timeseries

TRANSCRIPT

School of Computing, Engineering and Mathematics

TIME SERIES ANALYSIS AND FORECASTING OF THE UK

EXPORT

Khoa Truong

May 2015

Declaration

I declare that no part of the work in this report has been submitted in support of an application

for another degree or qualification at this or any other institute of learning.

Khoa Truong

i

Acknowledgements

First of all, I would like to express my deepest gratitude to my supervisors Dr Alexey Chernov and

Dr Laurie Smith who have given me generous guidance and support till the end of this project. I

am very thankful and grateful to have them as my supervisor and motivational support.

Beside my supervisors, I am highly indebted to all the academic lecturers who have given me an

opportunity to explore mathematics and an unforgettable university experience.

I would like to express my gratitude to my mother who has always been there for me and given

me financial support as well as unequivocal encouragement through out my life, for which, no

matter what and how much I do, it would never be enough to return the favour.

Finally, I am very proud to be a part of Brighton University community. As a student here, I am

very thankful to those sta↵ who has provided me equipments, facilities and services to support in

carrying out this project.

ii

Abstract

Trade performance is considered to be an important element of UK GDP growth of which export

is an essential part. The aim of this paper is to give empirical insight into various forecasting

methods of modelling the UK export series based on time series analysis.

Supervisor: Dr Alexey Chernov

iii

Contents

1 INTRODUCTION 1

1.1 Problem . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

1.2 Sampling and Series analysis . . . . . . . . . . . . . . . . . . . . . 3

2 THEORETICAL CONTEXT 4

2.1 Univariate time series - linear models . . . . . . . . . . . . . . 5

2.1.1 ARIMA(p,d,q) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

2.1.2 Dampen component on Exponential smoothing . . . . . . . 6

2.1.3 Linear models summary . . . . . . . . . . . . . . . . . . . . . . . 10

2.2 Univariate time series - nonlinear models . . . . . . . . . . . 10

2.2.1 Introduction to ARCH and GARCH . . . . . . . . . . . . . . . 11

2.3 Multivariate time series analysis . . . . . . . . . . . . . . . . . . 13

2.3.1 Introduction to VARX(p,s) . . . . . . . . . . . . . . . . . . . . . 13

2.4 Forecast Accuracy Instruments . . . . . . . . . . . . . . . . . . . 14

iv

3 LITERATURE REVIEW 16

3.1 UK Popularity Export Forecast Technique . . . . . . . . . . 17

3.2 Existence time series analysis on export application . . 18

4 METHODOLOGY 22

4.1 Export series regression analysis . . . . . . . . . . . . . . . . . . 23

4.2 Models in application . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

4.2.1 Linear regression with Autoregressive errors . . . . . . . . . . 25

4.2.2 VAR(3) and VARX(4,1) . . . . . . . . . . . . . . . . . . . . . . . 30

4.2.3 A(1,1,0), A(0,1,1) and A(1,1,1) . . . . . . . . . . . . . . . . . . 37

4.2.4 Exponential smoothing . . . . . . . . . . . . . . . . . . . . . . . . 44

4.2.5 AR(1)-GARCH(1,2) . . . . . . . . . . . . . . . . . . . . . . . . . . 47

4.2.6 Examing models goodness of fit . . . . . . . . . . . . . . . . . 51

5 FORECAST AND ACCURACY ANALYSIS 52

5.1 Forecast formulation . . . . . . . . . . . . . . . . . . . . . . . . . . . 53

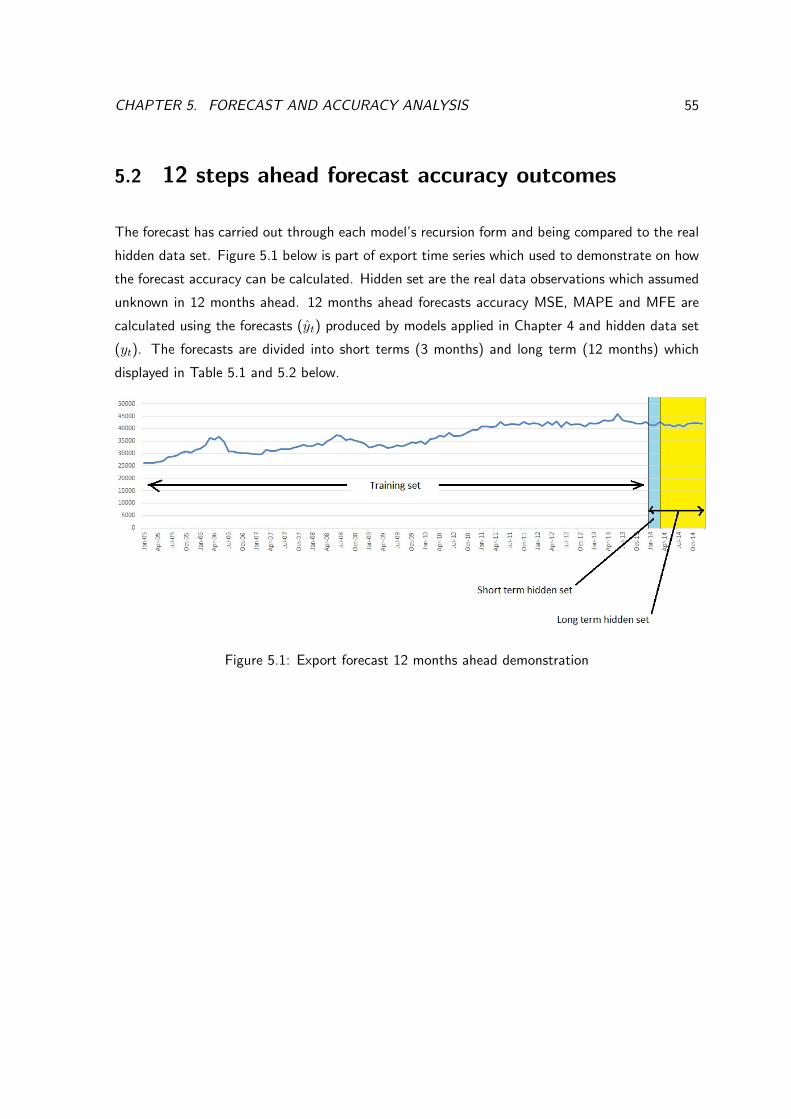

5.2 12 steps ahead forecast accuracy outcomes . . . . . . . . . 55

5.3 Accessing models validation . . . . . . . . . . . . . . . . . . . . . 62

5.3.1 Cross validation . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62

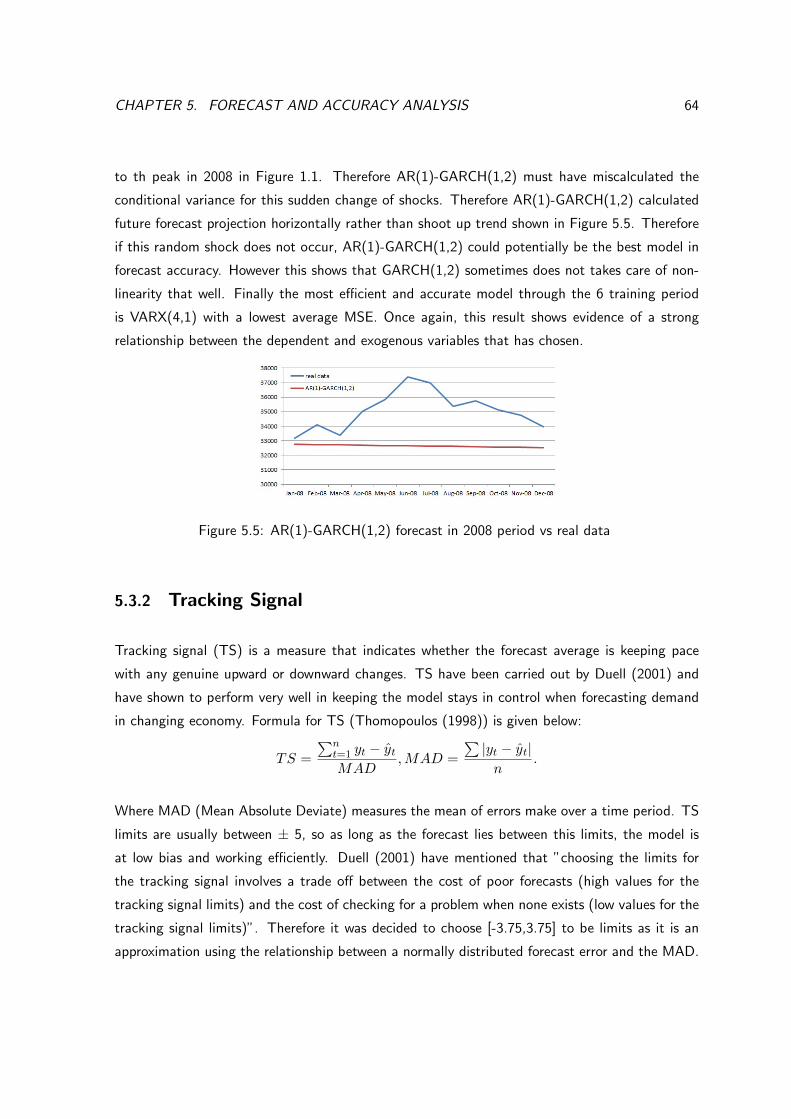

5.3.2 Tracking Signal . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64

5.3.3 Prediction Interval . . . . . . . . . . . . . . . . . . . . . . . . . . . 67

v

6 LIMITATION AND EXTENSION 70

7 CONCLUSION AND SUGGESTIONS 72

8 EVALUATION 74

9 REFERENCE 75

9.1 Books . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75

9.2 Journals . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 76

9.3 Websites . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77

9.4 Lecture notes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77

9.5 Thesis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77

9.6 Report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 78

9.7 Variables and Sources . . . . . . . . . . . . . . . . . . . . . . . . . . 78

10 APPENDIX 79

10.1 Modelling concepts . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79

10.1.1 ACF and PACF . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79

10.1.2 Stationary Time Series and White Noise . . . . . . . . . . . . 80

10.1.3 Parameter estimator . . . . . . . . . . . . . . . . . . . . . . . . . 80

10.1.4 Model Selection Through Criteria . . . . . . . . . . . . . . . . 80

10.2 SAS Syntax . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 81

vi

List of Figures

1.1 The UK export 14 years export (GBP milion) . . . . . . . . . . . . . . . . . . . 3

2.1 Damp e↵ect on Holt’s model . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

2.2 Damp a↵ect on Pegels exponential smoothing . . . . . . . . . . . . . . . . . . . 9

3.1 India meat export time series . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

3.2 Four di↵erent types of rice time series . . . . . . . . . . . . . . . . . . . . . . . 20

3.3 ANN vs exponential smoothing . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

4.1 UK export time series regression analysis . . . . . . . . . . . . . . . . . . . . . . 23

4.2 UK export 95% limits plot . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

4.3 UK export time series with outliers removed (red line) . . . . . . . . . . . . . . . 25

4.4 Identify autoregressive for the residuals . . . . . . . . . . . . . . . . . . . . . . . 26

4.5 MLE parameter estimations and model fitness . . . . . . . . . . . . . . . . . . . 26

4.6 Diagostics check for residuals in TR-AR(2) . . . . . . . . . . . . . . . . . . . . . 27

4.7 Export price (index points) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

vii

4.8 Identify autoregressive for the residuals of export against export price . . . . . . 28

4.9 MLE parameter estimations and model fitness . . . . . . . . . . . . . . . . . . . 29

4.10 Diagnostic checks for residuals in PR-AR(2) . . . . . . . . . . . . . . . . . . . . 30

4.11 Residuals diagnostic check . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

4.12 Model VAR(3) fitness diagnostics check . . . . . . . . . . . . . . . . . . . . . . 32

4.13 MLE parameter estimates for VAR(3) . . . . . . . . . . . . . . . . . . . . . . . 33

4.14 Exchange rate 1 Pound to USD (left) labour cost (right) . . . . . . . . . . . . . 34

4.15 Identifying rank r and exogenous variable association test . . . . . . . . . . . . . 34

4.16 Model VARX(4,1) fitness diagnostics check . . . . . . . . . . . . . . . . . . . . 35

4.17 MLE parameter estimates for VARX(4,1) . . . . . . . . . . . . . . . . . . . . . . 36

4.18 Correlogram of adjusted UK export series . . . . . . . . . . . . . . . . . . . . . 37

4.19 DF test non-stationary series . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

4.20 DF test for di↵erenced series . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

4.21 Correlogram of di↵erences series . . . . . . . . . . . . . . . . . . . . . . . . . . 38

4.22 Maximum likelihood estimations for A(1,1,0) (top), A(0,1,1) (middle), A(1,1,1)

(bottom) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

4.23 Residuals diagnostic plots (top: normality plots, middle: scatters of residuals,

bottom: corolelograms) for A(1,1,0) . . . . . . . . . . . . . . . . . . . . . . . . 41

