wolters kluwer 2005 half-year results

DESCRIPTION

TRANSCRIPT

1

3 August 2005 - Amsterdam

Q2/HY 2005 Results

Nancy McKinstry Chairman Executive Board/CEO

Boudewijn BeerkensMember Executive Board/CFO

3 August 2005 - AmsterdamQ2/HY 2005 Results 2

Agenda

Highlights

Key Performance Indicators

Divisional Operating Performance

Financial Performance

Outlook & Summary

Q&A

2

3 August 2005 - AmsterdamQ2/HY 2005 Results 3

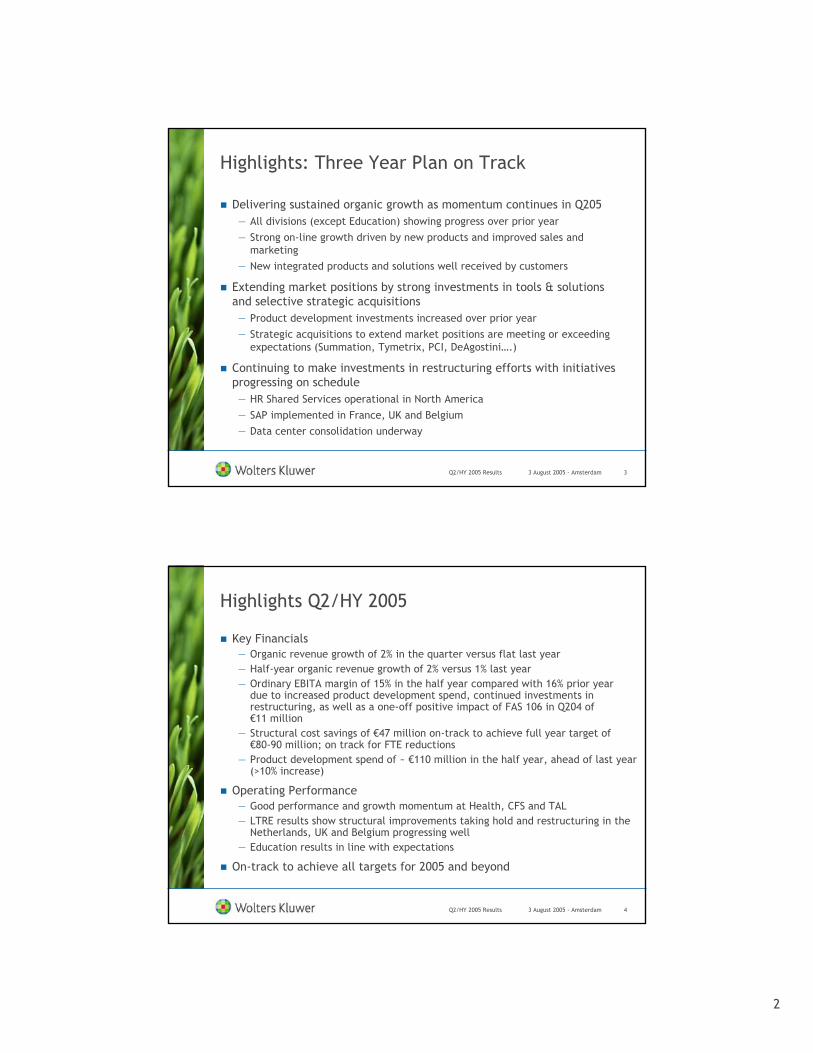

Highlights: Three Year Plan on Track

Delivering sustained organic growth as momentum continues in Q205— All divisions (except Education) showing progress over prior year

— Strong on-line growth driven by new products and improved sales and marketing

— New integrated products and solutions well received by customers

Extending market positions by strong investments in tools & solutions and selective strategic acquisitions— Product development investments increased over prior year

— Strategic acquisitions to extend market positions are meeting or exceeding expectations (Summation, Tymetrix, PCI, DeAgostini….)

