world view news in brief timeline russia opens up

TRANSCRIPT

WORLD VIEWRecent moves by US mobile operators to offer unlimited data on 4G highlight an unhealthy competitive environment

news in brief

3 Timeline A round-up of some of the major stories reported in our daily news service www.totaltele.com

reGiOnAL fOCUs

5 Russia opens up As financial investors eye up the potential of russia’s telecoms market, foreign telcos could be well advised to stay out.

netwOrk strAteGies

6 MVNOs in Africa there has been little MVnO activity in Africa to date, but there are signs that the market is poised for growth.

Us MObiLe MArket

10 Unlimited data smaller Us mobile operators are employing risky strategies in a bid to attract contract customers and keep pace with the big two.

stAtistiCs

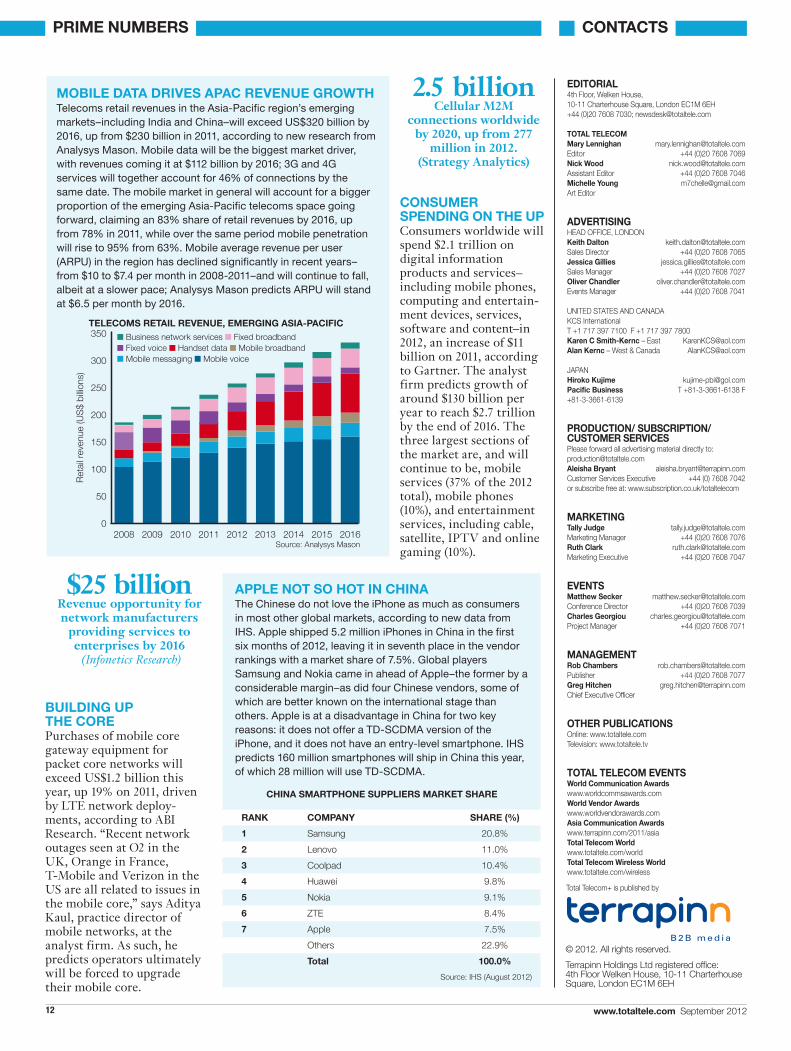

12 Prime numbers Asia-Pacific revenue growth, Apple’s position in China, mobile core gateway equipment, M2M and consumer spending.

LeaDeR cOntents

Mary Lennighan Editor

Total Telecom

Business anaLysis fOR teLecOMs pROfessiOnaLs SEpTEmbER 2012

the Us mobile market has for some time been viewed as a good bet for investors,

its structure and regulatory regime creating a positive environment, and companies like At&t and Verizon increasingly returning cash to shareholders in the form of dividends.

but for the smaller service provid-ers and for consumers, the market is far from healthy. As our story on p.10 shows, a duopoly is emerging at the top end, leaving the chal-lengers–the likes of sprint, t-Mobile UsA and a raft of smaller operators–to resort to what some see as desperate measures in order to keep up.

One week in August saw MetroPCs and t-Mobile UsA announce unlimited data plans for their 4G offerings (which in the case of the latter is an HsPA+ service, not Lte), at a time when At&t and Verizon are heavily promoting shared data plans with usage tiers to ensure customers are paying for what they consume. those following the unlimited data path will doubtless pick up the contract customers they covet as a

They could end up serving the US’s biggest data users for little return

result, but at what cost? they could well end up serving some of the country’s biggest data users for little return.

speaking of returns, some finan-cial analysts suggest that investors should be looking to russia’s tele-coms market, attracted by growth potential in mobile data and the likelihood of strong free cash flow generation. russia’s long-awaited accession to the world trade Organisation this summer is an added boon.

but the opportunity for foreign telecoms operators to make their presence felt in the market is likely to be limited (p.5).

indeed, the country’s only foreign player, tele2, has had a rough time of it and its inability to secure a 3G licence while its bigger rivals are starting to make plans for Lte means that its future in the market could be short-lived. Most are predicting a takeover by rostelecom, but analysts warn that the telco will have to get its skates on and broker a deal before its valu-ation slips along with its market share.

this month we also look at another market with strong poten-tial, although recent activity has been limited (p.6). regulatory rumblings and a scale-building partnership agreement, amongst other things, suggest that Africa’s MVnO market could be on the verge of a growth spurt. n

