xbrl as a tool for financial reporting

TRANSCRIPT

i

DECLARATION

This is to certify that this project entitled “XBRL as a Tool for Financial Reporting: Adoption by the

Zimbabwean Companies” which is submitted by me in partial fulfilment of the requirement for the

award of the degree Bachelor of Business Studies Honours Degree (Management) by the University of

Zimbabwe comprises only my original work and due to acknowledgement has been made in the text to

all other materials used.

Signature………………………

Name of student: CHIBOWA MARTHA DATE……………………..

APPROVAL

This is to certify that, this research report has been under my supervision as a University supervisor.

Supervisor……………………

Date……………………………

ii

DEDICATION

To The Lord God Almighty.

Affectionately to my parents (Mr & Mrs Chibowa).

iii

ACKNOWLEDGEMENTS My special thanks and appreciation goes to my supervisor Mr K. O. Kadare for persevering throughout

the time it took to complete this research project and for his continued support. Special thanks also go to

XBRL consortium for their daily updates to me which were highly beneficial during data gathering.

I sincerely acknowledge my parents for their continued support and guidance and making my dreams

possible.

I thank also my friends and everyone who shared their knowledge and opinions with me that made this

research successful.

Special acknowledgement goes to the Lord Almighty for His mercies and the spirit of knowledge,

wisdom and understanding that He continues to give unto us.

iv

ABSTRACT The main aim of this study was to investigate the reasons why Zimbabwean countries have not yet

adopted XBRL. XBRL is a business reporting language that uses extensible mark-up language and

hypertext mark-up language and is computer readable. Increased use of computers and the internet led

to the development of XBRL by the XBRL global consortium. Its development has greatly changed

financial reporting process in several countries. From the aim of the researcher, findings showed that

Zimbabwe has not yet adopted XBRL because of lack of awareness. Other reasons were because it had

not yet been made mandatory by the regulatory authorities and to some lesser extent resistance to

change. From the study, findings also indicated that there are vast merits of adopting XBRL as reported

from the empirical studies of the countries which have adopted XBRL as a tool for financial reporting.

The research showed that there is need for Zimbabwean companies to adopt XBRL as a tool for

financial reporting.

v

Contents DECLARATION .................................................................................................................................. i

DEDICATION ..................................................................................................................................... ii

ACKNOWLEDGEMENTS ................................................................................................................ iii

ABSTRACT ........................................................................................................................................ iv

Definition of terms and abbreviations ............................................................................................... viii

Definition of terms ........................................................................................................................ viii

abbreviations ................................................................................................................................. viii

CHAPTER 1 ........................................................................................................................................ 1

1.0 INTRODUCTION ..................................................................................................................... 1

1.1 BACKGROUND TO THE STUDY .......................................................................................... 1

1.2 PROBLEM STATEMENT ........................................................................................................ 2

1.3 OBJECTIVES OF THE STUDY ............................................................................................... 2

1.4 RESEARCH QUESTIONS........................................................................................................ 3

1.5 JUSTIFICATION OF THE STUDY ......................................................................................... 3

1.6 METHODOLOGY..................................................................................................................... 3

1.7SCOPE OF THE STUDY ........................................................................................................... 4

1.8 LIMITATIONS OF THE STUDY ............................................................................................. 4

1.9 ORGANISATION OF THE STUDY ........................................................................................ 4

CHAPTER 2 ........................................................................................................................................ 5

LITERATURE REVIEW .................................................................................................................... 5

2.0 Introduction ................................................................................................................................ 5

2.1 About XBRL .............................................................................................................................. 5

Figure 2.1: information flow using the general ledger..................................................................... 6

Figure 2.2: information flow using XBRL....................................................................................... 6

2.2 XBRL and its impact on financial reporting .............................................................................. 7

Figure 2.3: Data acquisition and analysis ........................................................................................ 8

2.2.1 XBRL and the accounting conceptual framework: qualitative characteristics ................... 9

2.2.2 XBRL in relation to accounting theories .............................................................................. 10

Table 2.1: theories .......................................................................................................................... 10

2.3 XBRL adoption: Evidence from different countries ................................................................ 11

2.4 advantages and disadvantages of XBRL .................................................................................. 13

2.4.1 Costs and demerits of XBRL implementation .................................................................. 13

2.4.2 Reported advantages of XBRL ......................................................................................... 13

2.5 Summary .................................................................................................................................. 14

CHAPTER 3 ...................................................................................................................................... 15

METHODOLOGY............................................................................................................................. 15

vi

3.0 Introduction .............................................................................................................................. 15

3.1 Research design........................................................................................................................ 15

3.2 Dependent Variables ................................................................................................................ 15

3.2.1 Awareness ......................................................................................................................... 16

3.2.2 Technology adaptation ...................................................................................................... 16

3.2.3 Size of business transaction .............................................................................................. 16

3.2.4 Policies and regulations .................................................................................................... 16

3.2.5 Availability of other tools ................................................................................................. 17

3.3 Data collection instruments ...................................................................................................... 17

3.3.1 Interview ........................................................................................................................... 17

3.3.2 data archives ...................................................................................................................... 18

3.4 Target population ..................................................................................................................... 18

3.5 Data analysis ............................................................................................................................ 18

3.6 Conclusion ............................................................................................................................... 18

Chapter 4 ............................................................................................................................................ 19

Data analysis and presentation ........................................................................................................... 19

4.0 Introduction .............................................................................................................................. 19

4.1 Data Findings and Interpretation .............................................................................................. 19

4.1.1 Impact of all variables ....................................................................................................... 19

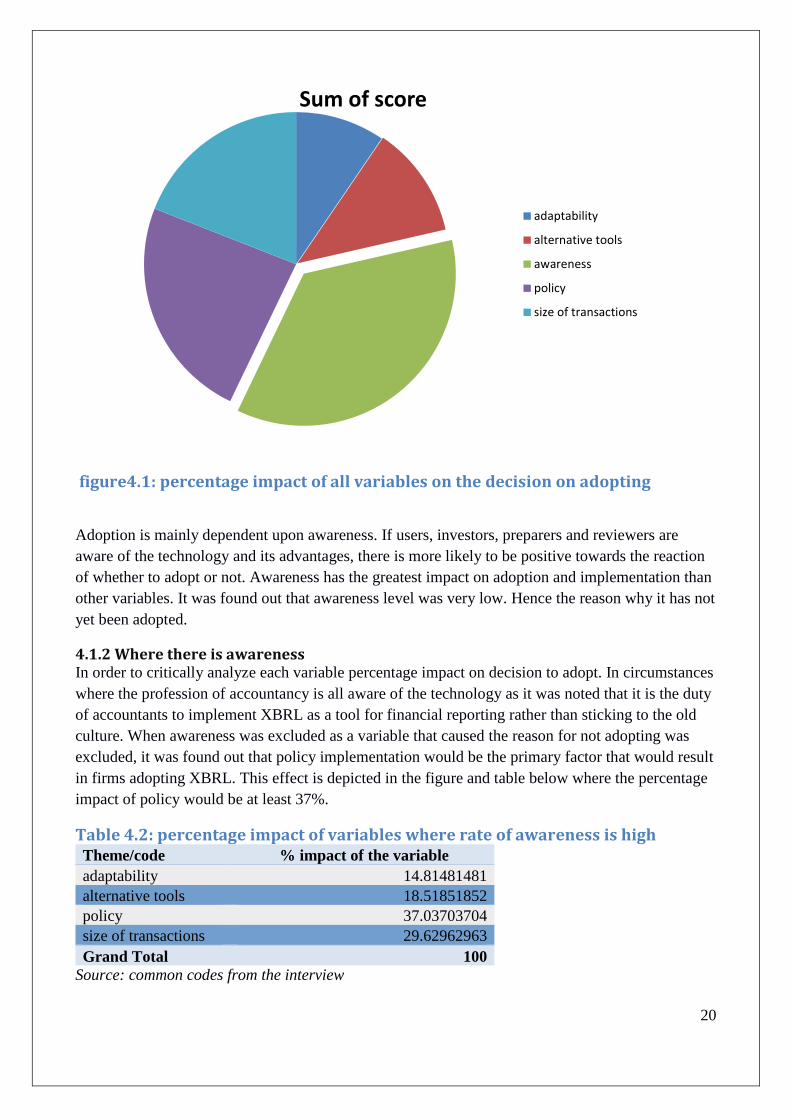

Table 4.1: point scores of variables and expressed as a percentage of the total score ................... 19

figure4.1: percentage impact of all variables on the decision on adopting .................................... 20

