xmi 2016 annual report - xcellon capitalall information contained in this publication is copyrighted...

TRANSCRIPT

January 2017

Xcellon Market Intelligence (XMI)Xcellon Capital Advisors Ltd.

2016Annual Economic Report

2016 Annual Economic Report © All Rights Reserved XCELLON MARKET INTELLIGENCE (XMI)

DISCLAIMERAll information contained in this publication has been researched and compiled from sources believed to be accurate and reliable at the time of publishing.

However, in view of the natural scope for human and/or mechanical error, either at source or during production, Xcellon Capital Advisors accepts no liability whatsoever for any loss or damage resulting from errors, inaccuracies or omissions affecting any part of the publication. All information is provided without warranty, and Xcellon Capital Advisors makes no representation of warranty of any kind as to the accuracy or completeness of any information hereto contained.

All Rights Reserved. © 2017 Xcellon Capital Advisors Ltd.All information contained in this publication is copyrighted in the name Xcellon Capital Advisors, and as such no part of this publication may be reproduced, repackaged, redistributed, resold in whole or in any part, or used in any form or by any means graphic, electronic or mechanical, including photocopying, recording, taping, or by information storage or retrieval, or by any other means, without the express written consent of the publisher.

Table of Contents

NIGERIA IN 2017: Separating Expectations from Realities ................................................. Page 3

Global Market Update .............................................................................................................. Page 6

Oil Market Update .......................................................................................................................Page 14

Nigeria Economic Update...........................................................................................................Page 15

Nigeria Economic Outlook..........................................................................................................Page 18

Global Economic Outlook.......................................................................................................... Page 21

02

NIGERIA IN 2017: Separating Expectations from Realities

The year 2016 went down as one of the toughest and most challenging years for most Nigerians. The

challenges experienced by most citizens and business operators in the country in 2016 may not be quickly

forgotten. Their effects may even linger for the foreseeable future. This is due to the far-reaching

implications of some underlying factors in the macro environment such as the devaluation of the naira, high

inflation, amongst others. A negative fourth quarter 2016 GDP growth figure would mean that the year recorded one of the worse GDP

slumps in 12 years. Data from the National Bureau of Statistics (NBS) show a consistent decline in the

country's aggregate output in the first three quarters (Q1 = -0.36%; Q2 = -2.06%; Q3 = -2.24) of the year,

with the country officially entering a recession in the second quarter of the year. The decline recorded in

aggregate output was in stark contrast with a prolonged 5%-7% GDP growth rate recorded annually

between 2005 and 2014.

During the presentation of the 2017 budget to the national assembly, President Buhari himself

characterized the current situation as the worst economic crisis in the history of Nigeria. Who will argue with

that? If 2016 was dismal in terms of economic performance, what can we expect in 2017? How realistic are

our expectations that 2017 will be better? Let's look at some pointers and try to decipher these questions.

Outlook for 2017

True, the shock waves arising from the crude oil price drop and the slide in domestic output were the major

factors responsible for the recession. Nevertheless, the weak policy response from the government made

macroeconomic conditions worse. But there seems to be some silver linings. Based on a projection by the

International Monetary Fund (IMF), the current negative trend is expected to reverse in 2017 as Nigeria's

economy is expected to grow at 0.6% compared to an estimated -1.7% GDP growth rate in 2016.

Also, the International Energy Agency (IEA) has said that the glut in the international oil market will gradually

begin to recede. This will lead to price recovery that is projected to reach $60 per barrel of crude oil. Prices

have edged up to $56-$57 per barrel. This price level is supported by the production cuts agreement

reached by the Organisation of the Petroleum Exporting Countries (OPEC) – an agreement that has been

long overdue but that is also contingent on some non-OPEC members agreeing to production cuts.

On the home front, what factors can we expect to influence economic growth and impact lives in 2017?

Temper your Expectations

It is quite normal that following a difficult 2016, most people would hope for a healthy rebound as fast as

possible. Unfortunately, we might have to wait for much longer. Whereas Nigeria is expected to grow in

2017, the pace of growth will only be marginal. Only in 2018/2019 can we realistically attain positive

economic growth rates that would get close to what the country used to have in the 10 years before 2015.

The reason we need to temper our expectations is we have to take into account lost productivity and

foregone investment opportunities. Sectors of Nigeria's economy such as agriculture, mining,

IT/telecomnication, financial services, news media and music/movie industries would experience

accelerated recovery than say construction, housing, manufacturing, transportation/logistics, oil and gas,

power, etc.

03

2016 Annual Economic Report © All Rights Reserved XCELLON MARKET INTELLIGENCE (XMI)

NIGERIA IN 2017: Separating Expectations from Realities

A persistent high interest rates regime, coupled with high exchange rate plus forex scarcity, could conspire

to throw a monkey wrench into any potential rapid rebound. By the time we enter into the second quarter of

2017 and beyond, it is possible that conditions would normalize. But this scenario would depend on whether

the Central Bank of Nigeria (CBN) would lower its Monetary Policy Rate (MPR) from the current high of 14%

and if inflation reverses course from the current uptrend.

Spending Nigeria out of Recession

The caption of the 2017 budget proposal that was submitted to the National Assembly in December was:

“Budget of Recovery and Growth.” An important development was that the budget was submitted about one

week earlier (December 14, 2016) compared to the date the 2016 Appropriation Bill was submitted

(December 22, 2015). The size of the budget at N7.2 trillion is also quite encouraging. Over 30% is

earmarked for capital expenditures, which is a shift from previous budgets. The Ministry of Power, Works

and Housing is getting N527 billion, and Transportation N262 billion. The impetus does exist for massive

infrastructure spending that could catalyze growth and job creation.

