winning strategies 2014

TRANSCRIPT

A STUDY BYDEVELOPMENT COUNSELLORS INTERNATIONAL

IN ECONOMIC DEVELOPMENT MARKETING

A VIEW FROM CORPORATE AMERICA

WINNING STRATEGIES

2014

2

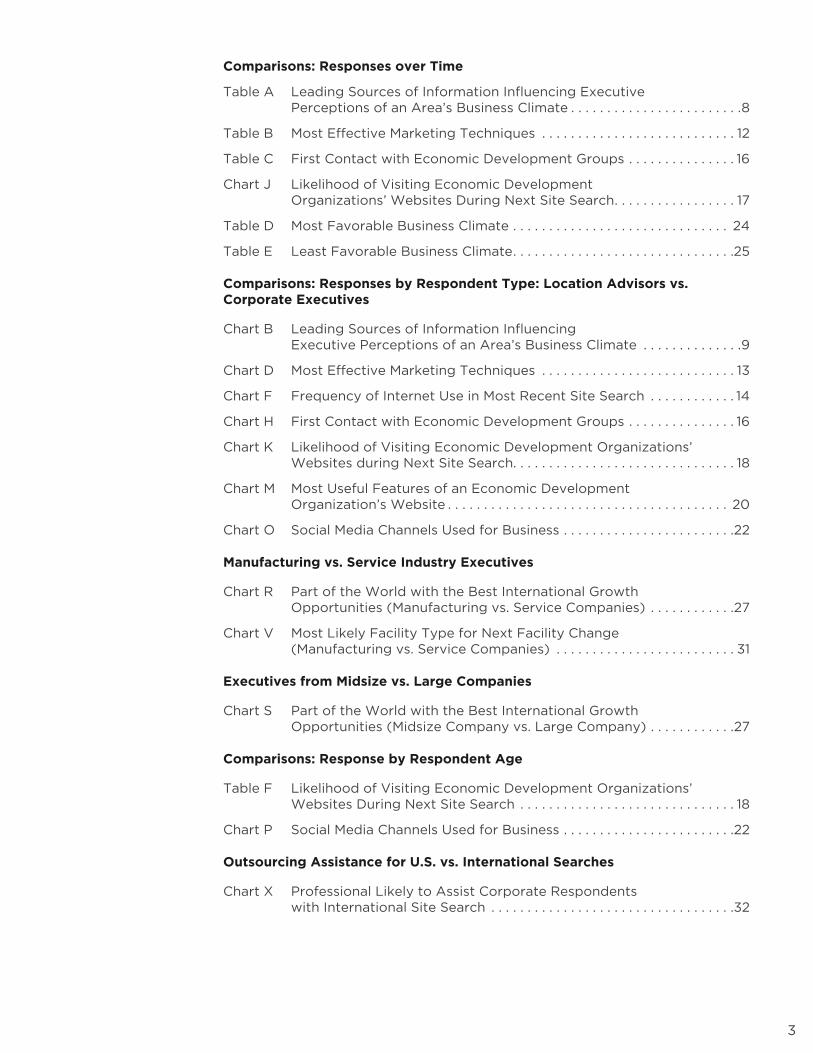

Table Of Contents

Index Of Charts And

Tables

Executive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4

Introduction and Methodology . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .6

Influencing Executive Perceptions: Leading Sources of Information . . . . . . . . . . .7

Best Marketing Techniques from the Customer’s Perspective . . . . . . . . . . . . . . . 11

The Web and Site Selection . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

First Contact: When Site Selectors Turn to Economic Development Groups . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Web Design: Important Information for Site Selectors . . . . . . . . . . . . . . . . . . . . . . 19

Social Media and Executive Decision Makers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Best and Worst Places for Business . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .23

The International Perspective . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

The Consultants Speak: Best Economic Development Groups . . . . . . . . . . . . . . 29

Looking Forward: Corporate Projected Location Decisions in 2014 and 2015 . . . . . . . . . . . . . . . . . 30

A Word About DCI . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

Appendix A: Questionnaire and Invitation to Participate . . . . . . . . . . . . . . . . . . . 34

Appendix B: Most Favorable Business Climate Rankings for All States . . . . . . 38

Appendix C: Least Favorable Business Climate Rankings for All States . . . . . . 39

Appendix D: Demographic Profile of Respondents . . . . . . . . . . . . . . . . . . . . . . . . 40

2014 Survey Results

Chart A Leading Sources of Information Influencing Executive Perceptions of an Area’s Business Climate . . . . . . . . . . . . . .7

Chart C Most Effective Marketing Techniques . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Chart E Frequency of Internet Use in Most Recent Site Location Search . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Chart G First Contact with Economic Development Groups . . . . . . . . . . . . . . . 15

Chart I Likelihood of Visiting Economic Development Organizations’ Websites During Next Site Search . . . . . . . . . . . . . . . . . 17

Chart L Most Useful Features of an Economic Development Organization’s Website . . . . . . . . . . . . . . . . . . . . . . . . . . 20

Chart N Social Media Channels Used for Business . . . . . . . . . . . . . . . . . . . . . . . . 21

Chart Q Part of the World with the Best International Growth Opportunities . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

Chart T Drivers for International Expansion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

Chart U Most Likely Facility Type for Next Facility Change . . . . . . . . . . . . . . . 30

Chart W Location Advisors: Most Common Type of Relocation Project . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

3

Comparisons: Responses over Time

Table A Leading Sources of Information Influencing Executive Perceptions of an Area’s Business Climate . . . . . . . . . . . . . . . . . . . . . . . .8

Table B Most Effective Marketing Techniques . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Table C First Contact with Economic Development Groups . . . . . . . . . . . . . . . 16

Chart J Likelihood of Visiting Economic Development Organizations’ Websites During Next Site Search . . . . . . . . . . . . . . . . . 17

Table D Most Favorable Business Climate . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

Table E Least Favorable Business Climate . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .25

Comparisons: Responses by Respondent Type: Location Advisors vs. Corporate Executives

Chart B Leading Sources of Information Influencing Executive Perceptions of an Area’s Business Climate . . . . . . . . . . . . . .9

Chart D Most Effective Marketing Techniques . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Chart F Frequency of Internet Use in Most Recent Site Search . . . . . . . . . . . . 14

Chart H First Contact with Economic Development Groups . . . . . . . . . . . . . . . 16

Chart K Likelihood of Visiting Economic Development Organizations’ Websites during Next Site Search . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

Chart M Most Useful Features of an Economic Development Organization’s Website . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

Chart O Social Media Channels Used for Business . . . . . . . . . . . . . . . . . . . . . . . .22

Manufacturing vs. Service Industry Executives

Chart R Part of the World with the Best International Growth Opportunities (Manufacturing vs. Service Companies) . . . . . . . . . . . .27

Chart V Most Likely Facility Type for Next Facility Change (Manufacturing vs. Service Companies) . . . . . . . . . . . . . . . . . . . . . . . . . 31

Executives from Midsize vs. Large Companies

Chart S Part of the World with the Best International Growth Opportunities (Midsize Company vs. Large Company) . . . . . . . . . . . .27

Comparisons: Response by Respondent Age

Table F Likelihood of Visiting Economic Development Organizations’ Websites During Next Site Search . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

Chart P Social Media Channels Used for Business . . . . . . . . . . . . . . . . . . . . . . . .22

Outsourcing Assistance for U.S. vs. International Searches

Chart X Professional Likely to Assist Corporate Respondents with International Site Search . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .32

4

In 1996, Development Counsellors

International set out to provide the economic

development community with a unique

opportunity: a chance to hear from its target

audience. With a comprehensive survey

of corporate executives with site selection

responsibilities, DCI sought to understand

best practices in marketing places by going

directly to the “customer” of the economic

development world.

Since its inception, A View from Corporate

America: Winning Strategies in Economic

Development Marketing has become a

valuable and highly regarded resource among

economic development professionals. Now in

its seventh iteration, Winning Strategies has

expanded upon its original form to include

questions on international business climates,

as well as to provide an updated snapshot of

corporate America in 2014.

Key findings, based on the aggregate

responses of 356 participants in the 2014

survey, follow.

Executive Summary

5

• The leading sources of information

influencing executive perceptions of

a community’s business climate were

dialogue with industry peers, articles in

newspapers and magazines and business

travel .

• Internet/website followed by planned

visits to corporate executives rate highest

among all economic development

marketing tools . Media relations/publicity,

hosting special events and trade shows

were also identified as effective techniques

for communicating with decision makers.

• For the fourth consecutive time,

corporate executives and their advisors

indicate that they contact economic

development groups most frequently

following the development of the shortlist

of communities to request specific

information or to arrange a site visit .

