women and wealth: creating a strategy that works for you general financial strategies for women...

TRANSCRIPT

Women and Wealth:

Creating a Strategy That Works for You

General Financial Strategies for Women

Presented by: Natalie Lariccia and Katie Solvesky

Women control substantial wealth

Some economic factors about women: Women comprise 43% of top wealth

holders1

Women account for 37% of North American high-net-worth segment(more than $1 million in investable assets)2

1 Lisa Belkin, “The Power of the Purse,” The New York Times, August 2009.2 World Wealth Report 2011, Merrill Lynch Global Wealth Management and Capgemini, www.in.capgemini.com.

Women comprise almost half the work force

Some statistics about women in the workplace: Women comprise 46.7% of the total U.S.

labor force1

They account for 51.5% of persons employed in management/professional positions2

More than 8 million U.S. businesses are majority women-owned, with an economic impact of $3 trillion annually, translating into more than 23 million jobs3

Women receive more bachelor and advanced college degrees than men4

22% of married women earn more than their husbands5

1 Women’s Employment During the Recovery, U.S. Department of Labor, 2011, www.dol.gov.2 Bureau of Labor Statistics, “Employed persons by detailed occupation, sex, race, and Hispanic or Latino ethnicity,” 2010.3 The Economic Impact of Women-Owned Businesses in the United States, Center for Women’s Business Research, 2009.4 U.S. Census Bureau, Current Population Survey, 2010 Annual Social and Economic Supplement, April 2011.5 2010 Pew Research Center analysis of 1970 Decennial Census and 2007 American Community Survey.

Women influence most household financial decisions

1 Prudential Research Study, “Financial Experience & Behaviors Among Women, 2010–2011. 2 MSAO Strategic Insights and Intelligence team analysis of Spectrem Group’s 2008 Millionaire Investor survey data, August 25, 2008 . 3 MSAO Strategic Insights and Intelligence team analysis of Spectrem Group’s 2011 UHNW Investor and 2011 Millionaire Investor survey data, February 8, 2012.

Women are actively involved in household finances: 95% of women are financial decision makers and 84% of married women are either

solely or jointly responsible for household financial decisions1 Investment attitudes and behavior in a shared decision-making household tend to

resemble those of a female decision maker2 Women more readily recognize their Advisors’ worth and reward them with

loyalty3

Unique challenges

Women face unique challenges that can impact their ability to realize longer-term goals: Increased life expectancy/greater retirement needs1

Longer exposure to inflation/increasedhealth care costs

Long-term impact of time spent out of work force2

Earning 81.2% as much as men as a full-time worker3

1 U.S. Census Bureau, Life Expectancy by Sex, Age, and Race: 2008 (most recent statistics).2 The MetLife Study of Caregiving Costs to Working Caregivers: Double Jeopardy for Baby Boomers Caring for Their Parents, 2011.3 Bureau of Labor Statistics, Current Population Survey, “Median weekly earnings of full-time wage and salary workers by detailed occupation and sex, 2010,” April 2011.

75.580.5

Life Expectancy in Years1

Women Men

$.31

$.49

$.04

$.57

19601 2010

$2.73

$3.67

$.44

$1.37

20502

$7.33

$9.85

$1.18

$3.68

1 http://www.1960sflashback.com/1960/Economy.asp2 Assumed 2.5% Inflation Rate from 2010 through 2050

InflationA necessary planning factor

6

The top financial priorities identified by women are:1

Funding retirement Financial situation of children or

grandchildren Health, spouse’s health and becoming

a burden to family Adequate help to meet financial goals

Chief financial concerns

1 Wealthy Women Investors, Spectrem Group, 2011.

Hypothetical example for illustrative purposes only. Assumed minimum payment is calculated by using 2.5% of the balance

BudgetingDevelop a Budget and Stick to It

Create a budget to help plan for the long term

Become more aware of day-to-day cash flow and expenses

Pay down debt, especially high-interest debt

Consider health care and insurance options

Set up an emergency fund

High Interest Debt can be crippling

Paying the minimum balance on a $1,000 balance credit card with an 18% APR will take 153 months to pay off and you would have paid $1,115.41 in interest!

http://www.smartmoney.com/personal-finance/real-estate/to-rent-or-to-buy-9687/

Flexibility (can relocate easily) Can invest money elsewhere

(stock market) No upkeep fees

(drippy faucets, broken dishwashers, etc.)

