worldwide insurance 2008 top 10 strategic initiatives: it...

TRANSCRIPT

November 2007, Financial Insights #FIN209565 Financial Insights: Insurance Advisory Service: Looking Ahead

Worldwide Insurance 2008 Top 10 Strategic Init iat ives: I t 's a Mad, Mad, Mad, Mad World of Insurance Opportunit ies

I n s u r a n c e A d v i s o r y S e r v i c e A s i a / P a c i f i c I n s u r a n c e A d v i s o r y S e r v i c e E u r o p e a n I n s u r a n c e A d v i s o r y S e r v i c e C a n a d i a n F i n a n c i a l A d v i s o r y S e r v i c e

LOOKING AHEAD #FIN209565

Barry Rabkin L i -May Chew Rober t Burbach Simona Macel la r i

F I NA N C I A L I NS I G H T S O P I NIO N

The risk environment insurers face � comprising the risk landscape, regulatory activities, and competitive dynamics � continues to be in flux. But risk is the price of opportunity. The insurance industry strategic initiatives discussed in our 2008 forecast represent a set of activities insurers need to successfully implement to decide whether they want to pay that price and if so, what effort � as defined by the set of 10 initiatives taken as a whole � they need to successfully compete. In this risk environment, insurers face three decisions; the winning insurers will be those that profitably grow their top line by identifying the right balance of the second and third of these options:

● Maintain the status quo by providing coverages for their traditional exposures

● Continually make small incremental changes to their risk portfolio by offering products or services for some new customers in existing markets without taking on substantial new risks

● Take a financial leap of (actuarial) faith by deciding to offer new products or services that are significantly different from their existing book of business

Glo

bal H

eadq

uarte

rs: 5

Spe

en S

treet

Fra

min

gham

, MA

0170

1 U

SA

P.

508.

620.

5533

F

.508

.988

.676

1

ww

w.fin

anci

al-in

sigh

ts.c

om

#FIN209565 ©2007 Financial Insights, an IDC Company

T A B L E O F C O N T E N T S

P

In This Report 1 Methodology ............................................................................................................................................. 1 Situat ion Overview 1 Shifting Landscape of Risk: Mad with Opportunities or Just Madness?.................................................... 1 2007: A Gathering Storm Facing Insurers ................................................................................................ 3

A P&C Insurance Perspective ........................................................................................................... 3 An L&A Insurance Perspective.......................................................................................................... 4

2008: Insurance Industry's Tipping Point?................................................................................................ 5 Future Outlook 6 Top 10 Strategic Initiatives for 2008 ......................................................................................................... 8

Regulatory Compliance: Local Regulations, Global Impact............................................................... 8 Growth: Acquisitive and Organic Growth Both in Play....................................................................... 10 Core Administrative Systems: Rationalization Finally Under Way?................................................... 12 Ease of Doing Business: EDB Cascades Throughout the Entire Value Chain .................................. 12 Cost Improvement: Taking Center Stage .......................................................................................... 14 Risk Management: Responding to a Changing Landscape............................................................... 15 Channel Management: The Quest for Balance.................................................................................. 17 Competitive Posture: Competing as an Enterprise ............................................................................ 18 Business Models: The New Strategic Focus ..................................................................................... 19 Technology Refresh: The Web and Concomitant Business Applications Continue to Evolve ........... 20

Essential Guidance 22 Actions for Insurance Companies............................................................................................................. 22 Actions for Vendors .................................................................................................................................. 23 Learn More 25 Related Research..................................................................................................................................... 25

©2007 Financial Insights, an IDC Company #FIN209565

L I S T O F T A B L E S

P

1 Potential P&C Liability Claims from Global Warming ................................................................... 4

2 Selected U.S. Demographic Attributes.........................................................................................5

3 U.S. IRA Assets by Type of Financial Institution, 2001�2006 ...................................................... 6

4 Top 10 Strategic Initiatives for Global Insurance Industry for 2008.............................................. 7

5 Selected Global Regulatory Compliance Issues ......................................................................... 9

6 2008 Top 10 Strategic Initiatives by Business Discipline and Rank ............................................. 24

#FIN209565 ©2007 Financial Insights, an IDC Company

L I S T O F F I G U R E S

P

1 The Shrinking World of Risk ........................................................................................................ 2

2 Mapping Customer Lifetime Value ............................................................................................... 11

3 Selected Insurance Company Business Functions ...................................................................... 13

4 Insurance Industry BPO Investment Planning Horizon for Four Key Cross-Industry Functions...................................................................................................................................... 15

5 Changing Landscape of Risk ....................................................................................................... 16

6 Distribution Channel Management Vision .................................................................................... 18

7 Competing as an Enterprise......................................................................................................... 19

8 Business Models as Architectural Plans ...................................................................................... 20

9 The Evolving Web........................................................................................................................ 22

10 Willingness to Pay the Price of Opportunity ................................................................................. 23

©2007 Financial Insights, an IDC Company #FIN209565 Page 1

I N T H I S R E P OR T

Our third annual analysis of strategic IT initiatives for the insurance industry incorporates perspectives from our analysts in North America, Europe, and Asia. In this report, we identify the top 10 initiatives that will have key strategic importance during 2008 for life and annuity (L&A) and property and casualty (P&C) insurance companies around the world. We describe these initiatives, examine their impact on the insurance industry and the technology firms that serve them, and explain why they are (or should be) on the minds of chief executive officers at every insurance company worldwide.

The initiatives are not necessarily those of greatest spending, but making the right decision about these initiatives will position insurers well for the future. We offer a global perspective, focusing on trends that are relevant for insurers around the world. Our regional practices covering Europe and Asia/Pacific will publish companion studies highlighting the top 10 initiatives in the insurance industry for their respective regions.

M e t h o d o l o g y

Financial Insights surveyed and talked to insurance companies, technology firms, and other market participants around the world to gain an understanding of the initiatives that were rising to the surface as top priorities. This top 10 report represents a forward-thinking synthesis of all the data and discussions as well as our experience as insurance industry and technology analysts. Readers should not consider this discussion as an operational report or a report focused primarily on 2008. Instead, we discuss a portfolio of strategic initiatives that insurers must consider not only for 2008 but the five years ahead to better position themselves for longer-term competitive success.

