yemen development

TRANSCRIPT

YemenDevelopment Policy Review

Yemen

Develo

pm

ent P

olicy R

eviewT

HE

WO

RLD

BA

NK

10414-CoverFINAL.qxd 4/17/08 11:13 AM Page 1

43600

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

YemenDevelopment Policy Review

10414-00_FM.qxd 4/17/08 11:09 AM Page i

10414-00_FM.qxd 4/17/08 11:09 AM Page ii

YemenDevelopment Policy Review

Report No. 35393-RY

Social and Economic Development Sector UnitMiddle East and North Africa Region

10414-00_FM.qxd 4/17/08 11:09 AM Page iii

10414-00_FM.qxd 4/17/08 11:09 AM Page iv

E X E C U T I V E S U M M A R Y . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . xiii

Yemen Today: Mixed Development Outcomes . . . . . . . . . . . . . . . . . . . . . . 1Macroeconomic Outcomes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2Poverty and Unemployment Outcomes. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5Social Outcomes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6Achievability of the Millennium Development Goals (MDGs) . . . . . . . . . . 7Implementation of the Poverty Reduction Strategy. . . . . . . . . . . . . . . . . . . . 8Priorities for Reform . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Yemen Tomorrow: Prospects For Good Governance and Economic Growth . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11The Quality of Governance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11Understanding Yemen’s Poor Governance. . . . . . . . . . . . . . . . . . . . . . . . . . 12Understanding Yemen’s Recent Economic Experience . . . . . . . . . . . . . . . . 16Building the Will for Reform. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

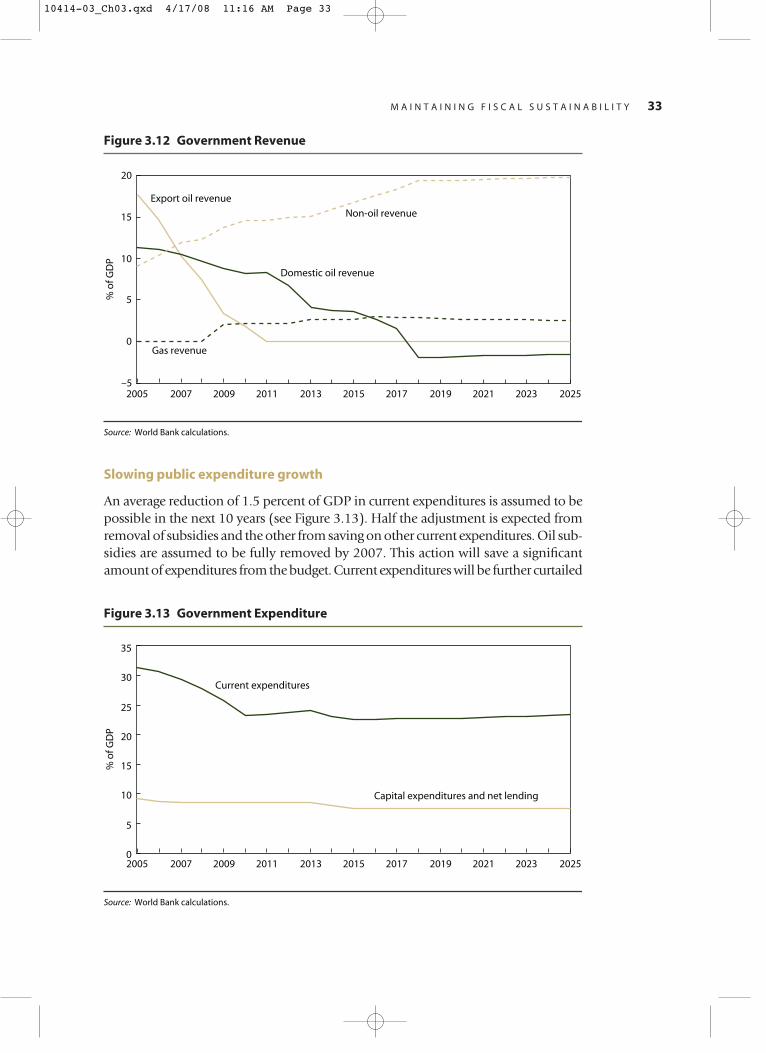

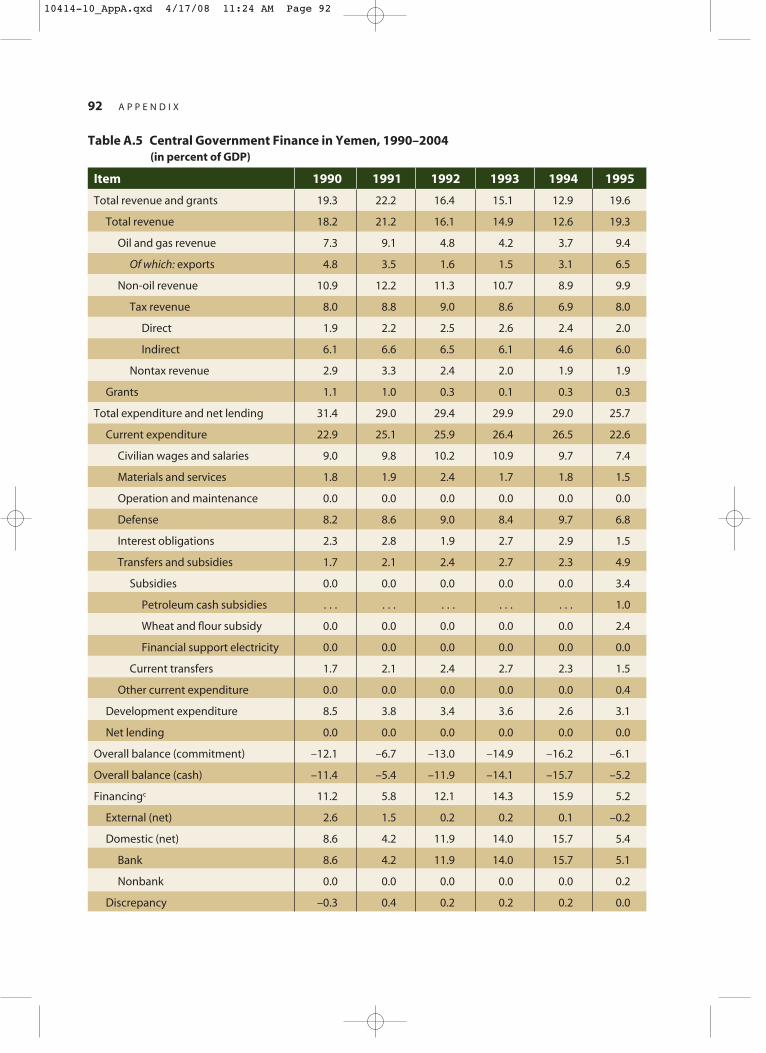

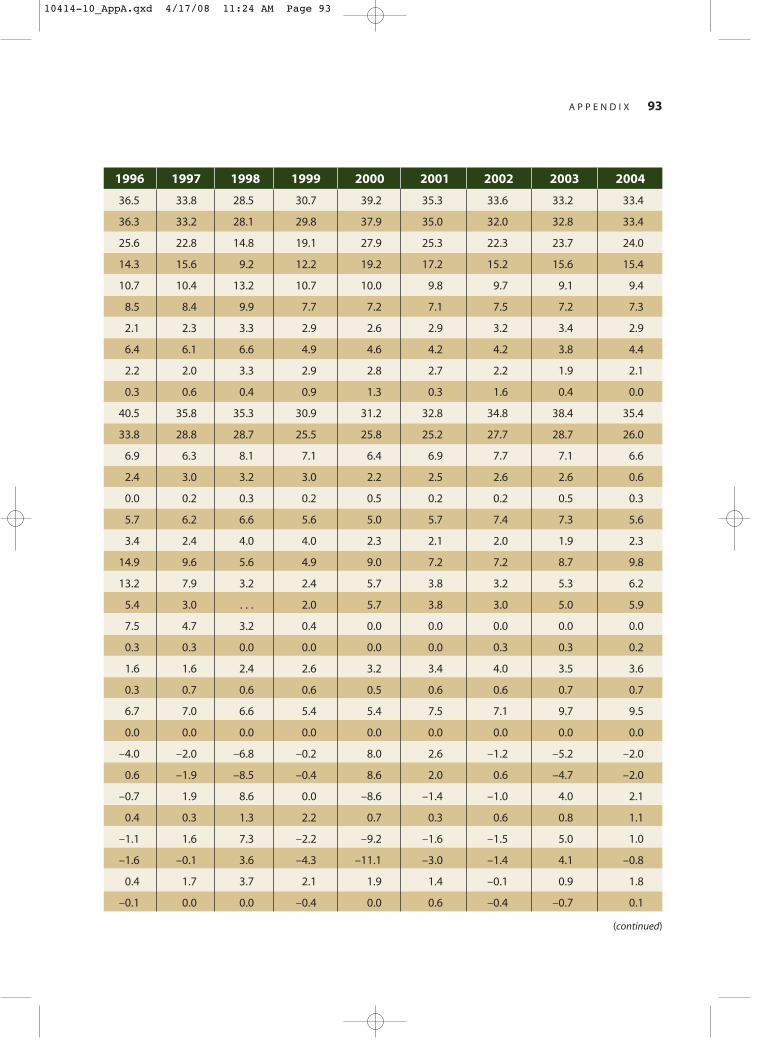

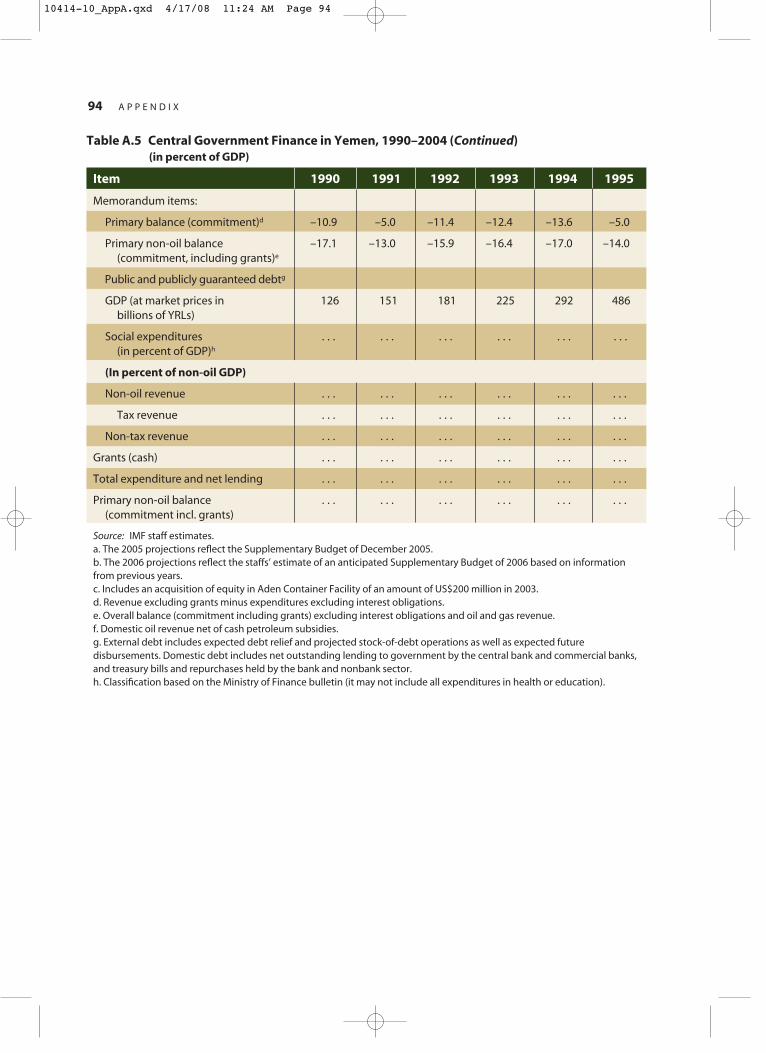

Maintaining Fiscal Sustainability . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23Yemen’s track record on fiscal sustainability . . . . . . . . . . . . . . . . . . . . . . . . 23Medium term outlook . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31Perilously Increasing Public Debt . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38External Debt Sustainability Critically Depends on Oil Price Trajectories . . . 40The Reform Agenda to Maintain Fiscal Balance. . . . . . . . . . . . . . . . . . . . . . 40

Improving the Investment Climate . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43The Reform Agenda to Improve the Investment Climate . . . . . . . . . . . . . . 48

4

3

2

1

v

Contents

10414-00_FM.qxd 4/17/08 12:14 PM Page v

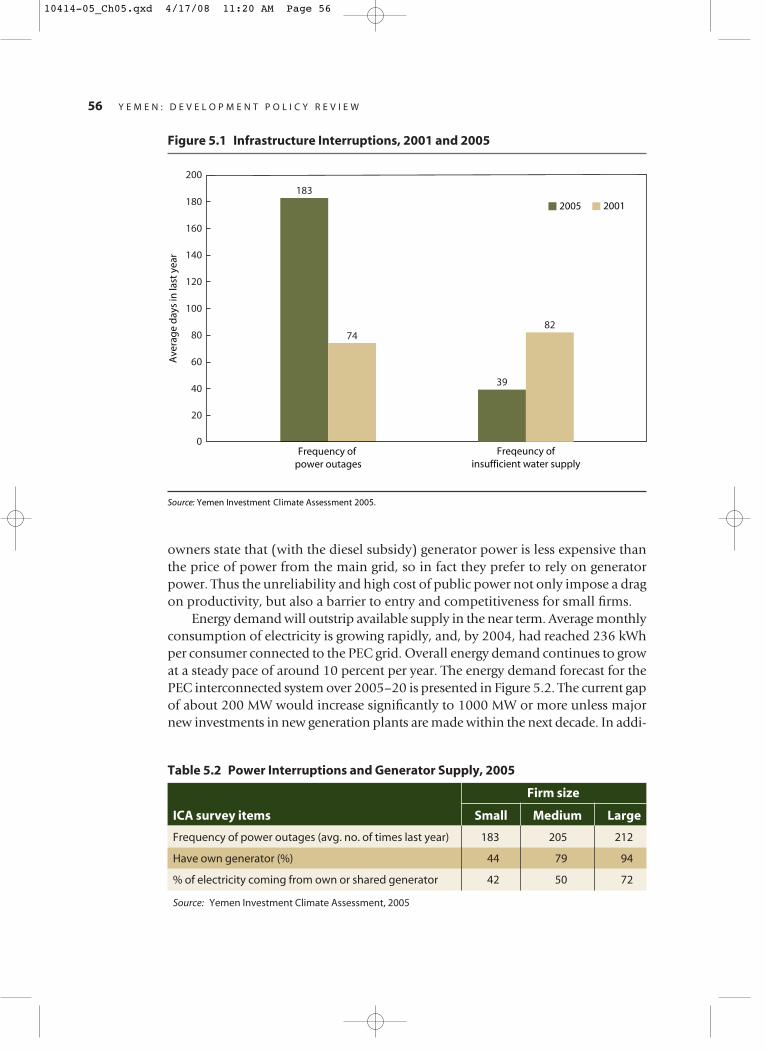

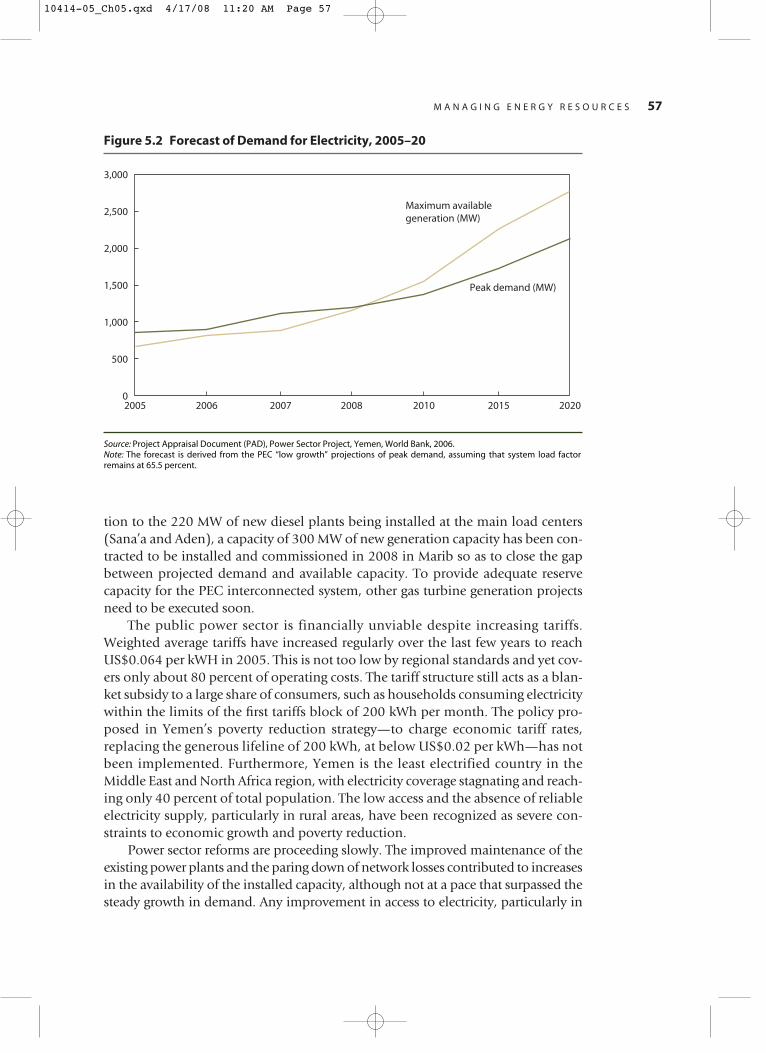

Managing Energy Resources . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51Conditions and Challenges in the Oil and Gas Sectors . . . . . . . . . . . . . . . 51The Reform Agenda for Oil and Gas. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52Conditions and Challenges in the Power Sector . . . . . . . . . . . . . . . . . . . . . 55The Reform Agenda in the Power Sector . . . . . . . . . . . . . . . . . . . . . . . . . . . 58

Managing Water Resources . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61Challenges in the Water Sector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62The Reform Agenda for Water Resources . . . . . . . . . . . . . . . . . . . . . . . . . . . 66

Slowing Population Growth . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69The Reform Agenda for Population Policy. . . . . . . . . . . . . . . . . . . . . . . . . . 73

7

6

5

vi C O N T E N T S

10414-00_FM.qxd 4/17/08 12:15 PM Page vi

List of Figures

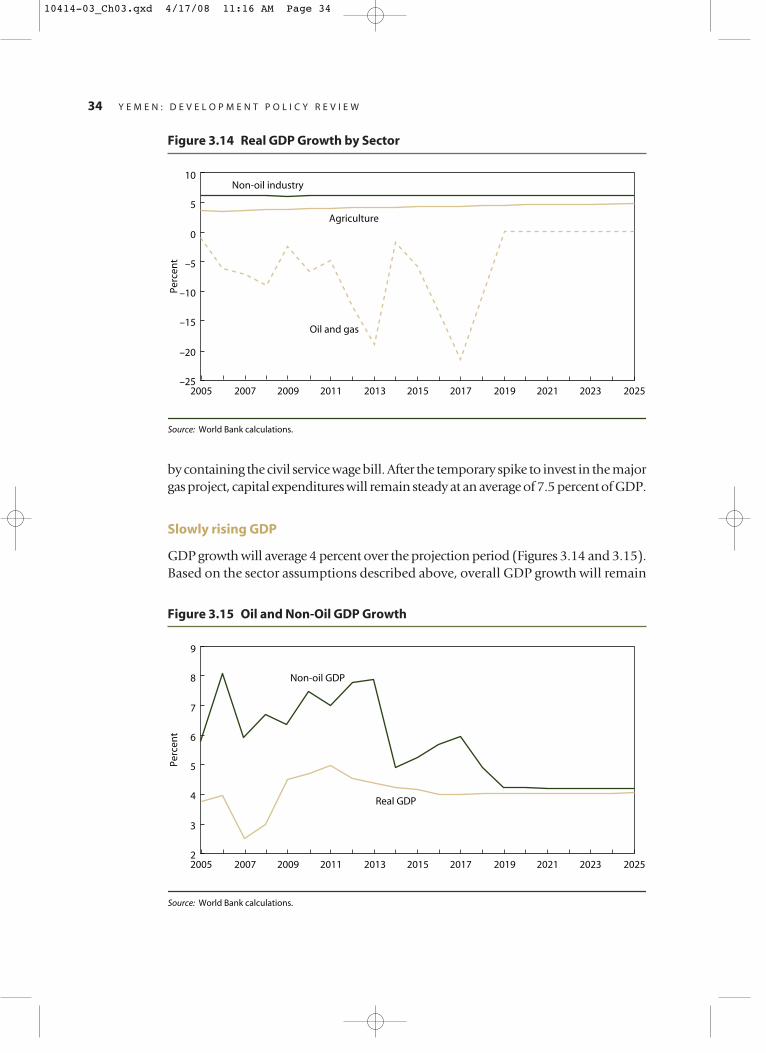

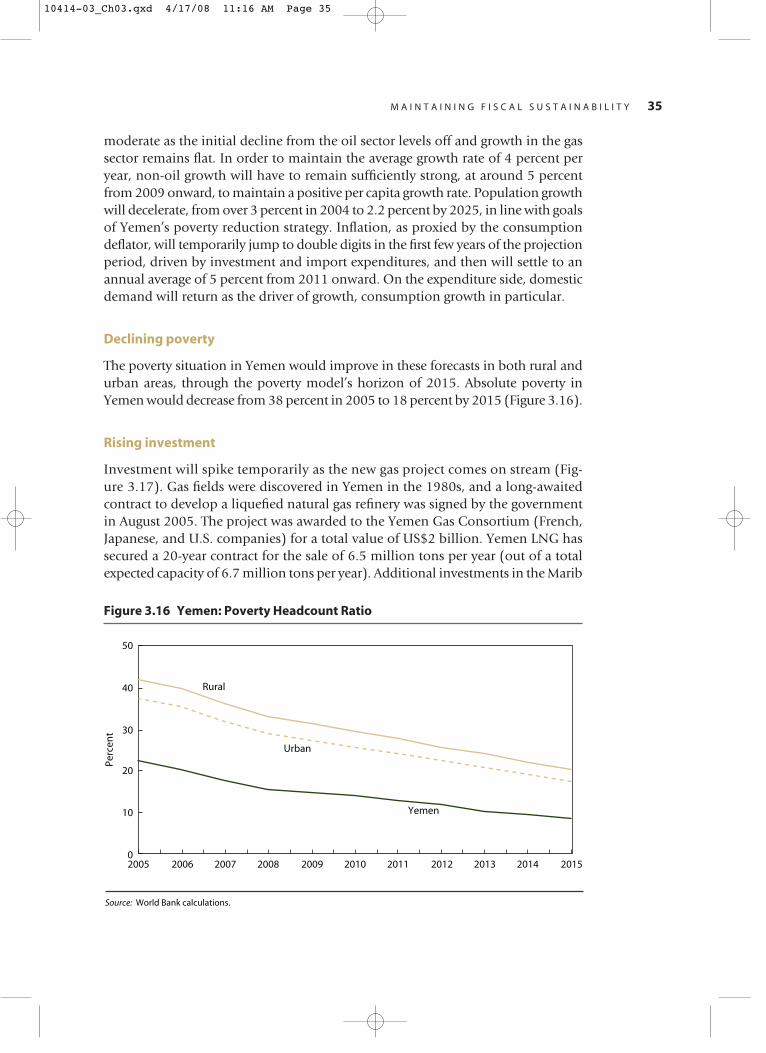

1 GDP Growth Over Recent Reform Periods . . . . . . . . . . . . . . . . . . . . . . . . . xiii2 Oil Production in Yemen. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . xv3 Quality of Governance in Yemen . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . xvii4 Fertility in Yemen . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . xviii1.1 Risk of Internal Conflict and Quality of Governance . . . . . . . . . . . . . . . . . . 31.2 Domestic Investment, percentage of GDP . . . . . . . . . . . . . . . . . . . . . . . . . . . 31.3 Foreign Direct Investment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42.1 Quality of Governance in yemen, 1996-2004 . . . . . . . . . . . . . . . . . . . . . . . 122.2 Quality of Governance in Yemen and Comparator Countries . . . . . . . . . . 133.1 Overall fiscal balance and oil Revenues . . . . . . . . . . . . . . . . . . . . . . . . . . . . 243.2 Primary non-oil balance (% of gdp) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 243.3 Primary Non-Oil Balance, with and without subsidies (% of gdp) . . . . . . 263.4 Oil Subsidies and Oil Prices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 263.5 Indirect Tales and Subsidies (% of gdp) . . . . . . . . . . . . . . . . . . . . . . . . . . . 273.6 Saving From Oil Revenue . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 283.7 Oil Revenue and Expenditures (% of GDP). . . . . . . . . . . . . . . . . . . . . . . . . 293.8 Current Expenditure Breakdown . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 293.9 Exports and the Real Effective Exchange Rate . . . . . . . . . . . . . . . . . . . . . . . 303.10 Evolution of External Debt . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 303.11 Evolution of Arrears. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31 3.12 Government Revenue . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 333.13 Government Expenditure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 333.14 Real GDP Growth by Sector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 343.15 Oil and Non-Oil GDP Growth . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 343.16 Poverty Headcount Ratio. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 353.17 Fixed Investment By Sector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 363.18 Direct Foreign Investment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 373.19 Projected Balance of Payments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 373.20 Yemen Oil Price . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 383.21 Indicators of Public Debt Under Alternative Scenarios . . . . . . . . . . . . . . . . 393.22 Indicators of Public and Publicly Guaranteed External Debt