• Sixty-three percent of respondents

indicated a strong likelihood that they

would use an economic development

organization’s website in their next site

location search .

• Respondents named incentives information

as the most useful feature of an economic

development organization’s website,

followed by workforce statistics and

demographic information .

• Among respondents who use social media

for business, LinkedIn is the most dominant

communications channel, with 77% of

location advisors and 72% of corporate

executives indicating that they use the

platform for business.

• The Wall Street Journal, both print and

online, ranked as the top news sources

for the survey audience, followed by local

daily newspaper and The New York Times.

• Forbes’ rankings/surveys, followed by

those in Site Selection, received the

most attention among respondents who

look to rankings as a source of valuable

information about a location’s business

climate .

• When asked to select the most favorable

business climates among the 50 states,

respondents gave Texas, Florida, Georgia

and North Carolina the highest tally in that

order, with Georgia and North Carolina

tying for third place. South Carolina and

Tennessee also ranked in the top five.

• Forty-seven percent of location advisors

identified manufacturing/production plant

as the most common type of relocation

project they expect to see from their

clients in the year ahead .

• Forty percent of executives anticipate

outsourcing a portion of the site selection

responsibilities in their next site selection

search. Of these respondents, 53% say they

would hire a real estate broker to assist in

the site selection process.

The Asia/Pacific region was identified as the part of the world with the best opportunities for international growth, followed by Western Europe.

The new set of questions aimed at foreign

direct investment revealed the following:

• China, the United Kingdom and Germany

were identified as the countries with the

most to offer for companies interested in

international expansion.

• When asked to indicate the primary drivers

for their company’s potential international

expansion, respondents chose market

access as the primary driver, followed by

cost savings.

6

Introduction And

Methodology

It is important to note that this survey, and

all preceding Winning Strategies surveys,

are studies of perceptions. A perception

is an attitude, belief or impression and not

necessarily a reflection of reality. Business

executives have certain identifiable opinions

and beliefs about doing business in the

United States and throughout the world.

Some of these perceptions may be accurate

and some may be genuine misperceptions.

In 2014, Development Counsellors International

conducted a survey of corporate executives

with site selection responsibilities to determine

the “customer’s perspective” on the most

effective strategies and techniques in economic

development marketing. It was the seventh

iteration of this survey since 1996 to determine

changes in the perceptions of corporate

decision makers in the United States .

A total of 356 responses were received from corporate executives and location advisors – the largest number in the survey’s history.

The survey audience consisted of executives

at a random selection of U.S. companies with

direct site selection responsibilities and was

heavily weighted toward the following business

titles: Chief Executive Officer, President, Chief

Financial Officer and Vice President. The

sample was augmented with an additional

survey audience of more than 300 location

advisors/consultants .

Starting in 2008, the survey has been

conducted completely online. Respondents

were contacted via email and invited to

participate in the survey. A hyperlink to access

the online questionnaire was provided and the

choice of a $10 Starbucks card or a $10 iTunes

card was offered for participation. A copy of

the questionnaire and email invitation can be

found in Appendix A.

In all, 356 responses were received. Respon-

dents were categorized as large company

executives, midsize company executives and

location advisors. In some instances, respon-

dents are compared in two, rather than three

groups: corporate executives and location

advisors. For other questions, the data was split

between respondents in different age groups.

Demographic information about the respondent

pool can be found in Appendix D. All surveys

were edited for completeness and the responses

to open-ended questions were coded.

7

How can an economic development

organization best promote a favorable

reputation among executive decision makers?

In order to begin to answer this question,

we must ask another: What sources of

information do executive decision makers

look to in developing perceptions of a

location’s business climate?

Dialogue with industry peers and articles in newspapers and magazines were the top two influencers.

For the seventh time, the Winning Strategies

survey asked corporate decision makers

with site selection responsibilities a series of

questions in order to determine the leading

sources of information influencing executive

perceptions of an area’s business climate.

Respondents were asked to choose three

from 13 possible responses: advertising (a

category that, in the past, was split into two

categories: print advertising and TV/radio

advertising), articles in newspapers and

magazines, business travel, dialogue with

industry peers, direct mail, meetings with

economic development groups, rankings/

surveys (previously called national surveys),

online sources (added in 1999), personal

travel, social media, TV and radio newscasts/

shows, word of mouth and other .

Influencing Executive

Perceptions: Leading Sources

Of Information

Chart A: Leading Sources of Information Influencing Executive Perceptions of an Area’s Business Climate

Dialogue with industry peers

Articles in newspapers and magazine

Business travel

Meetings with economic development groups

Rankings/surveys

Online sources

Word of mouth

Personal travel

Other

TV and radio newscasts/shows

Advertising

Direct mail

Social media

55%

44%

37%

31%

24%

22%

21%

13%

12%

9%

4%

2%

2%

8

As illustrated in Table A, the top five

influencers have remained relatively stable

since the survey was first conducted in 1996.

The only difference from the 2011 data to

this year is that business travel and rankings/

surveys switched places, the former moving

from fifth to third and the later moving from

third to fifth on the list. Consistent with all

previous years, social media, direct mail and

advertising were selected by the fewest

number of executives as being one of the top

three sources of information influencing their

perceptions of an area’s business climate.

Table A: Leading Sources of Information Influencing Executive Perceptions of Business Climate

Sources 2014 2011 2008 2005 2002 1999 1996

Dialogue with industry peers 55% 50% 61% 54% 56% 71% 68%

Articles in newspapers and magazines 44% 46% 53% 45% 62% 61% 60%

Business travel 37% 27% 42% 45% 47% 45% 52%

Meetings with economic development orgs. 31% 28% 32% 33% 21% 27% 24%

Rankings/surveys 24% 36% 22% 17% 23% 31% 34%

Online sources 22% 20% 28% 22% 9% 9% --

Word of mouth 21% 19% 19% 16% 29% 21% 24%

Personal travel 13% 9% 14% 13% 14% 8% 21%

Other 12% 13% 10% 14% 14% 8% 15%

TV/radio newscasts/shows 9% 14% 7% 5% 14% 7% 4%

Advertising 4% 3% -- -- -- -- --

Direct mail 2% 0% 2% 2% 2% 3% 1%

Social media 2% 0% -- -- -- -- --

9

Leading Sources of Information: Corporate Executives vs. Location Advisors

Do the subgroups of our survey audience

get their information from different sources?

The following chart illustrates how corporate

executives versus location advisors rate the

top six information sources.

As Chart B shows, separating responses

according to the subgroups of the survey

reveals that corporate executives value

dialogue with industry peers as their leading

source of information on an area’s business

climate, whereas location advisors value

meetings with economic development groups

the most in this regard. Additionally, while

corporate executives and location advisors

both value dialogue with industry peers (59%

and 48%, respectively), corporate executives

value meetings with economic development

groups significantly less than do location

advisors (19% versus 52%).

Chart B: Leading Sources of Information Influencing Executive Perceptions of an Area’s Business Climate (Response based on Respondent Type)

Dialogue with industry peers

Articles in newspapers and magazines

Business travel

Meetings with economic development groups

Rankings/surveys

Online sources

CorporateExecutives

Location Advisors

59%

48%

45%

41%

40%

32%

19%

52%

24%

24%

24%

19%

10

Where Are Executives Getting Their News?

Learning the specific sources of news

consumed by business leaders can help

economic development groups to create

more effective marketing programs. For this

reason, we asked respondents who chose

articles in newspapers and magazines, online

sources, rankings/surveys and/or TV and

radio newscasts/shows to indicate specifically

the media in these categories they most

frequently pay attention to. While the results

for TV and radio newscasts/shows were not

statistically significant, the most frequently

cited sources were CNN and Fox News.

The Wall Street Journal, both print and online, tops the list of most influential news outlets.

The Wall Street Journal, once again, ranked at

the top of the newspapers and magazines list,

though the percentage of respondents who

chose the outlet fell from 82% in 2011 to 65%

in 2014. The complete list follows:

65% Wall Street Journal

30% Local Daily Newspaper

24% New York Times

20% The Economist

15% Forbes

7% USA Today

6% Bloomberg Businessweek

6% Financial Times

3% Fast Company

3% Site Selection

3% Fortune

3% Time

Respondents who chose online sources

indicated that WSJ .com is a go-to online

source for information on a location’s

business climate .

