yachting in malta: a fiscal perspective pierre portelli 11 june 2015

TRANSCRIPT

Yachting in Malta:

A Fiscal Perspective

Pierre Portelli

11 June 2015

© 2015 KPMG, a Maltese civil partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The information contained in this slide pack is generic and brief and therefore should not be relied upon for any factual or planned transaction or event. Specific advice should be separately sought for each such transaction or event.

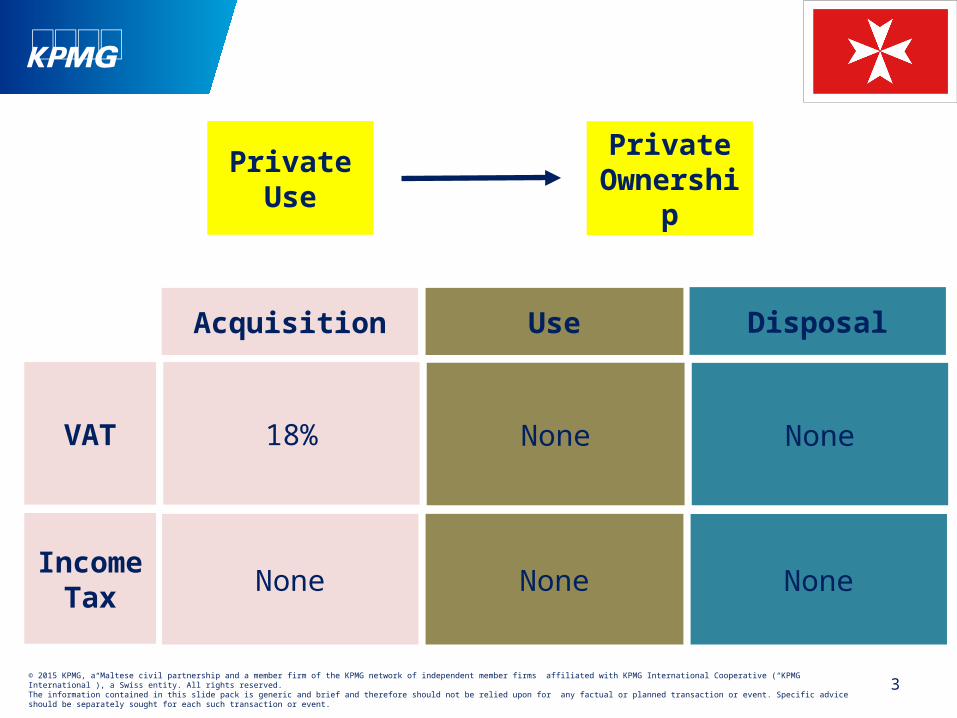

Purpose of Yacht Acquisition

2

Private Use PrivateOwnership

Lease

Commercial Operation

YachtAcquisition

© 2015 KPMG, a Maltese civil partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The information contained in this slide pack is generic and brief and therefore should not be relied upon for any factual or planned transaction or event. Specific advice should be separately sought for each such transaction or event.

3

Acquisition Use Disposal

Income Tax None None None

VAT 18% None None

Private Use PrivateOwnership

© 2015 KPMG, a Maltese civil partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The information contained in this slide pack is generic and brief and therefore should not be relied upon for any factual or planned transaction or event. Specific advice should be separately sought for each such transaction or event.

4

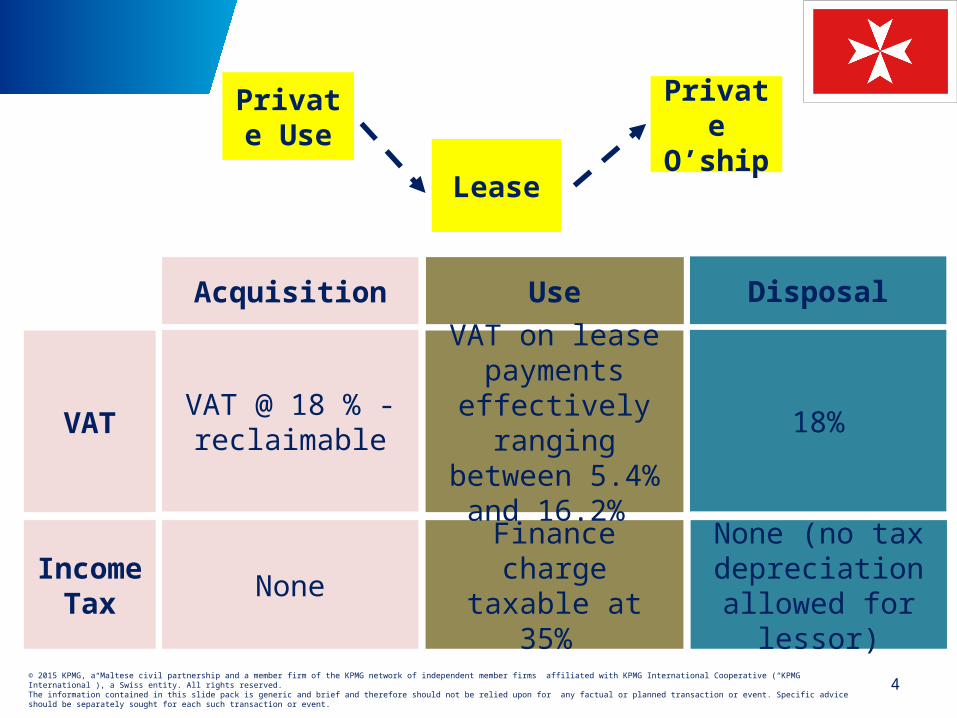

Acquisition Use Disposal

Income Tax None Finance charge

taxable at 35%

None (no tax depreciation

allowed for lessor)

VATVAT @ 18 % -reclaimable

VAT on lease payments

effectively ranging between 5.4% and

16.2%

18%

Private Use

PrivateO’ship

Lease

© 2015 KPMG, a Maltese civil partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The information contained in this slide pack is generic and brief and therefore should not be relied upon for any factual or planned transaction or event. Specific advice should be separately sought for each such transaction or event.