No Equity Annual rent increase

could outpace inflation

BudgetingBuy or Rent?

Renting

Pros Cons

Tax-break: deduct mortgage interest and property taxes

Potential tax-free capital gain Emotional satisfaction

Property tax and upkeep Mortgage costs Less flexibility should you

want to move; in very bad housing markets, you could lose principal

Buying

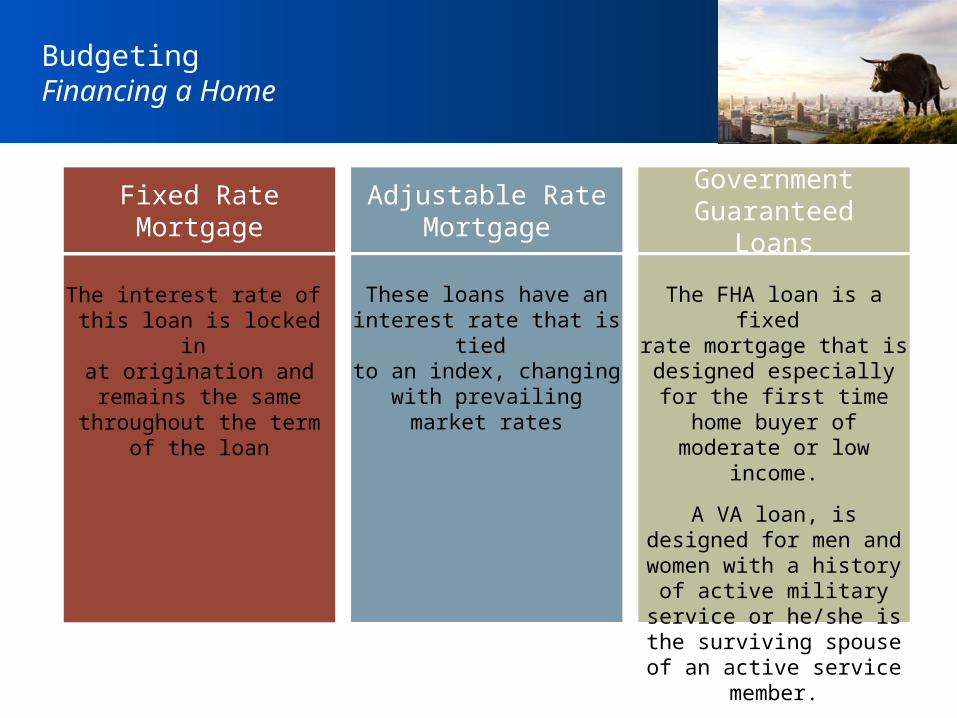

The interest rate of this loan is locked in

at origination and remains the same throughout the

term of the loan

These loans have an interest rate that is tied

to an index, changing with prevailing market rates

Adjustable Rate Mortgage

Fixed Rate Mortgage

BudgetingFinancing a Home

The FHA loan is a fixed rate mortgage that is

designed especially for the first time home buyer of moderate or low income.

A VA loan, is designed for men and women with a history of active military service or he/she is the surviving spouse of an active service member.

Government Guaranteed Loans

Investing

Taking control

Investors can take greater controlof their financial situation. Learn about investing Identify your financial goals

— Financial security of children/grandchildren

— Care of aging parents— Your own long-term care

Work with a Financial Advisor Monitor your portfolio Don’t procrastinate

A strategy defined by your goals

Your overall investment strategy depends on:

Your goals, timetable and tolerance for risk

A balance of stocks, bonds and cash

Monitoring and rebalancing your portfolio

??