4.1.2 Where there is awareness .................................................................................................. 20

Table 4.2: percentage impact of variables where rate of awareness is high .................................. 20

Figure 4.2: impact of variables where the level of awareness is high ........................................... 21

4.1.3 Overlooking other tools .................................................................................................... 21

Table 4.3: % impact in the case where users acknowledge the pitfalls of other tools ................... 22

Figure 4.3: impact of the variables on adoption in the case where level of awareness is high and

other tools are seen as inefficient. .................................................................................................. 22

4.2 Other findings in relation to research questions ....................................................................... 23

4.3 Summary .................................................................................................................................. 24

Chapter 5 ............................................................................................................................................ 25

Conclusion and Recommendations .................................................................................................... 25

5.0 Introduction .............................................................................................................................. 25

5.1 conclusion of the study ............................................................................................................ 25

5.2 Insight of the study ................................................................................................................... 25

5.3 Foresight of the study ............................................................................................................... 26

5.4 Recommendations .................................................................................................................... 26

vii

Reference list...................................................................................................................................... 27

APPENDICES ................................................................................................................................... 30

INDEPTH INTERVIEW GUIDE ...................................................................................................... 30

viii

Definition of terms and abbreviations

Definition of terms XBRL- electronic language for transmission of business and financial data

Taxonomy- long lists of agreed upon definitions for all the terms used in specific types of business

reports.

abbreviations

XBRL- extensible business reporting language

HTML- Hyper Text Markup Language

IFRS-International Financial Reporting Standard

ZIMRA-Zimbabwe Revenue Authority

ZSE- Zimbabwe Stock Exchange

SEC-Security Exchange Commission

1

CHAPTER 1

1.0 INTRODUCTION The research scope is to investigate the adoption of the extensible Business reporting Language

(XBRL) as a tool for financial reporting. The preliminary investigation of the literature of the

XBRL and adoption by other countries reveals that most European and companies on the U.S SEC

have adopted the XBRL as a financial reporting tool as a requirement by their SEC or compliance

with IFRS as an IFRS taxonomy and exclusively on the account of its benefits both short term and

long term over other financial reporting tools.

Having said this, it is to be investigated whether local companies are adopting the XBRL to provide

financial reports to its stakeholders and also to endeavour on the reasons for the adaptation of the

reporting language.

Taking into account commonly used accounting tools (such as excel and pastel) each firm might

have a preferable reporting tool it uses. The desired outcome of the study would be for most

companies to appreciate the benefits of using the XBRL such as improved accessibility,

interoperability and reuse of data , to mention a few.

The aforementioned could constitute an answer to effective and efficient financial reporting.

1.1 BACKGROUND TO THE STUDY Xbrl.org defines XBRL as a computer language that, through a process of tagging, makes

documents machine readable. The user's system can automatically extract the information without

copy-pasting or keying-in. XBRL converts financial information in a document (be it word, excel,

PDF etc. document) into a document file with XBRL codes making it computer readable. Once

entered into a database (e.g. ZSE database system), stakeholders for example financial analysts and

investors can instantaneously download it in a format that allows for immediate analysis and

comparison. It was developed by a global not for profit consortium, XBRL International for use

by different users for different uses (e.g. Government agencies that are improving government

reporting by standardising the way that consolidated reports are prepared and used within

government agencies or published into the public domain.

Research by Pinscher & Li (2008) have found out that most listed companies that adopted the

XBRL gave them a competitive advantage over their rivals who had not adopted the XBRL. Critics

of Dzinkowski (2013) cite that XBRL taxonomy enables unique identifying tags to be applied to

2

items of financial data such as ‘net profit’. The tags provide a range of information about the item,

such as whether it is a monetary item, percentage or fraction. This will make it easy for analysing

the information. Noting experiences in Israel's adaptation of XBRL, Malkelevich et al (2015)

concluded that beginning in 2008, the Israel Securities Authority (ISA) mandated that most public

Companies provide data to be converted into XBRL-tagged financial reports and displayed on the

ISA’s MAGNA website. Citing a research by Pinsker (2008) the South African company that

adopted XBRL in that year of the study wanted to comply with impending domestic legislation and

regulations (such as the Electronic Communications and Transactions Act 2002) . The U.S SEC

requires that all listed companies must submit the documents in XBRL code.

Most companies in Zimbabwe are still using other financial reporting tools and the Zimbabwe Stock

Exchange Commission has not yet mandated all the listed firms in its filing rules to use the XBRL

as the reporting language for financial data. Preliminary investigation shows that most companies

are using pastel and excel in Zimbabwe. In an article by the independent (2012) the Securities

Commission of Zimbabwe only commanded the listed companies to adhere to the International

Financial Reporting Standards (IFRS) and the listing rules. However XBRL is an IFRS taxonomy

and therefore, although not mandatory, it is the time for Zimbabwean companies to start shifting to

the XBRL.

This study will therefore focus on listed companies on their perspective on the XBRL and their

reactions since it has been long developed.

1.2 PROBLEM STATEMENT XBRL has been implemented by most companies in the first world countries and most research has

indicated that there are both costs and benefits attached to using XBRL as a reporting tool but

however it is still continuing to be more familiar in those countries than here in Zimbabwe. If so

why? Hence the need for the research on the why most local firms have not yet adopted XBRL and

benefits so far gained for those using the reporting language. The aforementioned fact has impelled

the research to be undertaken.

1.3 OBJECTIVES OF THE STUDY The intention of the research to be elaborated is to investigate the adoption of the extensible

Business Reporting Language by Zimbabwean listed companies as a tool for financial reporting.

More precisely:

To establish reasons on why most companies have not yet adopted the XBRL

3

To discover on the benefits of XBRL over other reporting tools.

To obtain an understanding and contribution of the XBRL to the accounting

profession and to financial reporting.

1.4 RESEARCH QUESTIONS Why is it that most companies have not yet adopted the XBRL?

What are the benefits of using the XBRL over other reporting tools?

Is XBRL an answer to effective financial reporting?

1.5 JUSTIFICATION OF THE STUDY This study shall be conducted to get an understanding on the reaction on XBRL implementation and

effects of the implementation of the XBRL as a financial reporting tool as there is a gap for that in

the Zimbabwean business environment.

To the researcher

The research is a requirement by the University of Zimbabwe for the completion of the honour's

Degree in Accountancy. It shall also develop and sharpen the researcher’s skills in doing research

projects.

To the University of Zimbabwe and the academia

The research is a contribution to the literature that may be used by current and future students

carrying out a research.

1.6 METHODOLOGY This study shall be conducted mainly based on the phenomenology philosophical view. As cited by

Remenyi et al (1998) from Cohen & Manion (1987) that phenomenology is a theoretical point of

view that advocates the study of direct experience taken at face value and one which sees behaviour

as determined by the phenomena of experience rather than by physically described reality. The data

shall be gathered with the use of interviews with accountants in public firms and other data shall be

gathered with the use of databases on information on the research.