S I T U A TI O N O VE R VI E W

S h i f t i n g L a n d s c a p e o f R i s k : M a d w i t h O p p o r t u n i t i e s o r J u s t M a d n e s s ?

The world continues to change and, in so doing, reshapes the landscape of risk. This year, traditional risks, such as product liability, are leaping to the foreground. Emerging risks, such as global warming, are quickly gaining visibility, and other risks, such as terrorism, unfortunately remain only too visible on the risk landscape.

Regulators around the world also reshape the risk landscape. Their actions, as well as the existing and emerging risks, constantly drive

Page 2 #FIN209565 ©2007 Financial Insights, an IDC Company

insurers to determine if, how, and for what price they want to enter new markets or stay in existing markets. Increasingly, there are instances of regulators in one part of the world impacting both regulators and insurers in other parts of the world. The date for the European Union's (EU's) Solvency II regulation may have slipped again � to 2012 � but insurers in Asia/Pacific and Canada are either making plans or considering the implications of following its requirements.

As Figure 1 graphically illustrates, the world of risk is getting much, much smaller. The forces behind this shrinking include:

● Regulators worldwide are paying more attention to each other's philosophies, whether EU's Solvency II or the United States' Sarbanes-Oxley Act.

● Insurers regardless of geographic location are paying attention to regulators in other countries, whether they have international operations in the affected countries or not.

● A growing number of exposures can or do impact individuals and businesses across the globe such as terrorism, product recalls, and potential planetary pandemics.

F I G U R E 1

T h e S h r i n k i n g W o r l d o f R i s k

Terrorism; World Trade/Recalls; Planetary Pandemics

Rationalized Global Regulatory Practices

Terrorism; World Trade/Recalls; Planetary Pandemics

Rationalized Global Regulatory Practices

Source: Financial Insights, 2007

©2007 Financial Insights, an IDC Company #FIN209565 Page 3

The intent of this report is to highlight for insurer and technology communities those strategic initiatives that will enable insurers to profit from the growing number of opportunities in this ever-shrinking world in 2008 and throughout the next five years.

2 0 0 7 : A G a t h e r i n g S t o r m F a c i n g I n s u r e r s

A P&C Insurance Perspective

The essence of achieving long-term success in the P&C insurance industry is having the ability to search and capture quality profit streams from best-of-class underwriting. This year, however, P&C insurers are striving to find or maintain a strong competitive position in a softening market.

Forces exist that will only exacerbate insurers' competitive position in 2008. P&C insurers have seen fewer hurricanes hit the U.S. coastline, but they've also seen floods in the United Kingdom and Storm Kyrill in Germany. Insurers have seen terrorism attacks in London, Frankfurt, and Glasgow, Scotland, but it's still not resolved how the EU and the U.S. government will shape and renew their respective government-backed terrorism legislation.

Other challenges include:

● Global warming. Several reports published this year strongly illustrate that P&C insurers and reinsurers ignore global warming at their financial peril regardless of their personal beliefs. A United Nations report titled Climate Change 2007 linked human activity � the burning of fossil fuels � to global warming. Three climate change experts stated in their recent paper on the topic that the insurance industry faces material liability exposures (see Table 1 for a list of potential liability risks).

● Product recalls. In 2007, China has become synonymous with product recalls. A wide range of products � pet foods, tires, toothpaste, and toys � sold in the EU, Canada, and the United States have been recalled. Mattel had three major recalls during the summer involving toys with unsafe levels of lead paint. The importer and the firm selling the product, regardless of where the product comes from, are potentially liable for damages.

● Spreading philosophy of entitlement. The new French government plans to draft legislation that would allow class-action suits by the end of this year. It would allow contingency fees for neither lawyers nor elected judges and jury trials. The legislation may include an opt-out principle that would enable consumers to benefit from a class action without formally joining it or appearing before a judge.

Page 4 #FIN209565 ©2007 Financial Insights, an IDC Company

T A B L E 1

P o t e n t i a l P & C L i a b i l i t y C l a i m s f r o m G l o b a l W a r m i n g

Line of Business Potential Claims Due To Commercial general liability • Negligence

• Personal injury • Third-party business interruption

Product liability • Materials contributing to climate change Environmental liability • Emitters of greenhouse gases Management liability • Corporate directors and officers working for companies that are emitters Political risk • New government policies established because of climate change (e.g.,

surtaxes on fuel consumption)

Source: Best's Review, 2007

An L&A Insurance Perspective

The essence of competitive success for L&A insurers centers on their ability to profitably meet or exceed the needs and expectations of various demographic groups. For L&A insurers, demographics is destiny. In 2007, L&A insurers in the United States specifically continued to face three challenges in managing current and future demographic changes (see Table 2):

● Managing the quickly approaching retirement tipping point in 2011 as boomers (people born between 1946 and 1964) begin to look to financial institutions for asset withdrawal/asset management advice, products, and services

● Offering products and services to a growing, ethnically diverse market in a manner that ethnic groups relate to and appreciate

● Creating or maintaining a portfolio of distribution channels, including Internet portals, required to reach and serve their target markets, regardless of age, ethnicity, or other demographic characteristic

The rest of the world is also impacted by the aging of the population. Two-thirds of all the seniors in the world who have ever lived are alive today. EMEA insurers are leveraging this fact to generate growth from products they say are geared specifically to the "third age" demographic segment as well as savings and retirement products for pre-retirees and seniors. In Japan, residents over 60 years of age compose a quarter of the population, a level forecast to reach 42% by 2040. With almost 60% of Japan's financial assets being held by the ballooning "silver population," demand for annuity products will continue to soar.

©2007 Financial Insights, an IDC Company #FIN209565 Page 5

T A B L E 2

S e l e c t e d U . S . D e m o g r a p h i c A t t r i b u t e s

Demographic Domain Attributes Living longer • Life expectancy of a newborn in 2005 is 78 years, up from 70 years in 1955.

• Half of Americans who reach 65 in 2007 are expected to live to age 83, and one-fifth are expected to reach age 90.

Living elsewhere • In 1910, each of the 10 most populous cities was within roughly 500 miles of the Canadian border.

• 2006 estimates show that seven of the top 10 most populous cities � and three of the top 5 � are in states that border Mexico.

• The 50 fastest-growing metropolitan areas are concentrated in the west and south.