? STOCKS

BONDS

CASH

Determining an appropriate asset allocation

20%

55%

25%40%

50%

10%

60%35%

5%

70%

25%

5%

80%

15%

5%

ConservativeModerately

Conservative ModerateModeratelyAggressive Aggressive

StocksBonds Cash

Merrill Lynch Asset Allocation Models

Source: Bank of America Merrill Lynch Research Investment Committee (RIC) Report, January 2011. Models are for illustrative purposes only. Merrill Lynch has changed the allocations for each model in the past and may change the allocations in the future, depending upon research and investment strategy recommendations.

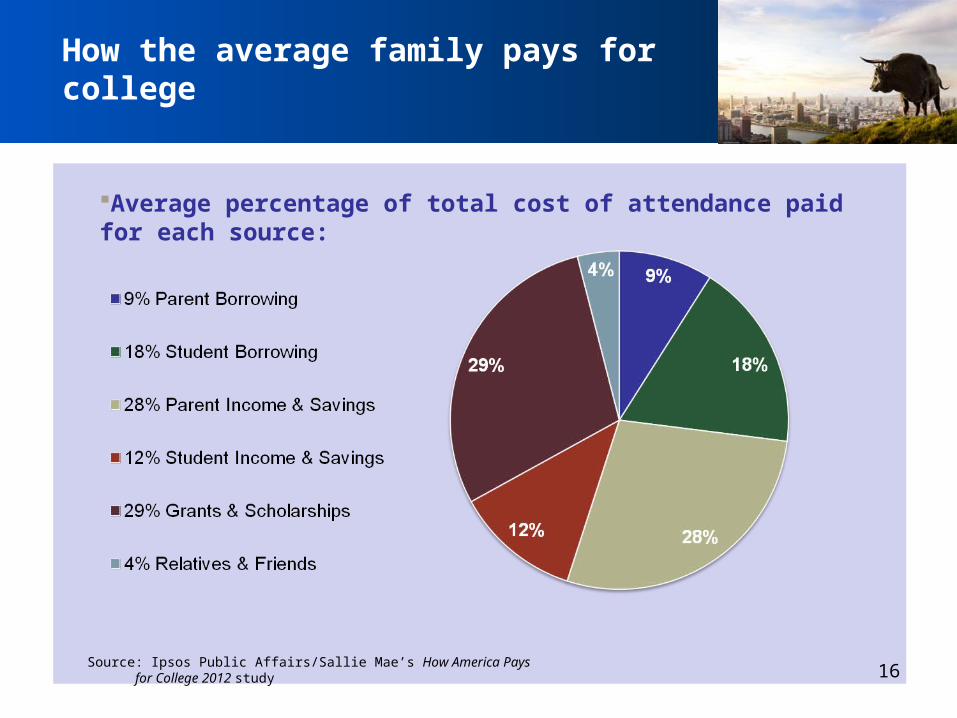

Education Planning

How the average family pays for college

Average percentage of total cost of attendance paid for each source:

Source: Ipsos Public Affairs/Sallie Mae’s How America Pays for College 2012 study16

Consider tax-efficient college planning options

Tax-advantaged college planning options

Section 529 college savings plans

Coverdell Education Savings Accounts

Uniform Gift/Transfer to Minors Act (UGMA/UTMA) custodial accounts

Please remember there's always the potential of losing money when you invest in securities.

Before you invest in a Section 529 plan, request the plan’s official statement from your Merrill Lynch Financial Advisor and read it carefully. The official statement contains more complete information, including investment objectives, charges, expenses and risks of investing in the plan, which you should carefully consider before investing. You should also consider whether your home state or your designated beneficiary’s home state offers any state tax or other benefits that are available only for investments in such state’s 529 plan. Section 529 plans are not guaranteed by any state or federal agency. 17

Retirement

16.5 to 1 3.3 to 1 2.3 to 1

"The 2009 Annual Report of the Board of Trustees of the Federal Old-Age and Survivors Insurance and Federal Disability Insurance Trust Funds," May 12, 2009.

