woongjin energy · •first adoption 100% diamond – wire wafer ... expected to have 20% m/s of...

TRANSCRIPT

1

Confidential. Not to be copied, reproduced or redistributed.

16th Aug, 2011

Woongjin EnergyGlobal NO.1 in the field of Single Crystalline Solar silicon in 2011

IR Conference 2011

Investor Relations

2

Confidential. Not to be copied, reproduced or redistributed.

This material contains the company’s current expectations regarding futurebusiness and financial performances, and forward-looking statements concerning the company’s management strategy, R&D activity, capex, and business plans.

Forward-looking statements are subject to risks and uncertainties that couldcause actual results and outcomes to differ materially from expectations. Thecompany does not guarantee the accuracy or completeness of any statementsthat do not relate strictly to historical or current facts.

Forward Looking Statement

3

Confidential. Not to be copied, reproduced or redistributed.

3

Confidential. Not to be copied, reproduced or redistributed.

I. Company Overview

II. Investment Highlights of Woongjin Energy

1. Secure and stable supply

2. Vertically Integrated Solar Value Chain

3. Diversification of the client base

4. Capacity Expansion

5. Cost Reduction & Competitive Leadership

6. Building eco-friendly system

III. Financial Review

IV. Appendices

Table of Contents

4

Confidential. Not to be copied, reproduced or redistributed.

I. Company Overview

Creating bright future

with solar energy

5

Confidential. Not to be copied, reproduced or redistributed.

General Status

Ownership Structure

Foundation November, 2006

Chairman & CEO Ph.D Oh, Myung & Ph. D Yoo, Hak-do

Location 1316 GwanPyung-Dong YuSeong-Gu, Daejeon

Business Ingot & wafer for Solar

Employees 524 people(as of Jun 30th, 2011)

Affiliates Woongjin Holdings and 30 subsidiaries

Website www.WoongjinEnergy.com

Company Overview

Stock Information

39.4%

31.3%

3.5%2.4%

18.5%4.9%

Woongjin Holdings and affiliate person

SunPower Corp.

Domestic Institutions

Foreign investors

Individual investors

ESOA(Public offering)

* As of Dec. 31th, 2010

Total issued shares 62,093,120

Paid-in capital KRW 31 Billion

Listing date June 30, 2010

Market cap.

(as of Aug 1th, 2011)KRW 872.4 Billion

- 52wk High: 23,350 KRW- 52wk Low: 12,250 KRW- As of Aug. 9th, 2011: 10,200 KRW

• Pursue a high quality & productivity in PV industry and make an effort quality improvement to be a Global No.1 company

6

Confidential. Not to be copied, reproduced or redistributed.

Company Overview

• Make a bright future by developing and supplying renewable energy

Company History

7

Confidential. Not to be copied, reproduced or redistributed.

Main products

PolySilicon Ingot Wafer

• Raw materials

for growing Ingot

• Material for Solar cell and

semiconductor

• Put Silicon in a grower

melting with high temp

growing Ingot from seed.

• Sawing mono ingot into

170~200㎛ slices for Solar cell

• Cell effciency 24.2%(World best)

• First adoption 100% diamond –

wire wafer process

• Specialized in high quality monocrystalline ingot and wafer production

• Global No.1 in the field of single Crystalline Solar silicon in 2011

On completion of building 2 in 2011, expected to have 20% M/S of single crystal ingot/wafer market

8

Confidential. Not to be copied, reproduced or redistributed.

I. Company Overview

Creating bright future

with solar energy

II. Investment Highlights1. Secure and stable supply

2. Vertically Integrated Solar Value Chain

3. Diversification of the client base

4. Capacity Expansion(Economics of Scale)

5. Cost Reduction & Competitive Leadership

6. Building eco-friendly system

9

Confidential. Not to be copied, reproduced or redistributed.