Increasing diversity • Nearly one in every 10 of the nation's 3,411 counties has a population that is more than 50% minority.

Sources: CDC National Center for Health Statistics, American Council of Life Insurers, and U.S. Census Bureau, 2007

2 0 0 8 : I n s u r a n c e I n d u s t r y ' s T i p p i n g P o i n t ?

The insurance industry will be market tested in 2008 by the changing risk landscape, regulatory actions, and concomitant competitor initiatives. How insurers react to these challenges will determine which way their future will tip: making do with a status quo that never really stays the same or gaining a competitive edge.

L&A insurers will need to develop products and services that consumers readily perceive as being better than the retirement offerings from investment firms and banks. In particular, capturing IRA assets hasn't been a competency of the U.S. L&A industry compared with other financial service institutions (see Table 3). Mutual fund and brokerage firms are continuing to grow their share of these assets.

L&A insurers, like other financial services industries selling asset accumulation or asset management products, will have to constantly prove to their prospects and regulators that they have suitable products and can be trusted not to employ inappropriate sales tactics. Attorneys general in at least two states in the United States filed suits against insurers in 2007. They and other state attorneys general will be watching L&A insurers extremely closely regarding annuity and long-term care (LTC) sales in 2008. In Japan, a number of life insurers admitted to nonpayment of $785 million of legitimate insurance claims.

Page 6 #FIN209565 ©2007 Financial Insights, an IDC Company

T A B L E 3

U . S . I R A A s s e t s b y T y p e o f F i n a n c i a l I n s t i t u t i o n , 2 0 0 1 � 2 0 0 6 ( $ B )

Year Mutual Funds Bank and Thrift

Deposits Life Insurance

Companies

Securities Held in Brokerage

Accounts Total Assets 2001 1,169 255 211 984 2,619 2002 1,045 263 268 956 2,533 2003 1,313 268 285 1,127 2,993 2004 1,494 270 282 1,238 3,284 2005 1,667 278 308 1,379 3,632 2006 1,972 313 323 1,624 4,232

Source: The U.S. Retirement Market, 2006, Investment Company Institute, July 2007

However, we expect that even in this more intense environment of being watched by government officials and regulators, L&A insurers will continue to develop and sell more complex products that leverage their underwriting skills in asset accumulation, asset management, and health issues. We will see insurers in 2008 offering products that commingle coverages from life insurance or annuities with long-term care coverage or annuities with 401(k) products.

P&C insurers will have to determine how to profitably succeed in 2008's soft market. Moreover, the P&C industry will be expected to articulate its risk management philosophy concerning global warming. We expect to see more P&C insurers follow a bifurcated approach:

● Providing incentives through reduced premiums to customers who reduce their carbon footprint in some measurable way

● Introducing insurance coverages with fairly restrictive terms and conditions for product liability or management liability exposures associated with corporate products or corporate actions that allegedly cause or exacerbate global warming

F U T U R E O UT L O O K

What constitutes opportunity? For both L&A and P&C insurers, one key metric to measure opportunity is realized profitability. Another key metric is to determine how much revenue or profit insurers are generating from products and services introduced to the market within the last two or three years. However, by the very nature of their businesses, the duration is different for L&A and P&C insurers. L&A insurers and commercial P&C insurers selling liability coverages must view their profitable opportunities through lenses focused several decades ahead in the future. Personal P&C insurers must balance the need to pay strict attention to the profit they generate within a 12-

©2007 Financial Insights, an IDC Company #FIN209565 Page 7

month period against identifying which of their existing policyholders they want to keep longer.

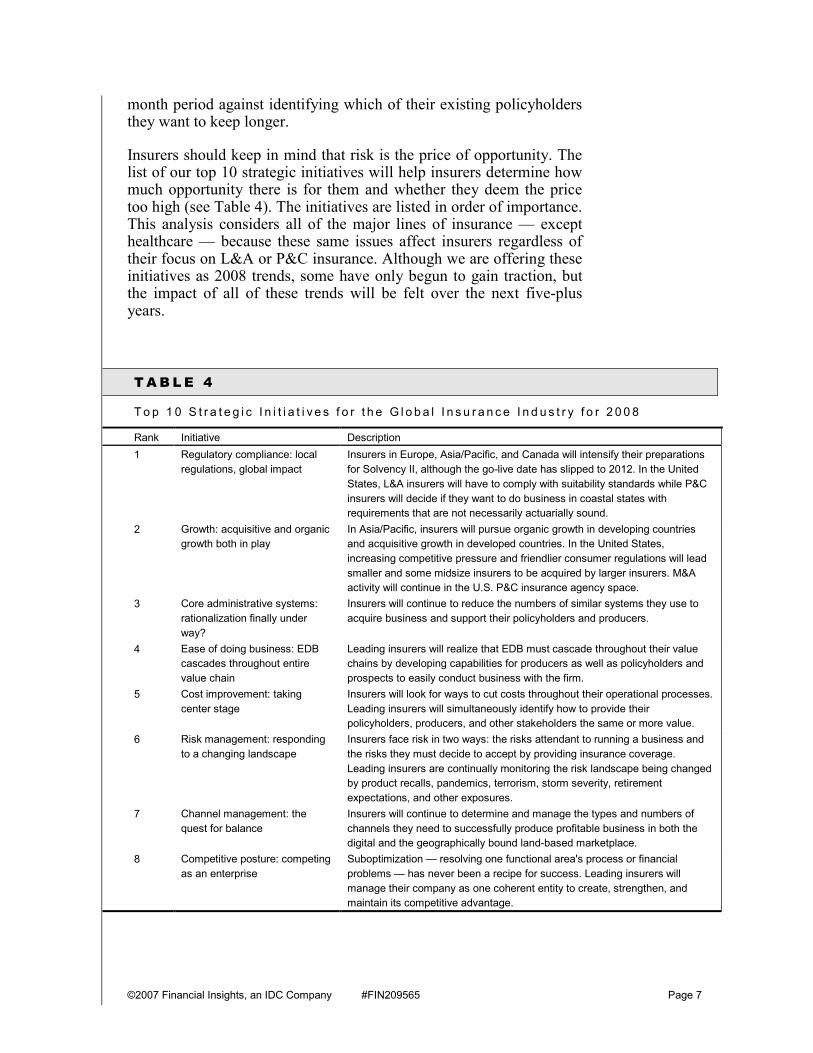

Insurers should keep in mind that risk is the price of opportunity. The list of our top 10 strategic initiatives will help insurers determine how much opportunity there is for them and whether they deem the price too high (see Table 4). The initiatives are listed in order of importance. This analysis considers all of the major lines of insurance � except healthcare � because these same issues affect insurers regardless of their focus on L&A or P&C insurance. Although we are offering these initiatives as 2008 trends, some have only begun to gain traction, but the impact of all of these trends will be felt over the next five-plus years.