cLicK HeRe

tO ReaD On

yOuR ipHOne/ipaD

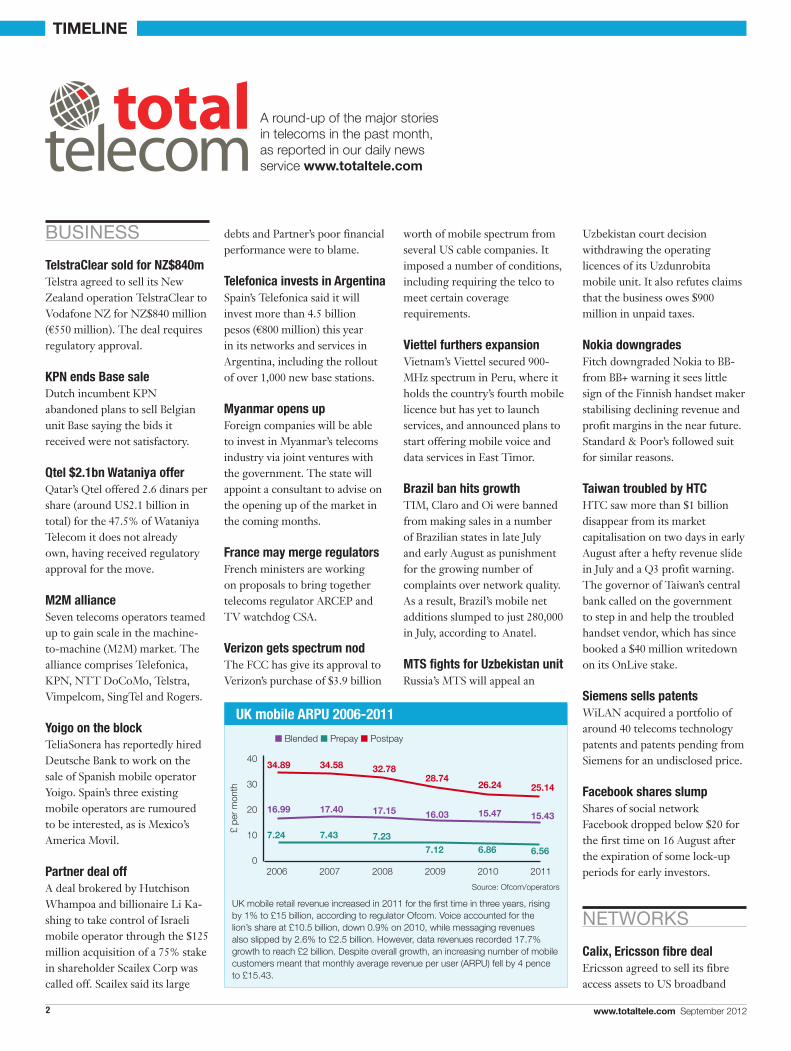

UK mobile ARPU 2006-2011

UK mobile retail revenue increased in 2011 for the first time in three years, rising by 1% to £15 billion, according to regulator Ofcom. Voice accounted for the lion’s share at £10.5 billion, down 0.9% on 2010, while messaging revenues also slipped by 2.6% to £2.5 billion. However, data revenues recorded 17.7% growth to reach £2 billion. Despite overall growth, an increasing number of mobile customers meant that monthly average revenue per user (ARpU) fell by 4 pence to £15.43.

Source: Ofcom/operators

debts and Partner’s poor financial performance were to blame.

Telefonica invests in Argentinaspain’s telefonica said it will invest more than 4.5 billion pesos (€800 million) this year in its networks and services in Argentina, including the rollout of over 1,000 new base stations.

Myanmar opens upforeign companies will be able to invest in Myanmar’s telecoms industry via joint ventures with the government. the state will appoint a consultant to advise on the opening up of the market in the coming months.

France may merge regulatorsfrench ministers are working on proposals to bring together telecoms regulator ArCeP and tV watchdog CsA.

Verizon gets spectrum nodthe fCC has give its approval to Verizon’s purchase of $3.9 billion

Business

TelstraClear sold for NZ$840m telstra agreed to sell its new Zealand operation telstraClear to Vodafone nZ for nZ$840 million (€550 million). the deal requires regulatory approval.

KPN ends Base saleDutch incumbent kPn abandoned plans to sell belgian unit base saying the bids it received were not satisfactory.

Qtel $2.1bn Wataniya offerQatar’s Qtel offered 2.6 dinars per share (around Us2.1 billion in total) for the 47.5% of wataniya telecom it does not already own, having received regulatory approval for the move.

M2M allianceseven telecoms operators teamed up to gain scale in the machine-to-machine (M2M) market. the alliance comprises telefonica, kPn, ntt DoCoMo, telstra, Vimpelcom, singtel and rogers.

Yoigo on the blockteliasonera has reportedly hired Deutsche bank to work on the sale of spanish mobile operator Yoigo. spain’s three existing mobile operators are rumoured to be interested, as is Mexico’s America Movil.

Partner deal offA deal brokered by Hutchison whampoa and billionaire Li ka-shing to take control of israeli mobile operator through the $125 million acquisition of a 75% stake in shareholder scailex Corp was called off. scailex said its large

worth of mobile spectrum from several Us cable companies. it imposed a number of conditions, including requiring the telco to meet certain coverage requirements.

Viettel furthers expansionVietnam’s Viettel secured 900-MHz spectrum in Peru, where it holds the country’s fourth mobile licence but has yet to launch services, and announced plans to start offering mobile voice and data services in east timor.

Brazil ban hits growthtiM, Claro and Oi were banned from making sales in a number of brazilian states in late July and early August as punishment for the growing number of complaints over network quality. As a result, brazil’s mobile net additions slumped to just 280,000 in July, according to Anatel.

MTS fights for Uzbekistan unit russia’s Mts will appeal an

A round-up of the major stories in telecoms in the past month, as reported in our daily news service www.totaltele.com

Uzbekistan court decision withdrawing the operating licences of its Uzdunrobita mobile unit. it also refutes claims that the business owes $900 million in unpaid taxes.

Nokia downgradesfitch downgraded nokia to bb- from bb+ warning it sees little sign of the finnish handset maker stabilising declining revenue and profit margins in the near future. standard & Poor’s followed suit for similar reasons.

Taiwan troubled by HTCHtC saw more than $1 billion disappear from its market capitalisation on two days in early August after a hefty revenue slide in July and a Q3 profit warning. the governor of taiwan’s central bank called on the government to step in and help the troubled handset vendor, which has since booked a $40 million writedown on its OnLive stake.

Siemens sells patentswiLAn acquired a portfolio of around 40 telecoms technology patents and patents pending from siemens for an undisclosed price.

Facebook shares slumpshares of social network facebook dropped below $20 for the first time on 16 August after the expiration of some lock-up periods for early investors.

neTWORKs

Calix, Ericsson fibre dealericsson agreed to sell its fibre access assets to Us broadband

tiMeLine

2 www.totaltele.com September 2012

2006 2007 2008 2009 2010 2011

34.89

16.99

7.24

34.58

17.40

7.43

32.78

17.15

7.23

28.74

16.03

7.12

26.24

15.47

6.86

25.14

15.43

6.56

n blended n prepay n postpay

£ pe

r m

onth

40

30

20

10

0

tiMeLine

equipment vendor Calix for an undisclosed sum. the pair also inked a three-year deal that will see ericsson sell Calix systems and software globally.

More net-sharing for VodaVodafone brokered a deal with rival 3 that will see the pair share mobile network infrastructure in ireland. the joint venture is due to be operational by the autumn.

UK LTE auction in 2013Ofcom has yet to set a firm date for the auction of 800-MHz and 2.6-GHz spectrum in the Uk but said it aims to open the process before the end of the year, with bidding to take place in 2013.

EvEv gets aheadMeanwhile Ofcom gave everything everywhere the go-ahead to refarm its 1800-MHz spectrum for Lte services; the oprator plans to launch this year. it subsequently sold 2x15 MHz of that spectrum to 3Uk.

Chilean ops win LTE spectrumClaro, entel and Movistar all won 2.6-GHz spectrum in Chile’s Lte auction, which raised a total of just over Us$12 million. entel paid the most for block b with a $8.8 million bid.

India LTE mega-dealsamsung received an order for Lte network equipment worth 1.2 trillion won (€860 million) from india’s infotel, according to a south korean press report.