The proposed benchmark oil price of $42.5 per barrel and target output level of 2.2 million barrels per day is

very critical to achieving the desired results. The key question is: can it get worse than what we witnessed in

2016? Radical reforms like the repeal of the outdated Land Use Decree, enactment of National Free

Compulsory Basic Education Law, plus passage of the long-pending Petroleum Industry Bill (PIB) will be

key to lasting legacies of the Buhari administration. If he can pull these off this year, then 2017 should be a

year to set the foundation for strong future economic growth.

Easing Pressure on Naira

More forex inflow from crude oil exports would lead to a much desired breather for the local currency in the

short run. To also reduce pressure on the naira, some measure of progress has to be achieved in

agricultural output, especially rice production. It should be noted that rice importation is amongst the top five

activities that gulp the country's forex. As some states begin to invest in rice production and milling, it is a

matter of time before Nigeria becomes self-sufficient in the grain and even begin to export same.

Processed agro products and other intermediary materials are increasingly being sourced locally. If all this

04

2016 Annual Economic Report © All Rights Reserved XCELLON MARKET INTELLIGENCE (XMI)

Breakdown

Amount (N ‘trillion)

Capital Expenditure 2.24

Non-Debt Recurrent Expenditure 2.98

Debt Service

1.66

Statutory Transfer

0.42

Total

7.30

Source: Budget Office

NIGERIA IN 2017: Separating Expectations from Realities

can be achieved to scale, the demand for forex would reduce. But it is a pipedream to expect the exchange

rate for the naira to recover to pre-2016 levels. Exchange rate stability and predictability as well as forex

availability will be major investment drivers in 2017.

Social Security Services and Quality of Life not Looking Good

I can boldly say this because it will take many years of sustained investments in social and economic

infrastructure to make a dent on poverty, joblessness and overall well-being in Nigeria. The gap remains

quite deep due to years of neglect in the education, healthcare, and power sectors. Not even with Nigeria

becoming the largest economy in Africa or recording consistent 5-7% GDP growth rate annually for almost a

decade did we see a steep decline in poverty and unemployment. The situation has worsened owing to the

precipitous devaluation of the naira, erosion of purchasing power and degrading asset value. Allocation of

more resources to the education sector (N448 billion – recurrent and capital) and healthcare sector (N303.9

billion – recurrent and capital) in the 2017 budget signals some effort to address poverty and inequality;

nevertheless, it will take much more than one year's budget to achieve positive outcomes.

Internal crises in the North-East and the Niger Delta regions are all outcomes of prolonged neglect by

successive governments. The security risks in these regions pose an existential threat to the country. It is

worth acknowledging that the singular greatest investment with the highest multiplier effect on social

progress is education

Political Stability and Clear Regulatory Environment translate to Greater Economic Prosperity

This is a simple logic that has been proven in several countries, including in Africa. The outcome of elections

and peaceful transfer of power, coupled with clear and predictable policy/regulatory environments pretty

much can determine how well a country performs. Nigeria avoided the crystallization of political risk in 2015

as it similarly did since 1999. However, the policy terrain since the emergence of the Buhari administration

has left much to be desired. It is imperative for 2017 to be different. Given the flurry of criticism the administration has faced in this regard, it is hoped that the economic team

has learned some vital lessons. The investment community won't condone the policy summersaults and

misdirected efforts of 2016 without voting with its wallet. In such circumstances, no amount of high oil price

will save Nigeria from a continuation of the 2016 debacle.

With the right mix of policies and programmes as enunciated in the government's economic recovery plan, it

is hoped that 2017 would be a banner year in the annals of Nigeria. Lessons learnt in 2015/2016 should be

guideposts for moving forward. But if we fail to plan and we cannot save for the rainy day, we would stay

longer in a slump that is avoidable and deny millions of Nigerians the opportunity to move closer to finding a

decent job and coming out of poverty.

Thank you,

Executive Chairman of Xcellon Capital Advisors Ltd

05

2016 Annual Economic Report © All Rights Reserved XCELLON MARKET INTELLIGENCE (XMI)

Global Market Update

The world economy experience another lackluster year in 2016 as regional growth imbalances remained

and political events in developed economies stirred additional risks. The culprits include structural

adjustments in many countries, efforts to reduce overcapacity, recurring natural disasters, geopolitical

events - such as Brexit, a coup d'état in Turkey and the ongoing civil war in Syria, among others - and

heightened uncertainty related to the policy changes in the U.S. and a number of other major economies.

The United States

The United States economic data in 2016 was broadly positive. Thanks to steady gains in the labor market,

including a post-recession drop in the unemployment rate, personal disposable income and household

spending have remained fairly solid throughout 2016 - boosted by buoyant consumer confidence, which

jumped to a nine-year high in

November 2016. In terms of

economic growth, after an extended

soft growth patch characterized by

five quarters of inventory correction,

GDP growth in Q3, at 3.2%, was the

fastest in two years. Meanwhile,

positive prospects for oil prices and

somewha t improv ing g loba l

c o n d i t i o n s s u p p o r t e d U . S .

manufacturing activity, with the ISM

index rising for a fourth consecutive

month to 54.7 in December and reaching the highest reading since December 2014.

As widely expected, the Federal Reserve's Open Market Committee (FOMC) announced its decision to

raise the target of the Federal Funds

rate from a range of between 0.25%

and 0.50% to between 0.50% and

0.75% at its final monetary policy

meet ing of the year held on

December 13 -14, 2016. The

pronouncement came a year after

the first U.S. interest rate hike since

the global financial crisis. The U.S.

monetary authority indicated that the

increase was warranted due to

“realized and expected labor market

conditions and inflation”. Also, the

committee signaled that the stance

of monetary policy remains “accommodative”, which would help achieve “some further strengthening” in

the labor market.