T A B L E 4

T o p 1 0 S t r a t e g i c I n i t i a t i v e s f o r t h e G l o b a l I n s u r a n c e I n d u s t r y f o r 2 0 0 8

Rank Initiative Description 1 Regulatory compliance: local

regulations, global impact Insurers in Europe, Asia/Pacific, and Canada will intensify their preparations for Solvency II, although the go-live date has slipped to 2012. In the United States, L&A insurers will have to comply with suitability standards while P&C insurers will decide if they want to do business in coastal states with requirements that are not necessarily actuarially sound.

2 Growth: acquisitive and organic growth both in play

In Asia/Pacific, insurers will pursue organic growth in developing countries and acquisitive growth in developed countries. In the United States, increasing competitive pressure and friendlier consumer regulations will lead smaller and some midsize insurers to be acquired by larger insurers. M&A activity will continue in the U.S. P&C insurance agency space.

3 Core administrative systems: rationalization finally under way?

Insurers will continue to reduce the numbers of similar systems they use to acquire business and support their policyholders and producers.

4 Ease of doing business: EDB cascades throughout entire value chain

Leading insurers will realize that EDB must cascade throughout their value chains by developing capabilities for producers as well as policyholders and prospects to easily conduct business with the firm.

5 Cost improvement: taking center stage

Insurers will look for ways to cut costs throughout their operational processes. Leading insurers will simultaneously identify how to provide their policyholders, producers, and other stakeholders the same or more value.

6 Risk management: responding to a changing landscape

Insurers face risk in two ways: the risks attendant to running a business and the risks they must decide to accept by providing insurance coverage. Leading insurers are continually monitoring the risk landscape being changed by product recalls, pandemics, terrorism, storm severity, retirement expectations, and other exposures.

7 Channel management: the quest for balance

Insurers will continue to determine and manage the types and numbers of channels they need to successfully produce profitable business in both the digital and the geographically bound land-based marketplace.

8 Competitive posture: competing as an enterprise

Suboptimization � resolving one functional area's process or financial problems � has never been a recipe for success. Leading insurers will manage their company as one coherent entity to create, strengthen, and maintain its competitive advantage.

Page 8 #FIN209565 ©2007 Financial Insights, an IDC Company

T A B L E 4

T o p 1 0 S t r a t e g i c I n i t i a t i v e s f o r t h e G l o b a l I n s u r a n c e I n d u s t r y f o r 2 0 0 8

Rank Initiative Description 9 Business models: the new

strategic focus Having the right price, the right product, or the right distribution channel is necessary but not sufficient. Leading insurers realize that competitive success in a continually changing marketplace demands their having a business model that enables agility, flexibility, and speed.

10 Technology refresh: the Web and concomitant business applications continue to evolve

Insurers will look more to emerging Web technologies (i.e., blogs and Second Life) and continue to build applications using existing Web technologies such as SOA, Web services, and business process management to sharpen their business strategies.

Source: Financial Insights, 2007

T o p 1 0 S t r a t e g i c I n i t i a t i v e s f o r 2 0 0 8

Regulatory Compliance: Local Regulations, Global Impact

Physicians take an oath to do no harm to their patients and to guide their diagnoses and treatment protocols. Regulators may not address life-threatening problems, but they do have to find the right balance between protecting both purchasers of and providers of insurance. Leaning too far to the consumer side of the ledger could create actuarially unsound conditions. Leaning too far to the insurance side of the ledger could create conditions in which insurance is either unavailable or unaffordable.

Asian insurers are facing a relatively easier environment than their peers in other regions. The ongoing liberalization efforts are making Asia's insurance markets more attractive. Governments in the area are reviewing and relaxing their regulatory frameworks to strike a better balance between promoting innovation and developing the market. State monopolies are being dismantled. Emerging economies are adopting open market concepts. All of this regulatory activity is driving international insurers to place Asia at the top of their own expansion lists. Moreover, this regulatory activity is causing the pace of consolidation to quicken as an increasing number of insurers are finding it hard to achieve the economies of scale and scope they need to profitably compete against the widening pool of insurers.

Insurers in the United States and EMEA are facing stricter regulatory conditions (see Table 5). L&A and P&C insurers are impacted by several factors:

● Terrorism legislation currently being shaped by both the EU and the United States would require insurers to take on more of the financial risk.

©2007 Financial Insights, an IDC Company #FIN209565 Page 9

● An Optional Federal Charter (OFC) would permit insurers doing business in the United States the self-selecting option to choose a single federal regulator or continue being regulated by each of the 50 state insurance commissioners.

● Similar to Basel II in the banking industry, Solvency II requires insurance companies to set aside regulatory capital based on the amount of risk they face, with incentives in the form of reduced capital requirements for companies that have strong risk management systems and robust internal controls. Insurers in Asia/Pacific are also making plans to operate under Solvency II requirements.

● In addition to needing to comply with Solvency II, P&C insurers in the United Kingdom also have to comply with contract certainty. According to the Financial Services Authority, which is an independent body that regulates the financial services industry in the United Kingdom, "contract certainty is the timely agreement of the terms of an insurance contract and provision of the insurance contract details to a customer. It brings greater certainty for buyers about what they have bought and for insurers about the risks they are covering, while also reducing risks for brokers."

● Suitability requirements are being considered in the United States to ensure that L&A insurers sell the appropriate annuity, long-term care, or other products to older prospects.

● P&C insurers doing business in Florida cannot form new so-called pup companies that do business only in that one state. This means that P&C insurers thinking about conducting business in Florida will have to decide if they want to share that state's hurricane risks with the risks they insure in all other states.