India 2G licence to cost $2.5bnindia has set a base price of inr140 billion ($2.5 billion) for a 5-MHz block of bandwidth in the upcoming re-auction of its cancelled 2G licences. following a deadline extension granted by the supreme Court, the government has until 11 January 2013 to conduct the sale.

AT&T to close 2G networkwith a view to closing down its 2G mobile networks by 2017, At&t is working on ways to encourage the 12% of its subscriber base still using 2G devices to upgrade.

Sprint rolls out lightRadioUs mobile operator sprint said it will become the first in the world to deploy Alcatel-Lucent’s lightradio mini base station technology.

Ericsson Egypt, Austria dealsVodafone egypt selected ericsson to supply it with new radio equipment as part of its mobile broadband upgrade plan. the vendor will also supply Lte equipment to telekom Austria and its Croatian unit Vipnet.

Thailand sets the date3G spectrum will be auctioned in thailand on 17 October, the regulator revealed. the country has been planning to award licences for well over a decade.

Third 3G network in TunisiaQtel-owned tunisiana launched 3G services in tunisia. its network covers 48% of the population; it aims to increase that to 87% early next year.

Lycamobile eyes Canadaeuropean MVnO specialising in low-cost international calls Lycamobile is in talks with a number of Canadian GsM operators with a view to brokering a network deal that would enable it to offer services in the country.

MeeGo lives onfinnish start-up Jolla, formed by a group of former nokia employees, announced plans to develop a range of smartphones based on the MeeGo operating system.

LucKy siXmarissa mayer became Yahoo’s sixth CEO in five years when she took on the position in July. 37-year-old mayer joined the Internet company from rival Google where she spent 13 years in a variety of roles, serving most recently as vice president of local, maps and location services. Mayer’s experience at Google should stand her in good stead as she pushes ahead with Yahoo’s ongoing turnaround plan. The company says she is undertaking a review of its businesses with a view to changing its strategy going forward. According to a stock exchange filing, that review will include Yahoo’s growth and acquisition strategy, the restructuring plan it implemented in the second quarter of 2012, and its cash position and planned capital allocation strategy. One possible outcome could see Yahoo reverse its may decision to return the bulk of the cash proceeds–estimated at more than US$ 4 billion–from its sale of a 20% stake in China’s Alibaba Group to shareholders. That revelation naturally led to speculation over Yahoo’s plans for the cash. In the meantime, Mayer is assembling a new team around her. Ross Levinsohn, who acted as interim CEO following Scott Thompson’s departure earlier this year, has left the company. Ron Bell was appointed Yahoo general counsel in August, having been with the company since 1999, and Mayer is rumoured to be keen to poach Katie Jacobs Stanton, an ex Google colleague, from Twitter.

PeOPLe

Voda clears deck at C&WVodafone made sweeping changes to the top management team at recent acquisition Cable & wireless worldwide. Vodafone Global enterprise CeO nick Jeffery replaced Gavin Darby at the helm, while C&w’s CfO, acting CtO and Hr head made way for Vodafone people.

Google axes 4,000 Moto jobs4,000 jobs will go at Motorola Mobility–around 20% of its workforce–as new owner Google seeks to turn the business around. A third of the handset maker’s 90 offices will close.

Millicom names CEOMillicom international Cellular named Hans-Holger Albrecht as its new CeO as of 31 October. He replaces Mikael Grahne.

ALU cuts staffAlcatel-Lucent will cut 5,000 jobs as part of a plan to realise an additional €750 million in cost savings. the vendor will narrow its focus to concentrate on its most profitable areas.

New Pacnet chiefPacnet appointed Carl Grivner as its new chief executive, replacing interim CeO brett Lay who returns to his role as CfO.

Jobs go at CiscoCisco will shed 1,300 jobs or 2% of its workforce as part of a cost-cutting drive. the cuts come in addition to the 6,500 employees Cisco said it would lose last July.

Sony sheds mobile roles1,000 jobs will go–15% of the workforce–at sony’s mobile phone business as the Japanese firm moves the unit’s HQ to tokyo from sweden.

3September 2012 www.totaltele.com

verizon.com/wholesale/globalsolutions Verizon Global Wholesale serves: Carriers - Wireless Providers - ISPs - Cable Operators - Resellers© 2012 Verizon. All services are provided by Verizon in accordance with certain rates, terms, conditions, and restrictions set forth in Verizon’s tariffs or in applicable agreements between Verizon and the carrier.

With Verizon Global Wholesale’s

flexible Ethernet and wireless

backhaul solutions, you can serve up a

range of bandwidth and performance

options for your customers. You

get all this from a single interface

that makes it easy to incrementally

add services as your customers’

needs grow. And as they do, we can

customize service agreements to help

you manage costs and ensure terms

and pricing are never hard for your

customers to swallow.

AN ETHERNET SOLUTION THAT MAKES ADDING SERVICES EASY? NOW THAT’S REFRESHING.

5September 2012 www.totaltele.com

ReGiOnaL fOcus

russia’s flourishing telecoms indus-try should be highly attractive to foreign investors, particularly in

light of the country’s formal accession to the world trade Organisation. but while investors are looking to put their money in, foreign telcos could be moving out.

investor interest is growing. earlier this year a group of funds led by Macquarie renaissance infrastructure fund (Mrif) invested $100 million in telecoms towers company russian towers, a rare private equity deal in the country.

it is easy to see why. the market is well developed but offers significant growth potential. Mobile subscribers in russia numbered 227.6 million at the end of June with penetration at 159.3%, according to Advanced Communications & Media. but smartphone penetration remains low, at around 25%, leaving room for ArPU growth, and analysts see strong free cash flow generation potential for the big telcos as the capital requirements associ-ated with 3G network rollout slow down.

Under its commitments to the wtO, russia has agreed to remove its 49% foreign direct investment cap on incum-bent telecoms operators four years after accession. but while financial investors

might well be keen to tap that opportu-nity, strategic investors are unlikely to take the plunge.

“i would be surprised to see any foreign telco moving into the market,” says emeka Obiodu, principal analyst, telco strategy, at Ovum. the kremlin would prefer the industry to be controlled by russians and could make life difficult for any foreign player. “foreign telcos haven’t had much success in the russian telecoms market,” Obiodu says, referring in partic-ular to fourth-placed mobile operator tele2, which is struggling to compete with the big three. there is also telenor, which holds 39.5% of the voting rights in number three operator Vimpelcom and has had a stormy relationship with fellow shareholder Altimo.

Mts, Megafon and Vimpelcom together had 187.4 million mobile custom-ers at mid-year, according to AC&M, or 82% of the market. tele2’s 21.6 million customers give it 10%, while fifth-placed rostelecom had 12.9 million (5.7%).

russia has been a key growth engine for tele2: it generated sek3.28 billion in revenues (€400 million) there in Q2–30% of its group sales and slightly more than it made in its home market sweden. but

now it risks being left behind. Unlike the big three russian-owned players, it has been unable to procure a 3G licence, and as they move towards rolling out 4G serv-ices, and smartphone penetration grows, its eDGe network will be inadequate and its market share will fall.

