world sugar outlook 2015

DESCRIPTION

What is the outlook for the sugar industry in the year 2015TRANSCRIPT

International Sugar Journal | ISJ's World Sugar Outlook 20153 PBwww.internationalsugarjournal.com

ISJ’s World Sugar Outlook 2015

Analysis and overview of the sugar and sweetener industries

JOURNAL

INTERNATIONALsugar

Sugar PlantSugar Refinery

Bioethanol PlantCogeneration PlantBio-based Industry

FROM BASIC ENGINEERING TO FULL TURNKEY PROJECT

Contact in Argentina: [email protected] www.dscontractors.com.ar

Contact in Brazil: [email protected] www.dsempral.com.br

Single Point Responsibility through EPC or EPCM+® with guaranteed:

Process Performances

Time Schedule

Budget

International Sugar Journal | ISJ's World Sugar Outlook 20154 5www.internationalsugarjournal.com

Extraction plants

Diffusers

Pulp presses

Fluidised-bed steam dryers

Evaporators

Crystallisation plants

Massecuite pumps

Centrifugals

Sugar dryers and coolers

Engineering and consulting

Assistance

E1810

The next generation – The new standardThe BMA E-series

Our revolutionary design focusing on sim-plicity and ease of operation as well as a decrease in downtime will exceed your utmost expectations: superior sugar qual-ity that suits your individual requirements, highest yields and low energy require-ments. That’s what we call efficient!

For further information contact: BMA, phone +49-531-8040, [email protected]; www.bma-worldwide.com

Passion

for

Progress

International Sugar Journal | ISJ's World Sugar Outlook 20154 5www.internationalsugarjournal.com

Contents

The EU sugar market post 2017 Leonardo Bichara Rocha

Editor: Arvind Chudasama MSc., MAgSt. (Qld), MCLIP Email: [email protected] Design and production: Snehal Sanghani Display and online advertising: Business Development Manager: Stuart Velden Direct: +44 (0)20 7017 7559 Email: [email protected] Marketing and circulation: Marketing Director Priyanka Adhikari Phone: +44 (0)20 3377 3045 Subscriptions: Phone: +44 (0)20 7017 5540 Email: [email protected] Publisher: Informa UK International Sugar Journal: Christchurch Court, 10-15 Newgate Street, London EC1A 7AZ, UK. Phone: +44 (0)20 7017 7500 Email: [email protected] www.agra-net.com

All technical articles have been approved by our panel of distinguished referees. Other editorial material appears at the discretion of the Editor. While information is compiled with all due care, Informa UK Ltd will not be liable for the consequences of anyone acting or refraining from acting in reliance on any information. ISBN 978-1-78207-335-2 ‘World Sugar & Ethanol Outlook’ is published annually by Informa UK Ltd. © 2014 Informa UK Ltd. Conditions of Sale: 1. All rights reserved, no part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise without prior written permission of the Publisher. Photocopying Licence: Informa UK Ltd. does not participate in a copying agreement with any Copyright Licensing Agency. Photocopying without permission is illegal. 2. All abstracting of the content for republication and sale must have prior permission from the Publisher. 3. The publication must not be circulated outside the staff who work at the address to which it is sent, without prior agreement with the Publisher.

Intercropping in sugarcane: A practice worth pursuing? Ramouthar, R. Rhodes, T. Wettergreen, U. Pillay, M.R. Jones, R. Van Antwerpen and S.D. Berry

Challenges and potential solutions for storage of large quantities of bagasse for power generation BS Purchase, S Rosettenstein and DV Bezuidenhoudt

Knowledge, an underexploited input for increasing not only cane productivity Arvind Chudasama

Figure 5: Exploded flange-‐connection of C-‐massecuite pipeline at outlet reheater (left) Bent floor-‐plates above place of explosion (right)

Several samples were taken around the spot where the accident occurred. The results given in (Table 2) indicate clearly that a chemical reaction, most probably due to Strecker degradation, took place that massively changed product characteristics.

Table 2: Chemical changes in products of C-‐massecuite degradation

Criteria Chemical change decrease of pH down to 4.9 decrease of polarization -‐ 11 % pol increase of reducing substances from 0.2 to 4.1 % dry matter increase of insolubles from 0.1 % to 6.3 % presence of furanes Yes

Even though the massecuite pipe above the centrifuges was open, massive increase in pressure occurred which finally led to the fatal explosion. The combination of high massecuite viscosity (after product) and a long distance between the place of heating and the discharge, caused that pressure to increase much faster than the massecuite could flow. It is after all an open question whether an open bottom valve of the vertical crystallizer would have been sufficient to avoid the pressure build-‐up.

Follow-‐up of the accident

The experience of such a fatal accident gave Suiker Unie the responsibility to take as much preventive measures as possible and to share the experience within the business. First actions taken were to repair the installation and to put fail-‐safe modifications in place before authorities gave permission to restart the production. In parallel much attention was paid to confidence building of the operators.

Strecker degradation an unknown phenomenon? Arend Wittenberg

Review and future options for computer modelling in the sugar industry F Plaza, GA Kent, DW Rackemann and DW Stephens

New build projects in the global sugar sector over July 2013 to August 2014 Arvind Chudasama

22

32

44

52

58

66

First estimate of the world sugar balance 2014/15 F.O. Licht

4

14

Intense sweeteners: Diversity prevails Lindsay Jolly

72

ISJ’s World Sugar Outlook 2015

Extraction plants

Diffusers

Pulp presses

Fluidised-bed steam dryers

Evaporators

Crystallisation plants

Massecuite pumps

Centrifugals

Sugar dryers and coolers

Engineering and consulting

Assistance

E1810

The next generation – The new standardThe BMA E-series

Our revolutionary design focusing on sim-plicity and ease of operation as well as a decrease in downtime will exceed your utmost expectations: superior sugar qual-ity that suits your individual requirements, highest yields and low energy require-ments. That’s what we call efficient!

For further information contact: BMA, phone +49-531-8040, [email protected]; www.bma-worldwide.com

Passion

for

Progress

International Sugar Journal | ISJ's World Sugar Outlook 20156 7www.internationalsugarjournal.com

First estimate of the world sugar balance 2014/15F.O. Licht

Email: [email protected] Tel: +49 (0)454 188 920 Website: www.agra-net.com

Introduction

World sugar futures remained under pressure in recent months as ample supplies of sugar are searching for a destination with the past 2013/14 (Oct/Sep) season producing a global surplus for the fourth consecutive season. Thus raw sugar prices hit 13.32 cents/lb on September 17, the lowest since May 2010, while October refined sugar futures touched $384.90 a tonne in the run-up to their expiry, the weakest for the front-month since April 2009.

The fast pace of crushing in Brazil’s key Centre South sugarcane region has added additional pressure on prices in October ‘14 as it increased available near-term supplies and made it more difficult for old-crop (2013/14) supplies from Thailand to find a final destination. Despite a fractional increase in CS sugar output in the season to mid-October there is unanimous agreement among analysts that cane and sugar totals will be sizeably reduced this year with a “sudden death” of the crushing season likely in coming weeks. A major element of weakness is the general lack of large-scale demand for sugar as many countries have already refilled inventories that were depleted during the deficit phase of the world sugar market. Last but not least, the sugar market was dealt another blow at the end of October when Brazilian president Dilma Roussef won another four-year term in office. Her tight victory in Sunday's election sent Brazilian financial markets plunging, as many investors had been hoping for pro-business challenger Aécio Neves. Adding pressure to the sugar market are concerns that subsidised

gasoline prices will remain in place with the re-election of Rousseff as her administration had used this tool to rein in inflation in recent years. The president of sugarcane industry group Unica called for a dialogue with Rousseff, asking her to clarify her stance on ethanol's place in Brazil's energy matrix.

Persisting weakness, and sometimes even further weakening of emerging market currencies against the US dollar have also added a bearish element to sugar prices. Many emerging market currencies continue to be plagued by political uncertainty as protests and geopolitical tensions have sprung up earlier this year.

Current indications are that the period of overproduction in the world sugar market may come to an end in 2014/15 with supply and demand almost matching. Our figures suggest that there will be a fractional deficit of 0.6 mln tonnes in 2014/15, which would follow an upwardly revised surplus of 4.7 mln tonnes in 2013/14. The numbers show that total output in 2014/15 on an Oct/Sep sugar year basis could be 178.7 mln tonnes, down from 181.4 mln the previous year but still 1.9 mln tonnes above apparent consumption. If around 2.5 mln tonnes of unrecorded consumption (the difference between exports and imports) are subtracted, the deficit in 2014/15 amounts to the aforementioned 0.6 mln tonnes (table 1).

We would like to recall that F.O. Licht does not include the sugar equivalent of beet and cane that were not processed into the end product crystal sugar (such as those used for fuel ethanol or biogas) in its sugar production estimates, which differs from the approach used

A major element of weakness is the general lack of large-scale demand for sugar as many countries have already refilled inventories that were depleted during the deficit phase of the world sugar market

International Sugar Journal | ISJ's World Sugar Outlook 20156 7www.internationalsugarjournal.com

by some sugar associations and official EU statistics. As always, all production figures are in raw value terms, which can be converted to white value terms by multiplying by 0.92.

Last but not least, it may be pointed out that our World Sugar Production forecasts are based on national crop years, while each country's numbers are recalculated to a uniform time period (in our case Oct/Sep) for our World Sugar Balance forecasts - the precondition for the calculation of the change in stocks (i.e. the surplus/deficit) during a given year (figure 1).