4.24 Ljung-Box statistic check residuals for A(1,1,0) . . . . . . . . . . . . . . . . . . 41

4.25 Residuals diagnostic plots (top: normality plots, middle: scatters of residuals,

bottom: corolelograms) for A(0,1,1) . . . . . . . . . . . . . . . . . . . . . . . . 42

viii

4.26 Ljung-Box statistic check residuals for A(0,1,1) . . . . . . . . . . . . . . . . . . 42

4.27 Residuals diagnostic plots (top: normality plots, middle: scatters of residuals,

bottom: corolelograms) for A(1,1,1) . . . . . . . . . . . . . . . . . . . . . . . . 43

4.28 Ljung-Box statistic check residuals for A(1,1,1) . . . . . . . . . . . . . . . . . . 43

4.29 Variation in Tt

from equation (2.9) . . . . . . . . . . . . . . . . . . . . . . . . . 45

4.30 Tt

equation (12) re-modelling using Hot’s winter seasonal . . . . . . . . . . . . 47

4.31 Heteroscedasticity test for the UK export time series . . . . . . . . . . . . . . . 47

4.32 Maximum likelihood parameter estimates and diagnostic check for mean equation

AR(1) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48

4.33 MLE for parameters and diagnostic check for AR(1)-GARCH(1,2) . . . . . . . . 49

5.1 Export forecast 12 months ahead demonstration . . . . . . . . . . . . . . . . . . 55

5.2 Models’s forecast for export price; VAR(3) (top left), VARX(4,1) (bottom left),

tradingeconomic.com’s model (bottm right) and real export price observations

(top right) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

5.3 Tradingeconomics.com forecast of export (black line) . . . . . . . . . . . . . . . 60

5.4 graphical image of forecast models vs original observations . . . . . . . . . . . . 61

5.5 AR(1)-GARCH(1,2) forecast in 2008 period vs real data . . . . . . . . . . . . . 64

5.6 Tracking signal plot . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65

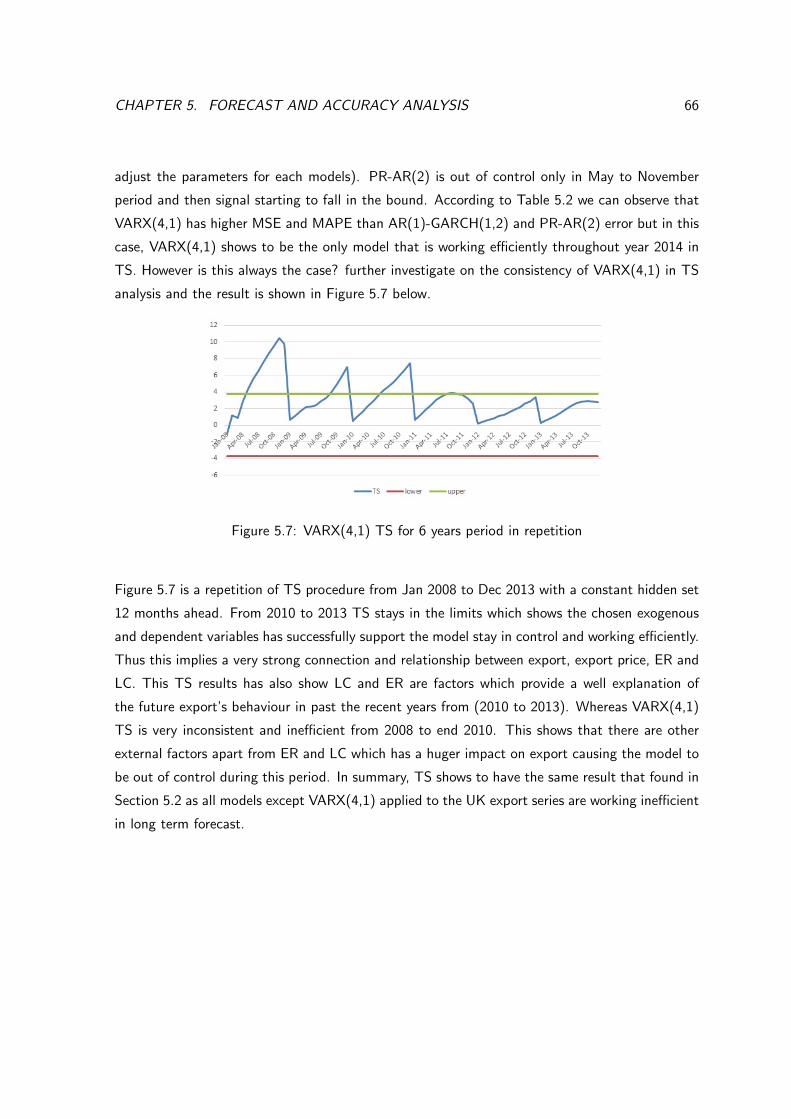

5.7 VARX(4,1) TS for 6 years period in repetition . . . . . . . . . . . . . . . . . . . 66

5.8 Models Prediction intervals . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68

5.9 AR(1)-GARCH(1,2) predicted volatile . . . . . . . . . . . . . . . . . . . . . . . 69

ix

7.1 VARX(3,1) forecast from Jan-15 to Dec-15 . . . . . . . . . . . . . . . . . . . . 73

x

Acronym Terminology

ARIMA Autoregressive Intergrated Moving Average

ES Exponential Smoothing

DP Damp Pegels

DT Damp Trend

ER Echange Rate

GARCH(p,q) Geralises Autoregressive Conditional Heteroskedasticity order (p,q)

PI Prediction Interval

HW Holt’s Winter

TR-AR(p) Time Regression Autoregressive order p

PR-AR(p) Price Regression Autoregressive order p

TA Trending Adjusted

TS Tracking Signal

VARX(p,s) Vector Autoregressive with Exogenous order p and s

LC Labour Cost

DF Dickey Fuller

ANN Artificial Neuron Network

SBC Schwarz Information Criteria

MLE Maximum Likelihood Estimator

MSE Mean Square Error

MFE Mean Forecast Error

ACF Autocorrelation Function

PACF Partial Autocorrelation Function

Table 1: List of abbreviation

xi

Chapter 1

INTRODUCTION

1.1 Problem

The world population is growing rapidly on a yearly basis and it is expected that demand for goods

will also increase proportionally, which implies that more resources in the UK are required in order

to supply the amount of goods to meet this demand. Ine�cient resource allocation is a factor

that could cause problems to arise as many exporters are unable to predict the uncertainty of the

ever changing commercial market. Nowadays, people can change their choices abruptly and this

can be very unpredictable, presenting one with a degree of uncertainty that can sometimes cause

exporters to miss the requirements of the market within the UK; causing them to misdirect their

supply and waste resources unnecessarily.

In the present, forecasting export o↵ers the means to best improve the decision-making and plan-

ning processes. The ability to forecast will grant firms to estimate and detect any alteration in the

commercial market for products from the UK since supply must meet demand. A well-educated

response to the market based upon statistical analysis will prove to be more profitable than simply

guessing. Meeting the future demand will lead to an increase in export, but access to accurate

forecasting calls for di↵erent methods to be applied on real time data.

1

CHAPTER 1. INTRODUCTION 2

We will explore several statistical methods to discover the optimum model to forecast the UK

export time series, primarily by reviewing various number of popular time series methodology

and claim factors e↵ecting the firms’s ine�cient resource allocation. The paper will go on to

fit the most suitable models to the series and finally analyse the accuracy of the forecasting

techniques. These methods are based on multivariate and univariate linear and non-linear time

series analysis, which have been widely researched to show a good fit. The Non-linear generalises

autoregressive conditional heteroskedasticity of order (1, 2), Regression autoregressive error with

exogenous of order (2) and Vector Autoregressive with exogenous variables order (4,1) have

produced the best forecast for the next 12 months. However to an extent, these models are

invalid in certain circumstances due to its inability to produce a satisfactory forecast, whereas

other models which have produced inaccurate forecasts for the next 12 months appears to pass all

these validations. This will be discussed in-depth and additional information will be comprehend

to support firms decision making and techniques to determine the sustainability of models that can

be employed on an export series; in order to produce the most su�cient and satisfying forecast.

Three measurements have been employed to determine the ”goodness of fit” for the model and

forecast accuracy and they are: MSE (mean square error), MFE (mean forecast error) and MAPE

(mean absolute percentage error).

CHAPTER 1. INTRODUCTION 3

1.2 Sampling and Series analysis

Figure 1.1 is the UK export series plot from the past 14 years spanning the period from January

2000 to December 2014 (measured in million GBP). The series contains a sample of monthly

data of 180 observations. During the period of January 2000 to January 2006 and of January

2009 to December 2014 illustrate the growing was stable within export. There was a high peak

around 2006, which partly relates to the Chinese economic boom, resulting in a huge increase

in shipments of machinery and transport equipment according to Department For International

Development (2011). This had a direct e↵ect on the UK export since its total export accounts

of 40% of machinery (tradingeconomic.com). Up until July 2010, there were two big drops in

export, one in October 2009 and another in July 2007 because of the UK deepest recession in the

history that resulted in huge jobs loss (BBC NEWS (2015)), which was also partly due to the EU

financial crisis. Since EU is the UK’s main export partner, this crisis has left the EU consumer’s

demand to fall, which led to a decline in the UK export. This incident has initiated an unstable

growth period for the UK export business. It is clear to see that the UK export has an upward

non-seasonal trend over the 14 years and does not fluctuate between each month. This shows a

strong relationship between time and UK export, which suggests that time series modelling can

be most appropriate in forecasting the UK export series.

Figure 1.1: The UK export 14 years export (GBP milion)

Chapter 2

THEORETICAL CONTEXT

A time series is a set of data observations varies in time. Time series analysis deals with the

methods of analyzing past data and then projecting the data obtain estimates of future values.

Time Series Analysis have been widely used nowadays especially in financial market such as

Economics variables, stock and exchange rate..etc. This chapter will be a brief description of

time series analysis and theory behind methods of modeling a time series which will be applied

in Chapter 4. Please see appendix for modelling concepts which covering these topics below if

necessary:

• ACF and PACF

• Stationary and white noise

• Parameter estimator: Maximum Likelihood Estimator (MLE)

• Model selection through criteria: Schwarz Information Criteria (SBC)

4

CHAPTER 2. THEORETICAL CONTEXT 5

2.1 Univariate time series - linear models

2.1.1 ARIMA(p,d,q)

For a linear univariate time series popular methods for modelling are Autoregressive (AR), Moving

Average models (MA) and a combination of both ARIMA introduced by Box and Jenkins in 1960.