Under Alternative Scenarios . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 414.1 Leading Investment Climate Constraints . . . . . . . . . . . . . . . . . . . . . . . . . . . 444.2 ranking of cost of doing business indicators . . . . . . . . . . . . . . . . . . . . . . . . 455.1 Infrastructure Interruptions—2001 and 2005 . . . . . . . . . . . . . . . . . . . . . . . 565.2 Yemen: Electricity Demand Forecast (2005-20) . . . . . . . . . . . . . . . . . . . . . 577.1 Total Fertility Rate . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70

List of Tables

1.1 Yemen: Sectoral Contribution to Real GDP, 1991-2004 (%) . . . . . . . . . . . . 41.2 Poverty Lines and Poverty Measures: 1992-1998. . . . . . . . . . . . . . . . . . . . . . 53.1 Non-Oil Exports Growth. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 325.1 Yemen—Petroleum Product Subsidies. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53

C O N T E N T S vii

10414-00_FM.qxd 4/17/08 12:16 PM Page vii

5.2 Power Interruptions and Generator Supply, 2005. . . . . . . . . . . . . . . . . . . . 566.1 Water Withdrawal by Using Sector in Yemen and Comparators, 1998-2002

(In Percent of Total) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 626.2 Reaching the Water Sector MDGs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64

List of Boxes

3.1 Fiscal Sustainability Analysis for Oil-Rich Countries. . . . . . . . . . . . . . . . . . 253.2 Promoting Non-Oil Exports . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 327.1. Lessons from MENA Countries that have Progressed Rapidly

in Fertility Control . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71

E N D N O T E S . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75

R E F E R E N C E S . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79

List of Appendix Tables

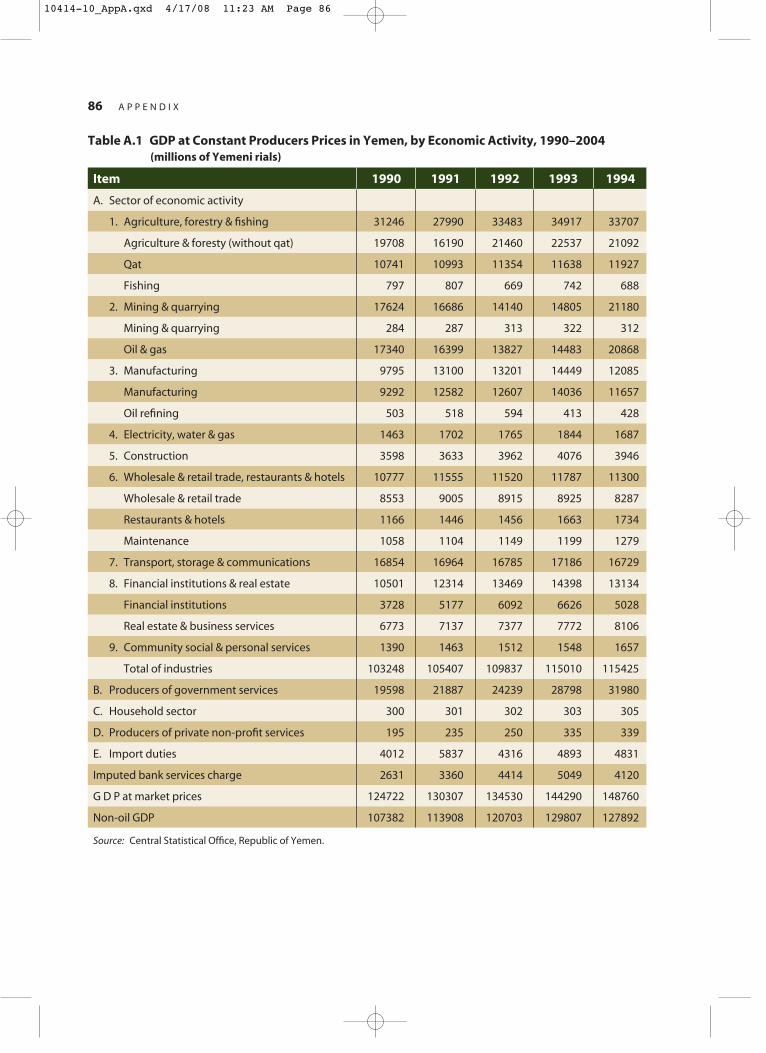

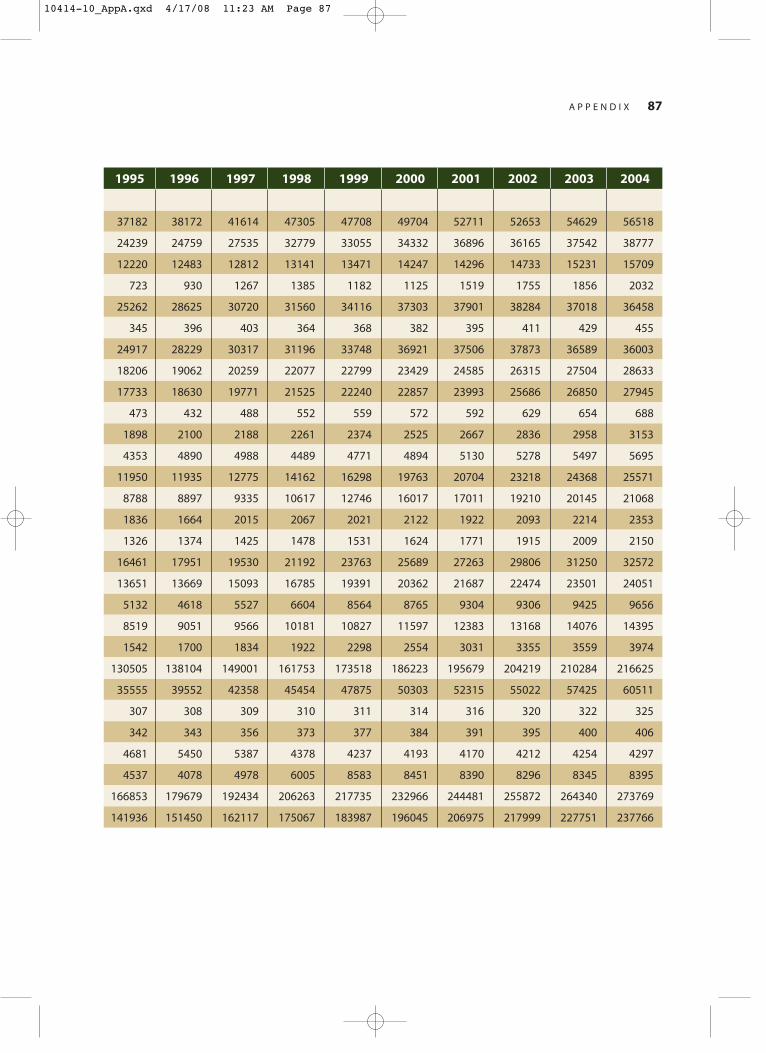

A1 GDP at Producers Prices by Economic Activity (in 1990 Constant Prices), 1990–2004 (Million Yemeni Rials) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 86

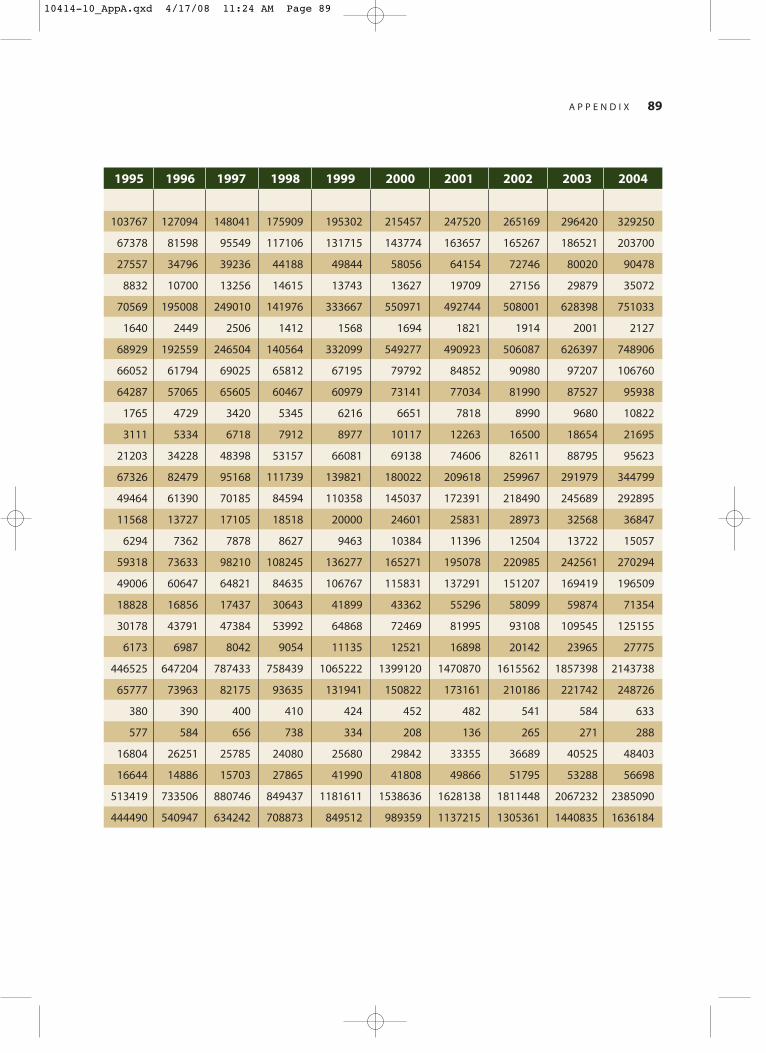

A2 GDP at Producers Prices by Economic Activity (in Current Prices), 1990–2004 (Million Yemeni Rials) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 88

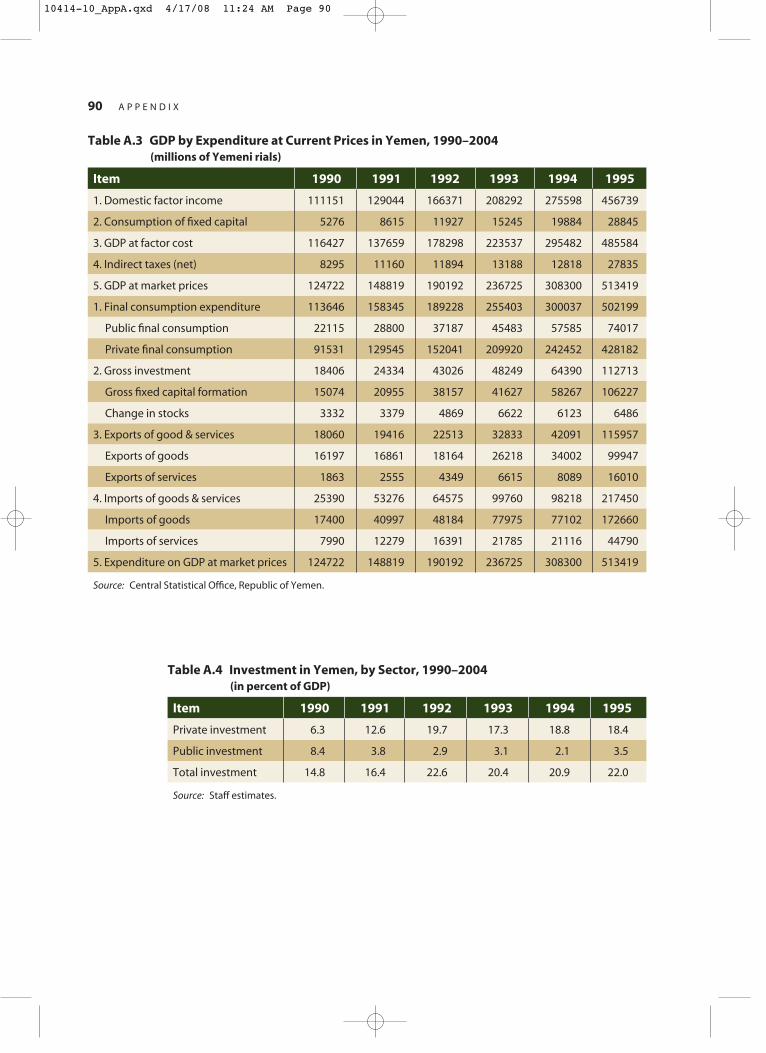

A3 GDP by Expenditure ( in Current Prices), 1990–2004 (Million Yemeni Rials) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 90

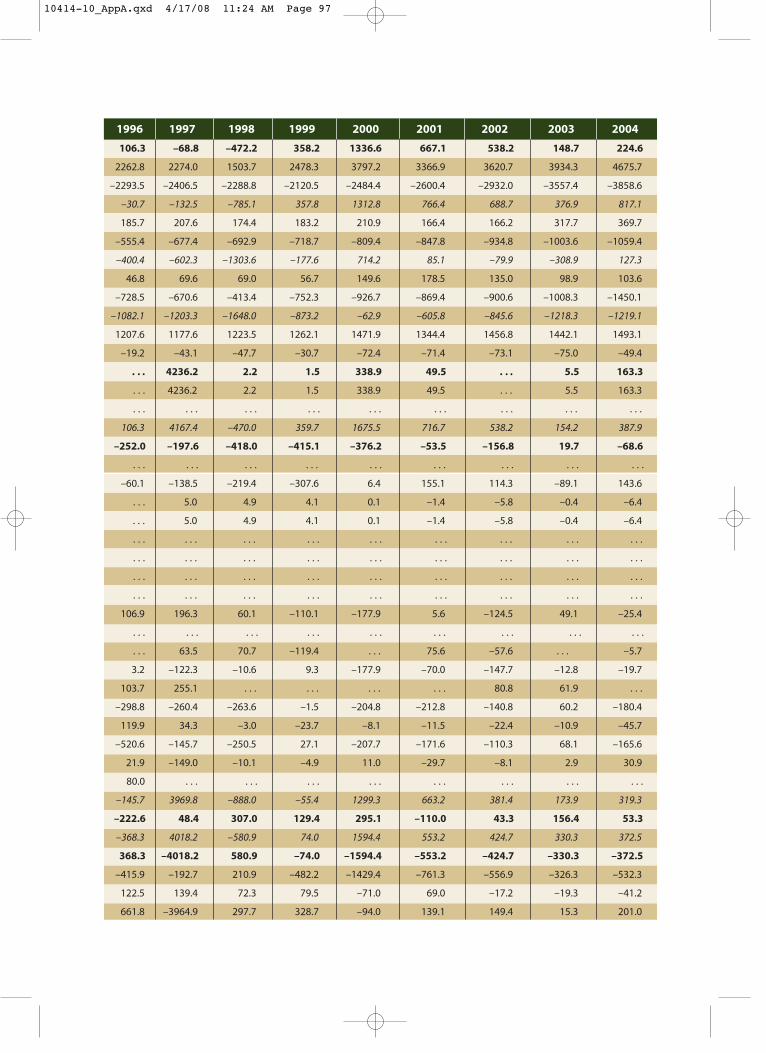

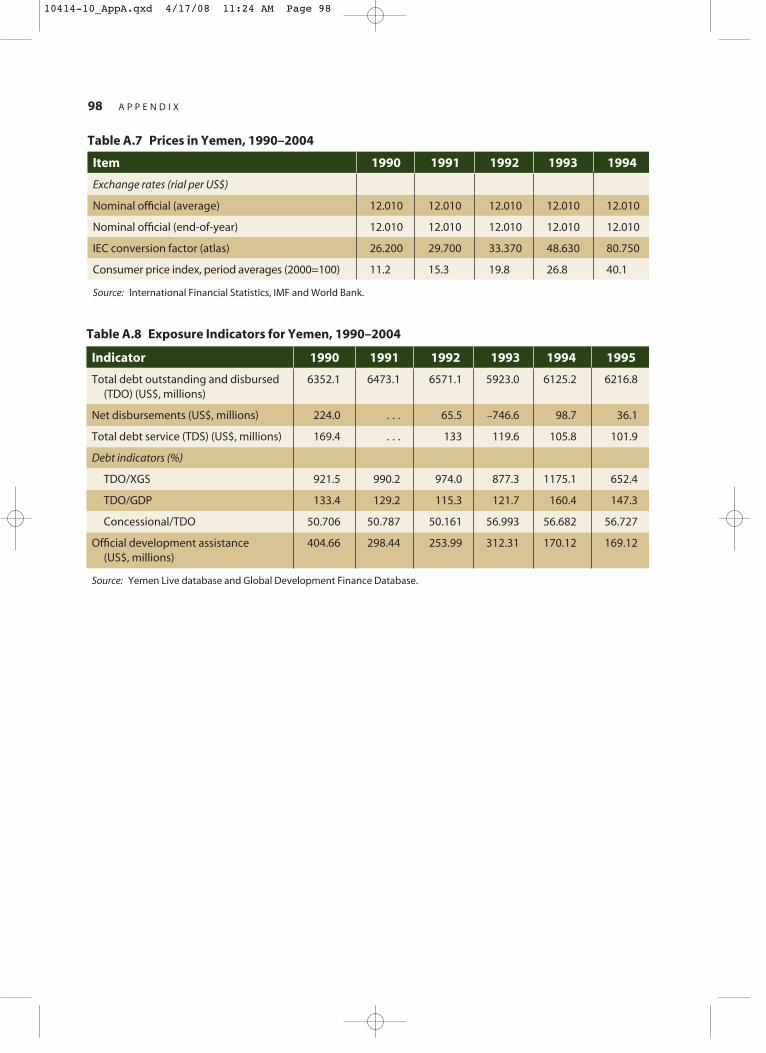

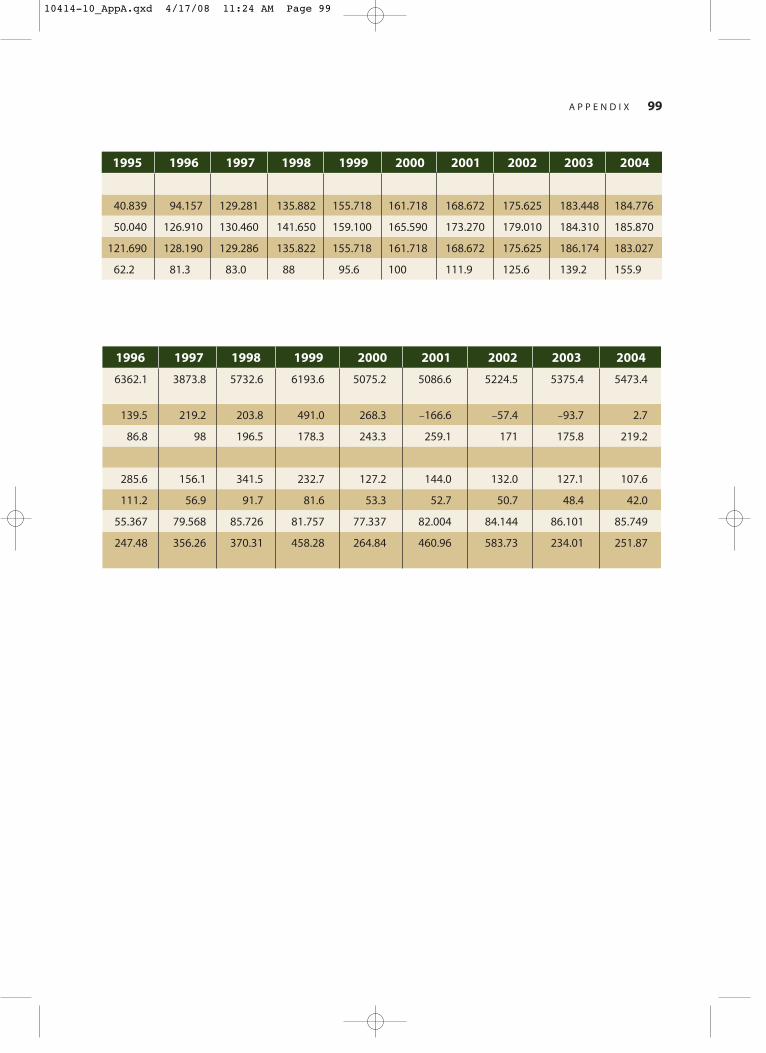

A4 Investment by sector (in percent of GDP) . . . . . . . . . . . . . . . . . . . . . . . . . . 90A5 Republic of Yemen: Central Government Finance, 1990–2004 . . . . . . . . . 92A6 Republic of Yemen: Balance of Payments (Analytic Presentation),

