working together to create value in the world of real estate · working together to create value in...

TRANSCRIPT

September 2015

Investor Presentation

58,000 employees, 230 offices, 80 countries, 1 global brand

Working together to create value in the world of real estate

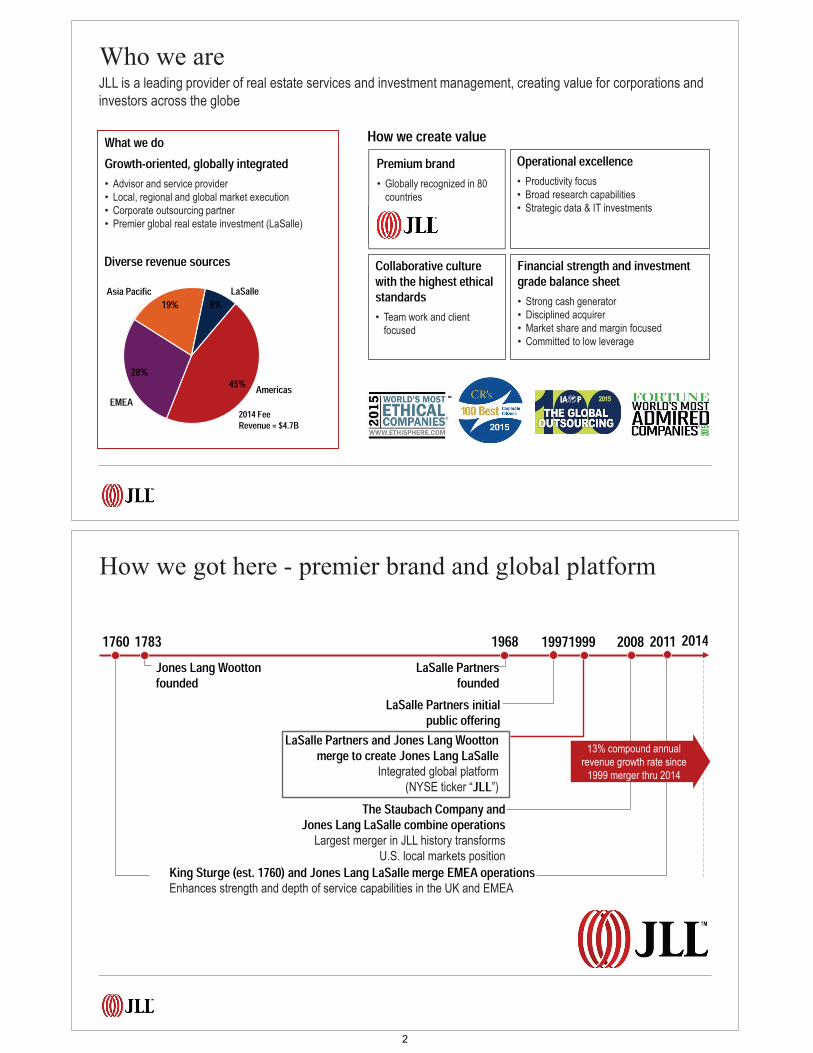

What we doGrowth-oriented, globally integrated• Advisor and service provider• Local, regional and global market execution• Corporate outsourcing partner• Premier global real estate investment (LaSalle)

Who we areJLL is a leading provider of real estate services and investment management, creating value for corporations andinvestors across the globe

Diverse revenue sources

45%28%

19% 8%

Americas

LaSalleAsia Pacific

EMEA2014 Fee Revenue = $4.7B

Operational excellence• Productivity focus• Broad research capabilities• Strategic data & IT investments

Collaborative culture with the highest ethical standards• Team work and client

focused

How we create value

Financial strength and investment grade balance sheet• Strong cash generator• Disciplined acquirer• Market share and margin focused• Committed to low leverage

Premium brand• Globally recognized in 80

countries

Jones Lang Wootton founded

1783 1968 19971999LaSalle Partners

foundedLaSalle Partners initial

public offeringLaSalle Partners and Jones Lang Wootton

merge to create Jones Lang LaSalleIntegrated global platform

(NYSE ticker “JLL”)

2008

The Staubach Company andJones Lang LaSalle combine operations

Largest merger in JLL history transforms U.S. local markets position

King Sturge (est. 1760) and Jones Lang LaSalle merge EMEA operations Enhances strength and depth of service capabilities in the UK and EMEA

1760

13% compound annual revenue growth rate since

1999 merger thru 2014

20142011

How we got here - premier brand and global platform

2

Fee Revenue ~4x

2004 2014

Note: All amounts in $ millions. 2004 market cap based on peak share price in the year. Current market cap based on August 2015 share price.

What we have accomplished

$1,167

$4,702

Market Cap~6x

2004 August 2015

Adjusted Operating Income~5x

$95

$510

2004 2014

$8,060

$1,247

Investment grade financial strength improved for future growth

Experienced leadership• Six-member Global Executive Board

combined 90-year tenure• 300+ International directors

Long history of profitable growth• 10-year compound annual fee

revenue growth = 15%• 80% organic and 20% from

M&A

78 acquisitions announced since 2005, executed and integrated based on:• Strategic alignment• Cultural fit• Financial discipline

Success through Global Financial Crisis by adapting to market cycles and capturing market share

How we earn fees

LeasingBroker transactions between tenants & landlords

Driven by economic growth and corporate confidence

Capital Markets & HotelsInvestment sales & finance arrangements

Driven by investor allocations to real estate and market liquidity

Property & Facility ManagementManagement & outsourcing of properties & portfolios

Driven by value enhancement for investors and corporate occupiers

Project & Development ServicesDesign & management of real estate projects

Driven by capital expenditure and expansion decisions

Advisory & OtherWorkplace strategy, valuation, consulting,advisory and sustainability

Driven by best practices in workplace productivity

LaSalle Investment ManagementReal estate investment management

Driven by investment performance and capital raising

MULTI-FAMILYRETAIL HOTEL

JLL has expertise in these real estate asset categories

INDUSTRIALOFFICE

3

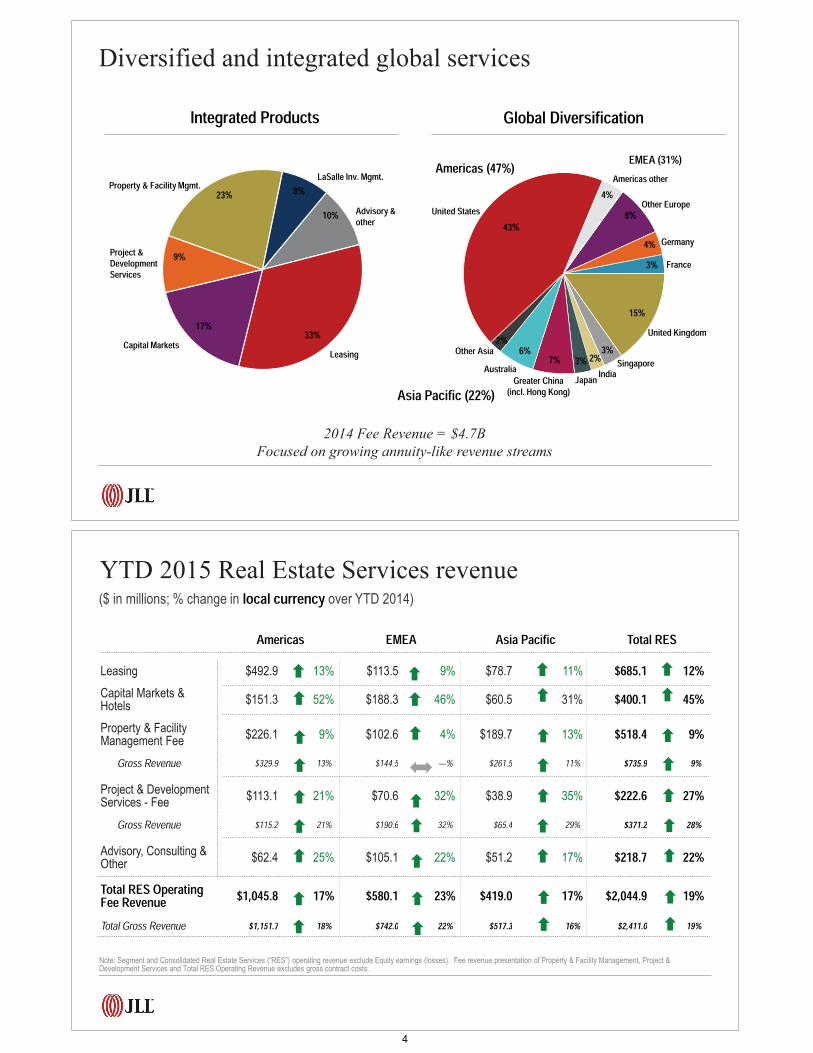

Integrated Products

Leasing

Advisory & other

LaSalle Inv. Mgmt.Property & Facility Mgmt.

