worldwide tax summaries · 2017-09-05 · worldwide tax summaries corporate taxes 2017/18 all...

TRANSCRIPT

www.pwc.com/taxsummaries

Worldwide Tax SummariesCorporate Taxes 2017/18

Quick access to information about corporate tax systems in 157 countries worldwide.

Africa

Worldwide Tax SummariesCorporate Taxes 2017/18

All information in this book, unless otherwise stated, is up to date as of 1 June 2017.

This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

© 2017 PwC. All rights reserved. PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details.

Foreword

As governments across the globe are looking for greater transparency and with the increase of cross-border activities, tax professionals often need access to the current tax rates and other major tax law features in a wide range of countries. The country summaries, written by our local PwC tax specialists, include recent changes in tax legislation as well as key information about income taxes, residency, income determination, deductions, group taxation, credits and incentives, withholding taxes, indirect taxes, and tax administration. All information in this book, unless otherwise stated, is up to date as of 1 June 2017.

Our online version of the summaries is available at www.pwc.com/taxsummaries. The Worldwide Tax Summaries (WWTS) website also covers the taxation of individuals and is fully mobile compatible, giving you quick and easy access to regularly updated information anytime on your mobile device.

Some of the enhanced features available online include Quick Charts to compare rates across jurisdictions. You may also access WWTS content through Tax Analysts at www.taxnotes.com.

If you have any questions, or need more detailed advice on any aspect of tax, please get in touch with us. The PwC tax network has member firms throughout the world, and our specialist networks can provide both domestic and cross-border perspectives on today’s critical tax challenges.

Colm KellyGlobal Tax & Legal Services LeaderPwC Ireland

Welcome to the 2017/18 edition of Worldwide Tax Summaries – Corporate Taxes, one of the most comprehensive tax guides available. This year’s edition provides detailed information on corporate tax rates and rules in 157 countries worldwide.

1www.pwc.com/taxsummaries Foreword

PwC Worldwide Tax Summaries2 Contents

Contents

Foreword ...............................................1

Country chapters Algeria ..................................................4Angola ................................................. 14Botswana ............................................27Cabo Verde ..........................................36Cameroon, Republic of ........................55Chad ...................................................69Congo, Democratic Republic of the ......83Congo, Republic of ..............................99Egypt .................................................120Equatorial Guinea .............................135Gabon ............................................... 142Ghana ...............................................158Ivory Coast (Côte d’Ivoire) ................. 172Kenya ................................................185Madagascar .......................................203Malawi .............................................. 213Mauritius ..........................................226Morocco ............................................244Mozambique .....................................256Namibia, Republic of .........................270Nigeria ..............................................287Rwanda .............................................303Senegal ............................................. 316South Africa ......................................326Swaziland .........................................345Tanzania ...........................................351Tunisia ..............................................365Uganda .............................................392Zambia .............................................. 413Zimbabwe .........................................428

Worldwide Tax Summaries Editorial Team ...................................441

Country chaptersAfrica

Algeria 4www.pwc.com/taxsummaries

Algeria

PwC contact

Lazhar SahbaniPricewaterhouseCoopers Algérie5 rue Raoul Payen - Hydra 16 035, AlgerTel: +213 21 98 21 47Email: [email protected]

Significant developments

The Finance Law for 2017 introduced a wide range of tax measures dedicated to increase the state’s revenues, as well as other provisions intended to stimulate the investment dynamic in the country. These include, notably, the following measures:

• Upward revision of value-added tax (VAT) rates: The standard VAT rate is increased from 17% to 19%, while the reduced VAT rate grows from 7% to 9%.

• Establishment of an obligation for companies carrying out transactions with related companies to keep analytical accounting.

• Increasing from 500,000 Algerian dinars (DZD) to DZD 2 million the penalty amount relating to a failure to provide or an incomplete production of transfer pricing documentation.

• Application of VAT under the self-assessment regime on the remunerations paid offshore and subject to a reduced withholding tax (WHT) rate by application either of domestic law such as international lease agreement and software remuneration or the double taxation provisions.

• Introduction of an energy efficiency tax.• Removal of the obligation to pay imports via the documentary credit.

Taxes on corporate income

Corporate entities are taxed on activities performed in Algeria via the following two regimes:

Standard tax regime

Resident companiesThe standard tax regime is applicable for all tax resident companies, which are taxed in Algeria on their worldwide income. The standard tax regime includes the following taxes:

• Impôt sur le Bénéfice des Sociétés (IBS) at the rate of:• 19% for manufacturing activities.• 23% for building activities, public works, and hydraulics, as well as tourist and

thermal activities, excluding travel agencies.• 26% for all other activities not mentioned above.

For mixed activities, companies should keep management accounts to determine the portion of each activity performed. Failing this, the highest rate (i.e. 26%) will be applicable for all of the taxable profits.

PwC Worldwide Tax SummariesAlgeria5

Algeria

Nil corporate annual tax returns include the payment of a minimum corporate tax amounting to DZD 10,000.

• Tax on business activity (TAP) at the rate of 1% for manufacturing activities, without any reduction. However, this tax is fixed at 2% for all other activities, with a reduction of 25% for some activities and locations, and computed based on the invoiced turnover.

• VAT at the rate of 19% or 9% (except any specific exemption). See VAT in the Other taxes section for more information.

• Branch tax set at the rate of 15% calculated on net profits after IBS. See the Branch income section for more information.

Non-resident companiesIn the absence of a double tax treaty (DTT), the basic principle that governs taxation of non-resident entities is that such entities are taxable in Algeria on their Algerian-source income whatever the way and wherever the location the work is carried out, provided only that the same are rendered or used in Algeria.

As a consequence, an entity will be liable for IBS via the WHT regime (see below) in Algeria through the execution of a related contract (services contract) to be performed in Algeria. From an Algerian point of view, such a contract is not an investment and is, by nature, temporary. Note that it is possible to execute several contracts under the same permanent establishment (PE).

In the presence of a DTT, a foreign company will be taxed in Algeria if it has a PE only.

Withholding tax (WHT) regimeNon-resident entities performing service contracts in Algeria are subject to the WHT regime. The 24% WHT, which encompasses the IBS, the TAP, and the VAT, is required to be levied on services only. The calculation base is the gross amount of the services invoiced.

Please note that Finance Law for 2017 subjects contracts that had been taxed under the 24% WHT to the Algerian VAT when its basis of calculation benefited from a reduction in the rate or rebates as provided for by the local tax legislation or the DTTs.

Local income taxesThere are no local or provincial taxes on income in Algeria. The TAP is being distributed for each district/location where there is a principal or secondary establishment.

Corporate residence

According to the provisions of Article 137 of the Algerian Tax Code, a company is considered as an Algerian tax resident entity in cases where it is incorporated under the Algerian law and is realising (i) commercial, industrial, or agricultural activities (physical presence obligation) or (ii) taxable profits through dependent agents. However, please note the existence of the PE concept, which can also refer to permanent place of business.

Algeria 6www.pwc.com/taxsummaries

Algeria

Permanent establishment (PE)The Algerian legislation introduces the PE concept in Article 137 of the Algerian Tax Code, relating to territoriality rules of IBS. This Article provides that IBS is due in Algeria on:

• Profits made by companies, which, without owning in Algeria an establishment or designated representatives, directly or indirectly perform an activity in Algeria resulting in a complete cycle of commercial operations.

• Profits made by companies using the assistance of representatives in Algeria that don’t have a separate professional personality from these companies.

Based on the above, a PE is created under Algerian law if a professional activity is performed in Algeria by a foreign entity and this activity is generating a complete business cycle, or in the case whereby a foreign company is making profits in Algeria through a dependent agent.

Other taxes

Value-added tax (VAT)VAT is applied on the supply of goods or services in Algeria. It includes all economic activities conducted in Algeria. The zero rate is also applied to all exports and sales to exempted sectors under specific regimes. The standard VAT rate is 19%. The reduced rate is 9%, applying to various basic items listed by law.

Monthly VAT returns and payments are due by the 20th day of the following month.

Customs dutiesAlgerian imports are subject to payment of customs duties in the following increments: duty-free, 5%, 15%, or 30%.

Specific customs exemptions and temporary admission regimes are granted to the oil and gas sector and to investments under the incentives tax regime of the National Agency of Investment (ANDI in French).

Excise taxesAll tobacco products are subject to excise tax.

Property taxesAn annual property tax is levied on real estates in Algeria. Rates depend on the location of real estate.

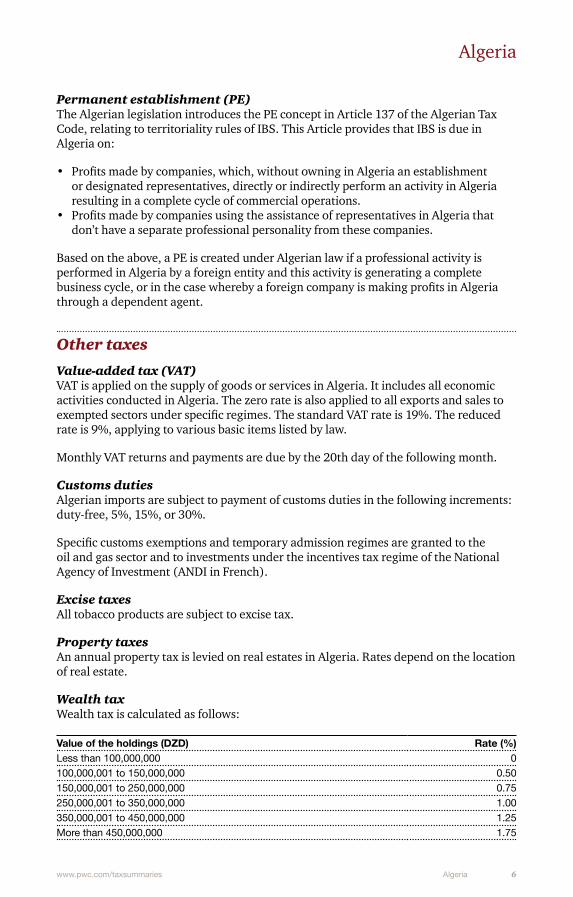

Wealth taxWealth tax is calculated as follows:

Value of the holdings (DZD) Rate (%)Less than 100,000,000 0100,000,001 to 150,000,000 0.50150,000,001 to 250,000,000 0.75250,000,001 to 350,000,000 1.00350,000,001 to 450,000,000 1.25More than 450,000,000 1.75

PwC Worldwide Tax SummariesAlgeria7

Algeria

Transfer taxesA transfer tax is applicable to land, buildings, and ongoing business at a rate of 5% for registration fees, plus 1% tax applicable for publication formalities of land and building transfer of ownership. Additionally, registration duties are due on the transfer of shares or movable assets and on the merger, demerger, increase, or decrease of the share capital of existing companies.

Stamp taxesStamp duty is levied at varying rates on transactions, including the execution of various documents and deeds.