Most researchers have found out that use of multi approaches is beneficial to a research hence this

study may be conducted using a pragmatic research approach. Information gathered shall be both

qualitative and quantitative so as to improve the quality of the findings. The researcher shall have

little or no control over some of the findings therefore implementing a positivist approach.

4

1.7SCOPE OF THE STUDY This study will be focusing on XBRL as a financial reporting in the Zimbabwean context. Primary

focus shall be on listed companies and their reaction to the adoption of the reporting language.

1.8 LIMITATIONS OF THE STUDY Matters or occurrences may arise which may be beyond the scope of the researcher, hence causing

limitations to the study. The limitation of validity and reliability may occur to the qualitative

information gathered by the researcher. Other limitations may include the gathering of evidence and

time constraints.

1.9 ORGANISATION OF THE STUDY This research shall be organised from all the subsequent four chapters as follows. Chapter 2 shall

look at the critical literature review on XBRL and financial reporting by other authors. Chapter 3

shall look at data gathering techniques used by the researcher. Chapter 4 will detail the findings of

the researcher about the study from the data or information gathered. Finally chapter 5 shall script

the conclusion of the researcher on the topic under study and the recommendations in relation to the

study or relative study.

5

CHAPTER 2

LITERATURE REVIEW

2.0 Introduction

Literature review is an objective and critical summary of the released literature of tremendous

relevance to the area of research under study. The foremost reason is to familiarize with current

thinking and research on a specific distinctive study area (Harvard University library). This

literature assessment is on financial reporting and XBRL. The literature review is limited to XBRL

and financial reporting, every other use of XBRL is excluded .This section provides a context and

background of the current study. Firstly, it provides an overview of XBRL and the development of

XBRL and its impact on financial reporting. The second section discusses XBRL and the

accounting conceptual framework and theories. This discussion is then followed by adoption of

XBRL which acknowledges literature on empirical studies from western, eastern, Europe, central,

and south countries of the world which shows the evidence of its adoption.

2.1 About XBRL

XBRL is a search facilitated technology that uniquely tags pieces of data in the financial statement

which identify the information structure and, or content for example whether it’s a dollar item or

quantity. It is a computer language which makes documents computer readable which was invented

by Charles Hoffman and developed by XBRL International, a global consortium (www.xbrl.org).

Most companies have a company website to communicate all types of information to interested

parties including financial information. This shows the growing use of computers and the Internet.

Stakeholders can download this information for their own particular use. If the file is in PDF

format, the user needs to have Adobe Acrobat to be able to read the file. Other formats to display

information are often hypertext markup language (HTML) which defines the appearance of

information on a computer. When calculations need to be done the information needs to be retyped

unless when the document was in Excel format. When comparing multiple years or the sector of the

business re-keying can be time consuming and susceptible to error.

The information required by each stakeholder is different and thus one report would not be

appropriate. Information is provided in the form of a general ledger using a chart of accounts where

the statement of comprehensive income, statement of financial position and cash flow statement

will then be generated. The statement can be in different formats depending on the needs of the

6

user. However this process is very costly (Elliot and Elliot 2011, p.785). The process is depicted in

the diagram below.

Figure 2.1: information flow using the general ledger

Source:www.xbrl.org.au/training/NSWWorkshop.pdf

The need to make multiple reports has led to the development of XBRL which is an extension of

HTML. XBRL makes it easier for direct system-system data sharing between corporations and its

stakeholders and it permits improved analytical capability. All numerical data will be uniformly

defined and presented. A company can easily select, store, analyze and exchange XBRL data. This

process is depicted in the diagram below.

Figure 2.2: information flow using XBRL

7

source:www.xbrl.org.au.training/NSWWorkshop.pdf

Financial statements presented in XBRL format are capable of being downloaded into an analyst or

investor's own spreadsheet, for example Microsoft excel. The analyst or investor does not need to

retype the information. XBRL allows any type of information to be transferred to a statistical

package without having to retype the information.

2.2 XBRL and its impact on financial reporting

Corporate diversification, the depth and speed of economic change and international relationships

has immensely modified the mode of financial reporting to Internet real time reporting which even

creates a competitive advantage and more useful to investors.

Extensible business reporting language (XBRL) is an open internet standard built on extensible

mark-up language (XML). XBRL provides more timely access to information, it creates

standardized environment which allows users to prepare, exchange and analyze financial

information on the Internet (Jianing, 2014). Mike Willis the Deputy Global Chief Knowledge

Officer of PwC defined the relation of accounting and XBRL postulating accounting as the

language of business and XBRL as the language of e-business. This indicates that there is a

relationship between accounting and XBRL , thus XBRL and financial reporting as accounting

comprises of financial reporting. Most researchers on the adoption of XBRL and financial reporting

stated that there are so many advantages of adopting the computer language and they postulated that

in the future it will be the principle of financial reporting as many first world countries have

implemented and mandated its use.

A research by Hodge; Kennedy and Maines, (2004) showed that, that who integrate and acquire the

knowledge easily facilitates directed searches and simultaneous presentation of related financial

statements. They also reported that it improves transparency of financial reporting. Although they

noted the merits, they also found out that despite some appreciating the benefits, many users were

not accessing the technology. The reason is because not everyone has got access to the Internet.

A study by Pinsker, (2003) showed that XBRL speeds up the auditing process. However the

auditor has to know how it operates and also the tagging system that was utilized by the corporate.

The analysis conjointly showed that XBRL presents better quality disclosure in layman's view, that

is, dissemination of understandable facts both financial and non-monetary with the aid of globally

providing standard terminology through an efficient accounting data system. This conjointly

8

mitigates benefits of selecting a financial reporting approach that artificially enhance financial

performance and condition, that is, financial statement fraud. This is enhanced through integration

as similar tags show the connection between items and therefore can be evaluated along.

The researcher also noted that the reporting language provides for real time reporting hence

stakeholders, for example potential investors or financial analysts, can make useful judgments

concerning the share price, for example. Having acknowledged most merits of XBRL in financial

reporting and auditing Pinsker, (2003) also found out that knowledge and experience on burl were

still low and found the need for companies to implement training and, or hiring experts on burl so

that they could implement it and start benefiting from its use.

In a case study by PwC of the investment management industry (trusted and efficient financial

reporting), reported that for a company to meet shareholder demand for transparency and greater

speed in financial reporting, businesses need to implement more effective ways of communication.

It recognized the strengths of XBRL in effectively and efficiently communicating financial

performance to its stakeholders.

From a conceptual framework developed by Hogarth, (1980) on how users of financial statements

acquire and use data for financial statement analysis depicted below. It can be seen that XBRL is

useful at every stage and makes it easier at each stage of data acquisition and analysis.

Figure 2.3: Data acquisition and analysis

Information acquisition- this is the stage where one finds and reads the information. The tagging

process makes it easy for one to specifically find the information he/she will be looking for and it’s

readily readable in any format (Cheung, 2011).

Information evaluation- the information can easily be evaluated to assess the condition and

performance of the firm. Integration makes it easier for the information in the reports to be

evaluated as similar tags encourage the data to be evaluated together (Hodge et al, 2004).

Information combination- this is the stage where the user assimilate implications and weigh to

arrive at a conclusion on the financial position or performance of the company. XBRL improves

multiple company financial information analysis (xbrl.org, 2008).

Information

acquisition

Information

Evaluation

Information

Combination

9

2.2.1 XBRL and the accounting conceptual framework: qualitative characteristics

Financial reporting includes disclosure of each monetary fact and reviews to the stakeholders that

offer essential records about the economic or financial health and operations of the organization.