Project & Development Services

Capital Markets 33%

10%8%

9%

Global Diversification EMEA (31%)

Other AsiaUnited Kingdom

FranceGermany

Other Europe

JapanGreater China(incl. Hong Kong)

Australia IndiaSingapore

Asia Pacific (22%)

Americas (47%)

United States43%

4%8%

4%3%

15%

3%2%3%7%2% 6%

Americas other 23%

Diversified and integrated global services

2014 Fee Revenue = $4.7B

Focused on growing annuity-like revenue streams

17%

($ in millions; % change in local currency over YTD 2014)

YTD 2015 Real Estate Services revenue

Note: Segment and Consolidated Real Estate Services (“RES”) operating revenue exclude Equity earnings (losses). Fee revenue presentation of Property & Facility Management, Project & Development Services and Total RES Operating Revenue excludes gross contract costs.

Americas EMEA Asia Pacific Total RESLeasing $492.9 13% $113.5 9% $78.7 11% $685.1 12%Capital Markets & Hotels $151.3 52% $188.3 46% $60.5 31% $400.1 45%Property & FacilityManagement Fee $226.1 9% $102.6 4% $189.7 13% $518.4 9%

Gross Revenue $329.9 13% $144.5 —% $261.5 11% $735.9 9%

Project & DevelopmentServices - Fee $113.1 21% $70.6 32% $38.9 35% $222.6 27%

Gross Revenue $115.2 21% $190.6 32% $65.4 29% $371.2 28%

Advisory, Consulting &Other $62.4 25% $105.1 22% $51.2 17% $218.7 22%Total RES OperatingFee Revenue $1,045.8 17% $580.1 23% $419.0 17% $2,044.9 19%Total Gross Revenue $1,151.7 18% $742.0 22% $517.3 16% $2,411.0 19%

4

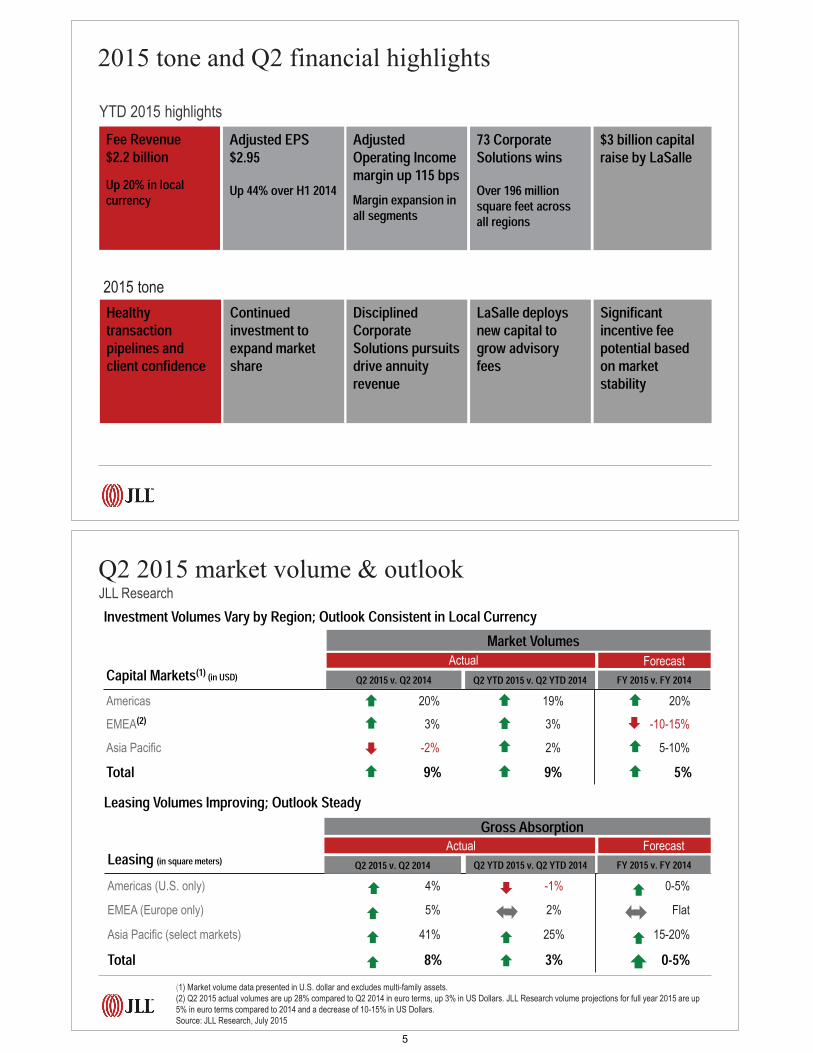

2015 tone and Q2 financial highlights

Adjusted EPS $2.95Up 44% over H1 2014

Fee Revenue $2.2 billionUp 20% in local currency

Adjusted Operating Income margin up 115 bpsMargin expansion in all segments

73 Corporate Solutions winsOver 196 million square feet across all regions

$3 billion capital raise by LaSalle

2015 tone

YTD 2015 highlights

Healthy transaction pipelines and client confidence

Continued investment to expand market share

Disciplined Corporate Solutions pursuits drive annuity revenue

LaSalle deploys new capital to grow advisory fees

Significant incentive fee potential based on market stability

JLL Research

Capital Markets(1) (in USD)Americas 20% 19% 20%

EMEA(2) 3% 3% -10-15%

Asia Pacific -2% 2% 5-10%

Total 9% 9% 5%

Leasing (in square meters)

Americas (U.S. only) 4% -1% 0-5%

EMEA (Europe only) 5% 2% Flat

Asia Pacific (select markets) 41% 25% 15-20%

Total 8% 3% 0-5%

Investment Volumes Vary by Region; Outlook Consistent in Local Currency

Q2 2015 market volume & outlook

Actual Forecast

Q2 2015 v. Q2 2014 Q2 YTD 2015 v. Q2 YTD 2014 FY 2015 v. FY 2014

Leasing Volumes Improving; Outlook Steady

Market Volumes

Actual Forecast

Q2 2015 v. Q2 2014 Q2 YTD 2015 v. Q2 YTD 2014 FY 2015 v. FY 2014

Gross Absorption

(1) Market volume data presented in U.S. dollar and excludes multi-family assets.(2) Q2 2015 actual volumes are up 28% compared to Q2 2014 in euro terms, up 3% in US Dollars. JLL Research volume projections for full year 2015 are up 5% in euro terms compared to 2014 and a decrease of 10-15% in US Dollars.Source: JLL Research, July 2015