2010 20251950

Not-so-good News: Social Security Is Threatened by an Aging Population

Ratio of Workers to Beneficiaries

Number of Defined Contribution PlansNumber of Defined Benefit Plans

Private Pension Plans, Participation, and Assets: Update(Data from tabulations of the U.S. Department of Labor's Form 5500)

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

1974 1986 19980

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

1974 1986 1998

Not Your Parent’s Retirement Plan

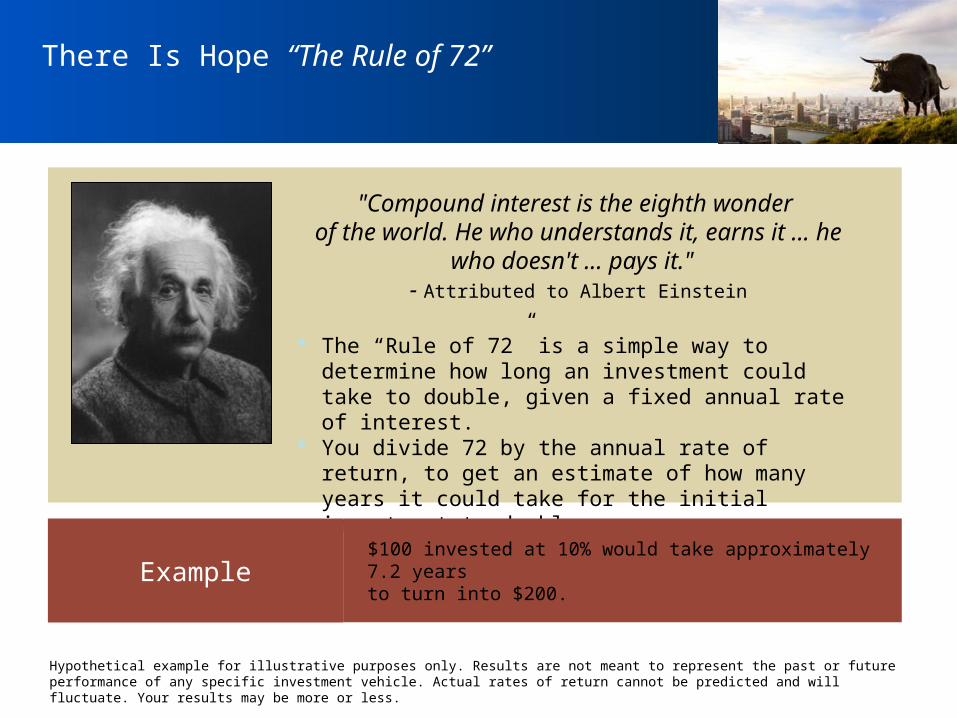

There Is Hope “The Rule of 72”

"Compound interest is the eighth wonder of the world. He who understands it, earns it ... he

who doesn't ... pays it." - Attributed to Albert Einstein

The “Rule of 72” is a simple way to determine how long an investment could take to double, given a fixed annual rate of interest.

You divide 72 by the annual rate of return, to get an estimate of how many years it could take for the initial investment to double.

Hypothetical example for illustrative purposes only. Results are not meant to represent the past or future performance of any specific investment vehicle. Actual rates of return cannot be predicted and will fluctuate. Your results may be more or less.

Example $100 invested at 10% would take approximately 7.2 years to turn into $200.

Start Saving As Soon As You Can

The sooner you start, the more money you could potentially have in retirement

This hypothetical illustration assumes an annual $5000 IRA contribution made at the beginning of each year for 35 years, a 7% annual rate of return, and no taxes on any earnings within the IRA. Hypothetical results are for illustrative purposes only and are not meant to represent the past or future performance of any specific investment vehicle. Investment return and principal value will fluctuate and when redeemed the investments may be worth more or less than their original cost.