For financial reporting to be effective and efficient, the records provided ought to fulfill the

following qualitative characteristics which can be understandability( i.e. ease of understanding of

the monetary assertion, guidelines, technique and assumptions used); relevance( i.e. records

furnished must be applicable to the user and of material effect); reliability( i.e. should be unfastened

from fabric error or bias); comparability( i.e. the statements or the reports ought to be without

problems compared, there ought to be consistency in presentation and disclosure from period to

period and inside the industry) and other qualitative traits which might be trustworthy presentation,

timeliness, prudence and neutrality.

From the literature review of several studies it is to be seen that XBRL enhances the characteristics

of quality information.

Effective: as it enhances the relevance of information to different stakeholders, a user can simply

query for the specific type of information he/she wants which will be pertinent and also real time

reporting makes information available timely.

Efficient: in the fact that it reduces costs associated with non-electronic financial reporting and the

need to convert into different formats which has anomalies when doing so due to inherent human

error.

Availability: in the sense that XBRL reports can be easily accessed by a user anywhere hence the

information is readily available and the information will be current.

Compliance with legal requirements: it is to be appreciated that IFRS has defined taxonomy of

XBRL and most revenue or filling authorities have adopted XBRL hence information reported will

be complying with the regulatory requirements.

Reliability: in the fact that XBRL provides reliable information as the tagging process can

specifically show each individual item and provides trustworthy information.

Comparability: inter-company can easily be made when the financial reports are made in XBRL

format

Full disclosure: lately reports were made in the form of a general ledger. Due to costs of financial

reporting, not all information could a company publish or issue to all its stakeholders. With XBRL

any user can access any information of any characteristics in the financial statements.

10

2.2.2 XBRL in relation to accounting theories

Table 2.1: theories

THEORY MERITS/ contribution of XBRL

Agency (Jensen & Meckling,

1976): aims to resolve the agency-

principle problem.

Resolves the agency-principle problem.

Resolves the problem of information

asymmetry as the interests of the managers

differs from that of owners (Chen et al, 2015).

Accounting theory: states the basic

accounting framework and

methodology to achieve uniformity

(Wolk, Dodd and Rozycki, 2008).

XBRL is based on a taxonomy hence has a

framework and methodology.

Shareholder wealth maximization

theory (Sharfman, 2015): aims to

increase shareholders wealth.

A research by Pinscher & Li (2008) indicated

that companies who reported in XBRL had

increased earnings per share as it gives a

competitive advantage. Reduced costs also

increases profits hence shareholder wealth

maximization.

Efficient Market Hypothesis: aims

to increase the efficiency in the

financial market (Malkiel, 2003).

XBRL results in real time financial reporting

hence efficiency in financial reporting.

Financial analysts can efficiently and easily

judge the EPS of a company on the stock

market using real time information causing

existing share prices to always reflect and

incorporate all relevant information

Stewardship theory: Donaldson,

(1991) states that it is based on the

assumption that managers are

responsible stewards.

XBRL enables full disclosure of financial

reporting hence managers a greater able to

report on the performance of the company.

11

This table shows that for every weakness or strength of a theory in accounting or an advantage,

XBRL provides a solution or enhances the strengths of the theory. The aforementioned relationship

with the conceptual framework and the theories and advantages related shows that there are more

benefits to XBRL. Most research has shown benefits than demerits of which the demerits are

primarily from lack of knowledge and computer illiteracy.

2.3 XBRL adoption: Evidence from different countries

This section shows the summary of the empirical studies carried out by different researchers for

different countries and companies and the results that were reported.

Europe- (xbrl.org.eu) indicated that European commission and the committee of European

banks that is entire banking industry implementation was inspired by XBRL promise of

efficient data gathering and automated analysis of information since there was a move to

electronic financial reporting. XBRL Europe was then developed to generate better

consistency, interoperability, global sharing and knowledge sharing.

China- from an interview conducted by Kernan, (2008) it was reported that the ministry of

finance and the revenue authority appreciated the implementation of XBRL. China is

credited as the first capital market to adopt quickly although XBRL filings from 2004 up to

2008 were unlikely to affect the capital markets (Songshenget al 2015). It was also reported

by Chen et al that in 2007 some firms on the Shanghai stock exchange (SHSE) and

Shenzhen stock exchange (SZSE) for the AAA stock market had adopted XBRL as a

standardized format for reporting. China reported that XBRL has facilitated knowledge

sharing, and inspired change. XBRL is more influential on a bigger supply chain.

Preliminary literature review shows that Chinese companies have quickly adopted XBRL

although America was the first to implement the electronic tool for financial reporting and it

also hopes to see extended use of XBRL even in small companies and mining.

America- XBRL was developed in America. The inventor had recognized anomalies and

inconveniences that arose when converting the data into readable format and the need for a

global access of data from anywhere. Kernan, (2008) postulated that although XBRL had

been made mandatory in USA by the SEC, the reason was China was moving faster than

them was because in China there was no need of shifting to it but it was installed by most as

a background system which would change any input into XBRL rather than wasting time

trying to acquaint with regulatory requirements.

12

India- According to a report by Shirdhankar (2014) it was conveyed that XBRL took a

wave in India in 2007 and was made mandatory in 2011 by the ministry of corporate affairs.

The other regulators were the Reserve Bank of India, Securities and Exchange Board of

India and the Insurance Regulatory and Development Authority of India. The ministry of

corporate affairs reported that above all other merits aforementioned, XBRL resulted in

more accurate handling of data, more effort is concentrated on analysis rather than time

consuming costly manual processes which require re-entering of data.

Israel- From an empirical study by Markelevich, Shaw and Weihs, (2015) the Israel

Securities Authority (ISA) mandated the implementation of XBRL in 2008. They reported

that during its first year of adoption a negative result came out. The ISA assumed that it

would increase direct foreign exchange although the researchers concluded that this was

probably that in 2008 there was a global crisis hence little movements in investments.

South Africa-: a research by Steedkamp and Nel, (2012) showed that there was slow

adoption of the technology as there was a very low level of awareness. The other reason

cited was that the reason why most firms had not adopted the technology was becomes it

was not yet mandatory as with other countries. The researcher looked at economic

circumstance as a variable that influenced adoption and the result was that it had no

significant influenced on the decision to adopt or not to adopt. Steedkamp & Nel also

concluded that the case for XBRL should be made stronger for adoption and awareness rate

to improve. Research also found out that its adoption was important and relevant to all

stakeholders interested in information management. South African Institute of Chartered

Accountants (SAICA) formed XBRL South Africa to encourage implementation of XBRL

in South Africa.

Company -Microsoft corporate in 2002 was reported to be the first technology company to

report in XBRL on the Internet. From a report by Neal Hannan, (2003) from Microsoft

corporate, he announced that Microsoft office 11 was to feature an XBRL add-in so that it

will be easy for management to easily communicate business performance and improve

support for corporate transparency.

Earlier studies on XBRL indicated that the technology was beneficial to the global world of

financial reporting. Most researchers did not look at the demerits or problems associated

with XBRL. Also there is no or limited literature on XBRL in Zimbabwe and Southern

African countries.

13

2.4 advantages and disadvantages of XBRL

2.4.1 Costs and demerits of XBRL implementation

Justification of XBRL adoption without noting the demerits would be irrational. Like any other

decision that can be made, XBRL has costs or demerits associated with it. Most research has

reported on the advantages of adopting XBRL. The costs of XBRL adoption have been overlooked

by most researchers. According to a survey by Choi et al (2008, p.71) cited by Ahrendt, (2009, p.

16) it was reported that most companies did not do a cost benefit analysis before the implementation

of XBRL. However the study also showed that XBRL was neither a costly or lengthy process.

There are costs associated with XBRL which are hardware and software costs, training costs and

maintenance costs as mentioned by Remenyi et al (2000, p.89).