1. Secure and stable supply

Stableproductsupply

590 650 650 650 650

5

355

1000

1355 1400

2010 2011(E) 2012(E) 2013(E) 2014(E)

Fabs 1&2 fab 3

SunPower Capacity Expansion(E)

2,0502,005

1,650

1,005

(Unit: MW)

• Woongjin Group and SunPower(US) signed a joint venture to create a

viable solar energy company for a stable ingot supply to SunPower

• Trustworthy partnership in terms of quality, supply and price

• Win-Win partnership and vertical integration, with long-term

contract(Until 2016)

Joint Venture & Captive Market

595

• Close and trustworthy partnership with SunPower

[[Source: SunPower Jun 7th,2011]

Fab 3Fab 1&2

10

Confidential. Not to be copied, reproduced or redistributed.

• Long term supply contract with SunPower Receive polySilicon from 2007 to 2016

• Raw materials supplied by Woongjin Polysilicon(PolySilicon will supply over 1,500 ton to WJE)

• We can obtain polysilicon with stable and reasonable prices through long term supply contract

2. Vertically Integrated Solar Value Chain

SolarCell / Panel

PolySilicon

Ingot / WaferInstallation

<Power Generation>

WJ Polysilicon WJ Energy SunPower / AUO SP SunPower

5,000 MT/yr.1GW (Ingot)

500MW (Wafer)> 1GW/yr.(E) >4GW/yr.(E)

17,000MT/yr.by 2013

2GW (Ingot)1.5GW (Wafer)

by 2013

> 2GW/yr.

by 2014(E) >6GW/yr.(E)

Hemlock,Wacker,OCI,GCL,REC, Tokuyama

LDK,GCL,Renesola, Solargiga,Yingli,REC,

MEMC,Trina

Suntech,JA Solar,Q-Cell,

Motech,Yingli,Jinko,Sharp

Canadian Solar,LDK

Company

Capacity(2011)

Expansion

Competitors

< < <

[Source: WJE Company]

11

Confidential. Not to be copied, reproduced or redistributed.

3. Diversification of the client base

OVERSEA

DOMESTIC

• Sales Contract (Jan. 2011 ~ Dec. 2011 )

• USD 36Mil.(on discussion extending contract)

• Sales Contract (Oct. 2010~ Dec. 2011 )

• USD 26Mil.

• Sales Contract(Aug. 2010 ~ Dec. 2011 )

• USD 108Mil.(on discussion extending contract)

• Sales Contract(Sep. 2010 ~ Dec. 2011)

• USD 19Mil.

• Qual sample tested.

• On Discussion long term contract

95%

5%

85%

15%

Current

SunPower

Others

Diversified client base

• Reduce dependence on SunPower over the long-term through the diversification of the client base

Company “L”Company “S”

As of Dec. 2009

As of Dec. 2010

60%

40%

As of Dec. 2011(E)

Establish

#2 Plant

• Expand production line for Mono N-type wafer

• Discuss continuous for supply 2011

Company “B”Company “C”

Company “I”

• Sales Contract(Oct. 2010 ~ Dec. 2013 )

• USD 44Mil.

Taiwan

Germany

Austria • Sales Contract(Mar. 2011 ~ Dec. 2015)

• USD 115Mil.

12

Confidential. Not to be copied, reproduced or redistributed.

4. Capacity Expansion(Economics of Scale)

Capacity Expansion(E)

(bn. KRW) Amount

2010(A) 141

2011(E) 156

2012(E) 175

2013(E) 180

(Unit: MW)

• Since 2010, Increased Capex amount for new business and capacity expansion.

• Global Leader in Solar Business by 2013

350 350 350 350

150

650 650 650

500

1000

2010A 2011(E) 2012(E) 2013(E)

Fab1 Fab2 Fab3

Capital Expenditure Estimate

21.3

244

432.5

514.4

2011(E) 2012(E) 2013(E) 2014(E)

Fab 3 Investment(Accumulated Capex)

• Objective: Potential Customers Serious CustomersMarket Leadership & Economy of scale through Capa expansion

• Scale: Capex : 514.4 billion KRW Capacity : 1 GW cf. Fab. 1&2 (1GW) + Feb.3(1GW) =Total : (2GW)Equipment : Grower : 384 EA / Wire – Saw : 72 EA

•Sales Portion

Fab 3 Investment Summary

(Unit: bn. KRW)

Debt financing269.3bn(KRW)

*CB,BW Issue( partially )

260.0bn(KRW)

* Could be change without notice

100

40 60

6040

Fab1 Fab2 FAB3

Non-SunPower

SunPower

13

Confidential. Not to be copied, reproduced or redistributed.