5

Investment thesis

Driving increased profitability & cash flow

for growthObjectives and results

Guiding principles

25 acquisitions announced since 2014 with total estimated value over $500M

Capitalize on growth opportunities

S&P upgrade to BBB+

Protect balance sheet

Outperformance versus the S&P 500

Drive shareholder value

Growth focused• Long-term revenue

growth

• Market share gains

• Margin accretion

Core businesses• Market-leading

Leasing & Capital Markets positions

• Corporate Solutions

• LaSalle Investment Management

Global brand• Superior client

relationships

• Collaborative, experienced and deep leadership bench

• Highest ethical standards and commitment to diversity

Financial strength• Strong cash flow & low

leverage

• Disciplined capital allocations

• Proactive risk mitigation

• Dividend payout

Productivity mindset• Infrastructure leverage

• Occupancy

• IT investments

Driving to Strategy 2020

Our strategy for continued success

Build our local and regional Markets

business

Strengthen our winning positions in Corporate

Solutions

Capture the leading share of global capital flows for

investment sales

Grow LaSalle Investment Management’s leadership

position

G1 G2 G3 G4

G5

Connections: Differentiate and Sustain

• Balance top-line growth

• Platform investments

• Productivity to maximize profit

• Leverage global position

• Industry consolidation to grow market share

• Increase productivity

• Manage costs to improve margins

• Maintain financial strength

• Flexibility to respond to uncertainty

6

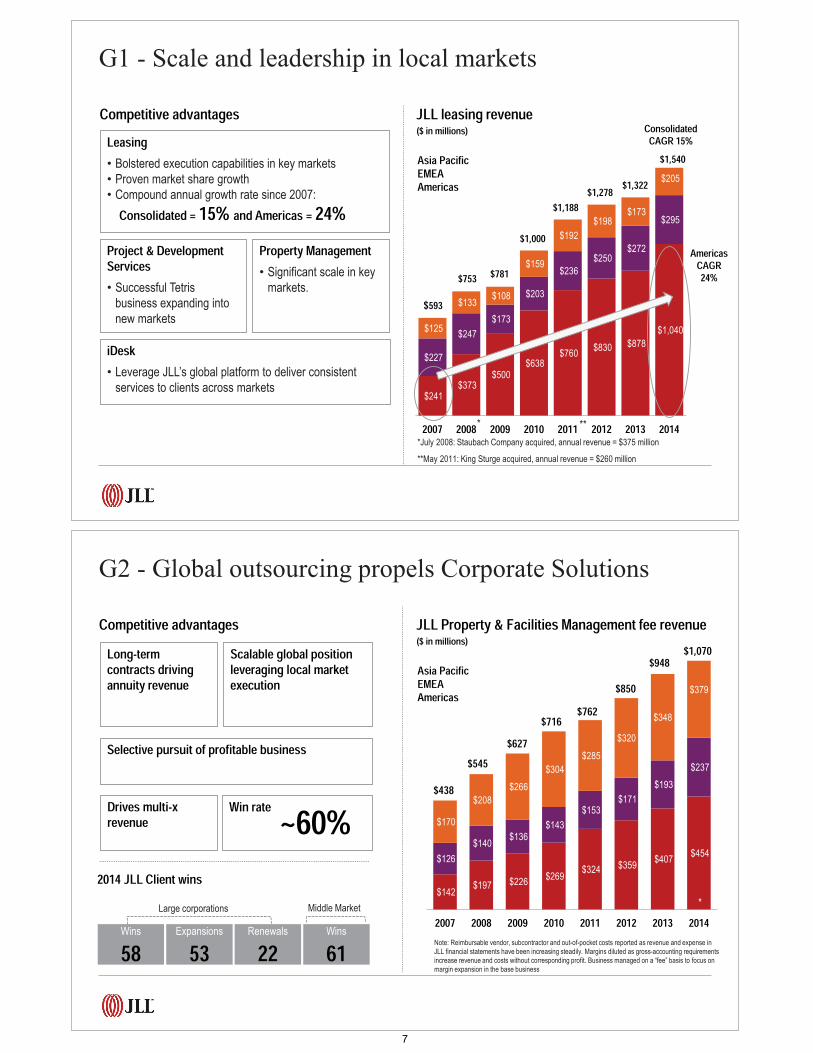

*July 2008: Staubach Company acquired, annual revenue = $375 million

**May 2011: King Sturge acquired, annual revenue = $260 million

($ in millions)

$241 $373

$500 $638

$760 $830 $878

$1,040

$227

$247

$173

$203

$236

$250 $272

$295

$125

$133 $108

$159

$192

$198 $173

$205

2007 2008 2009 2010 2011 2012 2013 2014

$593

$781$753

$1,000

$1,188$1,278

*

$1,322

ConsolidatedCAGR 15%

**

AmericasCAGR 24%

$1,540Leasing• Bolstered execution capabilities in key markets• Proven market share growth• Compound annual growth rate since 2007:

Consolidated = 15% and Americas = 24%Property Management• Significant scale in key

markets.

Project & Development Services• Successful Tetris

business expanding into new markets

iDesk• Leverage JLL’s global platform to deliver consistent

services to clients across markets

Competitive advantages JLL leasing revenue

Asia Pacific EMEA Americas

G1 - Scale and leadership in local markets

G2 - Global outsourcing propels Corporate Solutions

Note: Reimbursable vendor, subcontractor and out-of-pocket costs reported as revenue and expense in JLL financial statements have been increasing steadily. Margins diluted as gross-accounting requirements increase revenue and costs without corresponding profit. Business managed on a “fee” basis to focus on margin expansion in the base business

$142 $197 $226

$269 $324 $359

$407 $454

$126

$140 $136

$143

$153 $171

$193

$237

$170

$208

$266

$304

$285

$320

$348

$379

2007 2008 2009 2010 2011 2012 2013 2014

$438$545

$627$716 $762

$948$850

$1,070

2014 JLL Client wins

Wins

61Wins

58Expansions

53Renewals

22Large corporations Middle Market

Selective pursuit of profitable business

Long-term contracts driving annuity revenue

Scalable global position leveraging local market execution

Win rate30+

Drives multi-xrevenue ~60%

*

Competitive advantages($ in millions)JLL Property & Facilities Management fee revenue

Asia Pacific EMEA Americas

7

* May 2011: King Sturge acquired, annual revenue = $260 million

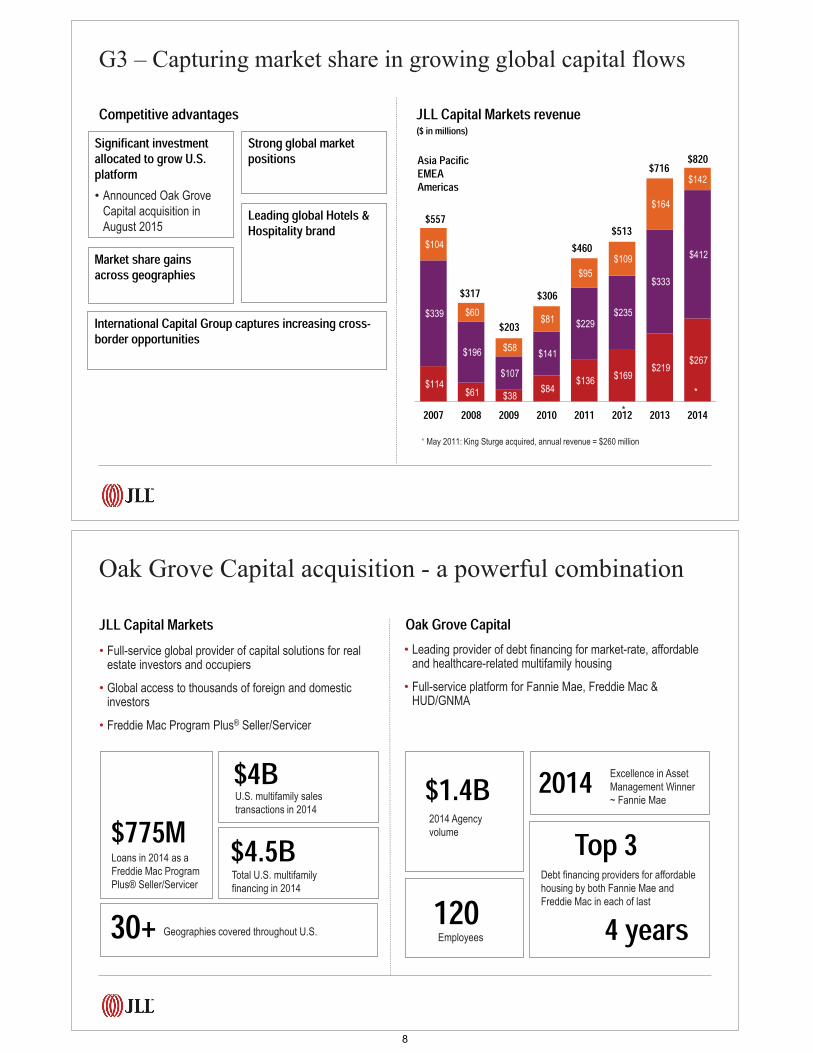

$114 $61 $38

$84 $136

$169 $219

$267

$339

$196

$107

$141

$229 $235

$333

$412 $104

$60

$58

$81

$95

$109

$164

$142

2007 2008 2009 2010 2011 2012 2013 2014

$557

$317

$203

$306

$460

*

$716

$513

*

$820

Market share gains across geographies

Strong global market positions

Significant investment allocated to grow U.S. platform• Announced Oak Grove

Capital acquisition in August 2015

Leading global Hotels & Hospitality brand

International Capital Group captures increasing cross-border opportunities

($ in millions)Competitive advantages JLL Capital Markets revenue

Asia Pacific EMEA Americas

G3 – Capturing market share in growing global capital flows

Oak Grove Capital• Leading provider of debt financing for market-rate, affordable

and healthcare-related multifamily housing

• Full-service platform for Fannie Mae, Freddie Mac & HUD/GNMA

• Full-service global provider of capital solutions for real estate investors and occupiers