Ahrendt (2009, p.15) as well acclaimed that companies are afraid of change and may resist it

especially if the current system is functioning well. Also a citation by him from (McCann, 2009)

stated that it might seem easy but it definitely takes time hence time consuming. Neal Hannon

reported that there may be costs if the company treat XBRL as an afterthought, if they hire a

consultant, no attempt has been made to examine the benefits and if none in the organization

understands XBRL. XBRL USA (2010) declared and acclaimed that real time Internet. Reporting of

burl is indeed a double edged sword as it may cause disproportionate volatility of share prices and

may cause the industry to base on short term reporting and it also reported that it may increase

information abuse.

An article by Quaglieri (2012) critiqued that as XBRL taxonomies are extensible they are too

adjustable which may allow companies to enter data which may not exist thus gearing financial

statement fraud. When auditing the financial statements in XBRL, Plumlee and Plumlee (2008)

noted that an assurance cannot be made on the reliability of statements in XBRL as attestations

could not be made on the free and fairness of the statements as there could be mis-tagging.

Semantic misrepresentation, incomplete or incorrect XBRL data and inadequate use of XBRL tags

were some of the shortfalls reported by Markelevich et al (2015).

2.4.2 Reported advantages of XBRL

The Accounting Institute of Chartered Public Accountants (AICPA) reported that XBRL has vast

advantages to the profession of accountancy. According to Steenkamp and Nel (2012); XBRL

enhances the automated process of data collection, that is, data from different divisions or regions

with different accounting system can be integrated cheaply, quickly and efficiently. XBRL

streamlines the preparation of financial reports for both internal and external decision making.

14

Noting an empirical study by Steenkamp and Nel (2012) the researchers postulated that XBRL

implementation is beneficial to companies as it facilitates foreign direct investment as the

information will allow international investors to read and analyze the statements regardless of their

language. Yen and Wang (2015) also acclaimed that it improves the stock market price hence

increased share price as also highlighted by Yu, Jia and Lin (2014).

XBRL will enable companies to benchmark themselves against their competitors or sectors

(Steenkamp and Nel, 2012). Furthermore, it facilitates the convergence of accounting standards by

aligning financial concepts among public taxonomies. As it facilitates principle based accounting, it

reduces the need to know the location of an item. Real time on-line reporting facilitates

transparency of the reports (Jones and Willis, 2003).As cited by Songsheng et al (2015) from

(Yoon, Zo, and Ciganek 2011) noted that as XBRL is an advanced information search engine, it can

therefore improve information disclosure quality.

2.5 Summary

From the aforementioned, it is evident that XBRL has been of rising concern in financial reporting.

At present XBRL is obligatory for financial reporting in a variety of countries. Having

acknowledged the advantages and disadvantages of XBRL, it is to be appreciated that as we are in

the era of Internet revolution, XBRL plays an important role in the accounting profession and

financial reporting. It is to be therefore reviewed on the reasons on why Zimbabwean companies

have not adopted XBRL foregoing the merits of using it and not gaining a competitive advantage in

the global market.

15

CHAPTER 3

METHODOLOGY

3.0 Introduction This section shall focus on the methods, techniques and procedures on how the researcher gathered

information so as to answer the research questions. As defined by Nangia (2008) research

methodology can be defined as a way of systematically solving research problems. As the research

methodology tries to solve the research problem the researcher structured this chapter in a way to

easily outline the variables and how the research question that is related to the variable was

answered. The rest of the chapter is laid out showing data collection instruments and their merits

and demerits, targeted respondents, data analysis and the conclusion.

3.1 Research design Research design can be defined as the basic methods of data collection. This study's research design

was influenced by the research questions and the theories that link the independent variable to the

dependent variables. An unstructured approach to answer the research questions was utilised by the

researcher as the approach is mostly appropriate so as to determine the extent of the research

problem principally to qualitative research. In order to ensure high quality of findings, the

structured approach was also utilised as some of the questions administered to the respondents had

suggested responses. An ex-post fact research, that is, descriptive methodology was used as the

researcher engaged in fact finding enquiries on whether companies are using XBRL as a tool for

financial reporting in Zimbabwe or not and to endeavour on some of the reasons why Zimbabwe

has not yet adopted XBRL since its inception.

3.2 Dependent Variables Subsequent study cited has shown that there is possibly a relationship between XBRL

implementation and the following variables which are lack of awareness, resistance to change,

technology adaptation, size of business and transactions, use of alternative tools and also policies

and regulations of a country or its stock market. It is therefore postulated that adoption is dependent

upon awareness plus willingness to adapt to change plus size of business plus the influence of

policies and regulations.

16

3.2.1 Awareness It is more likely that Zimbabwean companies have not yet adopted XBRL due to lack of awareness.

From a citation by Steenkamp and Nel (2015) from Pinsker (2003, p.734) from a survey conducted

in USA, it was found out there was a positive relationship between level of awareness and adoption

as it was reported that firms with auditors and accountants knowledgeable and aware of XBRL were

mostly likely to implement it. From the aforementioned advantages of XBRL it is postulated that if

investors are also aware of the merits of XBRL they can possibly be able to influence the industry

to turn to XBRL financial reporting. To mitigate agency costs and information asymmetries,

investors would mostly prefer XBRL reporting if they are aware of it and its merits as it is hold that

managers can only report information to their advantage rather than the owners or other

stakeholders. The question whether there is awareness which could answer as well the research

question 1.4.1 was addressed to the chartered accountants in accounting firms.

3.2.2 Technology adaptation As technology is changing quickly, it has greatly influenced financial reporting from paper to

paperless financial reporting where reports are made available on the internet. However these are

mostly in pdf format. Anomalies of reporting in pdf made the XBRL consortium to develop XBRL.

However it is not everyone who quickly adapts to technological change. From the empirical studies

by the aforementioned researchers, it was noted that first would countries like USA and UK were

quickly to adopt and the research by Steenkamp et al (2015) indicating that South Africa slowly to

adopt. This probably might indicate the fact that there is some extent of change resistance to

technological change or rather slow adaptation. The question on how long it takes for a crucial

change to be taken can possibly show the extent of speed of adoption if too long indicating

resistance to change.

3.2.3 Size of business transaction As reported by Shongsheng et al (2015) XBRL adoption results in increased earnings per share and

reduced cost of capital. However from a comment by the China finance minister interview by

Kernan (2008) the results could be only positive on a bigger supply chain. Smaller transactions

would only prove costly for real time financial reporting hence possibly the reason on why firms

have not yet adopted XBRL in Zimbabwe due to their size of transaction and the size of the firm in

terms of capital to implement XBRL which include training costs.

3.2.4 Policies and regulations Most regulatory authorities from China, India, Israel, UK, USA and other countries have

implemented XBRL afterthought of its advantages. The issue of policies and regulations also comes

back to the fact that regulators or policy makers may not be aware. Auditors, financial analysts or

17

the accountancy profession in Zimbabwe could influence the Zimbabwe stock exchange to regulate

and even mandate all listed companies to file in XBRL. From a research by Li and Nwaeze (2015)

it is noted that regulators are most likely to opt for XBRL as it reduces the burden for them to get

through so much information in pdf financial reports. It is therefore likely that if regulators for

example ZIMRA and financial analyst would change the policies and regulations of reporting in

XBRL.

3.2.5 Availability of other tools After having noted the demerits of XBRL and the fact that financial reporters are comfortable with

using formats already available like excel, XML, and pdf makes it possible to conclude that

availability of other tools has made the XBRL implementation slow globally. From the shortfalls of

XBRL by Markelevich et al (2015) of mistagging and not providing room for footnotes could also

indicate why XBRL has been overlooked. However it is to be acknowledged that it have vast

advantages and to answer whether it is an answer to financial reporting (research question 1.4.3).