The general idea of ARIMA(p,d,q) is modelling a stationary time series using the past values of

order p and past error terms of order q and d is the number of di↵erencing required to achieve

stationarity for a time series. The formal mathematical form of the ARIMA(p,d,q) (or often called

A(p,d,q)) model is given below in the form back shift operator:

Zt

= µ+✓(B)

�(B)✏t

, Zt

= (1�B)dyt

(2.1)

where ✓(B) =(1�P

q

q=1 ✓qBq) is a polynomial in B of order q and �(B)= (1�

Pp

p=1 �pBp) is a

polynomial in B of order p. Bnyt

= yt�n

or Bn✏t

= ✏t�n

and if p=q=0 then ✓(B) = �(B) = 1.

✏t

is a white noise process independent and identical distributed (i.i.d), ✏t

s N(0,�2)

Dickey Fuller test

Autocorrelation measures the correlation between some variable yt

, the lagged counterpart yt�1,

period and itself. A stationary time series is a conditional requirement in order to apply ARIMA

modelling, the most common way of detecting stationarity is through the observation of autocor-

relation. What we are looking for is if autocorrelation is decaying to zero exponentially fast or

where most lags lies between standard deviation but this approach is sometimes not appropriate

when dealing with data that is very random and messy. However Mahadeva and Robinson (2014)

have clear demonstrate on a unit root test namely Dickey Fuller test when dealing with messy

data and to help building model, this test following the null hypothesis process where a series can

be assumed to be stationary if it does not have a unit root. Given an AR(1) process:

yt

= � + �yt�1 + ✏

t

The null hypothesis process relies upon the equation coe�cient � where if |�| = 1 then the series

is non stationary and if |�| <1 then the series is in fact stationary. However, the problem here is

CHAPTER 2. THEORETICAL CONTEXT 6

Yt

and Yt�1 under the null hypothesis are non-stationary and when a times series is non-stationary

the normal central limit theorems apply so it is not possible to just readily test on � using an

ordinary t-test. Therefore, by taking Yt�1 from RHS and LHS of the AR(1) equation:

yt

� yt�1 = � + (�� 1)y

t�1 + ✏t

�yt

= � + �yt�1 + ✏

t

Now we have a di↵erenced dependent variable on the LHS and lag 1 on the RHS, so a series

is non-stationary when |�| = 0 and �yt

is then stationary. DF test does not follow a standard

t-distribution so Dickey and Fuller has to tabulate the asymptotic of the distribution. The DF

method is to calculate the t-statistic on � and if t > DF critical value, which then fails to reject

the non-stationarity and thus the method of di↵erencing �yt

has transformed the series to achieve

stationarity.

Extension of AR process

An AR process can be applied to the error term of a Linear Regression model when the residuals are

perceived to be correlated (Tsakiri (2014)). The model can be expressed in a form of regression

with the autoregressive white noise error term:

yt

= �0 + �1x1 + ....+ �i

xi

+ Zt

Zt

=pX

i=1

�p

Zt�p

+ ✏t

, where ✏t

s N(0,�2)

2.1.2 Dampen component on Exponential smoothing

Exponential smoothing arose in the 1950s from the original work of Brown (1962) and Holt

(1960) in time series forecast modelling. Unlike ARIMA exponential smoothing does not require

a stationary time series the method is based on the smoothing process of a series and the forecast

incorporates weighted averages into the methodology. Its method is to decompose the time series

into trend and level in order to predict the future values.

CHAPTER 2. THEORETICAL CONTEXT 7

Damp-Trend Exponential Smoothing (DTES)

DTES is an additive exponential smoothing method as shown below:

Lt

= ↵yt

+ (1� ↵)(Lt�1 + �T

t�1) (2.2)

Tt

= �(Lt

� Lt�1) + (1� �)�T

t�1 (2.3)

yt+h

= Lt

+hX

i=1

�iTt

(2.4)

where Lt

is the level at time t, Tt

is the growth rate at time t and yt+h

is the forecast h step

ahead of time t. An optimum exponential smoothing model (Table 2.1) are mainly depends on

its smoothing parameter 0 ↵ 1 which modifies the time series at each level given time t, 0� 1 trend parameter of time series and 0 � 1 is the autoregressive or the dampen parameter .

Models level trend damping

DT 0 ↵ 1 0< � 1 0< � < 1

Holt 0 ↵ 1 0< � 1 1

Double exponential smoothing (DES) 0< ↵ <1 0< ↵ 1 1

Simple Exponential Smoothing (SES) 0< ↵ < 1 0 0

SES with damped drift 0< ↵ < 1 0 0 < � < 1

SES with drift 0< ↵ < 1 0 1

Random walk with damped drift 1 0 0< � < 1

Random walk with drift 1 0 1

Random walk 1 0 0

Modified exponential smoothing trend 0 0 0< � < 1

Linear Trend 0 0 1

Simple average 0 0 0

Table 2.1: Exponential smoothing models with parameter restrictions

The DTES model has been proven by Flides (2008) with a benchmark that has been di�cult to

beat in empirical studies of forecast accuracy. Holt’s linear exponential smoothing method has

becomes the most popular approach for a trended time series. However, it often found Holt’s

CHAPTER 2. THEORETICAL CONTEXT 8

linear forecast criticised for tending too over forecast a time series in long term. Garder and

Mckenzie (2009, 2010) has addressed this problem by introducing 0< � <1 to modify the trend

component in Holts linear trend method (dampens the trend component) see Figure 2.1 for the

damp e↵ect. Therefore, as � tends toward 0 the dampening e↵ect becomes more pronounced and

reduces the forecasted values. Forecasts h steps ahead in equation (2.4) is now depending upon

the damping parameter and growth rate when 0< � <1 whereas if � =1 then the method turns

into Holts (linear) exponential smoothing where forecasting is now dependent on the series growth

rate which will produce just a straight line forecast. Garder and Mckenzie came with a conclusion

that a damped trend model is a good approximation to a linear trend at short lead-times and is

better for longer ones because the linearity must eventually break down.

Figure 2.1: Damp e↵ect on Holt’s model

Damp-Pegels Exponential Smoothing (DPES)

Having been motivated by the damp � parameter in its improvement for accuracy, Taylor (2003)

introduced damp Pegels exponential smoothing method. The method is modelling a time series

in multiplicative way but includes a dampening term, which leads to more robust forecasting

performance. DPES can be written in form below:

Lt

= yt

+ (1� )(St�1R

t�1�) (2.5)

Tt

= �St

St�1

+ (1� �)R�

t�1 (2.6)

CHAPTER 2. THEORETICAL CONTEXT 9

yt+h

= St

RPh

i=1 �i

t

(2.7)

Where Lt

is the level of the time series at time t, St

6= 0 and Tt

denotes the growth rate of

the time series at time t and yt+h

is the forecast h steps ahead. Taylor also has the same view

as Garder and Mckenzie for adding � to PES for believing that PES over forecasts in most of

the time series. If 0 < � < 1, the multiplicative trend is damped and the forecasts approach

an asymptote shown on Figure 2.2 as � tends to 0, the dampened component becomes more

powerful and e↵ectively pulls the forecast down significantly.

Figure 2.2: Damp a↵ect on Pegels exponential smoothing

Trend Adjusted Exponential Smoothing (TAES)

An alternative to Holts and Brown exponential smoothing is TAES. The additive model is given

below:

Ft

= yt�1 + ⇠(y

t�1 � yt�1) (2.8)

Tt

= Tt�1 + �(F

t

� yt�1) (2.9)

yt+h

= Ft

+ hTt

(2.10)

yt+h

is the forecast at a period of h ahead, Ft

is the forecast at time t Tt

is the forecasting trend,

Y is the original observation, yt

is predicted value and ⇠ and � are smoothing parameters. This

model uses both original observations and predicted values for forecasting the model describing a

CHAPTER 2. THEORETICAL CONTEXT 10

trend Tt

as being adjusted for forecasting h step a heads. This special case will be demonstrated

and explained more clearly in the methodology section.

In summary, there is still some limitations with the using ES as it su↵ers from not having an

objective statistical identification and diagnostic system for evaluating the goodness of compet-

ing exponential smoothing models. For example, the smoothing parameters of the models are

determined by fit and are not based on any statistical criteria like tests of hypothesis concerning

parameters or tests for white noise in the errors produced by the model (Fomby, 2008).

2.1.3 Linear models summary

In comparison, ES seems to have the advantage of its procedural simplicity whereas ARIMA models

require many stages of diagnostic checks to achieve a white noise for the error term. Also ES has

the ability to dampen its own trend over a period whereas ARIMA is just a constant projection of

forecasts ahead. Nevertheless, Both ARIMA and exponential smoothing shares similar identities

for example some exponential smoothing methods are shown to be special cases of the class of

Box-Jenkins models (Formby, 2008) and they both are linear predictors. Presumably, for a highly

fluctuate time series, both ARIMA and ES will only give linear forecast values. This sometimes

do not provide su�cient information for firms as uncertainty level is still high since firms may not

know when will be the next turning point? This has becomes problematic since all econometric

series are non-linear with highly fluctuate, this is a complex problem that require a method deals

non-linear time series.

2.2 Univariate time series - nonlinear models

It often found that linearly modelling econometric time series usually leave certain aspects of

economic financial data unexplained. Nevertheless modeling nonlinear time series allow the ex-

istence of di↵erent states of the world or regimes and to allow the dynamics to be di↵erent in

di↵erent regimes. Nonlinear models requires advanced level of understanding in time series as

formulation of these models requires many factors that a↵ects the behavior on a time series. A

very well-known model used by forecasters is artificial/fuzzy neutral network (ANN). This model

CHAPTER 2. THEORETICAL CONTEXT 11

operation is a process where a time series data input into a black box which will be trained using

machine learning technique then produce an output to be the forecast prediction. In applications,

ANN uses is wide spread in stock market, bond ratings, commodity and currency exchange, and

other di�cult-to-predict situations.

2.2.1 Introduction to ARCH and GARCH

An extension from Box and Jenkins models, autoregressive conditional heteroskedasticity (ARCH)

introduced by a Nobel Prize winner Robert F. Engle successfully applied on a non-linear time series.

ARCH has been popular in modelling econometric time series and most famous application on

modeling for stock prices with changing volatility. The term heteroskedasticity refers to unequal

variances on a time series whereas Box Jenkins based on some crucial assumptions, like linearity,

stationarity, and homoscedastic errors. Further more most of econometric time series are often

exhibit features which cannot be explained by linear models. In financial market, less firms choose

to continue to use the linear models as they cannot explain well the behaviour of an econometric

time series satisfactorily, so a model is needed to describe data sets in which variance changes

through time. Given a time series:

Yt

= E(Yt

|⌦t�1) + ✏

t

E(Yt

|⌦t�1) = µ(✓)

Linear models : V ar(Yt

|⌦t�1) = E(✏2

t

|⌦t�1) = �2

ARCH models : V ar(Yt

|⌦t�1) = E(✏2

t

|⌦t�1) = h

t

(✓)

Linear-models gives both conditional, unconditional variance constant (�2) and giving k-step-

ahead forecast error variance depends only on k. Whereas ARCH-models have conditional variance

varies with ⌦t�1 leaving unconditional variance constant and giving k-step-ahead forecast error

variance depends on ⌦t�1. Both linear and ARCH models have conditional mean varies with

⌦t�1. Therefore, ARCH process allows the condition variances to change over time as a function

of squares past errors leaving the unconditional variance constant so it is non-linear in variance

but linear in mean. Besides that, Berra and Higgins (1993) have also explained on other success

of ARCH:

CHAPTER 2. THEORETICAL CONTEXT 12

• ARCH models are simple and easy to handle

• ARCH models take care of clustered errors

• ARCH models take care of nonlinearities

• ARCH models take care of changes in the econometricians ability to forecast

Given an AR(1) process to be the mean equation which have defined in equation (2.1):

yt

= � + �yt�1 + ✏

t

where:

✏t

|⌦t�1 N(0, h

t

)

ARCH(q) process = ht

= ! +qX

i=0

↵i

✏2t�1

where ! > 0,↵i

� 0 for all i andP

q

i=0 ↵i

< 1 are required to be satisfied to ensure non-negativity

and finite unconditional variance of stationary {✏t

} series. The order of lag (q) determines the

length of time for which a shock persists in conditioning the variance of subsequent error. However,

when the order (q) of ARCH model is very large, estimation of a very large number of parameters

(↵) required. To overcome this di�culty, Bolerslev introduced a more general structure in which

the variance model looks more like an ARMA than an AR called generalize ARCH (GARCH) in

which conditional variance is also a linear function of its own lags.