The sharpest decrease in output is expected in South America, where total output is seen falling by 3.5 mln tonnes year-on-year to just below 44.0 mln. Asian sugar production in 2014/15 is seen down 2.1 mln tonnes on the year at 66.2 mln, which is however still within sight of last year’s all-time high of 68.2 mln tonnes. North & Central American sugar output may be hardly changed at 22.4 mln tonnes compared with 22.1 mln last year, while African production is seen up 0.5 mln tonnes at nearly 12.0 mln. The strongest rise in output will be seen in Europe where sugar production is headed for a 2.0 mln tonne annual increase to 29.5 mln tonnnes. Last but not least, Oceania's sugar production may reach 4.8 mln tonnes, up modestly from 4.6 mln the year before (table 2).

Europe

European sugar production will rise significantly in 2014/15 as weather conditions will allow yields to reach bumper levels in many EU countries while the area under cultivation has been rather unchanged.

EU sugar production is seen rising by 1.6 mln tonnes on the year to 18.6 mln after output shrank for two consecutive years in the wake of the bumper 19.1 mln tonne crop in 2011/12. A mild and short winter allowed beet sowing to start early and be completed in a timely manner with favourable conditions in the course of the long growing season leading to strong beet growth. As a result, most countries expect yields at or close to record levels.

Russia's 2014/15 beet campaign is characterized by lower yields due to drought damage in July and August. With the first rise in area under cultivation in three years partly compensating for this we currently expect sugar output to fall modestly to 4.5 mln tonnes from 4.7 mln a year ago.

Turkey’s area under beet rose further in 2014/15 due to another rise in the production quotas. Sugar output of the country's 33 factories this season is therefore seen up a bit

Table 1. World sugar balance Oct/Sep (1,000 tonnes, raw value)

Sugar 2014/15 2013/14 2012/13 2011/12 2010/11

Opening stocks 77,270.5 72,594.0 64,764.3 58,348.5 57,004.9

Production 178,743.7 181,404.0 184,443.1 174,785.3 165,473.6

Imports 61,295.6 62,135.3 62,799.6 60,194.9 59,643.1

Consumption 176,834.4 175,176.3 172,153.6 167,892.3 162,438.4

Exports 63,793.7 63,686.5 67,259.5 60,672.0 61,334.7

Ending stocks 76,681.7 77,270.5 72,594.0 64,764.3 58,348.5

+/-Production -2,660.3 -3,039.1 9,657.8 9,311.7 6,341.4

+/-% -1.47 -1.65 5.53 5.63 3.98

+/-Consumption 1,658.1 3,022.7 4,261.3 5,453.9 411.0

+/-% 0.95 1.76 2.54 3.36 0.25

Stocks in % of consumption

43.36 44.11 42.17 38.57 35.92

Global surplus/deficit

-588.8 4,676.5 7,829.7 6,415.8 1,343.6

Note: May not add due to roundings; consumption excluding unrecorded disappearance

120

130

140

150

160

170

180

190

55

60

65

70

75

80

85

2003

/04

2004

/05

2005

/06

2006

/07

2007

/08

2008

/09

2009

/10

2010

/11

2011

/12

2012

/13

2013

/14

2014

/15

Ending StocksConsumption (incl. ΔEx-Im)Production

Stocks Prod/Cons

World Sugar Balance(mln tonnes, raw value)

F.O. Licht

Figure 1. World sugar balance

Table 2. World sugar production by regions Oct/Sep (1,000 tonnes, raw value)

2014/15 2013/14 2012/13 2011/12 2010/11

EU 18,604 17,005 17,448 19,070 15,894

Europe 29,501 27,477 28,607 30,828 24,735

Africa 11,979 11,497 11,248 10,346 10,336

N. & C. America 22,394 22,147 23,549 20,475 18,848

South America 43,963 47,434 48,669 43,024 46,217

Asia 66,150 68,212 67,129 66,293 61,388

Oceania 4,757 4,638 5,241 3,820 3,949

Total 178,744 181,404 184,443 174,785 165,474

Note: May not add due to roundings

International Sugar Journal | ISJ's World Sugar Outlook 20158 9www.internationalsugarjournal.com

from last year, at 2.7 mln tonnes.Ukraine's sugar beet harvest is expected

to be sharply higher than last year due to a combination of a rise in area as well as higher beet yields and sugar content. This may lift sugar output to 1.9 mln tonnes from 1.3 mln a year ago.

Africa

African sugar production is expected to rise to 12.0 mln tonnes in 2014/15 from 11.5 mln in 2013/14 – driven by expansion in Ethiopia and Sudan.

Sugar production on the continent is on the rise due to significant investment in some countries to raise self-sufficiency and capitalise on improved and preferential access to the EU market. Some of the projects have already come online, while others are yet under construction or in the phase of ramping up production to the newly installed capacity.

In South Africa the Oct/Sep year cuts across two campaigns, including the tail end of the local 2014/15 crush and the start of the next 2015/16 crush. Sugar production in local crop year 2014/15 was affected by dryness after output rose to a nine-year high in 2013/14. Output in 2015/16 is seen recovering somewhat, which means output on an

Oct/Sep basis is seen up only slightly at 2.5 mln tonnes from 2.4 mln in 2013/14.

Egypt's sugar output is seen hardly changed at 2.1 mln tonnes with around half of it coming from beet and the other half from cane. While cane expansion possibilities are limited there is investment in beet sugar production and refining capacities which may raise output in coming years.

Following several delays Sudan's new White Nile Sugar Factory was finally inaugurated in July 2012 but ramp-up of production at the facility has not yet had a sizeable impact on the country's total output. In fact, output even decreased to 693,000 tonnes in 2013/14 with a modest rise to 800,000 tonnes currently factored in for 2014/15.

Zimbabwe's sugar industry recovery continues as Tongaat Hulett raised output for the fourth consecutive year in 2013/14 after the industry hit rock bottom in 2009/10. Output is likely to rise further in 2014/15 as improved rainfall has aided crop development. We currently assume output to reach 491,600 tonnes, which would be the highest since 2002/03 when 580,000 tonnes were produced.

Zambia's cane yields in 2014/15 are expected to improve after the previous season’s

disappointing result, given the favourable growing conditions experienced and the benefit of a stable power supply in terms of irrigation optimisation. Top producer Zambia Sugar commenced crushing in the last week of March and output is expected to reach a new record of 440,000 tonnes. A similar output level is assumed for 15/16.

The Mozambican sugar industry may produce around 425,000 tonnes of sugar in 2014/15, up from 414,200 tonnes a year ago due to a rise in area and a recovery in cane yields.

The Ethiopian Sugar Corporation (ESC) announced that expansion projects at three existing mills have been completed, and the first of a planned seven new mills – Tendaho – has started trial production this month. While most of the mills will only become operational from 2015/16 onwards, sugar output is provisionally projected to rise to 500,000 tonnes in 2014/15 from 355,000 a year ago.

North & Central America

Sugar production in North & Central America is estimated at 22.4 mln tonnes, up from 22.1 mln in the previous year. The largest producer is the US followed by Mexico and Guatemala.

US sugar production is seen rising modestly to 7.7 mln tonnes from 7.6 mln the year before as beet sugar production is forecast to rise to 4.4 mln tonnes this season, partly offset by a fall in cane sugar production to 3.3 mln tonnes.

Mexico's sugar production in 2014/15 is seen remaining at 6.3 mln tonnes after output dropped sharply last year from a record 7.3 mln in 2012/13. Area is seen largely unchanged on the year and so are yields.

Guatemala's sugar industry has been in expansion mode in recent years. The country's 12 mills produced a record 2.9 mln tonnes of sugar in 2013/14, which compares with as little as 2.2 mln just three years before. For 2014/15 we currently expect output to be down somewhat at 2.8 mln tonnes.

Cuba's sugar industry has repeatedly failed to reach its production targets set ahead of the new crushing season as organisational and industrial problems and antiquated machinery usually hinder the mills from crushing the cane in the optimum time frame. This seems unlikely to be different in 2014/15 when the official plan calls for an increase in output by 15-20%. Thus we do not see output exceeding 1.8 mln tonnes.

South America

South American sugar production is

First estimate of the world sugar balance 2014/15

International Sugar Journal | ISJ's World Sugar Outlook 20158 9www.internationalsugarjournal.com

estimated to be sizeably reduced at 44.0 mln tonnes in 2014/15 from 47.4 mln the year before.

Brazil's 2014/15 balance year production cuts through two Centre South (CS) campaigns. It includes the tail end of the 2014/15 CS crush (1 October to the end of crushing operations in the CS) and the beginning of the next 2015/16 CS crush (up to September 30). Actual 2014/15 balance year output will therefore very much depend on the first half of the local 2015/16 crush, which is still difficult to predict at this point. Making matters worse, the dryness this year has not only affected cane yields in the current 2014/15 harvest but also hindered planting for the 2015/16 crop and proper fertilizer application, meaning that its effects will be felt for more than just one single year. Given that a further deterioration in output cannot be excluded, Brazil's total sugar production in raw value terms in 2014/15 on an Oct/Sep basis may fall to 36.0 mln tonnes from 39.7 mln in 2013/14.

