The Bank now aims to address difficult preconditions

at an early stage as part of the pre-appraisal process, before Board approval, thereby reducing

delays. Most public sector operations also have simplified conditions precedent to first

disbursement, but meeting conditions precedent to effectiveness are still delayed from the side of

Government. The actions are in line with the Presidential Directive 02/2015.

63. Early sensitisation and conditional approval by authorities could help reduce start-up

delays: Critical delay factors relate to government policy requiring approval by cabinet, parliament

and attorney general before a loan agreement can be signed. To reduce delays, the Country Office

will start early sensitisation of approving authorities concerning project objectives, components,

cost/loan size and financing terms. Early sensitisation will entail obtaining approval from all relevant

authorities of the negotiated and initialled loan agreement prior to submitting a project to the Board.

64. Encourage task managers to use existing facilities to initiate pre-feasibility studies,

early procurement preparation, to help reduce start-up delays: The Bank has at its disposal

various trust funds and project preparation facilities that should be used more systematically to

initiate pre-feasibility, feasibility, design, and procurement preparation. This will contribute to

quicker start-up of operations and reduce delays related to procurement, disbursement, etc.

Implementation capacity and monitoring

65. Continue to support project implementation, monitoring and evaluation capacity

through training: As part of the measures to improve project implementation capacity, the Bank

12

should on a continuous basis organise project implementation training workshops in the areas of

procurement processing, familiarisation of standard bidding documents, setting up monitoring and

evaluation information systems, and contract and disbursement management. The Country Office

will continue to assist project accountants and procurement officers to identify implementation

issues as soon as they arise. Project staff will receive refresher training on the progress reporting

system in order to track outputs and outcome indicators, and assess performance in relation to

annual targets for disbursement and procurement.

Results Framework

66. Clear formulation of strategic objectives to strengthen indicator linkage and

measurability: A clear theory of change and results matrix will improve the linkage between the

Bank’s overall Strategy with that of the National Development Plans. Some objectives in the results

framework were too narrowly defined while indicators were vaguely specified and did not provide

adequate information on what was measured. The design of the Results Based Framework (Annex

A) has been improved through better formulation of strategic objectives and outcomes.

Bank Presence

67. The Bank’s physical presence in Zambia has made it possible to strengthen

relationships and enhance policy dialogue: The in-country presence has provided visibility,

direct and quick access to the government, cooperating partners, and the private sector. It has also

strengthened the relationship with Government and improved policy dialogue. Furthermore, it has

enabled building local networks and expanding the portfolio while leveraging finance from

development partners. The Bank will continue to strengthen its local presence and build capacity

to provide implementation support and supervision of Bank funded operations.

4. BANK GROUP STRATEGY FOR THE COUNTRY

This section provides the rationale for the selection of pillars based on selectivity criteria agreed with

the government. The section also outlines the Country Strategy’s objectives and outcomes

established for the next five years, and discusses the two selected pillars including the Banks

deliverables. Finally, the section provides an overview of the non-lending activities, the financing of

the Strategy, monitoring and evaluation, policy dialogue and the implementation risks.

4.1. Rationale and Strategic Selectivity

68. The design of the Country Strategy and

the overall results framework was based on a

set of alignment and selectivity criteria, Box 3.

In order to leave a visible footprint and avoid

spreading resources to thinly the focus was on a

few key sectors to ensure high development

impact, while retaining flexibility given Zambia’s

MIC status. The proposed pillars and strategic

objectives are the result of efforts by the

Government and the Bank to pursue a deeper

partnership between 2017 and 2021 and to support

Zambia’s aspirations under its NDP. A Country

Strategy Dialogue Mission took place from 23 to

27 January 2017 to validate the Strategic Approach. The selected pillars and sectors considered

for support, the key government policies, sector challenges and opportunities were discussed

during the mission. The main conclusions are summarised in Box 4, below.