Payroll taxesPersonal income tax (PIT) is withheld on salary and assimilated income (minus employee social security contributions) by applying the progressive scale rates (with a maximum rate of 35%). Additionally, training tax and apprenticeship tax are each levied at the rate of 1% of the payroll cost.

Social security contributionsSocial security contributions are levied at the rate of 35% on the gross salary (26% borne by the employer and 9% borne by the employee).

Bank domiciliation taxA 3% tax (Taxe de domiciliation bancaire) applies on the importation of services. Fixed fees are applicable for the importation of goods (DZD 10,000 per shipment).

Pollution taxAssets that may cause environmental damage are subject to a pollution tax.

Branch income

Branch tax is levied at the rate of 15%. Note that, since 2010, it is no longer possible to register a legal branch in Algeria. However, under certain conditions, a foreign company could operate in Algeria by registering its contract with the local tax authorities by registering a tax branch/PE. Under this scenario, a 15% tax rate applies on the deemed distribution of profits after tax, which may be reduced or removed by the applicable DTT provisions.

Income determination

Taxable income is determined using the accounting profits and adding back non-deductible expenses and deducting the allowable non-taxable incomes.

Inventory valuationThe inventory valuation method for tax purposes must match the accounting method as defined by the Algerian Financial Standards (SCF).

Capital gainsCapital gains realised on the sale of assets are taxed as ordinary income when realised by a company subject to IBS. For certain assets, 30% relief is given where the assets have been held for up to three years, and 65% relief is given where the movable assets

Algeria 8www.pwc.com/taxsummaries

Algeria

have been held longer. Capital gains on the disposal of assets can be exempted if the company commits to re-invest them within a three-year period.

Dividend incomeDividends to non-resident shareholders are subject to WHT at source of 15%, which may be reduced or neutralised by an applicable DTT. For resident shareholders, dividends are subject to WHT at source of 10%. If the dividends are received by a parent entity resident in Algeria, they are not included in the taxable profits for IBS purposes.

Interest incomeInterests paid are subject to 10% WHT and are included in the income of the beneficiary and subject to IBS if the beneficiary is a legal entity. Interests paid to a non-resident are generally subject to a 10% WHT. The rate may be reduced under an applicable DTT.

Rental incomeRental income is subject to IBS when received by a taxable corporate entity in Algeria. Rental income paid to non-residents is subject to 24% WHT, except for international lease agreements, where a reduction of 60% on the taxable basis is applicable, making the effective tax rate 9.60%. However, since January 2017, international lease agreements having benefited from the 60% taxable base reduction are subject to the Algerian VAT, which must be self-assessed by the local payer.

Royalty incomeSubject to DTT provisions, royalties are subject to 24% WHT. A reduction of 80% on the taxable basis is applicable for software, making the effective tax rate 4.80%. Since January 2017, the royalties on software having benefited from the 80% taxable base reduction are subject to the Algerian VAT, which must be self-assessed by the local payer.

Furthermore, the 24% WHT rate could change in presence of a DTT.

Unrealised gains/lossesRealised gains and losses are subject to IBS. However, unrealised gains and losses are not subject to IBS. There are specific provisions relating to the free re-evaluation of assets.

Foreign currency exchange gains/lossesForeign realised currency exchange gains/losses are subject to IBS.

Foreign incomeSubject to DTT provisions, income from other countries is liable to IBS in Algeria, except exportation revenues and revenues realised in hard currency by resident legal entities, which are exempted.

Deductions

Depreciation and amortisationThe depreciation rates are determined according to tax administration instructions and common usage, for example:

PwC Worldwide Tax SummariesAlgeria9

Algeria

• The depreciation rate for office items is 10% or 20%.• The depreciation rate for industrial buildings is 5%.• The depreciation rate for cars is 20% or 25%. The depreciation base for cars is

limited to DZD 1 million.

Accelerated depreciation rates, when justified, can be used, depending on the activity sector and the economic use of the assets.

GoodwillUnder the SCF, goodwill is registered in the local books as a non-current/intangible asset of the balance sheet and cannot be amortised. Consequently, the accounting of goodwill has no fiscal impact for companies.

Start-up expensesStart-up expenses are deductible when paid and cannot be capitalised and depreciated.

Interest expensesInterest expenses are deductible when paid.

Bad debtA bad debt provision becomes deductible when legal action has been taken to recover the debt or when evidence is provided that the receivable has become irrecoverable.

Charitable contributionsCharitable contributions are deductible, up to a limit of DZD 1 million.

Pension expensesPension expenses are deductible when paid.

Payments to directorsPayments to directors are deductible.

Research and development (R&D) expensesR&D expenses are fully deductible when paid by the entity bearing the expenses and when justified. Revenues derived from R&D activities are exempted from IBS, up to a limit of 10% of the taxable benefit or DZD 100 million. The exempted amount has to be reinvested in R&D activities.

Bribes, kickbacks, and illegal paymentsBribes, kickbacks, and illegal payments are non-deductible from the IBS basis.

Fines and penaltiesFines and penalties are non-deductible from the IBS basis.

TaxesTaxes duly paid are deductible, except for the IBS itself, which is not deductible. Also non-deductible for IBS purposes are the tax on apprenticeship and training and tax on passenger cars.

Net operating lossesCarryforward losses are permitted until the fourth fiscal year following the year of loss. Carryback losses are not permitted.

Algeria 10www.pwc.com/taxsummaries

Algeria

Payments to foreign affiliatesPayments to foreign affiliates are deductible.

Group taxation

When an Algerian company holds 90% or more of the shares of one or more Algerian companies, the group may choose to be taxed as a single entity. Hence, IBS is payable only by the parent company. Under this system, the profits and losses of all controlled subsidiaries in Algeria are consolidated. The consolidated group may also benefit from other tax advantages, such as exemption from VAT and TAP on the inter-group transactions.

Transfer pricingAn arm’s-length approach to transfer pricing applies. All entities registered with the tax department responsible for large-sized companies (Direction des Grandes Enterprises), in addition to the other foreign companies established in Algeria, must submit their transfer pricing documentation along with their annual tax returns (before 30 April of each year). Failing this, and should the documentation to support one’s transfer pricing practices not be provided within 30 days after a first request is made by the Algerian tax administration, a fine of 25% of the deemed transferred benefits on top of the late payment penalties of 25% are applicable.

Please note that, since 2017, related companies should keep management accounts in order to justify their transfer pricing policies, which should be provided upon tax administration request.

Thin capitalisationThere are no thin capitalisation provisions in Algeria.

Controlled foreign companies (CFCs)There are no CFC rules in Algeria.

Tax credits and incentives

Investment incentivesTax incentives can be granted to new investors, subject to the application of a specific request with the ANDI. The tax incentives can be granted for the investment phase and for the exploitation phase. They can be granted for a period of three years or five years, depending on the kind and the size of the business.

Other incentives can be granted for start-up businesses to encourage youth investment.

Many tax regimes and tax holidays/incentives are available to attract foreign direct investors in Algeria. For example, there is a temporary exemption from IBS for investing companies creating 100 jobs or more. VAT and custom duties exemptions are also available during the investment phase.

There is also a temporary exemption from IBS for companies that invest in certain strategic sectors, such as advanced technologies, the food industry, mechanics, and the automotive sector.

PwC Worldwide Tax SummariesAlgeria11

Algeria

There is a five-year reduction of IBS for companies whose securities are introduced on the stock exchange.

Foreign tax creditAlgerian tax law does not provide for unilateral tax relief. A DTT, however, may provide for bilateral relief.

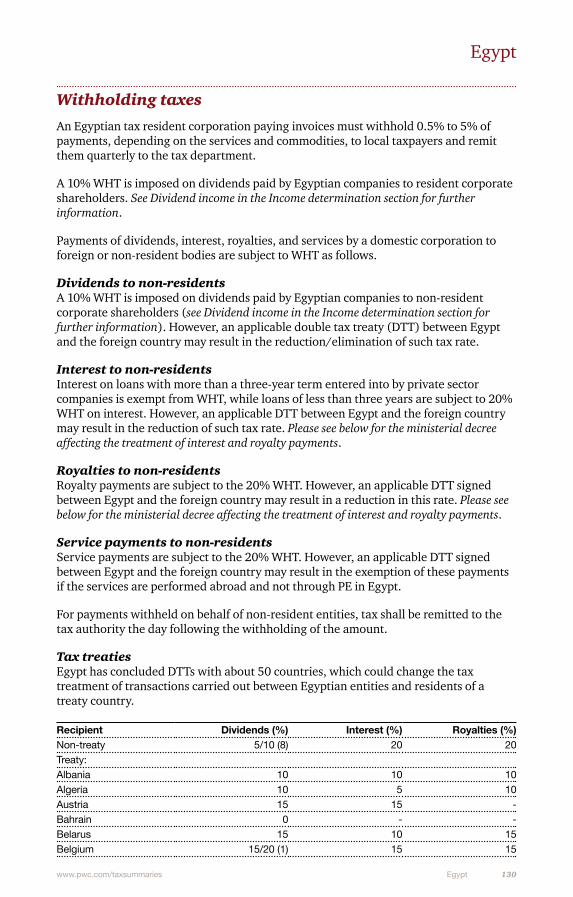

Withholding taxes

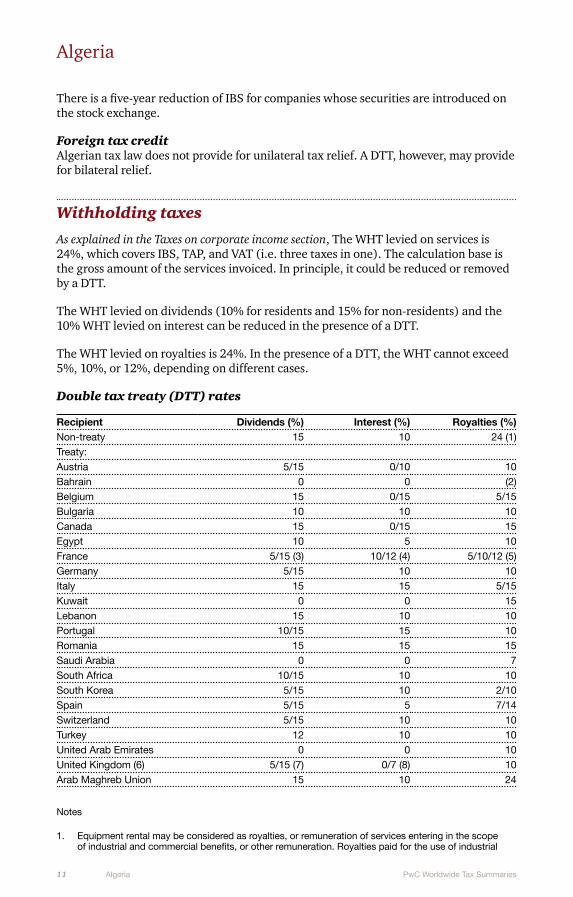

As explained in the Taxes on corporate income section, The WHT levied on services is 24%, which covers IBS, TAP, and VAT (i.e. three taxes in one). The calculation base is the gross amount of the services invoiced. In principle, it could be reduced or removed by a DTT.