06

2016 Annual Economic Report © All Rights Reserved XCELLON MARKET INTELLIGENCE (XMI)

In the summary of economic its projections, the U.S. Central Bank made relatively few changes to its

economic forecasts. However, it upgraded its projection for the Funds rate. The median projection for the

monetary policy rate showed three rate

increases in 2017- up from two in its

September 2016 forecasts - and no

changes in the number of hikes in 2018

and 2019. Longer-term projections for

the interest rate were also raised, with a

median projection increasing to 3.00%

from 2.875% previously.

The decision to increase interest rates in

December came before Donald Trump

takes office in January and as the new

administration contemplates tax cuts

that could boost economic activity and inflation. In a press conference after the rate announcement, Janet

Yellen mentioned that monetary policy makers “are operating under a cloud of uncertainty at the moment”

and added that, “changes in fiscal policy or other economic policies could potentially affect the economic

outlook.” She finalized by saying, “it is far too early to know how these policies will unfold. Moreover,

changes in fiscal policy are only one of the many factors that can influence the outlook in the appropriate

course of monetary policy.”

Trump, the new elected U.S. president pledged as much as $1 trillion in infrastructure investment and cuts

to corporate and individual income taxes. But the plans have not been thoroughly detailed; and whether it

will actually be backed by Congress is even less clear. The Federal Open Market Committee cited “realized

and expected labor market conditions and inflation” in increasing its benchmark rate a quarter percentage

point, according to a statement following a two-day meeting in Washington. New projections show central

bankers expect three quarter-point rate increases in 2017, up from the two seen in the previous forecasts in

September, based on median estimates.

Euro-zone

The economic situation in the Euro-zone continues to improve slightly. Germany and to some extent,

France remain the countries that are

mostly supporting the recovery trend.

But Spain and some per ipheral

economies are also enjoying a rebound

from the low levels seen in past years.

Positively, Q3, 2016 GDP growth was

better than expected at 0.4% quater-on-

quarter (q/q) seasonally adjusted growth

rate. This was up from Q3, 2016 when

growth stood at 0.3% q/q and only

slightly below the 0.5% q/q reached in

Q1,2016.

Global Market Update

07

2016 Annual Economic Report © All Rights Reserved XCELLON MARKET INTELLIGENCE (XMI)

The ECB decided to reduce its monetary stimulus, while clearly underscoring that it will continue

quantitative easing, at least for

the t ime be ing . The bank

confirmed that it would buy €80

billion in bonds per month until

March 2017, but added it would

prolong its asset purchases until

the end of 2017 at the lower rate

of €60 billion. Also, banking

sector-related weakness seems

to have abated to some extent,

while in Italy concerns about the

sector have risen again, after the

government's defeat in the most recent referendum about proposed constitutional changes, which led to the

resignation of the Prime Minister.

In the Eurozone, the latest industrial production figures were volatile to some extent, but have again recently

offered confirmation that the business environment has improved. Available data showed that industrial

sector in the region improved in November, growing at the fastest pace seen in 3 months. Industrial

production increased a seasonally-adjusted 1.5% from the previous month, above October's 0.1%

increase. November's acceleration reflected rebounds in the production of non-durable consumer goods

and intermediate goods. In addition, energy production ticked up from the previous month. However, output

of capital and durable consumer goods deteriorated. On an annual basis, industrial production rose 3.2% in

November (October: +0.8% year-on-year). Among the Euro area economies for which data are available,

the largest growth rates in production were recorded in Ireland (+16.3% m-o-m), the Netherlands (+3.5% m-

o-m) and Latvia (+2.8% m-o-m). On the flipside, the largest drops were recorded in Greece (-0.9% m-o-m)

and Portugal (-0.9% m-o-m). Regarding the region's largest economies, output grew across the board as

expansions were seen in France (+2.2% m-o-m), Germany (+0.3% m-o-m), Italy (+0.7% m-o-m) and Spain

(+1.7% m-o-m).

United Kingdom

The United Kingdom's economy continues to hold up well despite Brexit vote. A complete set of data

confirmed that GDP growth had decelerated

marginally in the third quarter, but that growth

remains robust compared to historical levels.

The economy was supported by a rebound in

exports while domestic demand disappointed.

Economic activity performed well as the

smooth political transition following the

resignation of former Prime Minister David

Cameron and the accommodative stimulus of

the Central Bank are keeping consumer and

business confidence at reasonable levels.

Global Market Update

08

2016 Annual Economic Report © All Rights Reserved XCELLON MARKET INTELLIGENCE (XMI)

Available data revealed the British economy advanced 0.6% percent on quarter in the three months to

September of 2016, the same as in the previous period and better than the second estimate of 0.5%

expansion. Household expenditure

continued to grow while fixed

investment rose at a slower pace

a n d n e t e x t e r n a l d e m a n d

contributed negatively. Compared

with the same period of 2015, the

economy advanced 2.2% following

a d o w n w a r d l y r e v i s e d 2 %

expansion in the precedent quarter.

However, the depreciation of the

pound , r i s i ng i n f l a t i on and

insufficient wage hikes risk eroded

household consumption. In the next

five years, the government projects

higher borrowing and a slower fiscal consolidation compared to the previous budget.