26% WSJ .com

17% Google.com

15% Economic Development Agency

Websites

13% Bloomberg .com

11% Bureau of Labor Statistics

11% CNN

11% NYTimes.com

11% Yahoo! Finance

Respondents who chose rankings/surveys

were asked to list the three sources for

surveys and rankings that they pay the most

attention to. The results are as follows:

26% Forbes

21% Site Selection Magazine

16% Area Development

14% Tax Foundation Business Tax

Climate Index

14% Wall Street Journal

5% Bloomberg

11

Best Marketing Techniques From

The Customer’s Perspective

Since 1996, the Winning Strategies

survey has asked respondents to rate

the effectiveness of seven conventional

marketing techniques used by economic

development groups. Respondents rated

each technique (advertising, direct mail,

Internet/website, media relations/publicity,

hosting special events, planned visits to

corporate executives, telemarketing and

trade shows) on a 1 to 5 scale, where 1 equals

“poor” and 5 equals “excellent.” The order in

the chart below is based on the percentage

of responses that were either a 4 or a 5.

Chart C: Most Effective Marketing Techniques (% Rating 4 or 5 on a 5-Point Scale)

Internet/website

Planned visits to corporate executives

Media relations/publicity

Hosting special events

Trade shows

Advertising

Direct mail

Telemarketing

67%

64%

48%

46%

38%

17%

14%

6%

12

Looking at responses over time in Table B,

we see the steady increase in perceptions of

Internet/website as an effective marketing

technique. In 2014, it took the number

one spot over planned visits to corporate

executives, which topped the list in 1996,

1999, 2002, 2005 and 2011.

Table B: Most Effective Marketing Techniques (% Rating 4 or 5 on a 5-Point Scale)

Technique 2014 2011 2008 2005 2002 1999 1996

Internet/website 67% 55% 56% 53% 34% 37% 18%

Planned visits to corporate executives

64% 57% 54% 55% 53% 46% 53%

Media relations/publicity 48% 33% 52% 50% 40% 38% 39%

Hosting special events 46% 35% 45% 49% 37% 42% 39%

Trade shows* 38% 35% -- 33% 32% 45% 39%

Advertising 17% 16% 15% 20% 21% 19% 19%

Direct mail 14% 15% 19% 23% 33% 25% 25%

Telemarketing 6% 4% 4% 6% 4% 6% 7%

*Trade shows was inadvertently excluded in the 2008 survey.

Separating responses according to the

three subgroups of the survey pool (large

company, midsize company and location

advisors) reveals that executives from

midsize companies (71%) find Internet/

website to be the most effective marketing

technique for economic development groups,

whereas location advisors select planned

visits to corporate executives (81%). Large

company executives are relatively split

between these two, with a slight preference

for Internet/website (57% vs. 56%). Media

relations/publicity and hosting special events

were also frequently given a 4 or a 5 by

location advisors .

The “customer” agrees: the Internet has become an increasingly effective marketing tool for economic development organizations.

13

Chart D: Most Effective Marketing Techniques (% Rating 4 or 5 on a 5-Point Scale) (Response based on Respondent Type)

Advertising

Direct mail

Internet/website

Media relations/publicity

Hosting special events

Planned visits to corporate executives

Trade shows

Telemarketing

24%

71%

37%

30%

50%

9%

42%

13%

57%

39%

30%

56%

2%

43%

12%

15%

4%

20%

65%

62%

72%

81%

5%

28%

Location Advisor

Large Company

Midsize Company

14

The Web And Site

Selection

As indicated by the 2011 data and further

reinforced by this year’s findings, the Internet

has become an instrumental part of the site

selection process. When asked to indicate,

on a scale of 1 to 5, where 1 is Not at all and 5

is Often, how often they used the Internet in

their last site search, 66% of the executives

responded with a 4 or 5—an increase of 18%

since 2011. The following chart shows the

distribution of responses.

Chart E: Frequency of Internet Use in Most Recent Site Location Search

Not at all Often

Not at all Often

Not at all Often

1 52 3 4

14%7% 12% 20% 46%

1 52 3 4

12%4% 14% 15% 56%

71%

1 52 3 4

17%10% 11% 23% 39%

62%

Just as was indicated by 2011 data, location

advisors use the Internet in their site

selection search slightly more than do

corporate executives. Approximately 56%

of location advisors selected the highest

ranking of 5 when responding to this

question versus 39% of corporate executives.

Overall, both groups use the Internet in the

site selection process relatively frequently,

with 71% of location advisors and 62% of

corporate executives selecting either a 4 or a

5 in response to this question.

Chart F: Frequency of Internet Use in Most Recent Site Location SearchNot at all Often

Not at all Often

Not at all Often

1 52 3 4

14%7% 12% 20% 46%

1 52 3 4

12%4% 14% 15% 56%

71%

1 52 3 4

17%10% 11% 23% 39%

62%

All

Location Advisors

Corporate Executives

Corporate executive use of the Internet for site searches jumped by 18% since 2011.

15

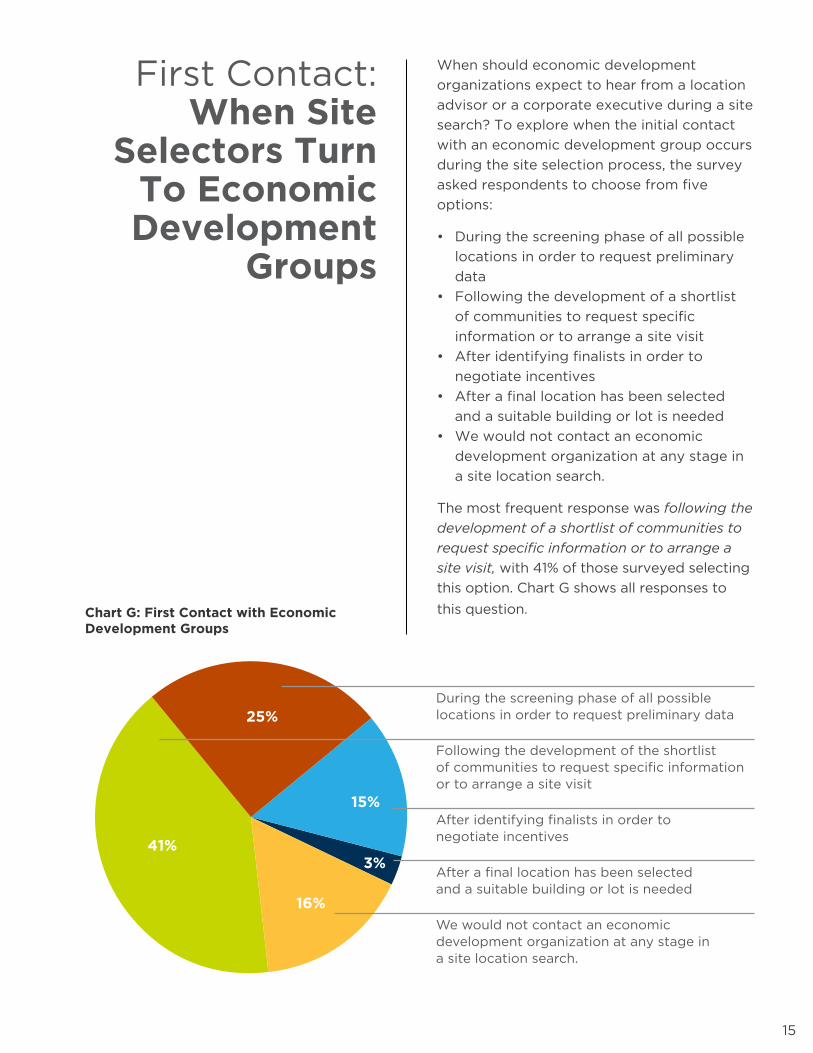

First Contact:When Site

Selectors Turn To Economic Development

Groups

When should economic development

organizations expect to hear from a location

advisor or a corporate executive during a site

search? To explore when the initial contact

with an economic development group occurs

during the site selection process, the survey

asked respondents to choose from five

options:

• During the screening phase of all possible

locations in order to request preliminary

data

• Following the development of a shortlist

of communities to request specific

information or to arrange a site visit

• After identifying finalists in order to

negotiate incentives

• After a final location has been selected

and a suitable building or lot is needed

• We would not contact an economic

development organization at any stage in

a site location search .

The most frequent response was following the

development of a shortlist of communities to

request specific information or to arrange a

site visit, with 41% of those surveyed selecting

this option. Chart G shows all responses to

this question .

During the screening phase of all possible locations in order to request preliminary data

Following the development of the shortlist of communities to request specific information or to arrange a site visit

After identifying finalists in order to negotiate incentives

After a final location has been selected and a suitable building or lot is needed

We would not contact an economic development organization at any stage in a site location search.

25%

41%

16%

15%

3%

Chart G: First Contact with Economic Development Groups

16

For the fourth consecutive time, responses

indicate that location advisors and corporate

executives are most likely to contact

economic development organizations for

the first time following the development

of a shortlist in order to request specific

information or to arrange a visit . Based on

the data in Table C, corporate executives and

their advisors continue to contact economic

development organizations later in the site

selection process or in some cases not at all.