T A B L E 5

S e l e c t e d G l o b a l R e g u l a t o r y C o m p l i a n c e I s s u e s

Insurer Type Issues Both L&A and P&C • Terrorism legislation (EU and United States)

• Optional Federal Charter (United States) • Solvency II (EMEA and Asia/Pacific)

L&A • Suitability (United States) P&C • Contract certainty (United Kingdom)

• No �pup� companies (Florida, United States)

Source: Financial Insights, 2007

Page 10 #FIN209565 ©2007 Financial Insights, an IDC Company

Insurers in one country � even if they are regional players � can no longer afford to ignore risk events or regulatory actions that seem to initially impact only other countries or other segments of financial services. It will be madness for either life or nonlife insurers to myopically focus solely on their own geographic area of risks or industry.

Growth: Acquisitive and Organic Growth Both in Play

Asia insurers are expanding their networks into other emerging countries within the region to establish their brands before going global. Insurers from Australia, Taiwan, Japan, and South Korea are venturing into neighboring Asia countries to establish new networks of channels and customers. Asia insurers are also generating organic growth by developing products to meet market demand for critical illness, annuities, and other products that meet the increasing personal wealth and standard of living in the region.

European insurers will continue building their operations in the small but fast-growing markets in both Central Europe and Asia/Pacific. Some European insurers have experienced dramatic growth in the Netherlands due to the insurance industry's management of the Dutch health system.

In the United States, the major growth trend of 2007 has been the emerging wave of P&C insurance agencies or insurance brokers going private, such as Hub International, USI Holdings, and Alliant Insurance Services. In each case, the management team stated it was committed to providing value to its policyholder and insurance carrier clients and to generating sustainable growth. One of these brokers specifically mentioned that 13,000 brokers in the marketplace accounting for over $20 billion in total annual revenue still remain, so acquisition success will remain a core competency of the firm.

Large insurance merger and acquisition activity in the U.S. insurance carrier space remains infrequent at best. But Liberty Mutual's $2.7 billion acquisition of Ohio Casualty Corp. in the middle of this year demonstrated that even the mega�tier 1 insurers are looking for acquisitions when the transaction broadens their reach into additional markets as this acquisition did for Liberty Mutual.

For either L&A or P&C insurers, organic growth is generated by one of two ways:

● New customers from existing markets

● New customers from new markets

Winning L&A insurers will take both paths in 2008 by developing products to better meet the needs of the pre-retirement market.

©2007 Financial Insights, an IDC Company #FIN209565 Page 11

Specifically, life insurers are developing hybrid long-term care and life insurance products, LTC and annuity products, or annuity products within 401(k) plans.

Leading insurers will use the more traditional business analytics as well as newer predictive analytics tools. Insurers use the former to segment their existing customers, producers, and territories. L&A and P&C insurers will use the latter to develop models and estimates of customer lifetime value (see Figure 2) while P&C insurers will develop estimates of probable maximum loss for severe weather-prone geographies.

F I G U R E 2

M a p p i n g C u s t o m e r L i f e t i m e V a l u e

Low HighGenerated Revenue over Time

Cus

tom

er C

osts

ove

r Tim

e

Low

High

Sweet Spot

Low HighGenerated Revenue over Time

Cus

tom

er C

osts

ove

r Tim

e

Low

High

Sweet Spot

Source: Financial Insights, 2007

The customer costs to the insurer over time include:

● Marketing costs to attract prospective customers to the firm or attract existing policyholders to consider new products or services

● Business acquisition costs, including sales and distribution expenses

● Servicing costs, including use of customer service representatives, servicing agents, or even home office staff to research and resolve policyholder problems or inquiries

Page 12 #FIN209565 ©2007 Financial Insights, an IDC Company

The revenue streams include not just premium and fee income but net revenue generated from lowering business acquisition costs and lowering service costs. Insurers are using all of these cost and revenue elements as they model and develop estimates of their customer lifetime value by products, by geographies, and by channel.

Core Administrative Systems: Rationalization Finally Under Way?

Market pressures are forcing insurers in the Asian region to streamline their core administrative system processes. In particular, India is changing from a state monopoly to an open market. Insurers are realizing that to better compete, they must update their decades-old core systems to move into new business areas and augment their existing lines of business. Leading insurers are also investing in advanced analytics to drive better decision making as well as improve their client and producer relationship capabilities.

EMEA insurers have almost completed a significant number of their IT infrastructure consolidation initiatives in 2007. In 2008, these insurers will address the standardization and rationalization of their core administrative systems including underwriting, claims, and risk management.

In the United States, P&C insurers are replacing their decades-old billing systems (see U.S. Property and Casualty Insurance Billing 2007�2012 Spending Forecast and Analysis: $how Me the Money!, Financial Insights #FIN208099, August 2007).

Ease of Doing Business: EDB Cascades Throughout the Entire Value Chain

The concept of being easy to do business with (EDB) as we know it in the insurance industry has been discussed for decades. EDB is primarily associated with the notion of making it easy for insurance agents or brokers to do business with the insurance carrier.

However, leading insurers realize they have to make it easy for not just their producers but also other major stakeholders such as their policyholders and even prospective customers to do business with the firm. These insurers are reviewing all of the major customer touch points (see Figure 3) to see how they can make these processes simpler and faster for their stakeholders to conduct business with them. Leading insurers have developed or are developing:

● Marketing processes that reach out to clients and prospects to make them aware of the firm's products and services through a growing panoply of media

©2007 Financial Insights, an IDC Company #FIN209565 Page 13

● Underwriting systems based on ACORD standards that both quickly capture the required data needed and enable real-time or near-real-time decisions about the policy application

● Distribution management systems that make it easier for agents � whether captive or independent � to do business with the firm because uploads and downloads are synchronized effectively and efficiently, producers can track status of policy applications or their commission payments, and producers can access whatever transaction or administrative query their policyholders have conducted with the insurer

● More responsive customer-facing capabilities to support policy administration transactions or queries using customer information management systems that provide a 360-degree view of all the products, services, and information queries associated with each policyholder (These systems also help identify cross-sell and upsell opportunities for producers or lead generation by customer service representatives.)