The usual approach to GARCH(p,q) models is to model an error term ✏t

in terms of a standard

white noise et

s N(0, 1) as ✏t

=pht

et

where ht

satisfies the type of recursion used in an ARMA

model:

GARCH(p,q) process = ht

= ! +qX

i=0

↵i

✏2t�i

+pX

j=1

�j

ht�j

(2.11)

A su�cient condition for the conditional variance to be positive is

! > 0,↵i

� 0, i = 1, 2, ...q (2.12)

CHAPTER 2. THEORETICAL CONTEXT 13

�j

� 0, j = 1, 2, .., p (2.13)

The GARCH(p,q) process is weakly stationary if and only if:

qX

i=0

↵i

+pX

j=1

�j

< 1

2.3 Multivariate time series analysis

When two or more variables are influence each other, multivariate time series analysis is most

suitable technique which can explain the interactions and co-movements among a group of time

series. Reason for employing this type of analysis is because future export values are generated

based various factors that e↵ects it.

2.3.1 Introduction to VARX(p,s)

Export is not only contemporaneously correlated to other macroeconomics variables, it also corre-

lated to each others past values. The VARX procedure can be used to model these types of time

relationships. Analyzing and modeling the export and its correlated variable jointly will develop a

better understanding in dynamic relationships between them. Further more, it will also increase

the accuracy of forecasts for each univariate time series by using extra information which available

from the related series and their forecasts. VARX(p,s) (SAS 2014) stands for vector autoregressive

model with exogenous variables. The form of the model can be written as:

yt

=pX

i=1

�i

yt�i

+sX

i=0

⇥⇤i

xt�i

+ ✏t

, where ✏t

s N(0,�2) (2.14)

where dependent variables yt

= (yt

, ..., ykt

)0, t = 1, 2.... denote a k-dimensional time series vector

and xt

= (xt

, ..., xkt

)0 are exogenous variables denote as k-dimensional time series vector. ✏t

=

(✏t

, ..., ✏kt

)0, is a vector white noise process.

CHAPTER 2. THEORETICAL CONTEXT 14

Cointegration

Two time series xt

and yt

are said to be cointegrated if they shares common stochastic drift

process. This means, there exists a parameter � such that Tt

= yt

+ �xt

is a stationary process.

A order of integration, denoted I(d) is minimum number of di↵erences ”d” required to achieve

a stationary time series, a vector of I(1) variables yt

is said to be cointegrated if there exist at

vector �i

such that �0i

yt

is trend stationary. If there exist r such linearly independent vectors

�i

, i = 1, ..., r, then yt

is said to be cointegrated with cointegrating rank r (Bent 2005, p.3). So if

the variables were cointegrated under rank r, we could estimate a Vector Error Correction model

(VECM) instead of transform a nonstationary time series stationary by di↵erencing. A VARX(p,s)

can be represent under Vector Error Correction form below:

�yt

= ⇧yt�1 +

p�1X

i=1

�⇤i

�yt�i

+ADt

+sX

i=0

⇥⇤i

xt�i

+ ✏t

Where ADt

is a constant, ⇧ = �0i

yt

and when ⇧ = 0 implies no cointergration between variables.

Johansen and Juselius proposed the cointegration rank test to determines the linearly independent

columns of ⇧.

2.4 Forecast Accuracy Instruments

Let yt

be h steps ahead predicted value produced by model and yt

be the real observation at time

t+h. Then the error term can be calculated as:

✏t

= yt

� yt

Thus, the model with best forecast accuracy is when ✏t

closest to 0. There has been many

measures of forecast accuracy which have been used in the past and forecasters have made di↵erent

advices about what should be applied when comparing the accuracy of forecast between models.

This section will be discussing some of forecast accuracy measurements in which Hyndman and

Koehler (2005) have suggested to performed well in M and M-3 competition: Mean Square Error

(MSE), Mean Absolute Percentage Error (MAPE) and Mean Forecast Error (MFE):

MFE =

P(y

t

� yt

)

n,MAPE =

P100���yt

� yt

yt

���

n,MSE =

1

n

nX

i=1

(yi

� yi

)2

CHAPTER 2. THEORETICAL CONTEXT 15

Where n is total number of observations. MSE measures whose scale depends on the scale of the

data. These are useful when comparing di↵erent methods on the same set of data, but should

not be used, for example, when comparing across data sets that have di↵erent scales. To address

this MAPE have the advantage of being scale-independent, and so are frequently used to compare

forecast performance across di↵erent data sets. MFE is the measures for bias of errors toward

over and under forecasting i.e if a forecast showing a negative MFE implies the model is over

forecasted.

Chapter 3

LITERATURE REVIEW

This chapter will review various methods of modelling the UK export and their accuracy. Further

more, we will review literature over existence research of time series analysis on exporting and a

brief discussion of forecast accuracy between methods has used in each paper.

16

CHAPTER 3. LITERATURE REVIEW 17

3.1 UK Popularity Export Forecast Technique

The most notable contribution to this literature is a large-scale research in the UK by Dia-

mantopoulos and Winklhofer (2003). This paper provided an insight in popularity forecasting

techniques that firms in the UK like to use in forecasting their export nowadays

The forecasting judgmental techniques incorporate intuitive judgments, opinions and subjective

probability estimates. Delphi method was initially introduced by Olaf Helmer (1962) and the

method has gained popularity in judgmental techniques. According to Helmer (1962, p.1), this

technique employed involves repeated individuals questioning of the experts (by interviews or

questionnaire) and avoid direct confrontation of the expert with one another. The questioning

process requires more than two rounds, experts are expected to provide a summary of their

forecasts and reasons for their judgment from previous round. These forecasts and judgments

will be taken in consideration and then an overall forecast will be produced. Diamantopoulos and

Winklhofer (2003) argued that judgmental forecast techniques are more widely used among firms

compared to statistical technique such as time series, regression. In order to apply successfully

judgmental technique, it requires contextual information which is defined as knowledge gained by

practitioners through experiences on the job, consisting of general forecasting experience in the

industry as well as specific product knowledge. This means that only people holding high position

in a company (i.e. managers, CEO) are able to carry out this task.

Diamantopoulos and Winklhofer surveys 1330 manufacture exporters in the UK to find out their

choice of techniques of forecasting exports. The result showed that 92% percent of the firms

use judgmental techniques and only 8% of statistical technique were employed. They came to

the final conclusion that judgmental technique is more popular amongst surveyed firms. This is

quite surprising as these statistical methods are becoming easy assessable nowadays, for example

computers, software are getting cheaper. There were also some controversies regarding the ap-

propriation of the survey. First, there was only 18% of firms responding to their surveys. Second,

a research reported by Sanders and Manrodt (1994) stated that large firms are more likely to

use statistical techniques due to its cost e�ciency. Therefore, it is insu�cient to conclude that

judgmental techniques are more widely utilized than statically.

Test result found high MAPE values for both judgmental and statistical techniques and for both

CHAPTER 3. LITERATURE REVIEW 18

techniques, short term forecast MAPE is significantly smaller (10%) than long term forecast

(35%). This suggests that short term prediction is significantly more accurate than long term

prediction and of the whole population tested, large proportion of 92% are judgmental technique

which are lies within 10% to 35%. This can conclude that judgmental technique is unreliable

in forecasting accuracy. On the other hand, most firms in UK who employ statistical technique

only for experimental reason is because statistical technique is sometimes unstable in long term

prediction due to a number of discontinuities (i.e it does not take into account of any unexpected

incident) which can only be explained by human judgmental. Therefore combining these two

techniques would produce a better forecasting in export. This paper may open up to an evidence

to why firms in the UK sometimes ine�ciently locate their resources where most of their decision

on how much to supply is based on their own judgment rather than a statistical point of view.

3.2 Existence time series analysis on export application

This section will review four existence research papers and aim to find out the e↵ectiveness of

di↵erent methods of modelling export series:

• Firstly, we will investigate on the e↵ectiveness on ARIMA ”Modelling and Forecasting Meat

Exports from India” carried out by Paul et al (2013).

• Secondly, we will go on review the forecast accuracy of ”Forecasting the Export Prices of

Thai Rice” by Feng et al (2007) using ANN in comparison to ARIMA.

• Thirdly, we will look at ”Forecasting Macroeconomics Variables” (i.e. income, unemploy-

ment rate..etc.) Onder et al (2013) usng ANN and exponential smoothing.

• Finally, we will review ”Forecasting International Trade” by Keck et al (2010) using multi-

variate and univariate time time series analysis.

The meat export time series shows an upward trend multiplicative time series but highly fluctuation

compared to the UK export series shown in Figure 3.1. Paul et al (2013) have successfully applied

a seasonal ARIMA model through ACF and PACF analysis. The model seems to fit well on the

series but in term of forecasting accuracy, seasonal ARIMA is over forecast of MAPE shows only

CHAPTER 3. LITERATURE REVIEW 19

10% error. The reason is that real data compared with the model forecasted values does not

follow the same pattern as the previous year pattern. They could have applied Pegels exponential

smoothing since the data seems to behave multiplicative and exponentially, hence the forecast

trend would look like distortion in between the fluctuations, which may produce a better result.

However the prediction interval for seasonal ARIMA on each month does not vary widely around

the forecasted values and the real observations, therefore the model is still quite adequate. Paul

et al (2013) came to a conclusion that seasonal ARIMA is the best model in modelling the India

meat export.

Figure 3.1: India meat export time series

Feng et al’s (2007) objective is to find an optimum forecast of the weekly Thai rice prices of

four di↵erent types of rice using ARIMA and ANN models. Jasmine and Glutinous rice has no

obvious trend as the time series follows a very random pattern, the rest seems to have an upward

trend and share similar pattern to the UK export time series (figure 3.2 ). The research team

has successfully applied four di↵erent ARIMA models on each category and fitted models are

almost perfect as accuracy estimates MSE, MAPE and others are showing values significantly

close to 0. However, there is a significant change on the forecast accuracy as error estimate

increases significantly in one category, MAPE increased from 0.9876% to 15% errors in glutinous

rice forecast. This is surprising as the past data does not fluctuate that high compared to jasmine

rice. ANN is then applied which act di↵erently to ARIMA as the formulation is to use the time

series data to develop an internal representation of the relationship between the variables, do not

make assumptions about the nature of the distribution of the data and importantly it takes care

CHAPTER 3. LITERATURE REVIEW 20

of non-linearity. The result was significantly improved as MAPE reduces to 11% errors as well

as the reduction in MAPE for other categories. Feng et al (2013) concluded that ANN is better

predictive accuracies.