The WHT levied on dividends (10% for residents and 15% for non-residents) and the 10% WHT levied on interest can be reduced in the presence of a DTT.

The WHT levied on royalties is 24%. In the presence of a DTT, the WHT cannot exceed 5%, 10%, or 12%, depending on different cases.

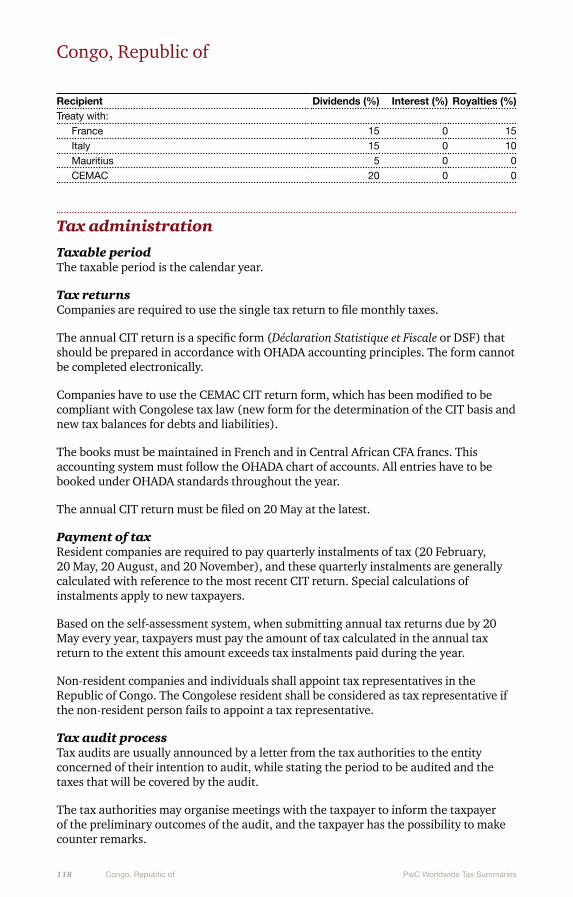

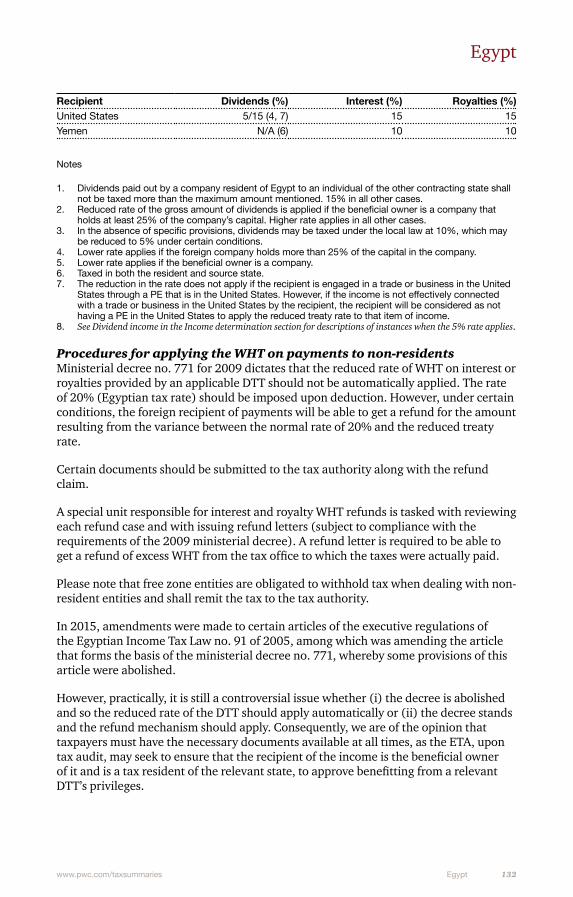

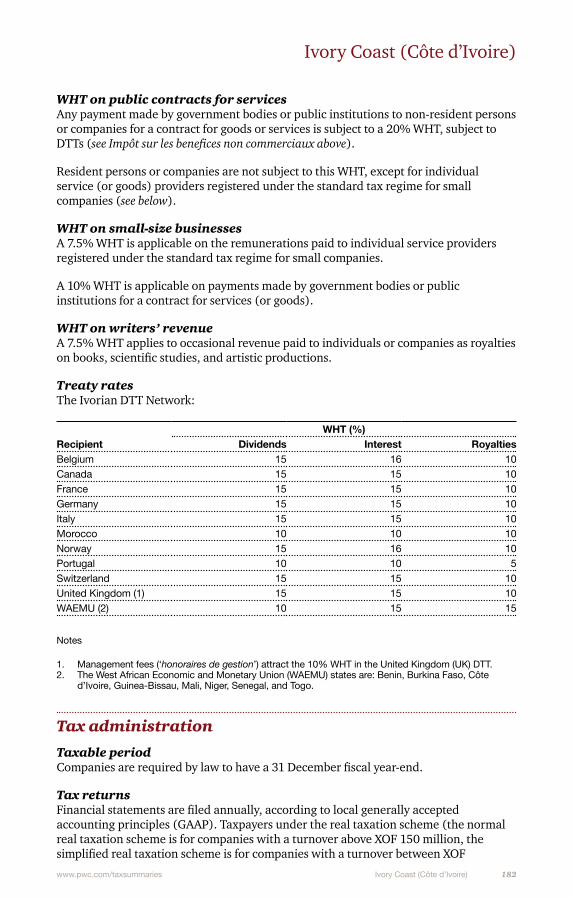

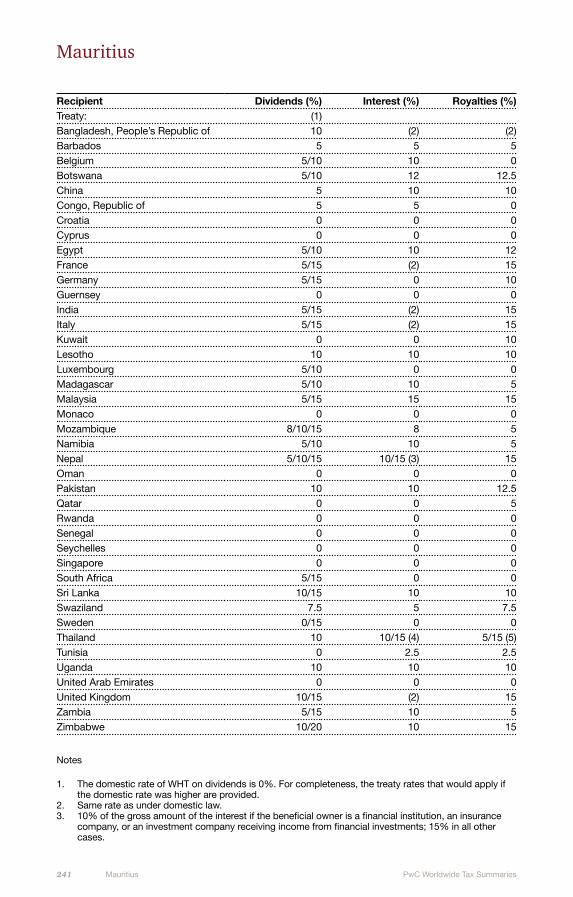

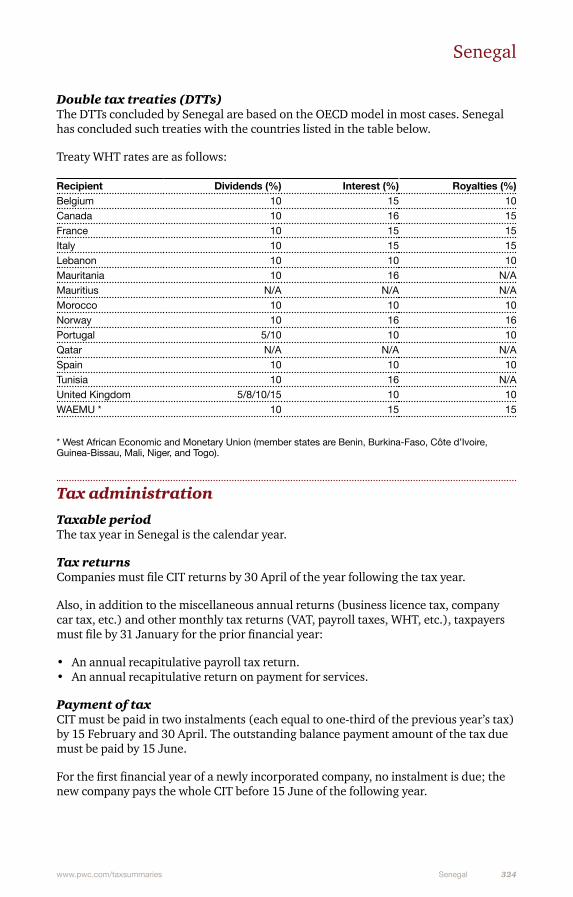

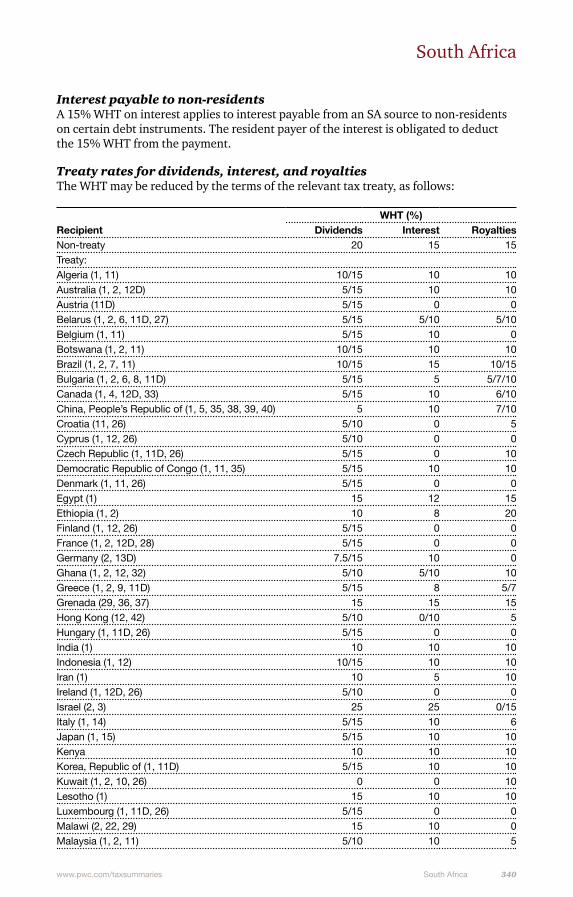

Double tax treaty (DTT) rates

Recipient Dividends (%) Interest (%) Royalties (%)Non-treaty 15 10 24 (1)Treaty:Austria 5/15 0/10 10Bahrain 0 0 (2)Belgium 15 0/15 5/15Bulgaria 10 10 10Canada 15 0/15 15Egypt 10 5 10France 5/15 (3) 10/12 (4) 5/10/12 (5)Germany 5/15 10 10Italy 15 15 5/15Kuwait 0 0 15Lebanon 15 10 10Portugal 10/15 15 10Romania 15 15 15Saudi Arabia 0 0 7South Africa 10/15 10 10South Korea 5/15 10 2/10Spain 5/15 5 7/14Switzerland 5/15 10 10Turkey 12 10 10United Arab Emirates 0 0 10United Kingdom (6) 5/15 (7) 0/7 (8) 10Arab Maghreb Union 15 10 24