5. Cost Reduction & Competitive Leadership

1st Charge(118kg) 2nd Charge(50kg)1st Ingot 2nd Ingot

GrowingProcess

GrowingProcess

• Less Quarts

• Less Electricity

• Less usage

• Increasing of productivity

• Decreasing of Unit Cost(USD 3Mil./yr.)

Ingot(Multi-Pulling)

• Woongjin Energy has high margin structure based on cost leadership

• Improving profitability as strengthening of competitive leadership such as Ingot, Wafer

< Increasing productivity 1.8X for 1 QZ crucible>

Wafer(Dimand Wiresaw)

SiC Slurry on Bare Wire

Coolant on Diamond Wire

Develop non-slurry wire-saw process

Increase productivity and secure cost competitiveness

• Increase productivity(capa 1.6X/unit)

• Lower Manufacturing cost

• Save Capex for Slurry recycle system(2 bil. KRW)

• Save Capex for wire saw(72ea → 36ea)

• Easy Coolant Recycle(Eco-friendly process)

14

Confidential. Not to be copied, reproduced or redistributed.

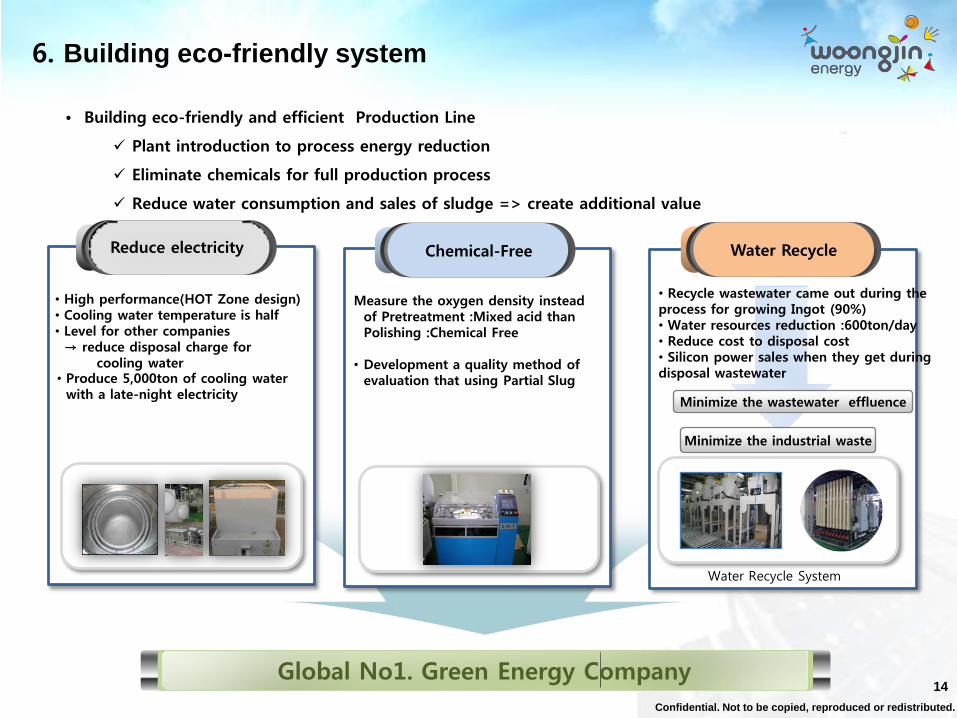

6. Building eco-friendly system

• Building eco-friendly and efficient Production Line

Plant introduction to process energy reduction

Eliminate chemicals for full production process

Reduce water consumption and sales of sludge => create additional value

222

Chemical-Free Water Recycle

• High performance(HOT Zone design)• Cooling water temperature is half • Level for other companies→ reduce disposal charge for

cooling water

Water Recycle System

Reduce electricity

• Produce 5,000ton of cooling water with a late-night electricity

• Recycle wastewater came out during the process for growing Ingot (90%)• Water resources reduction :600ton/day• Reduce cost to disposal cost• Silicon power sales when they get during disposal wastewater