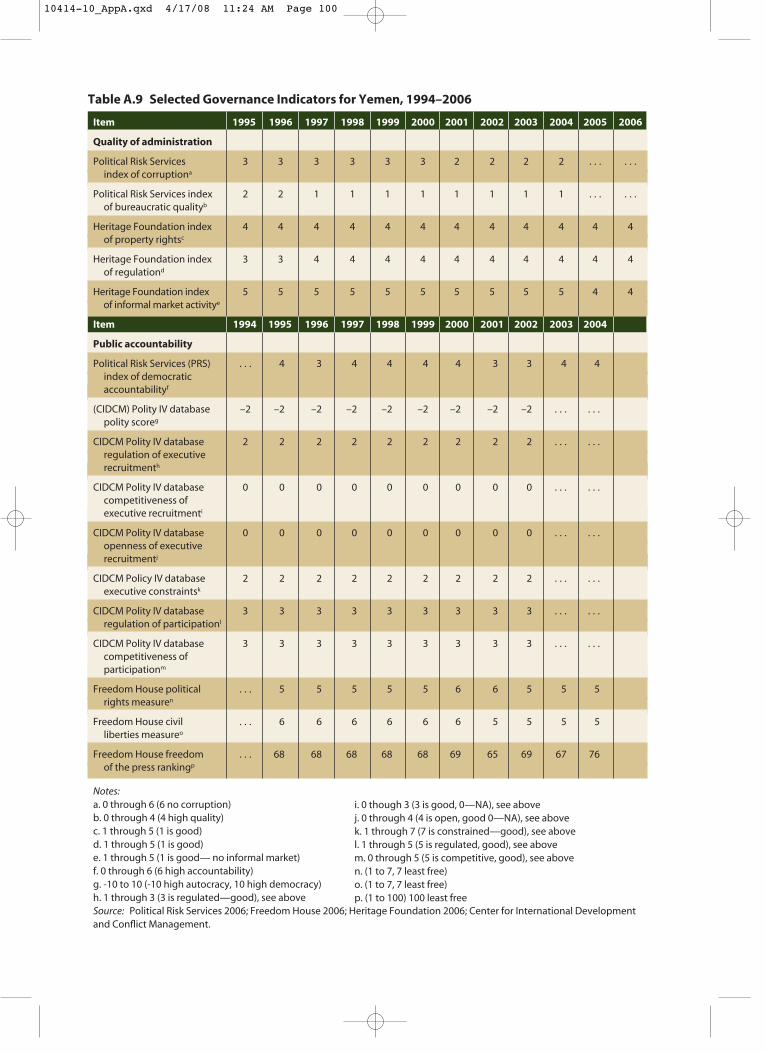

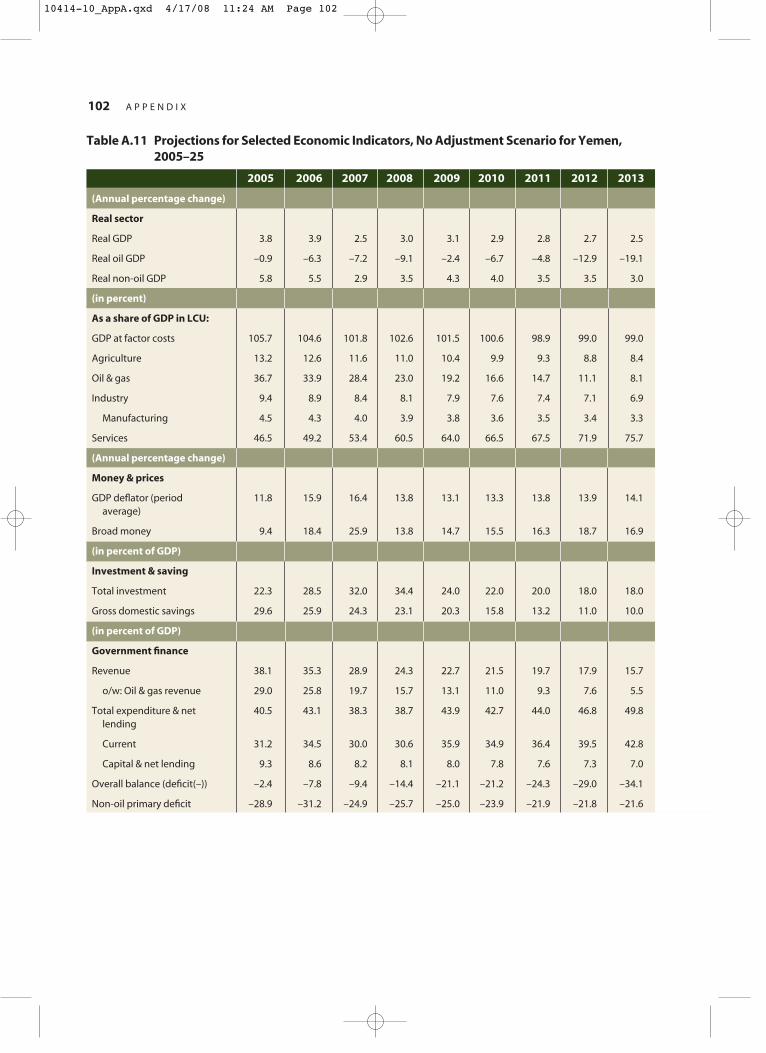

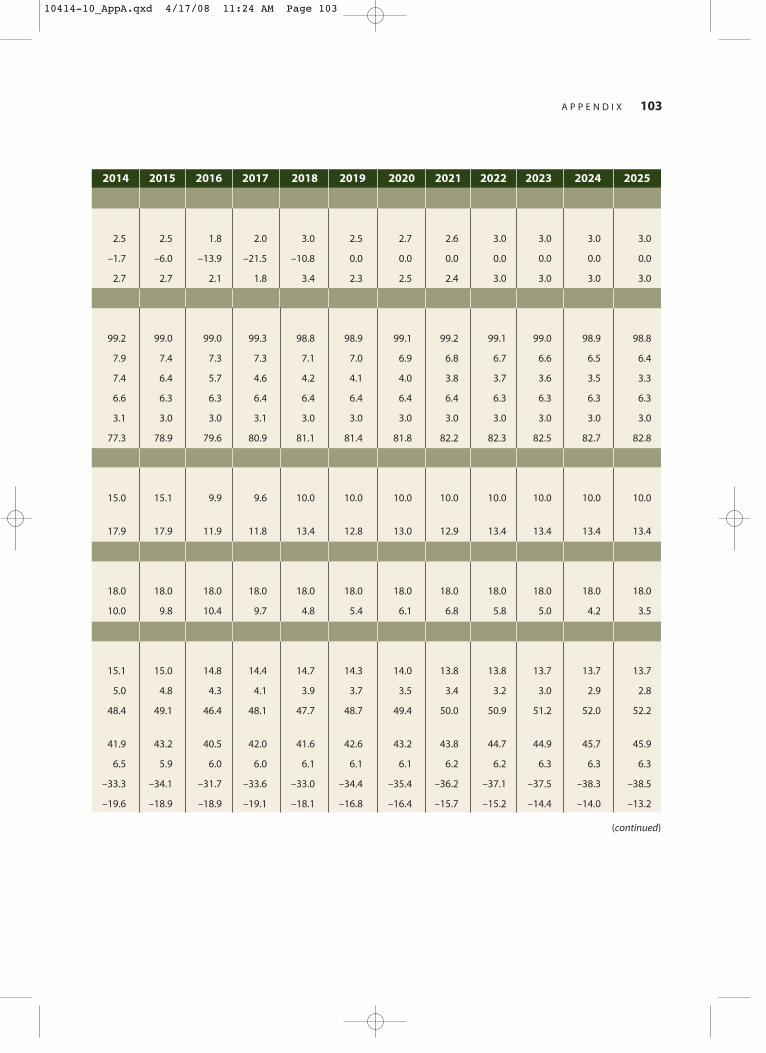

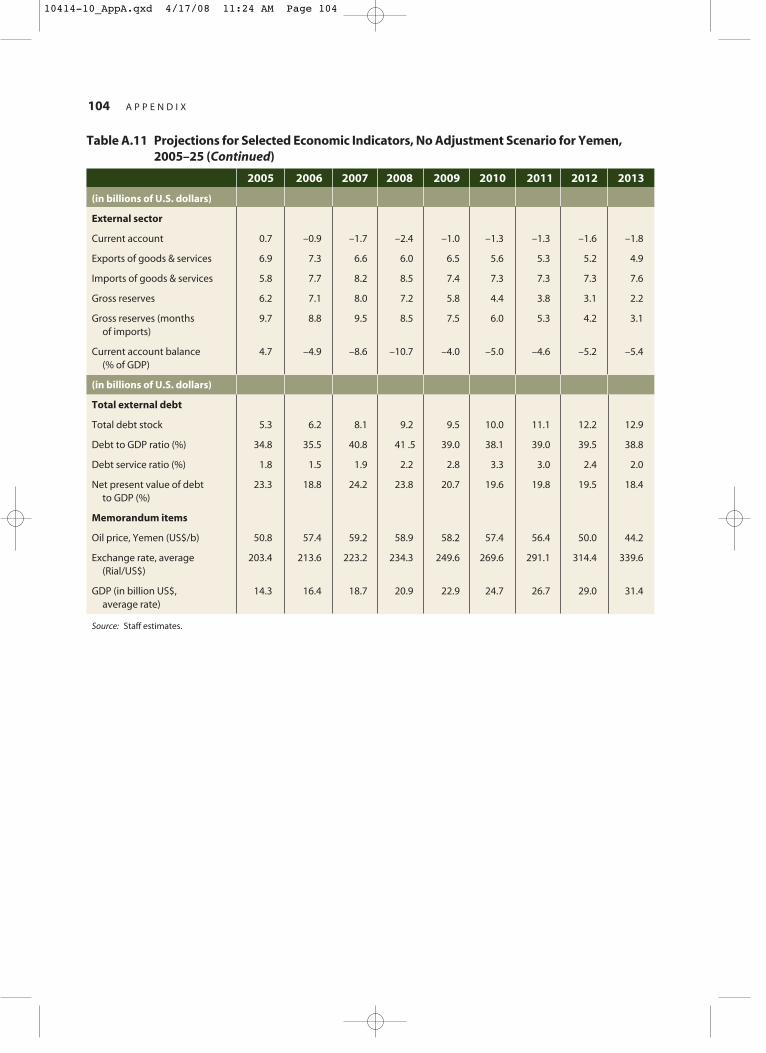

1990–2004. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 96A7 Republic of Yemen: Prices, 1990–2004 . . . . . . . . . . . . . . . . . . . . . . . . . . . . 98A8 Republic of Yemen—Key Exposure Indicators, 1990–2004 . . . . . . . . . . . . 98A9 Republic of Yemen: Select Governance Indicators, 1994–2006 . . . . . . . . 100A10 Alternative Governance indicators for Yemen, 1996–2004 . . . . . . . . . . . 101A11 Projections for Selected Economic Indicators: No Adjustment Scenario,

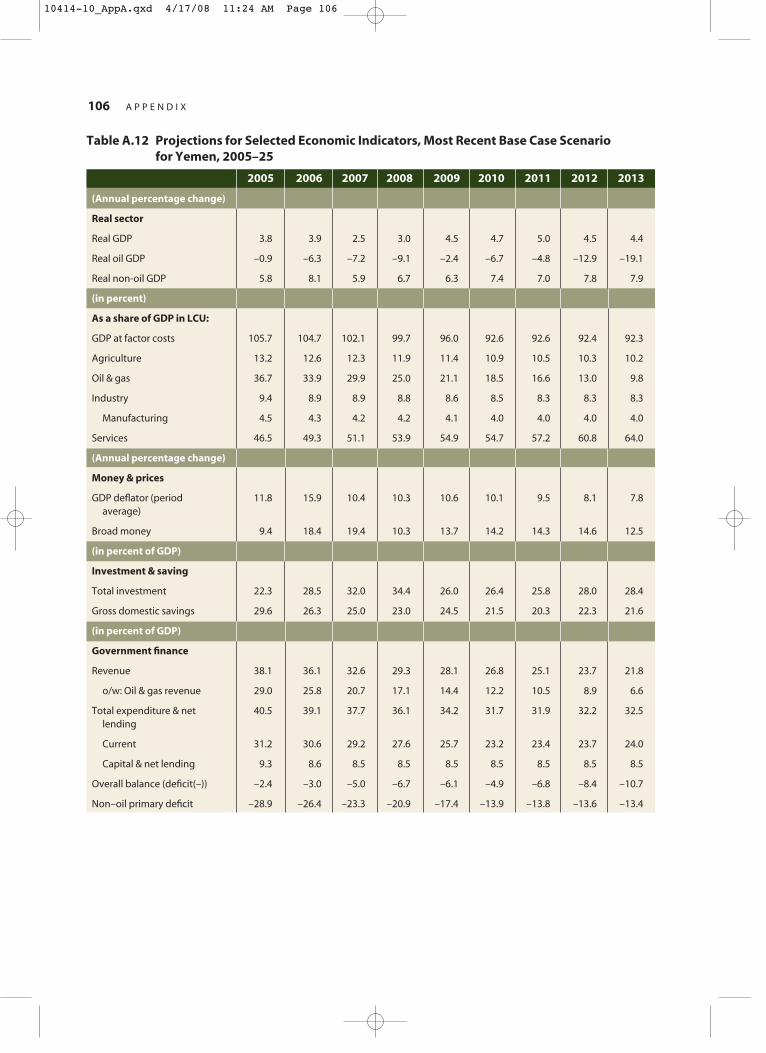

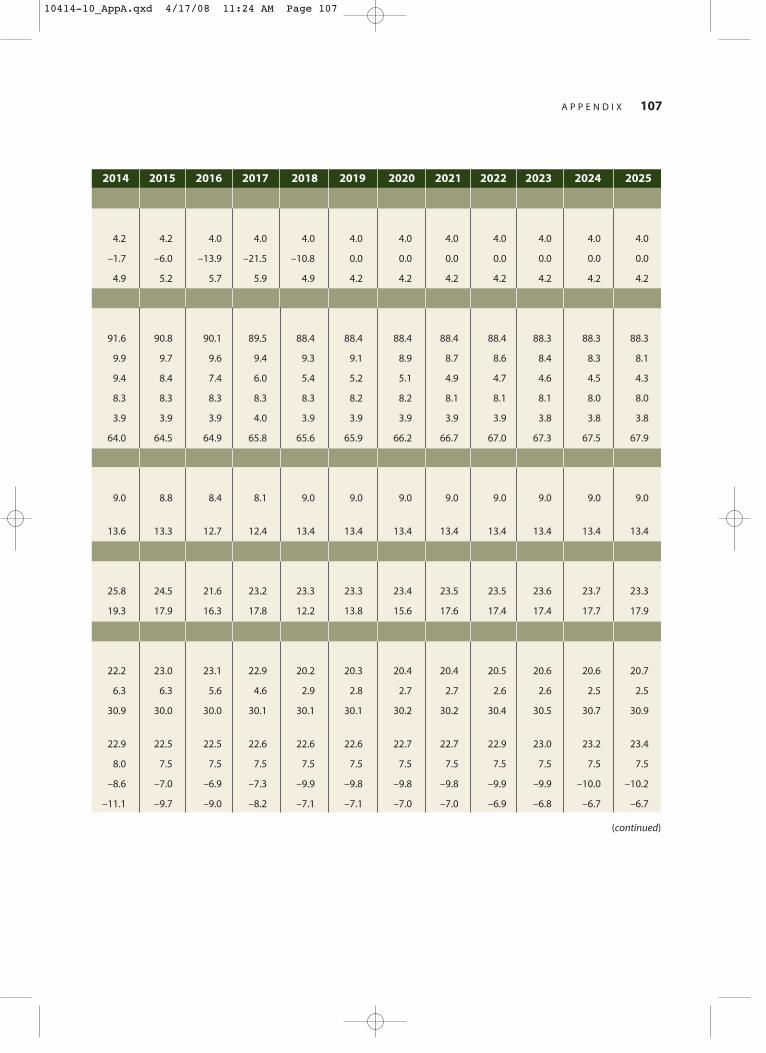

2005–25 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 102A12 Projections for Selected Economic Indicators: Most Recent Base Case

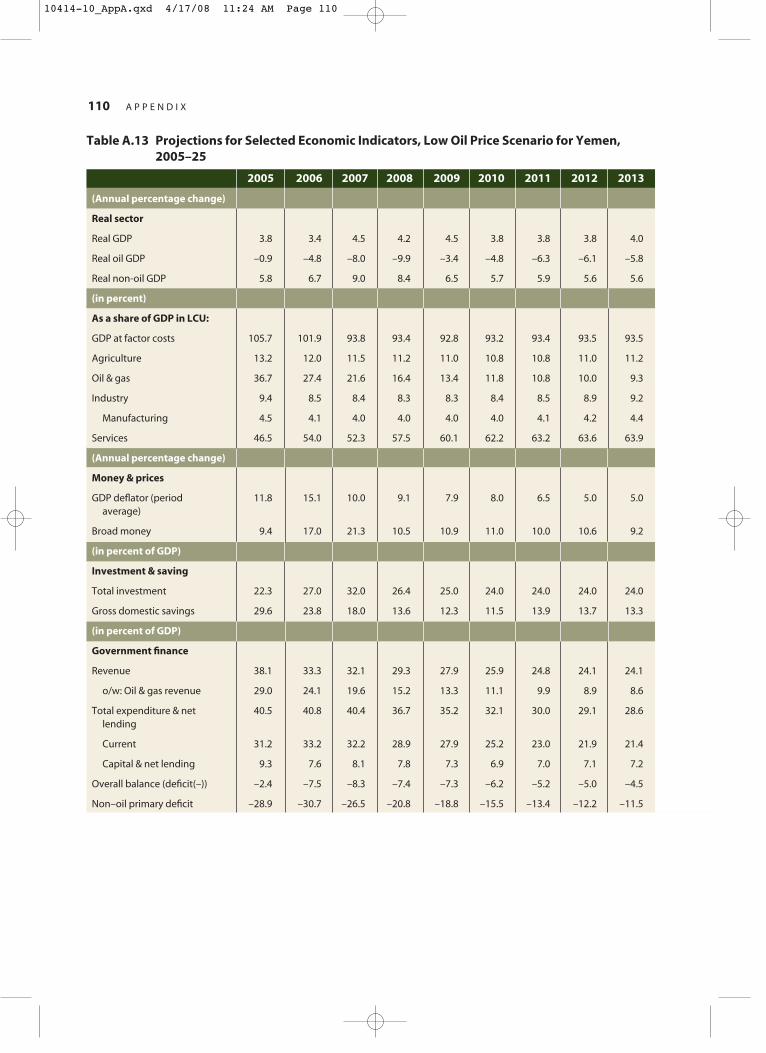

Scenario, 2005–25. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 106A13 Projections for Selected Economic Indicators: Low Oil Price Scenario,

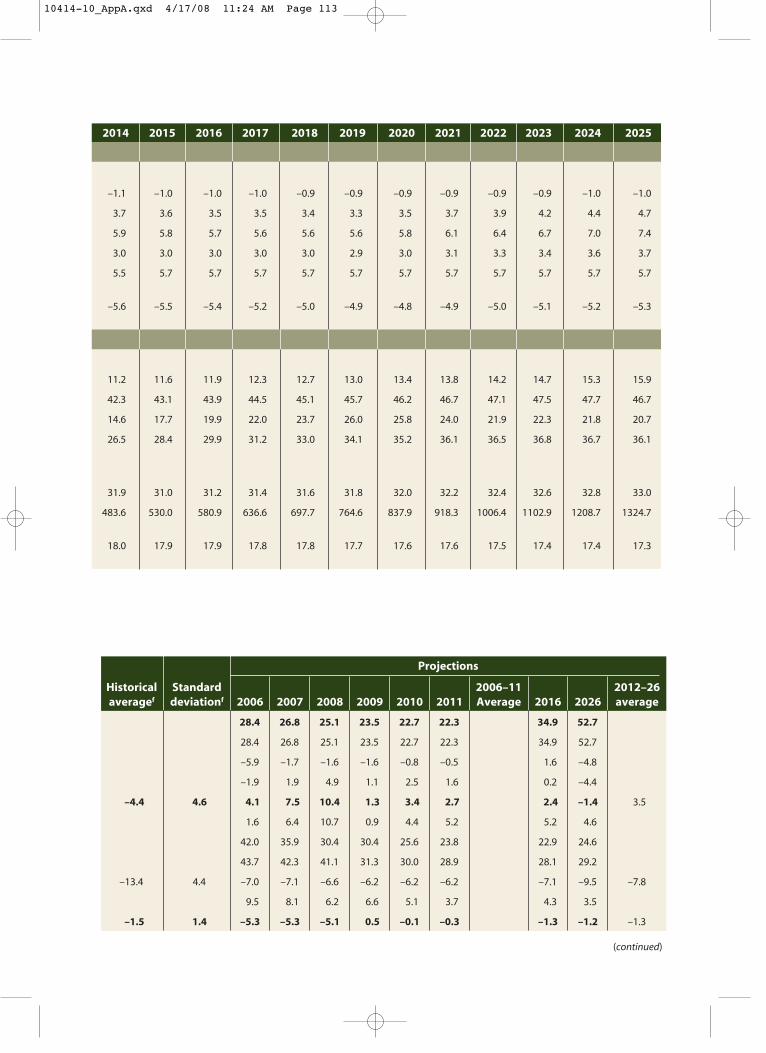

2005–25 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 110A14 Country: External Debt Sustainability Framework, Baseline Scenario,