Continuing to make investments in restructuring efforts with initiatives progressing on schedule— HR Shared Services operational in North America

— SAP implemented in France, UK and Belgium

— Data center consolidation underway

3 August 2005 - AmsterdamQ2/HY 2005 Results 4

Highlights Q2/HY 2005

Key Financials— Organic revenue growth of 2% in the quarter versus flat last year — Half-year organic revenue growth of 2% versus 1% last year— Ordinary EBITA margin of 15% in the half year compared with 16% prior year

due to increased product development spend, continued investments in restructuring, as well as a one-off positive impact of FAS 106 in Q204 of €11 million

— Structural cost savings of €47 million on-track to achieve full year target of €80-90 million; on track for FTE reductions

— Product development spend of ~ €110 million in the half year, ahead of last year (>10% increase)

Operating Performance— Good performance and growth momentum at Health, CFS and TAL — LTRE results show structural improvements taking hold and restructuring in the

Netherlands, UK and Belgium progressing well— Education results in line with expectations

On-track to achieve all targets for 2005 and beyond

3

3 August 2005 - AmsterdamQ2/HY 2005 Results 5

** After Tax *** Fully diluted

WACC is currently 8% after tax

Well On-Track to Achieve 2005 Guidance

€0.51

n/a

€182 mln

111%

16%

1%

HY04

€0.44

n/a

€23 mln

57%

15%

2%

HY05

€0.27

n/a

€11 mln

61%

17%

2%

Q205

€0.17

n/a

€12 mln

53%

14%

2%

Q105

€0.92-€1.01€1.02Ordinary EPS***

6-7%7%ROIC %**

≥ €250 mln€456 mlnOrdinary free cash flow

1-2%1%Organic revenue growth

15-16%16%Ordinary EBITA margin

95-105%

Target 2005*

126%Cash conversion

Key Financial Measures

2004Key Operational Measures

* At constant currencies EUR/USD 1.24

3 August 2005 - AmsterdamQ2/HY 2005 Results 6

(USD)(EUR)

(USD)(EUR)

16

3327

202160

Q205

20

3932

191158

Q204

0

0

Acquisition/Divestment

Change (million)

(5)

2

Total

(8)10Revenues

0(5)Ord. EBITA

Ord. EBITA margin%

CurrencyOrganicMillions

Health ResultsOrganic growth of 6% for the quarter and 4% for HY, on-track to achieve full year guidance of 3-5%

All customer units contributing to revenue growth, driven by:

— New product introductions— Strong online revenue growth (16%) — Good customer adoption of electronic drug

information/business intelligence tools

Margins impacted by investments in new products and FAS106 in Q204 ($ 4 mln)