The percentage of respondents who would

not contact an economic development

organization doubled from 2008 to 2011, and

remained stable in 2014.

Table C: First Contact with Economic Development Groups (Response over Time)

Timing of First Contact

2014 2011 2008 2005

During the screen-ing phase of all possible locations in order to request preliminary data

25% 24% 29% 27%

Following the development of the shortlist of com-munities to request specific information or to arrange a site visit

41% 40% 40% 48%

After identifying finalists in order to negotiate incentives

15% 13% 18% 15%

After a final location has been selected and a suitable building or lot is needed

3% 6% 5% 2%

We would not con-tact an economic development organization at any stage in a site location search .

16% 17% 8% 8%

Economic development groups continue to play an important role after a shortlist has been developed.

Consistent with findings of previous years,

location advisors are more likely to utilize

the services of an economic development

organization (none indicated they would

not contact an economic development

organization at any stage), and are more

likely to contact an organization earlier in the

site selection process.

Chart H: First Contact with Economic Development Groups (Response based on Respondent Type)

During the screening phase

Following the development of the shortlist

After identifying finalists

After a final location has been selected

We would not contact an economic development organization at any stage

CorporateExecutives

Location Advisors

24%

27%

31%

64%

17%

9%

5%

0%

23%

0%

17

Often, an executive’s first contact with an

economic development organization is

through the organization’s website. Regarding

the likelihood of visiting an economic

development organization’s website during

their next site location search, 63% of

respondents indicated a 4 or 5 on a scale of

1 to 5, where 1 is Low and 5 is High . Chart I

shows the distribution of all responses.

Chart J shows the change over time since

the question was first asked in 2002. The

percentage of executives planning to visit

an economic development organization’s

website in their next location search dipped

from 64% in 2008 to 47% in 2011 and rose

again to 63% in 2014.

The use of economic development websites by corporate executives in a site search jumped back up to 63% in the 2014 survey.

Not at all Often1 52 3 4

9%12% 16% 23% 40%

39%

2002

65%

2005

64%

2008

47%

2011

63%

2014

Chart J: Likelihood of Visiting Economic Development Organizations’ Websites During Next Site Search (% Rating 4 or 5 on a 5-Point Scale) (Response over Time)

Chart I: Likelihood of Visiting Economic Development Organizations’ Websites During Next Site Search

18

As Chart K shows, location advisors are more

likely to visit an economic development

organization’s website than the corporate

respondents.

Age does not appear to be a significant

factor in the likelihood of visiting an

economic development organization’s

website during a site location search.

In a counter-intuitive finding, the ends of the

age spectrum — executives 39 and younger

and executives 60 and older — are more

likely to visit an economic development

website than executives in the 40-49 and

50-59 age range.

Chart K: Likelihood of Visiting Economic Development Organizations’ Websites During Next Site Search (Distribution of Responses on a 1-5 Scale) (Response based on Respondent Type)

53%

Not at all Often

Not at all Often

1 52 3 4

11%19% 17% 28% 25%

1 52 3 4

8%1% 15% 17% 62%

79%

Table F: Likelihood of Visiting Economic Development Organizations’ Websites During Next Site Search (Distribution of Responses on a 1-5 Scale) (Response based on Respondent Age)

Under 39 years 40 - 49 50 - 59 Over 60 years

1 4% 16% 11% 14%

2 4% 8% 11% 7%

3 27% 18% 19% 9%

4 27% 28% 21% 26%

5 38% 30% 38% 44%

“4” or “5” 65% 58% 59% 70%

CorporateExecutives

LocationAdvisors

19

Website Design: Important

Information For Site Selectors

How can economic development organization

websites be more effective in supplying

relevant information to location advisors and

corporate executives? In order to get the

answer to this question, we asked respondents

to indicate which features are most important

to the usefulness of an economic development

organization’s website. The survey presented

14 features that are commonly included in

the design of an economic development

organization’s website:

• Comparisons to competitor locations (e.g.

cost comparisons)

• Searchable database of available buildings

and sites

• Demographic information (e.g. population,

income, age distribution, educational

attainment)

• Incentives information

• Major employer list

• Educational institution information (K-12

and post-secondary)

• Maps of the community

• Current press releases/announcements

• Quality of life information (e.g. cost of

living, cultural/recreational opportunities)

• Target industries and related information

• Testimonials from local companies

• Video content

• Workforce statistics (e.g. labor force,

employment by industry/occupation)

• Staff contact information

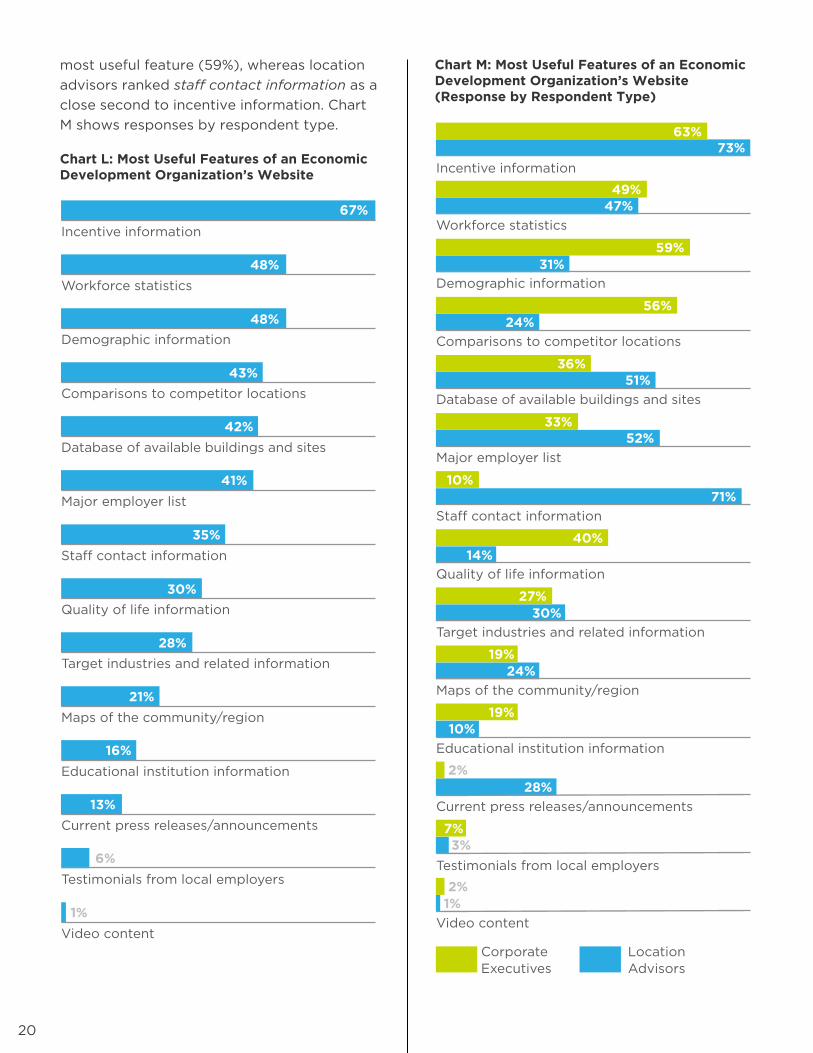

Incentives information was selected by 67%

of respondents, workforce statistics by 48%

and demographic information by 46%. The

responses remained remarkably consistent

with results from past years. Chart L on page

20 shows all responses.

Comparing the survey’s subgroups shows

that both location advisors (73%) and

corporate executives (63%) find incentive

information to be the most useful feature of

an economic development organization’s

website. Corporate executives find

demographic information to be the second

20

most useful feature (59%), whereas location

advisors ranked staff contact information as a

close second to incentive information . Chart

M shows responses by respondent type.

Chart L: Most Useful Features of an Economic Development Organization’s Website

Incentive information

Workforce statistics

Demographic information

Comparisons to competitor locations

Database of available buildings and sites

Major employer list

Staff contact information

Quality of life information

Target industries and related information

Maps of the community/region

Educational institution information

Current press releases/announcements

Testimonials from local employers

Video content

67%

48%

48%

43%

42%

41%

35%

30%

28%

21%

16%

13%

6%

1%

Chart M: Most Useful Features of an Economic Development Organization’s Website (Response by Respondent Type)

Incentive information

Workforce statistics

Demographic information

Comparisons to competitor locations

Database of available buildings and sites

Major employer list

Staff contact information

Quality of life information

Target industries and related information

Maps of the community/region

Educational institution information

Current press releases/announcements

Testimonials from local employers

Video content

CorporateExecutives

Location Advisors

73%

47%

31%

24%

51%

52%

71%

14%

30%

24%

10%

28%

3%

1%

63%

49%

59%

56%

36%

33%

10%

40%

27%

19%

19%

2%

7%

2%

21

Social Media And Executive

Decision Makers

For the second time, Winning Strategies

asked location advisors and corporate

executives which social media channels they

currently use for business purposes. The

survey presented seven options: blog forums,

Facebook, LinkedIn, Twitter, YouTube, other

social media channels and I do NOT use social

media for business. Respondents were asked

to check all that apply. Just as 2011 data

revealed, LinkedIn is the most widely used

social media outlet for business, with 74% of

all respondents selecting this option. Chart N

shows the full distribution of responses.