The question would its reported advantage Zimbabwe stock market and accountancy profession was

asked.

3.3 Data collection instruments It is noted that XBRL implementation and adoption investigation findings application is on pure

research methodological approach. The objectives of the study, as descriptive to the phenomenon

and correlation to the variables, took use of qualitative enquiry mode in conducting the study.

Interviews were used as an instrument for primary data collection with guided interview questions.

However were an interview was not appropriate due to time constraints, a questionnaire was

administered which had both closed and open ended questions. To answer the question whether

XBRL is an answer to effective financial reporting and its contribution to the accountancy

profession, archival research was used where the researcher made use of available literature in data

and textual archives.

3.3.1 Interview Merits

The response rate is high

Allows room for probing which increases data accuracy

There is always clarification of questions and answers

new points can be drawn out from the conversation

Demerits

Subject to time constraints for face to face interview

18

Interviewees at times may not be willing to give sensitive information

3.3.2 data archives Merits

provides vast information

information can be compared cross sectional

access to longitudinal data and global information

Demerits

unreliability of data

irrelevance of some data to the subject

3.4 Target population As accountants are responsible for XBRL implementation as noted from literature reviewed, it is

therefore pointed out that it is then the chartered accountants who can have possibly evidence or

concrete reasons why XBRL has since yet not been adopted by Zimbabwean companies. Steenkamp

and Nel (2015) conducted their research with the data collected through a structured, self-

administered website based survey sent to chartered accountants as they will or are primarily

responsible for XBRL implementation. Chartered accountants in accounting firms have more

information in the industry since they engage with companies from different sectors hence would

have a more sharper perspective on the reasons why there is not yet adoption and implementation of

XBRL and whether if its implementation would benefit Zimbabwe.

3.5 Data analysis Basic examination of the information obtained was done as a method for checking the precision and

legitimacy. The analyst exhibited the information utilizing rates from point scoring which were

figured in order to demonstrate the diverse reaction for every inquiry and the researcher chose to

utilize them since they are easily comprehended even by layman. Charts were also used to clearly

indicate the extent of the effect of a variable on the adoption on XBRL.

3.6 Conclusion This section brought up the examination system which was potentially reasonable for this study. The

specialist pointed in-depth meeting as the information accumulation technique including utilization of a

questionnaire and information archives in order to accomplish the exploration targets. The section

additionally introduced the focused respondents which are the Chartered accountants and the variables

indicated out the inquiries answer the exploration question inquired. A brief strategy for information

investigation was sketched out which will be completely exhibited in chapter 4

19

Chapter 4

Data analysis and presentation

4.0 Introduction Chapter 3 highlighted data gathering technique in order to address the research questions so as to

achieve the research objectives. This chapter will discuss the findings of the study. Findings of an

analytical survey will be discussed in this chapter and the results from inquires made. Impact of the

variables were analyzed and presented on pie charts to clearly show their effect on the choice of

adoption of XBRL. This chapter will knock off with a brief summary of the findings.

4.1 Data Findings and Interpretation It emerged from the data findings that the variables postulated had a greater contribution to why

Zimbabwe has not yet adopted XBRL for financial reporting. It is evident that the global

technological environment is quickly changing and hence the need to move with the change. From

the study, it was found out that level of awareness of the XBRL technology was low hence why

companies have not yet adopted the technology.

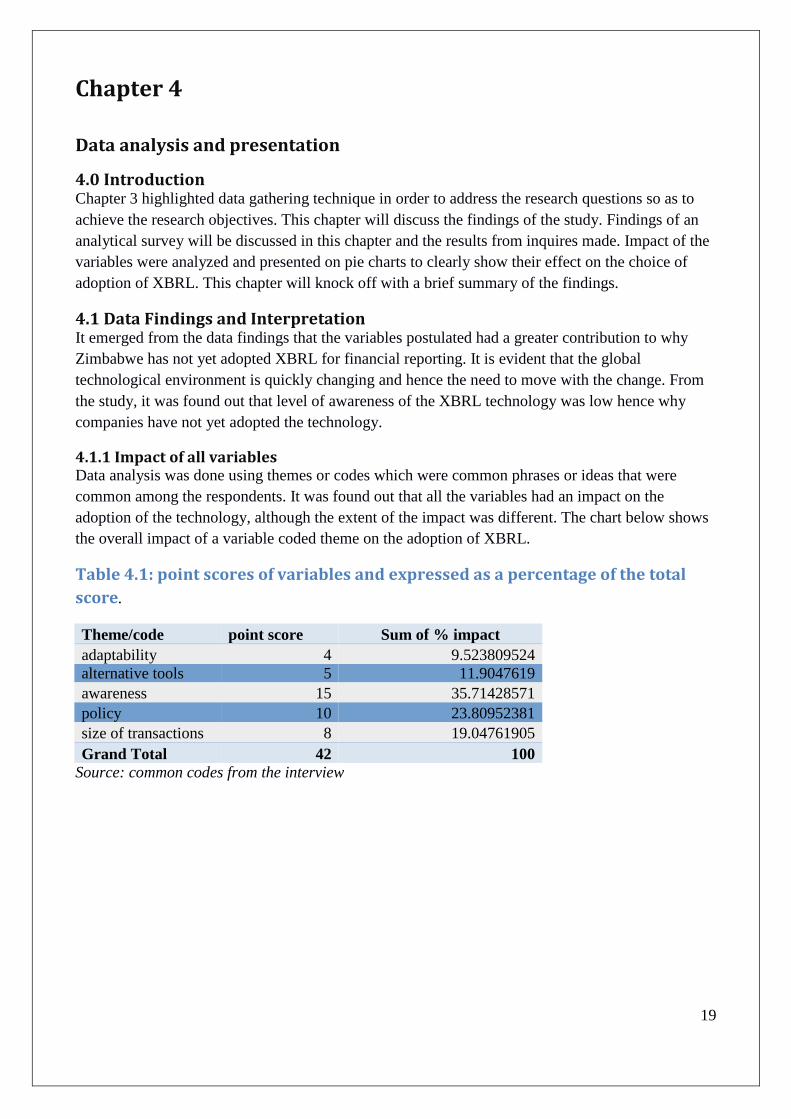

4.1.1 Impact of all variables Data analysis was done using themes or codes which were common phrases or ideas that were

common among the respondents. It was found out that all the variables had an impact on the

adoption of the technology, although the extent of the impact was different. The chart below shows

the overall impact of a variable coded theme on the adoption of XBRL.

Table 4.1: point scores of variables and expressed as a percentage of the total

score.

Theme/code point score Sum of % impact

adaptability 4 9.523809524

alternative tools 5 11.9047619

awareness 15 35.71428571

policy 10 23.80952381

size of transactions 8 19.04761905

Grand Total 42 100

Source: common codes from the interview

20

figure4.1: percentage impact of all variables on the decision on adopting

Adoption is mainly dependent upon awareness. If users, investors, preparers and reviewers are

aware of the technology and its advantages, there is more likely to be positive towards the reaction

of whether to adopt or not. Awareness has the greatest impact on adoption and implementation than

other variables. It was found out that awareness level was very low. Hence the reason why it has not

yet been adopted.

4.1.2 Where there is awareness In order to critically analyze each variable percentage impact on decision to adopt. In circumstances

where the profession of accountancy is all aware of the technology as it was noted that it is the duty

of accountants to implement XBRL as a tool for financial reporting rather than sticking to the old

culture. When awareness was excluded as a variable that caused the reason for not adopting was

excluded, it was found out that policy implementation would be the primary factor that would result

in firms adopting XBRL. This effect is depicted in the figure and table below where the percentage

impact of policy would be at least 37%.