Figure 3.2: Four di↵erent types of rice time series

Macroeconomics variables consist of 8 time series and modeling using ANN and exponential

smoothing. All 8 time series behave di↵erently and some of them have very high variance compared

to others. Of the 9 exponential smoothing models applied on these series, Holt’s, Brown’s and

quadratic trend exponential smoothing have shown to have best fit and perform well in the

low variance time series. However, for forecast accuracy, ANN models show a more convincing

results for high variance time series because the way neutral network designed deals of outliers,

high fluctuation and non-linearity produce a more realistic result show in figure 3.3. Exponential

smoothing (green line) prediction is linearly whereas ANN (red line) prediction follows sort of the

past data pattern. The research team came with a conclusion that exponential smoothing only

perform well in short term plus the advantage of their simplicity, whereas ANN might be more

accurate in forecasting but it is too di�cult as there can be infinite number of ways to set up

network. Hence, choosing the right network can become confusing and need some theoretical

knowledge on macro economy.

CHAPTER 3. LITERATURE REVIEW 21

Figure 3.3: ANN vs exponential smoothing

Keck et al’s (2010) aim is to develop a time series model to forecast the growth in imports by

major advanced economies. They have applied ARIMA(p,1,0) and VARX models to the time

series. VARX models have been found to be the best model in forecasting and Keck et al (2010)

concluded this success is partly due to GDP chosen to be an exogenous variable and the utilize

of GARCH in taking care of non-linearity and clusters.

In conclusion, for this literature review, any econometric time series where the fluctuation is

high (high variance) implies weak correlation between time and dependent variables. It may be

appropriate to apply non-linear model rather than linear model, since a non-linear model gives a

more clear picture to firm, whereas liner-model may assume the future export is increasing linearly

at any point in the future. However, the UK export series have low fluctuation, therefore there is

no guarantee that non-linear model would perform best in forecasting, thus linear models should

also be appropriate to apply to the UK export series.

Chapter 4

METHODOLOGY

This chapter will apply Regression with AR errors, ARIMA, ES, GARCH/ARCH and VARX models

to the UK export time series. It was decided to train the data from January 2000 to December

2013 leaving January 2014 to December 2014 to be a hidden data set which will be used later in

chapter 5 to analyses each models forecast accuracy. It will assumes that all calculations, tests

and other statistical diagnostics up to a 95% significant level. The SAS package and SAS (2014)

user’s guide for ARIMA, Autoreg and Varmax procedures are used to compute these models while

Excel is used compute Exponential Smoothing methods. SAS procedures are given in appendix.

22

CHAPTER 4. METHODOLOGY 23

4.1 Export series regression analysis

There has been much debate in the literature regarding what to do with extreme or influential

data points. From Figure 1.1 we can observe that there are few influential data point with high

peak compare to the rest of the data. A simple regression with 95% confident limits is applied

to export series to identify any outliers within the series using SAS procedure [1].

yt

= �0 + �1t+ ✏t

(4.1)

where �0 =19574, �1=143.42301.

Figure 4.1: UK export time series regression analysis

Figure 4.1 Rstudent plot found very few outliers above the 95% limit and very high cook’s distance.

Percentage Residuals histogram shows no obvious skew, which may assume the data is normally

distributed.

In Figure 4.2 below, the 3 outliers are also outside the 95% confident limits although the R-

square is showing a good correlation. Schwager and Margolin (1982) have mentioned the e↵ects

CHAPTER 4. METHODOLOGY 24

Figure 4.2: UK export 95% limits plot

of outliers as it can have serious impact on statistical analysis:

• Firstly, they generally serve to increase error variance and reduce the power of statistical

tests.

• Secondly, if non-randomly distributed they can decrease normality, altering the odds of

making both Type I and Type II errors of the hypothesis test.

• Thirdly, they can seriously bias or influence estimates that may be of substantive interest.

Further more, Section 3.2 have also provided evidence of existence research’s evaluation on e�-

ciency of linear predictors when dealing with a low variance time series, therefore, having outliers

will increase the variance which sometimes misleading the direction of linear predictor to the fu-

ture forecast. In order to overcome all these di�culties, the 3 outliers must be eliminated for a

better forecast result. It was found that these outliers have a relative high peak is in 2006, these

points have identified in Section 1.2 to be the unexpected China and India economy booming

that a↵ected the UK export. Before and after 2006 period, we observed from Figure 4.2 that

the series is growing at a stable rate as all the points are lies in the limits. Therefore it is very

unlikely for the same incident to takes place again and it is 95% confident that the forecast for

the next 12 months will also lies between this limit. Thus these outliers may be considered to be

influential points and linear models would be more su�cient in modelling the UK export without

CHAPTER 4. METHODOLOGY 25

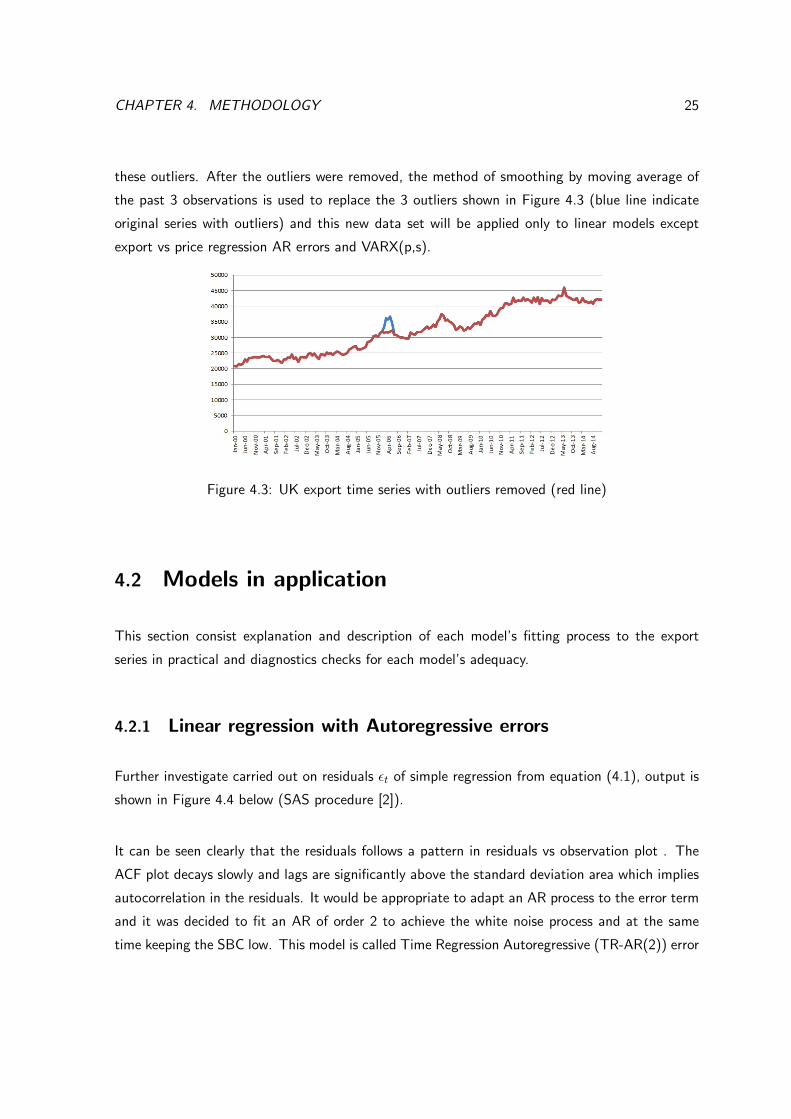

these outliers. After the outliers were removed, the method of smoothing by moving average of

the past 3 observations is used to replace the 3 outliers shown in Figure 4.3 (blue line indicate

original series with outliers) and this new data set will be applied only to linear models except

export vs price regression AR errors and VARX(p,s).

Figure 4.3: UK export time series with outliers removed (red line)

4.2 Models in application

This section consist explanation and description of each model’s fitting process to the export

series in practical and diagnostics checks for each model’s adequacy.

4.2.1 Linear regression with Autoregressive errors

Further investigate carried out on residuals ✏t

of simple regression from equation (4.1), output is

shown in Figure 4.4 below (SAS procedure [2]).

It can be seen clearly that the residuals follows a pattern in residuals vs observation plot . The

ACF plot decays slowly and lags are significantly above the standard deviation area which implies

autocorrelation in the residuals. It would be appropriate to adapt an AR process to the error term

and it was decided to fit an AR of order 2 to achieve the white noise process and at the same

time keeping the SBC low. This model is called Time Regression Autoregressive (TR-AR(2)) error

CHAPTER 4. METHODOLOGY 26

Figure 4.4: Identify autoregressive for the residuals

which can be written in the form below:

yt

= �0 + �1t+ Zt

Zt

= �1Zt�1 + �2Zt�2 + ✏t

, Where ✏t

s N(0,�2) (4.2)

Where �0, �1, �1, �2 are the model parameters which shown in SAS output Figure 4.5 below:

Figure 4.5: MLE parameter estimations and model fitness

From Figure 4.5 MLE test for all parameters are significantly < 0.05 which implies these param-

eters are su�cient for TR-AR(2), so parameters below are correspond to Figure 4.5:

�0 = 19843,�1 = 139.0876,�1 = �0.6205,�2 = �0.2814

CHAPTER 4. METHODOLOGY 27

The Durbin-Watson test for positive autocorrelation in residuals found that the p-value>0.05

which fail to reject positive autocorrelation in residuals. Further diagnostic check for this shown

in Figure 4.6, we can observe no significant lags in ACF, no obvious skew in histogram QQ plot

and white noise test shows all lags are below the 5% confident level. Thus we can confirm ✏t

in equation (4.2) to be a white noise. However we can observed few outliers in standardized

residuals which lies outside [-2,2] bound, but not too significant. Further research has carried out

and found no literature to identify these outliers and thus these outliers is retained in this model.

Hence adequacy for TR-AR(2) errors is comfirmed.

Figure 4.6: Diagostics check for residuals in TR-AR(2)

Having motivated by regression model above, further research has found that the general Ex-

port price for goods and services is to be the most fluently variable to the UK export. Export

price contains 168 observations monthly data from Jan 2000 to Dec 2013 and collected from

Tradingeconomic.com shown in Figure 4.7 below

CHAPTER 4. METHODOLOGY 28

Figure 4.7: Export price (index points)

The relationship between export and its price can be easily explained as a negative correlation. This

means export will decrease as its price increase. We can observe this relationship by comparing

Figure 4.7 to figure 1.1 for example during the period from Jan 2000 to Oct 2004 both export and

its price shows to have no movement until 2006 when the price fall leads to export to increase.

Both export and price have been run through SAS to identify autocorrelation in residuals and

output is shown in Figure 4.8 below ((SAS procedure [3]).