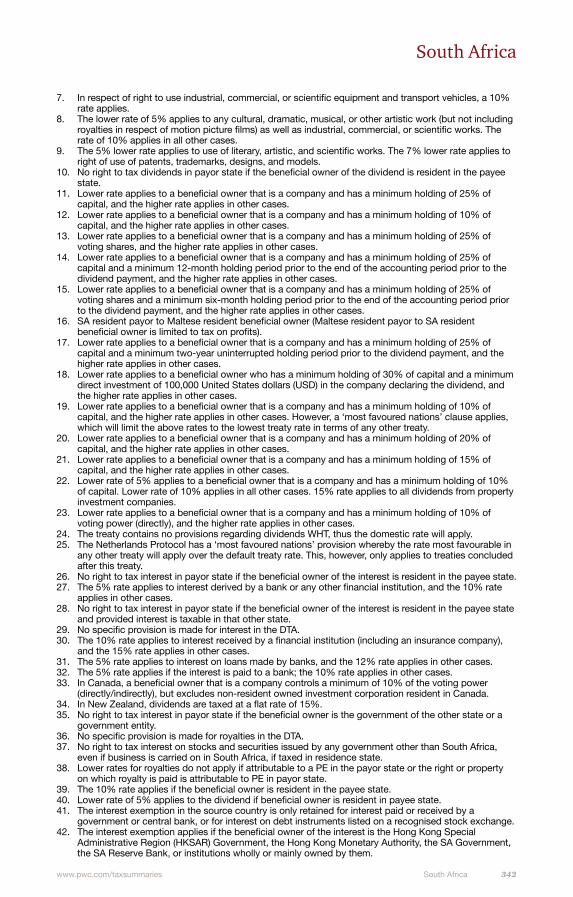

Notes

1. Equipment rental may be considered as royalties, or remuneration of services entering in the scope of industrial and commercial benefits, or other remuneration. Royalties paid for the use of industrial

Algeria 12www.pwc.com/taxsummaries

Algeria

equipment in the frame of an international leasing contract is subject to a tax allowance of 60% applied on the basis of such WHT. Thus, the effective tax rate of WHT will be 9.6% = 24% * (1 - 60%). For software, a reduction of 80% is applicable, making the effective tax rate 4.80%. VAT should be self-assessed in this case.

2. Domestic rate applies. There is no reduction under the treaty.3. 5% if the beneficial owner is a company that directly or indirectly holds at least 10% of the capital of

the company paying the dividends. 15% in all other cases.4. 10% if the beneficial owner is resident in Algeria and interests sourced from France and 12% if the

beneficial owner is resident in France and interests sourced from Algeria.5. 5% for royalties paid for the use of, or the right to use, any copyright of literary, artistic, or scientific

work, including cinematographic films, or films, tapes, and other means of image or sound reproduction. In other cases, 10% if royalties sourced from France and 12% if royalties sourced from Algeria.

6. DTT provisions entered into force on 1 January 2017 in Algeria for WHTs and other taxes.7. 5% if the beneficial owner is a company (other than a partnership) that directly holds at least 25% of

the capital of the company paying the dividends. 15% in all other cases.8. 0% if the interests are paid: (i) to the United Kingdom (UK) state, its central bank, a political

subdivision, or a local authority, (ii) by the Algeria state, its central bank, a political subdivision, a local authority, or a statutory body, (iii) if the interests are paid in respect of a loan, debt-claim, or credit that is owed to, or made, provided, guaranteed, or insured by, Algeria, or a political subdivision, local authority, or export financing agency in Algeria. 7% in all other cases.

Tax administration

Taxable periodThe taxable period is the fiscal year, which corresponds generally to the calendar year. For periodic activity, the fiscal year could be different from the calendar year.

Tax returnsCompanies are required to file an annual tax return before 30 April of the following year together with a detailed statement of proceeds paid to third parties with respect to subcontracted services, hiring of personnel and equipment, leases, and technical assistance services, as well as transfer pricing documentation. Monthly tax returns, which include VAT, IBS instalments, WHTs, PIT, and payroll taxes, should be filed within 20 days of the following month.

Payment of taxIBS is paid when the tax return is submitted after offsetting the corporate income instalments already paid before the IBS liquidation. Three IBS instalments are due on 20 March, 20 June, and 20 November, equal each to 30% of the IBS of the previous year.

Tax audit processAs a general rule, the tax administration informs the company when a tax audit has to be performed. The tax audit notification indicates the audited taxes (in all cases: IBS/TAP/VAT) and the concerned period. The company can be assisted by an expert, and it can ask the tax administration about several issues subject to audit. The tax audit is concluded by sending a final tax reassessment notification.

Some discounts or moderations can be granted to a debtor that is usually punctual in meeting its tax obligations and honouring its debts. For this purpose, taxpayers may, if indigent or hinders introduce a release request to the tax administration, seek remission or moderation of direct taxes properly established. A payment schedule may be granted to a company or to an individual in order to honour, progressively, their liabilities.

Taxpayers may also apply for some reconsideration by the tax administration. There are two alternatives:

PwC Worldwide Tax SummariesAlgeria13

Algeria

• Applications for reconsideration by the tax administration (recours gracieux). The application may refer to direct and assimilated taxes, related penalties, recovery penalties, and fiscal fines.

• Conditional rebate (remise conditionnelle). Conditional rebate could relate to penalties and fiscal fines. It may concern tax penalties applied under direct taxes, turnover taxes, registration fees, stamp duties, indirect taxes, and non-codified taxes. In order to enjoy these arrangements, the taxpayer must make a written application to the competent authority to which the conditional rebate is requested.

Statute of limitationsSubject to some exceptions, the fiscal statute of limitations is four years.

Topics of focus for tax authoritiesThe tax administration will focus on non-deductible expenses, the declaration of turnover, and, more often, on transfer pricing issues.

Other issues

Exchange controlsA non-resident foreign company can open a non-resident account in local currency (i.e. dinars), called an ‘INR account’, based on the contract to be performed and on its registration to tax. An INR account can be used only for the object (purpose) for which it is opened.

A non-resident foreign company can also open a CEDAC (Compte Etranger en Dinars Algériens Convertible) account, which must be credited only from abroad in foreign currency.

The CEDAC account allows payment in dinars as well as in hard currency. Furthermore, there is no restriction or limitation for transferring any remaining sum in the CEDAC account back abroad in foreign currency or for drawing any foreign payment instrument. The exchange rate that will be used for converting dinar to foreign currency is the official rate at the date of the debit.

Please note that a non-resident foreign company will not be able to transfer any balances from INR accounts to its CEDAC account or abroad without the express authorisation of the central bank, except in case of reimbursing temporary funding from the CEDAC account (such reimbursement must be for the exact same amount).

Please note that trading companies cannot pay any dividends to their foreign shareholders.

Choice of business entityForeign companies can run a business in Algeria through various forms of legal entities (e.g. joint stock company [SPA], limited liability company, partnership company), a joint venture or consortium, or PE. As for legal entities, the foreign companies should comply with the local shareholding requirement. Indeed, the foreign company cannot hold more than 49% of joint venture share-capital in Algeria.

Angola 14www.pwc.com/taxsummaries

Angola

PwC contact

Luis AndradePricewaterhouseCoopers (Angola), LimitadaEdificio PresidenteLargo 17 de Setembro n.º 3 , 1º andar - Sala 137Luanda – República de AngolaTel: +244 227 286 109Email: [email protected]

Significant developments

The major recent tax changes were the following:

• Law No. 5/16, of 17 May 2016, which introduced a Special Gambling Tax. This tax is applicable to the gross revenue arising from the exploration of gambling activities.

• Law No. 22/16, of 30 December 2016, which revoked the Special Contribution on Banking Operations.

• Under the Corporate Income Tax (CIT) Code’s transitional rules, the Autonomous Taxation (AT) enters into force in 2017. Unduly documented expenses, non-documented expenses, and confidential expenses will be subject to AT at rates ranging between 2% and 50%.

Taxes on corporate income

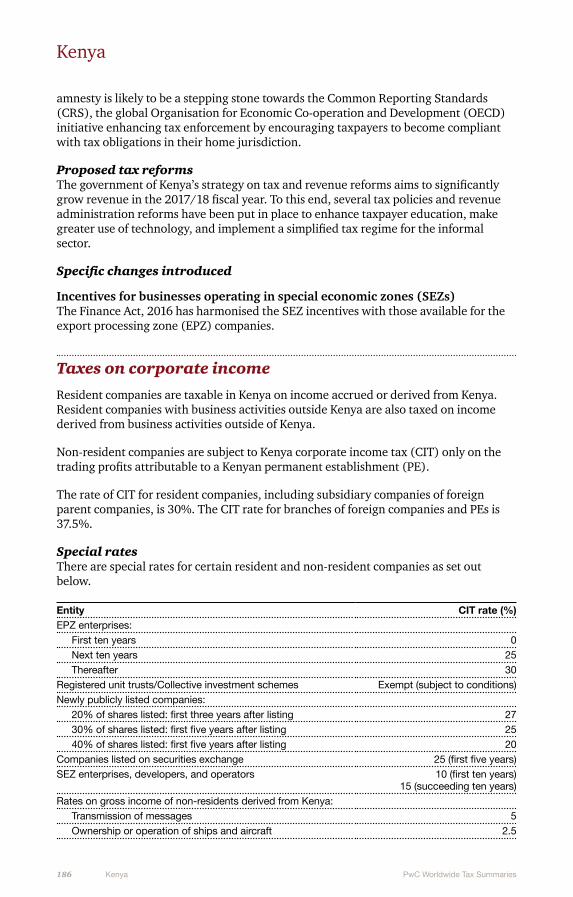

CIT is levied, currently at a 30% rate, on the profits deriving from business activities carried out in Angola by resident entities or non-resident entities with a tax permanent establishment (PE), as defined by Angolan domestic legislation.

Tax residents are taxed on worldwide profits, while PEs are liable to taxation on the profits attributable to the PE, sales in Angola of goods or merchandise of the same or a similar kind to that sold by the PE, and to any other business activity that is of the same or similar kind to that conducted by the PE.