Table 4.2: percentage impact of variables where rate of awareness is high Theme/code % impact of the variable

adaptability 14.81481481

alternative tools 18.51851852

policy 37.03703704

size of transactions 29.62962963

Grand Total 100

Source: common codes from the interview

Sum of score

adaptability

alternative tools

awareness

policy

size of transactions

21

Figure 4.2: impact of variables where the level of awareness is high Policy implementation would force firms to adopt XBRL. From the literature review it was seen

that most companies and countries which had adopted XBRL was because it had been mandated by

the stock exchange commission or the revenue authority. Where there is no implementation firms

will be reluctant to adopt the reporting language, hence the case for Zimbabwe. Companies will

only adopt XBRL, in the case that there is already awareness, when the Zimbabwe revenue

authority has mandated the companies to report real time on-line rather than periodically or in the

case that the stock exchange committee mandates every listed company to report using XBRL for

easy data analysis.

4.1.3 Overlooking other tools Arguments may be made on the reason to adopt when there are already available tools which are

said to efficient enough instead of incurring more costs in the implementation of a new system.

From the argument in chapter 2, it was found out that from all the shortfalls of other tools, for

example using Portable Document Format (pdf) or hyper markup language (HML) for on-line

reporting, XBRL has many advantages over the reporting tools currently used in Zimbabwe. In

order to justify the study, the variable availability of other tools was excluded in order to critically

identify the reason why XBRL has not yet been implemented. The outcome is depicted in the figure

and chart below where it was found out that policy implementation would only result in a much

greater reason why firms have not yet adopted XBRL. Policy implementation would only drive or

force firms to implement XBRL. Size of transactions would also force the adoption of XBRL as

reported by China that it mainly benefits companies in relation to enterprise resource planning

(ERP) if the size of their transactions are large and need regular updating of the data in the system.

If the size of transactions is small or infrequent, it will tend to be costly to implement XBRL. Hence

the reason why Zimbabwe has not had the eagerness to adopt the reporting language as capacity

utilization is still low since economy failure and financial crisis of 2002 up to 2008 as compared to

China, Europe and the USA.

Total

adaptability

alternative tools

policy

size of transactions

22

Table 4.3: % impact in the case where users acknowledge the pitfalls of other tools Theme/code % impact of the variable

adaptability 18.18181818

policy 45.45454545

size of transactions 36.36363636

Grand Total 100

Source: common codes from the interview

Figure 4.3: impact of the variables on adoption in the case where level of awareness is high and other tools are seen as inefficient.

Overally, it can be critiqued that where there is no awareness all other variables will be nullified or

invalid as there cannot be policy implementation without awareness, resistance to change without

the change or new technological improvement being known. This is the reason why analysis was

further made in the case that there is awareness so as not to overshadow other variables. Research

has found out that when individual are resistant to change as they may feel insecure they take the

avoidance approach where they may pretend as if they do not know about the change that is

occurring or appear to be unknowledgeable or uneducated about the subject. XBRL is an up surging

technology which raises concern and the bone to contention on the possible reason of overlooking

the technology when it has so many merits that could benefit the capital market, if not the whole

business sector due to effective and efficient financial reporting.

Total % impact

adaptability

policy

size of transactions

23

4.2 Other findings in relation to research questions In addressing research question on the benefits of the reporting language over other tools, literature

survey showed that it has been so far by the early implementers of XBRL as beneficial to corporate

reporting and hence the reason why the consortium has still been updating regularly the technology,

supporting the current implementers and users, training all interested parties for a little fee on how it

works and as well encouraging companies to adopt XBRL, mostly chartered accountants to know

how it works and its benefits.

It was noted that no technical knowledge is required in order to be acquainted with XBRL, as some

perceive it as so difficult to learn even to use. Use of tagging data items makes it much easier for a

financial statement preparer to prepare the financial statements in the case where too many items

will have to be prepared. Keying and tagging present data in the easiest way as there is no need to

know the location or destination where the data has to be but the fact that keying determines the

location the location of data that is where it should be and where one who queries the data will find

the information.

Integration of XBRL technology into the company accounting and reporting system will produce

the actual benefits. This can be manifested in the reduction in current manual efforts in data

gathering, grouping and recording in order to prepare the financial statements. Too much

documentation of transaction which may carry so much diverse account names may present a

problem and susceptibility to error when it comes to the issue of auditing the statement and

controls. XBRL improves the auditability of the financial statements which are in XBRL and the

process can be quick hence effective as manual documentation will be meager than when the full

system is not keyed or coded electronically.

Some arguments for not adopting and overlooking the reporting language were that it was perceived

that it was costly to implement. However, it can be further critiqued that implementation is just like

an investment which tend to appear costly in the first year of capitalization of the investment but

yields better sub-sequentially. It was argued by the AICPA that there are certainly misconceptions

about XBRL in regard to resources required when implementing XBRL. Its initial costs can be so

much outweighed by its benefits. It can be implemented for cost accounting, performance

measurement, analysis and decision making purpose in addition to real time financial reporting.

In addressing research question on whether the reporting language is an answer to financial

reporting and a contribution to the accountancy profession, it was found out that XBRL could be

beneficial to the chartered accountants as preparers of financial statements and also that it proves to

be effective and efficient way of financial reporting as compared to other forms or tools for

financial reporting.

XBRL reduces time spent manually finding and preparing information. A fully automated

information exchange also improves the data quality; this is also beneficial to creditors, analysts and

investors. It also results in fewer burdens to the accountant from the pressure by management to

issue out the financial statements as there is quick preparation of data, quick data analysis and

redistribution to management and stakeholders for better informed decision making use.

24

Standardized information formats would assist chartered accountants in gathering, managing and

reporting financial information accurately. As the technology was developed by a chartered

accountant, he saw the need which was there to develop a new tool that would overcome the

anomalies in data interpretation and updating from the use of other system. The motives in

development of XBRL are the benefits for the accountants in effective and efficient financial

reporting and the accountancy profession. Some arguments against the profession were made

previously in the need for financial reporting when the market is assumed to be efficient by the

efficient market hypothesis and the burden on the investor or user to go through statements which

may be nearly a hundred or more of pages. These critiques however can be made void with the

implementation of XBRL as it results in no need for an investor to go through the whole statement

but query for a specific set of data or data item. The AICPA argued that the accounting profession

and more so those it serve would benefit from the standardization of data.

4.3 Summary This chapter concentrated on the findings of the research. From the opinions gathered and the

literature survey it was found out that XBRL implementation was most dependent upon awareness

followed by mandating a policy. Furthermore, it was instituted that XBRL would positively impact

on the profession of accountancy and benefit accountants in-terms of preparing and analyzing

financial statements. The outcome of the research was that no firm or company in Zimbabwe is

using XBRL due to lack of awareness and the fact that it is not mandated although to some extent it

was influenced by the fact that people are resistant to change. From the opinions gathered and the

literature survey all the research questions were fully addressed. Conclusion of the findings and the

recommendations are set in the next chapter.

25

Chapter 5

Conclusion and Recommendations

5.0 Introduction

This chapter consists of the overall conclusions to the study and recommendations. It is scheduled

as follows. Firstly conclusions from the findings laid out in chapter 4 followed by the insight of the

study, that is, the critical brainstorm of the study. After that follows the fore sight which is the

prudent vision of the future in relation to the study. The chapter knocks off with the

recommendations.

5.1 conclusion of the study

Adoption of XBRL has been on rise in countries such as the UK, USA, China, India and also

African countries in the Eastern such as Israel. In the Southern African countries, it was indicated

from the surveys by other researchers that South Africa had traces of evidence of adoption although

SAICA highlighted the fact that awareness level was very low and need to educate so as to give

awareness to the stakeholders or those served by the profession of accountancy.