69. Maintaining strong growth has been a challenge in recent years. The Zambian economy

is struggling in the aftermath of a collapse in copper prices and electricity shortages. Investor

confidence has been hit hard as a result. The exchange rate depreciated sharply, inflation soared,

the fiscal deficit widened, and public debt rose rapidly in 2014 and 2015. The increase in debt

The following criteria were applied in designing the

Strategy and selecting priorities:

- Country priority and continuation of current support,

- Utilise the Banks comparative advantage in

infrastructure development, while seeking opportunities

for partnerships,

- Synergies between national projects and those in

neighbouring countries,

- Complies with the division of labour, and

- Complies with the Bank’s strategy and priorities (Ten-

Year Strategy and High-5s)

Box 3: Alignment and Selectivity Criteria

13

slowed in 2016 with the stabilisation of the Kwacha. Much of the problems emanated from the

collapse in copper prices, fiscal indiscipline, and policy uncertainties.

70. Despite that Zambia is a

MIC, poverty continues to

exceed 54% with rural poverty

around 77%. Social indicators

are improving, but continue to

mimic those in low income

countries.

71. Zambia is still early in its

transition from low income, but

needs to deepen its reforms, not

least in the private sector. The

recent declining trend in growth

may exacerbate the country’s

already high income inequality and persistent unemployment. These issues are linked to the

absence of productive employment opportunities for the growing population. Tackling structural

unemployment is important to improve the quality of economic growth. Private sector led

investment is essential if Zambia is to unleash its growth potential. This will require decisive

reforms and innovative policies to increase productivity, competitiveness and diversification.

72. Addressing infrastructure bottlenecks will promote development and support growth

in the private sector and lower business costs. Expanding rural electrification and supporting

the growing industry and household demand for electricity requires reforms in the power sector

and new investments. Improving transport linkages between rural production areas and urban

markets will spur private sector growth and create more opportunities in agriculture, forestry and

aquaculture. Access to improved water and sanitation in rural and peri-urban areas remains limited

to many citizens. Increasing access to these services will contribute to a healthy and productive

population. Achieving water security is furthermore an enabler for private sector development,

reducing business costs, and creating employment opportunities in the private sector.

73. Zambia’s NDP 2017-2021 recognizes that a new economic model for economic

development is required. The past mineral-driven and public-sector led growth models need to

be reviewed to make the case for a national transformation to stimulate private sector led growth.

Transforming the structure of the economy has long been recognized, but the sense of urgency is

more apparent. An ambitious agenda for new sources of economic growth and employment needs

to be set. High and sustainable growth requires a productivity-driven economy. This approach

requires Government to facilitate a business friendly environment through regulatory and

structural adjustments while seeking to support private-sector investments. Investments in

productive infrastructure will address key bottlenecks to growth. Appropriate safeguards and

rationalisation of bureaucratic procedures, allows greater use of Public Private Partnerships that

would mobilize and enhance private sector participation in the economy.

74. While the Bank cannot address all facets of Zambia’s growth challenges, it can provide

support in priority areas: The Bank’s resources are limited, but can be utilised to crowd in

additional resources. The Bank’s experience in facilitating national and regional projects,

combined with expertise in the various sectors and an understanding of the country’s knowledge

requirements could be brought to bear. The Strategy will ensure that Bank support remains well-

aligned to the Government’s development agenda.

4.2. Development and Strategic Objectives and Outcomes

75. Reducing poverty and inequality, and eliminating the vulnerabilities of large sections of the

population remain the principal challenges to inclusive growth. In view of the persistence of

insufficient formal job growth, the quality of growth deserves greater attention. The government

- The mission took place during the final preparation of the NDP 2017-21

and confirmed that the selected sectors are high priority to the Government.

- The government was advised that ADB resources where dependent on

macroeconomic factors that could deteriorate.

- A pipeline of potential projects was agreed.

- A list of possible studies, capacity building and other non-lending

activities was discussed. This list to be prioritized following the CSP

approval.

- Performance Improvement Plan for 2017 discussed and approved.

- During the mission various government counterparts also expressed the

need for expanding rail to reduce the loads on roads, while the ICT sector

proposed a need for carrying out a situation analysis of the telecoms sector.