• Global access to thousands of foreign and domestic investors

• Freddie Mac Program Plus® Seller/Servicer

$775MLoans in 2014 as a Freddie Mac Program Plus® Seller/Servicer

$4.5BTotal U.S. multifamily financing in 2014

$4BU.S. multifamily salestransactions in 2014

30+ Geographies covered throughout U.S. 4 years

$1.4B2014 Agencyvolume Top 3

Debt financing providers for affordable housing by both Fannie Mae and Freddie Mac in each of last 120

Employees

2014 Excellence in Asset Management Winner~ Fannie Mae

JLL Capital Markets

Oak Grove Capital acquisition - a powerful combination

8

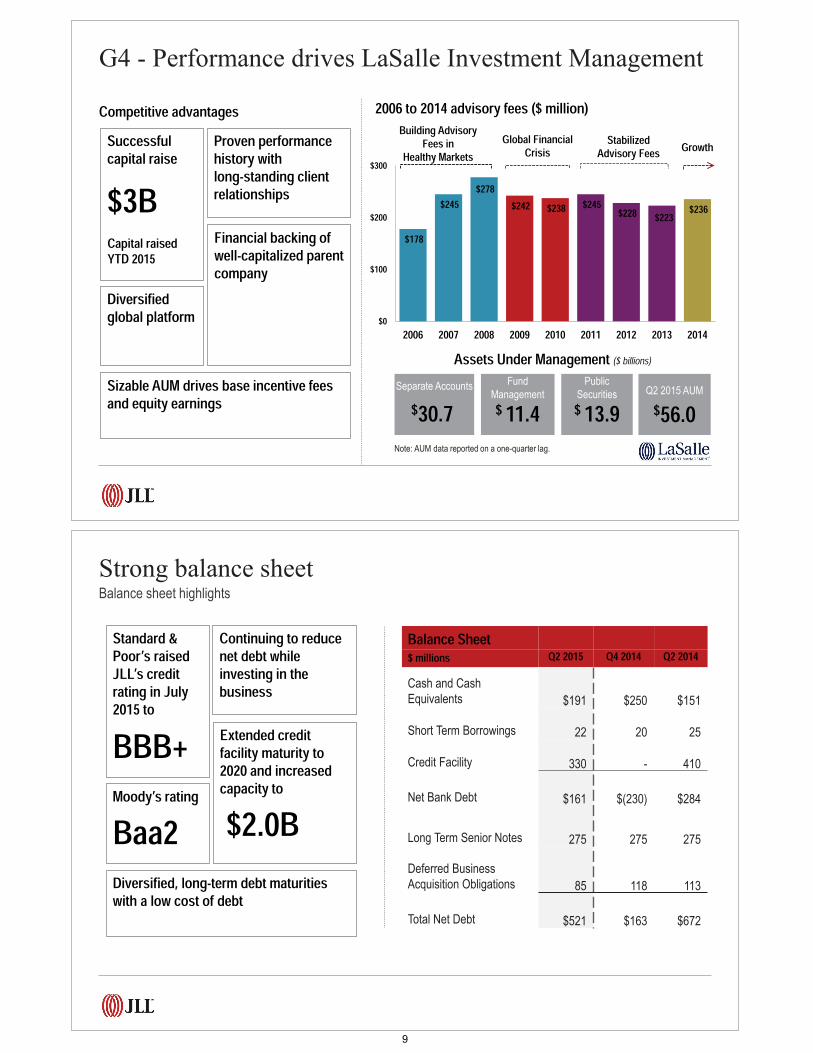

Assets Under Management ($ billions)

Note: AUM data reported on a one-quarter lag.

Q2 2015 AUM

$56.0Separate Accounts

$30.7Fund

Management

$ 11.4Public

Securities

$ 13.9

$178

$245 $278

$242 $238 $245 $228 $223 $236

$0

$100

$200

$300

2006 2007 2008 2009 2010 2011 2012 2013 2014

Building Advisory Fees in

Healthy MarketsGlobal Financial

CrisisStabilized

Advisory Fees Growth

G4 - Performance drives LaSalle Investment Management

Successful capital raise

Proven performance history with long-standing client relationships

Financial backing of well-capitalized parent company

Diversified global platform

Sizable AUM drives base incentive fees and equity earnings

$3BCapital raised YTD 2015

Competitive advantages 2006 to 2014 advisory fees ($ million)

Balance sheet highlights

Balance Sheet$ millions Q2 2015 Q4 2014 Q2 2014Cash and Cash Equivalents $191 $250 $151

Short Term Borrowings 22 20 25

Credit Facility 330 - 410

Net Bank Debt $161 $(230) $284

Long Term Senior Notes 275 275 275

Deferred Business Acquisition Obligations 85 118 113

Total Net Debt $521 $163 $672

Strong balance sheet

Standard & Poor’s raised JLL’s credit rating in July 2015 to

Continuing to reduce net debt while investing in the business

Extended credit facility maturity to 2020 and increased capacity to Moody’s rating

Diversified, long-term debt maturities with a low cost of debt

BBB+$2.0BBaa2

9

(1) Includes deferred business acquisition payments and earn outs paid during the period for transactions closed in prior periods(2) Includes contributions of $32M partially offset by capital distributions of $20M(3) Excludes investments in joint venture entities, capitalized leases and tenant improvement allowances that are required to be consolidated under U.S. GAAP(4) Full years 2014, 2013, 2012, 2011, 2010 (5) Other Financing Activities include debt issue costs and share activity related to taxes on stock awards

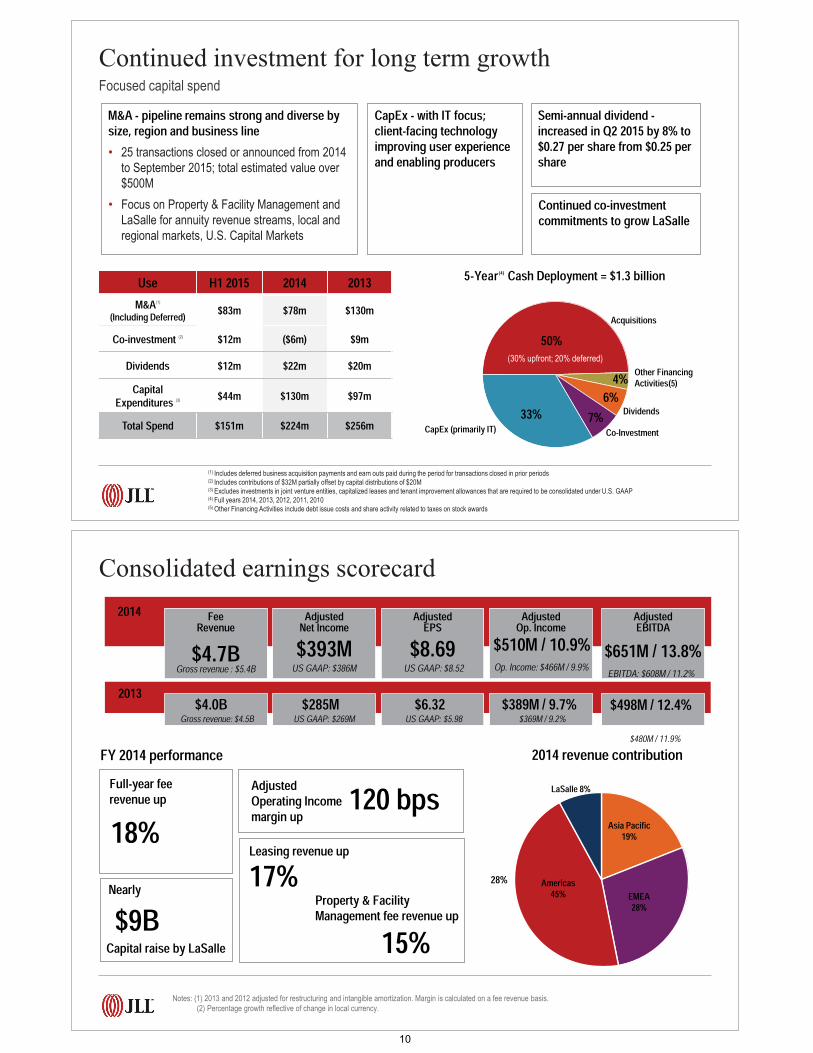

Continued investment for long term growth

Use H1 2015 2014 2013M&A(1)