Colombia's sugar production in 2014/15 is projected to be hardly changed on the year at 2.4 mln tonnes after output in calendar 2014 recovered from a very poor crop in calendar 2013.

Argentina may produce 2.1 mln tonnes of sugar in 2014/15, up from 1.8 mln in 2013/14 when output was affected by bad weather. Crushing in Argentina usually starts in May and ends in Nov/Dec, which means that Argentina's Oct/Sep 2014/15 production is made up mostly of what is locally referred to as the 2015 crop.

Peru is seen producing 1.2 mln tonnes of sugar in 2014/15, practically unchanged on the year.

Asia

The unabated rise in Asian cane sugar production seems to come to a halt in 2014/15 (for the time being) as several large-scale producers in the region are bound for a drop in output in the new season. The continent's cumulative output will still be the third-highest ever.

India's sugar industry is still caught between a rock and a hard place as the perennial heating-up of tension between millers, farmers and the government is delaying the start of the new crushing season. Despite the pile-up of huge arrears last season cane prices are still offering better returns to farmers than competing crops and the Indian Sugar Mills Association (ISMA) sees the acreage under cultivation in 2014/15 down only about 1% on the year at 5.294 mln ha. With a larger share of high-yielding cane varieties reported to be under cultivation we

currently assume a rise in sugar output to 27.0 mln tonnes (24.8 mln tonnes white value) from 26.5 mln a year ago, which would be the fifth consecutive year when the country's sugar production is set to exceed domestic consumption.

China's sugar market is still characterised by heavy imports which are pressuring domestic prices. Given that producers are operating in the red the acreage under cultivation has dropped for the new season. With challenging weather adding to the industry's woes cane sugar production may fall to 13.4 mln tonnes from 14.5 mln a year ago.

Thailand produced a record 11.6 mln tonnes of sugar in 2013/14, but dry weather in key growing areas is seen leading to a drop in sugar output to 10.5 mln tonnes in the new season.

Pakistan's cane sugar production surged to a record 5.9 mln tonnes in 2013/14 from 5.5 mln the year before as farmers expanded cane cultivation. With the industry reeling under excess supplies we have penciled in a slight drop to 5.4 mln tonnes in 2014/15, but some sources say a further rise to 6.5 mln tonnes may be on the cards.

Raw sugar production in the Philippines is forecast to rise fractionally year-on-year reaching around 2.5 mln tonnes.

Crushing in Indonesia usually starts in May and continues into December, which means that the crush affects to balance years. Most of 2014/15 balance year production is made up of what is usually referred to as the 2015 crush. Output is seen rising to about 2.7 mln tonnes in 2014/15, up from 2.5 mln a year ago.

Vietnam raised sugar output by 4% in 2013/14 due to a rise in the acreage under cane. The industry is suffering from high stocks, a problem that is exacerbated by cheaper sugar smuggled across the country's porous borders. However, acreage under cultivation is seen hardly changed on the year and output could therefore again reach about 1.7 mln tonnes.

Oceania

Sugar production in Oceania is estimated at nearly 4.8 mln tonnes, up from 4.6 mln a year ago.

Australia's sugar production in 2014/15 (Oct/Sep) is forecast to reach 4.5 mln tonnes, up from 4.4 mln last year. Harvesting in Australia usually starts around May/June, with large-scale processing taking place from July onwards to October before production volumes drop off significantly up to the end of the crush. The number for 2014/15 therefore includes the tail

International Sugar Journal | ISJ's World Sugar Outlook 201510 11www.internationalsugarjournal.com

end of this year's improved crush and the better part of the next 2015 crush, which we provisionally see at the same level as this year.

Fiji's sugar production in 2014/15 is seen rising to 210,000 tonnes from 199,000 expected for 2013/14. The industry is currently on a modest recovery path.

Sugar production in industrialised countries to recover

Sugar production in industrialised countries is seen recovering to 42.4 mln tonnes in 2014/15 after falling to 40.2 mln the year before. This would be within striking distance of the then 12-year high touched in 2011/12. Output in developing countries is forecast to fall by 4.9 mln tonnes to 136.4 mln – reflecting the projected sharp drop in Brazil.

Sugar production in importing countries is expected to remain unchanged at 87.6 mln tonnes, while sugar production in exporting countries is seen falling to 91.1 mln tonnes from last year's 93.7 mln.

World sugar consumption

What will shape world sugar demand in 2014/15?

It is widely accepted mainstream economic wisdom that population growth as well as economic growth are not only the key drivers of global sugar consumption, but also for many other staple foods (figure 2). In the case of sugar this is due to the fact that a rising standard of living usually leads to higher consumption of processed foods such as dairy, soft drinks etc. which have high sugar content. Also, the so-called income elasticity of sugar demand is usually higher for low-income countries than those in high-income countries (table 3).

It therefore always deserves taking a look at the growth prospects for the global economy, which is still struggling to get on track. But despite setbacks, an uneven global recovery continues. Largely due to weaker-than-expected global activity in the first half of 2014, the IMF in October reduced its growth forecast for the world economy downward to 3.3% for this year, 0.4 percentage points lower than in the April 2014 World Economic Outlook. The global growth projection for 2015 was lowered to 3.8%.

But despite the importance of these “general” drivers of consumption it is worth to take a second look at a few other developments that have sprung up earlier this year. Most of these can be described as impediments to growth. Firstly, the World Health Organization (WHO) in March launched a public consultation on its new draft guideline on sugars intake. With an expert peer-review process and the public consultation having been completed by the end of March, the draft guidelines are now being finalised.

The objective of this guideline is to provide recommendations on the consumption of free sugars to reduce the risk of diseases in adults and children, with a particular focus on the prevention and control of weight gain and dental caries. The WHO notes that there is increasing concern that consumption of free sugars, particularly in the form of sugar-sweetened beverages, may result in both reduced intake of foods containing more nutritionally adequate calories and an increase in total caloric intake, leading to an unhealthy diet, weight gain and increased risk of diseases.

New WHO draft guideline proposals

WHO’s current recommendation, from 2002, is that sugars should make up less than 10% of total energy intake per day. The new draft guideline also proposes that sugars should be

Table 3. World sugar consumption by regions Oct/Sep (1,000 tonnes, raw value)

2014/15 2013/14 2012/13 2011/12 2010/11

EU 19,173 18,856 18,948 18,955 19,072

Europe 31,247 30,941 30,997 30,995 30,862

Africa 19,646 19,521 18,963 18,396 17,525

N. & C. America 20,687 20,952 20,696 19,608 19,501

South America 21,356 21,165 21,126 21,045 20,455

Asia 82,184 80,886 78,665 76,146 72,393

Oceania 1,715 1,712 1,706 1,703 1,703

Total 176,834 175,176 172,154 167,892 162,438

Note: May not add due to roundings

100

120

140

160

180

World Sugar Consumption(mln tonnes, raw value)

F.O. Licht

Figure 2. World sugar consumption

First estimate of the world sugar balance 2014/15

International Sugar Journal | ISJ's World Sugar Outlook 201510 11www.internationalsugarjournal.com

less than 10% of total energy intake per day, but it further suggests that a reduction to below 5% of total energy intake per day would have additional benefits. Five per cent of total energy intake is equivalent to around 25 grams (around 6 teaspoons) of sugar per day for an adult of normal Body Mass Index (BMI).

The suggested limits on intake of sugars in the draft guideline apply to all monosaccharides (such as glucose, fructose) and disaccharides (such as sucrose or table sugar) that are added to food by the manufacturer, the cook or the consumer, as well as sugars that are naturally present in honey, syrups, fruit juices and fruit concentrates.

When finalised, the recommendations in this guideline can be used by program managers and policy planners to assess current intake of free sugars relative to a benchmark and develop measures to decrease intake of free sugars, where necessary, through public health interventions, the WHO said.

Policymakers in the UK seem to be beyond what the WHO is still thinking about. Campaign group Action on Sugar has stepped up its rhetoric with a seven-point plan to tackle childhood obesity - including proposals for a sugar tax, which it claimed was a direct response to an appeal from health secretary

Jeremy Hunt.Action on Sugar, which met with the health

secretary in April, said it had handed over its proposals in June, following a request by Hunt to suggest ways to tackle childhood obesity. Hunt eventually denied the government was planning a sugar tax, despite press revelations in early June that Public Health England had been drawing up proposals in draft plans for a new Department of Health consultation set to be launched June 26.

The seven measures called for are:

• Reduce added sugars by 40% by 2020 by reformulating food.

• Cease all forms of targeted marketing of ultra-processed, unhealthy foods and drinks to children.

• Dissociate physical activity with obesity via banning junk food sports sponsorships.

• Reduce fat in ultra-processed foods, particularly saturated fat - 15% reduction by 2020.

• Limit the availability of ultra-processed foods and sweetened soft drinks as well as reducing portion size.

• Incentivise healthier food and discourage drinking of soft drinks by introducing a sugar tax.

According to a survey by public health advocates released October 13, a majority of Mexicans say they are drinking less sugary drinks this year

International Sugar Journal | ISJ's World Sugar Outlook 201512 13www.internationalsugarjournal.com

• Remove responsibility for nutrition from the Department of Health and return it to an independent agency.A Department of Health spokesman said

that "childhood obesity is at its lowest since 1998 but more should be done." With the UK heading for general elections in 2015, shadow health secretary Andy Burnham confirmed (the opposition) Labour party was planning to slap new regulations on sugar levels in children's food if it came to power, although he repeated Labour's opposition to a sugar tax.