Box 4: Main Conclusions from the Bank Dialogue Mission

14

is therefore investing in high impact infrastructure to improve regional competitiveness and

supporting a sound business friendly environment to attract investments to create jobs.

76. The overall development objective of the Country Strategy is to: reduce poverty and

malnutrition, and lessen vulnerability through a dynamic and sustainable private sector that

creates jobs. This objective can be achieved by pursuing two strategic objectives that: raise

productivity and strengthen trade competitiveness, to expand non-traditional exports and reduce

vulnerability to copper; and create a business friendly environment to support diversification and

industrialization while improving nutrition. The key strategic outcomes that will lead to achieving

the strategic objectives are: i) improved connectivity to regional and domestic markets, ii)

expanded utility services through more efficient, green and sustainable utilities, iii) improved

business environment to attract investors, iv) enhanced competition to drive a dynamic and

diversified economy that creates jobs, v) enhanced production through stronger linkages between

rural production areas and urban markets, and vi) strengthened value chains to improve

productivity while enhancing nutrition. The theory of change framework is presented in Figure 5.

77. In order to achieve the strategic outcomes while underpinning Government’s own efforts, the

Bank support will be organized around two pillars: i) support to infrastructure development; and ii)

support to private sector development. The interventions under these complimentary pillars will

contribute to economic diversification through improving productivity and promoting industrialization

thereby contributing to inclusive and sustainable growth. The proposed pillars are consistent with the

core operating priorities of the Bank’s Ten Year Strategy and the High-5s, and priority actions of

Zambia’s National Development Plan. Strategic alignment is shown in Table 2, below.

Pillar 1: Support to Infrastructure Development

78. The Government recognises that infrastructure is a crucial driver to enhance competitiveness,

private sector development, income growth and ultimately poverty reduction. The Bank will support

the Government initiatives by emphasizing infrastructure investments in energy, transport, and water.

These investments will be directed to removing key constraints and bottlenecks to competitiveness and

diversification, see Annex A. The focus on energy, transport and water will improve the investment

climate and will facilitate the entry of private investments within these sectors, especially energy, and

in other sectors, such as industry, enterprise development and agro-industries. Physical investments

will be combined with policy reforms and capacity building, which are equally important in facilitating

private investment. To foster the sustainability of the infrastructure to be developed, sector skills

development and climate smart components will be integrated into investment programmes.

Figure 5: Country Strategy Results Framework and Pillars

15

Energy: The absence of stable, reliable and adequate power supply is the most severe infrastructure

constraint affecting economic development. Private investors and development partners have been

hesitant to invest in the sector for several reasons, including the absence of institutional

arrangements to mobilize private sector, low electricity tariffs that do not reflect costs, a financially

stressed public sector utility, and inadequate human resource capacity.

In pursuance of economic diversification Zambia has large and unexploited hydropower potential.

Given the region’s recent electricity supply deficits, Zambia has the potential to export clean

electricity if harnessed. Responding to the need of expanding electricity supply, the Bank will

support the government’s priority of ensuring availability of sufficient and affordable energy with

a view to enhancing competitiveness and efficiency. Reliable energy supply will promote

industrialisation that in turn will lead to more employment. Increased energy supply will also

create opportunities for energy export through the Southern Africa Power Pool. To support the

government achieve its energy goals, and in line with Light-up and Power Africa and the New

Deal on Energy, the Bank will operationalise this sector through investment operations (including

in IPPs), policy advisory services and sector reforms to: i) improve access to electricity in urban

and rural areas (off-grid and mini-grids will also be considered); ii) increase energy efficiency; iii)

support clean power development; iv) facilitate regional cooperation and integration; v) strengthen

utilities, sector governance and financial restructuring; and vi) promote private sector participation.

The Bank will work on both supply and demand sides. The Bank will promote Public Private

Partnerships for renewable energy generation and distribution to supplement scarce public resources.

Transport: The Government recognises the role transport infrastructure plays as a catalyst to

economic development. Government priorities are driven by improving connectivity, with emphasis

being placed on rural (national) connectivity to complement the gains in regional connectivity.