“there is a credible exit plan for tele 2 and that is to sell out to rostelecom,” says Obiodu. in order to retain its value the company needs to move quickly, but rostelecom CeO Alexander Provotorov says “not yet”.

“we do not have any formal discus-sions with tele2 currently,” he said on the telco’s quarterly results call last month. However, tele2 is an obvious fit for rostelecom, which is in the process of merging with state-run telecoms holding company svyazinvest and admits it is looking to bulk up its mobile business by absorbing small regional players.

so, with a new russian player gearing up to challenge the big three, overseas players are effectively shut out.

but there is money to be made, for example, by a company willing to finan-cially back a local player, Obiodu explains. “there are still bountiful opportunities for someone to go in.” n

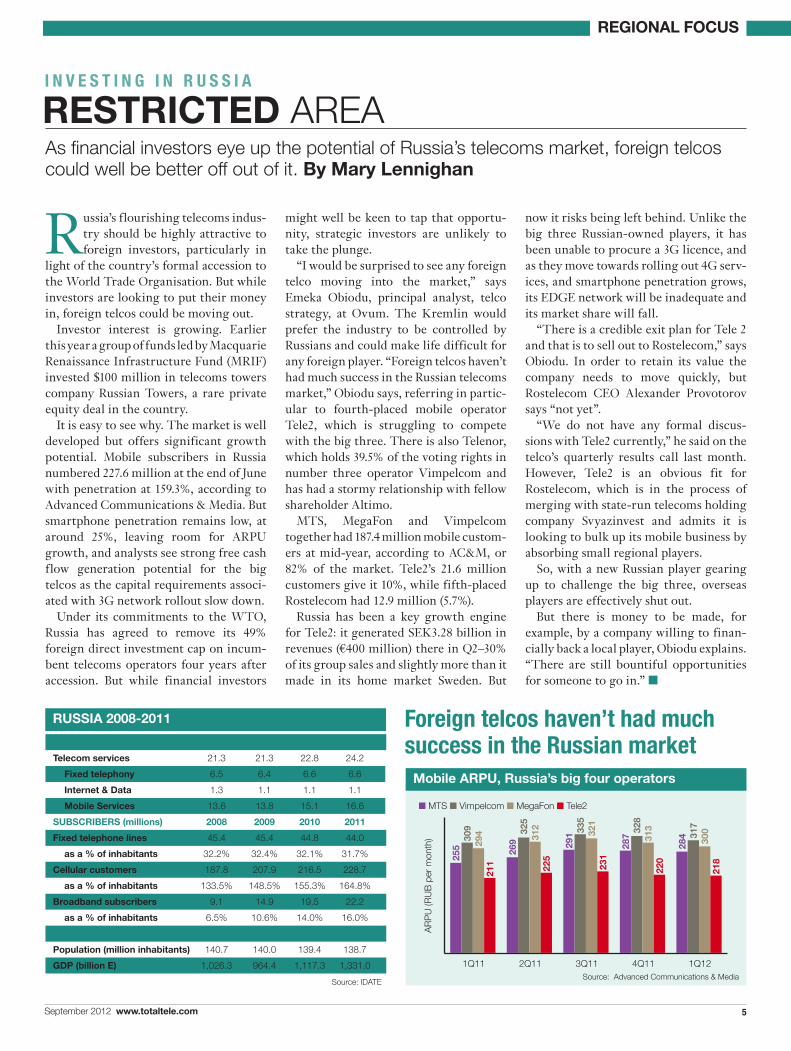

As financial investors eye up the potential of Russia’s telecoms market, foreign telcos could well be better off out of it. By Mary Lennighan

RestRicteD AREA I N V E S T I N G I N R U S S I A

Foreign telcos haven’t had much success in the Russian marketMaRKets (e billion) 2008 2009 2010 2011

telecom services 21.3 21.3 22.8 24.2

fixed telephony 6.5 6.4 6.6 6.6

internet & Data 1.3 1.1 1.1 1.1

Mobile services 13.6 13.8 15.1 16.6

suBscRiBeRs (millions) 2008 2009 2010 2011

fixed telephone lines 45.4 45.4 44.8 44.0

as a % of inhabitants 32.2% 32.4% 32.1% 31.7%

cellular customers 187.8 207.9 216.5 228.7

as a % of inhabitants 133.5% 148.5% 155.3% 164.8%

Broadband subscribers 9.1 14.9 19.5 22.2

as a % of inhabitants 6.5% 10.6% 14.0% 16.0%

MacRO-ecOnOMic Data 2008 2009 2010 2011

population (million inhabitants) 140.7 140.0 139.4 138.7

GDp (billion e) 1,026.3 964.4 1,117.3 1,331.0

Source: IDATE

Russia 2008-2011

Mobile aRpu, Russia’s big four operators

1Q11 2Q11 3Q11 4Q11 1Q12Source: Advanced Communications & media

255 26

9 291

287

28430

9 325

335

328

317

294 31

2

321

313

300

211 22

5

231

220

218

n mTS n Vimpelcom n megaFon n Tele2

AR

pU

(RU

b p

er m

onth

)

verizon.com/wholesale/globalsolutions Verizon Global Wholesale serves: Carriers - Wireless Providers - ISPs - Cable Operators - Resellers© 2012 Verizon. All services are provided by Verizon in accordance with certain rates, terms, conditions, and restrictions set forth in Verizon’s tariffs or in applicable agreements between Verizon and the carrier.

With Verizon Global Wholesale’s

flexible Ethernet and wireless

backhaul solutions, you can serve up a

range of bandwidth and performance

options for your customers. You

get all this from a single interface

that makes it easy to incrementally

add services as your customers’

needs grow. And as they do, we can

customize service agreements to help

you manage costs and ensure terms

and pricing are never hard for your

customers to swallow.

AN ETHERNET SOLUTION THAT MAKES ADDING SERVICES EASY? NOW THAT’S REFRESHING.

6 www.totaltele.com September 2012

netWORK stRateGies

Virtual operators have carved out a significant presence in many global mobile markets, but have

yet to make their impact felt in Africa. However, there are indications that the market is poised for growth.

in recent years a handful of virtual players, some mobile virtual network operators (MVnOs) in the traditional sense and others operator sub-brands or highly-targeted niche players, have come to market in Africa, one of the most high profile being set’Mobile, launched by footballer samuel eto’o in Cameroon late last year. And a number of markets are on the verge of opening up to MVnOs.

but these new entrants, and those yet to come, have some major hurdles to overcome if they are to build successful African MVnO businesses. Leveraging established brands from other industries will be an important weapon, especially in countries where the low-cost market, traditionally the remit of the MVnO, is still fiercely contested by the mobile network operators themselves. African MVnOs also face challenges when it comes to building the necessary scale, working with regulatory regimes, and finding a willing host network.

nonetheless, analysts see potential in the market.

“MVnO set-up costs continue to fall, and African MVnOs can benefit from that as well as learning from the experi-ence of success and failure in other markets,” says tim Heal, consultant with CsMG. “Mobile is often a great channel for brands to get closer to their custom-ers. And outside of big brands, there are lots of different kinds of niches that MVnOs can fill. there are always going to be opportunities and always going to be people trying their hand.”