According to the campaign director for Action on Sugar, Katherine Jenner, EU law would likely see a sugar tax as an illegal barrier to trade, adding that her group would rather use pricing as an incentive. Jenner said one option is to use the sweetener aspartame, which is cheaper than sugar, to bring down both price and calorie content. Jenner told delegates at the UK Soft Drinks Industry Conference in London in May that soft drinks makers need to "act now or be forced to act later" when it comes to reducing sugar levels. Urging manufacturers to "quietly" reformulate their sugary drinks to reduce sugar content, Jenner said there will have to be consensus among the industry, health groups and government to make voluntary reductions work, adding that there is going to be a limited window of opportunity for voluntary reformulation.

Mexico introduces sugar tax

While a UK tax on sugar may not see the light of day, Mexico introduced a one peso (eight US cents) per litre tax on sugary drinks and an 8% tax on junk food such as potato chips, chocolates, candies and ice cream as part of a wider tax overhaul effective January 1, 2014. This made Mexico the first major soda market to tax high-calorie sodas, which could be a game changer as other countries may consider following suit.

Mexicans are the world's biggest soda drinkers, guzzling about 707. 8-ounce servings, on average, per year, according to Beverage Digest. The United States is the only other country in the same ballpark, clocking in at 701 servings.

According to a survey by public health advocates released October 13, a majority of Mexicans say they are drinking less sugary drinks this year. Just over half the 1,500 people who participated in the August survey said they have lowered their consumption of sugary drinks versus last year, while 98% said they considered drinking soda raises their risk for developing

diabetes and obesity. Nearly a fifth still drink more than three liters of soda a week, although in last year's survey a quarter of respondents drank that amount.

Carbonated beverage sales for Mexico's biggest soft-drink bottler, Coca-Cola Femsa, fell by 6.4% in Mexico during the first half of 2014, compared with the same period of 2013. The company blamed the slide on the soft-drink tax, bad weather, and a weak economy. Fellow Mexican Coke bottler Arca-Continental's sparkling drink sales in Mexico dropped 4.7% for the same period.

A separate study conducted earlier this year by Mexico's National Institute of Public Health measured the decline in sugary beverage consumption at 10% during the first three months of 2014, compared with the same period last year. That study also reported a 7% rise in purchases of beverages that are not subject to the new tax, such as plain bottled water and milk.

All in all, the tax appears to be crimping consumption of soda and sugary juices, with total sugar consumption in 2013/14 seen at 4.5 mln tonnes, down from nearly 4.7 mln a year earlier. Given that consumers tend to become accustomed to price increases over time we have assumed a similar consumption level in 2014/15.

Elsewhere, we assume that low domestic sugar prices in China as well as ongoing growth in the downstream food and beverage industries will continue to drive sugar consumption, with the total seen rising to 16.7 mln tonnes in 2014/15 from 16.2 mln a year ago. Prices in the domestic market have fallen further in the past year and are now ruling at about CNY4,000 per tonne, down from as much as CNY5,300 at this time a year ago. Low sugar prices are also supporting sugar consumption in India where prices are currently near year-ago values. All in all, we currently expect a rise in Indian consumption to 26.5 mln tonnes in 2014/15 from 26.1 mln in 2013/14.

Total Asian sugar consumption in 2014/15 is estimated to rise by 1.6% on the year to 82.2 mln tonnes, mainly a result of population and economic growth. Asia has been very much the powerhouse of world sugar consumption growth since the late 1980s. European sugar consumption is seen up a bit at 31.2 mln tonnes in 2014/15, while sugar consumption in North & Central America is expected to reach 20.7 mln tonnes, down from nearly 21.0 mln a year ago with the sugar tax in Mexico being a key contributor. Sugar consumption in South America is seen up only very little

Total Asian sugar consumption in 2014/15 is estimated to rise by 1.6% on the year to 82.2 mln tonnes

First estimate of the world sugar balance 2014/15

International Sugar Journal | ISJ's World Sugar Outlook 201512 13www.internationalsugarjournal.com

at 21.4 mln tonnes, compared with 21.2 mln last year. By far the largest consumer is Brazil with offtake in 2014/15 estimated at 12.8 mln tonnes, practically unchanged year-on-year due to a slack economy and already high per capita consumption. Sugar consumption in Africa is seen rising to 19.6 mln tonnes from 19.5 mln a year ago. Consumption in Oceania, at around 1.7 mln tonnes, is very stable with practically no year-on-year change. Australia accounts for the better part of total offtake, estimated at just above 1.3 mln tonnes.

All in all, we expect global sugar consumption to rise by 1.0% in 2014/15 and the total could reach 176.8 mln tonnes, up around 1.7 mln tonnes from last year. The forecast is rather conservative and may be revised upwards later in the year, if the necessity arises.

Sugar consumption in importing countries to reach all-time high

Developing countries are seen recording 1.5% growth in sugar consumption in 2014/15, with total consumption of these countries estimated at 129.5 mln tonnes - or about 73% of global demand. Sugar demand in industrialised countries continues to hover in a very narrow range between 46 and 47.5 mln tonnes. Offtake in 2014/15 is put at 47.3 mln tonnes, down fractionally from 47.5 mln last year.

Sugar consumption in importing countries is forecast to rise by 1.1% this year to 131.2 mln tonnes, a new all-time high. Major driver in this category is ongoing growth in India and China. Sugar offtake in exporting countries is seen rising only 0.5% in 2014/15, with the total estimated at 45.6 mln tonnes compared with 45.4 mln a year ago. Growth in this group of countries tends to be lower than in importing countries as ample availability of the sweetener comes along with rather high per caput consumption and therefore limited further growth potential.

Exportable production seen falling to 2010/11 level

Exportable production (production minus consumption) is estimated to reach 49.9 mln tonnes in 2014/15, down from 53.4 mln last year and the 2012/13 record of 56.6 mln tonnes. In fact, this will be the lowest level since 2010/11.

The effective decline will be even stronger as 4.4 mln tonnes of the total is being accounted for by the European Union, whose exports to the world market will remain limited at 1.374 mln tonnes of white sugar by the end of the 2016/17 season, or for another three seasons.

Exportable production from Africa is seen remaining rather unchanged at 2.4 mln tonnes (compared with 2.1 mln in 2013/14) as the increase in production on the continent is only sufficient to cover rising domestic demand which is fuelled by population growth. This may change from 2015/16 when several new mills are scheduled to come on stream in Ethiopia with the first one having started trial production earlier this month.

Exportable production in North & Central America is also seen hardly changed at 6.4 mln tonnes compared with 6.3 mln a year ago, with availability from the region’s three major exporters – Mexico, Guatemala and Cuba – seen rather stable.

Exportable production in Brazil is seen down sharply at 23.3 mln tonnes from nearly 27.0 in 2013/14 - due to the fact that sugar output will drop significantly in the current crushing season with no improvement foreseen for 2015/16. If realized, this would be the lowest availability of Brazilian sugars since the 2011/12 season.

Exportable production in Asia is seen falling to 8.3 mln tonnes from 9.9 mln last year due to the expected strong decrease in Thai output with Pakistan also seen having less sugar on hand to export this season.

For the fear of being repetitive, a flow figure such as exportable production does not account for stocks. This is of especial significance in the upcoming season as the strong increase in global stocks over the past few seasons should largely offset the reduced availability of sugar for export from the fresh crops. Thailand is just one example where traders still have sizable amounts of old-crop sugar for sale before fresh supplies enter the warehouses from next month. Despite a reduction in domestic inventories over the past year, India also still has ample sugar for export - if world prices allow the country to enter the export market. However, exports are not a feasible option at present world market quotations with the new government still undetermined over the continuation of an export subsidy introduced during 2013/14. Australia's exportable production in 2014/15 is seen up a bit at 3.2 mln tonnes.

Import demand seen falling further from 2012/13 all-time high

Gross imports are estimated to fall slightly to 61.3 mln tonnes in 2014/15 from 62.1 mln the year before.

China continues to import much beyond its requirements, taking over the role of the US Federal Reserve for the sugar market. The

International Sugar Journal | ISJ's World Sugar Outlook 201514 15www.internationalsugarjournal.com

Federal Reserve has been purchasing inferior assets of poor quality in recent years which neither the banks nor other investors wanted. Instead of acting in its historical role as the ‘lender of last resort’, the Federal Reserve has on its own expanded its mandate to become the ‘buyer of last resort’. The same is true for China as the country has been purchasing raw sugar from the

world market as if there is no tomorrow. In fact, Chinese refiners have been purchasing sugar for which there was no other demand, soaking up a significant chunk of the global surplus and thereby providing support to global sugar values which would otherwise have pressured international prices even further.

In fact, imports reached an astounding 4.1 mln tonnes in the recently-concluded 2013/14 season, up from 3.7 mln a year earlier and not far below a record 4.3 mln tonnes imported in 2011/12. Anecdotal evidence suggests that warehouses are brimming over in the country and the question is how long imports can continue at this level. With the further decline in domestic prices in recent months it seems likely that imports will fall in 2014/15 as out-of-quota imports do not make economic sense any longer. For 2014/15 we have therefore provisionally pencilled 2.5 mln tonnes of imports into our balance sheet.