(Including Deferred) $83m $78m $130mCo-investment (2) $12m ($6m) $9m

Dividends $12m $22m $20mCapital

Expenditures (3) $44m $130m $97mTotal Spend $151m $224m $256m

5-Year (4) Cash Deployment = $1.3 billion

50%

4%6%

7%33%

Acquisitions

Co-Investment

Other Financing Activities(5)

DividendsCapEx (primarily IT)

(30% upfront; 20% deferred)

Focused capital spend

CapEx - with IT focus; client-facing technology improving user experience and enabling producers

M&A - pipeline remains strong and diverse by size, region and business line• 25 transactions closed or announced from 2014

to September 2015; total estimated value over $500M

• Focus on Property & Facility Management and LaSalle for annuity revenue streams, local and regional markets, U.S. Capital Markets

Semi-annual dividend -increased in Q2 2015 by 8% to $0.27 per share from $0.25 per share

Continued co-investment commitments to grow LaSalle

2013 $285M $6.32 $389M / 9.7%$4.0BUS GAAP: $269M US GAAP: $5.98 $369M / 9.2%Gross revenue: $4.5B

Notes: (1) 2013 and 2012 adjusted for restructuring and intangible amortization. Margin is calculated on a fee revenue basis. (2) Percentage growth reflective of change in local currency.

2014 FeeRevenue$4.7B

AdjustedNet Income$393M

AdjustedEPS$8.69

Adjusted Op. Income$510M / 10.9%

Adjusted EBITDA

Gross revenue : $5.4B Op. Income: $466M / 9.9%US GAAP: $8.52US GAAP: $386M$651M / 13.8%EBITDA: $608M / 11.2%

$498M / 12.4%$480M / 11.9%

Consolidated earnings scorecard

28%

18%Full-year fee revenue up

$9B

120 bps

Nearly

Capital raise by LaSalle

Adjusted Operating Income margin upLeasing revenue up17%

Property & Facility Management fee revenue up

15%Americas

45% EMEA28%

Asia Pacific19%

LaSalle 8%

FY 2014 performance 2014 revenue contribution

10

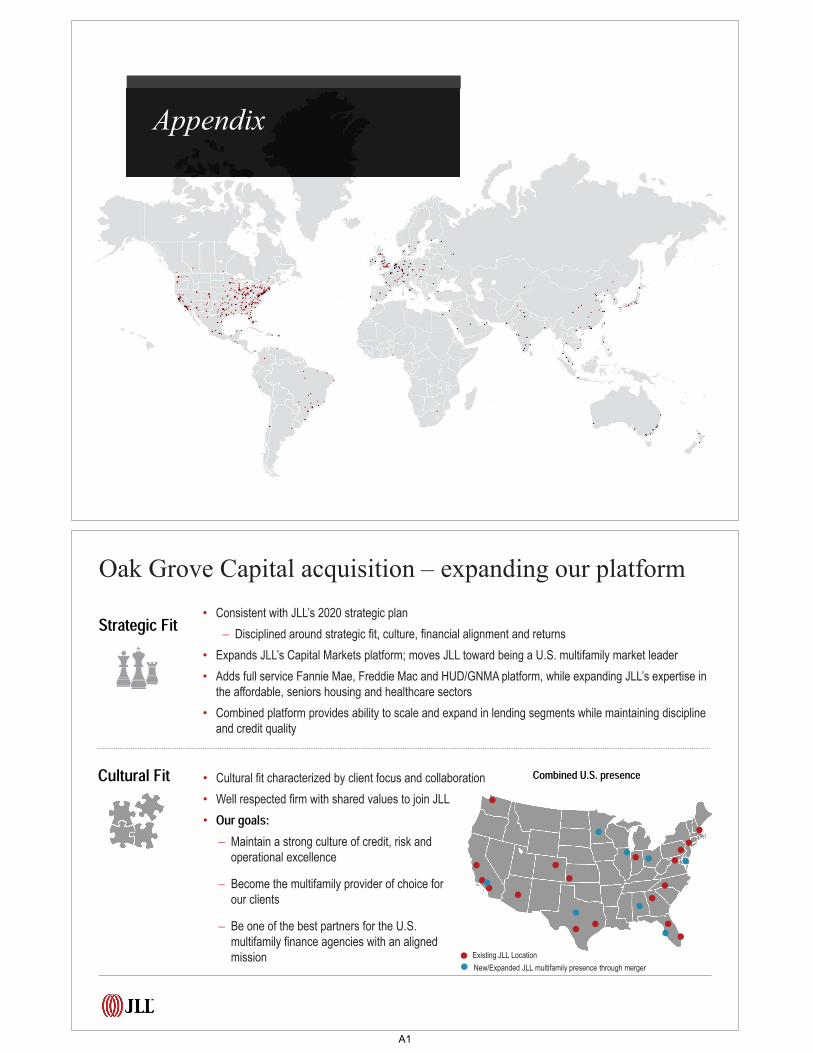

Appendix

Strategic Fit • Consistent with JLL’s 2020 strategic plan

Disciplined around strategic fit, culture, financial alignment and returns

• Expands JLL’s Capital Markets platform; moves JLL toward being a U.S. multifamily market leader

• Adds full service Fannie Mae, Freddie Mac and HUD/GNMA platform, while expanding JLL’s expertise in the affordable, seniors housing and healthcare sectors

• Combined platform provides ability to scale and expand in lending segments while maintaining discipline and credit quality

• Cultural fit characterized by client focus and collaboration

• Well respected firm with shared values to join JLL

Combined U.S. presence

• Our goals: Maintain a strong culture of credit, risk and operational excellence

Become the multifamily provider of choice for our clients

Be one of the best partners for the U.S. multifamily finance agencies with an aligned mission Existing JLL Location