Pharma Solutions

18%

Clinical Tools7%

Medical Research

45%

Professional & Education

30%

4

3 August 2005 - AmsterdamQ2/HY 2005 Results 7

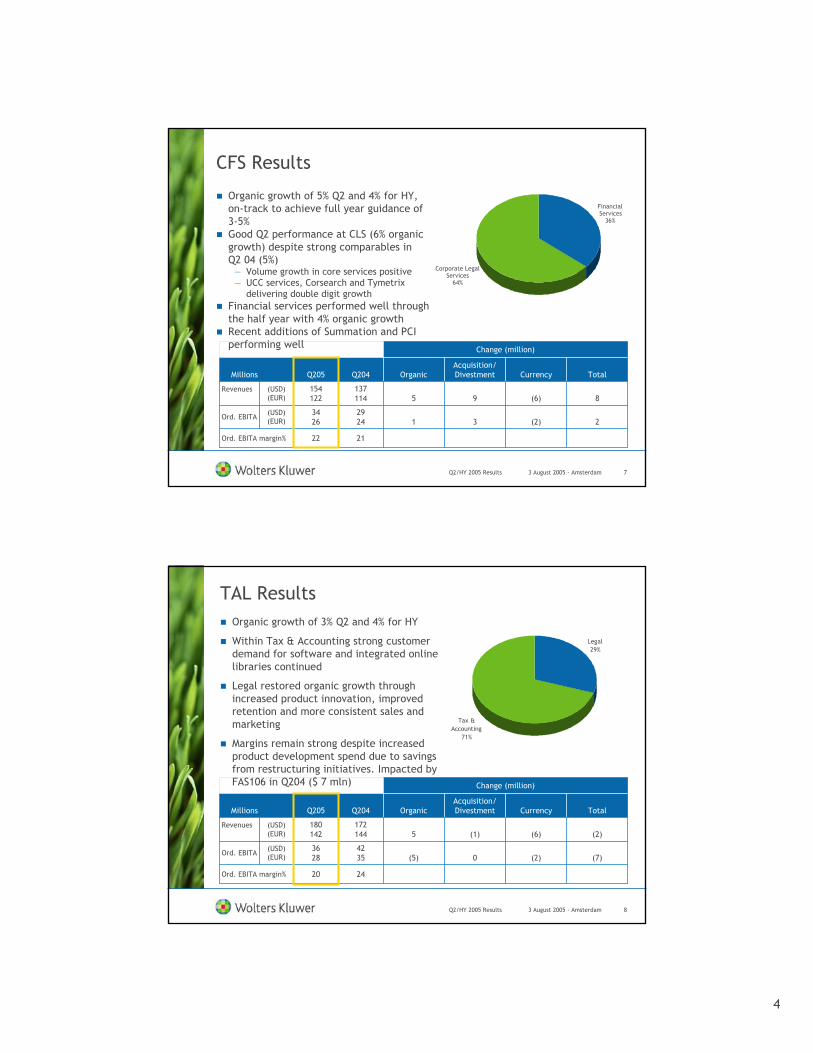

CFS Results

Financial Services

36%

Corporate Legal Services

64%

(USD)(EUR)

(USD)(EUR)

22

3426

154122

Q205

21

2924

137114

Q204

3

9

Acquisition/Divestment

Change (million)

2

8

Total

(6)5Revenues

(2)1Ord. EBITA

Ord. EBITA margin%

CurrencyOrganicMillions

Organic growth of 5% Q2 and 4% for HY, on-track to achieve full year guidance of 3-5%Good Q2 performance at CLS (6% organic growth) despite strong comparables in Q2 04 (5%)

— Volume growth in core services positive— UCC services, Corsearch and Tymetrix

delivering double digit growthFinancial services performed well through the half year with 4% organic growthRecent additions of Summation and PCI performing well

3 August 2005 - AmsterdamQ2/HY 2005 Results 8

TAL Results

Legal29%

Tax & Accounting

71%

(USD)(EUR)

(USD)(EUR)

20

3628

180142

Q205

24

4235

172144

Q204

0

(1)

Acquisition/Divestment

Change (million)

(7)

(2)

Total

(6)5Revenues

(2)(5)Ord. EBITA

Ord. EBITA margin%

CurrencyOrganicMillions

Organic growth of 3% Q2 and 4% for HY

Within Tax & Accounting strong customer demand for software and integrated online libraries continued

Legal restored organic growth through increased product innovation, improved retention and more consistent sales and marketing

Margins remain strong despite increased product development spend due to savings from restructuring initiatives. Impacted by FAS106 in Q204 ($ 7 mln)

5

3 August 2005 - AmsterdamQ2/HY 2005 Results 9

LTRE ResultsFlat organic growth; improvement on last year (-3%)

Growth momentum in Spain, France, Central Europe and Italy continued

Restructuring progressing well in the Netherlands, UK and Belgium

Continued strong on-line growth across the board

Plans fully in place to manage further pruning of products

FR18%

IT/SP19%

GER/CEE15%

TLR6%

BEL8%

UK13%

SC3%

NL18%

15

49

322

Q205

17

56

335

Q204

(1)

(10)

Acquisition/Divestment

Change (million)

(7)

(13)

Total

0(3)Revenues (EUR)

1(7)Ord. EBITA (EUR)

Ord. EBITA margin%

CurrencyOrganicMillions

3 August 2005 - AmsterdamQ2/HY 2005 Results 10

Education ResultsResults in line with expectations (1% organic growth for Q2; -1% for HY) and on track to achieve 1-2% organic growth for 2005

Performance Education second half weighted

Good HY performance in the Netherlands and Belgium; challenging markets remain in Sweden and Germany

Margins strong as 2004 restructuring yields savings

Other5%

Netherlands30%

Sweden34%

UK22%

Germany / Aus9%

25

21

88

Q205

24

21

87

Q204

0

0

Acquisition/Divestment

Change (million)