Given that several countries have already used the market's drop to ever fresh lows in 2012/13 and 2013/14 to scale up imports and refill depleted inventories we think that import demand will moderate somewhat in 2014/15. Still, the projected import level of 61.3 mln tonnes is still rather high and compares with a record 62.8 mln tonnes imported in 2012/13.

Russia's imports may rise to 1.5 mln tonnes in 2014/15 from an estimated 1.1 mln the year before as a decline in domestic beet sugar output is seen raising import needs. If realized, this would be the highest Russian import level since 2010/11 when nearly 2.6 mln tonnes were brought in.

Indonesia is seen importing 3.7 mln tonnes of sugar in 2014/15, up from 3.2 mln a year

earlier. Domestic consumption is on the rise due to economic and population growth, while domestic production is stagnating. Making matters worse for domestic millers, the rise in demand is almost exclusively fuelled by growth in the food and beverage industries, which rely on refined sugar produced from imported raws instead of domestically produced plantation white sugar.

The United States imported about 3.4 mln tonnes of sugar in 2013/14 with Mexico supplying about 1.9 mln tonnes of deliveries. With ending stocks in 2013/14 being at the low end of what USDA considers a comfortable level and stagnant domestic production the country may even import a little more in 2014/15. This is despite a preliminary agreement struck with Mexico in recent days to limit unfettered access of Mexican sugar to the US market.

Total Asian sugar imports are estimated to reach 28.9 mln tonnes in 2014/15, down from 30.5 mln last year. European imports are seen up slightly at 11.8 mln tonnes from 11.3 mln a year ago, mostly due to the above-mentioned higher deliveries to Russia. African imports are seen falling modestly to 12.5 mln tonnes from 12.9 mln last season, due to higher domestic availability. North & Central American imports are bound to rise modestly to 5.5 mln tonnes from 5.2 mln a year ago due to the expected increase in US imports. Sugar imports into South America are negligible but seen rising somewhat to 2.1 mln tonnes from 1.8 mln a year ago.

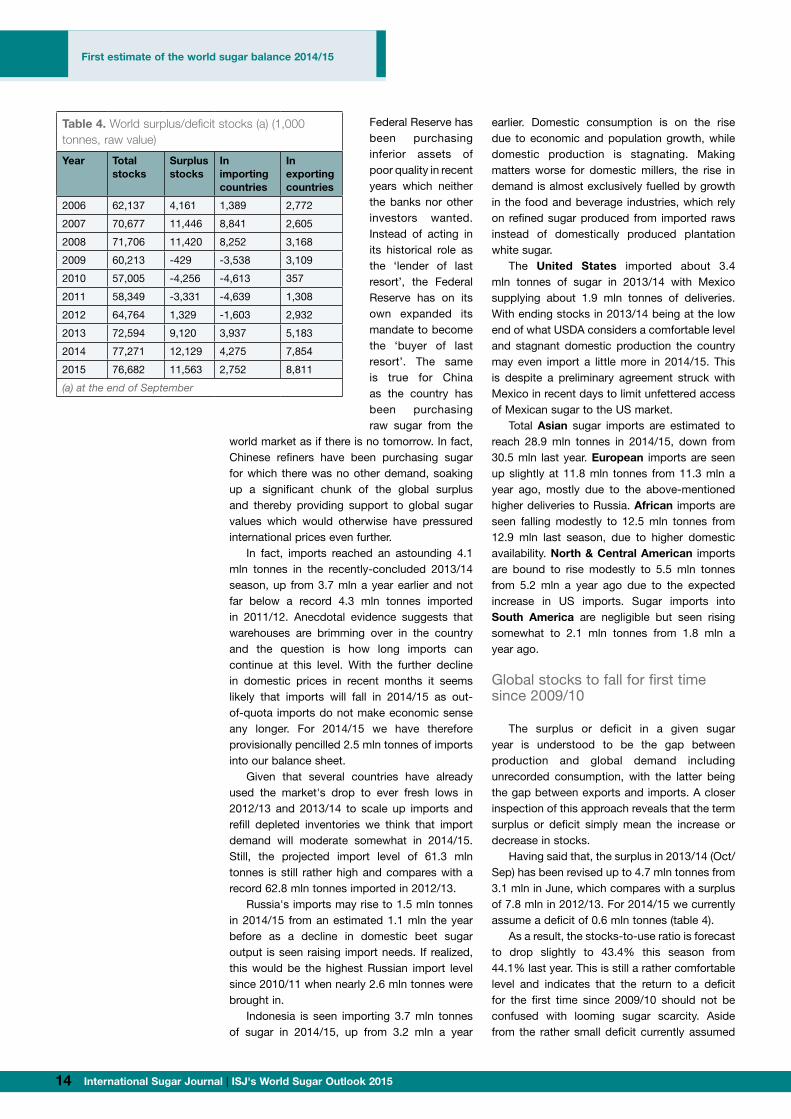

Global stocks to fall for first time since 2009/10

The surplus or deficit in a given sugar year is understood to be the gap between production and global demand including unrecorded consumption, with the latter being the gap between exports and imports. A closer inspection of this approach reveals that the term surplus or deficit simply mean the increase or decrease in stocks.

Having said that, the surplus in 2013/14 (Oct/Sep) has been revised up to 4.7 mln tonnes from 3.1 mln in June, which compares with a surplus of 7.8 mln in 2012/13. For 2014/15 we currently assume a deficit of 0.6 mln tonnes (table 4).

As a result, the stocks-to-use ratio is forecast to drop slightly to 43.4% this season from 44.1% last year. This is still a rather comfortable level and indicates that the return to a deficit for the first time since 2009/10 should not be confused with looming sugar scarcity. Aside from the rather small deficit currently assumed

Table 4. World surplus/deficit stocks (a) (1,000 tonnes, raw value)

Year Total stocks

Surplus stocks

In importing countries

In exporting countries

2006 62,137 4,161 1,389 2,772

2007 70,677 11,446 8,841 2,605

2008 71,706 11,420 8,252 3,168

2009 60,213 -429 -3,538 3,109

2010 57,005 -4,256 -4,613 357

2011 58,349 -3,331 -4,639 1,308

2012 64,764 1,329 -1,603 2,932

2013 72,594 9,120 3,937 5,183

2014 77,271 12,129 4,275 7,854

2015 76,682 11,563 2,752 8,811

(a) at the end of September

First estimate of the world sugar balance 2014/15

International Sugar Journal | ISJ's World Sugar Outlook 201514 15www.internationalsugarjournal.com

TECHNOLOGIES THERMIQUES

• Without gaskets, without�back flushing• Clear free flow channels for mixed, limed or clarified juice• Use of low pressure vapours and condensates• Compact and easy to clean• Robust and maintenance free• Multi-streams juice heaters available• Molasse cooler

the solution to your heat transfer

EASY TO CLEAN AND WIDE GAP WELDED PLATE HEAT EXCHANGERS PLATULAR®

platular®C U S T O M - B U I L T A N D V E R S A T I L E

H E A T T R A N S F E R S O L U T I O N SF O R T H E S U G A R I N D U S T R Y

www.barriquand.com +32 4377 42 49

for the new season it also takes time for the statistical surpluses and deficits to filter through into the physical market. This may be different in 2015/16 if the trend of falling production amid further rising consumption continues, with the dire financial situation of many sugar industries across the globe possibly supporting such a development.

Surplus stocks are those in excess of what is needed for an uninterrupted flow in the pipeline from factory to user and to cover consumption between the end of one production cycle and the beginning of the next. These point in the same direction and could remain at a rather high 11.5 mln tonnes at the end of September 2015, down only slightly from an estimate of 12.1 mln for September 2014. Whatever approach is applied it is evident that the market is still awash with sugar.

Outlook

Current indications for 2014/15 are that global sugar production will fall for the second consecutive season while consumption continues to rise modestly. This means that the world sugar market will likely see its first statistical deficit since 2009/10.

But even if there should be a deficit in 2014/15 it usually takes some time until a change in the market balance from surplus to deficit, or vice versa, makes its way into the trade flows. Stocks have accumulated during four seasons of global surplus and some countries are even brimming over with sugar. This is likely to cushion the market to some extent and may prevent a violent surge in values.

While the 2014/15 deficit will be a rather modest one of only 0.6 mln tonnes that should not have the potential to shatter global sugar markets, it is a clear indication that the tide is turning. Many domestic sugar industries across the world are suffering from selling sugar at prices below the cost of production, which is unsustainable in the long run and may further affect output in coming years.

Last but not least, 58 mills have already closed down in Brazil since 2008/09 but the situation for the local industry may even turn from bad to worse with the incumbent Dilma Roussef winning another four-year term in office at the Brazilian presidential elections on October 26. So while the market remains well supplied for the time being there are indeed some bullish elements on the horizon.

International Sugar Journal | ISJ's World Sugar Outlook 201516 17www.internationalsugarjournal.com

The EU is the world’s second largest sugar consumer (after India) as well as the world’s third largest sugar producer (after Brazil and India). The

bloc is also one of the world’s largest sugar importers – it was the largest importer of sugar between 2008 and 2011, losing the first spot to China in 2012. Prior to 2006, the EU was the world’s second largest exporter (after Brazil). Since 2006, following a policy that encouraged production cuts in the bloc, sugar exports have collapsed from over 6 mln tonnes to less than 2 mln tonnes, while imports, by contrast, have risen from around 2.5 mln tonnes to around 4 mln tonnes, raw value – see Fig. 1.

The impact of the 2006 reform on the industry

The 2006 Reform of the EU Sugar Regime had the main objective of incentivizing sugar production to migrate to more cost effective regions by offering higher cost producers a chance to surrender production quotas and leave the industry upon compensation.1 The Reform was implemented in the wake of a WTO panel ruling, which established that EU sugar exports, at the time in the order of around 5 mln tonnes a year, were cross-subsidised and, as such, should be capped to no more than 1.35 mln tonnes, white value. The European Commission, in a 2011 full impact assessment study2, considered the 2006 Reform to be relatively successful, as it eliminated some key

The EU sugar market post 2017 Leonardo Bichara Rocha*

FO Licht Sugar & Sweeteners Report The EU Sugar Market Post 2017

________________________________________________________________________________ 2

-4,000

-2,000

0

2,000

4,000

6,000

8,000

Thou

sand

tonn

es, r

aw v

alue

Fig. 1: EU Imports and Exports of Sugar

Imports Exports Net Exports

The EU is the world’s second largest sugar consumer (after India) as well as the world’s third largest sugar producer (after Brazil and India). The bloc is also one of the world’s largest sugar importers – it was the largest importer of sugar between 2008 and 2011, losing the first spot to China in 2012. Prior to 2006, the EU was the world’s second largest exporter (after Brazil). Since 2006, following a policy that encouraged production cuts in the bloc, sugar exports have collapsed from over 6 mln tonnes to less than 2 mln tonnes, while imports, by contrast, have risen from around 2.5 mln tonnes to around 4

mln tonnes, raw value – see Fig. 1.

Fundo Internacional de Desenvolvimento Agrícola – IFAD, Escritório Conjunto das Nações Unidas Elevador Lacerda, Praça Municipal Thomé de Souza , CEP: 40.020-010 , Salvador, Bahia

Brazil | Tel: +55-71 3183 5721 | Email: [email protected]

Figure 1. EU imports and exports of sugar

International Sugar Journal | ISJ's World Sugar Outlook 201516 17www.internationalsugarjournal.com

market control measures of domestic support, such as price intervention, production and export refunds. The Reform ended in 2009/10, with over 5.2 mln tonnes of quota sugar, white value, renounced. However, some 1 mln tonnes of quota sugar had been purchased by groups, mostly in France and Germany, leading to a net reduction in EU-wide production quotas in the order of 4 mln tonnes. Currently, several regulatory measures still apply: a) minimum beet prices; b) sugar production quotas; c) production charges (levied on the quota, amounting to EUR 12/tonne for sugar and inulin syrup and EUR 6/tonne for isoglucose); d) carry forward; e) private storage aid (never applied in practice); f) withdrawal schemes. The import duties have been and will be maintained at the level of EUR 419/tonne for white sugar and EUR 339/tonne for raw sugar, with CXL sugar imported at a EUR 98/tonne duty, and access for preferential partners of the EPA/EBA group and others kept within a duty free quota free mechanism.

As production of both sugar and isoglucose (HFS – High Fructose Syrup) is still regulated by fixed quotas distributed to Member countries, any production above the quotas cannot be freely released into the EU market. Instead, it

needs to be sold to the chemical or bioethanol industry or exported within the WTO limits of 1.35 mln tonnes. Sugar production quotas in the EU have fallen from 17.4 mln tonnes in 2005/06 to 13.3 mln tonnes in 2009/10 (rising slightly to 13.5 mln tonnes with the accession of Croatia in 2013). Isoglucose production

quotas fell only slightly from about 800 thousand tonnes to 700 thousand tonnes now. Sugar production quotas have been significantly reduced in Italy, Spain and Greece and production stopped altogether in five Member States - Ireland, Latvia, Slovenia, Bulgaria and continental Portugal. As a result, there has been a further concentration of production in the leading Member States: the market share of France and Germany increased from 43% of EU production to 52% on average. Sugar conglomerates such as Südzucker, AB Sugar, Tereos, Nordzucker, Pfeifer und Langen and Cristal Union have expanded output to reach 80% of the bloc’s total production.

The EU sugar industry is today a leaner industry, with significantly higher sugar/sugarbeet yields from a much-reduced number of players (factories) and on a reduced crop area. The number of beet sugar factories decreased sharply from 191 prior to 2006 to

108 in 2012/13.3 Sugar beet areas declined sharply from 2.2 mln ha in 2002/03 to 1.7 mln ha in 2012/13. By contrast, average sugar beet yields have increased from about 60 tonnes/ha to over 70 tonnes/ha in recent years – see table 1. Average sugar yields per ha also rose significantly from 9 tonnes/ha to over

Table 1. Selected indicators of the EU's sugar industry

Material 04/05 05/06 06/07 07/08 08/09 09/10 10/11 11/12 12/13

Sugar beet area (mln ha)

2.146 2.142 1.690 1.564 1.363 1.338 1.586 1.624 1.636

Sugar beet production (mln t)

129.448 132.112 100.792 95.185 83.778 90.682 103.815 123.977 114.548

Sugar beet yields (t/ha)

60.3 61.7 59.6 60.9 61.5 67.8 65.4 76.3 70.0

Sugar beet producer price (USD/t)

53.5 54.8 43.6 43.2 45.9 41.1 41.9 47.1 n/a

Beet sugar production (in mln mtrv)

21.258 21.887 15.614 16.338 15.244 15.574 15.725 18.875 17.620

Source: ISO/FAO

The EU sugar industry is today

a leaner industry, with significantly

higher sugar/sugarbeet

yields from a

much-reduced number of players

Currently, several regulatory measures still apply: a) minimum beet prices; b) sugar production quotas; c) production charges

International Sugar Journal | ISJ's World Sugar Outlook 201518 19www.internationalsugarjournal.com

11 tonnes/ha while sugar beet prices have declined from an average of over USD 50/tonne to just over USD 40/tonne. Of importance, since 2005, average beet yields in the EU have risen by 20%, whilst maize and wheat yields have not shown any significant upward trend.

Sugar consumption and trade

The EU is a mature sugar market, with a high level of per capita consumption – 39kg in 2012 compared to a world average of 25kg. According to the ISO Sugar Consumption model, similarly to other developed markets, but unlike developing countries, sugar consumption growth in the EU can be largely explained by population growth – elasticity of demand of 66% - and to a lesser extent by income growth – elasticity of demand of 30%4.

Of interest, the EU received a major boost to its overall consumption levels from the accession of ten new member countries in 2004, which brought additional sugar consumption of 3 mln tonnes. The further enlargement of membership with the incorporation of Bulgaria and Romania in 2007 added another one mln tonnes, taking overall consumption to over 18 mln tonnes, raw value. Since then, consumption has been rising slowly at an average rate of about 1% a year, excepting the year of 2009, when consumption slumped as a result of the world financial crisis.

Since 2007 gross sugar imports have been consistently larger than 3 mln tonnes, raw value, while net sugar imports by the EU have averaged about 2 mln tonnes a year.

Figure 2 shows total EU imports of white and raw sugar between 2002 and 2012. Raw sugar imports traditionally account for up to 80% of the total volume of EU imports, with the sugar sourced mainly from traditional preferential partners of the ACP/LDC group (duty free) and CXL countries (import duty of EUR 98/tonne). White sugar imports originate mainly from the West Balkans and other European countries as well as more recently from Mauritius, the largest ACP sugar exporter to the EU. Sugar imports from ACP (African, Caribbean and Pacific) countries and LDCs (Least Developed Countries) are now duty-free quota-free. The EU has also signed some Free Trade Agreements with Latin American countries and others. Last but not least, the Commission has kept its prerogatives to allow duty-free imports of sugar and isoglucose for industrial use until 2016/17, which has been set at a level of 400 thousand tonnes since the 2008/09 season, although only a fraction of these quotas have in reality been filled.

Non-LDC ACP sugar imports

Total sugar imports from non-LDC ACPs have averaged around 1.3 mln tonnes over the past few seasons. Several ACP countries have been struggling to increase sugar production for further exports due to difficulties encountered to modernize their industries amid an increasingly competitive environment internationally. Among all LDCs and ACPs, the share of non-LDC ACPs has fallen from nearly 90% in the middle of the past decade to less than 70% now.

The largest non-LDC ACP sugar exporter to the EU is Mauritius, with a share of around 30% of total ACP shipments. Since 2009, Mauritius has been exporting white sugar to Südzucker under a 6-year contract. The other non-LDC ACPs export mostly raw sugar to the EU. While countries like Swaziland have managed to nearly double the volume of exports over recent years to over 250 thousand tonnes, raw value, others like Fiji and Jamaica faced difficulties, with shipments falling by as much as 50%.

Duty-free quota-free exports for ACPs will from October 2014 become conditional on their joining Economic Partnership Agreements.5 In the framework of EPAs, the EU grants duty-free quota-free access to the products originating in ACP countries (with a transition period for sugar) while ACPs offer progressive liberalisation of trade and can exclude products from liberalisation. By 7 February 2014, there were seven regions with on-going EPA negotiations with the EU: Caribbean, Pacific, West Africa, Central Africa, Southern African Development Community (SADC), Eastern and Southern Africa (ESA) and East African Community (EAC). Of interest, some countries within these regions have also initiated bilateral “stepping stone” (or “interim”) EPAs. Interim agreements establish

FO Licht Sugar & Sweeteners Report The EU Sugar Market Post 2017

________________________________________________________________________________ 5

with the sugar sourced mainly from traditional preferential partners of the ACP/LDC group (duty free) and CXL countries (import duty of EUR 98/tonne). White sugar imports originate mainly from the West Balkans and other European countries as well as more recently from Mauritius, the largest ACP sugar exporter to the EU. Sugar imports from ACP (African, Caribbean and Pacific) countries and LDCs (Least Developed Countries) are now duty-free quota-free. The EU has also signed some Free Trade Agreements with Latin American countries and others. Last but not least, the Commission has kept its prerogatives to allow duty-free imports of sugar and isoglucose for industrial use until 2016/17, which has been set at a level of 400 thousand tonnes since the 2008/09 season, although only a fraction of these quotas have in reality been filled.

Source: ISO

Non-LDC ACP sugar imports Total sugar imports from non-LDC ACPs have averaged around 1.3 mln tonnes over the past few seasons. Several ACP countries have been struggling to increase sugar production for further exports due to difficulties encountered to modernize their industries amid an increasingly competitive environment internationally. Among all LDCs and ACPs, the share of non-LDC ACPs has fallen from nearly 90% in the middle of the past decade to less than 70% now. The largest non-LDC ACP sugar exporter to the EU is Mauritius, with a share of around 30% of total ACP shipments. Since 2009, Mauritius has been exporting white sugar to

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Tota

l im

port

s by

the

EU

in t

hous

and

tonn

es

Years

Fig. 2: EU Imports of White and Raw Sugar, 2002-2012 (Raw Value, Thousand Tonnes)

Raw Sugar White Sugar

Figure 2. EU imports of white and raw sugar, 2002-2012 (raw value, thousand tonnes)

The EU sugar market post 2017

International Sugar Journal | ISJ's World Sugar Outlook 201518 19www.internationalsugarjournal.com

provisions on market access of goods but leave other aspects of the EPA (services, investments and trade related matters) open for further negotiations.

Sugar imports under Everything-but-Arms (EBA) initiative

Sugar imports by the EU from LDC (Least Developed Countries) producers are currently regulated by the Everything But Arms (EBA) initiative on a duty-free quota-free basis. In 2012 imports from this group of countries reached a record 600 thousand tonnes, significantly higher than the less than 200 thousand tonnes prior to the Reform of the EU sugar regime. As a result, the share of LDCs in total ACP/LDC preferential exports to the EU has increased from around 10% in the middle of the past decade to over 30% now.

The bulk of current deliveries from the LDC group come from seven countries: Mozambique, Zambia, Sudan, Cambodia, Malawi, Madagascar and Laos. Exports from Mozambique and Zambia have risen quite spectacularly over the recent years, with Mozambique shipping a record 234 thousand tonnes to the bloc in 2012, up from less than 40 thousand in 2006. Among other top LDC exporters, countries like Cambodia and Laos only started shipping sugar to the EU from 2008. Raw sugar deliveries from Cambodia in 2012/13 tripled to 50,700 tonnes as new mills came on stream and local output continues to rise.

CXL imports

The third category of sugar imports comprise sugar bought under special CXL arrangements, which incur an import duty of EUR 98/tonne for an annual quota of up to 677 thousand tonnes and include quantities calculated from compensatory adjustments regarding traditional partners of newer member states, such as Finland, Romania and Bulgaria. It also includes

India under special duty-free access for 10 thousand tonnes. Actual export volumes by CXL quota holders have been greater, as the commission has increased access through exceptional measures at times of low export availability from preferential partners.

Preferential import schemes with European Countries

Other agreements include duty-free tariff quotas for white sugar imports from western Balkan countries – known as the 'Balkans Initiative', which was adopted in 2000. This grants tariff quotas to eligible sugar products originating in Serbia, Albania, Bosnia and Herzegovina and the former Yugoslav Republic of Macedonia, the largest of which being the 180 thousand tonne quota held by Serbia. Moldova benefits from an Autonomous Trade Preferences agreement with the European Union, which includes a sugar export quota of 34 thousand tonnes. In addition, in 2012, it was agreed to establish export quotas for Ukrainian sugar to the EU at the amount of 20 thousand tonnes per year.

The new free trade agreements

On 26 June 2012, the EU signed a trade agreement with Colombia and Peru, which came into effect on March 1st 2013. The agreement with Colombia and Peru includes opening of a duty-free TRQ for 84,000 tonnes of sugar, of which Colombia has received 62,000 tonnes and Peru 22,000 tonnes.

On 29 June 2012, the EU signed with Central America an agreement leading to duty-free tariff quotas for agricultural products, which include sugar. The agreement was put in place in 2013. The trade deal has been applied with Honduras, Nicaragua and Panama since 1 August 2013, with Costa Rica and El Salvador since 1 October 2013 and with Guatemala since 1 December 2013.

Table 2. Total sugar imports by the EU from CXL countries (Thousand Tonnes, Raw Value)6

Origin 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Brazil 45 65 165 164 165 855 993 775 1,161 1,720 1,066

Cuba 94 66 110 40 63 131 73 125 75 74 210

Australia 1 2 1 1 1 18 11 27 0 12 13

India 57 18 22 11 28 48 14 14 5 28 17

Total CXL 197 151 298 216 257 1,052 1,091 941 1,241 1,834 1,306

Share of Brazil (in %) 22.8 43.0 55.3 76.0 64.3 81.2 91.0 82.3 93.5 93.7 81.6

Source: ISO

The EU is a mature sugar market, with a high level of per capita consumption – 39kg in 2012 compared to a world average of 25kg

International Sugar Journal | ISJ's World Sugar Outlook 201520 21www.internationalsugarjournal.com

For Panama, the EU has opened a duty-free import quota for sugar and sugar-containing products of 12,000 tonnes (in raw sugar equivalent) for 2013, which rises to 12,360 tonnes for calendar 2014 and will be increased by 360 tonnes each year from January 2015. For the other countries in Central America excluding Panama, the agreement allows duty-free imports of sugar and sugar-containing products at 150,000 tonnes (raw sugar equivalent) for 2013, rising to 154,500 tonnes for calendar 2014 and by 4,500 tonnes each year from January 2015.

Sugar refining

The reliance on rising quantities of sugar imports over the past eight years has aided the further development of raw sugar refining sector in the EU. Since 2006, new refineries have been opened in Member States where there was no refining activity before, like Denmark, Italy and Spain7. Second, some significant raw sugar refining capacity has been added to the EU with the accession of both Romania and Bulgaria, which traditionally imported some 300 and 500 thousand tonnes, respectively, of raw

sugar for refining. All in all, there are today 34 refineries today in the EU, of which 30 are defined as full-time refiners.8 Full-time refineries (until marketing year 2016/17) currently have a 3 months’ window to apply in priority for import licenses of raw sugar. Once this prerogative expires in 2016/17, all operators, including part-time refineries, beet processors that refine off crop or co-refine, as well as traders, will be able to apply for licenses since the first day of the marketing year.

The 2017 reform

On 26 June 2013 a political agreement on the Reform of the CAP was reached between the Commission, the European Parliament and the Council. The agreement included extending the current market provisions for sugar until 2016/17 and abolishing sugar and isoglucose production quotas, as well as minimum beet prices, thereafter.

The new regime will still have general safeguard measures that the European Commission can use in case of market disturbances. For example, it will be still possible to make use of private storage aid in case of domestic prices falling significantly below the reference prices, which will be kept unchanged:

i. For white sugar: EUR 404.4/tonne;ii. For raw sugar: EUR 335.2/tonne;

Until 2016/17, it will still be a prerogative of the Commission to adopt acts determining the appropriate quantity of out-of-quota sugar and imported raw sugar that can be released onto the Union market. The quotas for the production of sugar, isoglucose and inulin syrup at national or regional level during the transitional period until 30 September 2017 remain fixed at basically the final level of quotas allocated in marketing year 2010/2011.9 The transitional provisions still allow for out-of-quota to be transferred to the chemical or ethanol industry, to be carried forward to the next marketing year, to be released into the domestic market under special circumstances or exported within quantitative limits. Otherwise they are still subject to a surplus levy.

Isoglucose: How big a threat?

One of the key market focuses regarding the consequences of the 2017 Reform of the EU Sugar Regime is the potential threat coming from isoglucose, consumed by industrial users (especially soft drink industry but also dairy products) and produced mainly from maize (but also wheat) starch. Similarly to the sugar sector, isoglucose production in the EU has become more concentrated. Quotas for production of isoglucose are now concentrated in only nine member states, as opposed to 13 member states prior to the 2006 Reform .

Some market analysts estimate that up to 30% of the EU’s sugar consumption could be substituted by isoglucose, but that would mean an almost 100% penetration of isoglucose in the beverage industry, which is unlikely. As of early 2014, isoglucose prices were lower than sugar prices by some 10-20%10, although this gap could easily disappear and even change signs with additional sugar output following the abolition of quotas in 2017.

Isoglucose production is unlikely to rise in regions where there is already a grains production deficit in the EU. This includes the UK and Ireland in northern Europe, the Netherlands and Belgium as well as most of southern Europe, i.e. Portugal, Spain, Italy and Greece. Nevertheless, following the dismantling of production quotas, isoglucose output may rise in grains surplus regions, which include France, Germany and Poland, Austria and the Czech Republic. In these countries, the relative price between sugar and grains will be an important variable in determining the extent to which there will be substitutability in production between sugar and grains.

Quotas for production of isoglucose are now concentrated in only nine member states, as opposed to 13 member states prior to the 2006 Reform

The EU sugar market post 2017

International Sugar Journal | ISJ's World Sugar Outlook 201520 21www.internationalsugarjournal.com

The EU sugar market post 2017: ISO assessment and forecast

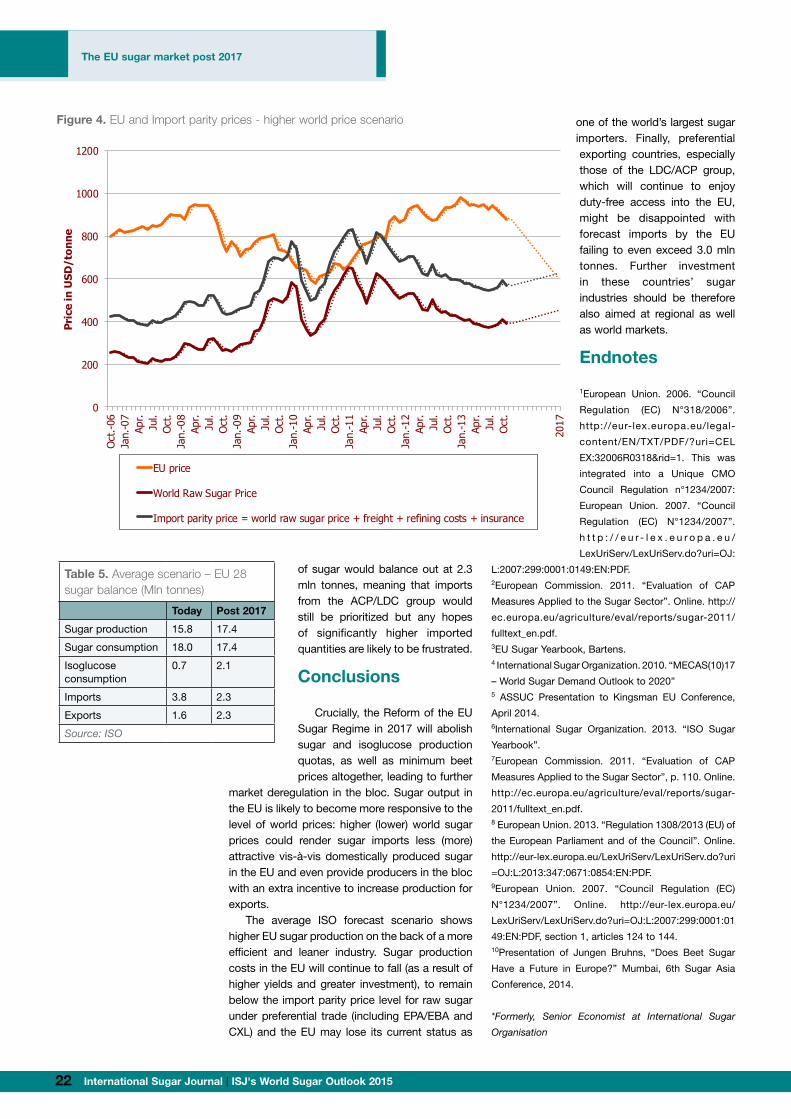

In a recent paper on the EU Sugar Market Post 2017 (MECAS(14)05), the ISO envisaged two scenarios for EU sugar production/consumption and trade in 2017. The first scenario is where sugar prices are relatively high in the EU – at USD 700/tonne for domestic white sugar- but relatively low in the world market – at USD 350/tonne for raw sugar – see fig. 3. In this scenario, EU sugar producers would be unable to avoid a higher penetration of isoglucose in the bloc’s industrial sweeteners consumption and would also fail to expand their presence into a depressed world market. Although this scenario sees the average EU sugar price falling, it will still remain above the threshold level of USD 650/tonne below which sugar starts to be considered as more cost-competitive than isoglucose in a quota-free environment. Production/consumption of isoglucose would rise to 2.7 mln tonnes, compared to 700 thousand tonnes today. Consequently, sugar consumption would fall from 18 mln tonnes to 16.8 mln tonnes.

Crucially, imports of sugar under preferential agreements would remain profitable, with import parity, even with payment of the full CXL duty, still lower than EU prices. Imports are projected to remain as high as 3.0 mln tonnes. Exports to the world market would be around 2.0 mln tonnes – see table 3.

In the second scenario, EU sugar prices would be relatively low at USD 600/tonne, with

world raw sugar prices higher than in the first scenario at USD 450/tonne – see fig. 4. In this scenario, sugar would be able to fend off some of the threat coming from isoglucose production. Here we estimate production/consumption of isoglucose rising to only 1.5 mln tonnes. At the same time, domestically produced sugar would be cheaper than imported sugar under preferential agreements, whether they incur the CXL duty or not. This means that sugar production within the EU would also have an incentive to expand to export, as the EU price would be closer to the world market price. In this scenario, sugar production could expand by as much as 3.2 mln tonnes. Imports from the world market would drop to 1.5 mln tonnes, and exports would be as high as 2.5 mln tonnes – see table 4.The average scenario forecasts a balanced market in the EU, with production and consumption of sugar at 17.4 mln tonnes, and isoglucose production/consumption rising by 1.4 mln tonnes to 2.1 mln tonnes – see table 5. Imports and exports

Table 3. Scenario 1 – EU 28 sugar balance (Mln tonnes)

Today Post 2017

Sugar production 15.8 15.8

Sugar consumption 18.0 16.8

Isoglucose consumption

0.7 2.7

Imports 3.8 3.0

Exports 1.6 2.0

Source: ISO

FO Licht Sugar & Sweeteners Report The EU Sugar Market Post 2017

________________________________________________________________________________ 10

. Source: ISO Table 3: Scenario 1 – EU 28 sugar balance (Mln tonnes) Today Post 2017 Sugar production 15.8 15.8 Sugar consumption 18.0 16.8 Isoglucose consumption 0.7 2.7 Imports

3.8 3.0 Exports 1.6 2.0 Source: ISO In the second scenario, EU sugar prices would be relatively low at USD 600/tonne, with world raw sugar prices higher than in the first scenario at USD 450/tonne – see fig. 4. In this scenario, sugar would be able to fend off some of the threat coming from

isoglucose production. Here we estimate production/consumption of isoglucose rising to only 1.5 mln tonnes. At the same time, domestically produced sugar would be cheaper than imported sugar under preferential agreements, whether they incur the CXL duty or

0

200

400

600

800

1,000

1,200

Oct

.-06

Jan.

-07

Apr.

Jul.

Oct

.Ja

n.-0

8Ap

r.Ju

l.O

ct.

Jan.

-09

Apr.

Jul.

Oct

.Ja

n.-1

0Ap

r.Ju

l.O

ct.

Jan.

-11

Apr.

Jul.

Oct

.Ja

n.-1

2Ap

r.Ju

l.O

ct.

Jan.

-13

Apr.

Jul.

Oct

.

2017

Pric

e in

USD

/ton

ne

Fig. 3: EU and Import Parity Prices - Lower World Price Scenario

EU price

World Raw Sugar Price

Import parity price = world raw sugar price + freight + insurance + refining costs+ CXL duty

Figure 3. EU and import parity prices - lower world price scenario

Table 4. Scenario 2 – EU 28 sugar balance (Mln tonnes)

Today Post 2017

Sugar production 15.8 19.0

Sugar consumption 18.0 18.0

Isoglucose consumption

0.7 1.5

Imports 3.8 1.5

Exports 1.6 2.5

Source: ISO

International Sugar Journal | ISJ's World Sugar Outlook 201522 23www.internationalsugarjournal.com

of sugar would balance out at 2.3 mln tonnes, meaning that imports from the ACP/LDC group would still be prioritized but any hopes of significantly higher imported quantities are likely to be frustrated.

Conclusions

Crucially, the Reform of the EU Sugar Regime in 2017 will abolish sugar and isoglucose production quotas, as well as minimum beet prices altogether, leading to further

market deregulation in the bloc. Sugar output in the EU is likely to become more responsive to the level of world prices: higher (lower) world sugar prices could render sugar imports less (more) attractive vis-à-vis domestically produced sugar in the EU and even provide producers in the bloc with an extra incentive to increase production for exports.

The average ISO forecast scenario shows higher EU sugar production on the back of a more efficient and leaner industry. Sugar production costs in the EU will continue to fall (as a result of higher yields and greater investment), to remain below the import parity price level for raw sugar under preferential trade (including EPA/EBA and CXL) and the EU may lose its current status as

one of the world’s largest sugar importers. Finally, preferential exporting countries, especially those of the LDC/ACP group, which will continue to enjoy duty-free access into the EU, might be disappointed with forecast imports by the EU failing to even exceed 3.0 mln tonnes. Further investment in these countries’ sugar industries should be therefore also aimed at regional as well as world markets.

Endnotes

1European Union. 2006. “Council

Regulation (EC) N°318/2006”.

http://eur-lex.europa.eu/legal-

content/EN/TXT/PDF/?uri=CEL

EX:32006R0318&rid=1. This was

integrated into a Unique CMO

Council Regulation n°1234/2007:

European Union. 2007. “Council

Regulation (EC) N°1234/2007”.

h t t p : / / e u r - l e x . e u r o p a . e u /