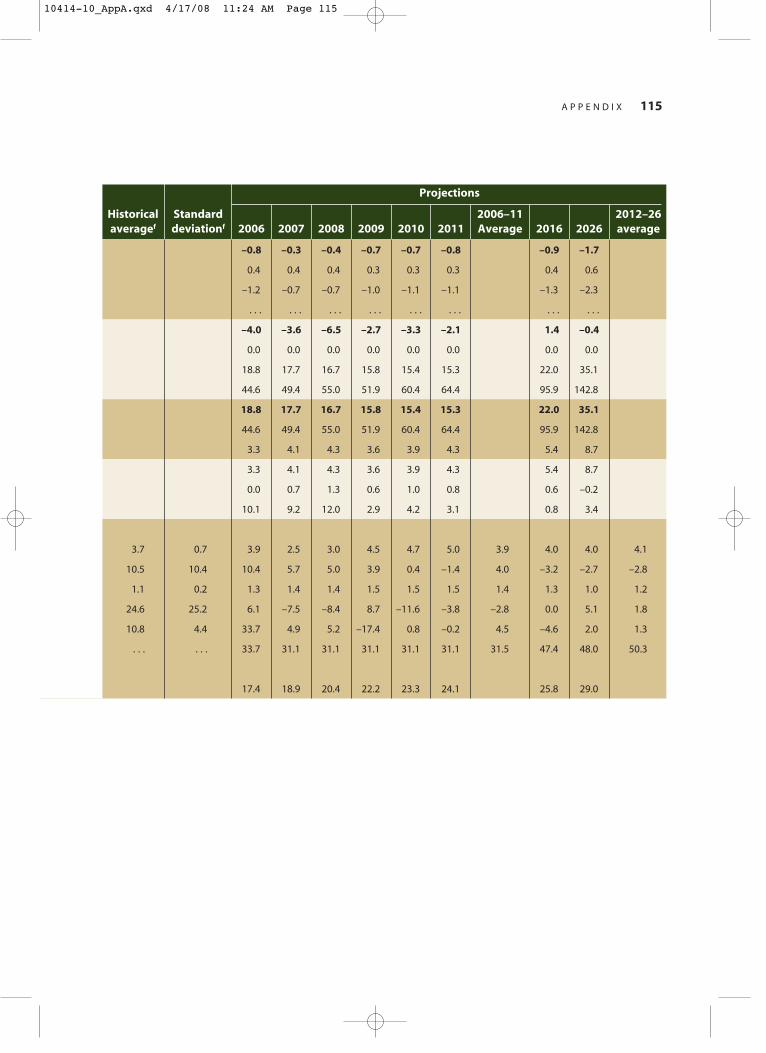

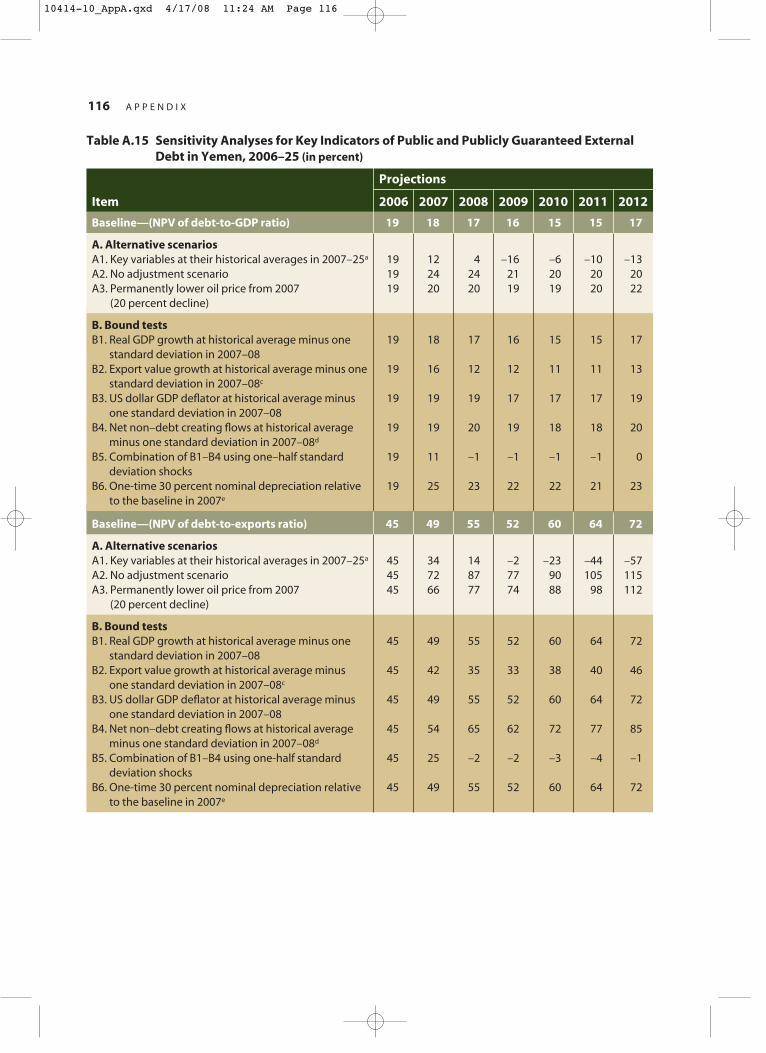

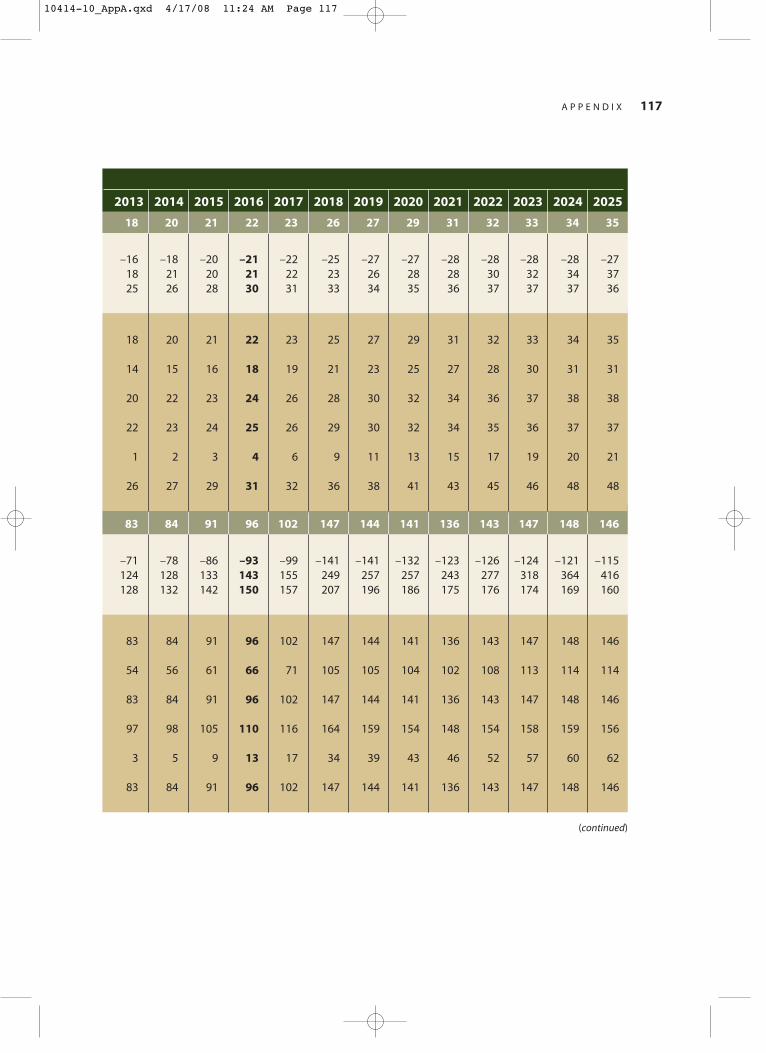

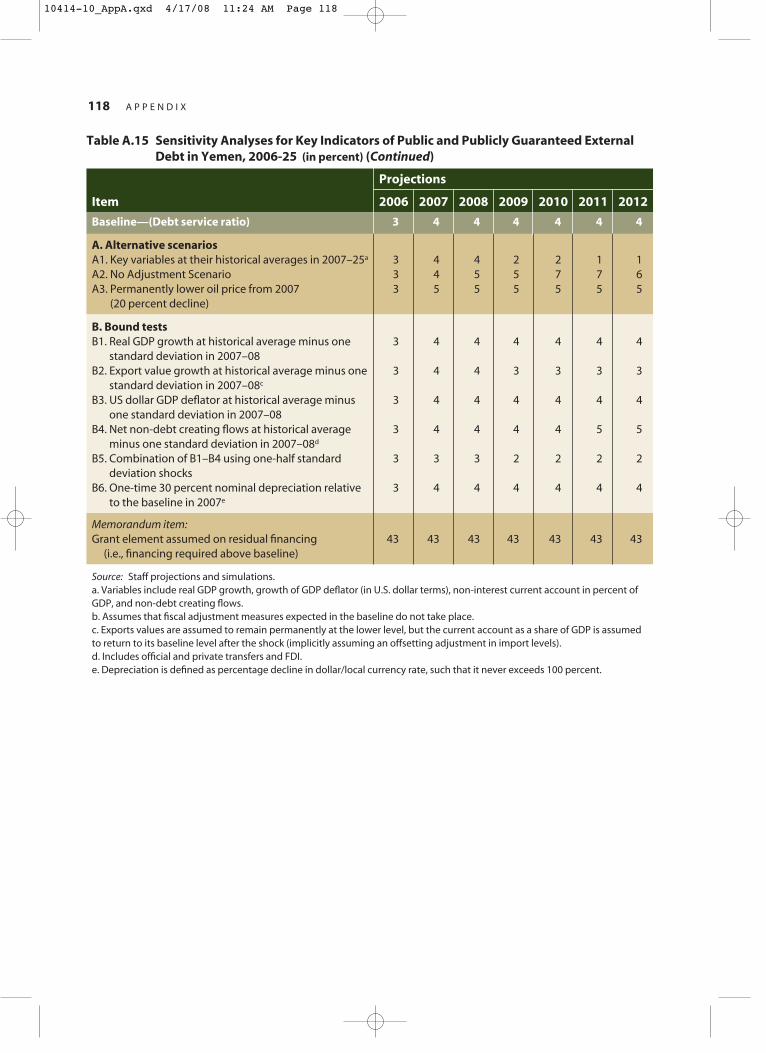

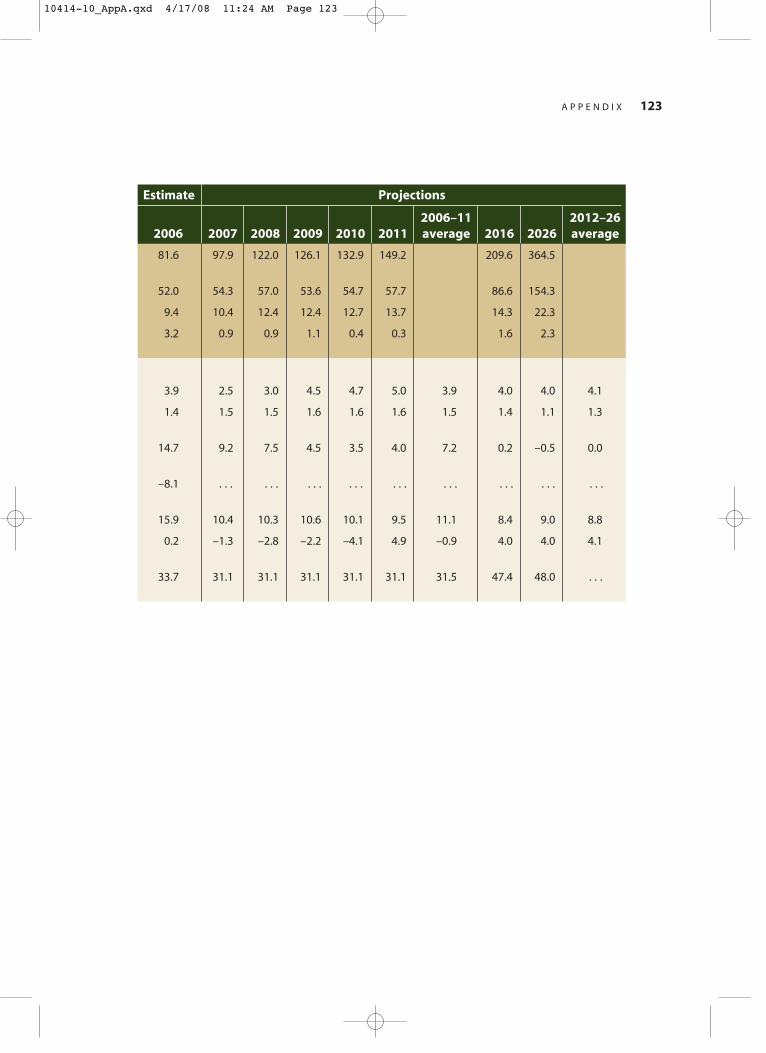

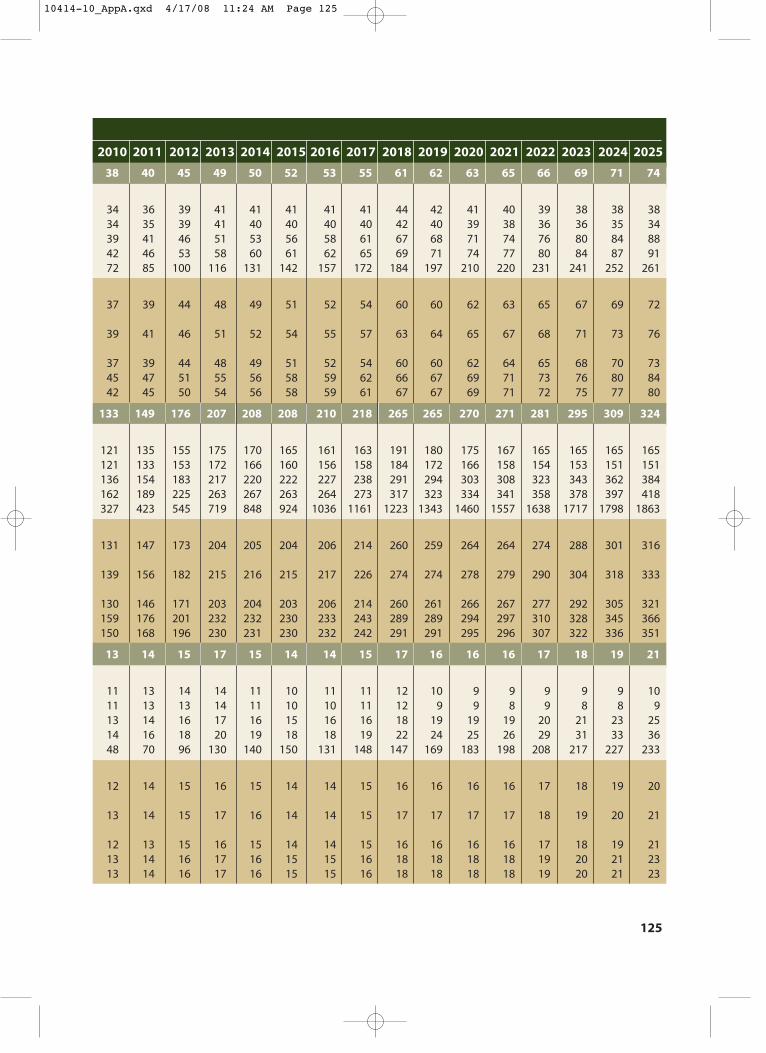

2006–2026 (in percent of GDP). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 112A15 Country Sensitivity Analyses for Key Indicators of Public and

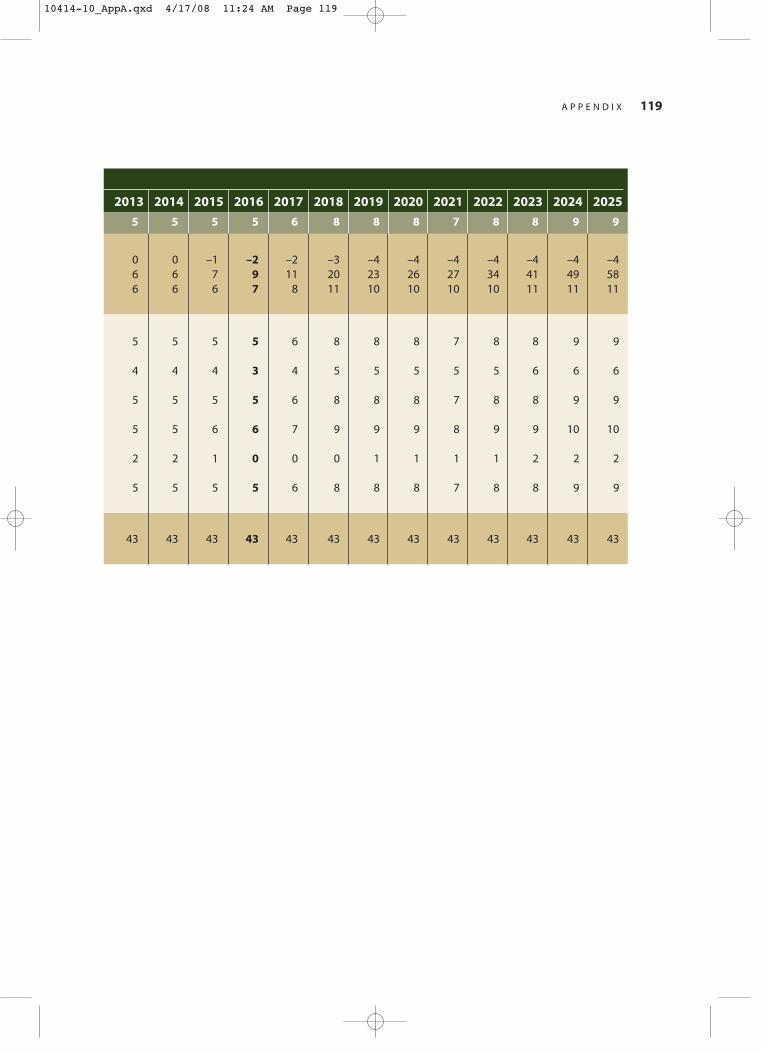

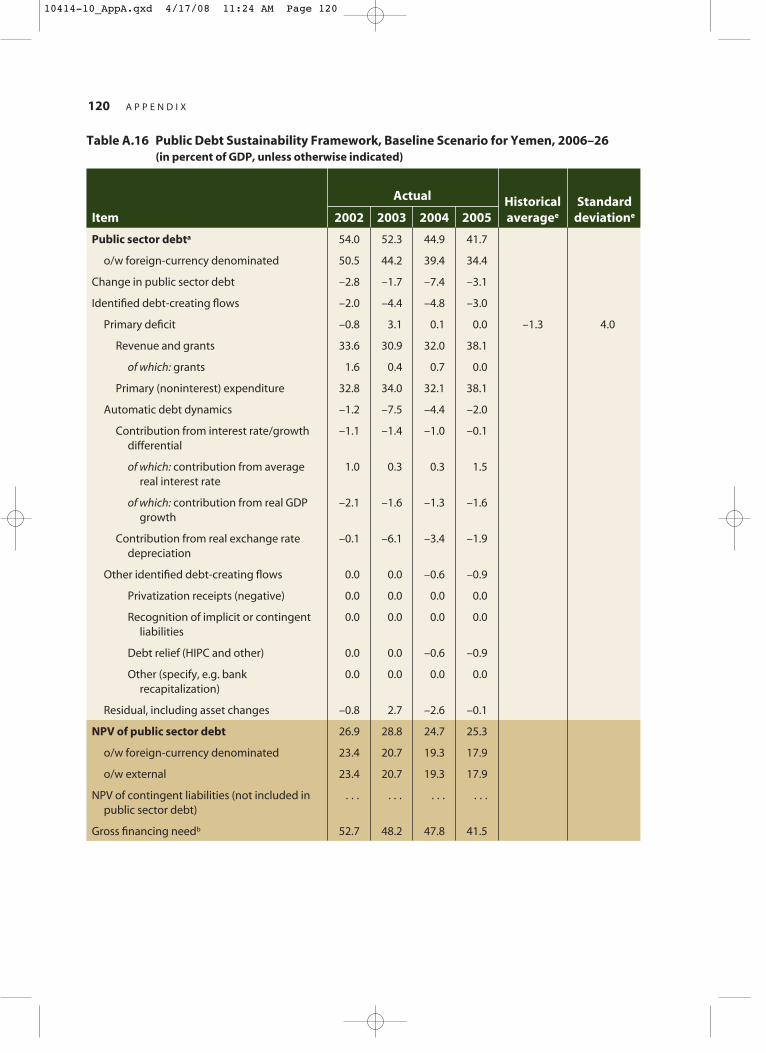

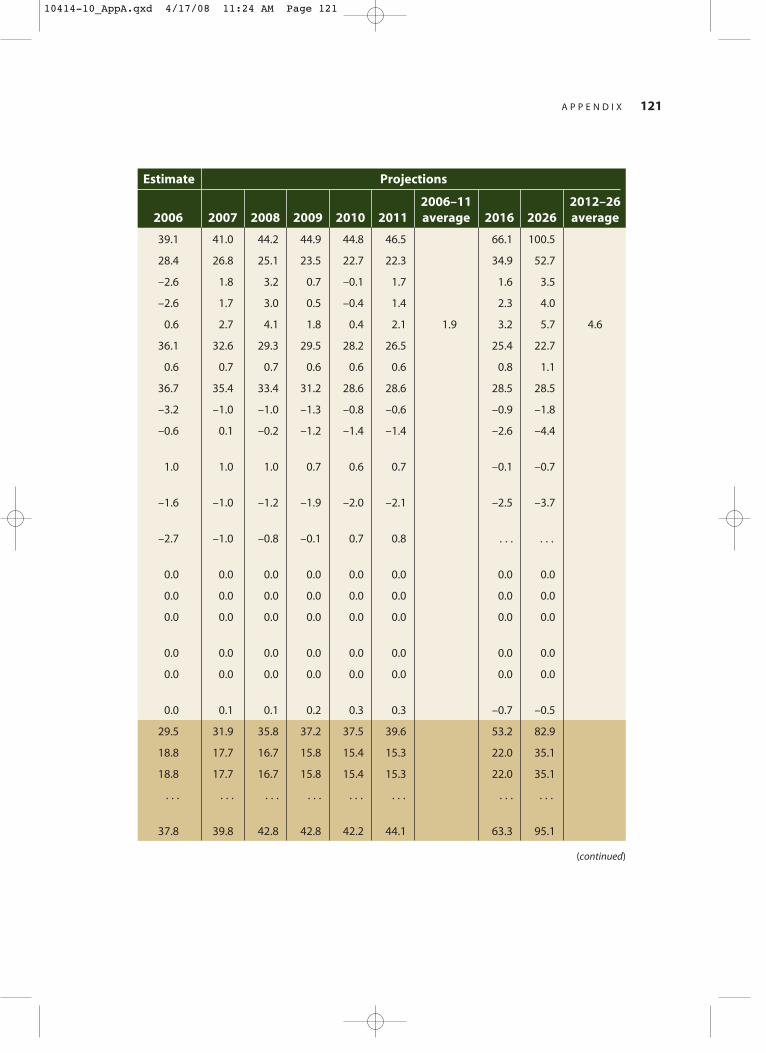

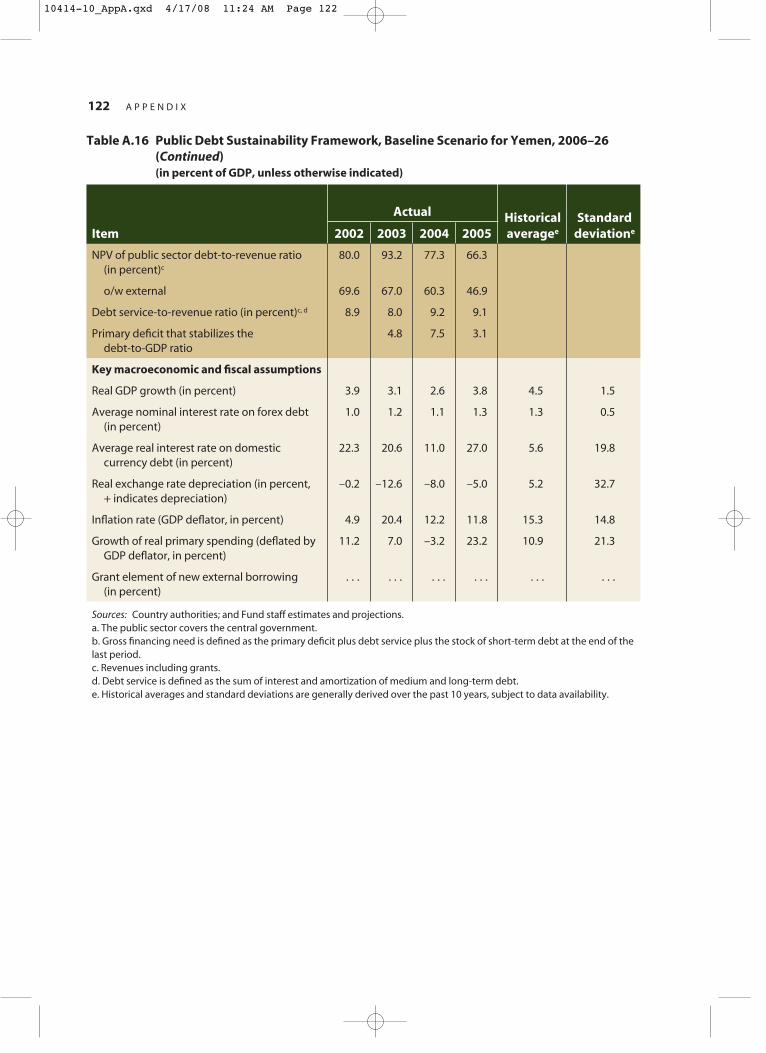

Publicly Guaranteed External Debt, 2006–25 (in percent). . . . . . . . . . . . 116A16 Yemen: Public Sector Debt Sustainability Framework, Baseline Scenario,

2006–2026 (in percent of GDP). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 120A17 Yemen: Sensitivity Analysis for Key Indicators of

Public Debt 2006–2025 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 124A18 Millennium Development Goals for Yemen, 1990–2004 . . . . . . . . . . . . 126A19 Progress under the first poverty reduction strategy in

Yemen, 2003–05 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 128A20 Specific measures to reduce fertility and maternal mortality in Yemen . . . . 129

viii C O N T E N T S

10414-00_FM.qxd 4/17/08 12:16 PM Page viii

CURRENCY AND EQUIVALENTS(As of March 27, 2006)

Currency Unit – Yemeni Rial (YR)US$1 = YR 196

FISCAL YEARJanuary 1-December 31

AFMIS Accounting and Financial Management System

AFPPF Agriculture and Fisheries Production Promotion Fund

A21A Agenda 21 for Agriculture

COCA Central Organization for Control and Audit

CM Certified Midwife

CPIA Country Policy and Institutional Assessment

DFID Department for International Development

DHS Demographic and Household Survey

EITI Extractive Industries Transparency Initiative

EIU The Economic Intelligence Unit

ERF Economic Research Forum

ERP Economic Reform Program

ESMAP Energy Sector Management Assistance Program

FDI Foreign Direct Investment

FHS Family health Survey

FP Family Planning

GAREW-GARWSP General Authority for Rural Water

ix

Acronyms and Abbreviations

10414-00_FM.qxd 4/17/08 11:09 AM Page ix

GCC Gulf Cooperation Council

GDI Gender Development Index

GDP Gross domestic product

GEF Global Environmental Facility

GoY Government of Yemen

GPC General People’s Congress

GST General Sales Tax

HBS Household Budget Survey

HCC Higher Committee for Coordination

HD Human Development

HDI Human Development Index

HIS Health Information System

HU Health Unit

ICA Investment Climate Assessment

IDA International Development Association

IEC Information, Education, and Communication

IMCI Integrated Management of Childhood Illnesses

IMF International Monetary Fund

IMR Infant Mortality Rate

JIA Judicial Inspection Authority

KAP Knowledge, Attitude and Practice

KIT Royal Tropical Institute

KKM Kaufmann, Kraay and Mastruzzi

LAEO Literacy and Adult Education Organization

LC Local Corporations

LDA Local Development Association

MAI Ministry of Agriculture and Irrigation

MCA Millennium Challenge Account

MDGs Millennium Development Goals

MENA Middle East and North Africa

MNA Middle East and North Africa

MNSIF Middle East and North Africa Finance, Private Sector and

Infrastructure Department

MoCS Ministry of Civil Service

MoE Ministry of Education

MoF Ministry of Finance

MoJ Ministry of Justice

MoPHP Ministry of Population and Public Health

x A C R O N Y M S A N D A B B R E V I A T I O N S

10414-00_FM.qxd 4/17/08 11:09 AM Page x

MMR Maternal Mortality Rate

MWE Ministry of Water and Environment

NGOs Non Governmental Organizations

NPC National Population Council

NPP National Population Policy

NWRA National Water Resources Authority

NWSA National Water and Sanitation Authority

NWSSIP National Water Sector Strategic Investment Plan

ORS Oral Rehydration Solution

PAP Population Action Program

PDRY People’s Democratic Republic of Yemen

PEC Public Electricity Corporation

PFM Public Financial Management

PRS Poverty Reduction Strategy

PRSP Poverty Reduction Strategy Paper

PSA Production Sharing Agreements

PSP Private Sector participation

PWP Public Work Program

RH Reproductive Health

SFD Social Fund for Development

SDP Service Delivery Points

SJC Supreme Judicial Council

TFR Total Fertility Rate

UAE United Arab Emirates

UN United Nations

UNDP United Nations Development Program

UNESCO United Nations Educational, Scientific and Cultural

Organization

UNICEF United Nations Children’s Fund

US United States

GST General Sales Tax

WB World Bank

WHO World Health Organization

YAR Yemen Arab Republic

YEM Yemen

YR Yemeni Rial

YSV Yemen Strategic Vision

A C R O N Y M S A N D A B B R E V I A T I O N S xi

10414-00_FM.qxd 4/17/08 11:09 AM Page xi

Vice President Daniela GressaniCountry Director Emmanuel Mbi

Chief Economist & Sector Director Mustapha K. NabliSector Manager Miria Pigato

Task Manager Srinivasan Thirumalai

Team Members. Isabelle Chaal (Team Assistance), Ingrid Ivins (MacroeconomicAnalysis), Thilakaratna Ranaweera (Macroeconomic Projections and Scenarios),Carolin Geginat (Debt Sustainability Analysis), Hadi Esfahani (Political Economyof Reforms), GV Rao (Research and Database), Irina Shaorshadze (Research Assis-tance), Claudia Nassif (Judicial, Legal Reforms and Land Registration, Fisheries),Gail Richardson and Sharon Beatty (Population Policy), Jonathan Walters, TjaardaP. Strom Van Leeuven, Somin Mukherjee, Pierre Audinet (Energy Sector issues),Maher F. Abu-Taleb, Naji Abu-Hatim (Water). Yahia Alanssi provided valuablehelp in facilitating country consultations. Hadi Esfahnai, professor at University ofIllinois at Urbana-Champaign and Sharon Beatty, consultant provided backgroundpapers on political economy of reforms and population policy, respectively. Spe-cial thanks to Mustapha Rouis, Country Manager, Yemen, and peer reviewers BrianPinto and Dorsati Madani for valuable suggestions in guiding the work. EmmanuelMbi, Mustapha K. Nabli, Miria Pigato and Farrukh Iqbal provided critical com-ments and guidance in writing the report.