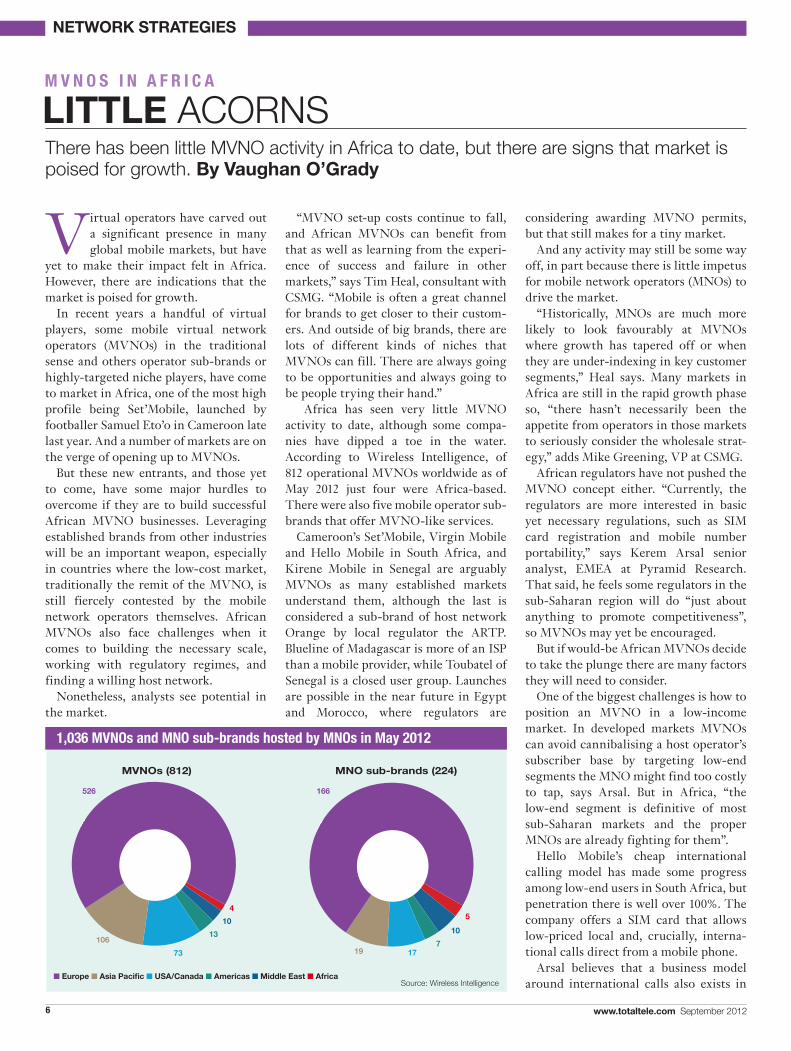

Africa has seen very little MVnO activity to date, although some compa-nies have dipped a toe in the water. According to wireless intelligence, of 812 operational MVnOs worldwide as of May 2012 just four were Africa-based. there were also five mobile operator sub-brands that offer MVnO-like services.

Cameroon’s set’Mobile, Virgin Mobile and Hello Mobile in south Africa, and kirene Mobile in senegal are arguably MVnOs as many established markets understand them, although the last is considered a sub-brand of host network Orange by local regulator the ArtP. blueline of Madagascar is more of an isP than a mobile provider, while toubatel of senegal is a closed user group. Launches are possible in the near future in egypt and Morocco, where regulators are

considering awarding MVnO permits, but that still makes for a tiny market.

And any activity may still be some way off, in part because there is little impetus for mobile network operators (MnOs) to drive the market.

“Historically, MnOs are much more likely to look favourably at MVnOs where growth has tapered off or when they are under-indexing in key customer segments,” Heal says. Many markets in Africa are still in the rapid growth phase so, “there hasn’t necessarily been the appetite from operators in those markets to seriously consider the wholesale strat-egy,” adds Mike Greening, VP at CsMG.

African regulators have not pushed the MVnO concept either. “Currently, the regulators are more interested in basic yet necessary regulations, such as siM card registration and mobile number portability,” says kerem Arsal senior analyst, eMeA at Pyramid research. that said, he feels some regulators in the sub-saharan region will do “just about anything to promote competitiveness”, so MVnOs may yet be encouraged.

but if would-be African MVnOs decide to take the plunge there are many factors they will need to consider.

One of the biggest challenges is how to position an MVnO in a low-income market. in developed markets MVnOs can avoid cannibalising a host operator’s subscriber base by targeting low-end segments the MnO might find too costly to tap, says Arsal. but in Africa, “the low-end segment is definitive of most sub-saharan markets and the proper MnOs are already fighting for them”.

Hello Mobile’s cheap international calling model has made some progress among low-end users in south Africa, but penetration there is well over 100%. the company offers a siM card that allows low-priced local and, crucially, interna-tional calls direct from a mobile phone.

Arsal believes that a business model around international calls also exists in

There has been little MVNO activity in Africa to date, but there are signs that market is poised for growth. By Vaughan O’Grady

LittLe ACORNSM V N O S I N A F R I C A

1,036 MVNOs and MNO sub-brands hosted by MNOs in May 2012

Source: Wireless Intelligence

MVnOs (812) MnO sub-brands (224)

526 166

4510

10137

73 17

10619

n europe n Asia Pacific n usa/canada n americas n Middle east n africa

September 2012 www.totaltele.com 7

netWORK stRateGies

between friendi and Virgin also hints at a move in this direction,” says Arsal.

working with one host network opera-tor across multiple countries sounds ideal: it could mean the same technology platform, contractual agreements and volume discounts on wholesale rates. but CsMG’s Heal has some caveats. will all local versions of regional giant Mtn, say, want to work with the same MVnO? what if an MnO is the incumbent in one market but the challenger in another? if so, they would likely have different stra-tegic objectives. there will be financial pressure on MVnOs to take the best deal in each market, even if that means working with different MnOs.

but scale certainly does help. so far there hasn’t been sufficient activity in Africa to attract aggregators–MVnAs–which enable MVnOs to launch at a lower cost of entry and often greatly facilitate the set-up process. MVnAs would normally establish scale of their own by working with a number of MVnOs. the single enabler–MVne–model through which operators can cost-effectively host specific strategic MVnOs is more likely in the near term.

but even with a great business case and the practical details worked out, timing can defeat a budding MVnO. Greening says he worked on a very promising MVnO launch in Uganda; at least, it was promising until the local mobile network operators engaged in an all-out price war, partly fuelled by bharti Airtel’s entry into the market (through the acquisition of Zain in 2010). “their low-cost, aggressive pricing model contributed to the massive reduction in retail rates. it completely blew the business case for any MVnO wanting to enter the market,” Greening says. “stability of retail pricing will be a key driver as to whether MVnOs can be sustainable in low ArPU markets.”