At its meeting on December 15, the Monetary Policy Committee (MPC) of the Bank of England (BoE) voted

to keep the Bank rate unchanged at 0.25% and to keep the total stock of purchased assets at GBP435

billion - financed by the issuance of Central Bank reserves. Both decisions were taken unanimously. The

MPC commented that data released since its last meeting in November point to moderate growth of the

economy, mainly underpinned by solid consumption growth. However, economic activity is expected to

weaken going forward. In November, the BoE set out its inflation and GDP growth projections for the short

and medium term. The Bank expects the economy to grow at a moderate pace in 2016 and decelerate in

2017. This is due to the high likelihood of a slower increase in real household income, which would in turn

negatively affect household spending. The Bank commented that “the timing and extent of this slowing will

depend crucially on the evolution of wages and how resilient household spending is to the pressure on real

incomes from higher inflation.” Moreover, there are escalating concerns that UK-based businesses' access

to EU markets will be reduced significantly, thus harming the economy.

While the UK government has gained some clarity lately about the potential timeline of the Brexit

negotiations, the procedure, content and certainly the form of the outcome remain widely unclear. This

uncertainty will remain an issue for the coming months and is expected to negatively impact the economic

development of the UK. Importantly, parliament has recently voted for the Brexit and endorsed the March

timeline to start negotiations, hence triggering Article 50. There is still the ruling of the Supreme Court, which

has to decide on the formal involvement of parliament in the negotiations. This is crucial, as the most recent

vote by the House of Commons was a non-binding motion by the Labour Party. It is expected that the

Supreme Court will finalise its ruling by January. If the government appeal is rejected, the Prime Minister will

likely present a short bill to approve Article 50, which will have to pass through the House of Commons and

the House of Lords with more room for debate. This will likely only be passed with some delays and

amendments, and while it seems that the March deadline may be met, such an outcome could create further

uncertainty. Most importantly, parliament will likely demand more transparency about the negotiation

strategy, an element that the government does not want to provide, given its obvious sensitivity. Finally, the

procedures for Scotland remain unclear.

Global Market Update

09

2016 Annual Economic Report © All Rights Reserved XCELLON MARKET INTELLIGENCE (XMI)

Canada

The economy of Canada continues to improve slightly, along with a better situation in the US, its most

important trading partner, as well as improvements in the oil sector. After Q3, 2016, GDP growth was

announced at 3.5% q-o-q Seasonally Adjusted Annual Rate (SAAR), while industrial production continued

its growth trend. In October 2016, it rose by 1.9% y-o-y, after a rise of 3.3% in September. Output from the

mining, oil and gas sector remained an important driver, with overall sector growth of 3.2% y-o-y. Also, the

PMI for manufacturing improved and rose to 51.9 in December, compared to 51.5 in November.

JAPAN

Available data revealed that Japan economy grew at a faster rate in the third quarter of 2016 relative to the

Q1 and Q2 of the year, according to revised data released on 8 December. On an annual basis, economic

activity rose 1.1% in Q3 - an acceleration over Q2's 0.9% and Q1's 0.4% rise. Meanwhile, GDP rose 1.3% in

Q3, 2016 over the previous quarter in seasonally adjusted annualized terms (SAAR). The growth

represented a deceleration from the 1.8% expansion in Q2.

Looking into the Q4, 2016, the growth rate is expected to accelerate as Japan's key index of indicators

designed to show the current state

of the economy rose in November to

its highest level in two years and

eight months, with industrial output

and consumption improving. The

index of coincident indicators, such

as industrial output, retail sales and

new job offers, rose 1.6 points from

October to 115.1, against the 2010

base of 100, the Cabinet Office said

in its preliminary report. The figure

was the highest since March 2014, a

month before the 3 percentage-point consumption tax hike to 8 percent in April that hurt household

spending and business investment at home, choking economic growth. The government kept unchanged

i ts basic assessment of the

coincident index, saying it suggests

the economy is “improving.” The

assessment is defined as indicating

t he l i ke l i hood o f econom ic

expansion. In November, the

nation's industrial output grew a

seasonally adjusted 1.5 percent

from a month earlier, as a weaker

yen and a recovery in the U.S.

economy prompted export-oriented

manufacturers to boost production,

the government said.

Global Market Update

10

2016 Annual Economic Report © All Rights Reserved XCELLON MARKET INTELLIGENCE (XMI)

Japanese consumer sentiment rose from November's 40.9 to 43.1 in December, which marked the highest

point since September 2013. The consumer confidence index measures consumers' expectations for the

next six months on a scale of 0–100, where 100 indicates that all see their living standards improving.

December's reading reflected a broad-based improvement as all the main sub-components of the index

gained ground from the previous month's result. Households' perceptions of their job prospects improved

the most, followed by their views on their willingness to buy durable goods and their overall livelihood.

Consumers' assessments of their income growth rose only mildly in the same month but hit a 43-month

high.

The core consumer price index was entirely flat in November compared to the previous month, below

October's 0.2% rise. November's reading mainly reflected that higher prices for clothes and footwear,

furniture and household utensils, and fuel, light and water were offset by lower costs for medical care and

culture and recreation. Core prices were down 0.4% from the same month last year in November. Overall

inflation rose to 0.5% in November from 0.1% a month earlier and marked the highest level since May 2015.

Core prices for Tokyo - available one month in advance of the national figures and thus a leading indicator

for countrywide inflation - fell 0.6% in December from the same month last year (November: -0.4% year-on-

year).

China

Despite increasing government spending, the Chinese economy was on a softer gear in the 2016 as

available data showed a growth

rate of 6.7% in the first three quarter

of 2016 the as compared to an

a v e r a g e o f 7 . 0 % i n t h e

corresponding period of 2015.