Minimize the wastewater effluence

Minimize the industrial waste

Global No1. Green Energy Company

Measure the oxygen density instead of Pretreatment :Mixed acid than Polishing :Chemical Free

• Development a quality method of evaluation that using Partial Slug

15

Confidential. Not to be copied, reproduced or redistributed.

III. Financial Review

16

Confidential. Not to be copied, reproduced or redistributed.

1. WJ Energy Condensed Income Statement

Revenue Breakdown

2Q 11 2Q 10 (+/-) 1H 11 1H 10 (+/-)

Revenue 80.7 33.1 143.8% 157.2 64.7 143.0%

Ingot 52.1 28.8 80.9% 89.5 56.4 58.7%

Wafer 26.8 2.1 1176.2% 64.0 6.5 884.6%

Other 1.8 2.2 -18.2% 3.7 1.8 105.6%

Gross Profit 13.2 16.6 -20.5% 26.6 32.6 -18.4%

Ingot 15.3 16.1 -5.0% 27.6 32.1 -14.0%

Wafer -3 0.2 -1600.0% -3.1 0 -

Other 0.9 0.3 200.0% 2.1 0.5 320.0%

EBITDA 16.9 18.2 -7.1% 34.3 35.8 -4.2%

Operating Profit 9.9 14.8 -33.1% 21.1 29.1 -27.5%

Non-Operating Income 1.2 0.8 50.0% 3.8 0.8 375.0%

Non-Operating Expenses 1.4 1.4 0.0% 34.4 2.6 1223.1%

Interest Expenses 1.4 1.4 0.0% 2.4 2.5 -4.0%

EBiT 9.7 14.2 -31.7% 21.6 27.4 -21.2%

Net Profit 9.6 10.9 -11.9% 18.9 20.9 -9.6%

Condensed Income Statement

37.4

52.1

28.8

37.2

26.8

2.1

1.91.8

2.2

1Q 11 2Q 11 2Q 10

Ingot Wafer Orher

14.6% 12.3%

44.7%

• 2Q FY11 Sales : Decline German MKT Reduce PV support policy

• Despite of declined MKT, sales increased through capa expansion and wafer sales(YoY 143.8%)

• Operating profit : Polysilicon price up(1Q) / ASP down(1H)

• Net income totaled 9.6 billion won, improved by 3.2% QoQ and declined by -11.9% YoY.

17

Confidential. Not to be copied, reproduced or redistributed.