The growing use of internet and changes in technology has since affected financial reporting

although other companies or firms have not yet been affected especially small firms. To reach all

the stakeholders, nearly most companies have a website were all the information about them is

found including their reports. Some even provide the figures of earnings per share on their website

for the investors or potential investors to see the return the company gives and how much it is

performing in the overall market against competitors. Also the Zimbabwe stock exchange provides

updates online on the earnings per share of companies. Use of XBRL makes it simpler for

companies to update their information reported. In order to avoid anomalies in updating, inserting

and delete the data, XBRL was developed to reduce human interference which results in errors. This

is mainly the reason why it was developed, has been implemented by some, mandated by some

regulatory authorities and continues to be encouraged to be adopted by most that have been using

the reporting language. The benefits are not only for the user or for data analysis, findings also

show that it results in an increase in return on investment as the costs will outweigh the benefits and

also increases the earnings per share of the investors. Financial reporting hence does not become a

cost to the company but a competitive advantage.

XBRL adoption and implementation in Zimbabwe showed that there were no companies which had

yet adopted the reporting language as a tool for financial reporting. Several variables were the

reasons why there had not been the implementation of XBRL to date in Zimbabwe although the

XBRL consortium has reported that there was a positive reaction globally.

5.2 Insight of the study

Of all the reasons pointed out, it can be concluded that awareness was the main reason why firms

had not yet adopted the reporting language regardless of the efforts by XBRL consortium to raise

levels of awareness globally. Level of awareness in Zimbabwe was found out to be very low of

which those with the knowledge assumed it to be a complex technology to even start to learn about.

Some perceived it as unnecessary for the implementation of XBRL mainly because of effect of

resistance to change. ZIMRA introduced fiscal registers in 2011 but is still facing problems since

26

the tax collectors are still being prejudiced. In a report by Newsday (13 may 2016) it was reported

that ZIMRA was advising users of the fiscal register to link their fiscal devices to ZIMRA. Need for

electronic real time update by ZIMRA shows the importance of real time reporting from the

companies by the regulatory authority, hence the need to know about XBRL.

Where there is resistance to change, people often chose avoidance. This was seen by the researcher

as the reason why it was pointed that lack of awareness was the main reason why companies in

Zimbabwe had not yet adopted XBRL. Adverse behavioural reactions have geared the resistance to

the adoption of the new technology. Where there is resistance because of fear of unknown, failure;

technology; loss of status or job, biases and natural resistance, it is management's duty to

communicate the reasons or benefits of the change to the workers so that change is not resisted. It is

crucial to be cautious about the manner in which change is introduced during implantation as it may

only result in negative reaction by the users. However it is noted that if top management is

characterised of older individuals not educated about the technology, they are the ones who resist

the change and it is the duty of those who are young, educated and comfortable to technological

change to implement it, thus young chartered accountants.

5.3 Foresight of the study

Technology is rapidly changing. IFRS formulated taxonomy for XBRL and has since supported the

use of the reporting language. It can be predicted that IFRS in the future may mandate financial

reporting in XBRL in order to achieve uniformity, efficient and effective financial reporting

globally as since some institutes of chartered accountants, for example AICPA, SAICA, CICA to

mention a few have advised the use of the reporting language. It is probable that XBRL will either

be optional or mandatory form of listing on the stock exchange, where optional most firms will opt

because of the rising use of internet and need to reach a diverse range of users or stakeholders

especially potential investors. Continued development and advancement of XBRL indicates that

benefits will continue to grow.

5.4 Recommendations

It is therefore advisable from the above analysis that accountants should expand their knowledge on

XBRL as it shows that it shall or has a greater impact on the profession and financial reporting in

order to improve the reporting process. Accountants need to understand the degree of human

interference in the data access, validation and analysis facet of their company or clients' reporting

process so as to make informed recommendations in setting up XBRL in accounting soft wares and

also information processing systems as proposed by Microsoft corporate.

It was noted that for the capital market to benefit from the claimed merits of XBRL, it should be

mandated by the regulatory authorities such as ZIMRA or Zimbabwe Stock Exchange commission

for every listed company to do real time online reporting of their trading results.

For the academia or student accountants, there should be the efforts in gaining knowledge about

XBRL as suggested by Elliot and Elliot (2008), as this creates a competitive advantage in gaining

knew uncommon knowledge.

It is to be further researched on technological change and financial reporting, how the changes are

affecting financial reporting and actions taken by financial preparers or reporters

27

Reference list

Ahrendt, B 2009, ''What Are The Costs And Benefits Of XBRL In The Financial Services

Industry?''Master Thesis Economics &Informatics. P.15-17 Available At

Https://Thesis.Eur.Nl/Pub/6405/6405-Ahrendt.Pdf Accessed On (21/04/16)

AICPA, ‘Return On Investment On XBRL’, Journal Of Accountancy,June 2007

Available At Http://Www.Journalofaccountancy.Com/Issues/2007/Jun/Roionxbrl.Html Accessed On

15/04/2016

Kernan K, ’XBRL Around The World’, Journal Of Accountancy AICPA, October 2008

Available At Http://Www.Journalofaccountancy.Com/Issues/2008/Oct/Xbrlaroundtheworld.Html

Accessed On 15/04/2016

Definition of XBRL available at http://www.xbrl.org.tw/ accessed on (13/04/16 13:00)

Integrating XBRL Into Your Financial Reporting Process (October 2011). Oracle white paper

available at http://www.oracle.com/us/solutions/integrat-xbrl-financial-repors-wp-518965.pdf

Benefits and Potential Uses of XBRL available at

http://www.aicpa.org/InterestAreas/FRC/AccountingFinancialReporting/XBRL/Pages/BenefitsandP

otentialUsesofXBRL.aspx

Harvard University Library 2016, Harvard Graduate School of Education. Available at

http://guides.library.harvard.edu/literaturereview accessed on (20/04/16 14:35).

Hannon, H 2006, ''Does XBRL Cost Much'', Strategic Finance available at

http://www.xbrl.org/ViewsOnXBRL/cost%20tooMuch_3623.pdf accessed on (21/04/16 14:5

Hodge, F.D, Kennedy J. J, and Maines L. L, (2004) ''Does Search‐Facilitating Technology Improve

the Transparency of Financial Reporting?''. The Accounting Review: July 2004, Vol. 79, No. 3, pp.

687-703 available at https://www.sec.gov/news/press/4-515/4515-6art.pdf accessed on (21/03/16

15:25)

Markelevich, A, Shaw, L, &Weihs, H 2015, 'The Israeli XBRL Adoption Experience', Accounting

Perspectives, 14, 2, pp. 117-133, Business Source Premier, EBSCOhost, viewed 29 April 2016.

Available at

http://web.a.ebscohost.com/ehost/pdfviewer/pdfviewer?vid=3&sid=1f7efcc0-d10f-4951-acc8-

fc0fe0fcfc57%40sessionmgr4002&hid=4114

Ju-Chun, Y, &Tawei, W 2015, 'The Association between XBRL Adoption and Market Reactions to

Earnings Surprises', Journal Of Information Systems, 29, 3, pp. 51-71, Business Source Premier,

EBSCOhost, viewed 4 May 2016.

Janvrin, D, Pinsker, R, &Mascha, M 2013, 'XBRL-Enabled, Spreadsheet, or PDF? Factors

Influencing Exclusive User Choice of Reporting Technology', Journal Of Information Systems, 27,

2, pp. 35-49, Business Source Premier, EBSCOhost, viewed 29 April 2016.

28

Ju-Chun, Y, &Tawei, W 2015, 'The Association between XBRL Adoption and Market Reactions to

Earnings Surprises', Journal Of Information Systems, 29, 3, pp. 51-71, Business Source Premier,