F I G U R E 3

S e l e c t e d I n s u r a n c e C o m p a n y B u s i n e s s F u n c t i o n s

Marketing Product Development

Strategy and Decision Support

Policy Administration and Customer Service Functions

Dis

trib

utio

n

Operational Functions

Human Resources; F&A, Procurement Selected Enterprise Resource Functions

Strategy and Marketing Functions

Und

erw

ritin

g

Cla

ims

Marketing Product Development

Strategy and Decision Support

Policy Administration and Customer Service Functions

Dis

trib

utio

n

Operational Functions

Human Resources; F&A, Procurement Selected Enterprise Resource Functions

Strategy and Marketing Functions

Und

erw

ritin

g

Cla

ims

Note: Customer touch points are in red.

Source: Financial Insights, 2007

Page 14 #FIN209565 ©2007 Financial Insights, an IDC Company

Cost Improvement: Taking Center Stage

Cost containment is taking center stage in Asia (along with growth). With increasing demand for financial and resource capacity to better manage more complex risks, including infrastructure projects and liability exposures, Asia/Pacific insurance chief executives are developing new strategies to control costs. This encompasses improving their specific capabilities in underwriting, risk management, and customer analytics as well as continuing to lower their operational costs.

Canadian insurers are also actively pursuing strategies to control expenses and remove costs. In response to a Financial Insights survey (see Canadian Insurance: Top Strategic Priorities and Key Enabling Technologies for 2007, Financial Insights #FIN208918, October 2007), insurers in Canada stated that changing customer demographics, an evolving regulatory environment, and increased competition are all influencing the operational capabilities needed to successfully compete.

EMEA insurers will continue to increasingly pursue offshore delivery and business process outsourcing (BPO) to control costs in addition to standardizing and rationalizing their core administrative systems. However, U.S. insurers are only looking to BPO to contain costs for select enterprisewide functions. An IDC survey of insurance executives found that insurers are currently using or planning to use BPO for human resources (HR), finance and accounting (F&A), procurement, and customer care (see Promises, Promises: Are U.S. Insurers BPO Believers Yet?, Financial Insights #FIN208697, September 2007). Insurers with 2,500�4,999 employees are planning to move faster to use BPO for all four of these functions than insurers with 5,000+ employees (see Figure 4).

©2007 Financial Insights, an IDC Company #FIN209565 Page 15

F I G U R E 4

I n s u r a n c e I n d u s t r y B P O I n v e s t m e n t P l a n n i n g H o r i z o n f o r F o u r K e y C r o s s - I n d u s t r y F u n c t i o n s

Shorter Term Longer Term

Within 12 months

Greater than 36 months12�24 months 24�36 months

Customer care Human resources

Procurement

F&A (insurers with 2,500�4,999 employees)

F&A (insurers with 5,000 or more employees)

Shorter Term Longer Term

Within 12 months

Greater than 36 months12�24 months 24�36 months

Customer care Human resources

Procurement

F&A (insurers with 2,500�4,999 employees)

F&A (insurers with 5,000 or more employees)

Base = insurers with at least 2,500 employees

Source: IDC's Vertical Market IT Solutions Survey, 2007

Risk Management: Responding to a Changing Landscape

The risk landscape is always in flux, presenting both L&A and P&C insurers with opportunities for new products or services. Of course, some insurers decide to avoid or minimize their exposure to some risks. Leading insurers determine how they can generate long-term profitability by covering risk in a way that benefits both the policyholder and the firm. Leading insurers accomplish this by developing a strategic approach to decide:

● Which risks they will cover with what types of insurance products at what price points

● How they will go to market to inform prospective clients that need insurance coverage for the specific risks

● How to best service both policyholders who purchase and channels that sell the insurance products for the specific risks

In 2008, leading insurers will have to decide what they want to do with two types of risk (see Figure 5):

● Risks that are continuing to demand attention: These risks include coastal property exposure in the United States and potentially flood plains in some parts of Europe, product liability associated with product recalls from Mattel or Topps Meat Plant, retirement risk of outliving one's assets, and global warming as more lawsuits are brought against companies whose products allegedly contribute to the build-up of greenhouse gases.

Page 16 #FIN209565 ©2007 Financial Insights, an IDC Company

● Risks that are just over the horizon: These risks include exposure from genetic engineering � and could include discrimination claims against life insurers or employers or errors and omissions (E&O) claims against genetic testing laboratories due to false positive results � and claims from nanotechnology exposures that are limited only by plaintiffs' attorneys' imaginations.

F I G U R E 5

C h a n g i n g L a n d s c a p e o f R i s k

Type of RiskTraditional Current Emerging

Insu

rabi

lity

High

LowGenetic engineering

Global warming

Nanotechnology

Terrorism

Asbestos

Silicosis

Coastal properties

Health

Cyberrisk

AutoHome

Marine

Life

Product liability

Medical liability

Natural catastrophes

Retirement

Type of RiskTraditional Current Emerging

Insu

rabi

lity

High

LowGenetic engineering

Global warming

Nanotechnology

Terrorism

Asbestos

Silicosis

Coastal properties

Health

Cyberrisk

AutoHome

Marine

Life

Product liability

Medical liability

Natural catastrophes

Retirement

Source: Financial Insights, 2007

The winning insurers will be those that develop models capturing the density or concentration of risk they will have in their portfolios for both specific risks and specific geographies. These insurers will also be proficient with predictive analytics and text mining because they will operate with the realization that data spans the spectrum from structured to unstructured data.

These insurers will also be continually scanning the environment for new risks and the changing nature of existing risks. They will constantly update both the more general risk landscape and the company's acceptable risk landscape to better understand where their profit streams will be generated.

©2007 Financial Insights, an IDC Company #FIN209565 Page 17

Channel Management: The Quest for Balance

Insurers continually wrestle with which channels to use to best reach their targeted customers and how to best manage the distribution channels they have or want. One interesting facet of the first issue is that the answer continually changes because the customers to be targeted depend on demographic shifts, business formation, and even availability of technology to prospective customers, producers, and the insurers themselves.

In Canada, insurers are increasingly both broadening their product range and moving into new distribution channels. In Asia/Pacific countries, a growing number of life insurance companies are using direct marketing to augment their insurance agencies. In the United Kingdom, a significant amount of automobile and homeowner's insurance is sold through alternative channels such as the Internet or even supermarkets.

Bancassurance for life insurance remains a critical channel in most of the world outside of the United States. Bancassurance represents 65% of life insurance premiums in Spain, 60% in France and Portugal, 50% in Belgium and Italy, and 47% in South Korea.