Yacht Leasing: Effective Rates

5

The effective VAT rates applicable to the VAT leasing structure are as follows:

© 2015 KPMG, a Maltese civil partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The information contained in this slide pack is generic and brief and therefore should not be relied upon for any factual or planned transaction or event. Specific advice should be separately sought for each such transaction or event.

Yacht Leasing - Conditions

6

• Lessor must be a Maltese company - lessee can be any Maltese or foreign person (natural or legal)

• Lease payments must be every month for a period of not exceeding 36 months

• Prior approval of the lease needs to be sought from the VAT Department

• VAT Department expects a profit on the lease

• First lease payment at least 40% of the cost of yacht.

© 2015 KPMG, a Maltese civil partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The information contained in this slide pack is generic and brief and therefore should not be relied upon for any factual or planned transaction or event. Specific advice should be separately sought for each such transaction or event.

Yacht Leasing – Income tax Guidelines

7

• The lessor charged to tax only on the annual finance charge

• The lessee is allowed a deduction in respect of the finance charge, repairs and maintenance and insurance

• Only the lessee may claim capital allowances

• Where the lessee exercises option to purchase the yacht, the purchase price shall be considered to be of a capital nature

© 2015 KPMG, a Maltese civil partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The information contained in this slide pack is generic and brief and therefore should not be relied upon for any factual or planned transaction or event. Specific advice should be separately sought for each such transaction or event.

Yacht Leasing – An Example

8

Cost of 30 metre yacht : € 10,000,000

Total lease payments ( to cover costs and lease profit): € 10,100,000

VAT on lease payments: 18% of 30% of total lease payments: € 545,400

VAT on disposal of yacht: 18% of 1% of € 10,000,000: € 18,000

Income tax on income: 35% of € 15,000: € 5,250

Total Taxes as a percentage of cost of yacht: 5.7 %

Tax payable if yacht leasing structure not applied: 18% x € 10,000,000: € 1,800,000

Tax saved with yacht leasing structure: € 1,231,600

Total Taxes:€ 568,400

© 2015 KPMG, a Maltese civil partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The information contained in this slide pack is generic and brief and therefore should not be relied upon for any factual or planned transaction or event. Specific advice should be separately sought for each such transaction or event.

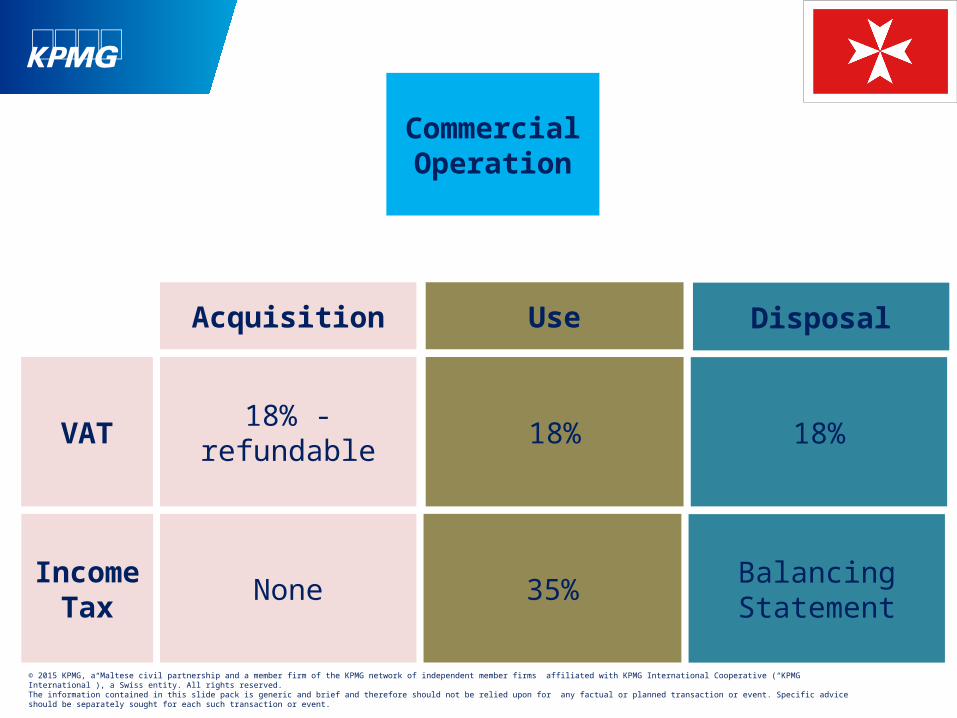

Acquisition Use Disposal

Income Tax None 35% Balancing

Statement

VAT 18% - refundable 18% 18%

Commercial Operation

The information contained in this slide pack is generic and brief and therefore should not be relied upon for any factual or planned transaction or event. Specific advice should be separately sought for each such transaction or event.

© 2015 KPMG, a Maltese civil partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The KPMG name, logo and ‘cutting through complexity’ are registered trademarks or trademarks of KPMG International Cooperative (KPMG International).

Pierre PortelliPartner

[email protected]: +356 2563 1132

Thank You