Chart N: Social Media Channels Used for Business

Blog forums

I do NOT use social media for business purposes

YouTube

Other

74%

24%

23%

22%

21%

17%

2%

The percentage of executives who do not

use social media for business (21%) has

decreased since 2011, when 38% indicated

that this option was true. Additionally,

corporate executives indicated using all

social media platforms for business—except

LinkedIn—more than or equal to location

22

advisors. Twitter and Facebook traded

places in 2014 versus 2011. Chart O shows all

responses by subgroup.

Chart O: Social Media Channels Used for Business (Response based on Respondent Type)

Blog forums

I do NOT use social media for business purposes

YouTube

Other

CorporateExecutives

Location Advisors

72%

77%

24%

24%

26%

17%

28%

11%

21%

20%

20%

9%

4%

0%

When comparing the use of social media

for business purposes among different age

groups, several patterns emerge. Since

2011, 30-somethings have increased their

use of Facebook for business purposes,

while 40-somethings have increased their

use of Twitter. Among all age groups, the

percentage of people who do not use social

media for business purposes has decreased,

whereas the use of LinkedIn has increased.

Chart P: Social Media Channels Used for Business (Response based on Respondent Age)

Blog forums

YouTube

Other

I do NOT use social media for business purposes

Under 39 40-49

50-59 60 and over

78%

61%

88%

74%

31%

13%

63%

24%

24%

22%

25%

29%

26%

4%

25%

34%

21%

17%

25%

24%

2%

0%

0%

11%

19%

35%

0%

18%

23

Best And Worst Places For

Business

DCI’s research on which states are winning

the “perception” contest has consistently

received intense attention from both the

news media and the economic development

community .

This year, in order to broaden the scope

of our study, we also gauged executives’

perceptions of non-U.S. locations as

candidates for their company’s potential

international expansion.

To determine U.S. state rankings, we asked

survey respondents to name three states

perceived as having the most favorable

business climates in the United States . We

also asked the same audience to select the

three states they perceive as having the

least favorable business climates among the

50 states.

Tax climate, pro-business environment and incentives are among those factors associated with winning states.

Overall, in the state rankings, respondents

selected Texas (49.7%) as having the most

favorable business climate, followed by

Florida (18.1%), Georgia and North Carolina

(17.6%), which tied for third place, South

Carolina (12.6%) and Tennessee (11.6%).

The top five responses are:

1 . Texas 49.7%

2 . Florida 18.1%

3 .Georgia

North Carolina17.6%

4 . South Carolina 12.6%

5 . Tennessee 11.6%

Why did the respondents select these states?

What qualities are associated with a winning

business climate? We asked respondents to

tell us in an open-ended question.

TIE

24

Among those who named Texas as having

a favorable business climate, the factors

mentioned most frequently were tax climate

(54%), pro-business environment (47%) and

incentives/financial assistance (18%).

Those who named Florida as having a

favorable business climate also frequently

mentioned tax climate (47%) and pro-

business environment (33%) as factors in

their positive perception of the state.

Since DCI began conducting this survey in 1996, the states in the top five have been relatively stable.

Those who named Georgia pointed to its

pro-business environment (34%), incentives

(31%) and workforce quality and availability

(31%) as indicators of its favorable business

climate. North Carolina was noted for its

pro-business environment (31%), workforce

quality and availability (31%) and its low

overall operating costs (25%).

Since DCI began conducting this survey in

1996, the states in the top five have been

relatively stable. Texas has held the #1 spot

since 1999, while North Carolina, which held

the #2 spot from 2002 to 2011, dropped

to third place. In a tie with Geogia, North

Carolina received 17% of the votes compared

to 27% in 2011 and 30% in 2008. Although

only 1% separated the second and third slots,

Florida jumped from #5 in 2011 to #2 in 2014

with 18% of respondents indicating it as the

best state for business in the current survey .

South Carolina, which was fourth this year,

was sixth in 2008 and third in 2002, 2005,

and 2011. Tennessee, which fell to fourth

place in 2008 and 2011, dropped to fifth

place. Table D presents how states have

ranked in the top five since 1996.

Table D: Most Favorable Business Climate (Response over Time)

2014 2011 2008 2005 2002 1999 1996

Texas50%

Texas49%

Texas 41%

Texas 33%

Texas 25%

Texas 30%

North Carolina 33%

Florida 18%

North Carolina27%

North Carolina 30%

North Carolina 26%

North Carolina 20%

California 22%

Texas 28%

Georgia; North Carolina 17% (tie)

South Carolina14%

Georgia 20%

South Carolina20%

South Carolina 18%

North Carolina 20%

Georgia 27%

South Carolina12%

Tennessee14%

Florida;Tennessee 15% (tie)

Georgia18%

Florida18%

Georgia17%

South Carolina 21%

Tennessee11%

Florida 14%

Nevada14%

Nevada16%

Georgia15%

Florida14%

Tennessee20%

25

States with the Worst Business Climates

The survey results also revealed the states

deemed to have the least favorable business

climates. The top five least favorable states

are identical to those from 2011, except that

Massachusetts traded places with Michigan,

putting the former at number five and the

latter at number six in 2014.

The top 5 responses were:

1 . California 74%

2 . New York 42%

3 . Illinois 34%

4 . New Jersey 16%

5 . Massachusetts 11%

In an open-ended question, respondents

were asked to explain why they perceive

certain states as having unfavorable business

climates . Overall, taxes was the reason listed

most frequently .

California was cited for having high taxes by

46% of respondents, while 43% said it was

too highly regulated . Cost/expense (29%)

and anti-business climate (15%) were also

mentioned in reference to the state .

Among those who named New York as

having an unfavorable business climate, 59%

listed taxes and 40% listed cost of living

and business as reasons for their negative

perceptions, while 24% of respondents said

the state is too highly regulated .

High taxes were the factor most frequently associated with states perceived as having unfavorable business climates.

Illinois’ taxes (44%), dysfunctional/corrupt

government (37%), cost/expense (17%) and

regulations/permitting (12%) earned the

state its position on the list of least favorable

business climates .

The list of states with the least favorable

business climates has remained remarkably

consistent over the years . California and

New York have swapped the first and

second place spots on this list since DCI first

conducted the survey in 1996, with California

in first place and New York in second place

since 2002. Massachusetts dropped out of

the top 5 in 2011 for the first time since 1996,

but re-joined the list in 2014. Table E shows

the changes over time .

Table E: Least Favorable Business Climate (Response over Time)

2014 2011 2008 2005 2002 1999 1996

California74%

California71%

California72%

California66%

California57%

New York29%

New York55%

New York42%

New York47%

New York42%

New York34%

New York36%

California25%

California47%

Illinois34%

Illinois24%

Michigan17%

Mass .22%

Mass .18%

Mass .19%

New Jersey20%

New Jersey16%

New Jersey24%

New Jersey14%

New Jersey21%

New Jersey15%

NewJersey14%

Mass .19%

Mass .11%

Michigan16%

Mass . 12%

Illinois 13%

Florida 10%

Connecticut 10%

Connecticut9%

26

The International Perspective

In 2014, for the first time, DCI expanded on

the previous questions to include international

business climates . We began by asking

respondents to indicate which part of the

world represents the best international growth

opportunity for their companies (Africa, Asia/

Pacific, Western Europe, Latin America, Eastern

Europe, Middle East) and followed up by asking

respondents to list the three specific countries

that they believe would offer the strongest

opportunities for international investment in

the next three years .

Asia/Pacific represents the best international growth opportunity for nearly 41% of corporate executives.

Overall, Asia/Pacific was selected most

frequently, followed by Western Europe .

Africa was not viewed as an opportunity

among any respondents. Chart Q shows the

distribution of responses.

Chart Q: Part of the World with the Best International Growth Opportunity

Asia/Pacific Western Europe Latin America

Eastern Europe Middle East Africa – 0%

41%

5%

19%

5%

29%

27

Executives involved in manufacturing and

those involved in services think differently

when it comes to where they see the most

opportunity for international growth;

manufacturing executives see the Asia/

Pacific region as representing the best

international growth opportunities for

their companies, whereas executives in the

services industry see Western Europe as a

most promising region in this regard.