There are two CIT payer groups:

• Group A: Public companies, private companies with a share capital above 2 million Angola kwanza (AOA), private companies with annual profits above AOA 500 million, and branches of foreign companies.

• Group B: Taxpayers not included in group A.

Special tax regimes apply to the oil and gas industry and to the mining industry.

Exemptions from CIT are provided for non-resident shipping and airline operators (as long as reciprocity exists in the foreign jurisdiction).

Investment income tax (Imposto sobre a Aplicação de Capitais or IAC)The IAC is due on interest, dividends, royalties, and other income of a similar nature. In Angola, the IAC Code divides such income into two sections, as follows:

Section ASection A includes:

PwC Worldwide Tax SummariesAngola15

Angola

• Interest on credit facilities.• Interest on loans.• Income derived from deferred payments.

The tax is due at the moment that the income starts to be due or is presumed to be due.

A minimum annual interest rate of 6% is deemed on loan agreements and credit facilities, except if another rate is proven through a written and stamped contract.

Section BSection B includes (amongst others):

• Dividends.• Repatriation of profits attributable to PEs.• Interest, premiums on the amortisation, reimbursement, and other forms of

remuneration of: (i) bonds and securities or other financial instruments issued by any company, (ii) treasury bills and treasury bonds, and (iii) Central Bank Securities.

• Interest on shareholder loans (or other shareholder financing). A deemed minimum annual interest rate equal to the rate used by the commercial banks is imposed.

• Indemnities paid to entities for the suspension of their business activity.• Capital gains on shares and other financial investments.• Royalties.

The concept of royalties includes payments of any kind received as a consideration for the use of, or the right to use, any copyright of literary, artistic, or scientific work, including cinematograph films, or films or tapes used for radio or television broadcasting, any patent, trademark, design or model, plan, secret formula or process, or for the use of, or the right to use, industrial, commercial, or scientific equipment or for information concerning industrial, commercial, or scientific experience.

ExemptionsThe following income is exempt from IAC:

• Interest on deferred payments regarding commercial transactions.• Payment of dividends to Angolan CIT payers that hold a participation higher than

25% for more than one year.• Interest from financial products approved by the Ministry of Finance that intend to

encourage savings, capped to capital invested of AOA 500,000 for each person.• Interest from housing saving accounts intended to encourage savings for main

permanent dwelling.

IAC rateThe IAC rate is 15%, except for certain income, for which the rate is 10% or 5%.

The tax rate is 10% for the following income (amongst others):

• Dividends and repatriation of profits.• Bond interest.• Interest from shareholder loans.• Capital gains.• Royalties.

Angola 16www.pwc.com/taxsummaries

Angola

The tax rate is 5% for the following income (amongst others):

• Interest and capital gains on bonds, securities, or other financial instruments issued by any company, Treasury Bills and Treasury Bonds, and Central Bank Securities, when these instruments are traded on a regulated market and have a maturity equal to or in excess of three years.

• Dividends and capital gains on shares when traded in a regulated market.

Assessment and paymentGenerally, for section B, the IAC is withheld by the payer entity.

On Section A, the IAC is paid and assessed by the receiving entity, through the filing of a tax return in January of the following year the tax relates to. If the income is paid to a foreign entity, then the obligation shifts to the Angolan resident paying entity.

Local income taxesThere are no provincial or local taxes on income in Angola.

Corporate residence

Business entities with a head office or effective management in Angola are considered resident entities and are taxed on worldwide income.

Permanent establishment (PE)Angola has not signed any double tax treaties (DTTs); consequently, its domestic tax provisions apply with regards to PE.

The Angolan concept of tax PE is inspired in the United Nations (UN) Double Tax Treaty Model. A foreign entity is deemed to create a PE in Angola if it:

• has a branch, an office, or place of management in Angola• has a construction or installation site, or provides supervision over such site, only

when such site or activities exceed a period of 90 days in any given 12-month period, or

• carries out services in Angola, including consulting, acting through employees or other personnel contracted for that end, when such services are provided for a period of at least 90 days in any given period of 12 months.

Other taxes

Consumption taxConsumption tax is due on imported or locally produced goods at rates varying from 2% up to 80%. The consumption tax is also due on some services, as follows:

Type of service Consumption tax rate (%)Hotel services and similar services 10Services relating to electronic communications and telecommunications, regardless of its nature

5

Water supply 5Electricity supply 5Lease of areas designated for collection and parking of vehicles 5

PwC Worldwide Tax SummariesAngola17

Angola

Type of service Consumption tax rate (%)Leasing of machinery and other equipment, if not subject to the IAC 5Leasing of areas used for conferences, colloquiums, seminars, exhibitions, showrooms, advertising, or other events

5

Consultancy services, namely legal, tax, financial, accounting, audit, information technology (IT), engineering, architecture, economic, and real estate

5

Photographic services, film processing and imaging, IT services, and construction of web sites

5

Private security services 5Tourism and travel services promoted by travel agencies or equivalent tour operators

5

Canteen, cafeteria, dormitory, real estate, and condominium management services

5

Car rental 5

Assessment and paymentThe consumption tax is assessed by:

• The manufacturers, in the case of goods produced in Angola.• Custom services, in the case of imports.• The service provider, in the case of services liable to tax. However, if the service

providers are non-resident entities in Angola, the obligation will revert to the resident acquiring entity.

Service providers are exempt from consumption tax if the services are provided to oil and gas companies, under certain conditions.

The consumption tax amount supported by oil and gas companies is deductible for petroleum income tax purposes.

Customs dutiesCustoms duties are levied on imports at ad valorem rates varying from 2% to 50% and consumption tax at ad valorem rates varying from 2% to 80%. The range of taxation for both consumption tax and import duties varies according to the type of goods. The rates are set out in the tariff book.

Listed equipment may be imported temporarily, if a bank guarantee is provided.

A 1% stamp duty is also due on importation plus customs fees (from 2%).

A special exemption regime applies for the oil industry for some listed equipment.

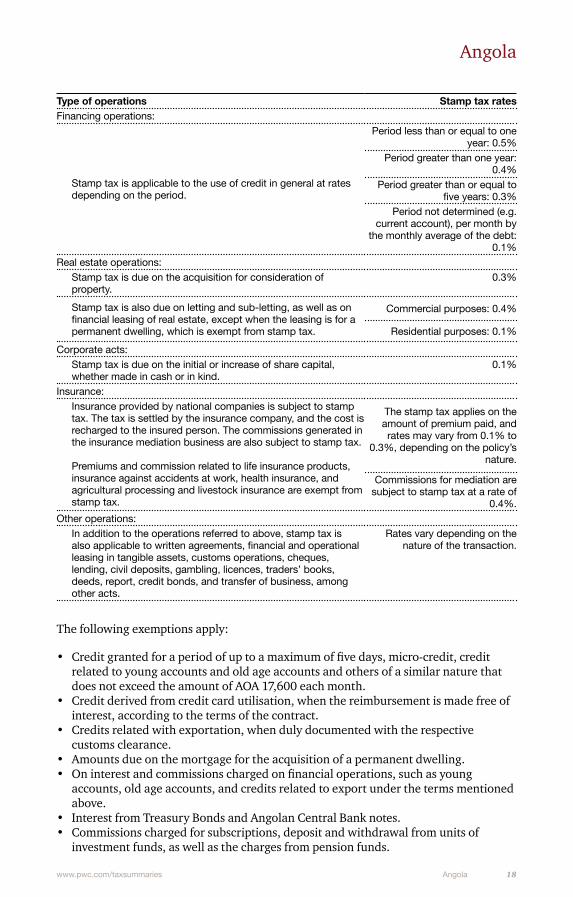

Stamp taxStamp tax is payable on a wide variety of transactions and documents, at specific amounts or at a percentage based on value.

Important examples include:

Type of operations Stamp tax ratesOn receipts:

Stamp tax on receipts (in cash or in kind). 1%

Angola 18www.pwc.com/taxsummaries

Angola

Type of operations Stamp tax ratesFinancing operations:

Stamp tax is applicable to the use of credit in general at rates depending on the period.

Period less than or equal to one year: 0.5%

Period greater than one year: 0.4%

Period greater than or equal to five years: 0.3%

Period not determined (e.g. current account), per month by

the monthly average of the debt: 0.1%

Real estate operations:Stamp tax is due on the acquisition for consideration of property.

0.3%

Stamp tax is also due on letting and sub-letting, as well as on financial leasing of real estate, except when the leasing is for a permanent dwelling, which is exempt from stamp tax.

Commercial purposes: 0.4%

Residential purposes: 0.1%

Corporate acts:Stamp tax is due on the initial or increase of share capital, whether made in cash or in kind.

0.1%

Insurance:Insurance provided by national companies is subject to stamp tax. The tax is settled by the insurance company, and the cost is recharged to the insured person. The commissions generated in the insurance mediation business are also subject to stamp tax.

Premiums and commission related to life insurance products, insurance against accidents at work, health insurance, and agricultural processing and livestock insurance are exempt from stamp tax.

The stamp tax applies on the amount of premium paid, and rates may vary from 0.1% to

0.3%, depending on the policy’s nature.

Commissions for mediation are subject to stamp tax at a rate of

0.4%.Other operations:

In addition to the operations referred to above, stamp tax is also applicable to written agreements, financial and operational leasing in tangible assets, customs operations, cheques, lending, civil deposits, gambling, licences, traders’ books, deeds, report, credit bonds, and transfer of business, among other acts.

Rates vary depending on the nature of the transaction.

The following exemptions apply:

• Credit granted for a period of up to a maximum of five days, micro-credit, credit related to young accounts and old age accounts and others of a similar nature that does not exceed the amount of AOA 17,600 each month.

• Credit derived from credit card utilisation, when the reimbursement is made free of interest, according to the terms of the contract.

• Credits related with exportation, when duly documented with the respective customs clearance.

• Amounts due on the mortgage for the acquisition of a permanent dwelling.• On interest and commissions charged on financial operations, such as young

accounts, old age accounts, and credits related to export under the terms mentioned above.

• Interest from Treasury Bonds and Angolan Central Bank notes.• Commissions charged for subscriptions, deposit and withdrawal from units of

investment funds, as well as the charges from pension funds.

PwC Worldwide Tax SummariesAngola19

Angola

• Commission charged on the opening and utilisation of saving accounts.• Credit operations (including interest) for periods not exceeding one year, provided

these are obtained exclusively to cover treasury needs, when realised between shareholders and entities in which a direct capital shareholding not lower than 10% is held and which has remained in their ownership for a year (consecutively), or since the incorporation of the respective entity.

• Loans bearing the characteristics of shareholder loans, including the respective interest, made by shareholders to the company in respect of which an initial period not shorter than one year is stated and no reimbursement is occurred before the end of that period.

• Treasury management operations carried out between companies within the same group.