From January to September 2016,

government spending rose 12.5%

compared to the same period a

year ear l ier whi le revenues

increased by 5.9%. Fixed-asset

investment grew by 8.2% year-on-

year, compared to 8.1% rise in the

first eight months of 2016. While investment by state firms jumped by 21.1% year-on-year; those by private

firms rose 2.5%, accelerating from a record low of 2.1% in January to August.

Figures released showed exports tumbled 10.0% year-on-year to US$184.51 billion in September 2016,

compared to a 2.8% drop in the prior month while market estimated a 3.0% drop. In the last twelve months

exports rose only in March (+10.7%). Imports unexpectedly dropped by 1.9% to USD142.52 billion,

following a 1.5% rise in August and missing expectations of a 1.0% growth. Considering the first nine

months of 2016, the services sector expanded 7.6% while the industry sector grew at a slower 6.1%. From

January to September 2016, final consumption accounted for 71.0% of Chinese economy. Meanwhile,

investment contributed 36.8% of growth and net exports were a 7.8% drag on growth. For 2016, the

Chinese government is targeting the economy to grow between 6.5 to 7.0%. A year earlier, the economy

expanded by 6.9%, the weakest since 1990.

Global Market Update

11

2016 Annual Economic Report © All Rights Reserved XCELLON MARKET INTELLIGENCE (XMI)

Exports fel l 6.1% annually in

December, following the 1.6% drop

recorded in November. Despite the

weakening of the yuan, global

uncertainties are hitting the all-

i m p o r t a n t e x t e r n a l s e c t o r .

Meanwhile, imports rose 3.1%

annually, which came in below the

4 . 7 % i n c r e a s e r e c o r d e d i n

November. As a result of the strong

rebound in imports, the trade surplus

declined from $59.6 bil l ion in

December 2015 to $40.8 billion in

December 2016. In the full year 2016, the trade balance posted a surplus of $510 billion, which was below

the $608 billion surplus in 2015.

Russia

GDP in Russia contracted by 0.4% y-o-y in 3Q16, the slowest pace since the onset of economic

deceleration in 1Q15. Household consumption showed a slower decline of 3.1% y-o-y in 3Q16 compared to

5.2% seen in the previous quarter. Gross fixed capital formation (GFCF) also decreased by a notably slower

pace, 0.5% y-o-y versus 4.3%. Exports increased nearly 7% y-o-y in 3Q16, from a largely unchanged level

of exports in the previous quarter. Imports continued slowing for the 12th consecutive quarter, though at a

lesser rate of 3.0% y-o-y, from 6.7% seen in 2Q16. The downward inflationary trend continued in December

posting 5.4%, its slowest rate of increase since June 2012. Following a depreciation of 2.7% in November,

the Russian ruble appreciated 3.4% m-o-m in December. At the same time, the benchmark interest rate was

kept unchanged at 10.0% by the country's central bank.The Markit Russia Manufacturing PMI rose to 53.7 in December from 53.6 in November of 2016. It is the

highest level in 69 months, driven by substantial increases in output and new order amid healthier labor

market, with job creation growing at the fastest pace since March 2011. At the same time, new export orders

contracted at the weakest pace in 40 months. Goods producers continued to reduce their inventory

holdings while backlogs of work broadly stabilised. The robust performance by services and manufacturing

at the end of 2016 is expected to positively influence Russia's GDP growth in 4Q16 and extend into 2017.

Brazil

The economic activity indicator published by Brazil's central bank showed a decline in GDP of 3.9% y-o-y in

October 2016. The decline eased during the first three quarters of 2016, contracting by 5.4%, 3.6% and

2.9% in 1Q16, 2Q16 and 3Q16, respectively. The Brazilian real was largely stable in December, somewhat

depreciating by 0.3% m-o-m, following a 4.9% depreciation during the previous month. The central bank

lowered its benchmark interest rate by 25 basis points (bp) to 13.75% in December as inflation continued to

ease. Inflation decreased to 6.6% y-o-y in December, down from 7.4% a month earlier, which was the lowest

rate since January 2015. The unemployment rate increased in November to another record-high level of

11.9%.

Global Market Update

12

2016 Annual Economic Report © All Rights Reserved XCELLON MARKET INTELLIGENCE (XMI)

India

India's gross domestic product advanced 7.3 percent year-on-year in the third quarter of 2016, following 7.1

percent expansion in the previous period. Private consumption expanded at a faster pace while

government spending slowed down and fixed investment dropped further. The Indian government is

pursuing a wide range of infrastructure projects, including development of major new industrial corridors

and accelerating investment in railways and power infrastructure in order to support the economy in 2017. A

key fiscal reform due to be implemented in India in 2017 is the new Goods and Services Tax (GST), which is

expected to boost Indian GDP growth by about 0.15%-0.25% in and after 2017 and deliver significant

efficiency gains to Indian industry by lowering the costs of logistics substantially.

South Africa

In South Africa, GDP sustained its low growth path in Q3, 2016, growing 0.7% y-o-y similar to the previous

quarter. Private consumption increased by 1.1% y-o-y in 3Q16, up from 0.8% in 2Q16, while government

consumption was growing slower at 1.1% y-o-y vs 1.5% in the previous quarter. Gross Fixed Capital

Formation contracted by 6.1% y-o-y, the most since 2Q10, and exports declined by 3.9% y-o-y, the first drop

since the financial crisis of 2008/09.

Global Market Update

13

2016 Annual Economic Report © All Rights Reserved XCELLON MARKET INTELLIGENCE (XMI)

After the historic joint OPEC and

non-OPEC decision towards the

end of the year 2016 to cut oil

production, the OPEC Reference

Basket (ORB) jumped nearly 20%

in December to end above $50

per barrel (/b) for the first time in a

year-and-a-half at $51.67/b as the

oil complex surged. In contrast,

the 2016 yearly average value

came in at its lowest in more than

12 years at $40.76/b, around 18%

less than in 2015. Crude oil

futures on both sides of the

A t l an t i c ra l l i ed sha rp l y i n

December, rising to well above

$50/b to reach their highest levels in 18 months. Both made big gains since the end of November.