branding, meanwhile, will be vital for would-be MVnOs. Cell C’s sub-brand red bull has the obvious youth appeal of a ‘cool’ drinks brand. kirene of senegal is even more interesting. kirene is the country’s largest water and non-alcoholic beverage distributor, as well as being

less developed markets. “there certainly is a potential for MVnOs that specialise in low-cost international calls regardless of penetration,” he says. “Most African countries have tight connections with european countries and there’s a market for two-sided affordable calls in this segment.”

whether this model takes off else-where, however, may depend on whether governments or incumbents in other countries relax their grip on this source of revenue.

but a simple, low-priced MVnO offer in general is unlikely to be a workable strategy in most African countries. And the high end should be managed with

care too. According to thecla Mbongue, senior research analyst at informa telecoms & Media, Virgin Mobile’s first foray into south Africa in 2006 foundered on the lack of a 3G network which the two big operators, Vodacom and Mtn, already had. Virgin works with third operator Cell C. “it was difficult to be a challenger in the high end segment when you did not have a strong data proposi-tion”, she says.

today Virgin’s subscription numbers are closing in on half a million, which probably makes it the biggest MVnO on the continent, although such figures only put it fifth in south Africa and barely noticeable behind the 60 million total of the big three.

Virgin is making moves to scale up though. earlier this year it agreed a part-nership with Dubai-based friendi Group to merge its south African business with friendi’s MVnO operations in Oman, Jordan and saudi Arabia. the merged entity was renamed Virgin Mobile Middle east & Africa. the new company has 1 million customers and aims to reach 5 million by 2015 both through organic growth and expanding to new markets. “i am excited about working closely with the Virgin Group on rolling out new MVnO operations across the Middle east and Africa,” said Mikkel Vinter, friendi Group CeO, in June.

“Pan-regional MVnOs are likely to be the trend; the new strategic alliance

There are always going to be opportunities and always going to be people trying their hand

Connected withyour world

■ Wide-reaching international coverage featuring innovative IP, Fiber, Ethernet & Satellite solutions

■ Robust solutions connecting the Middle East, Africa and other emerging markets

■ Full resilient network design and dedicated service management

Contact us Tel: +33 (0)1 84 88 05 88 [email protected]

www.pccwglobal.com

8 www.totaltele.com September 2012

netWORK stRateGies

OCT 29 – NOV 1, 2012 McCORMICK PLACE, CHICAGO

REGISTER TODAY AND SAVE $100 Off VIP and

Standard Conference Passes, use priority code: JHBQGC12

PROFITING FROM MOBILE BROADBAND INNOVATIONThe only event where you can connect with the entire 4G and mobile broadband industry, new products and over 200 exhibitors & sponsors!

4G World 2012 Conference and Expo focuses on the most challenging issues and obstacles facing operators as they try to manage the cost of unbridled traffic growth and exploit opportunities to capture sufficient revenues and generate a return on their 4G infrastructure investments.WWW.4GWORLD.COM

CORPORATE HOSTS

PREMIER SPONSORS

PUBLISHER OF THE OFFICIAL SHOW DAILY

ORGANIZED BY:

PREMIER MEDIA SPONSORS

OFFICIAL TECHNICAL TRAINING PARTNER

SPECIAL PROGRAM FEATURE SPONSOR

PLATINUM SPONSORS

GOLD SPONSORS

an MVnO. “they have their own distri-bution channels; they have something more to offer,” says informa’s Mbongue. this might be scratch cards offering airtime distributed with beverage bottles, or giving customers bottles of water in return for phone usage. “in terms of value-added services or customer loyalty they have a two-pronged offer,” she says.

equally plausible is the appeal to a group identity that drives toubatel, also in senegal. this service positions itself as a low-cost offer with a closed user group and a target market among the Mouride Muslim brotherhood (touba is a holy city in senegal). toubatel is a sub-brand of senegal’s third-largest mobile network operator expresso, which is itself a subsid-iary of sudan’s sudatel.

Madagascar’s wiMAX-based blueline service is even harder to define, offering tV services as well as mobile internet and phone services.

set’Mobile, on the other hand, which came to market in Cameroon last year, triggered much discussion. the service,

which borrows the name of the country’s world-famous footballer samuel eto’o, was initially interpreted by many Cameroonians as that of a new mobile network operator, Mbongue says. when the regulator clarified that it had not issued a mobile licence to the MVnO and the only licence it had was to resell traffic from existing MnOs, the joke among some Cameroonians was that set’Mobile was simply setting up ‘callboxes’–inter-net cafe-style businesses that hire out phones and airtime to people who are too poor to buy their own–since they were unfamiliar with the MVnO concept.

this is a customer education question that may yet cause some problems. in south Africa for example, “a lot of the customers are not aware that Virgin is an MVnO,” says Mbongue. it has a branded siM card and is therefore viewed as being a network. in senegal, meanwhile, the regulator insisted that, as kirene is not a licensed operator it had to rebrand its siM cards as ‘kirene avec Orange’, its host operator being incumbent sonatel,

which is owned by france telecom and offers services under the Orange brand.

Many of these issues (scale, set-up costs, pricing, and so on) are not confined to the African market. “new MVnOs typi-cally underestimate the rapid cash demand from growth and subscriber acquisition,” says Heal. “You have to have a really solid business case and stress-test it for a range of scenarios. MVnOs that focus on the low-cost segment need to think about the response from competi-tors–can the business still work if retail prices need to come down another 5%?”

but despite the challenges, Africa is still a promising market. “there will be some successes in the near term. there is activity in the market today, but unfortu-nately wholesale is not a priority for most MnOs,” says Greening. “Operators are currently reacting rather than proac-tively driving the MVnO market,” he adds. “As we see these markets mature and operators look for new ways to drive growth and retention then MVnO will become more important for them.” n

For sponsorship opportunities for either event contact [email protected]

This November Total Telecom brings you...

Total Telecom World conference and the 14th annual World Communication Awards

2 events hosted under one roof with the awards taking place on the evening of the conference

1 day conference13 November

The Lancaster LondonBook your place at:

www.totaltele.com/world

Awards ceremony and gala dinner13 November,

The Lancaster LondonBook your table at:

www.worldcommsawards.com

WORLDORLD2012

10 www.totaltele.com September 2012

recent moves by a number of mid-sized Us mobile operators to introduce unlimited data plans for

4G left the industry questioning why this is a viable business model for them, but not for the big two. the answer though is simple: it isn’t.

in the same week in August t-Mobile UsA and MetroPCs unveiled new unlim-ited data plans, starting at $70 and $55 per month respectively. third-largest player sprint already offers unlimited data on both its 3G and Lte networks, but the big two–At&t and Verizon wireless–have turned their backs on unlimited data, opting instead for tiered allowances to discourage excessive consumption.

but the challengers could be playing a dangerous game. while the plans could help them boost their subscriber bases, a difficult thing to do in a market that some are starting to call a duopoly, they also run the risk of attracting heavy data users who will increase the chances of conges-tion on their networks for little return.

