why is there excess volatility? an explanation based...

TRANSCRIPT

24.10.2009 Georges Harras/ETH Zürich D-MTEC/[email protected]

Why is there excess volatility?An explanation based on stochastic

resonanceby Georges Harras, Claudio Tessone and Didier Sornette

ETH Zürich DMTEC

24.10.2009 Georges Harras/ETH Zürich D-MTEC/[email protected]

What is excess volatility?

Too big changes in stock prices compared to changes

of their fundamentals like corporate earnings,

dividends, interest rates [1].

First documented by Robert Shiller in 1981 [2], where

he found that the volatility of the S&P 500 is 5-13 times

too high compared to the volatility of information about

future dividends.

[1] David Cutler, James Poterba, and Lawrence Summers. What moves stock prices? Journal of Portfolio Management, 12, 1989.

[2] Robert J. Shiller. Do stock prices move too much to be justified by subsequent changes in dividends? American Economic Review, 71:421—436, 1981.

24.10.2009 Georges Harras/ETH Zürich D-MTEC/[email protected]

What is excess volatility?

Dividend Discount Model:

pt=∑k=1

∞ d tk1r k

d kr

= dividend at time k

= discount rate

pt = price at time t

Because the future dividends are unknown:

p t∗= ptut

p p∗

pt∗=∑k=1

∞ d t k∗

1r kp t=Et [ p t

∗]

24.10.2009 Georges Harras/ETH Zürich D-MTEC/[email protected]

What is excess volatility?

Robert J. Shiller. Do stock prices move too much to be justified by subsequent changes in dividends? American Economic Review, 71:421—436, 1981.

24.10.2009 Georges Harras/ETH Zürich D-MTEC/[email protected]

Basic ideas of the model:

Agent i

private information

“What should I do?”

24.10.2009 Georges Harras/ETH Zürich D-MTEC/[email protected]

The model:

sit =D k t ∑j=1

N

ij⋅s jt f t i t =a t

log [ price t ]=log [ price t ]r t

return:

imitation term news term idiosyncratic term

Updating:

D(x) = sign(x) orD(x) = x orD(x) = sign(x) Heaviside( |x|thresholdi ).

r t =∑=1

at

=1N

24.10.2009 Georges Harras/ETH Zürich D-MTEC/[email protected]

The model:

N, the number of agents

f(t) is a Gaussian white noise, with

k(t), dynamic coupling constant

Control parameters:

ij=1

# of neighbors

i t ~N 0,Q2

f t ~N 0,A2

24.10.2009 Georges Harras/ETH Zürich D-MTEC/[email protected]

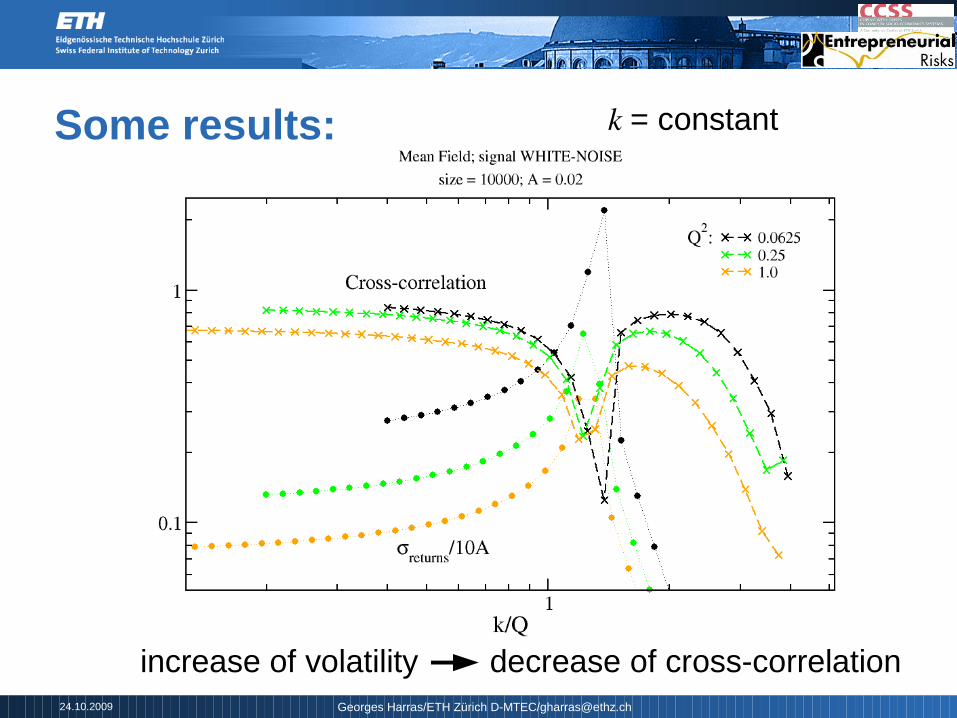

Some results: k = constant

increase of volatility by tuning k/Q

24.10.2009 Georges Harras/ETH Zürich D-MTEC/[email protected]

What is stochastic resonance?R

TSignal

Signal

T

24.10.2009 Georges Harras/ETH Zürich D-MTEC/[email protected]

Some results: k = constant

increase of volatility decrease of cross-correlation

24.10.2009 Georges Harras/ETH Zürich D-MTEC/[email protected]

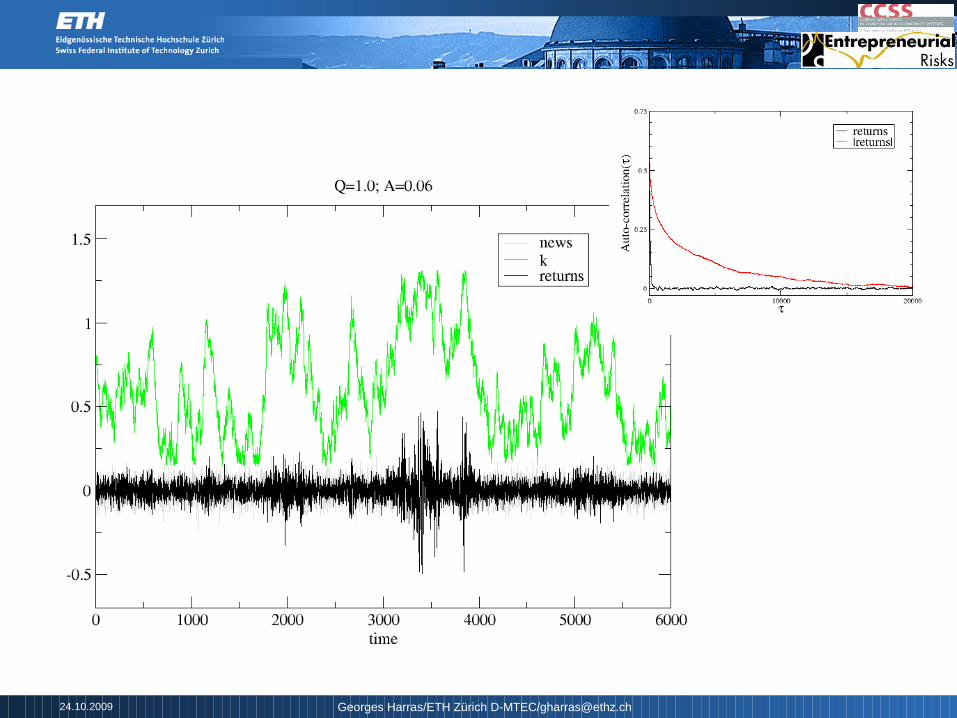

Some results: k = dynamic

clustered volatility

24.10.2009 Georges Harras/ETH Zürich D-MTEC/[email protected]

Conclusions:

We are able to explain excess volatility, having its origin

in the interaction of the agents with private information

Increase of volatility (stochastic resonance) in an wide

range of parameters and setups

Few assumptions are needed: 1) interacting agents, 2)

distribution of personal information, 3) external

influence

Clustered volatility originates from the dynamics in the

coupling strength

24.10.2009 Georges Harras/ETH Zürich D-MTEC/[email protected]

Outlook:

Different network-topologies

Solving for different demand functions D

Endogenize the dynamics of the coupling strength

Dependence of the results with the time window Δ of

returns

...

24.10.2009 Georges Harras/ETH Zürich D-MTEC/[email protected]