The team wishes to thank Dr. Mutahar Al-Abassy and Dr. Yahya Mutawakeel andhis team for providing valuable insights in the early stages of the work and for com-menting on the final draft. The DPR team owes it thanks also to government offi-cials, business leaders, parliamentarians and members of civil society for providingvaluable information and interview during DPR mission and for feedback duringconsultation on early results presented in Yemen Roundtable on Growth, Employ-ment and Social Progress, April 9-10, Sanaa, Yemen and a series of three workshopsin conjunction with Country Assitance Strategy consultation held from November19-22, 2005 in Aden and Sanaa, Yemen.

xii A C R O N Y M S A N D A B B R E V I A T I O N S

10414-00_FM.qxd 4/17/08 11:09 AM Page xii

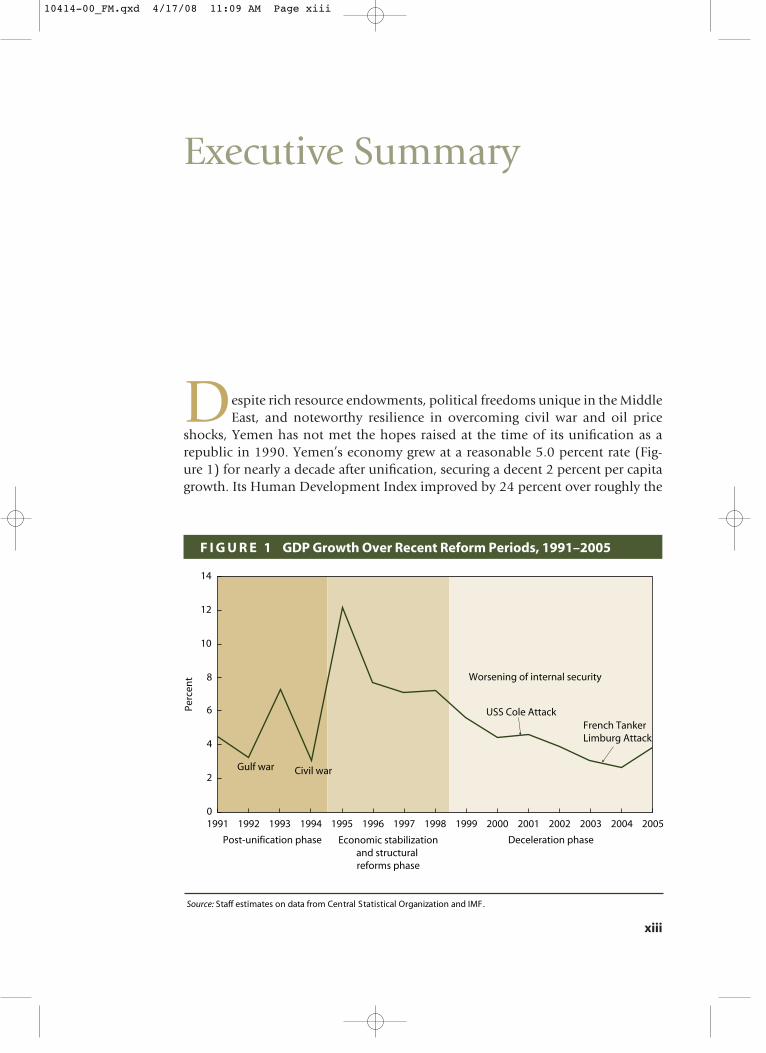

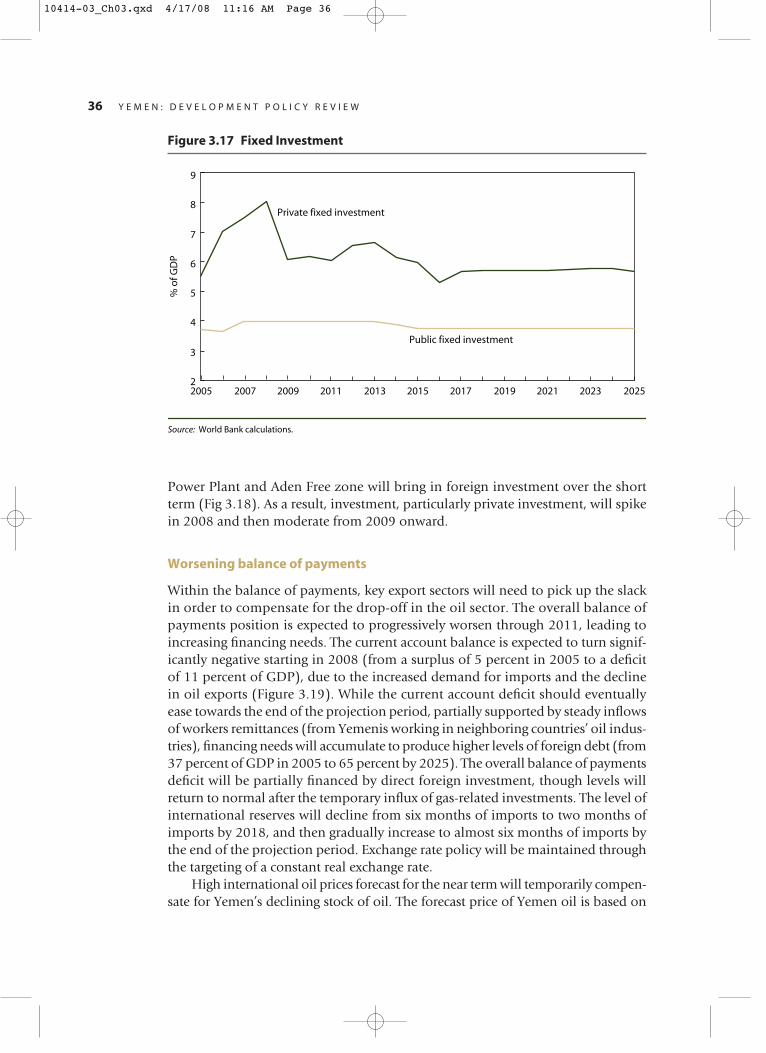

Despite rich resource endowments, political freedoms unique in the MiddleEast, and noteworthy resilience in overcoming civil war and oil price

shocks, Yemen has not met the hopes raised at the time of its unification as arepublic in 1990. Yemen’s economy grew at a reasonable 5.0 percent rate (Fig-ure 1) for nearly a decade after unification, securing a decent 2 percent per capitagrowth. Its Human Development Index improved by 24 percent over roughly the

xiii

Executive Summary

F I G U R E 1 GDP Growth Over Recent Reform Periods, 1991–2005

0

2

4

6

8

10

12

14

Perc

ent

1996

Post-unification phase Economic stabilizationand structural reforms phase

Deceleration phase

Worsening of internal security

USS Cole Attack

Gulf war Civil war

Source: Staff estimates on data from Central Statistical Organization and IMF.

20052004200320022001200019991991 1992 1993 1994 199819971995

French Tanker Limburg Attack

10414-00_FM.qxd 4/17/08 11:09 AM Page xiii

same period, reaching 0.489 by 2003—the second highest improvement for allcountries with low human development.1 Now, however, Yemen has lost momen-tum and trails behind most countries in important dimensions of development.

Today, Yemen is the second poorest country in the Middle East and NorthAfrica region, with 42 percent of its population counted as poor in 1998. GDP hasstagnated at around US$530 per capita in real terms since 2002. Unemployment,estimated at 11.5 percent in 1999, is expected to have worsened as the populationhas climbed at 3 percent a year and the labor force has burgeoned. Extreme genderinequalities persist. Malnutrition is so severe that Yemeni children suffer theworld’s second worst stunting in growth. And natural resources are increasinglyconstrained. Two-thirds of Yemen’s known oil reserves were depleted by 2003, andproduction has already begun to decline and will plummet by 2012 if no newreserves are discovered. Freshwater is also increasingly scarce: per capita avail-ability in Yemen is about 2 percent of the world average and projected to dimin-ish by a third in the next 20 years because of the expected increase in population.

Growth of gross domestic product has slowed as reforms have stalled

Compounding these economic, social, and resource problems are Yemen’s policyand institutional failings, which have prompted donors to cut aid. Yemen receiveda meager US$13 in development assistance per capita in 2004. In 2005, the Devel-opment Assistance Committee cut IDA 14 (2006–08) allocations to Yemen bynearly a third, and the U.S. government’s Millennium Challenge Corporationsuspended Yemen’s eligibility for assistance because of its worsening corruption,regulatory quality, and fiscal policies.

All of these identified challenges, if not well managed, could wreck macro-economic management, fail to revive private sector investment, further depletescarce resources, and add to human suffering, precisely at a time when the govern-ment expenditures will need to be pruned back substantially because of the declinein oil revenues. This Development Policy Review for Yemen reviews recent devel-opment outcomes, identifies key challenges that will affect Yemen’s development,and proposes a selective agenda of reforms. The reforms include measures toimprove fiscal and public sector management, combat corruption, strengthen judi-cial and legal systems, improve land registry, and revise energy, water and popula-tion policies. This report is intended to inform Yemeni authorities in finalizing thesecond Poverty Reduction Strategy Paper (2006–10). It also strives to raise aware-ness about the consequences of the impending oil depletion and to promote morediversified and sustainable development.

Challenges Ahead

The main challenges to Yemen’s growth are the impending rapid decline in oil revenues, the weak capacity of governance institutions, the pressures of high pop-ulation growth, and the worsening scarcity of freshwater. The country has yet to

xiv E X E C U T I V E S U M M A R Y

10414-00_FM.qxd 4/17/08 11:09 AM Page xiv

come to grips with the imminent oil decline and its consequences. The Govern-ment is concerned about governance problems and is recently attempting to speedup reforms. The last two challenges—high population growth and water crisis—are long recognized by the government, but reforms have been slow.

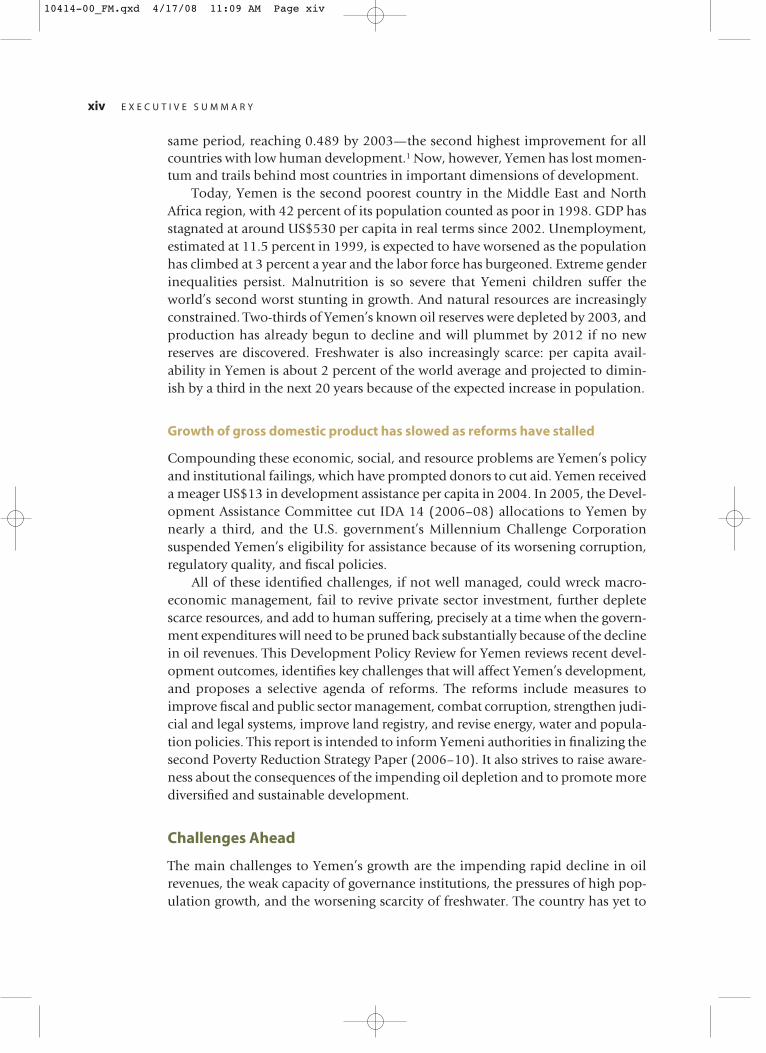

Depleting oil revenues

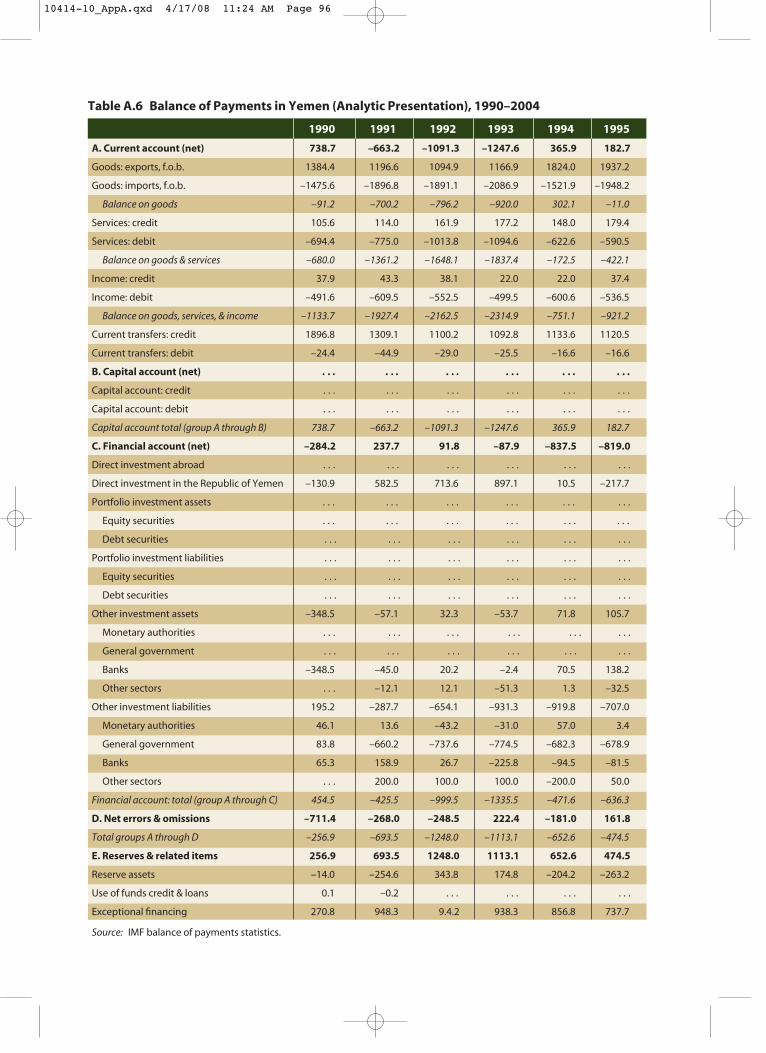

In 2000, Yemen developed a strategic vision for 2025, an ambitious plan for eco-nomic growth founded primarily on the continued extraction of presumed plen-tiful reserves of oil and gas. The proven2 reserves then were estimated to be 5.7 billion barrels; by the end of 2005, however, the proven reserves were only atenth as much.3 Oil production has leveled off since 2001 and started to decline.The sum total of proven and probable reserves now is expected to last for only eight years at the current rate of production (Figure 2). New discoveries thus far in 2005–06 could help in slowing the decline in production but not eliminate it4. With 90 percent of exports coming from oil and 70 percent of government revenue dependent on oil, the disappearance of oil as a revenue resource will haveserious consequences: unless non-oil exports grow rapidly, external debt willbecome unsustainable. The resource crunch for the government would under-mine hard-won macroeconomic stability and hinder provision of even basic social services.

E X E C U T I V E S U M M A R Y xv

F I G U R E 2 Oil Production in Yemen, 1986–2004 and Forecasts to 2010

0

50

100

150

200

250

300

350

400

450

500

1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Tho

usa

nd

bar

rels

/day

Past production Forecast

Scenario A

Scenario B

Source: World Bank 2004. Scenario A: PEPA estimates based on future oil production in existing production blocks. Scenario B: World Bank estimates based on data provided by industry and PEPA on existing and new production blocks.

10414-00_FM.qxd 4/17/08 11:09 AM Page xv

The government of Yemen has found it difficult to diversity exports.5 The dis-covery of oil in 1984 averted a crisis looming because of the collapse of remittanceflows and external assistance. The initial estimate of low oil reserves of 1 billionbarrels was tripled subsequently. The initial estimate of gas reserves at 4 trillions ofcubic feet (tcf) was eventually quadrupled. Even now, the government is eitherexploring or producing oil from only 29 of the possible 78 blocks,6 supporting thehope that more oil could be found. More active exploration for gas could raise theestimate of gas reserves, too.

Yemen’s oil production will soon fall off dramatically

Although oil reserves could increase in the future and gas exports could partiallyoffset the loss of oil revenues, reorienting to non-oil-based development is urgentfor two important reasons. First, export diversification will generate jobs. The entireoil sector employed only about 21,000 Yemenis in 2003, while some 190,000 newentrants to the job market sought work. With youth unemployment raging at 30 percent or more, the need for labor-intensive growth is urgent. Second, diversi-fying the export base will take time. The history of countries that achieved success-ful diversification, such as Costa Rica, Malaysia, or the United Arab Emirates,shows that it takes at least a decade or more for diversification polices to bear fruit.

Weak governance

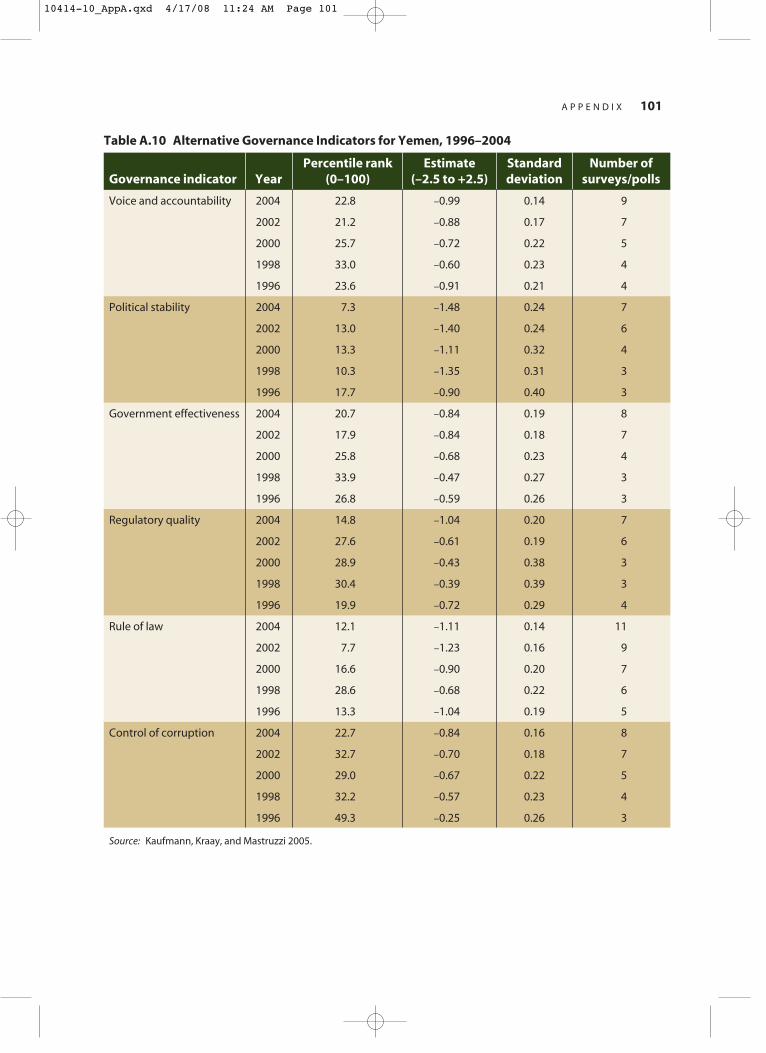

The quality of governance in Yemen deteriorated until 2004. Corruption andbureaucratic quality both worsened from 1996–98 to 2002–04. During the sameperiod, many other measures of administrative capacity, public accountability, andpolitical rights remained unchanged, but low. Besides, Yemen’s quality of gover-nance is the weakest among its neighbors.7

Since 2005, improvement in select governance components is discernible. Twoof the six dimensions of governance – control of corruption and regulatory qual-ity—improved in 2005 (Figure 3). Further, policy changes initiated since January2006 under the six-month National Reform Agenda8 (NAR) should also lead toimprovements in the future. Some of the completed reforms under the NAR thathave a bearing on governance quality are:

The independence of Central Organization for Control and Audit hasimproved. A new financial disclosure law for all public servants has been legislated.A substantial number of ghost workers and double-dippers have been identified.A new, internationally comparable, anti-corruption law is on the anvil and the gov-ernment is planning to join the Extractive Industry Transparency Initiative.

Judicial independence has improved. The President of the Republic is nolonger the head of Supreme Court. The judicial infrastructure is under improve-ment. The World Bank’s investment climate assessment of 2005 notes a dramaticdecline in percentage of firms identifying crime as serious constraint to businessbetween 2001 and 2005.

xvi E X E C U T I V E S U M M A R Y

10414-00_FM.qxd 4/17/08 11:09 AM Page xvi

Corruption is perceived to be a serious issue in Yemen, both by the govern-ment and by local firms. About 80 percent of the firms surveyed mentionedcorruption as a modest or very severe constraint on their operations. Many in-ternational rating agencies concur. Transparency International’s Corruption Per-ception Index places Yemen 103rd out of 159 countries surveyed in 2005. Since2003, the government has taken measures to set up laws and institutions for fight-ing corruption, and in 2005 it ratified the UN convention against corruption. Butto date, no case has been pursued against a high-profile person for corruption.

Severe water crisis

In Yemen’s water-scarce environment, the use of groundwater has been drivingrural growth for the past 30 years, but in an unsustainable and inequitable man-ner. Groundwater abstraction has steadily increased since the mid 1980s in mostareas of Yemen. There are about 50,000 private wells in the country (8,000 opera-tional wells in the Sana’a Basin alone, half of which are tubewells), together withmore than 200 drilling rigs. Groundwater use began to exceed recharge in the mid1980s, with more than 80 percent of abstraction going to irrigated agriculture. Atthe present rate of depletion, the sustainability of livelihoods is jeopardized.Already, farming has been scaled down or abandoned, and some communities andtowns are also running out of domestic water.

The average tariff in Sana’a for domestic water supply and sanitation is YR100 per cubic meter (US$0.52 per cubic meter), based on a typical household

E X E C U T I V E S U M M A R Y xvii

F I G U R E 3 Quality of Governance in Yemen, 1996–2005

–1.8

–1.6

–1.4

–1.2

–1

–0.8

–0.6

–0.4

–0.2

0

1996

Political stability/no violence

Regulatory quality

Rule of law

Control of corruption

Source: Governance Matters V: Governance Indicators for 1996–2005 by D. Kaufmann, A. Kraay, and M. Mastruzzi.

200520042003200220001998

Government effectiveness

Voice and accountability

10414-00_FM.qxd 4/17/08 11:09 AM Page xvii

that consumes less than 35 cubic meters per month. Given the efficiency losses inthe distribution system, the average monthly bill is not enough to cover operationsand maintenance costs plus depreciation, let alone investments. At these low levels of tariffs, consumers have no incentive for water conservation and suppliershave no incentive to improve performance.