“it’s definitely not sustainable long term,” says Dee burger, telecom practice leader at Capgemini. “they’ll pick up some customers and they’ll probably be profitable with it for a couple of years, but

long-term it will be a liability for them.”for now though, there are some argu-

ments in favour of un-capped usage.“if you look at t-Mobile [UsA], they’ve

been losing contract customers. the only thing moving upwards is prepay and M2M, which isn’t exactly where the money is going to come from...so [unlim-ited data] is one way to attract new contract customers,” says Jessica ekholm, research director at Gartner.

“it’s an obvious way to generate some positive marketing,” she adds.

indeed, the operators themselves say they are reacting to the high prices and complex tariff plans of their rivals.

“Our Unlimited nationwide 4G Data plan is the answer to customers who are frustrated by the cost, complexity and congested networks of our competitors,” says kevin McLaughlin, vice president, marketing, t-Mobile UsA. it is worth noting that t-Mobile’s 4G service runs on HsPA+ not Lte. Meanwhile, MetroPCs claims its $55-per-month unlimited Lte data plan can save users up to $2,200 in service costs over two years “compared to similar competitor offers”, something that could be music to the ears of the consumer in difficult economic times.

However, as burger suggests, unlim-ited data and more customers increases the risk of network congestion. “Actual data use has always exceeded what people projected. You can’t predict the evolution of devices or...services. they’ve got a year or two to offer these price plans, because data usage will be far different in 2017 to what it is in 2012,” he says.

but ekholm is less concerned. “with Lte it is still early days. it’s going to be a while before we start talking about congestion,” she says. “Video is going to be the big culprit but even then operators are investing in video optimisation and offloading technology.”

whatever the outcome, the analysts agree that the new price plans and related drive for customer additions are sympto-matic of a lack of competition in the Us mobile market that does not bode well for either operators or consumers.

“Verizon and At&t are so dominant, the rest of these guys are just hanging on...it’s partly why sprint, t-Mobile and MetroPCs are taking big risks like unlim-ited pricing,” burger says. “Duopoly is only a mild exaggeration.”

indeed, of the 310 million customers served by the top seven Us mobile opera-tors at the end of June, 65% belonged to either At&t or Verizon (see box).

“to have so few operators in such a huge market, it still has a way to go,” says ekholm. “the Us is not as competitive as europe by far. Prices are much higher than they are in europe.”

Unlimited price plans that include t-Mobile UsA’s ‘4G’ data bundle will start at $69.99 (€55.80) at launch. Verizon wireless’ share everything plan starts at $100 per month.

by comparison, t-Mobile in Germany from early september will offer custom-ers unlimited 100-Mbps Lte data for an extra €9.95 per month on top of its Complete Mobile tariffs, which start at €26.95. Local rival telefonica O2 Germany offers Lte price plans from €35.99;

pRicinG stRateGies

Smaller US mobile operators are employing risky strategies in a bid to attract contract customers and keep pace with the big two. By nick Wood

unHeaLtHy COMPETITIONU S M O B I L E M A R K E T

AT&T and Verizon: A US mobile market duopoly?

AT&T and Verizon Wireless have a stranglehold on the US mobile market, despite recent moves by third-placed Sprint to boost its subscriber base, an endeavour for which it has had to pay a hefty price. “I don’t think it’s a healthy market,” says Capgemini’s Dee Burger. “It would be better if AT&T and Verizon had stronger competitors.”

Industry body CTIA puts the total number of US wireless subscribers at the end of 2011 at 331.6 million; six months later the country’s seven largest operators had a combined 310 million customers (see chart). Seven operators sounds like plenty for a population of around 315 million, but AT&T and Verizon Wireless together boast the lion’s share of the total, with 105.2 million and 94.2 million customers respectively. Adding in the two other nationwide providers, Sprint and T-Mobile, the combined market share comes to 93%.

Consumers would benefit from more competition, says Ekholm. “There are ways to have more players in the market and still make a profit,” she insists.

But the battle for new customers is tough. Outside of the top three players, net additions were largely flat in the 12 months to 30 June. Sprint has stemmed customer losses in the last three quarters–in Q2 it reported 56.4 million subscribers, up from 52.1 million a year earlier–but the new subscribers have come with a large price tag. Sprint agreed to purchase $15.5 billion worth of iPhones over a four-year period. It doesn’t expect to profit from Apple’s coveted smartphone until 2015, something that provoked shareholder ire, although CEO Dan Hesse insists the Apple deal was a shrewd move. Sprint revealed recently that 40% of iPhone sales were to new customers in the second quarter.

September 2012 www.totaltele.com 11

pRicinG stRateGies

however, both usage and connection speed are capped. to get a smartphone up and running on Vodafone Germany’s Lte network costs €54.99 per month.

back in the Us, the market leaders are pushing customers towards plans that enable them to share data allowances between multiple devices.

Verizon was first to market in June with its share everything plan, which, as mentioned, costs $100 per month for one basic smartphone and 2Gb of data. to add an extra device–up to 10 are permit-ted–costs up to $40 a month extra, depending on the device. At&t followed suit a month later with its Mobile share plans, which follow almost exactly the same pricing model.

Capgemini’s burger supports the move. “they’re changing customer behaviour so they consume services in a way that means they can make some money,” he says. but ekholm has identified a down-side to shared data plans: customer

confusion. “if you look at online discus-sion, there are a lot of consumers saying they don’t get it,” she says. “As a consumer you have to be very savvy to make sure you’re getting the right amount of data.” indeed, various ‘cheat sheets’, fAQs, and data plan calculators have appeared online.

Ultimately though, mobile operators need to make returns on their network investments and unlimited tariffs may not enable them to do that in the long term.

“encouraging rational price plans is ultimately healthy for the market,” burger insists. n

Organised by:

www.totaltele.com/Þnancesummit

10 – 11 October 2012 GrandÊConnaughtÊRooms,ÊLondon

2ÊdayÊconferenceÊforÊthoseÊinvolvedÊinÊÞnanceÊ andÊinvestmentÊforÊglobalÊtelecommunications.

CONFERENCEÊBROCHUREÊISÊNOWÊAVAILABLEÊTOÊDOWNLOAD

TotalÊTelecomÊFinanceÊSummitBestÊpracticeÊÞnanceÊstrategiesÊ forÊglobalÊtelecoms

Sponsored by:

Top seven US mobile operators by subscribers, June 2011-June 2012

120

100

80

60

40

20

0

mob

ile s

ubsc

riber

s (m

illion

s)

n June 2011 n June 2012

AT&T VerizonWireless

Sprint T-mobile USA metropCS LeapWireless

US Cellular

Source: operators

12 www.totaltele.com September 2012

pRiMe nuMBeRs cOntacts

eDitORiaL4th Floor, Welken House, 10-11 Charterhouse Square, London EC1M 6EH +44 (0)20 7608 7030; [email protected]

tOtaL teLecOMMary Lennighan [email protected] Editor +44 (0)20 7608 7069nick Wood [email protected] Assistant Editor +44 (0)20 7608 7046Michelle young [email protected] Art Editor

aDVeRtisinGHEAD OFFICE, LONDON Keith Dalton [email protected] Sales Director +44 (0)20 7608 7065Jessica Gillies [email protected] Manager +44 (0)20 7608 7027Oliver chandler [email protected] Manager +44 (0)20 7608 7041