Chart R: Part of the World with the Best International Growth Opportunity (Responses based on Industry)

20%

8%28%

40%

18%

3%

3%

21%

50%

8%

Manufacturing Executives Responses

Services Executives Responses

Breaking responses down by company size

reveals that large companies are drawn

to the Asia/Pacific region (50%) when it

comes to international growth opportunities,

whereas midsize companies are drawn to

Western Europe (38%).

Chart S: Part of the World with Best International Growth Opportunity (Responses based on Company Size)

50%

2%

20%

6%

22%

32%

6%

38%

8%

17%

Midsize Company Responses

Large Company Responses

Asia/Pacific Western Europe Latin America

Eastern Europe Middle East Africa – 0%

28

Countries with the Strongest International Investment Opportunities

We asked executives to indicate which

countries they believe offer the strongest

international investment opportunities

for their company if they plan to explore

this option in the next three years. The

257 respondents to this question listed 57

countries; China (30%), the United Kingdom

(22%) and Germany (20%) were listed most

frequently .

China tops the list of countries with the strongest international investment opportunities for executives.

1 . China 30%

2 . United Kingdom 22%

3 . Germany 20%

4 . India 17%

5 . Brazil 14%

6 . Singapore 12%

7 . France 11%

8 . Mexico 10%

9 . Canada 7%

10. Australia 6%

Why Executives Explore International Expansion

Next, we asked executives to indicate

the primary drivers for their company’s

international expansion by checking all

that apply from a list of six items: market

access, cost savings, workforce/talent pool,

technology/product partnership, other and

we don’t have any plans for international

expansion . Market access followed by cost

savings was the most frequently checked

item by respondents with potential plans for

international expansion.

Executives identified market access as the primary driver for international expansion.

Chart T: Drivers for International Expansion

Market access Cost savingsWorkforce/

talent pool

OtherTechnology/

product partnership

35%

44%28%

7%

28%

29

The Consultants Speak:

Best Economic Development

Groups

Because location advisors have regular

contact with economic development groups

and would be able to provide an evaluation

based on experience, we asked them to

indicate up to three “Best in Class” regional

or community economic development

organizations and up to three “Best in Class”

state economic development organizations.

Among the location advisors, 63 respondents

named a total of 70 regional or community

economic development organizations and no

region earned more than 25% of all mentions.

Regional/community economic development

organizations with 10% or more recognition are:

Sixty-two consultants named 32 state-level

economic development agencies that they

consider “Best in Class.” The top responses are:

1 . Georgia Department of Economic Development 29%

2 . Louisiana Economic Development

Texas Governor’s Office of Economic Development23%

3 . South Carolina Department of Commerce 19%

4 . Michigan Economic Development 18%

5 . Kansas Department of Commerce

Missouri Partnership

Oklahoma Department of Commerce

16%

6 . Enterprise Florida

Economic Development Corporation of Utah

Virginia Economic Development Partnership

15%

7 . Indiana Economic Development Corporation 11%

TIE

TIE

TIE

1 . Kansas City Area Development Council 22%

2 . Charlotte Regional Partnership Columbus 2020

16%

3 . Greater Phoenix Economic Council 14%

4 . Greater Houston Partnership Nashville Chamber of Commerce

11%TIE

TIE

30

Looking Forward:Projected Location

Decisions In 2014 And 2015

DCI also asked corporate executives about

projected location decisions in 2014 and 2015.

Dipping slightly from 46% in 2011, 44% of

respondents indicated that their company will

make a location decision (move, expansion,

consolidation, etc.) in the next 24 months. An

additional 30% indicated they were not sure,

while 26% said their company would not make

a location decision in the next two years.

Down a notch, 44% of executives expect to make a location decision in the next 24 months.

What types of projects are being planned?

When asked to indicate from five different

facility types, which is the most likely

candidate for a facility change, respondents

most frequently indicated a manufacturing/

production plant (31%) followed by corporate,

division or regional headquarters (25%).

Chart U shows the distribution of responses.

Chart U: Most Likely Facility Type for Next Facility Change

Manufacturing/ production plant

Corporate, division or regional headquarters

Regional sales office or service center

Back office/ shared services facility

Distribution center

Other

25%

31%

11%

12%

5%

16%

31

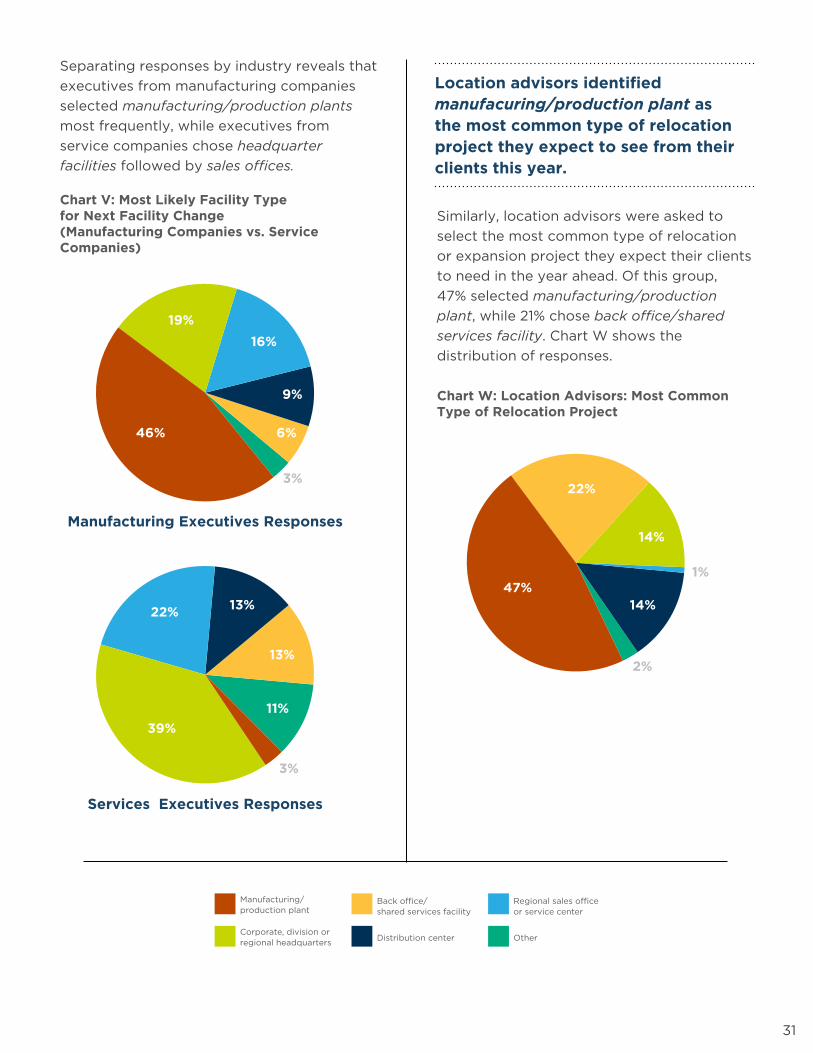

Separating responses by industry reveals that

executives from manufacturing companies

selected manufacturing/production plants

most frequently, while executives from

service companies chose headquarter

facilities followed by sales offices.

Chart V: Most Likely Facility Type for Next Facility Change (Manufacturing Companies vs. Service Companies)

13%

3%

13%

11%

22%

39%

6%46%

16%

19%

3%

9%

Manufacturing Executives Responses

Services Executives Responses

Similarly, location advisors were asked to

select the most common type of relocation

or expansion project they expect their clients

to need in the year ahead. Of this group,

47% selected manufacturing/production

plant, while 21% chose back office/shared

services facility. Chart W shows the

distribution of responses.

Chart W: Location Advisors: Most Common Type of Relocation Project

Manufacturing / production plant

Corporate, division or regional headquarters

Regional sales office or service center

Back office / shared services facility

Distribution center

Other

14%

14%

22%

47%1%

2%

Location advisors identified manufacuring/production plant as the most common type of relocation project they expect to see from their clients this year.

Manufacturing/ production plant

Corporate, division or regional headquarters

Back office/ shared services facility

Distribution center

Regional sales office or service center

Other

32

Outsourcing a Portion of the Site Selection Process

To further understand the corporate site

selection process, we asked corporate

respondents whether they anticipate

outsourcing a portion of the site selection

responsibilities in their next site selection

search. Dropping from 47% in 2011, 40%

answered “yes.”

Forty percent of executives anticipate outsourcing a portion of the site selection responsibilities in their next site selection search.

A higher percentage of large companies

(59%) will outsource a portion of the site

selection responsibilities versus midsized

companies (37%).