High population growth

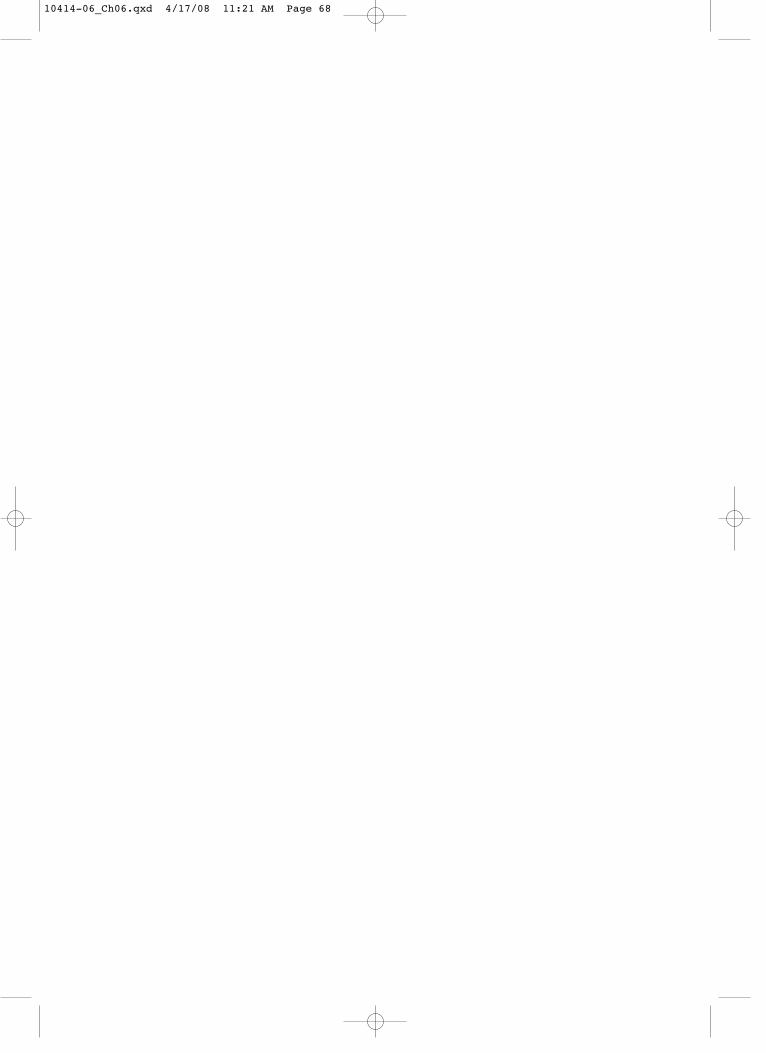

Yemen’s population growth, at 3 percent annually, is high by regional standardsand in comparison with countries with similar levels of per capita income. Yemen’sfertility rate began to slow in early 1990s, as economic and social developmentbrought conditions that have created a “demographic transition” to lowerbirthrates in many countries. But this transition appears to have stalled in Yemen(Figure 4). The rate of decline in the fertility rate has slowed between 1997 and2003.

The demographic transition to lower birth rates is slowing

On current trends, the population will nearly double to 40 million in 20 years,nearly 5 million higher than the target of the national population policy adoptedin 1997. Each new Yemeni child born is estimated to cost the government US$250annually in 2005 prices for education and health care.9 The slowing of fertilitydecline is mainly attributed to the slowing in the spread of contraceptive use since1997.

xviii E X E C U T I V E S U M M A R Y

F I G U R E 4 Fertility in Yemen, 1988–2004 and Forecasts to 2025

8.3

7.6 7.4

6.56.2

4

3.3

0

1

2

3

4

5

6

7

8

9

Target

Current Trend

Source: Staff calculations.

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 2024

10414-00_FM.qxd 4/17/08 11:09 AM Page xviii

The Reform Agenda

Yemen’s active reform program in the mid 1990s propelled economic growth (asseen in Figure 1), but the recent history of weak governance, widespread corrup-tion, and heightened risk of internal conflicts has undermined the implementationof many later reform efforts. Chapter 2 looks in detail at reforms in Yemen sincethe mid-1990s to compare the period of strong reform in 1995-98 with the slug-gish period that followed. That analysis underscores the importance of changes ininstitutional quality for the implementation of reforms. It thus is a foundation fordesigning current efforts to address Yemen’s four challenges.

The reform agenda encompasses five main goals: maintaining fiscal sustain-ability (the subject of Chapter 3), improving the investment climate (Chapter 4),managing energy resources (Chapter 5), managing water resources (Chapter 6),and slowing population growth (Chapter 7).

Maintaining fiscal sustainability

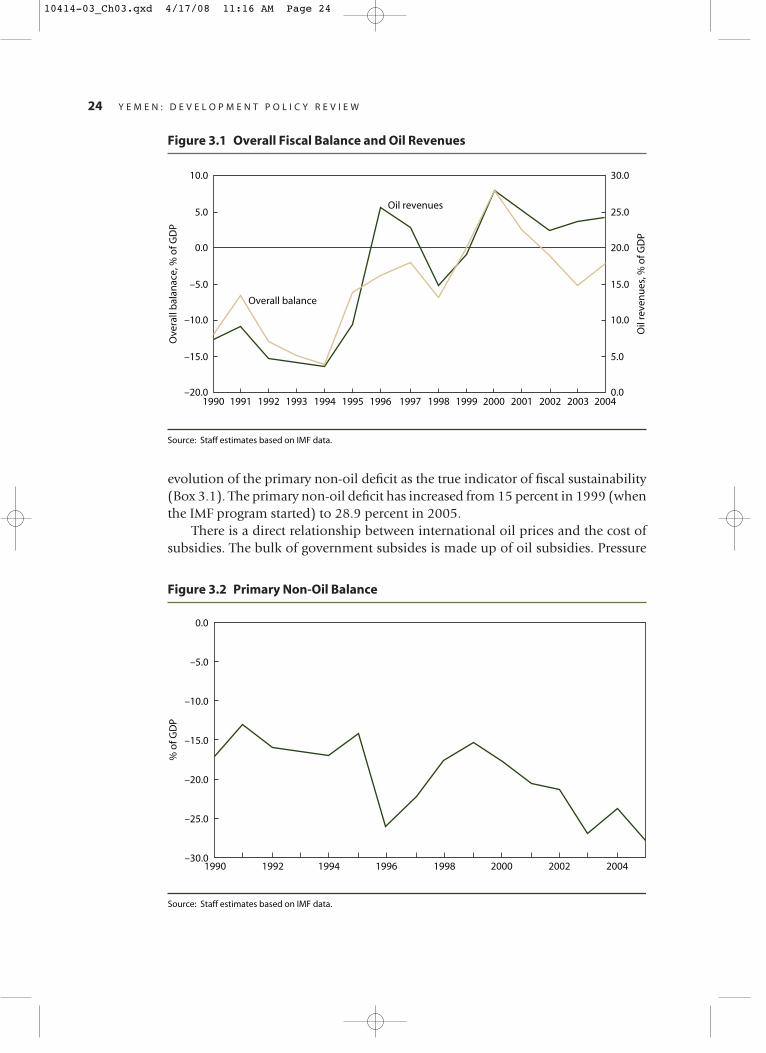

For a government like Yemen, drawing on substantial oil revenues, fiscal sustain-ability10 is a stringent requirement, because the mining of exhaustible oil reduceswealth for the next generation. The government has an obligation to preserve itswealth (absolutely or in per capita terms). When governance is weak, the sustain-ability rule is even more restricting, because domestic and foreign lenders demandmore immediate demonstration of credibility that their debt will be repaid.

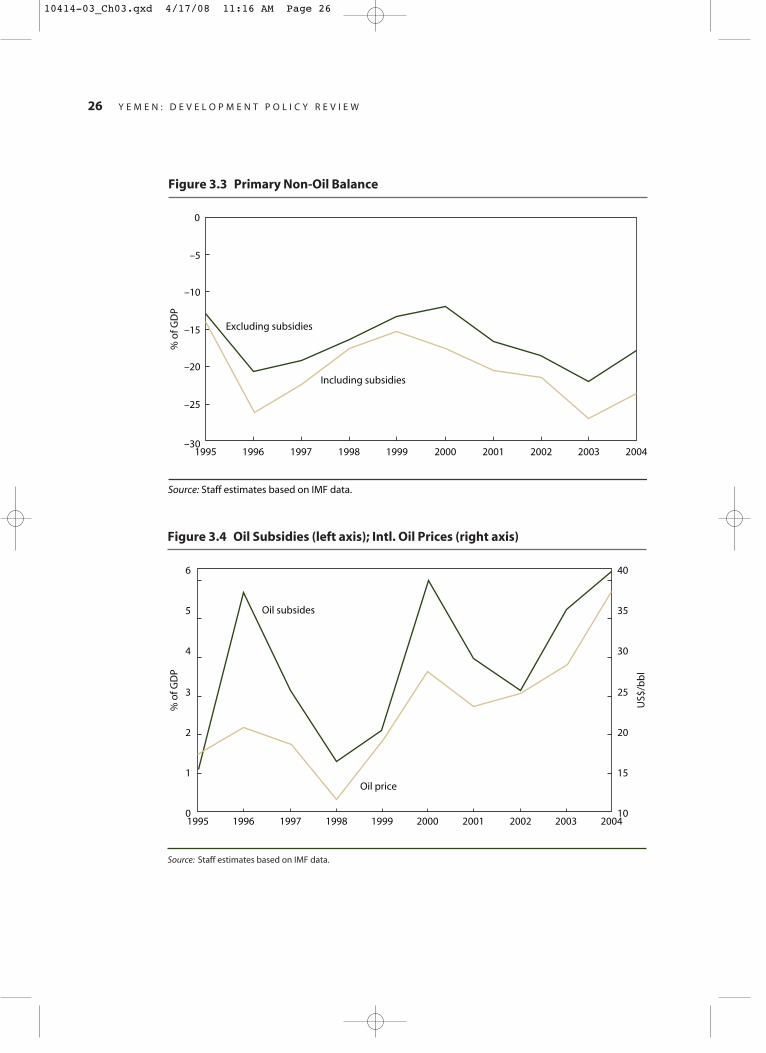

The track record of fiscal sustainability in Yemen is poor. The primary non-oildeficit—the correct indicator of fiscal sustainability—has stayed well above theoptimal11 level of 5 percent of GDP. Fiscal sustainability has steadily worsened.Since 1999, the cumulative depletion of oil wealth (derived from oil revenues)amounted to about US$19 billion. Since the Central Bank’s own foreign reservesincreased by about US$4 billion over this period, it can be presumed that onlyabout a quarter of the depleted oil wealth has been converted to financial wealth.Untargeted subsidies for domestic petroleum consumption and inadequate taxefforts lie at the root of this fiscal profligacy.

Looking forward, Yemen’s high risk of fiscal unsustainability and moderatestress in meeting external debt obligations calls for a variety of measures:

� Expenditures must be cut. Yemen needs to prune current expenditure from 31 per-cent of GDP in 2005 to 22 percent by 2015 and increase tax efforts from 7 per-cent of GDP to 14 percent by 2015. Even with these tough fiscal measures, thenet present value of government debt will increase from 25 percent of GDP to74 percent of GDP by 2025. If the tough fiscal measures are not implemented,the net present value of debt will balloon to 260 percent of GDP in the nexttwenty years. The level of domestic borrowing implied in this scenario carriesserious risk of inflation because of monetary financing. If Yemen continues toborrow at concessional rates, external debt could, on average, remain around 23 percent of GDP.

E X E C U T I V E S U M M A R Y xix

10414-00_FM.qxd 4/17/08 11:09 AM Page xix

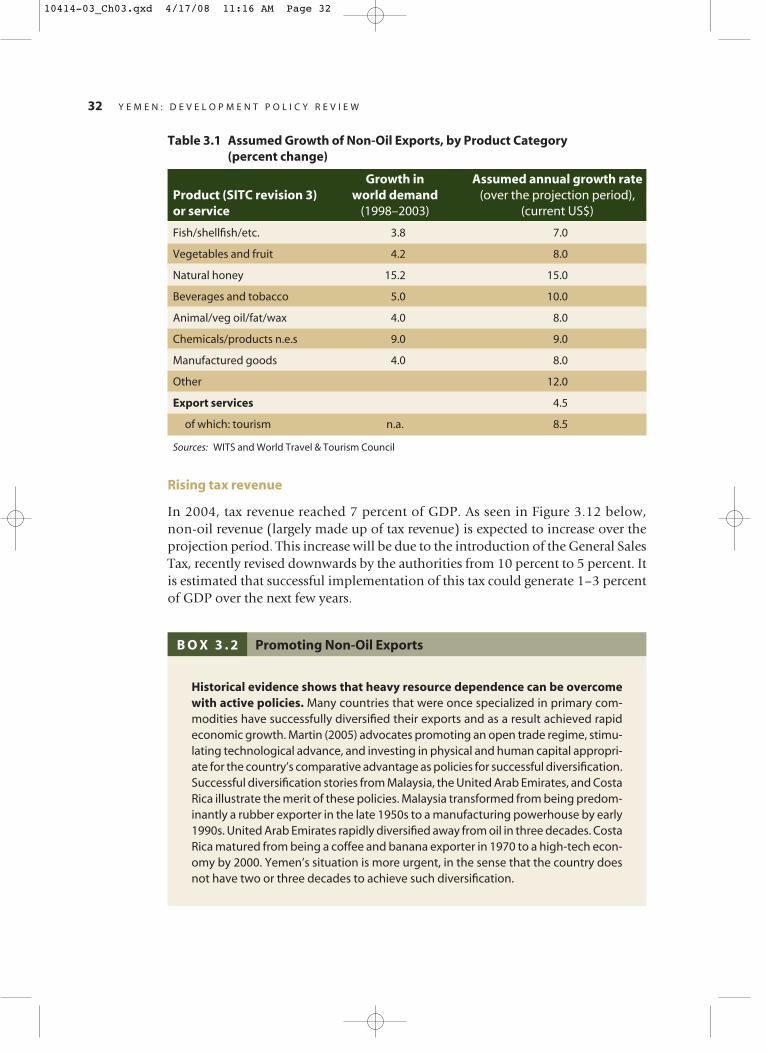

� Tax revenues need to be more than doubled. In 2004, tax revenue was 7 percent ofGDP. By 2015, tax revenues must raise to 15 percent of GDP to partly compen-sate for the loss of oil revenues. This increase will be due to the introduction ofthe general sales tax, recently revised downwards by the authorities from 10 per-cent to 5 percent. It is estimated that successful implementation of this tax couldgenerate 1–3 percent of GDP over the next few years.

� Public financial management must be improved. Completing reforms to publicfinancial management will hold the key to successful public expenditure man-agement. Public financial management needs to be strengthened in all majorareas – budget programming and prioritization; budget execution; treasury andcash management; internal controls; internal audit; external audit; financialreporting and oversight.

� Civil service reform must be completed. Completing civil service reforms is essen-tial to generate savings and build a competent civil service. Yemen’s civil serviceis considered to be underpaid, while at the same time overstaffed. The wage billaccounts for nearly one-quarter of the government’s current expenditure, one ofthe highest levels in Middle East and North Africa. The government started toimplement a four-stage National Wage Strategy in July 2005, and that planneeds to move forward.

Improving the investment climate

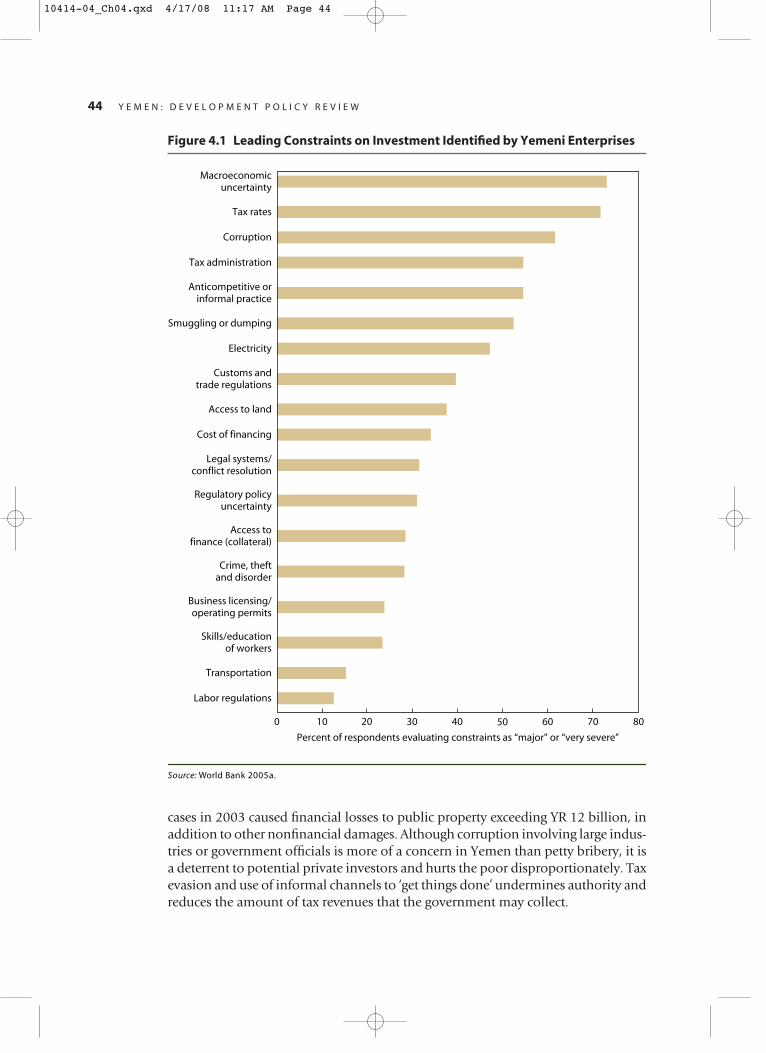

Private investment in Yemen has collapsed for lack of adequate returns. After peak-ing in 1998, private investment slumped in 1999 and continued to fall steadily toreach a mere 10 percent of GDP, halving from the average during the period ofreforms. After the initial enthusiastic response to stabilization and early reforms,private investors have held back on investment because of poor returns. Yemenishave consistently been saving more than they can invest since 1999. Most of banklending has been confined to trade credit. Foreign direct investment has beenrestricted to the oil sector.

The main constraints to investment in the private sector are identified by thenew Investment Climate Assessment (ICA) for Yemen. Based on firms’ own iden-tification of constraints and other analysis, the ICA finds four key areas where theinvestment climate constrains the ability of the private firms and investors torespond to market opportunities, stimulate growth, and generate jobs: (a) macro-economic instability, (b) tax and regulatory burdens, (c) weak governance, partic-ularly expressed as corruption and (d) inadequate infrastructure services, especiallyfor electricity, land, and water supply, and (e) insufficient access to finance.

Many of these constraints can be addressed by measures to strengthen gover-nance—notably, by creating greater accountability, transparency, and efficiency inthe judicial system. Though Yemen’s judiciary has newly acquired independenceunder the National Reform Agenda of 2006, judges and administrators are poorlytrained. The courts lack physical infrastructure to file and retrieve records quickly.The reform agenda is intended to do the following:

xx E X E C U T I V E S U M M A R Y

10414-00_FM.qxd 4/17/08 11:09 AM Page xx

� Speed the processing of cases. Providing training, computers, information manage-ment systems, and other resources to judges and court personnel would reducecase backlogs and accelerate the disposition of new disputes. Revising the pro-cedures for filing and resolving lawsuits would help to weed out procedures thatinvite delay and raise costs.

� Increase access to alternative dispute mechanisms: The creation of mediation andconciliation services and other alternatives to resolving disputes in the courtsreduces court costs, as does the introduction of small claim courts.

� Professionalize bench and bar. Professional training, now lacking in Yemen, isneeded to enhance the performance of the main actors and instill the values ofimpartiality, professionalism, competency, efficiency, and public service. Train-ing needs to target administrative and notary staff as well as judges, and addressthe different requirements in specialized courts.

� Improve the administration of land tenure security. This encompasses initiatives toincrease the limited demand for registration (by, for example, removing incen-tives for using court authentication as an alternative to registration), as well asenhance the quality and efficiency of registration services (by improving regis-tration processes and maintenance).

� Make state land management efficient. The present state land management processis in need of an overhaul. Key issues in improving state land management wouldinclude, among others, to more clearly define state-owned land in the law, setup a comprehensive and centralized inventory of state-owned land, betterenforce existing measures to curb land speculation, as well as to identify andapply standardized procedures for the disposition of state land.

� Take advantage from international experience in the current revision of the law gov-erning land registration. The government of Yemen is moving in the right direc-tion with its initiative to replace the current land registration law. The draft lawsproposed, however, show some weaknesses and could be amended to facilitateeffective registration, ensure financial sustainability of the registry system, andstrengthen the legal effect of the registry system.

Managing energy resources

Though Yemen’s oil reserves are depleting fast, management and investment of theremaining reserves, indicatively valued at US$ 30 billion (nearly 200 percent ofGDP) in 2005 prices, is of paramount importance to Yemen’s future. The govern-ment’s efforts to save oil revenues need to be strengthened. The government man-aged to add to its financial wealth only a quarter of the oil bonanza since 1999. Forimproving the management of oil and gas revenues, Yemen should consider join-ing the Extractive Industry Transparency Initiative, ending petroleum subsidies ina gradual but time-bound way, and improving the efficiency of the downstreampetroleum sector. An incentive framework to develop gas resources would alsohelp in finding and exporting gas. Additional reforms are also suggested in Chap-ter 5 to increase the reliability of electrical power generation.

E X E C U T I V E S U M M A R Y xxi

10414-00_FM.qxd 4/17/08 11:09 AM Page xxi

� Endorsing the Extractive Industries Transparency Initiative (EITI) would improve thegovernment’s credibility with civil society and the international donor commu-nity. This would call for regular publication of all oil, gas, and mining paymentsand revenues (by companies and by the government); making the publicationaccessible to the public; having payments and revenues subject to a credible,independent audit; and active engagement of the civil society in design, mon-itoring and evaluation of the EITI implementation process. Yemen placesdetailed oil sector information in the public domain, and is comparable tocountries that have already adopted the EITI12.

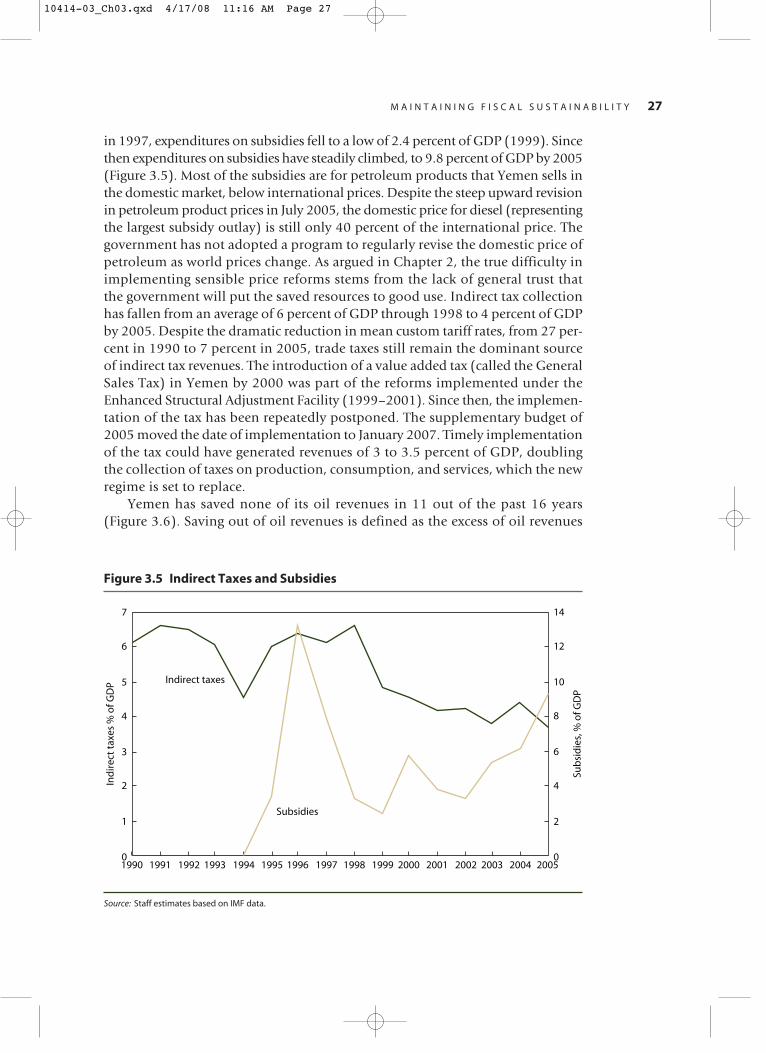

� Phasing out petroleum subsidies would improve macroeconomic stability. Despitethe steep raise in the administered prices of petroleum products for domesticconsumption, the subsidies remain large (9 percent of GDP in 2005), and theyare still well below international prices. Phasing the subsidy removal for all fueltypes gradually over two years would help avoid redirection of demand betweenfuels and allow the social protection mechanism to work.