New/Expanded JLL multifamily presence through merger

Cultural Fit

Oak Grove Capital acquisition – expanding our platform

A1

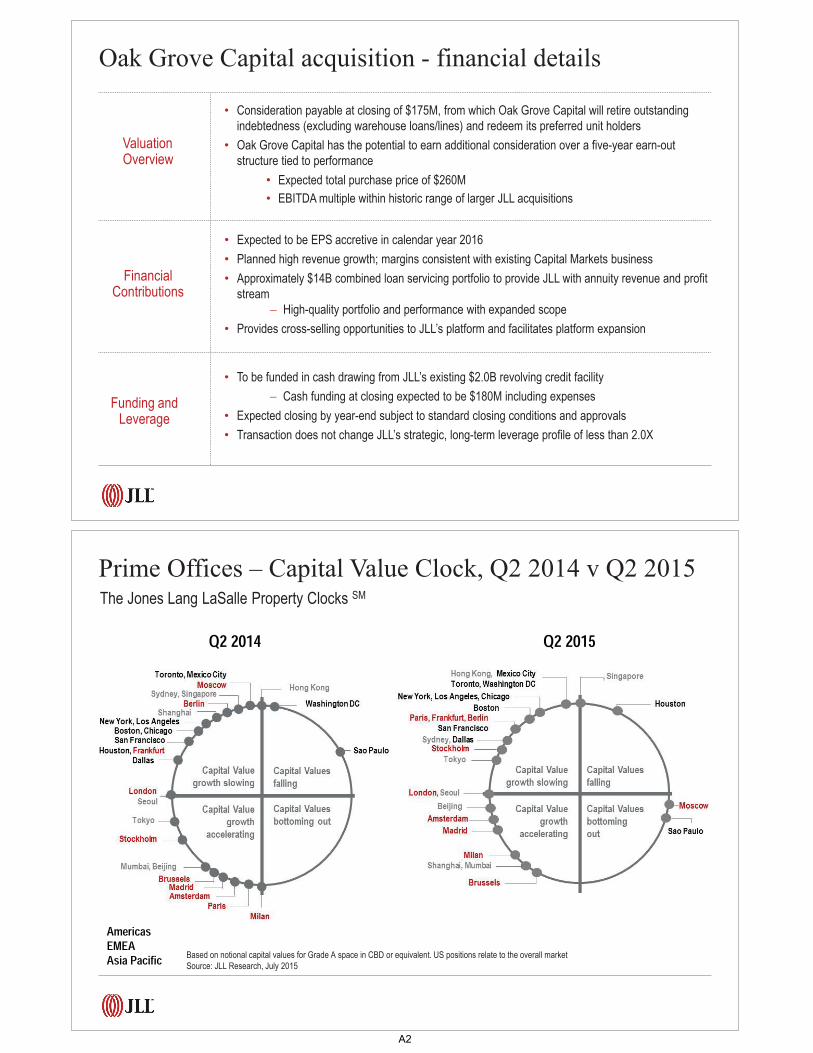

Oak Grove Capital acquisition - financial details

Valuation Overview

• Consideration payable at closing of $175M, from which Oak Grove Capital will retire outstanding indebtedness (excluding warehouse loans/lines) and redeem its preferred unit holders

• Oak Grove Capital has the potential to earn additional consideration over a five-year earn-out structure tied to performance

• Expected total purchase price of $260M

• EBITDA multiple within historic range of larger JLL acquisitions

Financial Contributions

• Expected to be EPS accretive in calendar year 2016

• Planned high revenue growth; margins consistent with existing Capital Markets business

• Approximately $14B combined loan servicing portfolio to provide JLL with annuity revenue and profit stream

High-quality portfolio and performance with expanded scope

• Provides cross-selling opportunities to JLL’s platform and facilitates platform expansion

Funding and Leverage

• To be funded in cash drawing from JLL’s existing $2.0B revolving credit facility

Cash funding at closing expected to be $180M including expenses

• Expected closing by year-end subject to standard closing conditions and approvals

• Transaction does not change JLL’s strategic, long-term leverage profile of less than 2.0X

Q2 2014 Q2 2015

Prime Offices – Capital Value Clock, Q2 2014 v Q2 2015

Based on notional capital values for Grade A space in CBD or equivalent. US positions relate to the overall market Source: JLL Research, July 2015

AmericasEMEAAsia Pacific

The Jones Lang LaSalle Property Clocks SM

A2

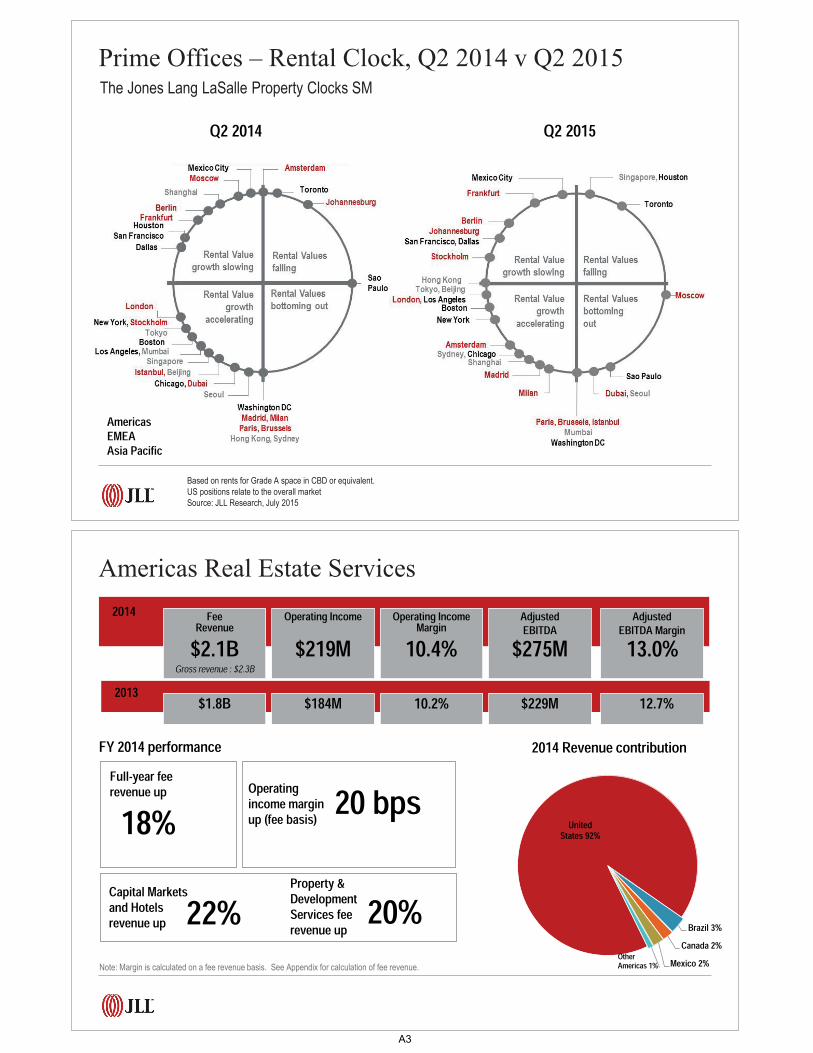

Based on rents for Grade A space in CBD or equivalent. US positions relate to the overall marketSource: JLL Research, July 2015

AmericasEMEAAsia Pacific

Prime Offices – Rental Clock, Q2 2014 v Q2 2015The Jones Lang LaSalle Property Clocks SM

Q2 2014 Q2 2015

2014 FeeRevenue Operating Income

$219MOperating Income Margin

10.4%AdjustedEBITDA$275M

AdjustedEBITDA Margin13.0%

Gross revenue : $2.3B 2013 $184M 10.2% $229M 12.7%$1.8B

$2.1B

2014 Revenue contribution

Note: Margin is calculated on a fee revenue basis. See Appendix for calculation of fee revenue.

United States 92%

Brazil 3%Canada 2%

Mexico 2%Other Americas 1%

18%Full-year fee revenue up

22%

20 bpsOperating income margin up (fee basis)