0

1

Total

01Revenues (EUR)

(1)1Ord. EBITA (EUR)

Ord. EBITA margin%

CurrencyOrganicMillions

6

3 August 2005 - AmsterdamQ2/HY 2005 Results 11

Supporting the integrated businesses

Off-shoring

Shared Services

Restructuring On-Track

Increased bandwidth with utilization of offshore IT and editorial resourcesExpansion of production and editorial center in Kuala Lumpur

SAP operational in France, UK and BelgiumHuman Resources shared services operational in NA

Business unitrestructuring

UK, Belgium and the Netherlands progressing well

Global contentPlatform

First release in August 2005

Data centerconsolidation

Operations and personnel transferred to outsource provider

3 August 2005 - AmsterdamQ2/HY 2005 Results 12

3 Year Strategy & Restructuring

± 800 (200 incr. spend over 3 yr period)

200+80

(CC = 265)

200+70

(CC = 255)

200+50

(AC = 220)

200Product development spend

± 215

103025-Non-exceptional restructuringcosts

-104496Exceptional restructuringcosts

100-110 (run-rate)

± 1800

Total

100-110

200

2006E

80-90

400

2005E

724521FTEreductions

7029Total cost savings

20042003EUR Million

AC = actual currenciesCC = constant currencies

7

3 August 2005 - AmsterdamQ2/HY 2005 Results 13

Impact of Restructuring

47

181

7

16

HY05

30

549

37

7

HY04

25

98

4

7

Q205

16

289

34

4

Q204

309253Non-exceptional restructuring costs

103443Exceptional restructuring costs

80-90

400

FY05E

22

83

Q105

724260FTE reductions

7014Total cost savings

FY04Q104EUR Million

3 August 2005 - Amsterdam

Financials

Boudewijn BeerkensMember Executive Board/CFO

8

3 August 2005 - AmsterdamQ2/HY 2005 Results 15

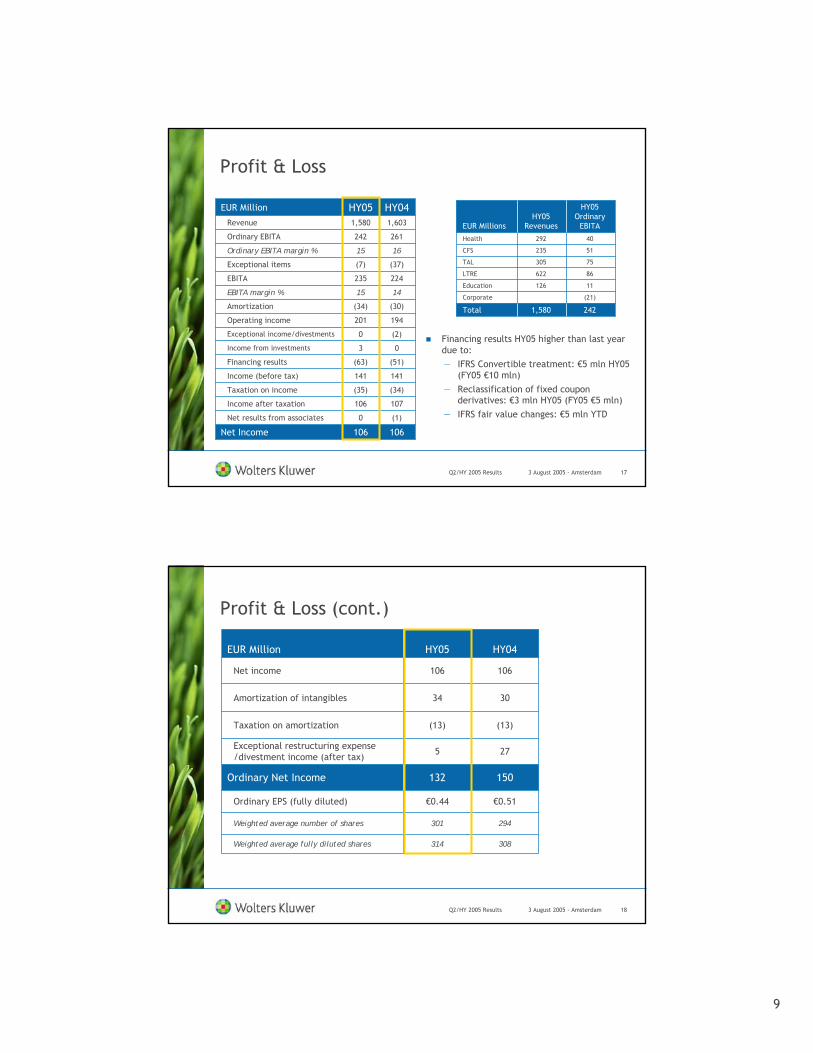

Financial Highlights

On-track to achieve FY KPI’s— Acceleration of organic revenue growth of 1% in HY04 to 2% in HY05

— Ordinary EBITA margin of 15% in the half year compared with 16% prior year due to increased product development spend, continued investments in restructuring, as well as a one-off positive impact of FAS 106 in Q204 of €11 million ($14 million)

— Increased restructuring expenditure (Shared services US, Fix and Transform and ETC in Europe) and increased product development spend (mainly CFS and Health)

Increased Financing costs due to IFRS

Net income in-line with last year at €106 million

Effective tax rate on pre-tax ordinary income of 28% is slightly below last year (28.5%)

Net debt increased with 4% to € 1.9 bln from € 1.8 bln due to acquisition spending

3 August 2005 - AmsterdamQ2/HY 2005 Results 16

Key Financials

(6)

2

Organic Growth

%

(6)