Figure 4.8: Identify autoregressive for the residuals of export against export price

We observed from ACF plot that lags are significantly outside standard error area. Again, we can

apply Price Regression AR error order 2 (PR-AR(2)) achieve the white noise process at the same

time keeping SBC stays low. The model equation can be written in form below:

yt

= �0 + �1pricet + Zt

Zt

= �1Zt�1 + �2Zt�2 + ✏t

, where ✏t

s N(0,�2) (4.3)

CHAPTER 4. METHODOLOGY 29

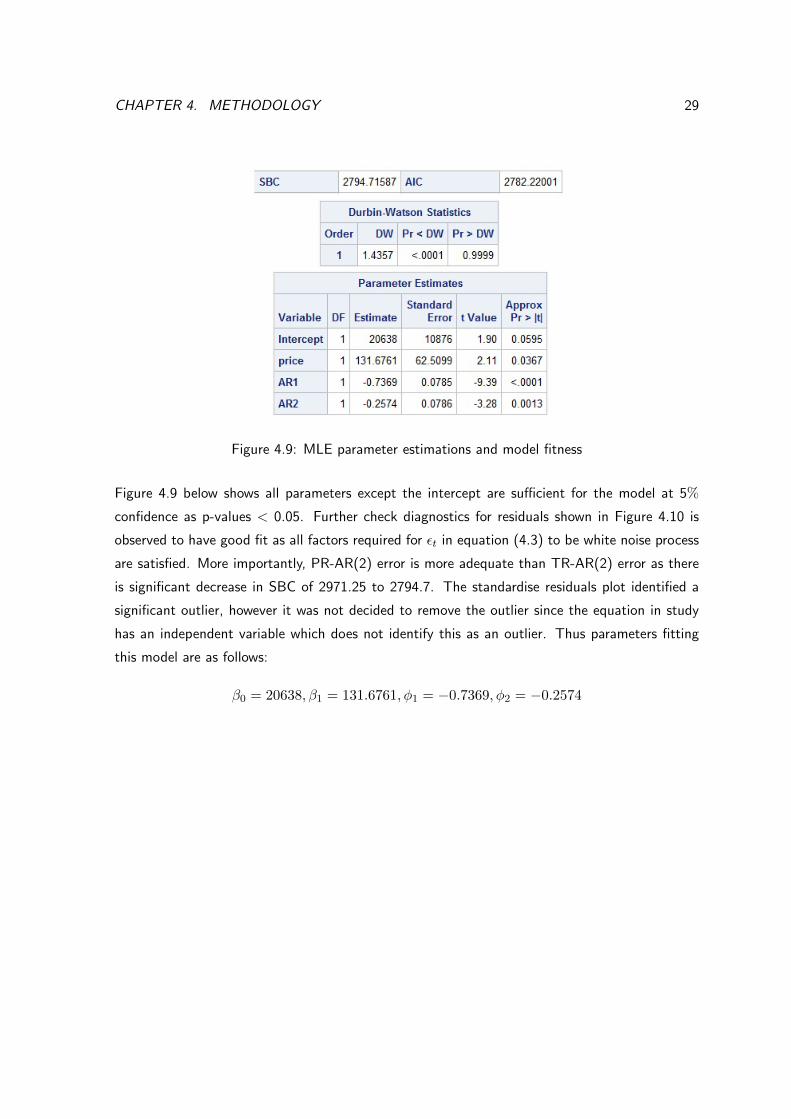

Figure 4.9: MLE parameter estimations and model fitness

Figure 4.9 below shows all parameters except the intercept are su�cient for the model at 5%

confidence as p-values < 0.05. Further check diagnostics for residuals shown in Figure 4.10 is

observed to have good fit as all factors required for ✏t

in equation (4.3) to be white noise process

are satisfied. More importantly, PR-AR(2) error is more adequate than TR-AR(2) error as there

is significant decrease in SBC of 2971.25 to 2794.7. The standardise residuals plot identified a

significant outlier, however it was not decided to remove the outlier since the equation in study

has an independent variable which does not identify this as an outlier. Thus parameters fitting

this model are as follows:

�0 = 20638,�1 = 131.6761,�1 = �0.7369,�2 = �0.2574

CHAPTER 4. METHODOLOGY 30

Figure 4.10: Diagnostic checks for residuals in PR-AR(2)

4.2.2 VAR(3) and VARX(4,1)

VAR(3)

One problem aroused from PR-AR(2) error model as it su↵ered from insu�cient information to

formulate the forecast ahead. This is because export is depending on export price, so without

the forecast ahead for export price it is not possible to carry out the forecast ahead for export.

However, this problem can be solved using VAR modelling 2 dependent variable.

Export and export price have been run through SAS to identify a suitable VAR(p) model and

output are showin in Figure 4.11 below (SAS procedure [4]):

CHAPTER 4. METHODOLOGY 31

Figure 4.11: Residuals diagnostic check

We observed from Figure 4.11 first Table that DF test indicates both series export and its price

are non-stationary with p-value > 0.05. The column Drift in ECM indicates that there is no

separate drift in the error correction model, and the column Drift in Process indicates that the

process has a constant drift before di↵erencing. Fifth column first row on second Table is the

test whether there is cointegrated process in both series at rank 0 (H0 : r = 0), the test show

p-value > 0.05 which cannot be rejected, whereas the test on second row show that there is no

cointegrated process at rank 1 (H0 : r = 1) as p-value <0.05 which reject the null hypothesis.

This implies that export and export price are cointegrated under rank=0. Thus we can fit VAR(p)

model under rank=0 and it was decided to choose p=3 in satisfying the vector white noise process

and lowest SBC. Output are shown in Figure 4.12 (SAS procedure [5]) below and VAR(3) can be

re-written in form of 2 univariate models below:

yexport,(t) = �+�1y

export,(t�1)+�2yexport,(t�2)+�3yexport,(t�3)+✏t, where ✏t

s N(0,�2) (4.4)

yprice,(t) = � + �1y

price,(t�1) + �2yprice,(t�2) + �3y

price,(t�3) + ✏t

, where ✏t

s N(0,�2) (4.5)

CHAPTER 4. METHODOLOGY 32

Figure 4.12: Model VAR(3) fitness diagnostics check

From Figure 4.12 first Table ANOVA diagnostics show that the data is a good fit to the two

univariate models (4.4) and (4.5) as p-value strongly reject the null hypothesis and R-square

very close to 1. We can observed a weak cross correlation of the residuals as all values in cross

correlation of residuals Table are significantly close to zero. In the Univariate model white noise

diagnostics Table:

• The second column shows Durbin Watson values are significantly higher than zero which

implies a strong evidence of uncorrelated in residuals for each univariate model (4.4) and

(4.5)

• The fourth column is the Jarque-Bera normality test show that the residuals are normal for

both univariate model (4.5) and (4.4) as p-value is significantly > 0.05.

• The sixth column test for unequal covariance show that p-value > 0.05 which fails to reject

the null hypothesis meaning each univariate model (4.4) and (4.5) has constant variance.

CHAPTER 4. METHODOLOGY 33

Finally, both (4.4) and (4.5) models AR diagnostics Table shows p-value is significant at 5% level

which implies residuals are uncorrelated in AR 1 to 4. Further more, Portmanteau test for cross

correlations of residuals Table show that p-value is significantly higher than 0.05 from lag 4 to 5

meaning vector error is uncorrelated. Finally, we have su�cient evidence to conclude VAR(3) is

in white noise process.

Figure 4.13: MLE parameter estimates for VAR(3)

We can observe from Figure 4.13 there are some parameters that are insu�cient for this model

as their p-value > 0.05 . However, residuals diagnostic above show the model is good fit and all

these parameters can be retained in this model. The model can be written in vector matrix form

below and parameters �i,(j,k) denote as ARi j k are corresponds to Figure 4.13:

yt

=

�1,(11) �1,(12)

�1,(21) �1,(22)

!yt�1+

�2,(11) �2,(12)

�2,(21) �2,(22)

!yt�2+

�3,(11) �3,(12)

�3,(21) �3,(22)

!yt�3+✏t, ✏t s N(0,�2)

VARX(4,1)

Export price is not the only factor influence export, further research has carried out and found 2

major economics factors that export and its price are mainly depends on are Exchange Rate (ER)

and Labour Cost (LC) shown in Figure 4.14.

CHAPTER 4. METHODOLOGY 34

Figure 4.14: Exchange rate 1 Pound to USD (left) labour cost (right)

These two variables has the same sample size as export and export price which collected from

tradingeconomic.com. Now ER is measuring in USD against 1 Pound and relationship between

export and ER can be described as negative correlation as the Pound gets weaker against USD, this

implies export becomes more a↵ordable and therefore increase the sales in export. LB is measures

in index points and it has negative correlation with export as LB increase will force firms to raise

export price up and leads to decrease in export sales. All variables applied in this model appears

have common stochastic drift, this is shown where each variable has similar peak during 2006 and

similar movement before and after 2006 which indicate the cointeration between these variables.

Causality and cointegration test have been carried out in confirming this association shown in

Figure 4.15 below (SAS procedure [6]):

Figure 4.15: Identifying rank r and exogenous variable association test

The null hypothesis of the Granger causality test is that group 1 variables are influenced only

by itself, and not by group 2. Thus we can clearly observe that p-value is <0.05 which reject

CHAPTER 4. METHODOLOGY 35

the null hypothesis so both export and its price are influenced by LC and ER . Thus we can lag

the exogenous variables by 1, so ”s” = 1. In VAR(3) model we have showed that export and

its price series are non-stationary through DF test. The coinegration test in Figure 4.15 shows

that both series in this case are cointegrated at rank 0 and 1 as their p-values are significantly >

0.05. However it would be more appropriate to model both series under rank 1 as their p-value

is showing a stronger indication of fail to reject the cointegration under rank 1. It was decided

to lag dependent variables by 4 to keep SBC stay lowest at the same time satisfying vector error

to be a white noise, so ”p” = 4. Output for VAR(4,1) diagnostics is shown in Figure 4.16 below

(SAS procedure [7]):

Figure 4.16: Model VARX(4,1) fitness diagnostics check

From Figure 4.16 ANOVA diagnostics show that the data is good fit the two univariate models

export and price as p-value strongly reject the null hypothesis and R-square significantly higher

than 0. However, portmanteau test in the cross correlations of residuals show that p-value is

< 0.05 which reject uncorrelated residuals in cross correlation. Nevertheless, We can observed

CHAPTER 4. METHODOLOGY 36

all tests and statistics from Figure 4.16 show to satisfy white noise process in residuals for both

univariate export and export price models. Also cross correlations of residuals Table show a very

weak cross correlation in the residuals as all values are very close to 0. Thus we may assume that

VARX(4,1) the vector error term is in white noise process and we can comfirm the adequacy for

VARX(4,1). Paramater estiamtes for VARX(4,1) are given in Figure 4.17 below:

Figure 4.17: MLE parameter estimates for VARX(4,1)

The t values and p-values corresponding to the parameters AR1 i j are missing because the

parameters AR1 i j have non-Gaussian distribution (SAS guide). From Figure 4.17, once again

we can retain the parameters for this models despite the MLE test indicates some parameters are

ine�ciency to the model because vector white noise process for VARX(4,1) is satisfied. Note the

D prefixed to a variable name in implies di↵erencing. Thus VARX(4,1) can be written in the

form below:

�yt

=

�1,(11) �1,(12)

�1,(21) �1,(22)

!yt�1 +

�2,(11) �2,(12)

�2,(21) �2,(22)

!�y

t�2 +

�3,(11) �3,(12)

�3,(21) �3,(22)

!�y

t�3

+

�4,(11) �4,(12)

�4,(21) �4,(22)

!�y

t�4 +

⇥⇤

0,(11) ⇥⇤0,(12)

⇥⇤0,(21) ⇥⇤

0,(22)

!xt

+

⇥⇤

1,(11) ⇥⇤1,(12)

⇥⇤1,(21) ⇥⇤

1,(22)

!xt�1 + ✏

t

where ✏t

s N(0,�2)

CHAPTER 4. METHODOLOGY 37

and parameters �i,(j,k) and ⇥⇤

i,(j,k) denote as ARi j k and XLi j k respectively are correspond

to Figure 4.17

4.2.3 A(1,1,0), A(0,1,1) and A(1,1,1)

The Box-Jenkins procedure is concerned with fitting an ARIMA model to data. It has three parts:

identification to see if the data may requires di↵erencing to achieve stationary, estimation to

see if parameter is e�cient for the model and verification to check error term truly is white noise.