• The exemption foreseen for the reporting of securities or equivalent rights includes other financial instruments negotiated on the regulated market.

• Sale of negotiable securities.• Transfer of real estate (under a merger, demerger, or incorporation operations if

approved by the tax authorities).• Employment contracts.• Exports, except for the export of products listed in the Stamp Tax Code table.• Insurance premiums and commissions related to life insurance, work accidents,

health, and agriculture and livestock insurance products.

Real estate income tax (IPU)IPU is levied on rental income earned by individuals or companies owning real estate assets. It is based on actual rental income when the assets are leased and on the assets’ registered value when the assets are not leased.

Leased assetsIPU is levied on rental income at a 25% nominal rate. However, the tax basis is only 60% of the rental income, as it is presumed that 40% relates to costs. Consequently, the effective IPU rate for rental income is 15%.

Assets that are not leasedIPU is levied as follows for the ownership of assets that are not leased:

Patrimonial value (AOA) IPU rate (%)Up to 5 million 0Over 5 million (on the excess) (1) 0.5

Notes

1. For example, an asset registered at AOA 35 million will pay IPU only on AOA 30 million, resulting in an IPU payable of AOA 150,000.

ExemptionsThe following entities are exempt from IPU:

• State public entities and associations that are granted with the public utility statute.• Property of Embassies or Consulates of foreign countries, provided there is

reciprocity.• Religious temples.

Angola 20www.pwc.com/taxsummaries

Angola

PaymentRents paid by Angolan companies or individuals that carry out a commercial activity are subject to withholding tax (WHT) of 15%. The IPU so withheld must be paid to the tax authorities by the end of the following month.

For property not leased, the respective owners must pay the IPU in January and July of the following year. The payment in four instalments (January, April, July, and October) is possible if approved by the tax authorities.

Filing requirementsIPU Model 1 must be filed by IPU taxpayers each January, disclosing the rents effectively received in the previous year, distinguishing the leases agreed and received.

Real estate transfer tax (SISA)SISA is levied at a 2% rate for all acts that involve the transfer for consideration of property.

The taxable basis is the higher of (i) the selling price or (ii) the property value registered for tax purposes.

The following entities are exempt from SISA:

• State public entities and associations that are granted with the public utility statute.• Property of Embassies or Consulates of foreign countries, provided there is

reciprocity.• Religious temples.

Payroll taxes

Employment income tax (IRT)Resident and non-resident individuals earning income from employment sourced in Angola (if paid for or borne by an Angolan employer) are subject to monthly taxation (IRT) at rates progressing from 0% to 17%. Angola operates a fairly straightforward pay-as-you-earn (PAYE) system, in which the Angolan employer withholds monthly from each employee’s gross compensation the Angolan income tax.

Individuals do not file tax returns, as the employment income tax is withheld at source by their employer.

Social security contributionsSocial security contributions are due on the gross income of employees at rates of 3% for the employee and 8% for the employer.

The contributions are intended to cover family, pension, and unemployment protection.

Special contributionThe Special Contribution is levied on payments due to non-residents under Foreign Technical Assistance and Management Contracts governed by the Presidential Decree 273/11.

This regime introduces restrictions on the payment for technical assistance and management services to foreign entities, particularly by imposing a special contribution

PwC Worldwide Tax SummariesAngola21

Angola

of 10% on the amount of the transfer due by the entity requesting the transfer of funds abroad.

This regime applies to both private and public companies. Petroleum activities are not liable to the special contribution.

Branch income

The repatriation of profits attributable to PEs of non-resident companies in Angola (e.g. branches of foreign entities) is taxable under the IAC at the rate of 10%.

Income determination

Inventory valuationInventory is valued at the historic acquisition cost. Any other method of valuation needs to be approved by the tax authorities.

Capital gainsCapital gains on fixed assets are taxed under CIT with no tax adjustments.

Capital gains arising from the disposal of shares, bonds, securities, or other financial instruments, Treasury Bills and Bonds, as well as Central Bank Securities, are taxable under the IAC Code.

Dividend incomeDividend income is only taxed under the IAC.

Interest incomeInterest income is only taxed under the IAC.

Rental incomeRental income on immovable property is only taxed under the IPU.

Royalty incomeRoyalty income is only taxed under the IAC.

Foreign incomeAn Angolan resident CIT payer is taxed on its worldwide income. No foreign tax credits are available to deduct against domestic tax.

No tax deferral provisions exist in Angola.

Deductions

DepreciationDepreciation should be computed using the straight-line method; any other method must be approved by the tax authorities.

The tax depreciation rates should respect the limits imposed by Presidential Decree no. 207/15, of 5 November.

Angola 22www.pwc.com/taxsummaries

Angola

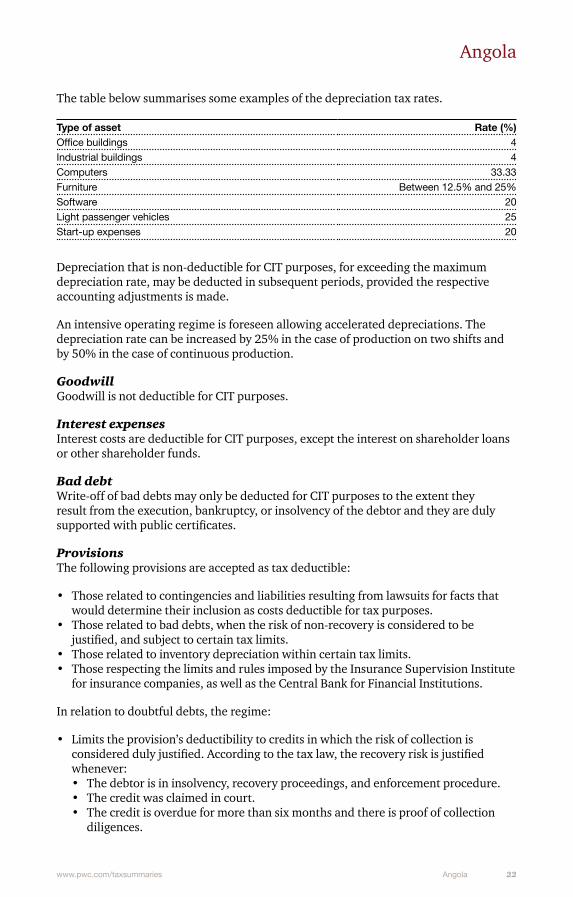

The table below summarises some examples of the depreciation tax rates.

Type of asset Rate (%)Office buildings 4Industrial buildings 4Computers 33.33Furniture Between 12.5% and 25%Software 20Light passenger vehicles 25Start-up expenses 20

Depreciation that is non-deductible for CIT purposes, for exceeding the maximum depreciation rate, may be deducted in subsequent periods, provided the respective accounting adjustments is made.

An intensive operating regime is foreseen allowing accelerated depreciations. The depreciation rate can be increased by 25% in the case of production on two shifts and by 50% in the case of continuous production.

GoodwillGoodwill is not deductible for CIT purposes.

Interest expensesInterest costs are deductible for CIT purposes, except the interest on shareholder loans or other shareholder funds.

Bad debtWrite-off of bad debts may only be deducted for CIT purposes to the extent they result from the execution, bankruptcy, or insolvency of the debtor and they are duly supported with public certificates.

ProvisionsThe following provisions are accepted as tax deductible:

• Those related to contingencies and liabilities resulting from lawsuits for facts that would determine their inclusion as costs deductible for tax purposes.

• Those related to bad debts, when the risk of non-recovery is considered to be justified, and subject to certain tax limits.

• Those related to inventory depreciation within certain tax limits.• Those respecting the limits and rules imposed by the Insurance Supervision Institute

for insurance companies, as well as the Central Bank for Financial Institutions.

In relation to doubtful debts, the regime:

• Limits the provision’s deductibility to credits in which the risk of collection is considered duly justified. According to the tax law, the recovery risk is justified whenever:• The debtor is in insolvency, recovery proceedings, and enforcement procedure.• The credit was claimed in court.• The credit is overdue for more than six months and there is proof of collection

diligences.

PwC Worldwide Tax SummariesAngola23

Angola

• Excludes from tax deductibility the provisions of credits covered by insurance, over shareholders and subsidiaries (at least 10% share), and over the state and public companies.

In relation to the losses incurred with inventories, the regime:

• Foresees different tax limits, depending on the sector of activity.• Imposes that the provision is calculated by the difference between the stock’s market

price and its acquisition cost.• Foresees a special regime for taxpayers engaged in editorial activities.

Charitable contributionsDonations are only deductible for CIT purposes if fully compliant with the Patronage Law. The requirements imposed by this law are very restrictive.

Fines and penaltiesFines and penalties are not accepted for tax purposes.

TaxesIndirect taxes are deductible for CIT purposes. Direct taxes are non-deductible, namely the CIT itself, IRT, IAC, IPU, or taxes paid on behalf of third parties (e.g. social security contribution and IRT supported on behalf of the employees).

Net operating lossesTax losses can be carried forward for three years.

Carryback of losses is not allowed.

Payments to foreign affiliatesPayments to foreign affiliates are accepted for tax purposes, although the arm’s-length principle should be complied with.

Group taxation

Major taxpayers that are members of an economic group may opt to be taxed under the tax regime of group taxation.

The option for the group taxation regime is available when:

• The company is included in the major taxpayers list.• The parent company holds, directly or indirectly, at least 90% of the share capital of

other companies (controlled entities), and more than 50% of the voting rights.

Some limitations apply and the option to apply group taxation depends on the approval of the tax authorities.

Transfer pricingUnder a special regime for ‘so called’ major taxpayers, being the ones identified in a list published by the Ministry of Finance, there are additional specific reporting and administrative obligations, namely the obligation of audited accounts and to prepare special transfer pricing documentation (e.g. the same will have to, under certain requisites, organise their transfer pricing documentation and submit it to the tax

Angola 24www.pwc.com/taxsummaries

Angola

authorities). This is applicable to those major taxpayers that have registered annual profits higher than 70 million United States dollars (USD).

Thin capitalisationThere are no thin capitalisation rules in Angola.

Controlled foreign companies (CFCs)There are no CFC rules in Angola.

Tax credits and incentives

Foreign tax creditNo foreign tax credits are available to deduct against domestic tax.

Private Investment LawThe implementation of investment projects in Angola in the amount equivalent to USD 1 million (for foreign investments) and USD 500,000 (for internal investments) may benefit from tax incentives for CIT, IAC, and SISA.

The extent of the incentives (tax rate reduction and period of the incentive) depends on several variables, such as the creation of jobs for Angolan citizens, the investment amount, the investment location, the sector of the activity of the investment, the equity held by Angolan shareholders, and the value added to the national market.

In addition, for investment projects in an amount equal to or above of USD 50 million, special benefits can also be obtained under negotiation with the cabinet of the President of the Republic.