In the year 2016, however, oil futures witnessed one of the worst slump cycles since the financial crisis in

2008, resulting in their lowest

yearly average in 12 years. ICE

Brent averaged $7.84 higher in

December at $54.92/b, while

NYMEX WTI soared $6.40 to

average $52.17/b. In yearly terms,

ICE Brent was 16% lower in 2016

at $45.13/b for 2016, while NYMEX

WTI declined 11%, to $43.47/b.

Both were at their lowest since

2004. Also, increasing US shale oil

production and the strengthening

US dollar had negative impacts on

WTI. For the year, the spread

narrowed considerably from

$4.87/b in 2015 to $1.66/b. Hedge

funds and other institutional

investors' bets on crude oil prices

rising hit fresh all-time highs in

December, providing additional

fuel to ongoing steady gains in prices. Production data indicates that global oil supply decreased by 0.30

mb/d in December to average 96.92 mb/d, higher by 0.71 mb/d y-o-y. A decrease in both non-OPEC supply,

including OPEC NGLs, of 0.08 mb/d and in OPEC crude production of 0.22 mb/d reduced overall global oil

output in December. The share of OPEC crude oil in total global production stood at 34.1% in December, a

decrease of 0.1% from the month before.

Oil Market Update

14

2016 Annual Economic Report © All Rights Reserved XCELLON MARKET INTELLIGENCE (XMI)

Nigeria Economic Update

Nigeria Struggles Amidst Storm

Nigeria's economy plunged into recession in 2016, recording three consecutive negative Gross Domestic

Product (GDP) growth rate through the nine months of the year. The country's aggregate output declined

0.36% year-on-year in Q1; dipped further by -2.06% in Q and finally plunged deeper into negative territory in

Q3, recording growth of -2.24% y-o-y (according to data from National Bureau of Statistics). Thanks to

sharp drop in economic

activities orchestrated by

foreign exchange scarcity,

decline in the crude oil prices,

reduced oil output, amongst

others. Though the country's

non-oil sector saw a return to

p o s i t i v e g r o w t h i n Q 3

(recording a tepid 0.03% y-o-y

growth from -0.36% in Q2 of

the same year), a 22.01% y-o-

y contraction in the oil sector

dragged down the country's

economic performance. This

came as a series of attacks on

hydrocarbon infrastructure by the militant Niger Delta Avengers (NDA) saw output dropped from an average

of 2.2mn barrels per day (b/d) in Q3, 2015 to 1.6mn b/d in Q3, 2016.

Inflation on Trajectory Growth

Nigeria's inflation rate maintained upward trend through the year 2016 hitting 18.6% year-on-year (highest

reading since October 2005) in

the last month the year. The

culprits were the devalued naira,

removal of fuel subsidy and

various economic challenges

being faced by the country.

Trend analysis revealed that the

country's Consumer Price Index

(CPI) logged 9.6% y/y at the

beginning of 2016; hit 16.5% y/y

in June and 18.5% in the 11th

month of the year. Despite the

Central Bank of Nigeria (CBN)

efforts to quell the inflationary

pressure, all the monetary policy

measures (conventional and

unconventional) were ineffectual at achieving the price stability in the short term.

15

2016 Annual Economic Report © All Rights Reserved XCELLON MARKET INTELLIGENCE (XMI)

Hawkish Monetary Policy Stance: The Dominant Theme in 2016

The Monetary Policy Committee (MPC) of the Central Bank of Nigeria (CBN) kept the MPR between 11

percent to 12 percent in the first half of 2016. However, the MPC voted to move it up to 14 percent in July

2016 as it was faced with a trade-off between restarting economic growth and curbing galloping inflation.

The CBN maintained an asymmetric corridor of +200 basis points and -500 basis points, around the MPR.

In a bid to rein in inflation arising from excess liquidity in the system, the MPC voted to increase the Cash

Reserve Ratio (CRR) by 250-point basis, from 20.0 percent to 22.5 percent in March 2016. CRR remained

at 22.5 percent for the rest of the year.

Inter-Bank Call/T-Bills Rates Spike

Interbank call rate was relatively stable during the first half of 2016. A sharp rise to 35.26% was however

recorded at the close of the second quarter of the year. In the third quarter of the year, it gradually dropped to

as low as 14.50% in September. It, however, spiked to 36.42% at the beginning of the fourth quarter of the

year. The Twelve months' deposit rate, Prime lending rate and maximum lending rate remained relatively

stable throughout the year 2016. Treasury bills, however, saw a steady rise from the beginning of the year

until October when it dropped 13.96% from its peak of 15.25% in August.

Flexible Exchange Rate: The Panacea?

The average Naira exchange rate was relatively stable at the inter-bank foreign exchange market in the first

half of the year. However, in June 2016, the Central Bank of Nigeria (CBN) introduced the flexible foreign

exchange rate policy that would allow the foreign exchange interbank trading window to be driven purely by

market forces. This new policy brought about volatility in the market. The year saw a continued weakening

of the Naira against all major international currencies. The naira remained significantly volatile on the

interbank foreign exchange market as well as in the parallel market.