(35 Years later)At Retirement

$5,000

$739,567

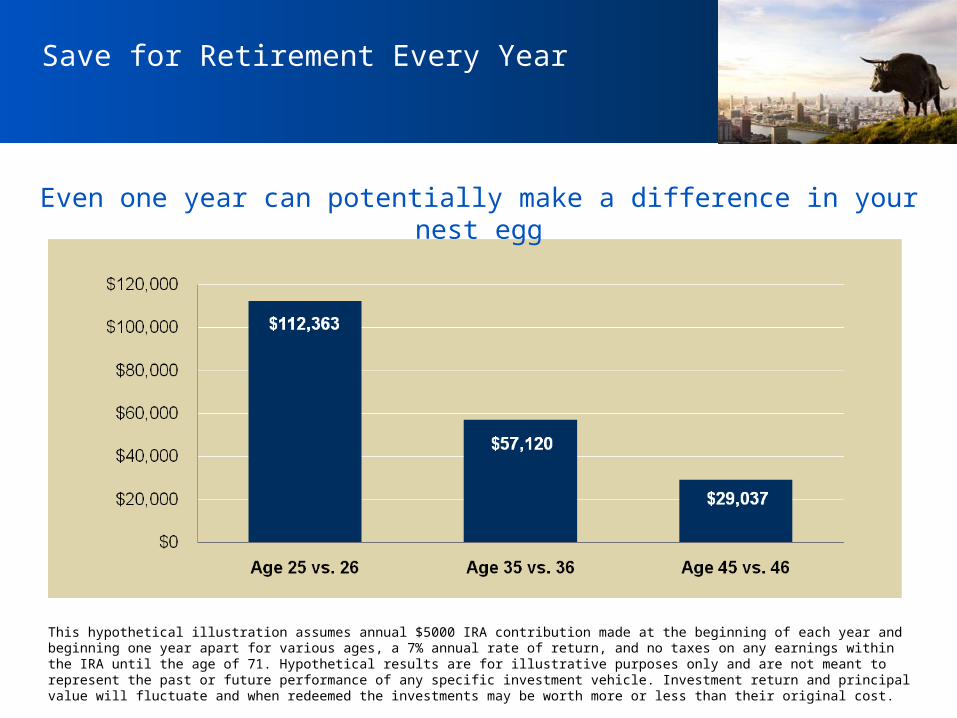

Save for Retirement Every Year

Even one year can potentially make a difference in your nest egg

This hypothetical illustration assumes annual $5000 IRA contribution made at the beginning of each year and beginning one year apart for various ages, a 7% annual rate of return, and no taxes on any earnings within the IRA until the age of 71. Hypothetical results are for illustrative purposes only and are not meant to represent the past or future performance of any specific investment vehicle. Investment return and principal value will fluctuate and when redeemed the investments may be worth more or less than their original cost.

Meet Your Company Match In 401(k) Plans

Many companies offer to match a percentage of employees’ 401(k) contributions

Investors should consider contributing at least as much as the company is willing to match

Don’t leave “free money” on the table by failing to contribute to your company’s 401(k)

¹ http://www.bls.gov/news.release/pdf/nlsoy.pdf, September 2010

The average person born in the latter years of the baby boom held

11 jobs from age 18 to age 441

Reasons to Invest EarlyImpacts on Your Paycheck

A pre-tax contribution to your retirement account reduces your take home pay less than the amount of your contribution.

Example

Mary is 35 and her annual salary is $50,000. She wants to contribute 5% of her salary to her 401(k) to take advantage of her company’s matching contributions and retire in 30 years.

Results- Mary’s monthly take-home pay would be reduced by: $156 - Her annual income tax bill would decrease by: $625 - With an employer match, at age 65 her account would

grow to: $395,291

This hypothetical illustration assumes a 5% contribution rate at the beginning of each year, a 6% annual rate of return, and a 25% federal tax bracket (state and local taxes are not included). It also assumes a company match of 100% for every dollar contributed up to 5% of eligible compensation. Hypothetical results are for illustrative purposes only and are not meant to represent the past or future performance of any specific investment vehicle. Investment return and principal value will fluctuate and when redeemed the investments may be worth more or less than their original cost. Taxes are due upon withdrawal. If you take a withdrawal prior to age 59½, you may also be subject to a 10% additional federal tax.

26

Risk in retirement

Types of risk to consider:

Market and sequence of returns Inflation Longevity/life expectancy Health care Asset allocation

27

Framework for building a retirement strategy

Different portfolios are designed to address separate needs:

A short-term portfolio is designed to supplement ongoing retirement income sources

An intermediate-term portfolio is designed to generate returns over a longer period of time, helping you keep pace with inflation and making it less likely you will outlive assets

A long-term portfolio is designed to fund wealth structuring goals

28

Managing your retirement assets

Remember to:

Review your portfolio annually or as needed

Consider whether rebalancing your portfolio is necessary

Continue to monitor your portfolio

Estate planning strategies

30

Getting in the know

Don’t rely on others to handle the details.