In 2008, an increasing number of insurers will develop a vision of a distribution channel management system having four key attributes (see Figure 6):

● Rich perspective. This attribute encompasses insurers' ability to understand all of the business they generate through any one channel in its totality. The attribute also enables insurers to get a single view of all the applicable channel data � territorial management data, channel governance data, and channel financial data � in a single view.

● Timeliness. This attribute addresses insurers' need to have real-time or near-real-time data flow between the channel and the insurer. The attribute also speaks to the insurer being able to create ad hoc customizable reports whenever needed quickly.

● Ability to work well with others. This attribute addresses the distribution channel management suite being plug-and-play between all of its own components as well as with the requisite insurer systems such as the financial systems or the channel reward and recognition systems. The attribute also addresses the need for the distribution channel management system to be easily accessible and have a customizable interface.

● Seamlessness. This attribute addresses the need for all the data that is flowing through the distribution channel management suite to be integrated.

Page 18 #FIN209565 ©2007 Financial Insights, an IDC Company

F I G U R E 6

D i s t r i b u t i o n C h a n n e l M a n a g e m e n t V i s i o n

Timeliness

Rich perspective

Seamlessness

Ability to work well with others

KeyAttributes

Timeliness

Rich perspective

Seamlessness

Ability to work well with others

KeyAttributes

Source: Financial Insights, 2007

Competitive Posture: Competing as an Enterprise

Insurance companies have traditionally suboptimized their various operational departments (e.g., marketing, underwriting, claims, customer service) depending on which area needed improvements most. But external stakeholders such as prospects, policyholders, or producers view the insurance company as one integrated firm that they do business with and not a compilation of functions.

Leading insurers in 2008 will begin to weave their various business functional processes together (see Figure 7) to better compete as a single entity in their markets of choice. These insurers will accomplish this by using ACORD standards and through more effective data management. These insurers will accomplish this by:

● Identifying the data flows they use and need throughout their extended value webs (These leading insurers will operate on the philosophy that their information flows are the lifeblood of a digital supply chain connecting all of their stakeholders, data providers, and internal functions.)

● Managing all of their business processes as a coherent whole even if some processes are managed by the insurance company and other processes are supported by one or more outsourcers

©2007 Financial Insights, an IDC Company #FIN209565 Page 19

F I G U R E 7

C o m p e t i n g a s a n E n t e r p r i s e

Weaving Processes and Data Flows Together

Weaving Processes and Data Flows Together

Source: Financial Insights, 2007

Business Models: The New Strategic Focus

Leading insurers in 2008 will realize that the business model is the new basis of competition. In a marketplace that is continually being reshaped by new risks, regulatory actions, competitive moves, and even new methods of applying technology, only insurers that can quickly adapt will succeed. To accomplish that, insurers must have a coherent business model that supports the firm's strategic vision. That also means the leading insurers will be the firms with a coherent strategy for uniquely differentiating themselves in the marketplace.

Some insurers will decide to remain or become:

● Customer centric, such as USAA in the United States or Directline in the United Kingdom

● A product manufacturer, such as John Hancock (a subsidiary of ManuLife)

● Low cost, such as GEICO

● Distribution agnostic/channel rich, like any number of insurers that use captive agencies, independent agencies, and the Internet to reach and serve their customers

Essentially, business models are similar to architectural plans (see Figure 8). The business model encompasses how the insurer will go to market, its product development speed, its reward and recognition policies, and which resources it needs and how it wants to obtain those resources.

Page 20 #FIN209565 ©2007 Financial Insights, an IDC Company

F I G U R E 8

B u s i n e s s M o d e l s a s A r c h i t e c t u r a l P l a n s

Customer-centric strategy

Product manufacturer strategy

Low-cost insurer strategy

Channel-rich strategy

Business models support insurance company strategy

Customer-centric strategy

Product manufacturer strategy

Low-cost insurer strategy

Channel-rich strategy

Business models support insurance company strategy

Source: Financial Insights, 2007

Technology Refresh: The Web and Concomitant Business Applications Continue to Evolve

The Internet has continued to redefine how insurers develop and deploy the processes they use to support their business operations and communicate with stakeholders, including internal staff, throughout their value chains. At this time in 2007, there are two major portfolios of Internet-driven technologies and applications (see Figure 9):

● Dynamic IT. These technologies enable CIOs to deliver increased flexibility and transparency to the lines of business without requiring large-scale replacement of existing systems. Two of the major technologies in this portfolio are service-oriented Architecture (SOA) and Web services. SOA is a business and technology architecture based on the use of autonomous application and system "services" abstracted from one another, independent of implementation. Web services software consists of application development and deployment tools, infrastructure software, and packaged applications that conform to standards for Web Services Architecture (WSA), which is a particular instantiation of SOA (see Worldwide SOA-Driven Software 2007�2011 Forecast: A Changing IT Lifestyle, IDC #207080, May 2007).

In Canada, a small but growing number of insurers are using SOA and Web services to improve their responsiveness to a changing

©2007 Financial Insights, an IDC Company #FIN209565 Page 21

market and regulatory environment. In the United States, insurers are on the fence but leaning toward adoption of SOA. A P&C insurer with 2006 revenue over $7 billion experimented with it and had unsuccessful results but is still planning other pilots. One L&A insurer with 2006 revenue of over $10 billion is in the planning stage. A second L&A insurer, with 2006 revenue of approximately $7 billion, is making a significant investment in SOA and Web services, albeit for what it calls an experiment. This L&A insurer is developing and using SOA and Web services to support enrollment functionality in its defined contribution area. It is experiencing a 30% to 40% payback on its investments in these technologies and plans to use these technologies to support other defined contribution functional areas.

● Enterprise 2.0. The essence of Web 2.0 is collaboration and socialization. The key technologies that enable these capabilities are blogs, wikis, instant messaging (IM), and podcasts. Youth around the globe use social Web sites such as Facebook and MySpace to make new friends and share their activities and thoughts. Corporations have slowly begun to use these same technologies � and a virtual reality online Web site called Second Life inhabited by both individuals and corporations � for business reasons such as communication and commerce.

Assicurazioni Generali, one of the largest insurance companies in the world, is based in Italy with reported net premiums of over 30 billion euros for the first half of 2007; it is opening an island in Second Life to market its brand to the younger prospects that visit this online world. Generali is sponsoring a James Bond�style car-race game in which the winner is the driver who has the least amount of damage when the race is over.