Identification

In order to succeed in applying ARIMA models, it is very important clarify whether a series is

stationary. The Uk export is considered to be a random walk which is non-stationary defined as:

Yt

= ✏1+✏2+ ...+✏t

. The export series has ran through SAS procedure [8] to identify dependence

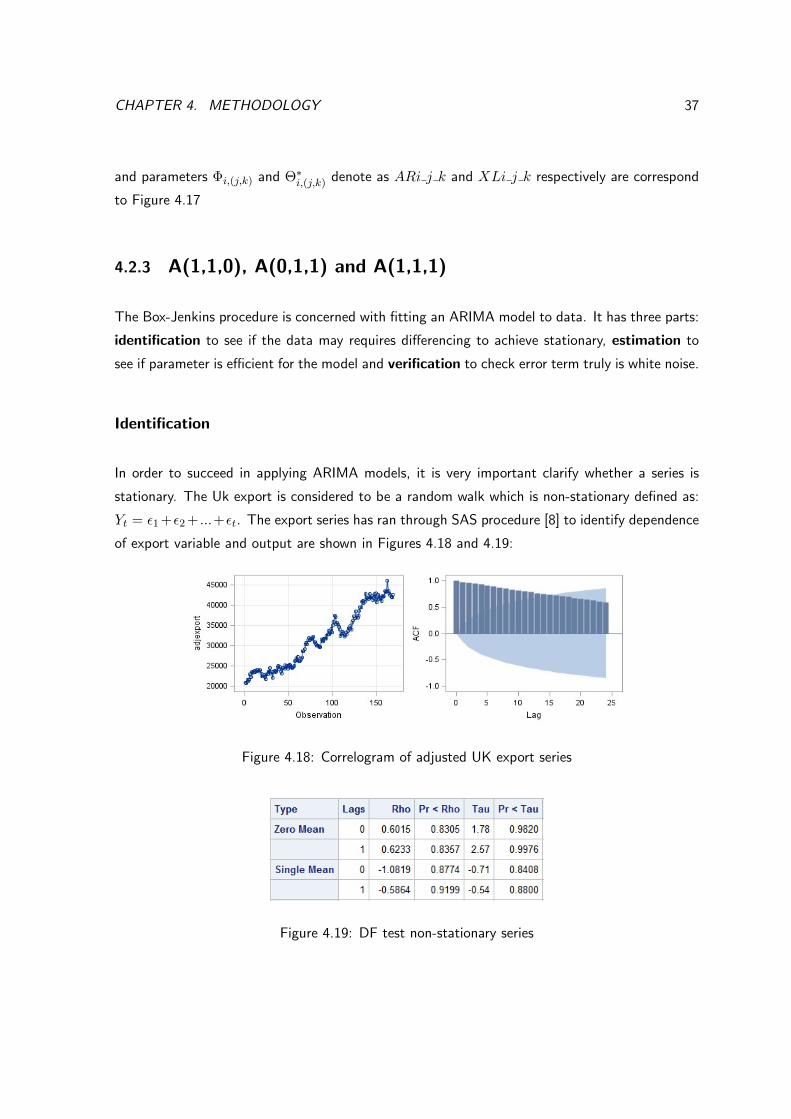

of export variable and output are shown in Figures 4.18 and 4.19:

Figure 4.18: Correlogram of adjusted UK export series

Figure 4.19: DF test non-stationary series

CHAPTER 4. METHODOLOGY 38

It is clearly to see from Figure 4.18 that lags in AFC plot are significantly above the standard error

area which implies dependent residuals in export variable and that they are not random. ACF is

decay at a very slow rate and the adjexport against time plot on left showing upward trend, it

does not show to have a constant mean and constant variance. DF test has carried out in Figure

4.19, DF test for zero and single mean shows that p-value is significantly > 0.05 which fail to

reject the non-stationary of this time series. Therefore, there is su�cient evidence to show that

the export series is non-stationary, so first di↵erence is required to this series.

Figure 4.20 and 4.21 are SAS output from SAS procedure [9]. Output below is the result after

the first di↵erenced to the export series.

Figure 4.20: DF test for di↵erenced series

Figure 4.21: Correlogram of di↵erences series

The di↵erenced series in Figure 4.21 (adjexport vs observation) plot shows that scatters are varies

constantly around mean of 0. However the variance seems to spread out widely from left to

CHAPTER 4. METHODOLOGY 39

right, so it is not possible to assume variance is constant, this may be due to the time series

is unstable at the at the period after 2006 when the trend grow at a faster rate than before.

Further check on ACF plot in Figure shows that lags are now inside the standard error area and

very close to 0 except lag 1. This indicate the export data set is random and series is stationary.

Further DF has carried out to confirm the series stationarity shown in Figure 4.20. DF test shows

p-value significantly < 0.0001 for both single mean and zero mean implies rejection on the null

hypothesis of non-stationary. Thereby, it is su�cient to conclude the series is stationary. Both

ACF and PACF seems to cut o↵ at lag 1 and unsure which is decay at faster rate, thus this

suggests A(1,1,0), A(0,1,1) and A(1,1,1) can be applied to the series. Thus, the equations (2.1)

above can be written without back shift operator as follows:

A(1, 1, 0) : yt

= � + yt�1 + �y

t�1 + �yt�2 + ✏

t

(4.6)

� = µ(1� �)

A(0, 1, 1) : yt

= µ+ yt�1 � ✓✏

t�1 + ✏t

(4.7)

A(1, 1, 1) : yt

= µ+ yt�1 + �y

t�1 + �yt�2 � ✓✏

t�1 + ✏t

(4.8)

Note all errors term above are i.i.d, ✏t

s N(0,�2)

Estimations

Figures 4.22 below are SAS output of parameter estimations of A(1,1,0), A(0,1,1) and A(1,1,1)

using SAS procedures [10].

Parameters estimates for equations (4.6),(4.7),(4.8) are shown Figure 4.22:

• For (4.6) �=171.977, �=-0.32924

• For (4.7) µ=129.29733, ✓=0.27665

• For (4.8) µ=129.43774, ✓=-0.055, �=-0.37845

MLE output found that t-test for A(1,1,1) have significant p-values > 0.05 for ✓ and �, thus, do

not reject the null hypothesis which implies ✓ = � = 0 in equation (4.8). Whereas A(1,1,0) and

CHAPTER 4. METHODOLOGY 40

A(0,1,1) p-values significantly < 0.05 which implies that ✓ and � are su�cient parameters that

suitable both model in equations (4.6) and (4.7).

Figure 4.22: Maximum likelihood estimations for A(1,1,0) (top), A(0,1,1) (middle), A(1,1,1)

(bottom)

CHAPTER 4. METHODOLOGY 41

Verification

Figures 4.23 to 4.28 below are SAS output of diagnostic check of models A(1,1,0), A(0,1,1) and

A(1,1,1) using SAS procedures [12].

Figure 4.23: Residuals diagnostic plots (top: normality plots, middle: scatters of residuals, bot-

tom: corolelograms) for A(1,1,0)

Figure 4.24: Ljung-Box statistic check residuals for A(1,1,0)

CHAPTER 4. METHODOLOGY 42

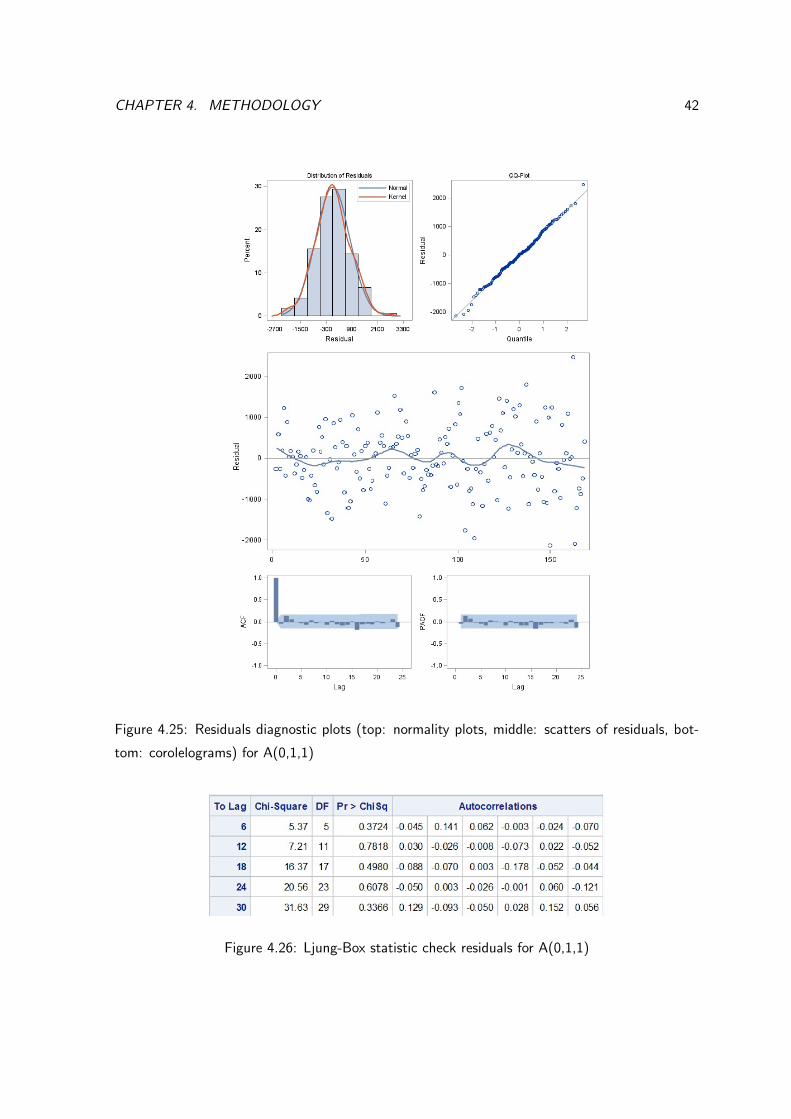

Figure 4.25: Residuals diagnostic plots (top: normality plots, middle: scatters of residuals, bot-

tom: corolelograms) for A(0,1,1)

Figure 4.26: Ljung-Box statistic check residuals for A(0,1,1)

CHAPTER 4. METHODOLOGY 43

Figure 4.27: Residuals diagnostic plots (top: normality plots, middle: scatters of residuals, bot-

tom: corolelograms) for A(1,1,1)

Figure 4.28: Ljung-Box statistic check residuals for A(1,1,1)

CHAPTER 4. METHODOLOGY 44

For the three models in Figure 4.23, 4.25 and 4.27, residuals in QQ plots shows points are lies

close to the fitted line although bottom left and top right has few points slightly o↵ the fitted

line. However, histogram plot shows kernel curves is almost fit the normal curves which appears

to have no obvious skew in the distribution. Scatter plots (residuals vs observation) shows no

obvious pattern, thus it is possible assume that the three linear ARIMA models is appropriate and

that the variance of the residual is constant. ACF for the three models shows no significant lag

outside of standard error area which may be implies residuals are independent. Further Ljuch-box

test is employed to test ✏t

dependency. Figure 4.24, 4.26 and 4.28 shows lags to 30 have p-

values significantly > 0.05, which fail to reject the null hypothesis meaning residuals for A(1,1,0),

A(0,1,1), A(1,1,1) are independent. Now there are su�cient evidence to satisfy the condition for

✏t

to be white noise process. However, despite the failure to reject null hypothesis for A(1,1,1)

parameter test, A(1,1,1) have clearly show to good fit through residuals diagnostics check. We

can conclude that A(1,1,0), A(0,1,1), A(1,1,1) models are adequate for the UK export series.

SBC in Table 4.1 show A(1,1,0) to be the most adequate model with lowest SBC.

Models SBC

A(1,1,0) 2713.700

A(0,1,1) 2716.874

A(1,1,1) 2713.734

Table 4.1: Models comparison

4.2.4 Exponential smoothing

For exponential smoothing DTES, DPES and TAES are most suitable model to satisfy the UK

export time series characteristic. This is because the three methods modelling trend and level

components of a time series. Excel package is mainly used in to perform ES models. To start o↵

with DTES and DPES models, equation Lt

at (2.2),(2.5) and Tt

at (2.3),(2.6) are assumed to be

coe�cient of simple regression model (4.1) where �0 is the intercept which also the level at time

t=0 and �1 is the trend of the fitted regression. Hence, L0= �0= 195.74 and T0=�1=143.42301.