Capital Markets and Hotels revenue up

Property & Development Services fee revenue up 20%

FY 2014 performance

Americas Real Estate Services

A3

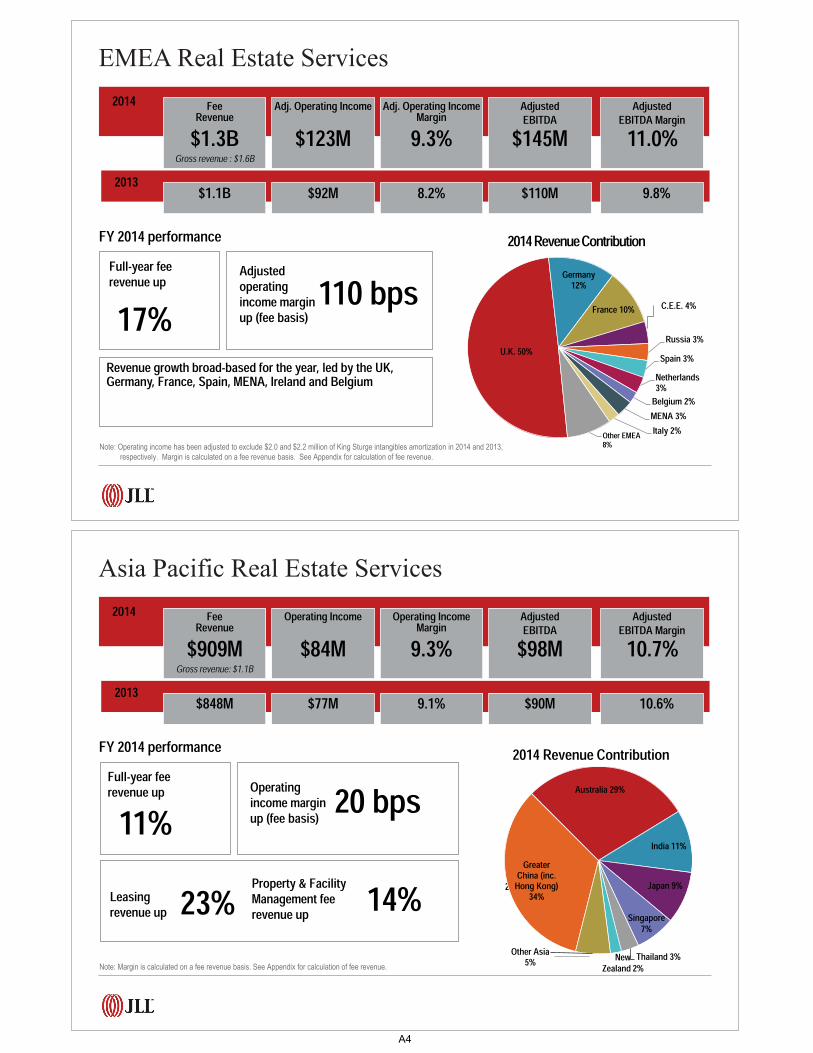

Note: Operating income has been adjusted to exclude $2.0 and $2.2 million of King Sturge intangibles amortization in 2014 and 2013, respectively. Margin is calculated on a fee revenue basis. See Appendix for calculation of fee revenue.

Germany 12%

France 10%

Russia 3%Spain 3%

Netherlands 3%

Belgium 2%MENA 3%Italy 2%Other EMEA

8%

U.K. 50%

C.E.E. 4%

Revenue growth broad-based for the year, led by the UK, Germany, France, Spain, MENA, Ireland and Belgium

17%Full-year fee revenue up 110 bpsAdjusted

operating income margin up (fee basis)

2014 Revenue ContributionFY 2014 performance

2014 FeeRevenue Adj. Operating Income

$123MAdj. Operating Income Margin

9.3%AdjustedEBITDA$145M

AdjustedEBITDA Margin11.0%

Gross revenue : $1.6B 2013 $92M 8.2% $110M 9.8%$1.1B

$1.3B

EMEA Real Estate Services

Note: Margin is calculated on a fee revenue basis. See Appendix for calculation of fee revenue.

34%

29%

11%Greater

China (inc. Hong Kong)

34%

Australia 29%

India 11%

Japan 9%

Thailand 3%Other Asia 5%

11%Full-year fee revenue up

23%

20 bpsOperating income margin up (fee basis)

Leasing revenue up

Property & Facility Management fee revenue up 14%

2014 Revenue ContributionFY 2014 performance

NewZealand 2%

2014 FeeRevenue Operating Income

$84MOperating Income Margin

9.3%AdjustedEBITDA$98M

AdjustedEBITDA Margin10.7%

Gross revenue: $1.1B 2013 $77M 9.1% $90M 10.6%$848M

$909M

Asia Pacific Real Estate Services

Singapore7%

A4

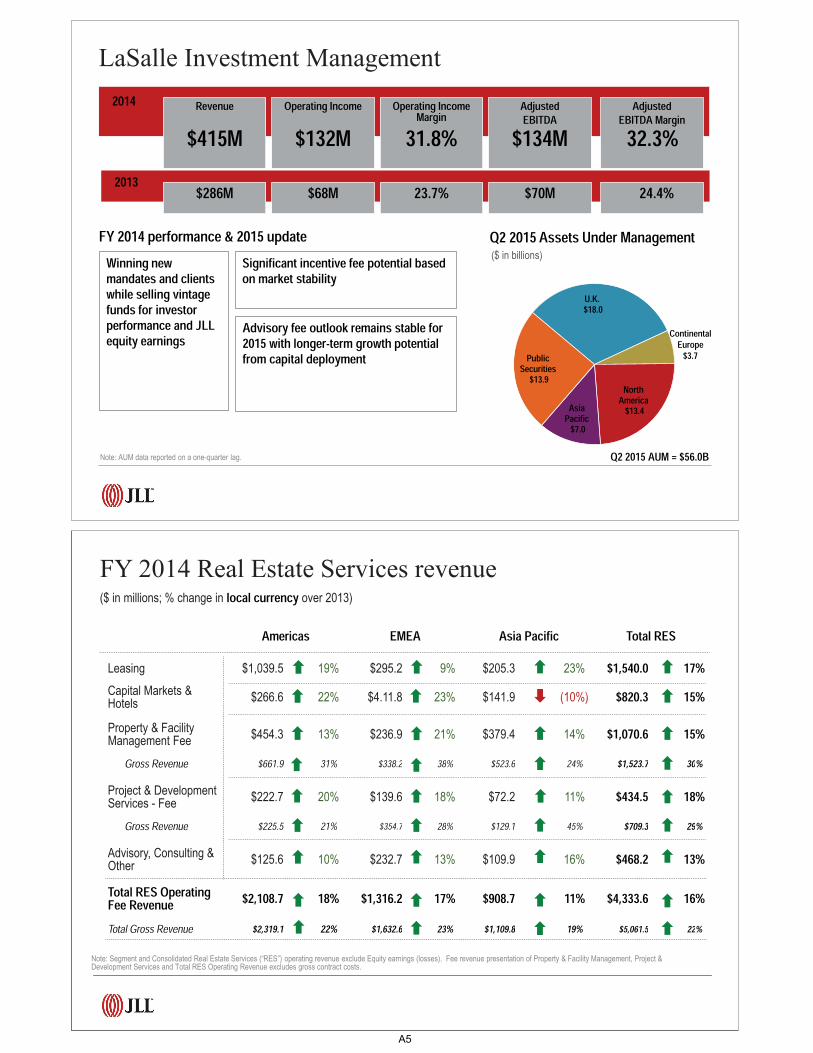

Q2 2015 Assets Under Management($ in billions)

Note: AUM data reported on a one-quarter lag. Q2 2015 AUM = $56.0B

U.K.$18.0

North America

$13.4 Asia Pacific

$7.0

Public Securities

$13.9

Advisory fee outlook remains stable for 2015 with longer-term growth potential from capital deployment

Winning new mandates and clients while selling vintage funds for investor performance and JLL equity earnings

Significant incentive fee potential based on market stability

FY 2014 performance & 2015 update

2014 Revenue Operating Income

$132MOperating Income Margin

31.8%AdjustedEBITDA$134M

AdjustedEBITDA Margin32.3%

2013 $68M 23.7% $70M 24.4%$286M

$415M

LaSalle Investment Management

Continental Europe

$3.7

Note: Segment and Consolidated Real Estate Services (“RES”) operating revenue exclude Equity earnings (losses). Fee revenue presentation of Property & Facility Management, Project & Development Services and Total RES Operating Revenue excludes gross contract costs.

FY 2014 Real Estate Services revenue ($ in millions; % change in local currency over 2013)

Americas EMEA Asia Pacific Total RESLeasing $1,039.5 19% $295.2 9% $205.3 23% $1,540.0 17%Capital Markets & Hotels $266.6 22% $4.11.8 23% $141.9 (10%) $820.3 15%Property & FacilityManagement Fee $454.3 13% $236.9 21% $379.4 14% $1,070.6 15%

Gross Revenue $661.9 31% $338.2 38% $523.6 24% $1,523.7 30%

Project & DevelopmentServices - Fee $222.7 20% $139.6 18% $72.2 11% $434.5 18%

Gross Revenue $225.5 21% $354.7 28% $129.1 45% $709.3 29%

Advisory, Consulting &Other $125.6 10% $232.7 13% $109.9 16% $468.2 13%Total RES OperatingFee Revenue $2,108.7 18% $1,316.2 17% $908.7 11% $4,333.6 16%Total Gross Revenue $2,319.1 22% $1,632.6 23% $1,109.8 19% $5,061.5 22%

A5

Note: Equity earnings of $27.1M and $38.5M in Q2 2015 and YTD 2015, respectively, are included in segment results, however, excluded from Consolidated totals. Year-over-year increases shown fee-based have been calculated using fee revenue, which excludes gross contract costs.