(5)

(5)

1

Constant Currencies

%

1415EBITA margin %

1615Ordinary EBITA margin %

(14)

(12)

(7)

(1)

Actual Currencies

%

1,6031,580Revenues

261242Ordinary EBITA

150132Ordinary Net Income

18223Free cash flow

€0.51€0.44Ordinary EPS (fully diluted)

HY04HY05EUR Million

9

3 August 2005 - AmsterdamQ2/HY 2005 Results 17

Profit & Loss

(2)0Exceptional income/divestments

(37)(7)Exceptional items

(30)(34)Amortization

1615Ordinary EBITA margin %

(1)0Net results from associates

107106Income after taxation

(34)(35)Taxation on income

141141Income (before tax)

(51)(63)Financing results

03Income from investments

194201Operating income

1415EBITA margin %

224235EBITA

1,6031,580Revenue

261242Ordinary EBITA

106106Net Income

HY04HY05EUR Million

(21)Corporate

2421,580Total

11126Education

86622LTRE

305

235

292

HY05Revenues

75

51

40

HY05Ordinary

EBITA

Health

CFS

TAL

EUR Millions

Financing results HY05 higher than last year due to:— IFRS Convertible treatment: €5 mln HY05

(FY05 €10 mln) — Reclassification of fixed coupon

derivatives: €3 mln HY05 (FY05 €5 mln) — IFRS fair value changes: €5 mln YTD

3 August 2005 - AmsterdamQ2/HY 2005 Results 18

Profit & Loss (cont.)

294301Weighted average number of shares

€0.51€0.44Ordinary EPS (fully diluted)

275Exceptional restructuring expense /divestment income (after tax)

(13)(13)Taxation on amortization

106106Net income

3034Amortization of intangibles

150132Ordinary Net Income

308314Weighted average fully diluted shares

HY04HY05EUR Million

10

3 August 2005 - AmsterdamQ2/HY 2005 Results 19

4632Deferred tax

3,0823,332Capital Employed

191200Provisions

2,0932,124Long-term liabilities

752976Group equity

(205)(480)Working capital

(1,934)(1,941)Total current liabilities

3,2873,812Total fixed assets

1,7291,461Total current assets

3,0823,332Total Financing

Dec 04June 05EUR Million

Consolidated Balance Sheet

Increase in fixed assets related to:

- Acquisitions (De Agostini, PCi, Nolis)

- Currency effect (stronger $)

Shareholders’ equity increase due to stronger US dollar and net income

3 August 2005 - AmsterdamQ2/HY 2005 Results 20

Cash Flow from Operating Activities

377Exceptional restructuring expense

20960Cash Flow from Operating Activities

315177Cash Flow from Operations

38Other

(28)(23)Appropriation of reorganizing provisions

(40)(38)Paid corporate income tax

(41)(64)Financing costs

4(109)Autonomous movements in working capital

194201Operating Income

8078Amortization & Depreciation

HY04HY05EUR Million Lower Cash flow from operations due to:

- increase in product development and restructuring spending

- increase of working capital including payments of royalties, profit sharing and bonuses

Financing costs higher due to interest payment on new € 700 m bond issued in 2003

11

3 August 2005 - AmsterdamQ2/HY 2005 Results 21

Cash Flow from Investments

-46Movement in bank overdrafts

-1Divestment of activities

-1Dividends received

(83)(18)Cash Flow Financing

(52)(288)Cash Flow Investments

20960Cash Flow from Operating Activities

(82)(69)Dividend payments

(1)(3)Movement in (long-term) loans

-8Exercise of stock options

-30Cash from derivatives

(25)(282)Acquisition spending

(27)(38)Capital expenditure fixed assets

HY04HY05EUR Million

Higher Capital expenditure due to IT spend in LTRE (UK - SAP) and US Shared Services (Perot transition)

Higher acquisition spending is mainly due to recent De Agostiniacquisition

Cash from derivatives: realized swap gains (FY 2005 will be € 100 m)

Dividend 2004 57% stock versus 49% over 2003

3 August 2005 - AmsterdamQ2/HY 2005 Results 22

0011Dividends received

404687Cash and cash equivalents as at January 1

18223Free Cash Flow

(27)(38)Capital expenditure fixed assets

20960Cash flow from operating activities

480447Cash and Cash Equivalents as at June 30

74(246)Net Cash Flow

26Exchange differences on cash equivalents

(83)(18)Cash flow financing

20960Cash flow from operating activities

(52)(288)Cash flow investments

HY04HY05EUR Million

Free Cash Flow

12

3 August 2005 - AmsterdamQ2/HY 2005 Results 23

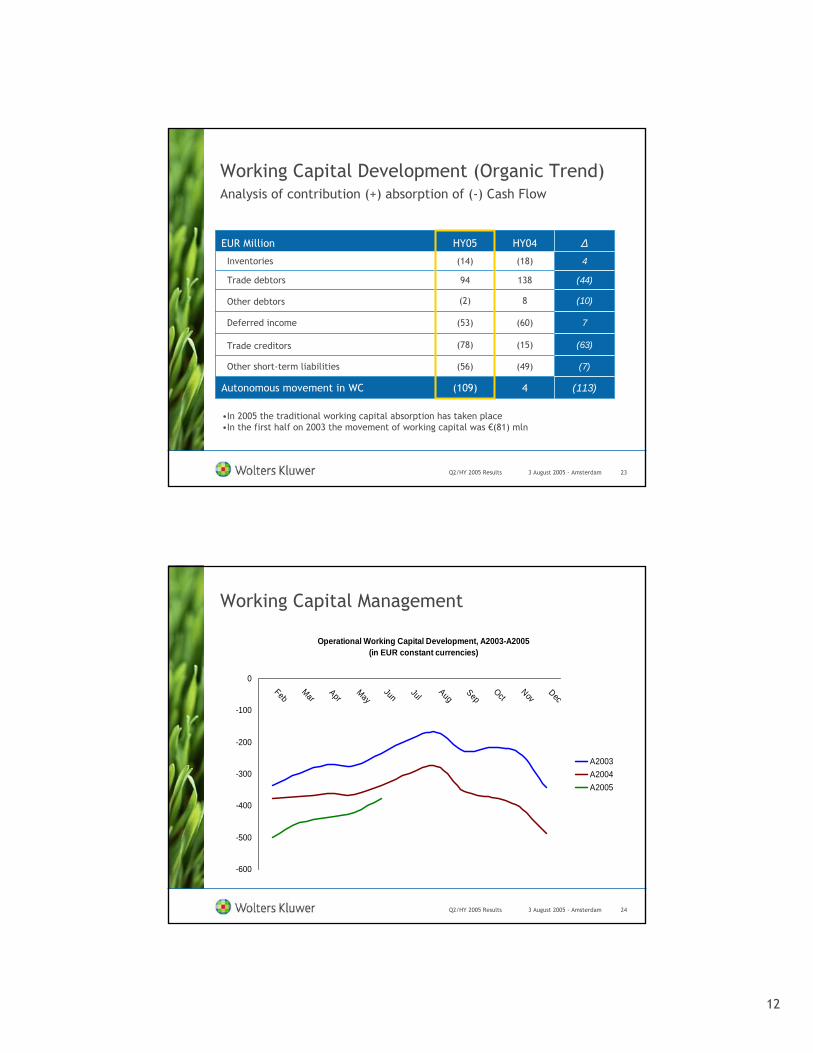

Working Capital Development (Organic Trend)