Special regulations also provide tax and customs incentives for investment projects in strategic economic development areas and sectors.

Reinvestment of reservesProfits retained and then reinvested in new installations or equipment during the following three financial years may be deductible from taxable income during the following three years after the investment is finalised, at up to 50% of the value reinvested.

Withholding taxes

WHT is applicable on payments of services (some exemptions apply) granted by resident and non-resident entities at the rate of 6.5%. For Angolan taxpayers, this is regarded as an advance CIT payment due at the year-end; the deduction of these WHTs against tax CIT payable is limited to a period of five years. For non-resident companies, this is a final tax.

Dividends, interest, and royalties are subject to WHT under IAC (see the Taxes on corporate income section for more information).

PwC Worldwide Tax SummariesAngola25

Angola

Tax administration

Taxable periodThe tax year follows the calendar year.

Tax returnsThe annual CIT return for Group A and B must be submitted by the last business day of May and April, respectively, following the year to which the income relates.

Payment of taxTaxpayers from Groups A and B that record sales (granting of services subject to WHT are excluded) are required to make advance CIT payments until the end of August and July, respectively.

This tax is to be calculated by applying the rate of 2% on the total amount of sales recorded by the taxpayers in the first half of the tax year. Advance payments are offset against the final CIT assessed.

Advance payments made in excess may be deducted from subsequent advance payments up to the statute of limitation period of five years.

The final tax must be settled by the last business day of the month of April (Group B) and May (Group A) of the following year.

Tax audit processThe tax authorities may carry out tax audits to the monthly and annual tax returns.

Taxpayers may challenge any decision and file an appeal to the Chief of the respective Tax Office within 15 days upon receiving the tax notification.

Based on an unsatisfactory decision of the Chief of the Tax Office, the taxpayer may also file a hierarchical appeal addressed to the National Director of Taxes (DNI) within 15 days upon receiving the tax notification.

The taxpayer still has the right to appeal against the final decision of the DNI in court within 60 days upon receiving the final decision from the DNI.

Statute of limitationsThe statute of limitations in Angola is five years.

Topics of focus for tax authoritiesThe main areas of focus of the tax authorities relate to:

• WHTs due (regarding several taxes: CIT, IPU, IAC, and IRT).• 1% stamp tax on receipts.• Deductibility of costs for CIT purposes.• Transfer pricing.

Legal regime on invoices and similar documentsInvoices or similar documents must comply with the legal regime of invoices and similar documents (governed by the Presidential Decree 149/13).

Invoices and similar documents must comply with the following requirements (amongst other):

Angola 26www.pwc.com/taxsummaries

Angola

• Include the name, firm, tax address, and tax number of the supplier.• Be duly dated, sequentially numbered.• Include details on the nature, quantity, and price of the goods and services, as well

as the taxes due.• Be written in Portuguese and expressly mention that they were computer processed.

Suppliers that do not comply with this regime will be subject to fines and penalties. In addition, the acquiring entities cannot deduct the cost for CIT purposes and will be subject to an autonomous taxation on an amount that varies depending on the extent of the failure.

Other issues

Intergovernmental agreements (IGAs)An agreement under the Foreign Account Tax Compliance Act (FATCA), between the government of Angola and the government of the United States (US), was signed on 9 November 2015. This FATCA regime aims to fight tax evasion of US taxable persons who hold financial assets through financial institutions outside the US territory.

Botswana 27www.pwc.com/taxsummaries

Botswana

PwC contact

Butler PhiriePricewaterhouseCoopersPlot 50371Fairground Office ParkGaboroneBotswanaTel: +267 395 2011Email: [email protected]

Significant developments

There have been no significant corporate tax developments in Botswana during the past year.

Taxes on corporate income

Botswana has a source-based taxation system.

Corporate income tax (CIT) is charged at a single flat rate of 22%. Manufacturing companies having the approval from the Minister of Finance for a special tax rate will be charged at the rate of 15%.

International Financial Services Centre (IFSC) profitsIFSC companies are currently taxed at a flat rate of 15%. Companies must apply for a certificate to be classified as IFSC companies, which deal only in specified services and only with non-residents.

Mining profitsMining profits, other than profits from diamond mining, are taxed according to the following formula:

Annual tax rate = 70 minus (1,500/x), where x is taxable income as a percentage of gross income.

The tax rate shall not be less than the flat CIT rate of 22%.

Diamond miningDiamond mining is usually taxed in terms of an agreement with the government of Botswana.

Local income taxesThere are no local, state, or provincial government taxes on income in Botswana.

Corporate residence

If a company’s registered office or place of incorporation is in Botswana or if the company is managed and controlled in Botswana, then the company is considered a resident of Botswana.

PwC Worldwide Tax SummariesBotswana28

Botswana

Permanent establishment (PE)PE has been defined in the Income Tax Act only in the limited context of interest, commercial royalty, and management or consultancy fee. However, PE is defined in all the double taxation agreements (DTAs) that Botswana has entered into with other contracting states. The definition of PE in the DTA follows the definition in the Organisation for Economic Co-operation and Development (OECD) Model Tax Convention on Income and Capital.

Other taxes

Value-added tax (VAT)VAT is imposed on taxable supplies and the importation of goods into Botswana. The standard VAT rate of 12% applies to all supplies that do not qualify for an exemption or are not zero-rated.

The VAT registration threshold is 1 million Botswana pula (BWP).

Vocational training levy (VTL)VTL is payable when submitting the VAT return by every taxpayer who is registered for VAT. It is calculated as a percentage of turnover ranging from 0.2% to 0.05%, depending on the turnover of the company.

Customs and excise dutiesCustoms and excise duties are charged on importation of goods (including currencies) into or exported out of Botswana. The import duties may also include anti-dumping and countervailing duties. No customs duties and excise duties are charged on trade between Botswana and South Africa, Lesotho, Namibia, and Swaziland, as these five countries constitute a Southern African Customs Union. In terms of the Botswana/Zimbabwe Trade Agreement, goods originating from either of the trading partners are exempted from payment of customs duties under the condition that the goods meet a minimum of 25% local content. Excise duty and local taxes, such as VAT, are due and payable where applicable.

Property taxesThere are no property taxes in Botswana.

Capital transfer tax (CTT)CTT is levied on the donee upon the transfer (by way of inheritance or gratuitous disposal of property) of tangible or intangible, movable or immovable, property, at 12.5%.

Transfer duties on immovable propertyTransfer duty is levied at 5% of the value of immovable freehold and leasehold property. The first BWP 200,000 of such value are exempt from transfer duty in case of transfer to a Botswana citizen.

In the case of agricultural property, transfer duty is levied at the rate of 30% for a non-citizen. This duty is 5% in the case of a Botswana citizen.

Stamp dutyThere is no stamp duty in Botswana.

Botswana 29www.pwc.com/taxsummaries

Botswana

Payroll taxesAn employer with resident employees earning income above the taxable threshold and non-resident employees must deduct tax by applying the relevant tax rate and remit to the Botswana Unified Revenue Services (BURS) on a monthly basis before the 15th day of the succeeding month. Every employer is required to submit an annual return within 31 days after the end of the tax year.

Social security contributionsThere are no social security taxes or contributions in Botswana.

Branch income

CIT payable on branch profits is 30%.

Income determination

Inventory valuationInventories are valued at cost less such amounts, if any, that the Commissioner General believes are reasonable as representing the amount by which the value of such stock has been diminished because of damage, deterioration, obsolescence, or other cause. Although not expressly excluded by legislation, last in first out (LIFO) has not been accepted in practice by the tax authorities.

Capital gainsGains from disposal of specified capital assets (immovable property and marketable securities, including shares in private companies) are included in taxable income in the hands of the corporate taxpayer. Acquisition costs of immovable property are subject to a 10% compound annual addition for inflation for the period from acquisition to 30 June 1982, and thereafter to an inflation addition based on the increase in the consumer price index to the date of sale. For other gains, no inflation allowances are granted, but the taxable gain is set at 75% of the total gain.

Currently, the sale of any shares, units, or debentures of a resident company is exempt from tax under any of the following circumstances:

• The resident company whose shares are being sold is a public company.• The shares, units, or debentures are traded on the Botswana Stock Exchange.• The company has released for trading 49% or more of its equity on the Botswana

Stock Exchange.

This exemption only applies if the shares, units, or debentures were held by the taxpayer for a period of at least one year prior to the date of disposal.

The aggregate amount of capital losses is offset against the aggregate amount of capital gains in the same tax year. Any excess of loss is deducted from aggregate gains over losses accruing in the succeeding tax year only. Capital losses cannot, in any circumstances, be deducted against other income.

Dividend incomeDividend income from local sources is not subject to tax.

PwC Worldwide Tax SummariesBotswana30

Botswana

Interest incomeIn the case of a resident company, interest income is included in gross income and taxed at the CIT rate. In the case of a non-resident company, interest income is subject to withholding tax (WHT), which constitutes a final tax.

Royalty incomeRoyalty income is included in gross income and taxed at the CIT rate. In the case of a non-resident company, royalty income is subject to WHT, which constitutes a final tax.

Partnership incomePartnership income is taxed in the hands of the partners, in proportion to their share in the partnership.

Foreign incomeResident corporations are not generally taxed on a worldwide income basis. However, interest and dividend income from a foreign source is taxed in the hands of the resident company on an accrual basis. Relief is given for any WHT imposed on such income.

Deductions

Depreciation and depletionAnnual and capital allowances available are as follows.

Companies other than mining companiesAnnual taxation allowances for expenditures incurred on machinery and equipment before 30 June 1982 can be claimed up to 100%. This allowance may be for any proportion of previously unclaimed expenditures. For expenditures incurred on machinery and equipment after 30 June 1982, annual allowances are granted, calculated on cost by the straight-line method on the basis of the expected useful lives of the individual assets. Guidelines are provided for expected useful lives of different categories of assets, which vary from four to ten years. Book depreciation is not required to conform to tax depreciation. The capital allowance claimable on a company motorcar is restricted to a maximum of BWP 175,000.

An initial allowance of 25% of cost is granted on certain industrial buildings. All industrial and commercial buildings (excluding residential properties) are granted a 2.5% annual allowance based on cost or, in the case of an industrial building on which an initial allowance has been claimed, the original cost less the initial allowance.

Balancing allowances and charges are brought to account on the disposal of assets on which allowances have been claimed. Where disposal value of an item of machinery or equipment exceeds the difference between expenditures incurred on the asset and allowances granted, the whole amount is taxable as corporate income or the balancing charge can be offset against further additions of new equipment, thus providing rollover relief. However, there is no rollover relief on motorcars except where the cars are used in a car rental or taxi service business.

Mining companiesIn ascertaining the business income for any tax year from a mining business, there shall be deducted from business income an allowance, to be known as a mining capital allowance, computed in accordance with 100% of the mining capital expenditure made

Botswana 31www.pwc.com/taxsummaries

Botswana

in the year in which such expenditure was incurred, with unlimited carryforward of losses.