Chart X shows what type of individual/

organization would be hired by executives

to assist with both U.S. and international

site searches . In U .S . searches, executives

are most likely to use real estate brokers

followed by site selection consultants. When

conducting international searches, executives

rely most commonly on real estate brokers

followed by lawyers.

Chart X: Professional Likely to Assist Corporate Respondents with Site Search (U.S. vs. International Site Search)

Accountant LawyerSite SelectionConsultant

Real EstateBroker

Other

15%

26%

1%

11%

30%

19%

53%

12%

24%

10%

United States

International

33

A Word About DCI

Development Counsellors International (DCI)

is the leader in marketing places. Since 1960,

we have worked with more than 450 cities,

regions, provinces, states and countries,

helping them attract both investors and

visitors. We specialize exclusively in all

phases of economic development and

tourism marketing .

Our areas of expertise include:

• Editorial Placement/Media Relations

• Lead Generation

• Location Advisor Relationship Building

• Perception Studies (Corporate Executives/

Site Selection Consultants)

• Social/Digital Media

• Media Training

• Talent Attraction Programs

• Special Events

• Marketing Blueprints and Strategies

• Website Development

• Tourism Development

• Crisis Communications

DCI has worked with more economic

development groups than all other marketing

agencies combined. The firm also frequently

forms alliances with local advertising, public

relations and marketing agencies to provide

specialized economic development input.

Interested in learning more? We’d love

to explore how we might assist your

community:

Andrew T. Levine

President/Chief Creative Officer

Development Counsellors International

215 Park Avenue South

New York, NY 10003

Phone: 212-725-0707 Ext. 107

Fax: 212-725-2254

andy .levine@aboutdci .com

www.aboutdci.com

34

Appendix A

Questionnaire and Invitation to Participate

Dear <Salutation>:

It will take you less than five minutes to complete the attached survey. But your comments will be of enormous help to the nation’s economic development professionals in better understanding the site selection needs of companies like yours.

Would you be kind enough to give us your opinions by clicking on the below link and answering the survey’s 15 questions?

The survey’s findings will be presented on Monday, October 20 at the International Economic Development Council’s 2014 Annual Conference in Dallas-Fort Worth . Your responses will be kept anonymous and confidential.

Thank you for your consideration of this request . P.S. We will gladly send your choice of a $10 Starbucks or $10 iTunes gift card for your participation. We’ll also be pleased to share an executive summary of the findings when reported in October. Sincerely, ANDY LEVINE President/Chief Creative Officer DEVELOPMENT COUNSELLORS INTERNATIONAL 215 Park Avenue South New York, NY 10003 T 212 725 0707 x 107 F 212 725 2254 E andy .levine@aboutdci .com www.aboutdci.com

Winning Strategies 2014 - Business Location Survey Corporate Executive Version

1 . Are you involved in the decision to relocate, expand, consolidate or build new facilities for your company?

❍❍ Yes (Continue)

❍❍ No (Please forward to the appropriate person in your organization)

2. The next time that your company will move, expand, consolidate or add a facility, which of the following functions would be the most likely candidate for such a change? (Please choose one of the following)

❍❍ Corporate, division or regional headquarters

❍❍ Manufacturing/production plant

❍❍ Regional sales office or service center

❍❍ Distribution center

❍❍ Back office/shared services facility (financial services, data processing or contact center)

❍❍ Other ____________________

3 . In your next location search, do you anticipate outsourcing a portion of the site selection responsibilities?

❍❍ Yes

❍❍ No

If yes is selected as answer to number 3, please answer the following question.

3a. What type of individual/organization is likely to assist you with the search?

Location of Search

United States

International Location

Accountant ❍ ❍

Lawyer ❍ ❍

Site Selection Consultant

❍ ❍

Real Estate Broker

❍ ❍

Other (please specify)

❍ ❍

35

4. In general, at what stage in a site selection

search do you FIRST contact economic

development organizations?

❍❍ During the screening phase of all possible

locations in order to request preliminary

data

❍❍ Following the development of the

shortlist of communities to request

specific information or to arrange a site

visit

❍❍ After identifying finalists in order to

negotiate incentives

❍❍ After a final location has been selected

and a suitable building or lot is needed

❍❍ We would not contact an economic

development organization at any stage in

a site location search

5. Please indicate the three U.S. states with

business climates you perceive as MOST

FAVORABLE, and then briefly indicate why.

State #1 ____________________________

Reason for State #1 __________________

State #2 ___________________________

Reason for State #2 __________________

State #3 ___________________________

Reason for State #3 __________________

6. Please indicate the three U.S. states with

business climates you perceive as LEAST

FAVORABLE, and then briefly indicate why.

State #1 ____________________________

Reason for State #1 __________________

State #2 ___________________________

Reason for State #2 __________________

State #3 ___________________________

Reason for State #3 __________________

7. What part of the world represents

the best INTERNATIONAL

GROWTH opportunity for your company?

(please select one)

❍❍ Africa

❍❍ Asia/Pacific

❍❍ Eastern Europe

❍❍ Latin America

❍❍ Middle East

❍❍ Western Europe

8. If you are exploring international investment in the next three years, what COUNTRIES do you believe offer the strongest investment opportunities for your company?

1 __________________________________

2 __________________________________

3__________________________________

9. What are the primary drivers for your company’s INTERNATIONAL expansion? (check all that apply)

❍❍ Market access

❍❍ Cost savings

❍❍ Workforce/talent pool

❍❍ Technology/product partnership

❍❍ Other ______________________

❍❍ We don’t have any plans for international expansion

10. In light of your responses to the previous questions, what are the three leading sources of information influencing your perceptions of an area’s business climate?

❍❍ Advertising

❍❍ Articles in newspapers and magazines

❍❍ Business travel

❍❍ Dialogue with industry peers

❍❍ Direct mail

❍❍ Meetings with economic development groups

❍❍ Rankings/surveys

❍❍ Online sources

❍❍ Personal travel

❍❍ Social media

❍❍ TV and radio newscasts/shows

❍❍ Word of mouth

❍❍ Other ____________________

In light of your responses to the previous questions, please answer one or more of the following questions.

10a. What type of advertising do you view as the most effective?

❍❍ Online

❍❍ Radio

❍❍ Television

36

10b. What newspapers and magazines do you read most frequently?

1 __________________________________

2 __________________________________

3 __________________________________

10c. What specific rankings/surveys do you pay the most attention to?

1 __________________________________

2 __________________________________

3__________________________________

10d. What online sources do you view most frequently?

1 __________________________________

2 __________________________________

3__________________________________

10e. What television and radio newscasts do you listen to or view most frequently?

1 __________________________________

2 __________________________________

3__________________________________

11. Please check all social media channels that you currently use for business purposes.

❍❍ Blog forums

❍❍ YouTube

❍❍ Other ____________________

❍❍ I do NOT use social media for business purposes

12 . In your most recent site location search, how often did you use the Internet as a source of community information?

❍❍ 1 (Not at all)

❍❍ 2

❍❍ 3

❍❍ 4

❍❍ 5 (Often)

13. What is the likelihood that you will visit an economic development organization’s website during your next site location search?

❍❍ 1 (Not likely)

❍❍ 2

❍❍ 3

❍❍ 4

❍❍ 5 (Extremely likely)

14. Which of the following features do you consider most important to the utility of an economic development organization’s website? (Please select up to five responses)

❍❍ Comparisons to competitor locations (e.g. cost comparisons)

❍❍ Searchable database of available buildings and sites

❍❍ Demographic information (e.g. population, income, age distribution, educational attainment)

❍❍ Incentive information

❍❍ Major employer list

❍❍ Educational institution information (K-12 and post-secondary)

❍❍ Maps of the community/region

❍❍ Current press releases/announcements

❍❍ Quality of life information (e.g. cost of living, cultural/recreational opportunities)

❍❍ Staff contact information

❍❍ Target industries and related information

❍❍ Testimonials from local employers

❍❍ Video content

❍❍ Workforce statistics (e.g. labor force, employment by industry/occupation)

15. Please rate the effectiveness of the following marketing techniques as a means of influencing your opinion when considering a new location.

1 2 3 4 5 Don’t Know

POOR ↔ EXCELLENT

Advertising ❍ ❍ ❍ ❍ ❍ ❍

Direct Mail ❍ ❍ ❍ ❍ ❍ ❍

Internet/ Website

❍ ❍ ❍ ❍ ❍ ❍

Media Relations/ Publicity

❍ ❍ ❍ ❍ ❍ ❍

37

1 2 3 4 5 Don’t Know

Hosting Special Events

❍ ❍ ❍ ❍ ❍ ❍

Planned Visits to Corporate Executives

❍ ❍ ❍ ❍ ❍ ❍

Telemarketing ❍ ❍ ❍ ❍ ❍ ❍

Trade Shows ❍ ❍ ❍ ❍ ❍ ❍

Business Classification: The last few questions will help classify your business. All data will be confidential.