� Improving efficiency in petroleum refining and distribution would conserve resourcesand improve fiscal sustainability. The absence of quality standards for refinedoil products combined with adopting inappropriate international referenceprices for calculating oil products that are sold domestically act as an incentiveto refineries to import low quality oil products for supplying to the domesticmarket and exporting higher quality products and crude oil. The power sectorsuffers from the varying and low quality of the fuel oil supply it is obligated tobuy from the government refineries. Yemen also lacks relevant environmentallaws and regulations on production and use oil and gas, and the establishmentof quality standards and requirements for oil products.

Managing water resources

The government is well aware of the water sector issues and started institutionalreforms since 1996 with donor support. Set against the key objectives in the watersector, the reform program has made a difference, but results have been slow. Inwater resources management, some instruments have been prepared and tested,but no significant reduction to groundwater overdraft, or improvement in inter-sectoral allocation or in water use efficiency is evident. In water supply and sanita-tion, reforms have started, but limited impact has been felt by the consumer, andonly in some urban areas. In irrigation, some efficiency gains have been achievedbut resource depletion has continued. In watershed management, resources andmanagement effort have been tied up in a controversial dams program, which ledto the neglect of broader objectives such as basin efficiency and poverty reduction.The reform agenda addresses:

� Depletion of groundwater. Lacking strong public governance structures, over-mining of groundwater can be controlled by alternative means. Such alternativemeans include intensive user involvement and organization, self-regulation by

xxii E X E C U T I V E S U M M A R Y

10414-00_FM.qxd 4/17/08 11:09 AM Page xxii

water user associations, monitoring and information sharing, tradable waterrights, and improving incomes through technological improvements.

� Watershed management. Current watershed management activities are concen-trated on the flawed small dams program, which does not often improve over-all basin efficiency and suffers from poor design, questionable contractingpractices, and low construction standards. Given the multi-institutional chal-lenge, there is scope for proactive involvement of donors and nongovernmen-tal organizations to relieve the burden on government agencies, which typicallyfind it hard to coordinate the multiple interventions needed for watershed management.

� Better allocation. Allocation of water to its best economic use can be improvedby introducing economic instruments. The problem with the present privatemarkets is that they are economically inefficient and informal. There is noenabling framework to encourage investment. Water rights are unclear and thereis no provision for equity or sustainable management in the source area. Thedevelopment of more formal water markets should be a priority. At the currentlow levels of tariffs for domestic water supply that does not even cover operat-ing and maintenance costs, consumers see no incentive for water conservationwhilst suppliers have no incentive to improve performance.

Slowing population growth

Speeding up the demographic transition is possible, as it has been achieved in Iranand Oman, countries culturally similar to Yemen. Iran lowered total fertility ratefrom 6.6 births per woman in 1985 to near replacement levels of 2 in 2005 byusing support from religious institutions, combined with sound maternal healthpolicies. In Oman, expansion of education opportunities for girls and health ser-vices seems to have helped in lowering the total fertility rate.

Yemen has a sound population policy that enjoys wide support. The Popula-tion Action Program 2001–10 follows a comprehensive and integrated approachof reproductive health care and human development. This comprehensive policyfollows international standards in targeting the most important known demo-graphic determinants and is consistent with the measures found to be successfulin other countries.

Implementation has been weak, however, because of limited resources andweak governance mechanisms. Per capita government expenditure on health isabout US$6, compared with the estimated requirement of US$54 per capita peryear needed to meet Yemen’s Millennium Development Goals for health. Imple-menting programs selectively to support information campaigns, health of chil-dren and mothers, and education of girls could help achieve reduction in fertility.

E X E C U T I V E S U M M A R Y xxiii

10414-00_FM.qxd 4/17/08 11:09 AM Page xxiii

10414-00_FM.qxd 4/17/08 11:09 AM Page xxiv

Yemen’s unification in 1990 has shaped the country’s subsequent development.The Yemen Arab Republic (North Yemen) was a lower middle-income coun-

try before 1990, functioning under a capitalist system. Compared with the People’sDemocratic Republic of Yemen (South Yemen), the North enjoyed a gross domesticproduct seven times larger, a population four times bigger, and a per capita GDPnearly 50 percent greater. The smaller and poorer South Yemen, however, had itsstrength in better health, education, and gender outcomes, because of 23 years ofsocialism preceding the unification. Some of the key problems facing united Yemenhave their origin in the era before unification and in the terms of merger. The largecivil service and difficulties in land titling are legacies of the socialist era of SouthYemen. Difficulties in improving health or gender outcomes arise from the relativelyconservative values in the northern part of Yemen.

Since unification, Yemen has successfully overcome a civil war in 1994, copedwith the return of around 800,000 Yemenis working in the Gulf countries, andweathered several adverse economic shocks, including interrupted flows of remit-tances, volatile oil prices, and suspension of most foreign aid. The negative spilloverfrom the Iraq War also affected Yemen. Yemen continues to suffer from internal secu-rity issues.13 Traffic through Aden—the best natural port in the region—has barelyrecovered to the levels of 1988.

Yemen continues to suffer from weak institutions and a high risk of internal con-flict. Although the World Bank ranks Yemen barely above the categorization of low-income countries under stress, the U.K. Department for International Development,an important bilateral donor for Yemen, has labeled Yemen as a fragile state sinceJanuary 2005.14 The index of failed states compiled by Foreign Policy magazine andthe Fund for Peace ranks Yemen eighth in a global list of 60 countries rated for riskof state failure, ahead of Afghanistan. The categorization of Yemen as a fragile stateunderscores its difficulties in initiating and sustaining sound economic and socialpolicies. This difficult operating environment calls for Yemen’s development part-ners to take a more selective, nuanced approach to reforms.

Yemen’s prospects are mixed, as democratic institutions are slowly taking rootbut the main engines of economic growth are sputtering. Helped by a vibrant but

1

Yemen TodayMixed Development Outcomes

1

10414-01_Ch01.qxd 4/17/08 11:15 AM Page 1

somewhat muzzled press (third worst in the Middle East and North Africa), anascent multiparty democratic tradition is taking root in Yemen. The holding ofthree multiparty parliamentary elections in 1993, 1997, and 2003, and the firstdirect presidential elections in 1999 are seen as substantial steps toward democ-racy. The passage of a law on local authority in 2000 is viewed as a major instru-ment of decentralization to elected councils at governorate and district levels.

Until 1984, foreign aid and worker remittances served as the main sources ofYemen’s foreign exchange. After the discovery of oil in 1984, it quickly emergedas the major foreign exchange earner, accounting for 90 percent of merchandiseexports. However, Yemen’s oil is depleting fast: at the current rate of production rate,oil supplies will be exhausted in merely eight years. Water resources, too, are scantand being overexploited. Demographic dynamics exacerbate the scarcity of Yemen’slimited and declining natural resources. High birth rates (six per woman) and pop-ulation growth (3 percent per year) combine with rising labor force participation(especially among women in rural areas) to keep Yemen’s labor force growing by3.8 percent per year. Thus Yemen faces the stark reality that, if oil runs out and thelooming water crisis cannot support sustained growth in agriculture, an exodus ofworkers abroad could become inevitable, unless non-oil sectors grow rapidly.

Macroeconomic Outcomes

For nearly a decade after the 1990 unification, Yemen achieved a reasonable annualGDP growth rate (around 5.2 percent), securing a decent 2 percent per capitagrowth. The integration of North and South Yemen provided a bigger market; newoil wells came on stream in 1994, boosting oil production by 80 percent; and a suc-cessful macroeconomic stabilization and reform program in the second half of the1990s controlled inflation, liberalized trade, reduced subsides, unified the exchangerate regime and reformed the financial sector. Economic growth peaked in the period1995 to 1998 (see Figure 1).

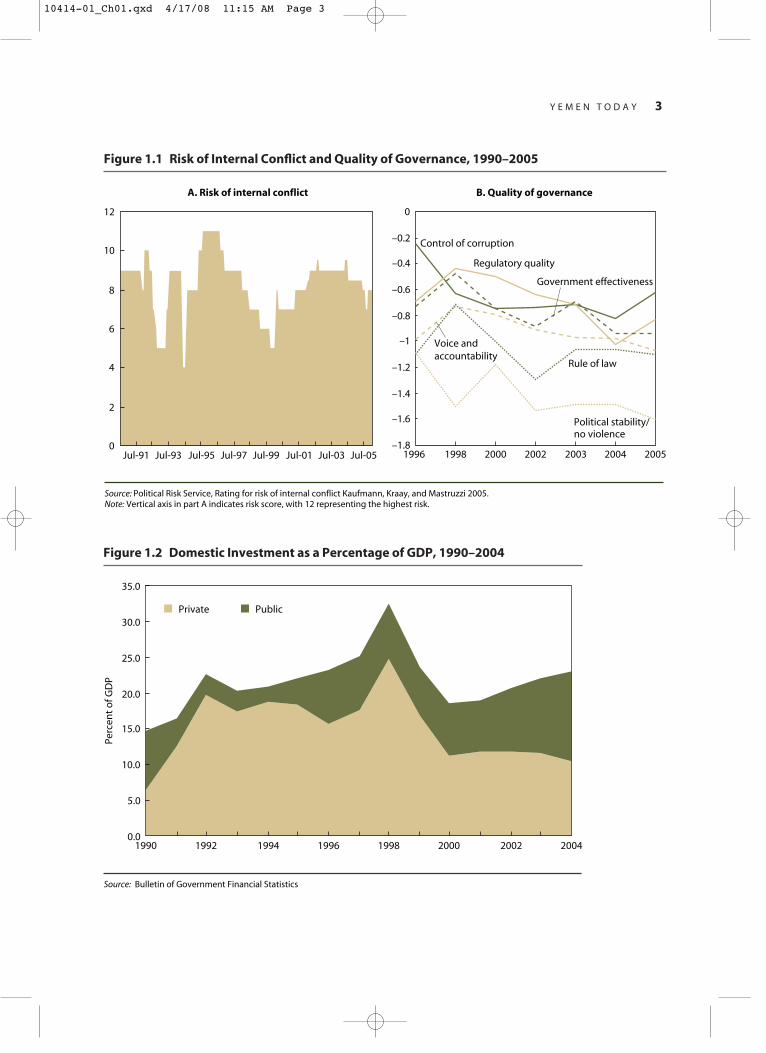

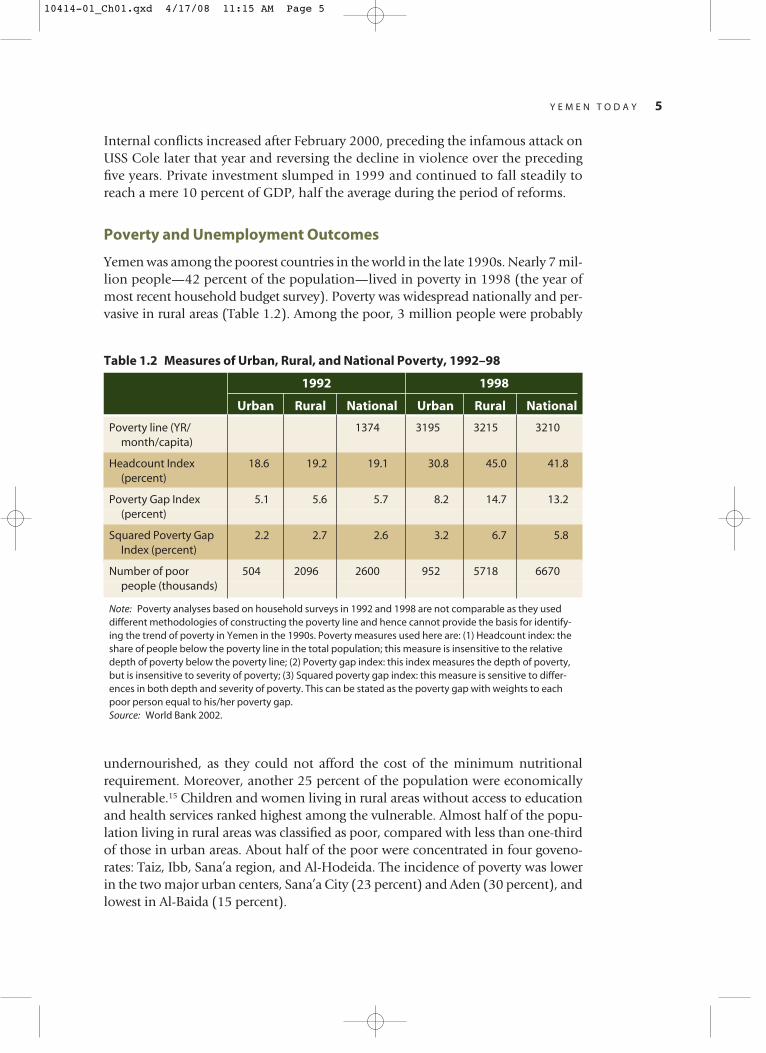

The steady decline in internal conflicts in the second half of the 1990s and theimprovement in four of the six dimensions of governance (Figure 1.1) encouraged asurge in domestic private investment (Figure 1.2). There was little support, however,from foreign direct investment (Figure 1.3). Endowed with a small manufacturingbase and rooted historically in a strong tradition of trading, Yemen’s economy isdominated by the service sector, which responded well in the reform period, pro-ducing nearly half of GDP (Table 1.1). Within the service sector, the trade, transport,and hospitality sectors were the main forces behind the growth spurt. Integration ofthe North and South also increased the internal flow of goods and people. The fiscaldeficit in this period was steadily shrinking under the stabilization program agreedwith the International Monetary Fund, and therefore much of the growth came fromprivate sector investment.

Since 1999 GDP growth has slipped steadily. Revenue from the dramaticincreases in oil prices since 2000 and the outbreak of anti-government rebellion inparts of the country distracted the government from maintaining the momentumof the reforms. Over this period, quality of governance also deteriorated steadily.

2 Y E M E N : D E V E L O P M E N T P O L I C Y R E V I E W

10414-01_Ch01.qxd 4/17/08 11:15 AM Page 2

Y E M E N T O D A Y 3

Figure 1.1 Risk of Internal Conflict and Quality of Governance, 1990–2005

Figure 1.2 Domestic Investment as a Percentage of GDP, 1990–2004

A. Risk of internal conflict

0Jul-91 Jul-93 Jul-95 Jul-97 Jul-99 Jul-01 Jul-03 Jul-05

2

4

6

8

10

12

Source: Political Risk Service, Rating for risk of internal conflict Kaufmann, Kraay, and Mastruzzi 2005. Note: Vertical axis in part A indicates risk score, with 12 representing the highest risk.

–1.8

–1.6

–1.4

–1.2

–1

–0.8

–0.6

–0.4

–0.2

0

1996

Political stability/no violence

Regulatory quality

Rule of law

Control of corruption

200520042003200220001998

Government effectiveness

Voice and accountability

B. Quality of governance

0.01990 1992 1994 1996 1998 2000 2002 2004

5.0

10.0

15.0

20.0

25.0

30.0

35.0

Perc

ent

of G

DP

Private Public

Source: Bulletin of Government Financial Statistics

10414-01_Ch01.qxd 4/17/08 11:15 AM Page 3

4 Y E M E N : D E V E L O P M E N T P O L I C Y R E V I E W

Figure 1.3 Foreign Direct Investment, 1990–2004

–400

–200

0

200

400

600

800

1000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

US$

mill

iion

s

Source: International Financial Statistics, IMF, various issues.

Table 1.1 Growth and Composition of GDP, by Sector, 1991–2004

Contribution to growth Share in growth Share in GDP

1991– 1996– 2001– 1991– 1996– 2001– 1991– 1996– 2001–95 00 04 95 00 04 95 00 04

GDP 6.1 7.1 4.2 100.0 100.0 100.0 100.0 100.0 100.0

Oil Sector 1.0 1.3 -0.1 16.4 18.1 -2.0 12.8 16.0 14.5

Non-oil sector 5.1 5.8 4.3 83.6 81.9 102.0 87.2 84.0 85.5

Agriculture 0.9 1.4 0.7 14.2 19.0 16.8 23.9 22.3 21.2

Industry 1.5 0.7 0.7 23.8 9.9 16.4 14.5 14.5 13.9

Services 2.8 3.8 2.9 45.6 53.0 68.8 48.8 47.2 50.4

Source: Staff estimates.

Several reform initiatives floundered: the privatization law of 1999 was never rat-ified, introduction of a general sales tax and the reduction in petroleum subsidieswere repeatedly shelved, political commitment for legal and judicial reformswavered, and the implementation of civil service modernization and health sectorreforms slowed. Since 2000, gains from strong oil prices contributed to terms oftrade gains averaging 4 percent of GDP, reversing the trend of the previous decade.

10414-01_Ch01.qxd 4/17/08 11:15 AM Page 4

Internal conflicts increased after February 2000, preceding the infamous attack onUSS Cole later that year and reversing the decline in violence over the precedingfive years. Private investment slumped in 1999 and continued to fall steadily toreach a mere 10 percent of GDP, half the average during the period of reforms.

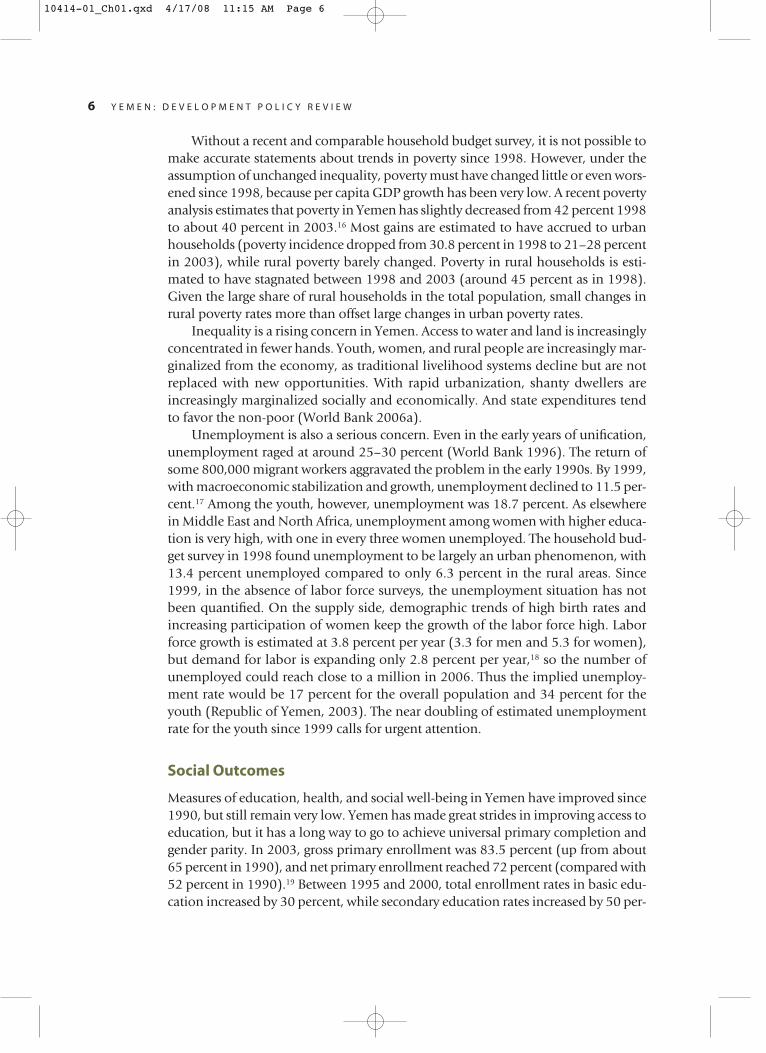

Poverty and Unemployment Outcomes

Yemen was among the poorest countries in the world in the late 1990s. Nearly 7 mil-lion people—42 percent of the population—lived in poverty in 1998 (the year ofmost recent household budget survey). Poverty was widespread nationally and per-vasive in rural areas (Table 1.2). Among the poor, 3 million people were probably

Y E M E N T O D A Y 5

Table 1.2 Measures of Urban, Rural, and National Poverty, 1992–98

1992 1998

Urban Rural National Urban Rural National

Poverty line (YR/ 1374 3195 3215 3210month/capita)

Headcount Index 18.6 19.2 19.1 30.8 45.0 41.8(percent)

Poverty Gap Index 5.1 5.6 5.7 8.2 14.7 13.2(percent)

Squared Poverty Gap 2.2 2.7 2.6 3.2 6.7 5.8Index (percent)

Number of poor 504 2096 2600 952 5718 6670people (thousands)

Note: Poverty analyses based on household surveys in 1992 and 1998 are not comparable as they useddifferent methodologies of constructing the poverty line and hence cannot provide the basis for identify-ing the trend of poverty in Yemen in the 1990s. Poverty measures used here are: (1) Headcount index: theshare of people below the poverty line in the total population; this measure is insensitive to the relativedepth of poverty below the poverty line; (2) Poverty gap index: this index measures the depth of poverty,but is insensitive to severity of poverty; (3) Squared poverty gap index: this measure is sensitive to differ-ences in both depth and severity of poverty. This can be stated as the poverty gap with weights to eachpoor person equal to his/her poverty gap.Source: World Bank 2002.

undernourished, as they could not afford the cost of the minimum nutritionalrequirement. Moreover, another 25 percent of the population were economicallyvulnerable.15 Children and women living in rural areas without access to educationand health services ranked highest among the vulnerable. Almost half of the popu-lation living in rural areas was classified as poor, compared with less than one-thirdof those in urban areas. About half of the poor were concentrated in four goveno-rates: Taiz, Ibb, Sana’a region, and Al-Hodeida. The incidence of poverty was lowerin the two major urban centers, Sana’a City (23 percent) and Aden (30 percent), andlowest in Al-Baida (15 percent).

10414-01_Ch01.qxd 4/17/08 11:15 AM Page 5

Without a recent and comparable household budget survey, it is not possible tomake accurate statements about trends in poverty since 1998. However, under theassumption of unchanged inequality, poverty must have changed little or even wors-ened since 1998, because per capita GDP growth has been very low. A recent povertyanalysis estimates that poverty in Yemen has slightly decreased from 42 percent 1998to about 40 percent in 2003.16 Most gains are estimated to have accrued to urbanhouseholds (poverty incidence dropped from 30.8 percent in 1998 to 21–28 percentin 2003), while rural poverty barely changed. Poverty in rural households is esti-mated to have stagnated between 1998 and 2003 (around 45 percent as in 1998).Given the large share of rural households in the total population, small changes inrural poverty rates more than offset large changes in urban poverty rates.

Inequality is a rising concern in Yemen. Access to water and land is increasinglyconcentrated in fewer hands. Youth, women, and rural people are increasingly mar-ginalized from the economy, as traditional livelihood systems decline but are notreplaced with new opportunities. With rapid urbanization, shanty dwellers areincreasingly marginalized socially and economically. And state expenditures tendto favor the non-poor (World Bank 2006a).

Unemployment is also a serious concern. Even in the early years of unification,unemployment raged at around 25–30 percent (World Bank 1996). The return ofsome 800,000 migrant workers aggravated the problem in the early 1990s. By 1999,with macroeconomic stabilization and growth, unemployment declined to 11.5 per-cent.17 Among the youth, however, unemployment was 18.7 percent. As elsewherein Middle East and North Africa, unemployment among women with higher educa-tion is very high, with one in every three women unemployed. The household bud-get survey in 1998 found unemployment to be largely an urban phenomenon, with13.4 percent unemployed compared to only 6.3 percent in the rural areas. Since1999, in the absence of labor force surveys, the unemployment situation has notbeen quantified. On the supply side, demographic trends of high birth rates andincreasing participation of women keep the growth of the labor force high. Laborforce growth is estimated at 3.8 percent per year (3.3 for men and 5.3 for women),but demand for labor is expanding only 2.8 percent per year,18 so the number ofunemployed could reach close to a million in 2006. Thus the implied unemploy-ment rate would be 17 percent for the overall population and 34 percent for theyouth (Republic of Yemen, 2003). The near doubling of estimated unemploymentrate for the youth since 1999 calls for urgent attention.