(113)

(7)

(63)

7

(10)

(44)

4

∆

(109)

(56)

(78)

(53)

(2)

94

(14)

HY05

(49)Other short-term liabilities

(15)Trade creditors

(60)Deferred income

4Autonomous movement in WC

8Other debtors

(18)Inventories

138Trade debtors

HY04EUR Million

Analysis of contribution (+) absorption of (-) Cash Flow

•In 2005 the traditional working capital absorption has taken place•In the first half on 2003 the movement of working capital was €(81) mln

3 August 2005 - AmsterdamQ2/HY 2005 Results 24

Operational Working Capital Development, A2003-A2005 (in EUR constant currencies)

-600

-500

-400

-300

-200

-100

0Feb

MarApr

MayJun Jul

AugSep

OctNov

Dec

A2003A2004A2005

Working Capital Management

13

3 August 2005 - AmsterdamQ2/HY 2005 Results 25

Acquisitions HY 2005

Acquisitions: Revenues

— De Agostini Professionale / UTET (Italy) - € 70 mln

— PCi (US) - $ 21 mln

— Nolis (France) - € 7 mln

— Eon (Romania) - € 1 mln

Total acquisition spending €282 million; including earn-outs of past deals

Total consideration on acquisitions was €295 million

All acquisitions are accretive to ordinary EPS in year 1 and cover their cost of capital within 3 to 5 years

3 August 2005 - AmsterdamQ2/HY 2005 Results 26

Summary

Supporting Operational Performance

Strong Financial Position

Facilitating growth opportunities

14

3 August 2005 - Amsterdam

Outlook

Nancy McKinstry Chairman Executive Board/CEO

3 August 2005 - AmsterdamQ2/HY 2005 Results 28

The Professional’s First Choice

Execute restructuring

Commitment to thoroughly know and understand our customers

Extend positions inhighest return markets

Deliver stronger growth

2005 Outlook: Growth Momentum Continues

Support the integrated businessShared services; Global Platform, SAP, Off-shoringData center consolidation

HealthCFSTax & Accounting

Continued investmentsNew productsStronger customer relationship

15

3 August 2005 - AmsterdamQ2/HY 2005 Results 29

2005 Outlook & Beyond: Reiterated

** After Tax *** Fully diluted

WACC is currently 8% after tax

€1.40-€1.50 €0.92-€1.01€1.02€1.18Ordinary EPS***

≥ WACC

≥ €300 mln

~ 100%

19-20%

4%

2007 Onwards*

95-105%126%109%Cash conversion

6-7%

≥ €250 mln

15-16%

1-2%

Target 2005*

1%-2%Organic Revenue growth

16%18%Ordinary EBITA margin

Key Financial Measures

7%7%ROIC %**

€456 mln€393 mlnOrdinary free cash flow

20042003Key Operational Measures

* At constant currencies EUR/USD 1.24

3 August 2005 - AmsterdamQ2/HY 2005 Results 30

Summary

Fulfilling the Promise to Be…

Momentum to deliver stronger and sustained growth

Restructuring progressing well with cost savings on target for full year

Customer adoption of online and integrated tools and solutions affirms core WK strategy

Three year strategy yielding results on all fronts

16

3 August 2005 - AmsterdamQ2/HY 2005 Results 31

The Professional’s First Choice

Provide information, tools and solutions to help professionals make their most critical decisions

effectively and improve their productivity

3 August 2005 - Amsterdam

Q2/HY 2005 Results

Nancy McKinstry Chairman Executive Board/CEO

Boudewijn BeerkensMember Executive Board/CFO