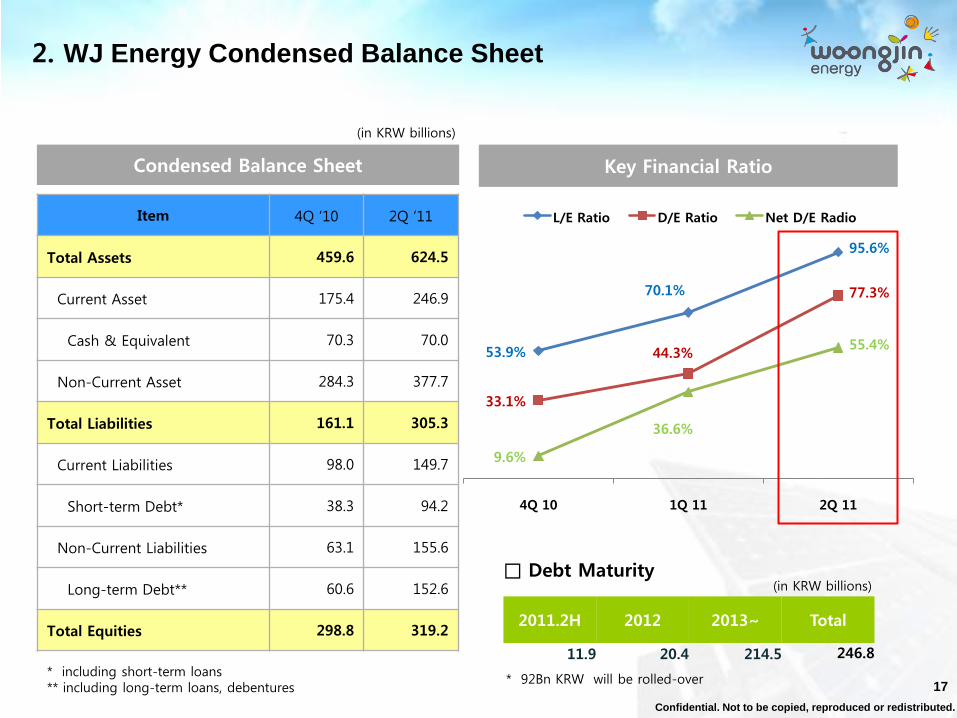

2. WJ Energy Condensed Balance Sheet

Item 4Q ‘10 2Q ‘11

Total Assets 459.6 624.5

Current Asset 175.4 246.9

Cash & Equivalent 70.3 70.0

Non-Current Asset 284.3 377.7

Total Liabilities 161.1 305.3

Current Liabilities 98.0 149.7

Short-term Debt* 38.3 94.2

Non-Current Liabilities 63.1 155.6

Long-term Debt** 60.6 152.6

Total Equities 298.8 319.2

Condensed Balance Sheet

(in KRW billions)

* including short-term loans ** including long-term loans, debentures

Key Financial Ratio

2011.2H 2012 2013~ Total

11.9 20.4 214.5 246.8

□ Debt Maturity(in KRW billions)

53.9%

70.1%

95.6%

33.1%

44.3%

77.3%

9.6%

36.6%

55.4%

4Q 10 1Q 11 2Q 11

L/E Ratio D/E Ratio Net D/E Radio

* 92Bn KRW will be rolled-over

18

Confidential. Not to be copied, reproduced or redistributed.

3. Performance & Forecast

Sales performance

(Unit : billion KRW)

2.8

67.7

118.9

160.3

441.4

FY 07 FY 08 FY 09 FY 10 FY 11(E)

Income performance

OP margin

NP marginOperating profit

Net profit

(Unit: billion KRW, %)

-88.2%

55.2%47.5%

36.9%

15.4%

-67.4%

49.9%34.5%

26.0%11.1%

-2.5

37.4

56.5 57.4

68.0

-1.9

33.841.0 44.3

49.2

FY 07 FY 08 FY 09 FY 10 FY 11(E)

• Sales increased rapidly with high profitability after the establishment

After establishment, Sales has greatly increased with a stable customer “SunPower”

Accomplished high productivity and competitive cost structure

• Aggressive expansion(Fab3) FY2015 1trillion sales(Global Top Tier)

CAGR : 254.3%

19

Confidential. Not to be copied, reproduced or redistributed.

Appendices

20

Confidential. Not to be copied, reproduced or redistributed.

Woongjin Food

Educationpublishing

Woongjin Mirae Mngt Academy

environmentmaterial

ConstructionsLeisure

Photovoltaic

Other

Listed

Woongjin Thinkbig

Woongjin CowayWoongjin Chemical

Kukdong Construction

Woongjin Ceramic

Woongjin Passone

Bookxen

Service/finance

Woongjin Poly Silicon

“Love and Love more”

• Established its first company Woongjin Think Big, an education & publishing company in 1980

• Based on the corporate philosophy of “Tto-tto Saran(Love and Love more)”

• Woongjin Group benefits from the synergies generated by 30 affiliates spread across a wide spectrum of industries

Appendix I : Overview of Woongjin Group

21

Confidential. Not to be copied, reproduced or redistributed.