GoodwillAmortisation of goodwill is not allowed as a tax deductible expense.

Start-up expensesStart-up expenses are not specified in the law. However, pre-incorporation expenses might be disallowed since, generally, expenses incurred when there is no income are not allowed.

Interest expensesInterest paid or accrued to a resident is deductible as an expense. Interest paid to a non-resident will be allowed as a deduction in the year where the relevant WHT on interest has been remitted to the BURS.

Bad debtBad debts written off and specific provisions for bad debt are allowed as a deduction when computing taxable income. General provisions are not allowed as a deduction.

Charitable contributionsDonations made to (i) any educational institution recommended by the Ministry of Education or (ii) any sports clubs or sports associations recommended by the Ministry responsible for sports, and approved by the Commissioner General, shall be deducted when arriving at taxable income, limited to 20% of the chargeable income.

Fines and penaltiesPenalties and associated interest are not allowed as a deduction.

TaxesAny taxes paid are specifically disallowed in computing a company’s taxable income.

Other significant itemsAn allowance is granted for dwelling houses erected for employees by a business other than a mining business. The amount of the allowance is the lower of cost or BWP 25,000 for each dwelling house constructed.

A deduction of 200% of the cost of an approved training expenditure is allowed.

Companies with shareholders having 5% or more of equity, either directly or indirectly, are classified as close companies, and there are additional tax regulations in respect of these shareholders.

Small companies, that is resident private companies whose gross income does not exceed BWP 300,000, may elect that the company be taxed as a partnership.

Expenses incurred by the company for having its shares listed on the Botswana Stock Exchange are deductible in determining the chargeable income of the company.

Net operating lossesLosses may be carried forward for five years, with the exception of mining and prospecting operations, for which there is no time limit. There is no allowance for carrybacks.

PwC Worldwide Tax SummariesBotswana32

Botswana

Payments to foreign affiliatesRoyalties, interest, and service fees paid to foreign affiliates are generally deductible, provided such amounts are at arm’s length and WHT is paid.

In the case of a mining company, head office expenses allowed as a deduction in ascertaining gross revenue from mineral licence shall be limited to 1.5% of gross income for the year of assessment, and any excess of such expense above the limit shall be treated and taxed as a dividend.

Where the interest rate on a loan made by a foreign-based mining company to an affiliate mining company resident in Botswana is considered by the commissioner to be in excess of the market rate, such excess will be disallowed as a deduction and taxed as a dividend.

Group taxation

There are no concessions for group taxation, other than for wholly-owned subsidiary companies of the Botswana Development Corporation Limited (BDC).

BDC was established in 1970 to be the country’s main agency for commercial and industrial development. The government of Botswana owns 100% of the issued share capital of the Corporation.

Where in any tax year a wholly owned subsidiary of BDC has incurred any assessed loss, such member may, during the current tax year, by notice in writing to the Commissioner General, elect that the whole or part of such assessed loss shall be deducted in ascertaining the chargeable income of one or more of the other wholly owned subsidiaries.

Transfer pricingBotswana currently does not have any transfer pricing regulations, so transfer pricing is currently monitored through the anti-avoidance provisions contained in Section 36 of the Income Tax Act.

The arm’s-length principle should always be followed in transactions between related parties. If such transactions have created rights or obligations that would not normally be created between independent persons dealing at arm’s length, the Commissioner General may determine the liability in such manner as deemed appropriate. However, related party balances arising out of normal trading transactions (e.g. credit purchases with a 30 day credit period) would not be subjected to these provisions.

Interest (at prime rate) should be charged/provided on loans from shareholders/amounts due to related parties. If no interest has been charged/provided, in terms of the close company legislation, the BURS may deem interest at the prime rate prevailing at the beginning of the tax year, as income in the hands of the lender without allowing the corresponding interest as a charge against the profits of the borrower. The borrower is obligated to deduct WHT at the prevailing rate on the deemed interest.

Amounts due from shareholders/directors may be deemed as dividend income and shall form part of the taxable income of the borrower, in which event these will be taxed at the prevailing dividend WHT rate in the hands of the borrower.

Botswana 33www.pwc.com/taxsummaries

Botswana

Thin capitalisationThin capitalisation rules can be found in the Income Tax Act, but only in relation to mining companies and IFSC companies.

Where a foreign controlled resident mining company has a foreign debt-to-equity ratio in excess of 3:1 at any time during the year of assessment, the amount of interest paid by the resident company during that year on that part of the debt that exceeds the ratio shall be disallowed as a deduction, and the amount so disallowed shall be treated and taxed as a dividend.

In case of an IFSC company, where an amount of foreign debt interest is allowable as a deduction in a particular tax year and, at any time during that tax year, the total foreign debt exceeds the foreign equity product for that year, then the amount of foreign debt interest ascertained in accordance with the following formula will be disallowed:

I x (A/B) x (C/365)

A = amount of the excess of the total foreign debt over the foreign equity product.

B = the total foreign debt.

C = the number of days in that tax year during which the total foreign debt exceeded the foreign equity product by that amount.

I = the foreign debt interest.

Controlled foreign companies (CFCs)There are no CFC rules in Botswana.

Tax credits and incentives

To encourage investment in Botswana, extra tax relief on revenue or capital accounts will be granted for specific business development projects if the government is satisfied that such projects are beneficial to Botswana.

Foreign tax creditA credit for the foreign WHT payable is permitted under domestic law. The credit, which is offset against the tax charged in Botswana, shall be the lessor of (i) the tax payable in the foreign country or (ii) the tax charged under the Botswana Income Tax Act on such amount.

Withholding taxes

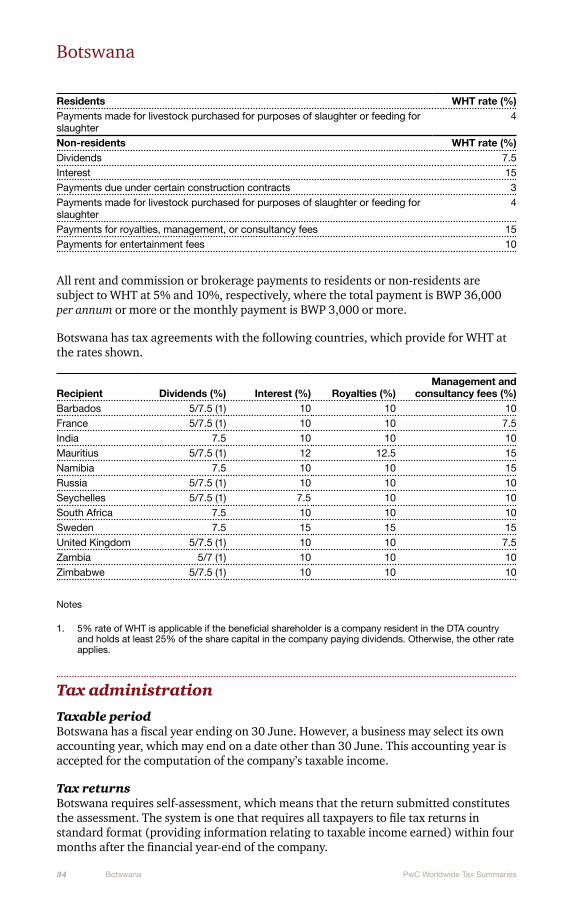

WHT, at the following rates, must be deducted from payments to residents and non-residents unless a DTA exists.

Residents WHT rate (%)Dividends 7.5Interest 10Payments due under certain construction contracts 3

PwC Worldwide Tax SummariesBotswana34

Botswana

Residents WHT rate (%)Payments made for livestock purchased for purposes of slaughter or feeding for slaughter

4

Non-residents WHT rate (%)Dividends 7.5Interest 15Payments due under certain construction contracts 3Payments made for livestock purchased for purposes of slaughter or feeding for slaughter

4

Payments for royalties, management, or consultancy fees 15Payments for entertainment fees 10

All rent and commission or brokerage payments to residents or non-residents are subject to WHT at 5% and 10%, respectively, where the total payment is BWP 36,000 per annum or more or the monthly payment is BWP 3,000 or more.

Botswana has tax agreements with the following countries, which provide for WHT at the rates shown.

Recipient Dividends (%) Interest (%) Royalties (%)Management and

consultancy fees (%)Barbados 5/7.5 (1) 10 10 10France 5/7.5 (1) 10 10 7.5India 7.5 10 10 10Mauritius 5/7.5 (1) 12 12.5 15Namibia 7.5 10 10 15Russia 5/7.5 (1) 10 10 10Seychelles 5/7.5 (1) 7.5 10 10South Africa 7.5 10 10 10Sweden 7.5 15 15 15United Kingdom 5/7.5 (1) 10 10 7.5Zambia 5/7 (1) 10 10 10Zimbabwe 5/7.5 (1) 10 10 10

Notes

1. 5% rate of WHT is applicable if the beneficial shareholder is a company resident in the DTA country and holds at least 25% of the share capital in the company paying dividends. Otherwise, the other rate applies.

Tax administration

Taxable periodBotswana has a fiscal year ending on 30 June. However, a business may select its own accounting year, which may end on a date other than 30 June. This accounting year is accepted for the computation of the company’s taxable income.

Tax returnsBotswana requires self-assessment, which means that the return submitted constitutes the assessment. The system is one that requires all taxpayers to file tax returns in standard format (providing information relating to taxable income earned) within four months after the financial year-end of the company.

Botswana 35www.pwc.com/taxsummaries

Botswana

Payment of taxUnder the self-assessment tax procedures, if the tax payable for a tax year exceeds BWP 50,000, then estimated tax is required to be paid in equal quarterly instalments over the period of 12 months ending on the company’s financial year-end date. Accordingly, the first quarterly payment should be made within three months of the beginning of the financial year and the balance quarterly payments at three monthly intervals thereafter. The final (balance) payment, if any, is to be made within four months from the end of the financial year, when submitting the return.

Where the tax is less than BWP 50,000, then the tax is payable within four months from the company’s financial year-end date.

Tax audit processThere is no prescribed audit process, and an audit can be initiated by any factor as determined by the BURS. The audit or inspection will commence with a request from the BURS for the taxpayer to make available any such records or information as may be required.

Statute of limitationsThe assessment should be made any time prior to the expiry of four years after the end of the tax year to which it relates to. Tax returns submitted that have been assessed may not be reopened after a period of four years from date of assessment by the BURS.

Topics of focus for tax authoritiesThe BURS is focusing on establishing and strengthening the Large Tax Payers Unit, minimising the tax gap, and introducing electronic filing.

Cabo Verde 36www.pwc.com/taxsummaries

Cabo Verde

PwC contact

Leendert VerschoorPricewaterhouseCoopers & Associados - SROC, Lda.Palácio SottomayorRua Sousa Martins 1 - 3º1069-316 LisboaPortugalTel: +351 213 599 642Email: [email protected]

Significant developments