Review and understand your estate plan

Ask your own personal legal advisor about asset titling and beneficiary designations

Find out:— Are you a personal representative

(executor) and/or a trustee?

— Are you familiar with your parents’ estate plan?

31

Reasons to have an estate plan

Your entire estate is taxable.

IRA and 401(k) assets Life insurance proceeds Real property, bank accounts

Your beneficiaries need liquidity to pay:

Estate tax Administrative expenses Outstanding debt

Neither Merrill Lynch nor its Financial Advisors provide tax, accounting or legal advice. Clients should review any planned financial transactions or arrangements that may have tax, accounting or legal implications with their personal professional advisors.

Provides benefits while you are still alive, including during incapacitation, and after death

Allows limited probate proceedings for pour-over will

Applies to all assets titled in the name of the trust

Addresses lifetime management of assets

Requires grantor-appointed trustee

Provides for the distribution of assets after your death

Applies to assets owned in your name not otherwise the subject of beneficiary designations

Does not address lifetime planning, e.g., incapacity

Is subject to probate proceedings Requires court-appointed

personal representative

Distributing your assets per your wishes

Living TrustWill

33

Be prepared for your discussion

Before meeting with your own personal legal advisor:

Prepare a family tree Make a list of everything you own Think about whom you want to

designate as beneficiaries, personal representative and /or trustee of your plan

Consider what you want to leave to whom and in what form

Indicate which charitable organizations you wish to support

Putting it all together

Best Practices to Help You Plan for your Future

Save Every Year

Pay Down Debt

Monitor and Adjust Your Portfolio

Start Saving As Soon As You Can

Meet Your Company’s 401(k) Match

Create A Budget

What about your life?

36

Consider this:

Are you living for today, maintaining a long-term horizon, or both? Is your financial strategy a balance between lifetime financial needs and the

legacy you would like to leave? Are you familiar with your investment portfolio? Do you feel you have the

right mix of stocks, bonds and cash to help meet your investment needs? Have you determined your tolerance—both financial and emotional—for

investment risk? Have you worked to develop strategies to help meet your philanthropic goals? Do you have a will and/or trusts? If so, are they current?

The information in this presentation is intended to be a general introduction of Merrill Lynch’s approach to wealth management. It is not intended to be either a specific offer by any Merrill Lynch entity to sell or provide, or a specific invitation to apply for, any particular product or service.

Merrill Lynch offers a broad range of brokerage, investment advisory (including financial planning) and other services. There are important differences between brokerage and investment advisory services, including the type of advice and assistance provided, the fees charged, and the rights and obligations of the parties. It is important to understand the differences, particularly when determining which service or services to select.

Any information presented about tax considerations affecting client financial transactions or arrangements is not intended as tax advice and should not be relied upon for the purpose of avoiding any tax penalties. Neither Merrill Lynch nor its Financial Advisors provide tax, accounting or legal advice. Clients should review any planned financial transactions or arrangements that may have tax, accounting or legal implications with their personal professional advisors.

Asset allocation, diversification and rebalancing do not assure a profit or protect against a loss in declining markets.

Investments in foreign securities involve special risks, including foreign currency risk and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are magnified for investments made in emerging markets.

Merrill Lynch Wealth Management makes available products and services offered by Merrill Lynch, Pierce, Fenner & Smith Incorporated (MLPF&S) and other subsidiaries of Bank of America Corporation.

Banking products are provided by Bank of America, N.A., and affiliated banks, members Federal Deposit Insurance Corporation (FDIC) and wholly owned subsidiaries of Bank of America Corporation.

Investment products:

MLPF&S is a registered broker-dealer, member Securities Investor Protection Corporation (SIPC) and a wholly owned subsidiary of Bank of America Corporation.

Are Not FDIC Insured Are Not Bank Guaranteed May Lose Value