Investment Asset Value Asset Portfolio

1,348.9

1,913.7

2,246.3 2,127.3

'08년말 '09년말 '10년말 '11년 1Q

(Unit: bil. KRW)

• Increase PV Biz(asset) value through continuous investment on WJ Energy & WJ Polysilicon

• Focus on PV Biz for new growth momentum

Appendix II : Focusing on PV Biz

* applying average stock price to listed subsidiaries and book value to unlisted subsidiaries

FY08A FY09A FY10A FY11 1Q

8.9% 9.5% 8.1% 6.8%

48.1% 48.9%39.3% 38.9%

9.5% 8.7%25.0% 25.3%

31.3% 31.3%26.7% 28.2%

2.1% 1.6% 0.9% 0.8%

FYO8A FY09A FY10A FY11 1Q

WJ Thinkbig WJ Coway WJE/WJP Kukdong Others

22

Confidential. Not to be copied, reproduced or redistributed.

'10년 '12년(E) '13년(E)

Capacity Expansion(E)

5,000

7,000

17,000

Period Total

Hyundai Heavy Indu. 5yr. $500mn

BYD (China) 3yr. $200mn

WoongjinEnergy 5yr. $300mn

Risun Solar (China) 5yr. $200mn

Exceeded 21%Q1 Target

(Unit : MT)

P1.5: +2,000

P2: +10,000

20%

32%

64%

77%

95%

1월 2월 3월 4월 5월(E)

(Unit : MT)

Operating Ratio

Sales Contract

Production Target & Shipment

Appendix III : Fast ramp-up of WJ Polysilicon

FY10A FY11(E) FY13(E)

Jan. Feb. Mar. Apr. May.

3,500

Q1 '11 Q4 '11

Production Target Shipment

• Producing over 9N grade polysilicon at 5,00MT/y capa, full ramp-up from 2Q 2011

23

Confidential. Not to be copied, reproduced or redistributed.

Listed Company

Non-Listed Company

WJ Coway

WJ Chemical

28.4%

45.2%

WJ Thinkbig

WJ Passone

32.4%

61.8%

66.5%

OPMS

WJ Foods

47.8%

WJ Energy

WJ Polysilicon

38.2%

50.8%

Kukdong E&C

94.7%

Rexfield C.C.

WJ Playdoci

43.2%

80.3%

Woongjin Holdings

Booxen

51.0%

Environment / MaterialEducation / Publishing OthersSolar Construction / Leisure

(As of March 31, 2011)

Holding

Co.IT / MRO

Appendix IV : WJ Group governance structure

24

Confidential. Not to be copied, reproduced or redistributed.

Fab 1 & 2 Fab 3(E)

Appendix IV : Facility Status

Location1316 KwanPyung-Dong,

Yuseong-Gu. Daejeon

AreaBuilding area : 13,992m2,

Total area : 36,527m2

ConstructionFab 1 : Mar. 2007

Fab 2 : Nov. 2009

Completion September 2010(Fab 1 & 2)

InvestmentFab 1 : 150 Bil. KRWFab 2 : 270 Bil. KRW

Production

capacity

Fab 1 2,000MT/yr.Fab 2 4,000MT/yr.

Location64-1 Tamnip-Dong,

Yuseong-Gu. Daejeon

AreaBuilding area : 19,507m2,

Total area : 33,059.m2

Construction October 2011

Completion December 2013

Investment 514.4 Bil. KRW

Production

capacity6,000MT/yr.

25

Confidential. Not to be copied, reproduced or redistributed.