For TAES F0 = first observation = y1 = 20925 and T0 = �1 = 143.423. Smoothing parameters

are obtained by using Excel solver to minimize the value of MSE. The results are shown on Table

CHAPTER 4. METHODOLOGY 45

4.2 below:

Models Parameter estimates damping (�)

holts ↵= 0.726456, � tends to 0 1

DTES ↵=0.7296, � =0.0046335 0.086

DPES = 0.999902 , �= 0.1583 1

DPSE =0.74043 , �= 1 0.0024135

TAES ⇠=0.725899,�=0.00092 n/a

Table 4.2: ES models fitting results

Both models DTES and DPSE shows to have a very strong dampen component, this means the

forecast ahead for holts and PES will be significantly pulled down due to this. All models except

DPSE shows to have a weak trend component where parameter are significantly close to 0. This

implies the level component for each model is one main factor deriving these models and their

forecasts.

Trend adjusted special case

Applying trend adjusted model have given an assess to a clear behaviour of the UK export Tt

in equation (2.9) and this behaviour is shown in Figure 4.29. This method is an attempt in

combining both linear seasonal Holt’s Winter (HW) (Hyndman and Athanasopoulos (2013)) and

non-seasonal method TAES in modelling the UK export.

Figure 4.29: Variation in Tt

from equation (2.9)

CHAPTER 4. METHODOLOGY 46

From the period from January 2005 to December 2013, Tt

seems to have multiplicative seasonal

component, thus it is likely for this cycle to repeat in the next period. Furthermore, realistically,

the UK export growth does not increase linearly as there is always up and down point over a

period. Equation (2.10) show that Yt+h

is depending on Tt

so by modelling and forecast Tt

with

the the adaptation of HW, an overall forecast for the UK export can become more realistic (up

and down rather than constantly linear). HWES Multiplicative is found to be most suitable in

method modeling Tt

:

Lt

= #(Yt

� St�p

) + (1� #)(Lt�1 +B

t�1)

Bt

= ⇠(Lt

� Lt�1) + (1� ⇡)B

t�1

St

= (yt

� Lt

) + (1� )St�p

Pt+h

= Lt

+ hBt

+ St�p+h

yt+h

= Ft

(from equation (2.8)) + Pt+h

(4.9)

Where Lt

is the level of series at time t, Bt

is the growth rate at time t, St

is the smoothed

seasonal value, p is the number of values within a period in the seasonal cycle, in this case p=32,

Pt+h

is the forecast h steps ahead, yt

is the original observation and yt+h

is the overall forecast

h step head of the UK export. This means the forecast for the export h steps ahead is being

adapted by HWES (equation (4.9) is equivalent to equation (2.10) but hTt

is being replaced by

Pt+h

because Tt

is being re-model using HW shown in Figure 4.30).

From Figure 4.29 observed allots of tiny fluctuation along the series, therefore in order to formulate

a robust forecast, moving average of the past 6 points has used to smooth out the series. This so

a clearer seasonal trend and pattern can be detected and the forecast will be less messy. The series

has ran through a simple regression and found intercept=�0= L0 = 67, trend=�1=B0=0.7589.

To formulate St

equation we calculate S0 to S�32 where:

S0 =Y32L0

, S�1 =Y31L0

, S�2 =Y30L0

.......S�p

.

Excel solver minimising MSE giving smoothing parameters # = 0.8, ⇠ = 0.4676 and = 1 with

MSE of 83.54. Now back to equation 4.9 the model fitted up to y168 which giving MSE of

794876.7. This MSE is still quite high, this maybe because Figure 24 Tt

series does not to follow

a decent seasonal trend and pattern over each cycle so it is not easy to model Tt

series perfectly.

CHAPTER 4. METHODOLOGY 47

Figure 4.30: Tt

equation (12) re-modelling using Hot’s winter seasonal

4.2.5 AR(1)-GARCH(1,2)

GARCH and ARCH models has used to fit the original data as it takes care of changes in variance

and outliers.

Heteroscedasticity test

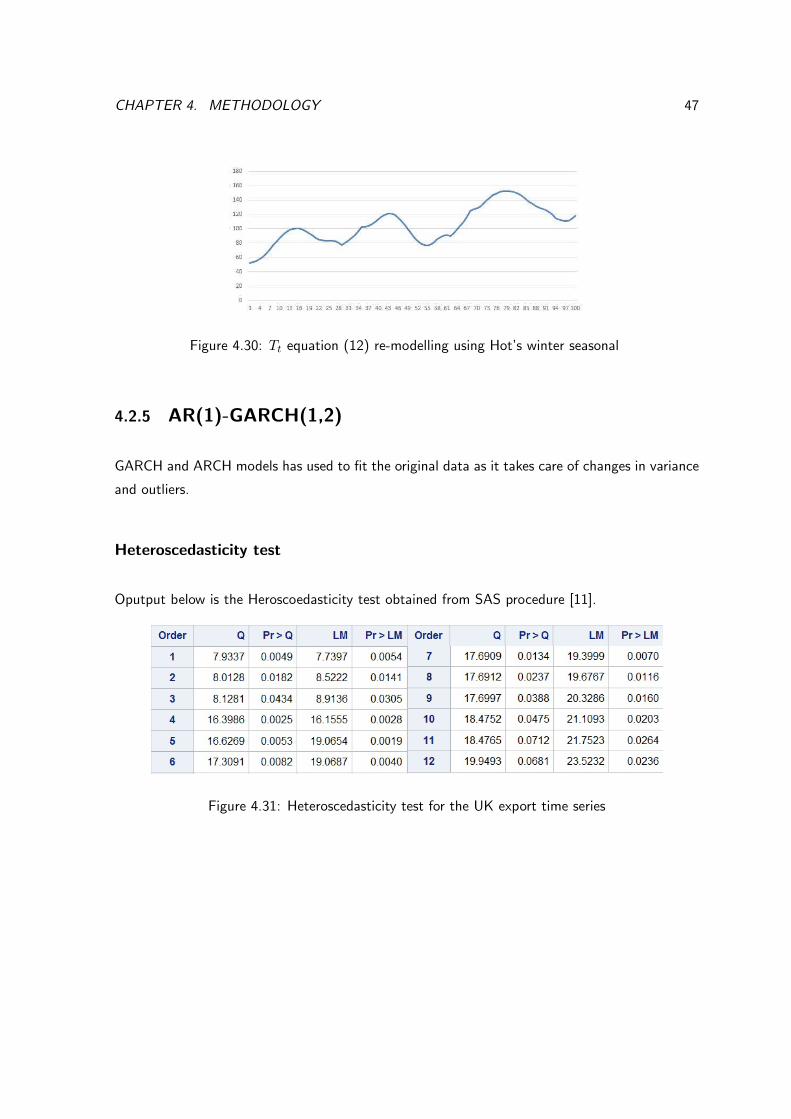

Oputput below is the Heroscoedasticity test obtained from SAS procedure [11].

Figure 4.31: Heteroscedasticity test for the UK export time series

CHAPTER 4. METHODOLOGY 48

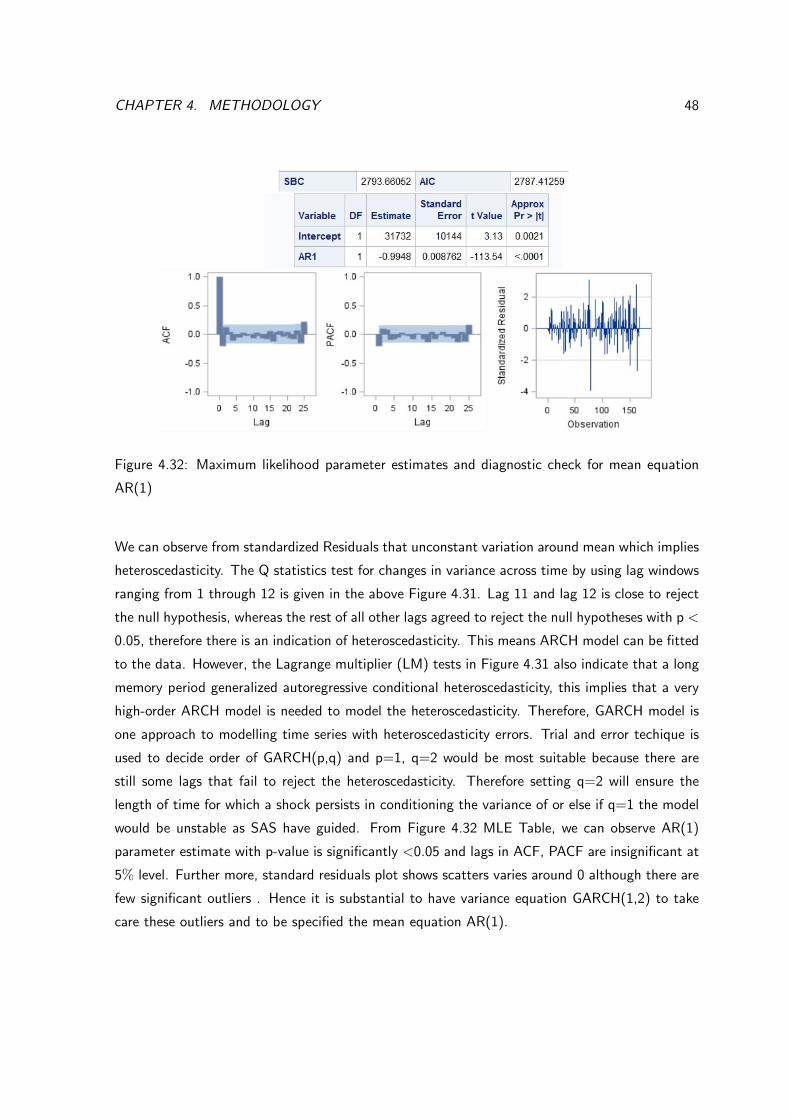

Figure 4.32: Maximum likelihood parameter estimates and diagnostic check for mean equation

AR(1)

We can observe from standardized Residuals that unconstant variation around mean which implies

heteroscedasticity. The Q statistics test for changes in variance across time by using lag windows

ranging from 1 through 12 is given in the above Figure 4.31. Lag 11 and lag 12 is close to reject

the null hypothesis, whereas the rest of all other lags agreed to reject the null hypotheses with p <

0.05, therefore there is an indication of heteroscedasticity. This means ARCH model can be fitted

to the data. However, the Lagrange multiplier (LM) tests in Figure 4.31 also indicate that a long

memory period generalized autoregressive conditional heteroscedasticity, this implies that a very

high-order ARCH model is needed to model the heteroscedasticity. Therefore, GARCH model is

one approach to modelling time series with heteroscedasticity errors. Trial and error techique is

used to decide order of GARCH(p,q) and p=1, q=2 would be most suitable because there are

still some lags that fail to reject the heteroscedasticity. Therefore setting q=2 will ensure the

length of time for which a shock persists in conditioning the variance of or else if q=1 the model

would be unstable as SAS have guided. From Figure 4.32 MLE Table, we can observe AR(1)

parameter estimate with p-value is significantly <0.05 and lags in ACF, PACF are insignificant at

5% level. Further more, standard residuals plot shows scatters varies around 0 although there are

few significant outliers . Hence it is substantial to have variance equation GARCH(1,2) to take

care these outliers and to be specified the mean equation AR(1).

CHAPTER 4. METHODOLOGY 49

Fitting GARCH(1,2) to AR(1)