Consolidated Fee - $1,182Gross - $1,374

LaSalle$105

EMEAFee - $327

Gross - $418

Q2 2015 and YTD performance

AmericasFee - $545

Gross - $598

Asia PacFee - $231

Gross - $280 Consolidated Fee - $2,211Gross - $2,577

LaSalle$203

EMEAFee - $581

Gross - $743

YTD 2015

AmericasFee - $1,047

Gross - $1,153

Asia PacFee - $419

Gross - $517

Q2 2015 YTD 2015YOY % Growth, Fee Revenue basis

LC USD Segment LC USD

12% 10% Americas 18% 16%

22% 6% EMEA 23% 7%

18% 8% Asia Pacific 17% 8%

38% 29% LaSalle 41% 32%

17% 9% Consolidated 20% 13%16% 8% Consolidated Gross Revenue 20% 11%

Q2 2015

Revenue ($ in millions)

Refer to page 16 for Reconciliation of GAAP Net Income to Adjusted EBITDA for the three and six months ended June 30, 2015, for details relative to these Adjusted EBITDA calculations. Segment Adjusted EBITDA is calculated by adding the segment’s depreciation and amortization to its reported operating income, which excludes restructuring and acquisition charges. Consolidated Adjusted EBITDA is the sum of the Adjusted EBITDA of the four segments.

Q2 Adj. EBITDA Margin, Fee Revenue YTD2015 2014 Segment 2015 2014

11.3% 12.2% Americas 10.7% 10.1%

11.7% 9.8% EMEA 7.0% 5.7%

8.6% 8.9% Asia Pacific 6.6% 6.0%

36.0% 28.0% LaSalle 32.7% 25.7%

13.3% 12.2% Consolidated 11.2% 9.4%

Q2 2015 and YTD performance

Consolidated $157

Q2 2015Asia Pac

$20EMEA$38

LaSalle$38

Consolidated $247

YTD 2015

Americas$61

Asia Pac$28

LaSalle$66

Americas$112

EMEA$41

Adjusted EBITDA ($ in millions)

A6

Note: Segment and Consolidated Real Estate Services (“RES”) operating revenue exclude Equity earnings (losses). Fee revenue presentation of Property & Facility Management, Project & Development Services and Total RES Operating Revenue excludes gross contract costs.

Americas EMEA Asia Pacific Total RESLeasing $263.7 6% $65.1 12% $50.2 11% $379.0 8%Capital Markets & Hotels $76.5 30% $113.2 38% $33.1 25% $222.8 33%Property & FacilityManagement Fee $111.9 8% $50.9 (3%) $95.8 13% $258.6 7%

Gross Revenue $163.4 9% $69.7 (10%) $130.0 9% $363.1 4%

Project & DevelopmentServices - Fee $60.4 22% $39.4 36% $21.6 38% $121.4 29%

Gross Revenue $61.8 23% $110.7 44% $36.1 20% $208.6 34%

Advisory, Consulting &Other $32.1 36% $57.6 24% $30.2 27% $119.9 27%Total RES OperatingFee Revenue $544.6 11% $326.2 21% $230.9 18% $1,101.7 16%Total Gross Revenue $597.5 12% $416.3 23% $279.6 14% $1,293.4 16%

Q2 2015 Real Estate Services revenue ($ in millions; % change in local currency over Q2 2014)

• Reimbursable vendor, subcontractor and out-of-pocket costs reported as revenue and expense in JLL financial statements

have been increasing steadily

• Gross accounting requirements increase revenue and costs without corresponding profit

• Business managed on a fee revenue basis to focus on margin expansion in the base business

Revenue

Gross contract costs

Fee revenueOperating expenses

Gross contract costs

Fee-based operating expensesOperating incomeRestructuring and acquisition charges

Adjusted operating income

Adjusted operating income marginNote: Consolidated revenue and fee revenue exclude equity earnings (losses). Restructuring and acquisition charges are excluded from adjusted operating income margin.

2015 2014 2015 2014

Three months ended June 30 Six months ended June 30

$ 1,373.5 $ 1,277.2 $ 2,577.0 $ 2,314.6

191.7 191.2 366.1 350.9

$ 1,181.8 $ 1,086.0 $ 2,210.9 $ 1,963.7

$ 1,270.5 $ 1,185.5 $ 2,421.4 $ 2,238.2

191.7 191.2 366.1 350.9

$ 1,078.8 $ 994.3 $ 2,055.3 $ 1,887.3

$ 103.0 $ 91.7 $ 155.6 $ 76.41.8 5.5 2.6 41.4

$ 104.8 $ 97.2 $ 158.2 $ 117.8

8.9% 9.0% 7.2% 6.0%

Fee Revenue/Expense Reconciliation ($ in Millions)

A7

GAAP net income attributable to common shareholders

Shares (in 000s)

GAAP diluted earnings per share

2015 2014 2015 2014

Three months ended June 30 Six months ended June 30

$ 90.1 $ 71.8 $ 132.0 $ 87.7

45,435 45,278 45,393 45,220

$ 1.98 $ 1.58 $ 2.91 $ 1.94

$ 90.1 $ 71.8 $ 132.0 $ 87.7

1.4 4.1 2.0 5.2

$ 91.5 $ 75.9 $ 134.0 $ 92.945,435 45,278 45,393 45,220

$ 2.01 $ 1.68 $ 2.95 $ 2.05

GAAP net income attributable to common shareholders

Restructuring and acquisition charges, net

Shares (in 000s)

Adjusted diluted earnings per share

Adjusted net income

Reconciliation of GAAP net income to adjusted net

income and earnings per share ($ in Millions)

GAAP net income

Interest expense, net of interest income

2015 2014 2015 2014

Three months ended June 30 Six months ended June 30

$ 91.4 $ 72.4 $ 134.7 $ 88.5

7.6 7.6 13.6 14.3

31.1 24.1 45.9 (5.0)

25.5 22.8 50.4 45.2

$ 155.6 $ 126.9 $ 244.6 $ 143.01.8 5.5 2.6 41.4

$ 157.4 $ 132.4 $ 247.2 $ 184.4

Provision for (benefit from) income taxes

Depreciation and amortization

EBITDARestructuring and acquisition charges

Adjusted EBITDA

Reconciliation of GAAP net income to adjusted EBITDA($ in Millions)

A8

Statements in this presentation regarding, among other things, future financial results and performance, achievements, plans

and objectives and dividend payments may be considered forward-looking statements within the meaning of the Private

Securities Litigation Reform Act of 1995. Such statements involve known and unknown risks, uncertainties and other factors

which may cause actual results, performance, achievements, plans and objectives of JLL to be materially different from those

expressed or implied by such forward-looking statements. For additional information concerning risks, uncertainties and other

factors that could cause actual results to differ materially from those anticipated in forward-looking statements, and risks to

JLL’s business in general, please refer to those factors discussed under “Business,” “Risk Factors,” “Management’s

Discussion and Analysis of Financial Condition and Results of Operations,” “Quantitative and Qualitative Disclosures about

Market Risk,” and elsewhere in JLL’s Annual Report on Form 10-K for the year ended December 31, 2014, in the Quarterly

Reports on Form 10-Q for the quarters ended March 31, 2015 and June 30, 2015, and in other reports filed with the Securities

and Exchange Commission. There can be no assurance that future dividends will be declared since the actual declaration of

future dividends, and the establishment of record and payment dates, remains subject to final determination by the Company’s

Board of Directors. Any forward-looking statements speak only as of the date of this presentation, and except to the extent

required by applicable securities laws, JLL expressly disclaims any obligation or undertaking to publicly update or revise any

forward-looking statements contained herein to reflect any change in JLL’s expectations or results, or any change in events.

Cautionary note regarding forward-looking statements

© 2015 Jones Lang LaSalle IP, Inc. All rights reserved. No part of this publication may be reproduced by any means, whether graphically, electronically, mechanically

or otherwise howsoever, including without limitation photocopying and recording on magnetic tape, or included in any information store and/or retrieval system without

prior written permission of Jones Lang LaSalle IP, Inc.

A9