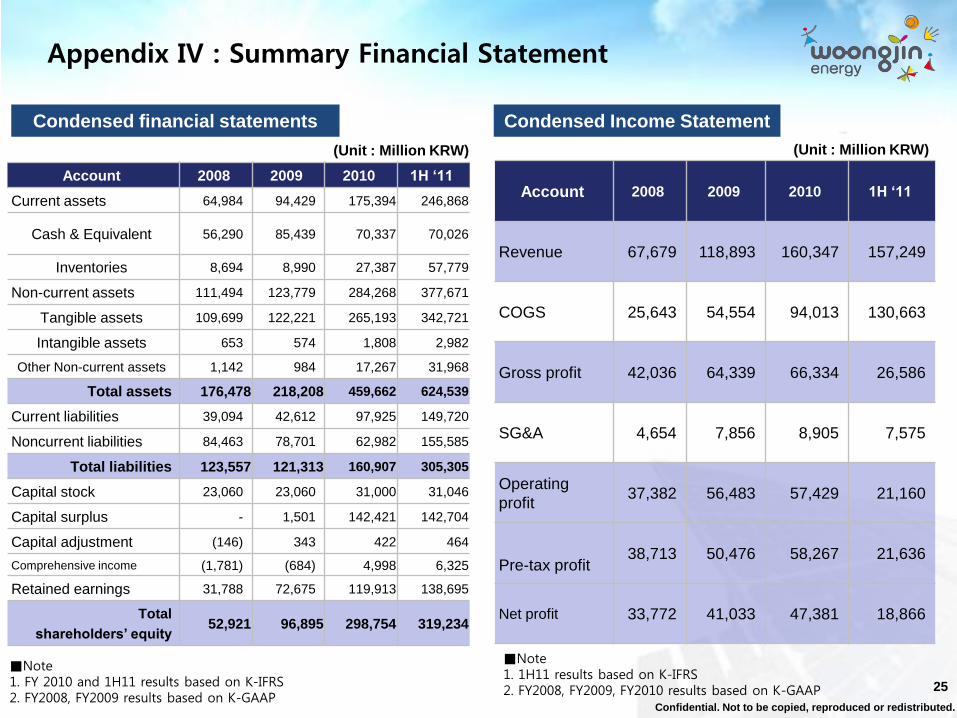

Appendix IV : Summary Financial Statement

Condensed financial statements

(Unit : Million KRW)

Condensed Income Statement

Account 2008 2009 2010 1H „11

Current assets 64,984 94,429 175,394 246,868

Cash & Equivalent 56,290 85,439 70,337 70,026

Inventories 8,694 8,990 27,387 57,779

Non-current assets 111,494 123,779 284,268 377,671

Tangible assets 109,699 122,221 265,193 342,721

Intangible assets 653 574 1,808 2,982

Other Non-current assets 1,142 984 17,267 31,968

Total assets 176,478 218,208 459,662 624,539

Current liabilities 39,094 42,612 97,925 149,720

Noncurrent liabilities 84,463 78,701 62,982 155,585

Total liabilities 123,557 121,313 160,907 305,305

Capital stock 23,060 23,060 31,000 31,046

Capital surplus - 1,501 142,421 142,704

Capital adjustment (146) 343 422 464

Comprehensive income (1,781) (684) 4,998 6,325

Retained earnings 31,788 72,675 119,913 138,695

Total

shareholders‟ equity52,921 96,895 298,754 319,234

Account 2008 2009 2010 1H „11

Revenue 67,679 118,893 160,347 157,249

COGS 25,643 54,554 94,013 130,663

Gross profit 42,036 64,339 66,334 26,586

SG&A 4,654 7,856 8,905 7,575

Operating

profit37,382 56,483 57,429 21,160

Pre-tax profit38,713 50,476 58,267 21,636

Net profit 33,772 41,033 47,381 18,866

(Unit : Million KRW)

■Note1. FY 2010 and 1H11 results based on K-IFRS2. FY2008, FY2009 results based on K-GAAP

■Note1. 1H11 results based on K-IFRS2. FY2008, FY2009, FY2010 results based on K-GAAP

26

Confidential. Not to be copied, reproduced or redistributed.

26

Confidential. Not to be copied, reproduced or redistributed.

Thank You