Social Outcomes

Measures of education, health, and social well-being in Yemen have improved since1990, but still remain very low. Yemen has made great strides in improving access toeducation, but it has a long way to go to achieve universal primary completion andgender parity. In 2003, gross primary enrollment was 83.5 percent (up from about65 percent in 1990), and net primary enrollment reached 72 percent (compared with52 percent in 1990).19 Between 1995 and 2000, total enrollment rates in basic edu-cation increased by 30 percent, while secondary education rates increased by 50 per-

6 Y E M E N : D E V E L O P M E N T P O L I C Y R E V I E W

10414-01_Ch01.qxd 4/17/08 11:15 AM Page 6

cent. However, the primary completion rate was only about 65 percent and hadfallen short of the two-thirds of population of the relevant age group by 2003. Theadult literacy rate was only 49 percent, and more than 70 percent of women wereilliterate. The government’s objective to achieve universal primary education in thenext ten years requires a much accelerated expansion of the basic education sector,as well as improved efficiency. However, with education spending at 8 percent ofGDP and 20 percent of total government expenditures, Yemen already spends muchmore on education than other countries in the region.

The health status of the Yemeni population is poor. Maternal mortality rate(570 per 100,000 live births) and total fertility rate (6.0 children per woman) arethe highest in the Middle East and North Africa region. Child malnutrition is alsothe highest in the region, and almost half of the Yemeni children suffer from stunt-ing. Contraceptive prevalence rate is very low at 23 percent. More than 1.2 millionYemenis have contracted malaria, and about 20,000 cases of tuberculosis have beenreported. Although a national strategy for combating HIV/AIDS has been devel-oped, no serious actions have been taken to implement it. The prevalence ofHIV/AIDS is not clearly known. In addition, the widespread chewing of Qat alsoaffects public health. Nonetheless, life expectancy has improved significantly forboth sexes since 1990. Women have increased their life expectancy from 52.6 yearsin 1990 to 58.1 in 2002. The infant mortality rate for every 1,000 births decreasedfrom 98 in 1990 to 83 in 2002. In 1998, total health spending was estimated at5.6 percent of GDP, of which about a third was from public sources (excluding allforeign assistance) and almost three-fifths came from private spending. At 3.3 per-cent of GDP, private (out-of-pocket) expenditures on health care in Yemen wereamong the highest in the region.

High rates of gender inequality stubbornly persist, although some progress hasbeen made. Yemen ranks 121 out of 140 countries on the Gender DevelopmentIndex (UNDP, 2005). Although in 1990 female literacy was as low as 12.9 percent,compared with 55.2 for males, by 2002 the female rate had increased to 28.5 per-cent, compared with 69.5 percent for males. Only 33 percent of rural girls wereenrolled in school, compared with 73 percent of rural boys and 78 percent of urbangirls. Female adult illiteracy (at 78 percent in rural areas and 40 percent in urbanareas) is more than twice that of males (32 percent in rural areas and 15 percent inurban areas). Young and relatively educated women (age 15–29) have a higher rateof unemployment than their male counterparts: 56 percent of all female unem-ployment is among young women compared with 47 percent for young men(World Bank 2004a).

Achievability of the Millennium Development Goals

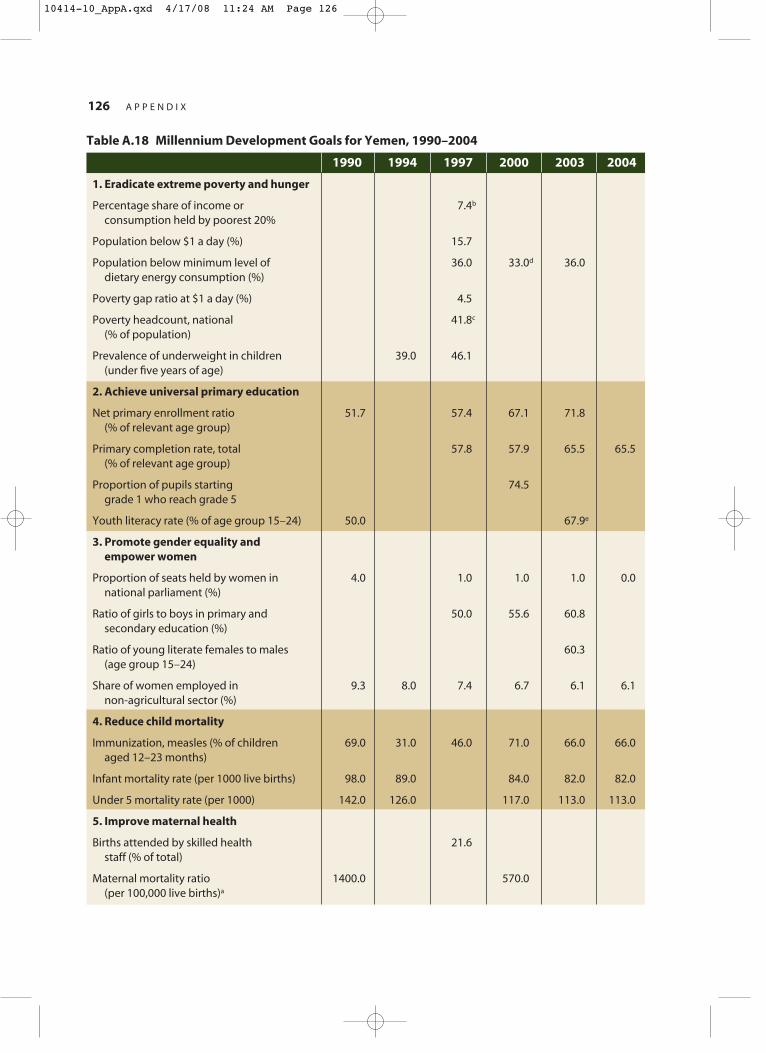

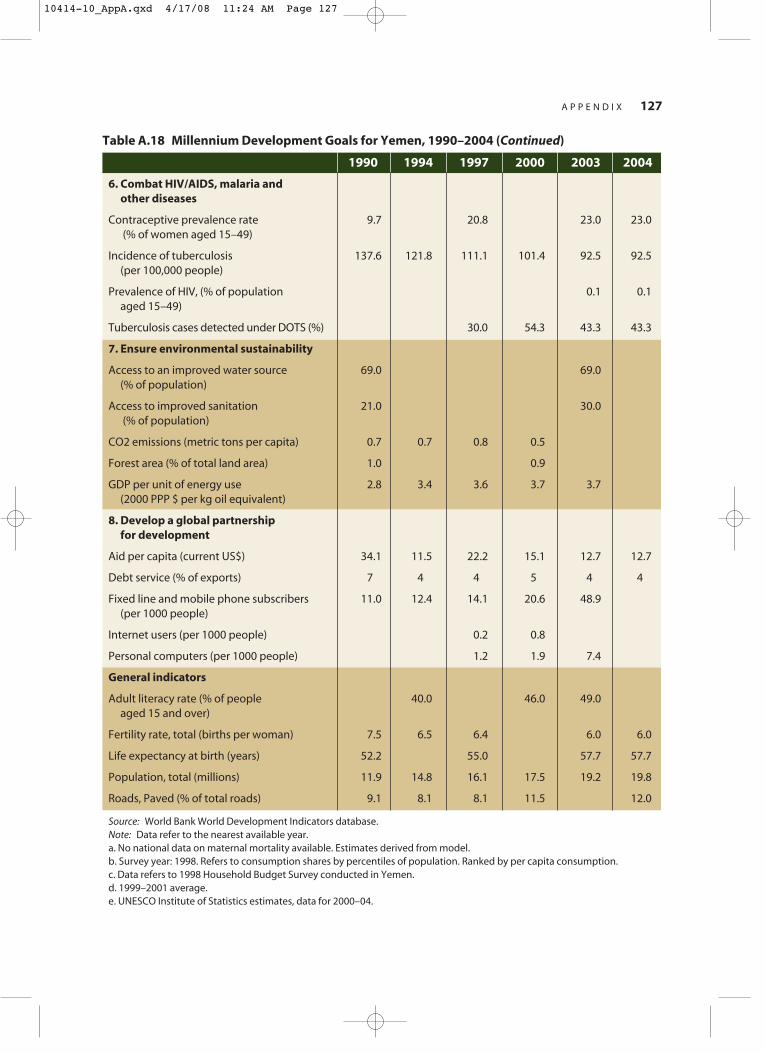

Yemen is unlikely to meet most of the Millennium Development Goals, except foruniversal primary education and child mortality (see Appendix Table A.18).

� Universal primary education is the goal most likely to be met in Yemen. Despitepoverty and rapid growth of the school age population, Yemen has been able to

Y E M E N T O D A Y 7

10414-01_Ch01.qxd 4/17/08 11:15 AM Page 7

increase gross enrollment rates from 73 percent to 83 percent over 1998–2002.However, the government and donors must make a strong and sustained com-mitment to mobilize resources and implement the policy and institutionalreforms needed, since global experience demonstrates that the last 5 percent isthe toughest to achieve.

� Reducing the mortality rate of children less than five years old (per 1000 live births)by two-thirds may be achievable, if neonatal and antenatal health care can beimproved. The mortality rate for this group went down from 142 in 1990 toabout 113 in 2003.

Nonetheless, targets on alleviating poverty, reducing gender inequality, safe-guarding maternal health, combating HIV/AIDS, and increasing access to environ-mental resources all seem much more elusive. At the current rate of progress, the goalof halving the percentage of people under the national poverty line is unlikely to bemet, but under optimistic scenarios the absolute poor (those living below the $1poverty line) could potentially be halved with sustained effort. Closing the persis-tent gender gap in secondary school enrollment is also unlikely, because of the cul-tural discrimination against girls and the high dropout rate for girls, linked largelywith early marriage. Early marriage and pregnancy, combined with the widespreadmalnutrition and anemia, the poor quality of health services, and the low levels ofhealth coverage, also challenge Yemen’s goal for reducing maternal mortality.Increasing the proportion of pregnancies covered by the health care system wouldgo a long way in achieving this goal. Limited financial and other resources will alsorestrict Yemen’s ability to achieve its goals of combating the spread of HIV/AIDS,malaria, tuberculosis, and other infectious diseases or halving the proportion ofpeople without sustainable access to safe drinking water. The water problem maybe addressed in urban areas with proper utility management and pricing, but ruralareas are threatened by overall depletion of aquifers due to unrestricted agriculturaluse of water.

The UN Millennium Project report estimated a total investment requirement ofUS$57.5 billion over 10 years to reach MDG goals. As recognized in the report, thesimple addition of costs of reaching individual goals is biased upwards because ofinterlinkages among targets. On an annual basis, the investment needs to meetMDGs amount to an astounding 38 percent of GDP, compared to the total expen-diture of central government of 40 percent of GDP in 2005. There is no definitefinancing plan to meet the investment requirements of MDGs for Yemen. Even if thedonors were willing to lend support for such massive investment efforts, it is not cer-tain Yemen will have the capacity to absorb this scale of investment in the near-term.

Implementation of the Poverty Reduction Strategy

The implementation of Yemen’s poverty reduction strategy remains tardy. Progressmade under Yemen’s first poverty reduction strategy during 2003 and 2004 fellshort of the targets in many respects. The main goal of reducing the percentage of

8 Y E M E N : D E V E L O P M E N T P O L I C Y R E V I E W

10414-01_Ch01.qxd 4/17/08 11:15 AM Page 8

the poor by 13 percent is not likely to have been met. It is most likely that povertyexperienced little change in the first two years of the poverty reduction strategy.Missed targets in the period include GDP growth, mortality indicators for infants,children and mothers, and access to water, roads, and electricity. However, therehave been some successes in meeting targets for basic education enrollment (forboth boys and girls), road rehabilitation and maintenance, power plant operationand expanded coverage for social protection (see Appendix Table A.19).

Stalled reforms and weak governance have hampered Yemen’s realization of itspoverty goals. The government attributes the weak performance to dampenedinvestor confidence and interest in the region following the Iraq War and a slow-down in economic reforms following the elections of April 2003. Insufficient actionto reform public sector management and governance may also have hampered theinvestment climate in Yemen. The unprecedented oil price increases since 2003 hadthe potential to offset any negative regional or internal security shocks. The gov-ernment opted, however, to delay key reform programs until mid-2005 and to con-tinue to subsidize domestic fuel at prices well below international levels. Thesemeasures contributed to a misallocation of scarce government resources, providedonly marginal benefits to Yemen’s poor, and added to the problems of governanceand corruption. Further delays in the adoption of an amended general sales tax—now scheduled for implementation on January 1, 2007—was also a setback, giventhe critical need for Yemen to shift to non-oil sources of revenue. The recent deci-sion to increase public wages and salaries also poses serious problems unless othermajor challenges in civil service wage structure of high compression ratio and exces-sive labor force are also not addressed in a timely manner.

Priorities for Reform

As Yemen strives to meet the challenges that lie ahead—including depleting oil rev-enues, weak governance, severe water stress, and burgeoning population growth—it must focus on easing the constraints that are most likely to bind its social andeconomic development. The reform agenda proposed here identifies those con-straints that pose immediate problems and longer-term risks, and it recommendsspecific remedies.

Growth diagnostics analysis is used here to identify the “binding” near-termconstraints. Low returns to investment are a constraint, as they negatively affect allpotential investors, whether foreign or domestic, and prevent private investmentfrom functioning as a driver of growth. Low returns to investment also lead to lowproductivity. Looking closer at the causes of low return to investment, three mainissues are identified as “binding” in the short term: weak property rights, inequitiesin the judicial system, and inadequate infrastructure for energy resources. These fac-tors have been confirmed by surveys and focus groups of local business owners. TheYemen Investment Climate Assessment (World Bank 2005a) also confirms thesefindings, while raising several additional concerns: potentially unstable macro-economic conditions and weaknesses in the tax and regulatory regimes. In fact,

Y E M E N T O D A Y 9

10414-01_Ch01.qxd 4/17/08 11:15 AM Page 9

more Yemeni firms reported feeling constrained by the investment climate than didfirms in most of the other Middle Eastern countries that participated in the assess-ment. Within the list of firms’ concerns, governance, regulations, unfair competition,and infrastructure (power and land) issues emerged as top constraints.20 Womenentrepreneurs are more constrained by some aspects of the Yemeni investmentclimate. Cultural norms and restrictions constrain women’s ability to participateas workers and entrepreneurs. In addition, lower rates of education and literacy,lack of critical mass, supportive institutions and services (including childcare andtransport) and entrepreneurial networks particularly constrain women.

The growth diagnostics and investment climate assessment have helped toidentify six priorities for reform that could secure better returns to private sectorinvestment:

� Strengthening governance and economic stability. Given the fragile or nearly fragilestate of Yemen’s political institutions, a study of the political economy of reformand institutions in Yemen is the focus of Chapter 2.

� Maintaining fiscal sustainability. Because the rapid depletion of oil reserves is goingto pose a daunting fiscal challenge, concerns about fiscal sustainability underpinthe pervasive concerns about Yemen’s macroeconomic stability and investmentclimate. Chapter 3 analyzes the prospects for better fiscal management to replacelost oil revenues.

� Improving the investment climate. Strengthening the governance environment forprivate sector development is addressed in Chapter 4, with emphasis on enforc-ing property rights, reforming the judicial system, and eliminating corruption.

� Managing energy resources. Reforms to better manage Yemen’s energy sectors,including oil, gas, and power, and to build more efficient downstream infra-structure is discussed in Chapter 5.

� Managing water resources. As Yemen faces a deepening water crisis because of dis-tortions in the pricing of water, the risk of failing to meet the minimum needs forpotable water could seriously compromise government’s goals, as discussed inChapter 6.

� Slowing population growth. Containing demand on social goods by slowing thegrowth of population, as discussed in Chapter 7, would also prove useful tostretch the rapidly dwindling resources of oil and water and help in the long runto promote growth by improving potential for savings by reducing the depen-dency ratio.

10 Y E M E N : D E V E L O P M E N T P O L I C Y R E V I E W

10414-01_Ch01.qxd 4/17/08 11:15 AM Page 10

Yemen’s recent history of weak governance, widespread corruption, and height-ened risk of internal conflicts has already prompted many careful analyses of

its political culture and economic policies. The reformers in Yemen have a goodunderstanding of what is needed. The political will for change is often weak, like inother developing countries, and the implementation of reforms often flounders. Thischapter examines Yemen’s political culture and recent reform experience to assess theprospects for broadly strengthening Yemen’s governance institutions and macro-economic stability. It looks in detail at reforms in Yemen since the mid-1990s to compare the period of strong reform in 1995–98 with the sluggish period thatfollowed, presenting an opportunity to observe how changes in institutional qualityaffect the implementation of economic policies.

The Quality of Governance

Public sector governance—the nexus of relationships among citizens, politicians,and the administrative bureaucracy of government—is perhaps the most evident andimportant barrier to economic development in Yemen today.

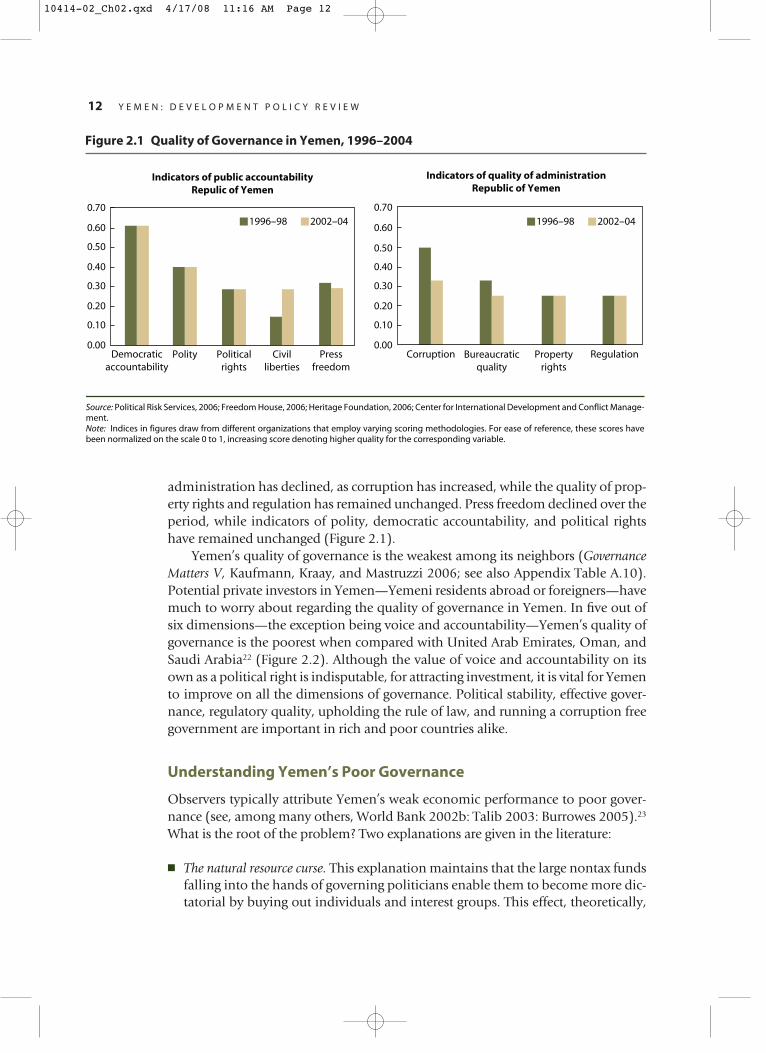

The poor functioning of market-supporting institutions blocks the entry ofmany new Yemeni businesses and constrains growth of established firms (WorldBank 2002). Using two alternative measures of governance quality, both of themfrom the World Bank, the conclusions remain the same. In most dimensions, thequality of governance worsened until 2004. By Kaufman et al measures of gover-nance (accountability, political instability and violence, government effectiveness,regulatory burden, rule of law, and control of corruption), the quality of governancein Yemen has mostly deteriorated since the mid-1990s to 2004, before improving in2005, as shown in Figure 1.1B (Chapter 1). The quality of governance has begunimproving in 2005 in two dimensions—control of corruption and regulatory qual-ity. By the alternative measures used by the World Bank (2003)21, which has dif-ferent dimensions of governance grouped under Public Accountability andBureaucratic quality, conclusions remain the same. The data from 1996 to 2004,spanning both active and sluggish reform periods, reveal that the quality of

11

Yemen TomorrowProspects for Good Governance and Economic Growth

2

10414-02_Ch02.qxd 4/17/08 11:16 AM Page 11

12 Y E M E N : D E V E L O P M E N T P O L I C Y R E V I E W

Indicators of public accountabilityRepulic of Yemen

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

Democraticaccountability

Polity Civilliberties

1996–98 2002–04 1996–98 2002–040.70

Indicators of quality of administrationRepublic of Yemen

Corruption Propertyrights

Regulation

Source: Political Risk Services, 2006; Freedom House, 2006; Heritage Foundation, 2006; Center for International Development and Conflict Manage-ment. Note: Indices in figures draw from different organizations that employ varying scoring methodologies. For ease of reference, these scores have been normalized on the scale 0 to 1, increasing score denoting higher quality for the corresponding variable.

Politicalrights

Pressfreedom

Bureaucraticquality

Figure 2.1 Quality of Governance in Yemen, 1996–2004

administration has declined, as corruption has increased, while the quality of prop-erty rights and regulation has remained unchanged. Press freedom declined over theperiod, while indicators of polity, democratic accountability, and political rightshave remained unchanged (Figure 2.1).

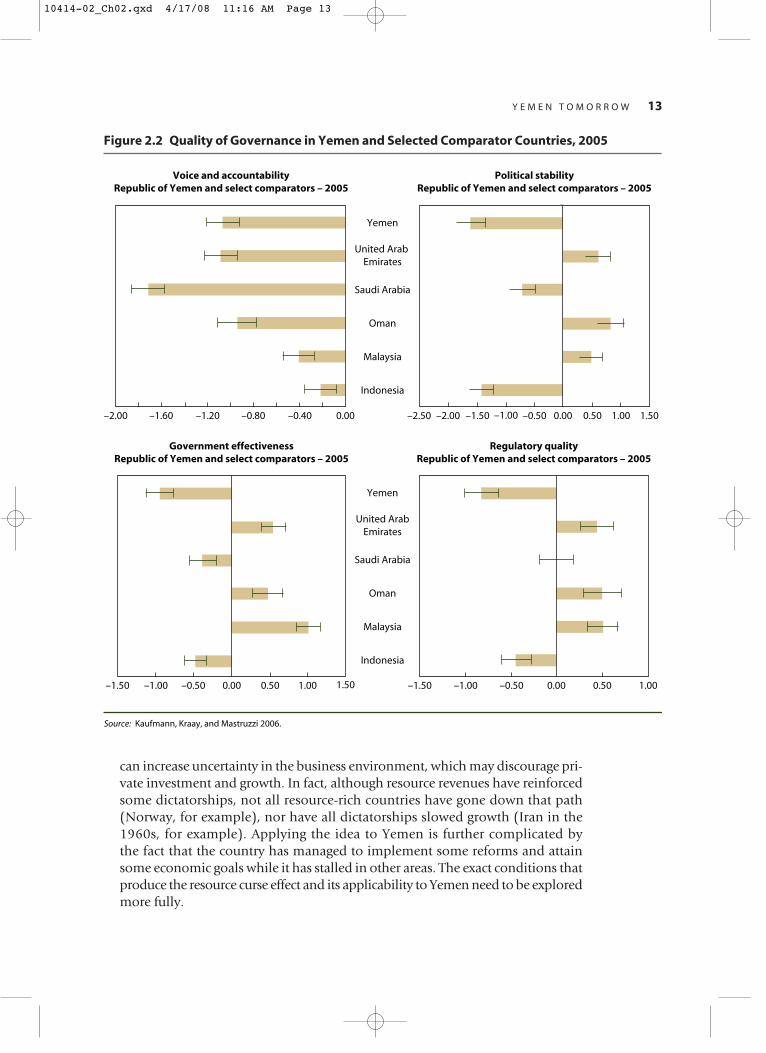

Yemen’s quality of governance is the weakest among its neighbors (GovernanceMatters V, Kaufmann, Kraay, and Mastruzzi 2006; see also Appendix Table A.10).Potential private investors in Yemen—Yemeni residents abroad or foreigners—havemuch to worry about regarding the quality of governance in Yemen. In five out ofsix dimensions—the exception being voice and accountability—Yemen’s quality ofgovernance is the poorest when compared with United Arab Emirates, Oman, andSaudi Arabia22 (Figure 2.2). Although the value of voice and accountability on itsown as a political right is indisputable, for attracting investment, it is vital for Yemento improve on all the dimensions of governance. Political stability, effective gover-nance, regulatory quality, upholding the rule of law, and running a corruption freegovernment are important in rich and poor countries alike.

Understanding Yemen’s Poor Governance

Observers typically attribute Yemen’s weak economic performance to poor gover-nance (see, among many others, World Bank 2002b: Talib 2003: Burrowes 2005).23

What is the root of the problem? Two explanations are given in the literature: