world beef report 17 08 2011

DESCRIPTION

weekly Beef ReportTRANSCRIPT

1

WORLD BEEF REPORT

Is a product from Tardáguila Agromercados. The reception of this information is subdued to service subscription. Any reproduc tion whitout citing the source and/or ilegal forwarding

of this material will be prosecuted citing authorial regulations (copyright).

FOB Mercosur

Global turmoil brings caution to the mar-ket Beef export operations from Mercosur im-proved significantly during the past week, with recovering prices in Russia and Chile. But turmoil since Monday in global markets forced demand to take the foot off the accel-erator and assume a more cautious attitude. The rating reduction over the US debt risk note was the final push for global markets to tumble down. Monday was entirely black and volatility reigned on Tuesday though, at the end, with a positive sign as the Dow Jones closed with ups of almost 4%. The Monday drop reached -5.4%. Commodities were no exception to the

general trend. On Monday, the CRB of Reuters-Jefferies fell to an 8-month floor. It

accumulated a 14.3% fall since its high peak in April. Meat industries as well suffered with big drops on share values of the main Brazil-ian meatpacking companies (see more under Brazil). Exporters explained that buyers are posi-tioning in shorter terms this week, buying less volumes but with no apparent thoughts about dropping prices further down. More demand than in the past week Sales to Russia increased last week, mainly from Uruguay, but the regional offer is still too short. In Brazil, despite the now lev-eled prices, demand from the local market remains high which leaves little for exports. The guess is what will happen with exports after a 4% devaluation of the Real this week.

Last week Uruguay Customs registers export requests for 1,411 tons of frozen beef

Global turmoil brings caution into beef export markets Good demand with improved prices in Russia and Chile Regional currency drops produces 8 cent fall in WBR/MSI More interest shown by Brazil for sheepmeat Bulky sales of Brazilian beef to the EU in July Brazil buys 22% more beef with five-fold increase on Australian sales Russia suspends two Paraguayan meatpacking units

Issue: 915/ Date: Wednesday, August 10th , 2011 / Editor: Rafael Tardáguila

Av. Gral Rivera 7111 Montevideo, Uruguay

Tel: (598) 2606 0676 Email: [email protected]

www.tardaguila.com.uy

Follow me

2

WORLD BEEF REPORT

Is a product from Tardáguila Agromercados. The reception of this information is subdued to service subscription. Any reproduc tion whitout citing the source and/or ilegal forwarding

of this material will be prosecuted citing authorial regulations (copyright).

to Russia, while in the prior two weeks it os-cillated around 850t. One operator said of chuck & blade sales at US$/t 4,550, 80 VL trimmings at US$/t 3,450, robbed at US$/t 4,050 and knuckle at US$/t 5,300, FOB in all cases. But exporters report chuck & blade sales at US$/t 4,600 and even US$/t 4,650 and trimmings at US$/t 3,500. ―A jump on trimmings, chuck & blade, robbed forequarters and even some round cuts ma-terialized‖, a Uruguayan exporter said. From Argentina reports say that cow full-sets to Russia now get US$/t 4,400 FOB. Higher quotations in Chile Demand from Chile reaches its seasonal peak to cover the added consumption of September national holidays. As the interest

from buyers faces a short regional supply, prices recovered strongly. Sales from Para-guay got US$/t 6,800 CIF Santiago for 19-cuts and new operations are mentioned at US$/t 7,000-7,200. However, importers han-dled these last prices with extreme caution. ―It’s impossible to transfer these prices to local consumption‖, they assured. Sales of 14-cuts from Argentina and Uruguay are re-ported at US$/t 6,400-6,500. At the same time, higher volumes could be arriving from Australia (―70 to 80 contain-

ers, near 1,500 tons‖ a Chilean source men-tioned), and operations at lower prices for after the national holidays have been agreed. Scant offer keeps chilled prices high EU prices for Argentine chilled beef remain firm, pressed by an extremely reduced offer. Unofficial Hilton permits granted at the begin-ning of the 2011/12 period are being com-pleted and everybody waits for the additional volumes. ―The Secretary of Inner Trade com-promised to distribute 10% of the quota during the first half of August, so it should be avail-able in the next few days‖, an industrialist told WBR. Argentine rump & loin prices in Ger-many remain between US$/t 16,800 and 17,000 FOB. In Argentina, it is considered probable that once the Hilton distribution is

over, prices may correct slightly down, espe-cially if the European economy has no notice-able improvement. From Uruguay, a wide range of prices is reported with a base of US$/t 15,200 to a peak of US$/t 15,800 for rump & loin to Germany. Operations registered in Cus-toms last week averaged US$/t 15,550. Hilton sales from Paraguay are reported at US$/t 14,300 FOB Buenos Aires. Financial troubles in Italy reduced demand for frozen beef strongly. The few operations of side cuts get lower prices week-over-week.

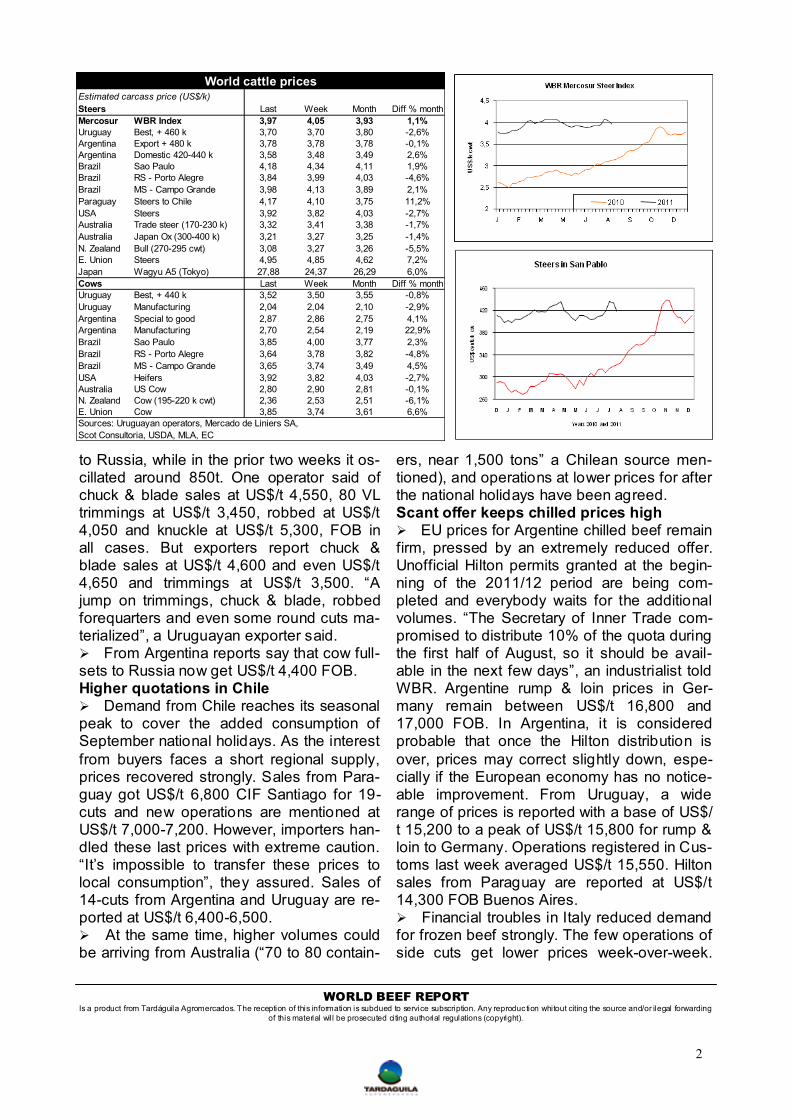

Estimated carcass price (US$/k)

Steers Last Week Month Diff % month

Mercosur WBR Index 3,97 4,05 3,93 1,1%

Uruguay Best, + 460 k 3,70 3,70 3,80 -2,6%

Argentina Export + 480 k 3,78 3,78 3,78 -0,1%

Argentina Domestic 420-440 k 3,58 3,48 3,49 2,6%

Brazil Sao Paulo 4,18 4,34 4,11 1,9%

Brazil RS - Porto Alegre 3,84 3,99 4,03 -4,6%

Brazil MS - Campo Grande 3,98 4,13 3,89 2,1%

Paraguay Steers to Chile 4,17 4,10 3,75 11,2%

USA Steers 3,92 3,82 4,03 -2,7%

Australia Trade steer (170-230 k) 3,32 3,41 3,38 -1,7%

Australia Japan Ox (300-400 k) 3,21 3,27 3,25 -1,4%

N. Zealand Bull (270-295 cwt) 3,08 3,27 3,26 -5,5%

E. Union Steers 4,95 4,85 4,62 7,2%

Japan Wagyu A5 (Tokyo) 27,88 24,37 26,29 6,0%

Cows Last Week Month Diff % month

Uruguay Best, + 440 k 3,52 3,50 3,55 -0,8%

Uruguay Manufacturing 2,04 2,04 2,10 -2,9%

Argentina Special to good 2,87 2,86 2,75 4,1%

Argentina Manufacturing 2,70 2,54 2,19 22,9%

Brazil Sao Paulo 3,85 4,00 3,77 2,3%

Brazil RS - Porto Alegre 3,64 3,78 3,82 -4,8%

Brazil MS - Campo Grande 3,65 3,74 3,49 4,5%

USA Heifers 3,92 3,82 4,03 -2,7%

Australia US Cow 2,80 2,90 2,81 -0,1%

N. Zealand Cow (195-220 k cwt) 2,36 2,53 2,51 -6,1%

E. Union Cow 3,85 3,74 3,61 6,6%

Sources: Uruguayan operators, Mercado de Liniers SA,

Scot Consultoria, USDA, MLA, EC

World cattle prices

3

WORLD BEEF REPORT

Is a product from Tardáguila Agromercados. The reception of this information is subdued to service subscription. Any reproduc tion whitout citing the source and/or ilegal forwarding

of this material will be prosecuted citing authorial regulations (copyright).

Values mentioned in Brazil were US$/t 7,700 and from Uruguay US$/t 7,300. Fluent operations to Israel Shipments to Israel are still good busi-ness for exporters. The usual price in sales from Uruguay is US$/t 6,400 FOB for the nesher rite. Some more interest for sheepmeat in Brazil Sheepmeat stocks in Brazil (high since the early year) fell and buyers are again showing interest on imports. ―There’s people buying for the year’s end‖, Fabrizio Azevedo of M. Foods, told WBR. He said that buyers from Marfrig and JBS travelled last week to Uruguay to close operations with offers be-tween US$/t 7,000 and 7,200 for shoulders

and US$/t 7,500 for legs. He considered that at these values, lamb prices should rise from the current R$/kg 16.5-17 (US$/kg 10.5) to R$/kg 19 (US$/kg 11.8). Strengthened US$ causes strong drop of WBR Mercosur Steer Index A strong revaluation of the US dollar caused an 8 cent drop in the WBR Mercosur Steer Index this week to situate in US$/kg 3.97 cw. In just two weeks the index lost US$ 0.11 (-2.6%). Prices of cattle in Brazil stabilized in Reales, so that devaluation of this currency was entirely transferred to ref-erences in US$. The Uruguayan Peso and the Paraguayan Guaraní also devaluated. In Paraguay, however, cattle prices remain very firm favored by a peak of demand from Chile and a very short offer. Steer prices in Paraguay are now the highest in the region, around US$/kg 4.30 cw for EU eligible ani-mals. FAO beef market projections

Higher prices for beef expected According to the last report from UN’s

Food & Agriculture Organization (FAO), a short supply will push beef prices into new records in the short term. The price index reached in May a new all-time record of 183 points. The report adds that international prices for all kinds of meats remained firm since January. The strengthening of values results from a short offer generated by ad-

verse weather conditions in late 2010, the re-building of stocks, animal diseases and higher component costs, which carried to a weaker growth on global beef production. In a 12-month perspective, both ovine and bovine meat registered strong increments on their price indexes which climbed 38% and 20% respectively since May 2010. Lower export stocks in producing countries, combined with a strong import demand, should keep meat prices climbing in the short term. At the same time, high grain values will continue limiting gains in the sector. Uruguay

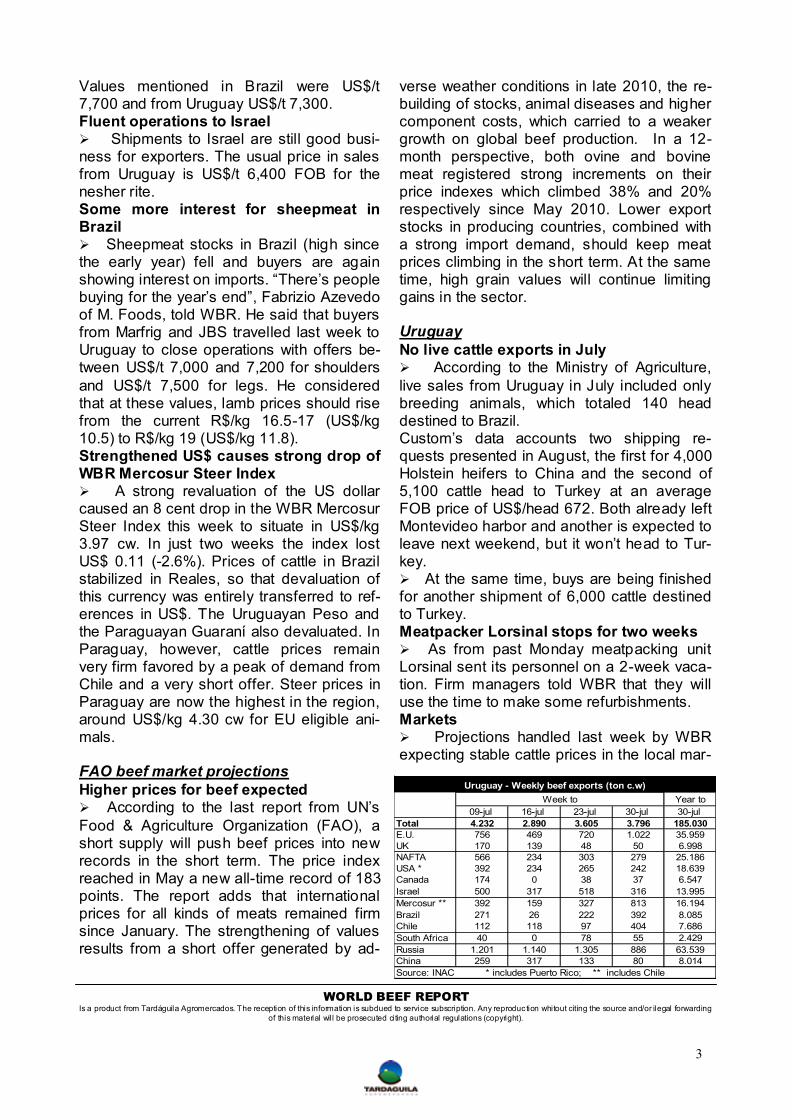

No live cattle exports in July According to the Ministry of Agriculture,

live sales from Uruguay in July included only breeding animals, which totaled 140 head destined to Brazil. Custom’s data accounts two shipping re-quests presented in August, the first for 4,000 Holstein heifers to China and the second of 5,100 cattle head to Turkey at an average FOB price of US$/head 672. Both already left Montevideo harbor and another is expected to leave next weekend, but it won’t head to Tur-key. At the same time, buys are being finished for another shipment of 6,000 cattle destined to Turkey. Meatpacker Lorsinal stops for two weeks As from past Monday meatpacking unit Lorsinal sent its personnel on a 2-week vaca-tion. Firm managers told WBR that they will use the time to make some refurbishments. Markets Projections handled last week by WBR expecting stable cattle prices in the local mar-

Year to

09-jul 16-jul 23-jul 30-jul 30-jul

Total 4.232 2.890 3.605 3.796 185.030

E.U. 756 469 720 1.022 35.959

UK 170 139 48 50 6.998

NAFTA 566 234 303 279 25.186

USA * 392 234 265 242 18.639

Canada 174 0 38 37 6.547

Israel 500 317 518 316 13.995

Mercosur ** 392 159 327 813 16.194

Brazil 271 26 222 392 8.085

Chile 112 118 97 404 7.686

South Africa 40 0 78 55 2.429

Russia 1.201 1.140 1.305 886 63.539

China 259 317 133 80 8.014

Source: INAC * includes Puerto Rico; ** includes Chile

Uruguay - Weekly beef exports (ton c.w)

Week to

4

WORLD BEEF REPORT

Is a product from Tardáguila Agromercados. The reception of this information is subdued to service subscription. Any reproduc tion whitout citing the source and/or ilegal forwarding

of this material will be prosecuted citing authorial regulations (copyright).

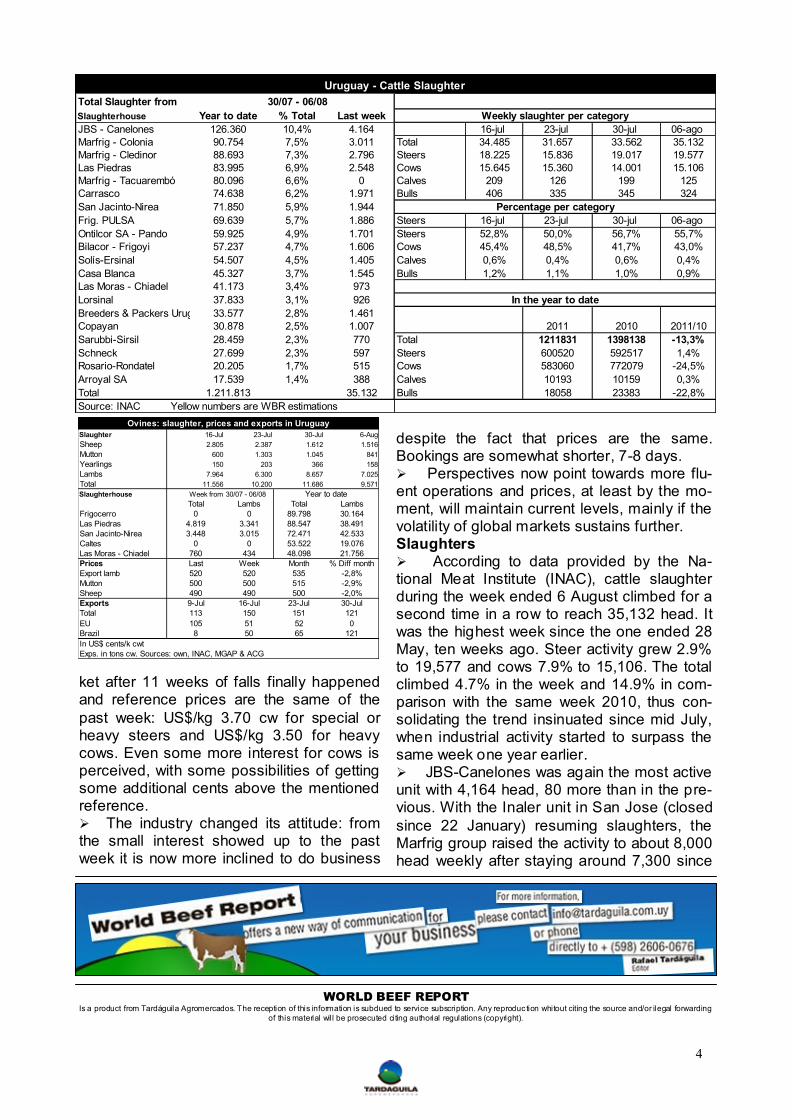

ket after 11 weeks of falls finally happened and reference prices are the same of the

past week: US$/kg 3.70 cw for special or heavy steers and US$/kg 3.50 for heavy cows. Even some more interest for cows is perceived, with some possibilities of getting some additional cents above the mentioned reference. The industry changed its attitude: from the small interest showed up to the past week it is now more inclined to do business

despite the fact that prices are the same. Bookings are somewhat shorter, 7-8 days. Perspectives now point towards more flu-ent operations and prices, at least by the mo-ment, will maintain current levels, mainly if the volatility of global markets sustains further. Slaughters According to data provided by the Na-tional Meat Institute (INAC), cattle slaughter during the week ended 6 August climbed for a second time in a row to reach 35,132 head. It was the highest week since the one ended 28 May, ten weeks ago. Steer activity grew 2.9% to 19,577 and cows 7.9% to 15,106. The total climbed 4.7% in the week and 14.9% in com-parison with the same week 2010, thus con-solidating the trend insinuated since mid July, when industrial activity started to surpass the same week one year earlier. JBS-Canelones was again the most active unit with 4,164 head, 80 more than in the pre-vious. With the Inaler unit in San Jose (closed

since 22 January) resuming slaughters, the Marfrig group raised the activity to about 8,000 head weekly after staying around 7,300 since

Total Slaughter from 30/07 - 06/08

Slaughterhouse Year to date % Total Last week

JBS - Canelones 126.360 10,4% 4.164 16-jul 23-jul 30-jul 06-ago

Marfrig - Colonia 90.754 7,5% 3.011 Total 34.485 31.657 33.562 35.132

Marfrig - Cledinor 88.693 7,3% 2.796 Steers 18.225 15.836 19.017 19.577

Las Piedras 83.995 6,9% 2.548 Cows 15.645 15.360 14.001 15.106

Marfrig - Tacuarembó 80.096 6,6% 0 Calves 209 126 199 125

Carrasco 74.638 6,2% 1.971 Bulls 406 335 345 324

San Jacinto-Nirea 71.850 5,9% 1.944

Frig. PULSA 69.639 5,7% 1.886 Steers 16-jul 23-jul 30-jul 06-ago

Ontilcor SA - Pando 59.925 4,9% 1.701 Steers 52,8% 50,0% 56,7% 55,7%

Bilacor - Frigoyi 57.237 4,7% 1.606 Cows 45,4% 48,5% 41,7% 43,0%

Solís-Ersinal 54.507 4,5% 1.405 Calves 0,6% 0,4% 0,6% 0,4%

Casa Blanca 45.327 3,7% 1.545 Bulls 1,2% 1,1% 1,0% 0,9%

Las Moras - Chiadel 41.173 3,4% 973

Lorsinal 37.833 3,1% 926

Breeders & Packers Uruguay 33.577 2,8% 1.461

Copayan 30.878 2,5% 1.007 2011 2010 2011/10

Sarubbi-Sirsil 28.459 2,3% 770 1211831 1398138 -13,3%

Schneck 27.699 2,3% 597 600520 592517 1,4%

Rosario-Rondatel 20.205 1,7% 515 583060 772079 -24,5%

Arroyal SA 17.539 1,4% 388 10193 10159 0,3%

Total 1.211.813 35.132 18058 23383 -22,8%

Source: INAC Yellow numbers are WBR estimations

Bulls

Cows

Steers

Calves

Total

Percentage per category

Uruguay - Cattle Slaughter

In the year to date

Weekly slaughter per category

Slaughter 16-Jul 23-Jul 30-Jul 6-Aug

Sheep 2.805 2.387 1.612 1.516

Mutton 600 1.303 1.045 841

Yearlings 150 203 366 158

Lambs 7.964 6.300 8.657 7.025

Total 11.556 10.200 11.686 9.571

Slaughterhouse Week from 30/07 - 06/08

Total Lambs Total Lambs

Frigocerro 0 0 89.798 30.164

Las Piedras 4.819 3.341 88.547 38.491

San Jacinto-Nirea 3.448 3.015 72.471 42.533

Caltes 0 0 53.522 19.076

Las Moras - Chiadel 760 434 48.098 21.756

Prices Last Week Month % Diff month

Export lamb 520 520 535 -2,8%

Mutton 500 500 515 -2,9%

Sheep 490 490 500 -2,0%

Exports 9-Jul 16-Jul 23-Jul 30-Jul

Total 113 150 151 121

EU 105 51 52 0

Brazil 8 50 65 121

In US$ cents/k cwt

Exps. in tons cw. Sources: own, INAC, MGAP & ACG

Ovines: slaughter, prices and exports in Uruguay

Year to date

5

WORLD BEEF REPORT

Is a product from Tardáguila Agromercados. The reception of this information is subdued to service subscription. Any reproduc tion whitout citing the source and/or ilegal forwarding

of this material will be prosecuted citing authorial regulations (copyright).

the third week of June. Some other units also increased their slaughter schedules; that was the case of Las Piedras, Ontilcor, San Jacinto and Bilacor. On the other hand, ovine slaughter dropped to 9,571 head, 18.1% below the previous and 53% below the same week 2010. Frigocerro, the most active unit with this species in the year, is still closed. 73% of the weekly slaughter were lambs. Brazil

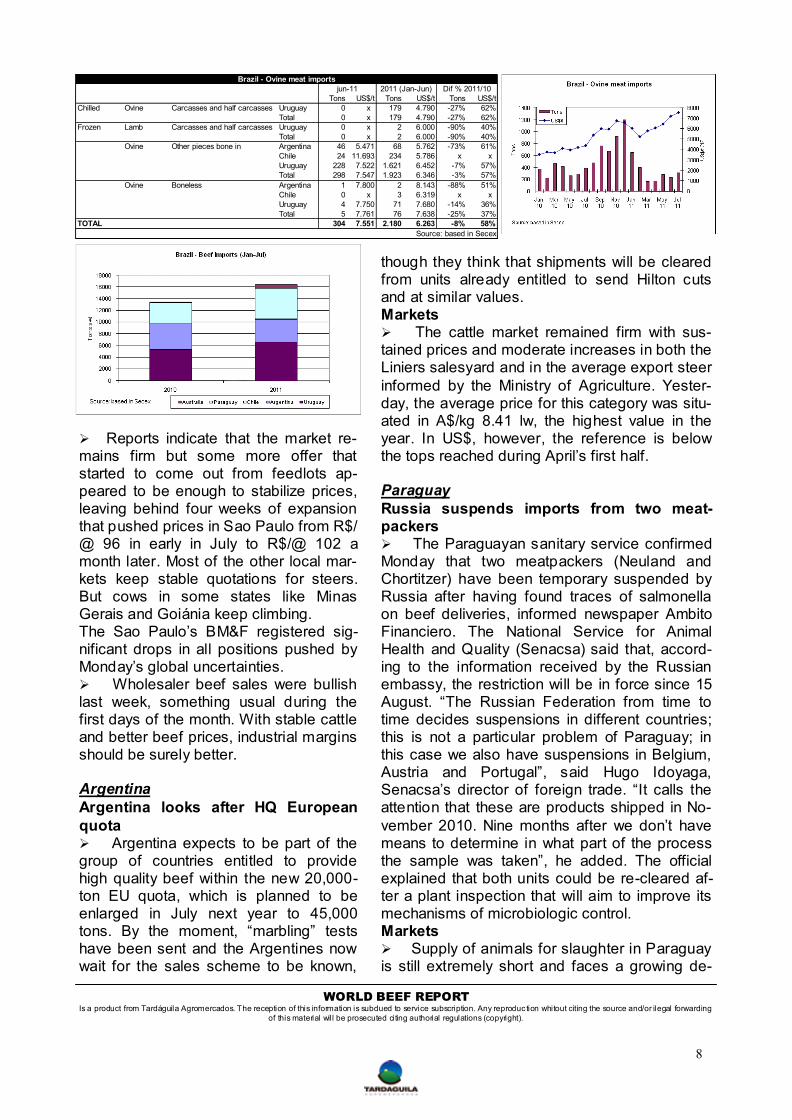

Beef exports to the EU at tops since October In July Brazil exported 4,146 tons of fresh beef to countries in the European Union, the highest monthly volume since

past October. Frozen beef sales to Ger-many totaled 334 tons, more than doubling those of June (154t), which were at that time the highest in the year to that country. The trade current more than trebled in the year to date. The main EU destinations for frozen beef were Italy and the Netherlands, both increasing their purchases in July and above the same period 2010. In total the EU bought 13,533 tons of Brazilian frozen beef in the year to date, 13% above year-on-year. Brazilian market operators told WBR that the situation was punctual and that offer dropped in the past two weeks. ―Due to the drought, there were more EU eligible animals, that’s why July shipments were so good‖, it was commented from Sao Paulo. On the contrary, all other destinations of this product - with the exception of Venezuela – reduced purchases in the year. July sales to Russia fell to 18,007 tons, the lowest volume since January; in

the year, Russia bought 4% less than in 2010. Other main destinations (Iran, Egypt and Hong Kong) reduced their demand around 30% in the year to date, while Venezuela climbed 34%. Month after month, processed beef sales to the US grow to total 1,158 tons in July, 45% above June and the highest vol-ume since the May 2010 suspension. Bra-

zil usually exported around 3,000 tons monthly of processed beef to the US. Beef imports grow 22% During the first seven months of the year Brazil imported 16,427 tons of beef, 21.8% above the 13,488 tons of the same period 2010. The main provider is Uruguay with 6,571t in the year, up 21.7% year-on-year. Sales from Paraguay also grow (+48% to 5,227 tons) and mainly from Australia. Although volumes are relatively small, it reached 648 tons in the year, 442% above Jan-Jul 2010. Mainly rump cap arrive from Australia. ―Though frozen, it’s a very good product that is gaining market over the imported from Uruguay‖, as it comes to butch-ers at R$/kg 31-32 (US$/kg 19-20) while the Uruguayan costs R$/kg 34-38 (US$/kg 21-

23.5), it was said in Brazil. On the contrary, sales from Argentina fell 10.6% to 3,977 tons. In July, Brazil imported 2,506 tons of beef, be-low the near 3,000 tons of May and June. The average CIF price in July was US$/t 8,361, 6.9% above June and 26.2% above July 2010. Ovine meat imports at lower levels Brazil imported 305 tons of ovine meat in July. Although being the biggest volume since February, it still is a very low level. The contrac-tion reaches 20% compared with July 2010. 76% of the imported sheepmeat came from Uruguay, followed by Argentina and Chile. At least by the moment there’s no Australian meat arriving in the market. The average CIF price was US$/t 7,551, 4.9% above June and 72% above July 2010. In the year to June imports totaled 2,180 tons, 8% below 2010 with a CIF average price

6

WORLD BEEF REPORT

Is a product from Tardáguila Agromercados. The reception of this information is subdued to service subscription. Any reproduc tion whitout citing the source and/or ilegal forwarding

of this material will be prosecuted citing authorial regulations (copyright).

climbing 58% to US$/t 6,263. Ukraine clears four slaughterhouses Ukraine cleared four new slaughterhouses for beef exports, announced yesterday the Bra-zilian Meatpackers’ Association (Abrafrigo). These are Tatuibi and Barra Mansa in Sao Paulo, Mafripar in Pará and Frigon in Rondônia. In 2010 Ukraine imported 10,300 tons of Brazil-ian beef valued in US$ 38.3 million. Russian official denies ban over Brazil According to the director of the Russian Sanitary and Phito-sanitary Control Service (Rosselkhoznadzor), Sergei Dankvert, his coun-try has not decided bans over Brazilian meat-packing units and is just applying ―temporary restrictions‖ to exports from some units, as more than half of the 249 Brazilian plants have no dif-

ficulties to sell meat to Russia. ―Currently, 116 Brazilian units are regularly selling meat to Rus-sia. Brazil, as the main supplier of these prod-ucts, provides 53% of Russian imports. There-fore, before complaining for the embargo, they should know that we, Russians, are demanding more surveillance over the conservation of these products in order to avoid the risk of transmissible diseases. For us, food products have to be 100% safe‖, Dankvert affirmed. Brazilian government criticized by meat ex-porters Main meat exporters in Brazil disapproved the government’s conduct in the negotiations aimed to lift the Russian embargo to 85 meat industrial units in three states (Mato Grosso, Paraná and Rio Grande do Sul) since 15 June, said Valor Economico. The poultry industry says the government needs to show ―a firm pulse‖ in the negotiations. The Executive Manager of the Brazilian Poultry Union, Francisco Turra, said the Russian market represents 10% of the total exported in 2010. ―The market could be dam-aged if the delays persist‖, he warned. Mean-while, the pork meat segment is even more wor-

ried as Russia is the main destination of its sales abroad. ―When the Brazilian delegation went to Russia they said that by July everything was to be resolved. We trusted for everything to be liberated by that date but we are still waiting‖, said the president of the Brazilian Swine Meat Producers’ and Exporters’ Association, Pedro Camargo Neto.

Tons US$/t Tons US$/t Tons US$/t

Fresh 4.146 9.806 22.076 9.782 -5% 28%

Chilled 1.302 11.326 8.543 11.976 -24% 38%

Netherlands 527 11.979 2.864 12.433 -31% 41%

Germany 347 11.010 2.223 11.845 23% 34%

Italy 87 11.240 927 11.772 -60% 38%

Sweden 81 12.187 828 13.104 8% 26%

Spain 128 8.962 767 9.551 -27% 33%

UK 46 11.073 326 11.522 36% 30%

Finland 46 13.522 321 14.447 -6% 24%

Portugal 23 8.710 175 9.349 -42% 37%

Denmark 10 9.600 56 13.032 13% 20%

France 6 10.350 55 9.345 -77% 42%

Frozen 2.845 9.110 13.533 8.397 13% 27%

Italy 1.338 8.164 7.506 8.163 5% 12%

Netherlands 778 9.789 3.274 8.653 41% 36%

Germany 334 11.202 981 9.219 265% 43%

Spain 199 9.112 515 9.718 14% 106%

UK 50 8.901 502 8.125 -42% 92%

Portugal 74 10.289 230 11.272 73% 78%

France 37 5.883 184 5.463 -14% 46%

Lithuania 0 x 125 3.980 x x

Sweden 23 14105 106 10408 187% 5%

Greece 0 x 87 5608 -63% 36%

Belgium 13 6600 13 6600 -85% 2%

Finland 0 x 10,885 13000 x x

Processed 3.087 6.029 32.542 5.823 -25% 41%

UK 1.745 5.611 18.892 5.309 -25% 48%

Netherlands 507 5.894 6.946 5.483 48% 32%

Italy 167 10.100 3.007 9.783 -29% 36%

France 193 5.588 1.162 5.088 -17% 21%

Sweden 112 6.545 803 6.730 -47% 78%

Belgium 253 6.504 630 6.553 -79% 65%

Germany 16 4.477 392 5.227 -82% 11%

Ireland 78 6.923 333 6.226 2% 8%

Malta 0 x 231 5296 -42% 69%

Finland 0 x 72 7.263 -59% 81%

Spain 17 4.779 51 5.127 -68% 56%

Monaco 0 x 22 4700 x x

Diff. % 11/10

Source: based in SECEX

Brasil - Beef exports to the EU

jul-11 2011 Jan-jul

7

WORLD BEEF REPORT

Is a product from Tardáguila Agromercados. The reception of this information is subdued to service subscription. Any reproduc tion whitout citing the source and/or ilegal forwarding

of this material will be prosecuted citing authorial regulations (copyright).

Strong fall of live cattle exports Brazilian live cattle exports fell strongly in July. According to data from the Ministry of De-velopment, Industry and Foreign Trade, 16,000 head were shipped, the lowest monthly number since 2006. The volume was 78% below the past year, while income dropped 50% to US$ 20.18 million. Out of that total, 14,100 animals were sold to Venezuela (87.5%) and the other 1,900 to Lebanon. The average price for these sales was US$/head 1,250. During the first seven months 2011, Brazil sold 206,000 cattle head against 365,000 in the same period last year. Global crisis seriously affect meatpackers’ shares Shares of the main Brazilian meatpacking

companies fell strongly early in the week as a result from global financial turbulences. Marfrig headed the trend Monday with a 25.7% drop. Minerva contracted 6.6% and JBS 4.9%. Prices upped yesterday first, but in Marfrigs case it fin-ished down again nearly 5%. Osvaldo Torres, professor of finance in the BBS Business School, told newspaper Tribuna do Norte some of the reasons why Marfrig could have been one of the most damaged by the trust crisis. He remembered that the company made important purchases in the past years, like Keystone and O’Kane. Besides, part of its debt is in foreign currency, which leaves the group more exposed to ―the humor of inves-tors‖. Eduardo Miziara of share fund Capitânia, added that a good part of what happened with company shares is related to moves made by the GWI Bank – a Marfrig partner – owned by Korean Mu Hak You. Miziara said this bank had bought 5.22% of the company shares and on Monday went out to the market to sell them. The move exacerbated the fall of share prices. An additional fact is that Marfrig shares’ be-

havior in the year was much better than its competitors JBS and Minerva. With this week’s falls, the shares of the two giants (Marfrig and JBS) dropped nearly 50% in the year to date. Markets The financial turbulence reduced strongly the Real quotation. It was yesterday quoting at R$/US$ 1.63, 4% below in the week. Price ref-erences in US$ fell due to this contraction.

Tons US$/t Tons US$/t Tons US$/t

Fresh 62.767 5.038 469.835 4.987 -20% 30%

Chilled 6.318 6.752 40.341 7.026 -13% 22%

Chile 1.696 5.219 9.348 5.497 39% 26%

Lebanon 1.280 5.966 8.206 6.109 -33% 20%

Saudi Arabia 637 5.875 5.206 5.674 -6% 25%

Algeria 533 5.175 3.062 5.185 176% 17%

Netherlands 527 11.979 2.864 12.433 -31% 41%

Jordan 453 5.043 2.712 5.006 -25% 21%

Germany 347 11.010 2.223 11.845 23% 34%

Un. Arab Emirates 281 5.772 1.937 6.173 -27% 23%

Italy 87 11.240 927 11.772 -60% 38%

Sweden 81 12.187 828 13.104 8% 26%

Spain 128 8.962 767 9.551 -27% 33%

UK 46 11.073 326 11.522 36% 30%

Frozen 56.449 4.846 429.494 4.796 -21% 31%

Russia 18.007 4.422 160.738 4.468 -4% 34%

Iran 9.636 5.246 85.457 5.265 -27% 33%

Egypt 9.331 4.267 43.196 4.262 -36% 20%

Hong Kong 5.130 4.230 33.907 4.166 -33% 21%

Venezuela 3.026 4.927 29.587 5.235 34% 17%

Saudi Arabia 947 4.811 13.269 4.636 -9% 26%

Israel 1.192 5.400 12.494 5.005 -32% 22%

Italy 1.338 8.164 7.506 8.163 5% 12%

Philippines 851 3.190 5.041 3.383 -41% 26%

Libia 400 4.442 3.719 4.130 -62% 26%

Singapure 327 4.714 3.657 4.932 37% 23%

Angola 345 4.845 3.611 4.685 -13% 27%

Netherlands 778 9.789 3.274 8.653 41% 36%

Un. Arab Emirates 332 7.933 2.831 6.657 -4% 29%

Irak 325 4.972 2.553 4.144 20% 22%

Kuwait 337 4.715 2.114 4.713 -9% 22%

Ukraine 541 4.251 2.007 4.398 -5% 70%

Offal 6.952 2.646 56.525 2.626 20% 13%

Hong Kong 4.704 3.021 40.312 2.942 32% 8%

Peru 531 2.003 3.833 1.763 -8% 39%

Ivory Coast 420 906 2.464 868 -15% 7%

Egypt 374 1.707 2.315 1.574 14% 44%

Gabon 83 1.129 956 1.002 77% 10%

Ukraine 163 3.794 944 3.442 11% 23%

Congo 103 1.013 697 964 806% 56%

Jerked 570 6.403 2.428 6.118 126% 31%

Angola 570 6.403 2.423 6.113 126% 31%

Bolivia 0 - 5 7.160 - -

Tripes, etc 5.992 3.906 38.770 3.777 4% 11%

Hong Kong 3.760 3.318 26.318 3.265 7% 12%

Russia 1.088 5.090 4.645 5.136 -11% 10%

Ukraine 314 5.035 1.587 4.962 -38% 9%

Italy 179 4.652 1.222 4.290 23% 24%

Lebanon 156 3.891 901 3.984 635% -11%

Spain 87 4.410 825 3.994 17% 21%

Processed 7.351 6.377 59.283 5.719 -28% 41%

UK 1.745 5.611 18.892 5.309 -25% 48%

Netherlands 507 5.894 6.946 5.483 48% 32%

USA 1.158 13.673 4.137 14.358 -69% 154%

Italy 167 10.100 3.007 9.783 -29% 36%

Jamaica 168 3.839 2.710 4.008 59% 26%

Japan 214 5.166 2.042 5.314 -2% 51%

Egypt 683 4.643 1.971 4.610 -11% 42%

Jordan 156 3.563 1.668 2.920 104% 9%

Canada 102 4.758 1.475 4.798 -34% 39%

France 193 5.588 1.162 5.088 -17% 21%

Angola 18 2.789 998 3.809 1052% 55%

Sweden 112 6.545 803 6.730 -47% 78%

TOTAL 83.633 4.885 626.842 4.773 -17% 28%

Brazil - Beef and by-products exports

jul-11 2011 (Jan-jul) Dif 11/10

Source: based in SECEX

8

WORLD BEEF REPORT

Is a product from Tardáguila Agromercados. The reception of this information is subdued to service subscription. Any reproduc tion whitout citing the source and/or ilegal forwarding

of this material will be prosecuted citing authorial regulations (copyright).

Reports indicate that the market re-mains firm but some more offer that started to come out from feedlots ap-peared to be enough to stabilize prices, leaving behind four weeks of expansion that pushed prices in Sao Paulo from R$/@ 96 in early in July to R$/@ 102 a month later. Most of the other local mar-kets keep stable quotations for steers. But cows in some states like Minas Gerais and Goiánia keep climbing. The Sao Paulo’s BM&F registered sig-nificant drops in all positions pushed by Monday’s global uncertainties. Wholesaler beef sales were bullish last week, something usual during the first days of the month. With stable cattle and better beef prices, industrial margins should be surely better. Argentina

Argentina looks after HQ European

quota Argentina expects to be part of the group of countries entitled to provide high quality beef within the new 20,000-ton EU quota, which is planned to be enlarged in July next year to 45,000 tons. By the moment, ―marbling‖ tests have been sent and the Argentines now wait for the sales scheme to be known,

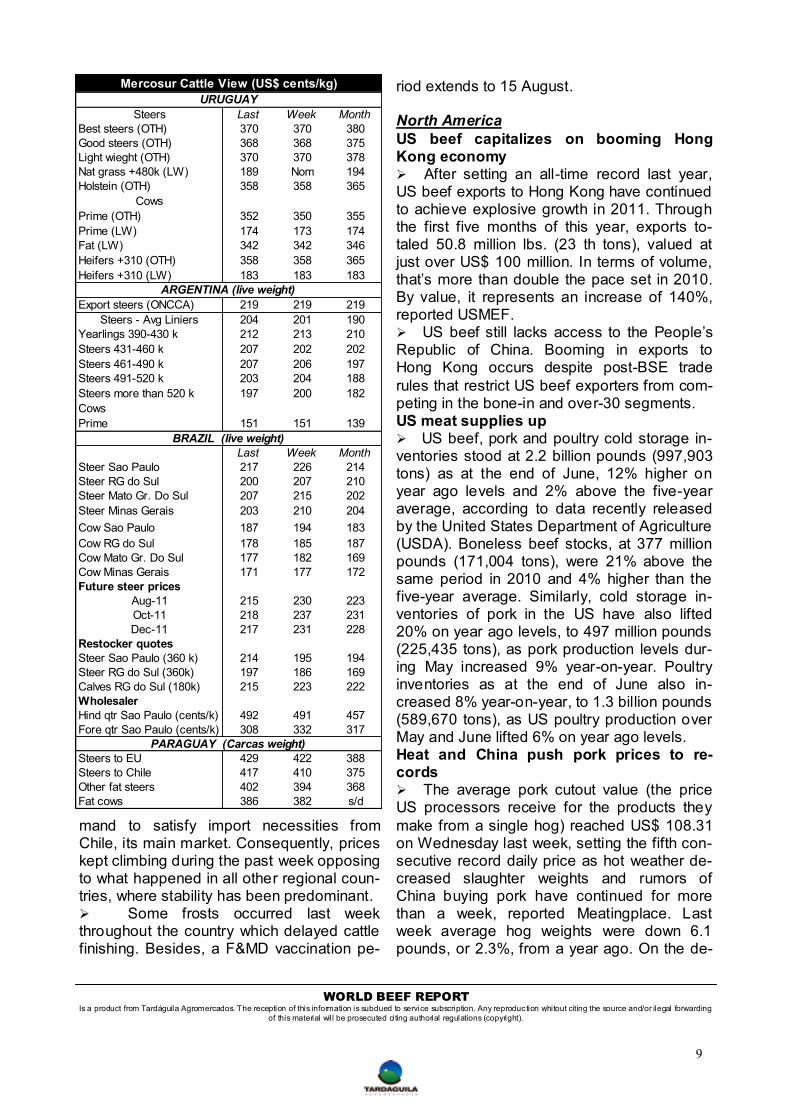

though they think that shipments will be cleared from units already entitled to send Hilton cuts and at similar values. Markets The cattle market remained firm with sus-tained prices and moderate increases in both the Liniers salesyard and in the average export steer

informed by the Ministry of Agriculture. Yester-day, the average price for this category was situ-ated in A$/kg 8.41 lw, the highest value in the year. In US$, however, the reference is below the tops reached during April’s first half. Paraguay

Russia suspends imports from two meat-packers The Paraguayan sanitary service confirmed Monday that two meatpackers (Neuland and Chortitzer) have been temporary suspended by Russia after having found traces of salmonella on beef deliveries, informed newspaper Ambito Financiero. The National Service for Animal Health and Quality (Senacsa) said that, accord-ing to the information received by the Russian embassy, the restriction will be in force since 15 August. ―The Russian Federation from time to time decides suspensions in different countries; this is not a particular problem of Paraguay; in this case we also have suspensions in Belgium, Austria and Portugal‖, said Hugo Idoyaga, Senacsa’s director of foreign trade. ―It calls the attention that these are products shipped in No-

vember 2010. Nine months after we don’t have means to determine in what part of the process the sample was taken‖, he added. The official explained that both units could be re-cleared af-ter a plant inspection that will aim to improve its mechanisms of microbiologic control. Markets Supply of animals for slaughter in Paraguay is still extremely short and faces a growing de-

Tons US$/t Tons US$/t Tons US$/t

Chilled Ovine Carcasses and half carcasses Uruguay 0 x 179 4.790 -27% 62%

Total 0 x 179 4.790 -27% 62%

Frozen Lamb Carcasses and half carcasses Uruguay 0 x 2 6.000 -90% 40%

Total 0 x 2 6.000 -90% 40%

Ovine Other pieces bone in Argentina 46 5.471 68 5.762 -73% 61%

Chile 24 11.693 234 5.786 x x

Uruguay 228 7.522 1.621 6.452 -7% 57%

Total 298 7.547 1.923 6.346 -3% 57%

Ovine Boneless Argentina 1 7.800 2 8.143 -88% 51%

Chile 0 x 3 6.319 x x

Uruguay 4 7.750 71 7.680 -14% 36%

Total 5 7.761 76 7.638 -25% 37%

TOTAL 304 7.551 2.180 6.263 -8% 58%

Source: based in Secex

Brazil - Ovine meat imports

jun-11 2011 (Jan-Jun) Dif % 2011/10

9

WORLD BEEF REPORT

Is a product from Tardáguila Agromercados. The reception of this information is subdued to service subscription. Any reproduc tion whitout citing the source and/or ilegal forwarding

of this material will be prosecuted citing authorial regulations (copyright).

mand to satisfy import necessities from Chile, its main market. Consequently, prices kept climbing during the past week opposing to what happened in all other regional coun-tries, where stability has been predominant. Some frosts occurred last week throughout the country which delayed cattle finishing. Besides, a F&MD vaccination pe-

riod extends to 15 August. North America

US beef capitalizes on booming Hong Kong economy After setting an all-time record last year, US beef exports to Hong Kong have continued to achieve explosive growth in 2011. Through the first five months of this year, exports to-taled 50.8 million lbs. (23 th tons), valued at just over US$ 100 million. In terms of volume, that’s more than double the pace set in 2010. By value, it represents an increase of 140%, reported USMEF. US beef still lacks access to the People’s Republic of China. Booming in exports to Hong Kong occurs despite post-BSE trade

rules that restrict US beef exporters from com-peting in the bone-in and over-30 segments. US meat supplies up US beef, pork and poultry cold storage in-ventories stood at 2.2 billion pounds (997,903 tons) as at the end of June, 12% higher on year ago levels and 2% above the five-year average, according to data recently released by the United States Department of Agriculture (USDA). Boneless beef stocks, at 377 million pounds (171,004 tons), were 21% above the same period in 2010 and 4% higher than the five-year average. Similarly, cold storage in-ventories of pork in the US have also lifted 20% on year ago levels, to 497 million pounds (225,435 tons), as pork production levels dur-ing May increased 9% year-on-year. Poultry inventories as at the end of June also in-creased 8% year-on-year, to 1.3 billion pounds (589,670 tons), as US poultry production over May and June lifted 6% on year ago levels. Heat and China push pork prices to re-cords The average pork cutout value (the price US processors receive for the products they

make from a single hog) reached US$ 108.31 on Wednesday last week, setting the fifth con-secutive record daily price as hot weather de-creased slaughter weights and rumors of China buying pork have continued for more than a week, reported Meatingplace. Last week average hog weights were down 6.1 pounds, or 2.3%, from a year ago. On the de-

Steers Last Week Month

Best steers (OTH) 370 370 380

Good steers (OTH) 368 368 375

Light wieght (OTH) 370 370 378

Nat grass +480k (LW) 189 Nom 194

Holstein (OTH) 358 358 365

Cows

Prime (OTH) 352 350 355

Prime (LW) 174 173 174

Fat (LW) 342 342 346

Heifers +310 (OTH) 358 358 365

Heifers +310 (LW) 183 183 183

Export steers (ONCCA) 219 219 219

Steers - Avg Liniers 204 201 190

Yearlings 390-430 k 212 213 210

Steers 431-460 k 207 202 202

Steers 461-490 k 207 206 197

Steers 491-520 k 203 204 188

Steers more than 520 k 197 200 182

Cows

Prime 151 151 139

Last Week Month

Steer Sao Paulo 217 226 214

Steer RG do Sul 200 207 210

Steer Mato Gr. Do Sul 207 215 202

Steer Minas Gerais 203 210 204

Cow Sao Paulo 187 194 183

Cow RG do Sul 178 185 187

Cow Mato Gr. Do Sul 177 182 169

Cow Minas Gerais 171 177 172

Future steer prices

Aug-11 215 230 223

Oct-11 218 237 231

Dec-11 217 231 228

Restocker quotes

Steer Sao Paulo (360 k) 214 195 194

Steer RG do Sul (360k) 197 186 169

Calves RG do Sul (180k) 215 223 222

Wholesaler

Hind qtr Sao Paulo (cents/k) 492 491 457

Fore qtr Sao Paulo (cents/k) 308 332 317

Steers to EU 429 422 388

Steers to Chile 417 410 375

Other fat steers 402 394 368

Fat cows 386 382 s/d

URUGUAY

ARGENTINA (live weight)

Mercosur Cattle View (US$ cents/kg)

BRAZIL (live weight)

PARAGUAY (Carcas weight)

10

WORLD BEEF REPORT

Is a product from Tardáguila Agromercados. The reception of this information is subdued to service subscription. Any reproduc tion whitout citing the source and/or ilegal forwarding

of this material will be prosecuted citing authorial regulations (copyright).

mand side, rumors persist about China — where high pork prices are leading inflation — coming into the US market for pork. Tyson expects improved scenario in 2012 Tyson Foods Inc. (TSN) said Monday in an earnings report that it expects improving conditions for both its pork and beef busi-

nesses in 2012 as demand world-wide out-strips supplies. In the beef sector, the company said that it should see a gradual reduction in fed cat-tle supplies of one to two per cent in fiscal 2012 in the US as well as exports to remain strong as compared to fiscal 2011. "Despite reduced domestic availability,

we expect adequate supplies in the regions we operate our plants. Based on these fac-tors, we expect the strong fundamentals in our Beef business to continue in fiscal 2012." Markets Amid market turmoil, cash cattle prices were up again last week. Prices were around US$/cwt 112-113, 4-5 cents up. In the Chicago futures market, fed cattle prices started the week with drops, accompa-nying the strong uncertainties of global mar-kets. However, contracts that expire this year were firm in the week. Compared with a week ago, next year contracts were more affected and premiums over current prices reduced. The wholesaler reference of boxed beef cutout value improved in the early week after consistent falls during the two previous. The drop of last week, jointly with cattle prices,

worsened the margins of the meatpacking industry, though they are still positive. The latest HedgersEdge packer margin index was plus US$ 33.20 a head, compared with US$ 40.95 the previous day. Market activity on imported beef was very slow and prices were US$ 1.00 to US$ 3.00 higher. Demand was light to moderate with

Cattle (US$/k) Last Week Month Var month % Cattle (US$/k) Last Week Month Var month %

Steer Choice 2,48 2,39 2,51 -1,2% Steers, Sel 1-2 2,38 2,48 2,50 -4,8%

Heifer Choice 2,48 2,40 2,51 -1,3% Heifer Sel 1-2 2,39 2,42 2,42 -1,5%

Carcass 181 kg Boning 2,25 2,27 2,31 -2,9% Cow, cut & ut 1-3 1,61 1,60 1,58 1,8%

Carcass 159 cutter 2,25 2,27 2,31 -2,9% Import price US$/ton, frozen, boneless )

Steer choice carc. 3,93 3,85 4,03 -2,4% Forequarter 3746 4026 4232 -11,5%

Heifer Choice Carc. 3,92 3,82 4,03 -2,7% Hindquarter s/d s/d 4073 -

Processing beef 90 3,96 3,99 4,08 -3,0% Clods s/d s/d s/d -

85 3,71 3,70 3,87 -4,0% Eye Round s/d s/d s/d -

75 3,14 3,14 3,31 -5,0% Knuckle s/d 4924 4710 -

USA: Selected primal cuts US$ / Ton Top Sirloin Butts s/d s/d s/d -

Ribeye(over 14 lb.) 11503 11313 12403 -7,3% Striploins s/d s/d s/d -

Shoulder Clod 4312 4025 4197 2,7% Montreal Wholesale Prices (US$/k)

Knuckle 4733 4533 4713 0,4% Steers & Heifers

Inside Round 4410 4239 4340 1,6% Sides 5,52 5,75 5,55 -0,6%

Outside Round 4333 4074 4164 4,1% Fore Quarter 5,83 6,06 5,94 -1,9%

Eye of round 5068 4810 4898 3,5% Hind Quarter 6,40 6,67 6,56 -2,4%

Strip Loin 10614 11157 11246 -5,6% Shank 4,02 4,17 4,11 -2,1%

Top Butt 7007 7059 6192 13,2% Cow

Tender Loin 18641 18929 19176 -2,8% Inside round 5,32 5,52 5,46 -2,6%

CME futures - Live Cattle (US$/k) Outside round 5,10 5,29 5,23 -2,6%

Last Week Month Var month % Sirloin tip - Knuckle 5,08 5,27 5,21 -2,6%

Aug-11 2,52 2,50 2,53 -0,5% Sirloin K Butt 4,99 5,18 5,12 -2,6%

Oct-11 2,59 2,60 2,66 -2,5% Rib eye roll 6,42 6,67 6,59 -2,6%

Dec-11 2,64 2,60 2,76 -4,4% Strip loin 5,88 6,11 6,04 -2,6%

Apr-12 2,75 2,78 2,80 -1,9% Boneless box beef 85% 4,56 4,74 4,69 -2,6%

Jun-12 2,69 2,72 2,70 -0,4% Trimmings fresh 60-65% 3,15 3,27 3,23 -2,6%

Sources: USA: USDA and CME. Canada: Cattle: USDA; Import prices: Department of Foreign Affairs and International Trade

Wholesale Prices: Agriculture and Agri Food Canada

CanadaUSA

Nafta markets

0-15 Days CL 5-Aug 29-Jul 8-Jul 5-Aug 29-Jul 8-Jul

Bull meat 95% n n n 4.486 4.453 4.365

Cow meat 95% n n n n n n

90% n n n 4.167 4.189 4.101

CFM Fores 85% n n n n n n

Trimmings 85% n n n 3.913 n 3.924

80% n n n n n 3.781

75% n n n n n n

16-45 días

Bull meat 95% n n n 4.519 4.453 4.365

Cow meat 95% n n n n n n

90% n n n 4.233 4.189 4.101

CFM Fores 85% n n n n n n

Trimmings 85% n n n 3.990 n 3.924

80% n n n n n 3.781

75% n n n n n n

USA - Import values

In US$/ton; n=no quote; Source: based in USDA

Uruguay Australia & New Zealand

11

WORLD BEEF REPORT

Is a product from Tardáguila Agromercados. The reception of this information is subdued to service subscription. Any reproduc tion whitout citing the source and/or ilegal forwarding

of this material will be prosecuted citing authorial regulations (copyright).

very light offerings. The USDA said that the weak US dollar and lower domestic lean prices continued to pressure the import mar-ket. Europe

Turkey bids import of 10,500 tons of live cattle Late last week a bid call for 10,500 tons

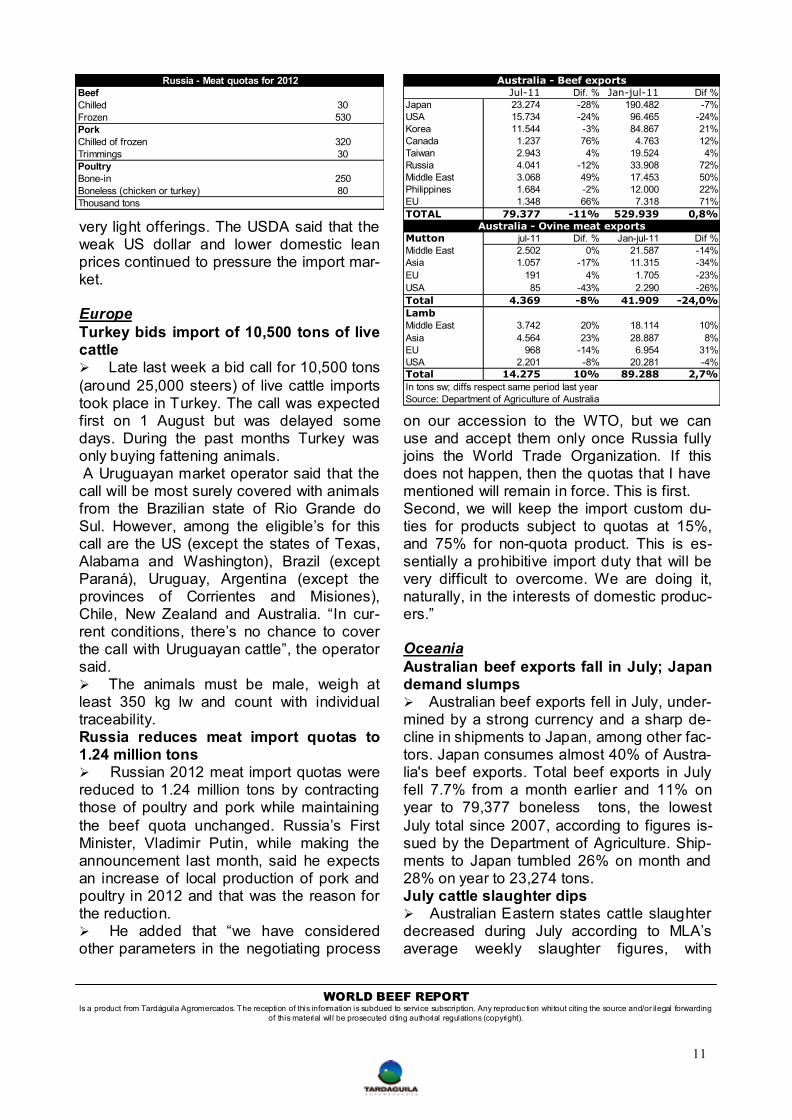

(around 25,000 steers) of live cattle imports took place in Turkey. The call was expected first on 1 August but was delayed some days. During the past months Turkey was only buying fattening animals. A Uruguayan market operator said that the call will be most surely covered with animals from the Brazilian state of Rio Grande do Sul. However, among the eligible’s for this call are the US (except the states of Texas, Alabama and Washington), Brazil (except Paraná), Uruguay, Argentina (except the provinces of Corrientes and Misiones), Chile, New Zealand and Australia. ―In cur-rent conditions, there’s no chance to cover the call with Uruguayan cattle‖, the operator said. The animals must be male, weigh at least 350 kg lw and count with individual traceability. Russia reduces meat import quotas to 1.24 million tons Russian 2012 meat import quotas were reduced to 1.24 million tons by contracting those of poultry and pork while maintaining

the beef quota unchanged. Russia’s First Minister, Vladimir Putin, while making the announcement last month, said he expects an increase of local production of pork and poultry in 2012 and that was the reason for the reduction. He added that ―we have considered other parameters in the negotiating process

on our accession to the WTO, but we can use and accept them only once Russia fully joins the World Trade Organization. If this does not happen, then the quotas that I have mentioned will remain in force. This is first. Second, we will keep the import custom du-ties for products subject to quotas at 15%, and 75% for non-quota product. This is es-sentially a prohibitive import duty that will be very difficult to overcome. We are doing it, naturally, in the interests of domestic produc-ers.‖ Oceania

Australian beef exports fall in July; Japan demand slumps Australian beef exports fell in July, under-mined by a strong currency and a sharp de-cline in shipments to Japan, among other fac-tors. Japan consumes almost 40% of Austra-lia's beef exports. Total beef exports in July fell 7.7% from a month earlier and 11% on year to 79,377 boneless tons, the lowest

July total since 2007, according to figures is-sued by the Department of Agriculture. Ship-ments to Japan tumbled 26% on month and 28% on year to 23,274 tons. July cattle slaughter dips Australian Eastern states cattle slaughter decreased during July according to MLA’s average weekly slaughter figures, with

Jul-11 Dif. % Jan-jul-11 Dif %

Japan 23.274 -28% 190.482 -7%

USA 15.734 -24% 96.465 -24%

Korea 11.544 -3% 84.867 21%

Canada 1.237 76% 4.763 12%

Taiwan 2.943 4% 19.524 4%

Russia 4.041 -12% 33.908 72%

Middle East 3.068 49% 17.453 50%

Philippines 1.684 -2% 12.000 22%

EU 1.348 66% 7.318 71%

TOTAL 79.377 -11% 529.939 0,8%

Mutton jul-11 Dif. % Jan-jul-11 Dif %

Middle East 2.502 0% 21.587 -14%

Asia 1.057 -17% 11.315 -34%

EU 191 4% 1.705 -23%

USA 85 -43% 2.290 -26%

Total 4.369 -8% 41.909 -24,0%

Lamb

Middle East 3.742 20% 18.114 10%

Asia 4.564 23% 28.887 8%

EU 968 -14% 6.954 31%

USA 2.201 -8% 20.281 -4%

Total 14.275 10% 89.288 2,7%

In tons sw; diffs respect same period last year

Source: Department of Agriculture of Australia

Australia - Beef exports

Australia - Ovine meat exports

Beef

Chilled 30

Frozen 530

Pork

Chilled of frozen 320

Trimmings 30

Poultry

Bone-in 250

Boneless (chicken or turkey) 80

Thousand tons

Russia - Meat quotas for 2012

12

WORLD BEEF REPORT

Is a product from Tardáguila Agromercados. The reception of this information is subdued to service subscription. Any reproduc tion whitout citing the source and/or ilegal forwarding

of this material will be prosecuted citing authorial regulations (copyright).

9-Aug 2-Aug 10-Aug-10

Uruguayan peso 19,39 18,45 20,81

Argentine peso 4,18 4,18 3,96

Brazil Real 1,626 1,567 1,758

Guaraní, Paraguay 3860 3850 4770

Canadian dollar 0,9946 0,9582 1,0273

Euro 1,4392 1,4175 1,3256

Pound 1,632 1,627 1,595

Rouble 29,560 27,842 29,860

Yen 77,085 77,185 85,680

Australian dollar 0,967 0,932 1,089

Exchange rates

All currency/US$, except euro and pound, US$/curr.

throughput 12% lower year-on-year. Num-bers were also historically low, falling 11%

in comparison to the five year monthly aver-age. The negative trend was reported in al-most every state, as a number of factors combined to restrict July turnoff. The main contributing reason was the slowdown in beef demand from export markets. Adding to this has been the recent strength of the A$, which has significantly eroded the com-petitiveness of Australian beef. Throughout July this translated into processors demand-ing fewer cattle as they reduced operations, with a slightly cheaper price trend in the physical markets. July lamb slaughter up Average weekly lamb slaughter, col-lected by MLA during July increased 5% year-on-year –the only month this year that lamb slaughter has been higher than the corresponding month in 2010. Despite the higher A$ towards the end of July, proces-sor demand for finished lambs to fill over-seas orders was reportedly strong. As sea-sonal conditions for winter have been better than previous years across the majority of states, producers have had the ability to

hold onto lambs further through winter.

Asia

China's pork prices decline for second week China's pork prices inched lower for the second week after months of surging prices that have been leading food inflation, Xinhua News Agency reported. Pork prices fell by

0.5% during the week ended July 31. The decline was 0.3% greater than that of the previous week, which marked the first such drop in three months. High pork prices have become a significant concern in China. The consumer price index, a main gauge of infla-tion, shot up to a three-year high of 6.5% in July, driven by surging food prices. Data from the National Bureau of Statistics showed that

pork prices in June surged by 57.1% year-on-year. Financial Times informed that the price rise was driven mostly by volatile and politi-cally sensitive food prices, which soared 14.8% in July from a year earlier, up from a 14.4% annual increase in June, according to data released by China’s National Bureau of Statistics on Tuesday. But despite the acceleration most econo-mists expect inflation to have peaked in July and to gradually moderate from now until the end of the year. Stabilization of pork prices in China, and falling prices of key commodities such as oil amid market turmoil and signs of slumping global growth will help.

Prices to Japan (C.I.F) 5-Aug 29-Jul 8-Jul Mthly Var %

Chilled

Grassfed fullsets 5.842 5.842 5.512 6,0%

Shortfed fullsets 6.504 6.460 6.173 5,4%

Frozen

Chuck/blade 4.696 4.696 4.696 0,0%

Thick flank 5.291 5.247 5.071 4,3%

Fore/hind blended s/d s/d 4.034 x

Topside 5.401 5.291 5.137 5,2%

Silverside 4.916 4.938 4.630 6,2%

Brisket 3.858 3.858 3.814 1,2%

To US (C.I.F.)

Bull 95 CL 4.405 4.354 4.189 5,2%

Cow 90 CL 4.145 4.145 3.968 4,4%

Cow 85 CL 4.034 4.001 3.902 3,4%

Shank 90 CL 4.079 4.079 3.946 3,4%

Trimmings 85 CL 4.023 3.968 3.902 3,1%

Trimmings 80 CL 3.616 3.726 3.671 -1,5%

Trimmings 75 CL 3.472 3.527 s/d x

Chucks 85 CL s/d s/d s/d x

U$S / ton CL Chemical Lean

Australia Beef Export Prices