C1. Which of the following best describes your primary business?

❍❍ Manufacturing

❍❍ Services

C2. What was the gross revenue last year for your company, including all plants, divisions, branches and subsidiaries?

❍❍ Less than $25 million

❍❍ $25 - $49 million

❍❍ $50 - $99 million

❍❍ $100 - $249 million

❍❍ $250 million - $499 million

❍❍ $500 million and higher

C3. Will your company make a location decision (move, expansion, consolidation, etc.) in the next 24 months?

❍❍ Yes

❍❍ No

❍❍ Not sure

C4. Please provide your age.

❍❍ Under 30 years

❍❍ 30 - 39

❍❍ 40 - 49

❍❍ 50 - 59

❍❍ Over 60 years

C5. Gender

❍❍ Male

❍❍ Female

Thank you for completing this survey. All responses will be kept confidential and you are not required to provide your name. But should you wish to receive a $10 Starbucks or a $10 iTunes card, please provide your contact information and your choice of gift card below. If you do not wish to provide your contact information, simply submit your survey.

In addition to your gift card, we would also be happy to send you an executive summary of the results after the research has been released in October 2014. Simply check the box below if you would like to receive the results.

Name _________________________________

Title __________________________________

Organization ___________________________

Street Address _________________________

City __________________________________

State _________________________________

Zip Code ______________________________

Email Address __________________________

Please send me:

❍❍ $10 Starbucks Card

❍❍ $10 iTunes Card

Please send me:

❍❍ An executive summary of the report

38

Appendix BMost Favorable Business Climate Rankings for All States

%

Texas 49.7%

Florida 18.1%

Georgia 17.6%

North Carolina 17.6%

South Carolina 12.6%

Tennessee 11.6%

California 11.1%

Indiana 10.6%

New York 10.6%

Louisiana 9.0%

Virginia 9.0%

Utah 8.5%

Nevada 8.0%

Ohio 6.0%

Arizona 5.5%

New Jersey 5.0%

South Dakota 5.0%

Colorado 4.5%

Michigan 4.5%

Oklahoma 4.5%

Pennsylvania 4.5%

Delaware 4.0%

Alabama 3.0%

Kansas 3.0%

%

Massachusetts 3.0%

Missouri 3.0%

Washington 3.0%

Illinois 2.5%

Mississippi 2.5%

Oregon 2.0%

Connecticut 1.5%

North Dakota 1.5%

Wisconsin 1.5%

Wyoming 1.5%

Arkansas 1.0%

Idaho 1.0%

Iowa 1.0%

Kentucky 1.0%

Maryland 1.0%

Nebraska 1.0%

District of Columbia 0.5%

Hawaii 0.5%

Maine 0.5%

Minnesota 0.5%

Montana 0.5%

New Hampshire 0.5%

New Mexico 0.5%

Vermont 0.5%

Note: Three states were not named by any respondents as having the most favorable business climate .

39

Appendix CLeast Favorable Business Climate Rankings for All States

%

California 74.1%

New York 41.8%

Illinois 34.4%

New Jersey 15.9%

Massachusetts 10.6%

Michigan 6.9%

Connecticut 5.8%

Texas 5.8%

Florida 5.3%

Alaska 4.8%

Hawaii 4.8%

Arizona 4.2%

Rhode Island 4.2%

Mississippi 3.7%

North Dakota 3.7%

Maryland 3.2%

Oregon 3.2%

Washington 3.2%

Ohio 2.6%

Arkansas 2.1%

Minnesota 2.1%

Montana 2.1%

Pennsylvania 2.1%

Idaho 1.6%

%

Louisiana 1.6%

Nevada 1.6%

North Carolina 1.6%

Vermont 1.6%

West Virginia 1.6%

Wisconsin 1.6%

Alabama 1.1%

Colorado 1.1%

Iowa 1.1%

New Mexico 1.1%

Wyoming 1.1%

Georgia 0.5%

Kansas 0.5%

Kentucky 0.5%

Maine 0.5%

Nebraska 0.5%

New Hampshire 0.5%

South Carolina 0.5%

South Dakota 0.5%

District of Columbia 0.5%

Note: Seven states were not named by any respondents as having the least favorable business climate .

40

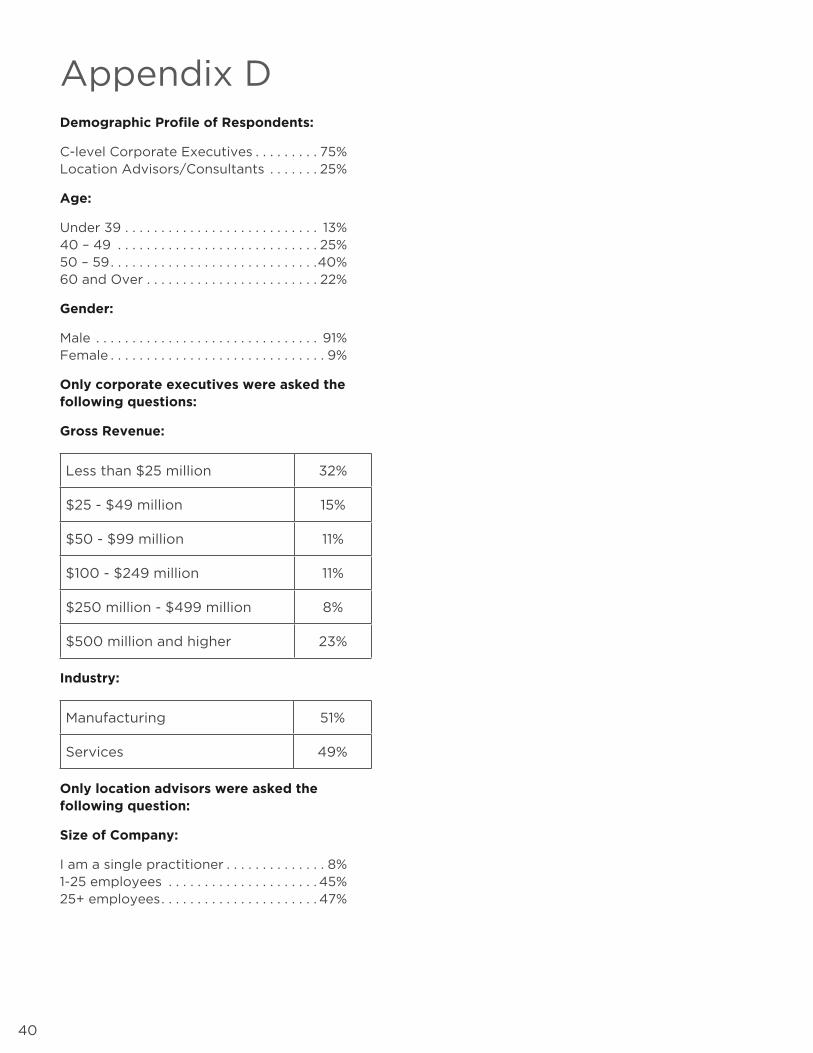

Appendix DDemographic Profile of Respondents:

C-level Corporate Executives . . . . . . . . . 75% Location Advisors/Consultants . . . . . . . 25%

Age:

Under 39 . . . . . . . . . . . . . . . . . . . . . . . . . . . 13%40 – 49 . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25%50 – 59 . . . . . . . . . . . . . . . . . . . . . . . . . . . . .40%60 and Over . . . . . . . . . . . . . . . . . . . . . . . . 22%

Gender:

Male . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 91%Female . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9%

Only corporate executives were asked the following questions:

Gross Revenue:

Less than $25 million 32%

$25 - $49 million 15%

$50 - $99 million 11%

$100 - $249 million 11%

$250 million - $499 million 8%

$500 million and higher 23%

Industry:

Manufacturing 51%

Services 49%

Only location advisors were asked the following question:

Size of Company:

I am a single practitioner . . . . . . . . . . . . . . 8%1-25 employees . . . . . . . . . . . . . . . . . . . . . 45%25+ employees . . . . . . . . . . . . . . . . . . . . . . 47%

Development Counsellors International

NEW YORK

215 Park Avenue South

New York, NY 10003

(212) 725-0707

DENVER

1786 Platte Street

Denver, CO 80202

(303) 627-0272

TORONTO

243 Queen Street West

Toronto, ON M5V 1Z4

(416) 362-0808

LOS ANGELES

5670 Wilshire Boulevard

Los Angeles, CA 90036

(323) 648-6629

www.aboutdci.com