Nigeria Market Update

16

2016 Annual Economic Report © All Rights Reserved XCELLON MARKET INTELLIGENCE (XMI)

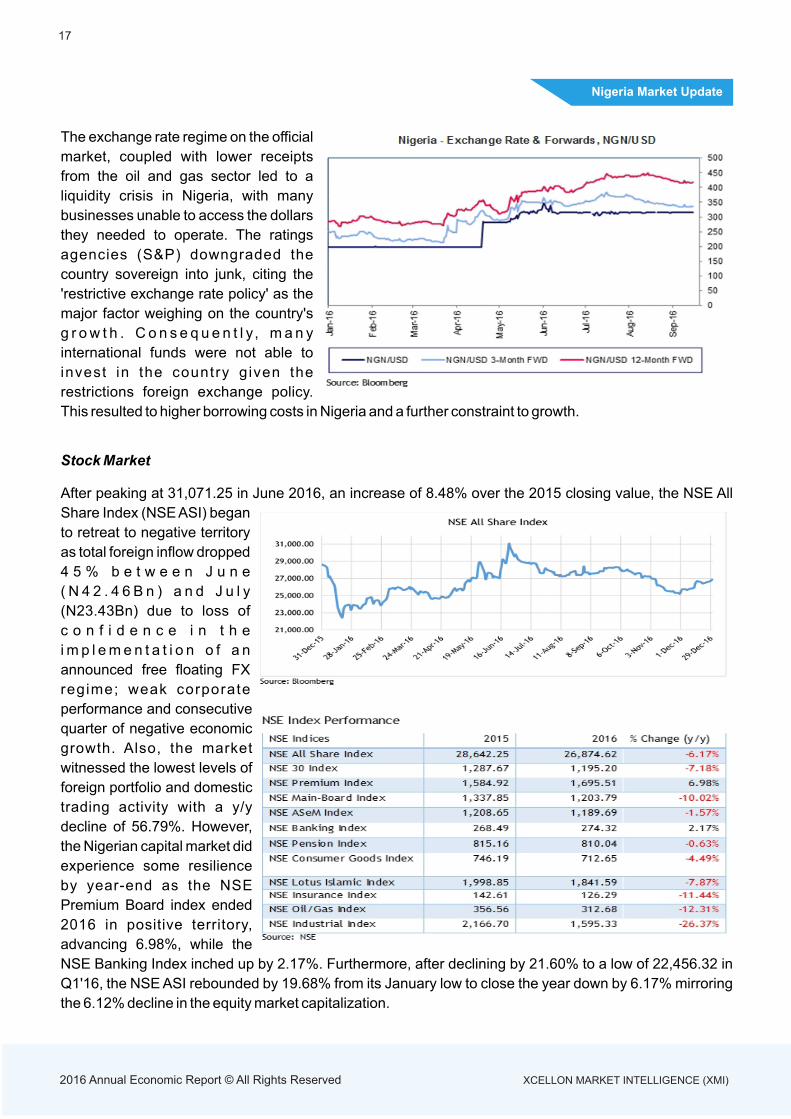

The exchange rate regime on the official

market, coupled with lower receipts

from the oil and gas sector led to a

liquidity crisis in Nigeria, with many

businesses unable to access the dollars

they needed to operate. The ratings

agencies (S&P) downgraded the

country sovereign into junk, citing the

'restrictive exchange rate policy' as the

major factor weighing on the country's

g r o w t h . C o n s e q u e n t l y, m a n y

international funds were not able to

invest in the country given the

restrictions foreign exchange policy.

This resulted to higher borrowing costs in Nigeria and a further constraint to growth.

Stock Market

After peaking at 31,071.25 in June 2016, an increase of 8.48% over the 2015 closing value, the NSE All

Share Index (NSE ASI) began

to retreat to negative territory

as total foreign inflow dropped

4 5 % b e t w e e n J u n e

( N 4 2 . 4 6 B n ) a n d J u l y

(N23.43Bn) due to loss of

c o n f i d e n c e i n t h e

i m p l e m e n t a t i o n o f a n

announced free floating FX

regime; weak corporate

performance and consecutive

quarter of negative economic

growth. Also, the market

witnessed the lowest levels of

foreign portfolio and domestic

trading activity with a y/y

decline of 56.79%. However,

the Nigerian capital market did

experience some resilience

by year-end as the NSE

Premium Board index ended

2016 in positive territory,

advancing 6.98%, while the

NSE Banking Index inched up by 2.17%. Furthermore, after declining by 21.60% to a low of 22,456.32 in

Q1'16, the NSE ASI rebounded by 19.68% from its January low to close the year down by 6.17% mirroring

the 6.12% decline in the equity market capitalization.

Nigeria Market Update

17

2016 Annual Economic Report © All Rights Reserved XCELLON MARKET INTELLIGENCE (XMI)

18

2016 Annual Economic Report © All Rights Reserved XCELLON MARKET INTELLIGENCE (XMI)

Nigeria Economic Outlook

Nigeria economy is expected to swing into positive territory in 2017 following the economic contraction the

country underwent in 2016, but this rebound will be far from spectacular. The continued imposition of capital

controls will weigh on growth and the improvement is expected to be sticky. While we expect there will be an

eventual further devaluation to the naira, encouraging a return in foreign investment, we do not expect that

this will take place within the first six months of the year, further pushing back the economic recovery.

Oil Recovery and Government Spending to Propel Growth

Fundamentally, the primary driver of the Nigerian economy, the oil and gas sector, is poised for a far better

2017 than 2016, and this is key to our expectation that Nigeria's real GDP growth will turn positive once

more. Although the sector only directly accounts for a little over 10% of GDP, it has traditionally been the

primary source of foreign exchange and of government revenues, and is a major determinant of investor

sentiment. The oil price slump which began in 2014 has been the primary source of Nigeria's recent

macroeconomic troubles, and arguably precipitated the renewed violence in the Niger Delta which further

exacerbated the country's woes. In 2017, we expect Nigeria not only benefit from higher global prices for

Brent crude but also a 19.0% rise in production to 2.1mn barrels per day (b/d). This will recoup the

production volumes lost in 2016 as a result of militant sabotage of pipelines and installations.