A U.S. L&A insurer is using blogs � a many-to-many medium � for its agents to communicate with each other and with the marketing and distribution executives in the home office to establish and share best practices throughout the agency plant. The blogs are easy to use, interesting, and actionable but, as importantly, have security and compliance controls.

Page 22 #FIN209565 ©2007 Financial Insights, an IDC Company

F I G U R E 9

T h e E v o l v i n g W e b

Web 1.0

Dynamic IT

Web 2.0

Enterprise 2.0

Web 3.0

?????

Increased Interaction and Productivity

Web 1.0

Dynamic IT

Web 2.0

Enterprise 2.0

Web 3.0

?????

Increased Interaction and Productivity

Source: Financial Insights, 2007

E S S E N T IA L GU I DA N C E

A c t i o n s f o r I n s u r a n c e C o m p a n i e s

We stated earlier in this report that risk is the price of opportunity. The changing risk landscape, regulator activities across the globe, and competitor initiatives are creating an environment that is rife with opportunity. One major challenge for insurance companies is to decide which risks (e.g., coastal property, global warming, product liability, retirement) they will provide coverage and services for to take advantage of the attendant opportunity of increased profitable market share (see Figure 10).

Leading insurers in 2008 will create a risk management portfolio that is a mixture of incremental changes to their current book of business with some disruptive alterations to their risk portfolio. An example of the former would be P&C insurers that identify areas on or near the coast where they can profitably provide homeowner's insurance with the applicable terms, conditions, and restrictions. An example of the latter would be P&C insurers that develop a coherent global warming approach to the products they develop for their target markets or L&A insurers that develop hybrid asset accumulation and asset management products that capture significant market share from investment firms.

©2007 Financial Insights, an IDC Company #FIN209565 Page 23

F I G U R E 1 0

W i l l i n g n e s s t o P a y t h e P r i c e o f O p p o r t u n i t y

Market Impact

Willingness to Pay Price of Opportunity

Low

High

High Low

Maintain status quo

Continual, incremental changes to risk portfolio

Disruptive alterations to risk portfolio

Market Impact

Willingness to Pay Price of Opportunity

Low

High

High Low

Maintain status quo

Continual, incremental changes to risk portfolio

Disruptive alterations to risk portfolio

Source: Financial Insights, 2007

A c t i o n s f o r V e n d o r s

Technology firms must continually prove to their insurance clients or prospects that they are knowledgeable about the insurance industry � or at least the segment of the industry their technology or services support � and the processes they enable or support. That is the entry fee for each vendor to sit at the table to begin the discussion of why it is the provider insurers should consider.

Technology firms must also develop their products and services as well as go-to-market approach based on an insurance company's four business disciplines. These disciplines are strategy, tactical, operational, and governance. Table 6 captures how the 2008 insurance top 10 strategic initiatives are dispersed across these disciplines with the initiative's 2008 rank also shown.

The main lessons for technology firms are that:

● Cost improvement, while important to insurers, did not place in the top 4 2008 strategic initiatives.

Page 24 #FIN209565 ©2007 Financial Insights, an IDC Company

● There is competitive space in the insurance industry for technology firms that participate in different niches (e.g., tracking compliance, business intelligence or analytics supporting decision-making, core administrative systems support) or different ways (i.e., bundled or unbundled).

● There is competitive advantage to be gained if they have core administrative solutions that enable better regulatory compliance, demonstrate why they can replace the multitude of core administrative systems insurers have in place, and provide the same or more value to stakeholders while reducing operational costs.

● Technology firms competing in areas such as analytics, data visualization, text data mining, knowledge management, or others that enable an insurer to develop a strong strategic competitive posture have an opportunity to build market share. In other words, the insurance market is not all about operational systems.

The technology providers that best understand how to serve their insurance clients' needs based on these 2008 top 10 initiatives will discover their own mad, mad, mad world of opportunity.

T A B L E 6

2 0 0 8 T o p 1 0 S t r a t e g i c I n i t i a t i v e s b y B u s i n e s s D i s c i p l i n e a n d R a n k

Discipline Initiative Initiative Rank Strategy • Growth: acquisitive and organic growth both in play 2 • Competitive posture: competing as an enterprise 8 • Business models: the new strategic focus 9 • Technology refresh: the Web and concomitant business applications continue

to evolve 10

Tactical • Ease of doing business: EDB cascades throughout entire value chain 4 • Cost improvement: taking center stage 5 Operational • Core administrative systems: rationalization finally under way? 3 • Channel management: the quest for balance 7 Governance • Regulatory compliance: local regulations, global impact 1 • Risk management: responding to a changing landscape 6

Source: Financial Insights, 2007

©2007 Financial Insights, an IDC Company #FIN209565 Page 25

L E AR N MO R E

R e l a t e d R e s e a r c h

● Canadian Insurance: Top Strategic Priorities and Key Enabling Technologies for 2007 (Financial Insights #FIN208918, October 2007)

● InsureTech 2007 Executive Survey: Insurance Insights for Asia (Financial Insights #FIN208461, September 2007)

● Promises, Promises: Are U.S. Insurers BPO Believers Yet? (Financial Insights #FIN208697, September 2007)

● Is the U.S. Insurance Industry Ready for Strategic Distribution Management? (Hint: No, Not Really.) (Financial Insights #FIN208240, August 2007)

● U.S. Property and Casualty Insurance Billing 2007�2012 Spending Forecast and Analysis: $how Me the Money! (Financial Insights #FIN208099, August 2007)

● Worldwide SOA-Driven Software 2007�2011 Forecast: A Changing IT Lifestyle (IDC #207080, May 2007)

● Worldwide Insurance 2007 Top 10 Strategic Initiatives: Carpe Diem � The Relentless Strategic Imperative (Financial Insights #FIN205386, February 2007)

C o p y r i g h t N o t i c e

Copyright 2007 Financial Insights, an IDC company. Reproduction without written permission is completely forbidden. External Publication of Financial Insights Information and Data: Any Financial Insights information that is to be used in advertising, press releases, or promotional materials requires prior written approval from the appropriate Financial Insights Vice President. A draft of the proposed document should accompany any such request. Financial Insights reserves the right to deny approval of external usage for any reason.