UNITED STATES AND CANADA KCS International T +1 717 397 7100 F +1 717 397 7800 Karen c smith-Kernc – East [email protected] alan Kernc – West & Canada [email protected]

JApAn Hiroko Kujime [email protected] Business T +81-3-3661-6138 F +81-3-3661-6139

pRODuctiOn/ suBscRiptiOn/custOMeR seRVicesPlease forward all advertising material directly to: [email protected] aleisha Bryant [email protected] Customer Services Executive +44 (0) 7608 7042 or subscribe free at: www.subscription.co.uk/totaltelecom

MaRKetinGtally Judge [email protected] Marketing Manager +44 (0)20 7608 7076Ruth clark [email protected] Marketing Executive +44 (0)20 7608 7047

eVentsMatthew secker [email protected] Conference Director +44 (0)20 7608 7039charles Georgiou [email protected] Project Manager +44 (0)20 7608 7071

ManaGeMentRob chambers [email protected] Publisher +44 (0)20 7608 7077Greg Hitchen [email protected] Chief Executive Officer

OtHeR puBLicatiOnsOnline: www.totaltele.comTelevision: www.totaltele.tv

tOtaL teLecOM eVentsWorld communication awards www.worldcommsawards.comWorld Vendor awards www.worldvendorawards.comasia communication awards www.terrapinn.com/2011/asiatotal telecom Worldwww.totaltele.com/world total telecom Wireless Worldwww.totaltele.com/wireless

Total Telecom+ is published by

© 2012. All rights reserved.

Terrapinn Holdings Ltd registered office: 4th Floor Welken House, 10-11 Charterhouse Square, London EC1M 6EH

2.5 billio�nCellular M2M

co�nnectio�ns wo�rldwide by 2020, up fro�m 277

millio�n in 2012. (Strategy Analytics)

appLe nOt sO HOt in cHinaThe Chinese do not love the iPhone as much as consumers in most other global markets, according to new data from iHs. Apple shipped 5.2 million iPhones in China in the first six months of 2012, leaving it in seventh place in the vendor rankings with a market share of 7.5%. Global players samsung and nokia came in ahead of Apple–the former by a considerable margin–as did four Chinese vendors, some of which are better known on the international stage than others. Apple is at a disadvantage in China for two key reasons: it does not offer a TD-sCDMA version of the iPhone, and it does not have an entry-level smartphone. iHs predicts 160 million smartphones will ship in China this year, of which 28 million will use TD-sCDMA.

$25 billio�n Revenue o�ppo�rtunity fo�r netwo�rk manufacturers

pro�viding services to� enterprises by 2016 (Infonetics Research)

MOBiLe Data DRiVes apac ReVenue GROWtHTelecoms retail revenues in the Asia-Pacific region’s emerging markets–including india and China–will exceed us$320 billion by 2016, up from $230 billion in 2011, according to new research from Analysys Mason. Mobile data will be the biggest market driver, with revenues coming it at $112 billion by 2016; 3G and 4G services will together account for 46% of connections by the same date. The mobile market in general will account for a bigger proportion of the emerging Asia-Pacific telecoms space going forward, claiming an 83% share of retail revenues by 2016, up from 78% in 2011, while over the same period mobile penetration will rise to 95% from 63%. Mobile average revenue per user (ARPu) in the region has declined significantly in recent years–from $10 to $7.4 per month in 2008-2011–and will continue to fall, albeit at a slower pace; Analysys Mason predicts ARPu will stand at $6.5 per month by 2016.

BuiLDinG up tHe cORePurchases of mobile core gateway equipment for packet core networks will exceed Us$1.2 billion this year, up 19% on 2011, driven by Lte network deploy-ments, according to Abi research. “recent network outages seen at O2 in the Uk, Orange in france, t-Mobile and Verizon in the Us are all related to issues in the mobile core,” says Aditya kaul, practice director of mobile networks, at the analyst firm. As such, he predicts operators ultimately will be forced to upgrade their mobile core.

cOnsuMeR spenDinG On tHe upConsumers worldwide will spend $2.1 trillion on digital information products and services–including mobile phones, computing and entertain-ment devices, services, software and content–in 2012, an increase of $11 billion on 2011, according to Gartner. the analyst firm predicts growth of around $130 billion per year to reach $2.7 trillion by the end of 2016. the three largest sections of the market are, and will continue to be, mobile services (37% of the 2012 total), mobile phones (10%), and entertainment services, including cable, satellite, iPtV and online gaming (10%).

Source: Analysys mason

teLecOMs RetaiL ReVenue, eMeRGinG asia-pacific350

300

250

200

150

100

50

02008 2009 2010 2011 2012 2013 2014 2015 2016

Ret

ail r

even

ue (U

S$

billio

ns)

n Business network services n Fixed broadband n Fixed voice n Handset data n mobile broadband n mobile messaging n mobile voice

cHina sMaRtpHOne suppLieRs MaRKet sHaRe

RanK cOMpany sHaRe (%)

1 Samsung 20.8%

2 Lenovo 11.0%

3 Coolpad 10.4%

4 Huawei 9.8%

5 Nokia 9.1%

6 ZTE 8.4%

7 Apple 7.5%

Others 22.9%

total 100.0%

Source: IHS (August 2012)

The Mobile Show EU is designed for your whole mobile team. In one location over 2 days, this 4 stream event will show you how to deliver a flawless mobile product. It covers the whole mobile process from developing apps to sealing the deal with a top quality mobile commerce site. With two additional streams dedicated to mobile advertising and m-loyalty you’ll be well set to engage and retain your mobile customers.

Register now to secure your place. Don’t forget your special discount codeto claim your Total Telecom 10% discount: JEWB

Ian CarringtonDirector Mobile EMEA

James Davlouros V.P. Mobile Business

Development Mastercard

Olivier RoparsSenior Director, Europe

Mobile CommerceeBay

Chief WonkaCo-founder

Ustwo

Jude BrooksDigital Marketing

ManagerCoca-Cola

Over 30 speakers including:

Mobile solutions for all brands17 - 18 October 2012, 200 Aldersgate, St Pauls, London, UK

www.terrapinn.com/mobileshoweu

The region's leading event for telecom operators2-3 October, Atlantis Hotel, The Palm, Dubai, UAE

Register now and get the offer price - on your phone

Scan this QR pattern with the camera on your smartphone to register

Don’t have a smartphone? You can also register and get the offer on our wesbite

www.terrapinn.com/twme/totaltele

Join us at Telecoms World Middle East to tackle the biggest issues bursting out of Telco boardrooms.

Insights from the biggest names in the industry:Dr Kim Kyllesbech Larsen, SVP Next Generation Technologies, Deutsche TelekomChris Harper, VP International Network, SprintAmol Patel, Head of Emerging Markets, PayPal Mobile

Register now to secure your placeCall +971 4 440 2520

2012

spon

sors

www.terrapinn.com/twme/totaltele