The other major positive in 2017 is that we expect that there will be greater public investment as the

government begins to implement an

expansionary budget plan. The grand

spending plans will be nowhere near realised

in full given the news in January 2017 that the

World Bank and the African Development

Bank have not been able to consider Nigeria's

borrowing requirements as the authorities

have not provided them with the requisite

paperwork will further impede spending.

Nevertheless, we do expect that there will be a

pick-up on 2016, when low government

revenues and delays to the budget being

passed by parliament meant that over the first

six months of the year, only NGN2.5tn of an NGN6.1tn budget for the year was spent.

Growth Expectation hinges on Naira Devaluation

Although the headline real GDP growth figure is expected in positive territory in 2017, there remain

significant headwinds, not least through the negative effects of a continuation of exchange rate policy. A key

constraint to stronger real GDP growth in 2017 will be a failure to devalue the naira within H1, meaning that

many of the problems which have held back Nigeria's recovery in 2016 will drag on through this year.

Following the relaxation of exchange rate policy announced in June 2016, we had expected that investor

sentiment would improve and inflows of dollars would pick up once more. However, the relaxation appears

to have been only partial, with bans still in place on the importation of 41 imports including rice, cement and

Economic Outlook

19

2016 Annual Economic Report © All Rights Reserved XCELLON MARKET INTELLIGENCE (XMI)

Nigeria Economic Outlook

steel pipes, and the central bank has been

intervening to keep the nai ra below

USD315/USD - compared to the parallel

market rate in excess of N450/$.

As oil revenues tick up in 2017, we expect that

the government will attempt to protect the peg

through the first half of the year, but a liquidity

crunch will continue to hamper business

activity and growth and will ultimately force a

devaluation in the second half. This will exert

negative pressure on growth in the short-term

through its effect on inflation, but a resultant

improvement in investor sentiment towards

Nigeria will see growth improve thereafter as investment picks up and dollar shortages are alleviated.

Retail Sector to come under Pressure

We anticipate that retail activity will remain weak over the course of 2017, constrained by diminishing

household spending power that is being

squeezed on multiple fronts. Inflation,

expected to be lower than the level seen in

2016, will remain high in 2017. As in 2016,

one of the key drivers of the elevated price

growth will be rising petrol prices which we

expect will be raised again this year as

effective subsidies are removed. Meanwhile,

we expect that household spending power

will also be negatively impacted by high

u n e m p l o y m e n t l e v e l s . N i g e r i a

unemployment rate had climbed to 13.9% in

Q3, 2016, compared to 9.9% in Q3, 2015 and

just 4.1% in 2010. We expect some

improvement in 2017, driven by the partial

recovery in the oil and gas sector. However,

Q3, 2016 data shows that online applications for the sector numbered 80 for every vacancy, and there

remains unmet demand for jobs. As a lagging indicator, unemployment levels will likely rise in the first half of

2017 before improving in H2.

Economic Outlook

20

2016 Annual Economic Report © All Rights Reserved XCELLON MARKET INTELLIGENCE (XMI)

Global Economic Outlook

Global economic activity is projected to pick up pace in 2017,

especially in emerging market and developing economies. However,

there is a wide dispersion of possible outcomes around the

projections, given uncertainty surrounding the policy stance of the

incoming U.S. administration and its global ramifications (according

to International Monetary Fund).

Advanced economies are projected to grow by 1.9 percent in 2017

and 2.0 percent in 2018. The forecast is particularly uncertain in light

of potential changes in the policy stance of the United States under

the new administration as stated by IMF.

The primary factor underlying the strengthening global outlook over

2017–2018 is, however, the projected pickup in Emerging Market and

Developing Economies (EMDEs') growth. The projection reflects to

an important extent a gradual normalization of conditions in a number of large economies that are currently

experiencing macroeconomic strains. EMDE growth is currently estimated at 4.1 percent in 2016, and is

projected to reach 4.5 percent for 2017. A further pickup in growth to 4.8 percent is projected for 2018.

While the balance of risks is viewed as being to the downside, there are also upside risks to near-term

growth. Specifically, global activity could accelerate more strongly if policy stimulus turns out to be larger

than currently projected in the United States or China. Notable negative risks to activity include a possible

shift toward inward-looking policy platforms and protectionism, a sharper than expected tightening in global

financial conditions that could interact with balance sheet weaknesses in parts of the euro area and in some

emerging market economies, increased geopolitical tensions, and a more severe slowdown in China.

While the Fed is looking to raise interest rates further in the near-term following the improvement of the US

economy. The fiscal stimulus plans of the new administration may trigger a more rapid rise in interest rates

than currently anticipated.

In the United Kingdom, the political uncertainty stemming from the referendum will continue to deter

investment. Growth is expected to decelerate in 2017 amid a slowdown in real household income growth.

However, accommodative policy action taken by the BoE is expected to soften the impact.

The Eurozone's uncertainties are seen as prevailing in 2017, both economically and politically. The federal

government elections in France and Germany will be important in the political debate. The latest

referendum on the constitution in Italy also highlighted that the Eurozone is in a fragile state in terms of its

political development.

In Japan, an accommodative monetary policy and a weaker yen are expected to boost growth next year.

That said, ambitious economic and social reforms are needed to ensure a healthier and more sustainable

growth trajectory. The main downside risk to growth next year will be increased protectionism under

Trump's administration.

Economic Outlook